GNI PROPOSALS ON NEW CONNECTIONS POLICY · GNI proposals on Connection Policy Dec 14 2 Background...

21

2015 GNI PROPOSALS ON NEW CONNECTIONS POLICY JANUARY 2015

Transcript of GNI PROPOSALS ON NEW CONNECTIONS POLICY · GNI proposals on Connection Policy Dec 14 2 Background...

2015

GNI PROPOSALS ON NEW CONNECTIONS POLICY

JANUARY 2015

GNI proposals on Connection Policy Dec 14 1

Contents

Background............................................................................................................................ 2

Rationale for Change............................................................................................................ 2

Proposal 1: Amendments to Financial Security Criteria ............................................ 3

Proposal 2: Inclusion of Transmission Revenue in all appraisals ............................. 8

Proposal 3: Amendment of Institutional I & C Customers .................................... 12

Proposal 4: Proposals on Existing Gas Areas ........................................................... 14

Proposal 5: Group Sites (different entities, same corridor) ..................................... 16

Proposal 6: Group Sites (same entity, different sites) ............................................... 17

Proposal 7: Treatment of CNG Connections ............................................................ 18

Summary & Conclusions .............................................................................................. 20

GNI proposals on Connection Policy Dec 14 2

Background

The Connections Policy was approved by the CER on 6th April, 2006 and is a

single connections policy dealing with connections to both the Transmission

and Distribution networks. The policy sets out the detailed criteria for the

evaluation of extensions to the gas network, including extensions to towns not

currently served by natural gas.

While there were some changes to the policy in the interim, the current policy

has been in effect since April 2006. This paper seeks to outline some proposed

amendments to the connections policy to enhance the level of economic

connections to the gas network.

The context of this review is that areas of the current policy may be hampering

the full realisation of the potential economically efficient demand and load

growth available for the gas network in Ireland. While the overall risk will be

increased, Gas Networks Ireland (GNI) believe that this is mitigated as these

proposed changes will facilitate additional connections, who would not

otherwise connect to the Natural Gas network under the existing Connections

Policy. The addition of the extra load to the system will have the effect of

reducing tariffs for existing customers in the long term.

Separate to this review of the Connections Policy, GNI is working on the roll-out

of a range of initiatives aimed at furthering public awareness of the availability

and benefits of natural gas versus other fuels. Initiatives to promote the use of

natural gas as a clean, efficient and cost competitive fuel for transport, along

with integration of biogas in the network are also currently being implemented.

Rationale for Change

There are significant benefits associated with increasing the load on the gas

network. A key benefit is the ability to spread the cost of running the network

over a larger customer base, thus achieving economies of scale and a lower

tariff rate for customers. New incremental load also offsets decreases in

consumption arising from the loss of existing gas sites (e.g. disconnected sites)

and/or lower gas usage by existing gas sites.

“Encouraging the connection of new customer load where it is efficient which

should in the medium and long term increase throughput and reduce unit

tariffs for all gas customers”

--- Current Connection Policy

GNI proposals on Connection Policy Dec 14 3

Proposal 1: Amendments to Financial Security Criteria

Background and Key Issues:

Under the provisions of the current connections policy, Financial Security (FS) is

required where the total cost of a connection, less the Customer Contribution,

is at least €250,000. Where a connection meets this threshold, the customer

must provide appropriate Financial Security in accordance with the Financial

Security policy and sign up to a Large Network Connection Agreement (LNCA).

In light of feedback from new and potential customers, a review of the €250k

threshold is appropriate. While there will always be increased risk associated

with adjusting the requirements of FS to make it easier for more customers to

connect to the network, it is important to ensure growth such that tariffs for

existing customers will not increase in the long term. This needs to be balanced

with the Regulated Asset Base being underpinned appropriately by the

provision of Financial Security.

It is not proposed to amend section 5.2.2 of the current Connections Policy

which states that for Large Daily Metered and Daily Meters customers, a de

minimis level of capacity will be set in the Capacity Register for the term

required to pay back the outstanding connection costs. The de minimis level of

capacity will be based on the projected load profile provided by the customer

and used in the connection appraisal.

The risk of an LDM or DM customer booking less capacity than was appraised

would therefore not materialise. The increased risk associated with the

proposed changes is reduced to the possibility of a new I&C customer

disconnecting. In practice, few large customers disconnect within their capacity

commitment period, and in general, if a large customer does disconnect, a new

customer will take over the premises.

