Accounting Equation Final

24

ACCOUNTING EQUATION

-

Upload

sunny-sahni -

Category

Documents

-

view

299 -

download

3

Transcript of Accounting Equation Final

ACCOUNTING EQUATION

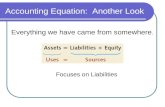

ACCOUNTING EQUATIONAn accounting equation is a statement of equality between the resources and the sources which finance the resources and is expressed as under

Illustration 1: Show accounting equation for following transactions

• Anil commenced business with Rs 50,000• Purchased a typewriter for Rs 7,000• Bought furniture from M/s Mukesh on credit Rs

3,000• Purchased goods for cash Rs 35,000• Sold goods for cash Rs 40,000 (costing Rs 30,000)• Withdrew goods for personal use (cost Rs 500, sale

price Rs 600) • Commission received Rs 1000 in cash.

Illustration 2: Show accounting equation for following transactions

• Sachin commenced business with Rs 100,000• Paid rent in advance Rs 3,000• Purchased a computer for Rs 15,000• Bought furniture from M/s Vinod on credit Rs 10,000• Purchased goods for cash from Yuvraj Rs 55,000• Purchased goods on credit from Virendra Rs 50,000• Sold goods for cash Rs 60,000 (costing Rs 55,000)• Withdrew goods for personal use (cost Rs 1,000, sale price Rs 1,100) • Goods destroyed by fire (cost Rs 500, sale price Rs 600) • Sold goods to Anil on credit Rs 50,000 (cost Rs 45,000)• Commission received Rs 1,500 in cash• Paid cash Rs 5,000 to M/s Vinod• Received cash Rs 49,500 from Anil in full settlement• Paid salary Rs 1,000 and outstanding salary Rs 1,500

JOURNALISING, POSTING & BALANCING

JOURNALIZINGMeaning of Account

• Account is a book-keeping device to record increases and decreases in each expenditure/income/asset/liability item•In its simplest form, an account has two equal sides divided by a vertical line in between (hence commonly called as 'T' account)•On its one side are recorded increases and on its other side are recorded decreases.•Following is an illustrative format of an "Account"

Cont.

Cash Account of XYZ for the month of January 2008Dr. Cr. Date Particulars Amount Rs Date Particulars Amount Rs

01-01-2008 To opening balance - 01-01-2008 To capital account 10,00,000 03-01-2008 By Bank Deposit Account 7,00,000 30-01-2008 To Sales Account 3,00,000 15-01-2008 By Purchases Account 2,00,000

18-01-2008 By Expenses account 32,000

31-01-2008 By Closing Balance 3,68,000

13,00,000 13,00,000

Types of Accounts

Traditional classification of accounts

Traditional Classification of Accounts Accounts equation

Personal Accounts-having debit balances (other than owner’s a/c)-having credit balances (other than owner’s a/c)-those relating to owner

Asset s Accounts

Liabilities Accounts

Capital Accounts

Real Accounts Assets Account

Nominal Accounts-relating to revenue-relating to expenses

Revenue AccountsExpenses Accounts

Types of Accounts

Illustration 1: Classify the following Accounts

Capital brought in Drawings A/cBuilding PurchasedPurchases A/cSales A/cCarriage inwards Carriage outwardsCash Received

Cash Interest paid Interest Received Commission paid Discount allowedConveyance charges Sales promotion Entertainment exp.

Subscription paid Light Power Bad debts recovered Furniture & Fixtures Wages & Salaries Outstanding salary Prepaid Rent Int. rec. in advance

THREE GOLDEN RULES

Debit the Receiver &Credit the Giver

Debit what comes in &Credit what goes out

Debit all expenses & losses & Credit all gains & profits

Interpretation of the three Golden Rules

Type of Accounts Rules for Debit Rules for Credit Closing Balance

For Assets A/cs Debit the increase Credit the decrease Debit

For Liability A/cs Debit the decrease Credit the increase Credit

For Capital A/cs Debit the decrease Credit the increase Credit

For Revenue A/cs Debit the decrease Credit the increase Credit

For Expense A/cs Debit the increase Credit the decrease Debit

Meaning and Format of Journal

Meaning :- A Journal is a book in which transactions are

recorded in the order in which they occur. A journal is called as book of prime entry or

original entry because all business transactions are entered first in this book

The process of recording a transaction in the journal is called Journalising

An entry made in the journal is called a ‘Journal Entry’

• Format :-Journal

Date Particulars LF Debit Rs Credit Rs

Date column – the date on which the transaction is entered is recorded

Particular column – first the names of the accounts to be debited, then the names of the accounts to be credited and lastly the narration (i.e. a brief explanation of the transaction) are entered

LF – the ledger page number containing the relevant account is entered at the time of posting.

