Challenges and Opportunities of Ethiopian Pulse Export

28

Challenges and Opportunities of Ethiopian Pulse Export Dawit Alemu Setotaw Ferede Endeshaw Habte Agajie Tesfaye Shenkut Ayele Research Report 80 የኢትዮጵያ የግብርና ምርምር ኢንስቲትዩት Ethiopian Institute of Agricultural Research

Transcript of Challenges and Opportunities of Ethiopian Pulse Export

Challenges and Opportunities

of

Ethiopian Pulse Export

Dawit Alemu

Setotaw Ferede

Endeshaw Habte

Agajie Tesfaye

Shenkut Ayele

Research Report 80

የኢትዮጵያ የግብርና ምርምር ኢንስቲትዩት Ethiopian Institute of Agricultural Research

Challenges and Opportunities

of

Ethiopian Pulse Export

©EIAR, 2010 ›=ÓU›=' 2003

Website: http://www.eiar.gov.et Tel: +251-11-6462633 Fax: +251-11-6461294 P.O.Box: 2003 Addis Ababa, Ethiopia

Copyediting: Abebe Kirub Page Design: Abebe Kirub Printing: Abesolom Kassa Binding and collation: Abesolom Kassa. Miftah Argeta, and Meseret Kebede Distribution: Solomon Tsega and Tigist Beshir Bibliographic input to WAICENT (FAO): Tigist Beshir ISBN: 978-99944-53-50-1

Challenges and opportunities of Ethiopian pulse export

1

Contents

Executive Summary ......................................................................................................................... 2 1 Introduction ............................................................................................................................ 4 2 Methodology .......................................................................................................................... 6 3 Results .................................................................................................................................. 7

3.1 Overview of pulse production in Ethiopia....................................................................... 7 3.1.1 Characteristics of Pulse production .................................................................... 7 3.1.2 Pulse production and supply in 2000/2001 E.C .................................................... 9

3.2 Pulse marketing system and costs ...............................................................................10 3.3 Trends in export of major pulse crops ..........................................................................12

3.3.1 Pulse export performance (2005 – 2008) .......................................................... 12 3.3.2 Seasonality of pulse export ............................................................................. 14 3.3.3 Destinations of pulse export ............................................................................ 16

3.4 Export and domestic market prices ..............................................................................19 3.5 Constraints and opportunities ......................................................................................21

3.5.1 Poor quality pulse seeds ................................................................................ 21 3.5.2 Limited volume of domestic production and huge demand ................................... 22 3.5.3 Impurities in the primary and secondary markets ................................................ 23 3.5.4 Unstable domestic market .............................................................................. 23 3.5.5 Relatively long market chain ........................................................................... 23 3.5.6 Misbehavior of brokers ................................................................................... 23 3.5.7 Capacity of exporters and wholesalers to store quality seeds ............................... 23 3.5.8 Transportation cost........................................................................................ 24 3.5.9 Variability in destination markets...................................................................... 24 3.5.10 Decline of demand in importing countries .......................................................... 24

4 Conclusion and Recommendations........................................................................................25 5 References ...........................................................................................................................26

Dawit Alemu et. al

2

Executive Summary

Pulses are one of the important Ethiopian agricultural export commodities and their performance in the export is influenced by the both domestic and international market situations. The overall situation of the production, marketing, and export of pulses that has direct linkage with Ethiopian export performance can be summarized as:

Increasing trend in the level of production due to increased productivity and area expansion;

Expansion in the type of pulse crops exported and the coming up of faba bean, lentil and field pea along with chickpea and haricot beans;

Relatively good production during the 2008 season due to increased productivity and also area expansion even though there was certain level of quality deterioration due to the late rain fall;

The 2008/09 marketing season for most of the pulses started immediately after harvest with higher prices that have started to decline in subsequent months after most of the wholesalers have bought. This has created disincentive to sell the collected produce during the normal marketing season and thus to opt to store;

Deterioration of quality in terms of mainly seed size and color due to use of poor quality seed mainly inappropriate varieties;

Huge domestic demand for most of the pulses, which gave incentive to farmers to have domestic demand oriented production;

Considerable improvement in the storage, cleaning and grading capacity of exporters and wholesalers with reduced quality and quantity losses;

Unstable domestic market, which can easily be influenced by the actions of few of the market actors like brokers and purchase announces of major purchases like WFP and EGTE;

Considerable variability of export destinations, which implies that our export destination is not stable that exporters do not have relatively longer trade relationship with their respective importers; and

Considerable impact of the recent global financial and economic crises on the demand for Ethiopian pulses.

The increased trend in the production of pulses due to productivity improvement and area expansion; the emergence of new pulse crops for export; improvement in the storage, cleaning, and grading capacity of exporters and wholesalers; and the existing favorable public support for export have supported the increase of export over the years. However, the export performance in the last quarter of 2008 and in the first quarter of 2009 has shown a declining trend. This is because of decline in international demand, poor seed quality of local production, huge domestic demand, and unstable

Challenges and opportunities of Ethiopian pulse export

3

domestic market. In order to overcome the stated constraints the following issues require urgent attention:

Improving the access and use of available improved varieties of pulse crops by farmers that have international demand along with recommended agronomic practices., which need to be augmented with promotion of farmers’ access to pulse markets with premium price for quality;

The existing domestic market for impurities (by-products from cleaning and grading activities) need to be regulated as this is increasing the cost of cleaning and grading for exporters, which in tern is reducing their competitiveness;

Promotion of availability of market information, which enable all market actors to make right market decision and also to reduce the impact of misbehaving brokers;

Transportation costs either from production areas to Addis Ababa and from Addis Ababa to Port of Djibouti or border of Sudan are found to be high limiting the competitiveness our export even, when there is a price adjustment of fuel, the transportation costs do not respond. Thus, there is a need to regulate the transportation costs;

Ethiopian pulses do not have mainstream international markets as the destination markets vary from year to year. In addition, competitors in the international markets do vary from year to year. Thus, it is important that public international market intelligence along with increasing the capacity of our exporters in market intelligence be promoted. This could be facilitated through Ethiopian Embassies located in several parts of the world. The exporters have expressed interests to participate in trade fairs, exhibitions and several other similar business related platforms to demonstrate their products. The embassies can trace such events and inform the exporters for possible participation;

To address the impact of reduction in international demand there is a need for short-term solution, which should be sought with joint effort of the public with relevant market actors and the Ethiopian Pulses, Oilseeds and Spices Processors and Exporters’ Association (EPOSPEA).

Dawit Alemu et. al

4

1 Introduction Historically, international trade in agriculture has been heavily distorted due to the nature of the production and products and the huge subsidies in developed countries and taxation in developing countries following the different importance in the economic contribution of the sector in respective countries and still the improvements in trade distortion are minimal. It is in the Uruguay round (the eighth round in 1994) that agriculture was included in the GATT negotiations, since the establishment of GATT in 1947 immediately after the World War II. Ethiopia along with other nine least developed countries is negotiating to join the WTO for improving its access to international markets. This still justifies the role of the state in agricultural trade. Thus, it is important that along with different domestic measures to improve the national competitiveness, there is a need to actively improve and negotiate international agricultural trade relations. Pulse export is one of the principal sources of the country’s foreign earnings next to coffee, chat, hides and skins, and oil crops. Following the market liberalization in the early 90s, the role of state marketing parastatals in the local and export markets has declined considerably with increasing involvement of private market agents and private exporters. The government has also took active role to improve the performance of the external sector by adopting various measures such as devaluation of the local currency, improving the licensing procedure and establishing and improving different organizations that have got direct link with export (Dawit and Demelash, 2003). In addition, there are export trade incentives introduced for enhancing the competitiveness of the country in export trade activities, which are the export trade duty incentive and export financing incentive schemes. The most important incentives for pulse export are related to export financing incentive schemes, which are export credit guarantee scheme, foreign exchange retention scheme, and foreign credit scheme. The export credit guarantee scheme provides exporters access to pre-shipment and post-shipment finance equivalent to the total value of the previous year export proceeds without any collateral requirement for existing exporters and with 20% and 30% collateral requirement for new producer exporters and new exporters, respectively. The foreign exchange retention scheme is implemented by allowing exporters to retain their foreign exchange earnings themselves into two types of foreign exchange accounts. In account “A” exporters are allowed to retain 10% of the proceed from their exporting for an indefinite period of time and the remaining 90% in account “B” for about 28 days to transact business related to current payment for the import of goods and related services, export promotion

Challenges and opportunities of Ethiopian pulse export

5

payment of advertisement and marketing expenses, training fee and educational expenses. The foreign credit scheme allows producer exporters to have access to foreign credit. Foreign credit is an interim financing provided by a supplier or a foreign partner, which is usually short term financing, but can include medium and long term financing. Dawit and Demelash (2003) have documented the dominance of haricot bean among exported pulses in both the pre-reform and post-reform period (before and after 1991) and rapid growth in the volume of export after the reform (compounded rate of annual growth of 24%). In recent years, the composition of pulse export has been changing as non-traditional export pulses like chickpea; faba bean and lentil have come into picture. This paper assesses the trend in the production, marketing and export of major pulse crops with due emphasis to the identification of major constraints and opportunities in promoting their export. Content wise, the report is organized sequentially where the overview of the trend in the production is presented first, followed by the description of the domestic marketing system, where the analysis of major market actors, marketing channels and margins is summarized. In the next section, the trend in pulse export in terms of the export performance, seasonality, and destination is presented followed by summary of margin analysis between producers and export prices. The major constraints and opportunities that needs due attention for improved export performance are describe before the conclusions and policy implications are presented.

