Indian Automobile Sector 31 March, 2016 - Systematix...

55

Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd. Investors are advised to refer through disclosures made at the end of the research report. Indian Automobile Sector A tale of two kingdoms Decoding forgotten domestic CV OEMs – expect Tata Motors to bounce back We are trying to decode two forgotten domestic CV OEMs (Tata Motors and Eicher Motors) under the weight/scale/outperformance of their premium cousins (JLR and Royal Enfield). We believe while the performance of JLR and RE will continue, focus needs to shift to their forgotten past hero, “CV Business”. After a careful study of their business strength and company specific drivers, keeping in mind the evolving CV market dynamics, we believe Tata Motors is the most preferred bet. Company-specific micro factors point that Tata Motors is most likely to outperform the industry in FY17/18. Our confidence on outperformance by these players within their respective segments are based on the strategic steps taken by Tata Motors’ management and changing industry dynamics: 1) focus on models to fill product white spaces and new launches with extensive testing/market seeding (avoid past approach), 2) improve competitiveness in PV with new launches (modular platform with eight launches based on Nexon) and reach earlier market share, 3) strengthen distribution network in the competitor stronghold (South for HCV), 4) sharp focus on leaner cost structure and vendor rationalisation and 5) bottom-up forecasting with management decentralisation for better/swift market responses. Bullish on Indian CVs – expect upcyle to continue till FY20 with marginal blip in FY18 CV segment stands to benefit immensely on the emerging economic milieu – improved operator profitability with balance sheet improvement (2/3 rd of the fleet out of financing obligations), government’s focus to improve infrastructure and mining (start of the tipper uptrend), regulatory changes (BSIV/BSVI, body/safety code, transportation overhaul) and large shift to tractor trailers and high tonnage MAVs (expected launch of 40T rigid by Tata and AL). We expect tractor trailers, tippers and buses to be the key growth driver over the next few years, and strong players in the segment are likely to benefit the most. M&HCV dynamics – tonnage upgrade and new peak in sight We estimate M&HCV (goods) volume and tonnage CAGR of 15% over the next four years due to infrastructure spending push, better freighter profitability, reefer trucks, obsolescence of old trucks due to rising entry restrictions in major cities and customer-driven switch to a younger fleet. We also expect buses volume CAGR of 18% on renewed focus on urban transportation, smart cities and structural reform (removal of STU monopoly) in many routes. We believe Tata Motors and AL will emerge as the key beneficiary of M&HCV trends due to a) superior product and higher market share in new emerging/growing categories and b) scale/cost advantage. Initiate coverage on Tata Motors (Buy, 41% upside) and Eicher (Hold, 3% upside) Our positive stance on Tata Motors is also guided by LCV/SCV recovery, distribution rejig to plug the weak spots, strong PV product line-up, margin expansion and dramatic improvement in standalone earnings. We are also optimistic on JLR growth with realistic margin assumption (15%) and signs of resolution of China bump, post JV structure changeover. Our neutral stance on Eicher Motors is guided by unrealistic Royal Enfield (RE) growth assumption by the street (>30% volume CAGR with continuous margin expansion) and resultant stock valuations. We expect a gradual step-up in VECV business (maintaining LMD truck and buses stronghold), with major improvement in HD segment (both domestic and exports) from FY18/19. Although we like the business and management for its strong execution and business passion, we believe investors should opt for better entry point as most positives are factored, while risks (growth maturity in RE, cash burning at Polaris JV, slower Pro series and powertrain volume ramp-up) are ignored. Systematix Institutional Equities 31 March, 2016 CV SECTOR REPORT Industry Automobiles CNX Auto v/s Sensex Source: Systematix Institutional Research Key picks CMP TP Upside Reco. (Rs) (Rs) (%) TTMT 389 550 41 Buy EIM 18,709 19,250 3 Hold Source: Systematix Institutional Research Priya Ranjan [email protected] +91 22 6704 8067 Bibhishan Jagtap [email protected] +91 22 6704 8058

Transcript of Indian Automobile Sector 31 March, 2016 - Systematix...

Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Investors are advised to refer through disclosures made at the end of the research report.

Indian Automobile Sector

A tale of two kingdoms

Decoding forgotten domestic CV OEMs – expect Tata Motors to bounce back

We are trying to decode two forgotten domestic CV OEMs (Tata Motors and Eicher Motors)

under the weight/scale/outperformance of their premium cousins (JLR and Royal Enfield). We

believe while the performance of JLR and RE will continue, focus needs to shift to their

forgotten past hero, “CV Business”. After a careful study of their business strength and

company specific drivers, keeping in mind the evolving CV market dynamics, we believe Tata

Motors is the most preferred bet. Company-specific micro factors point that Tata Motors is

most likely to outperform the industry in FY17/18. Our confidence on outperformance by

these players within their respective segments are based on the strategic steps taken by Tata

Motors’ management and changing industry dynamics: 1) focus on models to fill product

white spaces and new launches with extensive testing/market seeding (avoid past approach),

2) improve competitiveness in PV with new launches (modular platform with eight launches

based on Nexon) and reach earlier market share, 3) strengthen distribution network in the

competitor stronghold (South for HCV), 4) sharp focus on leaner cost structure and vendor

rationalisation and 5) bottom-up forecasting with management decentralisation for

better/swift market responses.

Bullish on Indian CVs – expect upcyle to continue till FY20 with marginal blip in FY18

CV segment stands to benefit immensely on the emerging economic milieu – improved

operator profitability with balance sheet improvement (2/3rd of the fleet out of financing

obligations), government’s focus to improve infrastructure and mining (start of the tipper

uptrend), regulatory changes (BSIV/BSVI, body/safety code, transportation overhaul) and

large shift to tractor trailers and high tonnage MAVs (expected launch of 40T rigid by Tata and

AL). We expect tractor trailers, tippers and buses to be the key growth driver over the next

few years, and strong players in the segment are likely to benefit the most.

M&HCV dynamics – tonnage upgrade and new peak in sight

We estimate M&HCV (goods) volume and tonnage CAGR of 15% over the next four years due

to infrastructure spending push, better freighter profitability, reefer trucks, obsolescence of

old trucks due to rising entry restrictions in major cities and customer-driven switch to a

younger fleet. We also expect buses volume CAGR of 18% on renewed focus on urban

transportation, smart cities and structural reform (removal of STU monopoly) in many routes.

We believe Tata Motors and AL will emerge as the key beneficiary of M&HCV trends due to

a) superior product and higher market share in new emerging/growing categories and b)

scale/cost advantage.

Initiate coverage on Tata Motors (Buy, 41% upside) and Eicher (Hold, 3% upside)

Our positive stance on Tata Motors is also guided by LCV/SCV recovery, distribution rejig to

plug the weak spots, strong PV product line-up, margin expansion and dramatic improvement

in standalone earnings. We are also optimistic on JLR growth with realistic margin assumption

(15%) and signs of resolution of China bump, post JV structure changeover.

Our neutral stance on Eicher Motors is guided by unrealistic Royal Enfield (RE) growth

assumption by the street (>30% volume CAGR with continuous margin expansion) and

resultant stock valuations. We expect a gradual step-up in VECV business (maintaining LMD

truck and buses stronghold), with major improvement in HD segment (both domestic and

exports) from FY18/19. Although we like the business and management for its strong

execution and business passion, we believe investors should opt for better entry point as

most positives are factored, while risks (growth maturity in RE, cash burning at Polaris JV,

slower Pro series and powertrain volume ramp-up) are ignored.

Systematix

Institutional Equities

31 March, 2016

CV SECTOR REPORT

Industry Automobiles

CNX Auto v/s Sensex

Source: Systematix Institutional Research

Key picks

CMP TP Upside Reco. (Rs) (Rs) (%)

TTMT 389 550 41 Buy

EIM 18,709 19,250 3 Hold

Source: Systematix Institutional Research

Priya Ranjan [email protected] +91 22 6704 8067

Bibhishan Jagtap [email protected] +91 22 6704 8058

31 March, 2016

2 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Contents

Charting the story ................................................................................................................................................................ 3

The jewels in domestic CV industry crown ............................................................................................................................. 4

Tata Motors – on the cusp of renaissance ............................................................................................................................... 6

CV OEMs: Strengths and ability to outscore ............................................................................................................................ 7

Commercial vehicles: Regaining the mojo ............................................................................................................................... 8

Companies Section ............................................................................................................................................................. 13

Tata Motors ....................................................................................................................................................................... 14

Eicher Motors .................................................................................................................................................................... 31

31 March, 2016

3 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Charting the story

Chart 1: CV industry volume growth assumption Chart 2: M&HCV industry growth to remain strong in FY17e

Source: SIAM, Systematix Institutional Research Source: SIAM, Systematix Institutional Research

Chart 3: Auto CV OEMs: AL and Tata Motors stand out on key operating benchmarks and overall score

Source: Systematix Institutional Research

Chart 4: Mix of HD trucks volume mix Chart 5: EBITDA margins of Tata, AL & VECV

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

4 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

The jewels in domestic CV industry crown

Prefer incumbent leaders - TTMT should start outgrowing the market

We expect auto industry’s volume growth to pick up meaningfully in FY17, backed by a) decline in ownership cost (fuel price decline and interest cost reduction), b) benign inflation, c) pick-up in economic activities and d) big thrust on infrastructure investment. We estimate these factors to drive domestic passenger vehicle and commercial vehicle volume CAGR of 14% and 19% respectively over the next three years. However, we would prefer players with product/distribution advantage, diversified portfolio in the segment, better chances of outperforming market growth rate, leaner cost structure and meaningful scale (top two players). Based on the above parameters, we prefer Tata Motors and initiate coverage on both Tata Motors and Eicher Motors.

