Chapter 12 - Accounting for Partnerships and Limited Liability Companies

1

CA. Kamlesh Vikamsey

LIMITED LIABILITY PARTNERSHIPS

– AN OVERVIEW

Presented by : CA Kamlesh Vikamsey

Organized by : Bangalore Branch of SIRC

CA. Kamlesh Vikamsey

Indian history• 2003: Naresh Chandra Committee Report highlighted need for LLPs &

suggested application of LLPs to Service industry, Chartered Accountants,

Lawyers, Architects, etc.

• 2005: J J Irani Expert Committee on Company Law recommended introduction

of LLPs-suggested small enterprises be included in scope of LLP & there should

be a separate LLP Act

• 2006: LLP Bill introduced in Parliament

• 2007: Bill referred to Parliamentary Standing Committee (PSC) for examination

• 2008: Lok Sabha passes New LLP Bill as revised by PSC

2

CA. Kamlesh Vikamsey

Indian history• 2009: LLP Act, 2008 receives presidential assent & is published in Official

Gazette

• 2009: LLP Act, 2008 gets notified w.e.f March 31st, 2009

CA. Kamlesh Vikamsey

Different Chapters of the Act• Chapter I-Preliminary (Ss. 1 & 2)

• Chapter II-Nature of LLP (Ss. 3-10)

• Chapter III-Incorporation & Incidental Matters (Ss. 11-21)

• Chapter IV-Partners & their Relations (Ss. 22-25)

• Chapter V-Extent & Limitation of Liability of LLP & Partners(Ss. 26-31)

• Chapter VI-Contributions (Ss. 32 & 33)

• Chapter VII-Financial Disclosures (Ss. 34-41)

• Chapter VIII-Assignment & Transfer of Partnership Rights (S.42)

• Chapter IX-Investigation (Ss. 43-54)

3

CA. Kamlesh Vikamsey

• Chapter X-Conversion to LLP (Ss. 55-58)

• Chapter XI-Foreign Limited Liability Partnerships (S. 59)

• Chapter XII-Compromise, Arrangement or Reconstruction of LLPs(Ss. 60-62)

• Chapter XIII-Winding Up & Dissolution (not notified as on date)(Ss. 63-65)

• Chapter XIV-Miscellaneous Provisions (Ss. 66-81)

• First Schedule-Mutual Rights & Liabilities of Partners & LLP

• Second Schedule-Conversion of Partnership Firm to LLP

• Third Schedule-Conversion of Private Company to LLP

• Fourth Schedule-Conversion of Unlisted Public Company to LLP

Different Chapters of the Act

CA. Kamlesh Vikamsey

Preliminary (Ch. I)• Short title, extent & commencement

This Act may be called the Limited Liability Partnership Act, 2008

It extends to the whole of India

All sections have been notified as on March 31st, 2009, vide notification no. S.O.891(E), except-

Clauses (c) and (u) of sub-section (1) of S. 2-Appellate Tribunal & Tribunal

Extent of applicability of Section 31 in respect of ‘Tribunal’

S. 51-Application by Central Government for Winding-up of LLP

Ch. X-Conversion to LLPs [Notified vide Notification no. S.O. 1323(E) dated May22nd, 2009]

Ch. XIII-Winding Up of LLPs

S. 72-Jurisdiction of Tribunal & Appellate Tribunal

Clauses (b), pertaining to its applicability to Ss. 51, 63 & 64; & (c) of S. 81

Second, Third & Fourth Schedule-Pertaining to Conversion of Firms & Companies(except Listed Companies) to LLPs [Notified vide Notification no. S.O. 1323(E)dated May 22nd, 2009]

4

CA. Kamlesh Vikamsey

Preliminary (Ch. I)Important Definitions:

• Body Corporate [S. 2 (1) (d)]:‘means a company defined in section 3 of the Companies Act, 1956 and includes-

(i) a limited liability partnership registered under this Act;

(ii) a limited liability partnership incorporated outside India; and

(iii) a company incorporated outside India,

but does not include-

(i) a corporation sole;

(ii) a co-operative society registered under any law for the time being inforce; and

