Investment horizons v2 - pionline.com

36

For Financial Intermediary, Institutional and Consultant use only. Not for redistribution under any circumstances. Research Insights at Schroders: – An intro to Carbon VaR – Income and rising rates – Does portfolio turnover lead to lower returns? – The end of LIBOR – Global Cities Index – Finding value in the securitized real estate market Investment Horizons Fall 2017

Transcript of Investment horizons v2 - pionline.com

For Financial Intermediary, Institutional and Consultant use only. Not for redistribution under any circumstances.

Research Insights at Schroders: – An intro to Carbon VaR – Income and rising rates – Does portfolio turnover lead to lower returns? – The end of LIBOR – Global Cities Index – Finding value in the securitized real estate market

Investment HorizonsFall 2017

Perspectives on measurement

We are pleased to off er Investment Horizons, a compilation of our latest research articles inspired by our global client engagements. In this edition we elected to focus on diff erent ways that investors gauge their investments.

As active managers, we’re always beholden to a standard much higher than any common benchmark index. So we’ve compiled articles that offer insights and, in certain cases, counterpoints to widely held views on a variety of investment measures.

Our fi rst article is on Carbon VaR, a new way to look at the investment risks to global equities as a result of the growing impact of climate change.

The next two articles provide perspective on the misconception that income investments always suffer during a rising rate environment, and that high turnover always means lower performance. Our research uncovers some interesting fi ndings.

Our Head of Credit Research offers his views on the recent announcement by the FCA to sunset LIBOR in 2021, a benchmark rate to which literally trillions of dollars of investments are pegged on a regular basis. Our Global Real Estate team provides a potentially better way to think about real estate investment with the Schroders Global Cities Index.

Our last article focuses on a specialized segment of the asset-backed market – US commercial real estate, or CMBS. Here, we see that some investors may be ignoring the lessons learned 10 years earlier and reaching for yield for the sake of familiarity – overlooking the true value in the private loans market.

We hope this edition provides some differentiated insights. As always, if there is anything you would like to discuss further, please contact your local Schroders representative.

Contents

4Carbon Value at Risk: the next generation of climate risk management – by Andrew Howard and Ovidiu Patrascu

With the signifi cant threat that higher carbon prices may have on companies’ future earnings and value, we have developed an alternative measure, Carbon Value at Risk, which provides a systematic and objective guide to better managing this risk.

24The King has no clothes: LIBOR’s procession is coming to an end – by David Knutson and Harold Thomas

LIBOR is a critically important reference rate for a substantial portion of the credit markets and the $350 trillion of fi nancial products that are priced off LIBOR. In our view, its imminent sun-setting and replacement by the end of 2021 is a matter worth following.

10Rising rates, reduced returns? – by Clement Yong

Investors in income yielding assets have become nervous that returns will be impaired if rates rise in the future. Our analysis shows that these concerns may be overdone as most income assets historically continued to generate positive returns during periods of rising rates. With income investing, patience is the key.

14Churn is not necessarily burn: debunking the myths of portfolio turnover – by Duncan Lamont and Kristjan Mee

There is a widely held assumption that portfolio turnover results in poorer outcomes for investors as a result of the additional costs it incurs. Our research challenges that simplistic assumption by instead focusing on added value net of costs.

28Global Cities: the future of real estate – by Hugo Machin and Tom Walker

It’s no secret that the world is urbanizing. The world is moving away from sovereign borders and, in our view, becoming defi ned by economically powerful Global Cities. Real estate investors can tap into this trend by being exposed to these huge and growing points of consumption.

31Fool’s gold: mining for “true” value in the US Commercial Real Estate Debt Market – by Michelle Russell-Dowe and Jeff rey Williams

The concept of proper compensation for risk should have been the primary lesson learned post global fi nancial crisis. But it would seem that the market has lost its memory and many investors are now combing through riskier securities in a search for yield. In many cases, we believe investors will end up with “fool’s gold”.

Carbon Value at Risk: the next generation of climate risk management

Introducing Carbon Value at RiskCarbon pricing looks likely to remain a key element of government climate policies for some time to come, with implications that will become much bigger as prices inevitably climb from the low levels of recent years. Large and widespread effects on competitiveness, cash fl ows and value are almost inevitable.

Most of our industry has not progressed far in examining, measuring or managing these risks. Carbon footprints remain the dominant measure of exposure, but at best provide an incomplete and at worst a misleading picture of the risks carbon pricing presents. We have developed an alternative measure, Carbon Value at Risk, which provides a systematic and objective guide to the risks to portfolios by analyzing the effect of higher carbon prices on companies’ earnings and value.

With Carbon VaR, we can model the effects of higher carbon prices on industry profi t pools, combining the impact of rising costs and indirect supply chain pressures, how both will be passed to the customer through higher prices and the consequences for customer demand. While simplifi ed, it refl ects a realistic view of the ways industries work, unlike measures such as carbon footprints that don’t even attempt.

Carbon footprints or Achilles heelDespite our many concerns about the usefulness of carbon footprints as a gauge for climate risk, they remain the measure our clients ask for most often. It is important to understand where they come from, what they represent and their weaknesses.

Carbon footprints are an attempt to compare the “carbon intensity” of different businesses by dividing reported or estimated “scope 1” and “scope 2” GHG emissions by either sales or market capitalization.1 Scope 1 emissions are those generated by the operations companies own and scope 2 emissions are those created to generate the power companies consume.2

Investors take the intensities calculated for individual companies and combine them using holding weights to arrive at overall portfolio values.

Intensities calculated using sales are a reasonable measure of how effectively companies manage the carbon effi ciency of their operations. They represent the emissions generated by activities within companies’ control – from their own facilities or their power use – relative to output levels. However, management effort is different to investment risk.

Intensities calculated using market capitalization are a cleaner measure of the emissions associated with investment in a fund. They represent the emissions attributable to a dollar investment in a portfolio. However, the effect of those emissions on companies’ earnings or values depends more on its business model, cost structure, industry dynamics and pricing power than on its carbon footprint. Value-based measures also introduce challenges comparing companies with different reliances on debt and equity.

The main attraction of carbon footprints is their apparent simplicity and consistency. Closer inspection highlights signifi cant variations in the estimates different research fi rms make for the same companies. These differences result from the need to estimate carbon intensities of companies which do not report GHG emissions. On average, only around 40% of large global companies report scope 1 or 2 emissions. Estimates are used for most large companies and results are therefore sensitive to the methodologies different fi rms use.

Carbon footprints remain the dominant measure of exposure, but at best provide an incomplete – and at worst a misleading – picture of the risks carbon pricing presents. We have developed an alternative measure, Carbon Value at Risk (VaR), which provides a systematic and objective guide to the risks to portfolios by analyzing the eff ect of higher carbon prices on companies’ earnings and value. Importantly, applying Carbon VaR to global equity markets highlights the scale of the risk as our modelling shows that around 20% of the cash fl ows global companies generate could be lost if carbon prices rose to $100/ton.

Andrew Howard,Head of Sustainable Research

Ovidiu Patrascu,Sustainable Investment Analyst

1 Almost all methods of calculating carbon footprints will provide outputs using both measures. Where companies report scope 1 or 2 emissions, those values are used. Where they are not, values are typically estimated based on companies’ activities and sometimes geographic domiciles, and those estimated values are used. Estimation methods can vary signifi cantly. GHG refers to greenhouse gas.2 Scope 3 emissions include those produced by all of a company’s suppliers (other than electricity providers) and those created when using the company’s products. Scope 3 emissions are rarely included in carbon footprint calculations; they are not widely disclosed and calculation methods can be very inconsistent.

4 Carbon Value at Risk: the next generation of climate risk management

We have looked at three of the most common footprint methods, (i) MSCI’s carbon intensity analysis, (ii) estimates by the CDP climate information group covering companies in high impact sectors and (iii) sector average intensities for those companies which do not report data, variations of which are used by many fi rms.

There is little relationship between the three methods. More than one-third of CDP’s estimates are over 50% higher or lower than MSCI’s values. Almost one-half of the sector-based estimates are similarly wide of MSCI estimates. The median difference between different estimates of carbon footprints for companies which do not report emissions is 40 ton/$million, a signifi cant difference equal to approximately a quarter of the average company’s carbon footprint.

Given signifi cant differences in the footprints of each sector, sector allocation choices rather than stock selection determine over 80% of a typical fund’s carbon footprint. As a result, fund carbon footprints are highly sensitive to sector exposures. All this means that, while we recognize the ubiquity of carbon footprints, we would caution against either trying to compare funds calculated using different methodologies or relying on those footprints as a measure of portfolio climate risk.

