SUPPLY AND DEMAND SIDE DAN CIURIAK...

56

Trade and development discussion paper no. 02/2010 SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS – POLICY OPTIONS DAN CIURIAK Munich, August 2010 bkp DEVELOPMENT RESEARCH & CONSULTING

-

Upload

dangkhuong -

Category

Documents

-

view

215 -

download

0

Transcript of SUPPLY AND DEMAND SIDE DAN CIURIAK...

Trade and development discussion paper no. 02/2010

SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR

ETHIOPIAN EXPORTS – POLICY OPTIONS

DAN CIURIAK

Munich, August 2010

bkp DEVELOPMENT RESEARCH & CONSULTING

Author: Dan Ciuriak. Email: [email protected] Copyright rests with the author. One of the founding principles of BKP Development Research and Consulting is to bridge the gap which all too often exists between development research and politics. The purpose of BKP Trade and Development Discussion Papers is to provide policy relevant insights which are based on thorough study, and to stimulate discussion about policies and strategies for development. The content of this discussion paper is the sole responsibility of the author and can in no way be taken to reflect the views of BKP Development Research & Consulting. BKP DEVELOPMENT RESEARCH & CONSULTING GMBH ROMANSTRASSE 74. 80639 MUNICH. GERMANY PHONE +49-89-1787 6047. FAX +49-89-1787 6049 E-MAIL [email protected]

Further information and other discussion papers can be obtained from: WWW.BKP-DEVELOPMENT.DE

TDDP 02/2010 PAGE i

Supply and Demand Side Constraints as Barriers for Ethiopian Exports – Policy Options1

DAN CIURIAK ABSTRACT This study seeks to identify and estimate the relative importance of supply- versus demand-side constraints on Ethiopia’s exports. Ethiopia has tried radically different trade strategies in the past, including a strategy of import replacement/protection for infant industries during the Imperial period, a heavily state-managed trading system during the military government era, and a market-oriented liberalized approach supported by the international financial institutions in the most recent period. It is presently engaged in various trade initiatives, including accession to the World Trade Organization, negotiations with the European Union on an Economic Partnership Agreement and with African regional partners towards a Tripartite Free Trade Area (TFTA). The study finds that the constraints on Ethiopia’s trade performance are mainly domestic, secondarily in its neighbourhood, and thirdly in its trade with African partners more generally. Ethiopia’s macroeconomic policy mix and high administrative costs of trade work both to depress the share of trade in economic activity and to widen the deficit on goods trade. At the same time, the high costs of firm formation and the high margins and concentrated market structure of producer services, both a function of domestic policy frameworks, help to explain the evidently under-developed state of Ethiopia’s private sector; unless addressed, this would limit the supply side response to trade liberalization. Optimistically, the paper argues that eminently achievable infrastructure and regional customs cooperation developments, in conjunction with domestic administrative process reforms, would be “game changers” for Ethiopia in terms of its trade performance and industrial development.

Ethiopia, exports, liberalization, trade costs, firm-level dynamics Keywords:

JEL Codes:

1 This is a revised version of a paper prepared for the Fifth Annual National Private Sector Development

Conference: Strengthening the Role of the Private Sector in International Trade Negotiations, Addis Ababa, 22 2010.

F13, F14, F15

TDDP 02/2010 PAGE iii

TABLE OF CONTENTS

1 INTRODUCTION .................................................................................................. 1

2 EVALUATING CONSTRAINTS TO ETHIOPIA’S EXPORTS .................................... 3

2.1 Constraints on Ethiopia’s exports are largely domestic and local .......... 3

2.2 Ethiopia’s trade imbalance: the policy mix as an export constraint ....... 5

2.3 Trade costs as a constraint on exports .....................................................9

2.4 Private Sector Under-Development as an Export Constraint ................ 15

2.5 Domestic producer service margins as an export constraint ................. 19

2.6 Thick borders as an export constraint .................................................... 20

2.7 Tariff Barriers Maintained by Ethiopia’s Regional Trading Partners: some “back of the envelope” quantitative assessments ....... 22

3 ADDRESSING SUPPLY-SIDE CONSTRAINTS TO ETHIOPIA’S EXPORTS ................ 25

3.1 The macroeconomic policy mix ............................................................... 25

3.2 Trade costs ............................................................................................... 26

3.3 Private Sector Development ................................................................... 26

3.4 Regional Trade Negotiations .................................................................. 27

3.5 Towards A Private-Public Partnership on the Trade Agenda ................ 27

4 CONCLUDING REMARKS ................................................................................... 28

REFERENCES .............................................................................................................. 29

APPENDIX 1: EAST AND SOUTH AFRICAN REGIONAL TRADE LIBERALIZATION ............................................................................................... 32

APPENDIX 2: CALIBRATING EXPECTED RELATIVE LEVELS OF TRADE ....................46

TDDP 02/2010 PAGE 1

1 INTRODUCTION Ethiopia has tried radically different trade strategies in the past, including a strategy of import replacement/protection for infant industries during the Imperial period, a heavily state-managed trading system during the military government era, and a market-oriented liberalized approach supported by the international financial institutions in the most recent period. Each of these trade regimes incorporated the policy objective of diversifying Ethiopia’s export palette to reduce dependence on coffee and other cash crops. Numerous trade-related technical assistance projects have already been implemented. Policies promoting exports have been adopted. However, Ethiopia finds itself in 2010 with an export palette of limited diversification and, notwithstanding rapid growth in exports, a steeply widening trade deficit, leaving it dependent on inflows of financial assistance to pay its import bill. In this context, Ethiopia is engaged in various trade initiatives: Negotiations towards trade agreements with regional partners, including regarding the

establishment of a Tripartite Free Trade Area (TFTA) comprising the members of the Common Market of Eastern and Southern Africa (COMESA), the East African Community (EAC) and the Southern African Development Community (SADC);

Negotiations with extra-regional partners, in particular the prospective Economic Partnership Agreement with the European Union; and

Accession to the World Trade Organization. It is salient and timely therefore to assess the relative importance of demand-side constraints on Ethiopia’s exports, some of which can be reduced through trade negotiations, versus supply-side constraints which require supportive domestic policies. In recent years, analysis of international trade has focused increasingly on firm-level dynamics. The new empirical literature shows that underlying the aggregate trends in exports and imports is a dynamic process of firms entering and exiting foreign markets, introducing new export products and dropping obsolete products, and diversifying across markets. Overall growth in a country’s exports depends importantly on the number of new entrants exceeding the number of established exporters being pushed out of export markets, and the number of new product introductions more than offsetting the number of old products losing markets. The new empirical literature also focuses on the costs of entering new markets and how reduction of these costs can generate trade in new products and markets where previously there was no trade. The focus has shifted from the country to the firm, from the static to the dynamic, and from the macroeconomic to the microeconomic underpinnings of trade.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 2

This paper seeks to bring this perspective to the analysis of Ethiopia’s trade performance and policies. It argues that a successful Ethiopian trade strategy must be conceived in a dynamic, longer-term framework which involves the ability to sustain: A flow of competitive industrial products gaining access to export markets to augment the

export palette and replace obsolete/uncompetitive products that lose their international market niche.

A flow of export market entrants, including firms newly establishing their first export market presence and existing exporters diversifying the destinations for their products, augmenting the population of exporting firms and replacing firms exiting export markets.

Improvements in physical infrastructure and logistical capacity to efficiently move goods and services to markets abroad, including transport and information & telecommunications (ICT) capabilities, in order to lower trade costs and thus to expand the number of firms that can enter foreign markets.

Institutional support to help firms surmount the manifold difficulties of entering foreign markets by reducing the up-front sunk costs of such entry, and creating as stable a trading environment as possible to minimize the frictional costs of failed export market entry.

The paper is organized in two parts. The first part evaluates constraints to Ethiopia’s trade. It addresses in turn: the relative importance of the major sources of constraints; the trade effects of Ethiopia’s macroeconomic policy mix; the major role of domestic administrative costs of importing and exporting as a determinant of Ethiopia’s trade performance and industrial development; the under-development of the private sector in the context of high costs of domestic market entry as a factor weakening the dynamics of export market entry; market structure issues and associated high producer services costs as an export constraint; the issue of “missing trade” with neighboring countries due to lacking physical infrastructure and inefficient border arrangements; and finally the traditional constraint on trade, namely tariff protection maintained by Ethiopia’s regional trading partners. The second part suggests how Ethiopia’s trading community might, in light of the foregoing evaluation of trade barriers, approach the complex tax of progressively dismantling them, in terms of both substance and process, including the important issue of sequencing. The details of the quantitative analysis reported in the main body of the paper are set out and discussed in Appendixes 1 and 2. In brief summary, the paper finds that the major constraints to Ethiopia’s trade performance are mainly domestic, secondarily in its neighborhood and thirdly in its trade with African partners more generally. Ethiopia’s macroeconomic policy mix and high administrative costs of trade work both to depress the share of trade in economic activity and to widen the deficit on goods trade. At the same time, the high costs of firm formation and the high margins and concentrated market structure of producer services, both a function of domestic policy frameworks, help to explain the evidently under-developed state of Ethiopia’s private sector; unless addressed, this would be a major factor in constraining the supply side response to trade liberalization. Optimistically, the paper argues that several eminently achievable infrastructure and regional cooperation developments, in conjunction with domestic administrative process reforms, would be “game changers” for Ethiopia in terms of its trade performance and industrial development.

TDDP 02/2010 PAGE 3

Given these domestic macroeconomic and microeconomic policies, Ethiopia would stand to benefit from regional trade liberalization; absent these policy reforms, Ethiopia would experience minor negative impacts on measurable factors and would be counting on non-measurable elements to realize benefits from trade liberalization. One way or the other, the paper argues that it is “safe to go in the water” for Ethiopia in respect of participation in the TFTA. It also recommends an exporter dialogue on the macroeconomic policy mix and suggests criteria for an export-friendly policy mix, and continued microeconomic framework reforms.

