Project rashmi steel

40

4Q 2012 and FY 2012 Results 6 February 2013 Lakshmi N Mittal, Chairman and Chief Executive Officer Aditya Mittal, Chief Financial Officer

-

Upload

ranadeep-poddar -

Category

Business

-

view

68 -

download

3

Transcript of Project rashmi steel

4Q 2012 and FY 2012 Results

6 February 2013

Lakshmi N Mittal, Chairman and Chief Executive Officer

Aditya Mittal, Chief Financial Officer

1

Disclaimer

Forward-Looking Statements

This document may contain forward-looking information and statements about

ArcelorMittal and its subsidiaries. These statements include financial projections and estimates

and their underlying assumptions, statements regarding plans, objectives and expectations with

respect to future operations, products and services, and statements regarding future performance.

Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,”

“target” or similar expressions. Although ArcelorMittal’s management believes that the

expectations reflected in such forward-looking statements are reasonable, investors and holders

of ArcelorMittal’s securities are cautioned that forward-looking information and statements are

subject to numerous risks and uncertainties, many of which are difficult to predict and generally

beyond the control of ArcelorMittal, that could cause actual results and developments to differ

materially and adversely from those expressed in, or implied or projected by, the forward-looking

information and statements. These risks and uncertainties include those discussed or identified in

the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de

Surveillance du Secteur Financier) and the United States Securities and Exchange Commission

(the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal’s Annual Report on Form

20-F for the year ended December 31, 2011 filed with the SEC. ArcelorMittal undertakes no

obligation to publicly update its forward-looking statements, whether as a result of new

information, future events, or otherwise.

2

Agenda

• Results overview and recent developments

• Market outlook

• Results analysis

• Outlook and guidance

3

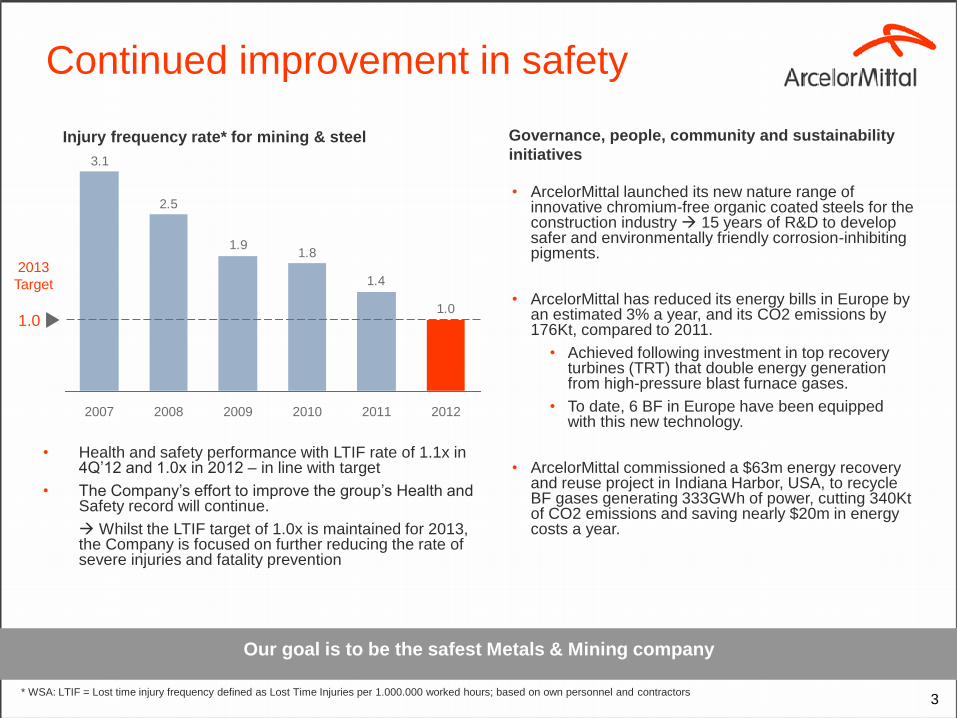

Continued improvement in safety

* WSA: LTIF = Lost time injury frequency defined as Lost Time Injuries per 1.000.000 worked hours; based on own personnel and contractors

Our goal is to be the safest Metals & Mining company

Governance, people, community and sustainability

initiatives

• ArcelorMittal launched its new nature range of innovative chromium-free organic coated steels for the construction industry 15 years of R&D to develop safer and environmentally friendly corrosion-inhibiting pigments.

• ArcelorMittal has reduced its energy bills in Europe by an estimated 3% a year, and its CO2 emissions by 176Kt, compared to 2011.

• Achieved following investment in top recovery turbines (TRT) that double energy generation from high-pressure blast furnace gases.

• To date, 6 BF in Europe have been equipped with this new technology.

• ArcelorMittal commissioned a $63m energy recovery and reuse project in Indiana Harbor, USA, to recycle BF gases generating 333GWh of power, cutting 340Kt of CO2 emissions and saving nearly $20m in energy costs a year.

Injury frequency rate* for mining & steel

1.0

1.4

1.81.9

2.5

3.1

1.0

2012 2011 2010 2009 2008 2007

2013

Target

• Health and safety performance with LTIF rate of 1.1x in 4Q’12 and 1.0x in 2012 – in line with target

• The Company’s effort to improve the group’s Health and Safety record will continue.

Whilst the LTIF target of 1.0x is maintained for 2013, the Company is focused on further reducing the rate of severe injuries and fatality prevention

4

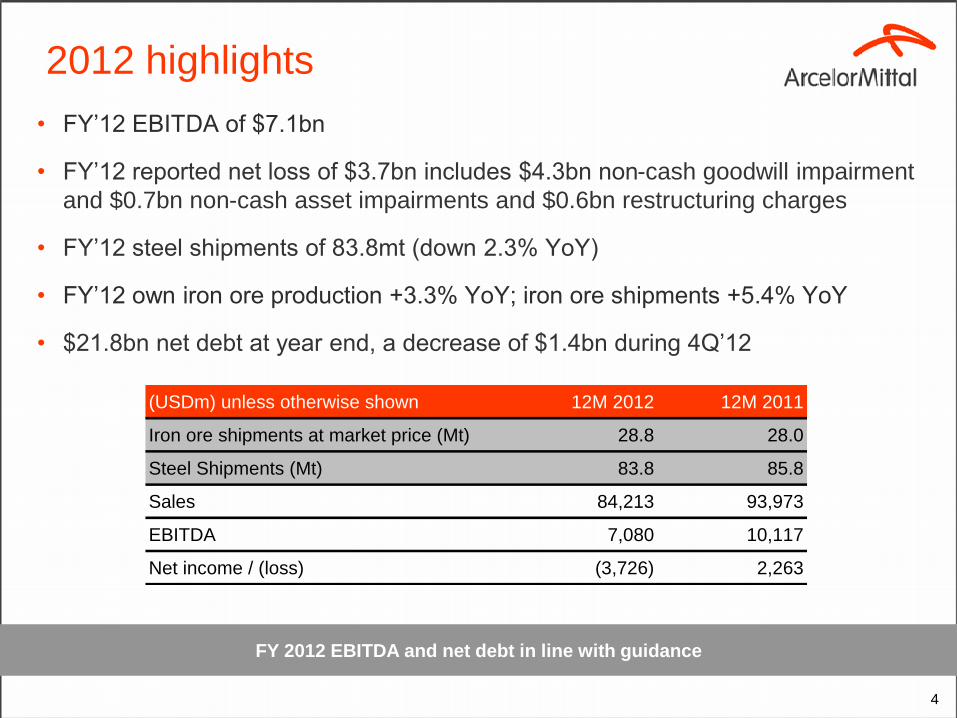

2012 highlights

• FY’12 EBITDA of $7.1bn

• FY’12 reported net loss of $3.7bn includes $4.3bn non-cash goodwill impairment

and $0.7bn non-cash asset impairments and $0.6bn restructuring charges

• FY’12 steel shipments of 83.8mt (down 2.3% YoY)

• FY’12 own iron ore production +3.3% YoY; iron ore shipments +5.4% YoY

• $21.8bn net debt at year end, a decrease of $1.4bn during 4Q’12

FY 2012 EBITDA and net debt in line with guidance

(USDm) unless otherwise shown 12M 2012 12M 2011

Iron ore shipments at market price (Mt) 28.8 28.0

Steel Shipments (Mt) 83.8 85.8

Sales 84,213 93,973

EBITDA 7,080 10,117

Net income / (loss) (3,726) 2,263

5

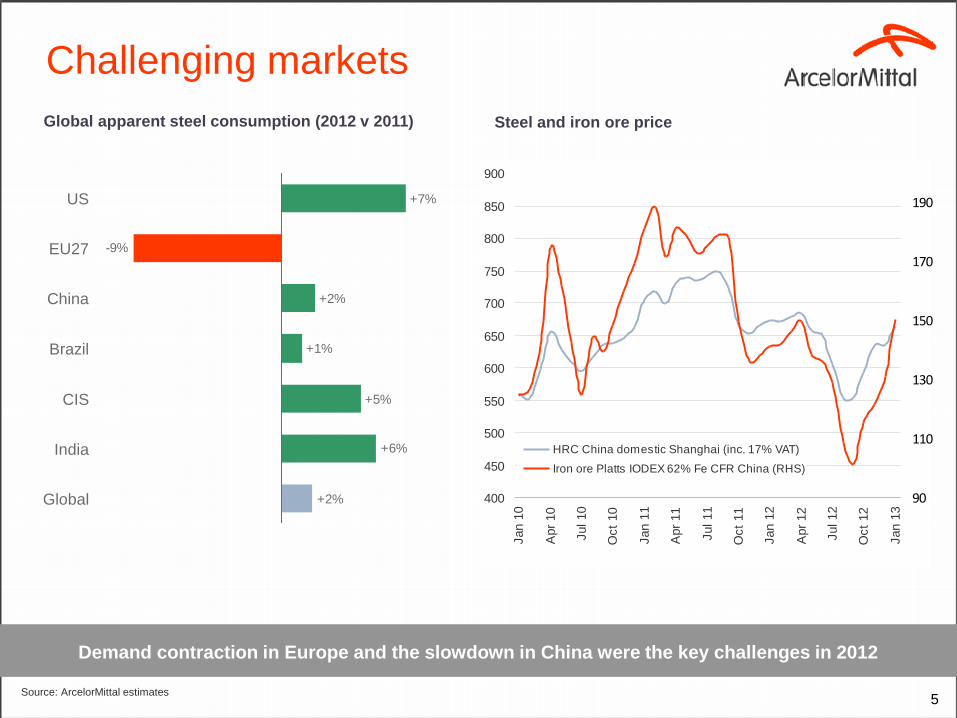

Challenging markets

1H

1,354 1,336

2,449 1,972

1,714

Global apparent steel consumption (2012 v 2011) Steel and iron ore price

+7%

+2%

+1%

+2%

+6%

+5%

-9%

CIS

Brazil

China

EU27

US

Global

India

Demand contraction in Europe and the slowdown in China were the key challenges in 2012

Source: ArcelorMittal estimates

400

450

500

550

600

650

700

750

800

850

900

Jan 1

0

Apr

10

Jul 10

Oct

10

Jan 1

1

Apr

11

Jul 11

Oct

11

Jan 1

2

Apr

12

Jul 12

Oct

12

Jan 1

3

90

110

130

150

170

190

HRC China domestic Shanghai (inc. 17% VAT)

Iron ore Platts IODEX 62% Fe CFR China (RHS)

6

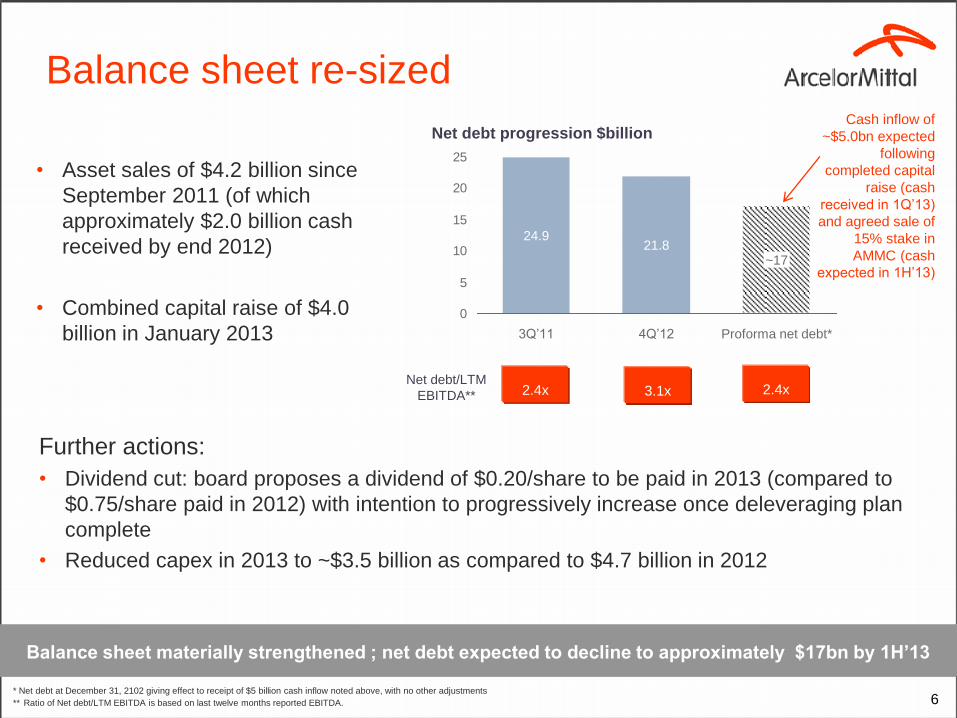

Balance sheet re-sized

• Asset sales of $4.2 billion since

September 2011 (of which

approximately $2.0 billion cash

received by end 2012)