More emissions are being priced, but costs are yet to riseCarbon pricing has expanded signifi cantly over the last 10-15 years. The number, stringency and economic impact of carbon markets have increased signifi cantly. Of the main ways to put a price on carbon, emissions trading schemes (ETS) represent two thirds, with carbon taxes making up the balance.3

Most schemes focus on carbon intensive sectors, but their scope is expanding to other industries. They are also expanding geographically to cover a signifi cant proportion of the world’s GHG emissions.

While the reach of carbon pricing schemes across global industries is spreading, their economic impact remains very limited. The current price of carbon implied by dividing the value of global emission markets by their volume stands at roughly $1.60 per ton of CO2. That is low. Data from the IEA implies that a barrel of oil creates 0.43 ton of CO2 in use. At current carbon prices, this values the CO2 contained in a barrel at less than $0.70, or under 2% of the average Brent crude price over the last year and approximately equal to its average daily fl uctuation. Prices on many individual carbon exchanges are higher, but still far too low to play a meaningful role in most companies’ strategic planning. Carbon prices will have to rise signifi cantly if governments are serious about honoring their collective commitment to limit temperature rises to 2°C over pre-industrial levels, or even hitting their own less ambitious national targets.

The usual approach to estimating how far carbon prices might rise relies on marginal abatement costs. These represent the carbon price at which different technologies deliver a positive return on investment.4 Lining technologies up from the least to the most attractive and fi nding the price needed to prompt enough GHG emission cuts to hit certain warming targets forms the basis for price projections using this technique.

It is a blunt approach and conclusions are indicative rather than precise estimates of the likely scale of increases. The chart in Figure 1 plots projections of the carbon prices needed to deliver emissions cuts in line with three possible temperature trends. These estimates are based on analyses by international and intergovernmental organizations, most of which use similar incentive price approaches. All point to a sharp rise in prices in the future.

Figure 1: Carbon prices would need to rise signifi cantly to meet the 2-degree target

Source: Historical data based on Point Carbon estimates of global carbon market values and BP emissions estimates; average prices divide the latter by the former. Forecasts based on estimates by intergovernmental organizations, including IEA, OECD and World Bank. Based on analyses available as of May 2017.

Increases on the scale implied by the chart – anywhere from $50 to $140 a ton – may appear ambitious, but the point of carbon pricing is to rebalance industry economics enough that they will incentivize signifi cant changes. That will only be achieved with prices high enough to drive big shifts in cash fl ows and value. It is therefore unsurprising that increases in carbon prices on the scale our analysis implies will have big impacts on growth and profi tability across many industries.

In previous research notes, we have highlighted the growing competitiveness of many clean technologies, such as renewable power, but given electricity generation represents around one quarter of total GHGs, it’s clear that policy changes will be needed to deliver changes on the scale required.

The methodology behind our Carbon VaRThe effects of applying higher prices to CO2 emissions will clearly be both dynamic and complex in ways carbon footprints cannot capture. That is why we have developed a systematic model capturing the impacts of each of these steps on the cash fl ows of global companies. The illustration in Figure 2 on the next page describes these steps in a hypothetical industry of three companies. It shows the changes in cash earnings as higher carbon prices reverberate across company and industry cost structures.

3 In emissions trading schemes, governments impose caps on total emissions by requiring companies to submit allocations for each ton of CO2 equivalent they emit, thereby allowing market forces to establish prices for those emission allocations. This ensures that allocations are used by the companies that value them most highly. Carbon taxes typically impose direct taxes at a fi xed price on companies’ emissions.4 McKinsey & Vattenfall produced the fi rst widely used marginal abatement curve (http://www.mckinsey.com/business-functions/sustainability-and-resource-productivity/our-insights/a-cost-curve-for-greenhouse-gas-reduction), although many others have been developed since using similar approaches.

Historical average price 6° path2° path 4° path

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

160140120100

80604020

0

US$/ton

5Carbon Value at Risk: the next generation of climate risk management

Figure 2: Modelling carbon pricing risks properly can create surprising results

For illustration only. Source: Schroders as of August 2017.

Modelling those steps relies on more information than companies report. We have therefore developed an estimating process to capture the three key variables:

– Emissions: We estimate the emissions needed to create each dollar of revenues by combining the three main sources of emissions:

– scope 1 from companies’ own operations

– scope 2 from the power they purchase

– scope 3, emissions released by other companies in their supply chains.

As discussed earlier, the fi rst two are fairly well reported, but the third is very rarely disclosed. We estimate suppliers’ emissions using input-output tables,5 which measure each industry’s reliance on inputs from other industries. All three sources are important in gauging companies’ exposures.

– Price: We apply a single global price to all carbon emissions, although in practice there are likely to be differences across regions and industries, even if pricing is becoming more co-ordinated.

– Demand effects: We use academic estimates of price elasticity in representative industries to estimate falls in demand as prices rise to offset industry costs.

By looking at the interaction of these factors at a company level, we can gauge the effect on fi nancial performance. For most it will lower profi ts, but for a few the introduction of a carbon price will raise returns. It is important to include all greenhouse gas emissions required to produce and sell a product, which conventional measures of carbon exposure (like the carbon footprint) do not.

Often it is those other supply chain emissions that are the most signifi cant. Indeed, in most industries, they are a much larger proportion of sales than the scope 1 and 2 emissions most analyses focus on (Figure 3).

We apply that framework to a global universe of listed companies. Figure 4 shows the scale of the impact on corporate revenues and cash earnings. The effect is material: carbon prices of $100/ton would result in about 20% of the cash earnings of listed companies being lost through the combination of forces included in our model.

Figure 3: Often most of the carbon is in the supply chain

Source: Schroders analysis based on ICB, BEA, SIC and Thomson Reuters data, as of December 2016.

Figure 4: The likely impact of raising carbon prices on the earnings of listed global companies

Based on pro-forma modelled impact on 2014-16 average earnings before interest tax and depreciation (EBITDA). Source: Schroders, as of December 2016.

We tested the model by asking what the demand effects would be of raising carbon prices to $100/ton. It showed a 30% reduction in the carbon emissions of global companies through volume cuts. This falls short of political targets, but is close enough that

Sector-based vs MSCI methodology

Direct and supplycosts rise as carbon

prices increase…

…so companiesraise prices to

offset the effect…

…which reducesvolumes…

…and leaves somecompanies’ margins up

and others down

Margins downSales before

Sales after

Margins unchanged

Direct operating costs

Supply chain costs

Direct operating costs

Supply chain costs

Direct operating costsSupply chain costs

Margins up

Com

pany

ACo

mpa

ny B

Com

pany

C

Indirect DirectOther supply chain (share total shown as %)

Con. ElectricityIron & Steel

Integrated Oil & GasExploration & Prod.

Food ProductsSpecialty Chemicals

Food Retail, WholesaleDivers. Industrials

AutomobilesBroadline Retailers

Heavy ConstructionPharmaceuticals

Drug RetailersMobile Telecom.

Fixed Line Telecom.Computer HardwareHealthcare Providers

BanksLife Insurance

Full Line Insurance

Ton per $m sales

3,5003,0002,5002,0001,5001,0005000

Carbon intensity of 20 largest industries

5 We use a similar approach to the Carnegie Mellon Green Institute (http://www.eiolca.net/), which tracks the fl ow of resources between economic sectors. Analysis is based on US sectoral economic data from the BEA, but we believe it is representative of global industries.

