ANNUAL REPORT 2018 - victoriabank.md · commercial bank into the largest financial group in Romania...

53

ANNUAL REPORT 2018

Transcript of ANNUAL REPORT 2018 - victoriabank.md · commercial bank into the largest financial group in Romania...

ANNUAL REPORT2 0 1 8

CONTENTSANNUAL REPORT 1

MANAGEMENT MESSAGE 4

SHAREHOLDERS OF THE BANK 6

BANK’S MANAGEMENT 8

Main events in 2018 10

MANAGEMENT REPORT 12

ECONOMIC CLIMATE 13

Macroeconomic situation 13

Evolution of the banking sector 15

ACTIVITY PERFORMANCE OF B.C. ”VICTORIABANK” S.A. 17

Evolution of financial results 17

Customer service 18

Work on deposit attraction 20

Lending activity 22

Customer operations 24

Banking card activity 25

Foreign exchange activity 26

Activity on the securities market and the capital market 27

STRATEGIC OBJECTIVES FOR 2019 29

Development strategy 29

PERSONNEL MANAGEMENT 30

RISK MANAGEMENT 32

CORPORATE GOVERNANCE 39

Corporate governance code applied by the bank with reference to the source

and place of publication 39

Degree of the bank compliance with the corporate governance code 42

Internal control system 42

Audit Committe report for 2018 43

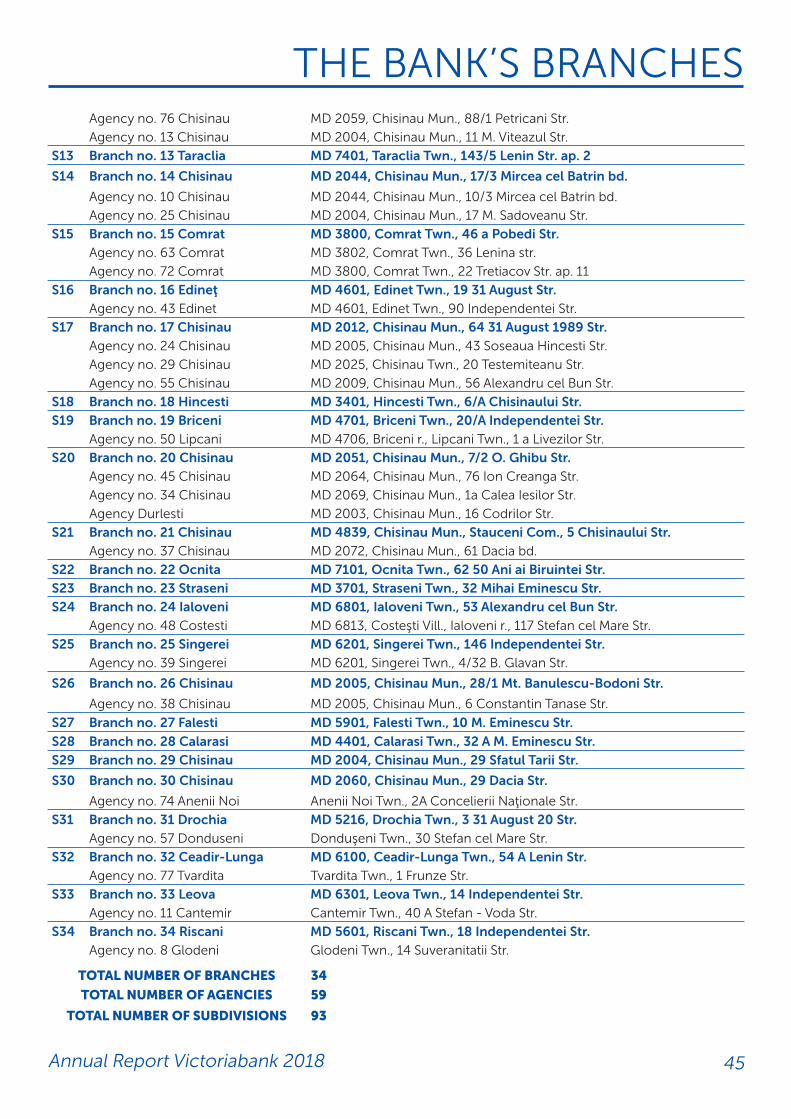

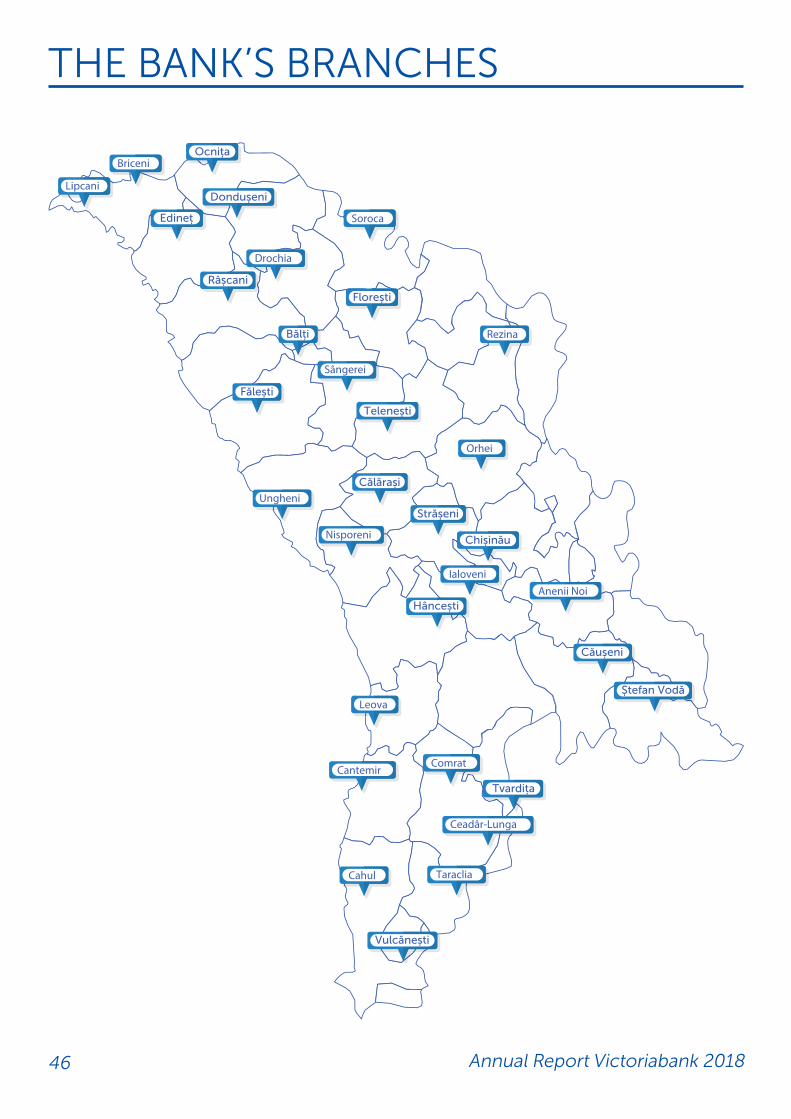

THE BANK’S BRANCHES 44

EXTERNAL AUDITOR’S REPORT 48

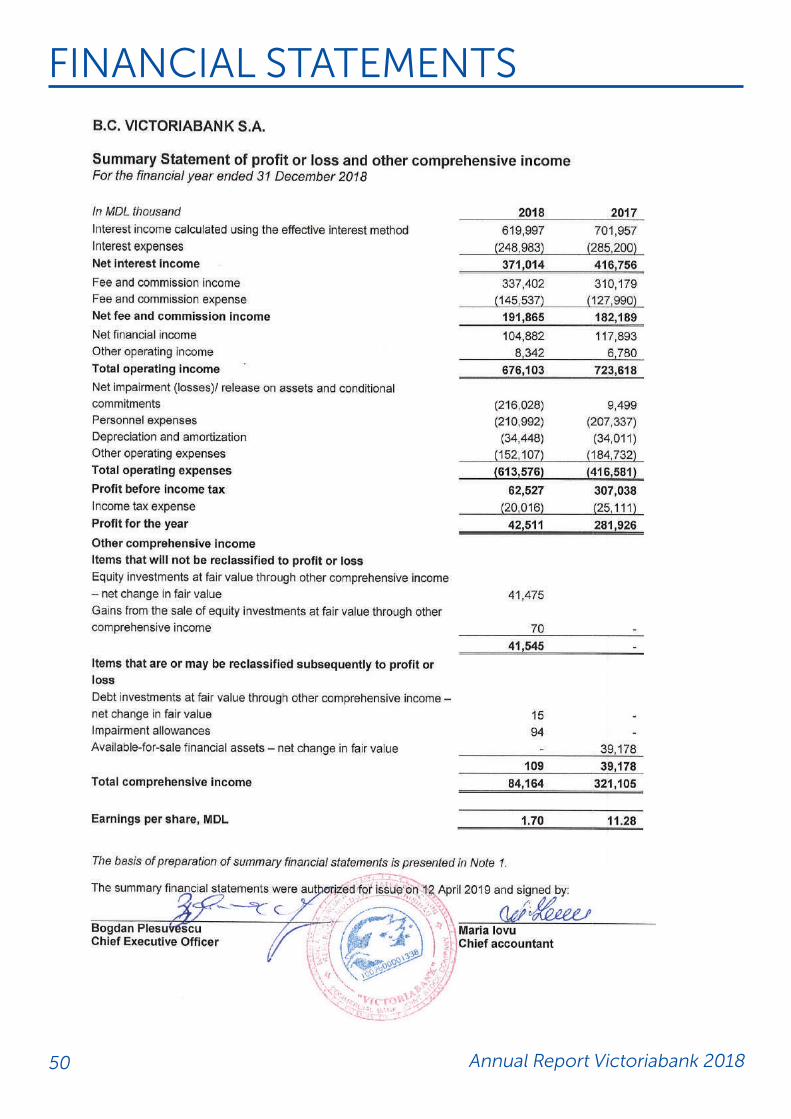

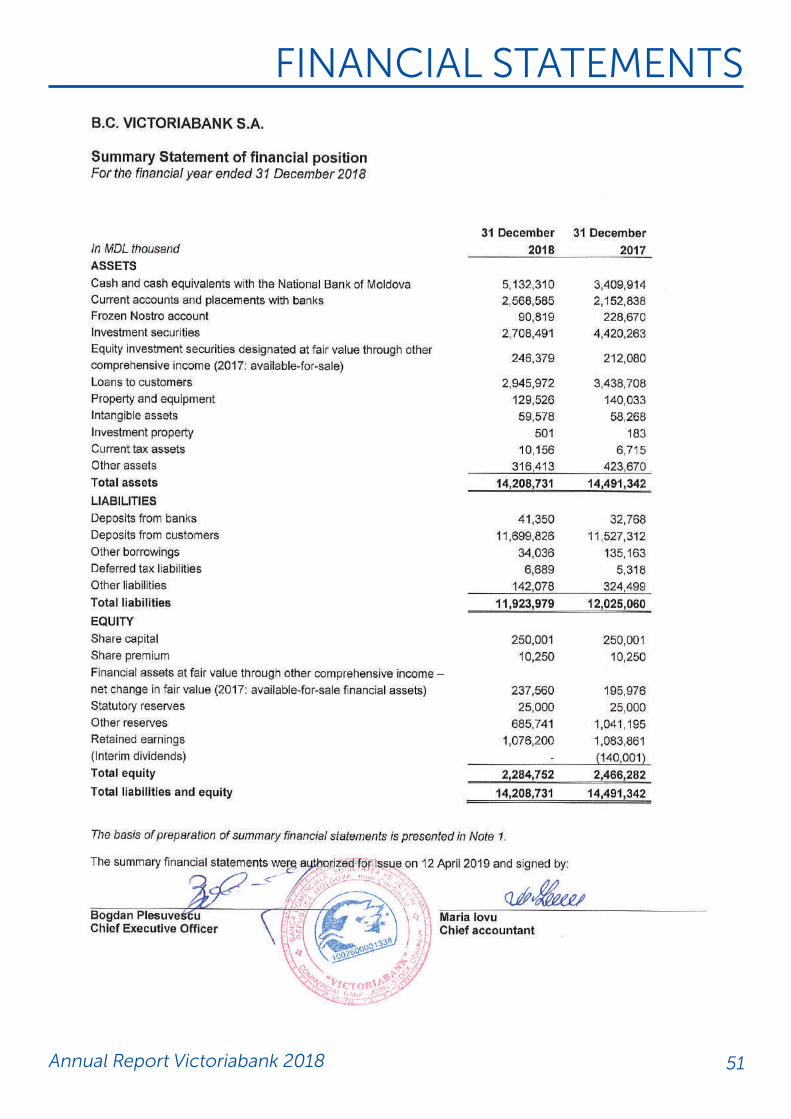

FINANCIAL STATEMENTS 50

4 Annual Report Victoriabank 2018

MANAGEMENT MESSAGE

Message from the President of Executive Board

2018 – the year of Victoriabank’s integration into the Banca Transilvania Financial Group

