Introduction to Accounting - Accounting Equation

45

National University (FAST-NU) Introduction to Accounting

-

Upload

rehman-tariq -

Category

Documents

-

view

136 -

download

22

Transcript of Introduction to Accounting - Accounting Equation

National University (FAST-NU)

Introduction to

Accounting

National University (FAST-NU)

Accounting Defined

IdentifiesIdentifies

RecordsRecords

CommunicatesCommunicatesRelevantRelevant

ReliableReliable

ComparableComparable

AccountingAccountingis a

system that

information

that is

to help USERS make better decisions.

to help USERS make better decisions.

National University (FAST-NU)

Identifying Business

Transactions

Recording Business Activities

Communicating

Business Activities

Accounting Activities

Accounting - “Language of Business”

National University (FAST-NU)

Accounting Activities

Identifying Business Activities

Selecting transactions and events that are

relevant to organization

Recording Business Activities

Keeping a chronological log of transactions

and events measured in Rupees and Classified &

Summarized in useful format

Communicating

Business Activities

Preparing accounting

reports. Also includes

analyzing & interpreting them

(to help Users in making better

decisions)

Accounting “is not an end in itself”

National University (FAST-NU)

Accounting as an Information System

National University (FAST-NU)

Accounting vs Bookkeeping

Bookkeeping is the mechanical and repetitive process of recording financial transactions and keeping financial records either manually and electronically.

Bookkeeping is a small part of accounting.

Accounting includes the design of an information system that meets user’s needs.

Accounting goals are the analysis, interpretation, and use of information.

National University (FAST-NU)

Users of Accounting Information

Internal Users External Users

Those directly involved in

managing and operating an organization

Those not directly involved in managing

and operating an organization

National University (FAST-NU)

Users of Accounting Information

Internal Users External Users

Accounting information helps users both internal and external to make better decisions

Accounting information helps users both internal and external to make better decisions

DirectorsManagers

Officers/employeesBudget OfficersInternal Auditors

Owner/ShareholdersCreditors/ Lenders

CustomersInvestors

External AuditorsBrokers/Financial Analyst

Financial Advisors

National University (FAST-NU)

Types of Accounting

Internal Users External Users

Financial Accounting

Area of accounting that serves the external users by providing them with the General-Purpose Financial Statements

Where general-purpose refers to the broad range of purposes for which external users rely on these statements

Management Accounting

Area of accounting that serves the decision-making needs of the internal users by providing them with the Specific-Purpose Financial Reports

Where specific-purpose refers to a particular decision/problem areas that requires specific reports to be prepared

National University (FAST-NU)

Types of Accounting(other differences)

Management Accounting

- For Internal Users

- For Planning and Control

- Not specific Format required

- Future Oriented

- No Time-Lines

- Not legally required

- No need to follow IAS

Financial Accounting

- Primarily for external Users

- For general-purpose

- Specific Format required

- Past Oriented

- Time-Lines

- Legally required

- Need to follow IAS

National University (FAST-NU)

Accounting and Technology (Computerized Accounting System)

Reduces time, effort and cost of record

keeping.

Improves clerical accuracy.

Changes the way we store, process and summarize large masses of data.

Technology

National University (FAST-NU)

ProprietorshipProprietorship PartnershipPartnership CorporationCorporation

Types of Business Ownership

Private-Sector Organizations

National University (FAST-NU)

Financial Accounting practice is governed by concepts and rules known as

Generally Accepted Accounting Principles (GAAP).

Financial Accounting practice is governed by concepts and rules known as

Generally Accepted Accounting Principles (GAAP).

Relevant Information

Relevant Information

Affects the decision of its users.

Affects the decision of its users.

Reliable InformationReliable Information Is trusted by users.

Is trusted by users.

Comparable Information

Comparable Information

Is helpful in contrasting organizations.

Is helpful in contrasting organizations.

