COMMERCE BANCSHARES, INC. · COMMERCE BANCSHARES, INC. ... 176 branches and 376 ATMs in our...

22

COMMERCE BANCSHARES, INC. David Kemper Chairman and Chief Executive Officer ANNUAL SHAREHOLDERS MEETING April 18, 2018

Transcript of COMMERCE BANCSHARES, INC. · COMMERCE BANCSHARES, INC. ... 176 branches and 376 ATMs in our...

COMMERCE BANCSHARES, INC.

David KemperChairman and Chief Executive Officer

ANNUAL SHAREHOLDERS MEETINGApril 18, 2018

2

CAUTIONARY STATEMENT

2

A number of statements we will be making in our presentation and in theaccompanying slides are “forward-looking statements” within themeaning of the Private Securities Litigation Reform Act of 1995, such asstatements of the Corporation’s plans, goals, objectives, expectations,projections, estimates and intentions. These forward-looking statementsinvolve significant risks and uncertainties and are subject to changebased on various factors (some of which are beyond the Corporation’scontrol). Factors that could cause the Corporation’s actual results todiffer materially from such forward-looking statements made herein orby management of the Corporation are set forth in the Corporation’s 2017Report on Form 10-K and the Corporation’s Current Reports on Form 8-K.

3

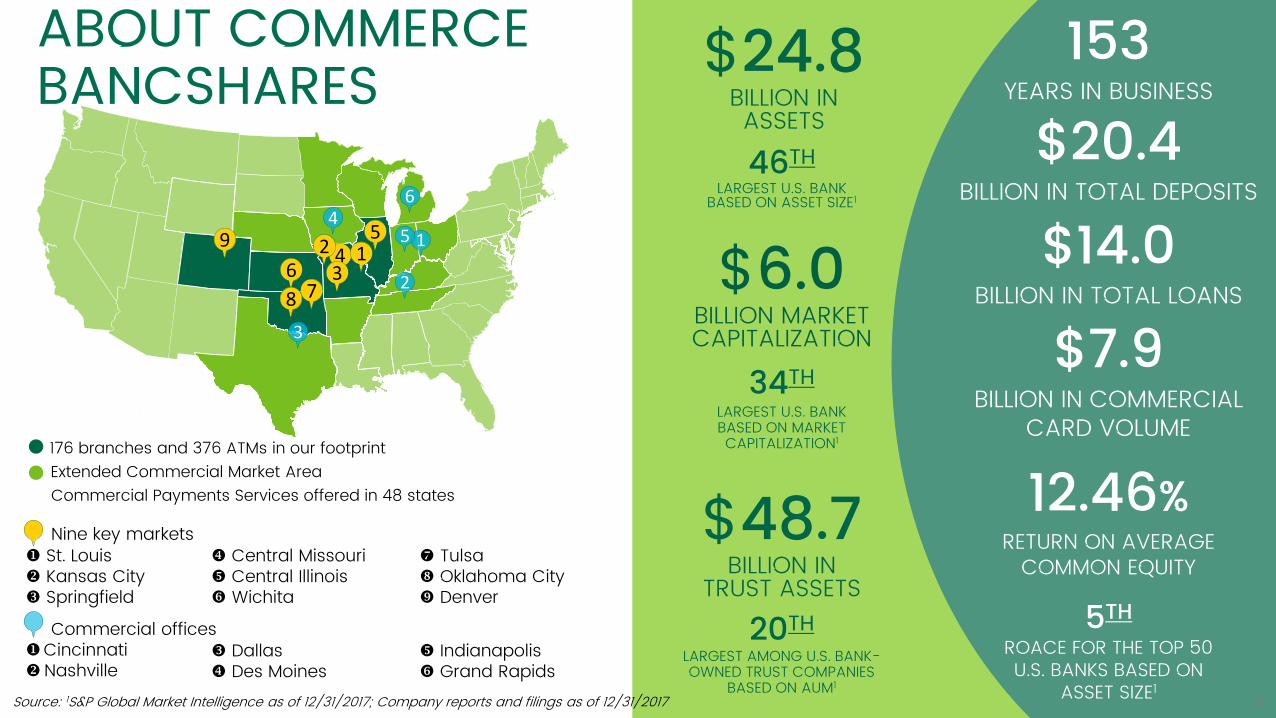

Nine key markets St. Louis Central Missouri Tulsa❖ Kansas City Central Illinois Oklahoma City Springfield Wichita Denver