Considering the above, and after completing an analysis of the need for

Financial Security, it is clear that the additional throughput stemming from

these otherwise non-users, will bring down the tariffs in the long term and

benefit all customers on the network. It is the view of GNI that the benefits of

additional growth outweighs the overall risk to the system as a result of the

changes proposed. For example, GNI have identified a number of customers

who have expressed interest in connecting but have highlighted the LNCA and

the Financial Security as a barrier to proceeding with a connection. GNI has

done some analysis and if three of these missed opportunities did connect to

the Natural Gas network, the impact is a potential 0.24% reduction in the

Distribution tariff.

GNI proposals on Connection Policy Dec 14 4

GNI proposed changes

Proposed amendments to the FS for new connections are outlined below:

i. Increase the FS threshold

ii. Introduce a tiered threshold for FS that recognises the relative payback

period for alternative projects

iii. Adjust the credit rating applied to Letters of Credit for Financial Security

associated with new connections

Proposal 1.1: FS Threshold

GNI believe it is appropriate the raise threshold at which Financial Security

applies. A base threshold of €500k is proposed as GNI’s view is that the current

threshold of €250k is too low.

Proposal 1.2: Tiered Threshold

GNI believe it is appropriate to introduce a tiered threshold to more

appropriately reflect the relative payback periods of alternative connections. If

Project A has a quicker payback period than Project B then all else being equal,

the relative financial risk of Project A is lower and this should be reflected by

the requirement for Financial Security.

The GNI proposals are as follows:

If the project becomes NPV positive in 7 years or more, and/or a supplemental

contribution is required, the proposed threshold for Financial Security is €500k.

If the project becomes NPV positive in years 4, 5 or 6, the proposed threshold

for Financial Security is €750k.

If the project becomes NPV positive in 3 years or less, the proposed threshold

whereby Financial Security is required, is €1m.

NPV Positive in Threshold LNCA Required FS Required

>= 7 years €500K Above Threshold only Above Threshold only

4-6 years €750K Above Threshold only Above Threshold only

<= 3 years €1m Above Threshold only Above Threshold only

Note: For all of the above cases, the current threshold is €250k and a Large

Network Connection Agreement is required.

GNI proposals on Connection Policy Dec 14 5

The proposal is that a Large Network Customer Agreement is only required

when the FS threshold is met, an NPV amount under the appropriate threshold

is covered by using the standard I&C Agreement. The benefit of this

amendment is that the FS requirement is more closely based on the risk profile

of the new connection regarding the speed of payback for investment in the gas

network i.e. recognising the relative risk of different projects with different

payback periods. If Project A has a quicker payback period than Project B then

all else being equal, the relative financial risk of Project A is lower and this

should be reflected by the requirement for Financial Security.

In this way, connections that cover their costs and contribute downward

pressure to tariffs in a relatively short period are facilitated and incentivised to

connect to the gas network through the removal of the requirement for

financial security.

Proposal 1.3 Financial Security Credit Ratings

Under the current financial security policy, if the connecting entity is rated BBB

or higher by S & P and/or BBB or higher by Fitch and/or Baa2 or higher by

Moody’s the customer will be exempt from providing financial security.

Connections by such entities are not considered the norm however. Financial

security is required in the majority of cases.

The most popular (and practical) form of financial security for new connections

is a letter of credit. Under the current financial security policy, the letter of

credit must be issued by either:

(a) a Bank with long term unguaranteed unsubordinated debt rated at least

AA by S&P and/or AA2 by Moody’s and/or AA by Fitch. OR

(b) a subsidiary of a Bank which has total balance sheet assets of not less

than €1,000 million (or equivalent in other currencies) and the long term

unguaranteed unsubordinated debt that is rated at least A by S&P or A2

by Moody’s or A by Fitch.

Whilst many banking institutions would have met this criteria when the policy

was initially written, the benchmark needs to be reviewed to allow connecting

customers procure a letter of credit from robust financial institutions that they

regularly transact with.

To achieve this, GNI’s view is that the financial security approach applied to

shippers’ financial security (which is typically of a much larger scale than new

connections) should be differentiated from that applied to new connections.

