MEGATRENDS IN HEALTHCARE CONSUMERISM: A 5 … · MEGATRENDS IN HEALTHCARE CONSUMERISM: A 5-YEAR...

41

MEGATRENDS IN HEALTHCARE CONSUMERISM: A 5-YEAR STUDY Christopher Neuharth, VP Product Design & Strategy Cathy Scozzari, Senior HR Generalist, Schreiner University Amy Christofis, Director, Client Services

Transcript of MEGATRENDS IN HEALTHCARE CONSUMERISM: A 5 … · MEGATRENDS IN HEALTHCARE CONSUMERISM: A 5-YEAR...

MEGATRENDS IN HEALTHCARE CONSUMERISM: A 5-YEAR STUDY

Christopher Neuharth, VP Product Design & Strategy Cathy Scozzari, Senior HR Generalist, Schreiner University

Amy Christofis, Director, Client Services

WHO WE ARE • 130 clients, including 20 of the largest carriers

• Health insurance enrollment and engagement solutions company

• Technology behind Medicare.gov, PlanFinder, 1-800-Medicare and Online Enrollment Center

• Individual, Group, Medicare, On/Off Exchange, Ancillary

• Broker, Affinity, Private Exchange distribution channels

• Decision support, enrollment, retention and engagement

• In–house user research and analytic teams drive product roadmap and UX

FOUNDED 1999

20 Million Consumers Annually Leading provider

of insurance enrollment platform solutions for Group,

Individual, Medicare, and Engagement

HEADQUARTERS

Brookfield, WI

INNOVATION CENTER

Chicago, IL

CNXR

12 / 12 / 14

CONSUMER DATA METHODOLOGY

• Conducted annually through direct-to-consumer panel

• ~8000 participants over the last 5 years (avg. ~1500 / yr)

• Screening process to include minimums by key demographics and status

• Conducted in consultation with 3rd-party data scientists & industry experts

• Compared against Connecture’s Analysis of its platform

• Supplemented by hundreds of 1-on-1 interviews with consumers

• Test, design, build, enhance, repeat approach to roadmap

SURVEY

ANALYSIS

INSIGHTS

5 MEGATRENDS IN THE LAST 5 YEARS

1. Access and choice have exploded

2. Consumers have become more confident purchasers

3. The burden is shifting back to the consumer

4. Demand and need for decision support tools has increased

5. More work to do on bending the cost curve

1. ACCESS AND CHOICE HAVE EXPLODED

ONLINE HEALTHCARE SHOPPING TRIPLED

Source: Connecture Consumer Survey

From 2012 to 2017, the amount of respondents who shopped online for health insurance increased by

3x 2012 2017

14%

42%

GROUP INSURANCE

81% Of customers at companies with

500+ employees enrolled online… 52% at <500

38% Had Shopped Online

(Up From 9.5% in 2012)

• Source: Connecture Consumer Survey

Source: Connecture Consumer Survey

EFFECT ON CONSUMERISM

CUSTOMERS WHO ENROLLED ONLINE (VS PAPER)

• Are more likely to be engaged in decision-making around healthcare costs (49% v 35%)

• And more interested in ancillary benefits

• Dental (75% v 62%)

• Life (35% v 23%)

• Gym Memberships (32% v 19%)

VS

Source: Connecture Consumer Survey

2. CONSUMERS HAVE BECOME MORE CONFIDENT PURCHASERS

EFFECT ON CONSUMERISM In 2012

37% Said they are comfortable shopping for health insurance by themselves with little assistance from others

In 2016

56% Said they would shop online

with little to no assistance

Source: Connecture Consumer Survey

MILLENNIALS (AGES ~18-35)

• Express the lowest level of satisfaction with their employers options for health insurance

• More likely to take into consideration what other people like them have purchased, or shop according to potential health events.

