Preparing for Global Change in the Petroleum Supply Chain 2006 Presentations/Vance Scott... ·...

74

Houston, Texas June 7, 2006 Preparing for Global Change in the Petroleum Supply Chain Preparing for Global Change in the Preparing for Global Change in the Petroleum Supply Chain Petroleum Supply Chain University of Nevada/COPPEAD Petroleum Executive Logistics Course

Transcript of Preparing for Global Change in the Petroleum Supply Chain 2006 Presentations/Vance Scott... ·...

Houston, Texas

June 7, 2006

Preparing for Global Change in the Petroleum Supply Chain

Preparing for Global Change in the Preparing for Global Change in the Petroleum Supply ChainPetroleum Supply Chain

University of Nevada/COPPEAD Petroleum Executive Logistics Course

A.T. Kearney 82/06.2006/13154 2

AgendaAgenda

About A.T. Kearney

Basics and fundamentals — Petroleum supply chains are complex and global

A look to the future

Keys to value

A.T. Kearney 82/06.2006/13154 3

About A.T. KearneyAbout A.T. Kearney

A.T. Kearney 82/06.2006/13154 4

A.T. Kearney is one of the world’s leading management consulting firmsA.T. Kearney is one of the world’s leading management consulting firms

Aerospace and

Defence Automotive

Communicationsand

High TechnologyFinancial

Institutions

Pharmaceuticaland

HealthcareEnergy Transportation

and Utilities

Consumer Goods

and Retail

Operations• Supply Chain• Next Generation

Manufacturing• Operating Asset

Effectiveness

Strategy and Organization

Technology Solutions

ServicePractices

Our global service and industry practices enable tailored solutions to specific issues

IndustryPractices

A.T. Kearney 82/06.2006/13154 5

We use deep energy expertise to accelerate and expand results for our clientsWe use deep energy expertise to accelerate and expand results for our clients

Selected Oil & Gas Clients Energy Practice• Over 300 professionals specializing in Oil, Gas,

and Chemicals

• Global practice: the group is managed as a fully integrated practice with no geographic or sub-practice boundaries so as to provide the best mix of people for any given engagement

• Serves the world's leading clients in all markets

• Capabilities include:– Strategy– Operations Strategy– Technology Strategy and Implementation– eBusiness Strategy– Merger Integration– Benchmarking– Restructuring– Process and Organisation Redesign– Procurement Effectiveness– Next Generation Cost Reduction– Sourcing– Supply Chain– Network rationalization– Commercial Optimization/Logistics Cost

Reduction– Contractor Optimization– Net Working Capital Reduction– Capital Projects Management

A.T. Kearney 82/06.2006/13154 6

Basics and fundamentals —Petroleum supply chains are complex and global

Basics and fundamentals —Petroleum supply chains are complex and global

A.T. Kearney 82/06.2006/13154 7

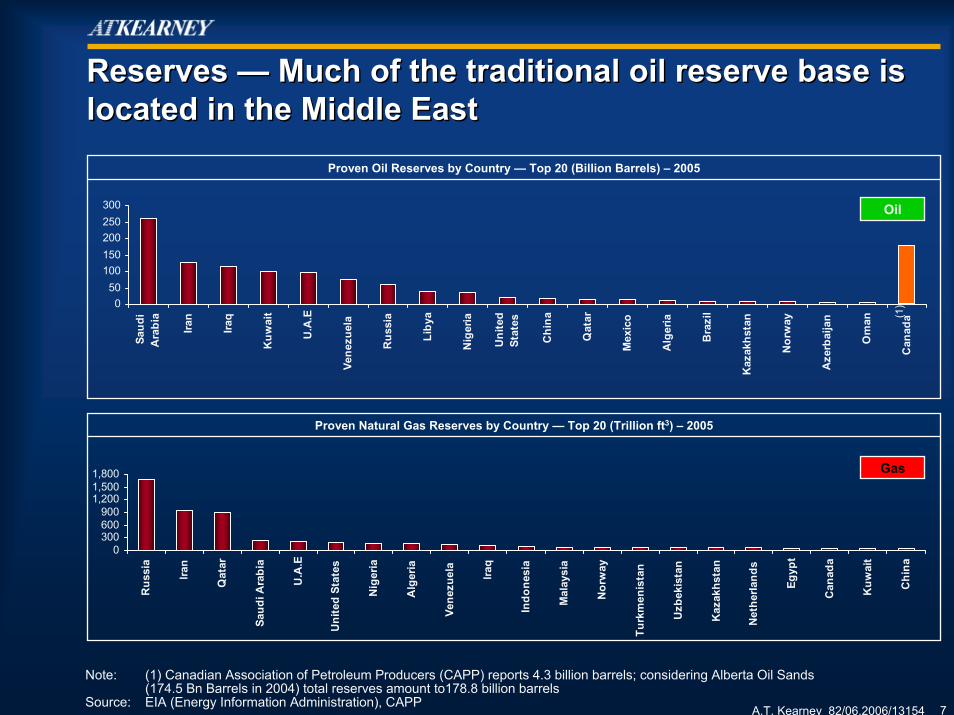

Proven Natural Gas Reserves by Country — Top 20 (Trillion ft3) – 2005

Proven Oil Reserves by Country — Top 20 (Billion Barrels) – 2005

050

100150200250300

Saud

iA

rabi

a

Iran

Iraq

Kuw

ait

U.A

.E

Vene

zuel

a

Rus

sia

Liby

a

Nig

eria

Uni

ted

Stat

es

Chi

na

Qat

ar

Mex

ico

Alg

eria

Bra

zil

Kaz

akhs

tan

Nor

way

Aze

rbai

jan

Om

an

Can

ada

Reserves — Much of the traditional oil reserve base is located in the Middle EastReserves — Much of the traditional oil reserve base is located in the Middle East

0300600900

1,2001,5001,800

Rus

sia

Iran

Qat

ar

Saud

i Ara

bia

U.A

.E

Uni

ted

Stat

es

Nig

eria

Alg

eria

Vene

zuel

a

Iraq

Indo

nesi

a

Mal

aysi

a

Nor

way

Turk

men

ista

n

Uzb

ekis

tan

Kaz

akhs

tan

Net

herla

nds

Egyp

t

Can

ada

Kuw

ait

Chi

na(1

)

Gas

Oil

Note: (1) Canadian Association of Petroleum Producers (CAPP) reports 4.3 billion barrels; considering Alberta Oil Sands(174.5 Bn Barrels in 2004) total reserves amount to178.8 billion barrels

Source: EIA (Energy Information Administration), CAPP

A.T. Kearney 82/06.2006/13154 8

Key Producing RegionsWorld Production

299

245

97

301

128

Asia Pacific

Europe & Eurasia

Americas

Africa

Middle East

US$ 1.07 trillion

Supply — The global crude oil production totals to US$ 1.07 trillionSupply — The global crude oil production totals to US$ 1.07 trillion

Crude Oil Production in 2004(1)

Europe & Eurasia

Oil

SaudiArabia43%

Iran17%

Others11%

Middle EastOthers

4%

Americas

US35%

Mexico18%Venezuela

15%

Canada14%

Brazil7%

Argentina4%

UnitedArabianEmirates

11%

Kuwait10%

Iraq8%

RussianFederation

43%Norway

18%

UnitedKingdom

12%

Others10%

Kazakhstan7%

Note: (1) Based on production volume times regional spot crude oil prices Source: BP Statistical review of world energy 2005

A.T. Kearney 82/06.2006/13154 9

130 129

110

5850 47 45 45 43

35 33 30 28 27 25 23 2218

14 14 12 11 11 10 10 10

Key Producing Countries(1)

(US$ Billion)

Kuw

ait

Vene

zuel

a

Mex

ico

Kaz

akhs

tan

Can

ada

Liby

a

Bra

zil

Alg

eria

Ang

ola

Indi

a

Uni

ted

Kin

gdom

Chi

na

Rus

sian

Fede

ratio

n

Supply — Saudi Arabia, Russian Federation and USA dominate crude oil productionSupply — Saudi Arabia, Russian Federation and USA dominate crude oil production

Regional Crude Oil Production Breakdown

80% of Global Market

50% of Global Market

Saud

iA

rabi

a

Mal

aysi

a

Egyp

t

Arg

entin

a

USA Ira

n

Nor

way

Uni

ted

Ara

bian

Emira

tes

Nig

eria

Om

an

Qat

ar

Indo

nesi

a

Iraq

Note: (1) Covering 90% of Entire Natural Gas Production in 2004Source: BP Statistical review of world energy 2005/A.T. Kearney analysis

Oil

Middle EastAsia PacificAmericasAfricaEurope

A.T. Kearney 82/06.2006/13154 10

Key Consuming RegionsWorld Consumption

445

280

288

6537

Asia Pacific

Europe & Eurasia

Americas

AfricaMiddle East

Demand — The global crude oil consumption totals to US$ 1.11 trillionDemand — The global crude oil consumption totals to US$ 1.11 trillion

Crude Oil Production in 2004(1)

Asia Pacific

Others10%

US$ 1.11 trillion Americas

US70%

Mexico6%

Canada8%

Brazil6%

Europe & Eurasia

Others46%

Germany13%

RussianFederation

13%

France10%

Italy9%

UnitedKingdom

9%

China29%

Japan23%

Other23%

India23%

SouthKorea10%

Indonesia5%

Australia4%

Note: (1) Based on production volume times regional spot crude oil pricesSource: BP Statistical review of world energy 2005/A.T. Kearney analysis

Oil

A.T. Kearney 82/06.2006/13154 11

311

8265

37 36 33 31 29 28 28 28 26 25 22 21 20 18 18 17 14 14 11 11 11 11

Key Producing Countries(1)

(US$ Billion)

Sout

h K

orea

Ger

man

y

Can

ada

Bra

zil

Spai

n

Indi

a

Chi

na

Rus

sian

Fede

ratio

n

Demand — The USA, China, Japan are the three dominant petroleum consumersDemand — The USA, China, Japan are the three dominant petroleum consumers

Regional Crude Oil Production Breakdown

Note: (1) Covering 85% of Entire Oil Production in 2004Source: BP Statistical review of world energy 2005/A.T. Kearney analysis

80% of Global Market

50% of Global Market

Thai

land

Taiw

an

Net

herla

nds

USA Ira

n

Bel

gium

&Lu

xem

bour

g

Aus

tral

ia

Indo

nesi

a

Saud

i Ara

bia

Japa

n

Mex

ico

Fran

ce

Italy

Uni

ted

Kin

gdom

`Oth

er S

. &C

ent.

Am

eric

a

Oth

er A

fric

a

Oth

er M

iddl

eEa

st

Oil

Middle EastAsia PacificAmericasAfricaEurope

A.T. Kearney 82/06.2006/13154 12

Asia PacificProduction vs. Consumption

Middle EastProduction vs. Consumption

Europe & Eurasia Production vs. Consumption

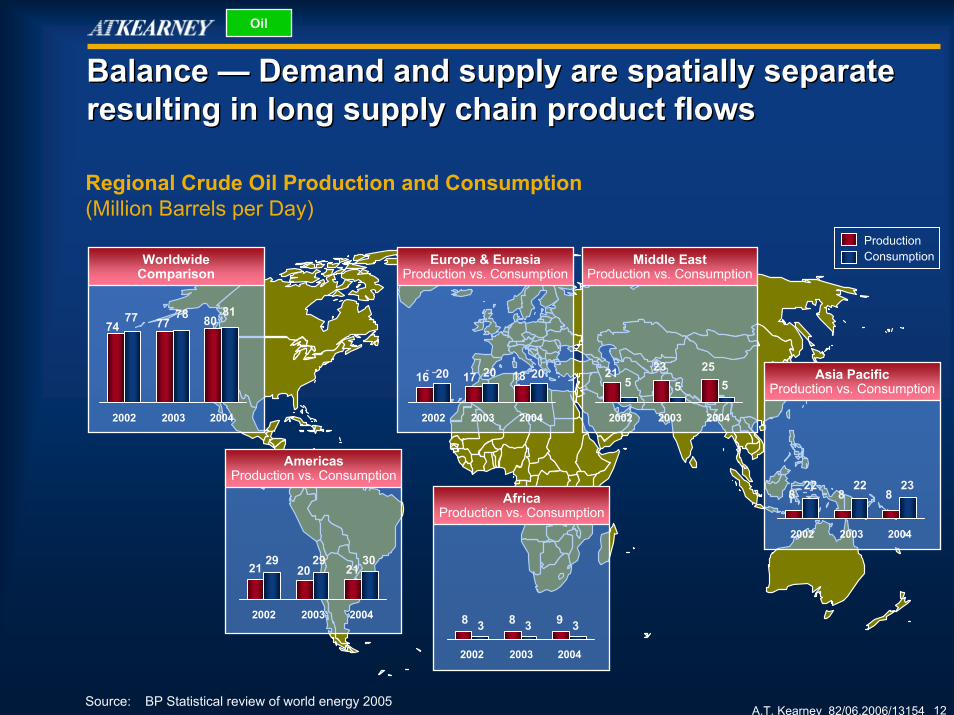

Balance — Demand and supply are spatially separate resulting in long supply chain product flowsBalance — Demand and supply are spatially separate resulting in long supply chain product flows

2002 2003 2004

Regional Crude Oil Production and Consumption(Million Barrels per Day)

16 20 17 20 18 20

WorldwideComparison

2002 2003 2004

7477 77

78 8081

2002 2003 2004

215

235

255

AmericasProduction vs. Consumption

21 2920

2921

30

AfricaProduction vs. Consumption

8 3

822

2002 2003 2004

822

823

2002 2003 2004

8 3 9 32002 2003 2004

Source: BP Statistical review of world energy 2005

ProductionConsumption

Oil

A.T. Kearney 82/06.2006/13154 13

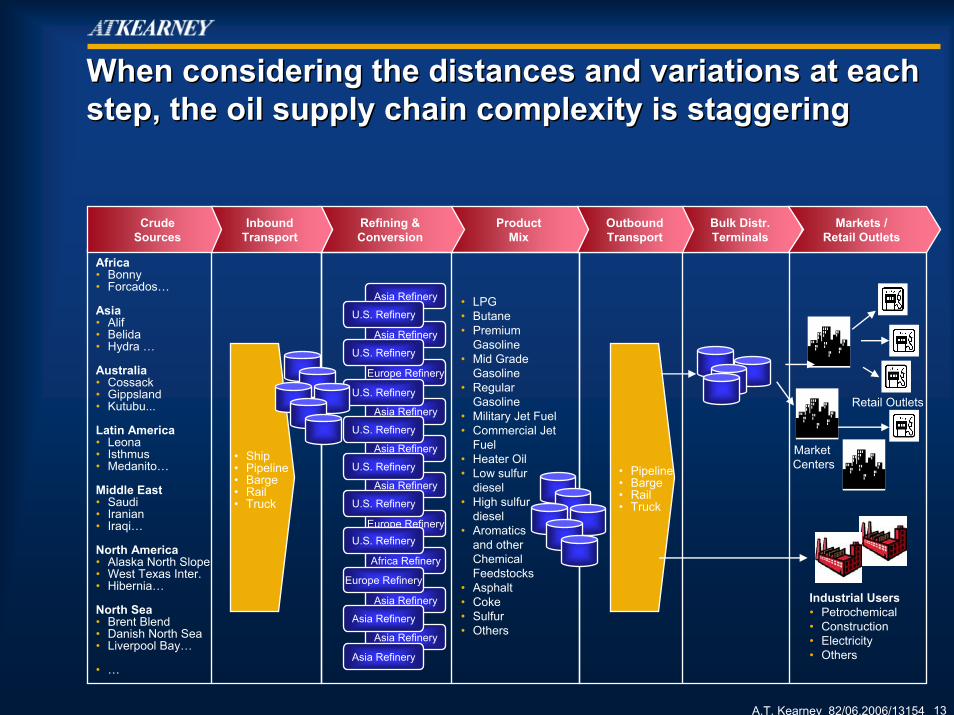

When considering the distances and variations at each step, the oil supply chain complexity is staggeringWhen considering the distances and variations at each step, the oil supply chain complexity is staggering

Africa• Bonny• Forcados…

Asia• Alif• Belida• Hydra …

Australia• Cossack• Gippsland• Kutubu...