GNI proposals on Connection Policy Dec 14 6

GNI proposed changes

Taking account of the current financial circumstance along with customer

feedback during discussions with potential new customers as part of the

connection process has highlighted difficulties for new customers (e.g. I&C

sector) in putting the required provisions of the current financial security policy

in place such that they are unable to use the banks they regularly transact with.

GNI therefore propose the addition of the following text within clause 3.2.1 of

the Financial Security Policy:

In respect specifically of new connections, and with the prior written approval of the Transporter and where the Financial Security Amount is less than or equal to €1,000,000, an irrevocable standby letter of credit in or substantially in the form attached at Appendix 1, or in such other form as may be acceptable to the Transporter (a “Letter of Credit”) issued for the account of the Counterparty in favour of the Transporter which Letter of Credit shall allow for partial drawings, if necessary, and shall provide for payment to the Transporter forthwith on demand and shall be issued by a Bank with long-term unguaranteed unsubordinated debt rated at least BBB by S&P and/or Baa2 by Moody’s and/or BBB by Fitch and which has total balance sheet assets of not less than €1,000 million (or equivalent in other currencies)

GNI proposals on Connection Policy Dec 14 7

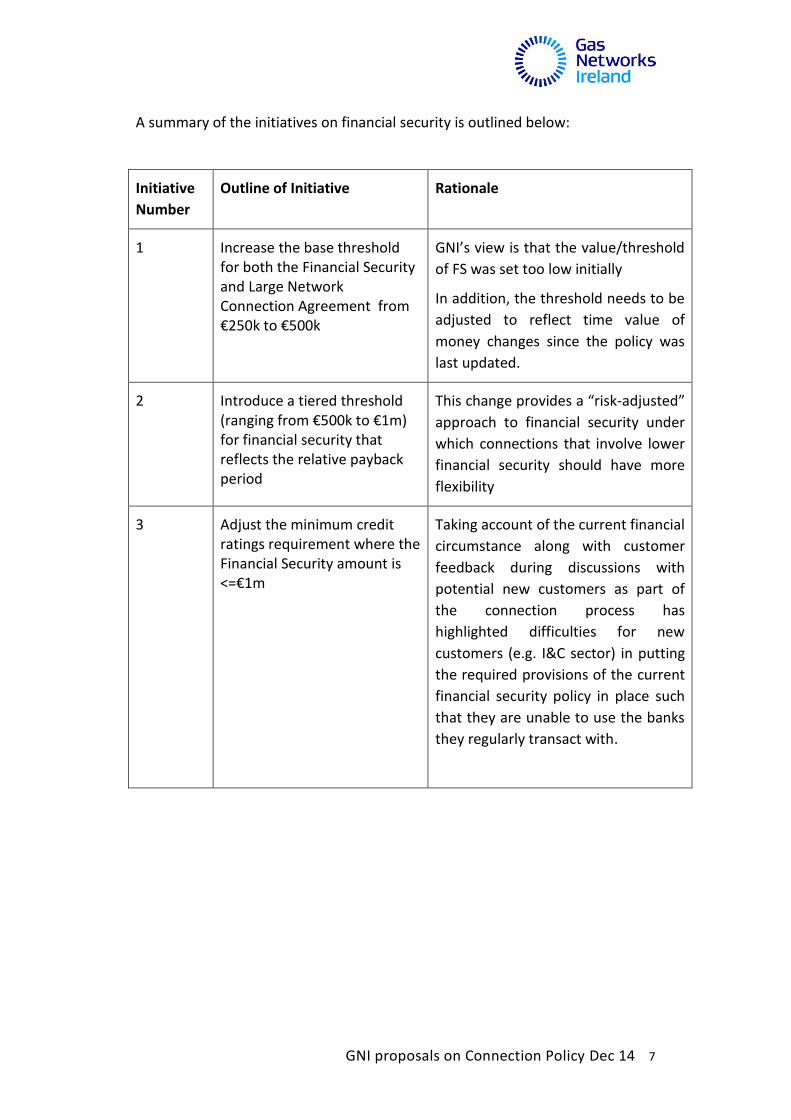

A summary of the initiatives on financial security is outlined below:

Initiative

Number

Outline of Initiative Rationale

1 Increase the base threshold for both the Financial Security and Large Network Connection Agreement from €250k to €500k

GNI’s view is that the value/threshold

of FS was set too low initially

In addition, the threshold needs to be

adjusted to reflect time value of

money changes since the policy was

last updated.

