Q2 2015 presentation

28

SECOND QUARTER 2015 July 21 st , 2015 Tele2 AB

-

Upload

tele2 -

Category

Investor Relations

-

view

3.240 -

download

1

Transcript of Q2 2015 presentation

SECONDQUARTER 2015July 21st, 2015

Tele2 AB

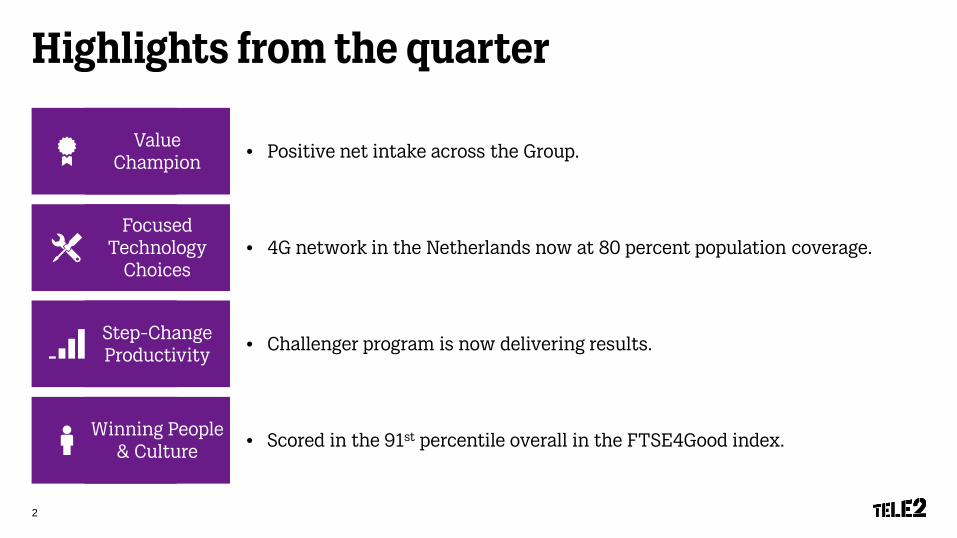

Highlights from the quarter

Winning People & Culture

Value Champion

Step-Change Productivity

Focused Technology

Choices

• Scored in the 91st percentile overall in the FTSE4Good index.

• 4G network in the Netherlands now at 80 percent population coverage.

• Positive net intake across the Group.

• Challenger program is now delivering results.

2

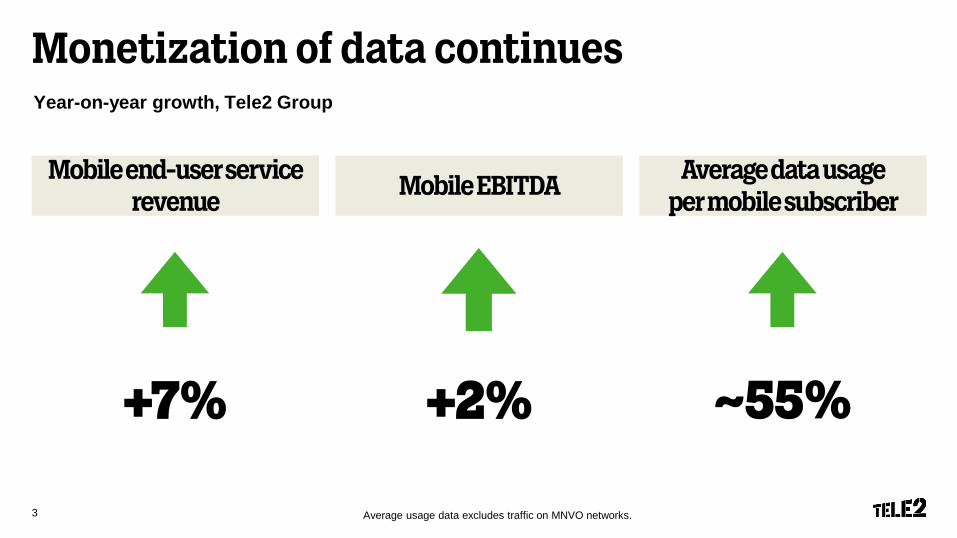

Monetization of data continues

Average usage data excludes traffic on MNVO networks.

Year-on-year growth, Tele2 Group

Mobile end-user service revenue

Mobile EBITDA Average data usage per mobile subscriber

+7% +2% ~55%

3

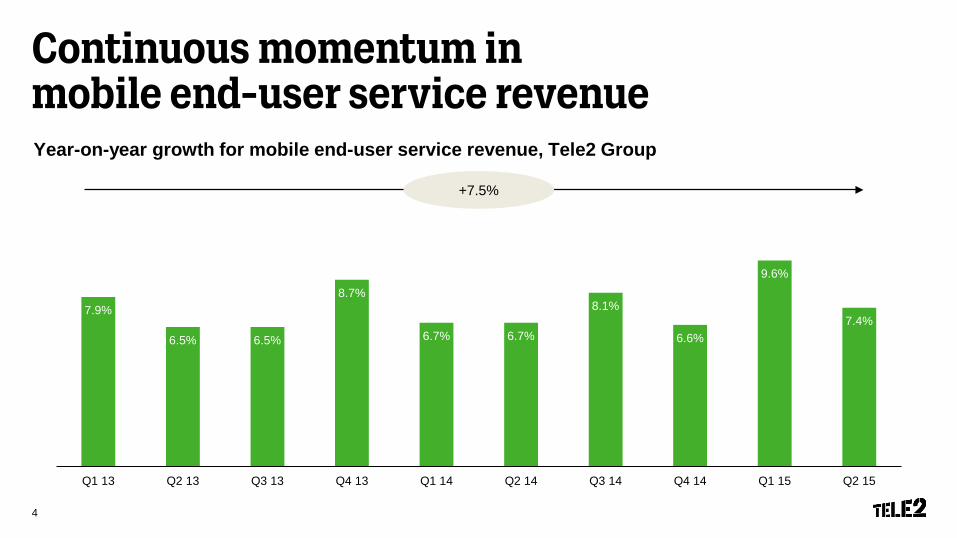

Continuous momentum in mobile end-user service revenue Year-on-year growth for mobile end-user service revenue, Tele2 Group