• Combined capital raise of $4.0

billion in January 2013 0

5

10

15

20

25

Proforma net debt*

~17

4Q’12

21.8

3Q’11

24.9

Further actions:

• Dividend cut: board proposes a dividend of $0.20/share to be paid in 2013 (compared to

$0.75/share paid in 2012) with intention to progressively increase once deleveraging plan

complete

• Reduced capex in 2013 to ~$3.5 billion as compared to $4.7 billion in 2012

2.4x Net debt/LTM

EBITDA**

Cash inflow of

~$5.0bn expected

following

completed capital

raise (cash

received in 1Q’13)

and agreed sale of

15% stake in

AMMC (cash

expected in 1H’13)

Net debt progression $billion

3.1x 2.4x

* Net debt at December 31, 2102 giving effect to receipt of $5 billion cash inflow noted above, with no other adjustments

** Ratio of Net debt/LTM EBITDA is based on last twelve months reported EBITDA.

Balance sheet materially strengthened ; net debt expected to decline to approximately $17bn by 1H’13

7

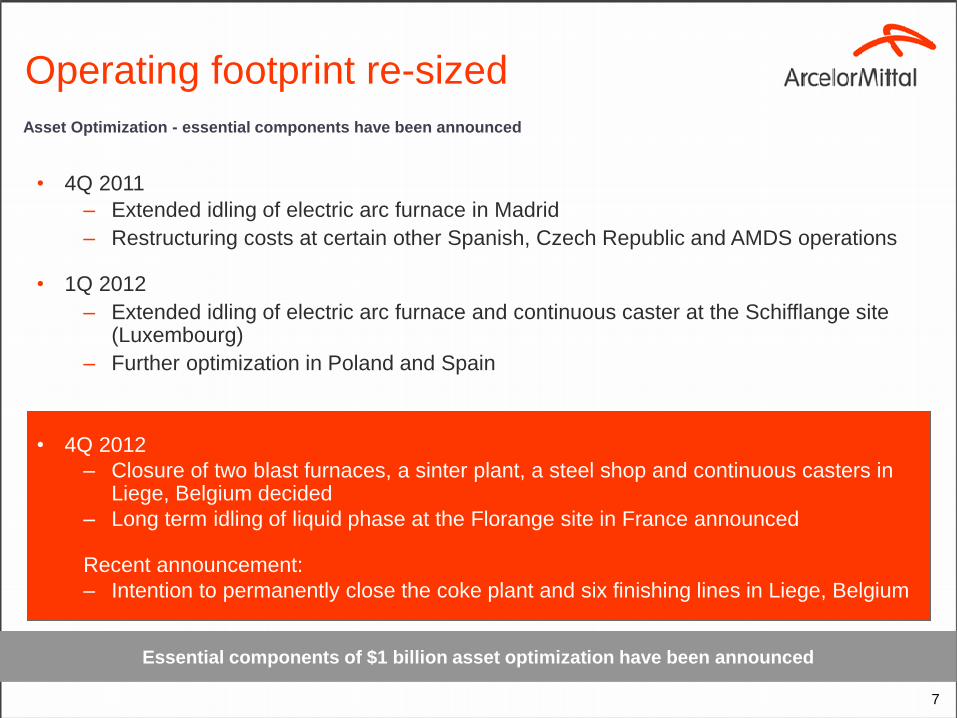

Operating footprint re-sized

Essential components of $1 billion asset optimization have been announced

Asset Optimization - essential components have been announced

• 4Q 2011

– Extended idling of electric arc furnace in Madrid

– Restructuring costs at certain other Spanish, Czech Republic and AMDS operations

• 1Q 2012

– Extended idling of electric arc furnace and continuous caster at the Schifflange site (Luxembourg)

– Further optimization in Poland and Spain

• 4Q 2012

– Closure of two blast furnaces, a sinter plant, a steel shop and continuous casters in Liege, Belgium decided

– Long term idling of liquid phase at the Florange site in France announced

Recent announcement:

– Intention to permanently close the coke plant and six finishing lines in Liege, Belgium

8

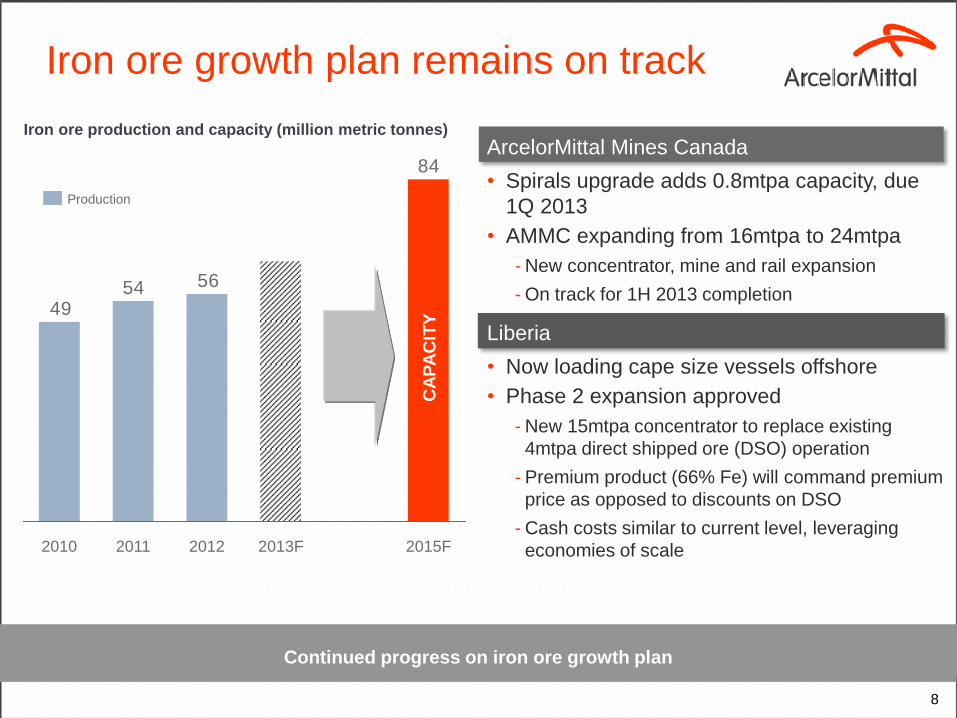

Iron ore growth plan remains on track

Iron ore production and capacity (million metric tonnes)

ArcelorMittal Mines Canada

• Spirals upgrade adds 0.8mtpa capacity, due

1Q 2013

• AMMC expanding from 16mtpa to 24mtpa

- New concentrator, mine and rail expansion

- On track for 1H 2013 completion

Liberia

• Now loading cape size vessels offshore

• Phase 2 expansion approved

- New 15mtpa concentrator to replace existing

4mtpa direct shipped ore (DSO) operation

- Premium product (66% Fe) will command premium

price as opposed to discounts on DSO

- Cash costs similar to current level, leveraging

economies of scale

84

565449

2015F 2010 2013F 2012 2011

Production

CA

PA

CIT

Y

Continued progress on iron ore growth plan

9

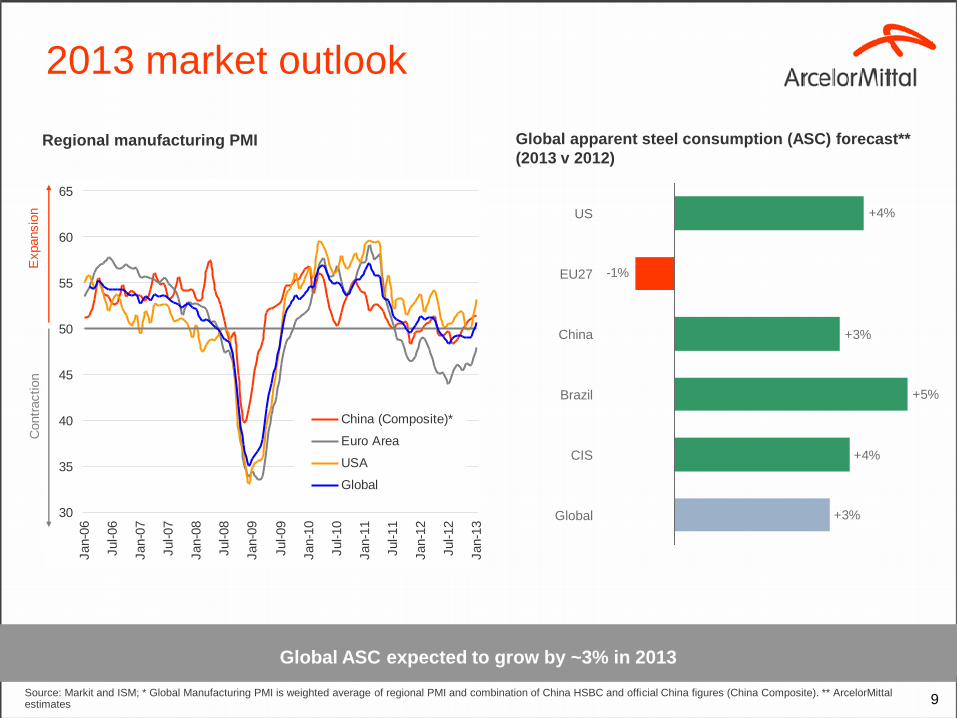

2013 market outlook

Regional manufacturing PMI Global apparent steel consumption (ASC) forecast**

(2013 v 2012)

+4%

+3%

+5%

+3%

-1%

+4%

Global

CIS

Brazil

China

EU27

US

Global ASC expected to grow by ~3% in 2013

Source: Markit and ISM; * Global Manufacturing PMI is weighted average of regional PMI and combination of China HSBC and official China figures (China Composite). ** ArcelorMittal estimates

30

35

40

45

50

55

60

65

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Jan-0

8

Jul-08

Jan-0

9

Jul-09

Jan-1

0

Jul-10

Jan-1

1

Jul-11

Jan-1

2

Jul-12

Jan-1

3

China (Composite)*

Euro Area

USA

Global

Expansio

nC

ontr

action

10

Financial results

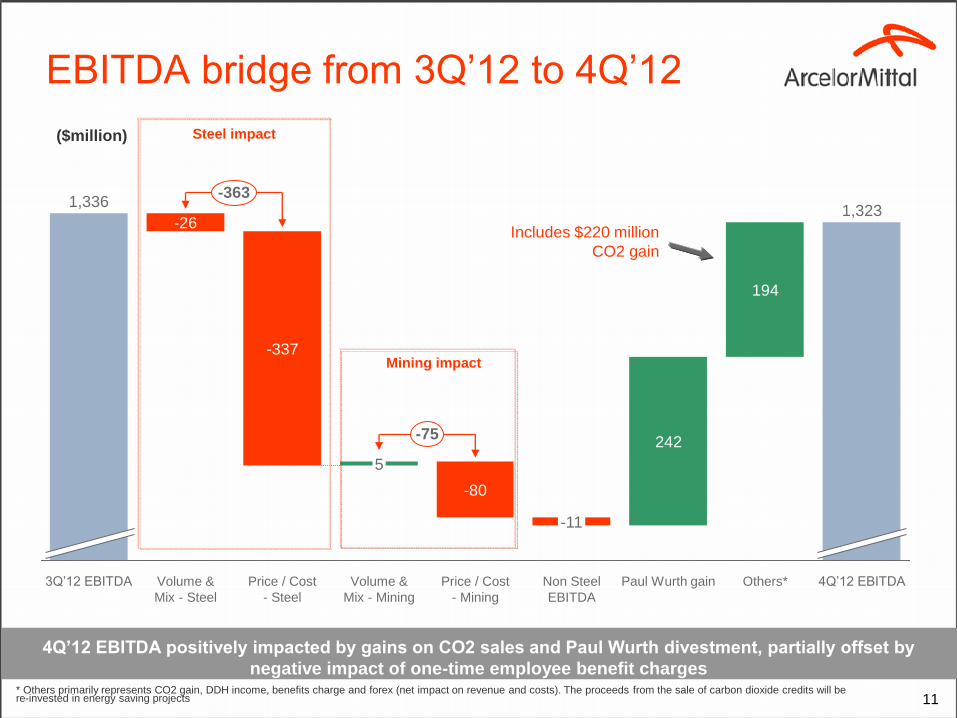

11 * Others primarily represents CO2 gain, DDH income, benefits charge and forex (net impact on revenue and costs). The proceeds from the sale of carbon dioxide credits will be re-invested in energy saving projects

EBITDA bridge from 3Q’12 to 4Q’12

4Q’12 EBITDA positively impacted by gains on CO2 sales and Paul Wurth divestment, partially offset by

negative impact of one-time employee benefit charges

248

753

241

3,413

2,582

61

Q1'11 EBITDA Volume & Mix Selling Price / Cost Non Steel EBITDA* Others** Q2'11 EBITDA

($million)

4Q’12 EBITDA Paul Wurth gain

-75

Others*

-363 1,336

-26

Volume &

Mix - Steel

-80

-11

1,323

242

Price / Cost

- Steel

Price / Cost

- Mining

5

Volume &

Mix - Mining

-337

194

3Q’12 EBITDA Non Steel

EBITDA

Includes $220 million

CO2 gain

Steel impact

Mining impact

3Q 2

012

Depreciation: (1,157)

Impairment: (130)

Restructuring: (98)

Interest: (479)

Forex and other: (103)

Current tax: (101)

Deferred tax: 58

Non-controlling: 20

Weighted Avg No of shares: 1,549

Diluted Weighted Avg No of shares:1,549

EPS = $ (0.46)/share

Diluted EPS = $ (0.46)/share

($ million)

12

EBITDA to net loss 4Q

201

2

Depreciation: (1,236)