2 EVALUATING CONSTRAINTS TO ETHIOPIA’S EXPORTS This section identifies and evaluates the relative importance of supply-side constraints facing Ethiopian exports. The focus is on merchandise exports. However, it is to be noted that, in 2008, services exports—mainly transportation services (principally Ethiopian Airlines and Ethiopian Shipping Lines), tourism, communications, and insurance and financial services—totaled about US$1.8 billion compared to goods exports of $1.6 billion2

.

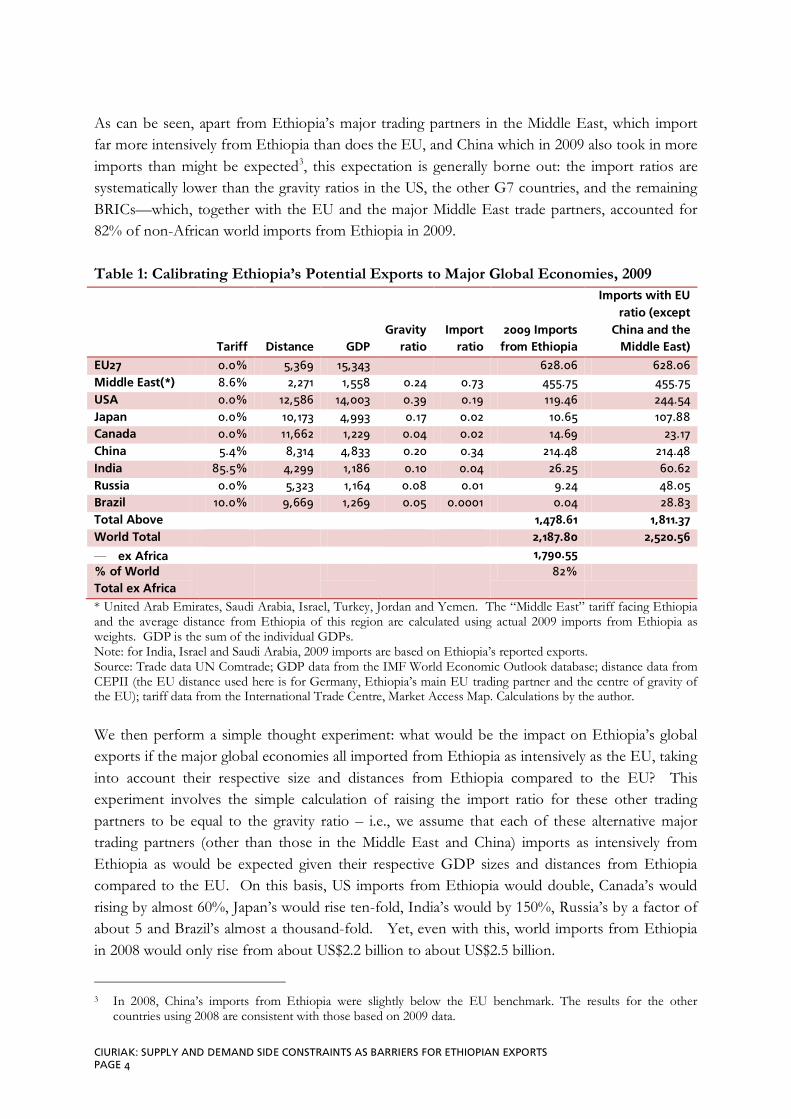

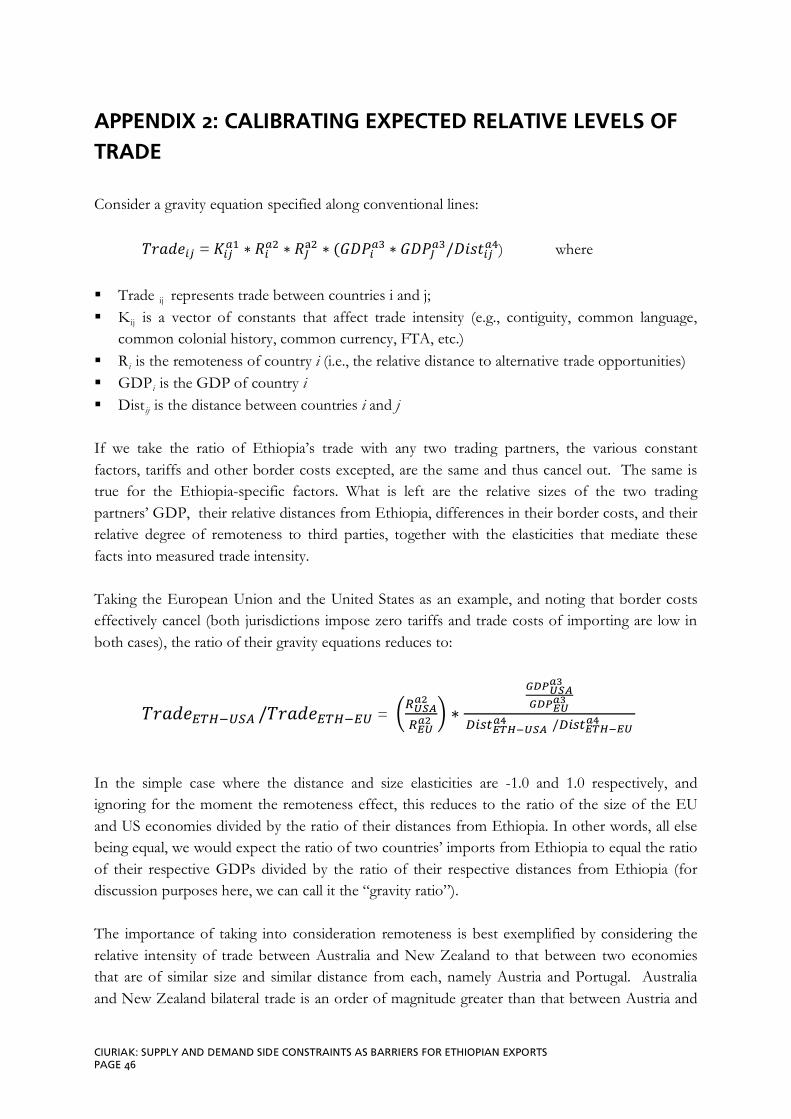

2.1 Constraints on Ethiopia’s exports are largely domestic and local In 2009, Ethiopia had worldwide goods exports of US$ 2.2 billion and worldwide goods imports of US$ 10.9 billion, for a goods trade deficit of US$ 8.7 billion. To what extent is the low level of exports plausibly to be attributed to demand-side constraints and where might these constraints principally be located? To answer these questions, we draw on the basic principles of the gravity model of trade which holds that the intensity of bilateral trade with individual trading partners increases with the size of the trading partner’s economy and decreases the further away that trading partner is. As elaborated in Appendix 2, all else being equal, we would expect the ratio of two countries’ imports from Ethiopia to be approximately equal to the ratio of their respective GDPs divided by the ratio of their respective distances from Ethiopia. Since the European Union (EU) provides Ethiopia with tariff-free access, and compared to the other major global economies has fewer alternative trading opportunities with economies similar to Ethiopia, we would expect the ratio of most countries’ imports from Ethiopia to EU imports from Ethiopia (the “Import ratio” in Table 1) to be somewhat smaller than their “Gravity ratio” (the ratios of their respective GDPs, divided by the ratios of their respective distances from Ethiopia).

2 Source: calculated by the author based on an estimated ratio of goods and services exports to GDP of 13.2

percent (DFAT, 2010) and the reported level of exports of goods from UN Comtrade. Note that data from the most recent IMF Article IV consultations, reported on a fiscal year basis, suggest a level of exports of non-factor services of about US$ 1.7 billion in calendar year 2008 compared to goods exports of about US$ 1.5 billion (International Monetary Fund 2009: Table 5(a) at p. 22). For a discussion of growth in Ethiopia’s services trade see Access Capital (2010).

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 4

As can be seen, apart from Ethiopia’s major trading partners in the Middle East, which import far more intensively from Ethiopia than does the EU, and China which in 2009 also took in more imports than might be expected3

, this expectation is generally borne out: the import ratios are systematically lower than the gravity ratios in the US, the other G7 countries, and the remaining BRICs—which, together with the EU and the major Middle East trade partners, accounted for 82% of non-African world imports from Ethiopia in 2009.

