Accounting Equation Powerpoint Notes

of 28

-

Upload

psrikanthmba -

Category

Documents

-

view

232 -

download

5

Transcript of Accounting Equation Powerpoint Notes

-

8/10/2019 Accounting Equation Powerpoint Notes

1/28

Accounting EquationAccounting Equation

&&

Accounting ConceptsAccounting Concepts

-

8/10/2019 Accounting Equation Powerpoint Notes

2/28

5 Ways to Classify Accounts5 Ways to Classify Accounts

1.1. AssetsAssets

2.2. LiabilitiesLiabilities

3.3. Owners EquityOwners Equity4.4. RevenueRevenue

5.5. ExpenseExpense

-

8/10/2019 Accounting Equation Powerpoint Notes

3/28

AssetAsset Asset = ownAsset = own

Anything of value that is ownedAnything of value that is owned

Used to acquire additional assets or to operate aUsed to acquire additional assets or to operate abusinessbusiness

Examples: cash, petty cash, supplies,Examples: cash, petty cash, supplies,equipment, accounts receivable, prepaidequipment, accounts receivable, prepaidinsuranceinsurance

-

8/10/2019 Accounting Equation Powerpoint Notes

4/28

LiabilityLiability

Liability = OweLiability = Owe

Amount the business owes to othersAmount the business owes to others

Examples: Accounts payable, notesExamples: Accounts payable, notespayable, other bills unpaidpayable, other bills unpaid

-

8/10/2019 Accounting Equation Powerpoint Notes

5/28

Owners EquityOwners Equity

Amount ownedAmount owned amount owedamount owed

Amount remaining after the value ofAmount remaining after the value of

a es s su rac e rom e asse sa es s su rac e rom e asse s

Owners equityOwners equity amount of businessamount of businessactually owned by the owneractually owned by the owner

-

8/10/2019 Accounting Equation Powerpoint Notes

6/28

Owners EquityOwners Equity

2 Most Common Accounts2 Most Common Accounts

1.1. CapitalCapital summarize owners equity insummarize owners equity inbusinessbusiness

2.2. DrawingDrawing used when an ownerused when an ownerwithdraws either cash or merchandise forwithdraws either cash or merchandise for

personalpersonaluse.use.

-

8/10/2019 Accounting Equation Powerpoint Notes

7/28

RevenueRevenue

Any income earned from the sale of goodsAny income earned from the sale of goods

or services and results in an increase inor services and results in an increase inowners equity.owners equity.

Examples: Sales, ServicesExamples: Sales, Services

-

8/10/2019 Accounting Equation Powerpoint Notes

8/28

ExpenseExpense

Price paid for goods or services used toPrice paid for goods or services used to

operate a business, resulting in a decreaseoperate a business, resulting in a decreasein owners equityin owners equity

Examples: Rent, Utilities, Advertising,Examples: Rent, Utilities, Advertising,WagesWages

-

8/10/2019 Accounting Equation Powerpoint Notes

9/28

Accounting EquationAccounting Equation

-

8/10/2019 Accounting Equation Powerpoint Notes

10/28

Double EntryDouble Entry--SystemSystem

Also called Duel Entry SystemAlso called Duel Entry System

Accounting EquationAccounting Equation mustmust always be inalways be in

a ancea ance

-

8/10/2019 Accounting Equation Powerpoint Notes

11/28

TransactionsTransactions

Changes in the accounting equationChanges in the accounting equation

Must always change 2 accounts to keepMust always change 2 accounts to keep

e accoun ng equa on n a ancee accoun ng equa on n a ance

Will always have a debit and a creditWill always have a debit and a credit

-

8/10/2019 Accounting Equation Powerpoint Notes

12/28

T accountsT accounts

Used to keep balances of accountsUsed to keep balances of accounts

Left side = DebitLeft side = Debit

Right side = CreditRight side = Credit

Debit Credit

Account Name

-

8/10/2019 Accounting Equation Powerpoint Notes

13/28

Normal BalancesNormal Balances

Side of account which increasesSide of account which increases

Assets = Left side increasesAssets = Left side increases

Liabilities = Right side increasesLiabilities = Right side increases

Owners Equity = Right side increasesOwners Equity = Right side increases

-

8/10/2019 Accounting Equation Powerpoint Notes

14/28

Accounting FrameworkAccounting Framework

All businesses must use the sameAll businesses must use the same

reporting practices to record financialreporting practices to record financialinformation.information.

PrinciplesPrinciples

SECSEC Securities and ExchangeSecurities and Exchange

CommissionCommission FASBFASB Financial Accounting StandardsFinancial Accounting Standards

BoardBoard

-

8/10/2019 Accounting Equation Powerpoint Notes

15/28

AICPAAICPA

American Institute of Certified PublicAmerican Institute of Certified Public

AccountantsAccountants National professional organization of CPAsNational professional organization of CPAs

rov es s w resources, n orma on,rov es s w resources, n orma on,and leadershipand leadership

Advocacy, Certification and Licensing,Advocacy, Certification and Licensing,

Recruiting and Education, and StandardsRecruiting and Education, and Standardsand Performanceand Performance

-

8/10/2019 Accounting Equation Powerpoint Notes

16/28

12 Accounting Concepts12 Accounting Concepts

1.1. EntityEntity Accounting records are kept forAccounting records are kept for

entities and not the people who own orentities and not the people who own orrun the company.run the company.

