Homework Econ Finishing Macro transition to Micro Chapters 16-19 Bonus Homework Due Tuesday, March...

70

Homework Econ Finishing Macro transition to Micro Chapters 16-19 Bonus Homework Due Tuesday, March 7, 2006 • AP Packet V – We will be working on many of the activities in the packet. Some will be for homework credit. Graphing Test! Not Adjusted! Total Points=100! March 8 th at the very earliest. March 10 th at the very latest.

-

Upload

howard-taylor -

Category

Documents

-

view

221 -

download

2

Transcript of Homework Econ Finishing Macro transition to Micro Chapters 16-19 Bonus Homework Due Tuesday, March...

Homework Econ

Finishing Macro transition to Micro Chapters 16-19

Bonus Homework Due Tuesday, March 7, 2006

• AP Packet V – We will be working on many of the activities in the packet. Some will be for homework credit.

Graphing Test! Not Adjusted! Total Points=100!March 8th at the very earliest.March 10th at the very latest.

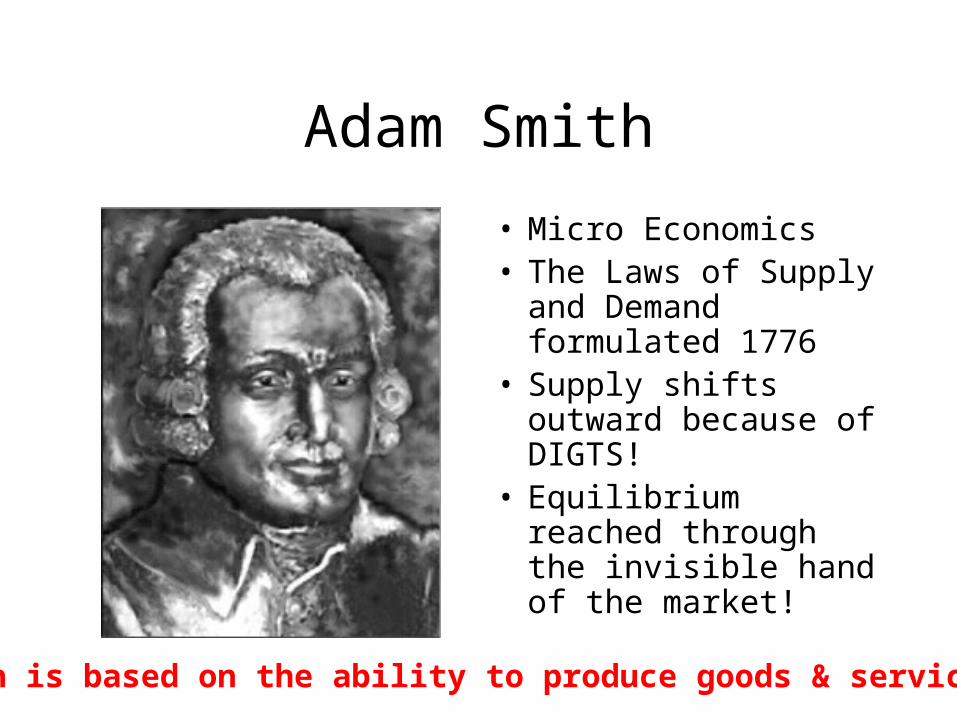

Adam Smith

• Micro Economics• The Laws of Supply

and Demand formulated 1776

• Supply shifts outward because of DIGTS!

• Equilibrium reached through the invisible hand of the market!

Wealth is based on the ability to produce goods & services!

David Ricardo Free Trade 1820’s

• Theories on Trade • Comparative Advantage• Trade is based on relative

opportunity cost.• Countries specialize in

production of products with the lowest opportunity cost.

Wealth is increased through specialization and trade!

J. B. Say 1830’s

• Supply creates its own demand!

• Aggregate supply is a vertical line!

• Demand determines only the price.

• Aggregate supply should be increased to improve standard of living!

Wealth is increased as output increases: “Supply creates Demand!

Classics and Keynes: AD-AS InterpretationClassics and Keynes: AD-AS Interpretation

Classical Economics...Classical Economics...

Classics and Keynes: AD-AS InterpretationClassics and Keynes: AD-AS Interpretation

Classical Economics...Classical Economics...Laissez-faireLaissez-faire

Classics and Keynes: AD-AS InterpretationClassics and Keynes: AD-AS Interpretation

Classical Economics...Classical Economics...Laissez-faireLaissez-faireVertical aggregate supply curveVertical aggregate supply curve

Classics and Keynes: AD-AS InterpretationClassics and Keynes: AD-AS Interpretation

Classical Economics...Classical Economics...Laissez-faireLaissez-faireVertical aggregate supply curveVertical aggregate supply curveStable aggregate demandStable aggregate demand

Classics and Keynes: AD-AS InterpretationClassics and Keynes: AD-AS Interpretation

Classical Economics...Classical Economics...Laissez-faireLaissez-faireVertical aggregate supply curveVertical aggregate supply curveStable aggregate demandStable aggregate demand

• Quantity of money held byQuantity of money held byhouseholds & businesseshouseholds & businesses

Classics and Keynes: AD-AS InterpretationClassics and Keynes: AD-AS Interpretation

Classical Economics...Classical Economics...Laissez-faireLaissez-faireVertical aggregate supply curveVertical aggregate supply curveStable aggregate demandStable aggregate demand

• Quantity of money held byQuantity of money held byhouseholds & businesseshouseholds & businesses

• Purchasing power of money isPurchasing power of money isdetermined by the price leveldetermined by the price level

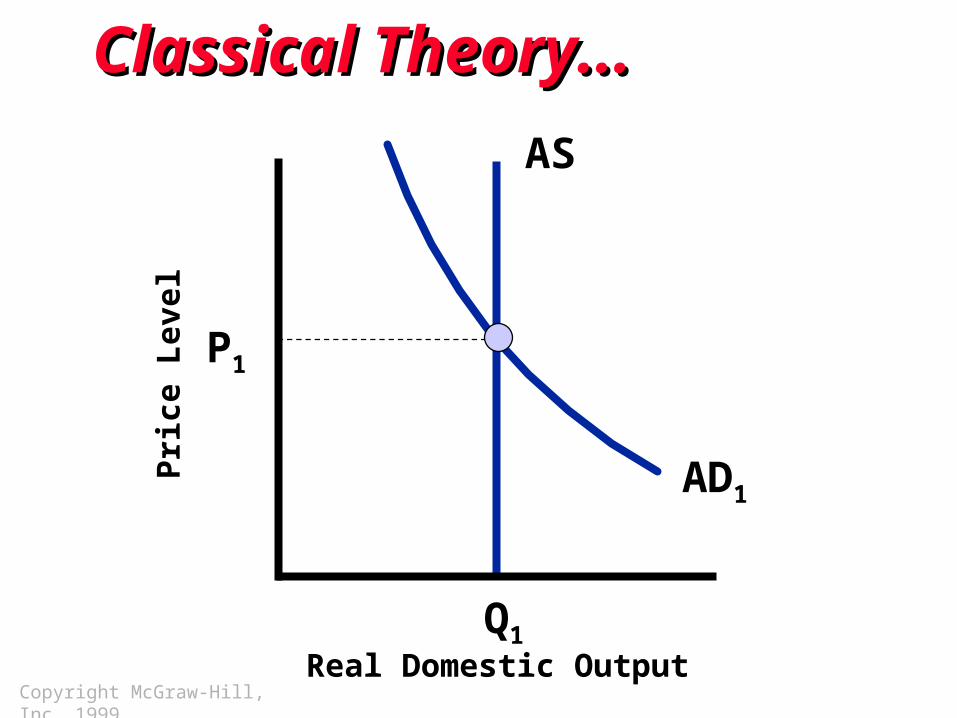

Classical Theory...Classical Theory...

P1

Q1

Pri

ce L

evel

Real Domestic Output

AS

AD1

Copyright McGraw-Hill, Inc. 1999

Classical Theory...Classical Theory...

P1

Q1

P2

Pri

ce L

evel

Real Domestic Output

AS

AD1

AD2

Copyright McGraw-Hill, Inc. 1999

John Maynard Keynes – 1930’s

• Father of Keynesian Economics

• Macro economies my be fine tuned!

• Fiscal policy may be used expand aggregate demand.

• Aggregate supply is horizontal not vertical

An absence of Demand makes Supply meaningless!

Milton Friedman 1950’s – 2000’s!

