Global Energy Scenarios 2050 25. Juni 2013. Paul Scherrer Institute, Switzerland Global Energy...

20

25. Juni 2013 PSI, 25. Juni 2013 PSI, Paul Scherrer Institute, Switzerland Global Energy Scenarios 2050 of the World Energy Council IEW 2013, Paris Martin Densing, Hal Turton, Evangelos Panos, Kathrin Volkart

Transcript of Global Energy Scenarios 2050 25. Juni 2013. Paul Scherrer Institute, Switzerland Global Energy...

25. Juni 2013PSI, 25. Juni 2013PSI,

Paul Scherrer Institute, Switzerland

Global Energy Scenarios 2050of the World Energy Council

IEW 2013, Paris

Martin Densing, Hal Turton, Evangelos Panos, Kathrin Volkart

Seite 2

Contents

• Why another global energy-system scenario-study?

• Regional disaggregation of the PSI/WEC model

• Model structure, scenario assumptions, and resultsfocusing on transport sector sub-model

[PSI/WEC Global Mobility 2050]

Global results of whole energy system are launched atWorld Energy Congress in Daegu, South Korea, Oct. 2013

Seite 3

Global energy scenarios: TPES and CO2 emissions

0204060

tCO

2/y

NA

Total Primary Energy Supply, year 2030

0%

20%

40%

60%

80%

100%6D

S

4DS

2DS

New

Pol

icy

Cur

rent

Pol

icy

450

Sup

ply

Effi

cien

cy Mix

Ref

eren

ce

Mou

ntai

ns

Oce

ans

Ref

eren

ce

Rev

olut

ion

New

norm

al

Out

look

ETP WEO GEA EIA Shell Green-peace

BNEFExxon

OthersRenewablesBiomassNuclearGasOilCoalFossil

Seite 4

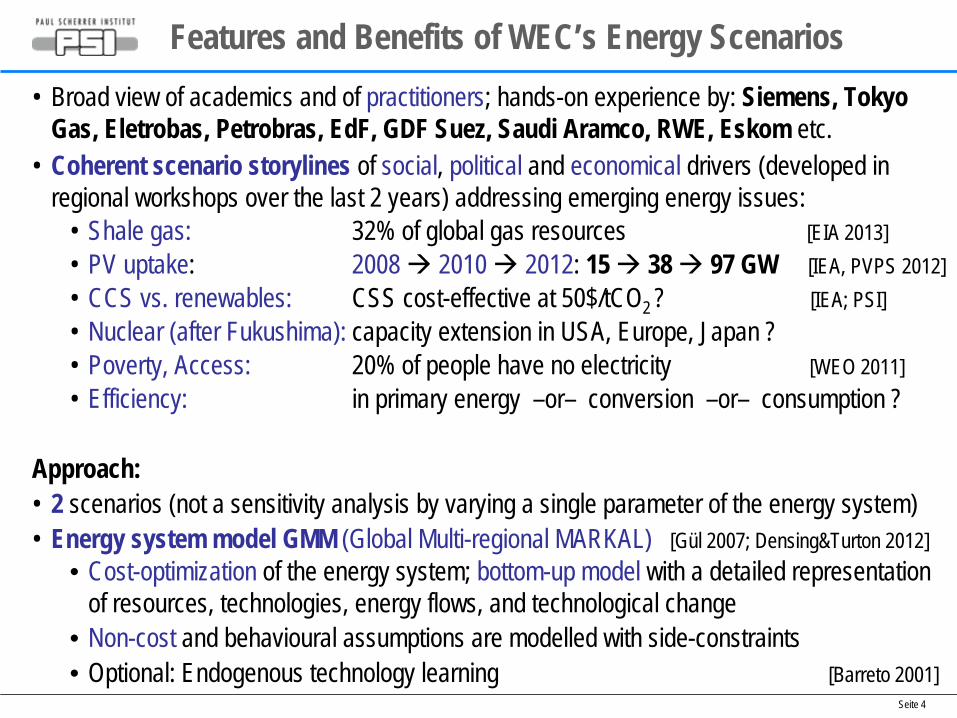

Features and Benefits of WEC’s Energy Scenarios• Broad view of academics and of practitioners; hands-on experience by: Siemens, Tokyo

Gas, Eletrobas, Petrobras, EdF, GDF Suez, Saudi Aramco, RWE, Eskom etc. • Coherent scenario storylines of social, political and economical drivers (developed in

regional workshops over the last 2 years) addressing emerging energy issues:• Shale gas: 32% of global gas resources [EIA 2013]• PV uptake: 2008 2010 2012: 15 38 97 GW [IEA, PVPS 2012]• CCS vs. renewables: CSS cost-effective at 50$/tCO2 ? [IEA; PSI]• Nuclear (after Fukushima): capacity extension in USA, Europe, Japan ?• Poverty, Access: 20% of people have no electricity [WEO 2011]• Efficiency: in primary energy –or– conversion –or– consumption ?

