Limited Partnerships and Limited Liability Companies Chapter 33.

24

Limited Partnerships and Limited Liability Companies Chapter 33

-

Upload

beverley-dickerson -

Category

Documents

-

view

221 -

download

0

Transcript of Limited Partnerships and Limited Liability Companies Chapter 33.

Limited Partnerships and Limited Liability Companies

Chapter 33

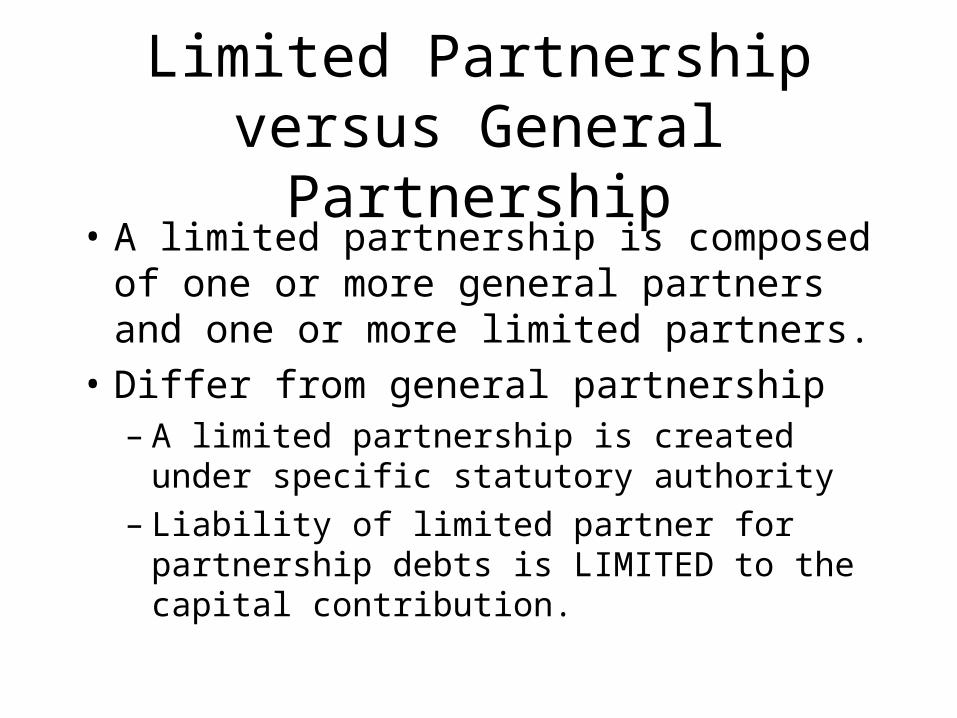

Limited Partnership versus General Partnership

• A limited partnership is composed of one or more general partners and one or more limited partners.

• Differ from general partnership– A limited partnership is created under specific

statutory authority– Liability of limited partner for partnership debts

is LIMITED to the capital contribution.

Formation• File a Certificate of Limited Partnership

– Name & address of limited partnership and of the general partners (not of limited partners); agent for service of process; latest date for dissolution

• Affidavit declaring the limited partner’s capital contributions

• Written, signed partnership agreement

• May contribute cash, property, services or promissory notes

• Admission of additional limited partner after formation

requires written consent from all partners. • Can’t use limited partner’s surname in partnership name

• Partnership’s name must contain Lmtd., or Limited

Defective Formation• Defective if a ailure to file a certificate of

limited partnership, or if the certificate does not substantially meet the statutory requirements.

• The possibility exists for liability as a general partner UNLESS– limited partner files a corrected certificate or an

amendment curing the defect; or– limited partner withdraws from the business and

renounces his interest in the partnership’s future profits.