Table 1: Calibrating Ethiopia’s Potential Exports to Major Global Economies, 2009

Tariff Distance GDP Gravity

ratio Import

ratio 2009 Imports

from Ethiopia

Imports with EU ratio (except

China and the Middle East)

EU27 0.0% 5,369 15,343 628.06 628.06 Middle East(*) 8.6% 2,271 1,558 0.24 0.73 455.75 455.75 USA 0.0% 12,586 14,003 0.39 0.19 119.46 244.54 Japan 0.0% 10,173 4,993 0.17 0.02 10.65 107.88 Canada 0.0% 11,662 1,229 0.04 0.02 14.69 23.17 China 5.4% 8,314 4,833 0.20 0.34 214.48 214.48 India 85.5% 4,299 1,186 0.10 0.04 26.25 60.62 Russia 0.0% 5,323 1,164 0.08 0.01 9.24 48.05 Brazil 10.0% 9,669 1,269 0.05 0.0001 0.04 28.83 Total Above 1,478.61 1,811.37 World Total 2,187.80 2,520.56

— ex Africa 1,790.55 % of World Total ex Africa

82%

* United Arab Emirates, Saudi Arabia, Israel, Turkey, Jordan and Yemen. The “Middle East” tariff facing Ethiopia and the average distance from Ethiopia of this region are calculated using actual 2009 imports from Ethiopia as weights. GDP is the sum of the individual GDPs. Note: for India, Israel and Saudi Arabia, 2009 imports are based on Ethiopia’s reported exports. Source: Trade data UN Comtrade; GDP data from the IMF World Economic Outlook database; distance data from CEPII (the EU distance used here is for Germany, Ethiopia’s main EU trading partner and the centre of gravity of the EU); tariff data from the International Trade Centre, Market Access Map. Calculations by the author. We then perform a simple thought experiment: what would be the impact on Ethiopia’s global exports if the major global economies all imported from Ethiopia as intensively as the EU, taking into account their respective size and distances from Ethiopia compared to the EU? This experiment involves the simple calculation of raising the import ratio for these other trading partners to be equal to the gravity ratio – i.e., we assume that each of these alternative major trading partners (other than those in the Middle East and China) imports as intensively from Ethiopia as would be expected given their respective GDP sizes and distances from Ethiopia compared to the EU. On this basis, US imports from Ethiopia would double, Canada’s would rising by almost 60%, Japan’s would rise ten-fold, India’s would by 150%, Russia’s by a factor of about 5 and Brazil’s almost a thousand-fold. Yet, even with this, world imports from Ethiopia in 2008 would only rise from about US$2.2 billion to about US$2.5 billion.

3 In 2008, China’s imports from Ethiopia were slightly below the EU benchmark. The results for the other

countries using 2008 are consistent with those based on 2009 data.

TDDP 02/2010 PAGE 5

Accordingly, we can safely conclude that main demand- and supply-side constraints on Ethiopia’s export performance lie not in global markets but in Ethiopia itself or in its local neighborhood—Africa.

2.2 Ethiopia’s trade imbalance: the policy mix as an export constraint

We next consider the implications of Ethiopia’s overall trade deficit. Trade deficits are not necessarily a policy “problem” in the sense that they require policy adjustments. In some cases, deficits may simply indicate a stronger growth performance in the deficit country than in its major trading partners. In a similar vein, they may reflect transient adverse terms-of-trade developments if prices for major export commodities fall while those for important imports rise. Such cyclical/transient deficits should however self-correct over the course of the business cycle. Deficits may also reflect an excess of investment opportunities that domestic savings cannot finance, resulting in net capital inflows and a mirror current account deficit. A rapidly growing developing country with strong domestic capital formation would, in the normal case, be in current account deficit, which in turn would largely consist of a goods trade deficit. Further, trade deficits are not necessarily indicative of a trade policy problem or by the same token a problem that can be solved by trade policy instruments alone. In general, high import taxes or barriers also act indirectly as a tax on exports; the net result is a lower trade share of GDP but there is no definitive implication for the balance of trade. The external balance is, in the long run, decided by other factors. However, in the highly important medium term, a country’s policy mix can contribute to an external deficit by, in effect, taxing exports. For example, the use of the exchange rate as an external anchor for monetary policy can lead to an increase in the real effective exchange rate and widen trade deficits in a medium-term context. For a country like Ethiopia, which is counting on an export-led development strategy, getting the policy mix right is thus very important. While an in-depth assessment of Ethiopia’s macroeconomic policy framework is well beyond the scope of the present paper, it is important to note that the macroeconomic policy framework in place during the 2000s did work to constrain Ethiopia’s exports. Ethiopia’s overall economic strategy was premised on rapid growth supported by significant increases in development assistance4

4 See the Sustainable Development and Poverty Reduction Program (SDPRP) prepared in 2002.

. An IMF study which examined the feasibility of Ethiopia’s plan noted that channeling part of the expected increase in domestic demand abroad through increased imports would serve to contain the potential wage and price pressures under this strategy; indeed, the study projected a significant widening in the external deficit (excluding official development assistance) from

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 6

about 13 percent of GDP in 2003 to 21 percent by 2015 (Andrews et al. 2005). The possibility of a real exchange rate appreciation under Ethiopia’s tightly managed floating exchange rate regime that could undermine export competitiveness was explicitly addressed and acknowledged as a risk (Andrews et al. 2005). While the risks entailed by this strategy were avoided by Ethiopia in the first half of the 2000s (aided by the fact that the US dollar, to which the birr was effectively pegged, depreciated globally during this period), they was actuated in the latter part of the 2000s as Ethiopian inflation accelerated and exchange rate management focused on containing inflationary pressures. The National Bank of Ethiopia acknowledged in its annual reports that “the continuous real appreciation of the Birr is likely to affect the competitiveness of the country’s exports” (National Bank of Ethiopia 2008), and noted its efforts to mitigate the problem while nonetheless grappling with the inflationary pressures. However, as clearly reflected in Ethiopia’s discussions concerning its policy mix with the IMF, the disinflationary policy goals were given precedence over those of export competitiveness in exchange rate management:

“The authorities agreed with staff that the exchange rate was overvalued at its June 2009 level; they viewed a real level closer to that observed in 2007 as being broadly appropriate from a medium-term perspective. Price competitiveness needed to be improved, but they argued that this could be achieved only gradually: they ruled out rapid adjustment via large step devaluation on the grounds that it would revive inflation, only recently brought under control. They saw a step adjustment on the scale of that implemented on July 10th as an important move towards correcting overvaluation. They underscored their commitment to achieving, over the medium-term, an appropriate level for the real exchange rate and would not hesitate to adjust the nominal exchange rate for this purpose, if needed. Staff emphasized the overarching importance of boosting Ethiopia’s production of tradable goods and services, arguing that some further real exchange depreciation would likely be needed over time to achieve this objective.” (International Monetary Fund 2009: 9)

Several issues are raised by the above considerations: 1. The mix of interest rate and other domestic monetary management tools versus the exchange

rate to achieve price stability. 2. The level of the exchange rate considered to be appropriate in the medium-term (i.e., was the

level in 2007 about right?). 3. The choice of exchange rate regime to minimize real exchange rate fluctuations. As regards the mix of instruments used for domestic price stability, it is useful to consider the issue in terms of the monetary conditions index, which expresses a given degree of monetary tightness as a weighted average of movements in interest rates and in exchange rates according to their estimated effects on aggregate demand5

5 For an example of the application of the monetary conditions index to the analysis of macroeconomic

imbalances, in this case those of Japan in the mid-1990s, see Figure 4.6: Monetary Conditions (MCI) in International Monetary Fund (1998: 113).

. In the 2000s, Ethiopia essentially combined a highly expansionary domestic interest rate policy, which in fact resulted in negative real interest rates, with a real appreciation of the birr to try and contain the resulting inflation. This policy mix tends to induce substitution of capital for labor in production and to substitute imports for domestic production while restraining exports and reducing savings. The opposite mix—higher interest rates and a lower exchange rate—induces substitution of labor for capital and domestic

TDDP 02/2010 PAGE 7

production for imports, while encouraging exports and domestic savings6. Certainly from Ethiopia’s export perspective, the latter mix is preferable; arguably, it is also preferable from other policy perspectives as well since it favors more intensive use of Ethiopia’s abundant factor of production, labor, an important consideration as Ethiopia seeks to commercialize its agricultural sector, which in turn raises the issue of finding employment for surplus labor in the rural sector7

; and it encourages domestic savings, a vital issue for sustaining growth in the longer run.

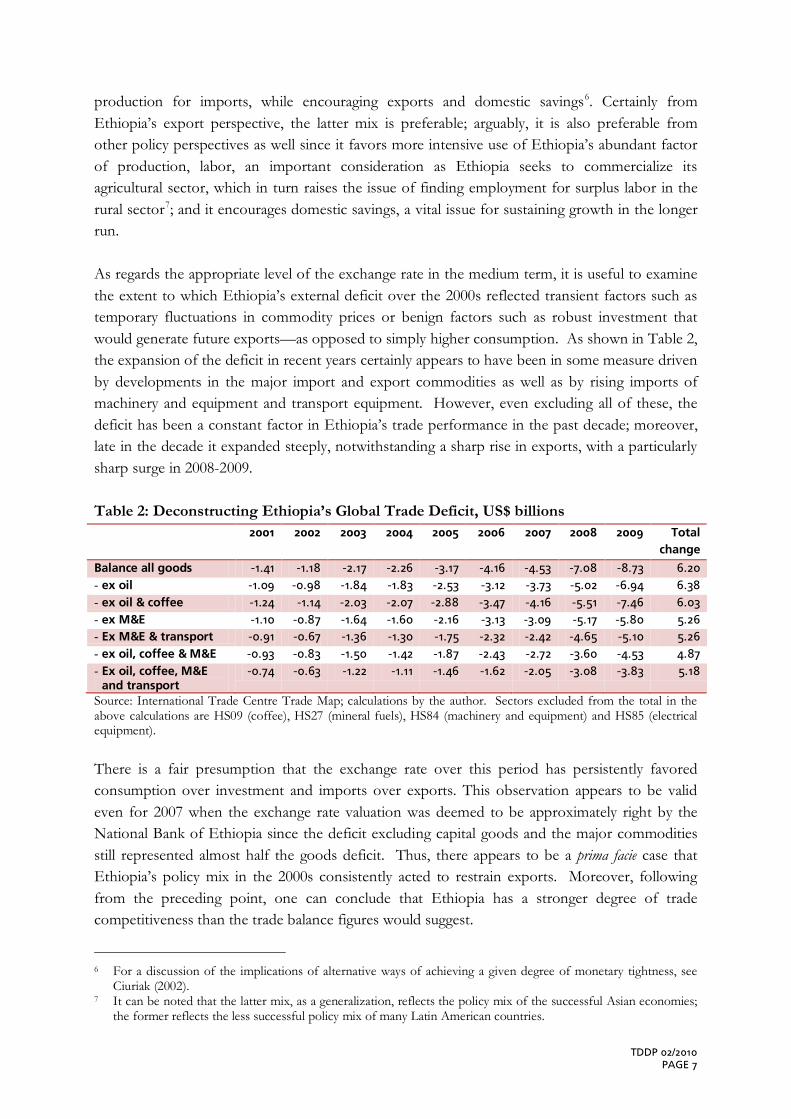

As regards the appropriate level of the exchange rate in the medium term, it is useful to examine the extent to which Ethiopia’s external deficit over the 2000s reflected transient factors such as temporary fluctuations in commodity prices or benign factors such as robust investment that would generate future exports—as opposed to simply higher consumption. As shown in Table 2, the expansion of the deficit in recent years certainly appears to have been in some measure driven by developments in the major import and export commodities as well as by rising imports of machinery and equipment and transport equipment. However, even excluding all of these, the deficit has been a constant factor in Ethiopia’s trade performance in the past decade; moreover, late in the decade it expanded steeply, notwithstanding a sharp rise in exports, with a particularly sharp surge in 2008-2009. Table 2: Deconstructing Ethiopia’s Global Trade Deficit, US$ billions 2001 2002 2003 2004 2005 2006 2007 2008 2009 Total