Impairment: (4,836)

Restructuring: (192)

Current tax: (94)

Deferred tax: 1,653

Non-controlling: 97

Weighted Avg No of shares: 1,549

Diluted Weighted Avg No of shares: 1,549

EPS = $ (2.58)/share

Diluted EPS = $ (2.58)/share

Net loss of $4.0bn in 4Q’12 primarily due to $5.0 bn charges including $4.3bn goodwill write down

($ million) Interest: (478)

Forex and other: (366)

Finance Cost

1,323

Net income

/ (Ioss)

1,656

Pre-tax

Profit /loss)

-3,987

Taxes and non-

controlling

Interest

-5,643

-844

Income

from Equity

142

Operating

Income/ (loss)

-4,941

Depreciation

impairment and

restructuring

charges

-6,264

EBITDA

-709

-23

-686 -582

-55

1,336

-49

-1,385

13

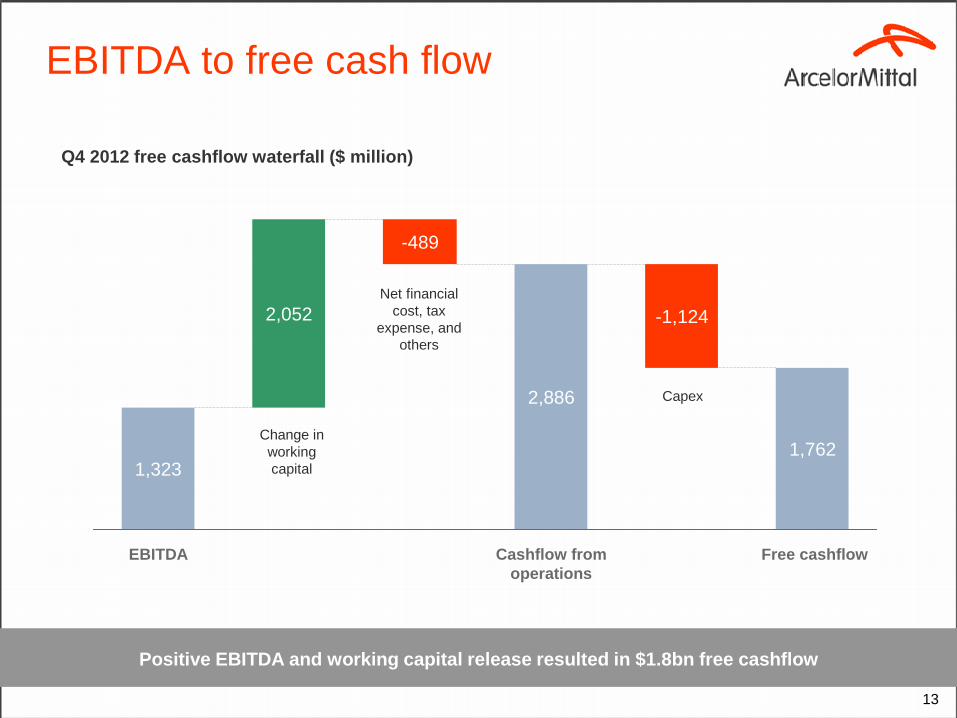

EBITDA to free cash flow

Q4 2012 free cashflow waterfall ($ million)

Positive EBITDA and working capital release resulted in $1.8bn free cashflow

1,762

-1,124

2,886

-489

2,052

1,323

Free cashflow Cashflow from

operations

EBITDA

Change in

working

capital

Net financial

cost, tax

expense, and

others

Capex

14

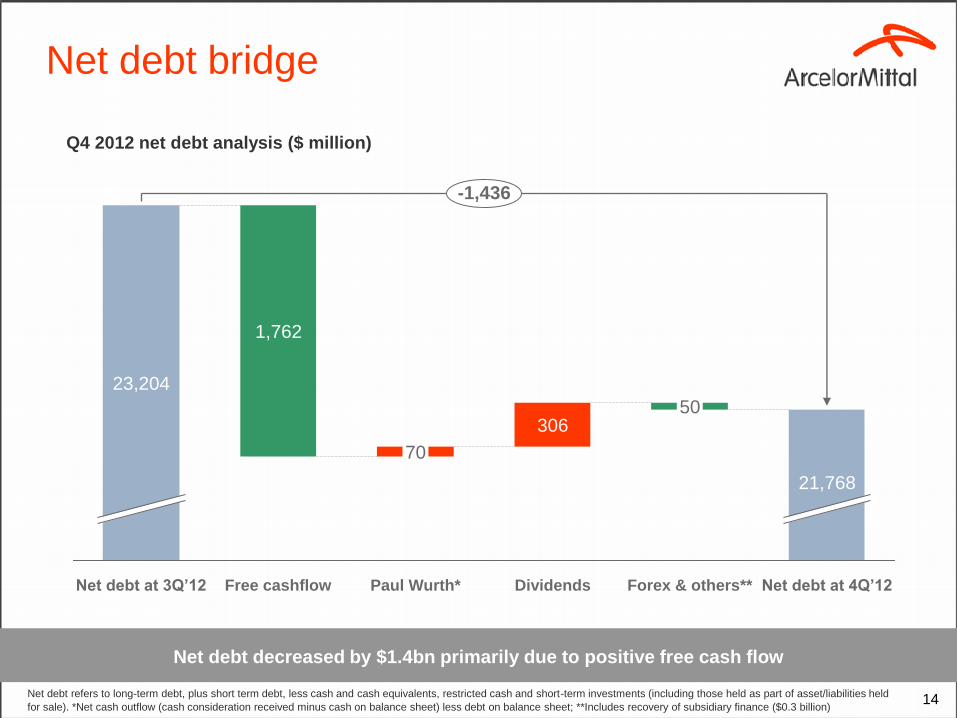

Net debt bridge

Q4 2012 net debt analysis ($ million)

Net debt decreased by $1.4bn primarily due to positive free cash flow

70

Free cashflow

1,762

Net debt at 3Q’12

23,204

306

Paul Wurth*

-1,436

Net debt at 4Q’12

50

21,768

Forex & others** Dividends

Net debt refers to long-term debt, plus short term debt, less cash and cash equivalents, restricted cash and short-term investments (including those held as part of asset/liabilities held

for sale). *Net cash outflow (cash consideration received minus cash on balance sheet) less debt on balance sheet; **Includes recovery of subsidiary finance ($0.3 billion)

15

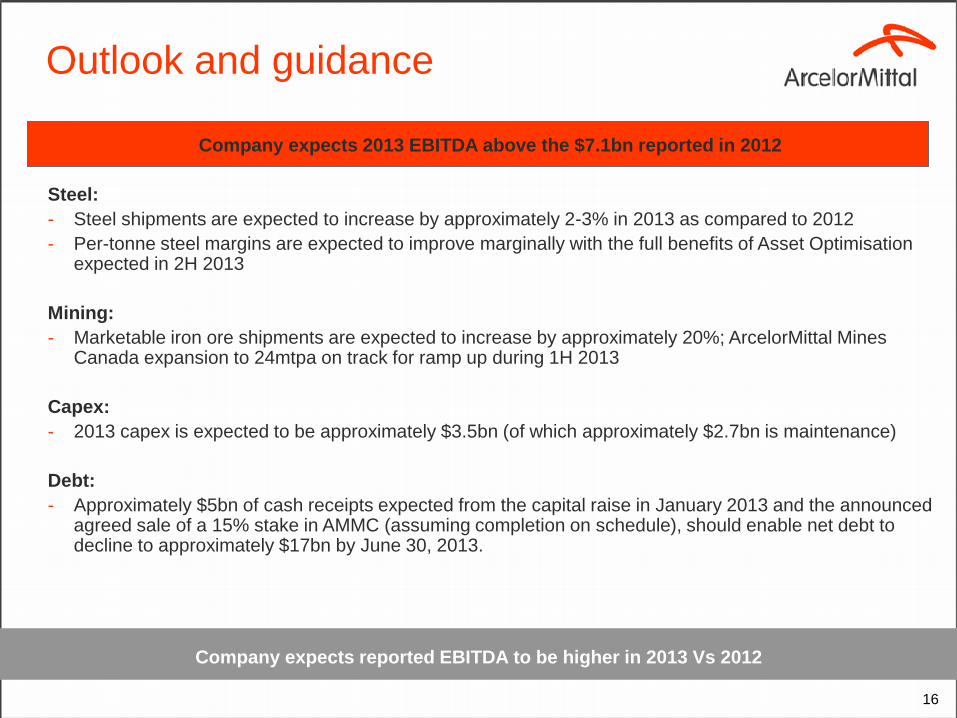

Outlook and guidance

16

Outlook and guidance

Company expects reported EBITDA to be higher in 2013 Vs 2012

Company expects 2013 EBITDA above the $7.1bn reported in 2012

Steel:

- Steel shipments are expected to increase by approximately 2-3% in 2013 as compared to 2012

- Per-tonne steel margins are expected to improve marginally with the full benefits of Asset Optimisation expected in 2H 2013

Mining:

- Marketable iron ore shipments are expected to increase by approximately 20%; ArcelorMittal Mines Canada expansion to 24mtpa on track for ramp up during 1H 2013

Capex:

- 2013 capex is expected to be approximately $3.5bn (of which approximately $2.7bn is maintenance)

Debt:

- Approximately $5bn of cash receipts expected from the capital raise in January 2013 and the announced agreed sale of a 15% stake in AMMC (assuming completion on schedule), should enable net debt to decline to approximately $17bn by June 30, 2013.

Appendix

18

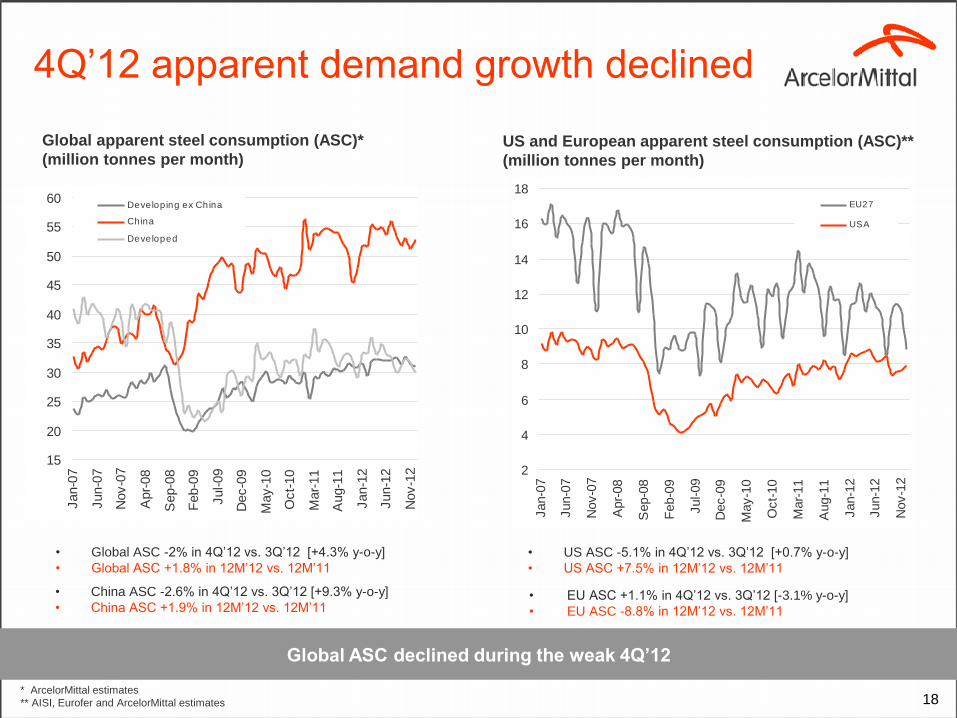

4Q’12 apparent demand growth declined

Global apparent steel consumption (ASC)*

(million tonnes per month) US and European apparent steel consumption (ASC)**

(million tonnes per month)

* ArcelorMittal estimates

** AISI, Eurofer and ArcelorMittal estimates

Global ASC declined during the weak 4Q’12

• China ASC -2.6% in 4Q’12 vs. 3Q’12 [+9.3% y-o-y]

• China ASC +1.9% in 12M’12 vs. 12M’11 • EU ASC +1.1% in 4Q’12 vs. 3Q’12 [-3.1% y-o-y]

• EU ASC -8.8% in 12M’12 vs. 12M’11

• Global ASC -2% in 4Q’12 vs. 3Q’12 [+4.3% y-o-y]

• Global ASC +1.8% in 12M’12 vs. 12M’11

• US ASC -5.1% in 4Q’12 vs. 3Q’12 [+0.7% y-o-y]