+7.5%

7.9%

6.5% 6.5%

8.7%

6.7% 6.7%

8.1%

6.6%

9.6%

7.4%

Q1 13 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

4

Kazakhstan: +65%

Latvia: +8%

Lithuania: +4%

Sweden: +1%

Netherlands: +8%

Austria: -1%*

Croatia: +7%

Germany: +6%

Estonia: +6%

Market year-on-year development

* Total net sales

Mobile end-user service revenue Data growth (MNO networks)

~70%

Q2 14 Q2 15

Sweden CEE

Kazakhstan

5

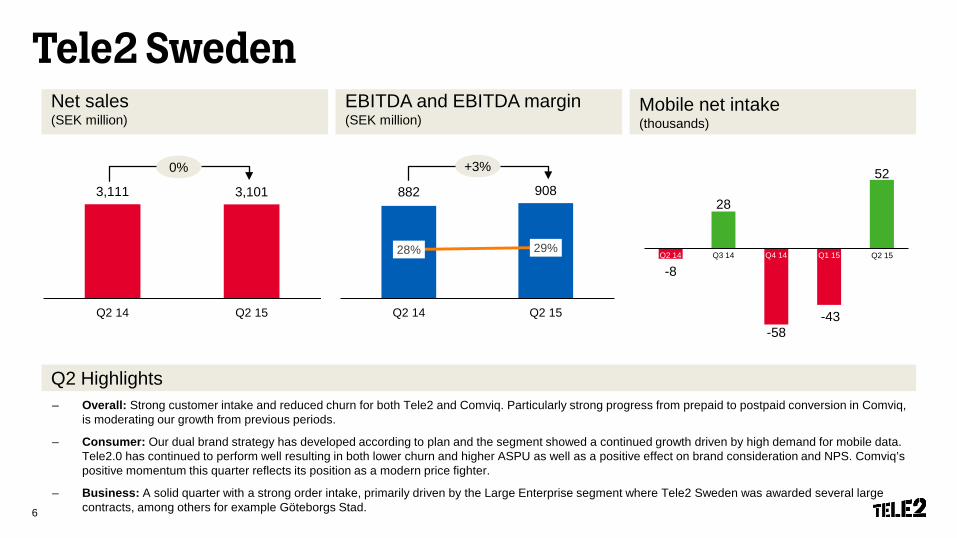

Tele2 SwedenNet sales(SEK million)

EBITDA and EBITDA margin(SEK million)

Mobile net intake(thousands)

– Overall: Strong customer intake and reduced churn for both Tele2 and Comviq. Particularly strong progress from prepaid to postpaid conversion in Comviq,is moderating our growth from previous periods.

– Consumer: Our dual brand strategy has developed according to plan and the segment showed a continued growth driven by high demand for mobile data. Tele2.0 has continued to perform well resulting in both lower churn and higher ASPU as well as a positive effect on brand consideration and NPS. Comviq’spositive momentum this quarter reflects its position as a modern price fighter.

– Business: A solid quarter with a strong order intake, primarily driven by the Large Enterprise segment where Tele2 Sweden was awarded several large contracts, among others for example Göteborgs Stad.

Q2 Highlights

3,111 3,101

Q2 14 Q2 15

0%

882 908

28% 29%

0%

10%

20%

30%

40%

50%

60%

Q2 14 Q2 150

100

200

300

400

500

600

700

800

900

1000

+3%

-8

28

-58-43

52

Q4 14 Q1 15Q2 14 Q3 14 Q2 15

6

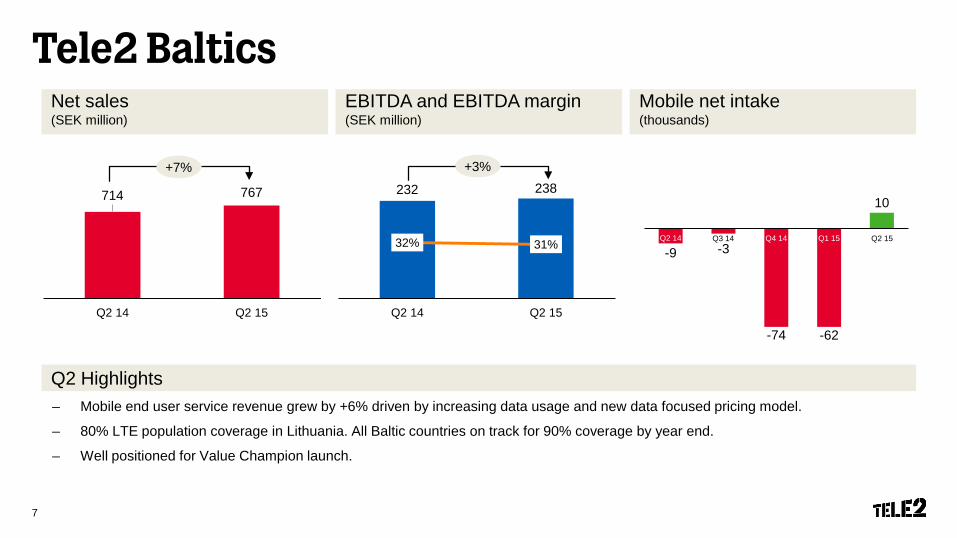

Tele2 BalticsNet sales(SEK million)

EBITDA and EBITDA margin(SEK million)

Mobile net intake(thousands)

– Mobile end user service revenue grew by +6% driven by increasing data usage and new data focused pricing model.