• A limited role for government!

• No Fiscal or Federal Reserve interventions

• Simply grow the money supply at 3-5% to grow the economy!

Increasing Money Supply will increase NGDP!MS * V = NGDP

VELOCITY: Stable or UnstableStable or Unstable

Monetarists: Monetarists: VV is Stable... is Stable...

AP Test 2004

VELOCITY: Stable or UnstableStable or Unstable

Monetarists: Monetarists: VV is Stable... is Stable...

Greater money supply causesspending and higher price levels

VELOCITY: Stable or UnstableStable or Unstable

Monetarists: Monetarists: VV is Stable... is Stable...

Greater money supply causesspending and higher price levels

Monetarists: Monetarists: Causes of InstabilityCauses of Instability

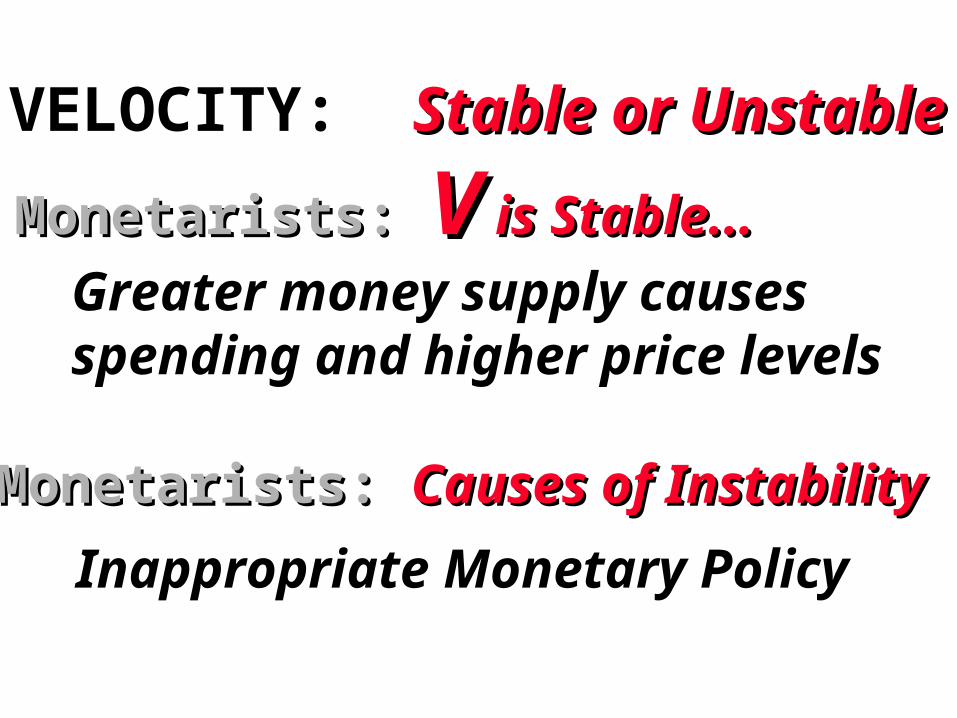

VELOCITY: Stable or UnstableStable or Unstable

Monetarists: Monetarists: VV is Stable... is Stable...

Greater money supply causesspending and higher price levels

Monetarists: Monetarists: Causes of InstabilityCauses of Instability

Inappropriate Monetary Policy

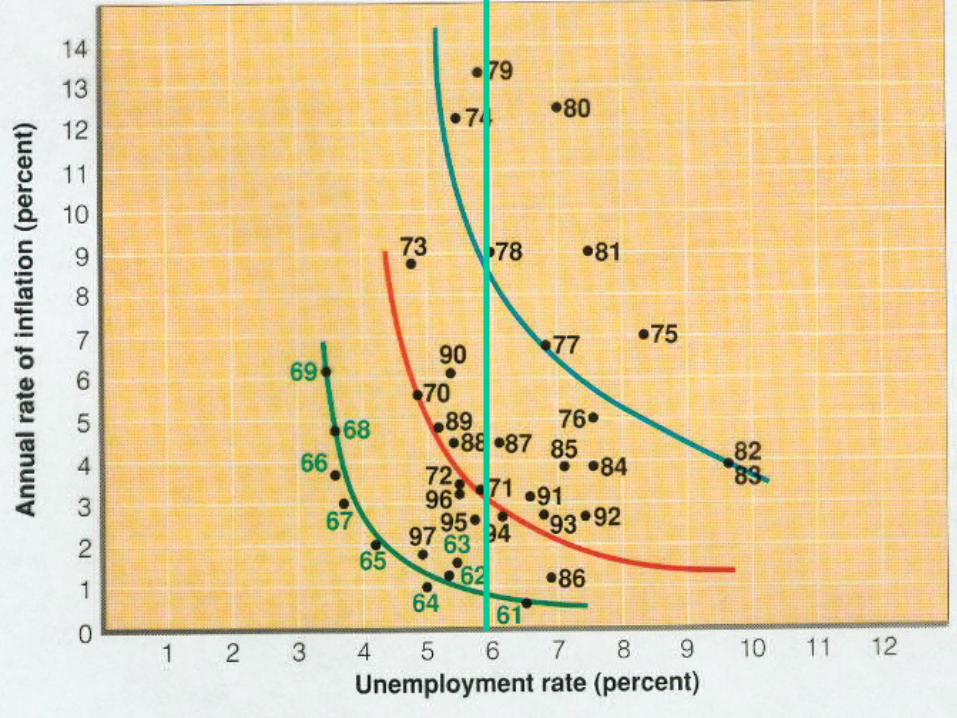

Alban W. Phillips

• Discovers and explained the relationship between inflation & unemployment!

• Discovered that they may not exist simultaneously!

Provide a Keynesian Trade Off Between Inflation & Unemployment!Fine Tuning An Aggregate Economy Was Possible!