Table 1: Tata Motors (Standalone): Key operating metrics

Tata Motors FY12 FY13 FY14 FY15 FY16e FY17e FY18e

Volume 906,255 809,112 566,960 526,045 509,647 609,942 705,534

Yoy (%) 13.1 (10.7) (29.9) (7.2) (3.1) 19.7 15.7

Revenue 540,055 443,739 339,070 358,905 407,954 504,295 585,311

EBITDA 44,119 21,446 (4,668) (8,000) 28,554 53,134 65,444

Adj. PAT 14,766 7,284 7,633 (43,015) 9,470 29,766 42,035

Source: Company, Systematix Institutional Research

Table 2: Tata Motors (JLR): Key operating metrics

JLR (GBP mn) FY12 FY13 FY14 FY15 FY16e FY17e FY18e

Volume 314,415 372,061 429,661 470,500 531,046 606,663 673,761

Yoy (%) 29.1 18.3 15.5 9.5 12.9 14.2 11.1

Revenue 13,512 15,784 19,386 21,866 21,965 25,595 28,994

EBITDA 2,027 2,339 3,393 3,758 3,216 3,939 4,382

Adj. PAT 1,468 1,261 1,742 2,038 1,358 1,975 2,349

Source: Company, Systematix Institutional Research

Table 3: Eicher Motors (VECV): Key operating metrics

Eicher Motors - VECV CY12 CY13 CY14 CY15e FY16e FY17e FY18e

Volume 48,262 40,550 39,892 46,270 49,854 60,944 62,820

Yoy (%) 17.9 (16.0) (1.6) 16.0 7.7 22.2 3.1

Revenue 52,933 50,127 56,350 72,327 78,156 96,609 107,411

EBITDA 3,998 3,971 3,831 5,736 6,408 9,394 9,337

Adj. PAT 3,303 2,883 1,894 2,991 3,294 5,322 5,152

Source: Company, Systematix Institutional Research

Table 4: Eicher Motors (RE): Key operating metrics

Eicher Motors - RE CY12 CY13 CY14 CY15e FY16e FY17e FY18e

Volume 113,432 178,121 302,592 452,069 506,700 620,000 745,000

Yoy (%) 52.0 57.0 69.9 49.4 12.1 22.4 20.2

Revenue 10,438 16,954 30,147 46,237 53,129 69,490 89,372

EBITDA 1,454 3,137 7,336 12,684 14,802 20,848 27,156

Adj. PAT 1,448 2,786 5,589 8,705 10,045 14,236 18,993

Source: Company, Systematix Institutional Research

31 March, 2016

5 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Table 5: Domestic OEMs valuation

Company Bloomberg Reco TP PER (x) EV/EBITDA (x)

FY17e FY18e FY17e FY18e

M&M MM IN Buy 1,635 18.0 14.8 13.2 10.8

Maruti Suzuki MSIL IN Buy 4,800 14.8 12.1 8.3 6.7

Ashok Leyland AL IN Buy 125 13.2 9.3 10.2 7.8

Tata Motors TTMT IN Buy 550 7.3 6.2 3.6 3.1

Hero MotoCorp HMCL IN NR NA 16.9 15.2 11.6 10.5

Bajaj Auto BJAUT IN NR NA 16.5 14.4 12.1 10.8

Eicher Motors EIM IN Hold 19,250 28.1 22.2 15.0 12.1

TVS Motor TVSL IN NR NA 22.6 17.8 14.4 11.8

Source: Bloomberg, Systematix Institutional Research ; Note: NR companies forward ratios based on Bloomberg consensus.

31 March, 2016

6 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Tata Motors – on the cusp of renaissance

We believe the key concerns on Tata Motors -- margin/profitability issue in domestic business and China/global growth and margin issues in JLR -- are likely to get addressed in the next 6-12 months at both company and market level. Our confidence is driven by:

Emerging visibility of domestic HD trucks market share bounce-back (higher market growth expectation in its superior product segment like tractor trailer and tippers), revival visibility of its key SCV segment, product launches in PV space (Nexon platform can be a potential game changer).

Return of SUV launch cycle in JLR (F-pace with very strong booking), revival of Chinese volume growth with Discovery Sports and XE launch expansion.

JLR margin moving to more realistic level (~15%) along with improvement in Chinese JV profitability post volume ramp-up. Return of domestic operating margin to 10%+ on LCV ramp-up beyond 20k/month.

Wipe-out of annual losses (~Rs15-16bn) in PV business post 20k+ monthly volume.

We initiate coverage on Tata Motors with a Buy rating and SOTP-based target price of Rs550.

Eicher Motors – Best in price while risks are ignored

Although near-term growth is robust, we will be cautious on its future and continuous occurrence probability. We believe export market development will be a long-term process (highlighted by company MD), with sustained brand building exercise, and we expect export market to reach 4% of total volume in FY20e, from 2% currently.

We estimate VECV HD truck segment CAGR of ~10% due to slow ramp-up of Pro6000 series and initial market seeding efforts. We have assumed flat-to-marginal dip in volume for FY18 due to pre-buying effect in FY17 arising from the emission norm change in FY18. Volvo’s 25% stake acquisition in Deutz (engine supply was supposed to be transferred from Deutz to VECV engine facility) has limited the engine volume opportunities too.

Market potential for a premium bike has the limitation of ~60-70k/month in India -- seen in the case of earlier premium Bajaj Pulsar (volume restricted to ~70k at peak) -- as brand fatigue and too much visibility seeps in. Although dealership expansion and market penetration (smaller towns and rural areas) opportunities exist, we believe this will also coincide with market share loss to HD, Triumph and UM’s mid-range bikes in bigger cities. We have seen this in the case of limited success of Continental GT or products with prices above Rs150k.

Expect VECV’s volume to post a CAGR of ~14% over FY16e-20e and growth to be driven by 14% and 17% LMD truck and buses volume growth respectively. We estimate HD truck segment CAGR of ~10% due to slow ramp-up of Pro6000 series and initial market seeding efforts. We have assumed flat-to-marginal dip in volume for FY18 due to the pre-buying effect in FY17 on emission norm changes.

We believe competitive and market share improvement pressures along with ROI linked engine supply orders (higher engine volume with lower engine margins) can keep margins below double digit in the medium term for VECV.

We initiate coverage on Eicher Motors with a Hold rating and a SOTP-based target price of Rs19,250 (implied 23.5x FY18e EPS).

31 March, 2016

7 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

CV OEMs: Strengths and ability to outscore

Players with India-centric model launches to outgrow the market in PV space

Since 2HFY15, CV cycle recovery started with HCV segment and aided by improved freighters’ profitability and balance sheet. Other CV segments like ICV too has started seeing improvement in early FY16 and LCV/SCV segment too joined the party at the fag end of FY16. We believe a revival of CV cycle will continue till FY20, with a moderate blip in FY18 on large pre-buying in FY17, before the BSIV emission norms kick in. Buses segment is likely to see 15% CAGR over many years on the government’s focus on public transport and reforms in public road transport sector in the current union budget. We believe LCV/SCV segment will see a major upswing in the coming years due to last mile connectivity requirement and penetration of hub/spoke model. While initial growth was led by MAVs, we have started to see large growth coming from tipper and tractor trailer segment. While AL was the clear winner in MAV segment growth, we highlight that Tata Motors will recover the partial market share loss with superior performance in both tipper and tractor trailer segment due to product advantage. New players like M&M and Eicher to remain on the fringe for the time being, given the distribution/resale value and product breadth across segments.

Chart 6: Auto CV OEMs: Tata Motors and AL stand out on key benchmarks and overall score

Source: Systematix Institutional Research

Leaders with matching abilities tend to defend or outgrow the market over medium to long-term. Here, we try to map out key domestic CV players’ strength and their ability to outscore on these factors coupled with their probability of success in new segment/product territory. Our above analysis suggests that players like Tata Motors and AL are best placed to maintain leadership in the respective segments.