Business is considered its own personBusiness is considered its own person

A business can marry (merger), haveA business can marry (merger), havekids (subsidiary), and die (discontinuekids (subsidiary), and die (discontinue

operations).operations).

-

8/10/2019 Accounting Equation Powerpoint Notes

17/28

Accounting ConceptsAccounting Concepts2.2. MoneyMoney--ManagementManagement for an accountingfor an accounting

record to be made, it must be able to berecord to be made, it must be able to beexpressed in monetary terms.expressed in monetary terms.

Financial statements show only aFinancial statements show only alimited picture of the business.limited picture of the business.

-

8/10/2019 Accounting Equation Powerpoint Notes

18/28

Accounting ConceptsAccounting Concepts3.3. Going ConcernGoing Concern financial statements arefinancial statements are

prepared with the expectation that aprepared with the expectation that abusiness will remain in operationbusiness will remain in operationindefinitely.indefinitely.

Assets cost can be (amortized)Assets cost can be (amortized)spread over its expected life.spread over its expected life.

LiquidatedLiquidated how quickly or the easehow quickly or the easean asset can be converted to cashan asset can be converted to cash

-

8/10/2019 Accounting Equation Powerpoint Notes

19/28

Accounting ConceptsAccounting Concepts4.4. Historical CostHistorical Cost the price paid to acquirethe price paid to acquire

the asset.the asset.

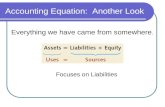

5.5. Dual Aspect (Accounting Equation)Dual Aspect (Accounting Equation)

Assets = Liabilities + Owners EquityAssets = Liabilities + Owners Equity

-

8/10/2019 Accounting Equation Powerpoint Notes

20/28

Accounting ConceptsAccounting Concepts6.6. ObjectivityObjectivity accounting entries will beaccounting entries will be

recorded on the basis ofrecorded on the basis of objectiveobjectiveevidence.evidence.

,,receipts, bank statements, calculatorreceipts, bank statements, calculatortapestapes

All information comes from sourceAll information comes from sourcedocuments and is based on FACTdocuments and is based on FACTnot opinion.not opinion.

-

8/10/2019 Accounting Equation Powerpoint Notes

21/28

Source DocumentsSource DocumentsA business paper which information isA business paper which information is

obtained.obtained.

rove a ransac on as occurre .rove a ransac on as occurre .

Examples: checks, purchase orders,Examples: checks, purchase orders,

invoice, receipts, calculator tapes,invoice, receipts, calculator tapes,memorandumsmemorandums

-

8/10/2019 Accounting Equation Powerpoint Notes

22/28

-

8/10/2019 Accounting Equation Powerpoint Notes

23/28

Accounting ConceptsAccounting Concepts8.8. ConservatismConservatism understating rather thanunderstating rather than

overstating revenue (income) andoverstating revenue (income) andexpense amounts that have a degree ofexpense amounts that have a degree of

..

Rule is to recognize revenue when it isRule is to recognize revenue when it isreasonably certain and measurable andreasonably certain and measurable andrecognize expenses as soon as reasonablerecognize expenses as soon as reasonable

possible.possible.

Better to err on caution than to inflate orBetter to err on caution than to inflate oroverstate positive results.overstate positive results.

-

8/10/2019 Accounting Equation Powerpoint Notes

24/28

Accounting ConceptsAccounting Concepts9.9. RealizationRealization Revenue (income) isRevenue (income) is

recognized when earned or realized.recognized when earned or realized. Seller receives cash or has a claim toSeller receives cash or has a claim to

sale of goods or services.sale of goods or services.

Recorded when received, not whenRecorded when received, not when

awardedawarded

-

8/10/2019 Accounting Equation Powerpoint Notes

25/28

Accounts ReceivableAccounts Receivable Customer has charged on account,Customer has charged on account,

sold on accountsold on account

NormalNormal debitdebit balancebalance

Asset account because money is owed toAsset account because money is owed tothe company and will be collected at athe company and will be collected at alater date.later date.

-

8/10/2019 Accounting Equation Powerpoint Notes

26/28

Accounts PayableAccounts Payable Company buys something on account andCompany buys something on account and

will pay at a later date.will pay at a later date.

orma re a anceorma re a ance

Liability account because money is owedLiability account because money is owed

to a vendor and must be paid laterto a vendor and must be paid later

-

8/10/2019 Accounting Equation Powerpoint Notes

27/28

Accounting ConceptsAccounting Concepts10.10. MatchingMatching Revenues and relatedRevenues and related

expenses must be recorded in the sameexpenses must be recorded in the sameaccounting period.accounting period.

11.11. ConsistencyConsistency Once an entity decides onOnce an entity decides on

a method of reporting it must keep thea method of reporting it must keep thesame method for all subsequent events.same method for all subsequent events.

-

8/10/2019 Accounting Equation Powerpoint Notes

28/28

Accounting ConceptsAccounting Concepts12.12. MaterialityMateriality accounting practice thataccounting practice that

records events that are significantrecords events that are significantenough to justify the usefulness of theenough to justify the usefulness of theinformation.information.

Example: We do not record aExample: We do not record atransaction each time we use atransaction each time we use asheet of paper as an Office Supplysheet of paper as an Office Supply

Expense; instead we wait until weExpense; instead we wait until wepurchase a large quantity and thenpurchase a large quantity and thenexpense it.expense it.