Accounting Equation 01

21

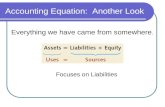

Accounting Equation 01 Review and Examples U.S. GAAP Codification , Accounting Textbooks Financial Accounting , Intermediate Accounting , Advanced Accounting U.S. GAAP by Topic , Accounting by Topic Accounting Equation 01 Basic form of an equation --> Left side = Right side 1. Balance Sheet Version Assets = Liabilities + Equity 2. Income Statement Version Net Income = Revenue - Expenses 3. Combined Version Assets = Liabilities + Equity ---> Equity = Beginning Equity + Net Income Assets = Liabilities + Beginning Equity + Net Income ---> Net Income = Revenue - Expenses Assets = Liabilities + Beginning Equity + Revenue - Expenses An Example of Combined Version At January 1, 2010, the balance of equity was $100,000. During the year of 2010, revenue and expenses were as follows Revenue = $300,000 Expenses = $240,000 What is the balance of equity at December 31, 2010? Equity = Beginning Equity + Revenue - Expenses --> $100,000 + $300,000 - $240,000 = $160,000 At December 31, 2010, Entity A had the following balances Assets = $280,000 Liabilities = $120,000 Equity = $160,000 Balance sheet version Assets = Liabilities + Equity --> $280,000 = $120,000 + $160,000 Combined version Assets = Liabilities + Beginning Equity + Revenue - Expenses

Transcript of Accounting Equation 01

Accounting Equation 01Review and Examples

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Accounting Equation 01

Basic form of an equation --> Left side = Right side

1. Balance Sheet VersionAssets = Liabilities + Equity

2. Income Statement VersionNet Income = Revenue - Expenses

3. Combined VersionAssets = Liabilities + Equity---> Equity = Beginning Equity + Net Income

Assets = Liabilities + Beginning Equity + Net Income---> Net Income = Revenue - Expenses

Assets = Liabilities + Beginning Equity + Revenue - Expenses

An Example of Combined Version

At January 1, 2010, the balance of equity was $100,000.During the year of 2010, revenue and expenses were as followsRevenue = $300,000Expenses = $240,000

What is the balance of equity at December 31, 2010?

Equity = Beginning Equity + Revenue - Expenses--> $100,000 + $300,000 - $240,000 = $160,000

At December 31, 2010, Entity A had the following balancesAssets = $280,000Liabilities = $120,000Equity = $160,000

Balance sheet versionAssets = Liabilities + Equity--> $280,000 = $120,000 + $160,000

Combined versionAssets = Liabilities + Beginning Equity + Revenue - Expenses--> $280,000 = $120,000 + $100,000 + $300,000 - $240,000

Cases and Practice Questions

Case 1:

Assets = $12,000Liabilities = $5,000Equity = $7,000Assets = Liabilities + Equity$12,000 = $5,000 + $7,000

Practice Question 1:

If Assets = $12,000 and Liabilities = $3,000what is the amount of equity?

--> Equity = Assets - Liabilities = $12,000 - $3,000 = $9,000

Case 2:

Revenue = $16,000Expenses = $10,000Net income = Revenue - Expenses = $16,000 - $10,000 = $6,000

Practice Question 2:

If Revenue = $16,000 and Expenses = $11,000what is the amount of net income?

--> Net income = Revenue - Expenses = $16,000 - $11,000 = $5,000

Case 3:

Assets = $25,000Liabilities = $11,000Beginning Equity = $10,000Revenue = $36,000Expenses = $32,000Assets = Liabilities + Beginning Equity + Revenue - Expenses$25,000 = $11,000 + $10,000 + $36,000 - $32,000

Practice Question 3:

In the following case, what is the amount of Beginning EquityAssets = $55,000Liabilities = $21,000Revenue = $76,000Expenses = $62,000Beginning Equity = ?

Assets = Liabilities + Beginning Equity + Revenue - Expenses$55,000 = $21,000 + ? + $76,000 - $62,000--> Beginning Equity = ? = $20,000

Double Entry Recording 01Debits and Credits

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Double Entry Recording 01

1. All accounting transactions are recorded--> using "Double Entry" recording system

2. Double Entry Recording System--> at least one "Debit" entry--> at least one "Credit" entry

3. An example of double entry recordingTransaction --> purchased merchandise and paid $3,200 in cash(1) One entry on debit --> merchandise 3,200(2) One entry on credit --> cash 3,200

debit credit

merchandise 3,200 cash 3,200

4. The sum of all debit entries = The sum of all credit entriesIf the sums of debit and credit entries are not equal for any journal entry--> the journal entry is not correct

