Massachusetts’ Competitive Position in Life Sciences ... Files/MA_LifeSciences_Summit_2003... ·...

50

Massachusetts’ Competitive Position in Life Sciences: Where Do We Stand? Professor Michael E. Porter Institute for Strategy and Competitiveness Harvard Business School Massachusetts Life Sciences Summit 12 September 2003 This presentation is composed of excerpts from reports and presentations created by the Boston Consulting Group, Professor Alan Clayton- Matthews, the Howell Group of Boston, the Massachusetts Biotechnology Council, MassMedic, the Massachusetts Medical Device Industry Council, the Massachusetts Technology Collaborative, the Milken Institute, the Monitor Company Group, Professor Michael E. Porter and the New England Healthcare Institute. See Sources.

Transcript of Massachusetts’ Competitive Position in Life Sciences ... Files/MA_LifeSciences_Summit_2003... ·...

Massachusetts’ Competitive Position in Life Sciences:Where Do We Stand?

Professor Michael E. PorterInstitute for Strategy and Competitiveness

Harvard Business School

Massachusetts Life Sciences Summit12 September 2003

This presentation is composed of excerpts from reports and presentations created by the Boston Consulting Group, Professor Alan Clayton-Matthews, the Howell Group of Boston, the Massachusetts Biotechnology Council, MassMedic, the Massachusetts Medical Device Industry Council, the Massachusetts Technology Collaborative, the Milken Institute, the Monitor Company Group, Professor Michael E. Porter and the New England Healthcare Institute. See Sources.

2LSConsolidated-20030806 2003 Life Sciences Summit

Situation Facing Massachusetts

Massachusetts is one of the world’s leading centers in Life Sciences, but the State is facing a crowded and increasingly competitive field

The Life Sciences cluster encompasses a wide range of products and services, including medical devices, pharmaceutical products, research and testing, and health care delivery

Massachusetts has a rich set of institutions in the field, but each tends to be narrowly focused on one aspect of the cluster

There has been no overarching strategy for the cluster and no structure to develop one

3LSConsolidated-20030806 2003 Life Sciences Summit

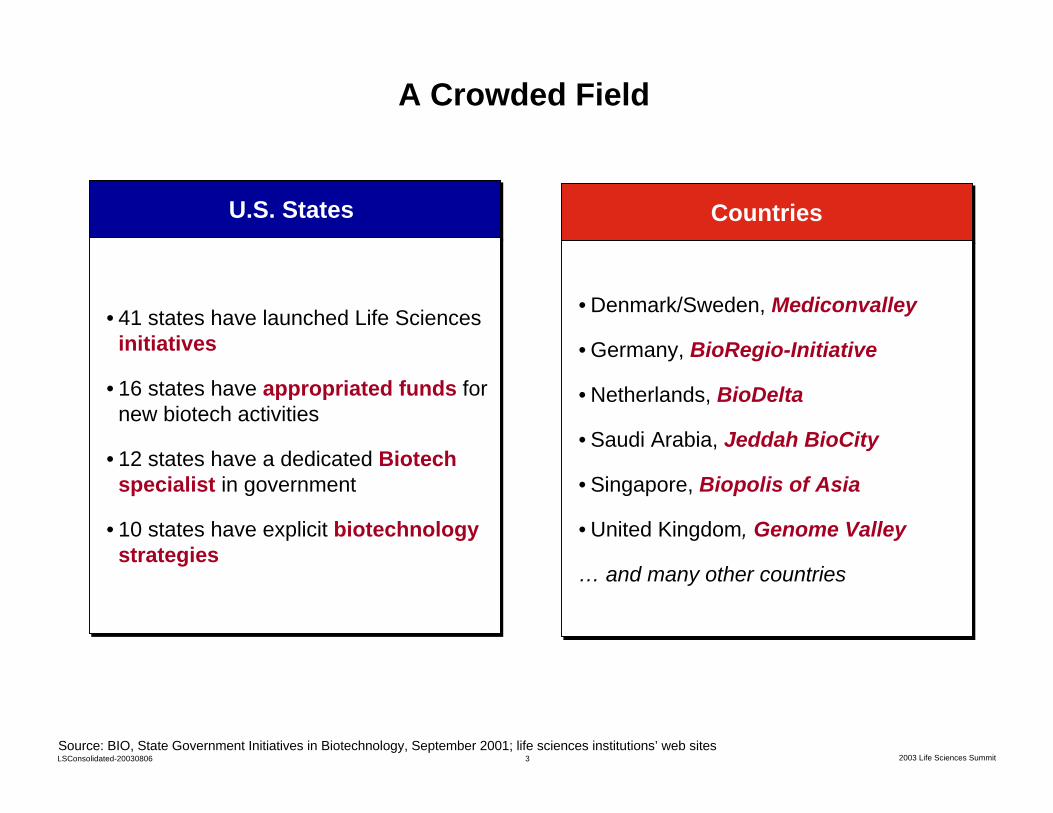

A Crowded Field

Source: BIO, State Government Initiatives in Biotechnology, September 2001; life sciences institutions’ web sites

U.S. States U.S. States

• 41 states have launched Life Sciences initiatives

• 16 states have appropriated funds for new biotech activities

• 12 states have a dedicated Biotech specialist in government

• 10 states have explicit biotechnology strategies

• 41 states have launched Life Sciences initiatives

• 16 states have appropriated funds for new biotech activities

• 12 states have a dedicated Biotech specialist in government

• 10 states have explicit biotechnology strategies

CountriesCountries

• Denmark/Sweden, Mediconvalley

• Germany, BioRegio-Initiative

• Netherlands, BioDelta

• Saudi Arabia, Jeddah BioCity

• Singapore, Biopolis of Asia

• United Kingdom, Genome Valley

… and many other countries

• Denmark/Sweden, Mediconvalley

• Germany, BioRegio-Initiative

• Netherlands, BioDelta

• Saudi Arabia, Jeddah BioCity

• Singapore, Biopolis of Asia

• United Kingdom, Genome Valley

… and many other countries

4LSConsolidated-20030806 2003 Life Sciences Summit

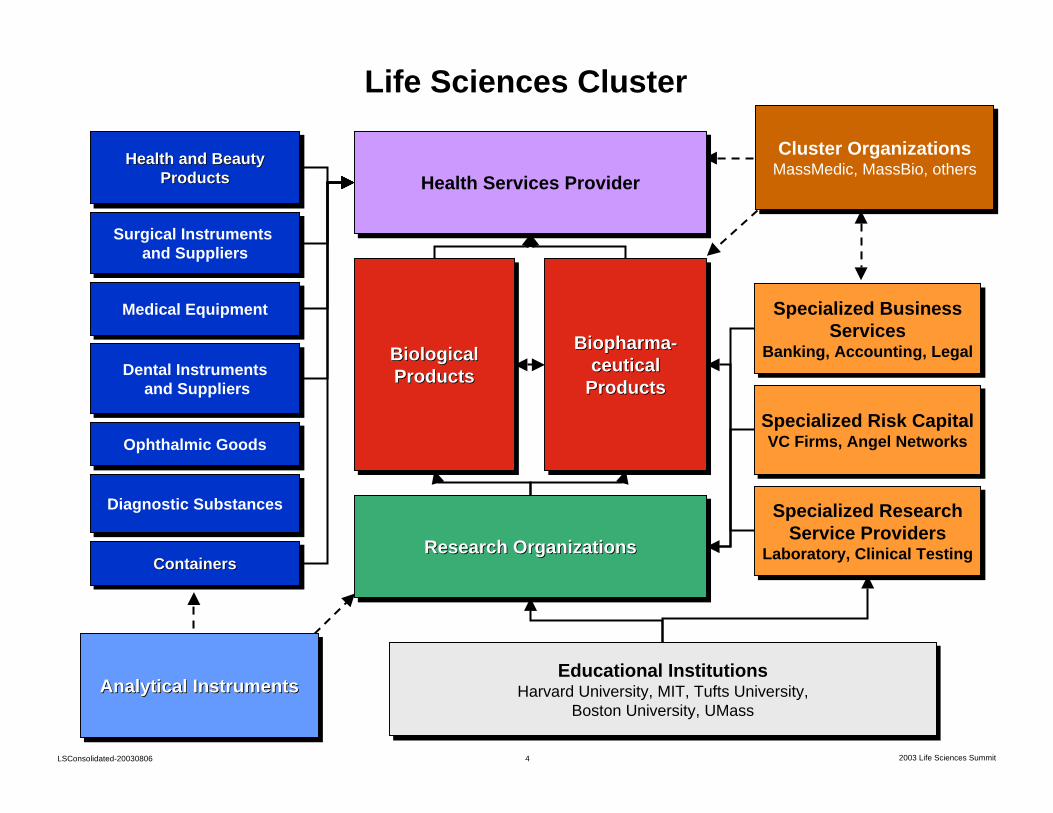

Life Sciences Cluster

Research OrganizationsResearch OrganizationsResearch Organizations

Biological Products

Biological Biological ProductsProducts

Specialized Risk CapitalVC Firms, Angel Networks

Specialized Risk CapitalVC Firms, Angel Networks

Biopharma-ceutical

Products

BiopharmaBiopharma--ceutical ceutical

ProductsProducts

Specialized BusinessServices

Banking, Accounting, Legal

Specialized BusinessServices

Banking, Accounting, Legal

Specialized ResearchService Providers

Laboratory, Clinical Testing

Specialized ResearchService Providers

Laboratory, Clinical Testing

Dental Instrumentsand Suppliers

Dental Instrumentsand Suppliers

Surgical Instruments and Suppliers

Surgical Instruments and Suppliers

Diagnostic SubstancesDiagnostic Substances

ContainersContainersContainers

Medical EquipmentMedical Equipment

Ophthalmic GoodsOphthalmic Goods

Health and Beauty Products

Health and Beauty Health and Beauty ProductsProducts Health Services ProviderHealth Services Provider

Educational InstitutionsHarvard University, MIT, Tufts University,

Boston University, UMass

Educational InstitutionsHarvard University, MIT, Tufts University,

Boston University, UMass

Cluster OrganizationsMassMedic, MassBio, othersCluster Organizations

MassMedic, MassBio, others

Analytical InstrumentsAnalytical InstrumentsAnalytical Instruments

5LSConsolidated-20030806 2003 Life Sciences Summit

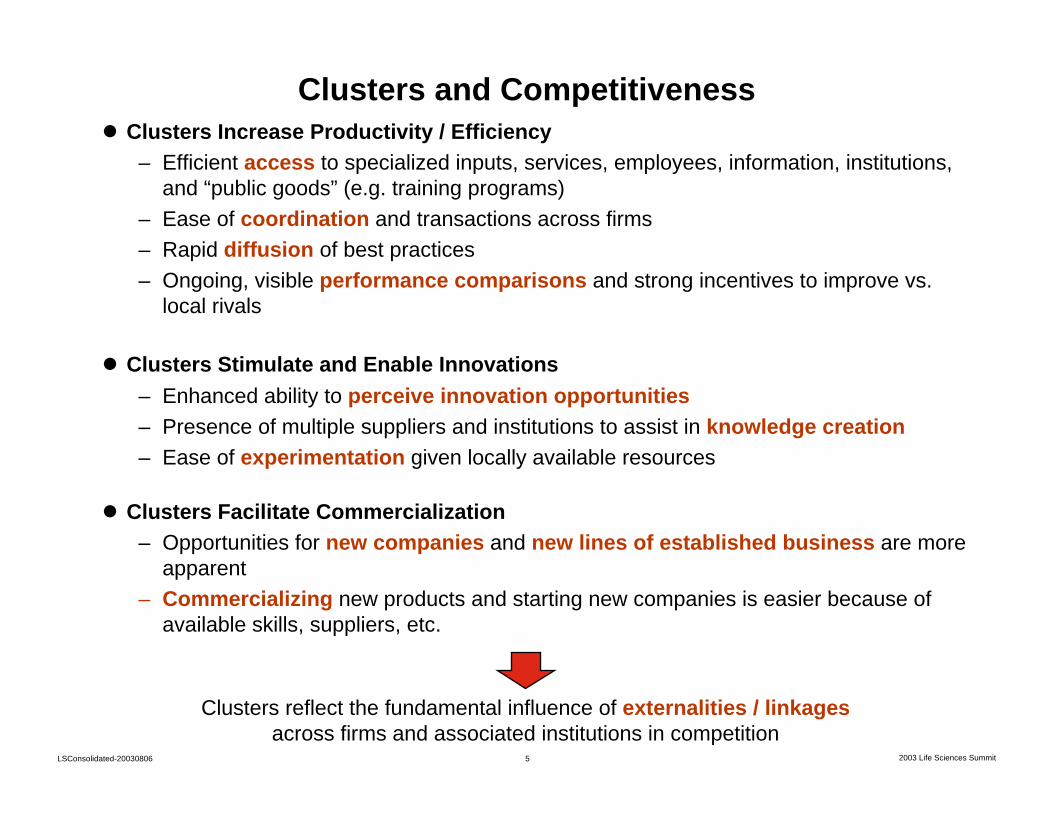

Clusters and CompetitivenessClusters Increase Productivity / Efficiency

– Efficient access to specialized inputs, services, employees, information, institutions, and “public goods” (e.g. training programs)

– Ease of coordination and transactions across firms– Rapid diffusion of best practices– Ongoing, visible performance comparisons and strong incentives to improve vs.

local rivals

Clusters Stimulate and Enable Innovations– Enhanced ability to perceive innovation opportunities– Presence of multiple suppliers and institutions to assist in knowledge creation– Ease of experimentation given locally available resources

Clusters Facilitate Commercialization– Opportunities for new companies and new lines of established business are more

apparent– Commercializing new products and starting new companies is easier because of

available skills, suppliers, etc.

Clusters reflect the fundamental influence of externalities / linkagesacross firms and associated institutions in competition

6LSConsolidated-20030806 2003 Life Sciences Summit

Institutions for CollaborationSelected Massachusetts Organizations

Economic Development InitiativesEconomic Development Initiatives

Massachusetts Technology CollaborativeMass Biomedical InitiativesMass DevelopmentMassachusetts Alliance for Economic Development

Massachusetts Technology CollaborativeMass Biomedical InitiativesMass DevelopmentMassachusetts Alliance for Economic Development

Life Sciences Industry AssociationsLife Sciences Industry Associations

Massachusetts Biotechnology CouncilMassachusetts Medical Device Industry CouncilMassachusetts Hospital Association

Massachusetts Biotechnology CouncilMassachusetts Medical Device Industry CouncilMassachusetts Hospital Association

General Industry AssociationsGeneral Industry Associations

Associated Industries of MassachusettsGreater Boston Chamber of CommerceHigh Tech Council of Massachusetts

Associated Industries of MassachusettsGreater Boston Chamber of CommerceHigh Tech Council of Massachusetts

University InitiativesUniversity Initiatives

Harvard Biomedical CommunityMIT Enterprise ForumBiotech Club at Harvard Medical SchoolTechnology Transfer offices

Harvard Biomedical CommunityMIT Enterprise ForumBiotech Club at Harvard Medical SchoolTechnology Transfer offices

Informal networksInformal networks

Company alumniVC communityUniversity alumni

Company alumniVC communityUniversity alumni

Joint Research InitiativesJoint Research Initiatives

New England Healthcare InstituteWhitehead Institute For Biomedical ResearchCenter for Integration of Medicine and Innovative Technology (CIMIT)

New England Healthcare InstituteWhitehead Institute For Biomedical ResearchCenter for Integration of Medicine and Innovative Technology (CIMIT)

7LSConsolidated-20030806 2003 Life Sciences Summit

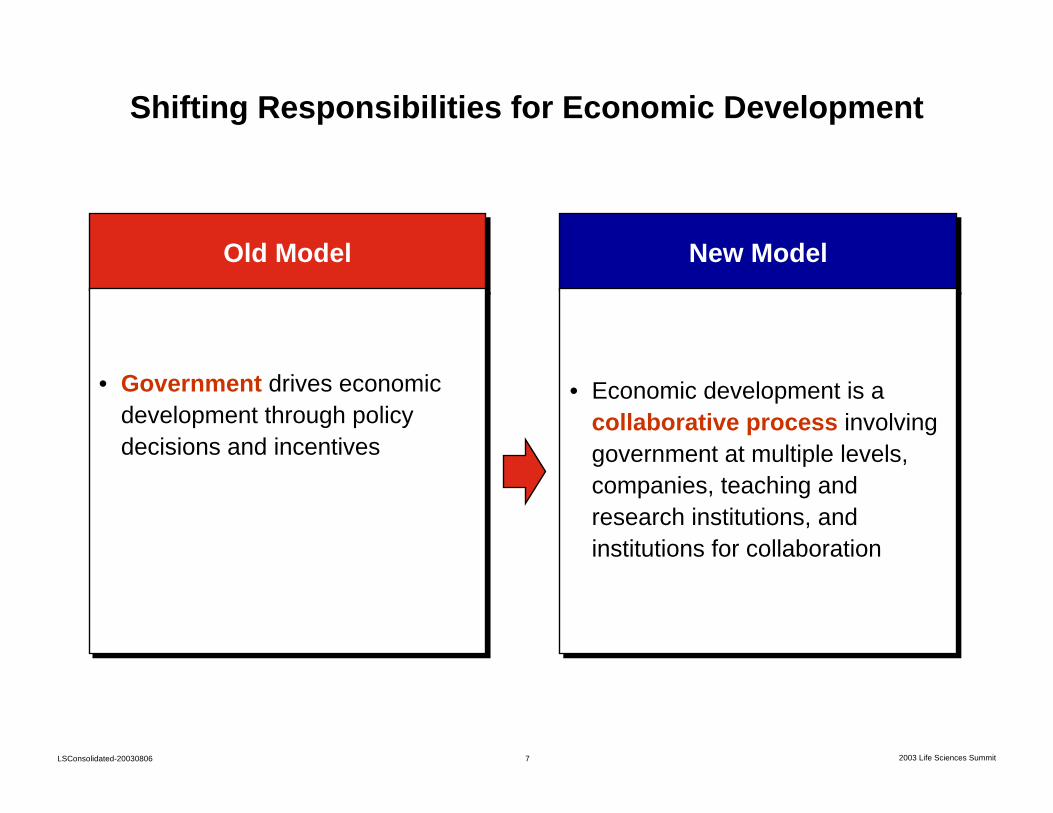

Shifting Responsibilities for Economic Development

Old ModelOld Model

• Government drives economic development through policy decisions and incentives

• Government drives economic development through policy decisions and incentives

New ModelNew Model

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

• Economic development is a collaborative process involving government at multiple levels, companies, teaching and research institutions, and institutions for collaboration