2 Introduce a tiered threshold (ranging from €500k to €1m) for financial security that reflects the relative payback period

This change provides a “risk-adjusted”

approach to financial security under

which connections that involve lower

financial security should have more

flexibility

3 Adjust the minimum credit ratings requirement where the Financial Security amount is <=€1m

Taking account of the current financial

circumstance along with customer

feedback during discussions with

potential new customers as part of

the connection process has

highlighted difficulties for new

customers (e.g. I&C sector) in putting

the required provisions of the current

financial security policy in place such

that they are unable to use the banks

they regularly transact with.

GNI proposals on Connection Policy Dec 14 8

Proposal 2: Inclusion of Transmission Revenue in all

appraisals

Each new connection provides incremental revenue for both the transmission

and distribution networks. However, under the current policy, only the

following sectors recognise transmission revenue in the appraisal exercise:

1. New Towns

2. Loads with consumption greater than 57.5 GWh/annum

3. Connections that involve investment in transmission assets

2.1 Transmission Exit Capacity Revenue:

At the time of the last policy change, there was extensive flexibility for shippers

to optimise their transmission exit capacity bookings through internal transfers

in their portfolio and trading with other shippers. Therefore it was very difficult

to determine the incremental benefit of a new connection on transmission exit

revenue.

A recent key change in the market has seen the removal of trading transmission

exit capacity on a secondary basis. In the new market structure, shippers need

to book peak capacity pertaining to each gas point and cannot rely on a

“portfolio” effect to transfer transmission exit between points (or trade with

shippers). It is therefore appropriate to recognise the incremental transmission

exit revenue benefit from each connection, and amend the Connection Policy

accordingly to reflect this.

With this in mind, it is proposed that transmission exit revenue be extended to

the appraisal of all categories of connection (i.e. Transmission exit revenue

should be included in the appraisal for all sectors). This would be based on a

commitment by the customer on de minimis transmission exit bookings for the

required period which ensures that the Transmission Exit Capacity revenue

does indeed materialise. Even though the fact that no Large Network

Connection Agreement would be applied, a contract is still put in place and the

customer would have an obligation to book the de minimis level of capacity as

per the Connections Policy. Under the current Connections Policy, only 80% of

Distribution revenues are generally included in the appraisal, therefore the de

minimis level of capacity only applies to Distribution Supply Point Capacity.

However, if Transmission revenues were included in the appraisals, it is

proposed that Transmission Exit Capacity would also be included in the de

minimis level of capacity required and the customer would be obliged to book

both the de minimis level of Distribution Supply Point Capacity and

Transmission Exit Capacity until the cost of the connection was paid off.