Dawit Alemu et. al

6

2 Methodology The study used both primary and secondary data where the secondary data was mainly sourced from the Ethiopian Revenue and Customs Authority and recent research publications. The primary data were generated through a rapid appraisal method where discussions were made with key informants from exporters, local traders, farmers, farmers’ marketing cooperatives and their unions, and experts. Checklists developed for the different data sources guided the data collection. The trend analysis made using the secondary data served as base for further design of the study and designing of the checklists. Overall, a value chain approach was employed to identify the constraints and opportunities at each level of the chain.

Challenges and opportunities of Ethiopian pulse export

7

3 Results

3.1 Overview of pulse production in Ethiopia

3.1.1 Characteristics of Pulse production

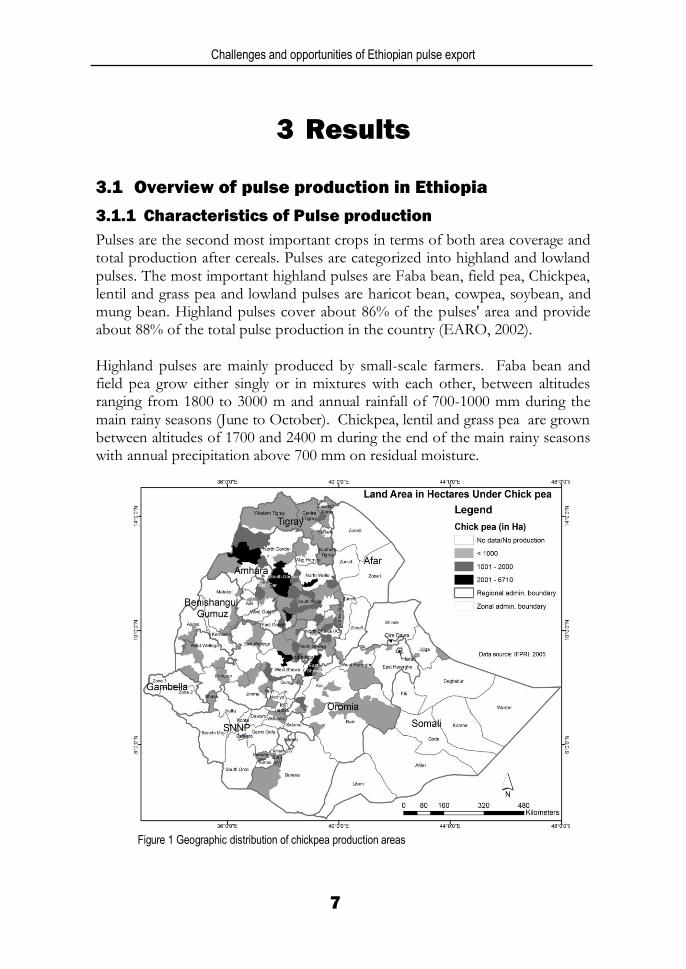

Pulses are the second most important crops in terms of both area coverage and total production after cereals. Pulses are categorized into highland and lowland pulses. The most important highland pulses are Faba bean, field pea, Chickpea, lentil and grass pea and lowland pulses are haricot bean, cowpea, soybean, and mung bean. Highland pulses cover about 86% of the pulses' area and provide about 88% of the total pulse production in the country (EARO, 2002). Highland pulses are mainly produced by small-scale farmers. Faba bean and field pea grow either singly or in mixtures with each other, between altitudes ranging from 1800 to 3000 m and annual rainfall of 700-1000 mm during the main rainy seasons (June to October). Chickpea, lentil and grass pea are grown between altitudes of 1700 and 2400 m during the end of the main rainy seasons with annual precipitation above 700 mm on residual moisture.

Figure 1 Geographic distribution of chickpea production areas

Dawit Alemu et. al

8

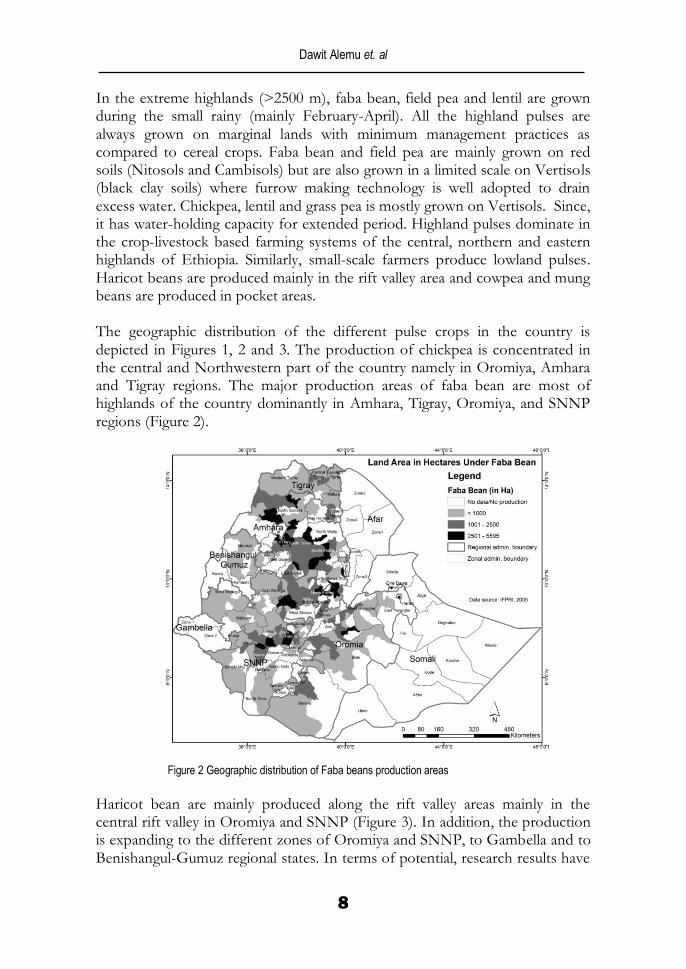

In the extreme highlands (>2500 m), faba bean, field pea and lentil are grown during the small rainy (mainly February-April). All the highland pulses are always grown on marginal lands with minimum management practices as compared to cereal crops. Faba bean and field pea are mainly grown on red soils (Nitosols and Cambisols) but are also grown in a limited scale on Vertisols (black clay soils) where furrow making technology is well adopted to drain excess water. Chickpea, lentil and grass pea is mostly grown on Vertisols. Since, it has water-holding capacity for extended period. Highland pulses dominate in the crop-livestock based farming systems of the central, northern and eastern highlands of Ethiopia. Similarly, small-scale farmers produce lowland pulses. Haricot beans are produced mainly in the rift valley area and cowpea and mung beans are produced in pocket areas. The geographic distribution of the different pulse crops in the country is depicted in Figures 1, 2 and 3. The production of chickpea is concentrated in the central and Northwestern part of the country namely in Oromiya, Amhara and Tigray regions. The major production areas of faba bean are most of highlands of the country dominantly in Amhara, Tigray, Oromiya, and SNNP regions (Figure 2).