US$tr8

7

6

5

4

3

2

1

0Volumesdecline

EBITDAwith

$100/tcarbon

Carbon cost

increase

Carbon costs fully passed on through price increases in aggregate,

CurrentEBITDA

Pricerises

6 Carbon Value at Risk: the next generation of climate risk management

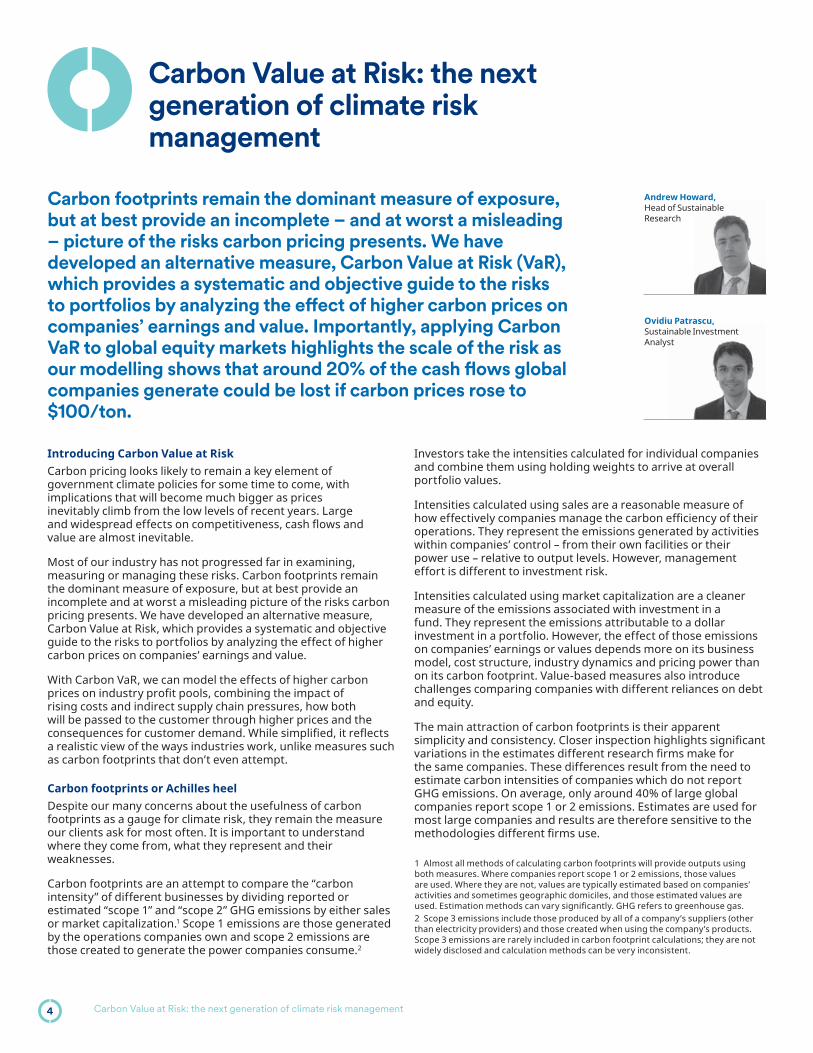

general effi ciency improvements and the closure of ineffi cient companies and capacity could close the gap.6

The impact stretches far beyond the most obvious sectors, such as energy and iron and steel production. In fact, using these assumptions, almost half of listed companies would face a rise or fall of more than 20% in EBITDA under our modellng.

Total changes in the most and least exposed sectors are shown in Figure 5, where we have focused on the largest sectors.7 The most exposed sectors are those which emit large quantities of greenhouse gases, margins are thin and price elasticity is high, so that falling volumes more than offset the benefi ts of rising prices.

Figure 5: Most and least exposed sectors

This framework underlines both the scale of impact climate change may have and the importance of stock selection over high level sector choices. Whereas companies’ carbon footprints are mostly explained by the sectors to which they belong, Carbon Value at Risk is mainly driven by company-specifi c factors. It means that knowing how cash fl ows would change within each sector becomes more important than selecting among different sectors.

Figure 6: Even in highly exposed sectors, the impact of climate change can differ widely

Source: Schroders, December 2016.

Source: Schroders, December 2016. Companies mentioned are shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell.

6 In the analysis described here we have assumed a carbon prices of $100/ton applied to all emissions globally and that 75% of companies’ non-personnel costs are variable (and therefore fall in proportion to declining volumes).7 Only sectors with larger sales than average are included.

-100% -80% -60% -40% -20% 0%

0%

Building Mat.& Fix.Iron & SteelCommodity ChemicalsSpecialty ChemicalsGeneral MiningAirlinesAuto PartsMulti UtilitiesIntegrated Oil & GasExploration & Prod.PipelinesAutomobilesIndustrial SuppliersCon. ElectricitySemiconductorsConsumer ElectronicsDelivery ServicesElectrical EquipmentTravel & TourismOil Equip. & Services

DefenseComputer ServicesDrug RetailersHeavy ConstructionPersonal ProductsFixed Line Telecom.BrewersSoft DrinksBroadcast & EntertainReinsuranceElectronic EquipmentMobile Telecom.Healthcare ProvidersPharmaceuticalsBanksLife InsuranceProp. & Casualty Ins.Full Line InsuranceInvestment ServicesSoftware

Most exposed

Least exposed

-8% -6% -4% -2%

Total EBITDA at risk from higher carbon prices

-10% 0% 10% 20% 30% 40% 50%

Du Pont

Eastman

Nan Ya Plastics

Basf

Dow Chemical

Lyondellbasell Inds

Asahi Kasei

Linde

Praxair

Air Liquide

Toray Inds.

Lg Chem 1Pf

Braskem On

Lotte Chemical

Shai.Petrochem

Mitsui Chemicals

Air Prds.& Chems.

Huntsman

Formosa

Sumitomo

Du Pont

Eastman

Nan Ya Plastics

Basf

Dow Chemical

Lyondellbasell Inds

Asahi Kasei

Linde

Praxair

Air Liquide

Toray Inds.

Lg Chem 1Pf

Braskem On

Lotte Chemical

Shai.Petrochem

Mitsui Chemicals

Air Prds.& Chems.

Huntsman

Formosa

Sumitomo

Carbon cost impact Change in EBITDA

Change in materials costs/sales

Change in personnel costs/sales

-120% -80% -40% 0%

Modelled change in carbon price related costs

Modelled change in cash earnings

Modelled impact of $100/ton carbon prices on top-20 global

7Carbon Value at Risk: the next generation of climate risk management

Conclusion

Applying Carbon VaR to global equity markets highlights the scale of the risk. Our modelling shows that around 20% of the cash fl ows global companies generate could be lost if carbon prices rose to $100/ton. On the other hand, there is no signifi cant correlation between individual companies’ Carbon Value at Risk and the carbon footprints investors look at most often. There is a danger that investors in low carbon investment products will fi nd themselves more exposed to climate risks than they expect.

Climate risks will be signifi cant and inescapable. Measuring and managing the investment risks is both critical and complex. Carbon pricing will be a key element of the policy changes ahead, if global political commitments are to prove realistic. The tools the majority of investors rely on most heavily do not fully capture those risks. In our view, Carbon VaR is a signifi cant step forward to helping us navigate the challenges ahead.

In the end, our modelling informs but cannot replace the judgement of experienced sector analysts able to bring their knowledge of industries and companies to the table. Carbon VaR helps identify risks by measuring the threats that companies face, but its strength lies in its integration into decision making rather than as a standalone criteria. As a result, just as we caution against viewing high carbon footprints as universally bad, we suggest that high Carbon VaR is simply one element of analysis to be considered alongside other analysis and valuation.

Detailed value analysis highlights the dangers of relying on shortcut approaches Figure 7 highlights the limited relationship between carbon footprints and our value-focused approach. Blue (darker) dots represent companies for which emissions are estimated and green (lighter) dots are based on reported emissions. While there is a positive relationship, it is weak. It is clear that both measures are capturing different aspects of performance and that treating carbon footprints as the sole measure of risk leaves investors open to major surprises.

Figure 7: Comparison of carbon footprints and Carbon Value at Risk of global equitiesCarbon footprint (t/$mn) vs Carbon VaR (%)

Carbon footprint (t/$mn)

Carb

on V

aR (%

)

0 1000 2000 3000 4000

Based on estimates

Based on reportedemissions

-100%

-75%

-50%

-25%

0%

25%

50%

Source: Schroders as of December 2016.

Our analysis allows us to gauge the risks facing portfolios, combining company Carbon Value at Risk estimates with portfolio weights. Figure 8 shows the effect on EBITDA of carrying out this exercise on some leading indices. While we consider our measure much more useful than carbon footprints, it still only represents one aspect of climate risk and should be considered alongside other sources of risk and opportunity, as well as an analysis of how companies respond to the pressures.

Figure 8: The effects on key benchmarks could be substantial

0%

-2%

-4%

-6%

-8%

-10%

-12%

-14%

-16%

-18%MSCIWorld

MSCIEm

S&P500

Portfolio value

FTSEAll Share

% of EBITDA at risk

Schroders portfolio value is based on a hypothetical strategy comprising the fi ve largest funds managed by Schroders. Calculated using constituents as of May 2017. Source: Datastream and Schroders May 2017. Actual risk portfolio analyses would vary.

8 Carbon Value at Risk: the next generation of climate risk management

Approximately 12,500 listed global companies are included in our analysis. Financial data are provided by Thomson Reuters. Greenhouse gas emissions data are provided by CDP, a charity established to improve carbon reporting, and Thomson Reuters. Analysis is based on average sales, cost and average scope one and two emissions over the previous three years.

We have used an input-output model to estimate the emissions generated in companies’ supply chains (other than power generation) using economic tables from 2007 provided by the US government’s Bureau of Economic Analysis. In the absence of better information, we assume every company in each industry has a similar supply chain. To get a more realistic estimate, we scale the supply chain exposure to emission pricing by companies’ non-personnel cash costs as an approximation of their materials purchases.