Commercial officesCincinnati Dallas Indianapolis❖Nashville Des Moines Grand Rapids

ABOUT COMMERCE BANCSHARES

9

76

543

2 1

3

1

28

45

6

Source: 1S&P Global Market Intelligence as of 12/31/2017; Company reports and filings as of 12/31/2017

176 branches and 376 ATMs in our footprintExtended Commercial Market AreaCommercial Payments Services offered in 48 states

$24.8BILLION IN ASSETS46TH

LARGEST U.S. BANK BASED ON ASSET SIZE1

$6.0BILLION MARKET CAPITALIZATION

$48.7BILLION IN

TRUST ASSETS

34THLARGEST U.S. BANK BASED ON MARKET CAPITALIZATION1

20THLARGEST AMONG U.S. BANK-OWNED TRUST COMPANIES

BASED ON AUM1

153YEARS IN BUSINESS

$20.4BILLION IN TOTAL DEPOSITS

$14.0BILLION IN TOTAL LOANS

3

$7.9BILLION IN COMMERCIAL

CARD VOLUME

12.46%RETURN ON AVERAGE

COMMON EQUITY

5THROACE FOR THE TOP 50 U.S. BANKS BASED ON

ASSET SIZE1

4

• Sophisticated payment system capabilities

• Broad consumer product offerings

• Private Banking; Trust; Capital Markets

• Shareholder driven and strong financial performance

• Competitive on unit costs

• Quickly adapt to customer needs and changing preferences

• Core values embraced by employees

• Award winning customer service

• Focus on the full client relationship

Customer relationship-basedCHALLENGE ACCEPTED

High performing teams and engaged workforce

Investment in distinctive, high-return businesses

Long history of top quartile credit quality metrics

Disciplined approach to acquisitionsFocus on operational efficiencies

Community Bank Super-Regional Bank

SUPER-COMMUNITY BANK PLATFORMA consistent strategy with a long term view

4

Giving to our VALUES

• Engaged, long-term leadership team

• Focus on people and talent development

• Knowledge of customers and markets

• Collaboration drives sales across business lines

• Focus on EPS growth• Investing in the

communities in which we operate

A STRONG EMPHASIS ON CULTURE

ENABLES EXECUTION OF CORPORATE STRATEGIES

We have a long term

iew

• Contributed $32 million to Commerce Bancshares Foundation to enable expanded community support

• Rated “outstanding” from the Federal Reserve for community reinvestment

• Employees heavily engaged in the communities we serve

75%

Commerce

78%

U.S. Financial Services Norm

74%

U.S. High Performance Norm

1The Korn Ferry Hay Group – 2017 survey results

2017 Employee Engagement1

We collaborate

as ne teamWe act with

ntegrity

5

We are ustomer

focusedWe strive for

xcellence

6

RECENT RECOGNITION

Ranked 62 out of 300 midsize employers (companies with 1,000 to 5,000 employees). Commerce ranks #2 among other banks on the list.

The award publicly recognizes Korn Ferry clients that have achieved best-in-class levels of engagement. Commerce is one of only three companies in the United States to receive this global award.

The 2017 Private Asset Management Awards recognize and reward top investment professionals, wealth advisors, legal firms, consultants and other key service providers operating within the private asset management industry.

6

Commerce Bank was recognized with eight Greenwich Excellence Awards in the following categories:

Middle Market Banking ($10-500MM)Cash Management - Overall SatisfactionCash Management - Overall Satisfaction - MidwestLikelihood to Recommend / Net Promoter ScoreLikelihood to Recommend / Net Promoter Score - MidwestOverall SatisfactionOverall Satisfaction - MidwestProactively Provides Advice – Midwest

Small Business Banking ($1-10MM)Likelihood to Recommend / Net Promoter Score - Midwest

Source: Commerce Trust Company, U.S. Bureau of Economic Analysis, Bloomberg

U.S. Real GDP Employment

-1,000

-800

-600

-400

-200

0

200

400

600

-7%-6%

-5%-4%

-3%-2%

-1%0%

1%2%

3%

201620142012201020082006200420022000

Monthly Increase (left axis)3 Month Change (right axis)