31 March, 2016

8 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Commercial vehicles: Regaining the mojo

Commercial vehicle industry – LCV/SCV to join M&HCV party in FY17

Our study of M&HCV tonnage capacity in the system along with mining sector headwinds and related tipper demand crash indicate a correction of haulage overcapacity and gradual recovery in tipper segment, which augurs well for the M&HCV segment. A meaningful recovery is also underway in <=16t haulage trucks, which are more dependent on an uptick in economic activity like agri goods and basic manufacturing. Average fleet utilisation (~75%) and freighter profitability have improved meaningfully in the last 12 months. The current shift to tractor trailer and high tonnage MAVs is expected to continue on poor operating economics of old trucks and compression of replacement cycle. Replacement demand is also aided by the restriction imposed by large customers, enforcement of entry norms in New Delhi (population of 60k trucks) on vehicle age and of trailer body code in Haryana. Also, ~75% of the existing fleet has moved out of the financing cycle at the first owner level and thus helping an operator to go for replacement cycle on improved balance sheet.

The government’s ambitious 30km/day road construction and revival of stalled projects are reigniting tipper demand in a major way. Sagar Mala/border road project, Namami Gange, will alone create >15k of annual truck demand, as per our calculation.

The government’s initiative to start coal mining in areas without rail links too is reviving tipper demand.

Expect BSIV implementation-led pre-buying surge to happen in FY17 before the emission norms are enforced.

Early signs of revival in SCV segment are visible and growth bounce-back in the category is expected to benefit OEMs like Tata Motors and M&M immensely.

Chart 7: M&HCV (goods) sales growth rate on upswing Chart 8: M&HCV (passenger) sales volume growth to pick up

Source: SIAM, Systematix Institutional Research Source: SIAM, Systematix Institutional Research

31 March, 2016

9 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Chart 9: M&HCV goods break-up by segment Chart 10: Market-share in 7.5-10t segment

Source: SIAM, Systematix Institutional Research Source: SIAM, Systematix Institutional Research

Chart 11: Market-share in 10-12t Chart 12: Market-share in 12-16.2t

Source: SIAM, Systematix Institutional Research Source: SIAM, Systematix Institutional Research

Chart 13: Market-share in 16.2-25t rigid segment Chart 14: Market-share in >25t rigid segment

Source: SIAM, Systematix Institutional Research Source: SIAM, Systematix Institutional Research

31 March, 2016

10 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Chart 15: Market-share in 26.4<35.2t haulage segment Chart 16: Market-share in the tractor/trailer segment

Source: SIAM, Systematix Institutional Research Source: SIAM, Systematix Institutional Research

Big push to infrastructure projects – a key demand driver going forward

Truck demand from the Infrastructure sector has a multiplier effect as one truck in an infrastructure project generates demand for two to three additional trucks for allied activities and material supply. Also, a truck’s lifecycle in infrastructure is shorter (four to five years) due to excessive and abusive use of trucks. Since the government is pushing for major infrastructure projects’ implementation like the annual highway building of >10,000km, Sagar Mala, border road projects of ~5,000km, Namami Gange, we expect a massive demand surge from the segment in the coming years.

M&HCV tonnage growth to outpace volume growth

We view the shift towards higher tonnage vehicle is permanent and is a logical progression due to better operating economics, driver shortage and consolidation of freight industry. Our interactions with OEM officials and channel partner suggest a freight industry consolidation and single truck operators getting attached to large fleet owners for business. We believe aggregation of fleet volume on truck route is the way forward to improve profitability. Apprehension related to system overcapacity creation on account of a shift to higher tonnage vehicle is a fallacy, given the current fleet tonnage capacity is barely 15-20% higher than the actual road freight volume.

Expected implementation of GST will have a positive impact on higher tonnage vehicle as it will improve the average turnaround time by 10-15% for an operator. Also, the current practice of setting up warehousing to beat multiplicity of taxes will get rationalised in the GST era, which will be a kicker for the higher tonnage vehicle demand as warehousing-on-the-wheel concept can kick in.

31 March, 2016

11 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Driver availability constraint – an enabler for higher tonnage vehicle

Driver shortage is a major issue for most fleet operators across the country. Improving education standards, rising alternate employment opportunity, social taboo as well as qualitative and quantitative family life are the key factors for driver shortage. Driver shortages are forcing fleet operators to rejig their business model with variable compensation structures and shift to high tonnage vehicles. Thus, a shift towards higher tonnage vehicle is permanent.

Return of tipper demand and acceleration in RMC truck demand

Tipper segment, after a 50% fall from ~60k units during 2011-14, has started to recover as demand from coal and bauxite are the key driver compared to iron ore in the previous cycle. Although key iron ore markets like Karnataka and Goa remain subdued, the government’s decision to start coal mines without rail connectivity has buoyed tipper demand.

We are witnessing good tipper demand traction from construction companies and mining segment. We believe tipper will be the key driver in the medium-to-long term as recovery is still at a nascent stage. Similarly, RMC (ready mix concrete) truck demand has risen significantly in the recent past and has considerable room for growth as RMC penetration is still ~6% in India, compared to 70% in developed markets and 35% global average. As construction is getting organised, we expect RMC truck market to explode in the coming years, from ~6-8k units per annum currently.

9-16t segment – recovery visible and Reefer trucks are the way forward

Agriculture segment (foodgrains and seasonal vegetables) is the backbone of 9-16t truck demand. Given agri production has started inching up after the weather issues since last two years, we expect the segment to witness robust growth, which will be largely replacement-led and industrial activity-led. However, we expect refrigerated trucks (Reefer) demand to improve significantly in the medium term due to government’s focus on wastage minimisation (15-30% wastage of horticulture crops during transportation) to tackle inflation.

Chart 17: Total foodgrain production in India Chart 18: Horticulture production growth in India

Source: Ministry of Agriculture, Systematix Institutional Research Source: Ministry of Agriculture, Systematix Institutional Research

31 March, 2016

12 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

Since horticulture production is growing at a much faster pace than foodgrain, we believe the refrigerated truck market has a huge potential from the current fleet size of ~10-15k units (current total industry volume), with annual volume of ~2k trucks. Based on our calculation, we expect the annual Reefer truck volume to reach ~10k units in the next two to three years as the government’s subsidy for Reefer trucks (Rs1.5lac) and ~40-50% shortfall in domestic cold storage capacity will play a major role. Further, the government’s push for a common and integrated national agriculture and horticulture market will be a key growth enabler.

Regulatory changes to bring major technological shift in CV industry

The CV industry will undergo a major transformation in the next few years with the government’s decision to advance BSVI to 2020 and skip BSV completely. With additional efforts to enforce bus body and truck body code, we may see the share of fully built vehicles jump significantly, from less than 10% currently. Although new players or global OEMs (Bharat Benz and VECV) believe these will be beneficial for them, in our view, the impact of these will be only felt after 2020 (if at all it happens) due to lack of preparatory timing for domestic OEMs. However, we believe the domestic OEMs will still manage to overcome this challenge due to their scale of operation.

31 March, 2016

13 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Indian Automobile Sector

COMPANIES SECTION

Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Investors are advised to refer through disclosures made at the end of the research report.

14

Tata Motors

Domestic business to transform while JLR stands tall

We initiate coverage on Tata Motors (TTMT), a niche global luxury car manufacturer and the dominant Indian commercial vehicle player, with a Buy rating and a target price of Rs550. We believe the company’s forgotten hero “domestic business” is on the cusp of a sharp turnaround after almost two years of underperformance, with pointed steps on distribution, product superiority in upcoming HCV drivers (tipper and tractor trailers), revival of LCV/SCV segment with all the financing write-downs behind us and a promising passenger vehicle line-up (particularly Nexon platform). We believe the company’s standalone business will get back to double-digit margins by FY18, while the hiccups in JLR will subside with a shift to SUV launch cycle along with China JV (CJLR) ramp-up gathering momentum. We also expect JLR margins to stabilise near sustainable 15%+ along with meaningful profit contribution from CJLR over the next two years.

Domestic business – fabulous rebound on cards: We believe the domestic business will see a major positive shift from FY17 onwards with all the key segments – HCV, LCV and passenger vehicle regaining their mojo in terms of volume and profitability. We highlight that while the M&HCV business has regained double digit margin in the current upcycle, volume and financing write-down pressure on LCV/SCV, sharp transitory losses in PV business (Rs15-18bn annually) and top leadership vacuum for long is camouflaging TTMT’s domestic business strength. We believe 20k+ LCV/SCV and 15k+ PV monthly volumes are the key monitorables which can sharply shoot up domestic profitability.

Expect 200bps market share gain in HCV in FY17e on tipper/TT product lead (weakness in rigid MAV), distribution amplification (South region) and decision decentralisation.

Estimate double-digit margin by FY18e on convergence of the corrective steps in key business and focus on costs/profitability under the new leadership.