Approach:• 2 scenarios (not a sensitivity analysis by varying a single parameter of the energy system)• Energy system model GMM (Global Multi-regional MARKAL) [Gül 2007; Densing&Turton 2012]

• Cost-optimization of the energy system; bottom-up model with a detailed representation of resources, technologies, energy flows, and technological change

• Non-cost and behavioural assumptions are modelled with side-constraints• Optional: Endogenous technology learning [Barreto 2001]

Seite 5

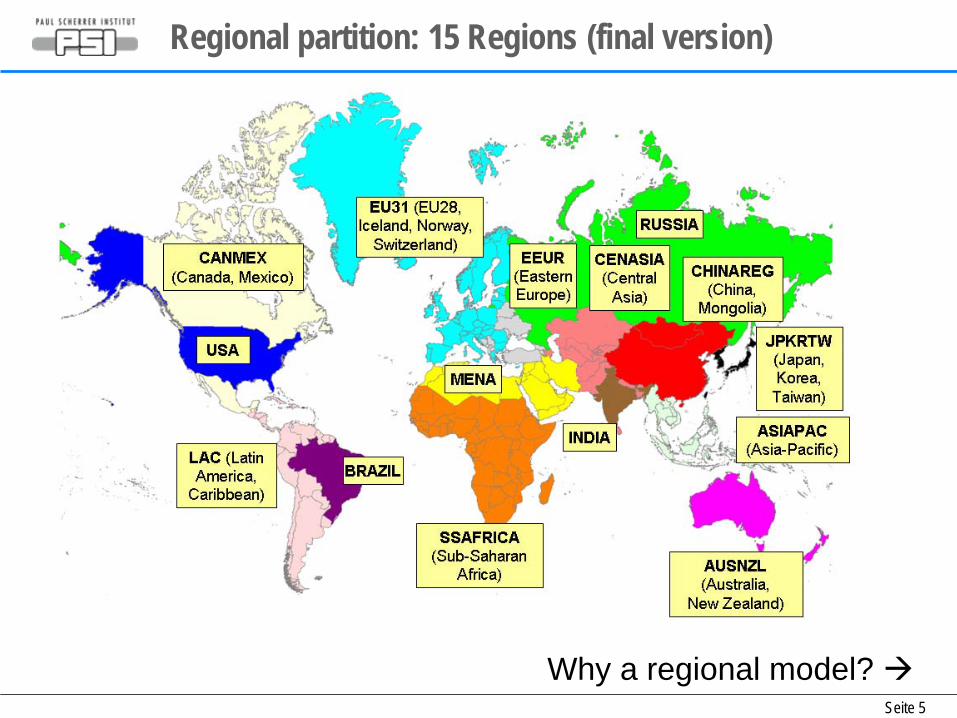

Regional partition: 15 Regions (final version)

Why a regional model?

Seite 6

Regional partition: Diversity of TPES and of trade

Domestic production of primary energy(year 2010)

Net import(% of total primary energy supply)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

ASIAPAC

AUSNZL

BRAZIL

CANMEX

CENASIA

CHINAREG

EEUREU31

INDIA

JPKRTW LA

CMENA

RUSSIA

SSAFRICA

USAWorld

GeothermalSolarWindHydroBiomassNuclearGasOilCoal

-150%

-100%

-50%

0%

50%

100%

ASIAPAC

AUSNZLBRAZIL

CANMEXCENASIA

CHINAREGEEUREU31IN

DIAJP

KRTW

LAC

MENARUSSIA

SSAFRICA

USA

BRAZIL: Bio -0.4%, Oil: 0.1%; CHINAREG: Gas 0.5%; INDIA: Gas 1.5%; LAC: Bio -0.4%; EU31: Bio: 0.3%

BiomassGasOilCoal

Source: IEA (2012), Energy Balances. Nuclear effi. 33%; geothermal effi. = 10%; solar, hydro and wind: actual production.