-5.0%-4.0%-3.0%-2.0%-1.0%0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

20011977 200519931981 1985 2009 2013 20171973 1989 1997

"Sustainable" Trend GrowthY-O-Y (left axis)

10-year Average

ECONOMIC THEMESWe expect growth to accelerate even further in 2018. It would not surprise us if growth approaches or even surpasses 3% this year. The key drivers to this growth are:• Increasing levels of employment• Growth in business and consumer confidence that is translating to increasing retail sales and a

deepening of the capital stock with investment in infrastructure and capital equipment• A continued recovery in the housing market• A positive tailwind from the global economy• Record stock prices• A boost from the Trump tax plan

7

THEMES IN THE BANKING INDUSTRY

8

• The traditional brick and mortar retail branch network remains relevant but with evolution of format and emphasis on strategic location

• Tech enhancements to the digital experience will continue to meet the customers changing needs; organic growth as a result

• Maintaining a balance between deposit retention and rate adjustments• Fraud and cyber crimes continue to be a big threat driving big

investments to improve security • Fintechs are no longer viewed strictly as a competitive threat but also

as potential partnership opportunities• Increased investments in innovation and an ongoing emphasis on

reducing operating costs• Introduction of new technologies, automated processes and the need

to replace aging core systems• Regulation is still a strong influence in the industry but pace of new

regulation is slowing; leadership changes at government agencies will continue to play a role

STRONG PERFORMANCE with ongoing refinement of the “Core Bank”• Super-Community Bank platform• Relationship-based banking• High-touch customer service• Full suite of product and service

offerings• Disciplined attention to risk return• Divest in businesses & activities

that no longer provide acceptable returns

• A highly engaged workforce• Focus on profitability and

shareholder return

MAINTAINING THE BALANCEDisciplined focus on PRIORITY BLUE CHIP investments

• Funding Future Growth• Expansion Market Growth• Transform the Retail Model• Enhance Private Client Model• Health Services Financing• Claims Payments• Commerce Bank Mortgage• Enterprise CRM• Succession Planning

9…emphasis on culture, collaboration & core values

10

CONSUMER BANKING

01,0002,0003,0004,0005,0006,0007,000

201720162015

Banking Channel PreferencesMonthly Banking Sessions (in thousands) Online BranchMobile

10

2016: 2017:

App Store Rating

2016:$19,157

2017:$25,500

Digital Loan Sales(000s)