Latin America• Leona• Isthmus• Medanito…

Middle East• Saudi• Iranian• Iraqi…

North America• Alaska North Slope• West Texas Inter.• Hibernia…

North Sea• Brent Blend• Danish North Sea• Liverpool Bay…

• …

Refining & Conversion

Product Mix

OutboundTransport

Bulk Distr.Terminals

Markets /Retail Outlets

Crude Sources

InboundTransport

• LPG• Butane• Premium

Gasoline• Mid Grade

Gasoline• Regular

Gasoline• Military Jet Fuel• Commercial Jet

Fuel• Heater Oil• Low sulfur

diesel• High sulfur

diesel• Aromatics

and other Chemical Feedstocks

• Asphalt• Coke• Sulfur• Others

• Ship• Pipeline• Barge• Rail• Truck

• Pipeline• Barge• Rail• Truck

Market Centers

Industrial Users• Petrochemical• Construction• Electricity• Others

Retail Outlets

Asia Refinery

Asia Refinery

Europe Refinery

Asia Refinery

Asia Refinery

Asia Refinery

Europe Refinery

Africa Refinery

Asia Refinery

Asia Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

Europe Refinery

Asia Refinery

Asia Refinery

A.T. Kearney 82/06.2006/13154 14

Key Producing RegionsWorld Production

1,052

892

323

279

145

Asia Pacific

Europe & Eurasia

Americas

Africa

Middle East

Supply — The Natural gas production totals to 2.69 trillion cubic metersSupply — The Natural gas production totals to 2.69 trillion cubic meters

Natural Gas Production in 2004

RussianFederation

56%Norway8%

United Kingdom

9%

Uzbekistan5%

Others15% Mexico

4%

Venezuela3%

Canada21%

Others6%

Argentina5%

2.69 Trillion Cubic Meters

Netherlands7%

Indonesia23%

Malaysia17%

China13%

Australia11%

Others27%

India9%

Gas

Source: BP Statistical review of world energy 2005

Europe & Eurasia Americas

Asia Pacific

US61%

A.T. Kearney 82/06.2006/13154 15

589

543

183

96 86 82 79 73 69 64 56 55 54 46 45 41 39 37 35 29 28 28 27 23 21

Saud

iA

rabi

a

USA

Trin

idad

& T

obag

o

Aus

tral

ia

Nor

way

Net

herla

nds

Iran

Vene

zuel

a

Can

ada

Uni

ted

Kin

gdom

Nig

eria

Uni

ted

Ara

bian

Emira

tes

Turk

men

ista

n

Alg

eria

Indo

nesi

a

Arg

entin

a

Qat

ar

Mal

aysi

a

Paki

stan

Indi

a

Uzb

ekis

tan

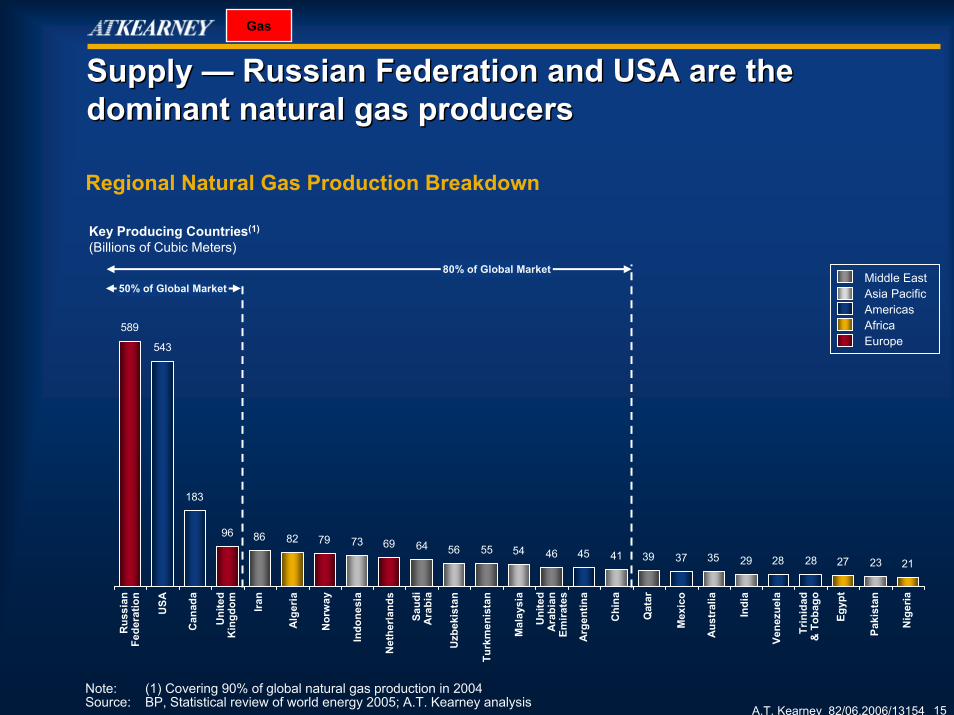

Supply — Russian Federation and USA are the dominant natural gas producersSupply — Russian Federation and USA are the dominant natural gas producers

Regional Natural Gas Production Breakdown

80% of Global MarketMiddle EastAsia PacificAmericasAfricaEurope

50% of Global Market

Key Producing Countries(1)

(Billions of Cubic Meters)

Chi

na

Mex

ico

Egyp

t

Rus

sian

Fede

ratio

n

Note: (1) Covering 90% of global natural gas production in 2004Source: BP, Statistical review of world energy 2005; A.T. Kearney analysis

Gas

A.T. Kearney 82/06.2006/13154 16

Key Consuming RegionsWorld Consumption

1,108

902

368

242

69

Asia Pacific

Europe & Eurasia

Americas

AfricaMiddle East

Demand — The global Natural Gas demand totals 2.69 trillion cubic metersDemand — The global Natural Gas demand totals 2.69 trillion cubic meters

Natural Gas Consumption in 2004

Europe & Eurasia

RussianFederation

36%

Germany8%

United Kingdom9%

Others15%

Americas

Ukraine6%

Malaysia9%

India9%

2.69 Trillion Cubic Meters

Source: BP Statistical review of world energy 2005

Italy7%

US72%

Canada10%

Mexico5%

Argentina4%

Venezuela3% Others

4%

Brazil2%

Japan20%

China11%

Indonesia9%

Others27%

Asia Pacific

Gas

A.T. Kearney 82/06.2006/13154 17

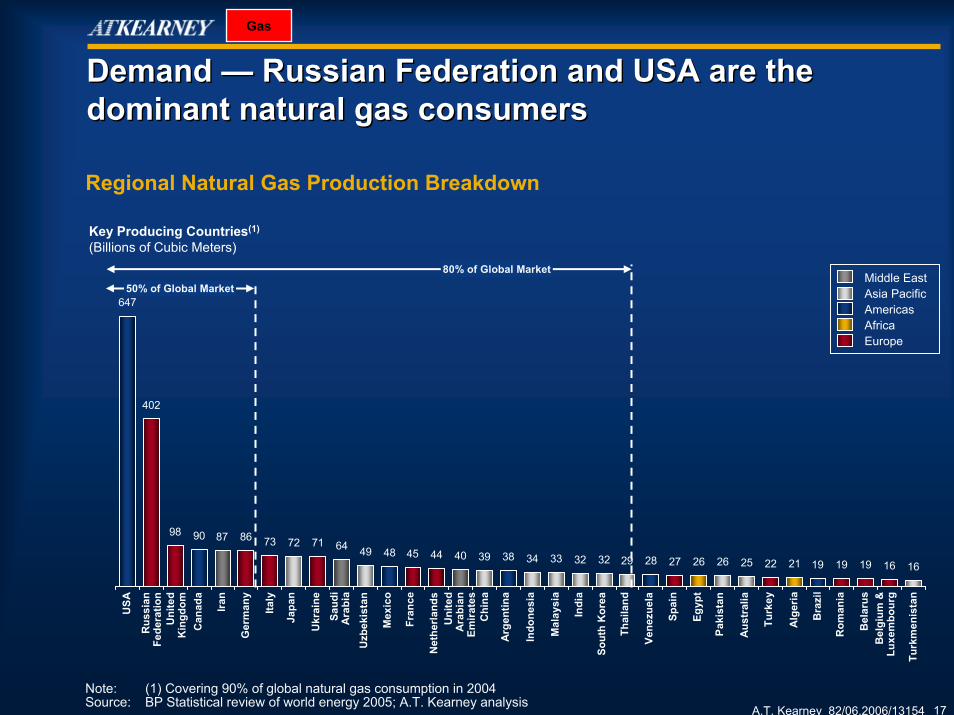

Demand — Russian Federation and USA are the dominant natural gas consumersDemand — Russian Federation and USA are the dominant natural gas consumers

Regional Natural Gas Production Breakdown

Note: (1) Covering 90% of global natural gas consumption in 2004Source: BP Statistical review of world energy 2005; A.T. Kearney analysis

Gas

647

402

98 90 87 86 73 72 71 64 49 48 45 44 40 39 38 34 33 32 32 29 28 27 26 26 25 22 21 19 19 19 16 16

Key Producing Countries(1)

(Billions of Cubic Meters)

Fran

ce

USA

Rom

ania

Turk

ey

Ukr

aine

Mex

ico

Iran

Vene

zuel

a

Can

ada

Uni

ted

Kin

gdom

Turk

men

ista

n

Uni

ted

Ara

bian

Emira

tes

Thai

land

Japa

n

Uzb

ekis

tan

Sout

h K

orea

Indo

nesi

a

Paki

stan

Indi

a

Net

herla

nds

Chi

na

Spai

n

Bel

gium

&Lu

xem

bour

g

Rus

sian

Fede

ratio

n

80% of Global Market

50% of Global Market

Ger

man

y

Italy

Saud

iA

rabi

a

Arg

entin

a

Mal

aysi

a

Egyp

t

Aus

tral

ia

Alg

eria

Bra

zil

Bel

arus

Middle EastAsia PacificAmericasAfricaEurope

A.T. Kearney 82/06.2006/13154 18

Asia PacificProduction vs. Consumption

Middle EastProduction vs. Consumption

Europe & Eurasia Production vs. Consumption

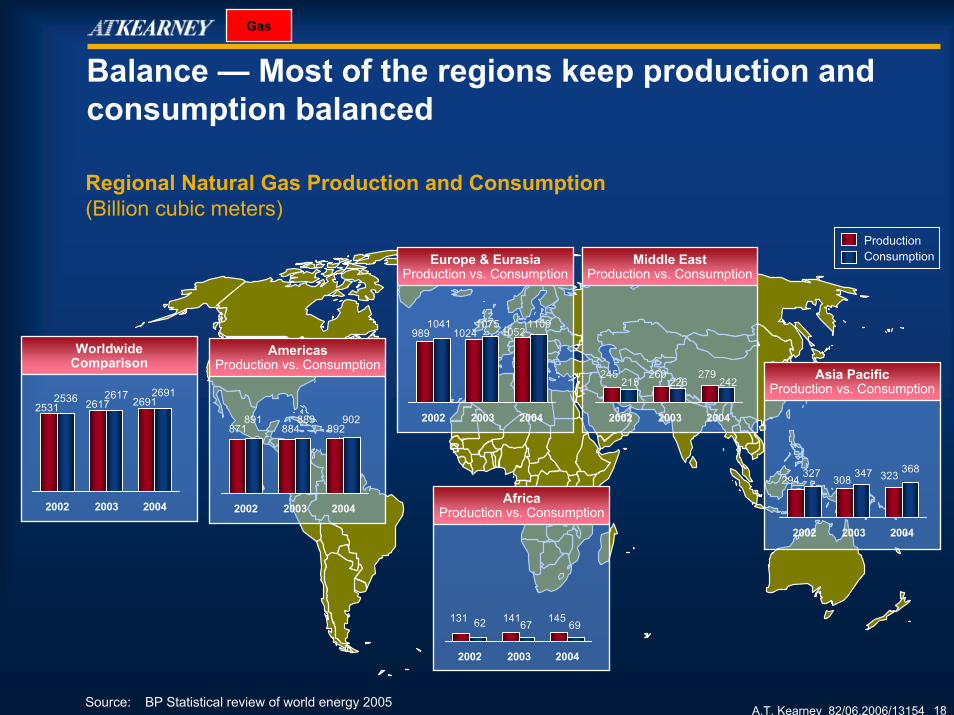

Balance — Most of the regions keep production and consumption balanced

2002 2003 2004

Regional Natural Gas Production and Consumption(Billion cubic meters)