Figure 2 Geographic distribution of Faba beans production areas

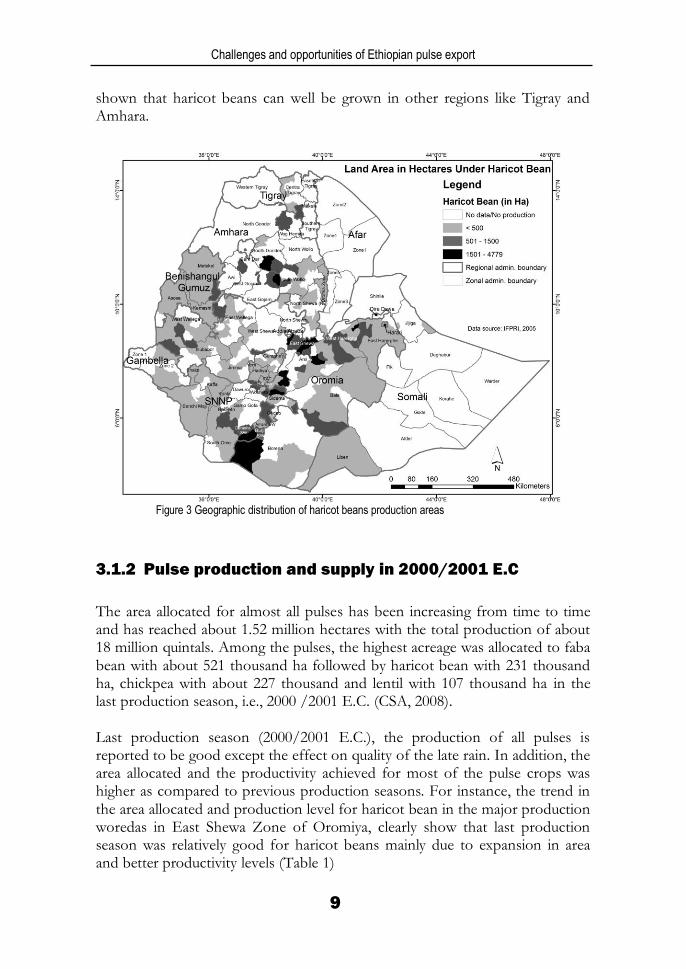

Haricot bean are mainly produced along the rift valley areas mainly in the central rift valley in Oromiya and SNNP (Figure 3). In addition, the production is expanding to the different zones of Oromiya and SNNP, to Gambella and to Benishangul-Gumuz regional states. In terms of potential, research results have

Challenges and opportunities of Ethiopian pulse export

9

shown that haricot beans can well be grown in other regions like Tigray and Amhara.

Figure 3 Geographic distribution of haricot beans production areas

3.1.2 Pulse production and supply in 2000/2001 E.C

The area allocated for almost all pulses has been increasing from time to time and has reached about 1.52 million hectares with the total production of about 18 million quintals. Among the pulses, the highest acreage was allocated to faba bean with about 521 thousand ha followed by haricot bean with 231 thousand ha, chickpea with about 227 thousand and lentil with 107 thousand ha in the last production season, i.e., 2000 /2001 E.C. (CSA, 2008). Last production season (2000/2001 E.C.), the production of all pulses is reported to be good except the effect on quality of the late rain. In addition, the area allocated and the productivity achieved for most of the pulse crops was higher as compared to previous production seasons. For instance, the trend in the area allocated and production level for haricot bean in the major production woredas in East Shewa Zone of Oromiya, clearly show that last production season was relatively good for haricot beans mainly due to expansion in area and better productivity levels (Table 1)

Dawit Alemu et. al

10

Overall, the productivity of haricot bean has increased on average from 8.20 quintal in 2004 to 17 q/ha in 2008 in these woredas in East Shewa zone of Oromiya. Thus, the production of pulse crops in the 2000/2001 E.C. production season was higher than the previous years implying the possible increase in marketable surplus thereby the export. However, it should be mentioned the most of the types of haricot bean varieties used for production in these woredas were not varieties with international demand. Table 1 Trend in the area and production of haricot bean in major woredas of East Shewa zone of Oromiya

Year Adami Tulu Adama Bosset Lume East Shewa

Zone

Area (ha) 2004 (1996/97) 29649 2898 6418 957 39922

2005 (1997/98) 18323 3695 8072 1027 31117

2006 (1998/99) 18000 3655 7653 1225 30533

2007 (1999/00) 18160 4012 7818 893 30883

2008 (2000/01) 17459 4195 8550 1246 31450

Production (q) 2004 (1996/97) 174,524.00 66,247.00 77,016.00 9,570.00 327,357.00

2005 (1997/98) 156,404.00 42,838.00 54,082.00 15,405.00 268,729.00

2006 (1998/99) 217,980.00 89,811.00 137,754.00 24,500.00 470,045.00

2007 (1999/00) 208,840.00 100,306.00 156,377.00 17,860.00 483,383.00

2008 (2000/01) 233,868.00 115,877.19 162,450.00 26,478.00 538,673.19

Average productivity (q / ha)

2004 (1996/97) 5.89 22.86 12.00 10.00 8.20

2005 (1997/98) 8.54 11.59 6.70 15.00 8.64

2006 (1998/99) 12.11 24.57 18.00 20.00 15.39

2007 (1999/00) 11.50 25.00 20.00 20.00 15.65

2008 (2000/01) 13.40 27.62 19.00 21.25 17.13

Source: respective woreda bureaus of Agriculture and Rural Development

3.2 Pulse marketing system and costs

Except for haricot beans, pulse-marketing system is highly underdeveloped and poorly organized. For instance, the domestic market accounts for over 80% of the total chickpea volume traded annually and the export market outlet is relatively new and highly variable depending on production conditions in the major importing countries in South Asia and competitiveness with other exporters. Haricot bean is the only pulse crop with relatively better marketing system, which traded through Ethiopian Commodity Exchange (ECX). Immediately after harvest of the last production season (2008) there was haricot bean trade with about a thousand quintals monthly but currently there is no offer at the exchange. Due to the production of pulses by small-scale farmers that are scattered over the different production areas of the country and the use of different varieties, there are different market actors that are involved along the chain and the pulse markets under these circumstances can be categorized into primary, secondary, and tertiary markets. The primary markets are rural spot markets where most of

Challenges and opportunities of Ethiopian pulse export

11

smallholder farmers sell their produce to assemblers and rural consumers. The sell of produce to primary cooperatives can also be considered as primary market. The secondary markets for pulses are woreda level markets where assemblers, brokers, woreda level wholesalers, processors (cleaning and grading), unions, and consumers exchange produces in a relatively higher volume. Woreda level retailers are also engaged in the secondary markets. The actors in the tertiary markets include urban wholesalers, exporters, processors, small retailers and supermarkets. The urban wholesalers represent as a major gateway to exporters and urban retailers. Except the parastatal the Ethiopian Grain Trade Enterprise (EGTE) and Farmers Marketing Cooperative Unions (FMCU), most of the urban wholesalers are based in Addis Ababa (dominantly at Ehil Berenda) and Nazareth (Adama). In most of the cases, exporters own cleaning and grading facilities. Transporters and quality certifying public organizations are also important actors in the chain. Export competitiveness can be influenced by the cost structure along the marketing channel. The cost structure of pulse exporters is estimated for haricot bean and it is expected that except the purchase cost the other costs are similar for other exported pulses. The major cost component for the exporters is the purchase cost from wholesalers, which is estimated to have 74% from the total cost. The other considerable cost components are impurities (on average about 10% impurity), which represented about 8% of the total cost. Similarly, transportation cost mainly transport to Port Djibouti contributed about 8% from the total cost (Table 2).