Total emissions exposure is calculated by combining scope one, scope two and other supply chain costs. We assume a price of $100 is imposed on every ton of CO2 created at any part of that value chain. We recognize that applying a single global price to every emitted tonne represents a simplifi cation, given the different schemes likely to be in place for different regions and activities.

We assume all of the increase in costs associated with higher carbon prices is passed onto customers. While the adjustment process may take some time, there is strong evidence that prices in any industry fi nd equilibrium to support returns on

investment at a level commensurate with companies’ costs of capital, industry consolidation and supply side discipline. Insofar as higher operating costs do not affect invested capital in our modelling, we assume prices rise by the same level for all companies in each sector, suffi cient to offset the increased carbon costs.

As prices rise in response to higher costs, we adjust (volume) demand in each industry using price elasticity assumptions specifi c to each industry. The key assumptions are described in the table below.

Recognizing that lower volumes will reduce costs, we assume 75% of companies’ non-personnel cash operating costs are variable and fall in line with lower demand. We adjust baseline sales, costs and EBITDA for the increase in costs likely to affect each specifi c company, the higher prices likely to be common to all companies in each sector and for volumes falling by a consistent level in each sector, reducing both revenues and costs. Comparing the resulting modelled EBITDA to the baseline EBITDA provides a measure of the value at risk from an increase in carbon prices.

In reality, the picture would be more nuanced. For example, volume and price changes would vary between different companies in a sector. Managements would respond by resetting strategies and reconfi guring assets, while alternative manufacturing technologies would become more competitive. As a result, the values we present refl ect value at risk rather than forecasts of future earnings changes.

GICS Sector* GICS Industry Groups Price elasticity of demand

Energy Energy 0.75Materials Materials 1.52Industrials Capital Goods 0.75

Commercial & Professional Services 1.00Transportation 1.00

Consumer Discretionary Automobiles & Components 2.80Consumer Durables & Apparel 1.20Consumer Services 1.50Media 1.00Retailing 0.70

Consumer Staples Food & Staples Retailing 0.25Food Beverage & Tobacco 0.25Household & Personal Products 0.25

Health Care Health Care Equipment & Services 0.17Pharmaceuticals, Biotechnology & Life Sciences 0.20

Financials Banks 0.56Diversifi ed Financials 0.15Insurance 0.25

Information Technology Software & Services 0.10Technology Hardware & Equipment 1.30Semiconductors & Semiconductor 3.50

Telecom Telecommunication Services 0.40Utilities Utilities 0.30Real Estate Real Estate 1.20

* Global Industry Classifi cation Standard, developed by MSCI and Standard & Poor’s. Source: Literature review and Schroders. Based on literature review conducted May 2017. The opinions stated in this report include some forward-looking statements and assumptions. We believe that we are basing our expectations and beliefs on reasonable data within the bounds of what we currently know. There can be no assurance, however, that events will occur as we expect or believe. This data is provided to you for information purposes only and should not be relied on to predict possible future performance. There can be no guarantee that these or any simulated and/or modelled results will occur, generate a positive return or protect against loss of principal.

Appendix - methodology, key assumptions and sources

9Carbon Value at risk: the next generation of climate risk management

Rising rates, reduced returns?

IntroductionA number of asset classes with income-generation properties have been popular among investors. These tend to be fi xed income assets or assets which share some of the income-generating characteristics of fi xed income. They include government bonds, investment grade credit, high yield debt, real estate investment trusts (REITs), emerging market debt (EMD) and high dividend equities. With cash rates and government bond yields falling to very low levels around the world, these income-generating assets have been increasingly in demand and have consequently enjoyed strong returns over recent years. However, with the US Federal Reserve raising interest rates, several rate-setters at the Bank of England voting for a rise, and questions being raised about whether the European Central Bank will be less accommodative, many investors are now wondering if the party is over and it is time to sell out of these asset classes.

Interest rate regimesTo answer this, we have looked at how these assets have performed during previous periods of rising yields. We used data on 10-year US Treasury yields since 1970 and split historic experience into periods of rising and falling yields,1 as shown in Figure 1. We determined these periods using a combination of qualitative and quantitative approaches to ensure that we captured longer-term movements in interest rates, rather than short-term fl uctuations. What is immediately clear is that pre-1980 experience was largely characterized by rising yields, but since then the opposite has largely been true, punctuated only by a number of short episodes when yields have risen.

Investors in income yielding assets have become nervous that returns will be impaired if rates rise in the future. Our analysis shows that these concerns may be overdone as most income assets historically continued to generate positive returns during periods of rising rates. Some assets have even performed better during such periods. Even looking at income on its own, levels have also been fairly stable when yields have risen and some assets have actually seen income levels increase during such periods. With income investing, patience is the key.

Clement Yong, CFAStrategist, Research and Analyst

Figure 1: Historical interest rate regimes US 10-year Treasury yield%

0

2

4

6

8

10

12

14

16

18

10y yieldFallingRising01/201501/201001/200501/200001/199501/199001/198501/198001/197501/1970

Source: Federal Reserve Bank of St Louis economic data (FRED), Datastream and Schroders. As of February 28, 2017. For purposes of our analysis we selected regimes based on long-term trends (greater than six months) in yield moves with a magnitude of greater than 100 basis points, except for the last period which, as of the time of original writing was 90 basis points. For more information, please refer to the full length version, Rising rates, reduced returns?

1 Throughout this paper, we have defi ned interest rate regimes using long-term government bond yields, specifi cally the 10-year US Treasury yield. We have also conducted the same analysis in terms of central bank policy rates and found that the conclusions are consistent under both approaches. We have therefore used the terms “interest rates” and “bond yields” interchangeably throughout the paper.

Rising rates, reduced returns?10

Income assets can still generate positive returns in rising rate environmentsFigure 2 shows the average annualized performance of a number of income assets over the periods of rising and falling rates set out in Figure 1. It is worth noting that data on most asset classes are only available since the early 1970s and some are much more recent. For example, local EMD returns data are only available since 2002. If we had only analyzed the trends when we had data for all assets (i.e. 2003 onwards), we would only be able to capture three rising and two falling interest rate regimes. The longer history has the benefi t of capturing more regimes and we are reassured by our fi nding that re-running the analysis over the post-2002 period would not materially alter our conclusions.2 With the exception of the two emerging market debt assets, all assets are US-based for reasons of data availability and reliability.

A number of points stand out, particularly:

1. All income assets have historically produced positive returns, on average, in rising rate environments, with the exception of government and corporate bonds.

2. Government bonds and investment grade corporate bonds have performed far worse when yields have been rising than when they have been falling.

3. Many other assets typically included in income portfolios have held up well, and some have actually performed better, when yields have been rising.

Although the effects of rising yields vary considerably, these conclusions should provide some comfort to income investors. Particularly interesting is that rising rates are actually good news for some assets, such as high yield debt, local- and hard-currency emerging market debt. As interest rates tend to rise in anticipation of stronger economic growth, assets which are more sensitive to economic growth (such as high yield debt, REITs and high dividend equities) can still have the ability to perform well during such times. An additional consideration that relates to equity investments is style bias, which can have an impact on returns independently of yield. For example, high dividend equities inherently have a value bias, so performance can be infl uenced by whether this particular style is in or out of favor.

Ultimately, the impact on the various income assets will depend on the reason for the change in yields. When yields rise in anticipation of stronger economic prospects, corporate fundamentals usually also improve. This in turn can boost

corporate earnings and, in consequence, equities. The creditworthiness of borrowers has also improved in such an environment, supporting corporate bonds (which is especially relevant for high yield debt). In contrast, if yields rise due to infl ation concerns while economic growth is weak, equities and credit assets are likely to fare far worse.

EMD assets, on the other hand, are an aggregate of emerging market exposures and so the effect of rising rates in the US will not be as direct as it is on some of the other income assets. For example, hard EMD is comprised of a Treasury yield and a credit spread so has a direct link with US yields. However, local EMD bonds are denominated in an emerging country’s local currency, so local interest rates, local infl ation and currency movement are what matter. Any link with US rates will be most keenly felt through the currency, with movements in US rates infl uencing the strength of the dollar and, in consequence, returns for local EMD investors.

Figure 2: Rising interest rates are not necessarily bad news for income assets

Average annualized performance in different interest rate regimes%

-5

0

5

10

15

20

25

FallingRising

High div equitiesLocal EMDHard EMDUS REITsUS HYUS IGUS Treasury

Asset classes shown refl ect widely used benchmark indices. Source: Bank of America Merrill Lynch (BAML), Datastream, FRED, Kenneth French, JP Morgan (JPM), MSCI and Schroders. As of February 28, 2017. Past performance is no guarantee of future results. Actual results would vary.

