Retailing industry outlook in Eastern Europe -...

32

Euromonitor International © Retailing industry outlook in Eastern Europe Retailing industry outlook in Eastern Europe Nikola Košutić

-

Upload

truongtruc -

Category

Documents

-

view

215 -

download

0

Transcript of Retailing industry outlook in Eastern Europe -...

Euromonitor International ©Retailing industry outlook in Eastern Europe

Retailing industry outlook in Eastern Europe

Nikola Košutić

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

2

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

3

Euromonitor International ©Retailing industry outlook in Eastern Europe

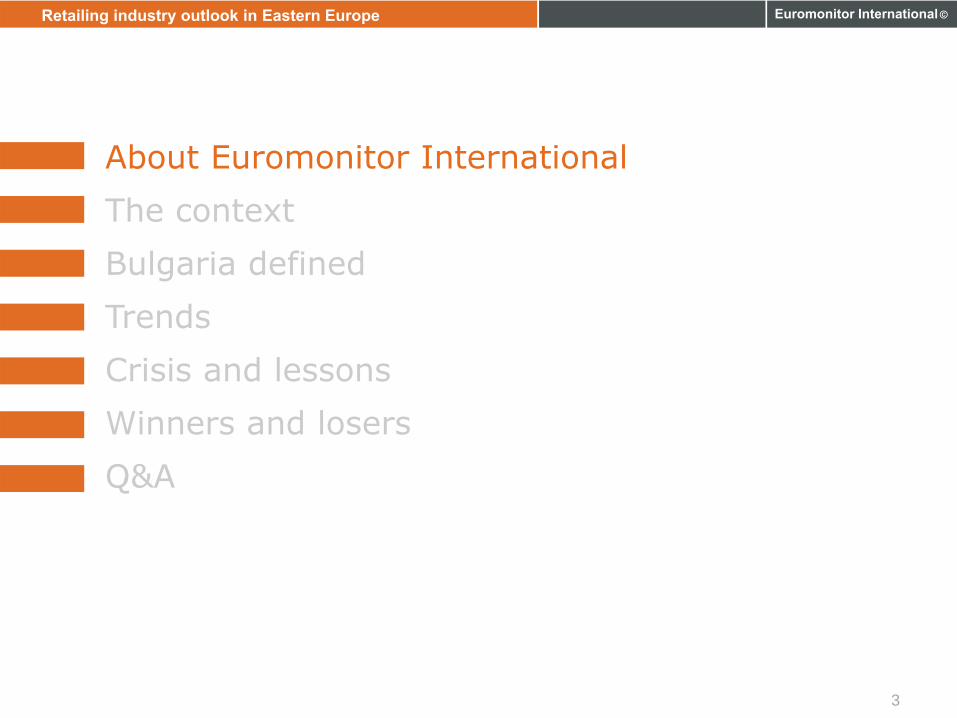

Euromonitor International

What?Who? Where?

A trusted business intelligence sourceHelping clients make informed strategic decisions600+ analysts in 80 countries400+ industry specialist and client support teams8 Regional research hubs: London, Chicago, Santiago, Vilnius, Cape town, Singapore, Shanghai, Dubai

Geographic reach: Industries: 95% of global consumer spendingCountries, Consumers: 205 countries

Statistics, reports, comments4,000 products and services115 million data points17,000 full text reports:global, regional, country, company

Industries

Countries

Consumers

“Euromonitor’s “Passport” is the Mercedes of business intelligence” E‐Content magazine

4

Euromonitor International ©Retailing industry outlook in Eastern Europe

Euromonitor research methodology

Desk researchin-house, client’s and secondary sources

Field work in-country and industry

Analysisvalidate, interpret, contextualize

Managementcoordination, engagement, consultation

Final deliverablePresented in custom format requested by the client or in “Passport”