• Prefer to sort through more than 5 plan choices

• More likely to consider new ancillary benefits like; ID Theft, Gym Memberships, Fitness Tracking, and Legal Services

Source: Connecture Consumer Survey

3. THE BURDEN IS SHIFTING BACK TO THE CONSUMER

CHOICE IS POSITIVE, BUT CONSUMERS DON’T NEED TOO MUCH

80% Of consumers consider less than 10 plans as a good amount to choose from when shopping for health plans

Source: Connecture Consumer Survey

MOVEMENT TOWARDS HIGH DEDUCTIBLES

% Shopping Online

% Deductibles Over 1k

PWC Touchstone Survey 2017 & Connecture Consumer Survey

4. DEMAND FOR DECISION-SUPPORT TOOLS HAS INCREASED

PERSONALIZATION WANTED Consumers prefer to provide personal information that will aide in choosing a health insurance plan:

Pers

on

aliz

atio

n

48%

48%

46%

40%

31%

provide my doctors names, drugs, and preferred plan options

see a list of potential health events and what they would cost me

answer lifestyle and budget questions to see plans recommended for people like me

provide expected doctor visits and conditions to get an estimate of cost

see plans are most frequently purchased by others like me

Source: Connecture Consumer Survey

SHOPPING METHODS VARY BY AGE SEGMENT Millennials prefer plans that match lifestyle, budget, and “what ifs” Seniors prefer plans that include doctors and prescriptions

Source: Connecture Consumer Survey

WHAT TO DO ABOUT IT • Don't look at decision support as a one-size-fits-all solution

• Apply a segmented and personalized experience

• Don’t get in the way of those who feel comfortable

• Provide robust and transparent recommendations to help those who need it

5. MORE WORK TO DO ON BENDING THE COST CURVE

TRADING NETWORKS FOR COST

71% Of consumers would consider switching their doctor(s) to save on plan costs

Source: Connecture Consumer Survey

INFORMED PLAN CHOICE HELPS

Decision support tools make consumers

3x More Likely to select best fit plan

Source: Connecture enrollment data and analysis

LACK OF AWARENESS

49% Aren’t sure about how much they spend on healthcare per month

Source: Connecture Consumer Survey

HIGH DEDUCTIBLE PLANS LOWER COSTS http://www.healthcostinstitute.org/files/CDHP%20Issue%20Brief_final.pdf

Source: Health Cost Institute

The Bankrate Money Pulse survey conducted by Princeton Survey Research Associates International

"My deductible is so high, it's not worth it to go to the doctor for most things"

- Mandy Pullen, a 44-year-old single mom in Waltham, Massachusetts

One Quarter of Americans say they or someone in their family has abstained from seeking necessary medical care because of high costs.

SO, WHERE ARE THE COSTS Roughly

25% Of the commercially insured population does not have a claim in a given year

42% Of the healthcare services are “shoppable”

Approximately

50% Of healthcare dollars are spent on 5 percent of the population

42% Source: Health Cost Institute

80% Are willing to talk to their doctor about prescription drug alternatives • People don’t realize they can switch. • Concerns about safety / side effects. • There’s a balance between convenience

and cost for people.

Source: Connecture Consumer Survey & User Research

DRUG ALTERNATIVES MAKE A DIFFERENCE

38 Million Drug Searches

Four Billion In Total Annual Savings

$958 Average Annual

Savings Per Search

Source: Connecture Usage Data

5 MEGATRENDS IN THE LAST 5 YEARS

1. Access and choice have exploded

2. Consumers have become more confident purchasers

3. The burden is shifting back to the consumer

4. Demand and need for decision support tools has increased

5. More work to do on bending the cost curve

EIIA/CONNECTURE PARTNERSHIP EIIA IS…

Broker that helps private colleges and universities offer strategic benefit packages that are sustainable and competitive.

EIIA’S UNIQUE CHALLENGE

Higher education tends to adopt trends in Employee Benefits very slowly, leaning towards offering one, rich PPO plan to employees, rather than a menu of offerings. Also, many private schools and universities are seeing increased regulation and strain on HR and budget, even as they experience pressures on

tuition.

ACA COMPLIANCE

EIIA’s clients have a lot on their plates when it comes to ACA compliance!