2 The only notable difference is that, over the shorter horizon, REITs and high dividend equities performed better when yields rose than they did when measured over the longer horizon. A major reason for this difference is that both assets performed very strongly leading up to the global fi nancial crisis (a period characterized by rising rates). We therefore prefer to conduct the analysis on varying time horizons to ensure that we capture the long-term trends for each asset.

Asset allocation can make a differenceThe variation in performance of income assets, combined with the fact that we found that most returns were positive during a rising yield environment, suggests that there are opportunities to add value from strategic asset allocation during times of rising rates. Investors therefore have to be cognizant of the different return profi les during such times. In our view, good income managers should still be able to deliver value, even though the environment may not appear ideal for their portfolios.

Rising rates, reduced returns? 11

Time horizon mattersInvestment in any asset class requires an adequate time horizon. Investment in income assets is no exception. In this section, we show that reacting purely to recent movements in interest rates may be unwise and that a suffi cient holding period does matter.

To show this, we looked at what happened to total returns when assets were held over the one- and three-year periods following a month when yields rose (and vice-versa when they fell). For example, take January 2003, a month when interest rates rose, we looked at returns over the February 2003-February 2004 and February 2003-February 2006 periods. Interest rates may or may not have still been rising by the end of these periods and, indeed, may have been falling by then. The point is that, at the beginning of these periods, we obviously can’t say for sure where interest rates will go in the future. What we are therefore testing is whether having patience when investing in income assets can lead to an improvement in outcomes, even without the benefi t of perfect foresight.

The most notable point is that one- and three-year average returns following a rise in yields have been positive for all income assets.

Recall that in Figure 2, the performance of government bonds and corporate bonds during rising interest rates were considerably poorer than their returns during periods of falling interest rates. From this new angle, the improved picture of returns from these two assets during times of rising rates is quite remarkable, especially over the three-year horizon (see circled bars).

The improvement in returns may be a result of market conditions reverting to the mean over the period in question, e.g. after a rise, yields fell again. Without perfect foresight, it is impossible to time precisely when to buy or sell and history is littered with failed predictions of when and how far yields would rise. Hence, being patient in income investing and not reacting when interest rates go up is a reasonable strategy and, more often than not, has generally led to an improvement in outcomes, historically.

Investing for incomeSo far, we have only measured the performance of income assets from a total return perspective. However, for many investors, a key purpose of income investing is to procure an adequate level of income to meet their needs, without necessarily requiring an increase in capital. In general, income levels are less sensitive to changes in interest rates than total returns. Companies are loath to cut dividends, given the negative signal that it sends to the market, while coupons on bonds are one of the fi rst claims on a company’s income, ranking above other demands. Income from existing investments is therefore somewhat insulated from changes in yield movements unless something quite serious happens to the source of the income.

While this is true for individual investments, the change in income levels may differ for the overall market. Some companies may be forced to cut their dividends or even default on their obligations. These events will have an infl uence on both the market’s income level and its price. To take these changes into account, we looked at the amount of income that $100 invested in a portfolio would generate at the start and end of each period, and then calculated the growth rate of that income. This allowed for both changes in the income yield itself (coupon yield for bonds, dividend yield for equities) and the value of the capital invested. We assumed that investors would withdraw all the income generated rather than reinvesting it during the period.

Let us take a hypothetical rising rate period by way of example. If the dividend yield from a group of equities is 3% at the start of this period, then $100 would generate $3 of income. If the market falls 10% over the period but the dividend yield increases by 7%, then the $100 has reduced to $90 and the dividend yield has risen to 3.2%, meaning that the amount of income has fallen to $2.88, a 4% reduction (see Figure 4 on the next page). So, even though coupon/dividend yields may rise in a rising rate environment, this is obviously somewhat offset if the capital value is severely impacted. Our analysis ensures that both these often contrasting impacts are captured.

Figure 3: The importance of time

Asset classes shown refl ect widely used benchmark indices. Source: Schroders, Datastream, BAML, FRED, Kenneth French, JPM, MSCI. As of February 28, 2017. Past performance is no guarantee of future results.

One- and three-year average annual returns following a month where yields have risen or fallen

Average 1y forward returns%

Average 3y forward returns%

0

2

4

6

8

10

12

14

16

18

FallingRisingHigh divequities

Local EMDHard EMDUS REITsUS HYUS IGUSTreasury

0

2

4

6

8

10

12

14

16

FallingRising

High divequities

Local EMDHard EMDUS REITsUS HYUS IGUSTreasury

Rising rates, reduced returns?12

Figure 5 confi rms that income levels are often more stable than total returns. With few exceptions, the impact of rising interest rates on income levels has been minimal and in some cases income levels actually picked up when yields rose (because companies increased their dividends as a result of growing corporate profi ts).3 In fact, income levels overall deteriorated more during times of falling interest rate environments than rising. Even though falling interest rate environments may have been more supportive for income asset prices, the fall in dividend and/or coupon yield has evidently been signifi cant.

It is evidently diffi cult to time precisely when to buy or sell income assets to procure the maximum level of income. A better strategy, we believe, is to stay invested in income assets, which will often lead to more favorable levels of income in all interest rate regimes. Certainly, our analysis of the historical record should provide reassurance to income investors about the risks to their income if interest rates rise. Income levels have historically been more stable than total returns, and, in some cases, have even increased as yields have risen. As with total returns, the impact varies by asset class, meaning that asset allocation can play a part in navigating these conditions.

Figure 4: Hypothetical example of the change in income level

Figure 5: Average annualized change in income levels in different interest rate regimes

Dividend yield%

2.9

3.0

3.1

3.2

3.3

Start End84.00

86.00

88.00

90.00

92.00

94.00

96.00

98.00

100.00

102.00$ Price

Start End2.82

2.84

2.86

2.88

2.90

2.92

2.94

2.96

2.98

3.00

3.02$ Income level

Start End

+7%-10%

-4%

%

-6

-4-4

-2

0

2

4

6

8

10

12

FallingRising

High divequities

LocalEMD

HardEMDUS REITsUS HYUS IG

USTreasury

Source: Schroders. For illustrative purposes only, based on mathematical principles.

Asset classes shown refl ect widely used benchmark indices. The coupon yields of all bond assets have been adjusted for market price, with the exception of local EMD, where market price data were not available. Source: Datastream, BAML, FRED, Kenneth French, JPM, MSCI and Schroders. As of February 28, 2017. Past performance is no guarantee of future results.

Conclusion

Rising rates do not necessarily spell doom for income assets. At such times, income investors should re-assess their assets and remind themselves of their purpose. If it is simply to procure a level of income to meet certain needs, we have shown that rising rates have not historically had too detrimental an impact on the level of income produced. But even if capital returns are important, returns have been strong from a number of income

assets when yields have risen, while the variation in performance between diff erent income assets has provided opportunities for good asset allocators. That said, history also suggests that trying to anticipate the market based on short-term interest rate movements is very diffi cult and, often, simply adopting a suitably long-time horizon may lead to an improvement in outcomes.

Rising rates, reduced returns?

3 It is worth noting that, had we assumed that income was reinvested, we would have found that income levels increased in all cases. However, because we are assuming that investors are invested to derive an income, we believe that this would not be a fair refl ection of their experience.

13

Churn is not necessarily burn: debunking the myths of portfolio turnover

Within emerging markets we do fi nd that higher levels of turnover are historically detrimental for performance over a three year horizon and that low turnover is a quality associated with top performing funds, although we must be careful not to confuse correlation with causation. Unlike US small cap funds, the average high turnover emerging market equity fund appears unable to add suffi cient value to offset the additional transaction costs it is exposed to. This makes intuitive sense with the higher cost nature of emerging markets a likely key driver.

Choosing the right active fund is always imperative but our analysis suggests that this is even more true among high turnover funds. The best high turnover US equity funds have underperform the best low turnover funds but the worst have done worse and there is an increased likelihood of a high turnover fund failing to survive over time. This last feature has been strongest among growth, small cap and emerging market equity funds.

Finally, high turnover funds have the undesirable feature that they have historically struggled versus low turnover funds in periods of falling markets and rising volatility, on average. This is made more pertinent by the fact that average turnover levels have increased in times of market stress, precisely the times when this characteristic has been detrimental to performance.

IntroductionTransaction costs, and by implication portfolio turnover, are a current bete noire of the asset management industry. In many cases this is valid. High levels of turnover can be indicative of a lack of conviction or undue short-termism and trading too often can eat into returns. However, it is unfair to suggest that all turnover is bad. If a fund manager sells a stock that subsequently

underperforms and replaces it with another that outperforms then the impact on performance may be positive, even after allowing for transaction costs. Conversely, if they hold onto stocks that have been underperforming, this could be a sign of a portfolio based on stale views.