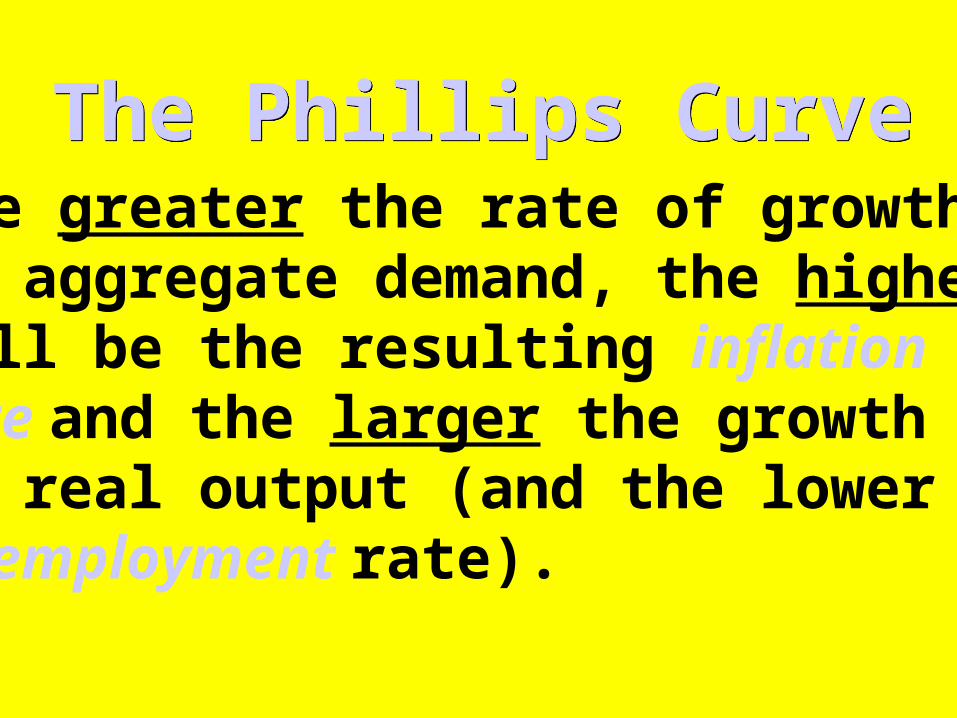

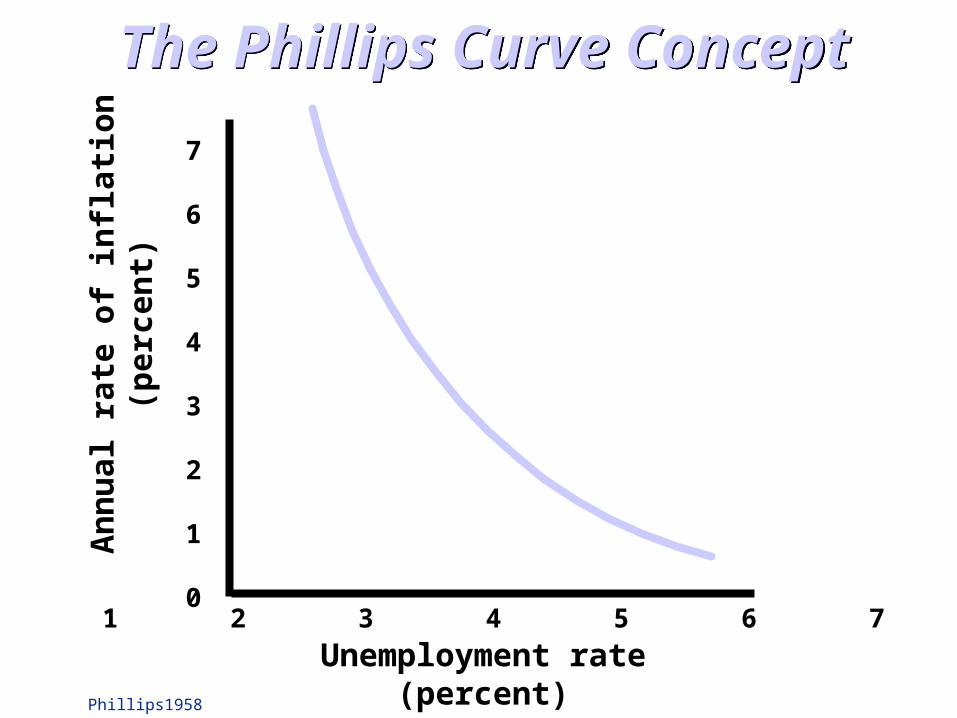

The Phillips CurveThe Phillips CurveThe greater the rate of growthof aggregate demand, the higherwill be the resulting inflationrate and the larger the growthof real output (and the lower theunemployment rate).

An

nu

al r

ate

of in

flat

ion

(per

cen

t)

Unemployment rate(percent)

7

6

5

4

3

2

1

01 2 3 4 5 6 7

The Phillips Curve ConceptThe Phillips Curve Concept

Phillips1958

An

nu

al r

ate

of in

flat

ion

(per

cen

t)

Unemployment rate(percent)

7

6

5

4

3

2

1

01 2 3 4 5 6 7

as inflation declines....

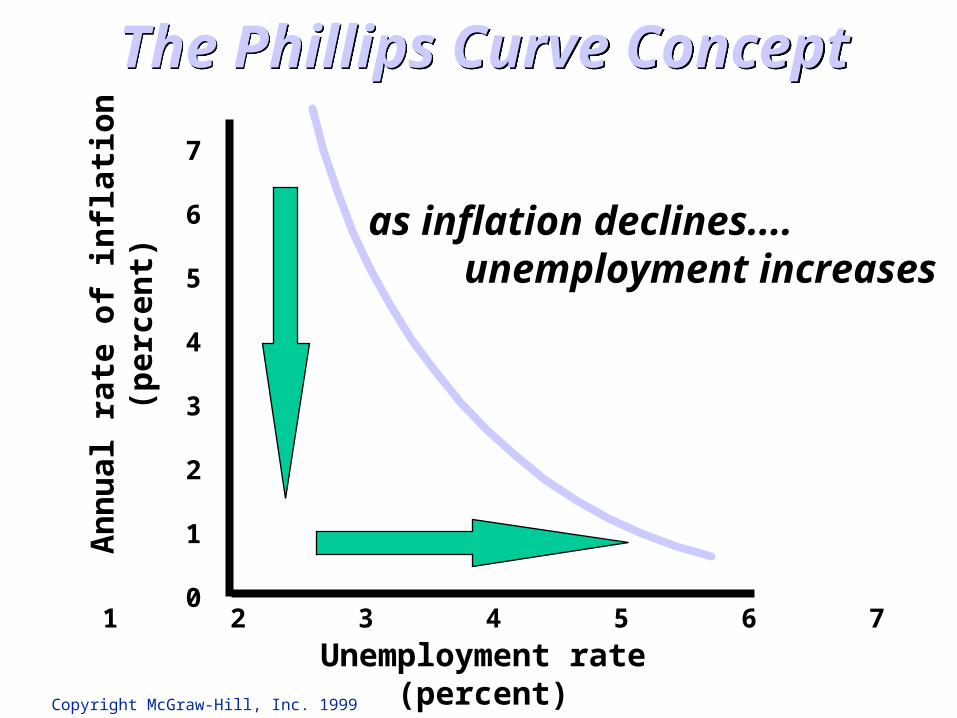

The Phillips Curve ConceptThe Phillips Curve Concept

Copyright McGraw-Hill, Inc. 1999

An

nu

al r

ate

of in

flat

ion

(per

cen

t)

Unemployment rate(percent)

7

6

5

4

3

2

1

01 2 3 4 5 6 7

as inflation declines....unemployment increases

The Phillips Curve ConceptThe Phillips Curve Concept

Copyright McGraw-Hill, Inc. 1999

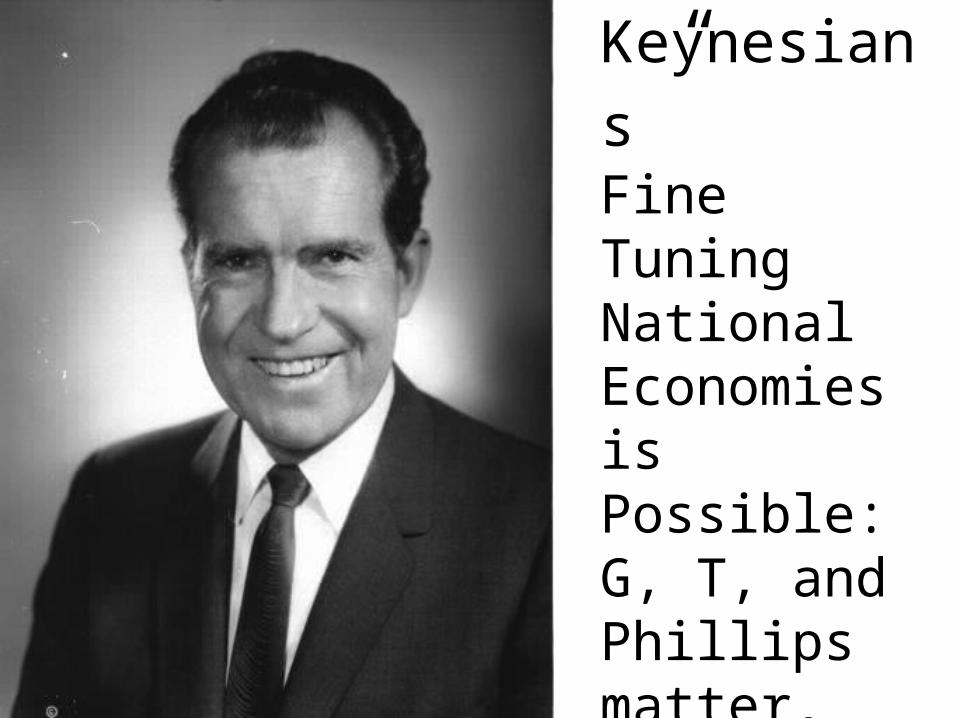

“We’re all

Keynesians”Fine Tuning National Economies is Possible: G, T, and Phillips matter, deficits don’t!

Stabilization Policy DilemmaStabilization Policy DilemmaPolicies to manage aggregate demand canbe used to choose a point on the PhillipsCurve, but such policies do not improvethe “unemployment rate-inflation rate”tradeoff embodied in the curve .

Policies to manage aggregate demand canbe used to choose a point on the PhillipsCurve, but such policies do not improvethe “unemployment rate-inflation rate”tradeoff embodied in the curve .

Stagflation: A Shifting Phillips Curve?

Stagflation: A Shifting Phillips Curve?

Can a Noble Prize be taken way?