8LSConsolidated-20030806 2003 Life Sciences Summit

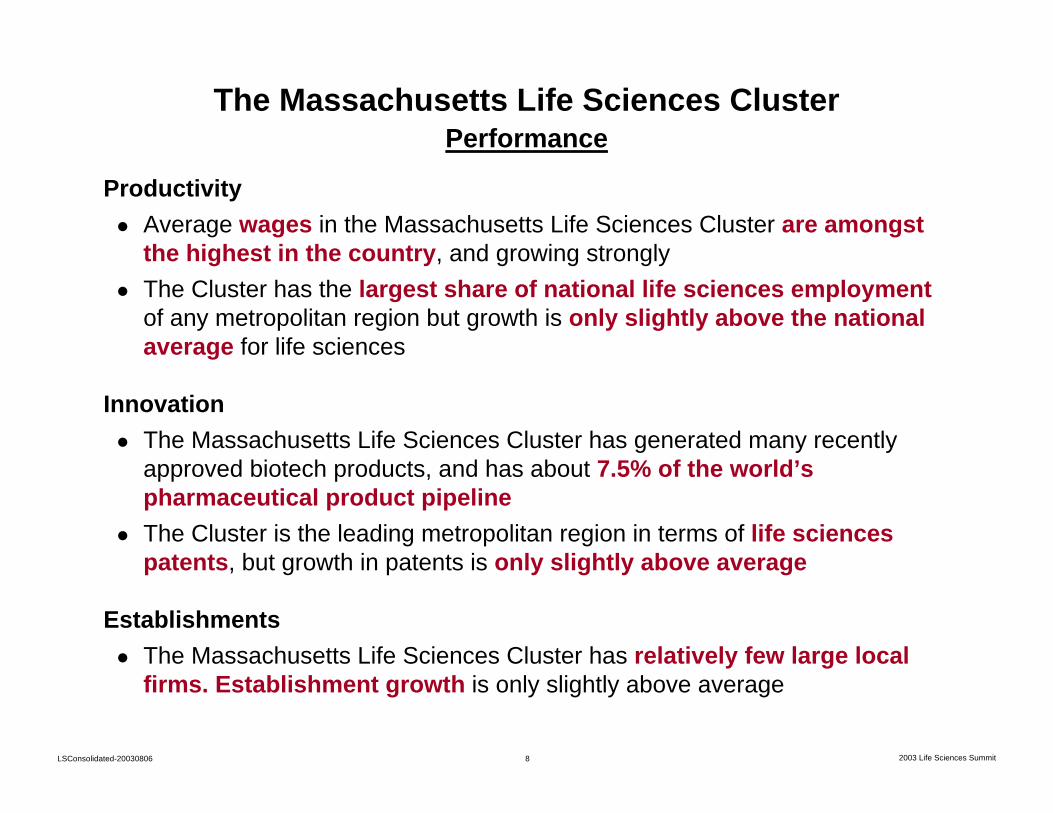

The Massachusetts Life Sciences ClusterPerformance

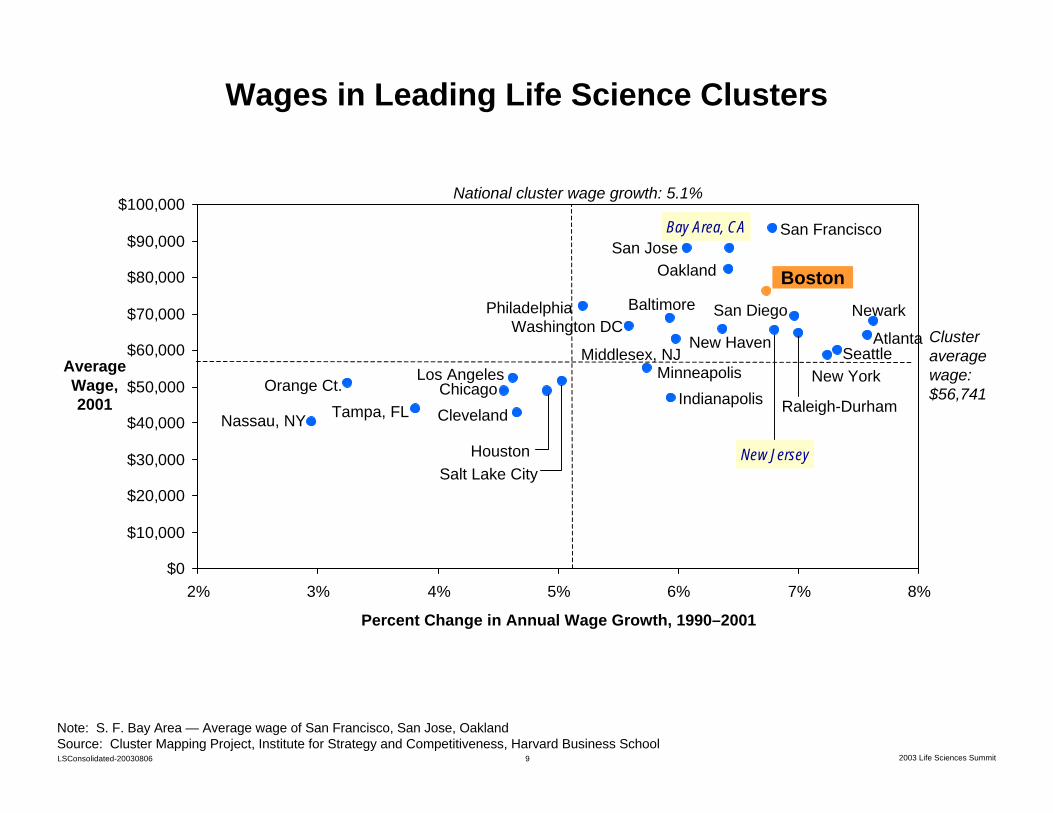

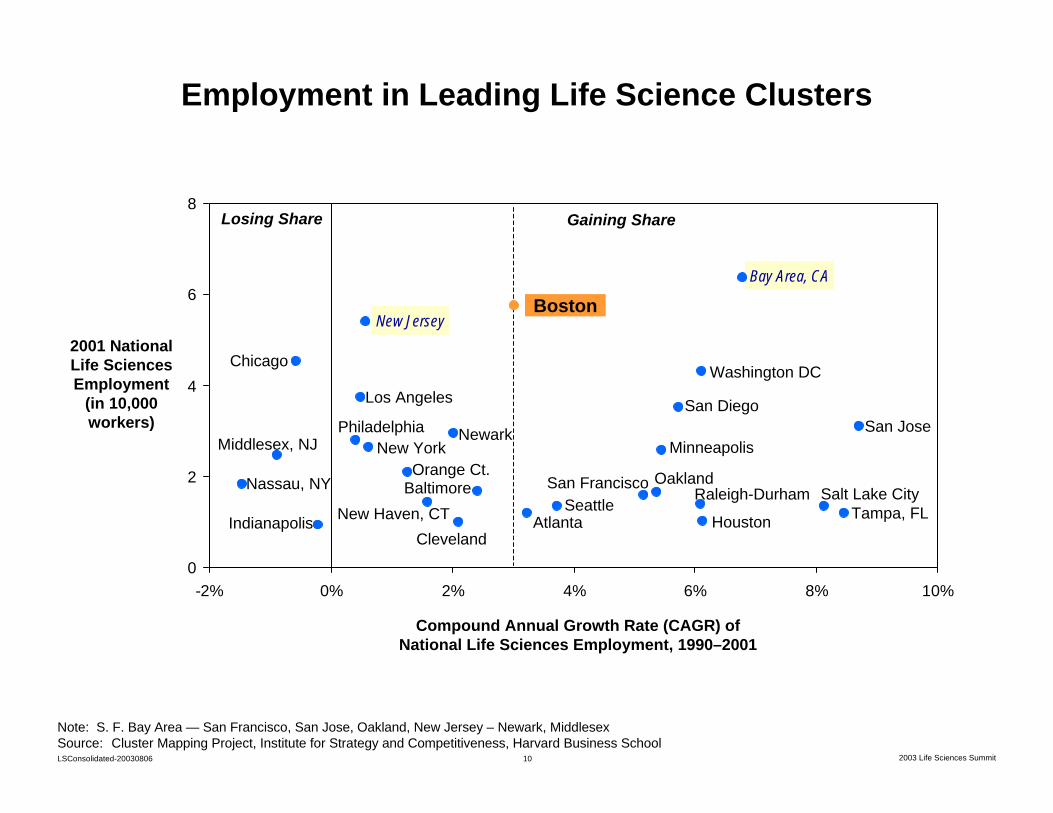

ProductivityAverage wages in the Massachusetts Life Sciences Cluster are amongst the highest in the country, and growing stronglyThe Cluster has the largest share of national life sciences employmentof any metropolitan region but growth is only slightly above the national average for life sciences

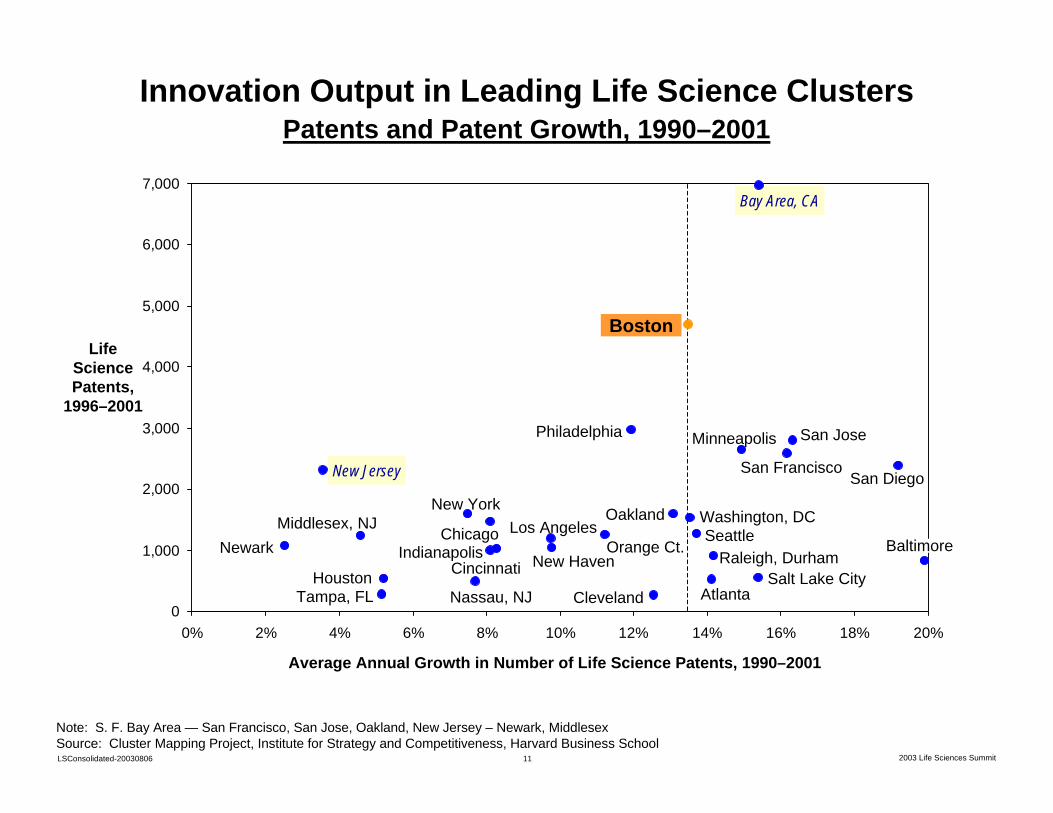

InnovationThe Massachusetts Life Sciences Cluster has generated many recently approved biotech products, and has about 7.5% of the world’s pharmaceutical product pipelineThe Cluster is the leading metropolitan region in terms of life sciences patents, but growth in patents is only slightly above average

EstablishmentsThe Massachusetts Life Sciences Cluster has relatively few large local firms. Establishment growth is only slightly above average

9LSConsolidated-20030806 2003 Life Sciences Summit

Bay Area, CA

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

2% 3% 4% 5% 6% 7% 8%

Average Wage, 2001

Note: S. F. Bay Area — Average wage of San Francisco, San Jose, OaklandSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

Percent Change in Annual Wage Growth, 1990–2001

Nassau, NY

Orange Ct. ChicagoLos Angeles

Salt Lake City

Minneapolis

BaltimorePhiladelphia

New Haven

Raleigh-Durham

Washington DC

New York

Oakland

Middlesex, NJ

San Jose

San Diego

Seattle

San Francisco

Newark

Boston

Atlanta

Houston

IndianapolisTampa, FL Cleveland

Cluster average wage: $56,741

National cluster wage growth: 5.1%

Wages in Leading Life Science Clusters

New Jersey

10LSConsolidated-20030806 2003 Life Sciences Summit

Bay Area, CA

New Jersey

0

2

4

6

8

-2% 0% 2% 4% 6% 8% 10%

Employment in Leading Life Science Clusters

2001 NationalLife Sciences Employment

(in 10,000 workers)

Note: S. F. Bay Area — San Francisco, San Jose, Oakland, New Jersey – Newark, MiddlesexSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

Compound Annual Growth Rate (CAGR) of National Life Sciences Employment, 1990–2001

Losing Share Gaining Share

Middlesex, NJ

Nassau, NY

Chicago

Los Angeles

PhiladelphiaNew York

Orange Ct.Baltimore

New Haven, CT

OaklandSalt Lake City

San Jose

Raleigh-Durham

Washington DC

San Diego

San Francisco

NewarkMinneapolis

SeattleIndianapolis Tampa, FLHouston

ClevelandAtlanta

Boston

11LSConsolidated-20030806 2003 Life Sciences Summit

Bay Area, CA

New Jersey

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0% 2% 4% 6% 8% 10% 12% 14% 16% 18% 20%

Innovation Output in Leading Life Science ClustersPatents and Patent Growth, 1990–2001

Los Angeles

Life Science Patents,

1996–2001

Average Annual Growth in Number of Life Science Patents, 1990–2001

ChicagoWashington, DC

San Diego

Newark

New York

Minneapolis San JosePhiladelphia

Orange Ct.Middlesex, NJ

Nassau, NJ

San Francisco

New Haven

Oakland

Salt Lake City

SeattleRaleigh, Durham

Note: S. F. Bay Area — San Francisco, San Jose, Oakland, New Jersey – Newark, MiddlesexSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

HoustonAtlanta

IndianapolisCincinnati

Tampa, FL Cleveland

Boston

Baltimore

12LSConsolidated-20030806 2003 Life Sciences Summit

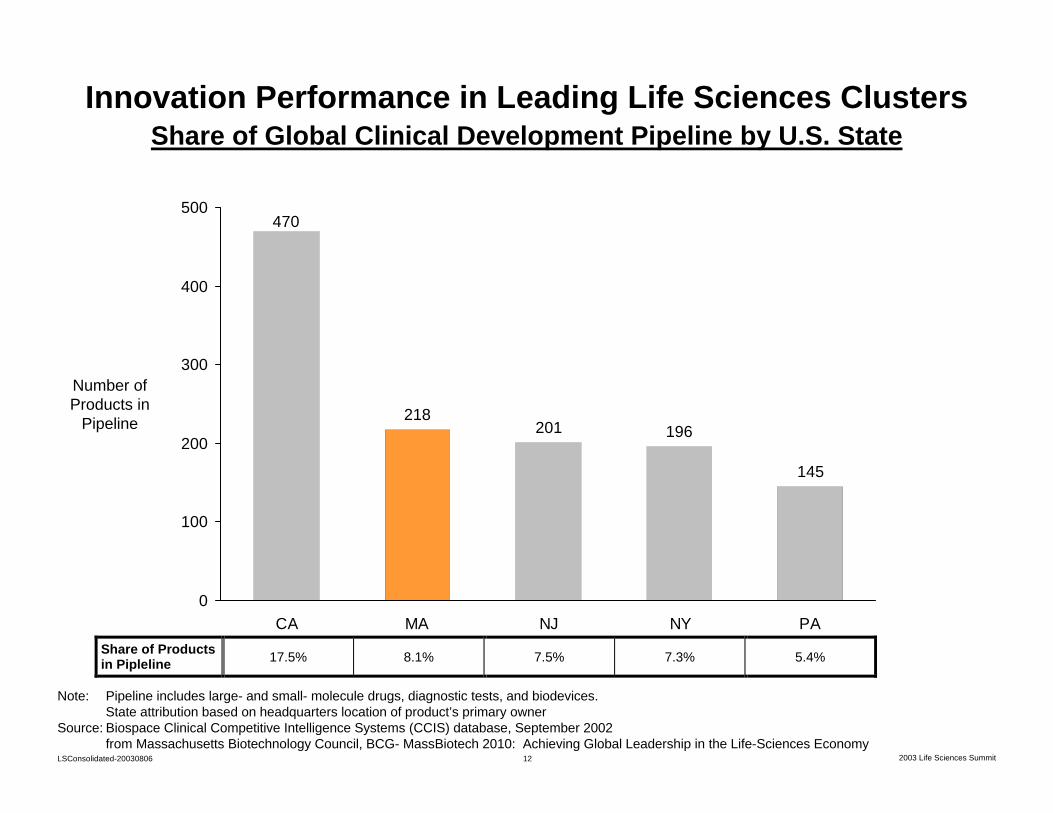

218201 196

145

470

0

100

200

300

400

500

CA MA NJ NY PA

Innovation Performance in Leading Life Sciences Clusters Share of Global Clinical Development Pipeline by U.S. State