(iii) any other body corporate (not being a company as defined in section 3of the Companies Act, 1956 or a limited liability partnership as defined in thisAct), which the Central Government may, by notification in the Official Gazette,specify in this behalf’

CA. Kamlesh Vikamsey

Preliminary (Ch. I)• Business [S. 2 (1) (e)]:

‘includes every trade, profession, service and occupation’

• Financial Year [S. 2 (1) (l)]:

‘in relation to limited liability partnerships, means the period fromthe 1st day of April of a year to the 31st day of March of thefollowing year:

Provided that in case of a limited liability partnership incorporatedafter the 30th day of September of a year, the financial year mayend on the 31st day of march of the year next following that year’

5

CA. Kamlesh Vikamsey

Preliminary (Ch. I)• Limited Liability Partnership Agreement [S. 2 (1) (o)]:

‘means any written agreement between the partners of the limitedliability partnership or between the limited liability partnership andits partners which determines the mutual rights and duties of thepartners and their rights and duties in relation to that limitedliability partnership’

• Registrar [S. 2 (1) (s)]:‘means a Registrar, or an Additional, a Joint, a Deputy or anAssistant Registrar, having the duty of registering companiesunder the Companies Act, 1956’

CA. Kamlesh Vikamsey

Preliminary (Ch. I)• S. 2 (2):

‘Words and expressions used and not defined in this Act defined inthe Companies Act, 1956 shall have the meanings respectivelyassigned to them in that Act’

6

CA. Kamlesh Vikamsey

Nature of Limited Liability Partnership (Ch. II)

• LLP is body corporate formed & incorporated under LLP Act[S. 3 (1)]

• LLP is legal entity separate from its partners [S. 3 (1)]

• LLP has perpetual succession [S. 3 (2)]

• Existence, Rights & Liabilities of LLP not affected by change inpartners [S. 3 (3)]

• Indian Partnership Act, 1932 does not apply to LLPs [S. 4]

• Partners

Individuals / Body Corporate can be partners [S. 5]

Minimum two partners [S. 6 (1)]

Maximum unlimited partners

CA. Kamlesh Vikamsey

Nature of Limited Liability Partnership (Ch. II)

• If no. of partners fall below 2 for more than 6 months, and

• Remaining partner has knowledge of such no. of partnersfalling below two for period more than 6 months

• Then remaining partner will be personally liable for liabilitiesincurred by LLP [S. 6 (2)]

7

CA. Kamlesh Vikamsey

Nature of Limited Liability Partnership (Ch. II)

• Designated Partners (DP) [S. 7 (1)]

At least two DPs

Only Individuals can be DPs

At least one resident in India

Every DP to obtain a Designated Partner Identification No. (DPIN)

• Responsibilities & Liabilities of DPs [S. 8]

Responsible for doing all acts, matters & things required to bedone by LLP w.r.t compliance of LLP Act including filing of anydocument, return, statement & like report under LLP Act & asspecified in LLP Agreement

Liable to all penalties imposed on LLP for any contravention ofabove

CA. Kamlesh Vikamsey

Nature of Limited Liability Partnership (Ch. II)

• Changes in DPs [S. 9]

LLP to appoint DP within 30 days of vacancy

If no DP is appointed or if, at any time, there is only 1 DP, eachpartner shall be deemed to be a DP

• Penalty for Contravention [S. 10]

For S. 7 (1): LLP & its every partner shall be fined > Rs. 10,000(Maximum Rs. 5 Lacs)

For Ss. 7 (4) & (5), 8 & 9: LLP & its every partner shall be fined >Rs. 10,000 (Maximum Rs. 1 Lac)

8

CA. Kamlesh Vikamsey

Nature of Limited Liability Partnership (Ch. II)

• Disqualifications of DPs

• R. 9 (1): No person can be DP of LLP, if-

He is adjudged as insolvent within preceding 5 years

He has suspended payment to his creditors & not made any composition with them within preceding 5 years

He is convicted by Court for any offence including moral turpitude & sentenced to imprisonment not less than 6 months