For Victoriabank, 2018 was a year of transition to a new business model, replicated from its major shareholder, Banca Transilvania. So far, the following principles in BT activity have been a priority for Victoriabank: ensuring transparency of activity, supporting businesses and indivi- duals, developing alternative banking channels, improving services and products and inte- grating the two banks’ teams. Thus, in just a year after entering the group, the following first results are already noticeable:

• Following the improved transparency of the bank’s shareholding structure, the intensive supervision regime of Victoriabank was cancelled;

• For the first time in Moldova, a platform for the sale of assets owned by the bank was launched, the amount of online sales conducted through it doubling compared to 2017;

• The amount of non-performing loans decreased by about 10 million EURO, as a result of the debt recovery strategy;

• The operations and the lending activities have been centralized following the reorga- nization of business lines;

• A new lending model for individuals was launched, similar to the one implemented by BT;

• Some BT products have been replicated to support businesses - CPAG (Contul Primul An Gratuit), a service package for start-ups, provided free of charge; ROFG (Rapid Ordinar Fără Garanții), a product specifically designed for SMEs and PSGB (Plafon de Scrisori de Garanții Bancare) for customers participating in auctions.

These results are due to the ambition and dedication of both teams, and last but not least, the support provided by the shareholders. I express my deepest gratitude for the trust put in Victoriabank and the plans of the whole team. Our efforts were and still remain focused on the welfare of investors, customers and the team.

Bogdan Plesuvescu,

President of the Executive Board

Victoriabank

5Annual Report Victoriabank 2018

MANAGEMENT MESSAGE

Message from the Chairman of the Board of Directors

2018 – a year of transformations for Victoriabank

Dear shareholders,

I feel honored to convey this message of deepest appreciation for your confidence in Victoriabank’s projects and achievements.

2018 was a year of major changes for Victoriabank, a year of entry of the first Moldovan commercial bank into the largest financial group in Romania - Banca Transilvania.

Banca Transilvania marked the beginning of a new chapter in the development of the banking sector and the overall business environment in the Republic of Moldova. In this first year since we’ve been one team, the bank’s reorganization plan has been launched by implementing the best BT practices in relations with customers, in terms of products and services, technology and team, and the results of the group’s involvement are already visible. The number of customers increased by almost 10%, reaching over 620,000. The credit portfolio for individuals grew by 26% and reached 844 million lei. Victoriabank has also made progress in terms of banking operations using bank cards: the number of cards issued in 2018 increased by 30% compared to 2017 and reached a total amount of around 310,000 cards in circulation. More than 500 Moldovan entrepreneurs have so far benefited from BT replicated products for businesses.

A very important factor in ensuring the success of group membership and in facilitating communication between the two parties is that both Victoriabank and its major shareholder BT operate in the same segment in the banking sector. This is an additional advantage for both banks, ensuring an exchange of experience, practices and strategies that result in even better performance.

Guided by Banca Transilvania, which in 2018 became the biggest financial group from Romania, we are convinced that in a short time we will be able to rich the same performance and to reconfirm our position on the market as ”The first Bank in Moldova”.