Number of Products in

Pipeline

Note: Pipeline includes large- and small- molecule drugs, diagnostic tests, and biodevices. State attribution based on headquarters location of product’s primary owner

Source: Biospace Clinical Competitive Intelligence Systems (CCIS) database, September 2002from Massachusetts Biotechnology Council, BCG- MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy

Share of Products in Pipleline 17.5% 8.1% 7.5% 7.3% 5.4%

13LSConsolidated-20030806 2003 Life Sciences Summit

Relative Performance

Competitive Assessment

Strategic Issues

Massachusetts' Competitive Position in Life Sciences

14LSConsolidated-20030806 2003 Life Sciences Summit

Assessing Life Sciences CompetitivenessSources of Data

Findings from recent studies of the cluster:– The Economic Contributions of Health Care to New England, New England

Healthcare Institute, Milken Institute, 2003– Massachusetts Life Sciences Data, Massachusetts Technology Collaborative,

2003– MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy,

Massachusetts Biotechnology Council, Boston Consulting Group, 2003– The Medical Device Industry in Massachusetts, Alan Clayton-Matthews,

MassMedic, Massachusetts Medical Device Industry Council, 2001

Survey of 250 Massachusetts’ companies, 50+ from the Life Sciences– Conducted by Monitor Company

125+ in-depth interviews with cluster leaders– Conducted by Monitor Group and the Boston Consulting Group

Analysis of regional and cluster data from the Institute for Strategy and Competitiveness at Harvard

15LSConsolidated-20030806 2003 Life Sciences Summit

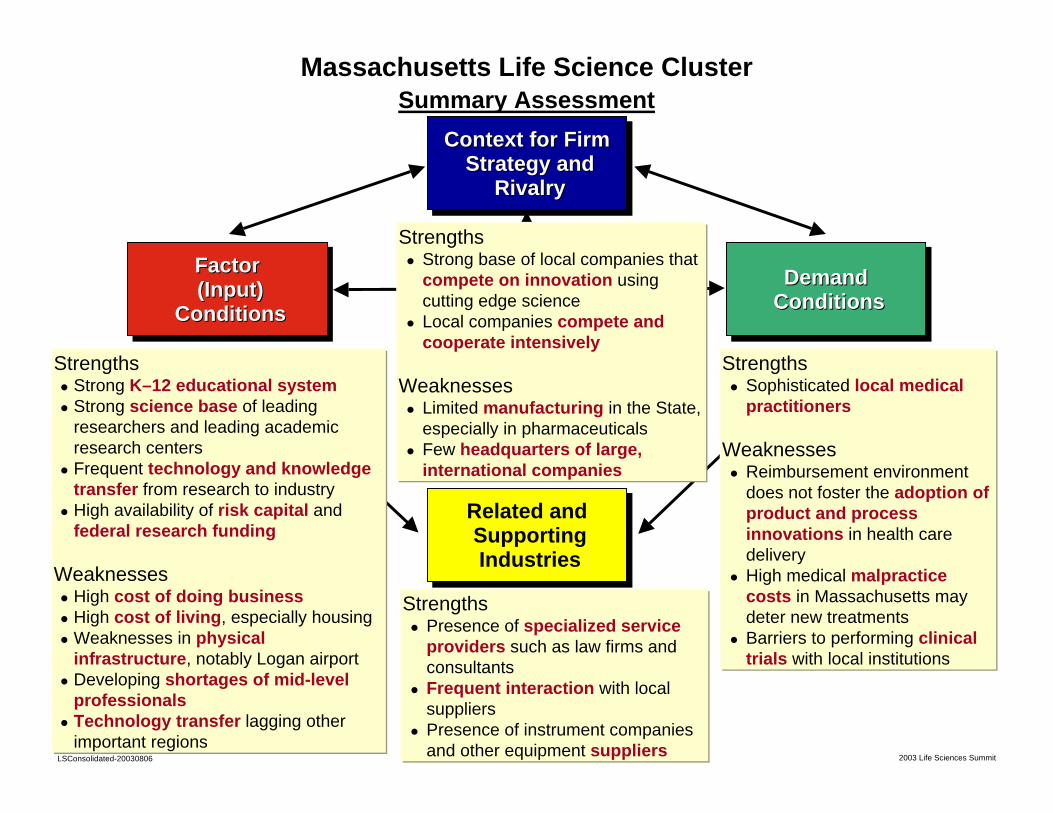

Massachusetts Life Science ClusterSummary Assessment

Demand ConditionsDemand Demand

ConditionsConditionsFactor(Input)

Conditions

FactorFactor(Input)(Input)

ConditionsConditions

Context for Firm Strategy and

Rivalry

Context for Firm Context for Firm Strategy and Strategy and

RivalryRivalry

Related and Supporting Industries

Related and Supporting Industries

StrengthsStrong base of local companies that compete on innovation using cutting edge scienceLocal companies compete and cooperate intensively

WeaknessesLimited manufacturing in the State, especially in pharmaceuticalsFew headquarters of large, international companies

StrengthsSophisticated local medical practitioners

WeaknessesReimbursement environment does not foster the adoption of product and process innovations in health care deliveryHigh medical malpractice costs in Massachusetts may deter new treatmentsBarriers to performing clinical trials with local institutions

StrengthsPresence of specialized service providers such as law firms and consultantsFrequent interaction with local suppliersPresence of instrument companies and other equipment suppliers

StrengthsStrong K–12 educational systemStrong science base of leading researchers and leading academic research centersFrequent technology and knowledge transfer from research to industryHigh availability of risk capital and federal research funding

WeaknessesHigh cost of doing businessHigh cost of living, especially housingWeaknesses in physical infrastructure, notably Logan airportDeveloping shortages of mid-level professionalsTechnology transfer lagging other important regions

16LSConsolidated-20030806 2003 Life Sciences Summit

Demand ConditionsDemand Demand

ConditionsConditionsFactor(Input)

Conditions

FactorFactor(Input)(Input)

ConditionsConditions

Context for Firm Strategy and

Rivalry

Context for Firm Context for Firm Strategy and Strategy and

RivalryRivalry

Related and Supporting Industries

Related and Supporting Industries

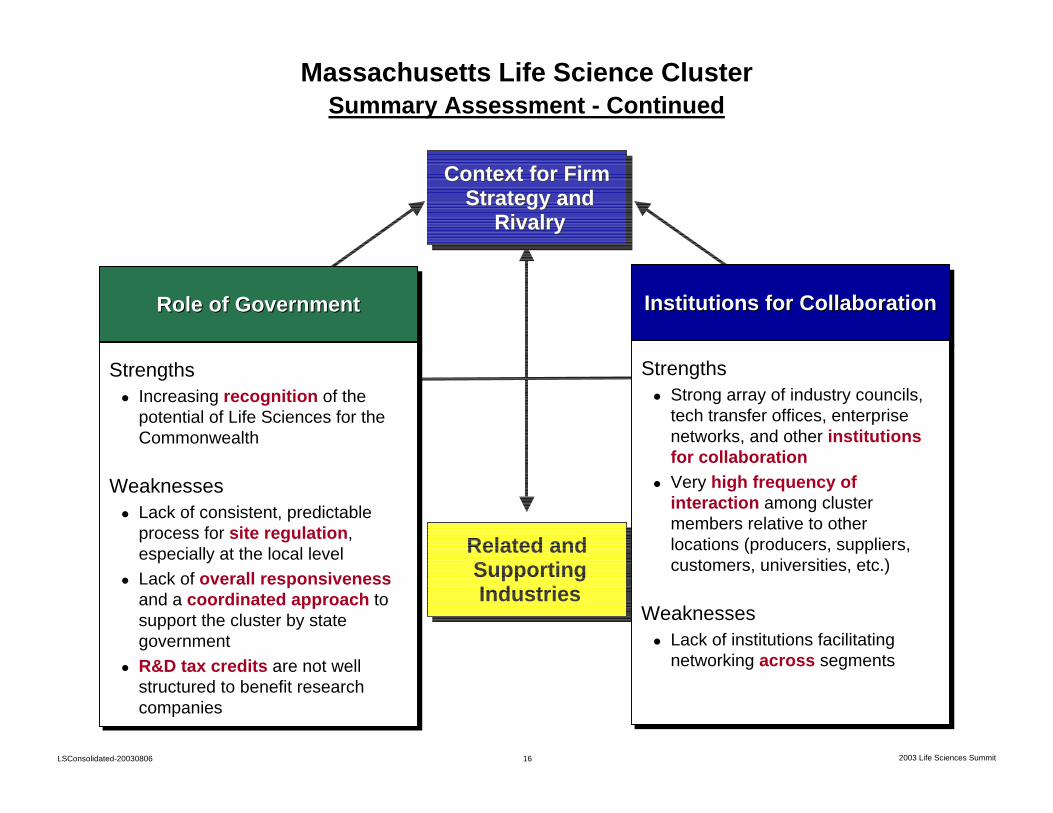

Massachusetts Life Science ClusterSummary Assessment - Continued

Role of GovernmentRole of GovernmentRole of Government

StrengthsIncreasing recognition of the potential of Life Sciences for the Commonwealth

WeaknessesLack of consistent, predictable process for site regulation, especially at the local levelLack of overall responsivenessand a coordinated approach to support the cluster by state government R&D tax credits are not well structured to benefit research companies

StrengthsIncreasing recognition of the potential of Life Sciences for the Commonwealth

WeaknessesLack of consistent, predictable process for site regulation, especially at the local levelLack of overall responsivenessand a coordinated approach to support the cluster by state government R&D tax credits are not well structured to benefit research companies

Institutions for CollaborationInstitutions for CollaborationInstitutions for Collaboration

StrengthsStrong array of industry councils, tech transfer offices, enterprise networks, and other institutions for collaborationVery high frequency of interaction among cluster members relative to other locations (producers, suppliers, customers, universities, etc.)

WeaknessesLack of institutions facilitating networking across segments

StrengthsStrong array of industry councils, tech transfer offices, enterprise networks, and other institutions for collaborationVery high frequency of interaction among cluster members relative to other locations (producers, suppliers, customers, universities, etc.)

WeaknessesLack of institutions facilitating networking across segments

17LSConsolidated-20030806 2003 Life Sciences Summit

New Jersey

Bay Area, CA

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

0% 10% 20% 30% 40% 50% 60%

Note: S. F. Bay Area — San Francisco, San Jose, Oakland, New Jersey – Newark, MiddlesexSource: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

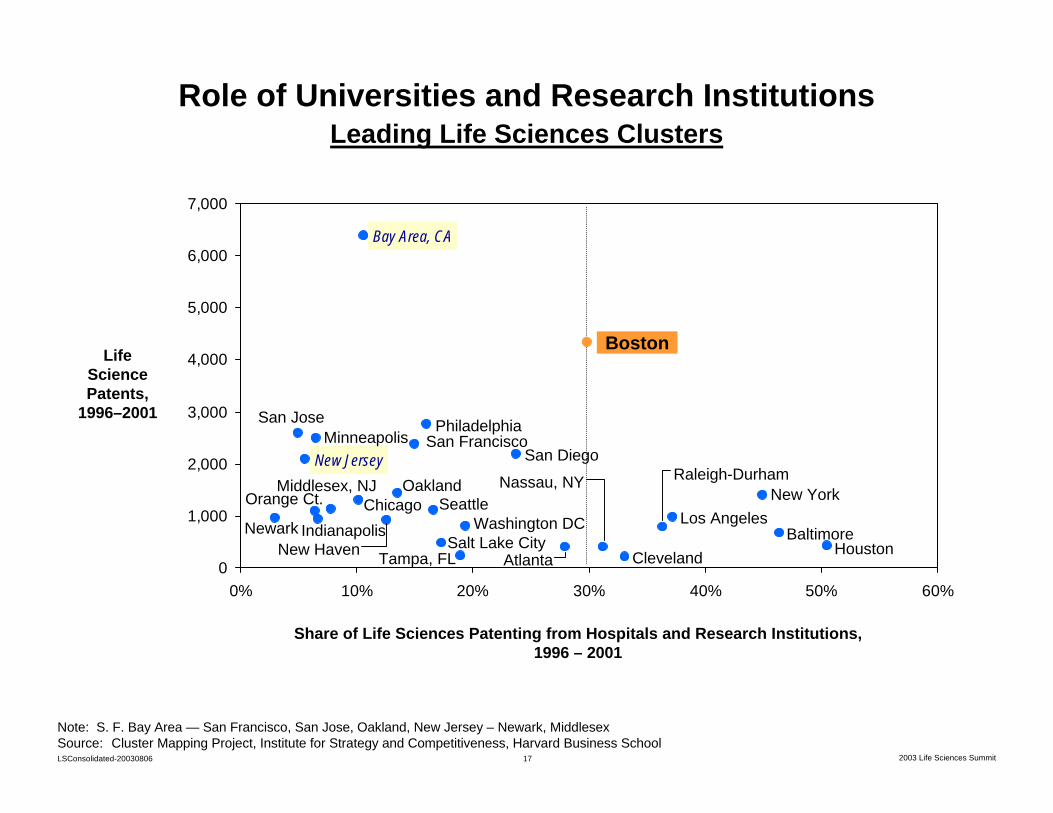

Share of Life Sciences Patenting from Hospitals and Research Institutions, 1996 – 2001

ChicagoLos Angeles

Philadelphia

New York

Washington DC

San DiegoMinneapolis

Boston

Role of Universities and Research InstitutionsLeading Life Sciences Clusters

Life Science Patents,

1996–2001

BaltimoreHoustonCleveland

Raleigh-DurhamOrange Ct.

IndianapolisNew Haven

Seattle

Salt Lake CityTampa, FL

Nassau, NY

Atlanta

Middlesex, NJ Oakland

San JoseSan Francisco

Newark

18LSConsolidated-20030806 2003 Life Sciences Summit

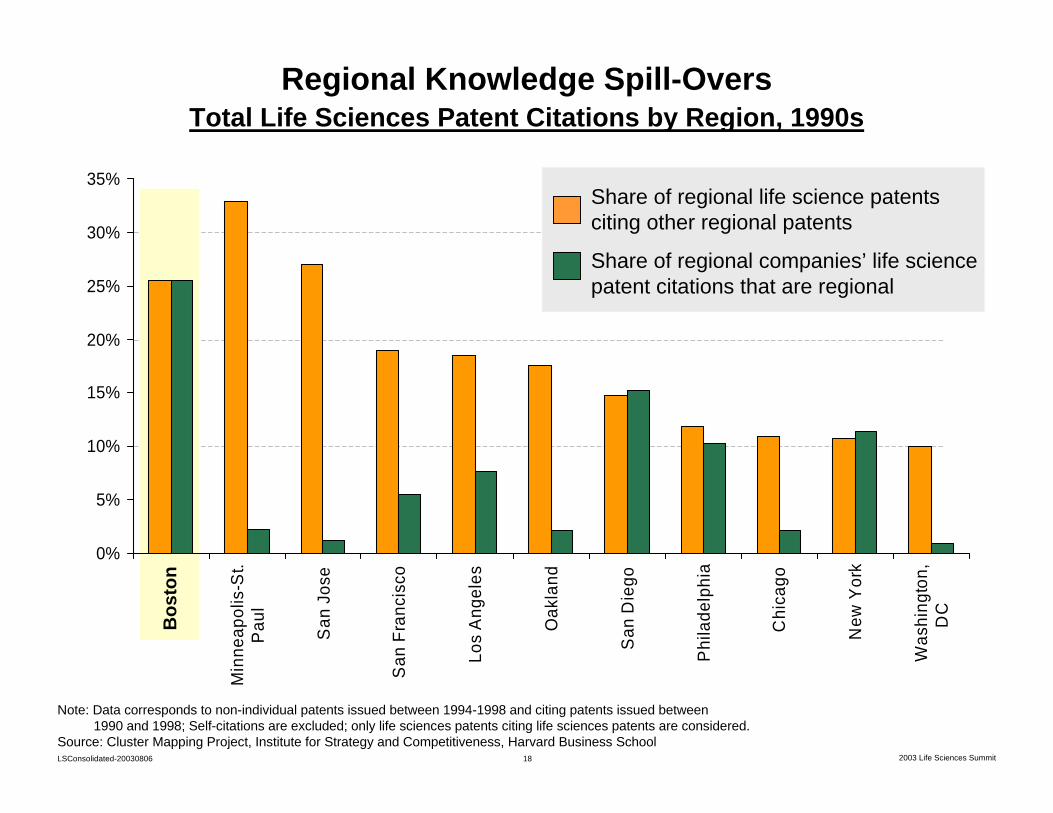

Regional Knowledge Spill-OversTotal Life Sciences Patent Citations by Region, 1990s

0%

5%

10%

15%

20%

25%

30%

35%

Min

neap

olis

-St.

Pau

l

San

Jos

e

San

Fra

ncis

co

Los

Ang

eles

Oak

land

San

Die

go

Phi

lade

lphi

a

Chi

cago

New

Yor

k

Was

hing

ton,

DC

Note: Data corresponds to non-individual patents issued between 1994-1998 and citing patents issued between 1990 and 1998; Self-citations are excluded; only life sciences patents citing life sciences patents are considered.