He is convicted by Court for offence under Section 30 of LLP Act

CA. Kamlesh Vikamsey

Incorporation & Incidental Matters (Ch. III)• Incorporation Document [S. 11]

Is among Prime Documents of LLP

Must be submitted to registrar in ‘Form-2’ [R. 11]

S. 11 (2) requires particular information to be contained in IncorporationDocument-

Name of LLP

Proposed Business of LLP

Address of Registered Office (RO)

Names & Addresses of Partners

Names & Addresses of DPs

Other Information as may be prescribed

• RO shall be place of all correspondence for LLP [S. 13 (1)]

On Contravening provisions relating to RO, LLP & its every partner shall bepunishable with fine upto Rs. 25,000 but not less than Rs. 2,000 [S. 13 (4)]

9

CA. Kamlesh Vikamsey

• Effect of Registration [S. 14]: LLP will be able to, in its own name-

Sue & be sued

Acquire, hold & develop or dispose off any property

Have common seal

Do & suffer such other acts & things as bodies corporate may lawfullydo or suffer

• Name of LLP must end with words ‘Limited Liability Partnership’ oracronym ‘LLP’ [S. 15 (1)]

• Change in name of LLP [S. 17]

• Penalty for improper use of words ‘Limited Liability Partnership’ or‘LLP’ [S. 20]

Punishable with fine of Rs. 50,000 but may extend upto Rs. 5 Lacs

• Publication of name, address of RO, Registration No. & Statement oflimited liability [S. 21]

Incorporation & Incidental Matters (Ch. III)

CA. Kamlesh Vikamsey

• Procedure for formation of LLP:

Check availability of name on site ‘llp.gov.in’

Acquire Digital Signature Certificate (DSC)

Acquire DPIN by applying in prescribed ‘Form-7’

Apply for Reservation of Name in prescribed ‘Form-1’

Apply for Incorporation Document in prescribed ‘Form-2’

Alongwith Incorporation Document, submit application for-

Information regarding LLP Agreement in ‘Form-3’

Appointment of Persons and their consent as such to act as Partners/ DPs in ‘Form-4’ & ‘Form-9’, respectively

Receive Form-2 duly signed by Registrar & certificate from registrarregarding incorporation, within 14 days of filing such documents

LLP is ready to function

Incorporation & Incidental Matters (Ch. III)

10

CA. Kamlesh Vikamsey

Incorporation & Incidental Matters (Ch. III)

CA. Kamlesh Vikamsey

Partners & their Relations (Ch. IV)• Eligibility to be partner [S. 22]

Persons who subscribe to Incorporation Document

By LLP Agreement

• Relationship of partners [S. 23]

Rights & duties of partners with other partners & with LLP governed by LLPAgreement

In absence of any agreement, principles set out in First Schedule will apply

• Cessation of Partnership Interest

In accordance with LLP Agreement [S. 24 (1)]

By resignation notice in writing of 30 days [S. 24 (1)]

On death, dissolution of LLP, or if he is of unsound mind or insolvent asdeclared by court [S. 24 (2)]

• Liability of Outgoing Partner [S. 24 (4)]

11

CA. Kamlesh Vikamsey

Partners & their Relations (Ch. IV)• Registration of changes in partners / details of partners to be

filed in prescribed time & in prescribed ‘Form-6’ [R. 22 (1)]

CA. Kamlesh Vikamsey

First Schedule (Ch. IV)Relates to mutual rights & duties between partners & LLP & its partners absence ofAgreement on such matters

• Partners of LLP entitled to share equally in capital & profits / losses

• Partners shall be indemnified by LLP in respect of payments made & liabilitiesincurred by him-

In ordinary & proper conduct of business of LLP

In anything necessarily done for Preservation of business or property of LLP

• LLP shall be indemnified by Partners for any loss caused by his fraud in conduct ofbusiness of LLP

• Partners may participate in management of LLP

• Partners shall not be entitled to any remuneration for acting in business ormanagement of LLP

• No partner may be introduced without consent of all other partners

• Any ordinary matter regarding LLP may be decided by resolution passed bymajority of partners