JLR business – return of SUV launch cycle and CJLR back on track: We expect the concern on JLR growth and slow ramp-up of Chinese JV to get addressed with the launch of F-Pace (Jag SUV)/new Discovery (2016/2017)/sub-Evoque SUV (2018)/Defender family (2018/19) and quicker/thoughtful product roll-out in CJLR after initial Evoque pricing debacle. JLR launch focus on sedans (XE, XF) in 2015 was also primarily responsible for the intermediate volume weakness due to brand weakness and lack of 2ltr gasoline engine, which is expected to reverse with F-Pace and new Discovery launch due to its existing strong SUV brand equity. We also believe XE’s launch along with a ramp-up of Discovery Sports can change CJLR’s profitability fortune and improve overall JLR meaningfully.

Estimate 10% and 15% standalone and JLR margins by FY18e: We estimate consolidated sales/EBITDA/PAT CAGR of 16%/24%/31% respectively during FY16e-18e, driven by 20% CAGR of standalone business (17%, 18% and 19% volume growth in M&HCV, LCV and PV business and 450bps margin expansion to 10.3%) and 13% volume growth for JLR with 15% margin (+100bps range; conservative as better margins in new SUVs on variant mix/pricing/discounts). We believe the company is in a sweet spot for standalone margin, with many levers to catapult to the earlier peak, and our JLR margin assumption being very conservative despite SUV launch (core strength) cycle.

Initiate coverage with Buy: At CMP, the stock trades at 7/6x FY17e/18e EPS. Our SOTP-based valuation comes to Rs550 (assigning 4x EV/EBITDA to consolidated EBITDA; implied 8.5x FY18e consol EPS). We are fairly confident on strong domestic business turnaround and change in JLR growth fortune post SUV launches, which are likely to increase earnings to 75% by FY18e. Key risks to our assumptions are a) sharp slowdown in global and Chinese luxury car demand, b) lack of product acceptability in domestic PV business and c) maintaining cost advantage in CV business post BSVI.

Systematix

Institutional Equities

31 March, 2016

Priya Ranjan [email protected] +91 22 6704 8067

Bibhishan Jagtap [email protected] +91 22 6704 8068

INITIATING COVERAGE

Sector: Auto Rating: Buy

CMP: Rs389 Target Price: Rs550

Stock Info

Sensex/Nifty 25,339/ 7,735

Bloomberg TTMT IN

Equity shares 3,396 mn

52-wk High/Low Rs573/ 266

Face value Rs2

M-Cap Rs1,242bn/ $19bn

3-m Avg volume $54.6mn

Financial Snapshot (Rs mn)

Y/E March FY16e FY17e FY18e

Net sales 2,705,274 3,178,992 3,616,168

EBITDA 389,714 503,778 586,469

PBT 154,408 227,483 266,102

Net Profit 122,572 180,915 211,680

EPS (Rs) 36.1 53.3 62.3

P/E (x) 10.8 7.3 6.2

EV/EBIDTA (x) 4.5 3.6 3.1

P/B (x) 1.6 1.3 1.1

RoE % 15.3 18.5 17.8

RoCE (%) 9.5 11.5 11.6

Shareholding pattern (%)

Dec ’15 Sep ’15 Jun’15

Promoter 33.0 33.0 34.3

–Pledged - - -

FII 41.9 41.7 42.2

DII 17.3 17.2 16.3

Others 7.8 8.1 7.2

Stock Performance (1-year)

31 March, 2016

15 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

FINANCIALS (CONSOLIDATED)

Profit & Loss Statement

YE: Mar (Rs mn) FY14 FY15 FY16e FY17e FY18e

Net sales 2,306,771 2,607,343 2,705,274 3,178,992 3,616,168

Growth % 23 13 4 18 14

Other income 21,566 20,620 21,220 21,432 21,655

Total income 2,328,337 2,627,963 2,726,493 3,200,424 3,637,822

Growth % 23 13 4 17 14

Raw material expenses (1,435,864) (1,599,200) (1,665,887) (1,920,254) (2,182,693)

Employee expenses (215,564) (255,490) (272,649) (316,842) (360,144)

Other Operating expenses (302,879) (352,135) (398,243) (459,550) (508,516)

EBITDA (Core) 374,029 421,138 389,714 503,778 586,469

Growth, % 40.8 12.6 (7.5) 29.3 16.4

Margin, % 16.2 16.2 14.4 15.8 16.2

Depreciation (110,782) (133,886) (166,921) (203,496) (242,446)

EBIT 263,248 287,252 222,793 300,281 344,022

Growth, % 38.6 9.1 (22.4) 34.8 14.6

Margin, % 11.4 11.0 8.2 9.4 9.5

Interest paid (47,338) (48,615) (46,644) (50,464) (55,014)

Other Income 8,286 8,987 9,886 10,875 11,962

Pre-tax profit 198,544 218,873 154,408 227,483 266,102

Tax provided (47,648) (76,429) (30,882) (45,497) (53,220)

Profit after tax 150,896 142,444 123,526 181,987 212,881

Others (Minorities, Associates) (595) (868) (1,088) (1,206) (1,335)

Net Profit 149,764 141,710 122,572 180,915 211,680

Growth, % 41.4 - (12.4) 47.6 17.0

Net Profit (adjusted) 139,910 139,863 122,572 180,915 211,680

Source: Company, Systematix Institutional Research

Balance Sheet

YE: Mar (Rs mn) FY14 FY15 FY16e FY17e FY18e

Cash & bank 297,118 321,158 310,467 291,013 354,153

Debtors 105,742 125,792 133,411 156,772 178,332

Inventory 272,709 292,723 296,468 348,383 396,292

Loans & advances 217,548 208,384 230,900 257,019 287,317

Other current assets 152,987 86,578 86,578 86,578 86,578

Total current assets 1,046,103 1,034,635 1,057,824 1,139,765 1,302,672

Investments 106,867 153,623 203,623 253,623 303,623

Gross fixed assets 1,379,071 1,629,036 1,979,036 2,399,036 2,799,036

Less: Depreciation (688,154) (744,241) (911,162) (1,114,658) (1,357,104)

Add: Capital WIP 332,626 286,401 286,401 286,401 286,401

Net fixed assets 1,023,542 1,171,196 1,354,275 1,570,778 1,728,332

Total assets 2,176,512 2,359,454 2,615,722 2,964,167 3,334,627

Current liabilities 715,986 858,389 877,253 981,081 1,076,901

Provisions 201,610 211,703 210,939 211,449 211,090

Total current liabilities 917,596 1,070,091 1,088,192 1,192,531 1,287,990

Non-current liabilities 604,414 679,933 727,476 797,476 867,476

Total liabilities 1,522,010 1,750,025 1,815,668 1,990,007 2,155,466

Paid-up capital 6,438 6,438 6,792 6,792 6,792

Reserves & surplus 643,858 598,658 787,840 960,741 1,164,406

Shareholders’ equity 654,502 609,429 800,054 974,160 1,179,161

Total equity & liabilities 2,176,512 2,359,454 2,615,722 2,964,167 3,334,627

Source: Company, Systematix Institutional Research

Cash Flow

YE: Mar (Rs mn) FY14 FY15 FY16e FY17e FY18e

Pre-tax profit 198,544 218,873 154,408 227,483 266,102

Depreciation 110,782 133,886 166,921 203,496 242,446

Chg in working capital 22,944 188,004 (15,780) 2,944 (4,307)

Total tax paid (47,648) (76,429) (30,882) (45,497) (53,220)

CFO 284,621 464,334 274,668 388,427 451,020

Capital expenditure (398,464) (281,540) (350,000) (420,000) (400,000)

Chg in investments (16,290) (46,757) (50,000) (50,000) (50,000)

CFI (414,754) (328,296) (400,000) (470,000) (450,000)

Free cash flow (130,132) 136,037 (125,332) (81,573) 1,020

Equity raised/(repaid) 128,556 (192,916) 65,582 (7,981) (7,471)

Debt raised/(repaid) 80,509 80,754 47,543 70,000 70,000

Dividend (incl. tax) 73 (12) 1,517 100 (410)

CFF 206,270 (113,845) 114,642 62,119 62,119

Net chg in cash 76,137 22,193 (10,691) (19,454) 63,139

Opening cash balance 211,127 297,118 321,158 310,467 291,013

Closing cash balance 297,118 321,158 310,467 291,013 354,153

Source: Company, Systematix Institutional Research

Ratios

YE: Mar FY14 FY15 FY16e FY17e FY18e

EPS (Rs) 43.5 43.5 36.1 53.3 62.3

P/E (x) 8.9 9.0 10.8 7.3 6.2

P/B (x) 1.9 2.1 1.6 1.3 1.1

EV/EBITDA (x) 4.2 3.9 4.5 3.6 3.1

EV/EBIT (x) 6.0 5.7 7.8 6.1 5.3

EV/Net sales (x) 0.7 0.6 0.6 0.6 0.5

RoE (%) 21.5 23.1 15.3 18.5 17.8

RoCE (%) 14.7 11.8 9.5 11.5 11.6

Fixed Asset turnover (x) 2.6 2.5 2.4 2.4 2.4

Debtors (days) 16.7 17.6 18.0 18.0 18.0

WC (days) 1.8 (21.5) (18.6) (16.2) (13.8)