Source: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

Share of regional life science patents citing other regional patents

Share of regional companies’ life science patent citations that are regional

Bos

ton

19LSConsolidated-20030806 2003 Life Sciences Summit

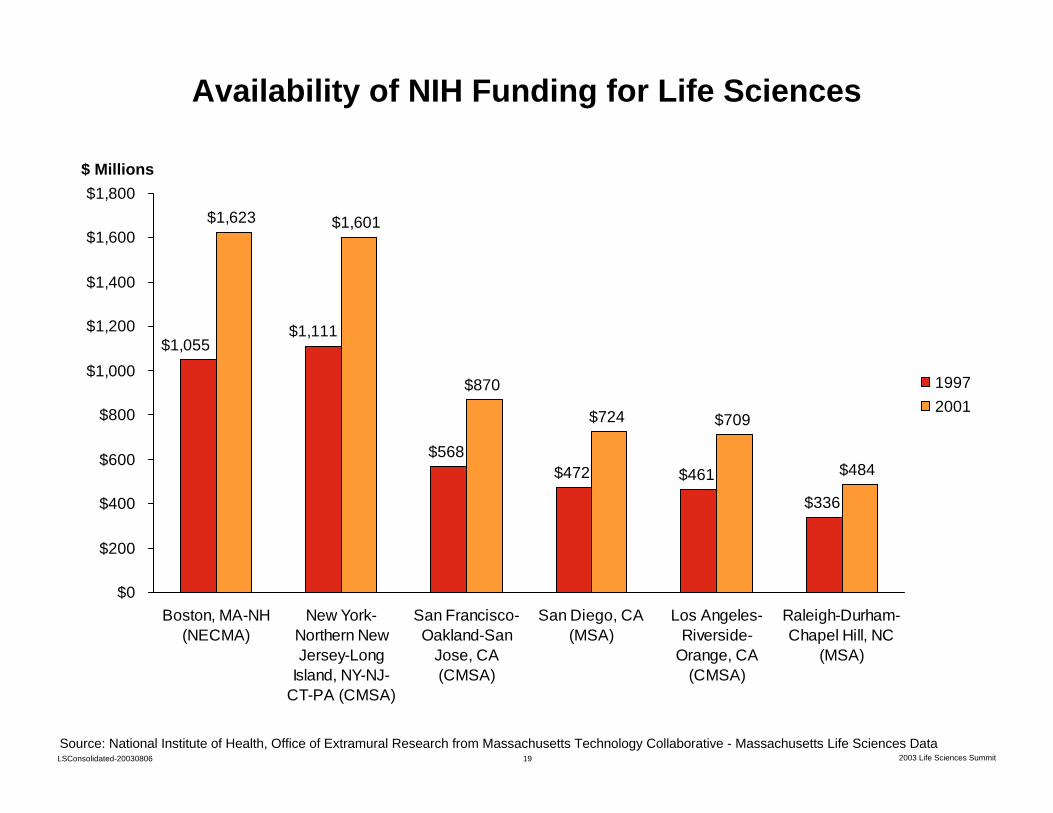

Availability of NIH Funding for Life Sciences

Source: National Institute of Health, Office of Extramural Research from Massachusetts Technology Collaborative - Massachusetts Life Sciences Data

$568$472 $461

$336

$1,623 $1,601

$870

$724 $709

$484

$1,111$1,055

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

Boston, MA-NH(NECMA)

New York-Northern NewJersey-Long

Island, NY-NJ-CT-PA (CMSA)

San Francisco-Oakland-San

Jose, CA(CMSA)

San Diego, CA(MSA)

Los Angeles-Riverside-

Orange, CA(CMSA)

Raleigh-Durham-Chapel Hill, NC

(MSA)

19972001

$ Millions

20LSConsolidated-20030806 2003 Life Sciences Summit

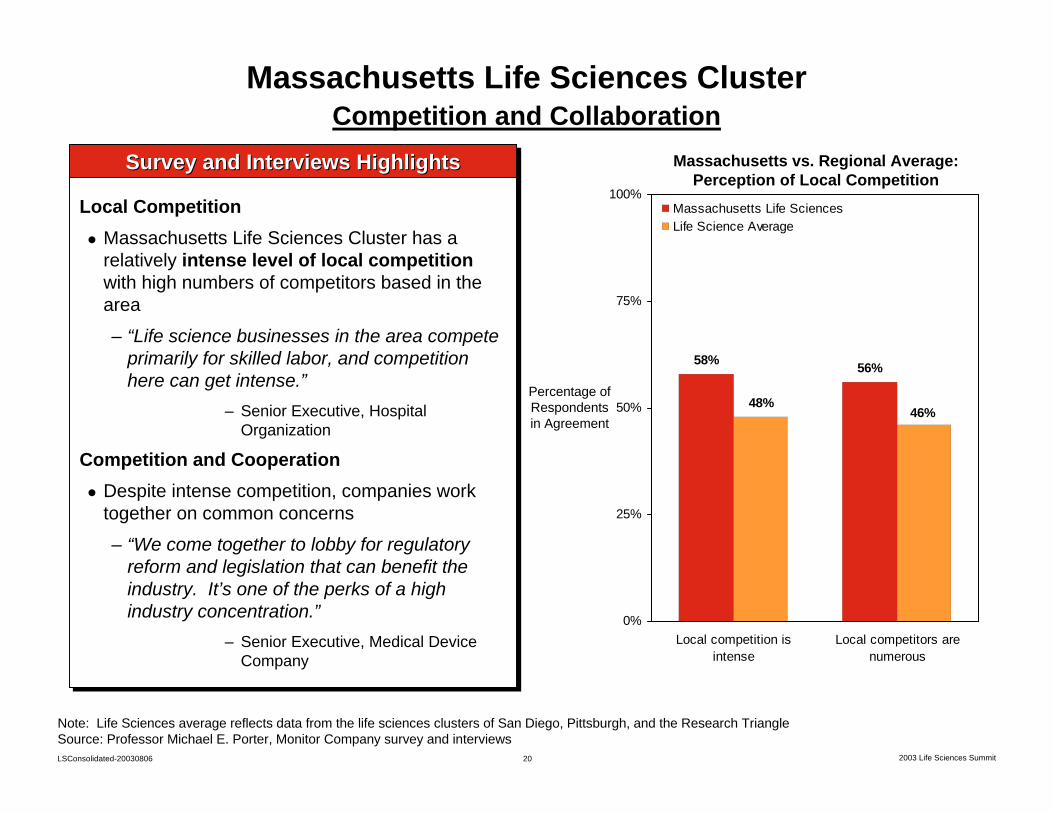

Massachusetts Life Sciences ClusterCompetition and Collaboration

Massachusetts vs. Regional Average: Perception of Local Competition

Survey and Interviews HighlightsSurvey and Interviews HighlightsSurvey and Interviews Highlights

Local CompetitionMassachusetts Life Sciences Cluster has a relatively intense level of local competition with high numbers of competitors based in the area– “Life science businesses in the area compete

primarily for skilled labor, and competition here can get intense.”

– Senior Executive, Hospital Organization

Competition and CooperationDespite intense competition, companies work together on common concerns– “We come together to lobby for regulatory

reform and legislation that can benefit the industry. It’s one of the perks of a high industry concentration.”

– Senior Executive, Medical Device Company

Local CompetitionMassachusetts Life Sciences Cluster has a relatively intense level of local competition with high numbers of competitors based in the area– “Life science businesses in the area compete

primarily for skilled labor, and competition here can get intense.”

– Senior Executive, Hospital Organization

Competition and CooperationDespite intense competition, companies work together on common concerns– “We come together to lobby for regulatory

reform and legislation that can benefit the industry. It’s one of the perks of a high industry concentration.”

– Senior Executive, Medical Device Company

Percentage of Respondents in Agreement

58% 56%

48%46%

0%

25%

50%

75%

100%

Local competition isintense

Local competitors arenumerous

Massachusetts Life SciencesLife Science Average

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter, Monitor Company survey and interviews

21LSConsolidated-20030806 2003 Life Sciences Summit

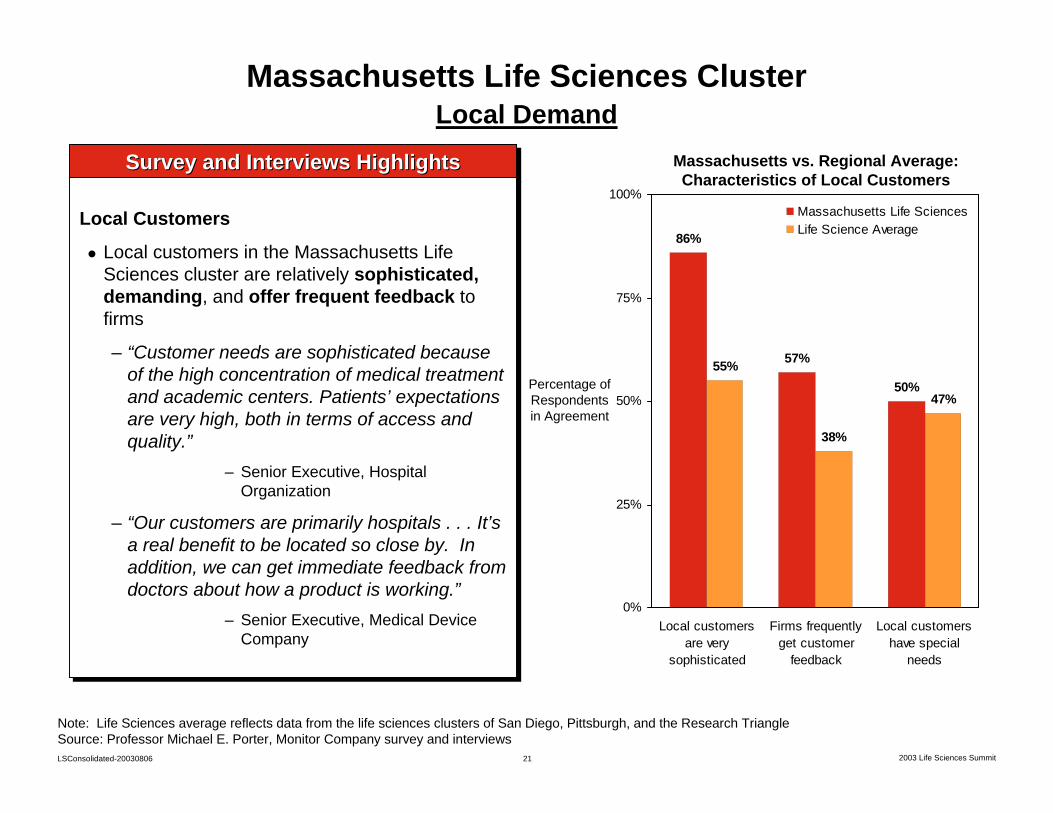

Massachusetts vs. Regional Average: Characteristics of Local Customers

Massachusetts Life Sciences ClusterLocal Demand

Survey and Interviews HighlightsSurvey and Interviews HighlightsSurvey and Interviews Highlights

Local Customers

Local customers in the Massachusetts Life Sciences cluster are relatively sophisticated, demanding, and offer frequent feedback to firms

– “Customer needs are sophisticated because of the high concentration of medical treatment and academic centers. Patients’ expectations are very high, both in terms of access and quality.”

– Senior Executive, Hospital Organization

– “Our customers are primarily hospitals . . . It’s a real benefit to be located so close by. In addition, we can get immediate feedback from doctors about how a product is working.”

– Senior Executive, Medical Device Company

Local Customers

Local customers in the Massachusetts Life Sciences cluster are relatively sophisticated, demanding, and offer frequent feedback to firms

– “Customer needs are sophisticated because of the high concentration of medical treatment and academic centers. Patients’ expectations are very high, both in terms of access and quality.”

– Senior Executive, Hospital Organization

– “Our customers are primarily hospitals . . . It’s a real benefit to be located so close by. In addition, we can get immediate feedback from doctors about how a product is working.”

– Senior Executive, Medical Device Company

Percentage of Respondents in Agreement

86%

57%

50%55%

38%

47%

0%

25%

50%

75%

100%

Local customersare very

sophisticated

Firms frequentlyget customer

feedback

Local customershave special

needs

Massachusetts Life SciencesLife Science Average

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter, Monitor Company survey and interviews

22LSConsolidated-20030806 2003 Life Sciences Summit

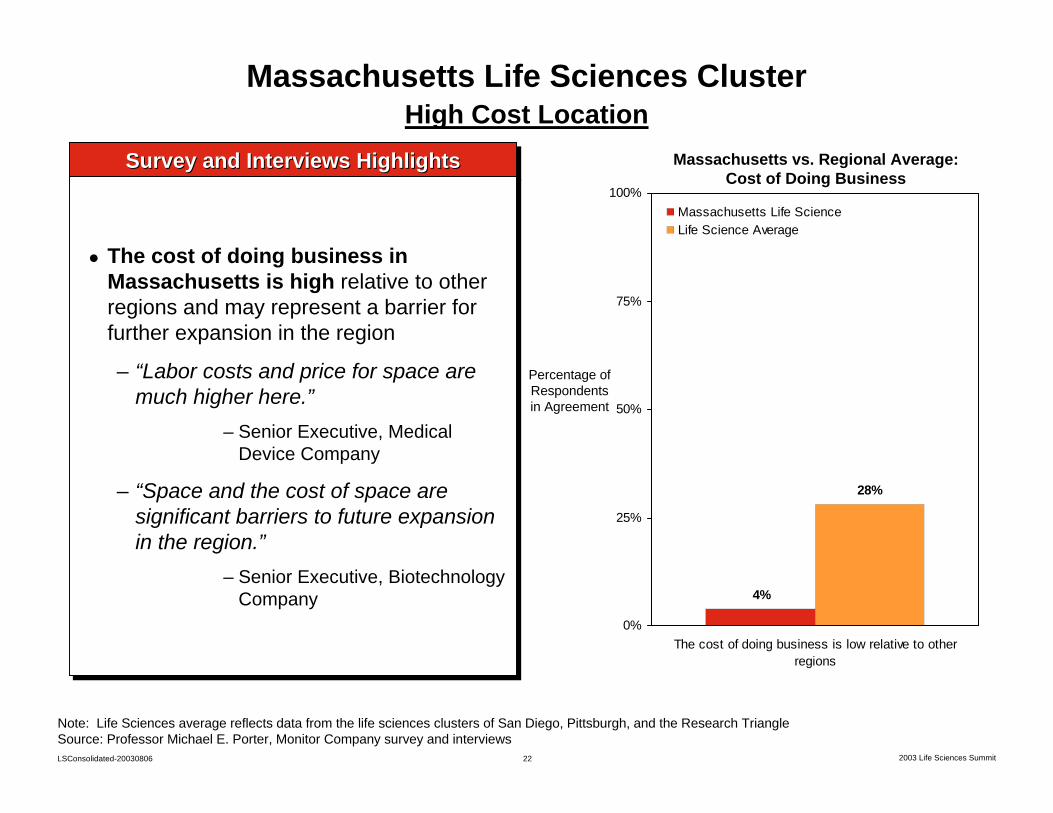

Massachusetts Life Sciences ClusterHigh Cost Location

Survey and Interviews HighlightsSurvey and Interviews HighlightsSurvey and Interviews Highlights

The cost of doing business in Massachusetts is high relative to other regions and may represent a barrier for further expansion in the region

– “Labor costs and price for space are much higher here.”

– Senior Executive, Medical Device Company

– “Space and the cost of space are significant barriers to future expansion in the region.”

– Senior Executive, Biotechnology Company

The cost of doing business in Massachusetts is high relative to other regions and may represent a barrier for further expansion in the region

– “Labor costs and price for space are much higher here.”

– Senior Executive, Medical Device Company

– “Space and the cost of space are significant barriers to future expansion in the region.”

– Senior Executive, Biotechnology Company

Massachusetts vs. Regional Average: Cost of Doing Business

4%

28%

0%

25%

50%

75%

100%

The cost of doing business is low relative to otherregions

Massachusetts Life ScienceLife Science Average

Percentage of Respondents in Agreement

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter, Monitor Company survey and interviews

23LSConsolidated-20030806 2003 Life Sciences Summit

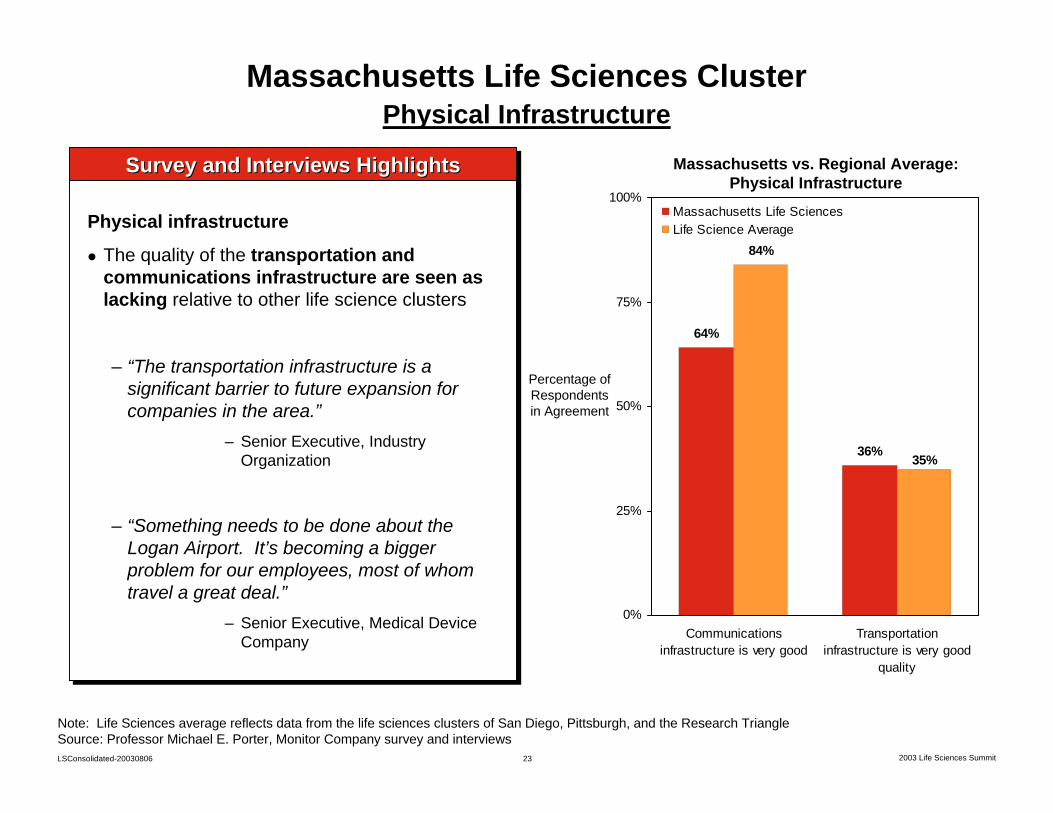

Massachusetts vs. Regional Average: Physical Infrastructure

Survey and Interviews HighlightsSurvey and Interviews HighlightsSurvey and Interviews Highlights

Physical infrastructure

The quality of the transportation and communications infrastructure are seen as lacking relative to other life science clusters

– “The transportation infrastructure is a significant barrier to future expansion for companies in the area.”