5

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

6

Euromonitor International ©Retailing industry outlook in Eastern Europe

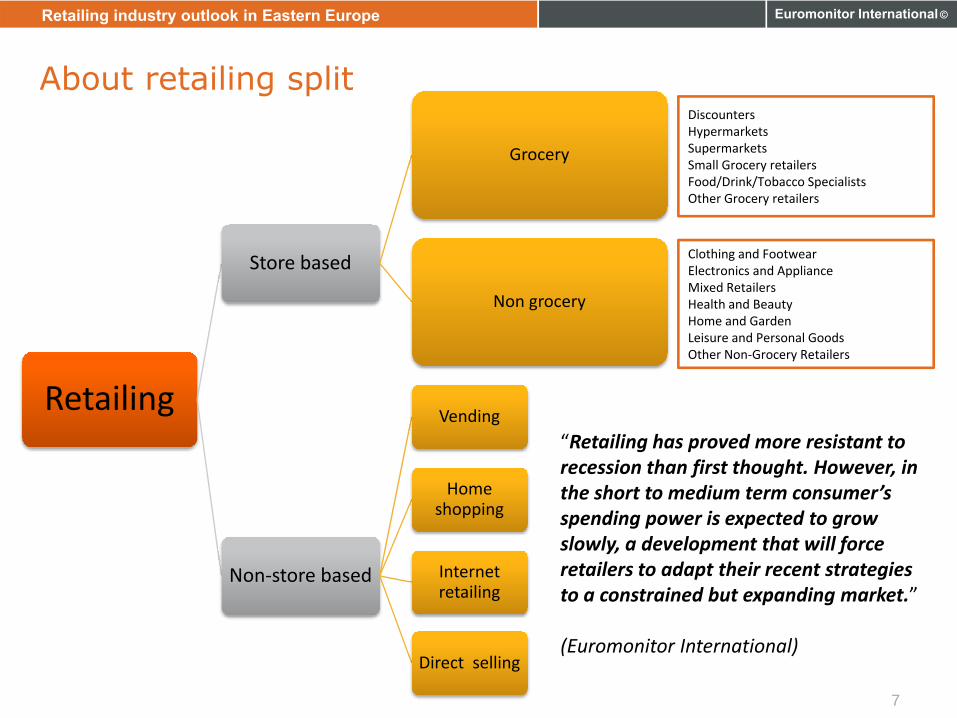

About retailing split

Retailing

Store based

Grocery

Non grocery

Non‐store based

Vending

Home shopping

Internet retailing

Direct selling

DiscountersHypermarketsSupermarketsSmall Grocery retailersFood/Drink/Tobacco SpecialistsOther Grocery retailers

Clothing and Footwear Electronics and ApplianceMixed RetailersHealth and BeautyHome and GardenLeisure and Personal GoodsOther Non‐Grocery Retailers

“Retailing has proved more resistant to recession than first thought. However, in the short to medium term consumer’s spending power is expected to grow slowly, a development that will force retailers to adapt their recent strategies to a constrained but expanding market.”

(Euromonitor International)