AdverseAdverse

AggregateAggregate

SupplySupply

ShocksShocks

Copyright McGraw-Hill, Inc. 1999

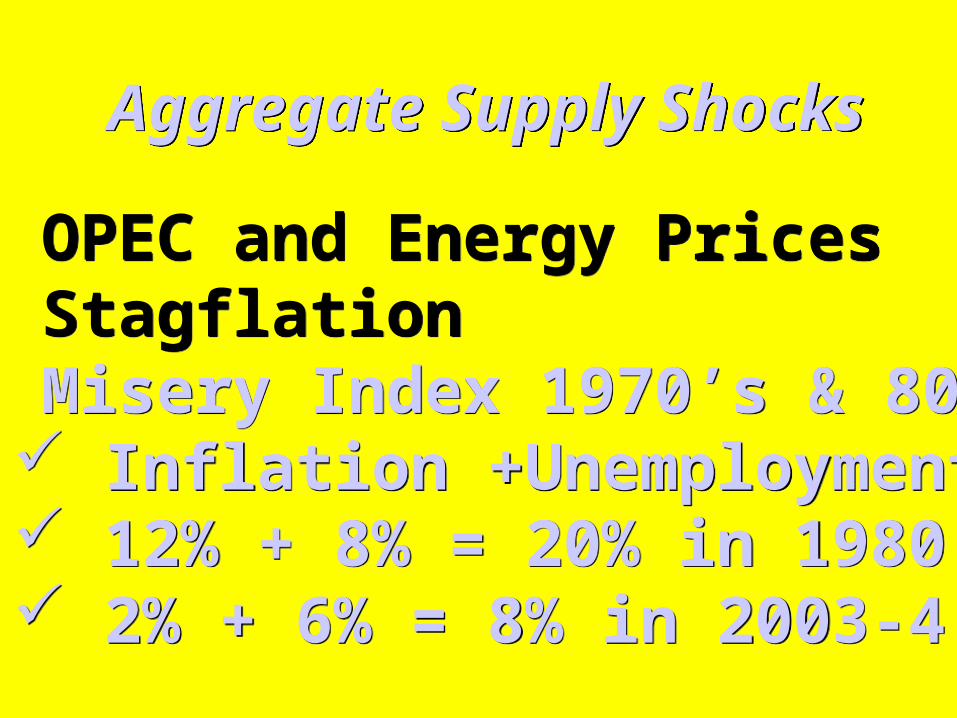

• OPEC and Energy Prices• Stagflation • Misery Index 1970’s & 80’s

Inflation +Unemployment 12% + 8% = 20% in 1980 2% + 6% = 8% in 2003-4

• OPEC and Energy Prices• Stagflation • Misery Index 1970’s & 80’s

Inflation +Unemployment 12% + 8% = 20% in 1980 2% + 6% = 8% in 2003-4

Aggregate Supply ShocksAggregate Supply Shocks

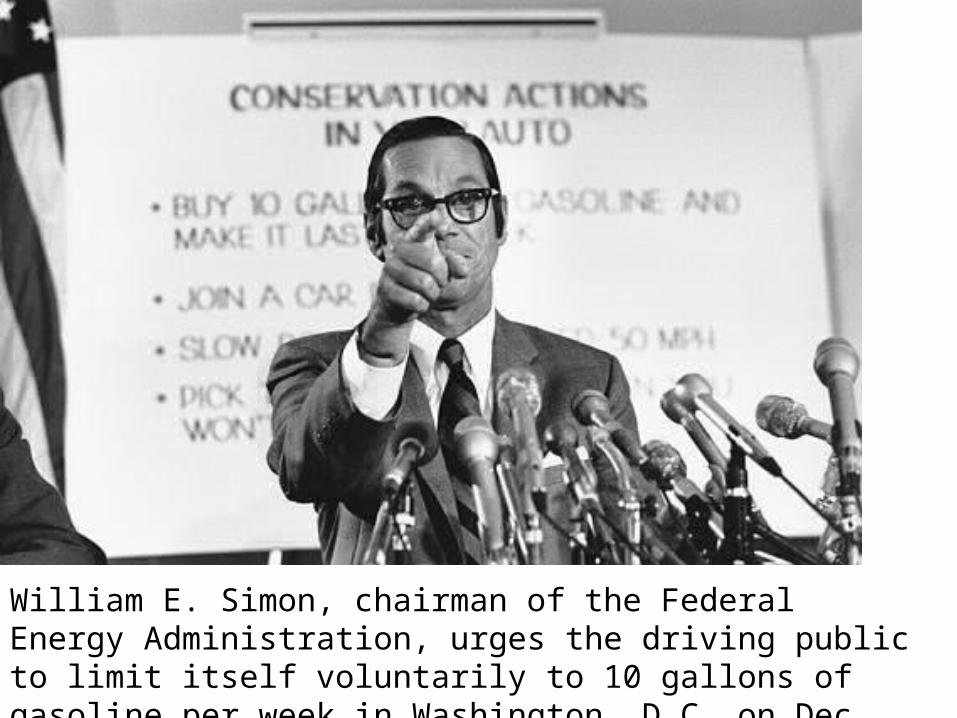

William E. Simon, chairman of the Federal Energy Administration, urges the driving public to limit itself voluntarily to 10 gallons of gasoline per week in Washington, D.C. on Dec. 20, 1973.

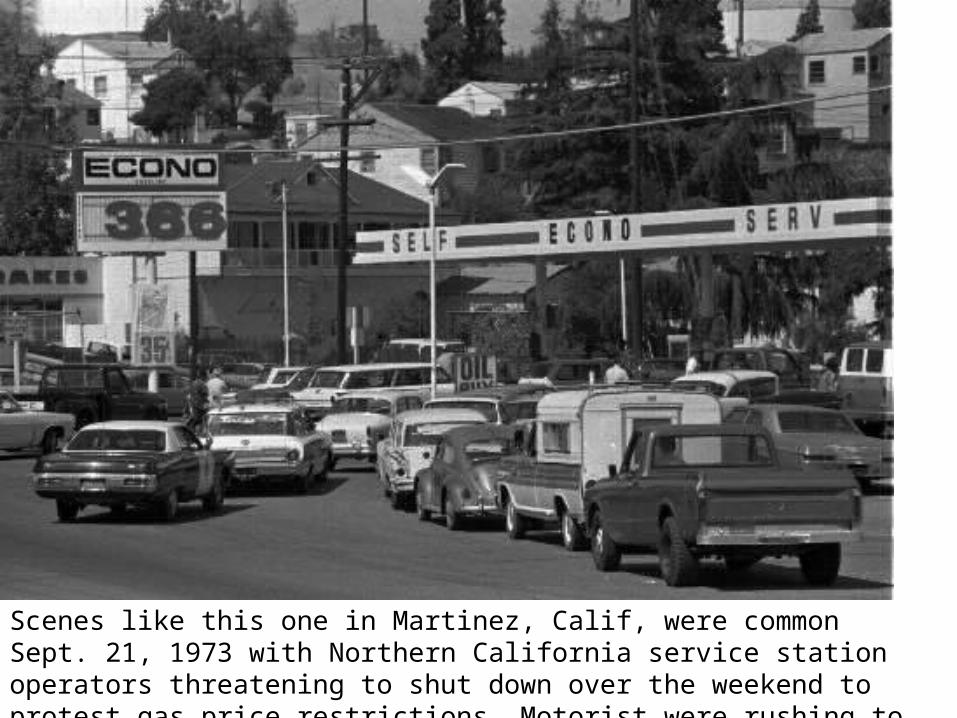

Scenes like this one in Martinez, Calif, were common Sept. 21, 1973 with Northern California service station operators threatening to shut down over the weekend to protest gas price restrictions. Motorist were rushing to fill their gas tanks.