12

CA. Kamlesh Vikamsey

First Schedule (Ch. IV)• However, change in nature of business may be decided only by consent of all

partners

• Every decision taken by LLP be recorded in minutes within 30 days of suchdecision

• Minute Book be maintained & kept at RO of LLP

• Partners must render true accounts & full information of all things affecting LLP toany partner or his legal representative

• Partners to account for & pay over all profits earned from business of similarnature & competing with LLP, to LLP if there is no consent from LLP in that respect

• Partners to account to LLP for any benefit derived by him without LLP’s consent,from any transaction concerning LLP or from use of name, property or businessconnection of LLP

• No partner may be expelled by a majority unless there is an express powerconferred by LLP Agreement to do so

• All disputes which cannot be resolved by LLP Agreement can be referred to forarbitration as per Arbitration and Conciliation Act, 1996

CA. Kamlesh Vikamsey

Liability of LLP & Partners (Ch. V)• Just like partnership, every partner is an agent; not of other

partners but of LLP [S. 26]

• LLP not bound by unauthorized acts of partners in dealing withperson if that person knows that the partner had no authority ordid not know him to be partner of LLP [S. 27 (1)]

• LLP liable in respect of wrongful acts or omissions of partners incourse of its business or with its authority [S. 27 (2)]

• Obligation of LLP is solely an obligation of LLP & shall be met outof property of LLP [S. 27 (3) & (4)]

• Partners not personally liable [S. 28 (1)]

• Liability of partner(s) committing wrongful acts or omissions willbe unlimited [S. 28 (2)]

• Partnership by Holding out [S. 29]

13

CA. Kamlesh Vikamsey

Liability of LLP & Partners (Ch. V)• Unlimited Liability in case of fraud [S. 30]

If fraud done with knowledge / authority of LLP, LLP’s & partner’sliability will be unlimited. LLP’s liability = Partner’s liability

Otherwise, LLP will not be liable

Imprisonment for 2 years & fine upto Rs. 5 Lacs

• Whistle Blowing [S. 31]

Court / Tribunal may reduce penalty if partner / employee assistsCourt / Tribunal

CA. Kamlesh Vikamsey

Contributions (Ch. VI)• Form of Contribution in any manner- in cash or in kind [S. 32 (1)]

• Accounting & Disclosure of Contribution must also involve thenature & amount of Contribution [S. 32 (2) & R. 23 (1)]

• R. 23 (2): Contribution in kind must be valued by practicing CA orCWA or approved valuer from panel maintained by CentralGovernment

• Obligation to Contribute as per LLP Agreement [S. 33 (1)]

• Creditor may enforce Original Obligation against partner in case ifhe was unaware of compromise between partners [S. 33 (2)]

14

CA. Kamlesh Vikamsey

Financial Disclosures (Ch. VII)• Maintain proper books of accounts as prescribed in R. 24-

Must disclose all sums of money expended & received & matters pertaining thereto

Must record all assets & liabilities of LLP

State all purchases & sales & record all information regarding inventories

Other particulars which partners may decide

• Cash or Accrual; Double-Entry System of Accounting [S. 34 (1)]

• Maintain books at RO for period of 8 years as per R. 24 (3)

• Prepare ‘Statement of Accounts & Solvency’ in prescribed ‘Form-8’ within 6 monthsfrom end of FY & must be signed by DPs [S. 34 (2)]

• Must be filed with ROC alongwith prescribed fees

• Audit as per prescribed rules [R. 24 (8)]

• File annual return (Form-11) with ROC within 60 days from end of FY [R. 25 (1)]

• Must be accompanied by certificate issued by CS confirming veracity of particulars /statements in such return, if turnover exceeds Rs. 5 Crores or Contribution exceeds Rs.50 Lacs, else certificate must be issued by DP [R. 25 (2)]

CA. Kamlesh Vikamsey

Assignment & Transfer of Partnership Rights (Ch. VII)

• Right of partner to share profits is transferable / assignable (inwhole or in part) [S. 42 (1)]

• Transfer does not imply that transferor / assignor has ceased to bepartner [S. 42 (2)]

• Likewise, transferee / assignee does not have right to participatein management [S. 42 (3)]