GNI proposals on Connection Policy Dec 14 9

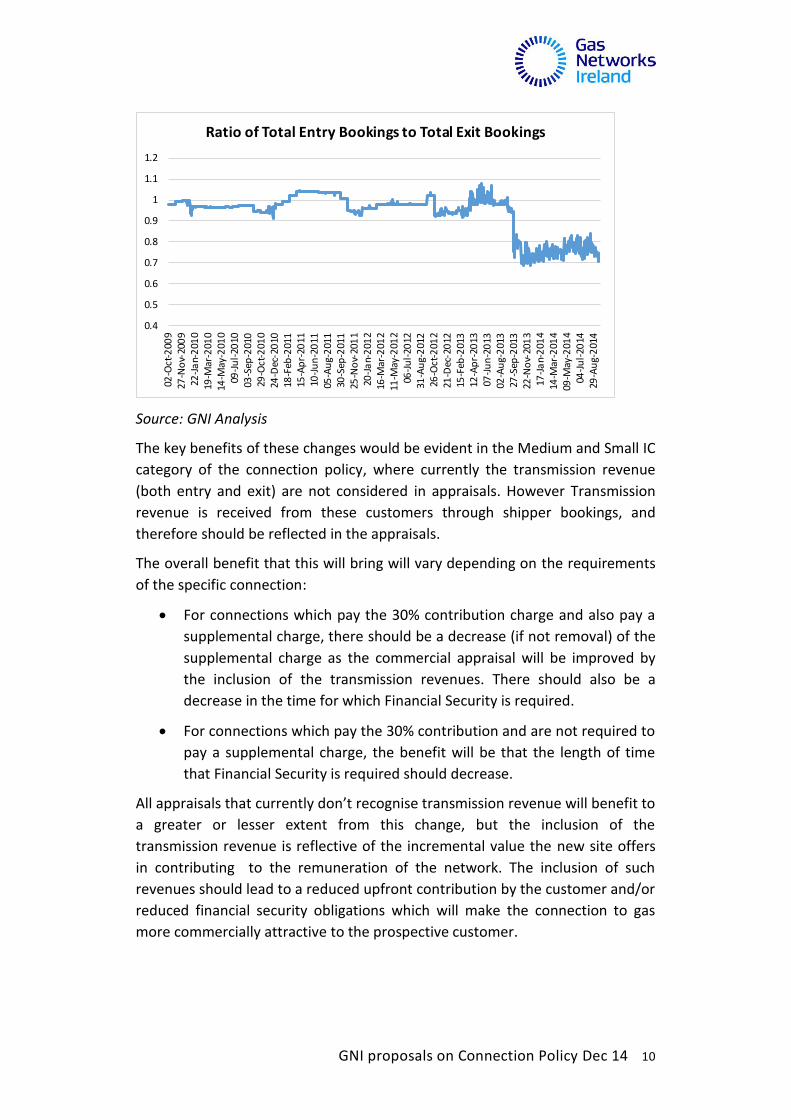

2.2 Transmission Entry Capacity Revenue:

In terms of transmission entry, shippers book this on a portfolio basis and are

able to trade transmission entry with other shippers. It is assumed each

connection will always offer incremental entry bookings to the network as the

shipper must increase entry bookings to accommodate the new load.

To establish what level of entry revenue is appropriate to include in the

appraisal, GNI have undertaken a study to review the relative ratio of total

transmission entry capacity bookings versus total exit bookings in recent years

to assess the incremental value of new connections in terms of increased total

transmission entry bookings. The findings are outlined in the chart below.

Before the removal of secondary transmission exit capacity, there was generally

a 1:1 ratio between entry and exit bookings, as shippers optimised their

aggregate entry and exit portfolios.

The impact of the removal of secondary exit capacity trading outlined above is

clearly evident, where the ratio falls from c. 1:1 to 0.8:1 in Gas Year 13/14. The

fall in the ratio is due to the following:

Exit: Since the removal of secondary exit capacity trading, shippers need to

book specific firm bookings prevailing to each exit gas point and can no longer

spread its exit capacity portfolio across its sites. Therefore the outcome is more

firm bookings on the exit side versus the previous regime which allowed a

“portfolio” approach.

Entry: In contrast, the market conditions for transmission entry remain

unchanged and therefore the ratio of entry bookings (which were not affected

by the market change) to exit bookings (which increased due to the market

change) has therefore decreased.

On this basis, GNI propose that a factor of 80% (0.8) be applied to peak day

bookings of each new connection entry revenue calculation. For example, if

peak = 100 KWh, then 80% * 100 KWh = 80KWh is the volume included for

incremental transmission entry revenue.

GNI proposals on Connection Policy Dec 14 10

0.4

0.5

0.6

0.7

0.8

0.9

1

1.1

1.202

-Oct

-200

927

-No

v-20

09

22-J

an-

201

019

-Mar

-201

014

-May

-201

009

-Ju

l-20

1003

-Sep

-201

029

-Oct

-201

024

-Dec

-20

1018

-Feb

-201

115

-Ap

r-20

1110

-Ju

n-2

011

05-A

ug-

201

130

-Sep

-201

125

-No

v-20

11

20-J

an-

201

216

-Mar

-201

211

-May

-201

206

-Ju

l-20

1231

-Au

g-2

012

26-O

ct-2

012

21-D

ec-2

012

15-F

eb-2

013

12-A

pr-

2013

07-J

un

-20

1302

-Au

g-2

013

27-S

ep-2

013

22-N

ov-

201

317

-Ja

n-2

014

14-M

ar-2

014

09-M

ay-2

014

04-J

ul-

2014

29-A

ug-

201

4

Ratio of Total Entry Bookings to Total Exit Bookings

Source: GNI Analysis

The key benefits of these changes would be evident in the Medium and Small IC

category of the connection policy, where currently the transmission revenue

(both entry and exit) are not considered in appraisals. However Transmission

revenue is received from these customers through shipper bookings, and

therefore should be reflected in the appraisals.