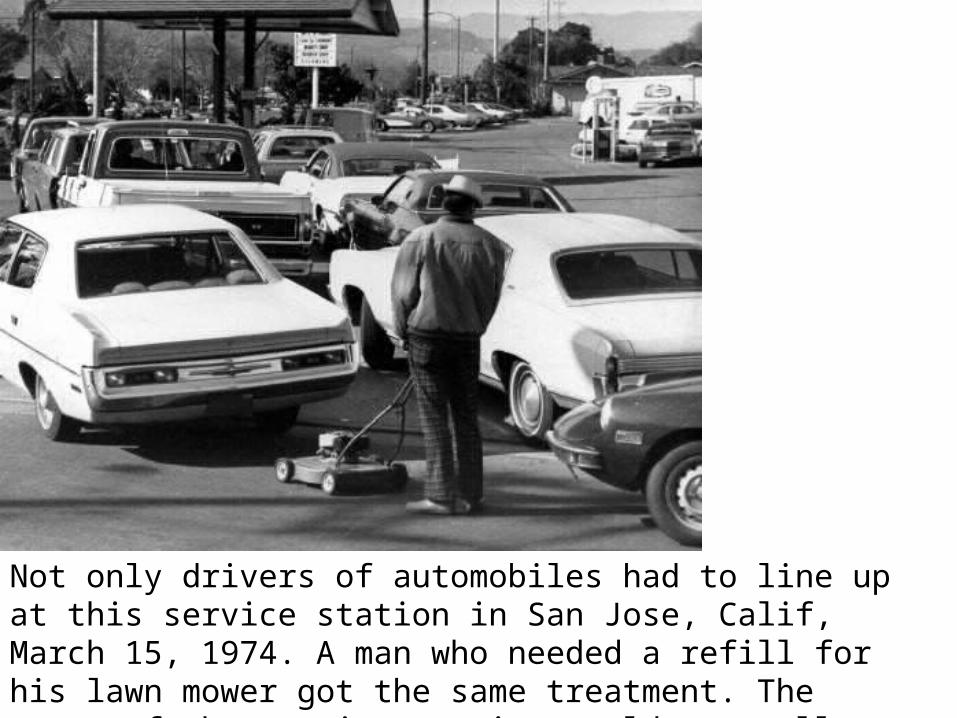

Not only drivers of automobiles had to line up at this service station in San Jose, Calif, March 15, 1974. A man who needed a refill for his lawn mower got the same treatment. The owner of the service station would not sell gas to people showing up with containers.

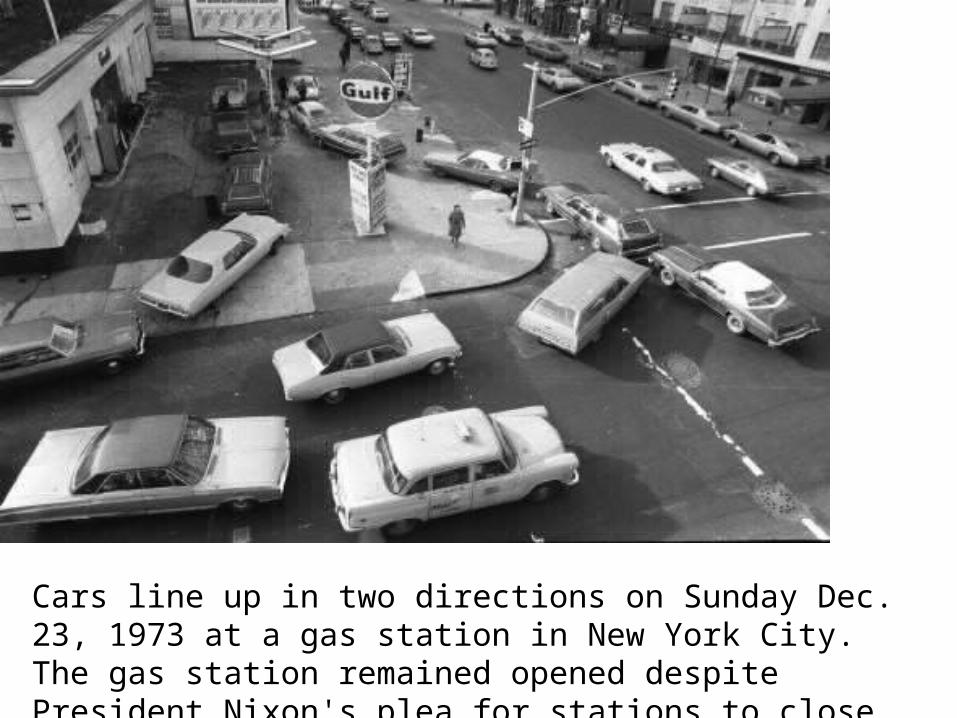

Cars line up in two directions on Sunday Dec. 23, 1973 at a gas station in New York City. The gas station remained opened despite President Nixon's plea for stations to close on Sundays.

This is an aerial View of the Safeway gas station, on Northern Blvd. and 36th street, in the Queens section of New York City on Feb. 8, 1974 during the energy crisis.

The pumps are here!

The line waiting forGas!

U.S. President Jimmy Carter signs his energy proposals in the Oval Office of the White House in Washington, D.C., Wednesday, Jan. 26, 1977. At left is his energy adviser James Schlesinger. The proposals are expected to help areas hit by the gas shortage.

o

P1

Q2

AD

AS1

AS2

Q1

P2

Aggregate Supply ShocksAggregate Supply Shocks

Pri

ce L

evel

Real domestic output

Negative growth with rising prices!

Natural Rate HypothesisNatural Rate Hypothesisdoubts the existence of an inverserelationship between inflation and unemployment....

doubts the existence of an inverserelationship between inflation and unemployment....

Two VariantsTwo VariantsAdaptive Expectations TheoryRational Expectations TheoryAdaptive Expectations TheoryRational Expectations Theory

Long-Run Vertical Phillips Curve Long-Run Vertical Phillips Curve Adaptive expectations implies a long-run Vertical Phillips Curve atthe Natural Rate of Unemployment

Adaptive expectations implies a long-run Vertical Phillips Curve atthe Natural Rate of Unemployment

Rational expectations implies thatthe workings of the economy is understood, and that fiscal andand monetary policy will beanticipated rendering the policyineffective

Rational expectations implies thatthe workings of the economy is understood, and that fiscal andand monetary policy will beanticipated rendering the policyineffective

An

nu

al r

ate

of in

flat

ion

(per

cen

t)

Unemployment rate(percent)

7

6

5

4

3

2

1

01 2 3 4 5 6 7

The Phillips Curve ConceptThe Phillips Curve Concept

Phillips1958

Short RunPhillipsCurves

Long RunPhillipsCurve

Stagflation

• The 1970’s saw a tripling of oil prices

• The 1970’s saw draught and a series of massive crop failures

• Aggregate supply shifted to the left

• Neither Keynesian nor Fed policy presents a good solution!

Donald H. Rumsfeld, and Uncle Richard B. Cheney

Arthur Laffer

David Stockman

That’s a voodoo economics if you ask me!