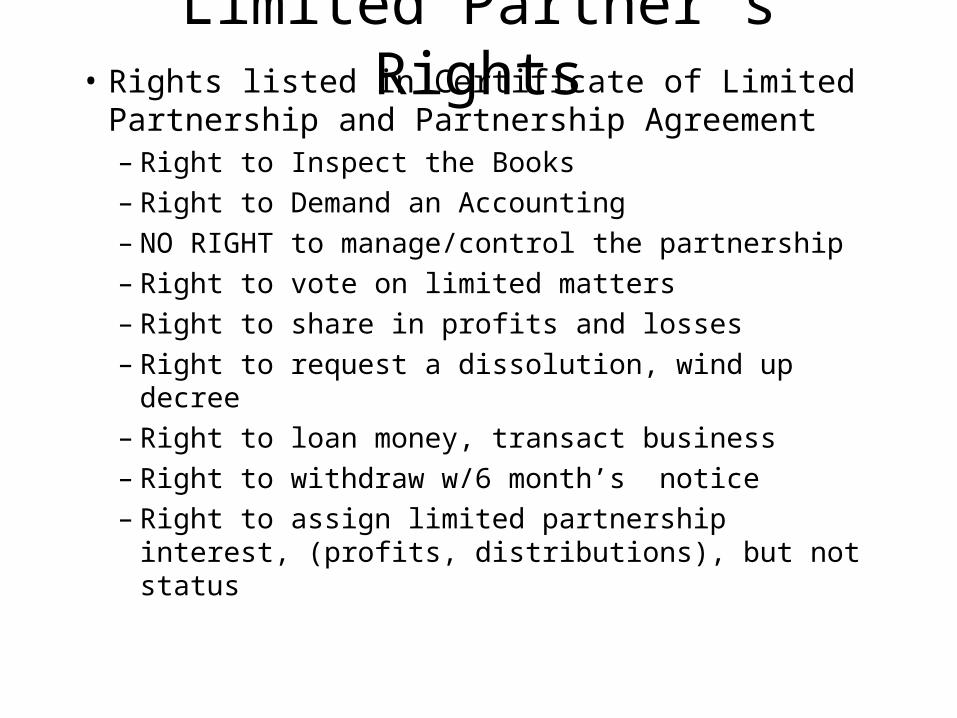

Limited Partner’s Rights• Rights listed in Certificate of Limited

Partnership and Partnership Agreement– Right to Inspect the Books– Right to Demand an Accounting– NO RIGHT to manage/control the partnership– Right to vote on limited matters– Right to share in profits and losses– Right to request a dissolution, wind up decree– Right to loan money, transact business– Right to withdraw w/6 month’s notice – Right to assign limited partnership interest, (profits,