Continue Expanding Digital CapabilitiesMobile Penetration

2016:49.4%

2017:54.7%

Mobile Deposit Use

2016:3.3%

2017:7.6%

as of 1/17/18

Period end balances, Information as of December 31, 2017

BILL ION$2.5Consumer

Loans

BILL ION$10.3

Consumer Deposits

Consumer Auto Loans

BILL ION$1.0

2016$10.2BILLION

2016$2.5BILLION 750

AverageFICO

2009$113.5 MILLION

$15MILLION

BranchExpense

Reductionsince 2009

11

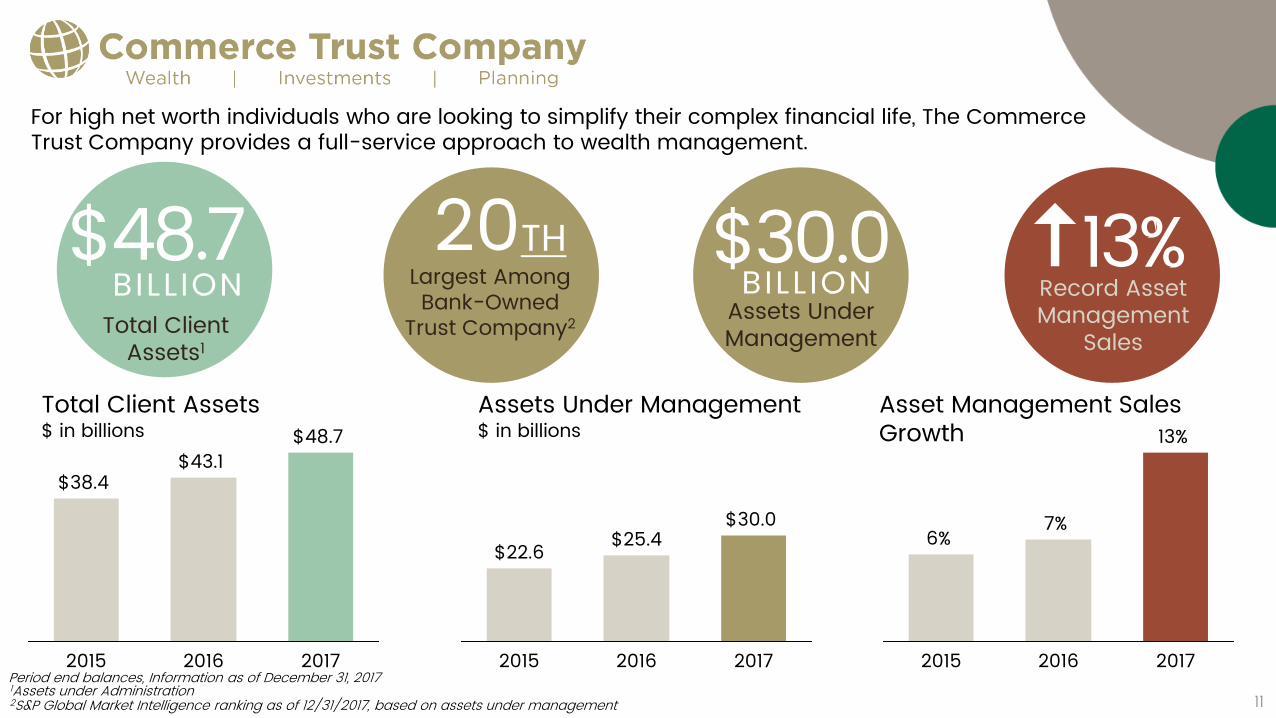

For high net worth individuals who are looking to simplify their complex financial life, The Commerce Trust Company provides a full-service approach to wealth management.

1Assets under Administration2S&P Global Market Intelligence ranking as of 12/31/2017, based on assets under management