Generally Accepted Accounting Principles

National University (FAST-NU)

Institute of Chartered Accountants of Pakistan

(ICAP)

Institute of Chartered Accountants of Pakistan

(ICAP)

Two Main Bodies to decide about Accounting Standards in Pakistan

Two Main Bodies to decide about Accounting Standards in Pakistan

Securities and Exchange

Commission of Pakistan (SECP)

Securities and Exchange

Commission of Pakistan (SECP)

International Accounting Standard (IAS) are to be followed in Pakistan

(according to Companies Ordinance 1984)

International Accounting Standard (IAS) are to be followed in Pakistan

(according to Companies Ordinance 1984)

Setting Accepted Standards

National University (FAST-NU)

Principles of Accounting

OBJECTIVES

To reveal how to maintain and produce accounting results.

To ensure that information provided by accounting records is Relevant, Reliable, and Comparable.

To ensure the different interested groups that the accounting Records are the Accurate Reflection of the business.

To introduce each and every business unit with the standardized Rules & Regulations pertaining to the maintenance of accounting records.

National University (FAST-NU)

Principles of Accounting

OBJECTIVES

To provide enough information to different users of accounting information as these different groups have different perception for same aspects of accounts.

To enable every concerned person and party to make comparison between different firms especially with regard to accounting information.

National University (FAST-NU)

Principles of Accounting

OBJECTIVES

Cost Principle Objectivity (Reliability) Principle Money Measurement Principle Going Concern Principle Business Entity Dual Aspect Realization Principle Accrual Principle

National University (FAST-NU)

Objectivity PrincipleAccounting information is

supported by independent, unbiased evidence.

Principles of Accounting

Cost PrincipleAccounting information is based

on actual cost.

Money Measurement PrincipleOnly those transactions will be

recorded which can be measured in money terms.

Now Future

Going-Concern PrincipleReflects assumption that the

business will continue operating instead of being closed or sold.

National University (FAST-NU)

Principles of Accounting

Dual aspect Concept Every transaction has at least

two effects and both of these affects should be recorded. It is applied to Accounting Equation

Realization PrinciplesRevenues should be recorded at the time when are earned, NOT at the time when are received.

Accruals PrinciplesExpenses should be recorded at

the time when are incurred, NOT at the time when are paid.

Business Entity Principle For accounting purposes, entity of

Owner is separate from entity of Business

National University (FAST-NU)

Accounting Equation

Cash (resource)Owned

Cash (resource)Owned =

ResourcesProvider(Owner)

ResourcesProvider(Owner)

Other ResourcesOwned

Other ResourcesOwned =

ResourcesProvider

(non-Owners)

ResourcesProvider

(non-Owners)

ResourcesOwned

ResourcesOwned =

ResourcesProvider(Owner)

ResourcesProvider(Owner)

ResourcesProvider

(non-Owners)

ResourcesProvider

(non-Owners)+

ResourcesOwned

ResourcesOwned = Claim of

Owner

Claim of Owner

Claim of non-owners

Claim of non-owners+

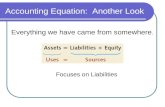

ASSETSASSETS = CAPITALCAPITAL LIABILITIESLIABILITIES+

National University (FAST-NU)

Accounting Equation

AssetsEquity & Liabilities

CapitalCapital LiabilitiesLiabilitiesAssetsAssets = +

National University (FAST-NU)

Expanded Accounting Equation

CapitalCapital LiabilitiesLiabilitiesAssetsAssets = +

RevenuesRevenues ExpensesExpensesOwner Capital

Owner Capital

Owner Withdrawals

Owner Withdrawals

_ + _

National University (FAST-NU)

Accounting Equation

LandLand

EquipmentEquipment

BuildingsBuildings

CashCash

VehiclesVehicles

Store Supplies

Store Supplies

Notes Receivable

Notes Receivable

Accounts Receivable

Accounts Receivable

Resources owned by

the company

Resources owned by

the company

ASSETS

National University (FAST-NU)

Accounting Equation

LIABILITIES

Taxes Payable

Taxes Payable

Wages Payable

Wages Payable

Notes Payable

Notes Payable

Accounts Payable

Accounts Payable

Creditors’ claims on

assets

Creditors’ claims on

assets

National University (FAST-NU)

Accounting Equation

CAPITAL

Owner’sclaims

on assets

Owner’sclaims

on assets

RevenuesRevenues

Owner Investments

Owner Investments

Owner Withdrawals

Owner Withdrawals

ExpensesExpenses

National University (FAST-NU)

Transactions & Accounting Equation

The accounting equation must remain in balance after each transaction.