• Transferee / assignee has no right to obtain any information oftransactions of LLP [S. 42 (3)]

15

CA. Kamlesh Vikamsey

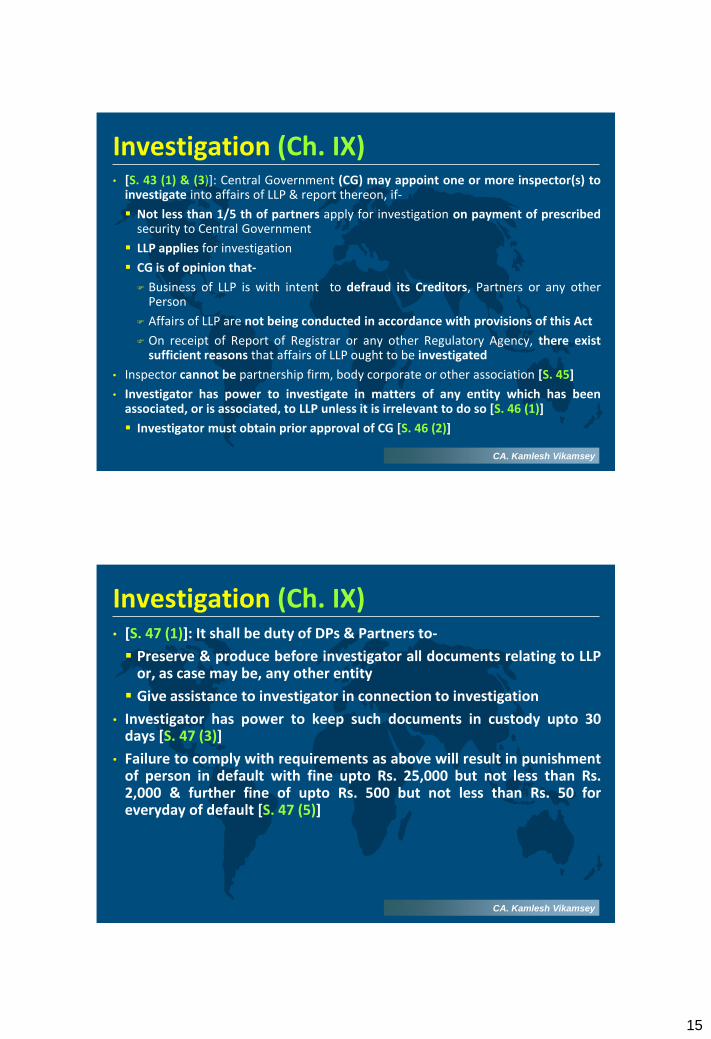

Investigation (Ch. IX)• [S. 43 (1) & (3)]: Central Government (CG) may appoint one or more inspector(s) to

investigate into affairs of LLP & report thereon, if-

Not less than 1/5 th of partners apply for investigation on payment of prescribedsecurity to Central Government

LLP applies for investigation

CG is of opinion that-

Business of LLP is with intent to defraud its Creditors, Partners or any otherPerson

Affairs of LLP are not being conducted in accordance with provisions of this Act

On receipt of Report of Registrar or any other Regulatory Agency, there existsufficient reasons that affairs of LLP ought to be investigated

• Inspector cannot be partnership firm, body corporate or other association [S. 45]

• Investigator has power to investigate in matters of any entity which has beenassociated, or is associated, to LLP unless it is irrelevant to do so [S. 46 (1)]

Investigator must obtain prior approval of CG [S. 46 (2)]

CA. Kamlesh Vikamsey

Investigation (Ch. IX)• [S. 47 (1)]: It shall be duty of DPs & Partners to-

Preserve & produce before investigator all documents relating to LLPor, as case may be, any other entity

Give assistance to investigator in connection to investigation

• Investigator has power to keep such documents in custody upto 30days [S. 47 (3)]

• Failure to comply with requirements as above will result in punishmentof person in default with fine upto Rs. 25,000 but not less than Rs.2,000 & further fine of upto Rs. 500 but not less than Rs. 50 foreveryday of default [S. 47 (5)]

