Engineering Systems Analysis for Design Massachusetts Institute of Technology Richard de Neufville ...

31

Engineering Systems Analysis for Design Massachusetts Institute of Technology Richard de Neufville Real Options SDM Slide 1 of 31 Richard de Neufville Professor of Engineering Systems and of Civil and Environmental Engineering MIT Real Options

-

Upload

peregrine-carpenter -

Category

Documents

-

view

215 -

download

0

Transcript of Engineering Systems Analysis for Design Massachusetts Institute of Technology Richard de Neufville ...

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 1 of 31

Richard de NeufvilleProfessor of Engineering Systems and of

Civil and Environmental EngineeringMIT

Real Options

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 2 of 31

Outline

Motivational Example: Garage Case

General Perspective

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 3 of 31

Garage Case Topics

Value at Risk

Analyzing flexibility using spreadsheet

Parking garage case

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 4 of 31

Value at Risk Concept

Value at Risk (VAR) recognizes fundamental reality: actual value of any design can only be known probabilistically

Because of inevitable uncertainty in – Future demands on system– Future performance of technology– Many other market, political factors

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 5 of 31

Value at Risk Definition

Value at Risk (VAR) definition:– A loss that will not be exceeded at some specified

confidence level– “We are p percent certain that we will not lose more

than V dollars for this project.”

VAR easy to see on cumulative probability distribution (see next figure)

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 6 of 31

Look at distribution of NPV of designs A, B:– 90% VAR for NPVA is -$91– 90% VAR for NPVB is $102

CDF

0%

20%

40%

60%

80%

100%

-400 -200 0 200 400 600

NPV

Cu

mu

lati

ve

Pro

ba

bil

ity

NPVA NPVB 90% VAR for NPVA

90%VAR for NPVB 10% Probability

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 7 of 31

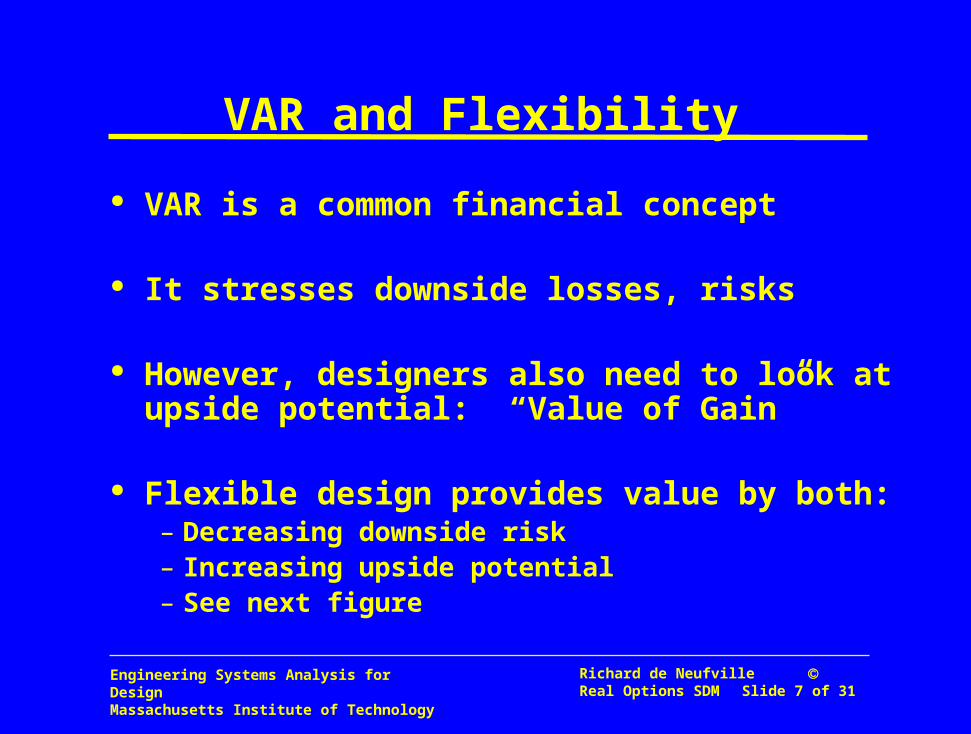

VAR and Flexibility

VAR is a common financial concept

It stresses downside losses, risks

However, designers also need to look at upside potential: “Value of Gain”