Arthur Laffer

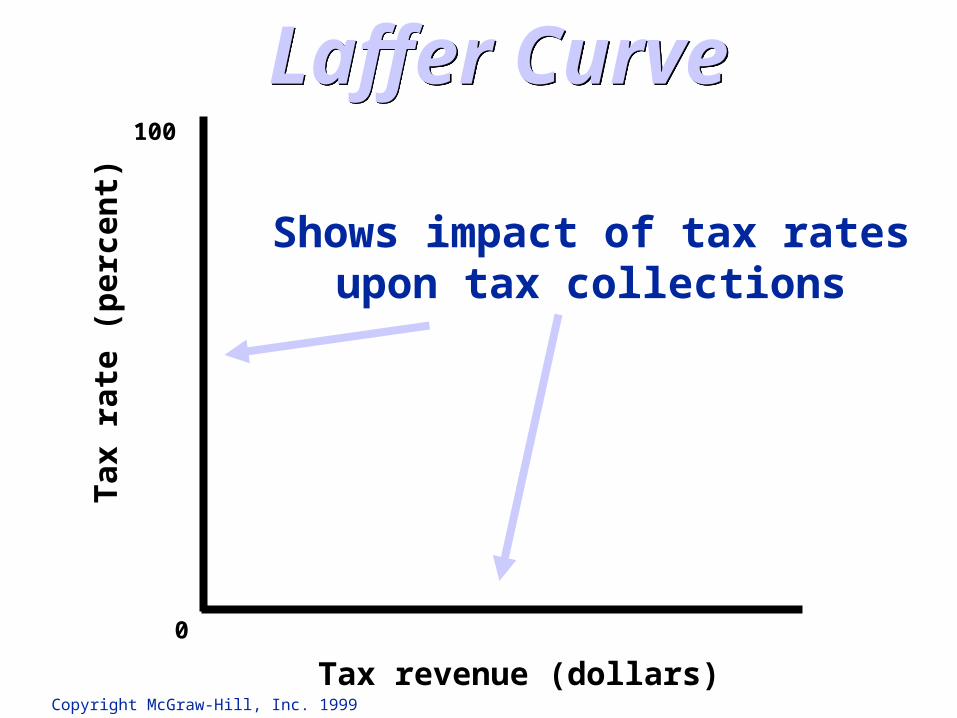

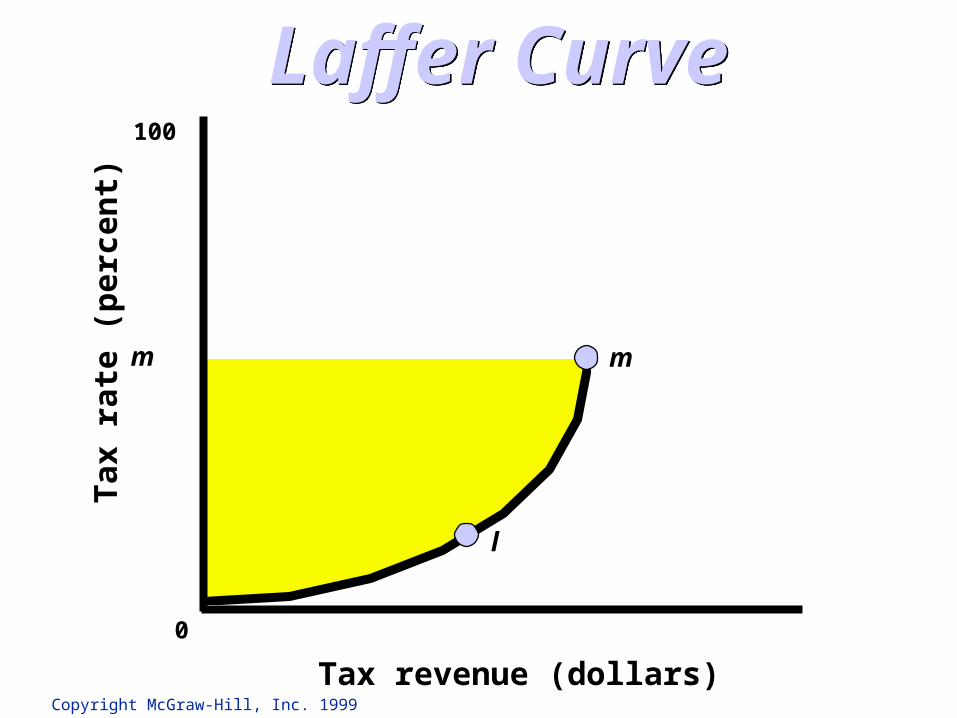

• Laffer’s curve became the basis for Reaganomics and the Tax Cutting policies of the Republican Party!

• Reagan’s tax cuts sent deficits soaring in the 1980’s

Tax cuts stimulate growth shifting AS outward ending Stagflation!

0

100

Shows impact of tax ratesupon tax collections

Laffer CurveLaffer Curve

Tax revenue (dollars)

Tax

rat

e (p

erce

nt)

Copyright McGraw-Hill, Inc. 1999

0

100

l

Laffer CurveLaffer Curve

Tax revenue (dollars)

Tax

rat

e (p

erce

nt)

Copyright McGraw-Hill, Inc. 1999

0

100

m m

l

Laffer CurveLaffer Curve

Tax revenue (dollars)

Tax

rat

e (p

erce

nt)

Copyright McGraw-Hill, Inc. 1999

0

100

m m

n

l

Laffer CurveLaffer Curve

Tax revenue (dollars)

Tax

rat

e (p

erce

nt)

Copyright McGraw-Hill, Inc. 1999

0

100

m m

n

l

Laffer CurveLaffer Curve

Tax revenue (dollars)

Tax

rat

e (p

erce

nt)

Copyright McGraw-Hill, Inc. 1999

Supply-Side EconomicsSupply-Side Economics

•Tax Cuts: To stimulate Business Investment To induce incentives to work•Deregulation of Business•Incentives to save and invest

• Laffer Curve as a ProofLess tax evasion

•Tax Cuts: To stimulate Business Investment To induce incentives to work•Deregulation of Business•Incentives to save and invest

• Laffer Curve as a ProofLess tax evasion

It’s All About Increased Output!

P

Q

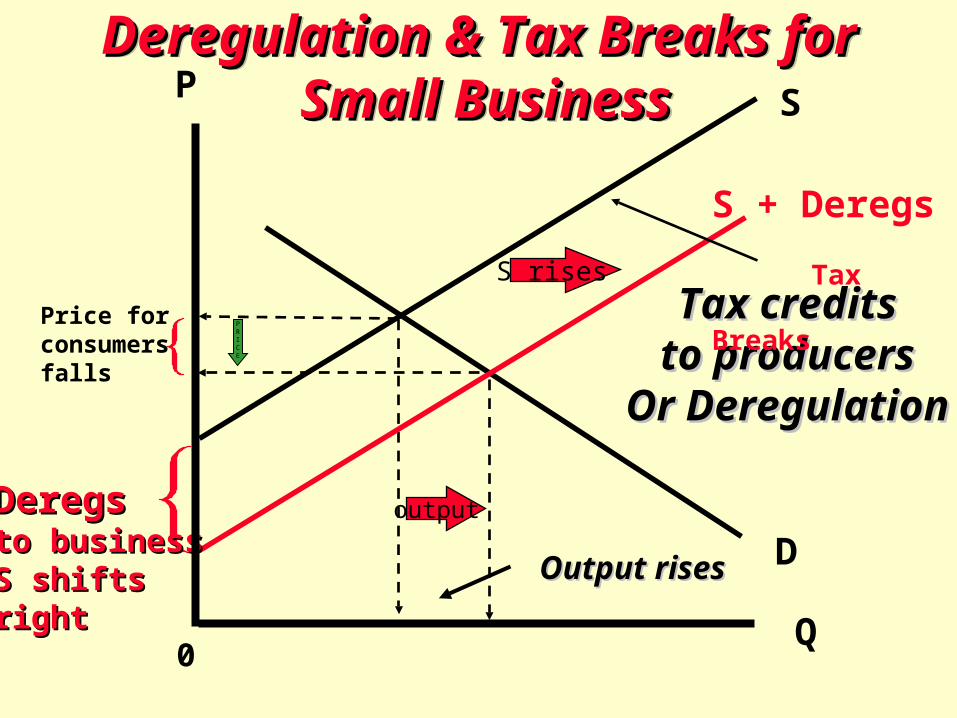

Deregulation & Tax Breaks forDeregulation & Tax Breaks for Small BusinessSmall Business

Deregulation & Tax Breaks forDeregulation & Tax Breaks for Small BusinessSmall Business

D

0

Tax creditsTax creditsto producersto producers

Or DeregulationOr Deregulation

S rises

S

S + Deregs

Tax Breaks

DeregsDeregsto businessto businessS shifts S shifts rightright

output

Output risesOutput rises

Price for consumersfalls

PRICE

o

P2

Q1

AD

AS2 = Sum allMicro Supply

AS1

Q2

P1

Supply-Side EconomicsSupply-Side Economics

Pri

ce L

evel

Real domestic output

Micro Growth of Small Business Spurs Aggregate Growth

StagflationCan End AsPrice LevelFalls andRGDP, Output, &EmploymentRise!

