TeliaSonera/Tele2 - competition · PDF fileTeliaSonera/Tele2 ACE 28. November 2015 The...

14

TeliaSonera/Tele2 ACE 28. November 2015 The Norwegian Competition Authority Katrine Holm Reiso

Transcript of TeliaSonera/Tele2 - competition · PDF fileTeliaSonera/Tele2 ACE 28. November 2015 The...

TeliaSonera/Tele2

ACE28. November 2015

The Norwegian Competition Authority

Katrine Holm Reiso

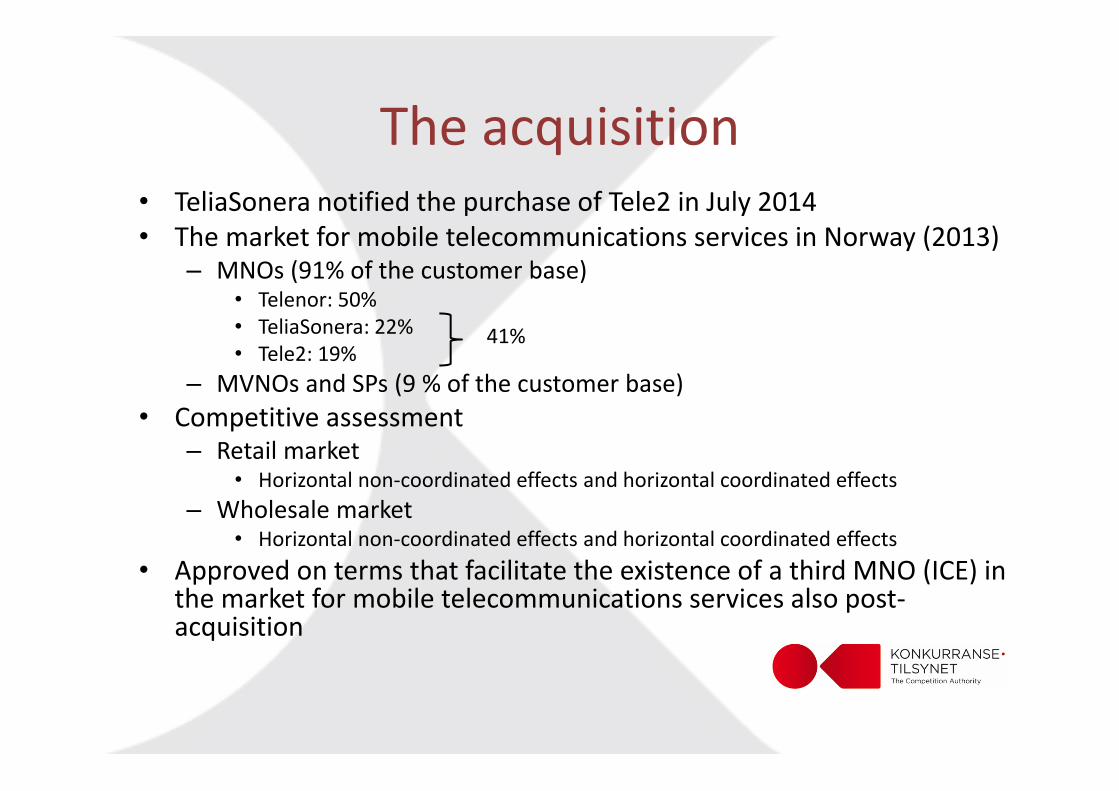

The acquisition • TeliaSonera notified the purchase of Tele2 in July 2014 • The market for mobile telecommunications services in Norway (2013)

– MNOs (91% of the customer base)• Telenor: 50%• TeliaSonera: 22%• Tele2: 19%

– MVNOs and SPs (9 % of the customer base)• Competitive assessment

– Retail market• Horizontal non‐coordinated effects and horizontal coordinated effects

– Wholesale market• Horizontal non‐coordinated effects and horizontal coordinated effects

• Approved on terms that facilitate the existence of a third MNO (ICE) in the market for mobile telecommunications services also post‐acquisition

41%

Today's topic

• Counterfactual– Hypothetical scenario of how the market would develop in absence of the acquisition

– Usually status quo (the situation at the time of notification)

• Pricing pressure analyses– Part of the assessment of horizontal non‐coordinated effects in the retail market

– The choice of counterfactual has implications for the pricing pressure analyses

Mobile operators

• Mobile Network Operators (MNO)– Own a mobile network– Authorization to use spectrum band(s) for mobile telecommunications

• Mobile Virtual Network Operators (MVNO)– No base stations or spectrum bands– Buy access to the MNOs networks

• Service Providers (SP)– Buy all services from MNOs or MVNOs– Resells services with their own brand name

MNOs in Norway in 2013• Telenor

– Largest player within mobile telecommunications services (50%)– Mobile network with nationwide population coverage