Net D/E ratio (%) 48.4 61.6 53.0 51.8 42.7

Revenue Growth (%) 23.3 12.9 3.7 17.4 13.7

EBIDTA Growth (%) 40.8 12.6 (7.5) 29.3 16.4

PAT Growth (%) 41.4 - (12.4) 47.6 17.0

EPS Growth (%) 40.2 - (16.9) 47.6 17.0

Source: Company, Systematix Institutional Research

31 March, 2016

16 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Charting the story

Chart 1: JLR volume growth to gather pace on SUV launches Chart 2: Domestic M&HCV and LCV growth chart

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 3: JLR average realisation to improve after blip in FY16e Chart 4: Standalone and JLR EBITDA margin trends

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 5: Earnings to accelerate on domestic turnaround Chart 6: Free cash flow trend of JLR

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

17 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Domestic business – return of golden goose

We believe TTMT’s domestic business is expected to return to its old glory as the key building blocks of all major businesses are either put in-place or weaknesses are getting addressed. Sharp focus on right/competitive/superior product launches in each segments (M&HCV, LCV, PV) along with improved customer focus and management decentralisation will improve market agility/responsiveness while avoiding the earlier mistake of hurried launches and bureaucratic/philanthropic market approach. TTMT has also embarked on a cost/vendor rationalisation drive to become more leaner and cost competitive under the new management, with some of the market share loss being deliberate to avoid SCV KYC scheme-like fiasco.

Chart 7: M&HCV business volume growth Chart 8: LCV business volume growth

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 9: PV business volume growth to accelerate

Source: Company, Systematix Institutional Research

31 March, 2016

18 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

The company has also recalibrated its distribution strategy to focus on the weak spots (Southern market for CV business) and rural market for SCV to diversify its business concentration and improve competitive challenges. Part of its recent market share loss in M&HCV has been attributed to product weakness in rigid MAVs and failure of its 37t vehicle on misplaced lift axle. We believe while the company is addressing product issues, a sharp growth upturn expected in tipper and TT segments bodes well for TTMT due to its product superiority versus major competitors. Signs of LCV/SCV segment recovery and impressive PV line-up (modular Nexon platform with eight models and Kite S) are expected to improve its volume and market share in both the segments significantly. We expect M&HCV, LCV and PV to register a volume growth of 17%/18%/19% during FY16e-18e.

New product launch – focus on design/reliability/exhaustive trials

We believe one of the key problems for TTMT has been its hurried product launches, lack of major pointed/regular investments on new products and lack of regular refreshes/refinements despite being a pioneer in many segments (MAVs, SCV, diesel, rural SUV), while customer impression being performance improvements only post launch. We believe the company has changed this approach in the last one to two years, with new launches only after extensive trails and new generation features aligned to customer tastes.

Chart 10: Nexon, Kite S, Signa trucks/1518 ICV

Source: Company

Nexon Kite S

1518 ICV Signa trucks

31 March, 2016

19 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Distribution reach – focus on qualitative increase and customer experience

We believe further quantitative distribution expansion-led growth will be limited for TTMT, given its strong nation-wide reach. However, a qualitative approach to weak geographies such as South (15 new dealerships in 2015), SCV rural outlets and similar opportunistic as well as targeted distribution reach can fetch a better yield. Also, an approach to train and penetrate/tie-up with secondary service providers along with mobile repair vans for shorter CV downtime will better its market/revenue share gains and improve vehicle resale value, given it has the maximum weightage on the purchase decision of CVs (TTMT has the highest resale value in industry). Secondary network tie-up improves genuine parts sales and penetration for OEMs, which is a highly profitable business.

Chart 11: Distribution network of Tata, AL, BB, VECV

Source: Company, Systematix Institutional Research

Duopoly may still exist; eye on BSVI preparedness

We believe the duopoly structure of HCV (TTMT and AL) and ICV (TTMT and VECV) industry to remain prevalent up to 2020, when the industry shifts to BSVI. However, lack of sufficient timeframe to prepare for BSVI norms will have to be watched carefully due to shortage of technology finalisation at the domestic players end. While global OEMs are slightly better prepared due to existing technology roadmap at their parent level, slackness at the end of domestic players can change the domestic duopoly structure significantly and can open the door for global OEMs in India.

Chart 12: HCV sales and market share Chart 13: LCV sales and market share

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

20 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Expect 20% revenue CAGR of domestic business in FY16e-18e

We expect the overall standalone business revenue to post a CAGR of ~20% over FY16e-18e and growth to be driven by both higher volume (18% CAGR) and realisation growth (2%). Our volume growth assumption for M&HCV, LCV and PV are 17%/18%/19% respectively.

Chart 14: Domestic volume and volume growth Chart 15: Domestic revenue and revenue growth

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Expect standalone EBITDA margin to bounce back to double digit

We believe TTMT’s standalone margin is likely to bounce back to 10%+ by FY17e-end or early FY18e, given the improvement in operating leverage on higher M&HCV and LCV volumes. Sharp capacity increase at LCV plants like Dharwad/Pantnagar among others will have significant operating leverage benefits. Cost and vendor rationalisation efforts to have positive margin impact too. We estimate domestic EBITDA margin to increase to 9.6%/10.3% in FY17e/18e from 5.8% in FY16e. We believe TTMT’s margin will recover to the earlier peak double digit level. Reduction in PV business losses and increase in LCV profitability on higher volume can scale up the margin significantly in the long term.

Chart 16: Domestic gross and EBITDA margin inch up Chart 17: Domestic business – EBITDA margin (FY18)

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

21 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Profitability to improve significantly

We expect TTMT’s standalone earnings to improve significantly to Rs38bn in FY18e from a reported loss in FY16. Key drivers for our earnings growth assumptions are 1) 17% volume CAGR respectively, 2) operating leverage on LCV and PV businesses and 3) 450bps margin expansion. We believe a robust profitability will also improve its already robust return ratios in the next couple of years.

Chart 18: PAT and PAT growth Chart 19: PAT margin trend

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

22 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

JLR business – falling in place after a year of hiccups

We believe JLR business will be back on track after a year of turbulence starting with the delay in engine plant and 2ltr diesel engine launch, product pricing issue of Evoque in China, slow ramp-up of CJLR amid working style difference between partners and staggered XE launch. We believe the delay in 2ltr gasoline engine launch has delayed XE launch in a key market like the US. Focus on sedan launches too had a bearing on overall volume growth due to the weakness in sedan brand equity.

Upcoming launches shifting to SUV segment (F-Pace, Discovery, Defender family, Sub-Evoque and so on) provide more volume comfort for JLR, given its strong brand equity in SUVs. Also, better acceptability of Discovery Sports in China along with ramp-up issue resolution in the Chinese JV and geographical spread of XE launch have improved growth and profitability visibility.

Chart 20: Jaguar volume growth Chart 21: Land Rover volume growth

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

SUV – key growth and most profitable segment

SUV remains the mainstay for JLR business and profitability as matching the sedan’s prowess to German peers is difficult to achieve. Global consumer shift towards SUV vehicle bodes well for JLR, being the most profitable product segment for the company. Also, gradual downscaling of vehicle engine options to in-house developed 2ltr engine (along with existing high power engine) will increase its addressable market significantly due to maximum volume being in the lower engine size. According to various studies, the global SUV market share in PV is expected to rise to 50% over the next few years, with higher SUV tilt in the luxury segment. JLR being the market leader in the high-end SUV segment, can easily encash on market opportunity by spreading to mid-luxury SUV segment on consumer preference.

Focus on development of engines above 2ltr

Post the 2ltr engine development, TTMT is planning to develop 3ltr engine and gasoline engines internally to reduce the dependence on Ford and meet future emission/fuel standards. The company is expanding its UK engine plant facility to increase in-house engine production and manufacture a wide variety of engines at its plant. We expect the gasoline 2ltr engine to be available from 2016, after a slight delay.

31 March, 2016

23 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

JLR – expect 13% volume and 15% revenue CAGR by FY18e

We expect JLR’s volume to post a CAGR of ~13% over FY16e-18e and growth to be driven by 32% in Jaguar and 8% in Land Rover volume growth respectively. In Jaguar too, the major growth contributor will be F-Pace. We believe our LR growth assumption is conservative and factors a major drop in Evoque to ~93k in FY18e, from FY15 peak of 123k units. We estimate 15% revenue CAGR during FY16e-18e, largely driven by volume. Partial business shift to Chinese JV and introduction of lower-priced model has impacted its overall revenue growth in FY16.