LiabilitiesLiabilities EquityEquityAssetsAssets = +

National University (FAST-NU)

Transactions & Accounting Equation

Impact of transaction:

(1) Cash (asset)

(2) J. Scott, Capital (equity)

Transaction 1:

J. Scott, the owner, contributed $20,000 cash to start the business.

National University (FAST-NU)

Transactions & Accounting Equation

J. Scott, the owner, contributed $20,000 cash to start the business.

National University (FAST-NU)

Transactions & Accounting Equation

Impact of transaction:

(1) Cash (asset)

(2) Supplies (asset)

Transition 2:

Purchased supplies paying $1,000 cash.

National University (FAST-NU)

Transactions & Accounting Equation

Purchased supplies paying $1,000 cash.

National University (FAST-NU)

Transactions & Accounting Equation

Transition 3:

Purchased equipment for $15,000 cash.

Impact of transaction:

(1) Cash (asset)

(2) Equipment (asset)

National University (FAST-NU)

Transactions & Accounting Equation

Purchased equipment for $15,000 cash.

National University (FAST-NU)

Transactions & Accounting Equation

Transition 4:

Purchased Supplies of $200 and Equipment of $1,000 on account.

Impact of transaction:

(1) Supplies (asset)

(2) Equipment (asset)

(3) Accounts Payable (liability)

National University (FAST-NU)

Transactions & Accounting Equation

Purchased Supplies of $200 and Equipment of $1,000 on account.

National University (FAST-NU)

Transactions & Accounting Equation

Transition 5:

Borrowed $4,000 from 1st American Bank.

Impact of transaction:

(1) Cash (asset)

(2) Notes payable (liability)

National University (FAST-NU)

Transactions & Accounting Equation

Borrowed $4,000 from 1st American Bank.

National University (FAST-NU)

Transactions & Accounting Equation

The balances so far appear below. Note that the Balance Sheet Equation is still in balance.

Now let’s look at transactions involving revenue, expenses and withdrawals.

National University (FAST-NU)

Transactions & Accounting Equation

Transition 6:

Rendered consulting services receiving $3,000 cash.

Impact of transaction:

(1) Cash (asset)

(2) Revenues (equity)

National University (FAST-NU)

Transactions & Accounting Equation

Rendered consulting services receiving $3,000 cash.

National University (FAST-NU)

Transactions & Accounting Equation

(Alternate approach)Rendered consulting services receiving $3,000

cash.

Assets = Liabilities +Owner's Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

Owner's Capital

Bal. 4,000$ 1,200$ 16,000$ 1,200$ 20,000$ (5) 3,000 3,000

7,000$ 1,200$ 16,000$ 1,200$ -$ 23,000$

National University (FAST-NU)

Transactions & Accounting Equation

Transition 7:

Paid salaries of $800 to employees.

Impact of transaction:

(1) Cash (asset)

(2) Salaries expense (equity)

Remember that the balance in the salaries expense account actually increases. But, equity actually decreases because expenses reduce equity.

National University (FAST-NU)

Transactions & Accounting Equation

Remember that expenses decrease equity.

Paid salaries of $800 to employees.

National University (FAST-NU)

Transactions & Accounting Equation

(Alternate approach)Paid salaries to employees, $800 cash.

Assets = Liabilities +Owner's Equity

Cash Supplies EquipmentAccounts Payable

Notes Payable

Owner's Capital

Bal. 4,000$ 1,200$ 16,000$ 1,200$ 20,000$ (5) 3,000 3,000 (6) (800) (800)

6,200$ 1,200$ 16,000$ 1,200$ -$ 22,200$

National University (FAST-NU)

Transactions & Accounting Equation

Transition 8:

J. Scott withdrew $500 from the business for personal use.

Remember that the balance in the J. Scott, Withdrawals account actually increases. But, equity actually decreases because withdrawals reduce equity.

Impact of transaction:

(1) Cash (asset)

(2) J. Scott, Withdrawals (equity)

National University (FAST-NU)

Transactions & Accounting Equation

Remember that withdrawals decrease equity.

J. Scott withdrew $500 from the business for personal use.