Seite 7

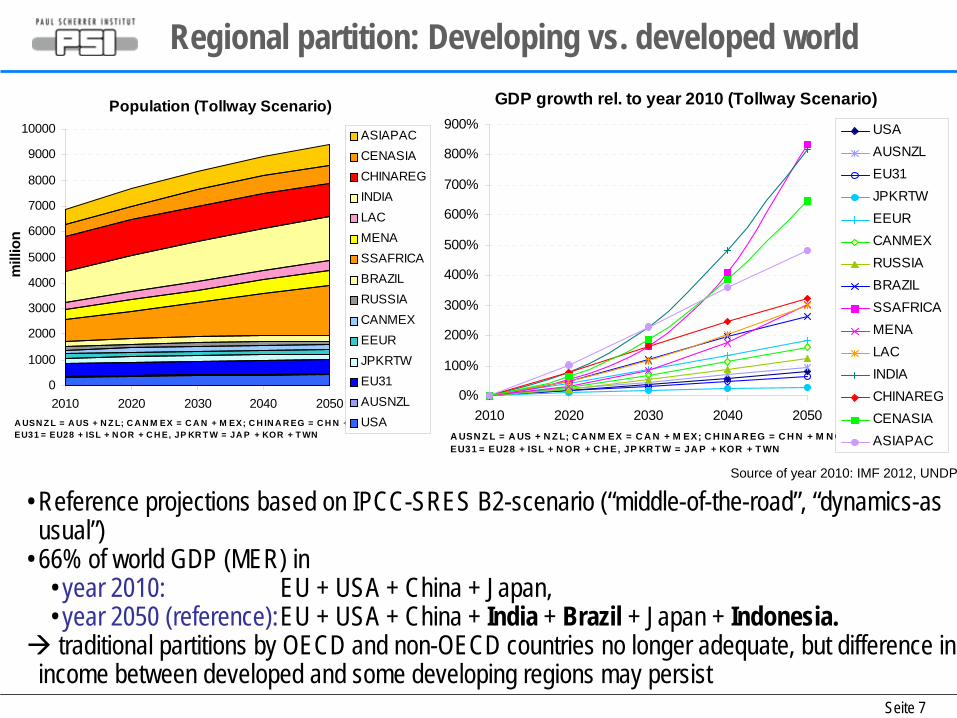

Regional partition: Developing vs. developed world

• Reference projections based on IPCC-SRES B2-scenario (“middle-of-the-road”, “dynamics-as usual”)

• 66% of world GDP (MER) in • year 2010: EU + USA + China + Japan, • year 2050 (reference):EU + USA + China + India + Brazil + Japan + Indonesia.

traditional partitions by OECD and non-OECD countries no longer adequate, but difference in income between developed and some developing regions may persist

Population (Tollway Scenario)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2010 2020 2030 2040 2050A USN Z L = A US + N Z L; C A N M EX = C A N + M EX; C H IN A R EG = C H N + M N G; EU31 = EU28 + ISL + N OR + C H E, JP KR T W = JA P + KOR + T WN

mill

ion

ASIAPACCENASIACHINAREGINDIALACMENASSAFRICABRAZILRUSSIACANMEXEEURJPKRTWEU31AUSNZLUSA

GDP growth rel. to year 2010 (Tollway Scenario)

0%

100%

200%

300%

400%

500%

600%

700%

800%

900%

2010 2020 2030 2040 2050A USN Z L = A US + N Z L; C A N M EX = C A N + M EX; C H IN A R EG = C H N + M N G; EU31 = EU28 + ISL + N OR + C H E, JP KR T W = JA P + KOR + T WN

USAAUSNZLEU31JPKRTWEEURCANMEXRUSSIABRAZILSSAFRICAMENALACINDIACHINAREGCENASIAASIAPAC

Source of year 2010: IMF 2012, UNDP

Seite 8

Reference Energy System (Flow of Energy Carriers)

GMM has approx. 400 technologies per region T&D: Transport and Distribution

Conversion ProcessesResources End-Use

Oil

Natural Gas

Biomass

OtherRenewables

Uranium

Coal

Refinery

Heat Plants

Methanol fromNatural Gas

BiofuelsProduction

Power Plants

HydrogenProduction

T&D

T&D

T&D

CNG

Residential/Commercial

Thermal

Residential/Commercial

Specific

Industry Specific

Industry Thermal

PersonalTransport

Aviation

Other Transport

Non-commercialBiomass

Oil Products

Coal

T&D

T&D

T&D

Transport Sector

Seite 9

Personal Transport Sector• Drivetrains: Internal Combustion Engine Vehicle (ICEV), Advanced ICEV, Hybrid Electric (HEV),

Plug-in (PHEV), Battery Electric (BEV), Hydrogen Fuel Cell with hybridisation (HFCV)• Fuels: conventional liquid (gasoline, diesel); alternatives fuels: natural gas, electricity, hydrogen,

different biofuels; fuel blending (e.g. maximal 10% (Bio-)Methanol into gasoline)

Gasoline ICEV

Gas. Adv. ICEV

Gasoline HEV

Diesel ICEV

Diesel Advanced ICEV

Diesel HEV

CNG ICEV

CNG HEV

BEV

PHEV

Hydrogen Hybrid

HFCVHydrogen Retail

Electricity (ELC)