From an end investor’s standpoint, what should matter most is whether turnover results in better or worse outcomes after all fees and expenses. In this paper we focus on this under-researched aspect by analyzing whether there is any evidence of a relationship between turnover and added value among active equity funds. We continue to develop our thinking in this area and further research may form the basis of future publications.

Our analysis focuses on US-domiciled active US equity and emerging market equity funds. Fund data is sourced from Morningstar to provide a comprehensive overview of the marketplace. As an example, our analysis of the 2015 calendar year covered over 2,100 funds. US equity funds are further broken down into style-neutral, value, growth, mid and small cap funds. We focus on these markets because US-domiciled funds are obliged to report portfolio turnover levels, as defi ned by the SEC,2 whereas there is no such requirement in other markets such as the UK. We relied on the US large cap market due to it being among cheapest in which to trade around the world. We cover US small cap stocks and emerging market equity funds as more expensive counter examples.

As the tax treatment of turnover varies considerably by jurisdiction and savings vehicle we have excluded any tax effects in our analysis. However, investors should be aware that turnover can have an impact on their post-tax returns and take this into account when considering investment strategy.

There is a widely held assumption that portfolio turnover results in poorer outcomes for investors as a result of the additional costs it incurs. Our research challenges that simplistic assumption by instead focusing on added value net of costs. We fi nd no evidence of a structural relationship between turnover and excess returns among active US equity funds over the 1991-2016 period.1 This includes small- and mid-cap funds, despite the higher costs of trading in these sectors. On average, high turnover active US equity funds have the ability to generate suffi cient value to off set additional transaction costs.

Duncan Lamont, CFAHead of Research and Analytics

Kristjan MeeStrategist, Research and Analytics

2 The lesser of purchases and sales divided by the average fund value over a 12 month period. The SEC methodology limits the impact of any fl ows into and out of a fund (which would raise the volume of purchases or sales) to focus on discretionary turnover by the fund manager.

1 The views and opinions expressed herein are based on analysis conducted using historical performance. Any forward-looking opinions stated are those of the authors and are not intended to offer any guarantee of future results. Past performance offers no guarantee of future results. More details provided on pages 22-23.

Churn is not necessarily burn: debunking the myths of portfolio turnover14

Variability in transaction costs and turnover levels by region and styleThe cost of portfolio turnover is driven partly by how often a fund manager trades but also by how much each trade costs. These transaction costs can take many forms, including:

– Explicit costs such as commissions and taxes

– Implicit costs such as bid/offer spreads and market impact (the cost of the amount that the market moves against you when you start dealing)

These vary considerably by market, as shown below.

Commissions vary from as low as 4 basis points in US large cap stocks to over 12 basis points in US small cap and emerging market stocks. Similarly, average bid-offer spreads are only around 3 basis points on average among US large caps, but

over 15 basis points in emerging markets and almost 25 basis points among US small caps. Intuitively, one might expect turnover to have a more negative impact on performance in high cost markets such as US small caps and emerging markets than in US large caps, the cheapest market in which to trade globally.

Turnover is highly variable across and within stylesThe other leg to the turnover-cost equation is the volume of turnover. This varies considerably across different styles of equity investment and there is also notable variation within each category. Turnover is often associated with active management but, as Figure 2 shows, even traditional equity indices experience some turnover, albeit at a fairly limited level. This occurs as companies enter and exit the index. So-called “smart beta” indices experience noticeably higher levels of turnover than traditional market cap indices, and as a result this is often constrained by the index provider (e.g. the MSCI large cap minimum volatility indices have a 20% turnover constraint without which their analysis suggests turnover could be more than three times as high). Active funds typically experience higher levels of turnover than most traditional and smart beta indices with the exception of momentum indices. These incur exceptionally high levels of turnover, often exceeding 100% in a 12 month period. Despite the higher costs of trading in smaller companies and emerging markets, it is interesting to note that small cap and emerging market funds and indices generally experience higher levels of turnover than US large caps. In theory, the combination of higher levels and costs of turnover creates a relative performance headwind in these sectors.

Some of these relationships are persistent over time. For example, value funds consistently exhibit lower turnover than other styles (Figure 3 on the next page). Two other features are notable. First, turnover increased across all styles around the time of the bursting of the Dotcom bubble and again during the Global Financial Crisis. Fund managers appear to increase turnover when markets are crashing. Secondly, average turnover levels have been declining over recent years in a number of sectors and turnover levels are now much more closely bunched across different sectors of the market than in the past.

Figure 1: Transaction costs vary signifi cantly by region and style

Source: ITG for commission data, as of December 2016, Schroders and Jefferies for indicative bid/offer spread, as of February 2017.

0

5

10

15

20

25

US SmallEmerging Mkts

US MidUKEurope ex UKJapanUS Large

Basis points

Indicative bid/offer spread Commission payable as % of trade value

Figure 2: Annual turnover varies by style

Source: MSCI, FTSE, Morningstar, Schroders. Data covers calendar year 2016 for active funds and FTSE indices, 12 months to end February 2017 for MSCI indices.

0102030405060708090

100

MSC

I USA

Mom

entu

m

Activ

e U

S Sm

all

Activ

e EM

Activ

e U

S M

id

Activ

e U

S G

row

th

Activ

eU

S Va

lue

FTSE

RAF

I US

1500

SM

ID

MSC

I USA

Smal

l Min

Vol

MSC

I Wor

ldM

ulti-

fact

MSC

I EM

ESG

Foc

us

FTSE

RAF

I EM

MSC

I USA

Enha

nced

Val

MSC

I USA

Equa

l-wgt

d

MSC

I EM

Qua

lity

FTSE

RAF

IU

S 10

00

MSC

I EM

Min

Vol

MSC

I USA

Min

Vol

MSC

I USA

Qua

lity

MSC

I USA

ESG

Foc

us

MSC

I USA

Sm

all

MSC

I EM

MSC

I USA

Traditional market cap index "Smart beta" index Average active

%

Churn is not necessarily burn: debunking the myths of portfolio turnover 15

Furthermore, even within these categories, there is tremendous variation in turnover levels among active funds as Figure 4 below shows. Although the distribution of value funds was skewed towards those with lower turnover in 2016, some have very high levels of turnover. Similarly, small cap and blend (the label assigned by Morningstar to portfolios where neither growth nor value characteristics predominate) funds had higher turnover on average during 2016 but some are towards the lower end ofthe scale. In all cases, the vast majority of funds had turnover below 100%.

Figure 3: Turnover varies by style...

Source: Morningstar, Schroders, data to end 2016.

Figure 4: ...and varies within styles

Source: Morningstar, Schroders, data to end 2016.

The turnover-performance relationship: US equity fundsHaving established that turnover levels and costs vary considerably, the obvious question to ask is whether this impacts performance? In the following sections we answer this for US and emerging market equity funds. Our analysis is on a contemporaneous (assessing turnover and performance over periods where they coincide) and predictive (assessing whether past turnover predicts future performance) basis, over one- and three-year horizons (methodology detailed on next page).

Figure 5 charts the median difference in performance between low (<25%) and high (>100%) turnover US large cap value funds on a year-by-year contemporaneous basis, i.e. it compares turnover in one year with performance in the same year. A positive reading arises when the median fund in the low turnover group outperforms the median fund in the high turnover group – our analysis is based on medians to avoid distortions from extreme values.

It is hard to spot any real trends in the performance of large cap value funds. Sometimes low turnover funds outperform and sometimes high, without exhibiting any real pattern. The difference in performance is usually small, although there are exceptions.

We have also analyzed this on a three-year basis as it could be argued that managers with low turnover may have longer investment horizons over which they anticipate their positions adding value. However, we fi nd no obvious difference in performance between low and high turnover US value funds over this longer time frame either. Nor is there any evidence that past turnover (on a one- or three-year basis) has any predictive power over future (one or three-year) relative returns for US value funds.

Analysis of other styles of US equity investments yields a similar apparently random distribution of results on both a contemporaneous and predictive basis. Table 1, on the next page, summarizes the median annual difference in excess return between low and high turnover funds over the 1991-2016 period. Most of the differences are not large and none are signifi cant in a statistical sense.3 This means that there is insuffi cient evidence to conclude that these differences are likely to have occurred by anything other than chance.

3 Although the difference between low and high turnover small cap equity funds on a three-year predictive basis has averaged 2.2%, this is largely due to strong outperformance of low turnover funds when the Dotcom bubble burst, rather than on a more generalized basis. Hence, it is fails to satisfy statistical tests of signifi cance.

0

25

50

75

100

125

150

175

200

'16'14'12'1008'06'04'02'00'98'96'94'92'90

Average turnover over time, %

Value Growth Mid Small EM Blend

0

20

40

60

80

100

SmallBlendEMMidGrowthValue

Percentage of funds within different turnover ranges-2016. Ranked from left to right in order of increasing average turnover

T<=25% 25%<T<=50% 0%<T<=75% 75%<T<=100% 100%<T

Figure 5: Does turnover imply performance?