– 80% LTE population coverage in Lithuania. All Baltic countries on track for 90% coverage by year end.

– Well positioned for Value Champion launch.

Q2 Highlights

714 767

Q2 14 Q2 15

232 238

32% 31%

0%

10%

20%

30%

40%

50%

60%

Q2 14 Q2 150

50

100

150

200

250

+7% +3%

-9 -3

-74 -62

10

Q4 14 Q1 15Q2 14 Q3 14 Q2 15

7

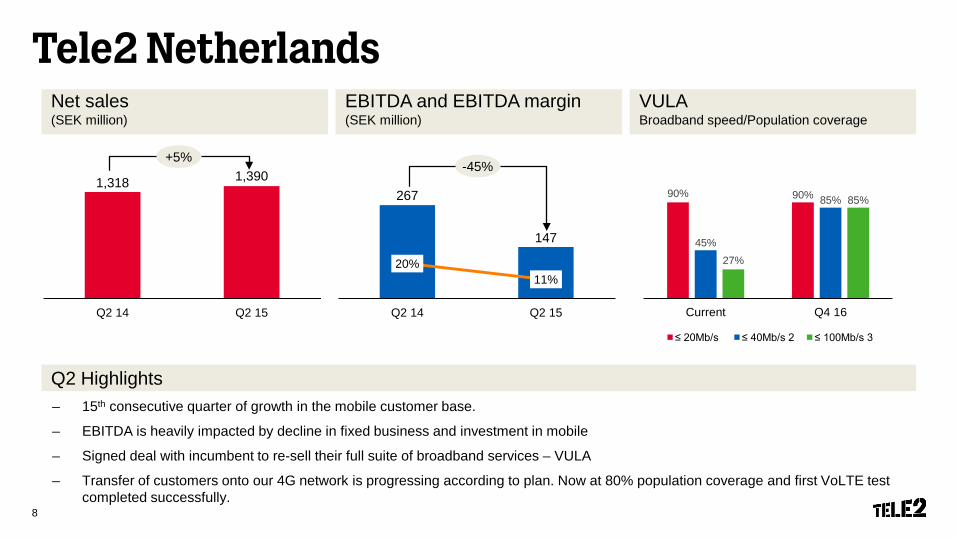

Tele2 NetherlandsNet sales(SEK million)

EBITDA and EBITDA margin(SEK million)

Q2 Highlights– 15th consecutive quarter of growth in the mobile customer base.

– EBITDA is heavily impacted by decline in fixed business and investment in mobile

– Signed deal with incumbent to re-sell their full suite of broadband services – VULA

– Transfer of customers onto our 4G network is progressing according to plan. Now at 80% population coverage and first VoLTE test completed successfully.

VULABroadband speed/Population coverage

1,318 1,390

Q2 14 Q2 15

267

147

20%11%

0%

10%

20%

30%

40%

50%

60%

Q2 14 Q2 150

50

100

150

200

250

300

+5%-45%

90% 90%

45%

85%

27%

85%

Current Q4 16

≤ 20Mb/s ≤ 40Mb/s 2 ≤ 100Mb/s 3

8

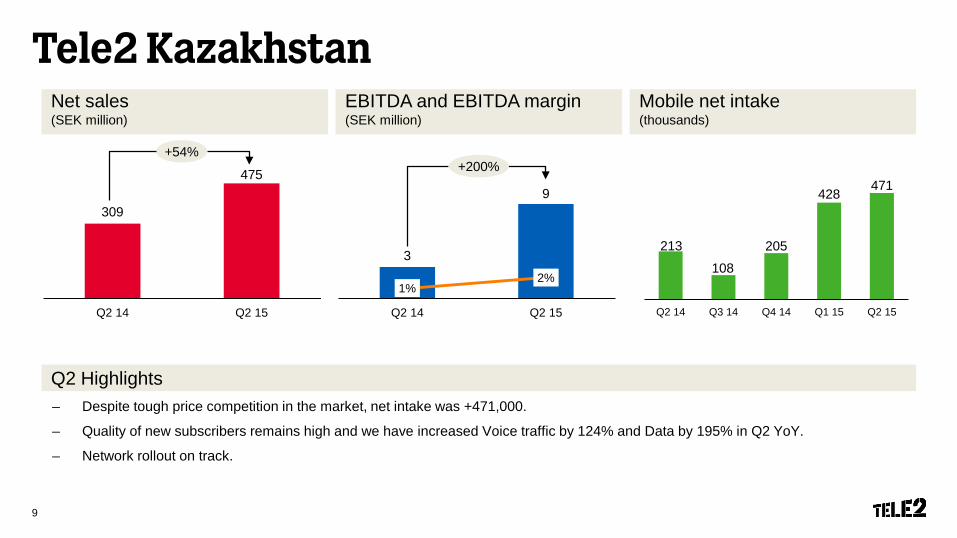

Tele2 Kazakhstan

– Despite tough price competition in the market, net intake was +471,000.

– Quality of new subscribers remains high and we have increased Voice traffic by 124% and Data by 195% in Q2 YoY.

– Network rollout on track.