Compression

Gasoline Retail Station

Diesel Retail Station

blend

blend

blend

blend

blend

blend

blend

blend

ELC

Blending Constraints

Short-Range Car Version

T&D

T&D

T&D

T&DEthanol (Bio)

Bio-Methanol

Biodiesel (FT)

Bio-Syngas

T&DDiesel

T&DGasoline

T&DMethanol

T&DNatural Gas

WEC/PSI (2011): Global Transport Scenarios 2050

~100 km actual drive

range

Seite 10

Other Surface Transport and Aviation Sector

• Trucks, buses, other commercial road vehicles, 2-wheel, rail, ships: aggregated by fuel option• Aviation: current + future technology

technologies categorized by• fuelling option, and• engine type

WEC/PSI (2011): Global Transport Scenarios 2050

Seite 11

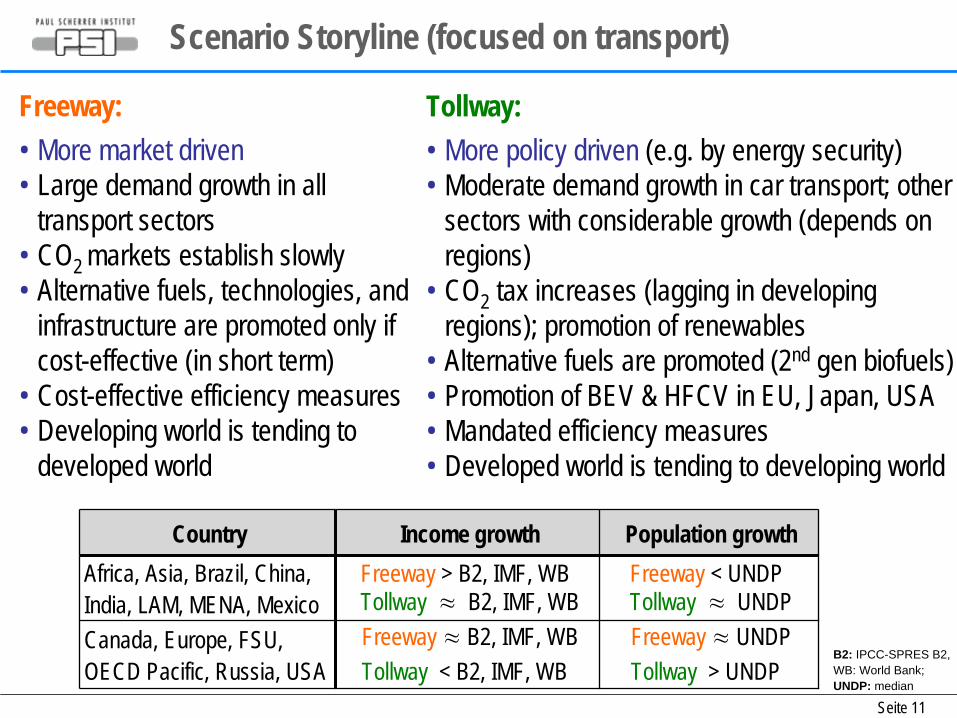

Scenario Storyline (focused on transport)

Freeway:• More market driven• Large demand growth in all

transport sectors• CO2 markets establish slowly• Alternative fuels, technologies, and

infrastructure are promoted only if cost-effective (in short term)

• Cost-effective efficiency measures• Developing world is tending to

developed world

Tollway:• More policy driven (e.g. by energy security)• Moderate demand growth in car transport; other

sectors with considerable growth (depends on regions)

• CO2 tax increases (lagging in developing regions); promotion of renewables

• Alternative fuels are promoted (2nd gen biofuels)• Promotion of BEV & HFCV in EU, Japan, USA• Mandated efficiency measures• Developed world is tending to developing world

Country Income growth Population growthAfrica, Asia, Brazil, China, India, LAM, MENA, Mexico