Chart 22: JLR’s volume and volume growth Chart 23: JLR’s revenue and revenue growth

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Conservative on margin – expect ~15% sustainable level

We believe JLR’s margin will stabilise ~15% in FY17e/18e on higher volume, superior mix of new launches in upcoming SUVs and higher parts supply to Chinese JV on business ramp-up and higher Chinese volume of imported models. However, we believe our margin assumption is conservative and it can reach ~16%+ on meaningful uptick in positive variant mix of upcoming launches, favourable currency and higher share of profitable geographies. We estimate 17% EBITDA CAGR during FY16e-18e on account of revenue growth and 50bps+ margin expansion.

Chart 24: JLR’s EBITDA margin Chart 25: JLR’s EBITDA/car

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

24 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Chart 26: JLR’s EBITDA and EBITDA growth assumption

Source: Company, Systematix Institutional Research

Profitability set to improve significantly

We expect JLR’s earnings to register 32% CAGR over FY16e-18e. Key drivers for our earnings growth assumptions are 1) 15% revenue CAGR, 2) 50bps+ margin expansion over FY16e-18e and 3) sharp improvement in CJLR profitability (GBP250mn by FY18e).

Chart 27: PAT and PAT growth Chart 28: PAT margin trend

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

CJLR (Chinese JV) – expect sharp jump in profitability

We expect a significant ramp-up of JV business with the launch of XE and strong traction of Discovery Sports volume in China. With the JV team cohesion issue now behind us, we expect significant improvement in CJLR profitability in FY17/18.

31 March, 2016

25 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Chart 29: CJLR profitability

Source: Company, Systematix Institutional Research

31 March, 2016

26 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Consolidated financial analysis

Expect 16% revenue CAGR between FY16e-18e

We expect consolidated revenue to post a CAGR of ~16% over FY16e-18e, driven by 20% growth in domestic business and 15% growth in JLR business. 18% and 13% volume CAGR in domestic and JLR will be the key revenue driver for each of the segment. We believe our revenue growth assumption is conservative for both domestic and JLR business.

Chart 30: Standalone and JLR volume growth assumption Chart 31: Consolidated revenue and revenue growth

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 32: Consolidated sales break-up by business Chart 33: Consolidated profit break-up by business (FY18)

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

27 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

We build consolidated margin of ~15% in FY17e/18e v/s 13% now

We believe margin is likely to go up to ~14.7%/15.2% in FY17e/18e on account of margin expansion in both domestic and JLR businesses. However, we believe our margin assumption is conservative due to potential surprise in JLR on superior mix and favourable currency. Also, revenue and margin assumption of domestic business is realistic in our view, which will significantly swing the profitability needle in the next two years. We expect consolidated EBITDA CAGR of 24% during FY16e-18e.

Chart 34: Consolidated gross margin Chart 35: Domestic and JLR EBITDA margin

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 36: Consolidated EBITDA and EBITDA margin assumption

Source: Company, Systematix Institutional Research

31 March, 2016

28 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Earnings set to improve significantly – 31% CAGR in FY16e-18e

We expect consolidated earnings to register 31% CAGR over FY16e-18e. Key drivers for our earnings growth assumptions are 1) sharp jump in domestic profitability from loss and JLR and JLR earnings CAGR of 32% and 2) 200bps consolidated margin expansion over FY16e-18e. We believe a sharp improvement in domestic/consolidated profitability will also improve its already robust return ratios in the next two years. We estimate consolidated RoE to improve to 18% by FY18e.

Chart 37: PAT and PAT growth Chart 38: PAT margin trend

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 39: Consolidated RoE trend

Source: Company, Systematix Institutional Research

31 March, 2016

29 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Valuation and view

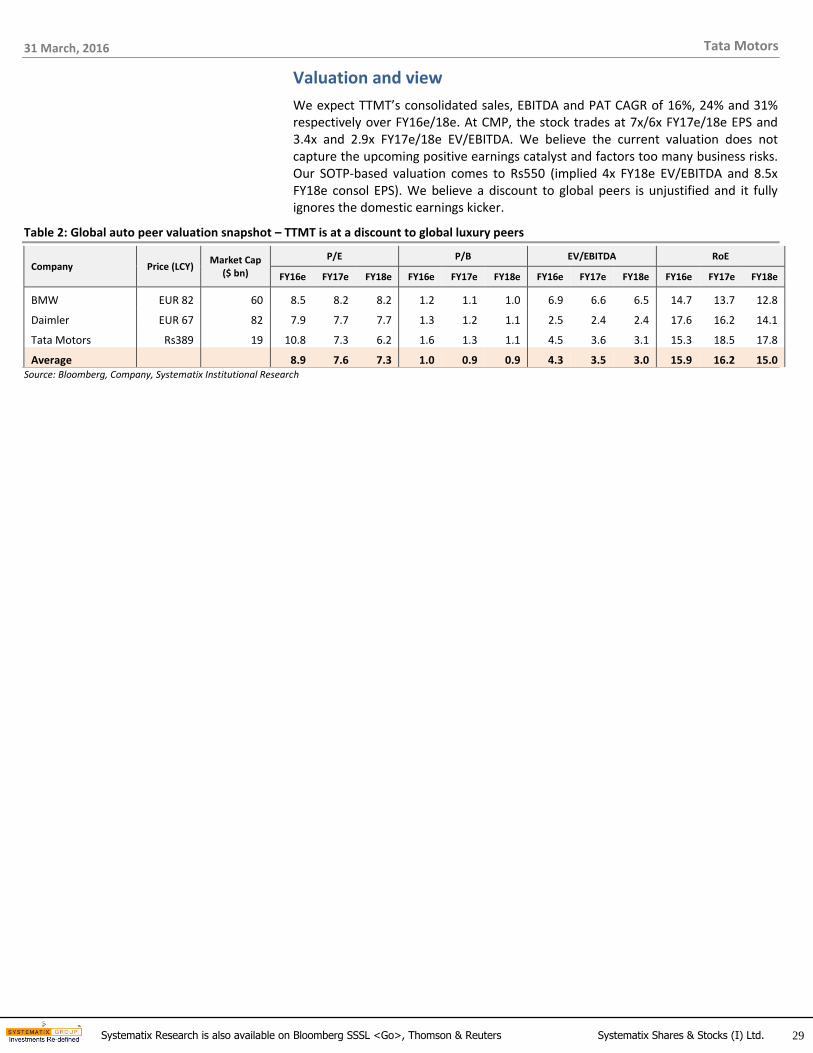

We expect TTMT’s consolidated sales, EBITDA and PAT CAGR of 16%, 24% and 31% respectively over FY16e/18e. At CMP, the stock trades at 7x/6x FY17e/18e EPS and 3.4x and 2.9x FY17e/18e EV/EBITDA. We believe the current valuation does not capture the upcoming positive earnings catalyst and factors too many business risks. Our SOTP-based valuation comes to Rs550 (implied 4x FY18e EV/EBITDA and 8.5x FY18e consol EPS). We believe a discount to global peers is unjustified and it fully ignores the domestic earnings kicker.

Table 2: Global auto peer valuation snapshot – TTMT is at a discount to global luxury peers

Company Price (LCY) Market Cap

($ bn)

P/E P/B EV/EBITDA RoE

FY16e FY17e FY18e FY16e FY17e FY18e FY16e FY17e FY18e FY16e FY17e FY18e

BMW EUR 82 60 8.5 8.2 8.2 1.2 1.1 1.0 6.9 6.6 6.5 14.7 13.7 12.8

Daimler EUR 67 82 7.9 7.7 7.7 1.3 1.2 1.1 2.5 2.4 2.4 17.6 16.2 14.1

Tata Motors Rs389 19 10.8 7.3 6.2 1.6 1.3 1.1 4.5 3.6 3.1 15.3 18.5 17.8

Average

8.9 7.6 7.3 1.0 0.9 0.9 4.3 3.5 3.0 15.9 16.2 15.0 Source: Bloomberg, Company, Systematix Institutional Research

31 March, 2016

30 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Tata Motors

Company background

Tata Motors is a part of the US$100bn Tata group founded by Jamsetji Tata in 1868. Tata Motors is a leading global automobile manufacturer, with a portfolio that covers a wide range of cars, sports vehicles, buses, trucks and defence vehicles. Tata Motors has auto manufacturing and assembly plants in Jamshedpur, Pantnagar, Lucknow, Sanand, Dharwad and Pune in India, as well as in Argentina, South Africa, Thailand and the United Kingdom. It has research and development centres in Pune, Jamshedpur, Lucknow and Dharwad, India and in South Korea, Spain and the United Kingdom. The company has built a strong global network of subsidiaries and associate companies, including Jaguar Land Rover in the UK and Tata Daewoo in South Korea.