5. Debit and credit sides of the accounting equationLeft side of the accounting equation = debit = assetsRight side of the accounting equation = credit = liabilities and equity

Assets = Liabilities + Equity

6. Debit side entries(1) Increase in assets(2) Decrease in liabilities(3) Decrease in equity

7. Credit side entries(1) Decrease in assets(2) Increase in liabilities(3) Increase in equity

8. Combined version of accounting equationAssets = Liabilities + Beginning equity + Revenue - Expenses

9. Debit side entries(1) Increase in assets(2) Decrease in liabilities(3) Decrease in equity(4) Decrease in revenue(5) Increase in expenses

10. Credit side entries(1) Decrease in assets(2) Increase in liabilities(3) Increase in equity

(4) Increase in revenue(5) Decrease in expenses

11. Normal Balances(1) Asset accounts have normal balances on debit side(2) Liability accounts have normal balances on credit side(3) Equity accounts have normal balances on credit side(4) Revenue accounts have normal balances on credit side(5) Expense accounts have normal balances on debit side

Practice Questions: Is it debit or credit?

decrease in expenses

credit

increase in expenses debit

increase in revenue credit decrease in revenue debit increase in liabilities credit decrease in liabilities debit decrease in equity debit increase in equity credit normal balances of equity accounts credit normal balances of asset accounts debit normal balances of liability accounts credit normal balances of expense accounts debit normal balances of revenue accounts credit decrease in cash account credit increase in inventory account debit increase in borrowings credit decrease in preferred stock debit increase in cost of goods sold debit decrease in accounts receivable credit increase in bonds payable credit

Debit Accounts 01Examples

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

The following accounts have normal balances on the debit side

1. Asset accounts2. Expense and loss accounts

Increases and decreases

1. Increases in asset accounts are recorded on the debit side2. Decreases in asset accounts are recorded on the credit side 3. Increases in expense and loss accounts are recorded on the debit side

4. Decreases in expense and loss accounts are recorded on the credit side

Examples of asset accounts

Cash and cash equivalents

Accounts receivable Notes receivable Interest receivable Rent receivable Inventories Merchandise Raw materials Work-in-process Finished goods Supplies Prepaid expenses Prepaid rent expense Prepaid insurance expense Prepaid interest expense Investment in debt and equity securities Trading securities Available-for-sale securities Held-to-maturity securities Property, plant and equipment Land Buildings Equipment Machinery Capitalized leases Leasehold improvements

Intangible assets Goodwill Trademarks Patents

Examples of expense and loss accounts

Cost of goods sold

Selling, general and administrative expenses Salaries expense Advertising expense Rent expense Travel expense Communication expense Insurance expense Supplies expense Utilities expense Depreciation expense Other expenses and losses Interest expense Loss on disposal of equipment Income tax expense

Credit Accounts 01Examples

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

The following accounts have normal balances on the credit side

1. Liability accounts2. Equity accounts3. Revenue and gain accounts

Increases and decreases

1. Increases in liability accounts are recorded on the credit side2. Decreases in liability accounts are recorded on the debit side 3. Increases in equity accounts are recorded on the credit side4. Decreases in equity accounts are recorded on the debit side 5. Increases in revenue and gain accounts are recorded on the credit side6. Decreases in revenue and gain are recorded on the debit side

Examples of liability accounts

Accounts payable

Notes payable

Salaries payable

Rent payable

Insurance payable

Interest payable

Income taxes payable

Dividends payable

Unearned rent revenue

Borrowings

Short-term borrowings

Long-term borrowings

Bonds payable

Capital lease obligations

Examples of equity accounts

Paid-in capital

Common stock Preferred stock Additional paid-in capital Retained earnings

Examples of revenue and gain accounts

Sales revenue

Services revenue Commissions revenue Interest revenue Rent revenue Dividend income Gain on sale of buildings

Asset Accounts 01Examples and Practice Questions

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Assets

1. Assets represent future economic benefits 2. Assets have normal balances on the debit side

3. Increases in asset accounts are recorded on the debit side4. Decreases in asset accounts are recorded on the credit side

Classification of assets

1. Assets are classified as current and noncurrent assets 2. Current assets are expected to be converted to cash or consumed--> within a year or normal operating cycle whichever is longer--> Codification link to current assets 3. Current assets include the following(1) Cash and cash equivalents(2) Receivables, current(3) Investments, current(4) Inventories(5) Prepaid expenses 4. Noncurrent assets are expected to be converted to cash or consumed--> after a year or normal operating cycle whichever is longer 5. Noncurrent assets include the following(1) Receivables, noncurrent(2) Investments, noncurrent(3) Property, plant and equipment(4) Intangible assets(5) Other noncurrent assets