The overall benefit that this will bring will vary depending on the requirements

of the specific connection:

For connections which pay the 30% contribution charge and also pay a

supplemental charge, there should be a decrease (if not removal) of the

supplemental charge as the commercial appraisal will be improved by

the inclusion of the transmission revenues. There should also be a

decrease in the time for which Financial Security is required.

For connections which pay the 30% contribution and are not required to

pay a supplemental charge, the benefit will be that the length of time

that Financial Security is required should decrease.

All appraisals that currently don’t recognise transmission revenue will benefit to

a greater or lesser extent from this change, but the inclusion of the

transmission revenue is reflective of the incremental value the new site offers

in contributing to the remuneration of the network. The inclusion of such

revenues should lead to a reduced upfront contribution by the customer and/or

reduced financial security obligations which will make the connection to gas

more commercially attractive to the prospective customer.

GNI proposals on Connection Policy Dec 14 11

For the avoidance of doubt, this proposed amendment is only applicable to

connections where transmission revenue is not recognised – where it is already

accounted for in appraisals (e.g. new towns) the appraisal continues as is.

Initiative

Number

Outline of Initiative Rationale

1 Include TX Exit Revenue (100%) to

all appraisals which currently don’t

recognise transmission revenue

Recent market changes which

removed secondary exit support

the inclusion of TX exit to all

sectors.

2 Include TX Entry Revenue (80%) to

all appraisals which currently do not

recognise transmission revenue.

Each new connection provides

some level of incremental entry

capacity to the network. Based on

historic data, a factor of 80% (0.8)

is proposed.

GNI proposals on Connection Policy Dec 14 12

Proposal 3: Amendment of Institutional I & C Customers

The connections policy outlines that an Institutional I&C Customer is one which

“as a result of their load characteristics are likely to remain connected to the

network for a longer period of time than a typical commercial enterprise.”

The current connections policy allows for a 20 year appraisal for such

connection types which are “institutional” in nature and a list of Institutional

I&C Customers is provided in Annex 3 of the current connections policy.

GNI propose to include five more connection types to this list:

Ports

Bus Stations

Waste Collection Depots

Biogas Injection Facility

Retail CNG Forecourts

The first two additions are institutional types which are built for long term use

(ports/bus stations). The remaining three additions are typically significant long

term investments to provide services on a long term basis to customers:

Waste collection depots are built to provide municipal services to customers

for a 20-30 year lifetime at a specific location

Biogas plants will inject gas into the grid at the specified location for a

prolonged period of time with potential expansion. Including biogas injection

facilities to the institutional I & C list would encourage more installations. This

in turn would support the requirement for EU Member States to undertake

measures to assist the wider use of gas from renewable sources. Note biogas

plants will typically be injecting/entering gas in the system whereas

conventional connections in the connections policy are exit points that offtake

gas from the grid. However, the exercise at the start of connecting the facility to

the gas grid by way of extending the gas network can follow the same

principles.

Retail CNG forecourts would be developed at strategic locations to provide

long-term refuelling services to CNG vehicles.

GNI proposals on Connection Policy Dec 14 13

To summarise, GNI would propose that the list would include new additions as

follows:

Current List Additional New Sites

Schools

Third Level Colleges

Hospitals

Prisons

Garda Stations

Stadiums

Airports (airport specific

infrastructure only)

Railway stations

Museums/Heritage Sites

Fire/Ambulance Station

Army Barracks

Government Buildings

Ports

Bus Stations

Waste Collection Depots

Biogas Injection Facility

Retail CNG Forecourts

Initiative

Number

Outline of Initiative Rationale

1 Amend institutional list to reflect

additions above

Extend list to other

forms of institutional

sites which merit a 20

year appraisal due to

longevity of tenure

GNI proposals on Connection Policy Dec 14 14

Proposal 4: Proposals on Existing Gas Areas

The purpose of this proposal is to develop a policy to allow for infill projects in

areas close to or including the existing gas network. The Connection Policy as it

stands does not specifically address opportunities for “infill” in urban or

suburban areas i.e. industrial zones/streets/regions that could be connected

with a minimal incremental increase to the existing infrastructure. There is

therefore the risk of missing opportunities for new connections and load

growth, as the existing gas infrastructure is not utilised to its fullest extent on

an economic basis. The existing Connections Policy does not facilitate the

efficient extension of the network into an area within an already connected

city/town. In practice, there are some areas within cities that could potentially

be the equivalent of a small town, however, there are limited methods of

connecting the areas outside of connecting a single customer (using a 7 or 20

year appraisal or appraise as a non-gas estate). This has resulted in potential

missed opportunities to grow the network in existing gas areas.