Net sales(SEK million)

EBITDA and EBITDA margin(SEK million)

Q2 Highlights

Mobile net intake(thousands)

309

475

Q2 14 Q2 15

3

9

1%2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Q2 14 Q2 150

1

2

3

4

5

6

7

8

9

10

+54%+200%

213

108

205

428 471

Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

9

Financial Overview

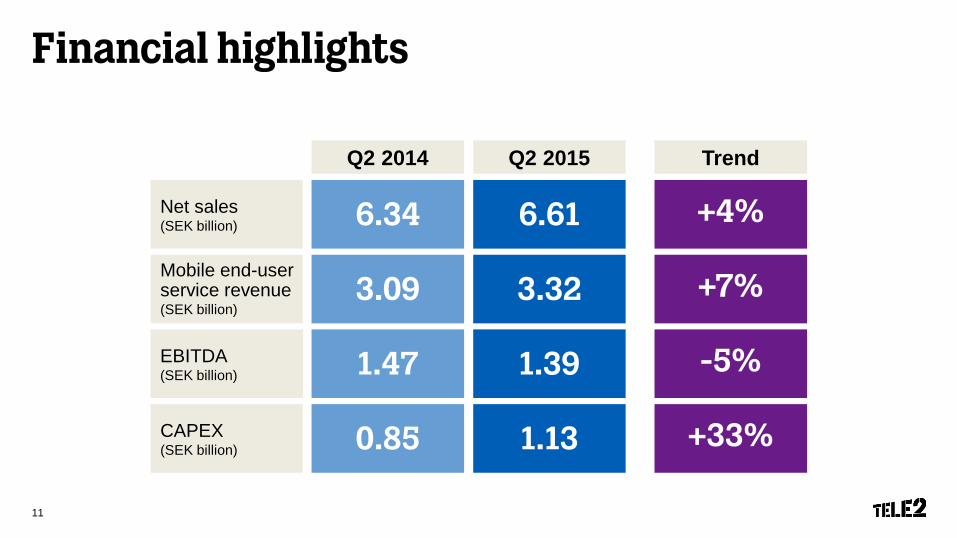

Financial highlights

Mobile end-user service revenue(SEK billion)

3.32

EBITDA(SEK billion) 1.39

CAPEX(SEK billion) 1.13

Net sales(SEK billion) 6.61

Q2 2015 Trend

+7%

-5%

+33%

+4%

3.09

1.47

0.85

6.34

Q2 2014

11

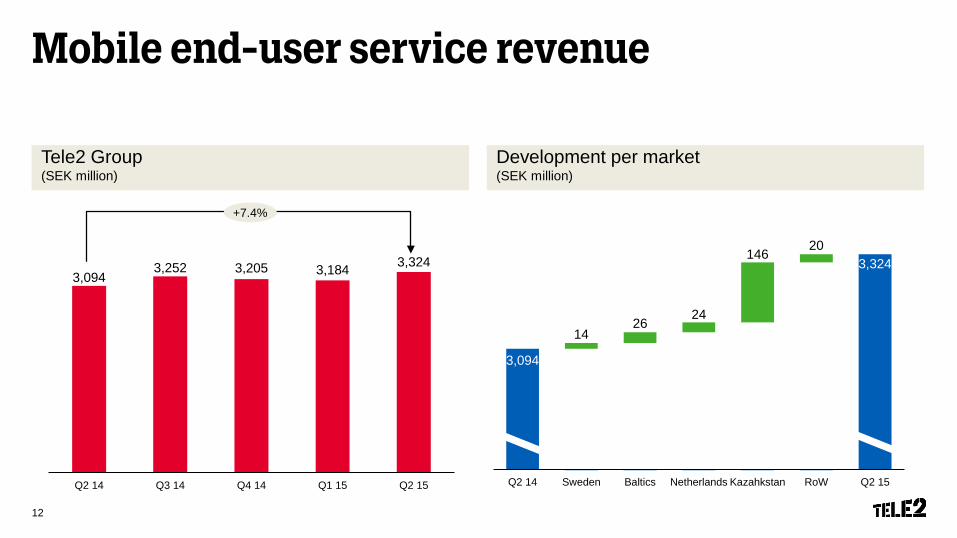

Mobile end-user service revenue

Tele2 Group(SEK million)

Development per market(SEK million)

3,205

3,0943,252 3,205 3,184 3,324

Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

+7.4%

3,094

3,324

1426

24

14620

Q2 14 Sweden Baltics Netherlands Kazahkstan RoW Q2 15

12

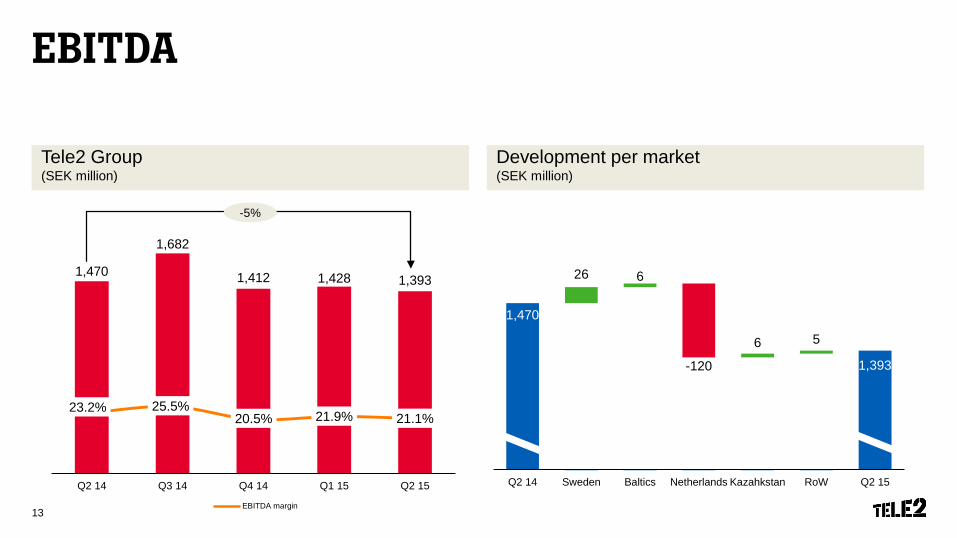

EBITDA

Tele2 Group(SEK million)