Table 2 Cost of haricot bean export

Cost components Range (birr /q)

Average (birr/ q)

% Share

Purchase from wholesalers 300 - 400 350.00 74.1

load/unload 7 - 8 7.50 1.6

packaging 4 - 10 7.00 1.5

Commission 2 - 3 2.50 0.5

Cleaning 20 - 25 22.50 4.8

Impurity (average 10%) 32 - 40 36.00 7.6

Transport 25 - 48 36.50 7.7

Transit & service 2.3 2.30 0.5

Overhead 5 - 10 7.50 1.6

Certification 0.72 0.72 0.2

Cost of value added by exporter 122.52 25.9

Total cost 472.52 Source: calculated based on five haricot bean exporter estimates for last export

Dawit Alemu et. al

12

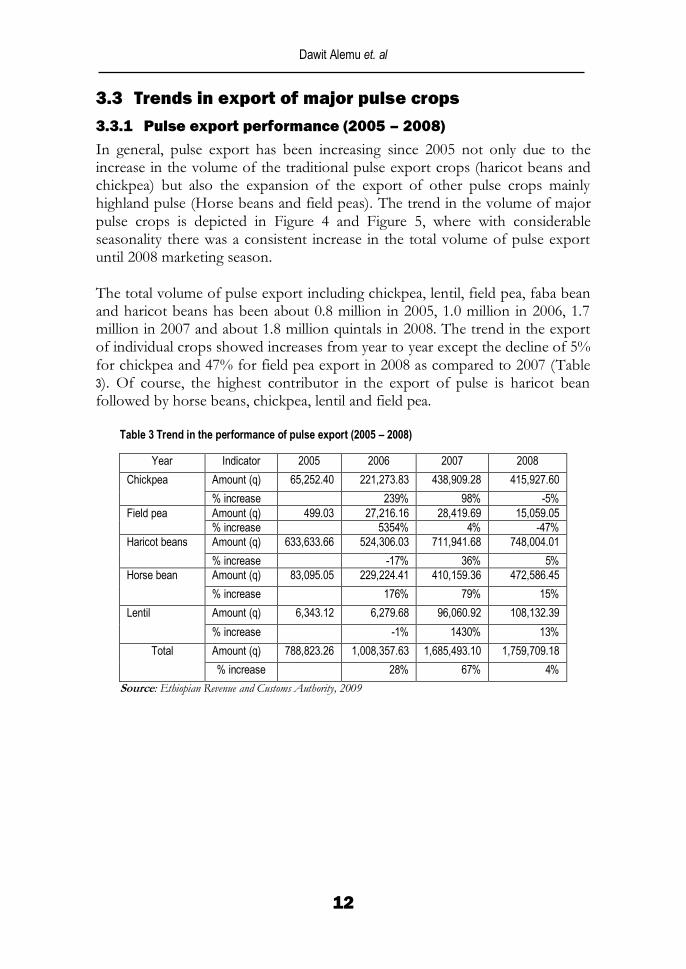

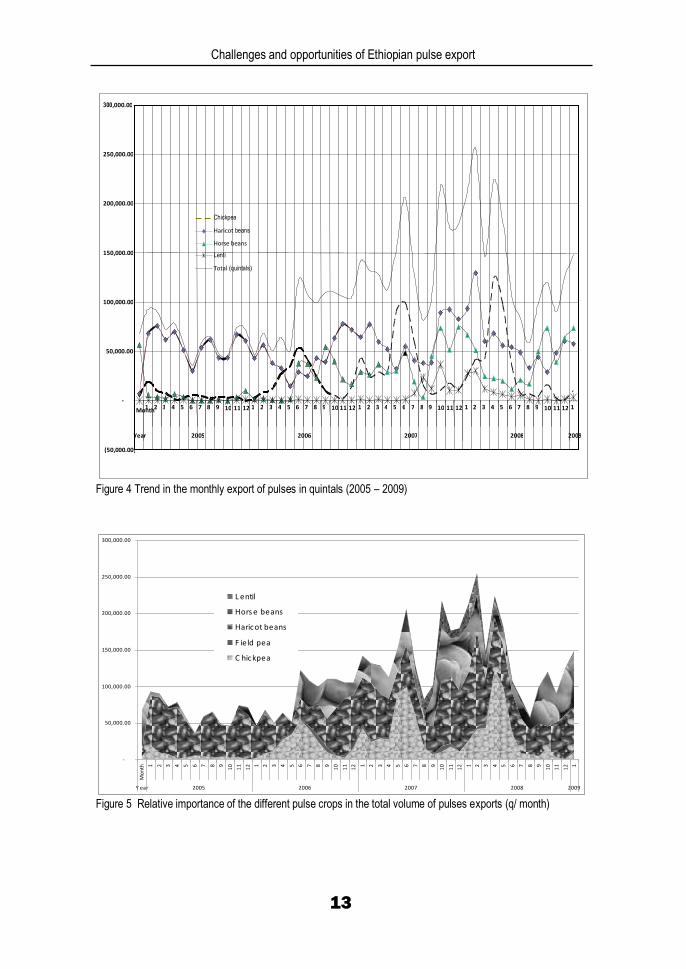

3.3 Trends in export of major pulse crops

3.3.1 Pulse export performance (2005 – 2008)

In general, pulse export has been increasing since 2005 not only due to the increase in the volume of the traditional pulse export crops (haricot beans and chickpea) but also the expansion of the export of other pulse crops mainly highland pulse (Horse beans and field peas). The trend in the volume of major pulse crops is depicted in Figure 4 and Figure 5, where with considerable seasonality there was a consistent increase in the total volume of pulse export until 2008 marketing season. The total volume of pulse export including chickpea, lentil, field pea, faba bean and haricot beans has been about 0.8 million in 2005, 1.0 million in 2006, 1.7 million in 2007 and about 1.8 million quintals in 2008. The trend in the export of individual crops showed increases from year to year except the decline of 5% for chickpea and 47% for field pea export in 2008 as compared to 2007 (Table

3). Of course, the highest contributor in the export of pulse is haricot bean followed by horse beans, chickpea, lentil and field pea.

Table 3 Trend in the performance of pulse export (2005 – 2008)

Year Indicator 2005 2006 2007 2008

Chickpea Amount (q) 65,252.40 221,273.83 438,909.28 415,927.60

% increase 239% 98% -5%

Field pea Amount (q) 499.03 27,216.16 28,419.69 15,059.05

% increase 5354% 4% -47%

Haricot beans Amount (q) 633,633.66 524,306.03 711,941.68 748,004.01

% increase -17% 36% 5%

Horse bean Amount (q) 83,095.05 229,224.41 410,159.36 472,586.45

% increase 176% 79% 15%

Lentil Amount (q) 6,343.12 6,279.68 96,060.92 108,132.39

% increase -1% 1430% 13%

Total Amount (q) 788,823.26 1,008,357.63 1,685,493.10 1,759,709.18

% increase 28% 67% 4%

Source: Ethiopian Revenue and Customs Authority, 2009

Challenges and opportunities of Ethiopian pulse export

13

Figure 4 Trend in the monthly export of pulses in quintals (2005 – 2009)

-

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

Mo

nth 1 2 3 4 5 6 7 8 9

10

11

12 1 2 3 4 5 6 7 8 9

10

11

12 1 2 3 4 5 6 7 8 9

10

11

12 1 2 3 4 5 6 7 8 9

10

11

12 1

Y ear 2005 2006 2007 2008 2009

L entil

Hors e beans

Haricot beans

F ield pea

C hickpea

Figure 5 Relative importance of the different pulse crops in the total volume of pulses exports (q/ month)

(50,000.00)

-

50,000.00

100,000.00

150,000.00

200,000.00

250,000.00

300,000.00

Month 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1 2 3 4 5 6 7 8 9 10 11 12 1

Year 2005 2006 2007 2008 2009

Chickpea Haricot beans Horse beans Lentil Total (quintals)

Dawit Alemu et. al

14

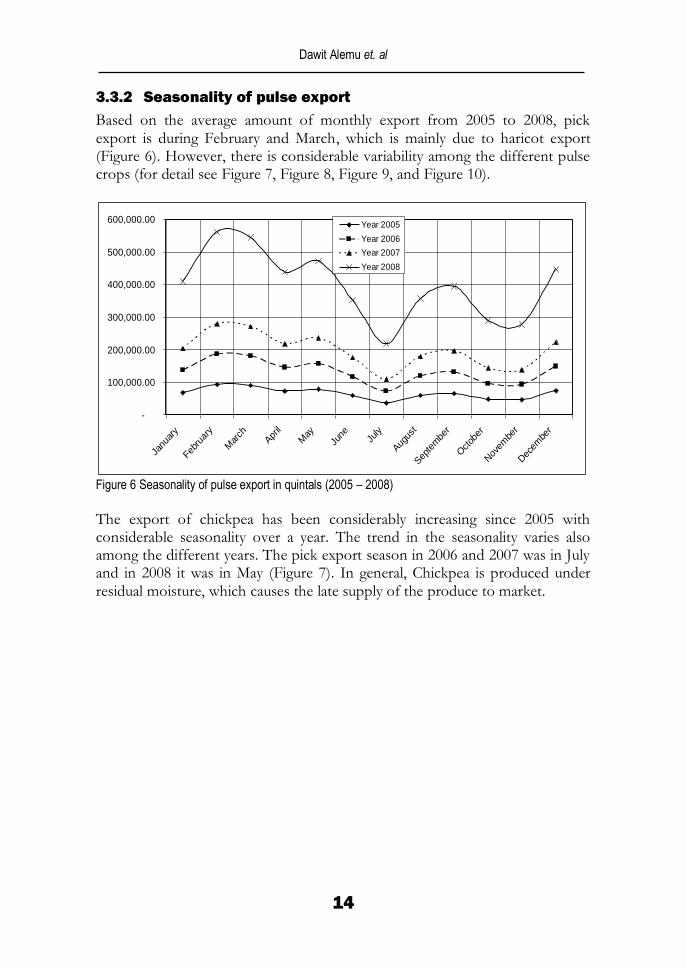

3.3.2 Seasonality of pulse export

Based on the average amount of monthly export from 2005 to 2008, pick export is during February and March, which is mainly due to haricot export (Figure 6). However, there is considerable variability among the different pulse crops (for detail see Figure 7, Figure 8, Figure 9, and Figure 10).