• US ASC +7.5% in 12M’12 vs. 12M’11

15

20

25

30

35

40

45

50

55

60

Jan-0

7

Jun-0

7

Nov-0

7

Apr-

08

Sep-0

8

Feb-0

9

Jul-09

Dec-0

9

May-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Jun-1

2

Nov-1

2

Developing ex China

China

Developed

2

4

6

8

10

12

14

16

18

Jan-0

7

Jun-0

7

Nov-0

7

Apr-

08

Sep-0

8

Feb-0

9

Jul-09

Dec-0

9

May-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Jun-1

2

Nov-1

2

EU27

USA

19

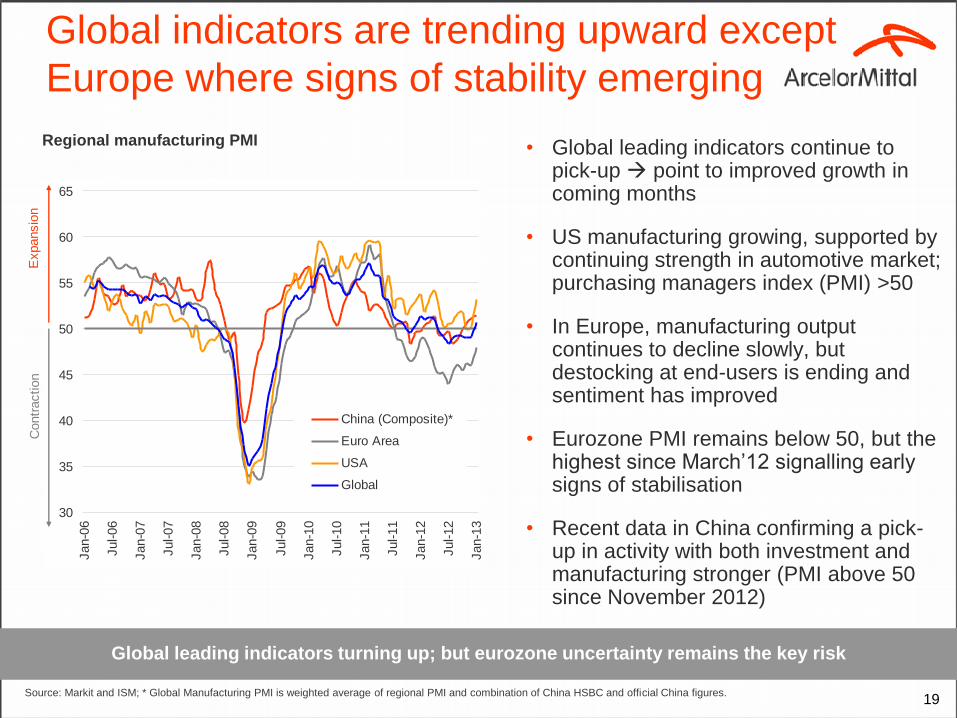

• Global leading indicators continue to pick-up point to improved growth in coming months

• US manufacturing growing, supported by continuing strength in automotive market; purchasing managers index (PMI) >50

• In Europe, manufacturing output continues to decline slowly, but destocking at end-users is ending and sentiment has improved

• Eurozone PMI remains below 50, but the highest since March’12 signalling early signs of stabilisation

• Recent data in China confirming a pick-up in activity with both investment and manufacturing stronger (PMI above 50 since November 2012)

Regional manufacturing PMI

Global leading indicators turning up; but eurozone uncertainty remains the key risk

Global indicators are trending upward except

Europe where signs of stability emerging

Source: Markit and ISM; * Global Manufacturing PMI is weighted average of regional PMI and combination of China HSBC and official China figures.

30

35

40

45

50

55

60

65

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Jan-0

8

Jul-08

Jan-0

9

Jul-09

Jan-1

0

Jul-10

Jan-1

1

Jul-11

Jan-1

2

Jul-12

Jan-1

3

China (Composite)*

Euro Area

USA

Global

Expansio

nC

ontr

action

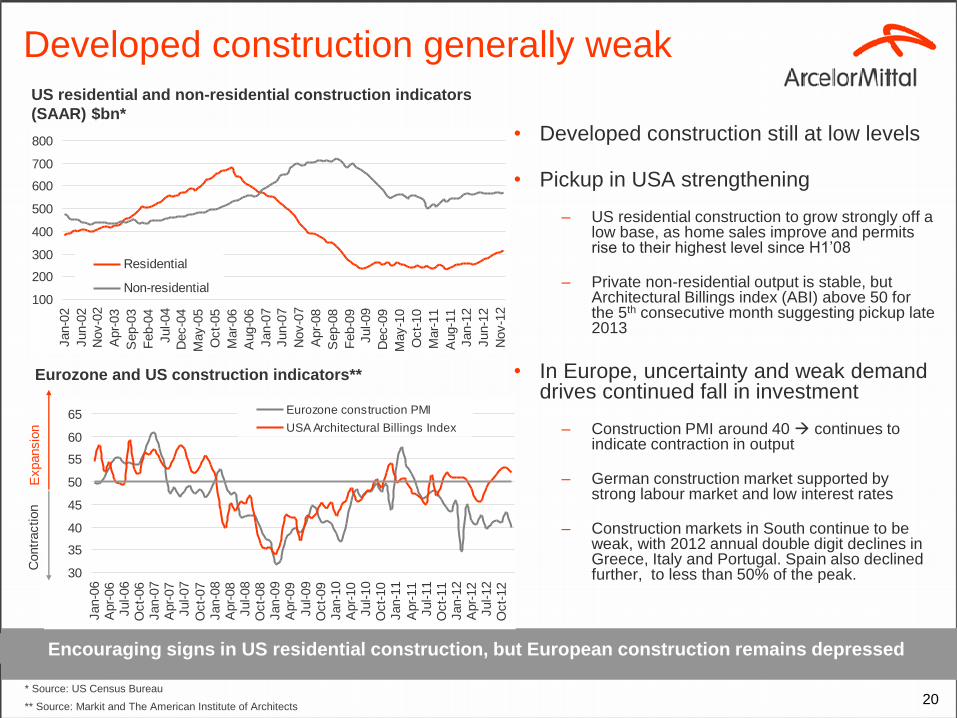

Developed construction generally weak

• Developed construction still at low levels

• Pickup in USA strengthening

– US residential construction to grow strongly off a low base, as home sales improve and permits rise to their highest level since H1’08

– Private non-residential output is stable, but Architectural Billings index (ABI) above 50 for the 5th consecutive month suggesting pickup late 2013

• In Europe, uncertainty and weak demand drives continued fall in investment

– Construction PMI around 40 continues to indicate contraction in output

– German construction market supported by strong labour market and low interest rates

– Construction markets in South continue to be weak, with 2012 annual double digit declines in Greece, Italy and Portugal. Spain also declined further, to less than 50% of the peak.

Eurozone and US construction indicators**

US residential and non-residential construction indicators

(SAAR) $bn*

Encouraging signs in US residential construction, but European construction remains depressed

20 * Source: US Census Bureau

** Source: Markit and The American Institute of Architects

100

200

300

400

500

600

700

800

Jan-0

2

Jun-0

2

Nov-0

2

Apr-

03

Sep-0

3

Feb-0

4

Jul-04

Dec-0

4

May-0

5

Oct-

05

Mar-

06

Aug-0

6

Jan-0

7

Jun-0

7

Nov-0

7

Apr-

08

Sep-0

8

Feb-0

9

Jul-09

Dec-0

9

May-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Jun-1

2

Nov-1

2

Residential

Non-residential

Expansio

nC

ontr

action

30

35

40

45

50

55

60

65

Jan-0

6A

pr-

06

Jul-06

Oct-

06

Jan-0

7A

pr-

07

Jul-07

Oct-

07

Jan-0

8A

pr-

08

Jul-08

Oct-

08

Jan-0

9A

pr-

09

Jul-09

Oct-

09

Jan-1

0A

pr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2A

pr-

12

Jul-12

Oct-

12

Eurozone construction PMI

USA Architectural Billings Index

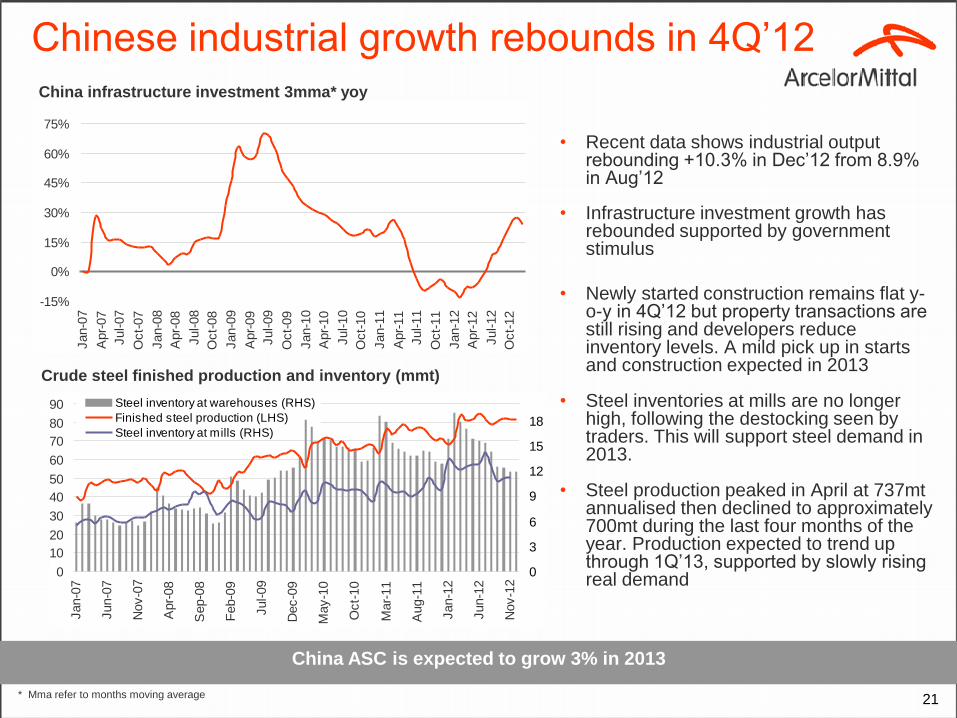

Chinese industrial growth rebounds in 4Q’12

• Recent data shows industrial output rebounding +10.3% in Dec’12 from 8.9% in Aug’12

• Infrastructure investment growth has rebounded supported by government stimulus

• Newly started construction remains flat y-o-y in 4Q’12 but property transactions are still rising and developers reduce inventory levels. A mild pick up in starts and construction expected in 2013

• Steel inventories at mills are no longer high, following the destocking seen by traders. This will support steel demand in 2013.

• Steel production peaked in April at 737mt annualised then declined to approximately 700mt during the last four months of the year. Production expected to trend up through 1Q’13, supported by slowly rising real demand

China ASC is expected to grow 3% in 2013

21

Crude steel finished production and inventory (mmt)

* Mma refer to months moving average

China infrastructure investment 3mma* yoy

0

10

20

30

40

50

60

70

80

90

Jan-0

7

Jun-0

7

Nov-0

7

Apr-

08

Sep-0

8

Feb-0

9

Jul-09

Dec-0

9

May-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Jun-1

2

Nov-1

2

0

3

6

9

12

15

18

Steel inventory at warehouses (RHS)

Finished steel production (LHS)

Steel inventory at mills (RHS)

-15%

0%

15%

30%

45%

60%

75%

Jan-0

7

Apr-

07

Jul-07

Oct-

07

Jan-0

8

Apr-

08

Jul-08

Oct-

08

Jan-0

9

Apr-

09

Jul-09

Oct-

09

Jan-1

0

Apr-

10

Jul-10

Oct-

10

Jan-1

1

Apr-

11

Jul-11

Oct-

11

Jan-1

2

Apr-

12

Jul-12

Oct-

12

1000

1200

1400

1600

1800

2000

2200

2400

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Fe

b-0

9

Ju

l-0

9

De

c-0

9

Ma

y-1

0

Oct-

10

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

1.6

1.8

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6EU (EASSC)

Months Supply

0

2000

4000

6000

8000

10000

12000

14000

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Fe

b-0

9

Ju

l-0

9

De

c-0

9

Ma

y-1

0

Oct-

10

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6USA (MSCI)

Months Supply

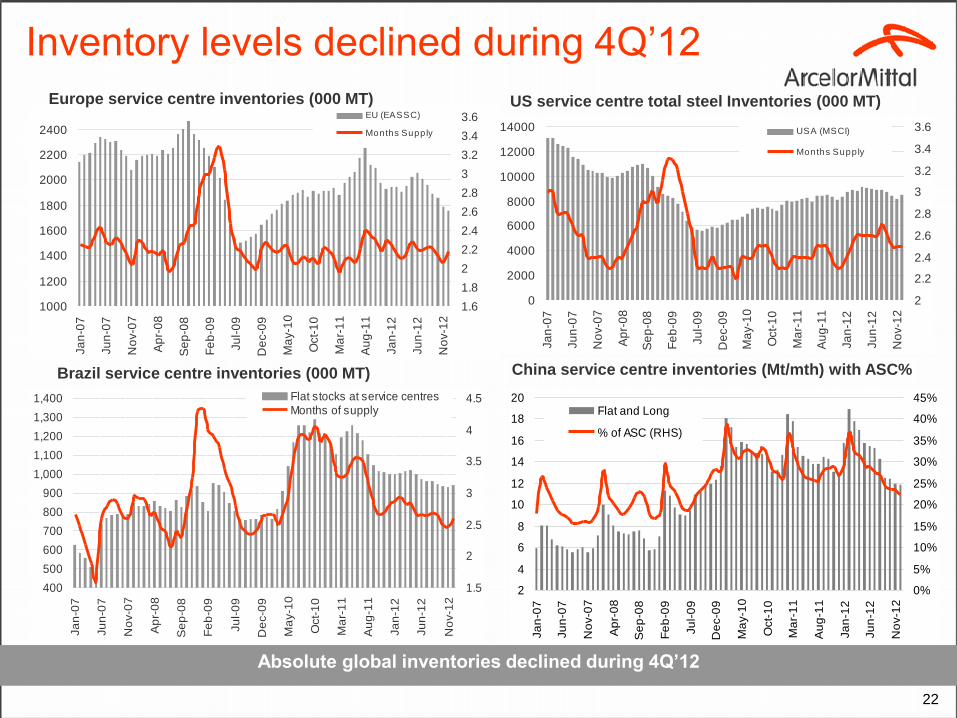

Inventory levels declined during 4Q’12

Europe service centre inventories (000 MT)

Brazil service centre inventories (000 MT)

US service centre total steel Inventories (000 MT)