change

Balance all goods -1.41 -1.18 -2.17 -2.26 -3.17 -4.16 -4.53 -7.08 -8.73 6.20 - ex oil -1.09 -0.98 -1.84 -1.83 -2.53 -3.12 -3.73 -5.02 -6.94 6.38 - ex oil & coffee -1.24 -1.14 -2.03 -2.07 -2.88 -3.47 -4.16 -5.51 -7.46 6.03 - ex M&E -1.10 -0.87 -1.64 -1.60 -2.16 -3.13 -3.09 -5.17 -5.80 5.26 - Ex M&E & transport -0.91 -0.67 -1.36 -1.30 -1.75 -2.32 -2.42 -4.65 -5.10 5.26 - ex oil, coffee & M&E -0.93 -0.83 -1.50 -1.42 -1.87 -2.43 -2.72 -3.60 -4.53 4.87 - Ex oil, coffee, M&E

and transport -0.74 -0.63 -1.22 -1.11 -1.46 -1.62 -2.05 -3.08 -3.83 5.18

Source: International Trade Centre Trade Map; calculations by the author. Sectors excluded from the total in the above calculations are HS09 (coffee), HS27 (mineral fuels), HS84 (machinery and equipment) and HS85 (electrical equipment). There is a fair presumption that the exchange rate over this period has persistently favored consumption over investment and imports over exports. This observation appears to be valid even for 2007 when the exchange rate valuation was deemed to be approximately right by the National Bank of Ethiopia since the deficit excluding capital goods and the major commodities still represented almost half the goods deficit. Thus, there appears to be a prima facie case that Ethiopia’s policy mix in the 2000s consistently acted to restrain exports. Moreover, following from the preceding point, one can conclude that Ethiopia has a stronger degree of trade competitiveness than the trade balance figures would suggest.

6 For a discussion of the implications of alternative ways of achieving a given degree of monetary tightness, see

Ciuriak (2002). 7 It can be noted that the latter mix, as a generalization, reflects the policy mix of the successful Asian economies;

the former reflects the less successful policy mix of many Latin American countries.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 8

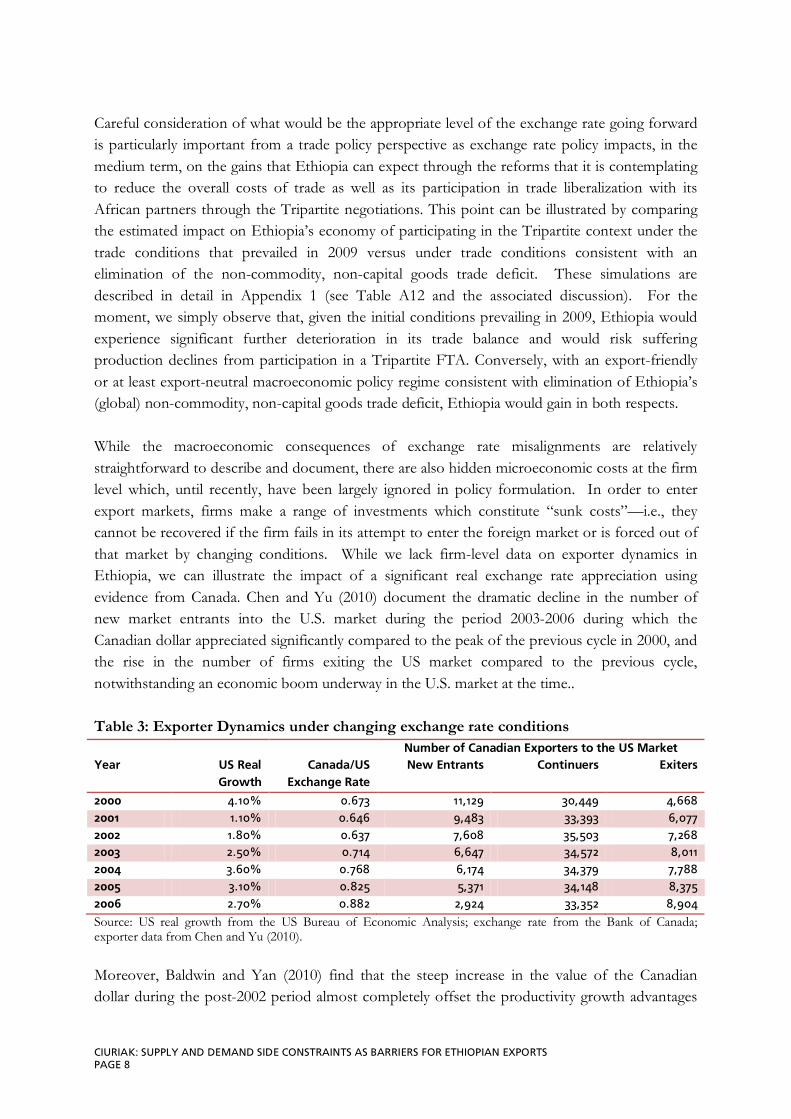

Careful consideration of what would be the appropriate level of the exchange rate going forward is particularly important from a trade policy perspective as exchange rate policy impacts, in the medium term, on the gains that Ethiopia can expect through the reforms that it is contemplating to reduce the overall costs of trade as well as its participation in trade liberalization with its African partners through the Tripartite negotiations. This point can be illustrated by comparing the estimated impact on Ethiopia’s economy of participating in the Tripartite context under the trade conditions that prevailed in 2009 versus under trade conditions consistent with an elimination of the non-commodity, non-capital goods trade deficit. These simulations are described in detail in Appendix 1 (see Table A12 and the associated discussion). For the moment, we simply observe that, given the initial conditions prevailing in 2009, Ethiopia would experience significant further deterioration in its trade balance and would risk suffering production declines from participation in a Tripartite FTA. Conversely, with an export-friendly or at least export-neutral macroeconomic policy regime consistent with elimination of Ethiopia’s (global) non-commodity, non-capital goods trade deficit, Ethiopia would gain in both respects. While the macroeconomic consequences of exchange rate misalignments are relatively straightforward to describe and document, there are also hidden microeconomic costs at the firm level which, until recently, have been largely ignored in policy formulation. In order to enter export markets, firms make a range of investments which constitute “sunk costs”—i.e., they cannot be recovered if the firm fails in its attempt to enter the foreign market or is forced out of that market by changing conditions. While we lack firm-level data on exporter dynamics in Ethiopia, we can illustrate the impact of a significant real exchange rate appreciation using evidence from Canada. Chen and Yu (2010) document the dramatic decline in the number of new market entrants into the U.S. market during the period 2003-2006 during which the Canadian dollar appreciated significantly compared to the peak of the previous cycle in 2000, and the rise in the number of firms exiting the US market compared to the previous cycle, notwithstanding an economic boom underway in the U.S. market at the time.. Table 3: Exporter Dynamics under changing exchange rate conditions Number of Canadian Exporters to the US Market Year US Real

Growth Canada/US

Exchange Rate New Entrants Continuers Exiters

2000 4.10% 0.673 11,129 30,449 4,668 2001 1.10% 0.646 9,483 33,393 6,077 2002 1.80% 0.637 7,608 35,503 7,268 2003 2.50% 0.714 6,647 34,572 8,011 2004 3.60% 0.768 6,174 34,379 7,788 2005 3.10% 0.825 5,371 34,148 8,375 2006 2.70% 0.882 2,924 33,352 8,904 Source: US real growth from the US Bureau of Economic Analysis; exchange rate from the Bank of Canada; exporter data from Chen and Yu (2010). Moreover, Baldwin and Yan (2010) find that the steep increase in the value of the Canadian dollar during the post-2002 period almost completely offset the productivity growth advantages