-

100,000.00

200,000.00

300,000.00

400,000.00

500,000.00

600,000.00

Janu

ary

Febru

ary

Mar

chApr

il

May

June Ju

ly

Aug

ust

Sep

tembe

r

Octob

er

Nov

embe

r

Dec

embe

r

Year 2005

Year 2006

Year 2007

Year 2008

Figure 6 Seasonality of pulse export in quintals (2005 – 2008)

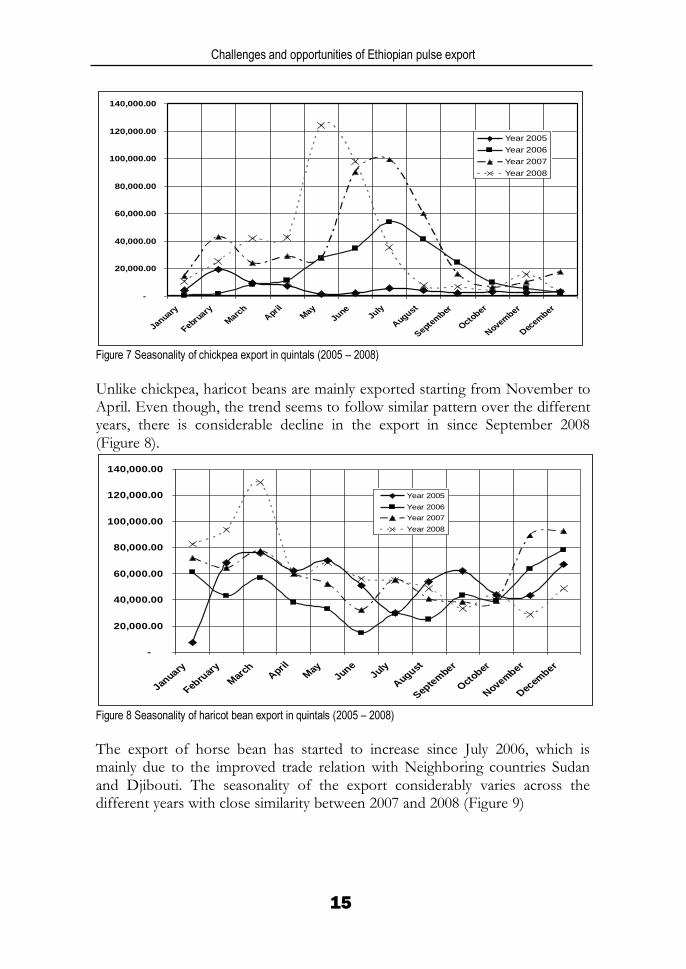

The export of chickpea has been considerably increasing since 2005 with considerable seasonality over a year. The trend in the seasonality varies also among the different years. The pick export season in 2006 and 2007 was in July and in 2008 it was in May (Figure 7). In general, Chickpea is produced under residual moisture, which causes the late supply of the produce to market.

Challenges and opportunities of Ethiopian pulse export

15

-

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

January

February

Marc

hA

prilM

ayJune

July

August

Septem

ber

Octo

ber

Novem

ber

Dec

ember

Year 2005

Year 2006

Year 2007

Year 2008

Figure 7 Seasonality of chickpea export in quintals (2005 – 2008)

Unlike chickpea, haricot beans are mainly exported starting from November to April. Even though, the trend seems to follow similar pattern over the different years, there is considerable decline in the export in since September 2008 (Figure 8).

-

20,000.00

40,000.00

60,000.00

80,000.00

100,000.00

120,000.00

140,000.00

January

Febru

ary

Mar

chApril

May

JuneJuly

August

Septe

mber

Oct

ober

November

Decem

ber

Year 2005

Year 2006

Year 2007

Year 2008

Figure 8 Seasonality of haricot bean export in quintals (2005 – 2008)

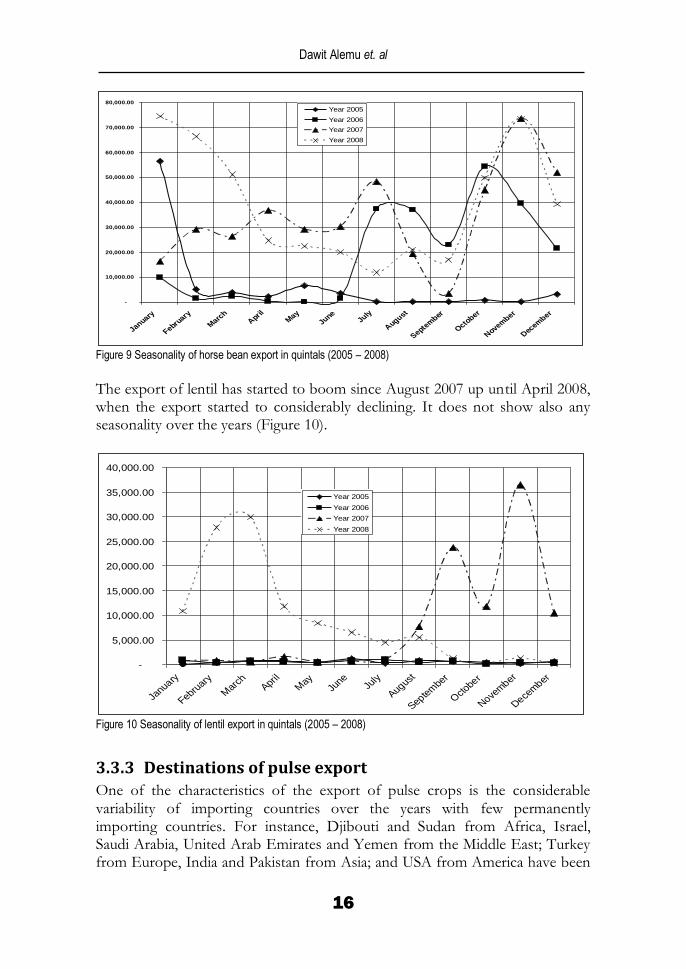

The export of horse bean has started to increase since July 2006, which is mainly due to the improved trade relation with Neighboring countries Sudan and Djibouti. The seasonality of the export considerably varies across the different years with close similarity between 2007 and 2008 (Figure 9)

Dawit Alemu et. al

16

-

10,000.00

20,000.00

30,000.00

40,000.00

50,000.00

60,000.00

70,000.00

80,000.00

January

February

Marc

hA

prilM

ayJune

July

August

Septem

ber

Octo

ber

Novem

ber

Dec

ember

Year 2005

Year 2006

Year 2007

Year 2008

Figure 9 Seasonality of horse bean export in quintals (2005 – 2008)

The export of lentil has started to boom since August 2007 up until April 2008, when the export started to considerably declining. It does not show also any seasonality over the years (Figure 10).