1,412

Development per market(SEK million)

1,470

1,682

1,412 1,428 1,393

23.2% 25.5%20.5% 21.9% 21.1%

0

200

400

600

800

1000

1200

1400

1600

1800

Q2 14 Q3 14 Q4 14 Q1 15 Q2 150.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

EBITDA margin

1,470

1,393

26 6

-120

6 5

Q2 14 Sweden Baltics Netherlands Kazahkstan RoW Q2 15

-5%

13

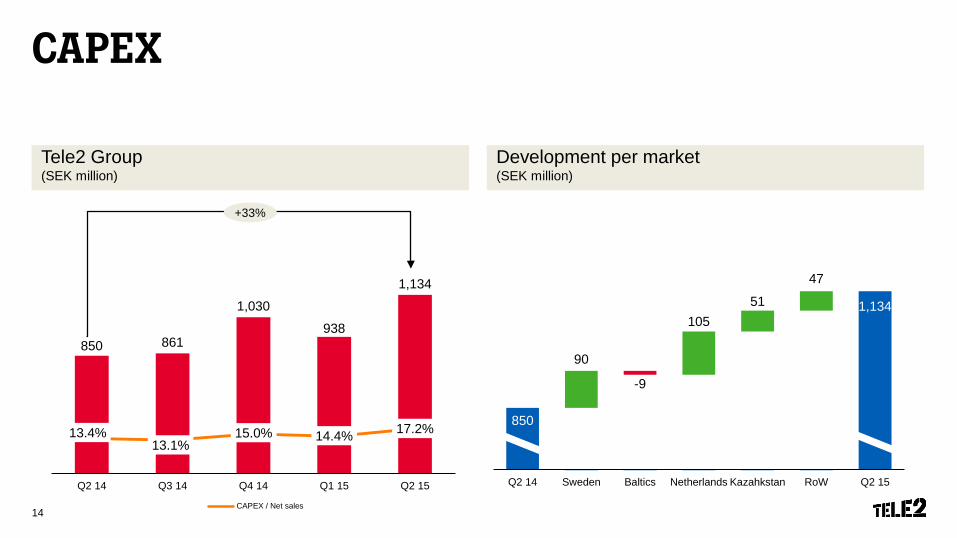

CAPEX

Tele2 Group(SEK million)

Development per market(SEK million)

850 861

1,030

938

1,134

13.4%13.1%

15.0% 14.4% 17.2%

300

500

700

900

1100

1300

Q2 14 Q3 14 Q4 14 Q1 15 Q2 150.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

CAPEX / Net sales

850

1,134

90

-9

10551

47

Q2 14 Sweden Baltics Netherlands Kazahkstan RoW Q2 15

+33%

14

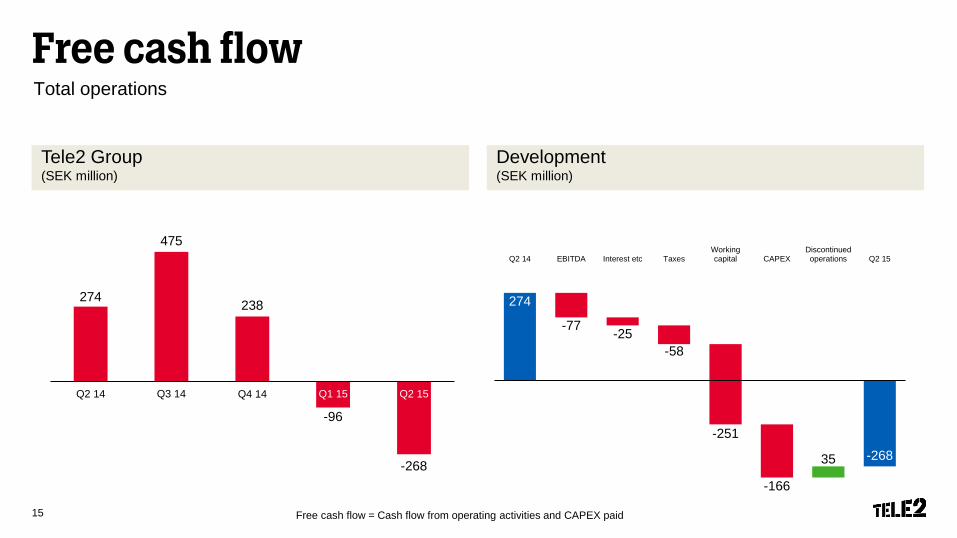

Free cash flowTotal operations

Tele2 Group(SEK million)

Development (SEK million)