TDDP 02/2010 PAGE 9

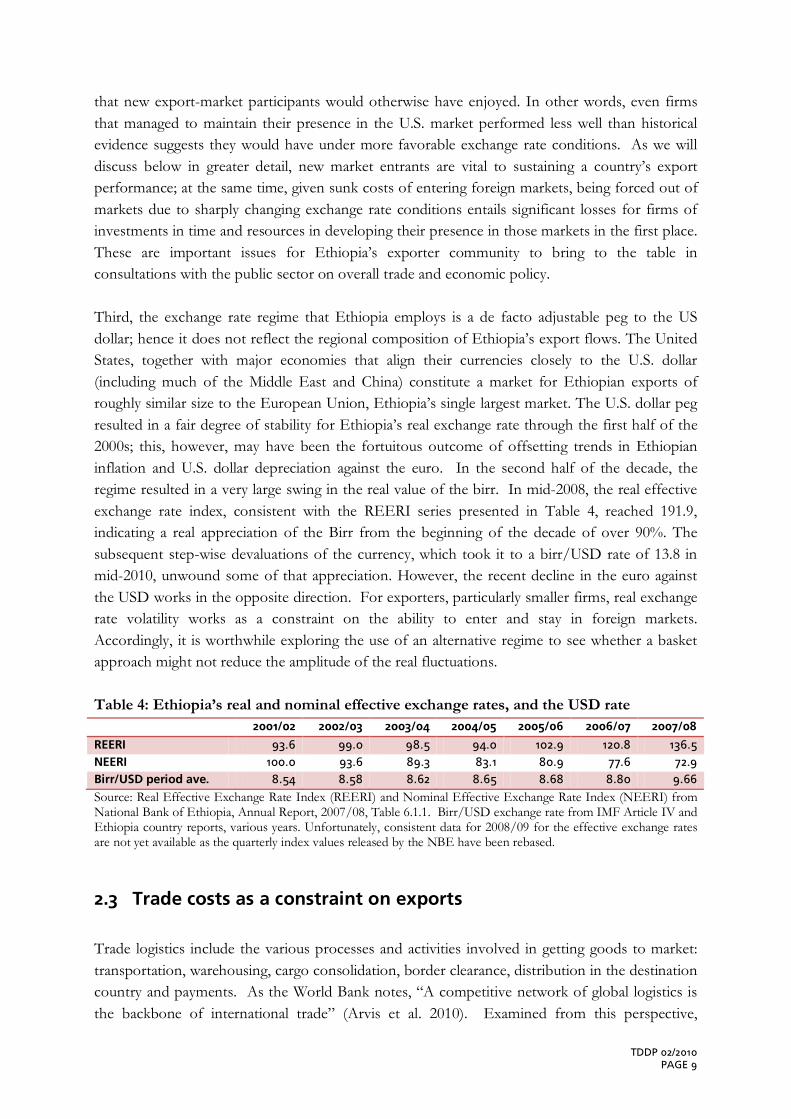

that new export-market participants would otherwise have enjoyed. In other words, even firms that managed to maintain their presence in the U.S. market performed less well than historical evidence suggests they would have under more favorable exchange rate conditions. As we will discuss below in greater detail, new market entrants are vital to sustaining a country’s export performance; at the same time, given sunk costs of entering foreign markets, being forced out of markets due to sharply changing exchange rate conditions entails significant losses for firms of investments in time and resources in developing their presence in those markets in the first place. These are important issues for Ethiopia’s exporter community to bring to the table in consultations with the public sector on overall trade and economic policy. Third, the exchange rate regime that Ethiopia employs is a de facto adjustable peg to the US dollar; hence it does not reflect the regional composition of Ethiopia’s export flows. The United States, together with major economies that align their currencies closely to the U.S. dollar (including much of the Middle East and China) constitute a market for Ethiopian exports of roughly similar size to the European Union, Ethiopia’s single largest market. The U.S. dollar peg resulted in a fair degree of stability for Ethiopia’s real exchange rate through the first half of the 2000s; this, however, may have been the fortuitous outcome of offsetting trends in Ethiopian inflation and U.S. dollar depreciation against the euro. In the second half of the decade, the regime resulted in a very large swing in the real value of the birr. In mid-2008, the real effective exchange rate index, consistent with the REERI series presented in Table 4, reached 191.9, indicating a real appreciation of the Birr from the beginning of the decade of over 90%. The subsequent step-wise devaluations of the currency, which took it to a birr/USD rate of 13.8 in mid-2010, unwound some of that appreciation. However, the recent decline in the euro against the USD works in the opposite direction. For exporters, particularly smaller firms, real exchange rate volatility works as a constraint on the ability to enter and stay in foreign markets. Accordingly, it is worthwhile exploring the use of an alternative regime to see whether a basket approach might not reduce the amplitude of the real fluctuations. Table 4: Ethiopia’s real and nominal effective exchange rates, and the USD rate 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08

REERI 93.6 99.0 98.5 94.0 102.9 120.8 136.5 NEERI 100.0 93.6 89.3 83.1 80.9 77.6 72.9 Birr/USD period ave. 8.54 8.58 8.62 8.65 8.68 8.80 9.66 Source: Real Effective Exchange Rate Index (REERI) and Nominal Effective Exchange Rate Index (NEERI) from National Bank of Ethiopia, Annual Report, 2007/08, Table 6.1.1. Birr/USD exchange rate from IMF Article IV and Ethiopia country reports, various years. Unfortunately, consistent data for 2008/09 for the effective exchange rates are not yet available as the quarterly index values released by the NBE have been rebased.

2.3 Trade costs as a constraint on exports Trade logistics include the various processes and activities involved in getting goods to market: transportation, warehousing, cargo consolidation, border clearance, distribution in the destination country and payments. As the World Bank notes, “A competitive network of global logistics is the backbone of international trade” (Arvis et al. 2010). Examined from this perspective,

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 10

Ethiopia is one of the most difficult places in the world from which to engage in the global economy. Ethiopia ranks 123rd out of 155 countries in the World Bank’s trade logistics survey (Arvis et al. 2010). Corroborating this finding, Ethiopia ranks 159th

in terms of trading across borders in the World Bank’s Doing Business survey.

One obvious consequence of relatively high trade costs is a relatively low trade share of GDP. Since some products must be imported regardless of the level of trade costs, whereas customers elsewhere have many alternative suppliers for each and every product that Ethiopia produces, the very, very low export share of GDP is perhaps an even better indicator of the impediments posed to trade by the costs of doing business across Ethiopia’s borders. The World Bank, in its Doing Business benchmarking methodology, breaks down trade costs into three general categories: the number of documents that must be processed to ship goods out of or into the country, the time it takes to carry out these procedures and to move goods to the nearest port, and the official fees and commercial costs involved in getting goods from the factory door to customers in other countries. Table 4 summarizes how Ethiopia ranks compared to the world’s best, to Africa’s best, and to the best in landlocked Africa in the latest rankings. Table 4: Costs of trading across borders in Ethiopia, 2010

ETH Best in World Best in Africa Best in Land-locked Africa (excluding SACU)

Export No. of Documents 8 2 France 4 Madagascar 6 Uganda et al.

Time (days) 49 5 Singapore etc. 11 Senegal 32 Mali

Cost (US$ per container) 1,940 450 Malaysia 690 Sao Tome & Principe

1,713 Malawi

Import No. of Documents 8 2 France 5 Djibouti 7 Uganda

Time (days) 45 3 Singapore 14 Senegal 34 Uganda

Cost (US$ per container) 2,993 439 Singapore 577 Sao Tome & Principe

2,570 Malawi

Source: World Bank, Doing Business 2010: Ethiopia. Ethiopia’s monetary and time costs of trade are, to some extent, elevated simply by its being landlocked. Trade costs in terms of both time and money are documented as being systematically higher for landlocked versus coastal countries, not only in Africa but also elsewhere, including in Europe (Arvis et al. 2010: Table 2.6). At the same time, as argued by Arvis et al. (2007, 2010), this is not because the distance to ports or the unit cost of transportation services are necessarily unusually high in landlocked countries—e.g., Addis Ababa is closer to a port than a major industrial centre like Munich, Germany, and in fact to a brand new container port at Doraleh, Djibouti, managed by a global port management company equipped to operate in a modern trade environment, and featuring all the modern physical infrastructure, including a quay of 1050m and draught of 18m to allow it serve 15,000 TEU super post-Panamax vessels, giant Gantry cranes to unload containers and the full gamut of modern information technology systems for

TDDP 02/2010 PAGE 11

trade in place8

. Rather, the problems lie in the poor state of transit systems (in particular of trade corridor infrastructure development and maintenance) as well as vulnerability of transportation services to rent-seeking activities (e.g., transit procedures that exploit monopoly advantages to extract payment of additional fees or duties or to make movement of goods subject to excessive control in the transit country).

As regards the physical aspects of transit systems, there appears to be much work to be done. According to material tabled at a December 2009 experts group meeting organized by the African Development Bank Group on transit ports servicing landlocked countries, which includes Ethiopia: Interfacing road and rail systems to most Sub-Saharan ports are in poor condition and do not

support container transport. Container usage is accordingly confined to ports and their immediate vicinity, with very low

volumes of containerized transit traffic into landlocked hinterland countries; imports move inland transported in general cargo.

Statistics are not available for Ethiopia itself but we note that a recent press report suggested that half the containers inbound for Ethiopia are unstuffed and 90 percent of the outward bound containers are stuffed in Djibouti9

, indicating considerable potential to reduce costs through seamless multi-modal links between freight forwarders located in Ethiopia and the port.

The importance of improving its transportation infrastructure has long been recognized in Ethiopia. A road development program was launched in 1997, with one of the first projects being the 442 km Modjo-Awash-Gewane-Mille portion of the import-export corridor. A $100 million loan from the World Bank was recently arranged for Stage II of the project. Moreover, upgrades have been made to the railway link to Djibouti (although it is still not functional and the plans for development of a full-fledged multi-modal link appear to remain on hold). And Ethiopian Shipping Lines is in the process of introducing multi-modal capacity within Ethiopia, including shipping goods to two dry ports in the country10

.