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

35,000.00

40,000.00

January

February

Marc

hApril

May

June

July

August

Septem

ber

Oct

ober

Novem

ber

Decem

ber

Year 2005

Year 2006

Year 2007

Year 2008

Figure 10 Seasonality of lentil export in quintals (2005 – 2008)

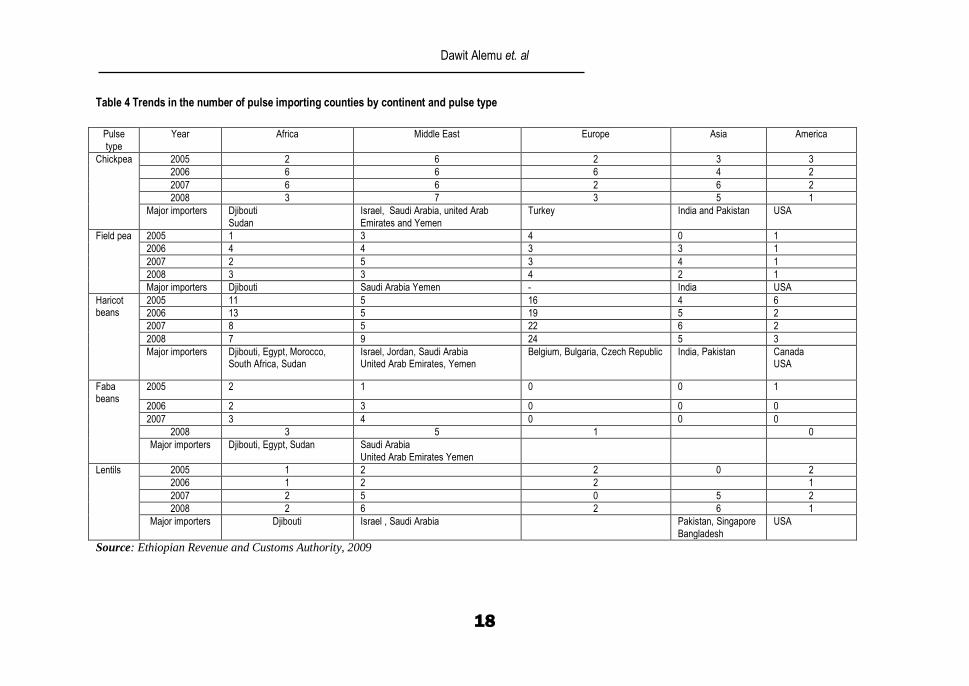

3.3.3 Destinations of pulse export

One of the characteristics of the export of pulse crops is the considerable variability of importing countries over the years with few permanently importing countries. For instance, Djibouti and Sudan from Africa, Israel, Saudi Arabia, United Arab Emirates and Yemen from the Middle East; Turkey from Europe, India and Pakistan from Asia; and USA from America have been

Challenges and opportunities of Ethiopian pulse export

17

importing chickpea each year since 2005(Table 4). Except horse beans, the other pulses are exported to all continents, showing the existence of demand all over the globe for these crops. Horse beans are mainly exported to neighboring Sudan and Djibouti and to the Saudi Arabia, United Arab Emirates, and Yemen in the Middle East. The variability of importing countries over the years implies the weak marketing linkage between Ethiopian exporters and foreign importers in respective countries, which can be characterized by ad hoc and temporary trade relationship.

Dawit Alemu et. al

18

Table 4 Trends in the number of pulse importing counties by continent and pulse type