Absolute global inventories declined during 4Q’12

22

China service centre inventories (Mt/mth) with ASC%

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Fe

b-0

9

Ju

l-0

9

De

c-0

9

Ma

y-1

0

Oct-

10

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

1.5

2

2.5

3

3.5

4

4.5Flat stocks at service centresMonths of supply

2

4

6

8

10

12

14

16

18

20

Ja

n-0

7

Ju

n-0

7

No

v-0

7

Ap

r-0

8

Se

p-0

8

Fe

b-0

9

Ju

l-0

9

De

c-0

9

Ma

y-1

0

Oct-

10

Ma

r-1

1

Au

g-1

1

Ja

n-1

2

Ju

n-1

2

No

v-1

2

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%Flat and Long

% of ASC (RHS)

23

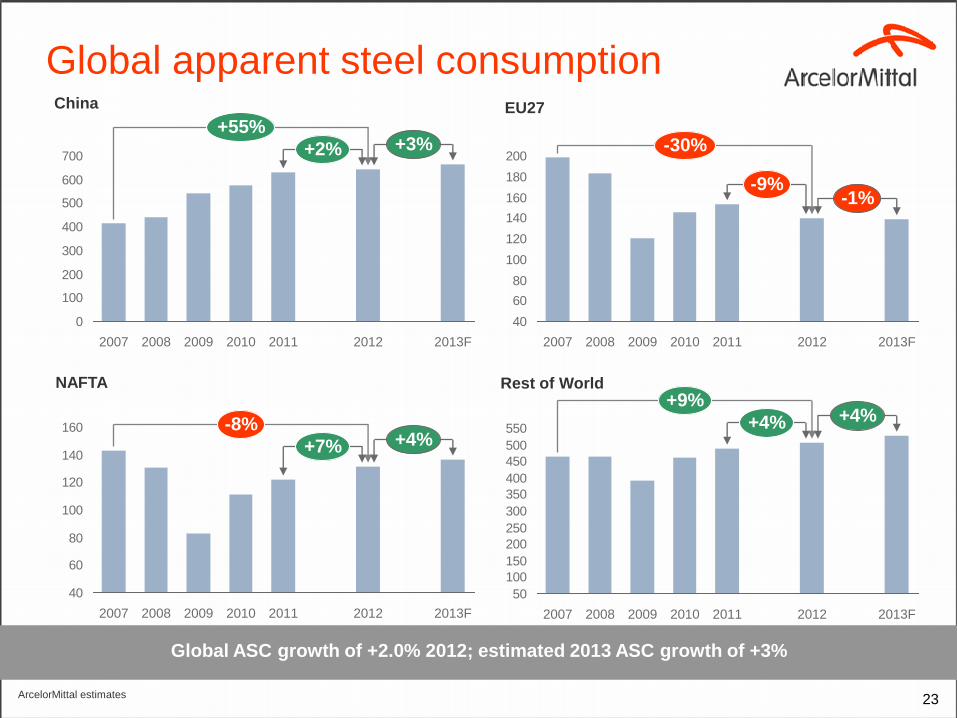

Global apparent steel consumption

Global ASC growth of +2.0% 2012; estimated 2013 ASC growth of +3%

China

NAFTA

EU27

Rest of World

0

100

200

300

400

500

600

700+3%

+55%

2013F 2012 2011 2010 2009 2008 2007

+2%

ArcelorMittal estimates

40

60

80

100

120

140

160

180

200

-9% -1%

-30%

2013F 2012 2011 2010 2009 2008 2007

40

60

80

100

120

140

160+4%

2013F

-8%

+7%

2012 2007 2009 2011 2010 2008

50

100

150

200

250

300

350

400

450

500

550 +4% +4%

2007 2011 2009 2013F 2012 2010

+9%

2008

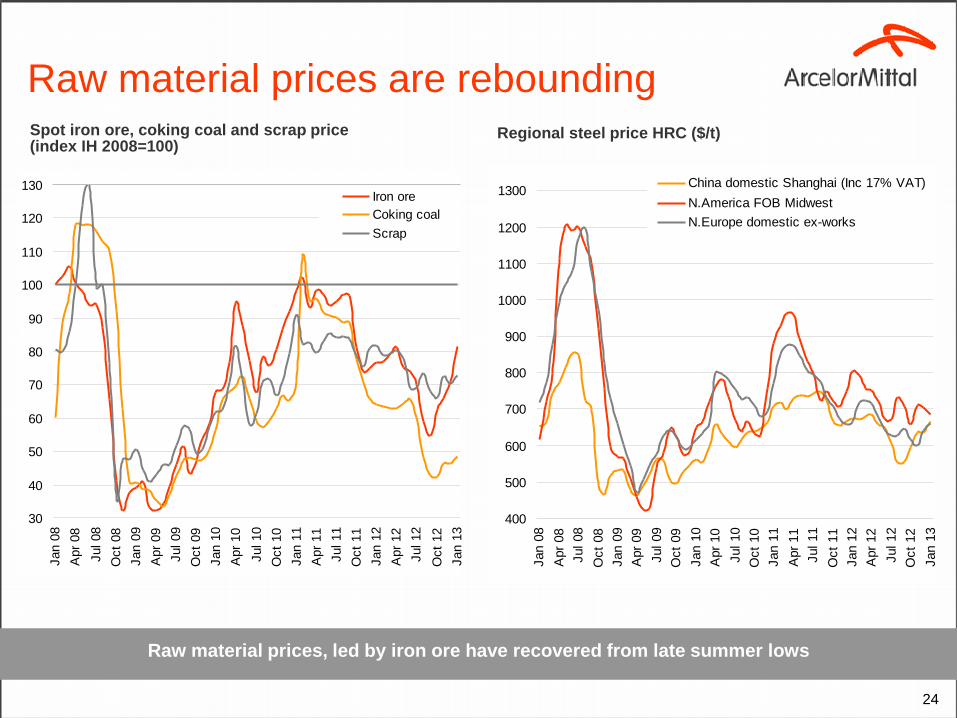

Raw material prices are rebounding Spot iron ore, coking coal and scrap price (index IH 2008=100)

Regional steel price HRC ($/t)

Raw material prices, led by iron ore have recovered from late summer lows

24

400

500

600

700

800

900

1000

1100

1200

1300

Jan 0

8

Apr

08

Jul 08

Oct

08

Jan 0

9

Apr

09

Jul 09

Oct

09

Jan 1

0

Apr

10

Jul 10

Oct

10

Jan 1

1

Apr

11

Jul 11

Oct

11

Jan 1

2

Apr

12

Jul 12

Oct

12

Jan 1

3

China domestic Shanghai (Inc 17% VAT)

N.America FOB Midwest

N.Europe domestic ex-works

30

40

50

60

70

80

90

100

110

120

130

Jan 0

8

Apr

08

Jul 08

Oct

08

Jan 0

9

Apr

09

Jul 09

Oct

09

Jan 1

0

Apr

10

Jul 10

Oct

10

Jan 1

1

Apr

11

Jul 11

Oct

11

Jan 1

2

Apr

12

Jul 12

Oct

12

Jan 1

3

Iron ore

Coking coal

Scrap

25

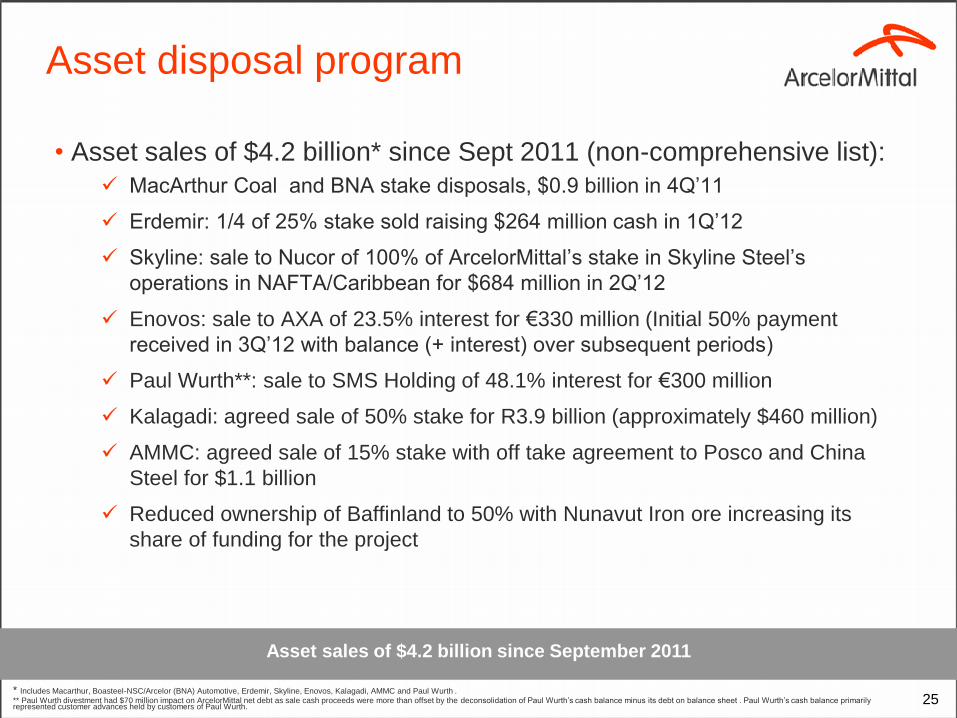

• Asset sales of $4.2 billion* since Sept 2011 (non-comprehensive list):

MacArthur Coal and BNA stake disposals, $0.9 billion in 4Q’11

Erdemir: 1/4 of 25% stake sold raising $264 million cash in 1Q’12

Skyline: sale to Nucor of 100% of ArcelorMittal’s stake in Skyline Steel’s

operations in NAFTA/Caribbean for $684 million in 2Q’12

Enovos: sale to AXA of 23.5% interest for €330 million (Initial 50% payment

received in 3Q’12 with balance (+ interest) over subsequent periods)

Paul Wurth**: sale to SMS Holding of 48.1% interest for €300 million

Kalagadi: agreed sale of 50% stake for R3.9 billion (approximately $460 million)

AMMC: agreed sale of 15% stake with off take agreement to Posco and China

Steel for $1.1 billion

Reduced ownership of Baffinland to 50% with Nunavut Iron ore increasing its

share of funding for the project

Asset sales of $4.2 billion since September 2011

* Includes Macarthur, Boasteel-NSC/Arcelor (BNA) Automotive, Erdemir, Skyline, Enovos, Kalagadi, AMMC and Paul Wurth .

** Paul Wurth divestment had $70 million impact on ArcelorMittal net debt as sale cash proceeds were more than offset by the deconsolidation of Paul Wurth’s cash balance minus its debt on balance sheet . Paul Wurth’s cash balance primarily represented customer advances held by customers of Paul Wurth.

Asset disposal program

Capex and growth plans

• Steel growth capex remains temporarily suspended

• 2013 capex to be lower than 2012 levels

• Focus remains on core growth capex in Mining: – Liberia: Phase 1 complete and running at

4mtpa DSO; commercial ramp-up underway

– Andrade mines (Brazil): Iron ore expansion to 3.5mtpa completed

– Liberia: Phase 2 approved: Expansion from 4mtpa DSO to 15mtpa concentrate by 2015

– AMMC: Expansion from 16mtpa iron ore to 24mtpa by 2013 underway

– AMMC: Further expansion to 30mtpa iron ore under study

26

FY 2012 capex spend of $4.7bn; FY 2013 capex expected at approximately $3.5bn

Upgrade railway line linking mine to port in Liberia

AMMC: Mont-Wright Mining Complex

27

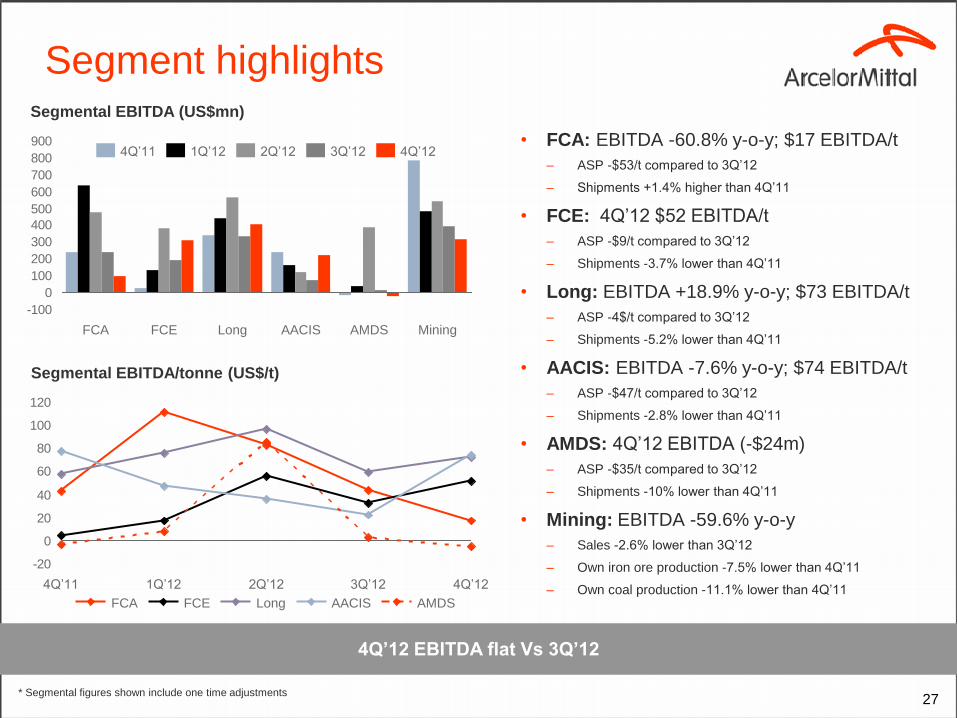

Segment highlights

4Q’12 EBITDA flat Vs 3Q’12

• FCA: EBITDA -60.8% y-o-y; $17 EBITDA/t

– ASP -$53/t compared to 3Q’12

– Shipments +1.4% higher than 4Q’11

• FCE: 4Q’12 $52 EBITDA/t

– ASP -$9/t compared to 3Q’12

– Shipments -3.7% lower than 4Q’11

• Long: EBITDA +18.9% y-o-y; $73 EBITDA/t

– ASP -4$/t compared to 3Q’12

– Shipments -5.2% lower than 4Q’11

• AACIS: EBITDA -7.6% y-o-y; $74 EBITDA/t

– ASP -$47/t compared to 3Q’12

– Shipments -2.8% lower than 4Q’11

• AMDS: 4Q’12 EBITDA (-$24m)