16

CA. Kamlesh Vikamsey

Investigation (Ch. IX)• [S. 48]: Investigator has power to seize documents relating to LLP, if he

believes that such documents may be-

Destroyed

Mutilated

Altered

Falsified or

Secreted

• Investigator shall make reports (Interim & Final) to CG & such reportsuch act as evidence in any legal proceeding [S. 49 & 54]

• Application by CG for Winding-up of LLP pursuant to investigation [S.51]

• Expenses of Investigation [S. 53]

CA. Kamlesh Vikamsey

Conversion of Firm to LLP (Ch. X)This part is governed by Section 55 & Second Schedule & is notified videnotification no. S.O. 1323(E)w.e.f May 31st, 2009

• All partners of LLP must be partners of original firm & no one else

• On such conversion-

All assets & liabilities of firm would get vested in LLP

Firm stands dissolved

Will be removed from records of Registrar of Firms

Every partner will continue to be personally liable jointly & severally withLLP, for liabilities prior to conversion / arising out of contract entered priorto conversion

Partner to be indemnified by LLP in respect of such liability subject toanything contrary in LLP Agreement

• Every official correspondence of LLP for 1 year, must bear a statement that itwas, from the date of registration converted from a firm into an LLP alongwithname & registration, if applicable, of firm from which it was converted

17

CA. Kamlesh Vikamsey

Conversion of Firm to LLP (Ch. X)• Partnership Firm proposing to convert to LLP must apply to ROC in

prescribed ‘Form-17 (Part A)’ alongwith Statement of Partners in‘Form-17 (Part B)’ [R. 38 (1)]

• ROC must issue certificate of registration in ‘Form-19’ [R. 32 (1)]

• Upon receipt of ‘Form-19’, LLP must apply, within 15 days ofregistration, to Registrar of Firms to strike-out name of Firm inprescribed ‘Form-14’ [R. 33 & 38 (3)]

For ‘Conversion of Firm to LLP’, the relevant Rule 38 is notified videNotification no. S.O. 1324(E) dated May 22nd, 2009 w.e.f May 31st, 2009

CA. Kamlesh Vikamsey

Conversion of Companies to LLP (Ch. X)This part is governed by Section 56 (for private companies) & Section 57 (for unlistedpublic companies)

• Governed by Third Schedule in respect of Private Companies

• Governed by Fourth Schedule in respect of Unlisted Public Companies

• Company can be converted into LLP provided-

All partners of LLP must be shareholders of that company & no one else

There is no security interest in its assets

• Upon conversion, all assets & liabilities get vested in LLP and principally all otherprovisions are similar as that for firms

• Listed Public Company cannot be converted into LLP

• Application for conversion to be made to ROC in prescribed ‘Form-18 (Part A)’alongwith Statement of Shareholders in ‘Form-18 (Part B)’ [R. 39(1) & 40(1)]

• Same procedures as regards conversion of Firms

Above referred Sections & Relevant Schedules are notified vide notification no. S.O.1323 (E) w.e.f May 31st, 2009

For ‘Conversion of Companies to LLP’, the relevant Rules 39 & 40 are notified videNotification no. S.O. 1324(E) dated May 22nd, 2009 w.e.f May 31st, 2009

18

CA. Kamlesh Vikamsey

Foreign LLPs (Ch. XI)• Foreign Limited Liability Partnerships [S. 59]

LLP Act gives power to CG to make rules for establishment of place ofbusiness of Foreign LLPs & conduct of business

Rules regarding setting up of Foreign LLPs in India is provided inChapter XI of LLP Rules, 2009

• R. 18 (3) provides that Foreign LLPs may reserve name by which they areknown in their country by application in ‘Form-25’

This reservation will be valid for 3 years & must be renewed

• R. 34 (1) provides for application to be filed with ROC alongwithprescribed documents in prescribed ‘Form-27’ within 30 days fromestablishment of business in India

• Every Foreign LLP must file Statement of Accounts & Solvency in ‘Form-8’ within 30 days from end of 6 months of FY [R. 34 (4)]