Freeway > B2, IMF, WBTollway ≈

B2, IMF, WBFreeway < UNDPTollway ≈

UNDPCanada, Europe, FSU, OECD Pacific, Russia, USA

Freeway ≈ B2, IMF, WBTollway < B2, IMF, WB

Freeway ≈ UNDPTollway > UNDP

B2: IPCC-SPRES B2, WB: World Bank; UNDP: median

Seite 12

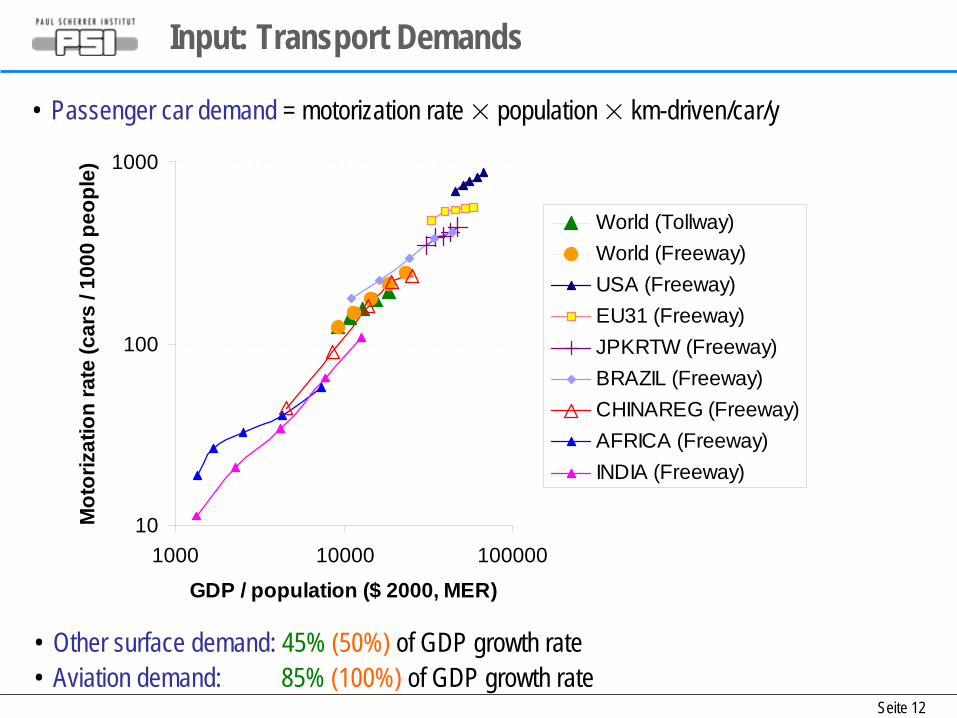

Input: Transport Demands

• Passenger car demand = motorization rate × population × km-driven/car/y

• Other surface demand: 45% (50%) of GDP growth rate• Aviation demand: 85% (100%) of GDP growth rate

10

100

1000

1000 10000 100000

GDP / population ($ 2000, MER)

Mot

oriz

atio

n ra

te (c

ars

/ 100

0 pe

ople

)

World (Tollway)World (Freeway)USA (Freeway)EU31 (Freeway)JPKRTW (Freeway)BRAZIL (Freeway)CHINAREG (Freeway)AFRICA (Freeway)INDIA (Freeway)

Seite 13

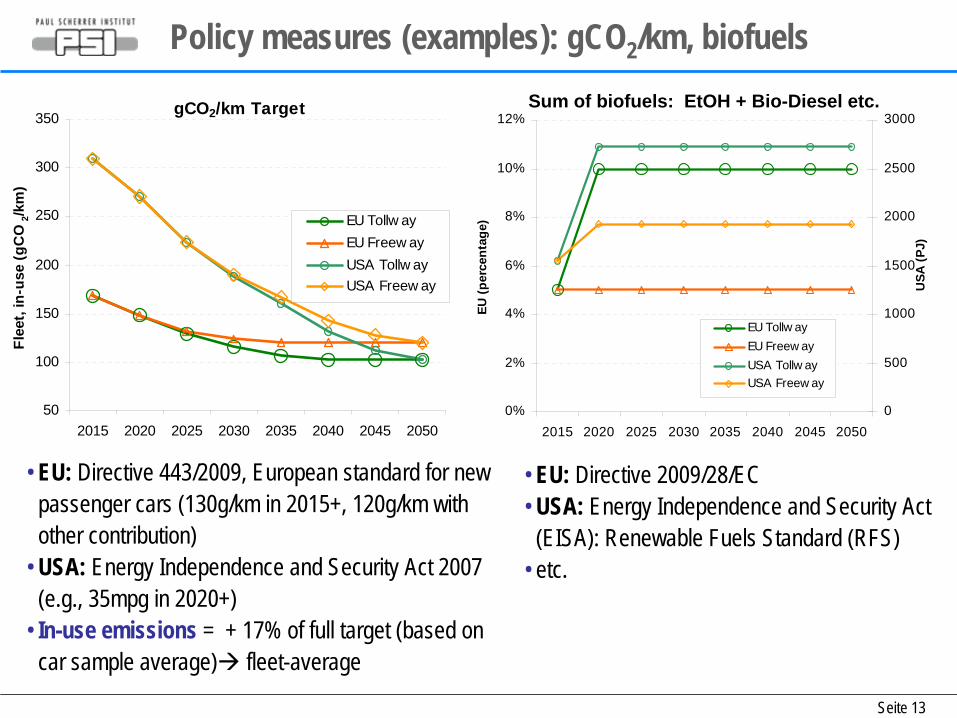

Policy measures (examples): gCO2 /km, biofuels

• EU: Directive 443/2009, European standard for new passenger cars (130g/km in 2015+, 120g/km with other contribution)