Net working capital

1. Net working capital = Current assets - Current liabilities2. Net working capital measures the margin of current assets over current liabilities3. More net working capital implies that the entity has more liquidity

Current ratio

1. Current ratio = Current assets / Current liabilities2. Current ratio measures whether the entity has enough current assets to pay off current liabilities. Current Assets Current Ratio = ---------------------- Current Liabilities

Practice Questions

1. Current assets = $300,000, Current liabilities = $200,000

2. What is the amount net working capital? Net working capital = current assets - current liabilities = $300,000 - $200,000 = $100,000

3. What is the current ratio? Current ratio = Current assets / Current liabilities = $300,000 / $200,000 = 1.50

Examples of current assets

Cash and cash equivalents

Accounts receivable Notes receivable Interest receivable Rent receivable Inventories Merchandise Raw materials Work-in-process Finished goods Supplies Prepaid expenses Prepaid rent expense Prepaid insurance expense Prepaid interest expense Trading securities Available-for-sale securities, current Held-to-maturity securities, current Other current investments

Examples of noncurrent assets

Notes receivable, noncurrent

Long-term loans Available-for-sale securities, noncurrent Held-to-maturity securities, noncurrent Other noncurrent investments Property, plant and equipment Land Buildings Equipment

Machinery Capitalized leases Leasehold improvements Intangible assets Goodwill Trademarks Patents

Liability Accounts 01Examples and Practice Questions

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Liabilities

1. Liabilities are present obligations to transfer resources in the future 2. Such obligations are due to past transactions or events 3. Past, present and future(1) due to past transactions or events(2) present obligations(3) future transfer of resources

Debits and credits

1. Liability accounts have normal balances on the credit side

2. Increases in liability accounts are recorded on the credit side3. Decreases in liability accounts are recorded on the debit side

Classification of liabilities

1. Liabilities are classified as current and noncurrent liabilities

2. Current liabilities are expected to require the transfer of resources--> within a year or normal operating cycle whichever is longer--> Codification link to current liabilities 3. Current liabilities include the following(1) Accounts payable(2) Notes payable, due within a year(3) Short-term borrowings(4) Income taxes payable 4. Noncurrent liabilities are expected to require the transfer of resources--> after a year or normal operating cycle whichever is longer

5. Noncurrent liabilities include the following(1) Notes payable, due after a year(2) Long-term borrowings(3) Bonds payable(4) Capital lease obligations

Practice Questions

Entity A has the following account balances as of December 31, 2010.

Accounts Balances

1 Accounts payable due within a year $50,000 2 Notes payable due in 2011 $70,000 3 Notes payable due in 2012 $40,000 4 Accounts receivable due within a year $10,000 5 Notes receivable due in 2012 $10,000 6 Bonds payable due in 2015 $80,000 7 Income taxes payable $30,000 8 Short-term borrowings $20,000

1. What is the amount of current liabilities?

Accounts Balances

1 Accounts payable due within a year $50,000 2 Notes payable due in 2011 $70,000 7 Income taxes payable $30,000 8 Short-term borrowings $20,000 Total current liabilities $170,000

2. What is the amount of noncurrent liabilities?

Accounts Balances

3 Notes payable due in 2012 $40,000 6 Bonds payable due in 2015 $80,000 Total noncurrent liabilities $120,000

(Note) The following items are not liabilities

Accounts Balances

4 Accounts receivable due within a year $10,000 5 Notes receivable due in 2012 $10,000

Examples of current liabilities

Accounts payable, due within a year

Notes payable, due within a year

Salaries payable

Rent payable

Insurance payable

Interest payable

Income taxes payable

Dividends payable

Unearned rent revenue

Short-term borrowings

Examples of noncurrent liabilities

Notes payable, due after a year

Long-term borrowings

Bonds payable

Capital lease obligations

Equity Accounts 01Examples and Practice Questions

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Equity

1. Equity represents the owners' equity

2. For corporations, shareholders are owners--> equity represents the shareholders' equity

3. Equity is a residual concept--> equity is what's left after subtracting liabilities from assets

4. Equity = Assets - Liabilities

Components of equity

1. Paid-in capital--> the amount shareholders contributed to the entity--> in exchange of the shares of common stock or preferred stock