9891041

10241075

10521109

WorldwideComparison

2002 2003 2004

25312536 2617

2617 26912691

2002 2003 2004

245215

260226

279242

ProductionConsumption

AmericasProduction vs. Consumption

2002 2003 2004

871891

884889

892902

AfricaProduction vs. Consumption

2002 2003 2004

131 62 14167

14569

2002 2003 2004

294 327 308 347 323 368

Source: BP Statistical review of world energy 2005

Gas

A.T. Kearney 82/06.2006/13154 19

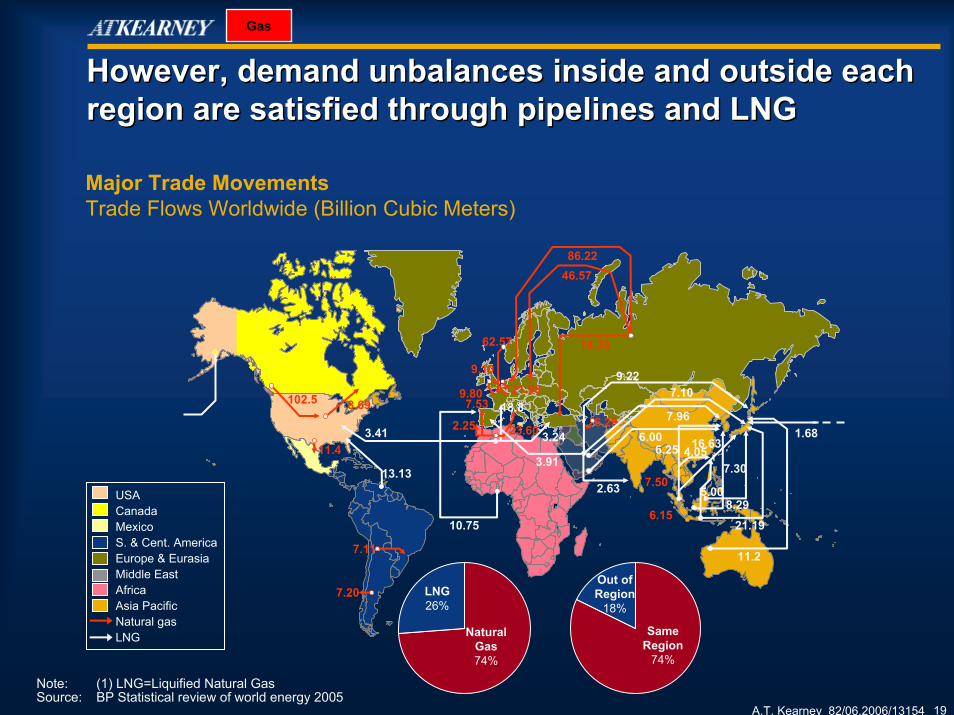

However, demand unbalances inside and outside each region are satisfied through pipelines and LNGHowever, demand unbalances inside and outside each region are satisfied through pipelines and LNG

USACanadaMexicoS. & Cent. AmericaEurope & EurasiaMiddle EastAfricaAsia PacificNatural gasLNG

LNG26%

Natural Gas74%

Out ofRegion

18%

Same Region

74%

Major Trade MovementsTrade Flows Worldwide (Billion Cubic Meters)

11.4

13.13

3.41

10.75

2.25

9.80

62.57

46.5786.22

1.68

7.30

8.296.15

2.63 7.50

102.5 8.69 7.53 18.8

14.35

6.29

3.91

7.96

7.109.22

6.004.05

16.63

5.00

21.19

11.27.11

7.20

9.1021.98

3.2423.606.25

Gas

Note: (1) LNG=Liquified Natural Gas Source: BP Statistical review of world energy 2005

A.T. Kearney 82/06.2006/13154 20

US supply chain infrastructure is one of the most complex systems in the worldUS supply chain infrastructure is one of the most complex systems in the world

US Petroleum Supply Chain Selected Physical Statistics(Latest Available Estimates)

Refining (March 2006) Pipelines (2004) Terminals (2003)

Barge (Excludes Ocean Tankers) Truck (2003) Rail (2003)Liquid carriers 3,614Throughput (kBPD) 4,180

Petroleum Tank Trucks (thousands) 170.4Throughput (kBPD) 600

Number of Tank Cars (thousands) 3,411Throughput (kBPD) 300

Number of Refineries (as of 1/1/05) 152Capacity (kBPD) 17,387Throughput (kBPD) 16,662Utilization (%) 85.7

Crude stocks (mBBL) 342Total stocks (mBBL) 1,691

Total Miles ~190,000• Crude trunk line ~55,000• Crude gathering line ~40,000• Refined Product ~95,000

Throughput (kBPD) 25,000Crude + Product

Number 1,612Total storage capacity (mBBL) 700Typical stocks (mBBL) 237Utilization (%) 34

Source: Energy Information Administration/Association of Oil Pipelines/BP Statistical Review 2003/Opis/Department of Transportation/A.T. Kearney Analysis

A.T. Kearney 82/06.2006/13154 21

Petroleum enters and leaves the US supply chain at many locationsPetroleum enters and leaves the US supply chain at many locations

Source: Energy Information Agency, 2002

US Petroleum Oil Flow — Supply Chain Energy Balance — 2002(Million Barrels per Day)

A.T. Kearney 82/06.2006/13154 22

1970 1980 1990 2000 2010 20250

5

10

15

20

25

30

Domestic supply

Consumption

History Projections

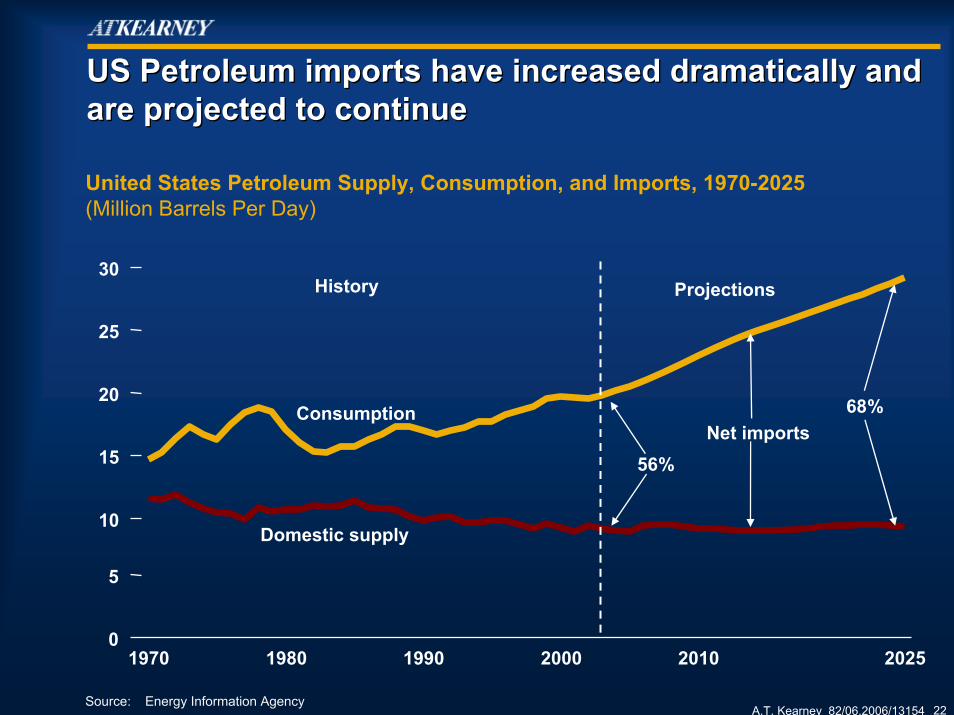

Net imports56%

68%

US Petroleum imports have increased dramatically and US Petroleum imports have increased dramatically and are projected to continueare projected to continue

Source: Energy Information Agency

United States Petroleum Supply, Consumption, and Imports, 1970-2025(Million Barrels Per Day)

A.T. Kearney 82/06.2006/13154 23

Key Import Source Countries – 2005Total = 12,353 kBPD

US imports from most nations continues to grow, with major share gains from the Persian Gulf and CanadaUS imports from most nations continues to grow, with major share gains from the Persian Gulf and Canada

Key Import Source Countries – 1983Total = 5,051 kBPD

US Crude Oil Import Sources

Other40%

United Kingdom

7%

Venezuela8%

Canada11%

Mexico16%

Saudi Arabia

7%Columbia

2%Nigeria

6%

Norway1%

Persian Gulf (Rest)

2%

Iraq0%

Source: Energy Information Administration; A.T. Kearney analysis

Iraq4%

Algeria4%

Angola4%

Russia3%

United Kingdom

3%

Persian Gulf (Rest)

2% Other20%

Nigeria9%

Mexico11%

Venezuela

12%

Saudi Arabia

12%

Canada16%

A.T. Kearney 82/06.2006/13154 24

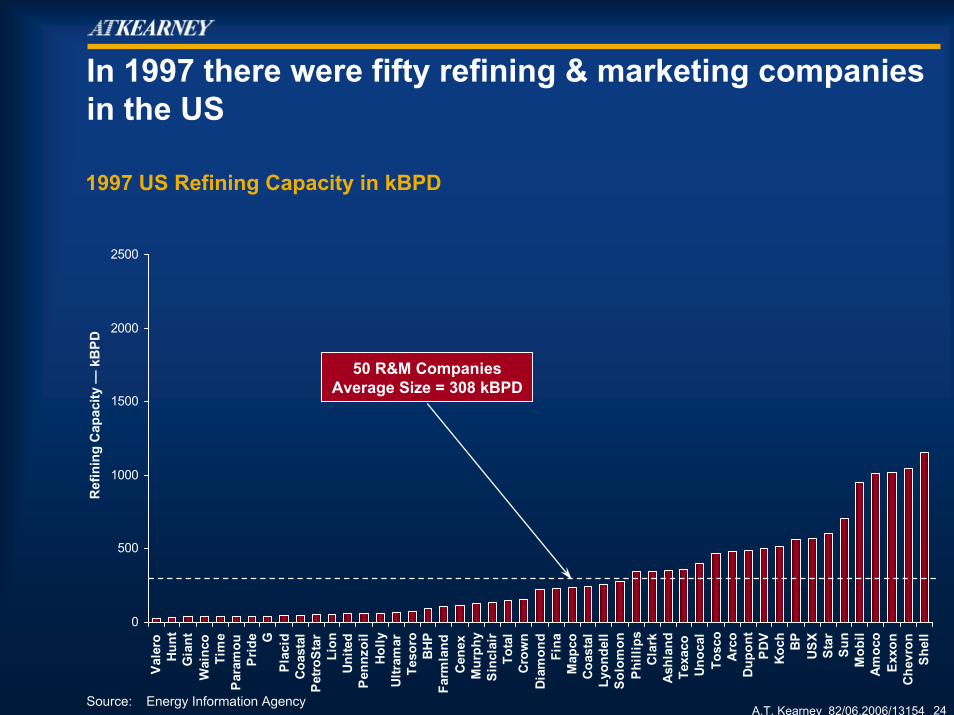

In 1997 there were fifty refining & marketing companies in the US

0

500

1000

1500

2000

2500

Vale

roH

unt

Gia

ntW

ainc

oTi

me

Par

amou

Prid

e GPl

acid

Coa

stal

Pet

roS

tar

Lion

Uni

ted

Pen

nzoi

lHo

llyU

ltram

arTe

soro

BH

PFa

rmla

ndC

enex

Mur

phy

Sinc

lair

Tota

lC

row

nDi

amon

dFi

naM

apco

Coa

stal

Lyon

dell

Solo

mon

Phi

llips

Cla

rkA

shla

ndTe

xaco

Unoc

alTo

sco

Arc

oD

upon

tP

DV

Koch BP

US

XSt

arS

unM

obil

Amoc

oEx

xon

Che

vron

She

ll

50 R&M CompaniesAverage Size = 308 kBPD

Ref

inin

g C

apac

ity —

kBPD

1997 US Refining Capacity in kBPD

Source: Energy Information Agency

A.T. Kearney 82/06.2006/13154 25

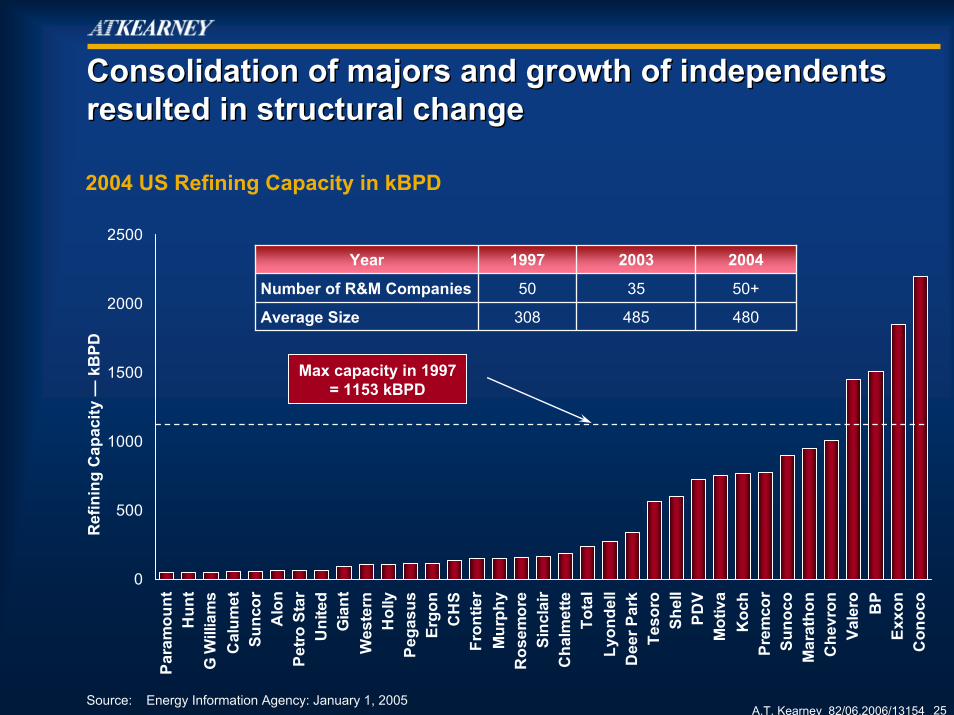

Consolidation of majors and growth of independents resulted in structural changeConsolidation of majors and growth of independents resulted in structural change