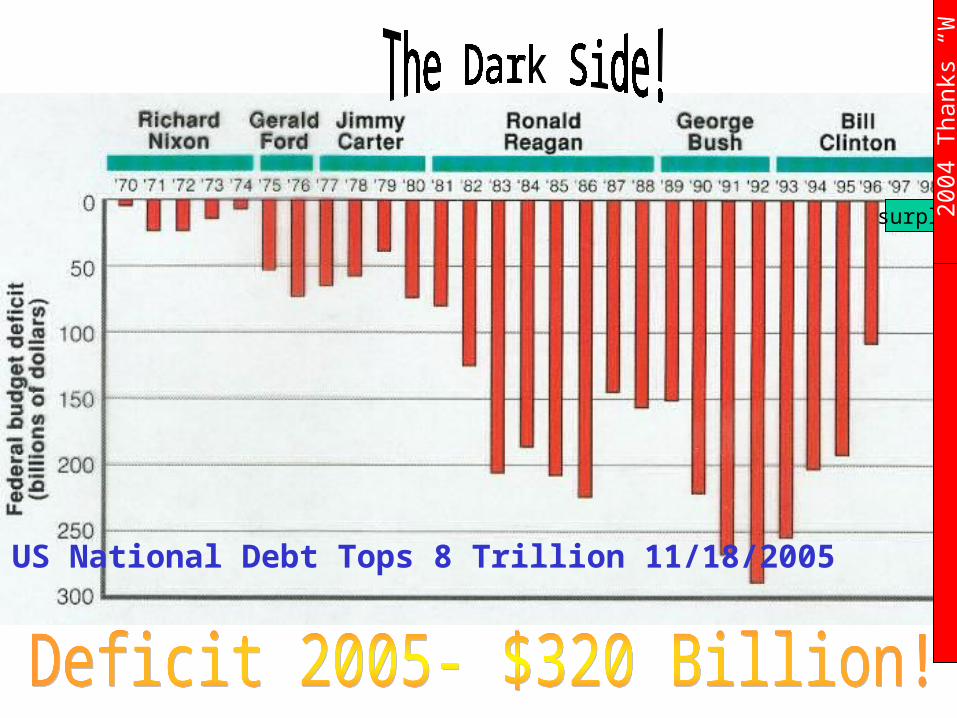

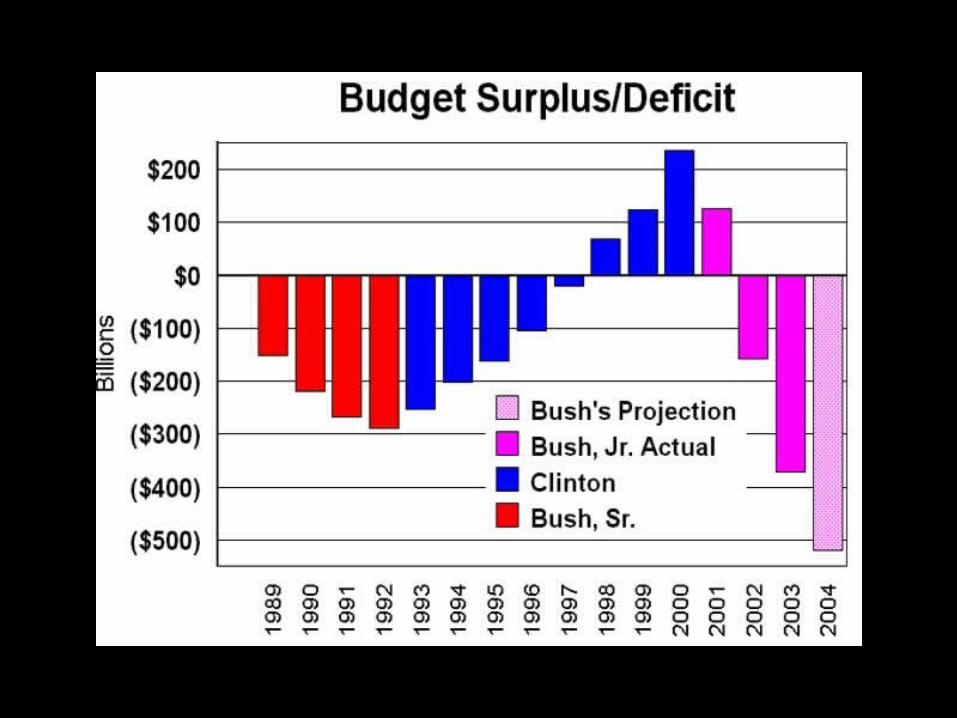

surplus

2 00 4

Th a

n ks

“ W”!

US National Debt Tops 8 Trillion 11/18/2005

No LoansFor College!

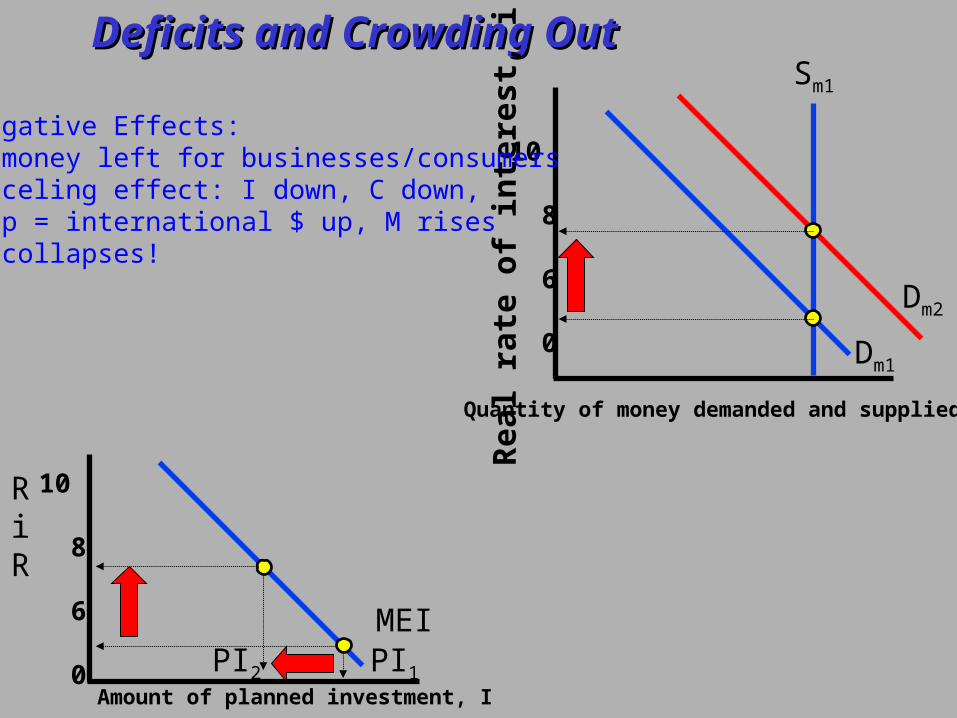

Deficits and Crowding OutDeficits and Crowding Out

Rea

l rat

e of

inte

rest

, i

10

8

6

0

Sm1

Quantity of money demanded and supplied

Dm1

Dm2

Amount of planned investment, I

RiR

10

8

6

0

MEIPI1PI2

The Negative Effects:1. No money left for businesses/consumers2. Canceling effect: I down, C down,3. i up = international $ up, M rises4. AD collapses!

Criticisms of the Laffer CurveCriticisms of the Laffer Curve• Taxes: Incentives and Time• Who Benefits from Tax Cuts• Position on Curve

• Taxes: Incentives and Time• Who Benefits from Tax Cuts• Position on Curve

Other Supply-Side IssuesOther Supply-Side Issues• Deficits

• Industrial regulation• Social regulation

• Reaganomics: success or failure

• Deficits• Industrial regulation• Social regulation

• Reaganomics: success or failure

GROWTH ofAggregate Supply?

GROWTH ofAggregate Supply?

Are we presently growingas a National Economy?

Two Economic Growth Definitions:Two Economic Growth Definitions:

• An increase in real GDP occurringover a period of time

• An increase in real GDP per capitaoccurring over a period of time

• An increase in real GDP occurringover a period of time

• An increase in real GDP per capitaoccurring over a period of time

Growth EconomicsGrowth Economics

Supplyside’s Goal:Shift AS, LRAS, PPC right!

Growth as a GoalGrowth as a GoalIngredients of Growth:Ingredients of Growth:

Quantity & quality of natural resources

Quantity & quality of human resources

Supply or stock of capital goods

Technology

Quantity & quality of natural resources

Quantity & quality of human resources

Supply or stock of capital goods

Technology

Growth EconomicsGrowth Economics

PRODUCTION POSSIBILITIESPRODUCTION POSSIBILITIES

Economic Growth

Q

Q

A

B

C

D

a

b

Cap

ital

Go

od

sC

apit

al G

oo

ds

Consumer GoodsConsumer Goods

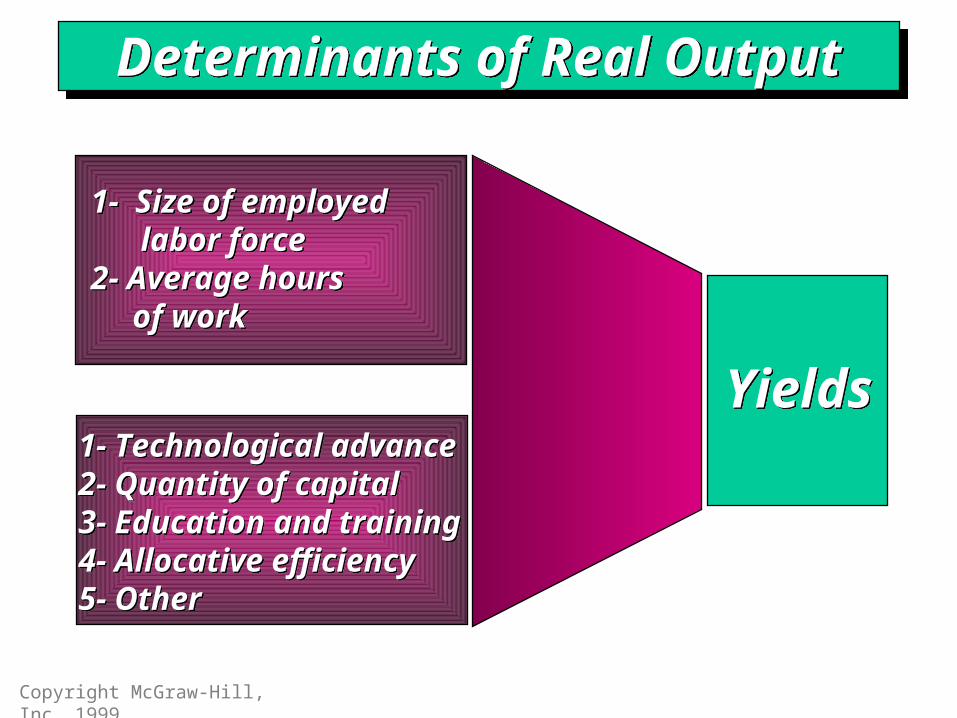

1- Size of employed labor force2- Average hours of work

1- Size of employed labor force2- Average hours of work

1- Technological advance2- Quantity of capital3- Education and training4- Allocative efficiency5- Other

1- Technological advance2- Quantity of capital3- Education and training4- Allocative efficiency5- Other

Determinants of Real OutputDeterminants of Real Output

1- Size of employed labor force2- Average hours of work

1- Size of employed labor force2- Average hours of work

1- Technological advance2- Quantity of capital3- Education and training4- Allocative efficiency5- Other

1- Technological advance2- Quantity of capital3- Education and training4- Allocative efficiency5- Other

YieldsYields

Determinants of Real OutputDeterminants of Real Output

Copyright McGraw-Hill, Inc. 1999

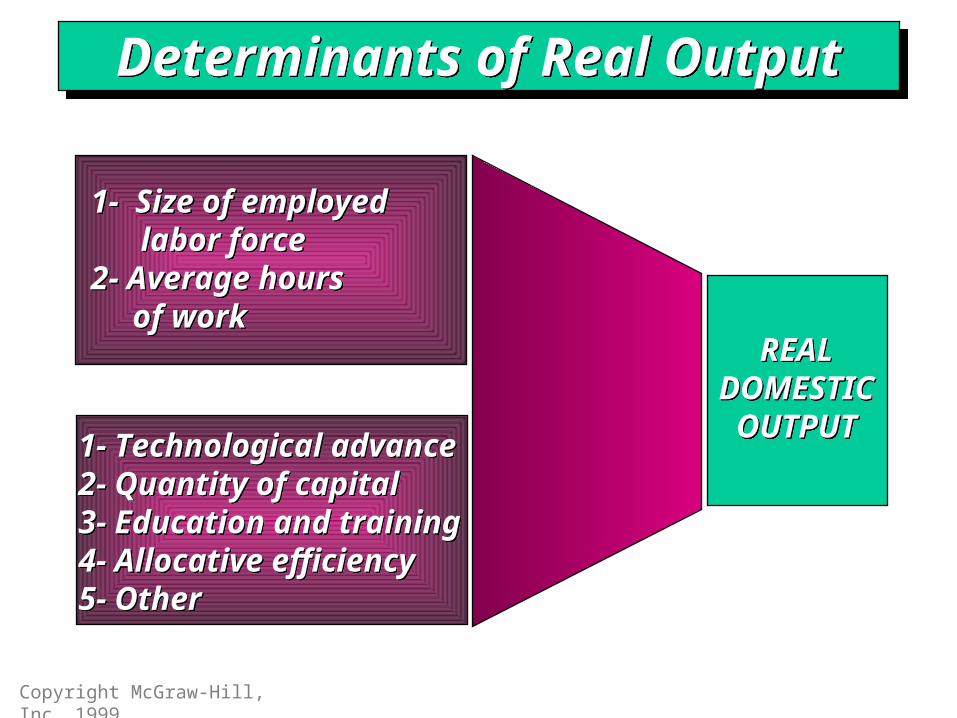

1- Size of employed labor force2- Average hours of work

1- Size of employed labor force2- Average hours of work

1- Technological advance2- Quantity of capital3- Education and training4- Allocative efficiency5- Other

1- Technological advance2- Quantity of capital3- Education and training4- Allocative efficiency5- Other

REALDOMESTIC

OUTPUT

REALDOMESTIC

OUTPUT

Determinants of Real OutputDeterminants of Real Output

Copyright McGraw-Hill, Inc. 1999

AD - AS FrameworkAD - AS FrameworkP

rice

Lev

el

RGDP – OUTPUT - EMPLOYMENT

o

P1

AS’2

LRAS1

$5 Trillion

LRAS2

$12 Trillion

AD1

AS’1

AD2

P2

PRODUCTION POSSIBILITIESPRODUCTION POSSIBILITIES

Economic Growth

Q

Q

A

B

C

D

a

b

Cap

ital

Go

od

sC

apit

al G

oo

ds

Consumer GoodsConsumer Goods

Real GDP has increasedsixfold since 1940

Real GDP has increasedsixfold since 1940

Improved Products and ServicesAdded LeisureEnvironmental Effects

Improved Products and ServicesAdded LeisureEnvironmental Effects

United StatesGrowth

United StatesGrowth

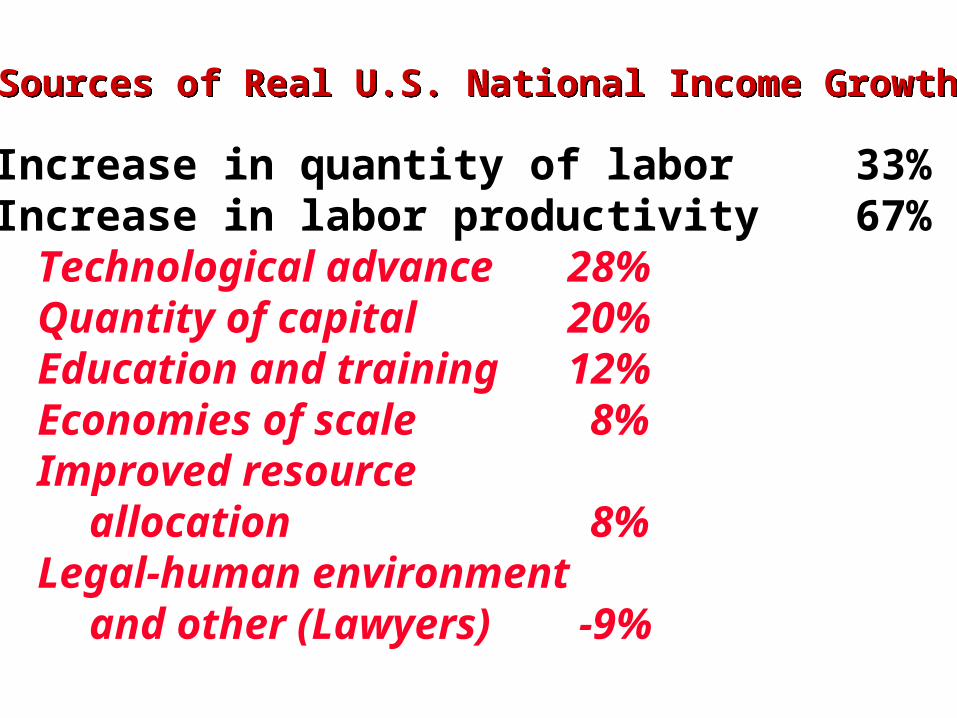

Sources of Real U.S. National Income GrowthSources of Real U.S. National Income Growth

Increase in quantity of labor 33%Increase in labor productivity 67% Technological advance 28% Quantity of capital 20% Education and training 12% Economies of scale 8% Improved resource

allocation 8% Legal-human environment

and other (Lawyers) -9%

Causes Slowed ProductivityCauses Slowed Productivity1- Labor Quality

Decline in experienceLess able workersSlowing of rise in educational attainment

2- Technological Progress3- Investment – 1990’s Bubble

Low saving rateImport competitionRegulationReduced infrastructure spending

1- Labor QualityDecline in experienceLess able workersSlowing of rise in educational attainment

2- Technological Progress3- Investment – 1990’s Bubble

Low saving rateImport competitionRegulationReduced infrastructure spending