Largest Among Bank-Owned

Trust Company2

20THBILL ION

$48.7Total Client

Assets1

BILL ION$30.0

Assets Under Management

13%Record Asset Management

Sales

2017

$48.7

2016

$43.1

2015

$38.4

Total Client Assets$ in billions

$22.6$30.0

2016

$25.4

2015 2017

Assets Under Management$ in billions

2017

13%

2016

7%

2015

6%

Asset Management Sales Growth

11Period end balances, Information as of December 31, 2017

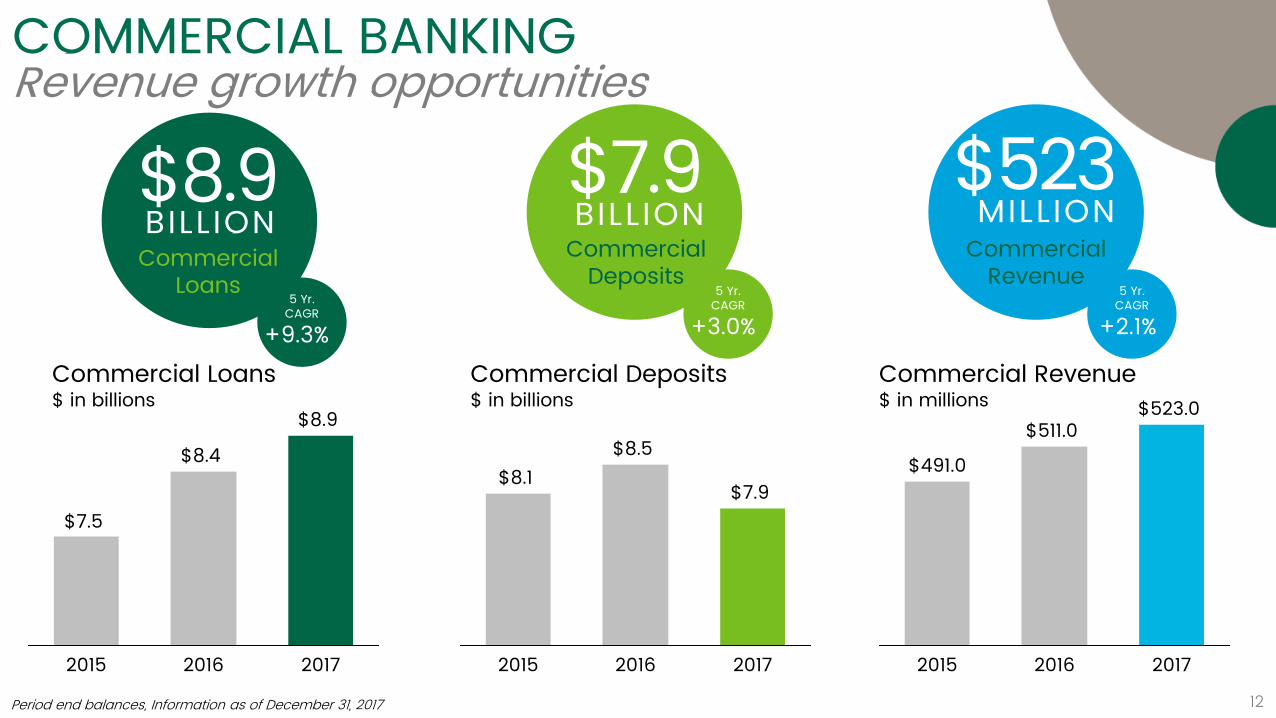

COMMERCIAL BANKINGRevenue growth opportunities

BILL ION$8.9Commercial

Loans

BILL ION$7.9Commercial

DepositsCommercial

Revenue

MILLION$523

5 Yr. CAGR

+9.3%

5 Yr. CAGR

+3.0%5 Yr.

CAGR

+2.1%

2017

$8.9

2016

$8.4

2015

$7.5

Commercial Loans$ in billions

$8.1

2017

$7.9

2016

$8.5

2015

Commercial Deposits$ in billions

2017

$523.0

2016

$511.0

2015

$491.0

Commercial Revenue$ in millions

12Period end balances, Information as of December 31, 2017

13

COMMERCIAL BANKING – EXPANSION MARKETS OFFERING GROWTH OPPORTUNITIES

$500$0

$2,000$1,500$1,000

2012

$608

2016

$1,542

2015

$1,338

2014

$1,091

2013

$962

2017

$1,793

DallasDenverOklahomaCincinnatiNashvilleExpansion Market Loan Growth$s in millions

16.2%

Total Company

4.3%

Expansion Markets

Loan Growth 2017 vs 2016

814

8 8814

2115

OklahomaDenver DallasNashville33

Cincinnati

Personnel Overview for Expansion Markets#of commercial bankers per market* (includes open positions)

2012 2017

Expansion Market Loan

Growth

since 2012195%

13* As of August 2017Period end balances, Information as of December 31, 2017

1414

MILLION$42

TreasuryServicesRevenue

Invoice Capture and Workflow Approval

Payments Hub

Remit Connect Health Services Financing Claims Payments

Supply Chain Finance

$

COMMERCIAL PAYMENTS

MILLION$145

Health Services Financing

Loans

MILLION$194

Payments Revenue

BILL ION$7.9Commercial Card Volume

EMBRACING INNOVATION IN THE PAYMENTS SYSTEMSOur full suite of products and services brings real value to client relationships

14Period end balances, Information as of December 31, 2017

60%

11%

7%

1%

13%

8%

Commerce Bank*

Net Interest Income

Wealth Management

Deposit Service Charges

Fees And Commissions

Card Income

Other

FEE INCOME AT 40% OF TOTAL REVENUE

$437 $448

2014 2017

$487

2016

$474

20152013

$419

2012

$400

Balanced mix of interest and non-interest income

Continued focus on growing fee income through new and existing product and services offeringsExamples:• Toggle™• Remitconnect™• Supply chain finance• Insurance claims payment processing• Accounts Payable automation• Swaps

73%

5%

6%

3% 3%

10%

Peer Banks*

*Source: S&P Global Market Intelligence & FIS as of 12/31/2017Peer Banks include: ASB, BKU, BOKF, CFR, FHN, FNB, FULT, HBHC, IBKC, ISBC, MBFI, PB, SNV, TCF, UMBF, UMPQ, VLY, WBS, WTFC