Flexible design provides value by both:– Decreasing downside risk– Increasing upside potential– See next figure

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 8 of 31

Sources of value for flexibility

Cumulative Probability

Value

Original distribution

Distribution with flexibility

Cut downside risks

Expand upside potential

Cut downside ; Expand Upside

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 9 of 31

Excel Analysis Sequence toillustrate value of flexibility

1: Examine situation without flexibility – This is Base case design

2: Introduce variability (simulation)a different design (in general)

3: Introduce flexibility=> a even different and better design

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 10 of 31

Parking Garage Case

Garage in area where population expands Actual demand is necessarily uncertain

Design Opportunity: Strengthened structure – enables future addition of floor(s) (flexibility)– costs more (flexibility costs)

Design issue: is extra cost worthwhile?

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 11 of 31

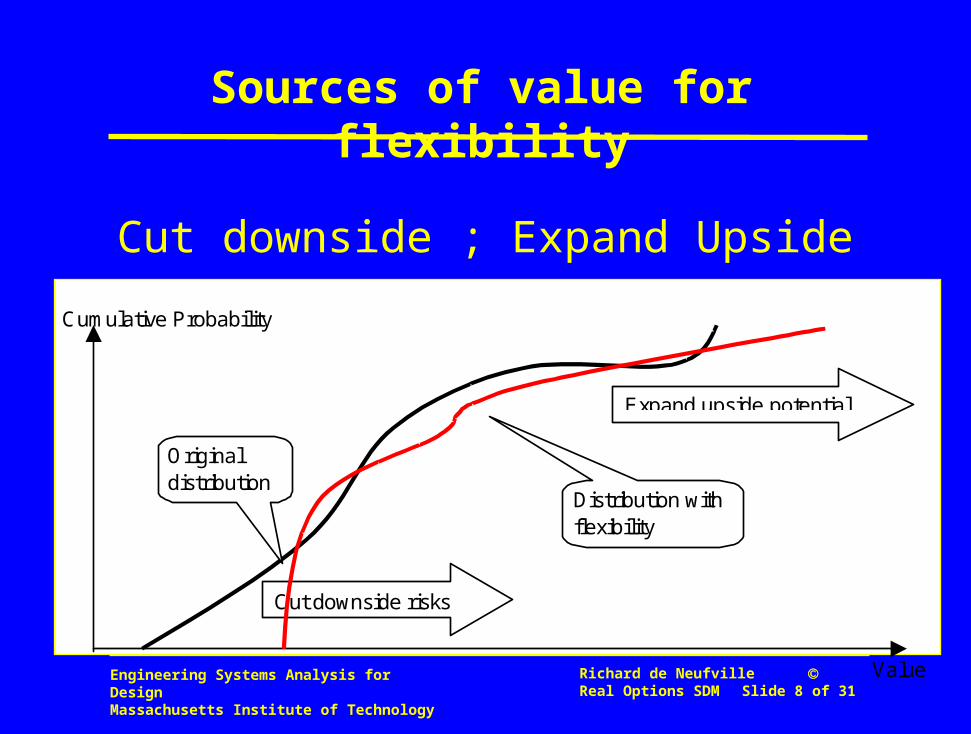

Parking Garage Case details

Demand– At start is for 750 spaces– Over next 10 years is expected to rise exponentially

by another 750 spaces– After year 10 may be 250 more spaces– could be 50% off the projections, either way;– Annual volatility for growth is 10%