-10

-8

-6

-4

-2

0

2

4

6

201520122009200620032000199719941991

Difference in median performance between low and high turnover large cap value funds, % 1-year contemporaneous basis

High turnover outperforming

Low turnover outperforming

Source: Morningstar, Schroders, data to end 2016.

Churn is not necessarily burn: debunking the myths of portfolio turnover16

Explanation of our methodology: Return analysisWe have analyzed the relationship between turnover and excess returns (the level of return that each fund has delivered relative to industry-standard benchmarks) among active US equity and US-domiciled emerging market equity funds on a net of fees basis. As explained earlier, we focus on these markets for reasons of data availability. As turnover levels vary by sector, US equity funds have been further split into blend (representing those funds with no style bias), value, growth, mid-cap and small cap funds to avoid our results being distorted by any style biases. Emerging market equity funds (dealt with later) have been treated as a whole due to their smaller sample size. By focusing on net of fees returns, our analysis captures all costs borne by investors, both explicit and implicit.

We have analyzed whether higher or lower turnover funds generate higher or lower excess returns over the period which the turnover corresponds (contemporaneous approach) and whether past turnover predicts future performance (predictive approach). This is an important distinction as turnover can be incorporated into a real life investment strategy if it holds predictive power over future return potential.

Analysis has been conducted by categorizing funds into fi ve different turnover ranges: less than 25%, 25%-50%, 50%-75%, 75%-100% and over 100%. For the emerging market return analysis there are insuffi cient funds within the 0-25% range in some of the early years to conduct meaningful analysis so we have combined the two lower ranges to form a 0-50% range for this sector. Relative performance of emerging market funds within the 0-25% and 25-50% ranges are similar so this does not materially impact our conclusions.

Table 1: Difference between median excess returns earned by low and high turnover funds, % annualized

None of theses data are statistically signifi cant

1yr Contemp-oraneous

1yr Predictive

3yr Contemp-oraneous

3yr Predictive

US Large Cap Value 0.0 -0.1 0.2 0.4

US Large Cap Growth -0.4 -1.3 0.0 -0.1

US Large Cap Blend 0.2 -0.5 0.6 0.0

US Mid Cap -0.9 -2.1 0.2 0.5

US Small Cap 0.8 -0.9 0.9 2.2

Figure 6 considers a different angle but with similar conclusions. Rather than asking whether high or low turnover funds are characterized by better or worse performance, we instead reverse the question and assess whether better or worse performers are characterized by high or low turnover. The conclusions are consistent with those outlined above. There is no difference in average turnover levels between top and bottom quartile performing value funds. Both top and bottom quartile performers have had average turnover of 52%. This conclusion is consistent across other styles of US equity funds.

Figure 6: Does performance imply turnover? Contemporaneous 1yr basis, Large cap value

Source: Morningstar, Schroders, data 1990-2016.

0

10

20

30

40

50

60

75%-100%50%-75%25%-50%<25%

Median turnover ratio

Performance quartile

Conclusion 1

We fi nd no evidence of a structural relationship between turnover and excess returns among active US equity funds. This is true on both a one- and three-year basis. This suggests that high turnover managers have at least enough skill to off set the additional

transaction costs they are exposed to. What is surprising is that this is true even in small caps where the costs of trading are noticeably higher.

Churn is not necessarily burn: debunking the myths of portfolio turnover 17

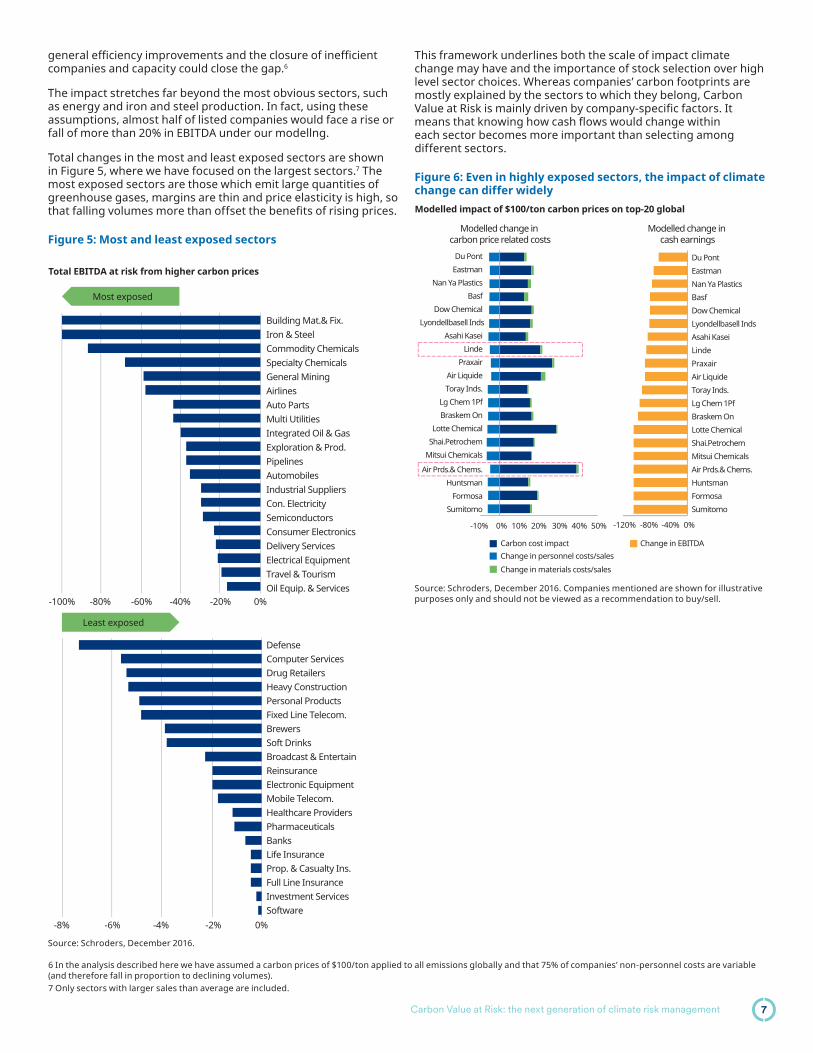

The turnover-performance relationship: emerging market equity fundsWhile we fi nd no evidence of a relationship between turnover and performance in US equity funds, low turnover emerging market equity funds consistently outperform high turnover funds over a three-year horizon (Figure 7) and this conclusion is statistically signifi cant,4 as shown in Table 2. Higher trading costs in emerging markets are likely to be at least partly to blame. However, this relationship does not appear to hold over a one-year horizon.

In terms of quantum, those funds with average turnover of less than 50% over a trailing three year period have on average outperformed those with turnover of more than 100% by 2.6% a year over the subsequent three years.

Table 2: Difference between excess returns earned by low and high turnover funds Figures in bold are statistically signifi cant

1yr Contemp-oraneous

1yr Predictive

3yr Contemp-oraneous

3yr Predictive

EM 0.6 0.2 1.7 2.6

Source: Morningstar, Schroders, data 1996-2016.

This link between turnover and performance in emerging market equity funds is reinforced by the analysis summarized in Figure 8. Top quartile performing emerging market funds on average have had annual turnover of 58%, around 15% less than the 72% average turnover of bottom quartile performers.

4 Statistical note: the rolling three-year analysis includes overlapping periods and serial correlation is present in the data. This biases the standard errors in regular statistical tests, which can result in a false positive result i.e. a conclusion of signifi cance when there is none. We have applied a Newey-West adjustment to the standard errors to correct for this. The conclusions of signifi cance are robust to this adjustment.

Figure 7: Low turnover emerging market funds outperform high turnover funds over a three-year horizon

Source: Morningstar, Schroders, data to end 2016.

-6

-4

-2

0

2

4

6

8

10

2016201320102007200420011998

Difference in median performance between low and high turnover funds (%) 3-year contemporaneous basis

3yrs ending

Low turnover outperforming

High turnover outperforming

-4

-2

0

2

4

6

8

10

12

201620132010200720042001

3 year predictive basis

3yrs starting

Low turnover outperforming

High turnover outperforming

Figure 8: Poor performing emerging market funds have higher turnover than strong performers

Source: Morningstar, Schroders, data 1996-2016.

0

10

20

30

40

50

60

70

80

75%-100%50%-75%25%-50%<25%

Median turnover ratio

Conclusion 2

Low turnover emerging market equity funds outperform high turnover funds over a three year (but not one-year) horizon. This conclusion is statistically signifi cant. Furthermore, top

quartile performers are likely to have lower turnover than poor performers.