– ASP -$35/t compared to 3Q’12

– Shipments -10% lower than 4Q’11

• Mining: EBITDA -59.6% y-o-y

– Sales -2.6% lower than 3Q’12

– Own iron ore production -7.5% lower than 4Q’11

– Own coal production -11.1% lower than 4Q’11

-100

0

100

200

300

400

500

600

700

800

900

Mining AMDS AACIS Long FCE FCA

4Q’12 3Q’12 2Q’12 1Q’12 4Q’11

Segmental EBITDA (US$mn)

-20

0

20

40

60

80

100

120

4Q’12 3Q’12 2Q’12 1Q’12 4Q’11

AACIS Long FCE AMDS FCA

Segmental EBITDA/tonne (US$/t)

* Segmental figures shown include one time adjustments

28

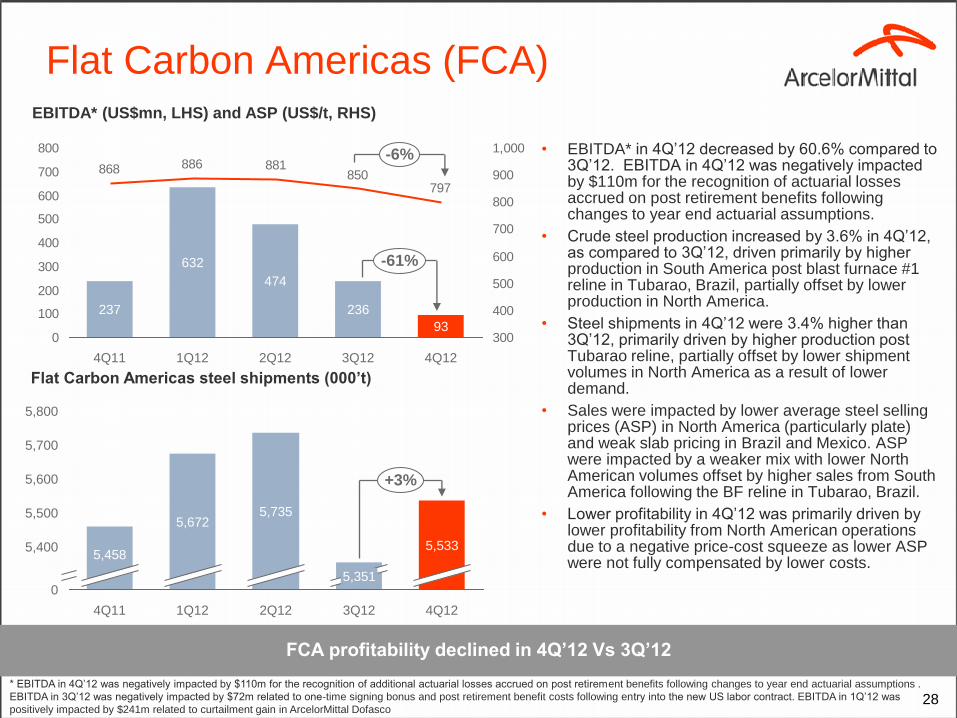

Flat Carbon Americas (FCA)

• EBITDA* in 4Q’12 decreased by 60.6% compared to 3Q’12. EBITDA in 4Q’12 was negatively impacted by $110m for the recognition of actuarial losses accrued on post retirement benefits following changes to year end actuarial assumptions.

• Crude steel production increased by 3.6% in 4Q’12, as compared to 3Q’12, driven primarily by higher production in South America post blast furnace #1 reline in Tubarao, Brazil, partially offset by lower production in North America.

• Steel shipments in 4Q’12 were 3.4% higher than 3Q’12, primarily driven by higher production post Tubarao reline, partially offset by lower shipment volumes in North America as a result of lower demand.

• Sales were impacted by lower average steel selling prices (ASP) in North America (particularly plate) and weak slab pricing in Brazil and Mexico. ASP were impacted by a weaker mix with lower North American volumes offset by higher sales from South America following the BF reline in Tubarao, Brazil.

• Lower profitability in 4Q’12 was primarily driven by lower profitability from North American operations due to a negative price-cost squeeze as lower ASP were not fully compensated by lower costs.

FCA profitability declined in 4Q’12 Vs 3Q’12

797850

881886868

0

100

200

300

400

500

600

700

800

300

400

500

600

700

800

900

1,000-6%

-61%

4Q12

93

3Q12

236

2Q12

474

1Q12

632

4Q11

237

5,800

5,700

5,600

5,500

5,400

0

4Q12

5,533

3Q12

5,735

4Q11 2Q12

5,672

+3%

5,351

5,458

1Q12

EBITDA* (US$mn, LHS) and ASP (US$/t, RHS)

Flat Carbon Americas steel shipments (000’t)

* EBITDA in 4Q’12 was negatively impacted by $110m for the recognition of additional actuarial losses accrued on post retirement benefits following changes to year end actuarial assumptions .

EBITDA in 3Q’12 was negatively impacted by $72m related to one-time signing bonus and post retirement benefit costs following entry into the new US labor contract. EBITDA in 1Q’12 was

positively impacted by $241m related to curtailment gain in ArcelorMittal Dofasco

29

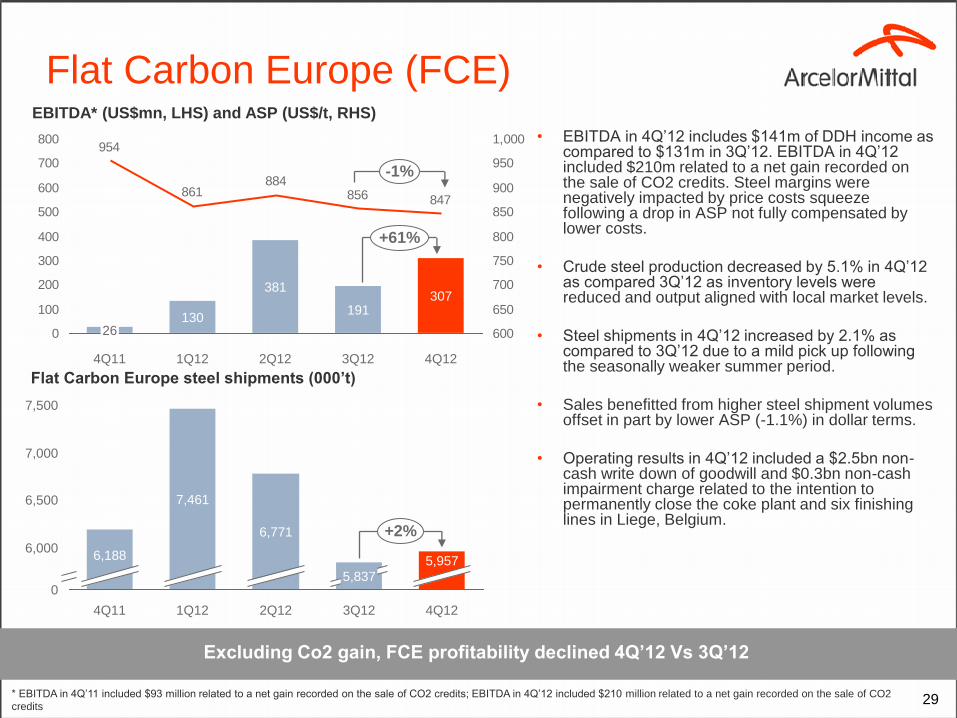

Flat Carbon Europe (FCE)

• EBITDA in 4Q’12 includes $141m of DDH income as compared to $131m in 3Q’12. EBITDA in 4Q’12 included $210m related to a net gain recorded on the sale of CO2 credits. Steel margins were negatively impacted by price costs squeeze following a drop in ASP not fully compensated by lower costs.

• Crude steel production decreased by 5.1% in 4Q’12 as compared 3Q’12 as inventory levels were reduced and output aligned with local market levels.

• Steel shipments in 4Q’12 increased by 2.1% as compared to 3Q’12 due to a mild pick up following the seasonally weaker summer period.

• Sales benefitted from higher steel shipment volumes offset in part by lower ASP (-1.1%) in dollar terms.

• Operating results in 4Q’12 included a $2.5bn non-cash write down of goodwill and $0.3bn non-cash impairment charge related to the intention to permanently close the coke plant and six finishing lines in Liege, Belgium.

Excluding Co2 gain, FCE profitability declined 4Q’12 Vs 3Q’12

847856884

861

954

0

100

200

300

400

500

600

700

800

600

650

700

750

800

850

900

950

1,000

-1%

+61%

4Q12

307

3Q12

191

2Q12

381

1Q12

130

4Q11

26

7,500

7,000

6,500

6,000

0

4Q11

7,461

5,837

6,771

1Q12

6,188

2Q12

+2%

4Q12

5,957

3Q12

EBITDA* (US$mn, LHS) and ASP (US$/t, RHS)

Flat Carbon Europe steel shipments (000’t)

* EBITDA in 4Q’11 included $93 million related to a net gain recorded on the sale of CO2 credits; EBITDA in 4Q’12 included $210 million related to a net gain recorded on the sale of CO2

credits

30

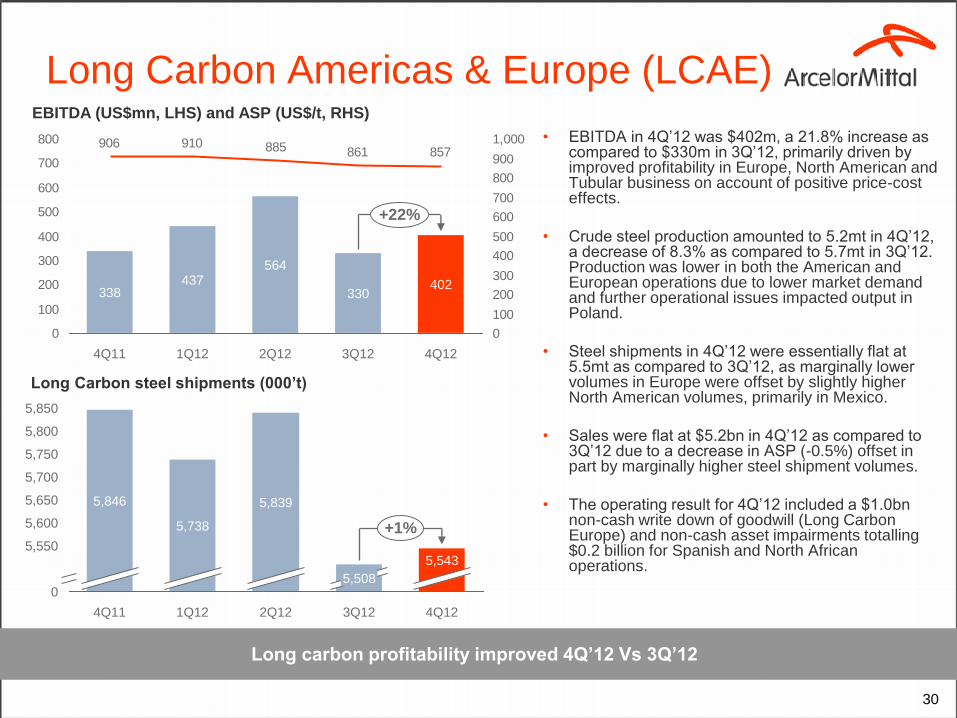

Long Carbon Americas & Europe (LCAE)

• EBITDA in 4Q’12 was $402m, a 21.8% increase as compared to $330m in 3Q’12, primarily driven by improved profitability in Europe, North American and Tubular business on account of positive price-cost effects.

• Crude steel production amounted to 5.2mt in 4Q’12, a decrease of 8.3% as compared to 5.7mt in 3Q’12. Production was lower in both the American and European operations due to lower market demand and further operational issues impacted output in Poland.

• Steel shipments in 4Q’12 were essentially flat at 5.5mt as compared to 3Q’12, as marginally lower volumes in Europe were offset by slightly higher North American volumes, primarily in Mexico.

• Sales were flat at $5.2bn in 4Q’12 as compared to 3Q’12 due to a decrease in ASP (-0.5%) offset in part by marginally higher steel shipment volumes.

• The operating result for 4Q’12 included a $1.0bn non-cash write down of goodwill (Long Carbon Europe) and non-cash asset impairments totalling $0.2 billion for Spanish and North African operations.