Average annual revenue/space used = $10,000

The discount rate is taken to be 12%

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 12 of 31

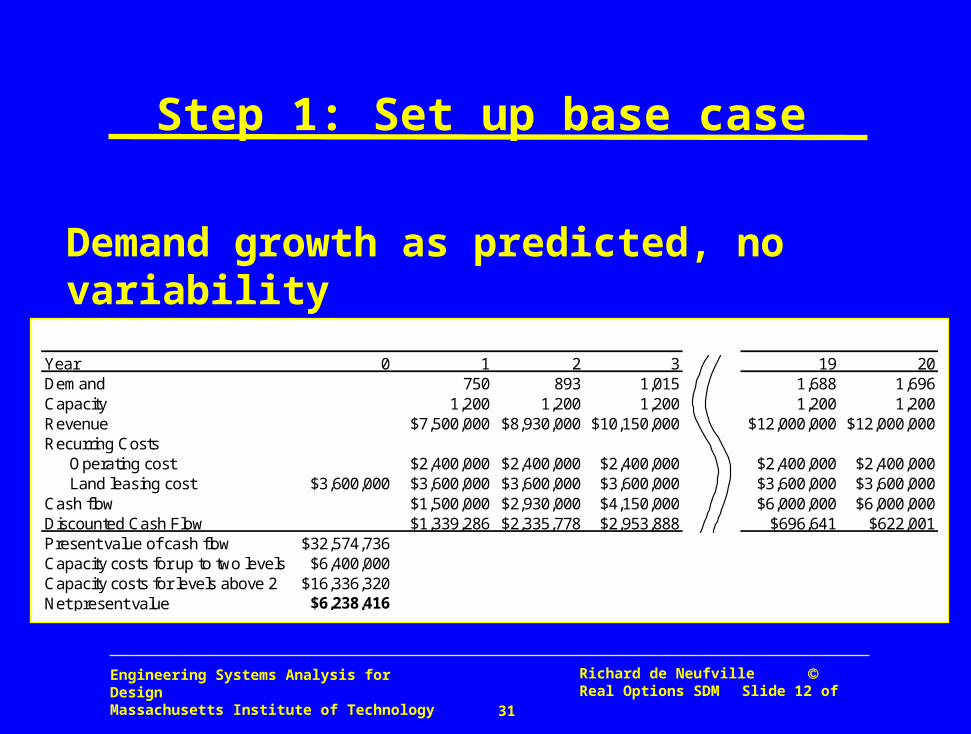

Step 1: Set up base case

0 1 2 3 19 20Demand 750 893 1,015 1,688 1,696Capacity 1,200 1,200 1,200 1,200 1,200Revenue $7,500,000 $8,930,000 $10,150,000 $12,000,000 $12,000,000Recurring Costs

Operating cost $2,400,000 $2,400,000 $2,400,000 $2,400,000 $2,400,000Land leasing cost $3,600,000 $3,600,000 $3,600,000 $3,600,000 $3,600,000 $3,600,000

Cash flow $1,500,000 $2,930,000 $4,150,000 $6,000,000 $6,000,000Discounted Cash Flow $1,339,286 $2,335,778 $2,953,888 $696,641 $622,001Present value of cash flow $32,574,736Capacity costs for up to two levels $6,400,000Capacity costs for levels above 2 $16,336,320Net present value $6,238,416