CA. Kamlesh Vikamsey

Compromise, Arrangement or Reconstruction of LLPs(Ch. XII)• Compromise or Arrangement of LLPs [S. 60]

• Power of Tribunal to enforce Compromise or Arrangement [S. 61]

• Provisions for Reconstruction or Amalgamation of LLPs [S. 62]

19

CA. Kamlesh Vikamsey

Winding Up and Dissolution (Ch. XIII)This Chapter has not been notified as yet

• Winding Up and Dissolution [S. 63]

• Circumstances of Winding Up [S. 64]

• Rules relating therein [S. 65]

CA. Kamlesh Vikamsey

Miscellaneous (Ch. XIV)• Transactions of Partner with LLP [S. 66]

Partner who transacts or lends money to LLP has same rights &obligations as aperson who is not partner

• Application of provisions of Companies Act [S. 67 & Q. 55 of FAQs]

• E-Filing of Documents [S. 68]

• Payment of Additional Fee [S. 69]

• Enhanced Punishment [S. 70]

• Application of Other Laws not barred [S. 71]

• Jurisdiction of Tribunal & Appellate Tribunal [S. 72]

• Offences & Penalties [Ss. 73, 74 & 76]

• Powers of Registrar to Strike-off names of Defunct LLPs [S. 75 & Q. 53 of FAQs]

• Jurisdiction of Courts [S. 77]

• Miscellaneous Powers to make Rules, amend Schedules & remove difficulties [Ss. 78,79 & 80]

• Transitional Provisions [S. 81]

20

CA. Kamlesh Vikamsey

Some Issues• Companies can apply for conversion only if there is no Security

Interest on its assets

• Why introduce a restrictive clause in case of Companies?

CA. Kamlesh Vikamsey

Some Issues• According to S. 71, provisions of LLP Act will not be in derogation

to provisions of other Acts

• The question which arises is as to whether CAs are allowed toform LLPs or convert their firms into LLPs?

• As per Chartered Accountants Act & Regulations, at variousplaces, the words ‘partnership’ & ‘firm’ are used withoutassigning any particular meaning to it

• Will a LLP meet the requirements of CA Act & Regulations?

• This would require amendments to certain Acts which arerelevant to professional services [Q. 56 of FAQs]

21

CA. Kamlesh Vikamsey

Some Issues• If firm of CAs convert into LLP, what will be auditee’s stand?

• Does conversion amount to ‘Casual Vacancy’ as per CompaniesAct?

• Would another resolution be required to appoint an LLP asauditors?

• As per Clause 14 of Second Schedule, appointment of firm in anyrole or capacity shall operate as if LLP was appointed

Effect of such Clause?

• Some clarifications / amendments are required in the CompaniesAct

CA. Kamlesh Vikamsey

Some Issues• S. 36 of LLP Act provides for inspection of all documents including

Statement of Accounts & Solvency filed by LLP with ROC, by anyperson

• Question arises as to whether this is acceptable to ProfessionalFirms like lawyers, CAs, CWAs, etc?

22

CA. Kamlesh Vikamsey

Some Issues• The LLP Act has incorporated procedures for conversion of

companies to LLP by way of Third & Fourth Schedules

• However, there is no procedure for LLPs to be converted tocompanies

• Amendments required to be made in this regard in Companies Act[Q. 46 of FAQs]

CA. Kamlesh Vikamsey

Some Issues• As per Clause 5 of Second Schedule, LLP, upon receipt of ‘Form-

19’ from ROC must submit an application to concerned Registrarof Firms in prescribed ‘Form-14’ for striking-out name of Firmfrom its Records

• Is this required in case of Unregistered Firms?

23

CA. Kamlesh Vikamsey

Some Issues• Whether Stamp Duty is payable on Incorporation of LLPs?

• If so, how much?

• Whether Companies & Firms will be exempt from Stamp Dutiesupon conversion to LLPs?