15

Non-Interest Income$ millions

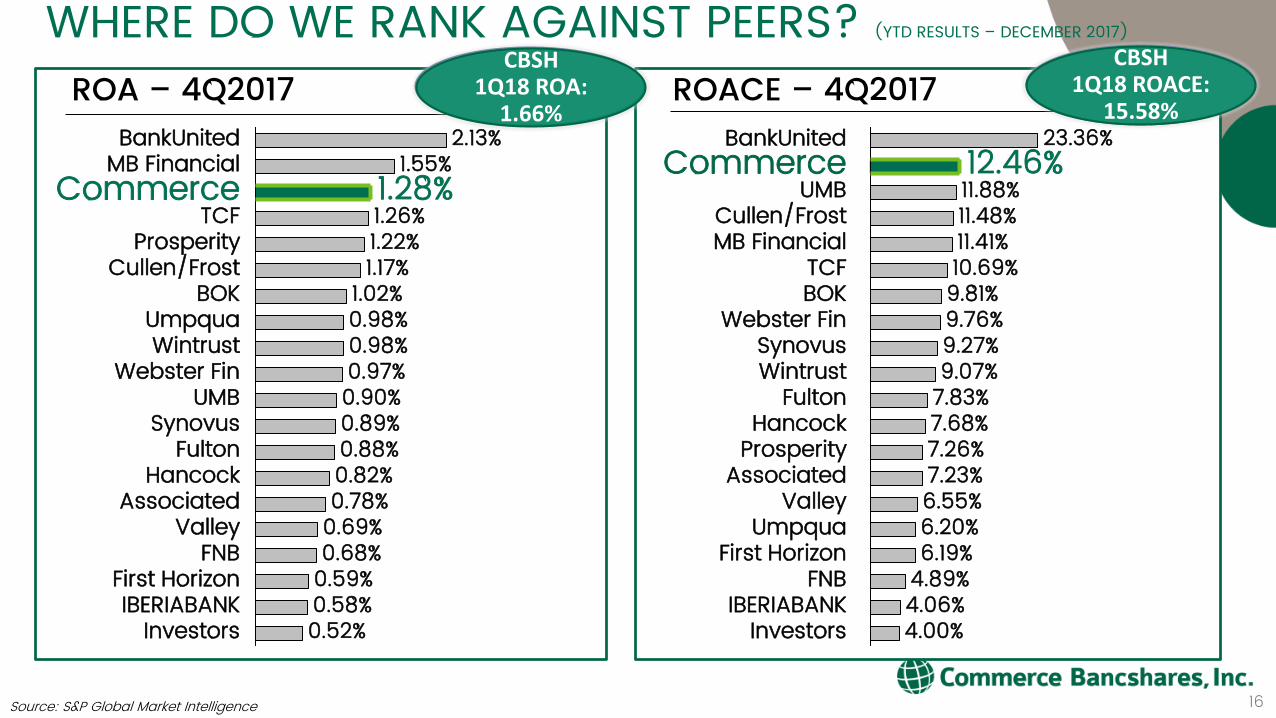

ROACE – 4Q2017ROA – 4Q2017WHERE DO WE RANK AGAINST PEERS? (YTD RESULTS – DECEMBER 2017)

MB Financial 11.41%Cullen/Frost 11.48%

UMB 11.88%Commerce 12.46%

BankUnited 23.36%

Investors 4.00%IBERIABANK 4.06%

FNB 4.89%First Horizon 6.19%

Umpqua 6.20%Valley

10.69%

6.55%Associated 7.23%

Prosperity 7.26%Hancock 7.68%

Fulton 7.83%Wintrust 9.07%Synovus 9.27%

Webster Fin 9.76%BOK 9.81%TCF

0.88%0.89%

UMB 0.90%Webster Fin 0.97%

Wintrust 0.98%Umpqua 0.98%

BOK 1.02%Cullen/Frost 1.17%

Prosperity 1.22%TCF 1.26%

Commerce

Synovus

0.52%InvestorsIBERIABANK 0.58%

First Horizon 0.59%FNB 0.68%

Valley 0.69%Associated 0.78%

Hancock 0.82%Fulton

1.28%MB Financial 1.55%BankUnited 2.13%

16Source: S&P Global Market Intelligence

CBSH 1Q18 ROA:

1.66%

CBSH 1Q18 ROACE:

15.58%

2017 YEAR END EARNINGS$ in millions 2016A 2017A Actual

% Incr.Net interest income $ 680 $ 734 8%Non-interest income 446 461 3%

Total revenue 1,127 1,195 6%Securities gains/(losses) (0) 25 NMNon-interest expense (689) (744) 8%Provision for loan losses (36) (45) 25%