Victor Turcan,

Chair of the Board

Victoriabank

6 Annual Report Victoriabank 2018

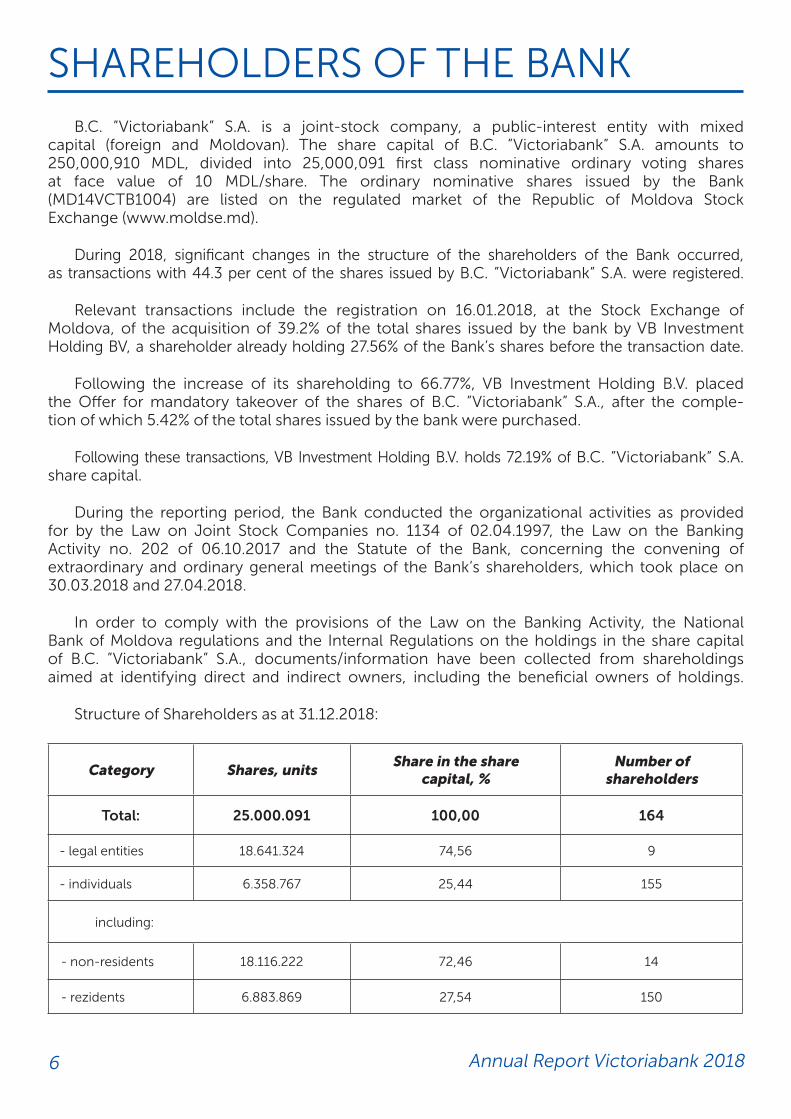

SHAREHOLDERS OF THE BANKB.C. ”Victoriabank” S.A. is a joint-stock company, a public-interest entity with mixed

capital (foreign and Moldovan). The share capital of B.C. ”Victoriabank” S.A. amounts to 250,000,910 MDL, divided into 25,000,091 first class nominative ordinary voting shares at face value of 10 MDL/share. The ordinary nominative shares issued by the Bank (MD14VCTB1004) are listed on the regulated market of the Republic of Moldova Stock Exchange (www.moldse.md).

During 2018, significant changes in the structure of the shareholders of the Bank occurred, as transactions with 44.3 per cent of the shares issued by B.C. ”Victoriabank” S.A. were registered.

Relevant transactions include the registration on 16.01.2018, at the Stock Exchange of Moldova, of the acquisition of 39.2% of the total shares issued by the bank by VB Investment Holding BV, a shareholder already holding 27.56% of the Bank’s shares before the transaction date.

Following the increase of its shareholding to 66.77%, VB Investment Holding B.V. placed the Offer for mandatory takeover of the shares of B.C. ”Victoriabank” S.A., after the comple- tion of which 5.42% of the total shares issued by the bank were purchased.

Following these transactions, VB Investment Holding B.V. holds 72.19% of B.C. ”Victoriabank” S.A. share capital.

During the reporting period, the Bank conducted the organizational activities as provided for by the Law on Joint Stock Companies no. 1134 of 02.04.1997, the Law on the Banking Activity no. 202 of 06.10.2017 and the Statute of the Bank, concerning the convening of extraordinary and ordinary general meetings of the Bank’s shareholders, which took place on 30.03.2018 and 27.04.2018.

In order to comply with the provisions of the Law on the Banking Activity, the National Bank of Moldova regulations and the Internal Regulations on the holdings in the share capital of B.C. ”Victoriabank” S.A., documents/information have been collected from shareholdings aimed at identifying direct and indirect owners, including the beneficial owners of holdings.