– Senior Executive, Industry Organization

– “Something needs to be done about the Logan Airport. It’s becoming a bigger problem for our employees, most of whom travel a great deal.”

– Senior Executive, Medical Device Company

Physical infrastructure

The quality of the transportation and communications infrastructure are seen as lacking relative to other life science clusters

– “The transportation infrastructure is a significant barrier to future expansion for companies in the area.”

– Senior Executive, Industry Organization

– “Something needs to be done about the Logan Airport. It’s becoming a bigger problem for our employees, most of whom travel a great deal.”

– Senior Executive, Medical Device Company

Massachusetts Life Sciences ClusterPhysical Infrastructure

Percentage of Respondents in Agreement

64%

36%

84%

35%

0%

25%

50%

75%

100%

Communicationsinfrastructure is very good

Transportationinfrastructure is very good

quality

Massachusetts Life SciencesLife Science Average

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter, Monitor Company survey and interviews

24LSConsolidated-20030806 2003 Life Sciences Summit

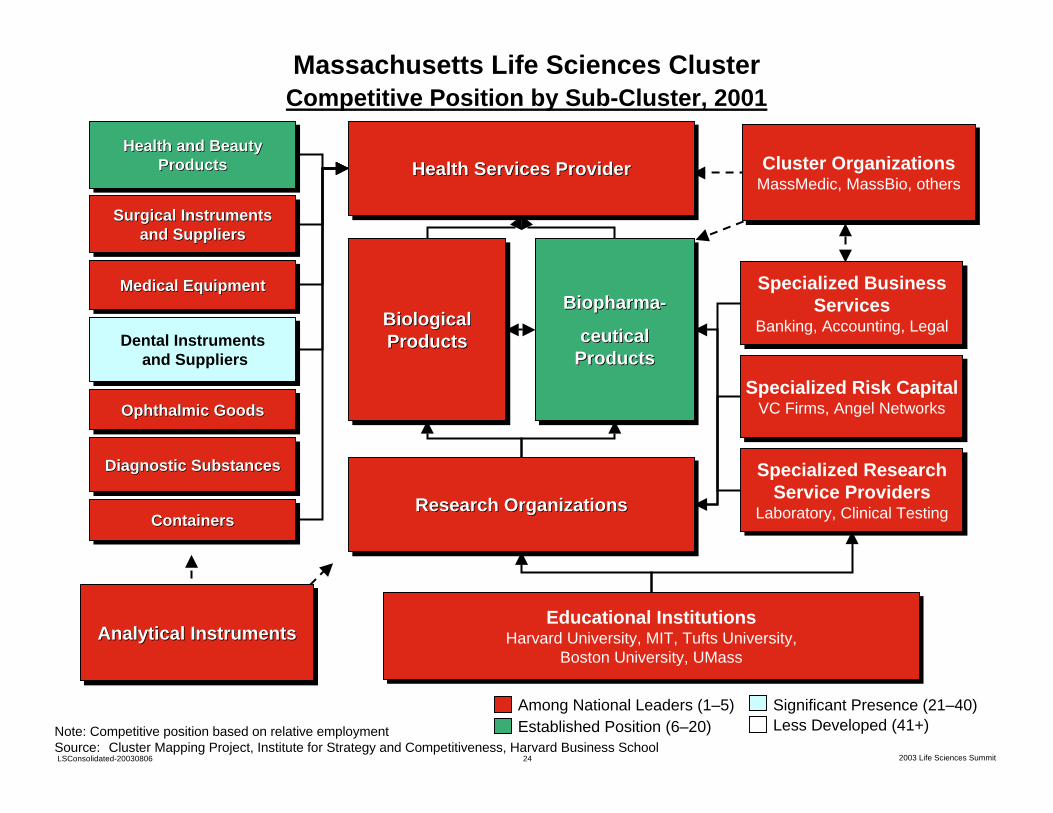

Research OrganizationsResearch OrganizationsResearch Organizations

Biological Products

Biological Biological ProductsProducts

Specialized Risk CapitalVC Firms, Angel Networks

Specialized Risk CapitalVC Firms, Angel Networks

Biopharma-

ceutical Products

BiopharmaBiopharma--

ceutical ceutical ProductsProducts

Specialized BusinessServices

Banking, Accounting, Legal

Specialized BusinessServices

Banking, Accounting, Legal

Specialized ResearchService Providers

Laboratory, Clinical Testing

Specialized ResearchService Providers

Laboratory, Clinical Testing

Dental Instrumentsand Suppliers

Dental Instrumentsand Suppliers

Surgical Instruments and Suppliers

Surgical Instruments Surgical Instruments and Suppliersand Suppliers

Diagnostic SubstancesDiagnostic SubstancesDiagnostic Substances

ContainersContainersContainers

Medical EquipmentMedical EquipmentMedical Equipment

Ophthalmic GoodsOphthalmic GoodsOphthalmic Goods

Health and Beauty Products

Health and Beauty Health and Beauty ProductsProducts Health Services ProviderHealth Services ProviderHealth Services Provider

Educational InstitutionsHarvard University, MIT, Tufts University,

Boston University, UMass

Educational InstitutionsHarvard University, MIT, Tufts University,

Boston University, UMass

Cluster OrganizationsMassMedic, MassBio, othersCluster Organizations

MassMedic, MassBio, others

Analytical InstrumentsAnalytical InstrumentsAnalytical Instruments

Among National Leaders (1–5)Established Position (6–20)

Significant Presence (21–40)Less Developed (41+)Note: Competitive position based on relative employment

Source: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

Massachusetts Life Sciences ClusterCompetitive Position by Sub-Cluster, 2001

25LSConsolidated-20030806 2003 Life Sciences Summit

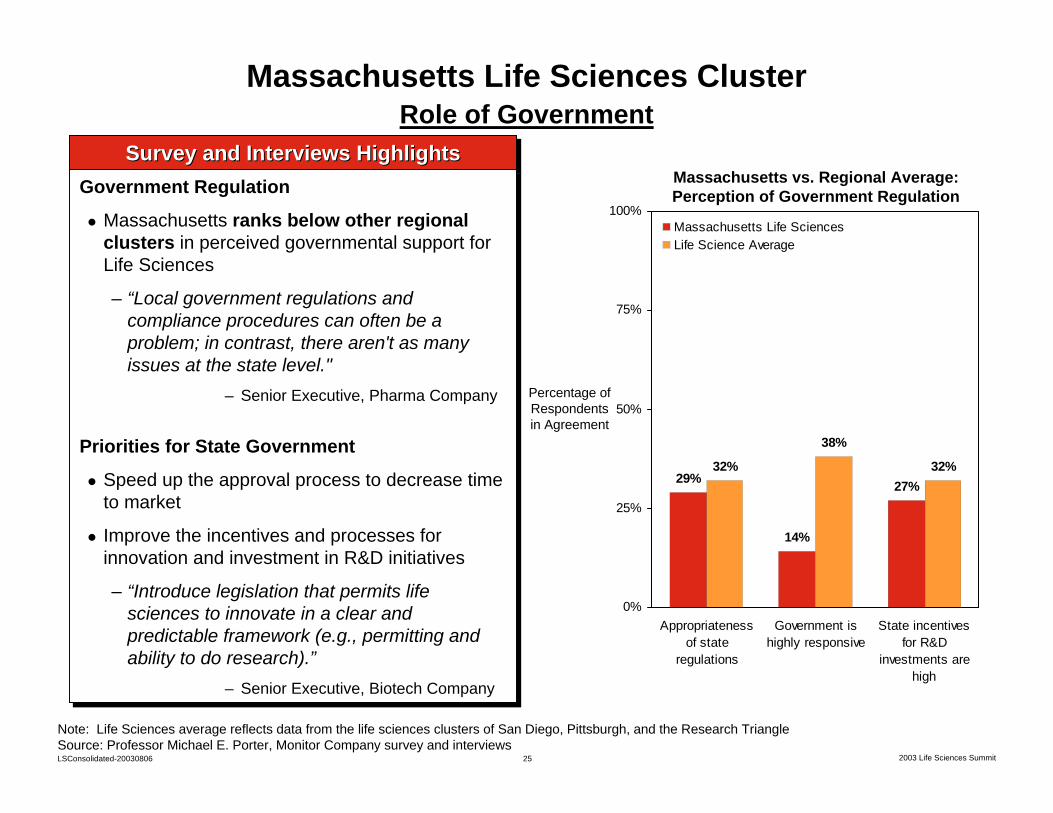

Massachusetts Life Sciences ClusterRole of Government

Massachusetts vs. Regional Average: Perception of Government Regulation

Survey and Interviews HighlightsSurvey and Interviews HighlightsSurvey and Interviews HighlightsGovernment Regulation

Massachusetts ranks below other regional clusters in perceived governmental support for Life Sciences

– “Local government regulations and compliance procedures can often be a problem; in contrast, there aren't as many issues at the state level."

– Senior Executive, Pharma Company

Priorities for State Government

Speed up the approval process to decrease time to market

Improve the incentives and processes for innovation and investment in R&D initiatives

– “Introduce legislation that permits life sciences to innovate in a clear and predictable framework (e.g., permitting and ability to do research).”

– Senior Executive, Biotech Company

Government Regulation

Massachusetts ranks below other regional clusters in perceived governmental support for Life Sciences

– “Local government regulations and compliance procedures can often be a problem; in contrast, there aren't as many issues at the state level."

– Senior Executive, Pharma Company

Priorities for State Government

Speed up the approval process to decrease time to market

Improve the incentives and processes for innovation and investment in R&D initiatives

– “Introduce legislation that permits life sciences to innovate in a clear and predictable framework (e.g., permitting and ability to do research).”

– Senior Executive, Biotech Company

Percentage of Respondents in Agreement

29%

14%

27%32%

38%

32%

0%

25%

50%

75%

100%

Appropriatenessof state

regulations

Government ishighly responsive

State incentivesfor R&D

investments arehigh

Massachusetts Life SciencesLife Science Average

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter, Monitor Company survey and interviews

26LSConsolidated-20030806 2003 Life Sciences Summit

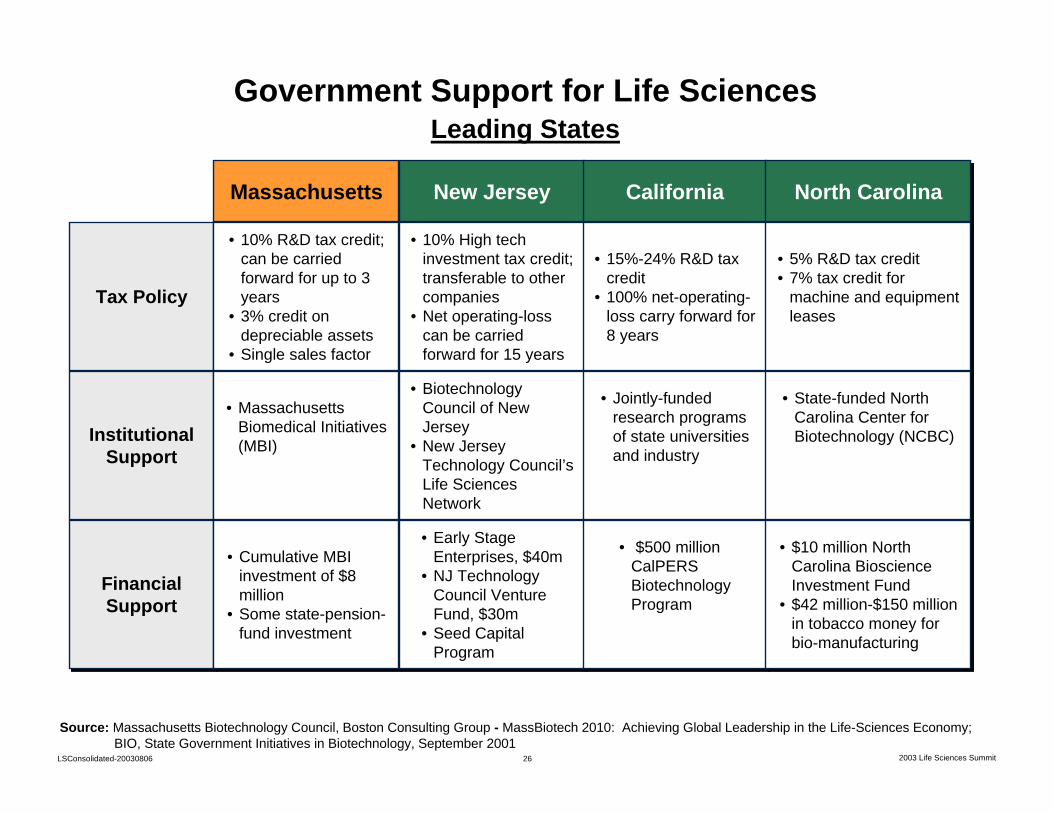

Tax PolicyTax Policy

Institutional Support

Institutional Support

Financial Support

Financial Support

Source: Massachusetts Biotechnology Council, Boston Consulting Group - MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy; BIO, State Government Initiatives in Biotechnology, September 2001

Government Support for Life SciencesLeading States

MassachusettsMassachusetts New JerseyNew Jersey

• 10% R&D tax credit; can be carried forward for up to 3 years

• 3% credit on depreciable assets

• Single sales factor

• 10% R&D tax credit; can be carried forward for up to 3 years

• 3% credit on depreciable assets

• Single sales factor

• 10% High tech investment tax credit; transferable to other companies

• Net operating-loss can be carried forward for 15 years

• 10% High tech investment tax credit; transferable to other companies

• Net operating-loss can be carried forward for 15 years

• Massachusetts Biomedical Initiatives (MBI)

• Massachusetts Biomedical Initiatives (MBI)

• Biotechnology Council of New Jersey

• New Jersey Technology Council’s Life Sciences Network

• Biotechnology Council of New Jersey

• New Jersey Technology Council’s Life Sciences Network

• Cumulative MBI investment of $8 million

• Some state-pension-fund investment

• Cumulative MBI investment of $8 million

• Some state-pension-fund investment

• Early Stage Enterprises, $40m

• NJ Technology Council Venture Fund, $30m

• Seed Capital Program

• Early Stage Enterprises, $40m

• NJ Technology Council Venture Fund, $30m

• Seed Capital Program

CaliforniaCalifornia North CarolinaNorth Carolina

• 15%-24% R&D tax credit

• 100% net-operating-loss carry forward for 8 years

• 15%-24% R&D tax credit

• 100% net-operating-loss carry forward for 8 years

• 5% R&D tax credit• 7% tax credit for

machine and equipment leases

• 5% R&D tax credit• 7% tax credit for

machine and equipment leases

• Jointly-funded research programs of state universities and industry

• Jointly-funded research programs of state universities and industry

• State-funded North Carolina Center for Biotechnology (NCBC)

• State-funded North Carolina Center for Biotechnology (NCBC)

• $500 millionCalPERSBiotechnology Program

• $500 millionCalPERSBiotechnology Program

• $10 million North Carolina Bioscience Investment Fund

• $42 million-$150 million in tobacco money for bio-manufacturing

• $10 million North Carolina Bioscience Investment Fund

• $42 million-$150 million in tobacco money for bio-manufacturing

27LSConsolidated-20030806 2003 Life Sciences Summit

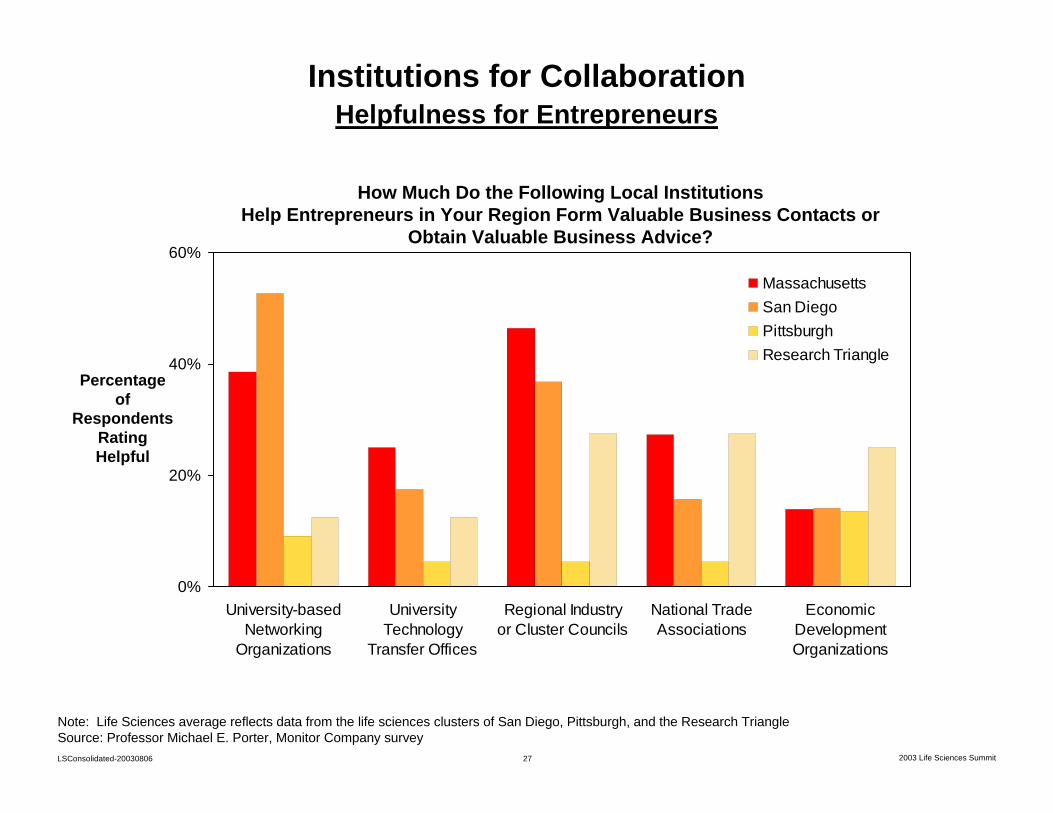

Institutions for CollaborationHelpfulness for Entrepreneurs

How Much Do the Following Local InstitutionsHelp Entrepreneurs in Your Region Form Valuable Business Contacts or

Obtain Valuable Business Advice?