Free cash flow = Cash flow from operating activities and CAPEX paid

274

475

238

-96

-268-400

-300

-200

-100

0

100

200

300

400

500

600

Q2 14 Q3 14 Q4 14 Q1 15 Q2 15

274

-77 -25-58

-251

-166

35 -268

Q2 14 EBITDA Interest etc TaxesWorkingcapital CAPEX

Discontinuedoperations Q2 15

Q2 15

15

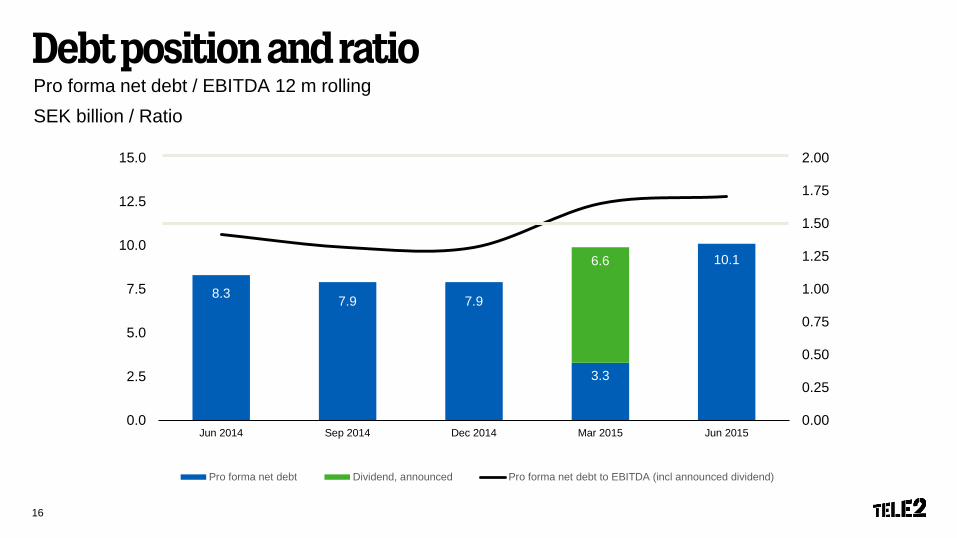

Debt position and ratioPro forma net debt / EBITDA 12 m rollingSEK billion / Ratio

8.3 7.9 7.9

3.3

10.16.6

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

0.0

2.5

5.0

7.5

10.0

12.5

15.0

Jun 2014 Sep 2014 Dec 2014 Mar 2015 Jun 2015

Pro forma net debt Dividend, announced Pro forma net debt to EBITDA (incl announced dividend)