Structure of Shareholders as at 31.12.2018:

Category Shares, unitsShare in the share

capital, %Number of

shareholders

Total: 25.000.091 100,00 164

- legal entities 18.641.324 74,56 9

- individuals 6.358.767 25,44 155

including:

- non-residents 18.116.222 72,46 14

- rezidents 6.883.869 27,54 150

7Annual Report Victoriabank 2018

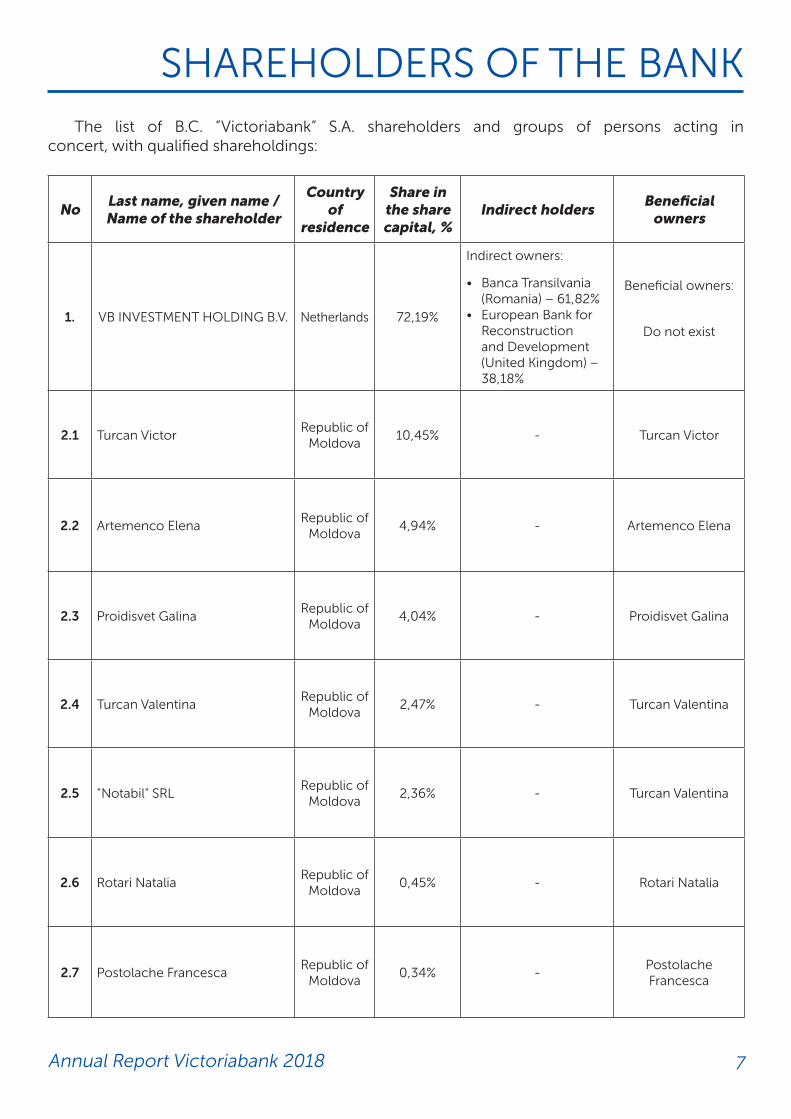

The list of B.C. ”Victoriabank” S.A. shareholders and groups of persons acting in concert, with qualified shareholdings:

NoLast name, given name / Name of the shareholder

Country of

residence

Share in the share capital, %

Indirect holdersBeneficial

owners

1. VB INVESTMENT HOLDING B.V. Netherlands 72,19%

Indirect owners:

• Banca Transilvania (Romania) – 61,82%

• European Bank for Reconstruction and Development (United Kingdom) – 38,18%

Beneficial owners:

Do not exist

2.1 Turcan VictorRepublic of

Moldova10,45% - Turcan Victor

2.2 Artemenco ElenaRepublic of

Moldova4,94% - Artemenco Elena

2.3 Proidisvet GalinaRepublic of

Moldova4,04% - Proidisvet Galina

2.4 Turcan ValentinaRepublic of

Moldova2,47% - Turcan Valentina

2.5 "Notabil" SRLRepublic of

Moldova2,36% - Turcan Valentina

2.6 Rotari NataliaRepublic of

Moldova0,45% - Rotari Natalia

2.7 Postolache FrancescaRepublic of

Moldova0,34% -

Postolache Francesca

SHAREHOLDERS OF THE BANK

8 Annual Report Victoriabank 2018

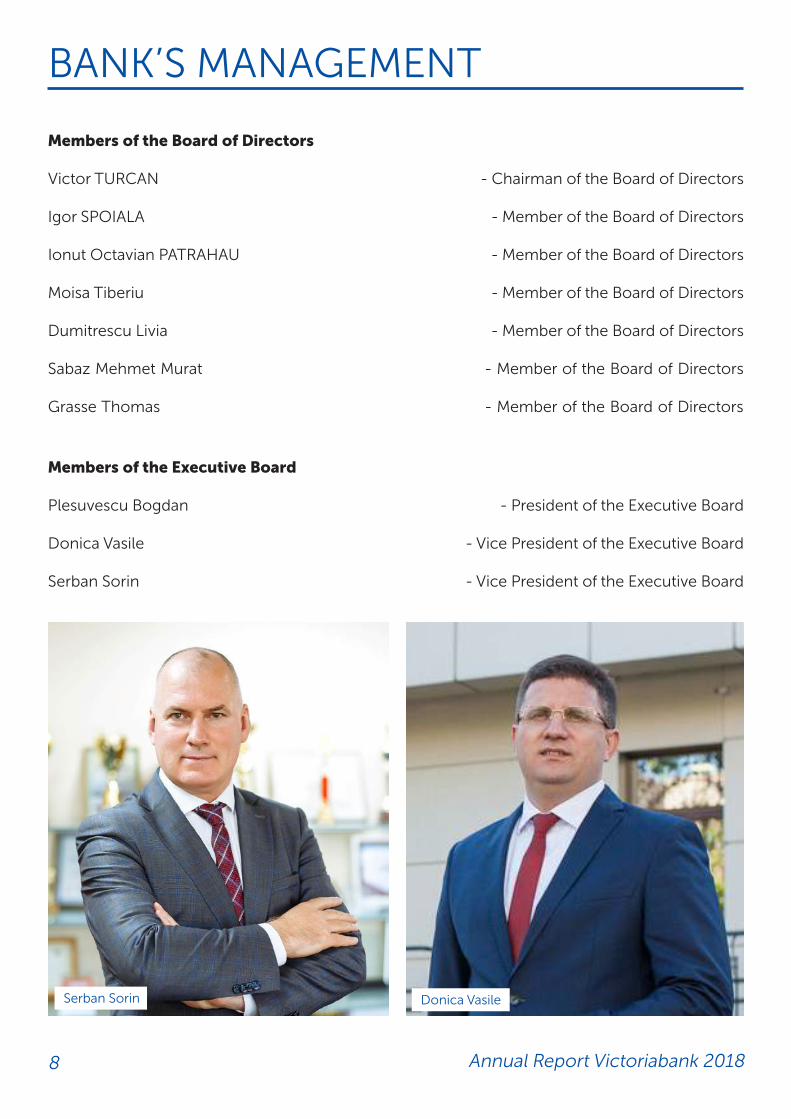

BANK’S MANAGEMENT

Members of the Board of Directors

Victor TURCAN - Chairman of the Board of Directors

Igor SPOIALA - Member of the Board of Directors

Ionut Octavian PATRAHAU - Member of the Board of Directors

Moisa Tiberiu - Member of the Board of Directors

Dumitrescu Livia - Member of the Board of Directors

Sabaz Mehmet Murat - Member of the Board of Directors

Grasse Thomas - Member of the Board of Directors

Members of the Executive Board

Plesuvescu Bogdan - President of the Executive Board

Donica Vasile - Vice President of the Executive Board

Serban Sorin - Vice President of the Executive Board

Donica Vasile Serban Sorin

9Annual Report Victoriabank 2018

BANK’S MANAGEMENT

Plesuvescu Bogdan

10 Annual Report Victoriabank 2018

The year 2018 was full of important events in terms of new product launches, digitization of processes and the engagement of B.C. ”Victoriabank” S.A. in activities with social, cultural and economic impact. The main events of the year are presented below:

January:

B.C. ”Victoriabank” S.A. became part of Banca Transilvania’s financial group.

February:

Victoriabank implemented the cash-in function at its ATMs, which allows customers to deposit money on their card and current accounts. Thus, refilling the card account has be-come easier than ever, without depending on the work schedule of the Bank’s subdivisions and without having to submit any identity document.

March:

On March 5, 2018, Banca Transilvania and the European Bank for Reconstruction and Development (EBRD) became majority shareholders, holding 66.77% of the share capital of B.C. ”Victoriabank” S.A.