• It must be noted that Stamp Duties are legislations of respectiveStates & therefore clarity is needed from them [Q. 47 of FAQs]

CA. Kamlesh Vikamsey

Comparison with CompaniesBasis Company LLP

Governing Law Companies Act, 1956 Limited Liability Partnership Act,2008

Name Must contain suffix ‘Ltd’ or ‘PvtLtd’

Must contain suffix ‘LLP’

Common Seal Common Seal is compulsory Common Seal is optional

OrganizationalStructure

Rigid & governed by CompaniesAct

Flexible & governed by LLPAgreement

Appointment ofAuditors

Specific Resolution required forappointment of auditors at everyAGM

Auditors shall be deemed to be re-appointed in case no specificappointment is made (unlessotherwise decided)

Audit All companies are subject to auditof accounts

Only LLPs having turnover of morethan Rs. 40 Lacs or contribution ofmore than Rs. 25 Lacs are subject toaudit of accounts

24

CA. Kamlesh Vikamsey

Comparison with Partnership FirmsBasis Partnership Firms LLP

Governing Law Partnership Act, 1932 Limited Liability Partnership Act,2008

Registration Not Compulsory; but is preferred Compulsory

Creation By partnership Agreement By Law

Legal Status Partners collectively known as‘Firm’; no separate legal status

LLP has separate legal status apartfrom partners

Succession Firm would cease to exist onchange in partnership, unlessotherwise provided in agreement

LLP would not be affected on changein partnership (PerpetualSuccession)

Ownership ofAssets

Partnership cannot own assets inits name; assets must be in nameof Partners

LLP can own assets in its own name

Liability of Partners

Unlimited Limited

Minor’s Position Minor can be admitted to benefitsof Partnership

Law silent on position of Minors

CA. Kamlesh Vikamsey

Taxation of LLPs• Tax treatment of LLPs to be same as that of ‘Partnership Firms’

• S. 2 (23) of Income Tax Act, 1961 (IT Act) to include ‘LLP’ & its ‘Partners’

• Partner’s share of profit will be exempt [S.10 (2A) of IT Act]

• Partner’s remuneration will be subject to newly proposed limits-

• DPs must verify & sign on Income Tax Returns. In absence of DPs, anypartner must sign & verify [S. 140 of IT Act]

• In case LLP is wound up, every partner will be liable for payment of taxesdue unless he can prove that non-recovery cannot be attributed to hisacts [S. 167C of IT Act]

Slab of Book Profit Remuneration Allowable

On first Rs. 3 lacs or in case of loss Rs. 1.5 lacs or 90% of book profits, whichever is higher

On balance of book profit 60% of book profits

25

CA. Kamlesh Vikamsey

Taxation of LLPsTax implications on conversion of partnership firm / company to LLP

• No specific provision introduced in Income-tax Act for this

• Memo explaining Finance (No.2 Bill) 2009 mentions that:

As a LLP & a general partnership firm is being treated as equivalent(except for recovery purposes) in the Act, the conversion from ageneral partnership firm to LLP will have no tax implications if :

the rights and obligations of the partners remain the same afterconversion &

if there is no transfer of any asset or liability after conversion

No mention on tax implications on conversion of company into LLP

CA. Kamlesh Vikamsey

Taxation of LLPs• Provisions in IT Act, 1961 relating to companies are not applicable

to LLPs:

LLPs not liable to DDT u/s 115-O

LLPs not liable to MAT u/s 115JB

Deemed Dividend u/s 2 (22) (e) is not applicable

S. 79 on ‘Carry forward & Set-off of Losses in certain cases’ isnot applicable

• LLPs not liable to pay surcharge on income tax like firms

26

CA. Kamlesh Vikamsey

Recent Notification

• Company Law Board notified to address all appeals against refusalto register LLPs upon conversion till such time National CompanyLaw Appellate Tribunal (NCLAT) is constituted

[vide Notification no. G.S.R. 385 (E) and 386 (E) dated June 4th,2009]

CA. Kamlesh Vikamsey

In case of any difficulty…Office of the Registrar

Limited Liability Partnerships

Ministry of Corporate Affairs,

3rd Floor, “Paryavaran Bhawan”,

CGO Complex, Lodhi Road,

New Delhi (India)- 110003

Phone - +91-11-24362189

Email: [email protected], [email protected]

27

CA. Kamlesh Vikamsey

Thank you…