• TeliaSonera– Second largest player within mobile telecommunications services (22%)– Mobile network with nationwide population coverage

• Tele2 – Third largest player within mobile telecommunications services (19%)– Mobile network with 75% population coverage– Needed to buy access (roaming) from Telenor/TeliaSonera

• ICE – Offered mobile broadband –not mobile telecommunications services – Mobile network with 75% area coverage –not compatible with mobile

telecommunications services

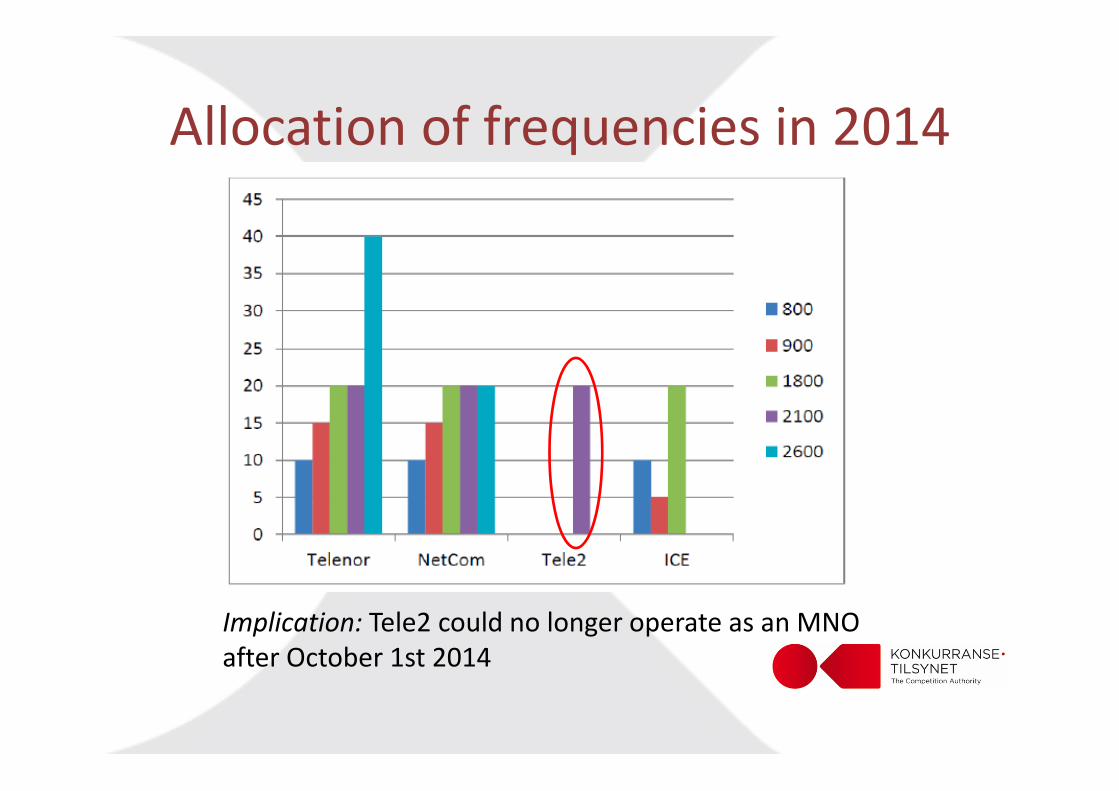

The spectrum auction in 2013

• Auctions are used to allocate spectrum bands– Organized by the Norwegian Communication Authority

• The spectrum auction in December 2013 – 800, 900 and 1800 MHz spectrum– Necessary to have low frequencies (800 and 900) for coverage and high frequencies (1800) for capacity

– Bidders: Telenor, TeliaSonera, Tele2 and ICE– Expected winners: Telenor, TeliaSonera and Tele2

Allocation of frequencies in 2014

Implication: Tele2 could no longer operate as an MNO after October 1st 2014

The Norwegian Competition Authority’s assessment

• Tele2 as an MVNO –No– An unprofitable and risky alternative– Statements by Tele2: "[...] not commercially viable over time." and "[...] not a real option for Tele2"

• Tele2 as an MNO with ICE –Yes – Tele2 has an overall MNO strategy in all countries– Tele2 (network) and ICE (frequencies) had complementary inputs ‐ economically rational to reach an agreement

– Tele2 had parallel negotiations with ICE throughout the sales process with TeliaSonera

• The choice of counterfactual has implications for the assessment of the acquisition