Year

Demand growth as predicted, no variability

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 13 of 31

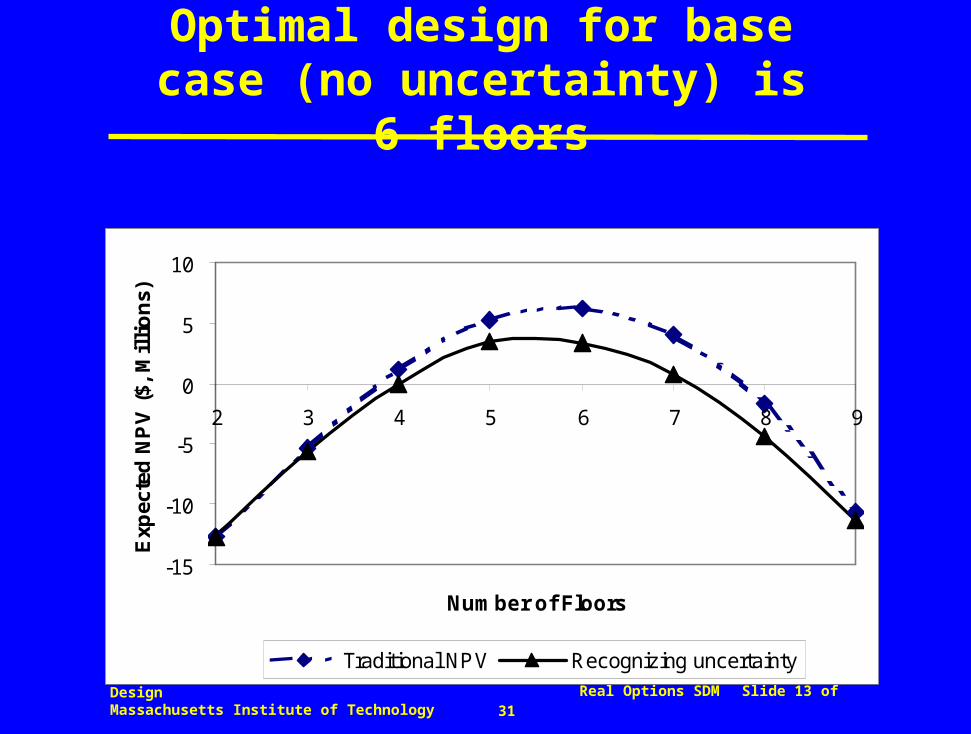

Optimal design for base case (no uncertainty) is 6 floors

-15

-10

-5

0

5

10

2 3 4 5 6 7 8 9

Number of Floors

Exp

ecte

d N

PV

($,

Mil

lio

ns)

Traditional NPV Recognizing uncertainty

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 14 of 31

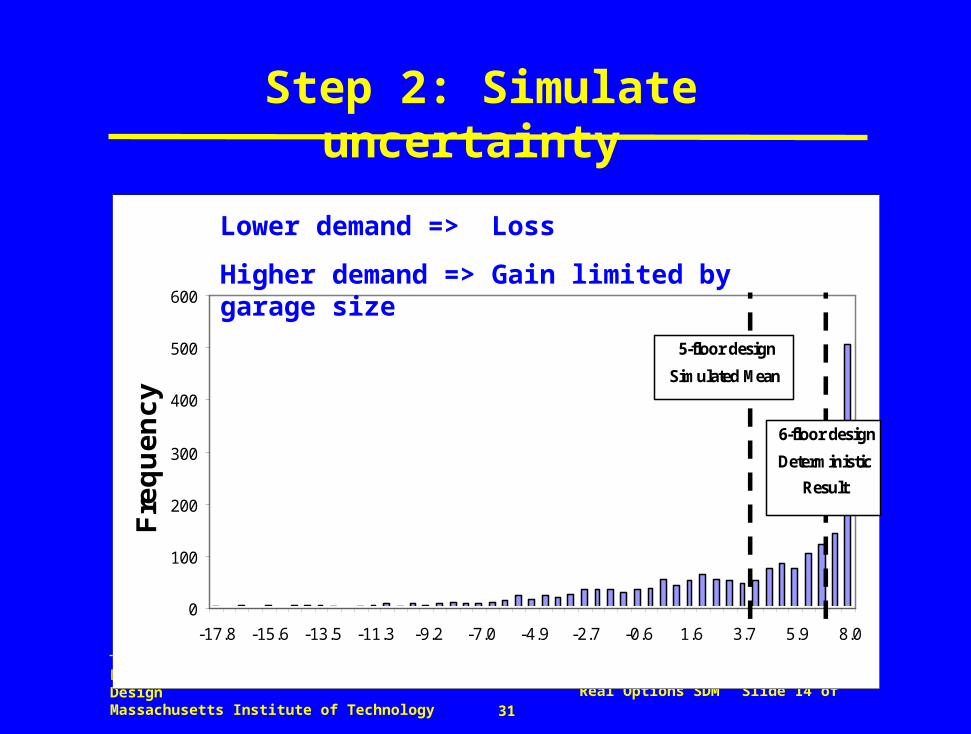

Step 2: Simulate uncertainty

0

100

200

300

400

500

600

-17.8 -15.6 -13.5 -11.3 -9.2 -7.0 -4.9 -2.7 -0.6 1.6 3.7 5.9 8.0

Fre

qu

en

cy

5-floor design

Simulated Mean

6-floor design

Deterministic

Result

Lower demand => Loss

Higher demand => Gain limited by garage size

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 15 of 31

NPV Cumulative Distributions

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

-20 -15 -10 -5 0 5 10

Pro

bab

ilit

y

CDF for Result of

Simulation Analysis (5-

floor) Implied CDF for

Result of

Deterministic NPV

Analysis (6-floor)