Table 3: Key management team

Name Designation Profile

Cyrus P Mistry Non-Executive Director and Chairman

He is a graduate of civil engineering from the Imperial College London (1990) and has an MSc in Management from the London Business School (1997). Mistry was appointed as a Director of Tata Motors with effect from May 29, 2012, and as deputy chairman of the company with effect from Nov 7, 2012. He was earlier managing director of the Shapoorji Pallonji group and was also responsible for building the infrastructure development vertical in Shapoorji Pallonji group.

Guenter Butschek CEO and Managing Director (Tata Motors)

He is a graduate in Business Administration and Economics, with a diploma from the University of Cooperative Education Stuttgart, Germany. He was previously associated with the Airbus group, where he served as COO of Airbus and a member of the Group Executive Committee. Prior to Airbus, he worked at Daimler AG, where he gained more than 25 years of experience in international automotive management, holding functions like production, industrialisation and procurement. Butschek was appointed as an Additional Director of Tata Motors with effect from Feb 15, 2016.

C Ramakrishnan President and Group Chief Financial Officer

He holds a Bachelor's degree in Commerce and is a Chartered Accountant and a Cost Accountant. He has been the Group Chief Financial Officer at Tata Motors since Sept 18, 2007 and serves as its President and Compliance Officer. Ramakrishnan is responsible for Finance, Accounts, Taxation, Business Planning, Investor Relations, Treasury, CRM & DMS and IT. He served as Vice-President of Chairman's office and Executive Director of Finance of Tata Motors.

Ralf Speth Non-Executive Director (CEO, JLR)

He has done his engineering from Rosenheim University, Germany and is a Doctorate of Engineering in Mechanical Engineering and Business Administration from Warwick University. Speth was appointed to the post of Chief Executive Officer at Jaguar Land Rover on Feb 18, 2010. He served BMW for 20 years, and was with Ford Motor Company’s Premier Automotive Group as Director of Production, Quality and Product Planning.

Ravindra Pisharody Executive Director (Commercial Vehicles)

He is an alumnus of IIT, Kharagpur and IIM, Kolkata. He is the Executive Director (Commercial Vehicles) since June 21, 2012, having joined Tata Motors as Vice-President Commercial Vehicles (Sales & Marketing), in 2007. Before joining Tata Motors he worked with Castrol Ltd, a subsidiary of BP, and with Philips India, a subsidiary of the Dutch company in various roles.

Mayank Pareek President (Passenger Vehicle Business Unit)

He is a Post Graduate Diploma in Business Management from IIM, Bangalore and a Bachelor of Engineering Degree from IIT, BHU. He has been President of Passenger Vehicle Business Unit at Tata Motors since October 2014. He began his career in 1982 with BHEL and worked in the manufacturing function and joined Maruti Udyog in 1991. Pareek served as the Chief Operating Officer and Managing Executive Officer of Marketing & Sales at Maruti Suzuki until May 2, 2014.

Source: Company

Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Investors are advised to refer through disclosures made at the end of the research report.

31

Eicher Motors

Strong business with high valuation and limited upside

We initiate coverage on Eicher Motors (EIM), a cult cruiser bike manufacturer and a key Indian commercial vehicle player (VECV; JV with Volvo group) with a Hold rating and a target price of Rs19,250. Renaissance of the cult “Royal Enfield” brand in India in the last five years, with product interventions/quality improvement is commendable. We believe the company’s relatively less-talked hero in recent times “VECV” will be the key mid-term driver as all the success recipe is in place – diminution of CV pricing gaps on industry’s technology shift, fortification of back-end (sales/service/parts set-up) and accessibility of high HP engine (legacy issue). We believe EIM’s resolve to replicate the Indian success in global mid-size bike market will be arduous and time consuming as domestic RE market is hitting near-term capacity and relative market maturity bumps.

Payoff time for VECV – all inputs are perfectly placed: We believe the VECV business will see major positive shift in the next three years, with both HCV and exports business are on a take-off stage, while maintaining the strength of LMD and Bus segments. In our view, higher HP engine availability with domestic plant (Volvo technology and key issues in EIM’s legacy HD range), reduction of pricing gaps with incumbents on diminution of technology gaps (BSIV in Apr-17/BSVI in Apr-20) and other regulatory interventions (on-board-diagnostic and inconformity compliance) and sales/service/parts network expansion will provide impetus to VECV HCV business from FY18. Recalibration of exports focus with products developed for local market needs (Indonesia/South Africa among others) and using Volvo group’s distribution network (UD, Renault, Mack) is expected to start contributing from 2018 onwards.

Expect LMD market share to remain ~35% due to customer traction, while the Bus and HCV market share to improve 25% and 6% respectively on filling of product gaps

Estimate LMD/Bus/HCV CAGR of 14%/17%/10% over the next four years

Royal Enfield (RE) – focus on repeating Indian success elsewhere: We expect the domestic RE growth rate to normalise (16% CAGR) over the next five years, from a hyper growth phase (54% CAGR during CY10-15), despite lots of penetration opportunity. We believe RE will focus initially on commonwealth countries (brand legacy) and countries with biking culture like Spain with product launches suitable to these markets. The export market development will be a long-term process (highlighted by MD), with sustained brand building exercise, and we expect the export market to reach 4% of total volume in FY20e, from 2% currently. We believe the low hanging fruits have been plucked in the domestic market and an incremental pull will require further cult design (not impossible, but tough). The management’s focus shift to overseas market partly reaffirms our view.

Estimate 35% and 32% standalone and consolidated earnings CAGR: We estimate consolidated sales/EBITDA/PAT CAGR of 21%/26%/32% respectively over the next four years, driven by 14% and 16% volume growth in CV and RE business. We expect RE business sales/EBITDA/PAT CAGR of 25%/28%/30% on 16% volume CAGR and 300bps margin expansion. We believe the company is in a sweet spot for RE margin, with many levers to grow it further. VECV margins to rebound to earlier levels of 9% as volume/pricing of Pro series improves on BSIV.

Initiate coverage with Hold: At CMP, the stock trades at 28x/22x FY17e/18e EPS. Our SOTP-based valuation comes to Rs19,250 (assigning 25x and 15x PER to RE and VECV respectively; implied 23x FY18e consolidated EPS). Although near-term growth is robust, we are cautious on its future occurrence probability. Key risks to our assumptions are a) lack of export take-off in RE, b) lack of product acceptability in CV business and c) product performance issue in RE, post BSVI implementation in 2Ws.

Systematix

Institutional Equities

31 March, 2016

Priya Ranjan [email protected] +91 22 6704 8067

Bibhishan Jagtap [email protected] +91 22 6704 8068

INITIATING COVERAGE

Sector: Auto Rating: Hold

CMP: Rs18,709 Target Price: Rs19,250

Stock Info

Sensex/Nifty 25,339/ 7,735

Bloomberg EIM IN

Equity shares 27 mn

52-wk High/Low Rs21,618/ 13,930

Face value Rs10

M-Cap Rs507bn/ $8bn

3-m Avg volume $18mn

Financial Snapshot (Rs mn)

Y/E March FY16e FY17e FY18e Net Sales 130,723 165,509 196,164

EBIDTA 21,599 31,713 37,935

PBT 18,570 28,268 33,951

Net Profit 11,401 17,642 22,277

EPS (Rs) 419.9 649.8 820.5

P/E (x) 43.4 28.1 22.2

EV/EBIDTA (x) 22.5 15.0 12.1

P/B (x) 11.8 9.1 7.2

RoE (%) 27.2 32.3 32.4

RoCE (%) 22.9 29.5 29.3

Shareholding pattern (%)

Dec ’15 Sep ’15 Jun ’15

Promoter 54.8 54.9 54.9

–Pledged - - -

FII 26.6 27.2 27.1

DII 5.0 4.2 5.0

Others 13.6 13.7 13.0

Stock Performance (1-year)

31 March, 2016

32 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Eicher Motors

FINANCIALS (CONSOLIDATED)

Profit & Loss Statement

YE: Mar (Rs mn) CY14 CY15 FY16e FY17e FY18e

Net sales 85,987 117,268 130,723 165,509 196,164

Growth, % 29 36 11 27 19

Other income 1,396 1,970 2,169 2,383 2,628

Total income 87,383 119,238 132,892 167,892 198,792

RM expenses (57,660) (77,082) (84,888) (104,395) (123,515)

Employee expenses (6,596) (8,302) (9,134) (11,382) (13,447)

Other expenses (76,235) (101,165) (111,293) (136,179) (160,857)

EBITDA (Core) 11,148 18,073 21,599 31,713 37,935

Growth, % 56.3 62.1 19.5 46.8 19.6

Margin, % 13.0 15.4 16.5 19.2 19.3

Depreciation (2,198.2) (3,430.9) (4,011.4) (4,545.2) (5,179.2)

EBIT 8,950 14,642 17,587 27,168 32,756

Growth, % 53.5 63.6 20.1 54.5 20.6

Margin, % 10.4 12.5 13.5 16.4 16.7

Interest paid (97.8) (80.6) (60.0) (60.0) (60.0)