• USA: Energy Independence and Security Act 2007 (e.g., 35mpg in 2020+)

• In-use emissions = + 17% of full target (based on car sample average) fleet-average

• EU: Directive 2009/28/EC• USA: Energy Independence and Security Act

(EISA): Renewable Fuels Standard (RFS)• etc.

gCO2/km Target

50

100

150

200

250

300

350

2015 2020 2025 2030 2035 2040 2045 2050

Flee

t, in

-use

(gC

O2/k

m)

EU Tollw ayEU Freew ayUSA Tollw ayUSA Freew ay

Biofuel Target (Tollway vs. Freeway Scenario)

0%

2%

4%

6%

8%

10%

12%

2015 2020 2025 2030 2035 2040 2045 2050

EU (p

erce

ntag

e)

0

500

1000

1500

2000

2500

3000

USA

(PJ)

EU Tollw ayEU Freew ayUSA Tollw ayUSA Freew ay

Sum of biofuels: EtOH + Bio-Diesel etc.

Seite 14

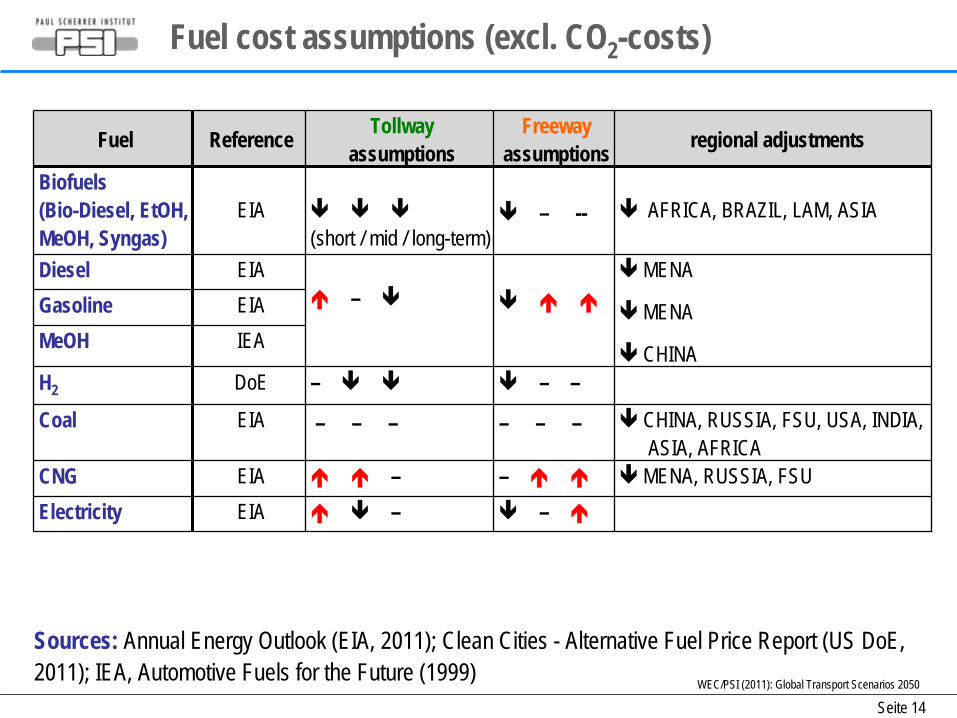

Fuel cost assumptions (excl. CO2 -costs)

WEC/PSI (2011): Global Transport Scenarios 2050

Sources: Annual Energy Outlook (EIA, 2011); Clean Cities - Alternative Fuel Price Report (US DoE, 2011); IEA, Automotive Fuels for the Future (1999)

Fuel Reference Tollwayassumptions

Freewayassumptions regional adjustments

Biofuels(Bio-Diesel, EtOH, MeOH, Syngas)

EIA (short / mid / long-term)