0

500

1000

1500

2000

2500

Para

mou

ntH

unt

G W

illia

ms

Cal

umet

Sunc

orA

lon

Petro

Sta

rU

nite

dG

iant

Wes

tern

Hol

lyPe

gasu

sEr

gon

CH

SFr

ontie

rM

urph

yR

osem

ore

Sinc

lair

Cha

lmet

teTo

tal

Lyon

dell

Dee

r Par

kTe

soro

Shel

lPD

VM

otiv

aK

och

Prem

cor

Suno

coM

arat

hon

Che

vron

Vale

ro BP

Exxo

nC

onoc

o

Ref

inin

g C

apac

ity —

kBPD

Year 1997 2003 2004

Number of R&M Companies 50 35 50+

480Average Size 308 485

2004 US Refining Capacity in kBPD

Source: Energy Information Agency: January 1, 2005

Max capacity in 1997= 1153 kBPD

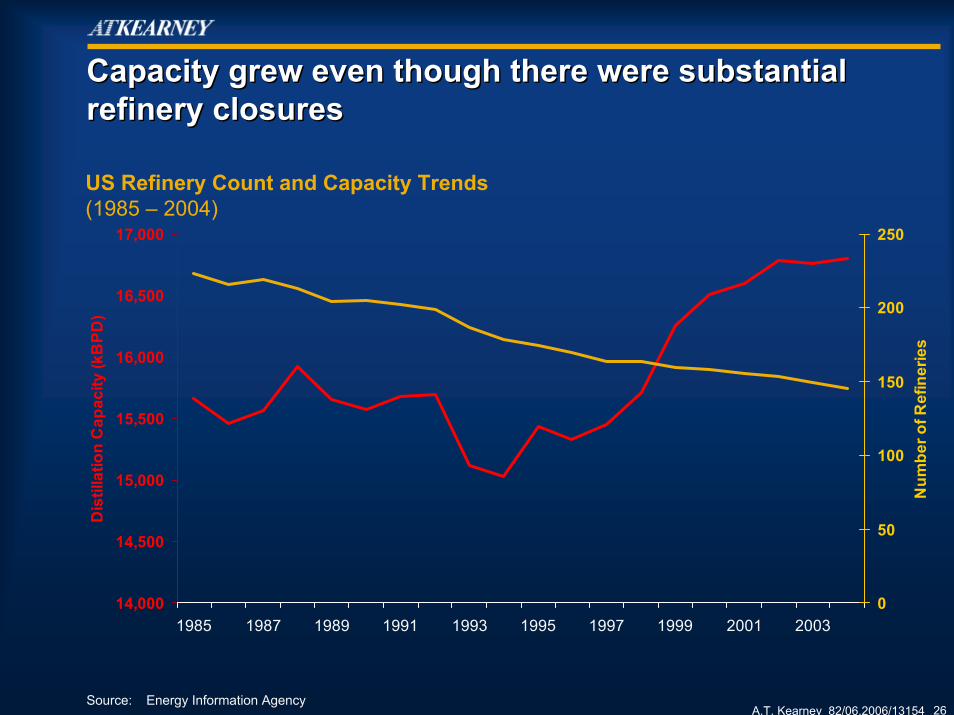

A.T. Kearney 82/06.2006/13154 26

Capacity grew even though there were substantial refinery closuresCapacity grew even though there were substantial refinery closures

14,000

14,500

15,000

15,500

16,000

16,500

17,000

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003

Dis

tilla

tion

Cap

acity

(kB

PD)

0

50

100

150

200

250

Num

ber o

f Ref

iner

ies

US Refinery Count and Capacity Trends(1985 – 2004)

Source: Energy Information Agency

A.T. Kearney 82/06.2006/13154 27

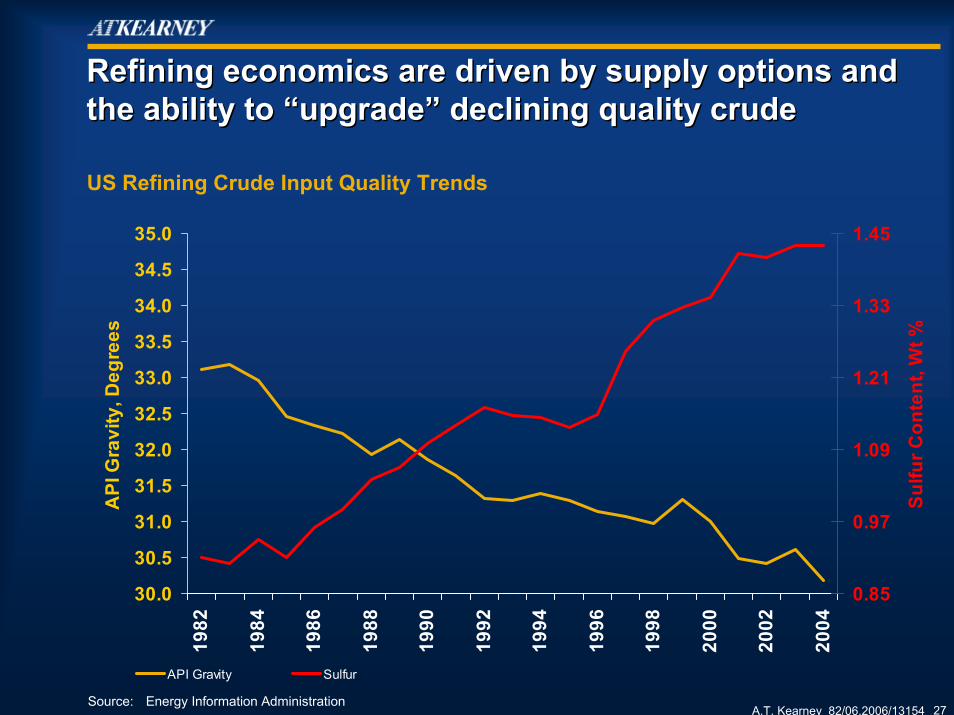

Refining economics are driven by supply options and the ability to “upgrade” declining quality crudeRefining economics are driven by supply options and the ability to “upgrade” declining quality crude

30.0

30.5

31.0

31.5

32.0

32.5

33.0

33.5

34.0

34.5

35.0

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

API

Gra

vity

, Deg

rees

0.85

0.97

1.09

1.21

1.33

1.45

Sulfu

r Con

tent

, Wt %

API Gravity Sulfur

US Refining Crude Input Quality Trends

Source: Energy Information Administration

A.T. Kearney 82/06.2006/13154 28

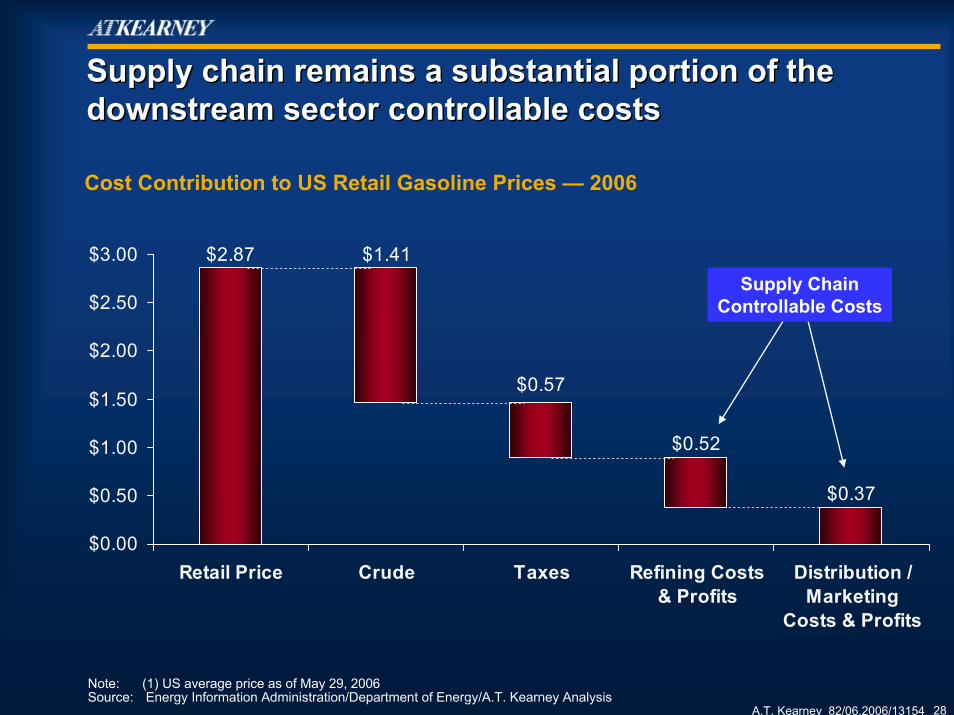

Supply chain remains a substantial portion of the downstream sector controllable costs Supply chain remains a substantial portion of the downstream sector controllable costs

$0.37

$0.52

$2.87 $1.41

$0.57

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

Retail Price Crude Taxes Refining Costs& Profits

Distribution /Marketing

Costs & Profits

Cost Contribution to US Retail Gasoline Prices — 2006

Note: (1) US average price as of May 29, 2006Source: Energy Information Administration/Department of Energy/A.T. Kearney Analysis

Supply ChainControllable Costs

A.T. Kearney 82/06.2006/13154 29

A Look to the FutureA Look to the Future

A.T. Kearney 82/06.2006/13154 30

The Global Business Policy Council provides deep insight into future trendsThe Global Business Policy Council provides deep insight into future trends

The Global Business Policy Council (GBPC) was formed over a decade ago with the objective of providing early warningagainst accelerating shifts in economics, politics, technology, demographics, and culture that are poised to shape and shakethe global business environment

Membership in the GBPC is limited to a select group of corporate leaders (~50) and their companies joined by a small group of world-renowned policy makers, scholars, and other thought leaders and their companies.

Each year, these members have threeopportunities to gather for two-to-three days of intense discussion and reflection on the forces shaping a volatile and continually changing global business environment

The Council produces a series of intellectualcapital products that provide a broad rangeof insights on important global trends

Why is this so important?

A.T. Kearney 82/06.2006/13154 31

72%63% 67%

62%

33%25%

17% 17% 19%

66%

51%43%

38% 35% 35% 32% 28% 27%

Traditional risks are giving way to a number of emerging risks to which companies are exposed Traditional risks are giving way to a number of emerging risks to which companies are exposed

Traditional RisksDecrease of 6 – 24%

Since 2003 Emerging Risks

Increase of 4 – 11% since 2003

Most Critical Risks to Firm Operations (2005)(% of Total Respondents)

Government Regulation /

Legal Decisions

Country Financial

Risk

Currency / Interest

Rate Volatility

Political and Social

Disturban-ces

Disruption of Key

Supplier / Customer /

Partner

Corporate Governance

Issues

IT Disruption

Theft of Intellectual Property

Product Quality / Safety

Problems

Source: A.T. Kearney Global Business Policy Council, 2006.

20052003

A.T. Kearney 82/06.2006/13154 32

Large firms often attribute earnings under-performance to unexpected external events Large firms often attribute earnings under-performance to unexpected external events

43% of Fortune 100 companies blamed unexpected external events for failure to meet earnings expectations

43% Blame External Events

External Events Reported in 2003 Annual Reports of the Fortune 100

Note: (1) Percentages do not add up due to multiple events reported by some companiesSources: A.T. Kearney Global Business Policy Council analysis of companies annual reports

20%

12%

12%

11%

9% Terrorism

Foreign Exchange Crisis

September 11th

War in Iraq

Crisis in Latin America

A.T. Kearney 82/06.2006/13154 33

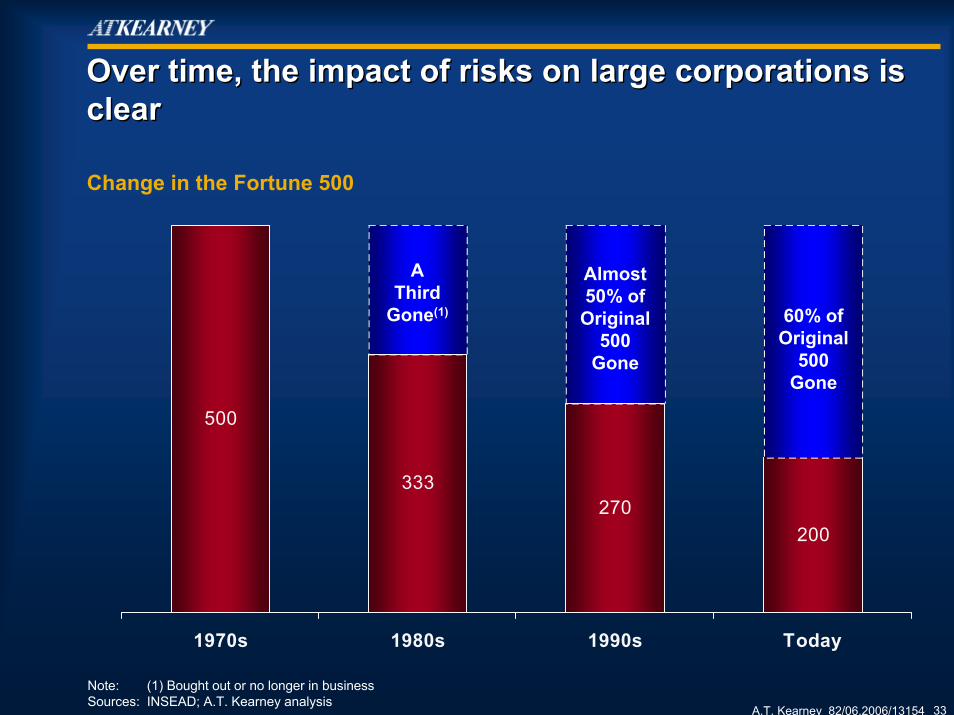

Over time, the impact of risks on large corporations is clearOver time, the impact of risks on large corporations is clear

200270

333

500

Today1990s1980s1970s

Almost 50% of

Original 500

Gone

A Third

Gone(1) 60% of Original

500 Gone

Change in the Fortune 500

Note: (1) Bought out or no longer in businessSources: INSEAD; A.T. Kearney analysis

A.T. Kearney 82/06.2006/13154 34

To better understand risks, A.T. Kearney focuses on the forces reshaping the worldTo better understand risks, A.T. Kearney focuses on the forces reshaping the world

A.T. Kearney 82/06.2006/13154 35

The implications for oil and gas supply chains are immenseThe implications for oil and gas supply chains are immense

• Sourcing• Labor Conditions• Environment• Privacy

• Increasing segmentation

• Shift of location of demand

• Fundamental shift in customer demand and labor supply

• Major growth outside US

• New competitors

• Potential supply disruptions

New ConsumersGlobalization

Natural Resources &Environment

Demographics

Regulation & Activism

Wildcards

Technology & Innovation

• Continuous opportunities/threats from new products, processes, technologies

A.T. Kearney 82/06.2006/13154 36

Developed Nations• Expansion of Older Population• Environmental and Social Responsibility Preferences

Emerging Nations• Access and Economic Development• Technology Growth

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006E 2007E 2008E 2009E 2010E

Economic performance and customer preferences drive global demand for petroleumEconomic performance and customer preferences drive global demand for petroleumIncreased Demand — Worldwide Revival of Economy

Further influenced by political unrest in certain regions (e.g. Middle East)

GDP Top 30 Countries

Demographics

Source: Global Insight, A.T. Kearney analysis

A.T. Kearney 82/06.2006/13154 37

Industries, including petrochemicals, are rebalancing to meet demographic and preference shiftsIndustries, including petrochemicals, are rebalancing to meet demographic and preference shiftsUnprecedented Demand Shifting —Fundamental Relocation of Industries

After China, India is likely to be the next area for major growth

Demographics

Source: Global Insight, A.T. Kearney analysis

China

EU

NAFTA

Exports of Finished Goods

Future Exports of Petrochemicals

A.T. Kearney 82/06.2006/13154 38

By 2020, middle income spending will shift to emerging markets — how will you seize the market opportunity?By 2020, middle income spending will shift to emerging markets — how will you seize the market opportunity?