Pulse

type

Year Africa Middle East Europe Asia America

Chickpea 2005 2 6 2 3 3

2006 6 6 6 4 2

2007 6 6 2 6 2

2008 3 7 3 5 1

Major importers Djibouti

Sudan

Israel, Saudi Arabia, united Arab

Emirates and Yemen

Turkey India and Pakistan USA

Field pea 2005 1 3 4 0 1

2006 4 4 3 3 1

2007 2 5 3 4 1

2008 3 3 4 2 1

Major importers Djibouti Saudi Arabia Yemen - India USA

Haricot beans

2005 11 5 16 4 6

2006 13 5 19 5 2

2007 8 5 22 6 2

2008 7 9 24 5 3

Major importers Djibouti, Egypt, Morocco, South Africa, Sudan

Israel, Jordan, Saudi Arabia United Arab Emirates, Yemen

Belgium, Bulgaria, Czech Republic India, Pakistan Canada USA

Faba beans

2005 2 1 0 0 1

2006 2 3 0 0 0

2007 3 4 0 0 0

2008 3 5 1 0

Major importers Djibouti, Egypt, Sudan

Saudi Arabia

United Arab Emirates Yemen

Lentils 2005 1 2 2 0 2

2006 1 2 2 1

2007 2 5 0 5 2

2008 2 6 2 6 1

Major importers Djibouti Israel , Saudi Arabia

Pakistan, Singapore

Bangladesh

USA

Source: Ethiopian Revenue and Customs Authority, 2009

Challenges and opportunities of Ethiopian pulse export

19

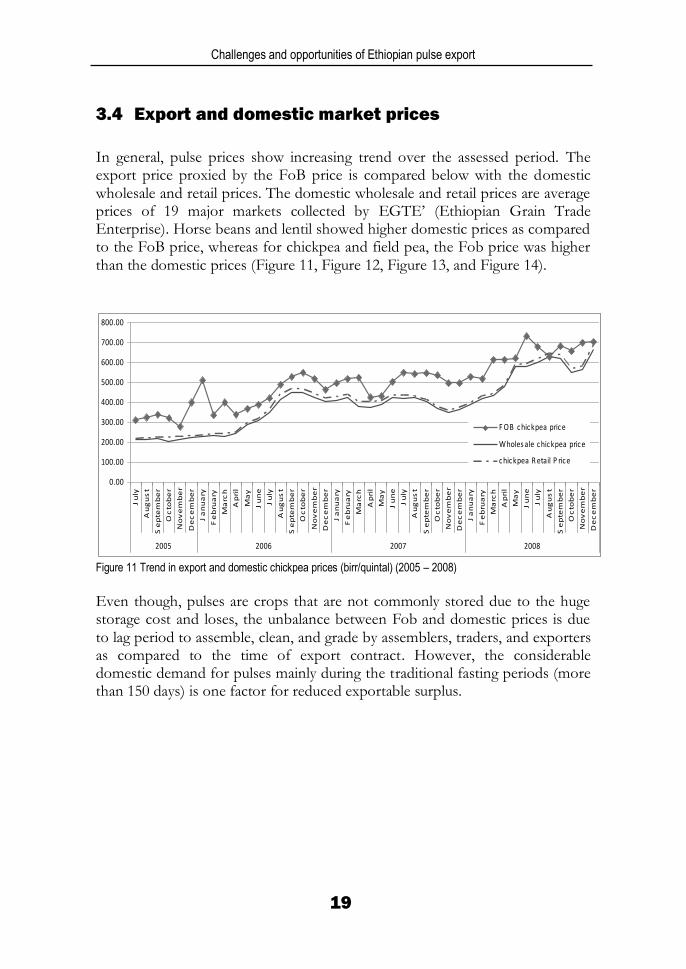

3.4 Export and domestic market prices

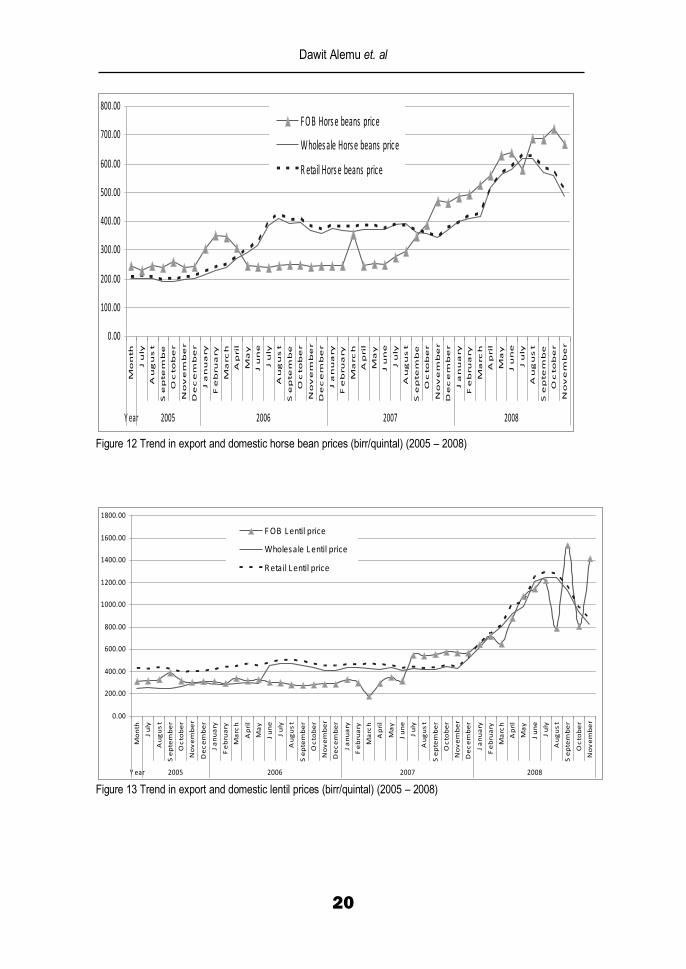

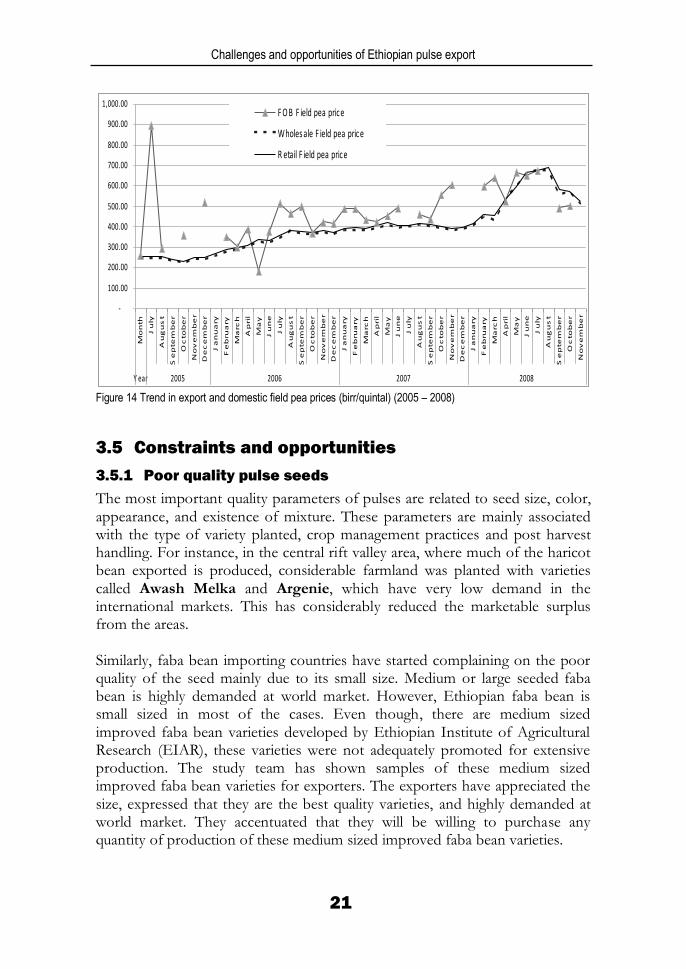

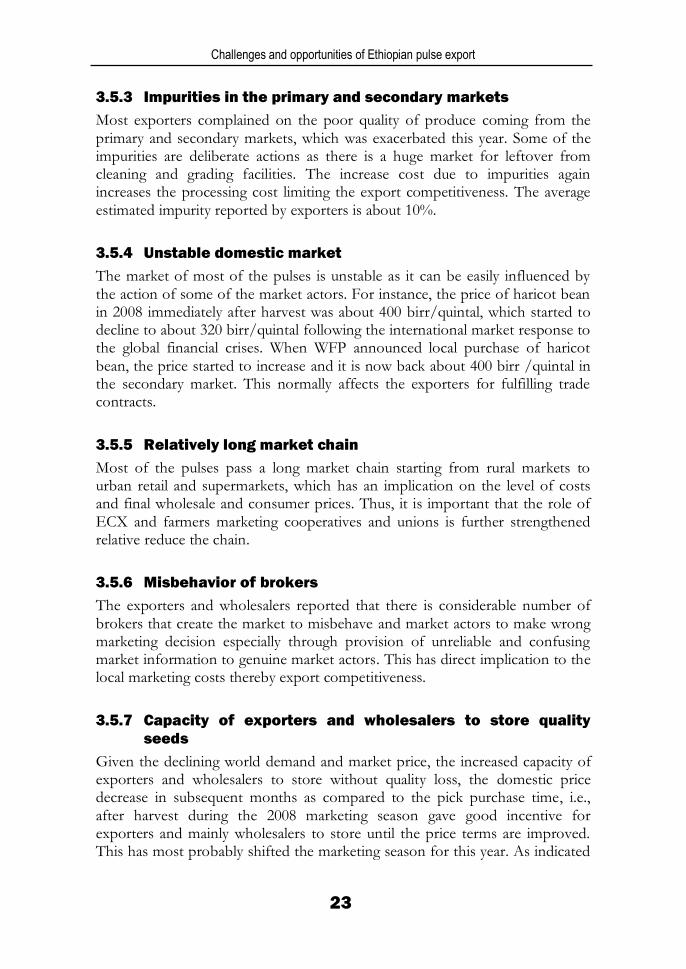

In general, pulse prices show increasing trend over the assessed period. The export price proxied by the FoB price is compared below with the domestic wholesale and retail prices. The domestic wholesale and retail prices are average prices of 19 major markets collected by EGTE’ (Ethiopian Grain Trade Enterprise). Horse beans and lentil showed higher domestic prices as compared to the FoB price, whereas for chickpea and field pea, the Fob price was higher than the domestic prices (Figure 11, Figure 12, Figure 13, and Figure 14).

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

2005 2006 2007 2008

F OB chickpea price

Wholes ale chickpea price

chickpea R etail P rice

Figure 11 Trend in export and domestic chickpea prices (birr/quintal) (2005 – 2008)

Even though, pulses are crops that are not commonly stored due to the huge storage cost and loses, the unbalance between Fob and domestic prices is due to lag period to assemble, clean, and grade by assemblers, traders, and exporters as compared to the time of export contract. However, the considerable domestic demand for pulses mainly during the traditional fasting periods (more than 150 days) is one factor for reduced exportable surplus.

Dawit Alemu et. al

20

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

Mo

nth

Ju

ly

Au

gu

st

Se

pte

mb

e

Oc

to

be

r

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rc

h

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

e

Oc

to

be

r

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rc

h

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

e

Oc

to

be

r

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rc

h

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

e

Oc

to

be

r

No

ve

mb

er

Y ear 2005 2006 2007 2008

F O B Hors e beans price

Wholes ale Hors e beans price

R etail Hors e beans price

Figure 12 Trend in export and domestic horse bean prices (birr/quintal) (2005 – 2008)

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

1400.00

1600.00

1800.00

Mo

nth

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

Y ear 2005 2006 2007 2008

F OB L entil price

Wholesale L entil price

R etail L entil price

Figure 13 Trend in export and domestic lentil prices (birr/quintal) (2005 – 2008)

Challenges and opportunities of Ethiopian pulse export

21

-

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

1,000.00

Mo

nth

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

De

ce

mb

er

Ja

nu

ary

Fe

bru

ary

Ma

rch

Ap

ril

Ma

y

Ju

ne

Ju

ly

Au

gu

st

Se

pte

mb

er

Oc

tob

er

No

ve

mb

er

Y ear 2005 2006 2007 2008

F O B F ield pea price

Wholes ale F ield pea price

R etail F ield pea price

Figure 14 Trend in export and domestic field pea prices (birr/quintal) (2005 – 2008)

3.5 Constraints and opportunities

3.5.1 Poor quality pulse seeds

The most important quality parameters of pulses are related to seed size, color, appearance, and existence of mixture. These parameters are mainly associated with the type of variety planted, crop management practices and post harvest handling. For instance, in the central rift valley area, where much of the haricot bean exported is produced, considerable farmland was planted with varieties called Awash Melka and Argenie, which have very low demand in the international markets. This has considerably reduced the marketable surplus from the areas. Similarly, faba bean importing countries have started complaining on the poor quality of the seed mainly due to its small size. Medium or large seeded faba bean is highly demanded at world market. However, Ethiopian faba bean is small sized in most of the cases. Even though, there are medium sized improved faba bean varieties developed by Ethiopian Institute of Agricultural Research (EIAR), these varieties were not adequately promoted for extensive production. The study team has shown samples of these medium sized improved faba bean varieties for exporters. The exporters have appreciated the size, expressed that they are the best quality varieties, and highly demanded at world market. They accentuated that they will be willing to purchase any quantity of production of these medium sized improved faba bean varieties.