Debit amount – the amount to be debited is entered

Credit Amount – the amount to be credited is entered

Steps in journalisingStep 1 – Ascertain what accounts are involved in a transactionStep 2 – Ascertain what is the nature of the accounts involvedStep 3 – Ascertain which rule of debit and credit is applicable for each of the

accounts involvedStep 4 – Ascertain which account is to be debited and which is to be creditedStep 5 – Record the date of the transaction in the ‘Date column’Step 6 – Write the name of the account to be debited, very close to the left

hand side in the ‘Particulars column’ along with abbreviation ‘Dr’ and the amount to be debited in the ‘Debit Rs column’ against

the name of the account.Step 7 – Write the name of the account to be credited in the next line

preceded by the word ‘To’ at a few spaces towards right in the ‘Particulars column’ and the amount to be credited in the ‘Credit Rs column’ against name of the account

Step 8 – Write ‘Narration’ in the next line in the ‘Particulars column’Step 9 – Draw a line across the entire ‘Particulars column’ to separate one

journal entry from the other

Illustration 3: Analyse the following transactions

1. Federer started his business with cash2. Borrowed cash from Andy3. Purchased furniture with cash4. Purchased furniture from Paes on credit5. Purchased goods from Nadal on credit6. Returned goods to Nadal7. Sold goods for cash8. Sold goods to Sampras9. Sampras returned goods10. Received cash from Sampras11. Paid cash to Paes12. Deposited cash in Bank13. Withdrew cash for personal use14. Withdrew from bank for office use

15. Withdrew from bank for personal use 16. Paid Nadal by cheque17.Paid salary18.Paid rent by cheque19.Goods withdrawn for personal use20. Paid an advance to suppliers of goods21.Received an advance from customers22.Paid interest on loan23.Paid installment of loan24.Interest allowed by bank25.Purchased computer from Bill on cr

Following is the illustrative analysis of transactions

Sr. No

Accounts involved Nature of the A/cs involved

How Affected To be debited / Credited

1 Cash A/cCapital A/c

RealPersonal

Cash is coming in Federer is the giver

DebitCredit

2 Cash A/cLoan from Andy A/c

RealPersonal

Cash is coming in Andy is the giver

DebitCredit

3 Furniture A/cCash A/c

RealReal

Furniture is coming inCash is going out

DebitCredit

4 Furniture A/cPaes A/c

RealPersonal

Furniture is coming inPaes is the giver

DebitCredit

5 Purchases A/cCash A/c

RealReal

Goods coming inCash is going out

DebitCredit

Advantages of Journal1. Chronological Record :

Journal is a chronological record in the sense that it records the transactions in the order in which they occur

2. Explanation of Transaction :Each journal entry in the journal carries narration which gives a brief explanation of the transaction

3. Recording of both aspects :Since both the aspects (i.e. debit & credit of a transaction are recorded, the possibility of committing error is reduced and detection of errors if any becomes easier.

Limitations of Journal1. Repetative in nature and therefore requires

more time to record– e.g. for every sales transaction one has to write down the sales account and the narration

2. Does not provide information on prompt basis

3. The journal becomes bulky and voluminous

Illustration 4 Journalise the following transactions in the books of Tom Cruise

Date Transaction Rs.