0%

20%

40%

60%

University-basedNetworking

Organizations

UniversityTechnology

Transfer Offices

Regional Industryor Cluster Councils

National TradeAssociations

EconomicDevelopmentOrganizations

MassachusettsSan DiegoPittsburghResearch Triangle

Percentage of

Respondents Rating Helpful

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter, Monitor Company survey

28LSConsolidated-20030806 2003 Life Sciences Summit

Relative Performance

Competitive Assessment

Strategic Issues

Massachusetts' Competitive Position in Life Sciences

29LSConsolidated-20030806 2003 Life Sciences Summit

Competitive AgendaMassachusetts State Government

• Address weaknesses in the physical infrastructure, especially in transportation

• Increase the supply of housing to lower the cost of living in the State

• Work with local governments to identify, develop, and permit promising sites for life sciences companies (e.g., single site locator)

• Improve the structure of R&D incentives for life sciences companies

• Create a clear point of contact for existing companies in the Life Sciences cluster as well as potential out-of-state investors

• Participate actively in the Life Sciences cluster development process

• Increase the overall responsiveness of state government to business needs

• Address weaknesses in the physical infrastructure, especially in transportation

• Increase the supply of housing to lower the cost of living in the State

• Work with local governments to identify, develop, and permit promising sites for life sciences companies (e.g., single site locator)

• Improve the structure of R&D incentives for life sciences companies

• Create a clear point of contact for existing companies in the Life Sciences cluster as well as potential out-of-state investors

• Participate actively in the Life Sciences cluster development process

• Increase the overall responsiveness of state government to business needs

30LSConsolidated-20030806 2003 Life Sciences Summit

Competitive AgendaMassachusetts Life Sciences Cluster

• Improve technology transfer

• Make Massachusetts' health care delivery the most advanced and innovative in the nation- Create and environment and rules that facilitate the introduction of new

treatments- Adopt new service delivery technologies (e.g., IT)

• Secure the State’s medium skilled workforce position

• Expand clinical trials in the State

• Capture more downstream manufacturing

• Improve technology transfer

• Make Massachusetts' health care delivery the most advanced and innovative in the nation- Create and environment and rules that facilitate the introduction of new

treatments- Adopt new service delivery technologies (e.g., IT)

• Secure the State’s medium skilled workforce position

• Expand clinical trials in the State

• Capture more downstream manufacturing

31LSConsolidated-20030806 2003 Life Sciences Summit

0

50

100

150

200

250

300

-10% 0% 10% 20% 30% 40% 50%

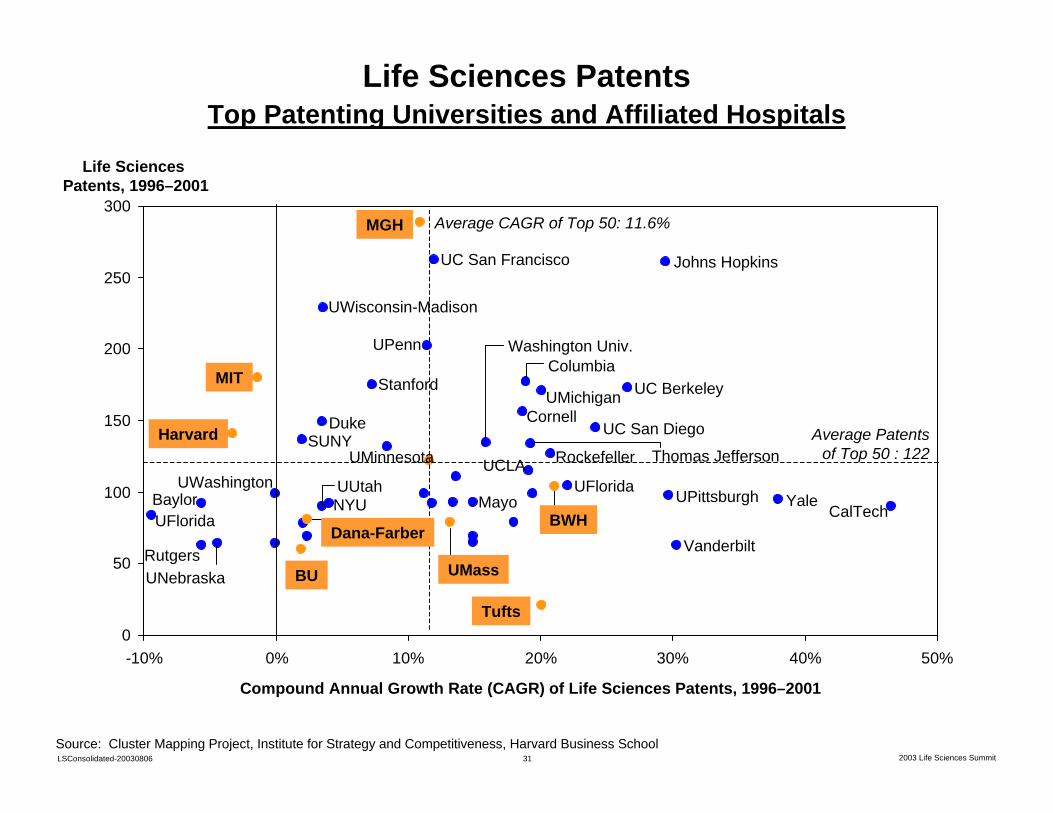

Life Sciences PatentsTop Patenting Universities and Affiliated Hospitals

Source: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School

Life Sciences Patents, 1996–2001

Compound Annual Growth Rate (CAGR) of Life Sciences Patents, 1996–2001

Average CAGR of Top 50: 11.6%

UC San Francisco

MGH

Johns Hopkins

UMichigan

Rockefeller

UC Berkeley

UC San Diego

Tufts

Vanderbilt

Harvard

UPenn

UWisconsin-Madison

UFlorida

MIT

CalTech

SUNYUCLA

Columbia

CornellAverage Patents

of Top 50 : 122

UMass

Dana-Farber

Stanford

Duke

UMinnesota

Washington Univ.

Thomas Jefferson

YaleUPittsburghBaylorUWashington

RutgersUNebraska

NYUUUtah UFlorida

Mayo

BU

BWH

32LSConsolidated-20030806 2003 Life Sciences Summit

0

1

2

3

4

5

6

-10% -5% 0% 5% 10% 15% 20% 25% 30%

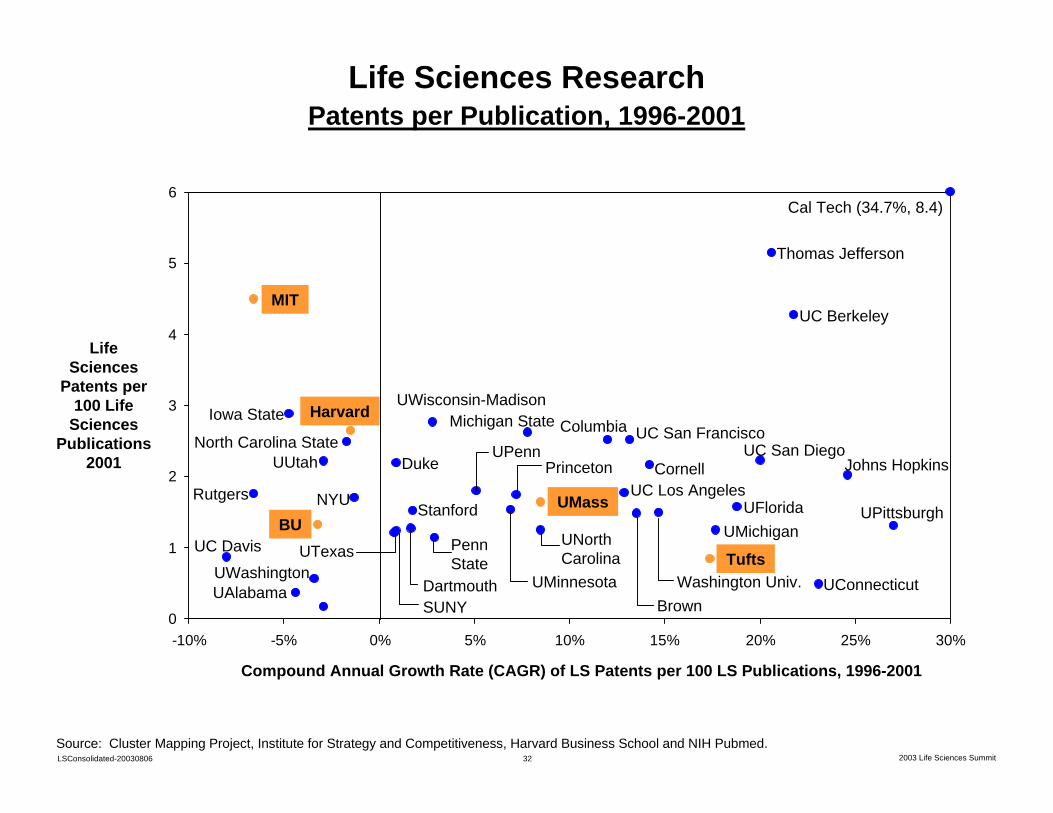

Life Sciences ResearchPatents per Publication, 1996-2001

Life Sciences

Patents per 100 Life

Sciences Publications

2001

Compound Annual Growth Rate (CAGR) of LS Patents per 100 LS Publications, 1996-2001

Cal Tech (34.7%, 8.4)

Source: Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School and NIH Pubmed.

Thomas Jefferson

UC BerkeleyMIT

Iowa State

Johns Hopkins

UPittsburgh

UConnecticutTufts

UC San Diego

UFloridaUMichigan

UC San Francisco

CornellUC Los AngelesRutgers

UC Davis

UAlabamaUWashington

BUNYU

UUtahNorth Carolina State

HarvardUWisconsin-Madison

UMass

Columbia

Washington Univ.Brown

Michigan State

Princeton

UNorthCarolina

UMinnesota

UPennDuke

Stanford

PennState

DartmouthSUNY

UTexas

33LSConsolidated-20030806 2003 Life Sciences Summit

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

-40% -30% -20% -10% 0% 10% 20% 30% 40%

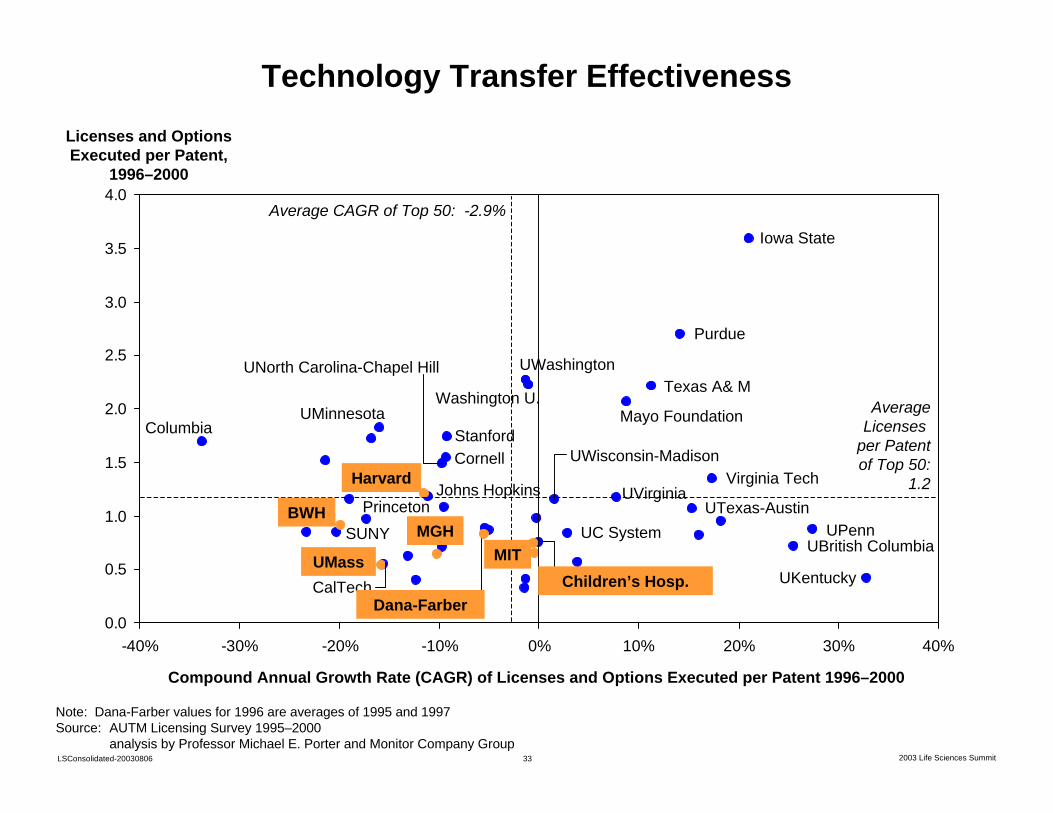

Technology Transfer Effectiveness

Note: Dana-Farber values for 1996 are averages of 1995 and 1997Source: AUTM Licensing Survey 1995–2000

analysis by Professor Michael E. Porter and Monitor Company Group

Iowa State

Licenses and Options Executed per Patent,

1996–2000

Compound Annual Growth Rate (CAGR) of Licenses and Options Executed per Patent 1996–2000

Average CAGR of Top 50: -2.9%

Purdue

Columbia Stanford

UWashington

Washington U.

UPenn

UKentucky

UBritish Columbia

Texas A& M

Mayo Foundation

Virginia TechUWisconsin-Madison

UNorth Carolina-Chapel Hill

Cornell

UMinnesota

UTexas-AustinUVirginiaJohns Hopkins

SUNY

UMass

UC SystemPrinceton

CalTech

AverageLicenses

per Patentof Top 50:

1.2Harvard

MGHMIT

Children’s Hosp.Dana-Farber

BWH

34LSConsolidated-20030806 2003 Life Sciences Summit

Technology and Knowledge TransferKey Issues

• The transfer of technology from research to commercialization is traditionally a key competitive advantage of the Massachusetts Life Sciences cluster

However• Other regions are catching up

– Life Sciences research institutions in Massachusetts show only average performance on a number of technology transfer indicators

• Tech transfer performance is seen as lagging in some institutions, with cumbersome decision-making processes and inappropriate understanding of appropriate deal structures

• The context for technology and knowledge transfer is changing– Pharmaceutical companies entering the cluster will need to establish new

relationships with local research institutions• Massachusetts’ traditional approach of knowledge transfer via small start-up

companies needs to evolve

35LSConsolidated-20030806 2003 Life Sciences Summit

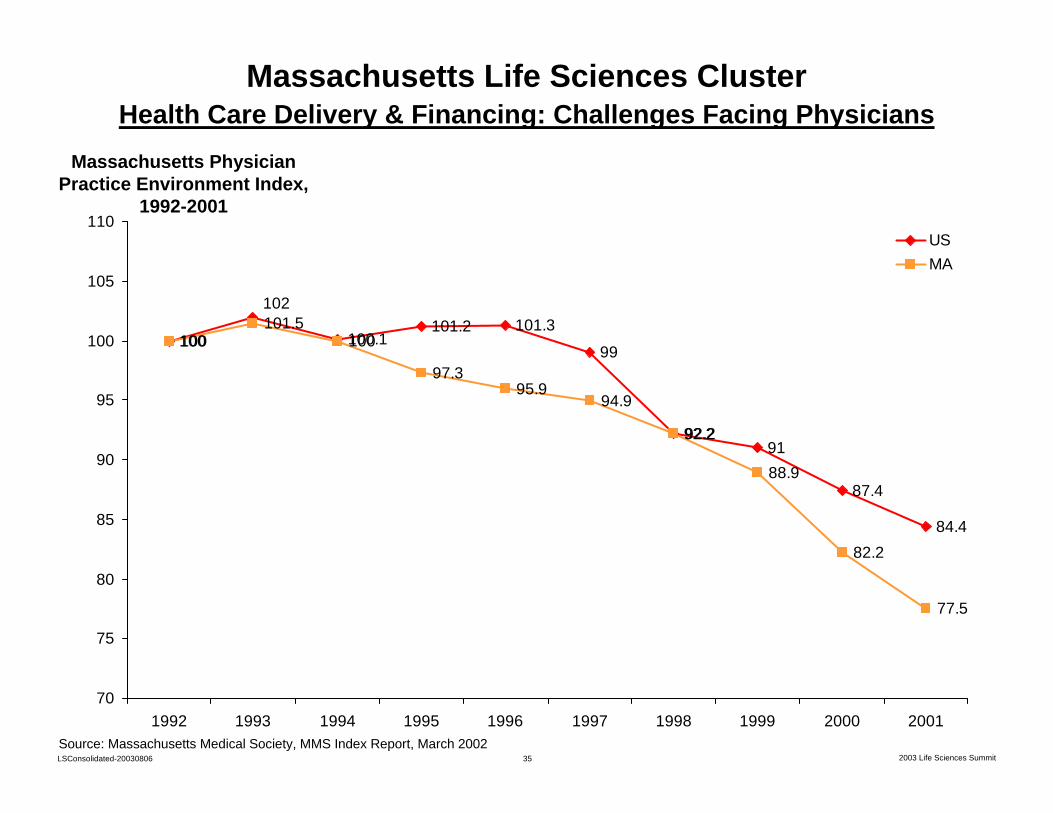

100 100.1101.2 101.3

99

92.291

87.4

84.4

101.5100

97.395.9

94.9

92.2

88.9

82.2

77.5

102

100

70

75

80

85

90

95

100

105

110

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

USMA

Source: Massachusetts Medical Society, MMS Index Report, March 2002

Massachusetts Physician Practice Environment Index,

1992-2001

Massachusetts Life Sciences ClusterHealth Care Delivery & Financing: Challenges Facing Physicians