2. Retained earnings--> net income is accumulated in retained earnings--> dividends are paid from retained earnings

Debits and credits

1. Equity accounts have normal balances on the credit side

2. Increases in equity accounts are recorded on the credit side

3. Decrease in equity accounts are recorded on the debit side

Practice Questions

1. Issuance of common stock

Entity A issued 8,000 shares of common stockPar value = $1 per shareIssue price = $10 per share

debit credit

Cash 80,000 Common stock 8,000 Additional paid-in capital 72,000

2. Issuance of common stock with no par value

Entity B issued 7,000 shares of common stockNo par valueIssue price = $20 per share

debit credit

Cash 140,000 Common stock 140,000

Retained earnings

1. Net income is added to retained earningsEnding retained earnings = Beginning retained earnings + Net income

2. Dividends decrease retained earningsEnding retained earnings = Beginning retained earnings + Net income - Dividends declared

Practice Questions

1. Dividends are declaredEntity C has 500,000 shares of common stock outstanding--> and declared $3 per share dividends

debit credit

Retained earnings 150,000 Dividends payable 150,000

2. Entity D had $230,000 balance of retained earnings as of December 31, 2009.During 2010, Entity D earned $60,000 net income and declared $15,000 dividends.What is the ending balance of retained earnings as of December 31, 2010?

Ending retained earnings= Beginning retained earnings + Net income - Dividends declared= $230,000 + $60,000 - $15,000 = $275,000

Examples of equity accounts

Common stock

Preferred stock Additional paid-in capital Retained earnings

Revenue Accounts 01Examples and Practice Questions

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Revenue Accounts 01Examples and Practice Questions

Revenue

1. Revenue is the increase in resources from the operations of an entity

2. Increase in resources may be (A), (B) or (C)(A) Increase in assets(B) Decrease in liabilities(C) Both (A) and (B)

Recognition of revenue

1. Recognition means "recording" in accounting2. Revenue is reported when it is recognized3. Revenue is recognized when it is earned and realized (or realizable)4. Realized means the collection of cash5. Earned means the delivery of products or services

Debits and credits

1. Revenue accounts have normal balances on the credit side

2. Increases in revenue accounts are recorded on the credit side3. Decrease in revenue accounts are recorded on the debit side

Examples of revenue accounts

Sales revenue

Services revenue Interest revenue Rent revenue

Practice Questions

1. On December 15, 2010Entity A sold 300 units of products at the price of $20 per unit

2. On December 15, 2010Entity A received $3,600 in cash

3. On January 27, 2011Entity A received $2,400 in cash

4. What is the amount revenue for 2010?300 units x $20 = $6,000

5. What is the balance of accounts receivable at December 31, 2010?$6,000 - $3,600 = $2,400

6. Prepare journal entries at the following dates(1) December 15, 2010(2) December 31, 2010(3) January 27, 2011

7. Journal entry at December 15, 2010

debit credit

Cash 3,600 Accounts receivable 2,400 Sales revenue 6,000

8. Journal entry at December 31, 2010--> No journal entry is required at December 31, 2010

9. Journal entry at January 27, 2011

debit credit

Cash 2,400 Accounts receivable 2,400

Expense Accounts 01Examples and Practice Questions

U.S. GAAP Codification , Accounting Textbooks

Financial Accounting , Intermediate Accounting , Advanced Accounting

U.S. GAAP by Topic, Accounting by Topic

Expense Accounts 01Examples and Practice Questions

Expense

1. Expense is the use of resources to generate revenue

2. Expense is recognized when related revenue is recognized--> this is called "matching principle"

* Debits and credits

1. Expense accounts have normal balances on the debit side

2. Increases in expense accounts are recorded on the debit side3. Decrease in expense accounts are recorded on the credit side

Examples of expense accounts

Cost of goods sold

Selling, general and administrative expenses Salaries expense Advertising expense Rent expense Travel expense Communication expense Insurance expense Supplies expense Utilities expense Depreciation expense Other expenses and losses Interest expense Income tax expense

Practice Questions

1. On November 1, 2010Entity A purchased 500 units of merchandise at the price of $10 per unitand paid full amount in cash

2. On November 12, 2010Entity A sold 200 units of merchandise at the selling price of $14 per unitand received full amount in cash

3. Prepare journal entries at the following dates(1) November 1, 2010(2) November 12, 2010

4. Journal entry at November 1, 2010

debit credit

Merchandise 5,000 Cash 5,000

5. Journal entry at November 12, 2010, to record revenue

debit credit

Cash 2,800 Sales revenue 2,800

6. Journal entry at November 12, 2010, to record expense

debit credit

Cost of goods sold 2,000 Merchandise 2,000

7. Sales revenue = $2,800Cost of goods sold = $2,000Gross profit = Sales - Cost of goods sold = $2,800 - $2,000 = $800

8. At December 31, 2010Balance of merchandise = 300 units x $10 = $3,000