7

Euromonitor International ©Retailing industry outlook in Eastern Europe

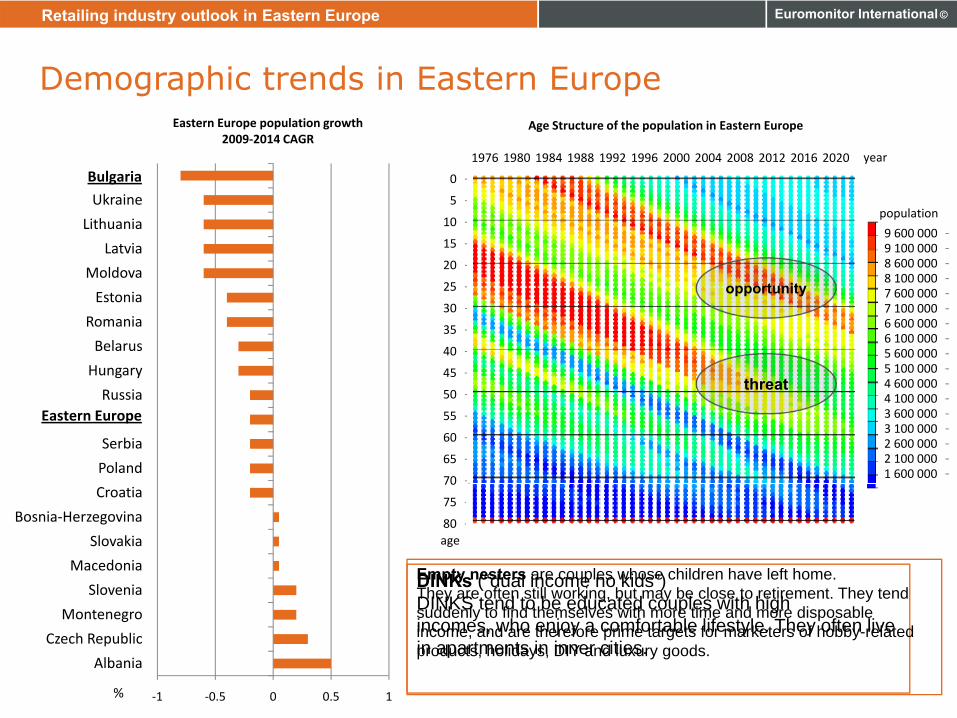

Demographic trends in Eastern Europe

‐1 ‐0.5 0 0.5 1

Albania

Czech Republic

Montenegro

Slovenia

Macedonia

Slovakia

Bosnia‐Herzegovina

Croatia

Poland

Serbia

Russia

Hungary

Belarus

Romania

Estonia

Moldova

Latvia

Lithuania

Ukraine

Eastern Europe population growth2009‐2014 CAGR

Eastern Europe

%

Bulgaria

DINKs (“dual income no kids”)DINKS tend to be educated couples with high incomes, who enjoy a comfortable lifestyle. They often live in apartments in inner cities.

Empty nesters are couples whose children have left home. They are often still working, but may be close to retirement. They tend suddenly to find themselves with more time and more disposable income, and are therefore prime targets for marketers of hobby-related products, holidays, DIY and luxury goods.

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

80

1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

1 600 0002 100 0002 600 0003 100 0003 600 0004 100 0004 600 0005 100 0005 600 0006 100 0006 600 0007 100 0007 600 0008 100 0008 600 0009 100 0009 600 000

year

age

population

Age Structure of the population in Eastern Europe

opportunity

threat

Euromonitor International ©Retailing industry outlook in Eastern Europe

Income trends in Eastern Europe

Annual disposable income per household in 2009 , EUR

Bulgaria: 5,839Eastern Europe 9,447Western Europe 39,112

annu

al income US$

age

400

2400

4400

6400

8400

10400

12400

14400

15 20 25 30 35 40 45 50 55 60 65 70 75

Income by age in EE

0

50

100

150

200

250

300

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2003 2004 2005 2006 2007 2008 2009