On this basis, GNI have two key proposals:

4.1 Introduction of a “Suburb” Policy

GNI would advocate the introduction of an infill suburb policy under the

following criteria:

(i) Use the mechanics of the new towns model(see description below)

to appraise these projects

(ii) Where the overall investment <= €1m

(iii) Where the upstream investment in the network is <=€100k

(iv) The largest user is <= 50% of the total projected volumes

New Towns Model: As per section 8 of the Connections Policy, New Towns are

evaluated over 25 years for both Industrial Commercial Customers and New

Housing to reflect the lower risk and broader growth opportunities of a

diversified area load base. The economic test includes both Transmission and

Distribution revenue and considers the long term potential of the entire area. It

is proposed that funding for such infill suburb projects would be applied to the

most economic projects with each project scored and appraised by GNI against

an annual funding allowance from the CER.

GNI proposals on Connection Policy Dec 14 15

4.2 Removal of Domestic Connection Fee in certain circumstances

At present new domestic connections pay a fee of €250. GNI believe there is

merit in waiving the domestic connection fee in certain circumstances to

increase/accelerate the rate of new domestic connections in new towns or

targeted suburbs/regions. To compete in the energy source market GNI need to

entice new customers to join the gas network. A removal of the domestic

connection fee in these circumstances will assist in the take up during various

campaigns.

Natural Gas is clean, convenient and cheap. Natural gas is always available, no

ordering or storage is required; it is compatible with contemporary appliances

and is the most environmentally friendly of all fossil fuels. The removal of the

connection fee in certain circumstances will encourage growth in the domestic

sector.

Initiative

Number

Outline of Initiative Rationale

1 Apply new infill “Suburb”

policy as outlined above.

The new towns model could

easily be adapted to

streets/zones/regions

(“suburbs”) and would provide

consistency of application in

growing out the network.

Previous I&C infill appraisals

didn’t include take up of

domestic connections arising as

a result of the infill project

2 Domestic Housing

contribution for targeted

suburb/urban areas and

new towns – allow the

domestic housing

connection fee to be

waived under certain

circumstances

Will increase/accelerate the rate

of connection in new towns and

ensures that no opportunities

are missed

GNI proposals on Connection Policy Dec 14 16

Proposal 5: Group Sites (different entities, same corridor)

This proposal will only come into effect when the total investment of the

project is greater than €1m. If the project is less than €1m, Proposal 4 (Infill

Suburb Proposals on Existing Gas Areas) will apply.

The current connections policy is silent on circumstances where GNI are

approached by a number of companies or entities simultaneously on a

corridor/route who collectively want to connect to the network. The current

policy appraises each connection query on a case-by-case basis and GNI would

like to formalise the approach for multi-clients on the same corridor. The

principle would remain that GNI are remunerated for the aggregate cost of the

connection, but a pro-forma share of costs would be proposed to the clients but

on a case by case basis, an alternative cost sharing mechanism could be

developed/agreed.

To reflect this into the policy, GNI propose that the following wording would be

added to the opening section of the Connections Policy which outlines the

objectives/principles of the policy:

“Joint cost sharing mechanisms for simultaneous multiple connections from one

aggregate project should be encouraged (e.g. a joint proposal from multiple

potential customers on the same corridor). The key component is that the

aggregate cost of the connection is fully paid through an appropriate cost

sharing mechanism funded by the various clients. This cost sharing mechanism

can be reviewed on a case by case basis”

Initiative

Number

Outline of Initiative Rationale

1 Apply multi-client model on

a case-by-case basis whilst

retaining the principles of

the Connections Policy.

The sharing mechanism

should be flexible (including

input from the clients

involved), with the key issue

being that the aggregate

cost of connection is

remunerated.

This provides clarity to

situations where multi-clients

simultaneously want to

connect to the grid.