Compare Actual (5 Fl) with unrealistic fixed 6 Fl design

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 16 of 31

Recognizing uncertainty => different design (5 floors)

-15

-10

-5

0

5

10

2 3 4 5 6 7 8 9

Number of Floors

Exp

ecte

d N

PV

($,

Mil

lio

ns)

Traditional NPV Recognizing uncertainty

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 17 of 31

Step 3: Introduce flexibility into design (expand when needed)

0 1 2 3 19 20Demand 820 924 1,044 1,519 1,647Capacity 800 800 1,200 1,600 1,600

Decision on expansion expandExtra capacity 400

Revenue $8,000,000 $8,000,000 $10,440,000 $15,190,000 $16,000,000Recurring Costs

Operating cost $1,600,000 $1,600,000 $2,400,000 $3,200,000 $3,200,000Land leasing cost $3,600,000 $3,600,000 $3,600,000 $3,600,000 $3,600,000 $3,600,000Expansion cost $8,944,320

Cash flow $2,800,000 -$6,144,320 $4,440,000 $8,390,000 $9,200,000Discounted Cash Flow $2,500,000 -$4,898,214 $3,160,304 $974,136 $953,734Present value of cash flow $30,270,287Capacity cost for up to two levels $6,400,000Capacity costs for levels above 2 $7,392,000Price for the option $689,600Net present value $12,878,287

Year

Including Flexibility => Another, better design:

4 Floors with strengthened structure enabling expansion

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 18 of 31

Summary of design results from different perspectives

Why is the optimal design much better when we design with flexibility?

Perspective Simulation Option Embedded Design Estimated Expected NPVDeterministic No No 6 levels $6,238,416

Recognizing Uncertainty Yes No 5 levels $3,536,474

Incorporating Flexibilty Yes Yes4 levels with strengthened

structure$10,517,140

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 19 of 31

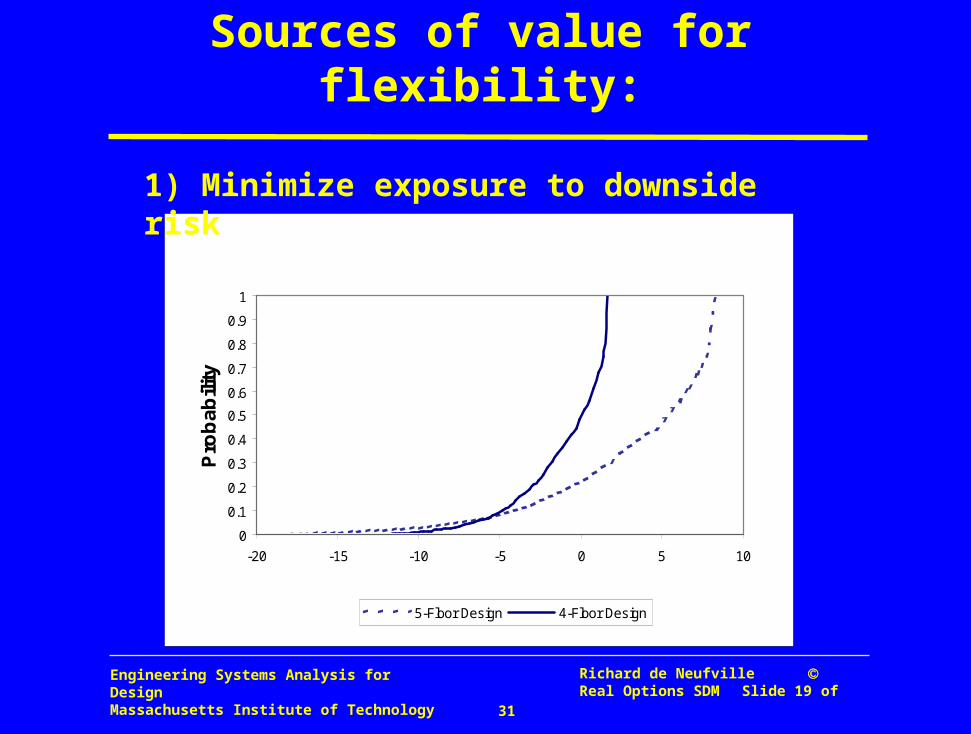

Sources of value for flexibility:

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

-20 -15 -10 -5 0 5 10

Pro

ba

bili

ty

5-Floor Design 4-Floor Design

1) Minimize exposure to downside risk

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 20 of 31

Sources of value for flexibility:

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

-20 -15 -10 -5 0 5 10 15 20 25 30 35

Pro

bab

ility

CDF for NPV

with Flexibility

CDF for NPV

without Flexibility

Mean for NPV

without Flexibility

Mean for NPV

with Flexibility

2) Maximize potential for upside gain

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 21 of 31

Comparison of designswith and without flexibility

Wow! Everything is better! How did it happen?

Root cause: change the framing of the problem

• recognize uncertainty ; add in flexibility thinking

Design Design with Flexibility Thinking Design without Flexibility thinking Comparison(4 levels, strengthened structure) (5 levels)

Initial Investment $18,081,600 $21,651,200 Better with optionsExpected NPV $10,517,140 $3,536,474 Better with optionsMinimum Value -$13,138,168 -$18,024,062 Better with optionsMaximum Value $29,790,838 $8,316,602 Better with options

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 22 of 31

Summary from Garage Case

Sources of value for flexibility– Cut downside risk– Expand upside potential

VAR chart is a neat way to represent the sources of value for flexibility

Spreadsheet with simulation is a powerful tool for estimating value of flexibility

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 23 of 31

“Options” Embody Idea of Flexibility

An “Option” provides a formal way of defining flexibility

An “Option” has a specific technical definition

Semantic Caution:– The technical meaning of an “option” is…

much more specific and limited than … ordinary meaning of “option” in conversation... where “option” = “alternative”

Pay careful attention to definition that follows!

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 24 of 31

Technical definition of an Option An Option is... A right, but not an obligation…

– “Exercise”, that is “use” only if advantageous– Asymmetric returns -- “all gain, no pain”– Usually acquired at some cost or effort

to take some action…– to grow or change system, buy or sell something, etc, etc,

now, or in the future... – May be indefinite – But can be for a limited time after which option expires

for a pre-determined price (the “strike” price). – Cost of action separate from cost of option

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 25 of 31

Financial Options

Focus first on financial options because – Consequences easiest to present– This is where options and valuation developed

Financial Options– Are tradable assets (see quotes finance.yahoo.com)– Sold through exchanges similar to stock markets– Are on all kinds of goods (known as “underlying

assets”)•Stocks, that is, shares in companies•Commodities (oil, meat, cotton, electricity...)•Foreign exchange, etc., etc.

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 26 of 31

Real Options

“Real” because they refer to project and systems– Contrast with financial options that are contracts

Real Options are focus of interest for Design– They provide flexibility for evolution of system

Projects often contain option-like flexibilities– Rights, not obligations (example: to expand garage)– Exercise only if advantageous

These flexibilities are “real” options

Let’s develop idea by looking at possibilities…

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 27 of 31

Real Options are Everywhere

Examples:

Lease equipment with option to buy at end of lease– Action is to buy at end of lease (or to walk away)– Lease period defined up-front (typically 2-3 years)– Purchase price defined in lease contract

Flexible manufacturing processes– Ability to select mode of operation (e.g. thermal power by

burning either gas or oil)– Switching between modes is action– Continuous opportunity (can switch at any time)– Switching often entails some cost (e.g.: set-up time)