annual disposable income consumer expenditure savings

Income, expenditure and savings growth in EE

EUR

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

0 5 000 10 000 15 000 20 000

Mean income 8,444

Median income 7,031

% of householdsIncome distribution in Eastern Europe

Annual disposable income EUR

Euromonitor International ©Retailing industry outlook in Eastern Europe

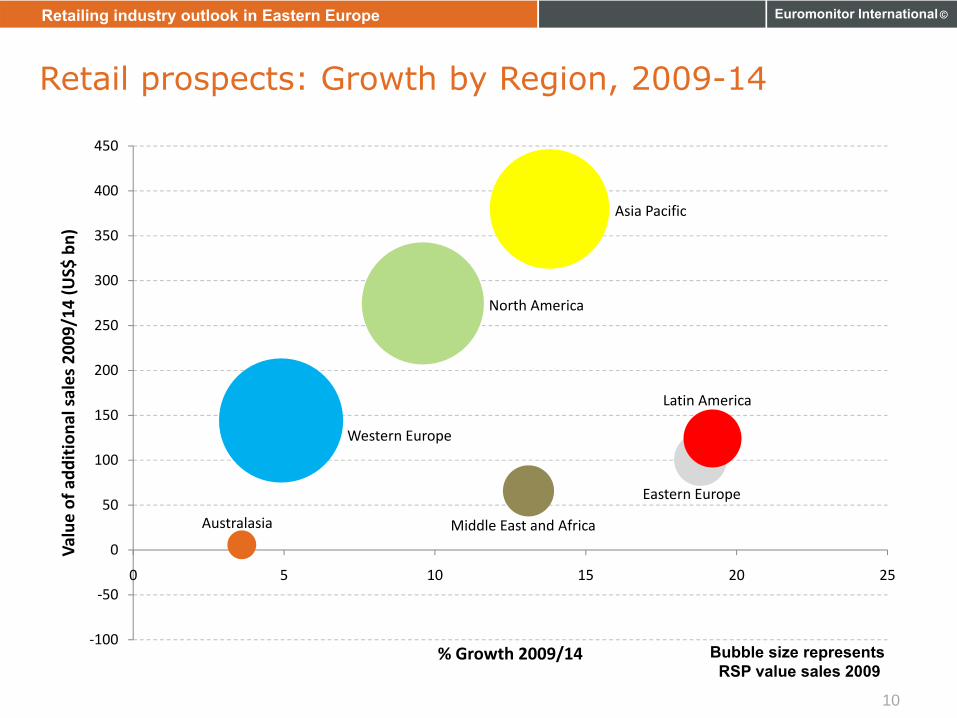

Retail prospects: Growth by Region, 2009-14

Asia Pacific

Australasia

Eastern Europe

Latin America

Middle East and Africa

North America

Western Europe

‐100

‐50

0

50

100

150

200

250

300

350

400

450

0 5 10 15 20 25

Value of add

itiona

l sales 2009/14

(US$

bn)

% Growth 2009/14 Bubble size representsRSP value sales 2009

10

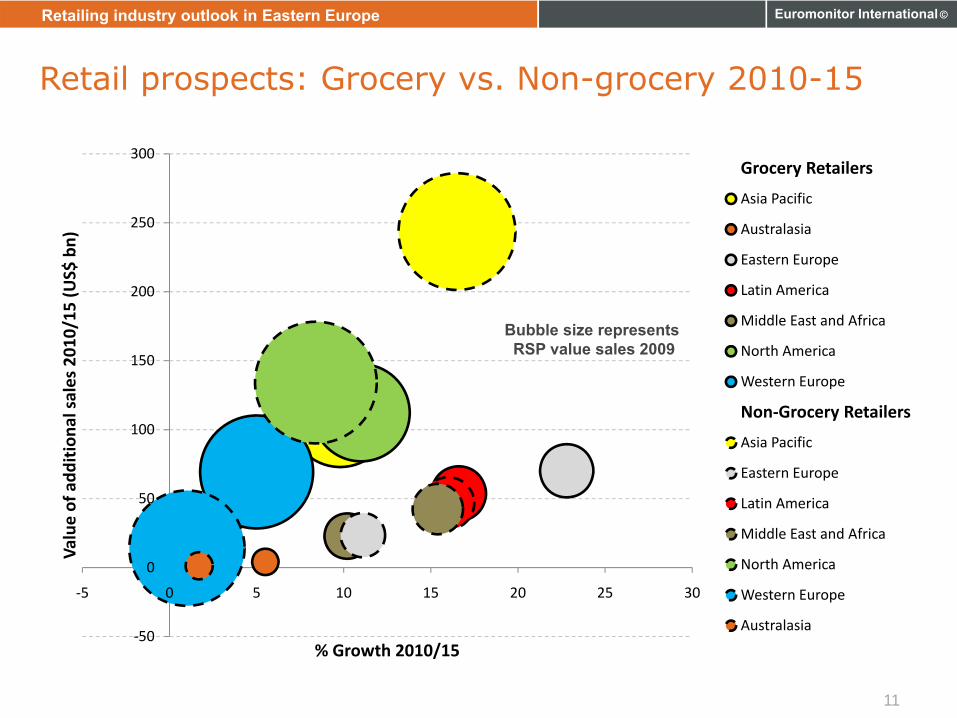

Euromonitor International ©Retailing industry outlook in Eastern Europe

‐50

0

50

100

150

200

250

300

‐5 0 5 10 15 20 25 30

Value of add

itiona

l sales 2010/15

(US$

bn)