Pretax income 401 431 7%Income taxes (124) (111) -11%Net income 277 320 16%

Non-controlling int. exp. (1) (1) NMNet inc attrib. to Commerce 275 319 16%

Less preferred stock div. (9) (9) 0%Net inc avail. to common

stock 266 310 17%

Diluted EPS $ 2.49 $ 2.89 16%17

ROA2016: 1.12%2017: 1.28%

ROACE2016: 11.33%2017: 12.46%

Efficiency Ratio2016: 61.04%2017: 62.18%

Cash Dividends2016: $0.8162017: $0.857

Ending Stock Price2016: $55.062017: $55.84

FINANCIAL HIGHLIGHTS QTDMARCH 31, 2018

$ millions (except EPS) 1Q2017 1Q2018 % changeNet Income attrib to Commerce $72 $101 40.3%

Return on Average Assets 1.15% 1.66% 44.3%

Return on Average Common Equity 11.74% 15.58% 32.7%

Efficiency Ratio 62.19% 58.21% -6.4%

Average Loans $13,537 $13,929 2.9%

Average Deposits $21,023 $20,161 -4.1%

Diluted EPS* $0.65 $0.92 41.5%

*Per shares figures have been restated for 5% stock dividend distributed in December 2017 18

COMMERCE BANK MAINTAINS SOLID PERFORMANCE OVER TIME

-0.5%

0.0%

0.5%

1.0%

1.5%

201620152014201320122011 2017201020092008

Return on Assets

Return on Average Common Equity

-5.0%

0.0%

5.0%

10.0%

15.0%

2017201620152014201320122011201020092008

Commerce Bank Large BanksPeer Banks

Source: S&P Global Market Intelligence; data as of 12/31/2017; CBI numbers via internal reporting

Peer Banks include: ASB, BKU, BOKF, CFR, FHN, FNB, FULT, HBHC, IBKC, ISBC, MBFI, PB, SNV, TCF, UMBF, UMPQ, VLY, WBS, WTFC; Large Banks include: JPM, BAC, C, WFC USB, PNC, FITH, RF

ROA 10-yr averageCBSH: 1.18% Peers: 0.63%

ROACE 10-yr average CBSH: 11.57% Peers: 5.53%

19

Dividends per share

*Including 2012 special dividend = $1.806All data has been restated for 5% stock dividend distributed in December 2017Net Income in the chart represents Net Income Available to Common ShareholdersSource: Corporate Finance

LONG TERM VIEW: NET INCOME AND EARNINGS PER SHARENe

t Inc

ome

$ 00

0s

$1.00

$350

300250

200150

10050

$1.50

$3.00

$2.00

$2.50

2017201620152014201320122011201020092008

Net IncomeEarnings Per Share

49TH CONSECUTIVE YEAR OF DIVIDEND GROWTHEPS REMAINS STRONG

Earn

ings

per

Sha

re

$0.86$0.61 $0.62 $0.64 $0.65 $0.69* $0.71 $0.74 $0.78 $0.82

20

STEADY SHAREHOLDER RETURNS as of December 31, 2017

Source: Corporate Finance, Bloomberg; data as of 12/31/2017

Total Shareholder ReturnsIndexed, 12/31/2007 = $100

Consistent, positive returns to shareholders Significant outperformance relative to banks over long period

0%

5%

10%

15%

20%

25%

10 Year5 Year3 Year1 Year

KBW Bank IndexNASDAQ Banks

S&P 500CBSH

Annualized ComparisonTotal Shareholder ReturnsPercent

3.03% 16.19% 17.43% 10.06%21.82% 11.39% 15.77% 8.49%5.46% 16.53% 18.66% 6.48%

18.59% 15.24% 18.18% 4.13%

$300

$250

$200

$150

$100

$50

$0201720152013201120092007

KBW BANK INDEXS&PNASDAQ

BANK INDEX

COMMERCE BANK

21

NOTICE: Due to technical difficulties, the recorded audio file for the Annual Shareholder meeting is of low quality. However, if you are interested in listening to the recorded message, you can access the recording by clicking on the link provided below.

2018 Shareholder Meeting Webcast Audio