36LSConsolidated-20030806 2003 Life Sciences Summit

Massachusetts Health Care DeliveryOverview

• Competitiveness and innovation in a region are strongly influenced by sophisticated local demand

• Having the most advanced health care delivery offers major benefits to the cluster as well as to patient care

• While Massachusetts is seen as the home of demanding companies, research institutions, and medical practitioners, cost pressures, and reimbursement structures have the potential to slow down innovation

– Health care delivery runs the risk of becoming driven by short-term cost reduction

37LSConsolidated-20030806 2003 Life Sciences Summit

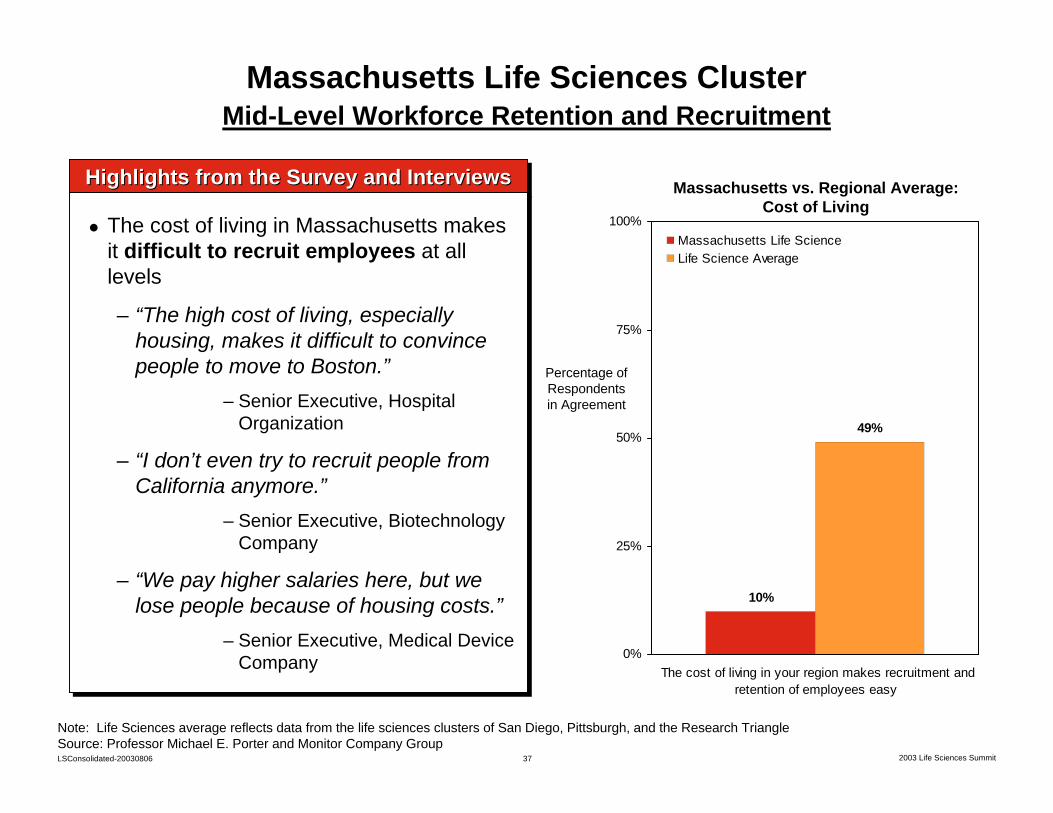

Massachusetts Life Sciences ClusterMid-Level Workforce Retention and Recruitment

Highlights from the Survey and InterviewsHighlights from the Survey and InterviewsHighlights from the Survey and Interviews

The cost of living in Massachusetts makes it difficult to recruit employees at all levels

– “The high cost of living, especially housing, makes it difficult to convince people to move to Boston.”

– Senior Executive, Hospital Organization

– “I don’t even try to recruit people from California anymore.”

– Senior Executive, Biotechnology Company

– “We pay higher salaries here, but we lose people because of housing costs.”

– Senior Executive, Medical Device Company

The cost of living in Massachusetts makes it difficult to recruit employees at all levels

– “The high cost of living, especially housing, makes it difficult to convince people to move to Boston.”

– Senior Executive, Hospital Organization

– “I don’t even try to recruit people from California anymore.”

– Senior Executive, Biotechnology Company

– “We pay higher salaries here, but we lose people because of housing costs.”

– Senior Executive, Medical Device Company

Massachusetts vs. Regional Average: Cost of Living

10%

49%

0%

25%

50%

75%

100%

The cost of living in your region makes recruitment andretention of employees easy

Massachusetts Life ScienceLife Science Average

Percentage of Respondents in Agreement

Note: Life Sciences average reflects data from the life sciences clusters of San Diego, Pittsburgh, and the Research TriangleSource: Professor Michael E. Porter and Monitor Company Group

38LSConsolidated-20030806 2003 Life Sciences Summit

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Biomed

ical E

ngine

ers

Bioche

mists/B

iophy

sicist

s

Biomed

ical te

chnic

ians

Intern

ists

Regist

ered n

urses

Post-s

econ

dary

biolog

y tea

chers

Enviro

nmen

tal an

d hea

lth sp

ecial

ists

Pharm

acy t

echn

ician

s

Post-S

econ

dary

healt

h spe

cialty

teac

hers

Medica

l equ

ipmen

t repa

irers

Radiol

ogy t

echn

icians

Medica

l app

lianc

e tec

hnici

ans

Anesth

esiol

ogist

s

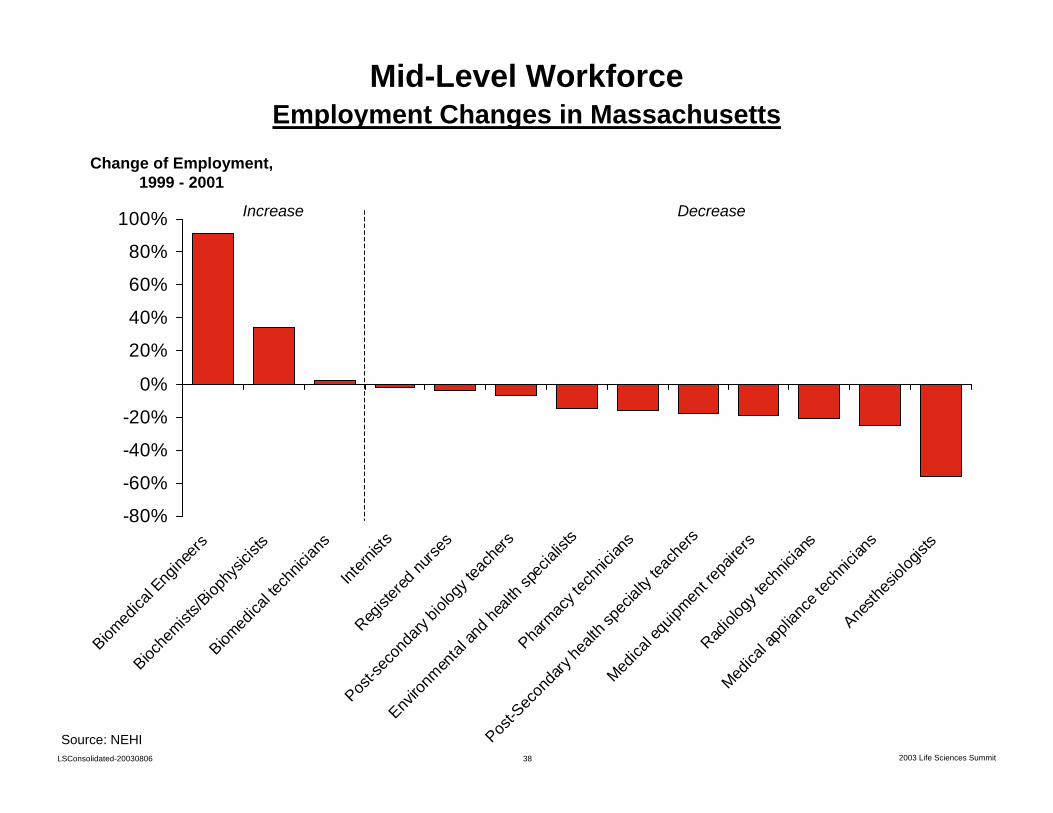

Mid-Level Workforce Employment Changes in Massachusetts

Source: NEHI

Change of Employment, 1999 - 2001

DecreaseIncrease

39LSConsolidated-20030806 2003 Life Sciences Summit

Mid-Level Workforce Overview

• The Massachusetts Life Sciences Cluster requires a strong base of mid-level professionals

– High cost of living makes the Boston-region increasingly unattractive

– The growth of corporate research facilities increases the pressure on hospitals and research institutions to compete for mid-level professionals

– Educational institutions need to be equipped to adjust supply to meet the need for mid-level professionals

• A strategy is needed to expand the supply of needed skills for the cluster

40LSConsolidated-20030806 2003 Life Sciences Summit

Nationwide, 2.3 million people participated in industry- and government-funded clinical trials in 2002

– In Massachusetts, an estimated 40 to 50,000 patients participated in clinical trials (ca. 2% of national trial participants vs. 2.2% of national population and 5.3% of life sciences employment)

The recruitment costs for volunteers are rising – Spending on recruiting volunteers is rising nationwide by 18% annually,

reaching $500m in 2002 (ca. $215 per volunteer)

The efficiency of carrying out clinical trials is declining – Nearly 25% of those enrolled in clinical trials drop out before the trial is

completed– Enrollment delays are increasingly pushing back the timetable for trials and

product introduction

Clinical TrialsCurrent Situation

Source: Center Watch; presented at MBC

41LSConsolidated-20030806 2003 Life Sciences Summit

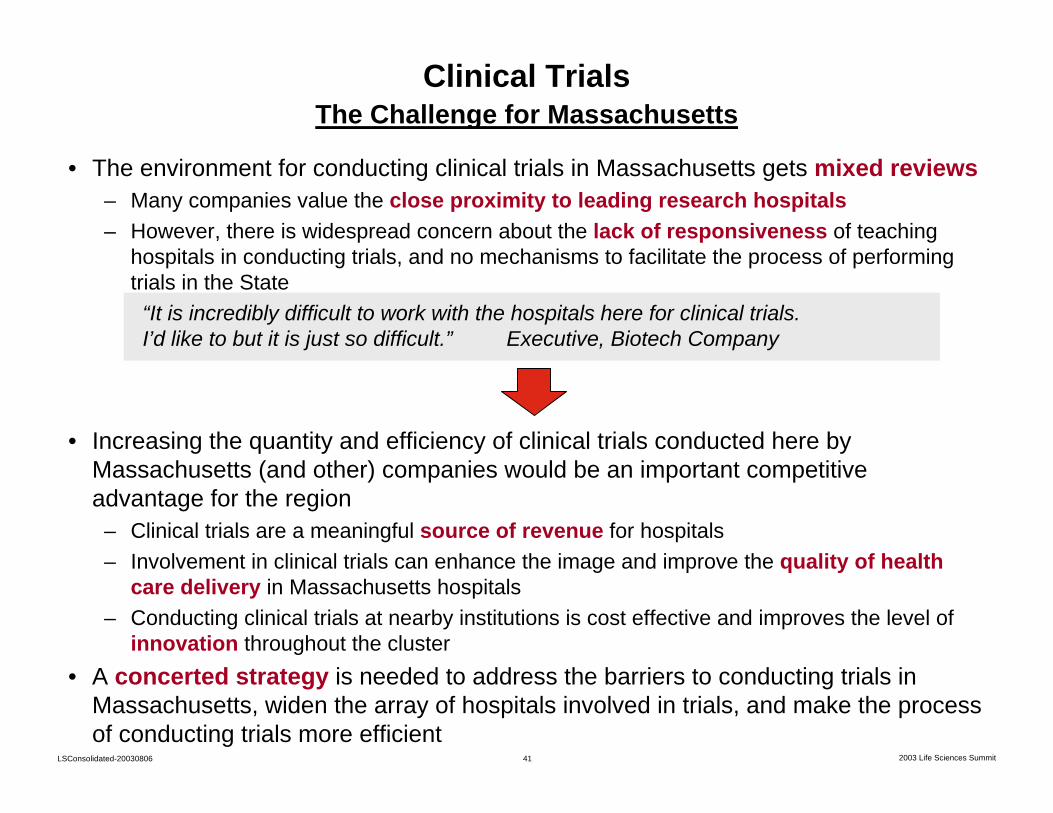

Clinical TrialsThe Challenge for Massachusetts

• The environment for conducting clinical trials in Massachusetts gets mixed reviews– Many companies value the close proximity to leading research hospitals– However, there is widespread concern about the lack of responsiveness of teaching

hospitals in conducting trials, and no mechanisms to facilitate the process of performing trials in the State

“It is incredibly difficult to work with the hospitals here for clinical trials. I’d like to but it is just so difficult.” Executive, Biotech Company

• Increasing the quantity and efficiency of clinical trials conducted here by Massachusetts (and other) companies would be an important competitive advantage for the region

– Clinical trials are a meaningful source of revenue for hospitals– Involvement in clinical trials can enhance the image and improve the quality of health

care delivery in Massachusetts hospitals– Conducting clinical trials at nearby institutions is cost effective and improves the level of

innovation throughout the cluster• A concerted strategy is needed to address the barriers to conducting trials in

Massachusetts, widen the array of hospitals involved in trials, and make the process of conducting trials more efficient

42LSConsolidated-20030806 2003 Life Sciences Summit

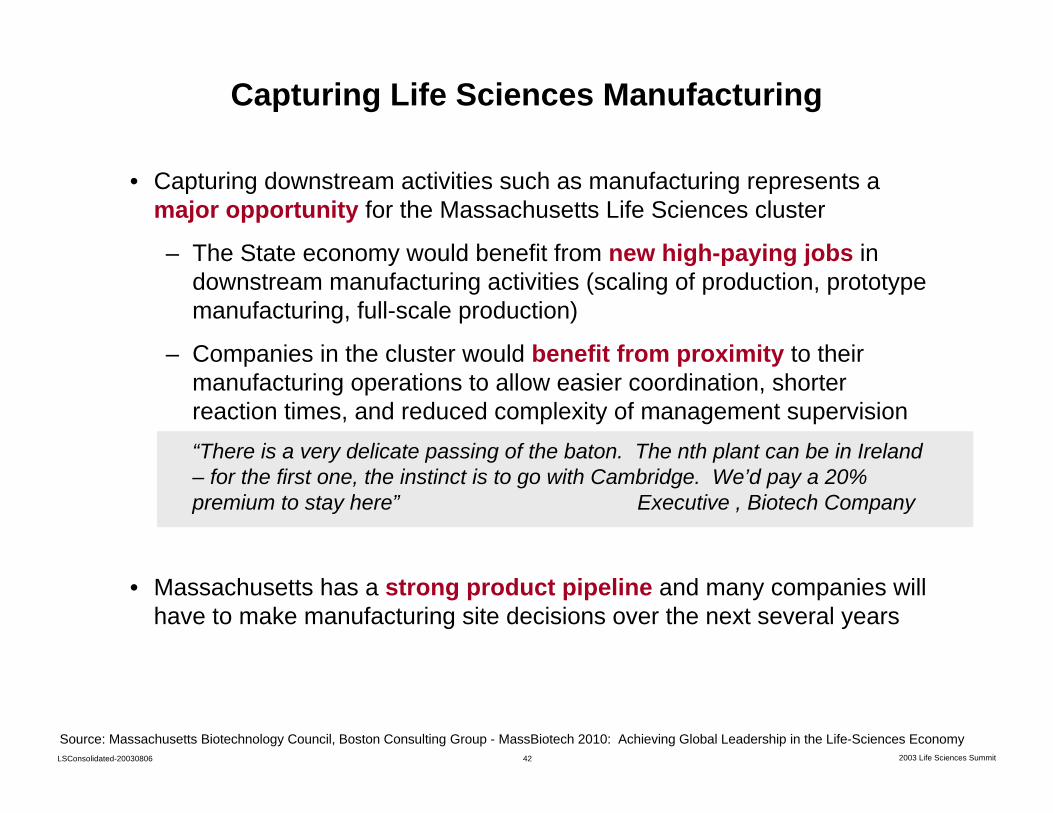

Capturing Life Sciences Manufacturing

• Capturing downstream activities such as manufacturing represents a major opportunity for the Massachusetts Life Sciences cluster

– The State economy would benefit from new high-paying jobs in downstream manufacturing activities (scaling of production, prototype manufacturing, full-scale production)

– Companies in the cluster would benefit from proximity to their manufacturing operations to allow easier coordination, shorter reaction times, and reduced complexity of management supervision“There is a very delicate passing of the baton. The nth plant can be in Ireland – for the first one, the instinct is to go with Cambridge. We’d pay a 20% premium to stay here” Executive , Biotech Company

• Massachusetts has a strong product pipeline and many companies will have to make manufacturing site decisions over the next several years

Source: Massachusetts Biotechnology Council, Boston Consulting Group - MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy

43LSConsolidated-20030806 2003 Life Sciences Summit

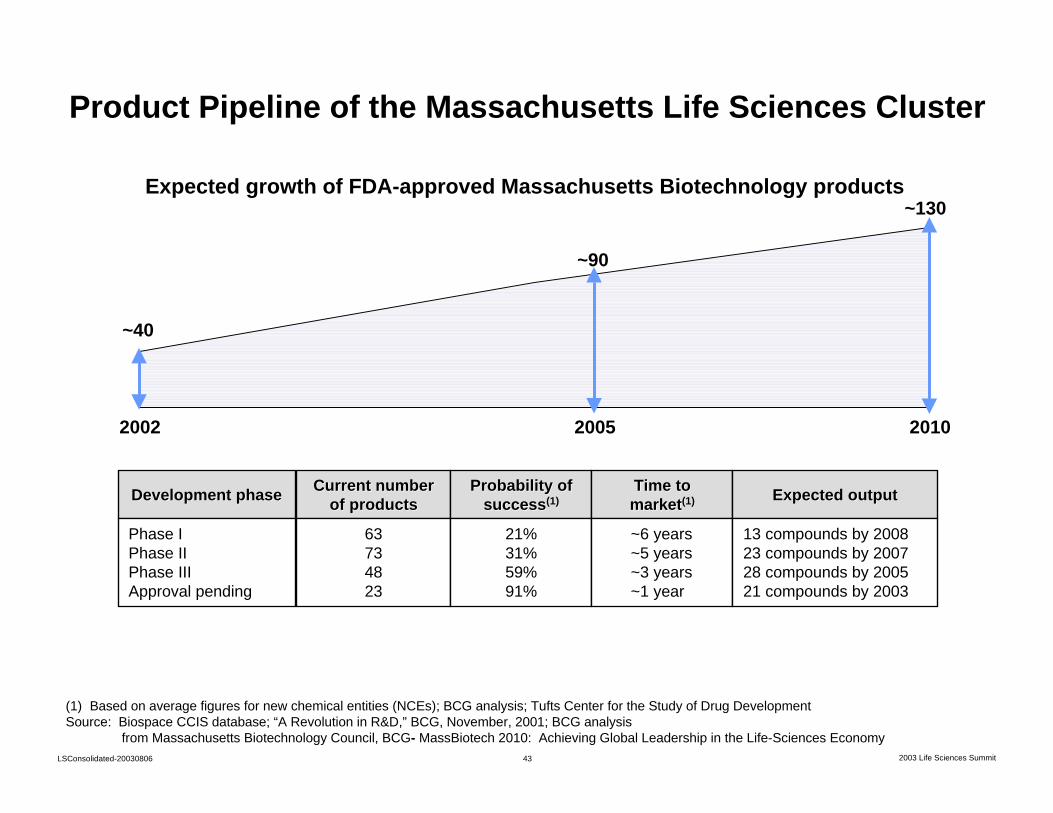

Product Pipeline of the Massachusetts Life Sciences Cluster

Expected growth of FDA-approved Massachusetts Biotechnology products

2002 2005 2010

~40

~90

~130

Development phaseDevelopment phase

Phase IPhase IIPhase IIIApproval pending

Current number Current number of productsof products

63734823

Probability of Probability of successsuccess(1)(1)

21%31%59%91%

Time to Time to marketmarket(1)(1)

~6 years~5 years~3 years~1 year

Expected outputExpected output

13 compounds by 200823 compounds by 200728 compounds by 200521 compounds by 2003

(1) Based on average figures for new chemical entities (NCEs); BCG analysis; Tufts Center for the Study of Drug DevelopmentSource: Biospace CCIS database; “A Revolution in R&D,” BCG, November, 2001; BCG analysis

from Massachusetts Biotechnology Council, BCG- MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy

44LSConsolidated-20030806 2003 Life Sciences Summit

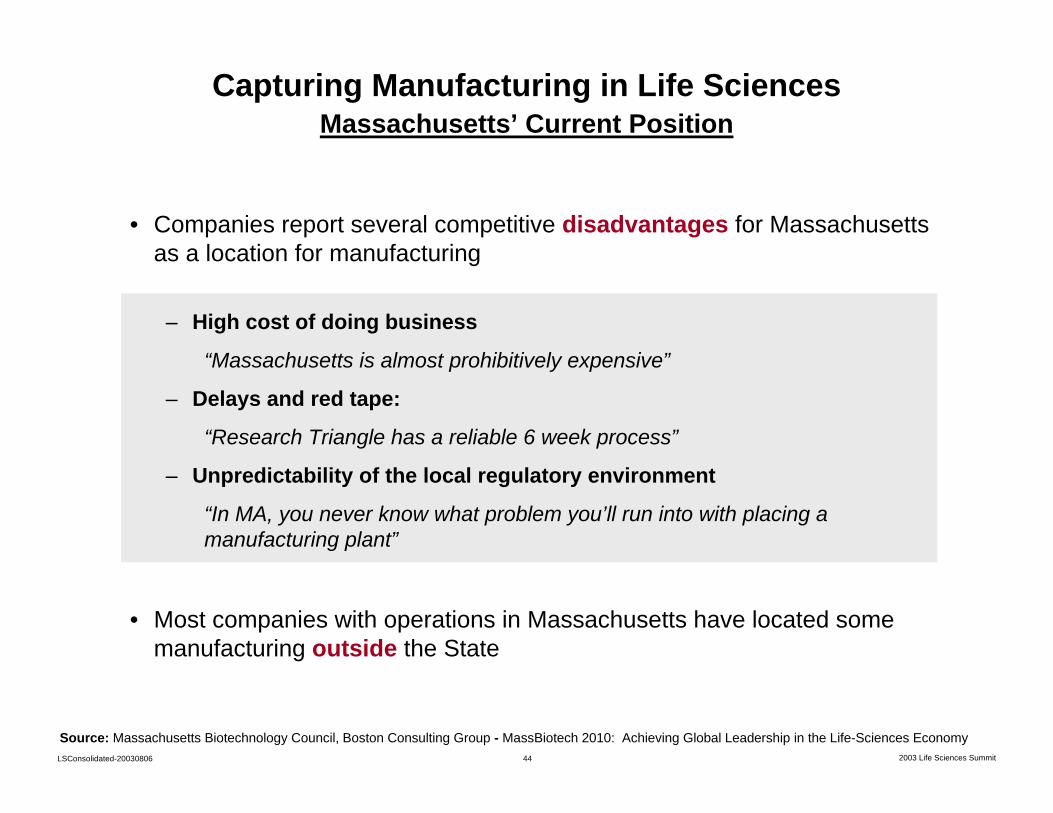

Capturing Manufacturing in Life Sciences Massachusetts’ Current Position

• Companies report several competitive disadvantages for Massachusetts as a location for manufacturing

– High cost of doing business

“Massachusetts is almost prohibitively expensive”

– Delays and red tape:

“Research Triangle has a reliable 6 week process”

– Unpredictability of the local regulatory environment

“In MA, you never know what problem you’ll run into with placing a manufacturing plant”

• Most companies with operations in Massachusetts have located some manufacturing outside the State

Source: Massachusetts Biotechnology Council, Boston Consulting Group - MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy

45LSConsolidated-20030806 2003 Life Sciences Summit

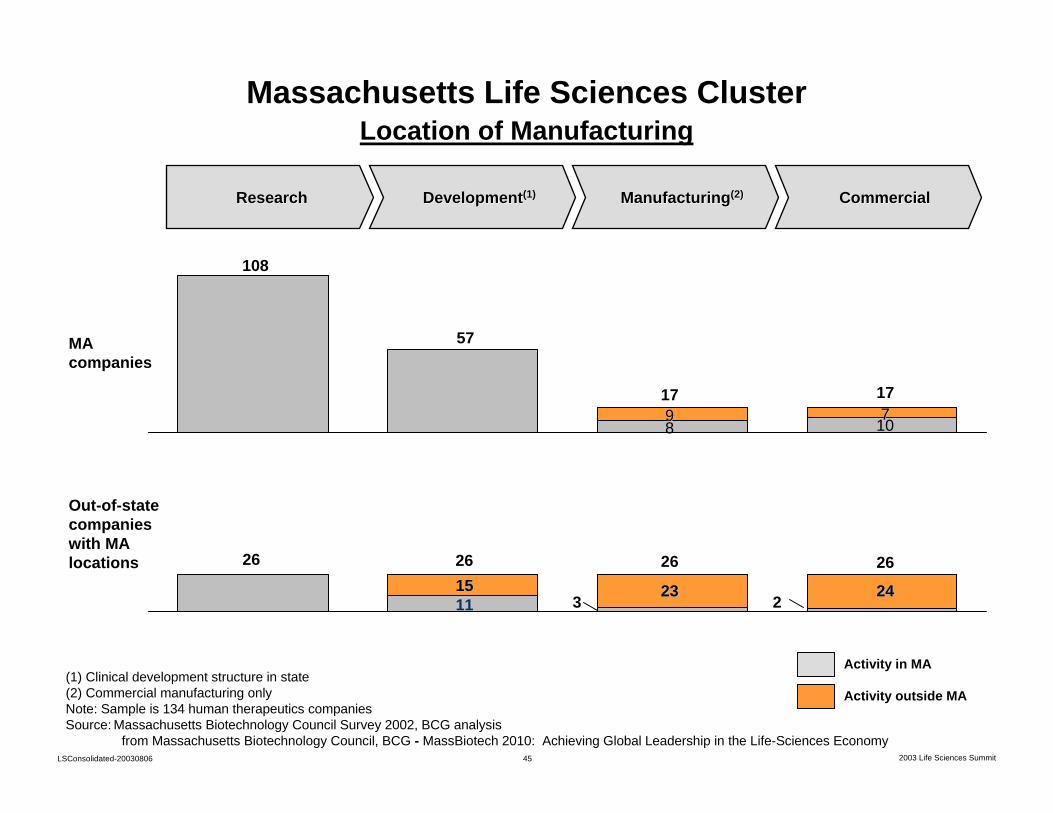

(1) Clinical development structure in state(2) Commercial manufacturing onlyNote: Sample is 134 human therapeutics companies Source: Massachusetts Biotechnology Council Survey 2002, BCG analysis

from Massachusetts Biotechnology Council, BCG - MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy

CommercialCommercialResearchResearch DevelopmentDevelopment(1)(1) ManufacturingManufacturing(2)(2)

MAcompanies

Out-of-state companieswith MA locations

Activity in MA

Activity outside MA

899 10107

7

26

111515

3 2323 2 2424

Massachusetts Life Sciences ClusterLocation of Manufacturing

108

57

26 26 26

17 17

46LSConsolidated-20030806 2003 Life Sciences Summit

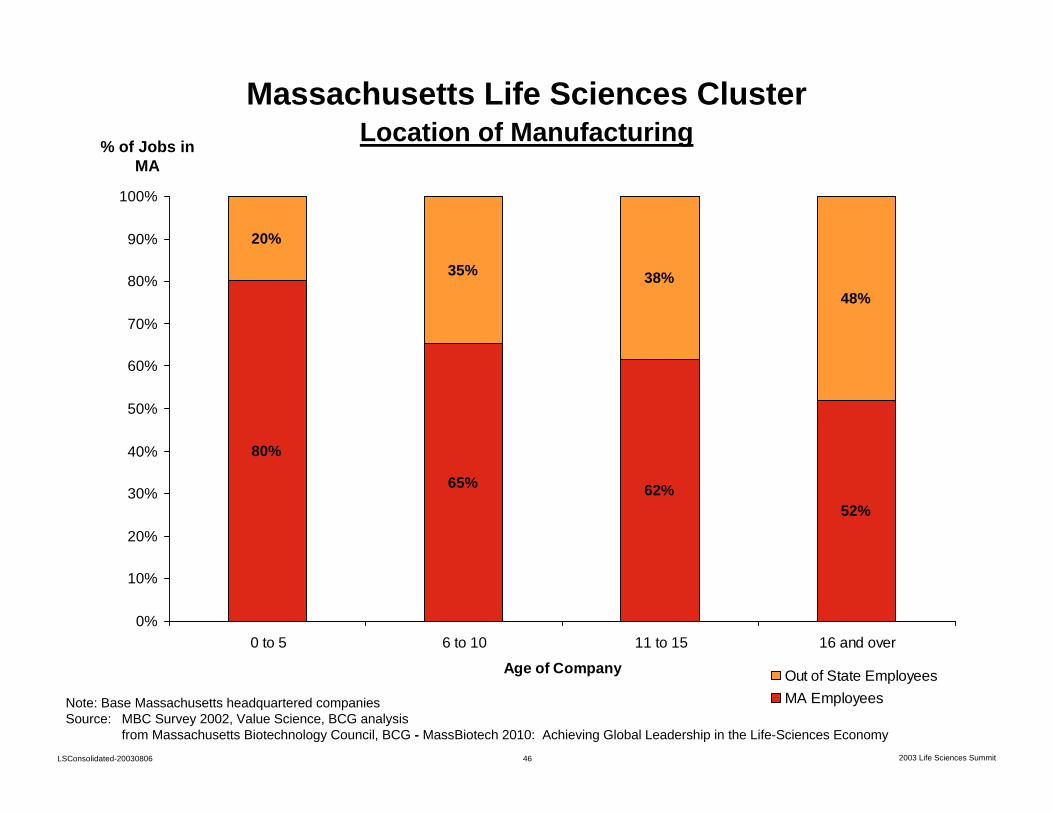

80%

65% 62%52%

20%

35% 38%48%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0 to 5 6 to 10 11 to 15 16 and over

Age of Company Out of State EmployeesMA EmployeesNote: Base Massachusetts headquartered companies

Source: MBC Survey 2002, Value Science, BCG analysisfrom Massachusetts Biotechnology Council, BCG - MassBiotech 2010: Achieving Global Leadership in the Life-Sciences Economy

Massachusetts Life Sciences ClusterLocation of Manufacturing% of Jobs in

MA

47LSConsolidated-20030806 2003 Life Sciences Summit

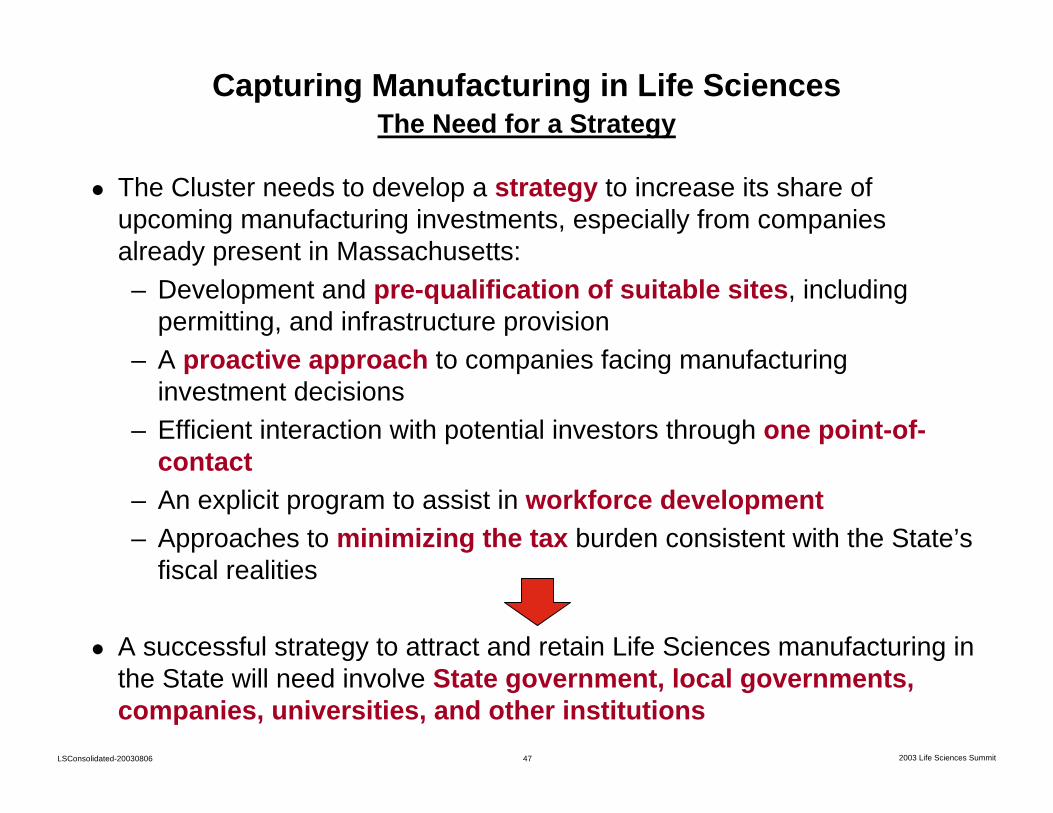

The Cluster needs to develop a strategy to increase its share of upcoming manufacturing investments, especially from companies already present in Massachusetts:– Development and pre-qualification of suitable sites, including

permitting, and infrastructure provision– A proactive approach to companies facing manufacturing

investment decisions– Efficient interaction with potential investors through one point-of-

contact– An explicit program to assist in workforce development– Approaches to minimizing the tax burden consistent with the State’s

fiscal realities

A successful strategy to attract and retain Life Sciences manufacturing in the State will need involve State government, local governments,companies, universities, and other institutions

Capturing Manufacturing in Life Sciences The Need for a Strategy

48LSConsolidated-20030806 2003 Life Sciences Summit

Other Strategic Issues Identified

Strategy for recruiting outside investors to the State

Biogrid / IT infrastructure for life sciences

Technology mapping and identifying technology gaps

49LSConsolidated-20030806 2003 Life Sciences Summit

Discussion Questions

Are these the right issues?

What are the priorities among them?

50LSConsolidated-20030806 2003 Life Sciences Summit

SourcesThe Economic Contributions of Health Care to New EnglandNew England Healthcare Institute, Milken Institutehttp://www.nehi.net/CMS/viewPage.cfm?pageId=29

Massachusetts Life Sciences DataMassachusetts Technology Collaborativehttp://www.mtpc.org/NewsandReports/the_index/index2001.pdf

MassBiotech 2010: Achieving Global Leadership in the Life-Sciences EconomyMassachusetts Biotechnology Council, Boston Consulting Grouphttp://www.massbiotech2010.org/report/

The Medical Device Industry in MassachusettsAlan Clayton-Matthews, MassMedic, Massachusetts Medical Device Industry Councilhttp://www.massmedic.com/01.pdf

Why Care? The Howell Group of Bostonhttp://www.whycare.info/pages/1/index.htm

Massachusetts Life Sciences ClusterProfessor Michael E. Porter and Monitor Company Group, L. P.

New Jersey Life Science Super-ClusterProfessor Michael E. Porter and Monitor Company Group, L. P.http://www.state.nj.us/prosperity/porter.shtml

The Boston Life-Sciences ClusterChristian HM Ketels, PHD, Institute for Strategy and Competitiveness, Harvard Business Schoolhttp://www.isc.hbs.edu/pdf/Boston_NHCM_CK_11-22-02.pdf