% Growth 2010/15

Grocery Retailers

Asia Pacific

Australasia

Eastern Europe

Latin America

Middle East and Africa

North America

Western Europe

Non‐Grocery Retailers

Asia Pacific

Eastern Europe

Latin America

Middle East and Africa

North America

Western Europe

Australasia

Bubble size representsRSP value sales 2009

Retail prospects: Grocery vs. Non-grocery 2010-15

11

Euromonitor International ©Retailing industry outlook in Eastern Europe

Retailing Industry overview –neighboring countries

‐12

‐8

‐4

0

4

8

0

20

40

60

80

100

market size per capita growth 08/09

Market sizes: relative size, Ukraine =100Per capita: EUR(excl. VAT), relative sizes, Slovenia=100Growth: Year‐on‐year EUR

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

13

Euromonitor International ©Retailing industry outlook in Eastern Europe

Bulgaria Defined 4.8 mn m²of selling space

7.2 bn €Retail Value

80 768Outlets

86 mn €Retail Value

Store ba

sed retailing

in 2009

Non

‐store retailin

g in 2009

Bulgaria

14

Euromonitor International ©Retailing industry outlook in Eastern Europe

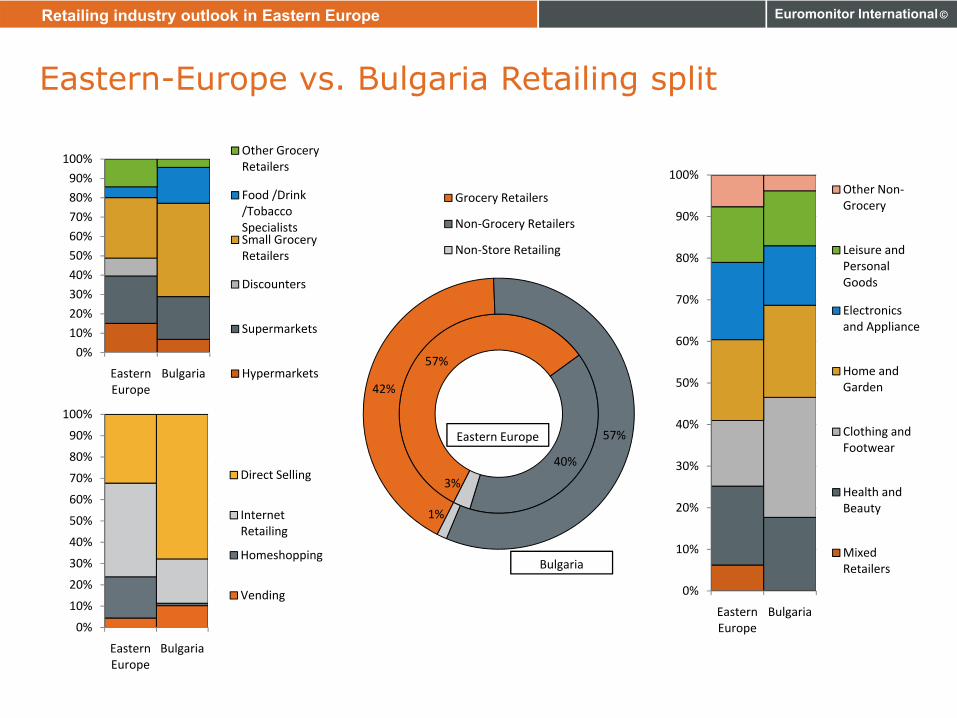

Eastern-Europe vs. Bulgaria Retailing split

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eastern Europe

Bulgaria

Direct Selling

Internet Retailing

Homeshopping

Vending

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eastern Europe

Bulgaria

Other Grocery Retailers

Food /Drink /Tobacco Specialists Small Grocery Retailers

Discounters

Supermarkets

Hypermarkets

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Eastern Europe

Bulgaria

Other Non‐Grocery

Leisure and Personal Goods

Electronics and Appliance

Home and Garden

Clothing and Footwear

Health and Beauty

Mixed Retailers

57%

40%

3%

42%

57%

1%

Grocery Retailers

Non‐Grocery Retailers

Non‐Store Retailing

Eastern Europe

Bulgaria

Euromonitor International ©Retailing industry outlook in Eastern Europe

Bulgaria-FMCG retail sizes, 08/09 growth and per capita comparison with EE leader

Beauty and Personal Care

Consumer Health Tissue and HygieneHome Care

Alcoholic Drinks Packaged FoodTobaccoSoft DrinksHot Drinks

519 million‐0.1%

321 million‐0.6%

2,120 million0.3%

152 million3.1%

150 million‐0.1%

154 million4%

93 million‐1%

271 million0.6%

1,342 million‐0.3%

*Market Sizes 2009 ‐ Retail/off‐trade Value RSP – EUR‐ Current (Nominal) prices ‐ Year‐on‐Year Exchange Rate