Churn is not necessarily burn: debunking the myths of portfolio turnover18

An opportunity and a risk: fund selection is more important than ever among high turnover funds

High turnover US equity funds exhibit greater dispersion of returnsWhile the median return may be a useful proxy for a likely outcome over time, it masks the possible range of outcomes (good and bad) that investors are exposed to. When looked at through this lens, there is a larger difference in performance between top and bottom decile performers among high turnover US equity funds than low turnover equivalents. This is shown in Figure 9 for value funds but also holds more generally – see boxed section for more detail on our approach.

This arises as the best performing high turnover funds have done better than the best performing low turnover funds but the worst have done worse. This can be seen in the second chart in Figure 9. This difference is persistent over time and is statistically signifi cant. It holds over one and three-year horizons and for other styles of US equity funds, with the difference greatest among small and mid cap funds (differences summarized in Table 3 on the next page). In practical terms, choosing the right fund can have a bigger impact on performance (for better or worse) in the high turnover part of the market.

Interestingly, this conclusion does not hold for emerging market equity funds (Figure 10) where, if anything, there is greater performance dispersion within low turnover funds. This occurs as the best performing low turnover emerging market funds outperform the best performing high turnover funds.

Explanation of our methodology: Dispersion analysisWe analyzed top and bottom decile excess returns in each calendar year among high turnover funds. The difference between these fi gures (the inter-decile range) is one measure of how well top performers have fared relative to poor performers. We carry out the same analysis for low turnover managers. We then calculate the difference between the high turnover fi gure and the low turnover fi gure. A higher result means that there is a bigger gap between good and bad managers in the high turnover space than in the low turnover space. These are shown on a calendar year basis for value and emerging market equity funds in the fi rst chart of Figures 9 and 10.

For example, in 2009 within the lowest turnover range (<25%), top decile value funds returned 11.1% and bottom decile funds returned -2.8%. On the other hand within the highest turnover range the numbers were 21.1% and -4.9% respectively. This means that the range of outcomes was 13.8% for low turnover funds and 25.9% for high turnover funds. The difference between these fi gures is 12.1%, which can be seen at the 2009 point in the fi rst chart of Figure 9.

Table 3 shows the median difference between the high turnover inter-decile range and the low turnover inter-decile range over time. Again, a positive fi gure indicates that there is greater dispersion of returns within high turnover funds than low turnover funds, on average. We carry out this analysis on a one- and three-year contemporaneous and predictive basis.

Figure 9: High turnover US equity funds earn higher highs and suffer lower lows than low turnover funds...US Large Value

-10

-5

0

5

10

15

201520122009200620032000199719941991

High turnover inter-decile range minus low turnover inter-decile range

High turnover has wider gap between good and bad performers

Low turnover has wider gap between good and bad performers

Figure 10: ...but this does not hold for emerging marketsEmerging markets

-25

-20

-15

-10

-5

0

5

10

15

2014201120082006200219991996

High turnover inter-decile range minus low turnover inter-decile range

High turnover has wider gap between good and bad performers

Low turnover has wider gap between good and bad performers

Source: Morningstar, Schroders, data 1996-2016.

-8

-6

-4

-2

0

2

4

6

8

10

>100%75%-100%50%-75%<50%

Median top and bottom decile excess returns

TurnoverTop decile excess return Bottom decile excess return

Source: Morningstar, Schroders, data 1990-2016.

-10

-8

-6

-4

-2

0

2

4

6

8

>100%75%-100%50%-75%25%-50%<25%

Median top and bottom decile excess returns

TurnoverTop decile excess return Bottom decile excess return

Churn is not necessarily burn: debunking the myths of portfolio turnover 19

Table 3: High turnover inter-decile range minus low turnover inter-decile rangeFigures in bold are statistically signifi cant

1yr Contemp-oraneous

1yr Predictive

3yr Contemp-oraneous

3yr Predictive

Large Cap Value

2.4 3.1 2.1 1.5

Large Cap Growth

3.1 4.2 2.9 1.2

Large Cap Blend

2.1 1.8 0.7 -0.1

Mid Cap 7.7 5.7 4.6 3.7

Small Cap 6.5 6.7 4.6 3.1

EM -1.4 -2.3 -1.7 -1.8

Source: Morningstar, Schroders, data 1990-2016 for all styles other than emerging markets which is 1996-2016.

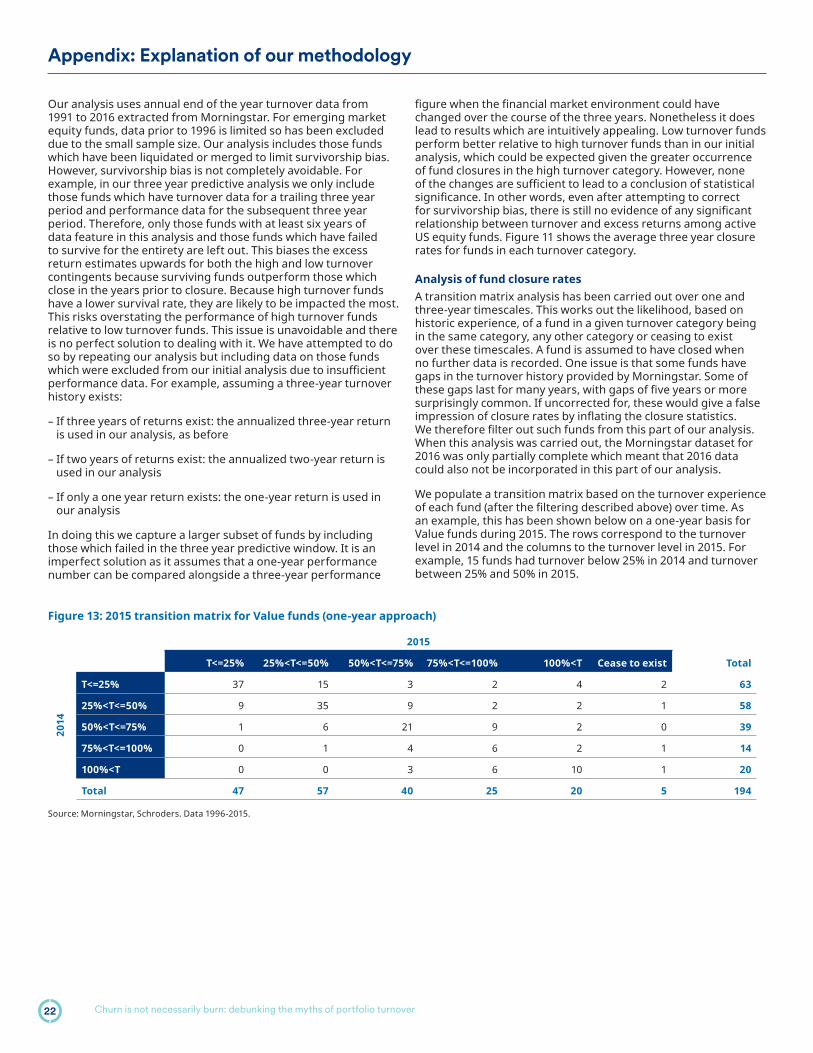

A decreased likelihood of a fund surviving over timeThe differences between high and low turnover funds are more fundamental than just returns. Our analysis indicates that high turnover funds have historically been more likely to be liquidated or merged than low turnover funds (Figure 11). In other words, high turnover funds have a lower survival rate. This has been true on average across all of the styles we have analyzed and is statistically signifi cant for growth, mid, small and emerging market equity funds on a three-year time horizon. This relationship has been especially strong among emerging market equity funds. Although it has also held on average for blend and value funds, these results are not signifi cant in a statistical sense.

Figure 11: High turnover funds suffer higher closure rates than low turnover funds

Source: Morningstar, Schroders. Data 1996-2015 average. Bottom two categories have been combined for EM due to limited number of funds in the lowest category in the early years.

0

5

10

15

20

25

30

35Average percentage of funds which cease to exist over a rolling 3yr timescale

T<=25% 25%<T<=50% 50%<T<=75% 75%<T<=100% 100%<TBlend Value Growth Mid Small EM

Conclusion 3

In our view, choosing the right fund is more important than ever among high turnover funds. Get it right and our analysis suggests that you may earn higher returns than the top performing low turnover funds. However, get it wrong and performance could

turn out poorer than the worst performing low turnover funds and there is also an increased likelihood that the fund you invest in is closed down or liquidated.

Churn is not necessarily burn: debunking the myths of portfolio turnover20

An undesirable feature of high turnover fundsHistorically, high turnover funds have tended to underperform low turnover funds when markets have been crashing or volatility increasing. They struggled relative to low turnover funds in both the Dotcom crash and Global Financial Crisis as Figure 12 shows (a fi gure greater than zero is indicative of low turnover funds outperforming).