Long carbon profitability improved 4Q’12 Vs 3Q’12

0

5,600

5,650

5,700

5,750

5,850

5,800

5,550

+1%

4Q12

5,543

2Q12

5,846

4Q11

5,738

1Q12

5,839

5,508

3Q12

EBITDA (US$mn, LHS) and ASP (US$/t, RHS)

Long Carbon steel shipments (000’t)

857861885910906

0

100

200

300

400

500

600

700

800

0

100

200

300

400

500

600

700

800

900

1,000

437

4Q11

338

+22%

4Q12

402

3Q12

330

2Q12

564

1Q12

31

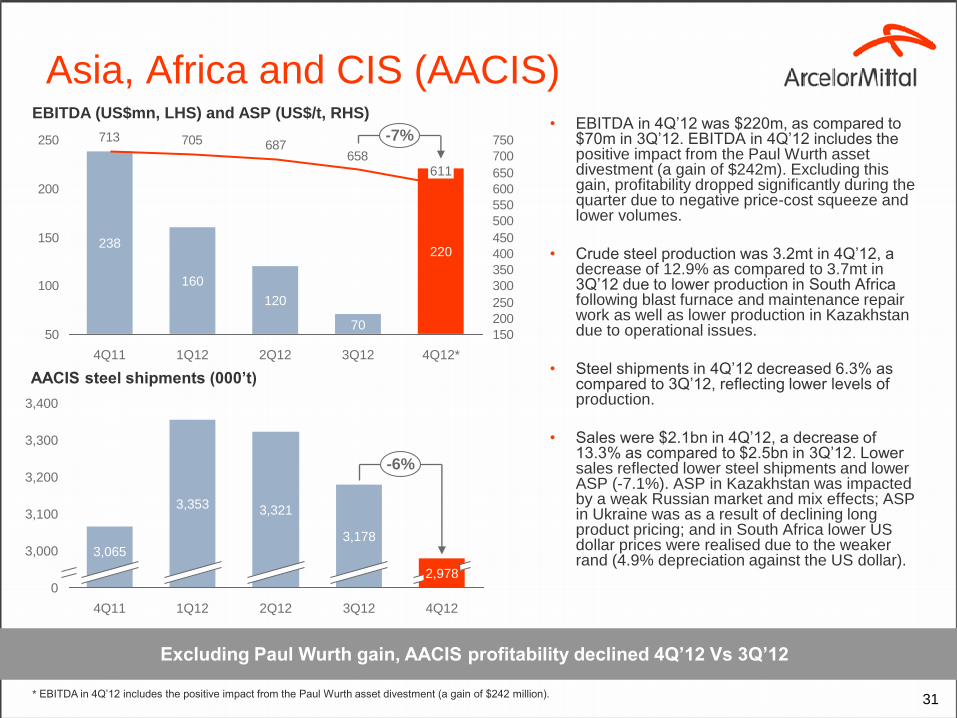

Asia, Africa and CIS (AACIS) • EBITDA in 4Q’12 was $220m, as compared to

$70m in 3Q’12. EBITDA in 4Q’12 includes the positive impact from the Paul Wurth asset divestment (a gain of $242m). Excluding this gain, profitability dropped significantly during the quarter due to negative price-cost squeeze and lower volumes.

• Crude steel production was 3.2mt in 4Q’12, a decrease of 12.9% as compared to 3.7mt in 3Q’12 due to lower production in South Africa following blast furnace and maintenance repair work as well as lower production in Kazakhstan due to operational issues.

• Steel shipments in 4Q’12 decreased 6.3% as compared to 3Q’12, reflecting lower levels of production.

• Sales were $2.1bn in 4Q’12, a decrease of 13.3% as compared to $2.5bn in 3Q’12. Lower sales reflected lower steel shipments and lower ASP (-7.1%). ASP in Kazakhstan was impacted by a weak Russian market and mix effects; ASP in Ukraine was as a result of declining long product pricing; and in South Africa lower US dollar prices were realised due to the weaker rand (4.9% depreciation against the US dollar).

Excluding Paul Wurth gain, AACIS profitability declined 4Q’12 Vs 3Q’12

3,400

3,100

3,300

3,200

0

3,000

-6%

4Q12

2,978

3Q12

3,178

2Q12 1Q12

3,353

4Q11

3,065

3,321

EBITDA (US$mn, LHS) and ASP (US$/t, RHS)

AACIS steel shipments (000’t)

658687705713

50

100

150

200

250

150

200

250

300

350

400

450

500

550

600

650

700

750-7%

4Q12*

220

3Q12 2Q12

238

70

120

160

1Q12 4Q11

611

* EBITDA in 4Q’12 includes the positive impact from the Paul Wurth asset divestment (a gain of $242 million).

32

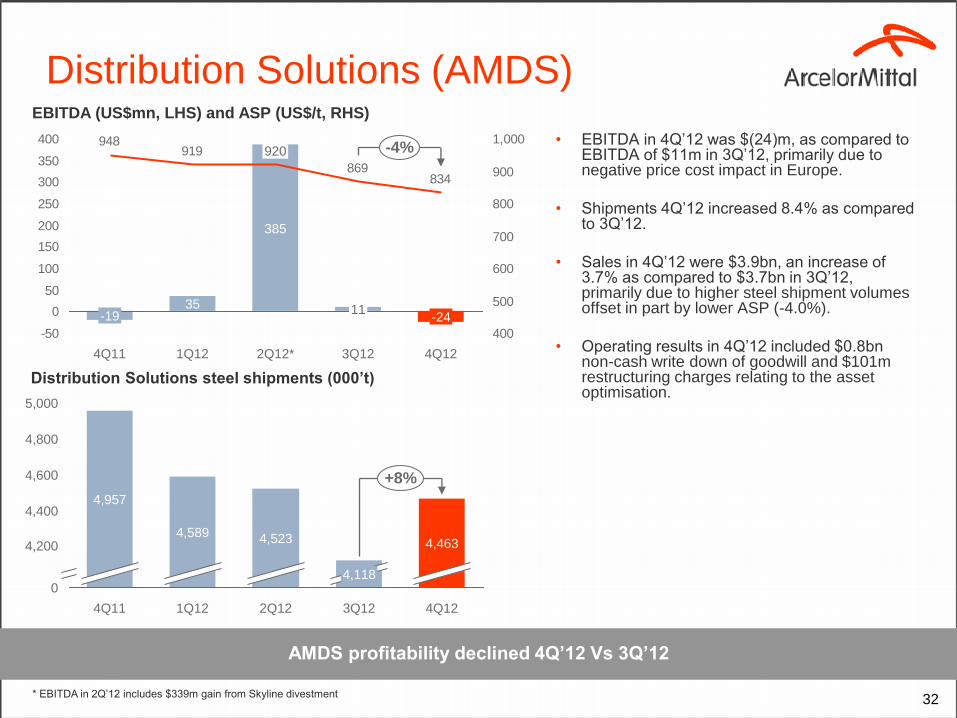

Distribution Solutions (AMDS)

• EBITDA in 4Q’12 was $(24)m, as compared to EBITDA of $11m in 3Q’12, primarily due to negative price cost impact in Europe.

• Shipments 4Q’12 increased 8.4% as compared to 3Q’12.

• Sales in 4Q’12 were $3.9bn, an increase of 3.7% as compared to $3.7bn in 3Q’12, primarily due to higher steel shipment volumes offset in part by lower ASP (-4.0%).

• Operating results in 4Q’12 included $0.8bn non-cash write down of goodwill and $101m restructuring charges relating to the asset optimisation.

AMDS profitability declined 4Q’12 Vs 3Q’12

4,800

4,600

4,400

4,200

5,000

0

+8%

4Q12

4,463

3Q12

4,118

2Q12

4,523

1Q12

4,589

4Q11

4,957

EBITDA (US$mn, LHS) and ASP (US$/t, RHS)

Distribution Solutions steel shipments (000’t)

834869

919948

-50

0

50

100

150

200

250

300

350

400

400

500

600

700

800

900

1,000-4%

4Q12

-24

3Q12

11

2Q12*

920

385

1Q12

35

4Q11

-19

* EBITDA in 2Q’12 includes $339m gain from Skyline divestment

33

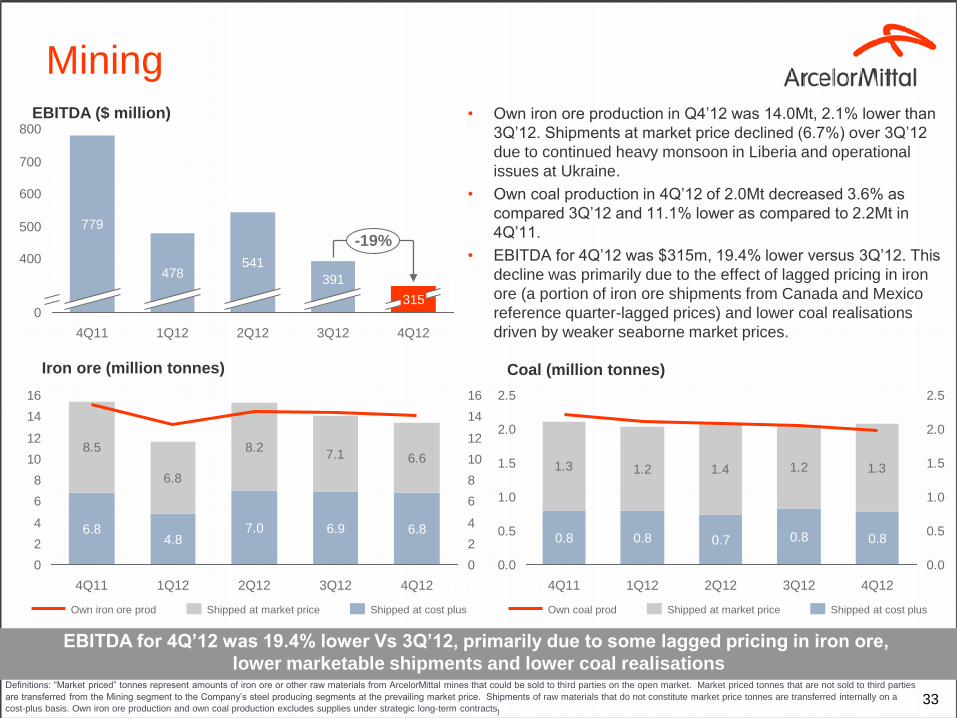

Mining • Own iron ore production in Q4’12 was 14.0Mt, 2.1% lower than

3Q’12. Shipments at market price declined (6.7%) over 3Q’12

due to continued heavy monsoon in Liberia and operational

issues at Ukraine.

• Own coal production in 4Q’12 of 2.0Mt decreased 3.6% as

compared 3Q’12 and 11.1% lower as compared to 2.2Mt in

4Q’11.

• EBITDA for 4Q’12 was $315m, 19.4% lower versus 3Q’12. This

decline was primarily due to the effect of lagged pricing in iron

ore (a portion of iron ore shipments from Canada and Mexico

reference quarter-lagged prices) and lower coal realisations

driven by weaker seaborne market prices.

EBITDA for 4Q’12 was 19.4% lower Vs 3Q’12, primarily due to some lagged pricing in iron ore,

lower marketable shipments and lower coal realisations Definitions: “Market priced” tonnes represent amounts of iron ore or other raw materials from ArcelorMittal mines that could be sold to third parties on the open market. Market priced tonnes that are not sold to third parties

are transferred from the Mining segment to the Company’s steel producing segments at the prevailing market price. Shipments of raw materials that do not constitute market price tonnes are transferred internally on a

cost-plus basis. Own iron ore production and own coal production excludes supplies under strategic long-term contracts)

600

500

0

400

800

700

1Q12

478

4Q11

-19%

4Q12

315

3Q12

391

2Q12

541

779

EBITDA ($ million)

8.5

6.8

8.27.1 6.6

0

2

4

6

8

10

12

14

16

0

2

4

6

8

10

12

14

16

4Q12

6.8

3Q12

6.9

2Q12

7.0

1Q12

4.8

4Q11

6.8

Shipped at cost plus Shipped at market price Own iron ore prod

Iron ore (million tonnes)

1.3 1.2 1.4 1.2 1.3

0.0

0.5

1.0

1.5

2.0

2.5

0.0

0.5

1.0

1.5

2.0

2.5

4Q12

0.8

3Q12

0.8

2Q12

0.7

1Q12

0.8

4Q11

0.8

Own coal prod Shipped at cost plus Shipped at market price

Coal (million tonnes)

34

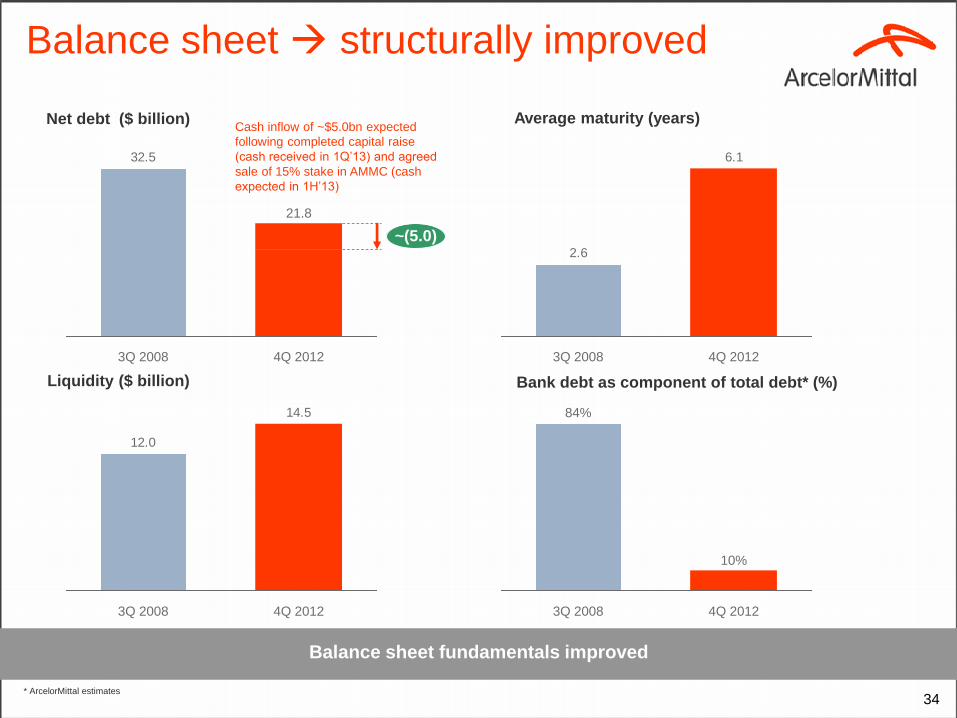

Net debt ($ billion)