16

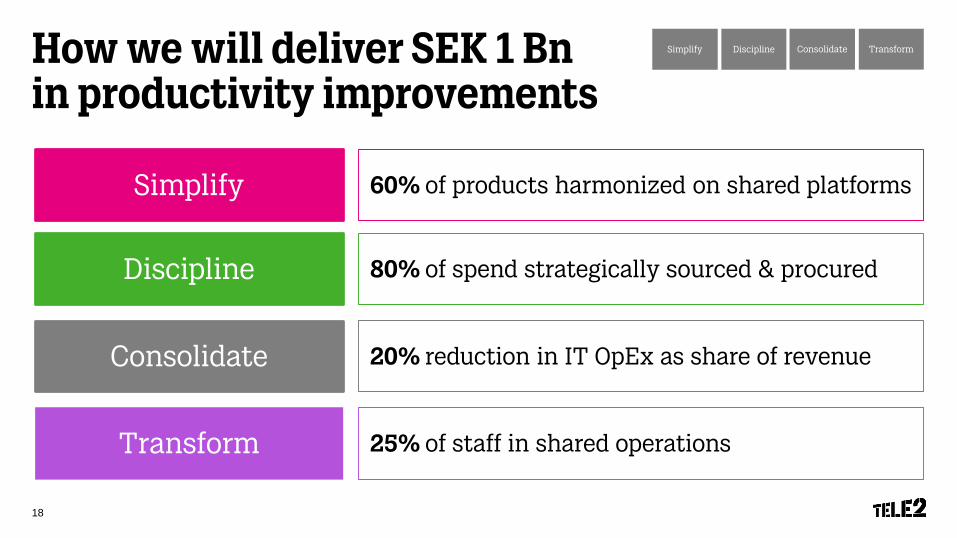

CHALLENGER PROGRAM

Step-change productivity

How we will deliver SEK 1 Bnin productivity improvements

Simplify

Transform

Consolidate

Discipline

Simplify Discipline Consolidate Transform

60% of products harmonized on shared platforms

80% of spend strategically sourced & procured

20% reduction in IT OpEx as share of revenue

25% of staff in shared operations

18

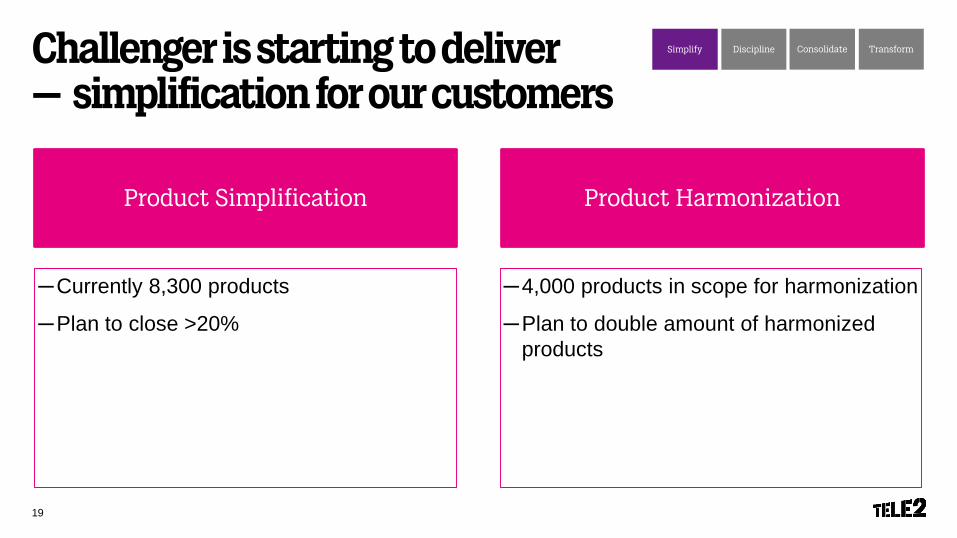

Challenger is starting to deliver – simplification for our customers

Simplify Discipline Consolidate Transform

Product Simplification

─ Currently 8,300 products

─ Plan to close >20%

Product Harmonization

─ 4,000 products in scope for harmonization

─ Plan to double amount of harmonized products

19

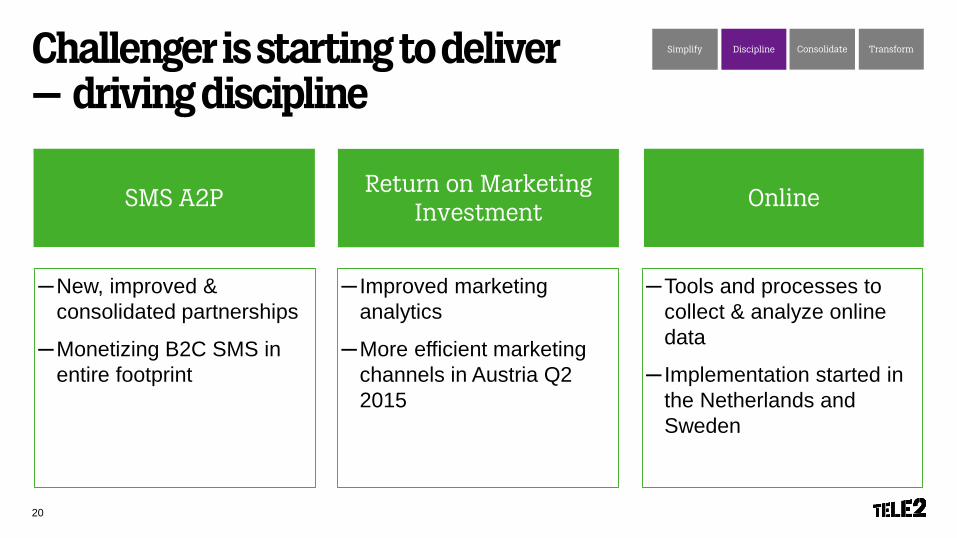

Challenger is starting to deliver – driving discipline

Simplify Discipline Consolidate Transform

SMS A2P

─ New, improved & consolidated partnerships

─ Monetizing B2C SMS in entire footprint

Online

─ Tools and processes to collect & analyze online data

─ Implementation started in the Netherlands and Sweden

Return on Marketing Investment

─ Improved marketing analytics

─ More efficient marketing channels in Austria Q2 2015

20

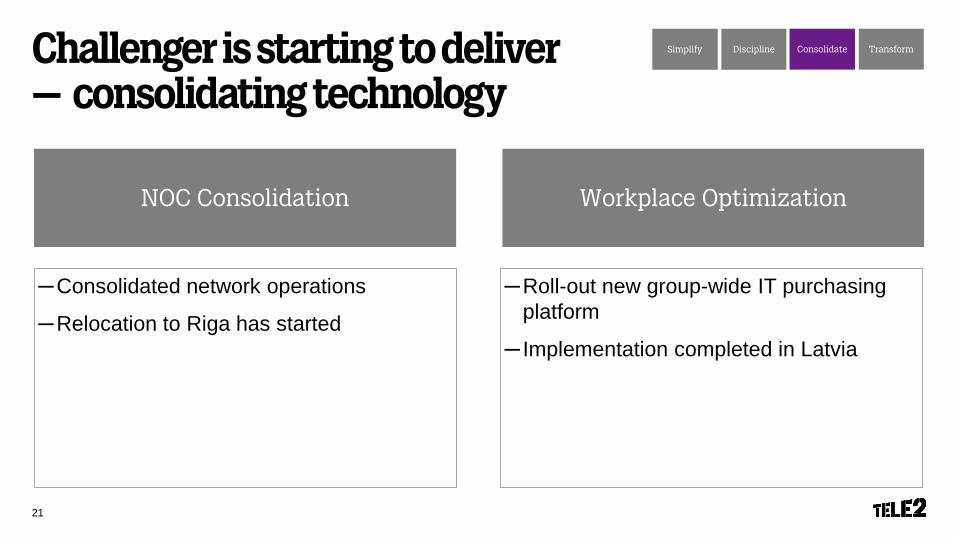

Challenger is starting to deliver – consolidating technology

Simplify Discipline Consolidate Transform

NOC Consolidation

─ Consolidated network operations

─ Relocation to Riga has started

Workplace Optimization

─ Roll-out new group-wide IT purchasing platform

─ Implementation completed in Latvia

21

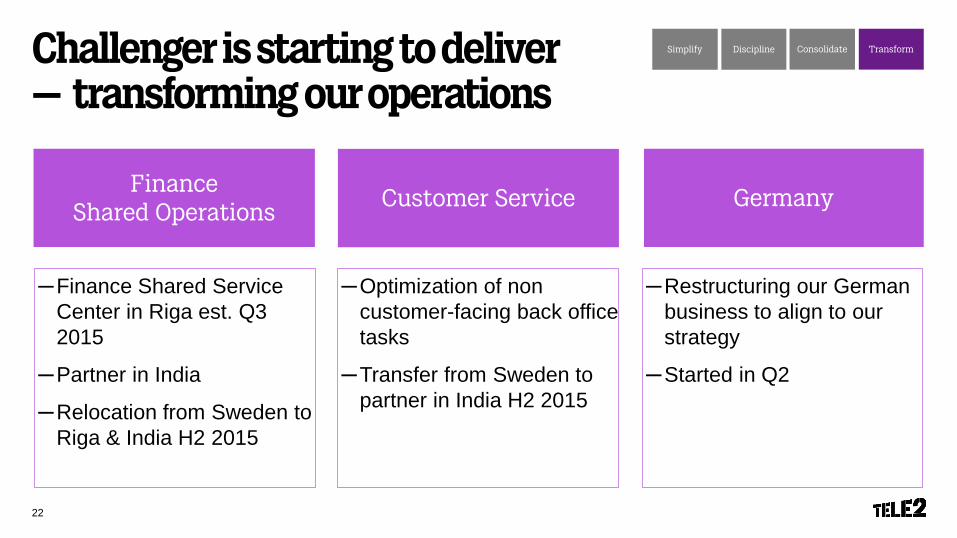

Challenger is starting to deliver – transforming our operations