However, as noted by Shelley (2009), multi-modal transport is dependent on rail for efficiency on journeys of more than about 600 km, which is what is needed to connect Ethiopia’s emerging industrial district in the Addis Ababa area to seaports. In the case of the Ethiopia-Djibouti line, tracks and bridges need to be improved to support heavy loads such as fuel oil tanks and faster trains. The level of ambition of the recent improvements to the railway link appears to fall well short of these standards—and stands in sharp contrast to the level of ambition shown in the building of Doraleh Port which leap-frogged the existing container ports in East Africa in terms of providing modern facilities. 8 See Eye for Transport. 2009. “DP World opens new Doraleh Container Terminal” February 10, 2009,

http://www.eft.com/content/dp-world-opens-new-doraleh-container-terminal; accessed August 9, 2010. 9 Tamrat G. Giorgis, “Djibouti Grants Monopoly on Part of Port Operation,” AllAfrica.com, 20 April 2010. 10 Capital Ethiopia, “Ethiopian Shipping Lines to Build Dry Port in Oromia State”,

http://www.capitalethiopia.com/index.php?view=article&id=12442%3Adukem-to-get-esl-container-terminal&option=com_content&Itemid=4.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 12

Given the cost advantages of high-speed trains—they use one-third as much energy as comparable air travel and less than one-fifth as much as road transport—high-speed rail has been described as a “game changer” for the United States (Gertler 2009). China has recognized these advantages and is moving rapidly to develop its own web of high-speed rail links: it has opened or will open 42 new high speed rail lines between 2009 and 2012, including a number that will handle freight11. Similarly, for Ethiopia, a high-speed modern rail link to Doraleh would be a “game changer”, effectively removing the cost handicap of being a landlocked, African country. To be sure, there are legitimate concerns about being hostage to rent extraction due to the lack of alternatives, but the answer to that surely is not to put the first line on hold but rather to fast-track a second line12

.

For potential gains from improved physical infrastructure to be realized, comparable improvements need to be made in border and transit procedures. Almost by definition, improving the efficiency of trade corridors requires regional cooperation and coordination, without which an individual country’s development initiatives in its own territory can yield little in the way of benefits. In this regard, for example, Uganda’s recent improvement in its rankings on the World Bank’s Logistics Performance Index is attributed to a successful project to facilitate transit at the Malaba Border Post in Kenya (Arvis et al. 2010: 19). Regional transit systems that facilitate transshipment of goods under customs control through a country have long been in place around the world. One example of such a system is the Transport International Routier (TIR) Convention, based on the UN Customs Convention on the International transport of Goods under Cover of TIR Carnets (1960). The TIR carnet, which is a single, harmonized transit document, reduces customs formalities at frontiers to a minimum. However, to be effective the system must be supported by a system of guarantees and an institutional framework of recognized freight operators. The system is used in Europe and elsewhere in the world. A similar system was formally adopted by the Economic Community of West African States (ECOWAS) in 1982 but failed to gain traction for lack of commitment in its implementation13

. Carnet-based systems are however part of the focus of the World Bank’s regional trade facilitation projects in Africa (Hoekman 2009). For Ethiopia, adopting such a system, in collaboration with Djibouti, would be an essential complementary reform to the recommended improvements in transport infrastructure.

Air cargo, which is particularly important for time-sensitive goods and which is not hostage to transit corridor issues can also face high trade costs since a very significant portion of the overall costs of trading across borders are administrative in nature. Djankov, Freund and Pham (2010) found that about 75 percent of the overall costs of trading across borders could be attributed, on average, to administrative costs. Importantly, they note that these costs tend to be nearly identical

11 New York Times, “China Sees Growth Engine in a Web of Fast Trains,” February 12, 2010. 12 We note that the physical capacity in the three major alternative ports, Port Sudan, Port of Assab and Berbera are

well short of the needs of large-scale modern container ships. Accordingly, even in the hopeful event of political stabilization in the Horn of Africa, the Djibouti option looms as the only realistic medium-term option.

13 The ECOWAS agreement was formally called the ECOWAS Transit Routier Inter-États (TRIE).

TDDP 02/2010 PAGE 13

for sea and air. For Ethiopia, reforms to import and export procedures that reduce the time it takes to execute trades would effectively move it closer to the global economy: distance can be measured in time, and for business time is money. Several other factors pertinent to the discussion of trade costs might be noted. First, with reference to the above discussion on trade imbalances, one “hidden” reason for high trade costs in Ethiopia is the great imbalance in goods trade: with goods imports 5 times the level of goods exports, a substantial proportion of the containers bound for Ethiopia leave empty. According to a recent press report, approximately 100,000 containers enter Djibouti with Ethiopia-bound goods while out-bound containers are estimated to reach between 30,000 and 40,000 units annually14. Since carriers build the cost of empty container retrieval into the prices they charge for loaded containers, this “deadheading” adds considerably to Ethiopia’s cost of trade15

. Accordingly, if Ethiopia adopts policies to reduce the imbalance in goods trade, it will also likely reduce the per-container cost of trade.

Second, in considering trade costs as an impediment to exports, it is important to recognize that high costs of importing are increasingly damaging for export performance since they make it more difficult for a country to participate in supply chains. Reflecting the increasing fragmentation of production across borders, one of the great drivers of global trade in recent decades has been trade in intermediate goods, which typically involve importing inputs for processing and then re-exporting the transformed components. In this context, time and money costs of importing products work just as perniciously to reduce exports as do costs directly associated with exporting. Ethiopia’s high cost of importing thus adds to the costs of exporting to form a powerful deterrence to its engaging in process trade. Third, long lead times for import and export are closely associated with heightened uncertainty concerning the exact amount of time that is required to import or export. Such uncertainty can be even more damaging for traders than the time costs themselves. As noted by Hummels:

“Lengthy shipping times impose inventory-holding and depreciation costs[16

] on shippers. Inventory-holding costs include both the capital cost of the goods while in transit, as well as the need to hold larger buffer-stock inventories at final destinations to accommodate variation in arrival time [...] These costs will be magnified in the presence of fragmentation. When countries specialize in stages of production and trade intermediate goods the inventory-holding and depreciation costs for early-stage value-added accrue throughout the duration of the production chain” (Hummels 2001).

14 Footnote 9 supra. 15 Empty container costs include repositioning of empty containers, terminal handling and storage fees, ship’s time,

and equipment per diems and repair. One estimate suggested that empty containers cost carriers, worldwide, almost US$ 23 billion in 2004 (UNESCAP: Container Port Volumes).

16 In Hummels’ analysis, depreciation captures any reason that a newly produced good might be preferable to an older good, including literal spoilage of fresh produce or cut flowers, items with immediate information content such as newspapers, and goods with complex characteristics for which demand cannot be forecast well in advance such as holiday toys and fashion garments.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 14

Overall, Hummels found that each day in transit is equivalent to a 0.8% ad valorem tariff on the goods being shipped. While this estimate is derived from comparing transportation time and costs across different transportation modes, he notes that

“the estimates are informative about many policies and sources of technological change that speed goods to market. For example, eliminating or streamlining elaborate customs procedures allow imported goods reach their destinations more quickly. Investing in more efficient port infrastructure may accomplish similar goals. The estimates [...] indicate that a four-day wait for customs inspection is equivalent to the cost of explicit tariffs for most manufactures” (Hummels 2001).

A related approach using a different methodology by Djankov, Freund and Pham (2010) arrived at a complementary conclusion that a one percent increase in the time to execute a trade reduced the value of trade by 1.3 percent. Armed with these estimates, it is possible to provide some indication of the scale of trade gains that could be achieved by Ethiopia by reducing trade costs. The perennial question in such exercises is on what basis to make assumptions concerning the degree of feasible cost reductions. A conservative approach is to assume cost reductions to the level consistent with “best in region” – in Ethiopia’s case, that would be best in landlocked Africa. On this basis, the time to export would be reduced from 49 days to 32 and to import from 45 to 34. Similarly, the cost of exporting a container would be reduced from US$1,940 to US$1,713; and of importing a container from US$2,993 to US$2,573. However, a more ambitious approach for Ethiopia would be to emulate the most successful reformers in the region and elsewhere. Delving into this issue in depth is well beyond the feasible scope of the present note but a few observations can be made. Ghana for instance made very significant reductions in clearance times through the Airport, with times reduced to an average of two to four hours, from the two to three days average prior to the implementation of its fully automated TradeNet system for customs information (International Trade Centre 2008). We note that Ethiopia automated its customs and tax administration in 2004 but has not implemented the risk-based customs controls which that system enables; thus whereas the ease of paying taxes in Ethiopia has substantially improved, the ease of trading across borders has not. Accordingly, the potential for significant trade cost reductions in the Ethiopian context are available—and presumably feasible, given the example of Ghana. To put the issue of trade costs into quantitative perspective, Table 5 calculates the implied trade levels in 2009 if Ethiopia: had trade costs in line with best-in-region; or reduced its administrative costs to the lowest time in any jurisdiction17

.

17 For this calculation, administrative costs are assumed as per the Djankov, Freund and Pham (2010) estimates to

be 75 percent of the time costs. The lowest time in any jurisdiction for exports and imports are in Denmark and Singapore respectively. Taking these times as close to what is achievable minimum in terms of pure administrative costs and adding in Ethiopia’s non-administrative time costs (assumed to be 25 percent of current time costs of trade), would reduce time to export and import in Ethiopia to 17.25 and 14.25 days respectively.