– --

AFRICA, BRAZIL, LAM, ASIA

Diesel EIA

–

MENA

MENA

CHINA

Gasoline EIAMeOH IEA

H2 DoE –

– –Coal EIA – – – – – – CHINA, RUSSIA, FSU, USA, INDIA,

ASIA, AFRICACNG EIA – – MENA, RUSSIA, FSUElectricity EIA

–

–

Seite 15

0

5000

10000

15000

20000

25000

30000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

billi

on v

-km

/y

Scenarios: Assumptions and Personal Car ResultsFreeway:• Market driven (market power)• Large demand growth in all transport

sectors• CO2 price is very slowly developing• Alternative fuels, technologies, and

infrastructure are promoted only if they are short-term cost-effective

0

5000

10000

15000

20000

25000

30000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

billi

on v

-km

/y

Tollway:• More regulative power of citizen/voter• Moderate demand growth in car transport; other sectors

with considerable growth (depends on regions)• CO2 price increases (lagging in developing regions)• Alternative fuels are promoted: 2nd generation biofuels

(larger targets), lower-carbon electricity• Promotion of BEV and HFCV in EU, Japan, and USA

Freeway Personal Cars: Tollway Personal Cars:

Liquid Fuel ICEVLiquid Fuel HybridLiquid Fuel Plug-inGas Fuel ICEVGas Fuel HybridHydrogen HybridHydrogen Fuel CellElectric Vehicle

WEC/PSI: Global Transport Scenarios 2050

• large increase in hybridisation (electric motor) in different degrees: HEV PHEV BEV

• moderate share of CNG and hydrogen FC vehicles

Seite 16

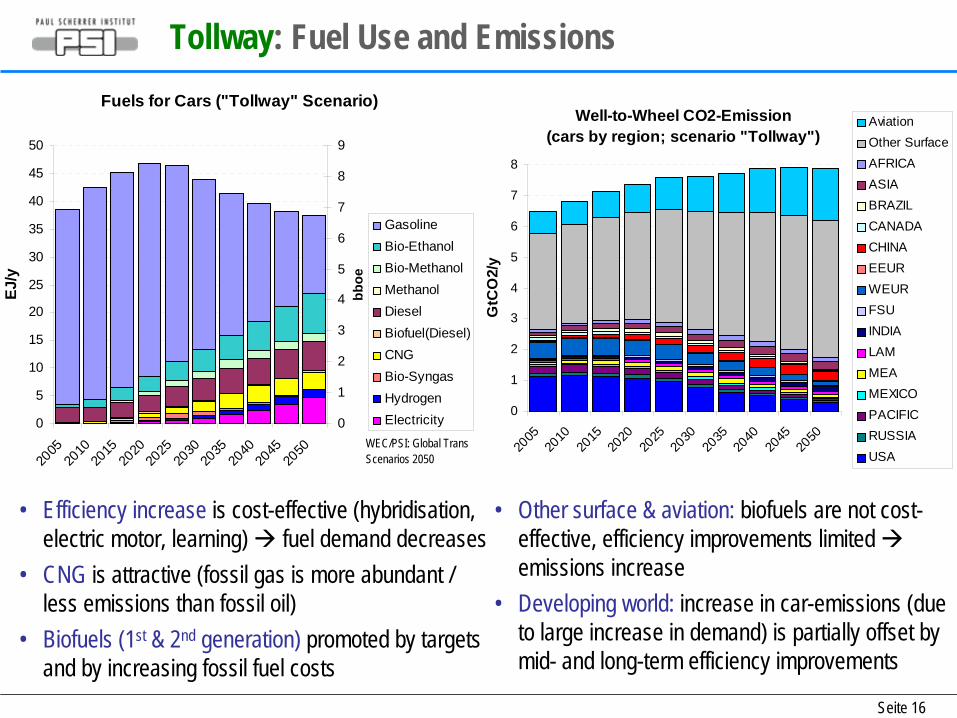

Tollway: Fuel Use and Emissions

• Other surface & aviation: biofuels are not cost- effective, efficiency improvements limited

emissions increase

• Developing world: increase in car-emissions (due to large increase in demand) is partially offset by mid- and long-term efficiency improvements

Fuels for Cars ("Tollway" Scenario)

0

5

10

15

20

25

30

35

40

45

50

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

EJ/y

0

1

2

3

4

5

6

7

8

9

bboe

• Efficiency increase is cost-effective (hybridisation, electric motor, learning) fuel demand decreases

• CNG is attractive (fossil gas is more abundant / less emissions than fossil oil)

• Biofuels (1st & 2nd generation) promoted by targets and by increasing fossil fuel costs

WEC/PSI: Global Transport Scenarios 2050

Well-to-Wheel CO2-Emission(cars by region; scenario "Tollway")

0

1

2

3

4

5

6

7

8

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

GtC

O2/

y

AviationOther SurfaceAFRICAASIABRAZILCANADACHINAEEURWEURFSUINDIALAMMEAMEXICOPACIFICRUSSIAUSA

GasolineBio-EthanolBio-MethanolMethanolDieselBiofuel(Diesel)CNGBio-SyngasHydrogenElectricity