Simplify Discipline Consolidate Transform

Finance Shared Operations

─ Finance Shared Service Center in Riga est. Q3 2015

─ Partner in India

─ Relocation from Sweden to Riga & India H2 2015

Germany

─ Restructuring our German business to align to our strategy

─ Started in Q2

Customer Service

─ Optimization of non customer-facing back office tasks

─ Transfer from Sweden to partner in India H2 2015

22

2015 2016 2017 2018

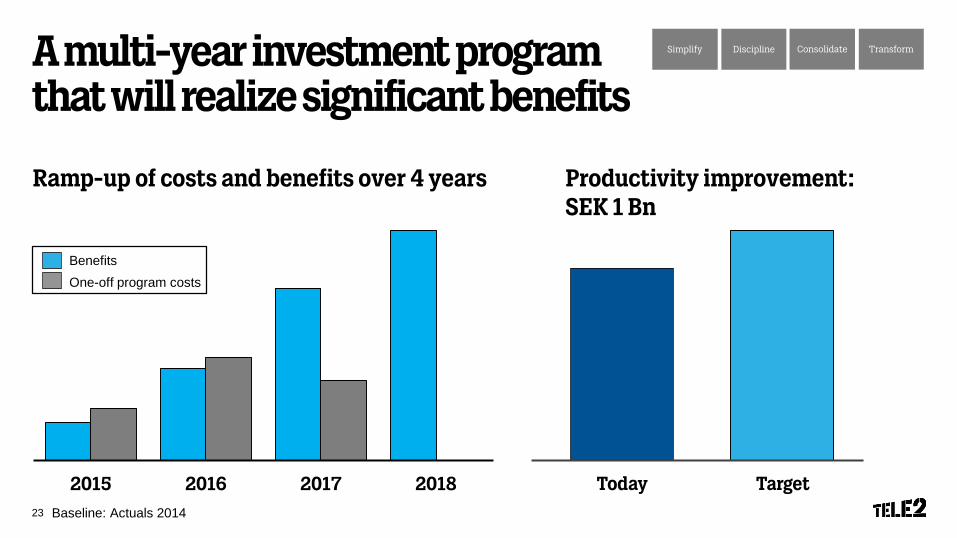

A multi-year investment program that will realize significant benefits

Baseline: Actuals 2014

Ramp-up of costs and benefits over 4 years

Simplify Discipline Consolidate Transform

Productivity improvement: SEK 1 Bn

Today Target

BenefitsOne-off program costs

23

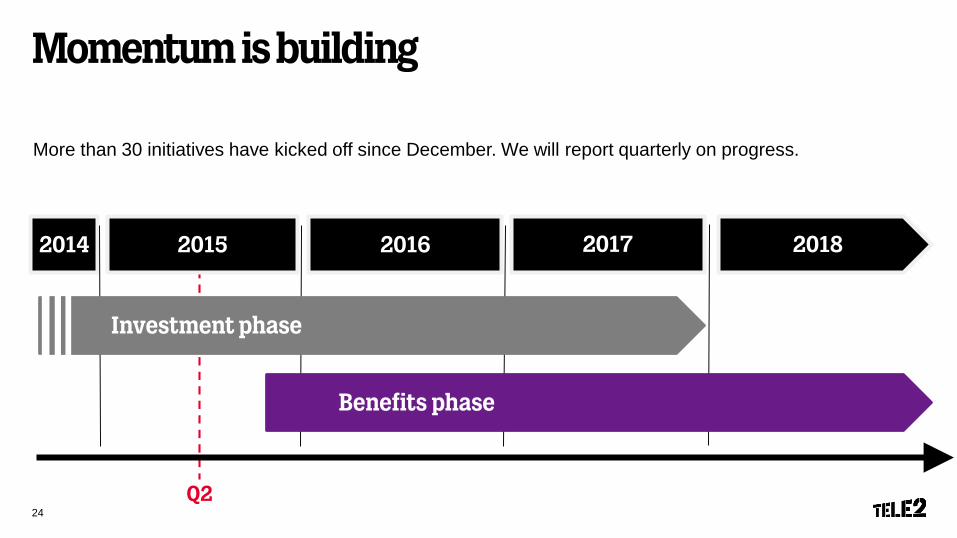

Momentum is building

2015 20162014

More than 30 initiatives have kicked off since December. We will report quarterly on progress.

Q2

2017 2018

Investment phase

Benefits phase

24

Q2 2015 Summary

25

Q2 2015 in short and key priorities moving forward

- Continued focus on Data monetization

- Getting ready for 4G launch in Netherlands and the Baltics

- Executing on the Challenger Program

Winning People & Culture

Value Champion

Step-Change Productivity

Focused Technology

Choices

26

Tele2’s Way2Win

The Tele2 Way

Where we focus

We are challengers, fast-movers and will always offer our customers what they need for less

We will be champions of customer value in everything we do

Mobile access is our core business

Europe and Eurasia are our

markets

Residential and Business

How we win

Focused Technology

Choices

Value Champion

Step-Change Productivity

Winning People & Culture

Vision

Mission

27

THEEND