01.04.2009 Tom Cruise started his business with cash 150,000

02.04.2009 Purchased goods 50,000

03.04.2009 Purchases goods for cash 40,000

04.04.2009 Purchased goods from Mr. John Travolta on credit 30,000

07.04.2009 Sold goods to Mr. Matt on cash 20,000

08.04.2009 Purchased goods from Mr. Ben 30,000

10.04.2009 Purchases goods from Mr. Harrison on credit 15,000

11.04.2009 Sold goods to Mr. Bruce 35,000

13.04.2009 Mr. Bruce returned the goods 10,000

14.04.2009 Received from Mr. Bruce (Allowed discount to him Rs 1,000) 24,000

15.04.2009 Returned goods to Mr. John Travolta 2,000

16.04.2009 Paid to Mr. Ben (Discount allowed by him Rs 500) 29,500

17.04.2009 Paid rent to Shyamlan 2,000

18.04.2009 Withdrew goods for personal use(cost Rs 2000, Selling price Rs 3,000)

20.04.2009 Paid salary to Ed 5,000

Compound Journal EntriesSometimes there are a number of transactions on the same date

relating to one particular account or of the one particular nature Such transactions may be recorded by means of a single journal entry instead of passing several journal entries.

Illustration: A running business was purchased by Mohan with following assets and liabilities

Cash Rs 2,000, Land Rs 4,000, Furniture Rs 1,000, Stock Rs 2,000, Creditors Rs 1,000, Bank overdraft Rs 2,000Date Particulars LF Dr. Amt Cr. Amt

xxxx Cash A/c 2,000Land A/c 4,000Furniture A/c 1,000Stock A/c 2,000 To Creditors A/c 1,000 To Bank Overdraft A/c 2,000 To Capital A/c 6,000(Being commencement of businessby Mohan by taking over a runningbusiness)

• Illustration 5: Journalise the following transactionsDec 1: Ajay started business with cash Rs 400,000Dec 3: Paid into the bank 200,000Dec 5: Purchased goods for cash Rs. 55,000Dec 8: Sold goods for cash Rs 40,000Dec 9: Purchased furniture on credit from Vikas for Rs 40,000Dec 12: Sold goods to Arvind for Rs 20,000Dec 14: Purchased goods from Nisha Rs 70,000Dec 15: Returned goods to Nisha Rs 15,000Dec 16: Received Rs 19,000 from Arvind in full settlementDec 18: Withdrew goods for personal use

Cont.

Dec 20: Withdrew cash for personal use Rs 5,000Dec 21: Paid telephone charges Rs 1,500Dec 22: Paid rent by cheque Rs 1,000Dec 23: Paid Rs 53,000 to Nisha in full settlementDec 24: Paid for stationery Rs 1,200, electricity Rs. 1,700Dec 25: Goods distributed as free sample Rs 2,000Dec 26: Salaries paid to staff Rs 5,000Dec 27: Received from Arvind Rs 19,000 in full

settlementDec 31: Interest allowed by bank Rs 2,000Dec 31: Bank charges debited by bank Rs 300

Illustration 6: Journalise the following transactions in the books of YuvrajDebit balance on April 1, 2009: Cash in hand Rs 70,000, Cash at bank Rs 125,000, Stock of goods Rs 60,000, Furniture Rs 12,000, Building Rs 10,000, Sundry Debtors: Wasim Rs 22,000, Anil Rs 15,000, and Ponting Rs 10,000Credit balance on April 1, 2009: Sundry creditors: Clark Rs 20,000, Dhoni Rs 12,000, Loan from Kim Rs 30,000Following are further transactions in the month of April 2009April 1: Purchased goods from Clark of Rs 45,000April 3: Received Rs 20,000 from Wasim and allowed him Rs. 2,000 as discount Cont.

April 6: Purchased goods from Dhoni Rs 80,000April 8: Purchased furniture from Tendulkar Rs 40,000April 9: Sold goods to Anil Rs 50,000April 10: Sold goods to Kaif on cash Rs 20,000April 12: Paid salary Rs 12,000, stationery Rs 3,500 April 15: Paid to Clark Rs 63,000 in full settlementApril 17: Withdrew goods for personal use Rs 2,000April 19: Interest allowed by bank Rs 4,000April 25: Sold goods for cash Rs 50,000April 28: Purchased goods by cheque Rs 40,000April 29: Received Rs 64,000 from Anil in full settlement

24