distributions), but not status

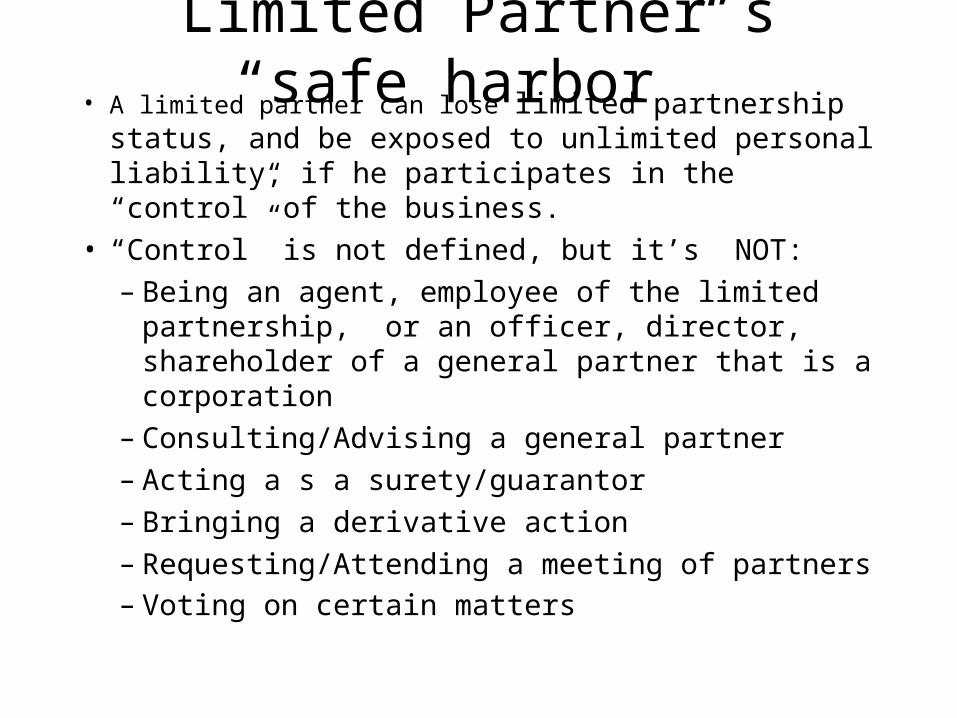

Limited Partner’s “safe harbor” • A limited partner can lose limited partnership status, and

be exposed to unlimited personal liability, if he participates in the “control” of the business.

• “Control” is not defined, but it’s NOT:– Being an agent, employee of the limited

partnership, or an officer, director, shareholder of a general partner that is a corporation

– Consulting/Advising a general partner– Acting a s a surety/guarantor– Bringing a derivative action– Requesting/Attending a meeting of partners– Voting on certain matters

Limited Partners May Vote on Extraordinary Matters

• Dissolution/winding up

• Amendment of partnership agreement or certificate of limited partnership

• Sale, lease, mortgage, exchange of all or substantially all of the partnership’s assets.

• Admission/Removal of ANY partner

• Any matter involving a potential conflict of interest b/w a partner and the limited partnership

• A change in the nature of the business

• Incurrence of debt other than in the ordinary course of business.

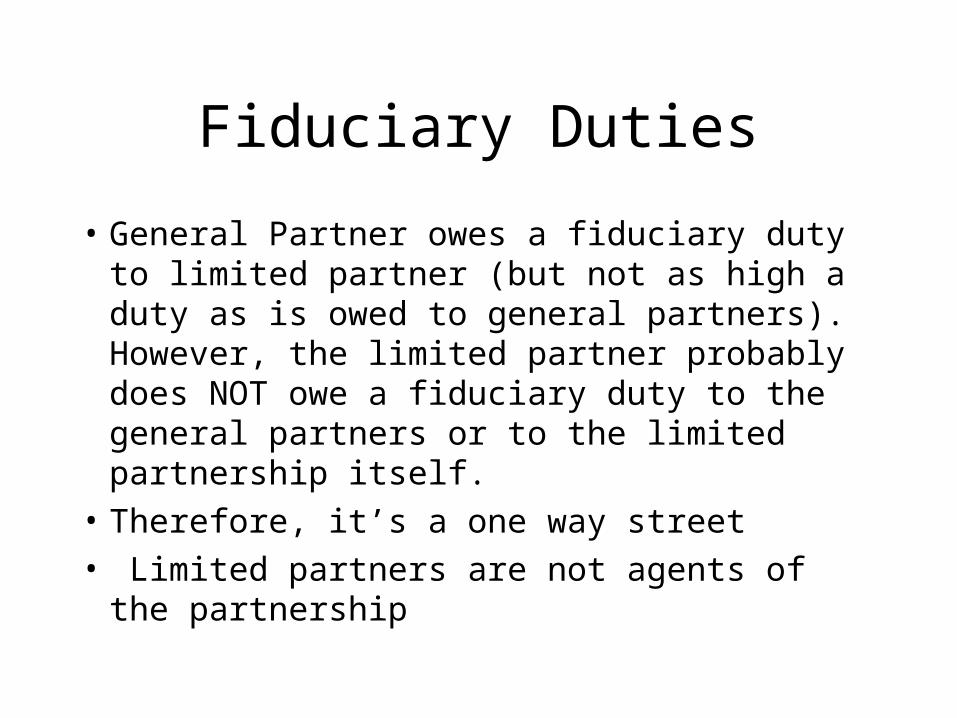

Fiduciary Duties

• General Partner owes a fiduciary duty to limited partner (but not as high a duty as is owed to general partners). However, the limited partner probably does NOT owe a fiduciary duty to the general partners or to the limited partnership itself.