Balance sheet fundamentals improved

Average maturity (years)

Liquidity ($ billion) Bank debt as component of total debt* (%)

Balance sheet structurally improved

32.5

21.8

~(5.0)

4Q 2012 3Q 2008

6.1

2.6

4Q 2012 3Q 2008

14.5

12.0

4Q 2012 3Q 2008

* ArcelorMittal estimates

4Q 2012

10%

3Q 2008

84%

Cash inflow of ~$5.0bn expected

following completed capital raise

(cash received in 1Q’13) and agreed

sale of 15% stake in AMMC (cash

expected in 1H’13)

35

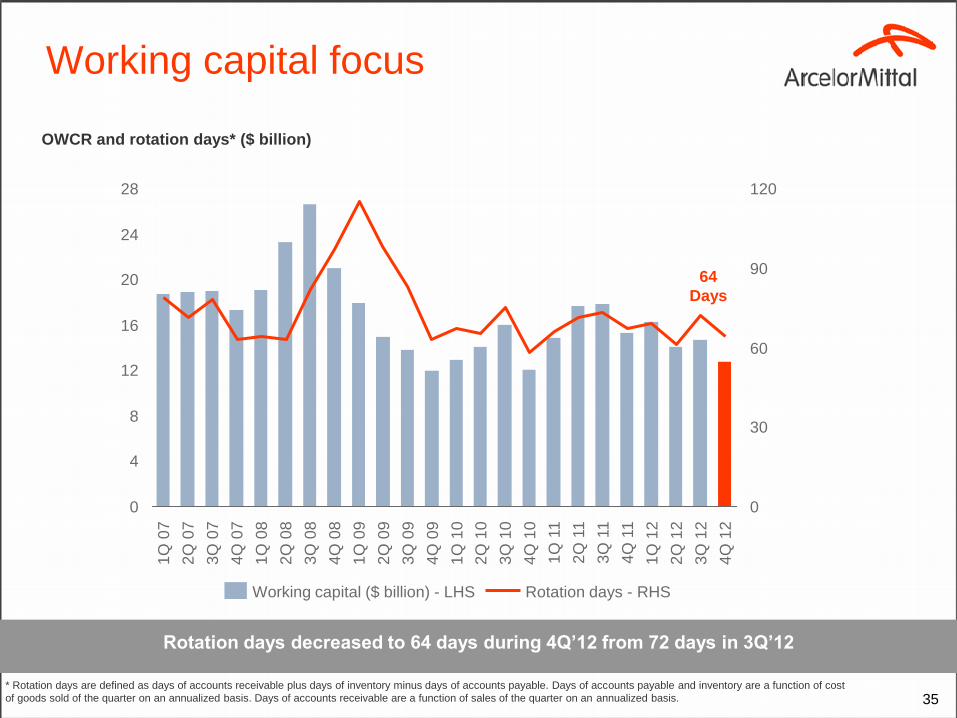

Working capital focus

OWCR and rotation days* ($ billion)

* Rotation days are defined as days of accounts receivable plus days of inventory minus days of accounts payable. Days of accounts payable and inventory are a function of cost

of goods sold of the quarter on an annualized basis. Days of accounts receivable are a function of sales of the quarter on an annualized basis.

Rotation days decreased to 64 days during 4Q’12 from 72 days in 3Q’12

0

4

8

12

16

20

24

28

0

30

60

90

120

3Q

08

2Q

08

1Q

08

4Q

08

2Q

10

4Q

10

1Q

11

3Q

10

1Q

10

4Q

07

4Q

09

2Q

09

3Q

09

1Q

09

3Q

11

2Q

11

2Q

12

3Q

12

1Q

12

4Q

11

4Q

12

3Q

07

2Q

07

1Q

07

Working capital ($ billion) - LHS Rotation days - RHS

64

Days

36

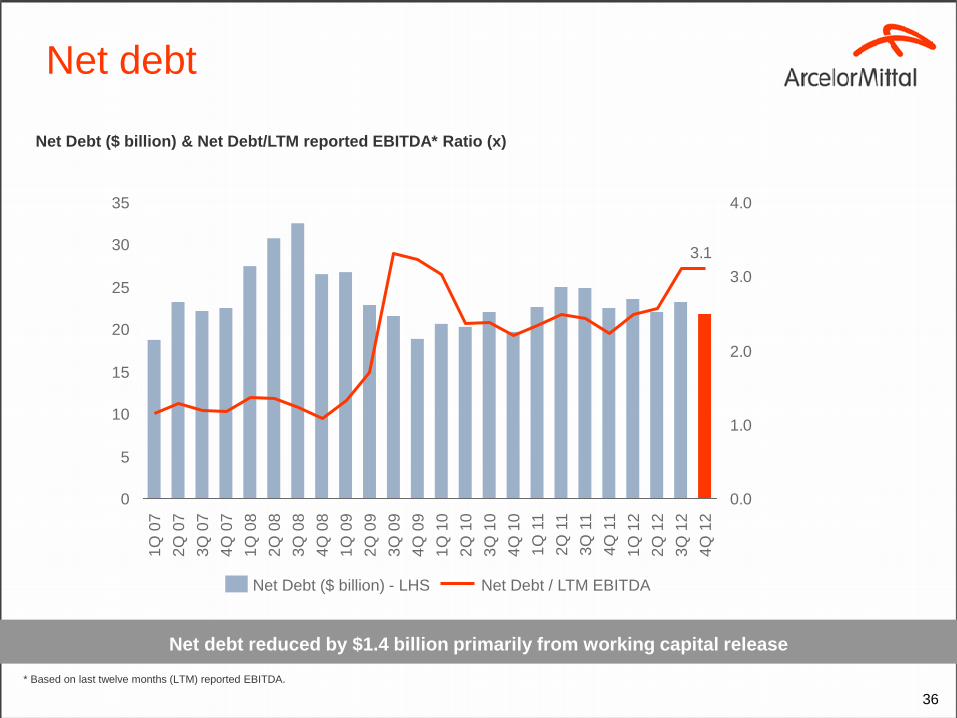

Net debt

Net Debt ($ billion) & Net Debt/LTM reported EBITDA* Ratio (x)

* Based on last twelve months (LTM) reported EBITDA.

Net debt reduced by $1.4 billion primarily from working capital release

3.1

0

5

10

15

20

25

30

35

0.0

1.0

2.0

3.0

4.0

1Q

12

4Q

11

3Q

11

2Q

11

1Q

11

4Q

10

3Q

10

2Q

10

1Q

10

4Q

09

3Q

09

2Q

09

1Q

09

4Q

08

3Q

08

2Q

08

1Q

08

4Q

07

3Q

07

3Q

12

2Q

12

2Q

07

1Q

07

4Q

12

Net Debt ($ billion) - LHS Net Debt / LTM EBITDA

37

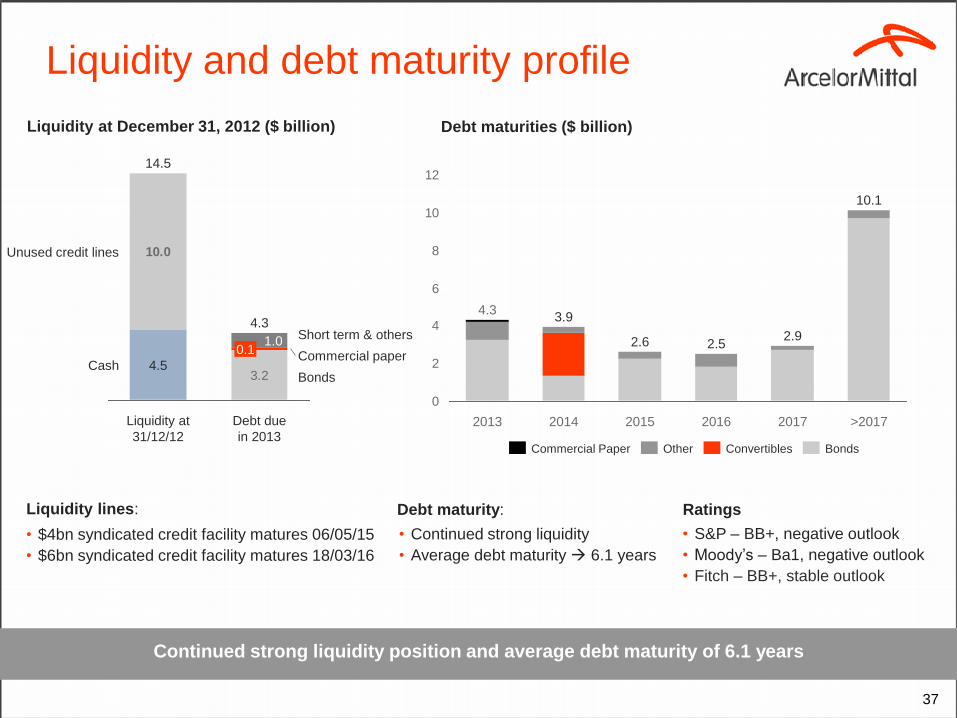

Liquidity and debt maturity profile

Debt maturities ($ billion) Liquidity at December 31, 2012 ($ billion)

Continued strong liquidity position and average debt maturity of 6.1 years

Liquidity lines:

• $4bn syndicated credit facility matures 06/05/15

• $6bn syndicated credit facility matures 18/03/16

• Continued strong liquidity

• Average debt maturity 6.1 years

Debt maturity: Ratings

• S&P – BB+, negative outlook

• Moody’s – Ba1, negative outlook

• Fitch – BB+, stable outlook

0

2

4

6

8

10

12

>2017

10.1

2017

2.9

2016

2.5

2015

2.6

2014

3.9

2013

4.3

Bonds Convertibles Other Commercial Paper

3.2

10.0

Bonds

Commercial paper

Short term & others

Cash

Unused credit lines

Debt due

in 2013

4.3

0.1 1.0

Liquidity at

31/12/12

14.5

4.5

38

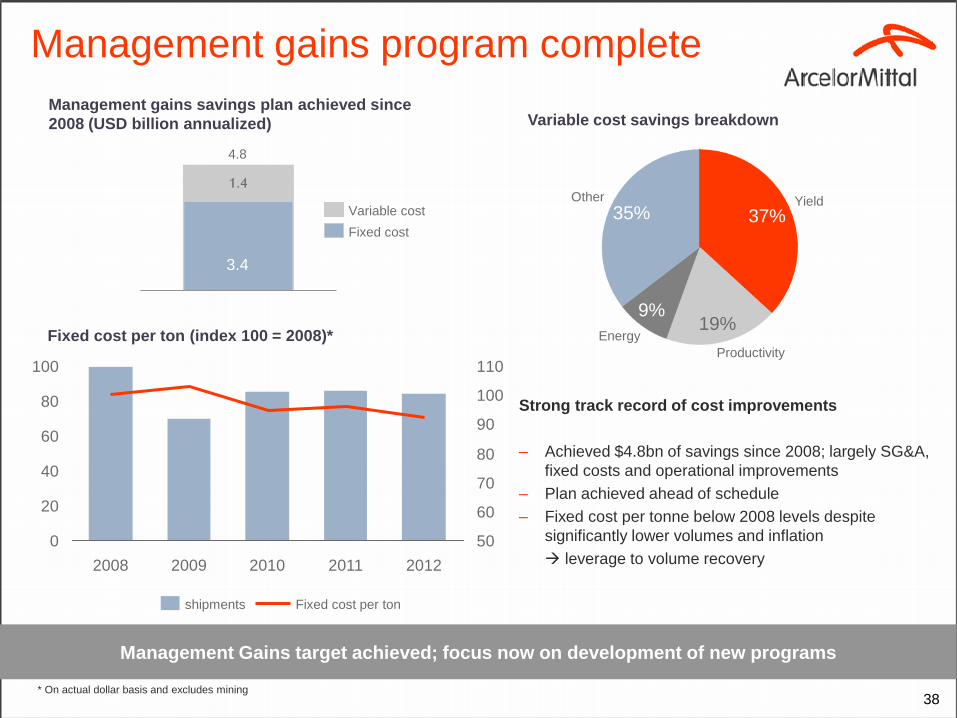

Management gains program complete

Strong track record of cost improvements

– Achieved $4.8bn of savings since 2008; largely SG&A,

fixed costs and operational improvements

– Plan achieved ahead of schedule

– Fixed cost per tonne below 2008 levels despite

significantly lower volumes and inflation

leverage to volume recovery

Management gains savings plan achieved since

2008 (USD billion annualized)

Management Gains target achieved; focus now on development of new programs

4.8

3.4

Fixed cost

Variable cost Other

35%

Energy

9%

Productivity

19%

Yield

37%

Variable cost savings breakdown

Fixed cost per ton (index 100 = 2008)*

0

20

40

60

80

100

50

60

70

80

90

100

110

2012 2011 2010 2009 2008

Fixed cost per ton shipments

* On actual dollar basis and excludes mining

39

Contacts

Daniel Fairclough – Global Head Investor Relations

+44 207 543 1105

Hetal Patel – UK/European Investor Relations

+44 207 543 1128

Valérie Mella – European and Retail Investor Relations

+44 207 543 1156

Maureen Baker – Fixed Income/Debt Investor Relations

+33 1 71 92 10 26

Thomas A McCue – US Investor Relations

+312-899-3927

Lisa Fortuna – US Investor Relations

+312-899-3985

![Quadrilateral Family[1] Rashmi Kathuria](https://static.fdocuments.us/doc/165x107/554cab70b4c905aa608b4606/quadrilateral-family1-rashmi-kathuria.jpg)