Other Income 1,074.4 838.7 1,042.4 1,160.0 1,255.0

Pre-tax profit 9,926 15,401 18,570 28,268 33,951

Tax provided (2,909) (4,706) (5,666) (8,198) (9,325)

PAT (Reported) 7,017 10,695 12,903 20,069 24,626

Growth, % 56.2 53.3 20.9 54.7 26.3

Net Profit (adjusted) 6,154 9,434 11,401 17,642 22,277

Source: Company, Systematix Institutional Research

Balance Sheet

YE: Mar (Rs mn) CY14 CY15 FY16e FY17e FY18e

Cash & bank 4,806 5,691 8,486 21,222 35,602

Debtors 5,622 7,834 8,091 10,018 11,193

Inventory 6,455 8,848 9,522 11,865 14,064

Loans & advances 8,578 9,756 11,152 13,944 16,010

Other current assets 557 1,063 802 802 802

Total current assets 26,018 33,192 38,052 57,852 77,672

Investments 10,777 16,114 20,042 18,605 20,398

Gross fixed assets 31,374 41,419 44,258 51,758 59,258

Less: Depreciation (8,280) (11,592) (15,103) (19,148) (23,828)

Add: Capital WIP 4,188 2,728 5,000 5,000 5,000

Net fixed assets 27,281 32,555 34,155 37,610 40,430

Total assets 64,076 81,862 92,248 114,066 138,501

Current liabilities 21,708 29,155 27,982 33,293 38,181

Provisions 3,213 2,052 5,774 7,553 11,072

Total current liabilities 24,921 31,206 33,756 40,846 49,253

Non-current liabilities 3,146 4,356 3,816 3,816 3,816

Total liabilities 28,067 35,563 37,572 44,662 53,069

Paid-up capital 271 272 272 272 272

Reserves & surplus 24,888 34,289 41,618 54,374 68,506

Shareholders’ equity 36,009 46,299 54,676 69,405 85,432

Total equity & liabilities 64,076 81,862 92,248 114,066 138,501

Source: Company, Systematix Institutional Research

Cash Flow

YE: Mar (Rs mn) CY14 CY15 FY16e FY17e FY18e

Pre-tax profit 9,926 15,401 18,570 28,268 33,951

Depreciation 2,198 3,431 4,011 4,545 5,179

Chg in working capital 475 1,540 (2,959) (1,222) (128)

Total tax paid (2,320) (3,922) (5,666) (8,198) (9,325)

CFO 10,280 16,450 13,956 23,392 29,678

Capital expenditure (8,282) (8,705) (5,611) (8,000) (8,000)

Chg in investments (2,522) (5,337) (3,927) 1,437 (1,793)

CFI (10,805) (14,042) (9,539) (6,563) (9,793)

Free cash flow (525) 2,408 4,418 16,829 19,884

Equity raised/(repaid) (4,995) (9,910) (9,510) (15,997) (17,839)

Debt raised/(repaid) (223) 427 (540) - -

Dividend (incl. tax) (857) (1,545) (424) (3,394) (4,642)

CFF (6,485) (11,401) (10,928) (19,844) (22,934)

Net chg in cash (7,010) (8,993) (6,511) (3,015) (3,050)

Opening cash balance 6,826 4,806 5,691 8,486 21,222

Closing cash balance 4,806 5,691 8,486 21,222 35,602

Source: Company, Systematix Institutional Research

Ratios

YE: Mar CY14 CY15 FY16e FY17e FY18e

EPS (Rs) 227.1 347.5 419.9 649.8 820.5

P/E (x) 80.3 53.8 43.4 28.1 22.2

P/B (x) 20.2 14.7 11.8 9.1 7.2

EV/EBITDA (x) 45.1 27.9 22.5 15.0 12.1

EV/Net sales (x) 5.8 4.3 3.7 2.9 2.3

RoE (%) 24.5 27.3 27.2 32.3 32.4

RoCE (%) 18.8 23.1 22.9 29.5 29.3

Fixed Asset turnover (x) 3.6 4.1 3.9 4.3 4.6

Dividend Yield (%) 0.3 - 0.7 0.8 1.3

Debtors days 23.9 24.4 22.6 22.1 20.8

WC days (9.3) (5.6) (5.6) (3.3) (7.5)

Revenue Growth (%) 28.3 36.5 11.5 26.3 18.4

EBIDTA Growth (%) 56.3 62.1 19.5 46.8 19.6

PAT Growth (%) 56.2 53.3 20.9 54.7 26.3

EPS Growth (%) 56.2 53.0 20.9 54.7 26.3

Source: Company, Systematix Institutional Research

31 March, 2016

33 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Eicher Motors

Charting the story

Chart 1: VECV’s volume growth to gather momentum Chart 2: RE’s volume growth to taper from earlier levels

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 3: RE average realisation growth Chart 4: EBITDA margin and gross margin expands

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 5: Earnings to accelerate on volume growth Chart 6: Free cash flow and free cash flow as % of EBITDA

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

31 March, 2016

34 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Eicher Motors

RE – domestic hyper growth phase over; search for new growth catalysts

We believe Royal Enfield’s (RE) multi-year hyper growth phase is almost over, with domestic demand growth being more secular and steady. So far, the company has been successful in widening its appeal to the new young and mobility-driven customers, without diluting its core brand equity among enthusiasts. The domestic low hanging fruits have been plucked by bringing the brand to mainstream premium bike segment, with much easier riding experience and improved after sales service. Although demographics indicate immense growth potential, we believe the market potential for a premium bike has volume limitation of ~60-70k/month as we have seen in the case of earlier premium Bajaj Pulsar (volume restricted to ~70k at peak), as brand fatigue and too much visibility seeps in.

Chart 7: Volume growth to normalise Chart 8: Revenue and revenue growth to normalise too

Source: Company, Systematix Institutional Research Source: Company, Systematix Institutional Research

Chart 9: RE model wise sales mix – Classic 350 is the key driver

Source: Company, Systematix Institutional Research

31 March, 2016

35 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Eicher Motors

Though dealership expansion and market penetration (smaller towns and rural areas) opportunities exist, we believe this will also coincide with market share loss to HD, Triumph and UM’s mid-range bikes in bigger cities. We have seen this in the case of limited success of Continental GT, where the products are positioned against global biggies such as Triumph or HD with 500cc+ engine. We believe competition will emerge in the mid-range bike segment with UM’s entry and a very attractive price range of Rs150-200k. We expect RE to register a volume growth of 16% during FY16e-20e, with growth being more front-ended (22% and 20% in FY17e and FY18e respectively). We believe the current monthly order intake of ~35-40 days of shipment would suffice the 700-750k annual volume, and demand visibility beyond that is limited.

31 March, 2016

36 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Eicher Motors

Customer tilt moving towards more commuters

Over the past few years, RE has considerably widened the customer base to leisure weekend/fortnightly bikers (100km usage per week) and young daily commuters, with entry level salary in the range of Rs50k+ without any financial/family liabilities. We believe this commuter tilt (partially promoted by company too with a disguised focus on improving the fuel economy of its engine) may help expand its catchment area initially but may restrict its halo effect in the long term as few of these users may not come back to buy another bike or may simply upgrade to more premium global brands like HD and Triumph when needed.

Two key segments driving RE’s strong growth

Weekend leisure driver (age group 35-45 years): We note these customers are typically an established professional whose daily transport mode is primarily a car, but uses RE for weekend long drives to nearby weekend gateways by using better and improved highways. This customer segment will have limited use and the replacement cycle will be very high, with few users unlikely to buy another bike.

Daily commuter (age group 21-30 years): These young and mobile customer segments using the bike on a daily basis for their commuting requirements. Typically, they have upgraded from an entry level sports motorcycle (Bajaj Pulsar, TVS Apache) to the cruiser segment after entry into workforce as a fresher. These users have a higher disposable income due to limited financial liabilities. We believe EIM is working on this segment, with improved fuel economy in its new 400cc and 600cc engines.

New product introduction – not every bike can add volume significantly

We believe the new launches such as Himalaya and Continental GT are unlikely to be the key future volume drivers like Classic, as these will be specialist enthusiast bikes, rather than the mass premium volume brand. We have seen a volume decline at Continental GT after the initial euphoria, which is a case in point. We believe the company is working on many new models for the export market to suit and penetrate these markets and is working on BSIV upgrade for its domestic models. We also note that RE bikes costing more than Rs150k (Thunderbird and Continental GT) have lesser appeal or sales traction than the sub-Rs150k units like Classic 350 or Bullet.

Chart 10: Continental GT Chart 11: Himalayan

Source: Company

31 March, 2016

37 Systematix Research is also available on Bloomberg SSSL <Go>, Thomson & Reuters Systematix Shares & Stocks (I) Ltd.

Eicher Motors

Exports market – unlikely to swing needle by FY20 in a major way