“The online enrollment tools, back-end improvement in benefit administration – including ACA compliance – and integrated offering for non-group eligible employees have created the perfect solution for our members.” Doug Maher Executive Director of Employee Benefits, EIIA

SCHREINER UNIVERSITY – A PERFECT FIRST CASE

PLAN COMPARISON

DECISION SUPPORT

EMPLOYEE COMMUNICATIONS

ADMINISTRATIVE FEATURES

SCHREINER’S STORY WHO IS SCHREINER UNIVERSITY? • Private Liberal Arts, Faith-Based Institution of Higher Education • Began as a military prep school before evolving into a four-year

institution • Located in Kerrville, Texas

EMPLOYEES • Wide range of employees with different benefit needs, risk tolerances,

and budgets: • PhD level, tenured professors • Retirees and First Time Employees • Administrators/Staff • Physical Plant Employees

• 3 Satellite locations with employees not immediately on campus

SCHREINER’S STORY IMPETUS FOR CHANGE • All information in one place • Streamlined enrollment

process • ACA Reporting Requirements

Support: 1094/1095 filing • Decision support • Change HR department's

focus

THE OLD WAY • Paper enrollment for most

benefits • Time consuming for HR • Employee reminders • Manual data entry into

payroll • Faxing forms to carriers

OBSTACLES TO CHANGE

• Varying degrees of comfort with technology

• Adversity to change

“My Benefit Basket has streamlined our employee benefit enrollment process. We have the employee log into the system and they shop for the benefits they need. Additionally, 1094/1095 reporting was a breeze!”

Schreiner’s Story – Recently implemented ‘Healthcoach’ through Medical Provider – Implemented TelaDoc this year

• Trying to increase employees virtual access to healthcare

– Encourage employees to find lowest cost Rx

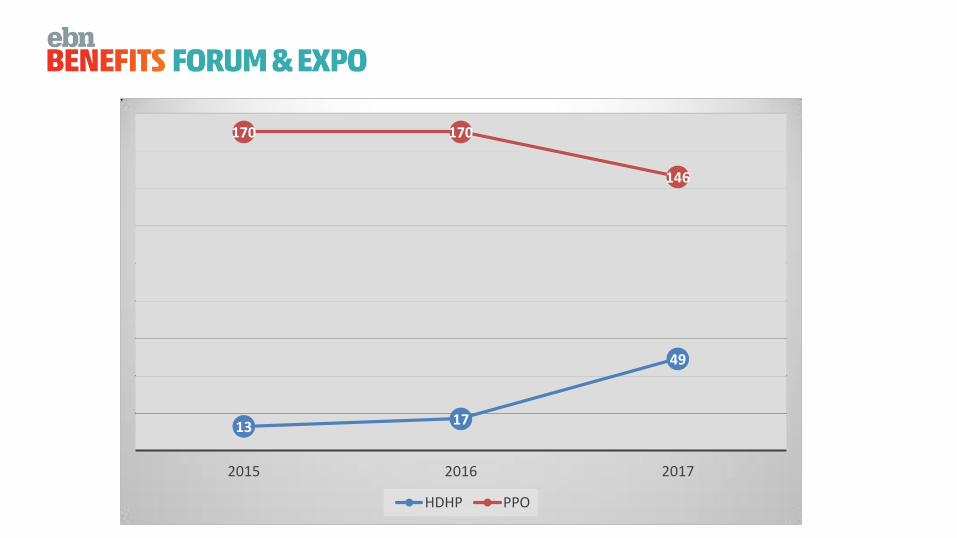

• Historical – In the past, very few people had enrolled in the HDHP plan

• Decision support tools helped employees see they might come out ahead with a higher deductible plan and migration has slowly increased each year

13 17

49

170 170

146

2015 2016 2017

HDHP PPO

ACA REPORTING

ACA reporting has placed a huge burden on large employers, and Schreiner is no exception

• Make ACA reporting easier for the employer – help free-up their time so they can focus

on other HR initiatives

TAKEAWAYS HR TECHNOLOGY SHOULD…

• Provide decision support specific to employees as they have diverse needs and goals

• Help engage employees – making the connection between one’s health and financial security is critical

• Be accessible from anywhere / anytime and provide robust information

And remember: there’s no such thing as over-communicating when it comes to benefits (and not just during open enrollment)

QUESTIONS? Contact us at [email protected] for more information