• Therefore, it’s a one way street• Limited partners are not agents of the

partnership

Sharing of Profits and Losses

• Allocated according to the Partnership Agreement.

• If Agreement is silent, profits and losses are allocated on the basis of the value of the contributions made by each limited partner.

• Contrary to the UPA & the rule for general partnerships which, unless the Agreement states otherwise, divides profits and losses equally...regardless of contributions

Liability• Limited Partners are liable only up their

capital contributions. • Limited partnership status could be lost upon:

defective formation; improper participation or control in the business; or, if a limited partner uses his surname in the partnership’s name.

• Liability for a false statement in the Certificate could extend to anyone who relied on the certificate.

Distributions

• Limited Partners may receive a share of the profits or other compensation, provided that after such payment, partnership assets are in excess of all liabilities to creditors.

• May receive a share in a proportion different than the way they share profits.

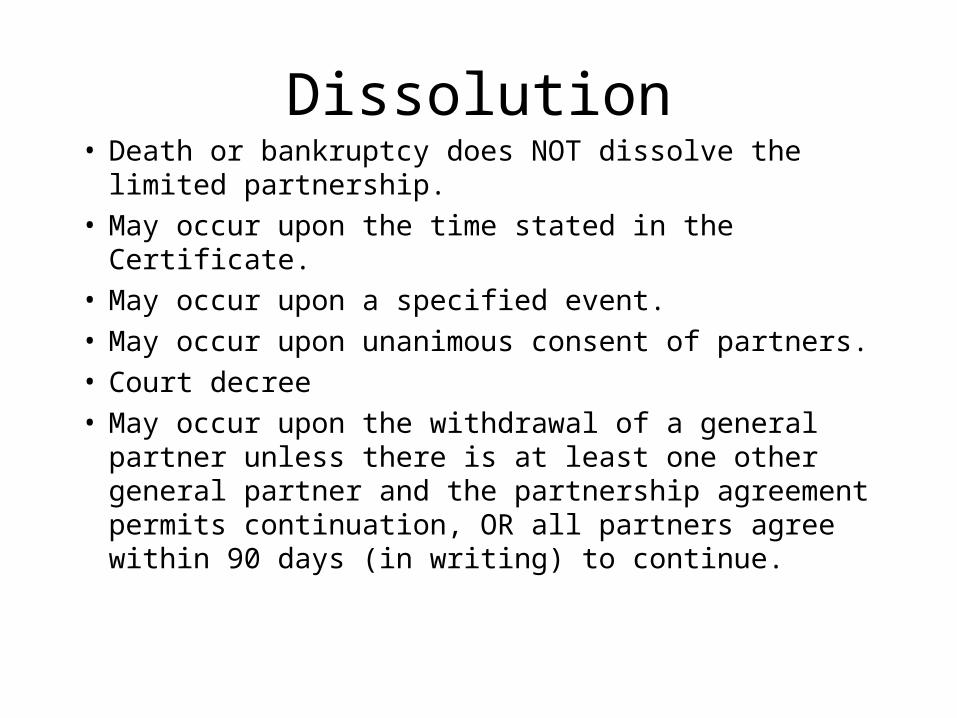

Dissolution• Death or bankruptcy does NOT dissolve the limited

partnership.

• May occur upon the time stated in the Certificate.

• May occur upon a specified event.

• May occur upon unanimous consent of partners.

• Court decree

• May occur upon the withdrawal of a general partner unless there is at least one other general partner and the partnership agreement permits continuation, OR all partners agree within 90 days (in writing) to continue.