Seite 17

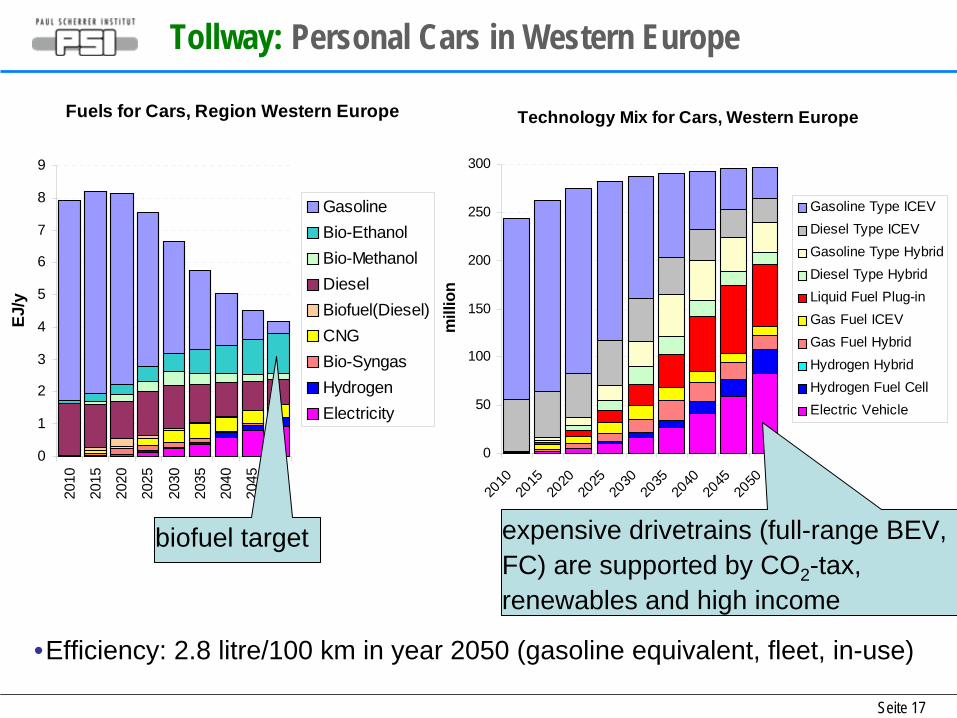

Tollway: Personal Cars in Western Europe

•Efficiency: 2.8 litre/100 km in year 2050 (gasoline equivalent, fleet, in-use)

Technology Mix for Cars, Western Europe

0

50

100

150

200

250

300

2010

2015

2020

2025

2030

2035

2040

2045

2050

mill

ion

Gasoline Type ICEVDiesel Type ICEVGasoline Type HybridDiesel Type HybridLiquid Fuel Plug-inGas Fuel ICEVGas Fuel HybridHydrogen HybridHydrogen Fuel CellElectric Vehicle

Fuels for Cars, Region Western Europe

0

1

2

3

4

5

6

7

8

9

2010

2015

2020

2025

2030

2035

2040

2045

2050

EJ/y

GasolineBio-EthanolBio-MethanolDieselBiofuel(Diesel)CNGBio-SyngasHydrogenElectricity

expensive drivetrains (full-range BEV, FC) are supported by CO2 -tax, renewables and high income

biofuel target

Seite 18

Tollway: Personal Cars in Latin America (excl. Brazil)

• Efficiency: 3.6 litre/100 km in year 2050 (gasoline equivalent, fleet, in-use)

Technology Mix for Cars, Region LAM

0

10

20

30

40

50

60

70

80

2010

2015

2020

2025

2030

2035

2040

2045

2050

mill

ion

Gasoline Type ICEVDiesel Type ICEVGasoline Type HybridDiesel Type HybridLiquid Fuel Plug-inGas Fuel ICEVGas Fuel HybridHydrogen HybridHydrogen Fuel CellElectric Vehicle

Fuels for Cars, Region LAM

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

2010

2015

2020

2025

2030

2035

2040

2045

2050

EJ/y

GasolineBio-EthanolBio-MethanolDieselBiofuel(Diesel)CNGBio-SyngasHydrogenElectricity

• Energy Security Gas

Seite 19

Conclusion

• Demand growth especially in aviation and personal cars in developing regions

• Gas in transport is a cost-effective option: low CO2 -emissions, gas resources are still abundant

• Alternative drivetrains enter gradually: HEV PHEV BEV• Commercial surface transport:

• Existing engines are relatively efficient (e.g. only few start-stop cycles disfavour electric motors)

• Aviation: Biofuels, Synfuels?

Outlook:• Launch of study for full energy system in Oct. 2013 in Daegu• Model Extensions: LCA integration,…

25. Juni 2013PSI,

Thank you!