TDDP 02/2010 PAGE 15

As can be seen from Table 5, even just moving to best-in-region on time costs of trade would imply a significant increase in the trade share of GDP in Ethiopia of about 13 percent, raising the value of goods trade by an amount equivalent to over 12 percent of Ethiopia’s 2009 GDP. Moving to world best in terms of administrative costs would imply a near-doubling of trade from the 38 percent of GDP in 2009 to the 70 percent range. Of course, such a reduction in trade costs could not take place overnight, nor would the response of the economy to such reforms be instantaneous—indeed steps would have to taken to improve the domestic supply response, as discussed next. Moreover, since the reductions in trade costs would be largely symmetric, facilitating both imports and exports, a rebalancing of the policy mix would be necessary as a precondition to undertaking the reforms. That being said, given current estimates of administrative costs of doing business across borders in Ethiopia, and in light of recent estimates of the trade impact of reducing these costs to levels that are in principle within Ethiopia’s grasp, Ethiopia’s low trade share of GDP can be largely attributed to its own administrative trade costs. Table 5: Trade Impact of Trade Cost Reductions Days pre- and

post reform Percent

reduction in time

Percent Increase in trade (DFP elasticity)

Trade Gain based on 2009 Levels (USD ‘000)

As a share of 2009 GDP

Moving to Best-in-Region Exports 49/32 34.7% 45.1% 986,740 2.8% Imports 45/34 24.4% 31.8% 3,468,718 10.0%

Moving to Global-Best in Administrative Costs Exports 49/17.25 64.8% 84.2% 1,842,882 5.3% Imports 45/14.25 68.3% 88.8% 9,696,644 27.9% Source: Estimates of time costs of trade form the World Bank, Doing Business; elasticity of trade gain to reduction in time costs of trade from Djankov, Freund and Pham (2010); remaining calculations by the author.

2.4 Private Sector Under-Development as an Export Constraint Controversies have long raged concerning the role of trade and trade policy in economic growth and development (see Easterly 2005; Rodriguez 2007; and Estevadeordal and Taylor 2008). New light is being shed on this area with the development of “new new trade theory” (Melitz 2003) and a rapidly growing empirical literature based on it (see Wagner 2007 for a recent survey). In this literature, firms of widely varying size and level of productivity co-exist in the same industry. Products of varying quality co-exist in the same markets. Firms face sunk costs of introducing their products into foreign markets in terms of obtaining market intelligence, identifying foreign partners, dealing with foreign regulatory requirements, setting up distribution and after-sales service networks, and so forth. Potential exporters also face uncertainty about success in foreign markets. They have less knowledge than established firms about these markets and about the local partners or agents they must engage (information asymmetries). International macroeconomic conditions, including business cycles and real exchange rates feature both volatility and protracted disequilibrium conditions that can affect a firm’s profitability in foreign markets (Baldwin and Lyons 1994). Accordingly, not all firms engage in trade and foreign investment and, of those that do, many enter fewer markets than they might optimally serve.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 16

Indeed only relatively highly productive firms can absorb the costs of entering export markets and only the most productive of these can absorb the still higher costs of investing abroad while remaining profitable in those markets (Helpman et al. 2003). The flux of entry into and exit out of various foreign markets of firms and of individual products—or change at the “extensive margin”—is high. This constitutes an important factor in determining a country’s overall trade growth, alongside changes in sales by existing exporters of established products in established markets (which represents change at the “intensive margin”). In the modern world, rapid technological change renders yesterday’s market-leading products obsolete tomorrow, and worldwide investment in skills and equipment, economic infrastructure and institutional reforms incrementally changes relative national capabilities from year to year. As a result, the workshops of the world migrate and some locales see their economic fortunes wither even as others prosper. Sustaining access to foreign markets is as hard as achieving it. Traditionally, the gains from trade were interpreted as arising from specialization. While this is typically true at the firm level, it is not necessarily true at the national level. Particularly at lower levels of economic development, trade expansion is characterized by a high degree of diversification of products and markets (Imbs and Wacziarg 2003). Underlying this dynamic is a stream of new firms and new products entering new markets. For example, China’s remarkable expansion of exports following its accession to the World Trade Organization was accomplished in good measure by expansion of the number of different products it exported: to the US market alone, the product count (taking exports at the HS10 digit level as constituting an individual product) increased from 9,249 in 1998 to 13,123 products in 2006 (Acharya 2010: 286). Thus, while it is important to take into account the products and markets that already figure in a country’s export activity, it is perhaps even more important to consider the scope for trade creation in areas which are currently not traded—i.e., to fill in the “zeros” in the country’s trade matrix of products and destinations. Export diversification has long been a goal incorporated in Ethiopia’s national strategy of Agricultural Development Led Industrialization (ADLI), with the attainable objective being seen as expanding the processing of primary agricultural products. The policy goals underpinning this strategy are consistent with traditional objectives of developing countries seeking to counter declining terms of trade for their commodities and reducing export instability through a “portfolio effect”, and by reducing instability to encourage firms to incur the sunk costs to enter foreign markets (Hesse 2008). However, the important lesson to draw form the recent trade literature is that, given an underlying population of firms of varying levels of productivity, trade liberalization naturally induces diversification insofar as the most productive firms in various sectors are provided new export opportunities that were not there before—even in sectors which overall suffer a contraction in output due to import competition. Since public authorities generally lack information on the productivity distribution of the country’s firms, there tend be surprises in the wake of trade liberalization in the form of unexpected export successes. Accordingly, in considering Ethiopia’s trade prospects, it is important not to limit attention to

TDDP 02/2010 PAGE 17

areas of current export activity and to consider the potential for trade diversification across a wide range of industrial sectors from lowered trade costs. The process of export diversification is very much in evidence in Ethiopia, as shown in Table 6 below. The first line of Table 6 shows Ethiopia’s exports in the product categories in which Ethiopia had zero value of exports in 2005 but positive values in 2009, of which there were 840 at the HS 6-digit level. Of these, 734 or over 87% were industrial products (HS25 or higher). As can be seen, Ethiopia expanded its exports very steeply in these categories. The second line shows the total value of exports in the 798 categories in which Ethiopia had zero value of exports in 2006 and positive values in 2009. Lines 3 and 4 repeat the exercise for the zero trade categories in 2007 and 2008. Table 6: Ethiopian export growth at the extensive margin, USD thousands, 2005-2009

Number of product categories 2005 2006 2007 2008 2009

840 0 7,477 84,124 260,476 593,159 798 0 65,475 149,886 291,643 525 0 114,750 238,270 348 0 36,619

Source: International Trade Centre, Trade Map. Calculations by the author. Reflecting the turnover of export products, Ethiopia also had 142 product categories in which it had positive exports in 2005 that went to zero by 2009; the total value of trade in these categories totaled US$ 75.62 million in 2005. This demonstrates the importance of maintaining a positive balance of new product introductions to replace products that are losing their global market niches. While Ethiopia is diversifying its export structure, the pace of diversification is low. The catch for Ethiopia appears to be its industrial structure, which is dominated by a relatively small number of government-owned firms and conglomerates, features a high degree of market concentration, and is characterized by relatively high administrative barriers to entry. Ethiopia ranks 93rd in the world in ease of starting a business under the World Bank’s Doing Business methodology. However, according to the most recent survey of Ethiopia’s manufacturing sector, there were only 1,930 manufacturers in the country in 2008/09 defined as “large and medium scale”, meaning they employ 10 or more persons and use power-driven equipment18. Total employment of these firms was just 133,673 persons. There were an additional 43,338 “small scale” manufacturing establishments, defined as those with fewer than 10 employees and using power-driven machinery, of which 23,047 fell into the category of grain mills19

. These small scale manufacturers employed an additional 138,951 persons. These are, it goes almost without saying, very small numbers for a country with a total population in excess of 80 million.

18 Central Statistical Agency, Manufacturing Industries Survey,

http://www.csa.gov.et/index.php?option=com_content&view=article&id=62&Itemid=489. 19 Central Statistical Agency, Ethiopian Small Scale Manufacturing Industries Survey,

http://www.csa.gov.et/index.php?option=com_content&view=article&id=92&Itemid=413.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 18

Market economies in general are characterized by a high rate of firm formation and disappearance. This appears to be an essential aspect of the market system in channeling scarce resources to their most profitable uses—in a sense, the market is a form of “search engine” that tries out various possible products to see which ones can be produced with sufficient profit to stay in the market over the longer term. But for such a search engine to identify profitable niches in a rapidly changing and fiercely competitive global economy, the search—which includes market entry by new firms with new products—must be made as easy as possible. Ethiopia’s ranking under the World Bank’s Doing Business methodology for starting a business improved significantly in 2010 due to a reduction in the number of procedures required to start a company, the time it took to start a company, and the minimum capital required. However, given the concentrated market structure, substantially freer market entry may be required to develop the number and diversity of private sector firms that is a prerequisite for trade liberalization to generate the economic gains that theory predicts. Building on the preceding point, it is not enough to simply foster firm formation. Ethiopia requires the emergence of many, many successful firms, selling competitive products in its home market. Successful firms and competitive products do not emerge on a sustained basis under just any conditions. The modern competitiveness literature emphasizes the importance of the industrial districts described as far back as Marshall (1879) as the spawning grounds for new firms and products. The essential idea in this literature is that positive externalities such as knowledge spillovers20

generated by close proximity of competing and complementary forms of human and physical capital enhance the ability of a region to compete. Firms in such industrial districts— “clusters” in modern jargon—sit in a rich context, connected to and getting feedback from, factor and product markets, suppliers and customers, collaborators and competitors. It is the information flow within this setting that helps firms overcome the limitations of their own knowledge and enables them to both identify market opportunities and to develop the products that meet the market’s needs.

Ethiopia has only very recently developed its first industrial park in Dukem, with China’s support. This is a vital first step in the direction of creating a viable, dynamic industrial culture in Ethiopia21

. Combined with further reduction in the cost of establishing new firms, the development of further industrial areas, and facilitation of links between these industrial areas and with Ethiopia’s institutes of higher learning, especially its engineering schools, would be an important step in reducing the microeconomic barriers to Ethiopia’s ability to export successfully.