GNI proposals on Connection Policy Dec 14 17

Proposal 6: Group Sites (same entity, different sites)

The current connections policy is silent on circumstances where GNI are

approached by a company/entity to connect a number of their locations e.g.

chain of retail outlets. The current policy appraises each connection query on a

case-by-case basis and GNI would like to formalise the approach for multi-sites

for the same client, recognising the “portfolio” benefit of getting all the sites

rather than potentially none.

If we consider the different sites as one entity rather than a number of different

sites and look at the NPV as a whole, GNI feel that this would encourage more

connections. If an entity is looking to set up or standardise multiple locations in

Ireland, being able to apply for new connections for all of their sites with one

enquiry could act as an incentive and it also offers economies of scale in

progressing the multiple connections under one aggregate project.

The risk in not considering this approach is that potential multi-national

companies and existing indigenous companies may not decide to expand / set

up in Ireland as they may take an ‘all or nothing’ approach with their sites.

Therefore GNI feels that multiple sites from the same company/entity should

be group-appraised, with net contribution calculated in aggregate as this will

encourage new connections overall.

Initiative

Number

Outline of Initiative Rationale

1 Multiple sites from the

same company/entity

would be group-appraised,

with net contribution

calculated in aggregate.

Recognises portfolio benefit of

multiple sites simultaneously

under one connection/one

contribution.

This initiative would assist in the rollout of CNG infrastructure particularly in the

event that an existing forecourt operator was interested in building a network

of filling stations to adopt the fuel.

GNI proposals on Connection Policy Dec 14 18

Proposal 7: Treatment of CNG Connections

The current connections policy is silent on the treatment of CNG connections as

this in itself is a new technology. GNI proposes to have a clear outline in the

policy regarding CNG connections. This will not preclude end users from

installing their own equipment once all safety requirements have been

satisfied, but where GNI build the compression and multi-storage equipment,

the investment must be remunerated under the principles of the connections

policy.

One of the critical elements of the market for natural gas in transport is the

availability of vehicles. Without a strategic network of refuelling infrastructure

the manufacturers will not commit vehicles to the market. Without GNI’s

involvement, refuelling ‘islands’ may appear without any unified national

network overview. GNI are of the opinion that the provision of CNG refuelling

stations at this early stage of the market will require the support and

involvement of the natural gas system operator.

The benefits of this approach are:

High quality refuelling infrastructure in the market;

Long-term view taken;

Market introduction supported;

Application of gas technical experience;

National infrastructure support;

Lower financial burden on end user;

Consistent technical application across the market; and

Higher probability of market adoption.

In line with the current Connections Policy, customers will make a contribution

of 30% towards the cost of the connection. An economic test will be

undertaken (in line with existing policy), which will dictate that if the customer’s

capacity charges over a seven year period do not meet the cost of the

remaining 70% of the cost of connection, the customer must pay the difference

GNI proposals on Connection Policy Dec 14 19

Initiative

Number

Outline of

Initiative

Rationale

1 Include

compression

and multi-stage

storage in the

connection.

Reduce costs for the gas user through

increased use of gas network assets and

long term reductions in tariffs

30% contribution from the customer and

economic test to protect the gas user from

inefficient investments

Maintains consistency of service and

quality

GNI responsible for maintenance and care

of the compression and storage

The inclusion of CNG in the connection will

allow GNI to provide necessary support to

the market development of CNG in Ireland.

Vehicle manufacturers and after sales

converters will not serve the Irish market

until sufficient refuelling infrastructure is in

place. To date private industry has failed to

provide the necessary refuelling

infrastructure and so the CNG in transport

market for Ireland has failed to develop.

GNI proposals on Connection Policy Dec 14 20

Summary & Conclusions

To summarise, GNI propose to amend the Connections Policy in the following

ways:

(i) Amend the FS provisions to include tiered thresholds

(ii) Recognise transmission revenue in all appraisals

(iii) Extend the list of I&C institutional customers

(iv) Formalise the development of infill suburb/urban projects

(v) Clarify treatment of group sites (different entities, same corridor)

(vi) Clarify treatment of group sites (same entity, different sites)

(vii) Clarify the treatment of CNG connections

Many of the changes are to provide clarity on the treatment of certain

connection types and to apply consistency (e.g. recognising transmission

revenue in all appraisals).

GNI believe the incorporation of these proposals are aligned with the overall

principles of the policy and will assist in economically and efficiently extending

the level of connections to the network, helping to spread the cost of the

network across a larger number of users.