Source: World Bank, EIU, U.S. Census Bureau, A.T. Kearney analysis

Middle Income Upper MiddleUpper Middle Upper Income Upper Income Scale: 10 million consumersScale: 10 million consumers

Total middle income consumers = 2.3 billion

(31% world population)

Ecuador

New ZealandIndonesia

Taiwan

Canada

Argentina

Chile

Peru

Central America

Ireland

Benelux

Italy

Portugal Austria Switzerland

Turkey

Iran

GreeceNorth Africa

South AfricaAustralia

Philippines

Thailand

Singapore

Hong Kong

South Korea

Columbia Venezuela

U.S. China

Mexico

Brazil

France

Spain

UK

Russia

EasternEurope

Japan

Germany

India

Israel

Iran

TurkeyItaly

Scandinavia

Globalization / New Consumers

A.T. Kearney 82/06.2006/13154 39

Ceyhan

Oil Fields Realistic Projects Postponed Projects2004 finalized Existing Pipelines

New pipelines and terminals are securing supply flexibility and connecting resources with customersNew pipelines and terminals are securing supply flexibility and connecting resources with customers

New Consumers

Oil & Gas Pipeline Projects

Source: DekaBank

China

Russia

Chad

Beijing

DaqingUlan-Ude

Irkutsk

Krasnojarsk

Novo-sibirsk

Tengiz

Baku

NovorossiskSamsun

Ventspils

Nachodka

Kola

Ürünqi

Clair OilOstsee-Pipeline

Chad-Cameroon

Baku-Ceyhan

Caspic Pipeline

Samsun-CeyhanSiberia-Beijing

Sibirien-Japanisches Meer

Sibirien-Nordostchina

Westsibirien-Westchina

Northern Gateway

A.T. Kearney 82/06.2006/13154 40

In the near term, global oil tanker capacity will not be the limiting factor for accessing customersIn the near term, global oil tanker capacity will not be the limiting factor for accessing customers

• Cyclical industry: just emerging from supply constraint situation

• Over 88 mm tons of orders (~11 mbd); 66mm tons (~8.3 mbd), between 2005-2007

• Oil demand is likely to increase 5.4 mbdthrough 2010 in the most aggressive IEA scenario

• Concerns on tanker supply post-2010 remain, given the dramatic oil demand growth in China, the Venezuelan output reduction and long-haul supply increase

But the shift in oil demand balance may cause capacity constraints in the mid- and long-term

0.0

2.0

4.0

6.0

8.0

10.0

2005 – 2007m

bd

Oil Demand Growth Tanker Capacity Growth

Oil Demand vs. Tanker Capacity Growth (2005-2007)

Globalization/New Consumers

Source: Deutsche Bank analyst reports; A.T. Kearney analysis

A.T. Kearney 82/06.2006/13154 41

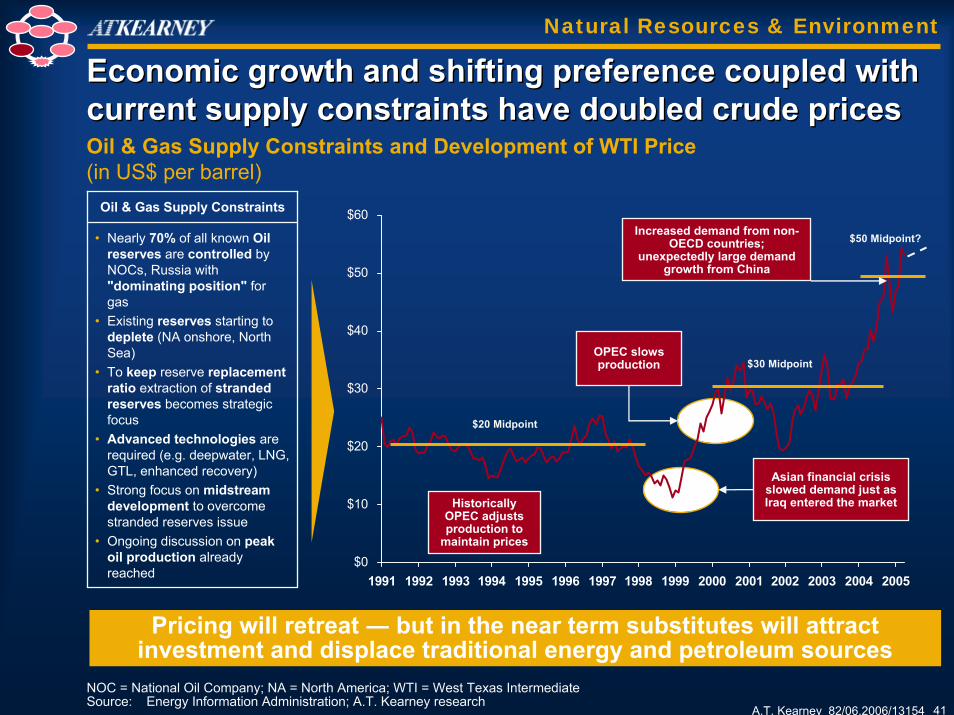

Economic growth and shifting preference coupled with current supply constraints have doubled crude pricesEconomic growth and shifting preference coupled with current supply constraints have doubled crude prices

NOC = National Oil Company; NA = North America; WTI = West Texas IntermediateSource: Energy Information Administration; A.T. Kearney research

$0

$10

$20

$30

$40

$50

$60

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

$20 Midpoint

$30 Midpoint

$50 Midpoint?

Asian financial crisis slowed demand just as Iraq entered the market

OPEC slows production

Increased demand from non-OECD countries;

unexpectedly large demand growth from China

Historically OPEC adjusts production to

maintain prices

Oil & Gas Supply Constraints

• Nearly 70% of all known Oil reserves are controlled by NOCs, Russia with "dominating position" for gas

• Existing reserves starting to deplete (NA onshore, North Sea)

• To keep reserve replacement ratio extraction of stranded reserves becomes strategic focus

• Advanced technologies are required (e.g. deepwater, LNG, GTL, enhanced recovery)

• Strong focus on midstream development to overcome stranded reserves issue

• Ongoing discussion on peak oil production already reached

Oil & Gas Supply Constraints and Development of WTI Price (in US$ per barrel)

Pricing will retreat ― but in the near term substitutes will attract investment and displace traditional energy and petroleum sources

Natural Resources & Environment

A.T. Kearney 82/06.2006/13154 42

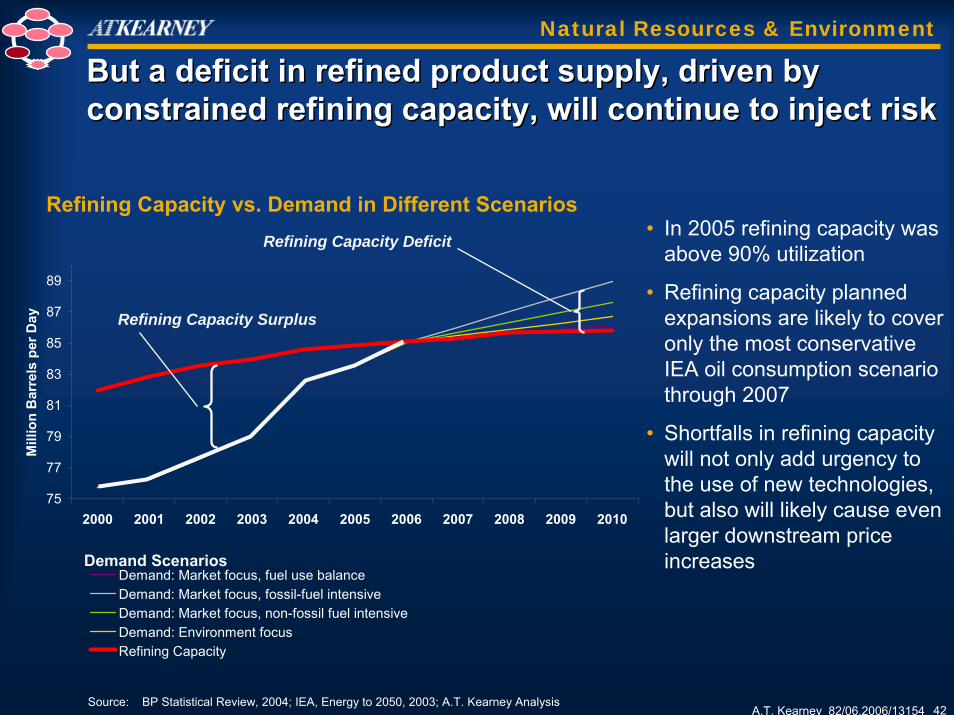

But a deficit in refined product supply, driven by constrained refining capacity, will continue to inject riskBut a deficit in refined product supply, driven by constrained refining capacity, will continue to inject risk

• In 2005 refining capacity was above 90% utilization

• Refining capacity planned expansions are likely to cover only the most conservative IEA oil consumption scenario through 2007

• Shortfalls in refining capacity will not only add urgency to the use of new technologies, but also will likely cause even larger downstream price increases

Refining Capacity vs. Demand in Different Scenarios

Source: BP Statistical Review, 2004; IEA, Energy to 2050, 2003; A.T. Kearney Analysis

75

77

79

81

83

85

87

89

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Mill

ion

Bar

rels

per

Day

Demand: Market focus, fuel use balanceDemand: Market focus, fossil-fuel intensiveDemand: Market focus, non-fossil fuel intensiveDemand: Environment focusRefining Capacity

Refining Capacity Surplus

Refining Capacity Deficit

Demand Scenarios

Natural Resources & Environment

A.T. Kearney 82/06.2006/13154 43

145

1563

67

94

206

445

300

North America

Western Europe

Total Atlantic Basin

Indus-trialized

Asia

China Rest of Asia

Total Pacific Basin

Total

Several regions are expected to face potential refined oil supply deficits over the next 5 years …Several regions are expected to face potential refined oil supply deficits over the next 5 years …

• Strong demand growth for middle and light distillates

• Strict fuel norms leading to closure of marginal units

• Few investments in new capacity

Key Drivers • Robust demand growth driven by overall economic growth in the region

• Growth in Chinese consumption driven by transportation and petrochemicals sector

• Closure of uneconomical & marginal units

Atlantic Basin Pacific Basin

Shift in location of demand

Expected Refined Oil Product Deficit Regions in 2010(Figures in mtpa1)

Note: (1) mtpa=Million Metric Tons per annum; 1 mtpa = 0.02 mbdSource: EIA Outlook, Analyst Reports, A.T.Kearney analysis

Natural Resources & Environment

A.T. Kearney 82/06.2006/13154 44

… with projected refined oil product capacities unable to address these deficits… with projected refined oil product capacities unable to address these deficits

Assumptions: Based on historical flows, it is assumed that 75% of Middle East production will be available for Asia Pacific, Eastern Europe, Latin America & Africa; surplus is assumed to serve North America and Europe demand

Source: EIA Outlook; Analyst Reports; A.T.Kearney analysis

33

20

15-94

S. Korea

IndustrializedAsia

MiddleMiddle--easteast

AfricaAfrica

Latin AmericaLatin America

Supply deficit Supply surplusLikely flows based on historical trends

West Europe East Europe

China

Pacific Basin (Unmet Demand)

Atlantic Basin (Unmet Demand)

Expected Demand Supply Scenario – 2010 (Figures in mtpa)

-50

-207-65

-15

Rest of Asia

North America

-67

-62

175

90

Natural Resources & Environment

A.T. Kearney 82/06.2006/13154 45

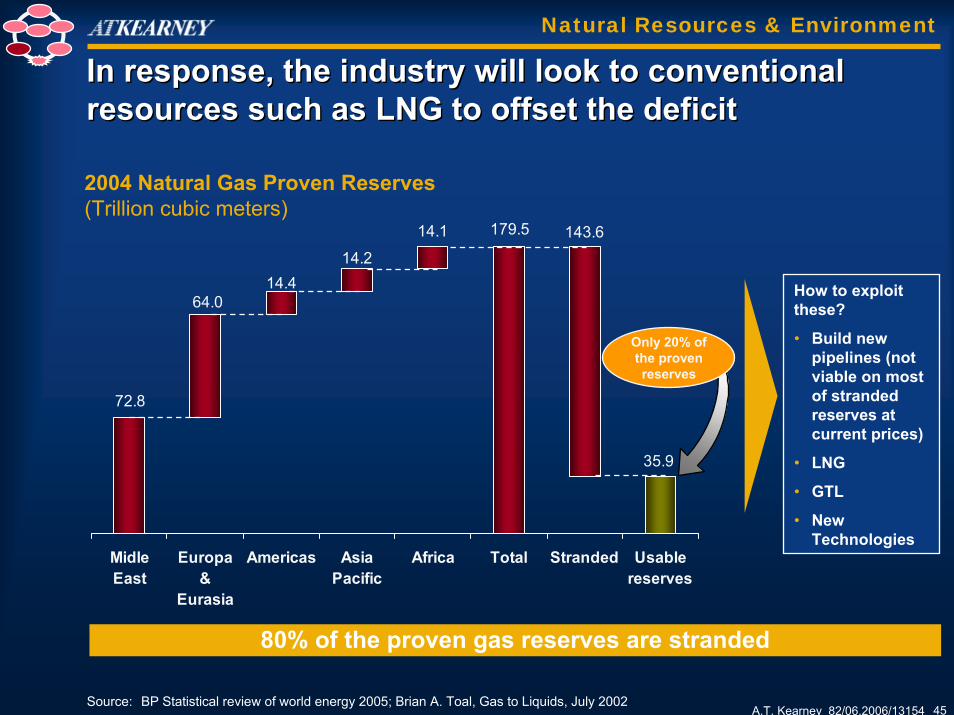

In response, the industry will look to conventional resources such as LNG to offset the deficitIn response, the industry will look to conventional resources such as LNG to offset the deficit

72.8

64.014.4

14.2

14.1 179.5 143.6

35.9

MidleEast

Europa&

Eurasia

Americas AsiaPacific

Africa Total Stranded Usablereserves

Only 20% of the proven reserves

How to exploit these?