20 In this context, externalities are aspects of a firm’s operations that have “public good” characteristics—that is,

the firm does not fully capture all the benefits of its activities. For example, a firm that pioneers the path to exporting a given product to a given market may be imitated by other firms that did not invest in the cost of developing that market. More generally, the interchange of ideas and often personnel amongst companies within a local region acts like technology transfer, expanding capabilities of firms at little cost.

21 We note that Ethiopian Shipping Lines has plans to situate a container terminal in Dukem, connecting it to dry ports within Ethiopia. Accordingly, things are moving in the right direction.

TDDP 02/2010 PAGE 19

2.5 Domestic producer service margins as an export constraint At the plant or establishment level, specialization typically allows the achievement of higher levels of productivity22

. One aspect of increased specialization of manufacturing firms is out-sourcing of various types of functions such as intermediate inputs and internal services to firms specializing in these functions. By the same token, to be competitive globally, manufacturing firms need to have access to efficient, low-cost industrial inputs and producer services, including in the latter case, distribution systems within the country, transport, telecommunications and finance. High margins in these areas can systematically depress the competitiveness of a country’s manufacturing sector. Accordingly, efforts to create a viable industrial culture in Ethiopia can thus be undermined by inadequate development or excessive costs in producer services. In turn, under-development of industry works in the longer term to constrain growth of competitive exports.

While the services sector in Ethiopia is expanding its share of economic activity (Access Capital 2010), there appear to be grounds for concerns that market structure in the producer services sector might represent a constraint on the development of the industrial sector. While a detailed investigation into this issue is well beyond the scope of the present note, we note some anecdotal evidence obtained from the turbulent conditions reported in the cement market in recent years, reflecting among other things: A temporary restriction on cement imports, which had been permitted since 2006 on the

franco valuta basis (i.e., by importers with independent access to foreign exchange23

A temporary shutdown in power supply to domestic cement manufacturers. ).

A financial market report on the Ethiopian cement sector during this period noted the very high margins between the ex-factory price of cement, reported at 155 birr per quintal (=100 kg), and the retail price in Addis Ababa, reported in the 325-350 range. It went on to comment on the impact of imported cement on the prices in the domestic market as follows:

“Data for the first four months for 2009 [...] show that cement import prices (CIF basis) averaged Birr 152 per quintal [...] though retail prices averaged Birr 276 during this time frame. This implies that Birr 124 (or 45 percent) of the retail price of domestic cement reflects some combination of domestic transport costs, official charges, and retailer margins. A sizeable entry of much lower-priced imports would normally be expected to bring down domestic prices, but the fact that this has not taken place in the Ethiopian context is somewhat puzzling: the possible culprits here are high transport costs, high retailer margins, and/or obstacles in the trading regime (such as limited cement import licenses being offered) that work to reduce the amount of imports that would otherwise enter the country” (Access Capital Research 2009).

22 For a discussion of plant- versus firm-level economies or diseconomies of scale and scope, see Lileeva and Van

Biesebroeck (2010). 23 We note that one of the benefits of WTO accession for the Ethiopian economy would likely be the elimination

of such irregular import procedures with regular tariff barriers. This would serve both to decrease uncertainty about access to imports while also levelling the playing field within Ethiopia in this regard, and transfer some of the monopoly rents in the system to government in the form of tariff revenues.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 20

Simply put, Ethiopia’s producer services appear to operate on the basis of high margins and low volumes; shifting to a low margin-high volume business strategy would fundamentally improve the ability of the underlying industrial sector to access export markets on a competitive basis, not least by gaining access to imported inputs at globally competitive prices.

2.6 Thick borders as an export constraint One of the features of Ethiopia’s pattern of bilateral trade is the remarkably low value of trade with its immediate neighbors. As a “stylized fact”, being adjacent to a trading partner doubles the intensity of trade with that partner compared to non-adjacent countries24

. To gain a sense of what might be more “normal” levels of bilateral trade between Ethiopia and its immediate neighbors, and thus a sense of what the boost to trade would be from a successful regional political process of regional community-building, we run a similar “thought experiment” to that in section 1.1 which considered how strong Ethiopia’s trade might be with the world’s major economies. In this case, we use Kenya’s trade with its immediate neighbors Tanzania and Uganda as benchmarks. The top panel in Table 7a below shows, from a Kenyan perspective, the tariffs it applies (“Tariff KEN M”), and that it faces(“Tariff KEN X) in trade with Tanzania and Ethiopia respectively. It also shows the bilateral distance between Kenya and each of these partners, the partners’ respective GDPs and the level of two-way trade they had with Kenya in 2008, based on the respective countries’ import statistics.

Table 7a: Benchmarking Ethiopia’s “missing” trade with immediate neighbors: 2008

Tariff KEN M

Tariff KEN X

Bilateral Distance

Partner GDP

2008 two-way

trade

2008 two-way trade adjusted

for tariffs

2008 two-way trade adjusted

for gravity

Kenya-Tanzania 0.0% 0.32% 550 20,721 536.18 216.39 Kenya-Ethiopia 1.45% 16.32% 1,186 25,658 33.40 33.90 124.20

Kenya-Uganda 0.0% 0.27% 479 14,529 586.75 221.38 Kenya-Ethiopia 1.45% 16.32% 1,186 25,658 33.40 33.90 157.87 Source: Tariff data from the International Trade Centre, Market Access Map; distance data from CEPII (figures used here are the regionally weighted distwces measure); GDP data are from the IMF, World Economic Outlook database; calculations are by the author. As can be seen, actual two-way trade between Kenya and Ethiopia amounted to US$ 33.4 million or only about 6 percent of the level of two-way trade between Kenya and Tanzania. However, this is not a fair comparison since the levels of tariffs in the two relationships are very different. Kenya applies no tariffs on its imports from Tanzania and Uganda and faces very low tariffs on its exports to these East African Community partners. By contrast, it levies a 1.45 percent tariff on Ethiopia and faces in turn a 16.32 percent tariff in Ethiopia. To level this playing field, we run a simulation using a standard partial equilibrium trade model to raise tariffs on trade between Kenya, Tanzania and Uganda equal to those that Kenya applies and faces in its trade with Ethiopia. The resulting trade levels are given in the next column in Table 7a; as can be seen,

24 The estimate is based on Frankel (2000: 5).

TDDP 02/2010 PAGE 21

Kenya’s bilateral trade with Ethiopia rises marginally due to the trade diversionary effects while its bilateral trade with both Tanzania (top panel) and Uganda (bottom panel) falls sharply. The final column shows the level of Kenya-Ethiopia trade taking into account the fact that Ethiopia had a GDP in 2008 that was 24 percent larger than Tanzania’s but its bilateral distance to Kenya was more than twice that of Tanzania’s; and the corresponding figures using Kenya-Uganda as the benchmark. Taking the gravity relationships into account (using conventional unitary elasticities for size and distance) results in an “expected” ratio of trade between Kenya and Ethiopia of about 57 percent of that between Kenya and Tanzania. Applying this ratio to the tariff-adjusted level of trade yields an estimate of how much two-way trade between Kenya and Ethiopia would have taken place in 2008, if the trading relationship were as intense as that between Kenya and Tanzania. The second panel runs the same experiment using the Kenya-Uganda relationship as a benchmark. We obtain a very similar level of “expected” trade for Kenya and Ethiopia of US$157.87 million or more than 4½ times the level observed. The average of the two estimates puts the “missing trade between Kenya and Ethiopia at a little over US$100 million. Applying the same principles to Ethiopia’s trade with its other neighbors provides a benchmark against which to evaluate observed trade levels. This experiment is carried out in Table 7b which seeks to identify the “missing” trade that could plausibly be attributed to the unsettled state of Ethiopia’s immediate neighborhood and under-developed level of regional cooperation. Table 7b: Evaluating Ethiopia’s “missing” trade with immediate neighbors: 2008

Distance GDP

Two-way trade 2008

Gravity Ratio to ETH/KEN

Implied Trade level

Missing trade

Djibouti 519 982 63.06 0.074 10.48 -52.59 Eritrea 586 1,476 0 0.099 13.95 13.95 Somalia 931 2,693 88.46 0.113 16.00 -72.46 Sudan (ex oil) 952 57,911 83.34 2.388 336.80 253.46 Uganda 1,178 14,529 1.12 0.484 68.28 67.17 Kenya 1,186 30236 33.40 1.000 141.04 107.63 Total 317.16 Total ex Djibouti and Somalia 442.21 Source: See Table 7a, except estimate for Somalia GDP, which is based on the CIA World Factbook estimate. The bottom line from Table 7b is that Ethiopia trades substantially less with its immediate neighbors than would normally be expected. Ignoring for the moment the special cases of Djibouti and (the former) Somalia, and excluding Ethiopia’s imports of oil from Sudan, the estimate of the total amount of under-trading in terms of two-way trade in 2008 is about US$ 440 million, with the implied trade level being 4.75 times larger than observed trade25

25 Part of this might, of course be explained by other factors that systematically affect trade costs, such as, for

example, the fact that Swahili is a national language in Uganda and is also a lingua franca in Tanzania and Kenya and elsewhere in the East African Community, but not in Ethiopia. Since English is also widely used as a lingua franca in the business community, it is difficult to know what part of the missing trade might be due to language/cultural factors. The above estimates based solely on size of economies, distance and bilateral tariffs is thus only a rough first indicator of the potential order of magnitude of the “missing trade” which is sufficient for the purposes of this paper, which is to provide broad quantitative parameters for Ethiopia’s trade potential. It

.

CIURIAK: SUPPLY AND DEMAND SIDE CONSTRAINTS AS BARRIERS FOR ETHIOPIAN EXPORTS PAGE 22