Distribution of Assets Upon Winding Up

• In settling accounts, the liabilities of the limited partnership shall be paid in the following order:– 1. Creditors, including limited partners for loans– 2. Limited partners for undistributed profits and

compensation– Limited partners for capital contributions.– General partners for loans– General partners for profits– General partners, for capital contributions

Limited Liability Companies• Hybrid of corporate and partnership characteristics • Partners are called members (owners) and they can

participate in management and control of business.

• Neither members nor managers personally liable for company debts; creditors must look to assets of the company. But, a manager may be personally liable to LC or third parties if a violation of criminal law, manager derives an improper personal benefit, willful misconduct, malicious purpose, willful disregard of human safety.

Formation

• Some states allow only one member; Florida requires at least TWO members.

• Filing of Articles of Organization

• Identify status by using the words “limited liability company”

• Contribution by cash, property, services rendered or promissory note.

Tax Consequences• Special tax treatment with losses passing through to shelter

investors’ other income under the federal income tax laws, and qualifies for taxation as a partnership (interest is considered personal property).

• Fails 2 of the 4 essential tests for “corporateness”– Does NOT meet continuity of life test.– Does NOT meet the free transferability test. LC

member’s interest & rights to profits/losses can be assigned ONLY upon consent of nonassigning members. Assignee can become member upon unanimous consent.

– May or may not meet centralized mgmt test.Mgmt of LC is vested in proportion to capital contributions but Articles may provided otherwise (1 member, 1 vote) or vest mgmt. in a manager elected annually by members.

– Meets lmtd. liability test; C’s can’t sue members.

Membership Rights• Operating Agreement states profits & losses.

If silent, it’s based on members’ contributions.

• Service of process may be served upon any “member”

• Power to elect managers (agents) who have authority to contractually bind the LC (manager-managed LC).

• If the articles vest management in its members, any one member may incur indebtedness or otherwise bind LC.

LLC Enjoys Powers Accorded Corporations

• Governed by internal by laws

• Msy sue or be sued in its own name

• Acquire/dispose of real & personal property.

• May hold title in its own name

• Make donations (scientific, charitable, etc.)

• May be a general or limited partner

• Able t appoint agents to bind company

Dissolution of LC

• Expiration of period of duration

• Unanimous written consent of all members

• Death, retirement, Expulsion of any member, unless business is to continue as designated within the Articles.

• (In Florida), when LC has less than 2 members

Limited Liability Partnerships• A general partnership which, by making a

statutory filing and becoming a registered limited liability partnership, limits the individual liability of its partners for obligations or liabilities of the partners (tort, contracts or otherwise) “arising from errors, omissions, negligence, malpractice, or wrongful acts committed by another partner or by an employee or agent of the partnership

Formation

• Name must contain words, “Registered Limited Liability Partnership” or “L.L.P” and name must be recorded with Dept. of State.

• Registration: name, address, description of business, effective date of partnership

• Fee of $100 per partner.

• Insurance

Insurance

• A copy of the insurance policy demonstrating the partnership carries at least the minimum coverage amount of liability insurance to cover errors, omissions, negligence, malpractice, wrongful acts.

• An affidavit sworn by a majority of partners that partnership has minimum coverage amount in funds to satisfy judgments.

• The minimum coverage amount is $100,000 multiplied by a number of general partners in excess of one, but in no event less than $200,000 or greater than 3 million.

Exceptions to Limited Liability• A partner in a registered limited liability partnership is

individually liable for:

– any errors, omissions, malpractice, wrongful acts committed by THE PARTNER HIMSELF or any person under the partner’s direct supervision and control in the activity of which the act occurred.

– Any debts for which the partner agreed in writing to be liable.

– If LLP is omitted from the name, any person who participates in or consents to omission is liable for damages occasioned by omission (but, there will be no liability if the claimant should have had actual notice that partnership was a LLP.)

Limited Liability Limited Partnerships

• Limited Partnership in which the liability of the general partner has been limited to the same extent as in an LLP.

• Not in Florida (?)