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

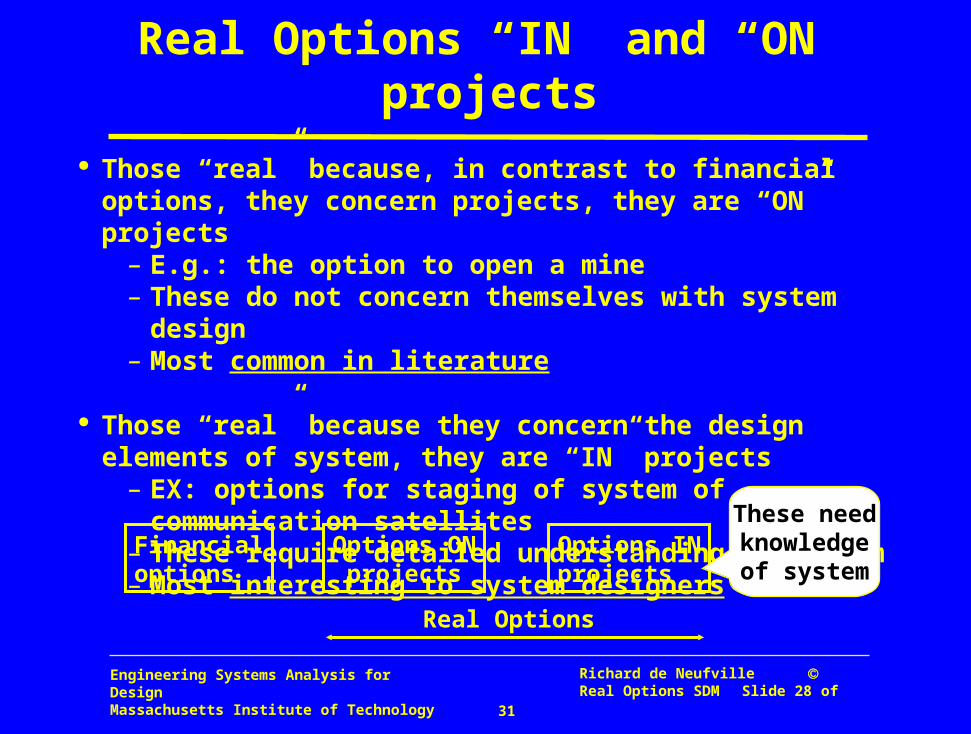

Richard de Neufville Real Options SDM Slide 28 of 31

Real Options “IN” and “ON” projects Those “real” because, in contrast to financial options, they

concern projects, they are “ON” projects– E.g.: the option to open a mine– These do not concern themselves with system design– Most common in literature

Those “real” because they concern the design elements of system, they are “IN” projects

– EX: options for staging of system of communication satellites– These require detailed understanding of system– Most interesting to system designers

Financialoptions

Options ON projects

Options INprojects

Real Options

These needknowledgeof system

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 29 of 31

Real Options “ON” projects These are financial options, but on technical things

They treat technology as a “black box”

Example: Antamina Copper– option to open the mine after a two-year exploration period– Uncertainty concerns: amount of ore and future price

=>uncertainty in revenue and thus in value of mine– Option is a Financial Call Option (on Mine as asset)

Differs from normal Financial Option because– Much longer period -- financial option usually < 2 years– Special effort needed to model future value of asset, it can’t

be projected simply from past data (as otherwise typical)