Dawit Alemu et. al

22

The poor quality of locally marketed pulse seed forces exporters to invest in cleaning and grading of the purchased seed in most cases by hand picking, which considerably increases the cost. This in turn has direct implication on the price competitiveness of our export. Export of pulses to neighboring countries like Sudan and Djibouti has created disincentive for quality production as it used to be possible to export whatever quality grade pulses. These countries are reported to clean and grade for re-exporting to other countries where our exporters are also exporting. However, there are different varieties for the different pulse crops that are released by the national research system that fulfill the required quality parameters in the international markets. 3.5.2 Limited volume of domestic production and huge demand

Over the years, the international demand for most of the pulses has been very high with major constraint lay with exporters to get the contracted amount of pulse from the domestic market. For instance, there have been considerable number of offers for haricot bean to major exporters but the problem was getting the offered quantity and quality at the required time from the domestic supply. The main reasons can be categorized into huge domestic demand, relatively small areas of production, and domestic demand oriented production rather than international demand. Domestic demand: The huge domestic demand for pulses competes seriously with the export. In general, pulses are found as one of the components of the daily meal of every Ethiopian. In addition, they are considered as substitutes of animal products. Production area: As compared to cereals, the land allocated to pulses is relatively small at national level. The land allocated for haricot beans, which used to be the dominant exported pulse crop has been very small as compared to other pulses, which were not exported like faba bean, field peas, and lentil. In the 2008 production seasons, the total land allocated for these crops ranged from 107 thousand ha for lentil to 521 thousand ha for faba beans. If the export of pulses is into increase then area expansion is mandatory. Of course, the trend in production area shows considerable increase from year to year. Domestic demand oriented production: In line with the huge domestic

demand, most farmers opt to produce locally preferred varieties of pulses, without considering the international demand or the demand revealed by our exporters.

Challenges and opportunities of Ethiopian pulse export

23

3.5.3 Impurities in the primary and secondary markets

Most exporters complained on the poor quality of produce coming from the primary and secondary markets, which was exacerbated this year. Some of the impurities are deliberate actions as there is a huge market for leftover from cleaning and grading facilities. The increase cost due to impurities again increases the processing cost limiting the export competitiveness. The average estimated impurity reported by exporters is about 10%.

3.5.4 Unstable domestic market

The market of most of the pulses is unstable as it can be easily influenced by the action of some of the market actors. For instance, the price of haricot bean in 2008 immediately after harvest was about 400 birr/quintal, which started to decline to about 320 birr/quintal following the international market response to the global financial crises. When WFP announced local purchase of haricot bean, the price started to increase and it is now back about 400 birr /quintal in the secondary market. This normally affects the exporters for fulfilling trade contracts.

3.5.5 Relatively long market chain

Most of the pulses pass a long market chain starting from rural markets to urban retail and supermarkets, which has an implication on the level of costs and final wholesale and consumer prices. Thus, it is important that the role of ECX and farmers marketing cooperatives and unions is further strengthened relative reduce the chain.

3.5.6 Misbehavior of brokers

The exporters and wholesalers reported that there is considerable number of brokers that create the market to misbehave and market actors to make wrong marketing decision especially through provision of unreliable and confusing market information to genuine market actors. This has direct implication to the local marketing costs thereby export competitiveness.

3.5.7 Capacity of exporters and wholesalers to store quality

seeds

Given the declining world demand and market price, the increased capacity of exporters and wholesalers to store without quality loss, the domestic price decrease in subsequent months as compared to the pick purchase time, i.e., after harvest during the 2008 marketing season gave good incentive for exporters and mainly wholesalers to store until the price terms are improved. This has most probably shifted the marketing season for this year. As indicated

Dawit Alemu et. al

24

in the export seasonality analysis for the different pulse crops, there is no clear season for Ethiopian pulse export as the pick months when the different crops are exported varies from year to year. 3.5.8 Transportation cost

High cost of transportation either from production areas to Addis Ababa and from Addis Ababa to Port of Djibouti or border of Sudan has been reported to be one of the problems faced by exporters. This has contributed for the increment of marketing costs and eventually uncompetitive price at world market. Therefore, the exporters complained that transportation cost should have been reduced accordingly when the price of fuel reduces at world and local market. 3.5.9 Variability in destination markets

Destination countries for the different exported pulses vary considerably from year to year except very few countries like neighboring countries (Sudan and Djibouti) and Israel, Yemen and Saudi Arabia in the Middle East, which consistently import from Ethiopia. This implies that our export destination is not stable that exporters do not have relatively longer trade relationship with their respective importers. One reason for the variability is the use of third party (trading houses) for the export rather than direct trade linkage with importing countries. 3.5.10 Decline of demand in importing countries

Following the financial crises in developed countries and the subsequent economic impact on their respective economies, overall international demand for agricultural commodities as it is for other industrial products had declined considerably. Most of the exporters have reported that they have faced a considerable reduction in demand. For instance, some countries, which used to be common importers of faba bean, such as Pakistan, declined to import faba bean from Ethiopia mainly due to inability to get adequate foreign currency. The other instance of decline is start of production of pulses by our importing countries. For instance, the largest importer of Ethiopian faba bean is Sudan, which has started producing itself and Since September 2008, the export of faba bean to Sudan has unusually declined. Similarly, Canada, China, and Argentina are becoming international actors in the marketing of haricot beans as they have started producing themselves.

Challenges and opportunities of Ethiopian pulse export

25

4 Conclusion and

Recommendations The increased trend in the production of pulses due to productivity improvement and area expansion; the emergence of new pulse crops for export; improvement in the storage, cleaning, and grading capacity of exporters and wholesalers; and the existing favorable public support for export have supported the increase of export over the years. However, the export performance in the last quarter of 2008 and in the first quarter of 2009 has shown a declining trend. The major reasons of this trend are related to international demand decline, poor seed quality of local production, huge domestic demand, and unstable domestic market. In order to overcome the stated constraints the following issues require urgent attention.

Improving access and use of improved varieties of pulses that have international demand is essential. This need to be augmented with promotion of farmers’ access to pulse markets with premium price for quality;

The existing domestic market for impurities (by-products from cleaning and grading activities) need to be regulated as this is increasing the cost of cleaning and grading for exporters, which in tern is reducing their competitiveness;

Promotion of availability of market information, which enable all market actors to make right market decision and to reduce the impact of misbehaving brokers;

Transportation costs either from production areas to Addis Ababa and from Addis Ababa to Port of Djibouti or border of Sudan are found to be high limiting the competitiveness our export even, when there is a price adjustment of fuel, the transportation costs do not respond. Thus, there is a need to regulate the transportation costs;

Ethiopian pulses do not have mainstream international markets as the destination markets vary from yearly. Similarly, competitors in the international markets vary from year to year. Thus, it is important that public international market intelligence along with increasing the capacity of our exporters in market intelligence is promoted. This can also be facilitated through Ethiopian Embassies located in several parts of the world. The exporters have expressed interests to participate in trade fairs, exhibitions and several other similar business related platforms to demonstrate their products. The embassies can trace such events and inform the exporters for possible participation; and

To address the impact of this year’s reduction in international demand there is a need for short-term solution, which should be sought with joint effort of the public with relevant market actors and the Ethiopian Pulses, Oilseeds and Spices Processors and Exporters’ Association (EPOSPEA).

Dawit Alemu et. al

26

5 References

Dawit Alemu and Demelash Seifu. 2003. Haricot bean marketing and export performance:

constraints and opportunities. Research Report No 54. Ethiopian Agricultural Research

Organization (EARO).

Bekele Shiferaw and Hailemariam Teklewold. 2007. Structure and functioning of chickpea

markets in Ethiopia.: evidence based on value chains linking smallholders and markets.

Improving productivity and Market access (IPMS) of Ethiopian Farmers Project.

Working paper 6. ILRI (International Livestock Research Institute), Nairobi, Kenya.

63pp.

Shiferaw B., Jones R., Silim S, Tekelewold H, and Gwata E. 2007. Analysis of production

costs, market opportunities and competitiveness of Desi and Kabuli Chickpeas in

Ethiopia. Improving productivity and Market access (IPMS) of Ethiopian Farmers

Project. Working paper 3. ILRI (International Livestock Research Institute), Nairobi, Kenya. 48pp.

Ferris S and Kaganzi E. 2008. Evaluating marketing opportunities for haricot beans in

Ethiopia. Improving productivity and Market access (IPMS) of Ethiopian Farmers

Project. Working paper 7. ILRI (International Livestock Research Institute), Nairobi,

Kenya. 48pp.

EARO. 2002. Crops Research Strategy. Ethiopian Agricultural Research Organization.

Addis Ababa Ethiopia.

CSA. 2008. Area and production of crops (private peasant holdings, meher season)

Agricultural Sample Survey 2007 / 2008 (2000 E.C.) (September – December 2007)

VOLUME I