Estonia by 390%

Slovenia by 170%

Croatia by 165%

Slovenia by 50%

Croatia by 130%

Czech Republic by 140%

Hungary by 60%

Croatia by 170%

Croatia by 200%

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

17

Euromonitor International ©Retailing industry outlook in Eastern Europe

Retailers Producers

Consumers Megatrends

Consumerism

Convenience shops vs. hypermarkets

Rise of discounters

Shopping malls

18

Euromonitor International ©Retailing industry outlook in Eastern Europe

Trends

Lowering costs

Advertising and marketing

New products development

Adding value

Producers

19

Euromonitor International ©Retailing industry outlook in Eastern Europe

Trends

Lowering margins

Private label

Value offers

Internet retailing

Retailers

20

Euromonitor International ©Retailing industry outlook in Eastern Europe

Trends

Price sensitivity

Environment

Health and Wellness

Status shopping

Convenience

Consumers M

21

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

22

Euromonitor International ©Retailing industry outlook in Eastern Europe

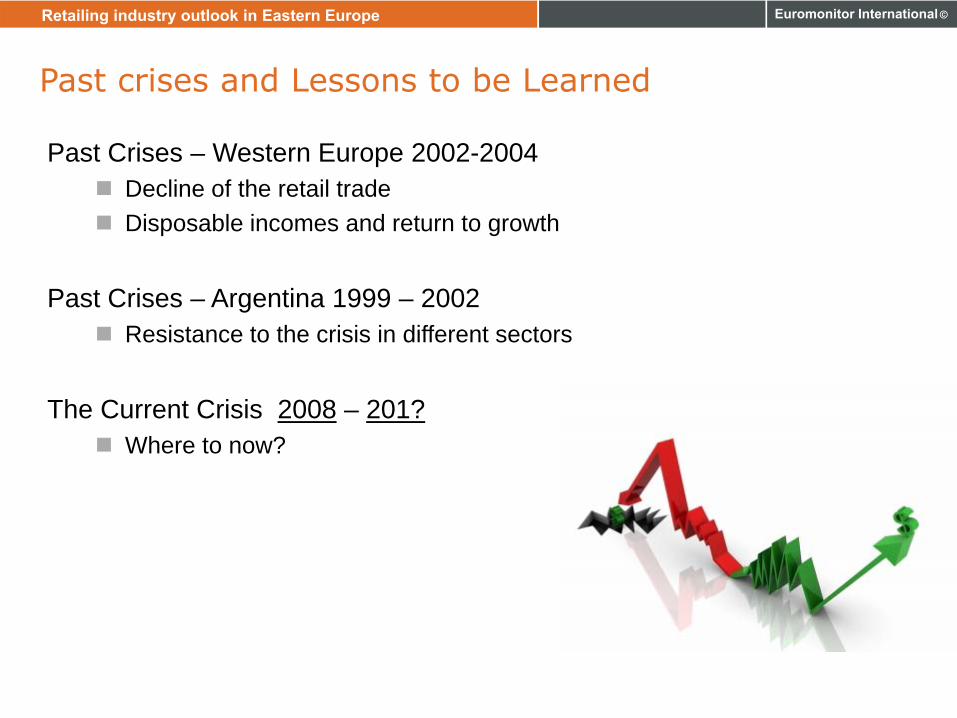

Past crises and Lessons to be Learned

Past Crises – Western Europe 2002-2004Decline of the retail tradeDisposable incomes and return to growth

Past Crises – Argentina 1999 – 2002Resistance to the crisis in different sectors

The Current Crisis 2008 – 201?Where to now?

Euromonitor International ©Retailing industry outlook in Eastern Europe

Way out of crisis in Bulgaria, possible scenario

Consistent Accelerated Transformed Newly Insignificantgrowth created

24

Euromonitor International ©Retailing industry outlook in Eastern Europe

About Euromonitor International

The context

Bulgaria defined

Trends

Crisis and lessons

Winners and losers

Q&A

25

Euromonitor International ©Retailing industry outlook in Eastern Europe

26

•Home and garden retailers•Leisure and personal goods retailers•Clothing and footwear retailers•Electronics and appliance retailers•“Traditional” retailers

•Hypermarkets•Supermarkets•Discounters•Internet retailing

Euromonitor International ©Retailing industry outlook in Eastern Europe

What will be drivers for growth?

How Will Retailers React?