• Build new pipelines (not viable on most of stranded reserves at current prices)

• LNG

• GTL

• New Technologies

Natural Resources & Environment

2004 Natural Gas Proven Reserves(Trillion cubic meters)

Source: BP Statistical review of world energy 2005; Brian A. Toal, Gas to Liquids, July 2002

80% of the proven gas reserves are stranded

A.T. Kearney 82/06.2006/13154 46

LNG is playing an increasingly important role in the international gas trade …LNG is playing an increasingly important role in the international gas trade …

Natural gas LNG

11.4

13.13

3.41

10.75

2.25

9.80

62.57

46.5786.22

7.30

8.296.15

2.63 7.50

1.68

102.5 8.69 7.53 18.8

14.35

6.29

3.91

7.96

7.109.22

6.00 4.0

5

16.63

5.00

21.19

11.27.11

7.20

Source: IEA, World Energy Outlook 2004

North America Asia Europe

0

100

200

300

400

500

600

700

800

1985 1990 1995 2002 2010 2020 2030

Natural Gas and LNG Trade Flows Worldwide 2004 (bcm)

LNG Volume & Development (bcm)

Note: bcm = Billion Cubic MetersSource: BP Statistical review 2005

Natural Resources & Environment

9.10

21.98

3.2423.606.25

A.T. Kearney 82/06.2006/13154 47

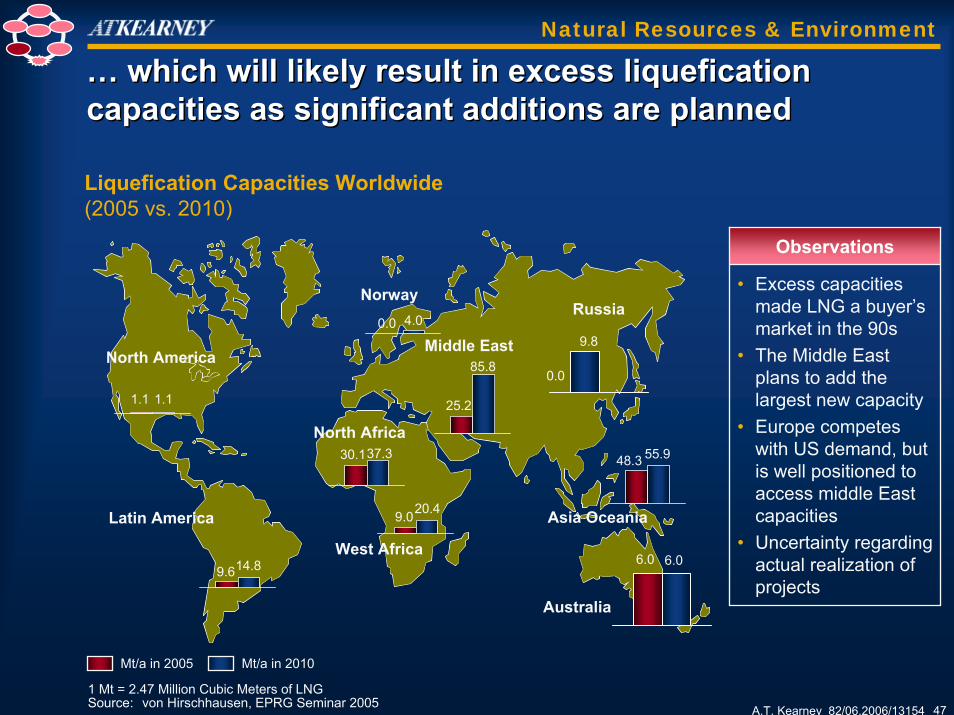

… which will likely result in excess liquefication capacities as significant additions are planned … which will likely result in excess liquefication capacities as significant additions are planned

Middle East

Australia

Asia Oceania

West Africa

Latin America

North America

NorwayRussia

6.0 6.0

0.0 4.0

0.0

9.8

9.020.4

9.614.8

1.1 1.1

48.3 55.9

25.2

85.8

North Africa30.137.3

Mt/a in 2005 Mt/a in 2010

Liquefication Capacities Worldwide (2005 vs. 2010)

Observations

• Excess capacities made LNG a buyer’s market in the 90s

• The Middle East plans to add the largest new capacity

• Europe competes with US demand, but is well positioned to access middle East capacities

• Uncertainty regarding actual realization of projects

1 Mt = 2.47 Million Cubic Meters of LNGSource: von Hirschhausen, EPRG Seminar 2005

Natural Resources & Environment

A.T. Kearney 82/06.2006/13154 48

The key conventional energy resources will face challenges after 2020The key conventional energy resources will face challenges after 2020

Conventional energy resources

Renewable resources

19901990 20002000 20102010 20202020 20302030 20402040

OilOil

Gas

Nuclear powerThe future of the nuclear energy The future of the nuclear energy supply depends on technology and supply depends on technology and regulatory advancesregulatory advances

GTL technologies opening GTL technologies opening opportunity for exploiting stranded opportunity for exploiting stranded gasgas

Resources will focus on limited Resources will focus on limited countries driven by distance from countries driven by distance from the marketthe market

Technology improvements could Technology improvements could retard the oil scarcityretard the oil scarcity

Competition with food and leisure Competition with food and leisure for land usefor land use

Prices will further be reduced, new Prices will further be reduced, new forms of energy storage requiredforms of energy storage required

Gas

Nuclear Power

Coal

Biofuels

Solar, wind & water

Source: A.T. Kearney; Shell Study 2050

Energy Resources Constraints

Technology & Innovation

A.T. Kearney 82/06.2006/13154 49

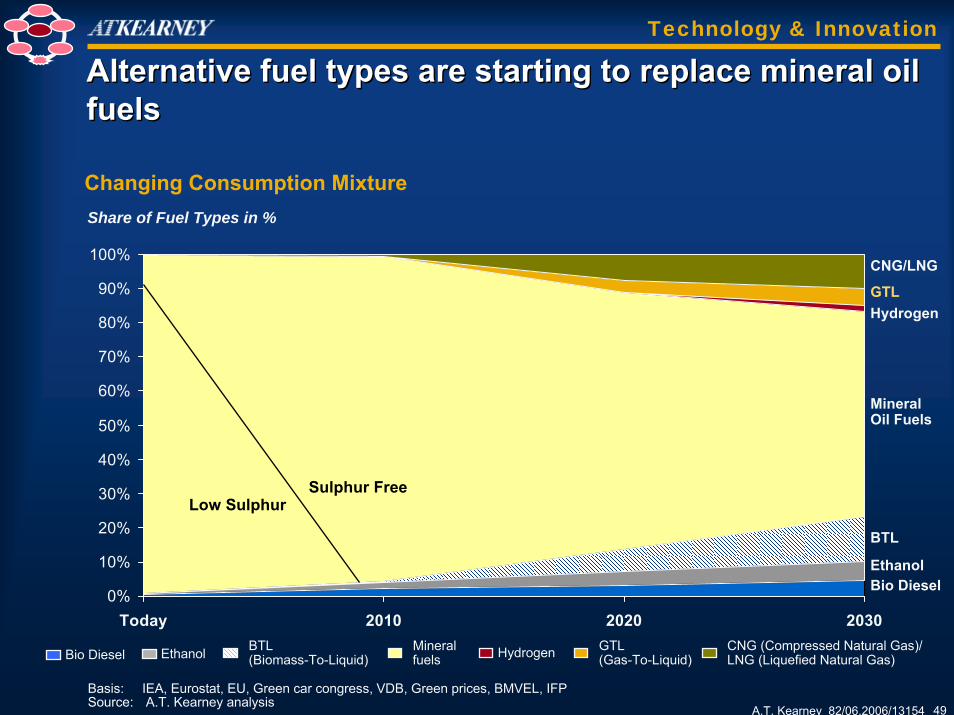

Alternative fuel types are starting to replace mineral oil fuelsAlternative fuel types are starting to replace mineral oil fuels

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Today 2010 2020 2030

Bio DieselEthanol

BTL

HydrogenGTL

CNG/LNG

MineralOil Fuels

Share of Fuel Types in %

Sulphur Free

Mineral fuelsEthanol BTL

(Biomass-To-Liquid) Hydrogen GTL (Gas-To-Liquid)

CNG (Compressed Natural Gas)/ LNG (Liquefied Natural Gas)

Low Sulphur

Changing Consumption Mixture

Basis: IEA, Eurostat, EU, Green car congress, VDB, Green prices, BMVEL, IFP Source: A.T. Kearney analysis

Bio Diesel

Technology & Innovation

A.T. Kearney 82/06.2006/13154 50

GTL has only recently become a competitive technologyGTL has only recently become a competitive technology

Technology & Innovation

GTL technology has a cost structure advantage at oil prices exceeding US$20 per bbl

Diesel Production Costs Comparison(US$/BBL)

Exploiting stranded gas reserves requires less capital than other unconventional hydrocarbon

development processes

Unconventional Petroleum Liquids Capital Investment Costs(Us$’000/Bpd)

Shale OilOil Sands

Extra-heavy Oil

Biomass –To-Liquids

Coal-To-LiquidsGas-To-Liquids

Oil Refinery

0 20 40 60 80 100 120 140 160

Notes: (1) International average gas prices, May 2006; US$ 1.00/MMBtu(2) ConocoPhillips estimates(3) Considering an average price of US$50 per bbl

Source: 2006 EIA Energy Outlook and Modeling Conference Handouts; Rentech Co.;A.T. Kearney analysis

RefineryGTL

2414

7

50

10

59

28

Cost Advantage:US$31/Bbl(3)

Equilibrium Price:US$20/Bbl

Feedstock(1)

Capex recovery & taxes(2)

Operating cost(2)

A.T. Kearney 82/06.2006/13154 51

GTL is a promising technology to substitute oil demand from stranded gas reservesGTL is a promising technology to substitute oil demand from stranded gas reserves

Technology & Innovation

Source: ConocoPhililps, 2005; New York Times, 5/2006; A.T. Kearney research

Drivers for Development

• Push to monetize stranded reserves

• Push to utilize wells that are too small for pipelines’ viability at current prices (e.g. Nigeria, Malaysia, South Africa)

• Decreasing cost and improvement of the technology

• Oil price that allows technology to be a viable alternative only since 2000

Investment and Interest Growing

• ExxonMobil, ConocoPhillips, Shell, Chevron, BP investing heavily in GTL technology in Africa, Asia, and Latin America

• US military is testing alternative fuels based on GTL technologies (5/06, New York Times)

• By 2020, GTL plants will produce ~1 mbd GTL products (~70+% from Qatar), and substitute up to 3% of world diesel and naphta markets

However, it is likely that before 2020, the technology will only relieve about 1% of oil demand

A.T. Kearney 82/06.2006/13154 52

Currently, tax breaks are major growth drivers for bio fuels with very few exceptionsCurrently, tax breaks are major growth drivers for bio fuels with very few exceptions

National bio diesel tax breaks compared to mineral diesel 2005 (€ ct/l)

Correlation between bio diesel tax breaks and market share per EU country Conclusions:

Positive correlation exists between bio diesel tax breaks and market share of bio diesel (e.g. Germany, France, Italy and Spain) with only few exceptionsSlovenia, Portugal and Greece with significant bio diesel share despite missing tax breaksCountries like UK and Hungary with relatively low bio diesel share despite significant tax breaks (but: Hungary's entry into EU 2005, UK with tax breaks since 2003)

Tax breaks and share of bio fuel per country (example bio diesel)

1) Quotas for the volume of bio diesel that receives tax breaksSource: A.T. Kearney analysis

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

0 10 20 30 40 50

GRMAIR, FIN, DEN

B GE, LIT Fr

UK

IT

LAT, POR, SLO

N

A

SW

SP

CZ

H

Share of bio dieselper country2005 (in % of diesel market)

Technology & Innovation

A.T. Kearney 82/06.2006/13154 53

Fuel Cells will create significant opportunities when commercializedFuel Cells will create significant opportunities when commercialized

0

5000

10000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Market Volume(1)

(US$ millions)

Portable

Stationary

MobilePrototype

phase

CommercialPhase

Expected MarketShare in 2015

Mobile

Portable

Stationary

PassengerCars

Other Cars &VehiclesBattery

Replacement

Generators

Commercial/Industrial

Residential30%

10%

2-10%(of new car

registrations)Prototype Phase

PrototypePhase

PrototypePhase

Launch

LaunchCommercial Phase

Launch

Launch

Commercial Phase

Launch

Launch

CommercialPhase

Best Case Scenarios

Fuel Cell Market Scenario 2015

Note: (1) Market covers only Fuel Cells, excl. revenues from new fuels Source: A.T. Kearney analysis

Technology & Innovation

A.T. Kearney 82/06.2006/13154 54

The race for the future energy technologies is still openThe race for the future energy technologies is still open

1800 1850 1900 1950 2000 …

Energy Technology Discontinuities

Wood,Wind,Water,Ani-mals

Steam Engine, Coal

Electric Dynamo,

Coal

Internal Com-

bustionEngine, Oil

Nu-clear

Power 1970–1990

CCGT Gas1) >1990

Solarenergy ?