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 30 of 31

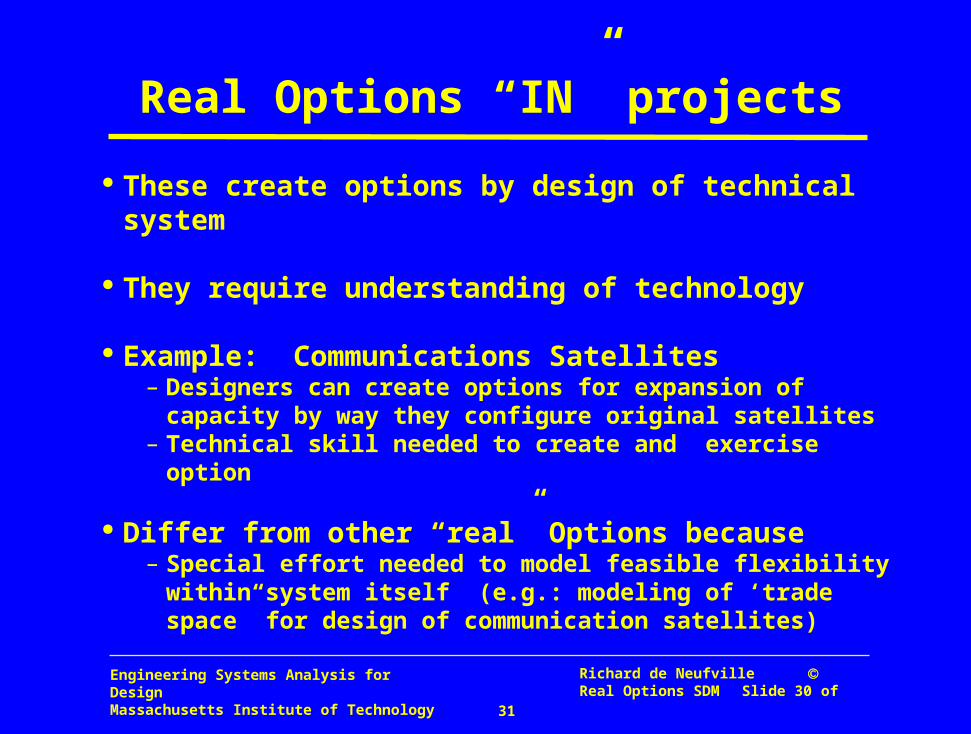

Real Options “IN” projects

These create options by design of technical system

They require understanding of technology

Example: Communications Satellites– Designers can create options for expansion of capacity

by way they configure original satellites– Technical skill needed to create and exercise option

Differ from other “real” Options because– Special effort needed to model feasible flexibility within

system itself (e.g.: modeling of ‘trade space” for design of communication satellites)

Engineering Systems Analysis for DesignMassachusetts Institute of Technology

Richard de Neufville Real Options SDM Slide 31 of 31

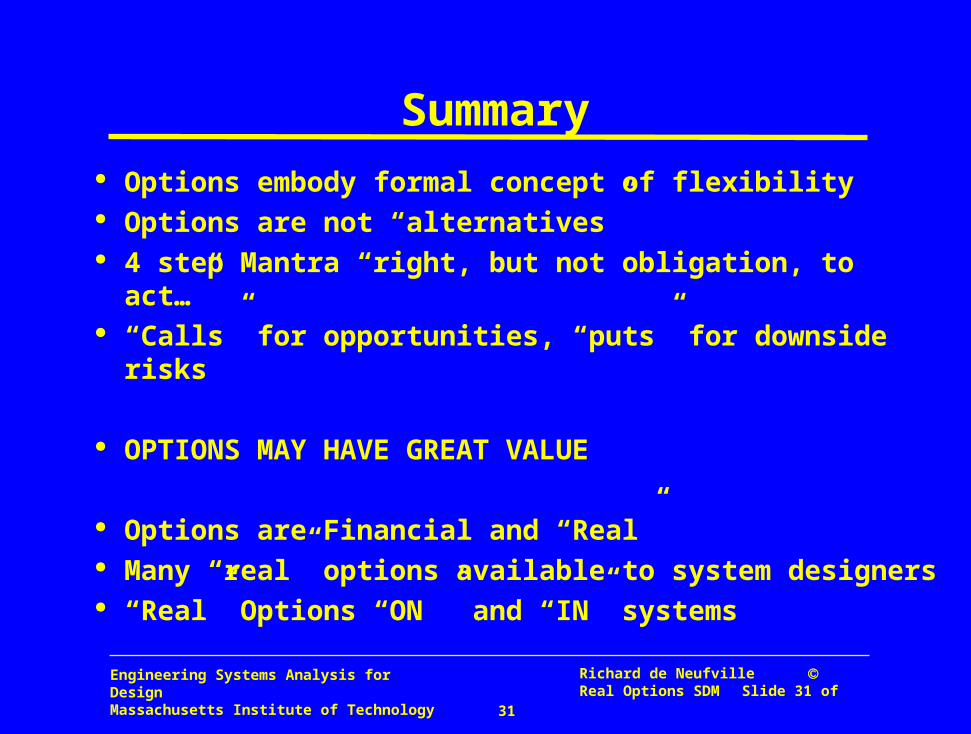

Summary Options embody formal concept of flexibility Options are not “alternatives” 4 step Mantra “right, but not obligation, to act…” “Calls” for opportunities, “puts” for downside risks

OPTIONS MAY HAVE GREAT VALUE

Options are Financial and “Real” Many “real” options available to system designers “Real” Options “ON ” and “IN” systems