Introduction to pricing pressure indicators

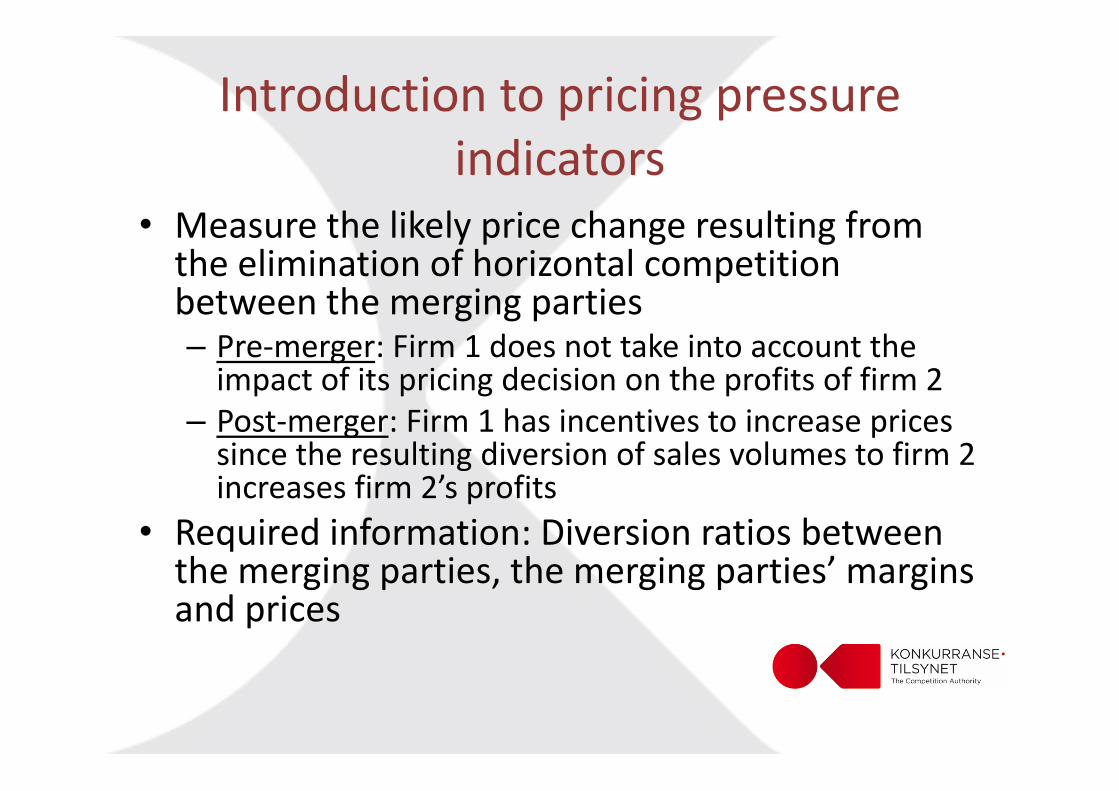

• Measure the likely price change resulting from the elimination of horizontal competition between the merging parties– Pre‐merger: Firm 1 does not take into account the impact of its pricing decision on the profits of firm 2

– Post‐merger: Firm 1 has incentives to increase prices since the resulting diversion of sales volumes to firm 2 increases firm 2’s profits

• Required information: Diversion ratios between the merging parties, the merging parties’ margins and prices

Pricing Pressure Indicators

• Gross Upward Pricing Pressure Index (GUPPI)*–

• Indicative Price Raise (IPR)**

– ∆

*Moresi (2010). "The use of upward price pressure indices in merger analysis.“**Hausman, Moresi og Rainey (2011). "Unilateral effects ofmergers with general linear demand."

Results

• Pricing pressure for TeliaSonera and Tele2 between [10‐20%] as a result of the acquisition– Assumption: No changes in marginal costs

• "[…] indicates that the parties have an incentive to undertake a lasting and significant price increase resulting from the concentration"

The Parties’ argumentsThe Parties’ arguments: Assessment by the NCA:Counterfactual: Tele2 as an MVNO1. Reduced marginal costs due

to the acquisition• Tele2 would no longer pay for

access (roaming) • →Pricing pressure reduced

2. The Parties have reduced incentives to compete absent the acquisition• Tele2 would buy access

(roaming) from TeliaSonera• →Pricing pressure reduced

Counterfactual: Tele2 as an MNO1. Reduced marginal costs absent

the acquisition• Tele2 would continue to develop

their network• Historical cost data underestimate

pricing pressure2. Tele2 would not buy access

from TeliaSonera • Tele2 would buy access (roaming)

from Telenor absent the acquisition

• Continued development of network → reduced roaming costs

Pricing pressure indicators –limitations

• Rivals reactions are not incorporated• Historical data• Measure short‐run effects• …

Moresi (2010)*: “[…], the GUPPI in and of itself is a useful screen and might be used as supporting “circumstantial” evidence, but it also is not a complete analysis of all the relevant competitive factors.”

• They give an estimate –not the true value*Moresi (2010). "The use of upward price pressure indices in merger analysis."

Thank you for your attention