Bio Fuels?

Fuel Cell hydrogen?

GTL?

New Technologies

Note: (1) Combined cycle gas turbineSource: A.T. Kearney; Shell Study 2050

• Commercial introduction of new primary energy takes ~ 25 years to obtain 1% of global market

• Future energy resources will focus on low emissions but several issues have still to be solved— Improving GTL technology— Nanotechnology:

– Hydrogen/energy storage– Costs– Efficiency

― Solar energy― Bio fuels scale economic

viability― Government efforts and

interests

Technology & Innovation

A.T. Kearney 82/06.2006/13154 55

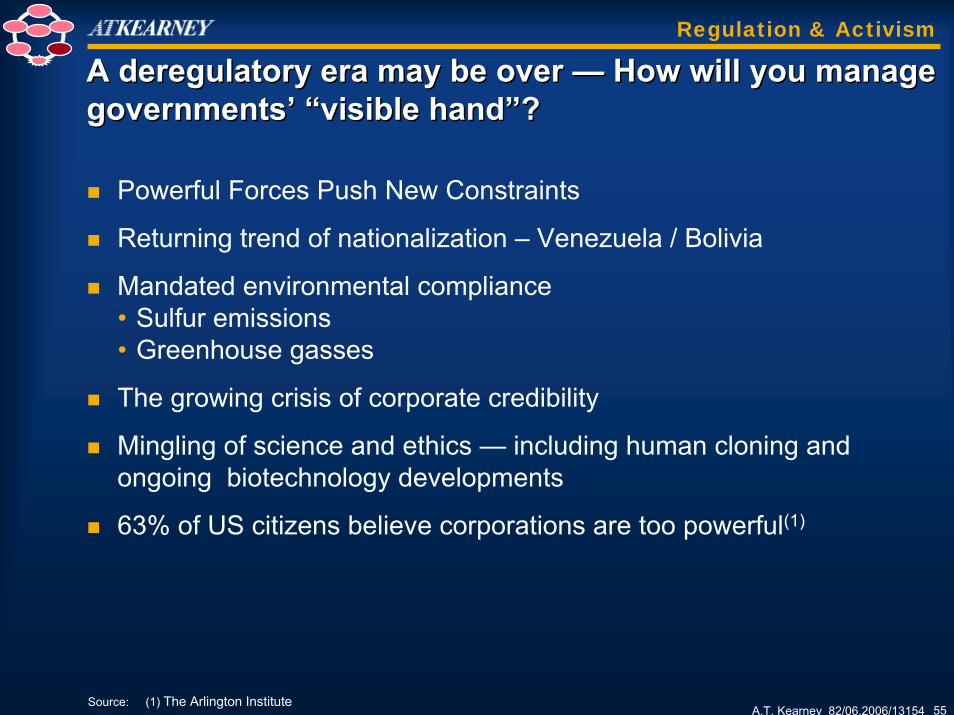

A deregulatory era may be over — How will you manage governments’ “visible hand”?A deregulatory era may be over — How will you manage governments’ “visible hand”?

Powerful Forces Push New Constraints

Returning trend of nationalization – Venezuela / Bolivia

Mandated environmental compliance• Sulfur emissions• Greenhouse gasses

The growing crisis of corporate credibility

Mingling of science and ethics — including human cloning and ongoing biotechnology developments

63% of US citizens believe corporations are too powerful(1)

Source: (1) The Arlington Institute

Regulation & Activism

A.T. Kearney 82/06.2006/13154 56

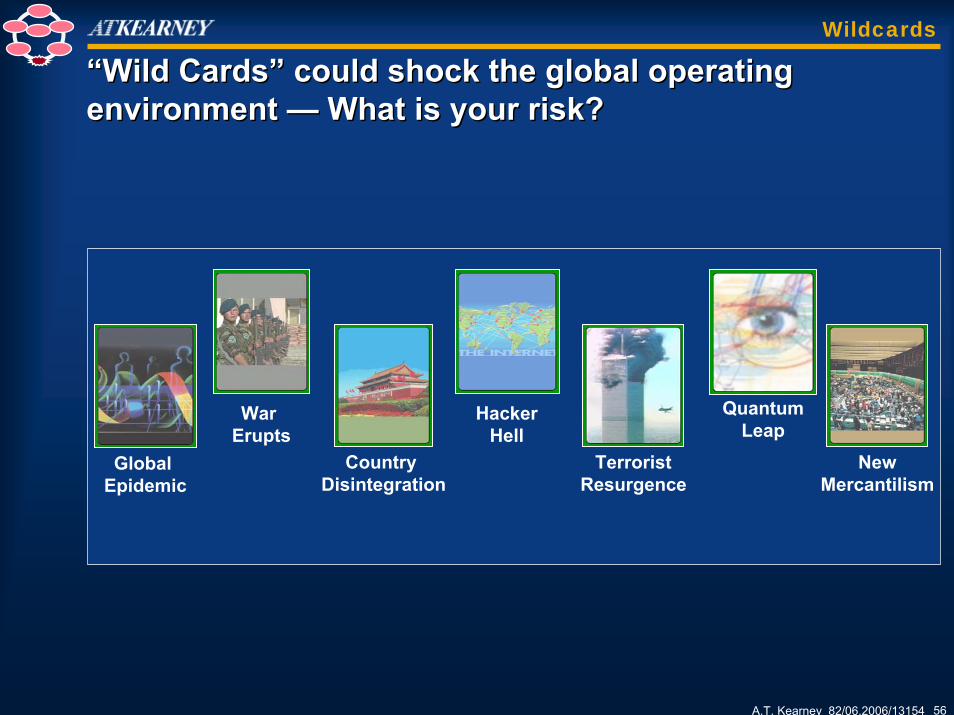

“Wild Cards” could shock the global operating environment — What is your risk?“Wild Cards” could shock the global operating environment — What is your risk?

Country Disintegration

War Erupts

NewMercantilism

TerroristResurgence

HackerHell

Global Epidemic

QuantumLeap

Wildcards

A.T. Kearney 82/06.2006/13154 57

Supply disruptions may occur because of disruption at a transit “chokepoint”…Supply disruptions may occur because of disruption at a transit “chokepoint”…

Supply Chokepoint — Oil & Gas:

Potential Transit Chokepoint Politically Unstable Country With Oil Or Gas Resources

Wildcards

A.T. Kearney 82/06.2006/13154 58

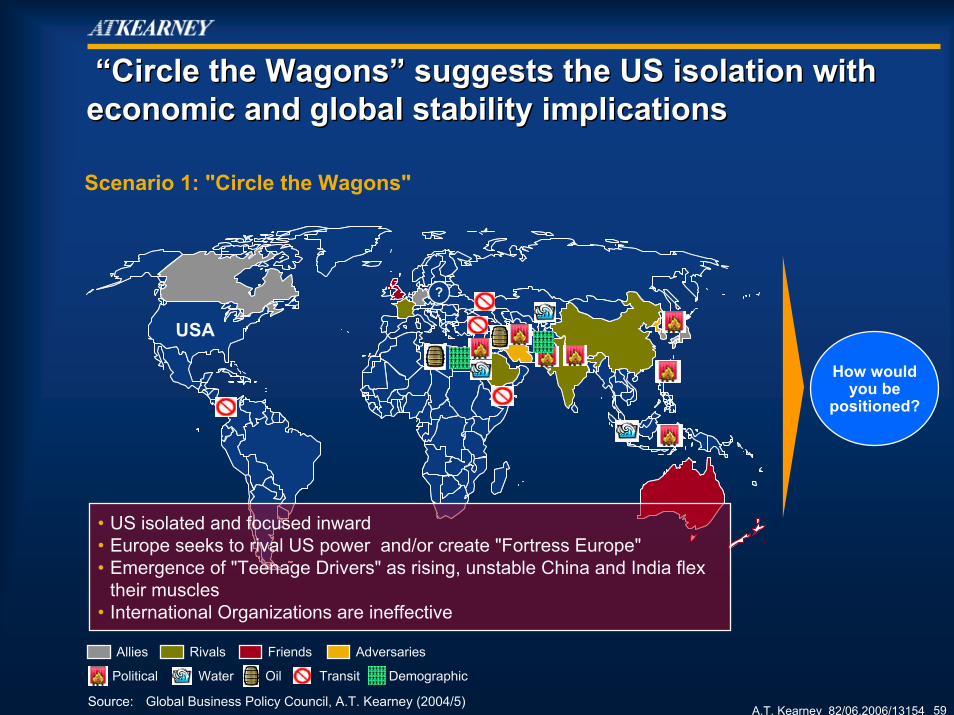

GBPC executives recently reviewed these major forces ― three future scenarios remained but were refinedGBPC executives recently reviewed these major forces ― three future scenarios remained but were refined

New ConsumersGlobalization

Natural Resources &Environment

Demographics

Regulation & Activism

Wildcards

Technology & Innovation

“Circle the Wagons” —suggests the US becomes isolationist

“Patchwork World” — the US remains engaged in world affairs, but with limited friends

“Open Society” —combines multilateral problem solving with global open markets

A.T. Kearney 82/06.2006/13154 59

“Circle the Wagons” suggests the US isolation with economic and global stability implications“Circle the Wagons” suggests the US isolation with economic and global stability implications

USA

Allies Rivals Friends Adversaries

Political DemographicWater Oil Transit

• US isolated and focused inward• Europe seeks to rival US power and/or create "Fortress Europe"• Emergence of "Teenage Drivers" as rising, unstable China and India flex

their muscles• International Organizations are ineffective

How wouldyou be

positioned?

Scenario 1: "Circle the Wagons"

Source: Global Business Policy Council, A.T. Kearney (2004/5)

?

A.T. Kearney 82/06.2006/13154 60

"Patchwork World" considers the US to remain engaged in world affairs, but with limited friends"Patchwork World" considers the US to remain engaged in world affairs, but with limited friends

USA

Allies Rivals Friends Adversaries

Political DemographicWater Oil Transit

• Resembles 2004• US engages on issues of national interest• Mixed EU-US relationship with both cooperation and tensions• Most conflicts remain localized• International Organizations remain active but weak

How wouldyou be

positioned?

Scenario 2: "Patchwork World"

Source: Global Business Policy Council, A.T. Kearney (2004/5)

?

A.T. Kearney 82/06.2006/13154 61

"Open Society" combines multilateral problem solving with global open markets"Open Society" combines multilateral problem solving with global open markets

USA

Allies Rivals Friends Adversaries

Political DemographicWater Oil Transit

• Emphasis on multilateral problem solving• Global problems moderated by action• Resumption of robust global growth and stability• Coalitions counter terror and local conflict

How wouldyou be

positioned?

Scenario 3: "Open Society"

Source: Global Business Policy Council, A.T. Kearney (2004/5)

?

A.T. Kearney 82/06.2006/13154 62

Keys to valueKeys to value

A.T. Kearney 82/06.2006/13154 63

History of A.T. Kearney's Assessment of Excellence in Supply Chain

1992 1996

1992 Leadership Practices In

Procurement Study

Participant Profile:• 25 from North

America

1996 Leadership Practices In

Procurement Study

Participant Profile:• 51 from Europe• 26 from North America

Participant Profile:• 86 from Europe• 40 from North America• 26 from Asia and

Emerging markets• 10 from South America

Participant Profile:• 53 from North

America• 45 from Europe• 31 from South

America• 18 from Asia and

Emerging markets

25 Total Participants77 Total Participants 1999

2002

2004

1999 Assessment of Excellence in

Supply Chain

2002 Assessment of Excellence in

Supply Chain

2004 Assessment of Excellence in

Supply Chain

162 Total Participants

147 Total Participants

300+Total Participants

Participant Profile:• 150+ from Europe• 130+ from N. Amer.• 50+ from Asia-Pacific• 30+ from S. Amer.

SupplierRelationshipManagement

Supply Management

Strategy

Organizational Alignment

StrategicSourcing

OperatingProcess Management

Knowledge/InformationManagementPerformance Management

Human Resources Management

A.T. Kearney conducts proprietary research to understand the practices driving value in supply chainA.T. Kearney conducts proprietary research to understand the practices driving value in supply chain

A.T. Kearney 82/06.2006/13154 64

5.3% 5.0%

8.1%

9.8%

3.6%

2.1%2.9%

1.9%

DirectMaterials

IndirectMaterials

CapitalExpenditure

Services

LeadersFollowers

7.1% 7.3%

3.2%

6.4%

4.7%6.1%

2.0% 1.5%

6.0% 5.8%

1999 2000 2001 2002 2003

Leaders

Industries Average (in which Leaders participate)

Source: A.T. Kearney AESC 2004 Survey

These practices are correlated to differentiated business performanceThese practices are correlated to differentiated business performance

Average Annual Savings Over Past Two Years Net Income Margin (1999 – 2003)

A.T. Kearney 82/06.2006/13154 65

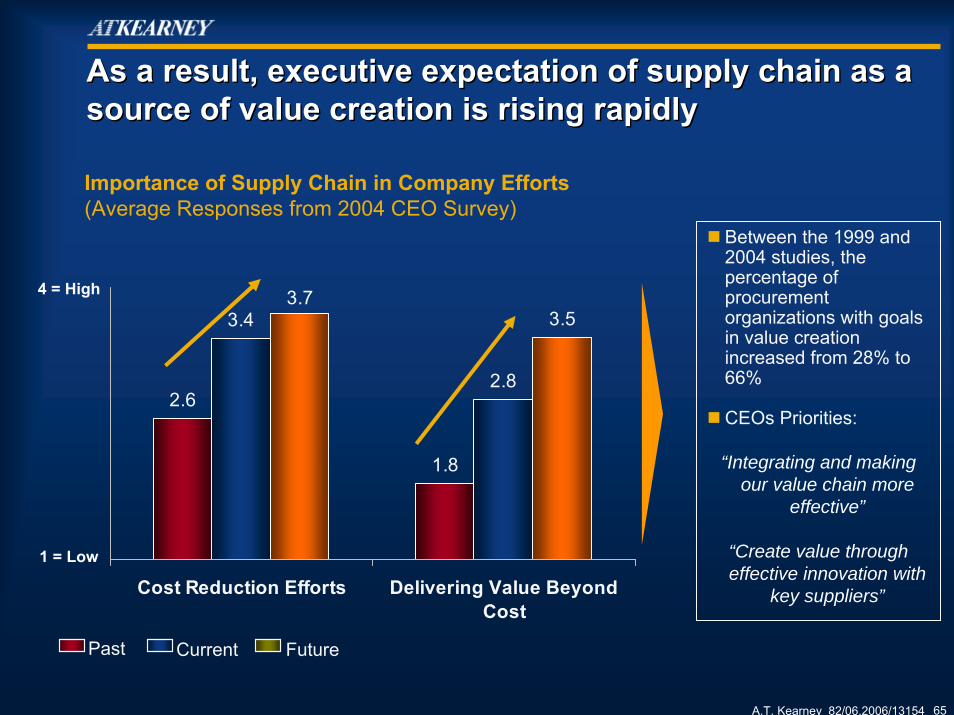

As a result, executive expectation of supply chain as a source of value creation is rising rapidlyAs a result, executive expectation of supply chain as a source of value creation is rising rapidly