Maintaining Margins

Value Offers

Private Label

Value AddingInternet Retailing

27

Euromonitor International ©Retailing industry outlook in Eastern Europe

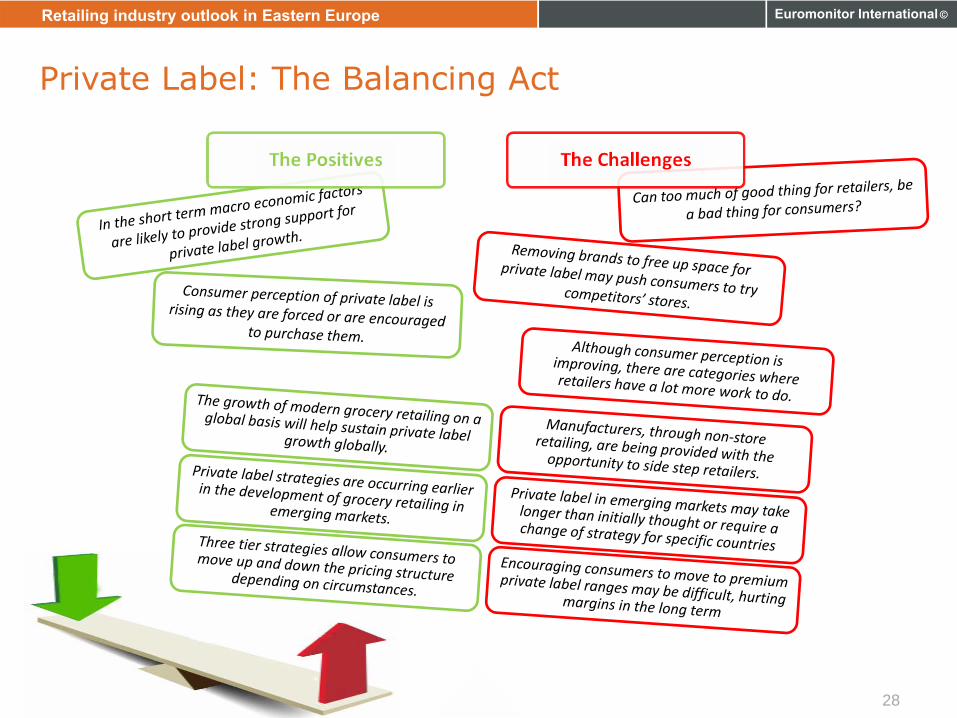

Private Label: The Balancing Act

28

Euromonitor International ©Retailing industry outlook in Eastern Europe

Adding Value: Tapping Into The Eco-Friendly Economy

Best Buy

Marks & SpencerP&G

29

Euromonitor International ©Retailing industry outlook in Eastern Europe

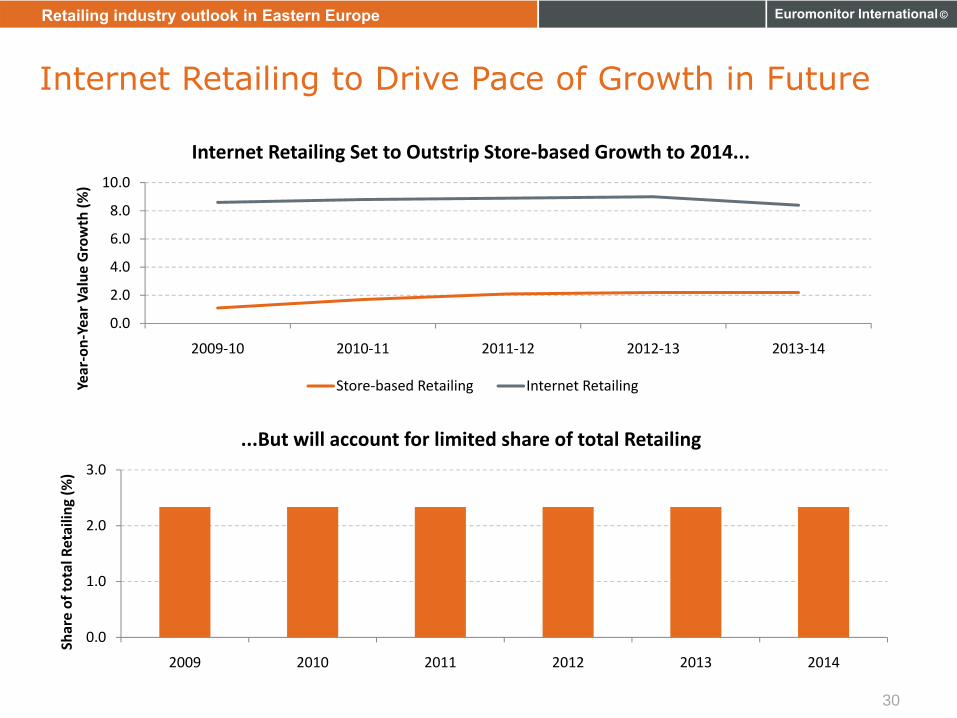

Internet Retailing to Drive Pace of Growth in Future

0.0

2.0

4.0

6.0

8.0

10.0

2009‐10 2010‐11 2011‐12 2012‐13 2013‐14

Year‐on‐Year Value

Growth (%

)

Internet Retailing Set to Outstrip Store‐based Growth to 2014...

Store‐based Retailing Internet Retailing

0.0

1.0

2.0

3.0

2009 2010 2011 2012 2013 2014

Share of to

tal R

etailin

g (%

)

...But will account for limited share of total Retailing

30

Euromonitor International ©Retailing industry outlook in Eastern Europe

Alice.com – Can manufacturers sidestep retailers?

Brands reclaim negotiating power?

Brands sidestep retailers?

E‐commerce grows in importance

Retailers gain power over brands

Private labels are launched

Retailers kowtow to brands

Brands have negotiating power

31

Euromonitor International ©Retailing industry outlook in Eastern Europe

For more information please contact:

Nikola Košutić, M.Sc.

Senior Research Analyst

Euromonitor International

32