1 = Low

4 = High

2.6

1.8

3.4

2.8

3.73.5

Cost Reduction Efforts Delivering Value BeyondCost

Importance of Supply Chain in Company Efforts(Average Responses from 2004 CEO Survey)

Past Current Future

Between the 1999 and 2004 studies, the percentage of procurement organizations with goals in value creation increased from 28% to 66%

CEOs Priorities:

“Integrating and making our value chain more

effective”

“Create value through effective innovation with

key suppliers”

A.T. Kearney 82/06.2006/13154 66

A.T. Kearney has identified four key levers for supply chain value creation A.T. Kearney has identified four key levers for supply chain value creation

Innovation

and Growth

Value C

hain

Optimiza

tion

Advanced

Cost Management

Risk M

anag

emen

t/

Supply Contin

uity

ValueCreation

A.T. Kearney 82/06.2006/13154 67

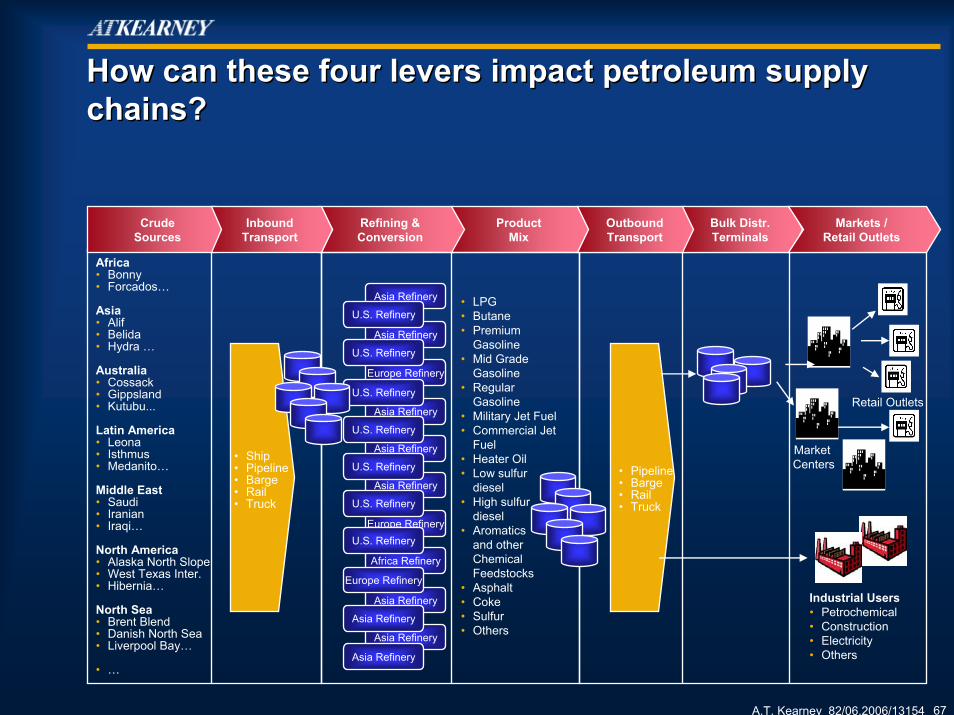

How can these four levers impact petroleum supply chains?How can these four levers impact petroleum supply chains?

Africa• Bonny• Forcados…

Asia• Alif• Belida• Hydra …

Australia• Cossack• Gippsland• Kutubu...

Latin America• Leona• Isthmus• Medanito…

Middle East• Saudi• Iranian• Iraqi…

North America• Alaska North Slope• West Texas Inter.• Hibernia…

North Sea• Brent Blend• Danish North Sea• Liverpool Bay…

• …

Refining & Conversion

Product Mix

OutboundTransport

Bulk Distr.Terminals

Markets /Retail Outlets

Crude Sources

InboundTransport

• LPG• Butane• Premium

Gasoline• Mid Grade

Gasoline• Regular

Gasoline• Military Jet Fuel• Commercial Jet

Fuel• Heater Oil• Low sulfur

diesel• High sulfur

diesel• Aromatics

and other Chemical Feedstocks

• Asphalt• Coke• Sulfur• Others

• Ship• Pipeline• Barge• Rail• Truck

• Pipeline• Barge• Rail• Truck

Market Centers

Industrial Users• Petrochemical• Construction• Electricity• Others

Retail Outlets

Asia Refinery

Asia Refinery

Europe Refinery

Asia Refinery

Asia Refinery

Asia Refinery

Europe Refinery

Africa Refinery

Asia Refinery

Asia Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

U.S. Refinery

Europe Refinery

Asia Refinery

Asia Refinery

A.T. Kearney 82/06.2006/13154 68

Risk management and supply continuity is the largest source of value in petroleum supply chainsRisk management and supply continuity is the largest source of value in petroleum supply chains

Refining & Conversion

Product Mix

OutboundTransport

Bulk Distr.Terminals

Markets /Retail Outlets

Crude Sources

InboundTransport

Ensuring adequate supplies of crude

Developing options for feedstock disruption

Contracting to ensure adequate logistics at each stage

Planning for capacity needs at each level

Meeting product mix requirements to prevent lost sales

Building supply chain scenario models based on global forces and potential outcomes to model risk and identify response strategies

…Innovation

and Growth

Value C

hain

Optimiza

tion

Advanced

Cost Management

Risk M

anag

emen

t/

Supply Contin

uity

ValueCreation

A.T. Kearney 82/06.2006/13154 69

Supply chain can help innovation and growthSupply chain can help innovation and growth

Refining & Conversion

Product Mix

OutboundTransport

Bulk Distr.Terminals

Markets /Retail Outlets

Crude Sources

InboundTransport

Exploring new technologies to upgrade crudes

Investing in and evaluating technologies for alternative fuels

Explicit evaluation of forward and backward integration

Partnering with suppliers that can provide innovation in manufacturing, logistics, technology

Identifying new markets and developing creative solutions for access

Creating market segmentation approaches to identify needs and drive growth

…Innovation

and Growth

Value C

hain

Optimiza

tion

Advanced

Cost Management

Risk M

anag

emen

t/

Supply Contin

uity

ValueCreation

A.T. Kearney 82/06.2006/13154 70

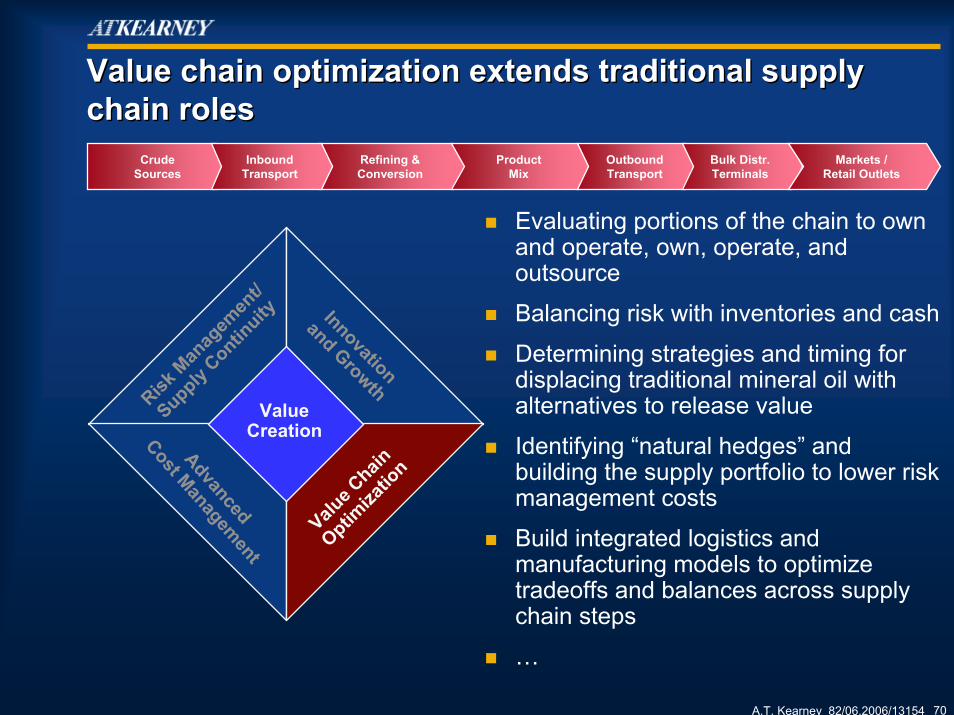

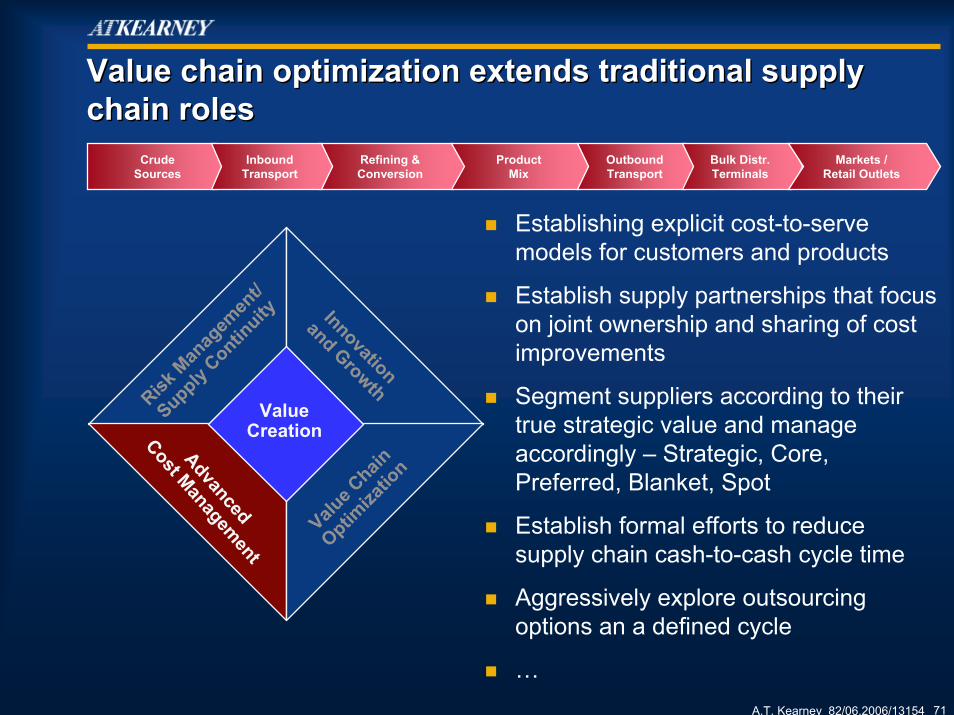

Value chain optimization extends traditional supply chain rolesValue chain optimization extends traditional supply chain roles

Refining & Conversion

Product Mix

OutboundTransport

Bulk Distr.Terminals

Markets /Retail Outlets

Crude Sources

InboundTransport

Evaluating portions of the chain to own and operate, own, operate, and outsource

Balancing risk with inventories and cash

Determining strategies and timing for displacing traditional mineral oil with alternatives to release value

Identifying “natural hedges” and building the supply portfolio to lower risk management costs

Build integrated logistics and manufacturing models to optimize tradeoffs and balances across supply chain steps

…Innovation

and Growth

Value C

hain

Optimiza

tion

Advanced

Cost Management

Risk M

anag

emen

t/

Supply Contin

uity

ValueCreation

A.T. Kearney 82/06.2006/13154 71

Value chain optimization extends traditional supply chain rolesValue chain optimization extends traditional supply chain roles

Refining & Conversion

Product Mix

OutboundTransport

Bulk Distr.Terminals

Markets /Retail Outlets

Crude Sources

InboundTransport

Establishing explicit cost-to-serve models for customers and products

Establish supply partnerships that focus on joint ownership and sharing of cost improvements

Segment suppliers according to their true strategic value and manage accordingly – Strategic, Core, Preferred, Blanket, Spot

Establish formal efforts to reduce supply chain cash-to-cash cycle time

Aggressively explore outsourcing options an a defined cycle

…

Innovation

and Growth

Value C

hain

Optimiza

tion

Advanced

Cost Management

Risk M

anag

emen

t/

Supply Contin

uity

ValueCreation

A.T. Kearney 82/06.2006/13154 72

In summary…In summary…

A.T. Kearney 82/06.2006/13154 73

Hydrocarbon supply chains must anticipate and adapt to the coming change Hydrocarbon supply chains must anticipate and adapt to the coming change

Over the last 20 years, refiners consolidated inefficient and excess capacity and are beginning to make gains in business returns

These returns can rapidly evaporate if supply chains fail to deliver feedstock, materials, labor and sales product to customers

Enormous amounts of infrastructure and capital are invested in the fixed asset base — particularly in the US

These investments are at risk from changing conditions• Crude quality• Shifting demographic and economic centers — China and India• Potentially disruptive technologies• Increasing “visible hand” of governments

Petroleum supply chains that employ leading practices can anticipate these changes, capture additional value and thrive well into the future

Houston, Texas

June 7, 2006

Preparing for Global Change in the Petroleum Supply Chain

Preparing for Global Change in the Preparing for Global Change in the Petroleum Supply ChainPetroleum Supply Chain

University of Nevada/COPPEAD Petroleum Executive Logistics Course

![GLOBAL SUPPLY CHAIN MANAGEMENT [Author] [Institution] › portfolio › Global Supply Cha… · GLOBAL SUPPLY CHAIN MANAGEMENT [Author] [Institution] GLOBAL SUPPLY CHAIN MANAGEMENT](https://static.fdocuments.us/doc/165x107/5f0434ae7e708231d40cd5e9/global-supply-chain-management-author-institution-a-portfolio-a-global-supply.jpg)