Since March 5, 2018, the management of B.C. ”Victoriabank” S.A., the third largest bank in the Republic of Moldova, has two new members, Bogdan Plesuvescu - President of the Executive Board and Vasile Donica - Vice President of the Executive Board, approved by the National Bank of.

B.C. ”Victoriabank” S.A. successfully passed the certification procedure confirming compli- ance with the security requirements in the process of storing, transmitting and processing cardholder data according to the PCI DSS standard. The certification was conducted by Compliance Control Ltd., the leading provider of information security solutions.

B.C. ”Victoriabank” S.A. launches the macroeconomic analysis and forecasting service, which will provide information on the latest macroeconomic and financial developments and the short and medium term prospects for the Republic of Moldova and the international environ- ment for both bank customers and the general public. Thus, the Bank team will develop and publish weekly macroeconomic analysis reports, in collaboration with an expert recognized in Romania and internationally, Dr. Andrei Radulescu, Director of Macroeconomic Analysis at Banca Transilvania. The ”VB Weekly” Newsletter will analyze the recent developments of macro-financial indicators in the Republic of Moldova and abroad (Europe, Russia, United States and Romania). The report is informative and can be used by the population and compa- nies (customers or potential customers) to provide a sound basis for consumer and investment decisions.

May:

Sorin Serban joins Victoriabank’s top management, as Vice President, Chief Risk Officer.

Victoriabank comes with a new approach for customers by reorganizing two main business lines - retail and corporate.

June:

For the first time in the Republic of Moldova, Victoriabank launched the website for the sale of immovable (industrial buildings, land, houses/villas, apartments, office premises) and movable assets (goods, rights, vehicles, machinery). The website is designed for all business

MAIN EVENTS IN 2018

11Annual Report Victoriabank 2018

people and investors, regardless of the economic sector in which they operate, but also individu-als who want to purchase apartments, vehicles or other assets under insolvency proceedings.

B.C. ”Victoriabank” S.A. launched the VictoriaMobile digital fingerprint authentication tool!

B.C. ”Victoriabank” S.A. - partner of ”Fosfor” electronic music festival.

July:

The bank launched the VB Lunch card, the digital version of the printed lunch tickets.

The newspaper Ziarul Financiar, Banca Transilvania and Victoriabank organize the Confe- rence ”100 ideas for growth: Republic of Moldova - Romania. Investments, trade, financing”, in Chisinau. This is the first ZF initiative of this kind dedicated to business partnerships between the two countries.

Victoriabank together with Banca Transilvania supported the TIFF Chisinau Festival - the largest film festival in Romania, which has already become a tradition in Moldova.

August:

B.C. ”Victoriabank” S.A. launched a new concept of lending to individuals, consisting of 3 new products: real estate credit, no-collateral consumer credit and collateral guaranteed consumer credit, in compliance with the highest consumer rights protection standards.

Victoriabank’s mobile banking application becomes even more secure with Face ID or Touch ID logging for all customers using Apple smartphone.

The Executive Board of the National Bank of Moldova (NBM) decided to terminate the intensive supervision regime of B.C. ”Victoriabank” S.A. since 22.08.2018, based on the NBM’s finding that the Bank has a transparent structure and complies with the requirements laid down in the normative acts of the National Bank. At the same time, the Bank’s new Board of Directors, operational since 09.08.2018, was also approved.

September:

B.C. ”Victoriabank” S.A. comes closer to its customers by simplifying the transfer and settlement of foreign currency transactions, executing transfers to customers holding an account with Banca Transilvania with a commission of EUR 10.

Victoriabank supports the National Opera and Ballet Theater ”Maria Biesu”.

Victoriabank supports the Ethno Jazz Festival 2018, the XVIIth edition of the most popular and long-lived jazz festival in Chisinau.

150 branches and agencies of Transilvania Bank accept cash transactions in Moldovan Lei, such as: foreign exchange, withdrawals or cash deposits.

October:

B.C. ”Victoriabank” S.A. launches the First Year FREE Account with Victoriabank - FYFA

November:

Victoriabank supports the Generosity Gala for the fourth consecutive years; Victoriabank provides financial support to CCF Moldova (Child, Community, Family), a representative of HHC UK (Hope and Homes for Children).

MAIN EVENTS IN 2018

MANAGEMENT REPORT2 0 1 8

13Annual Report Victoriabank 2018

ECONOMIC CLIMATE MACROECONOMIC SITUATION

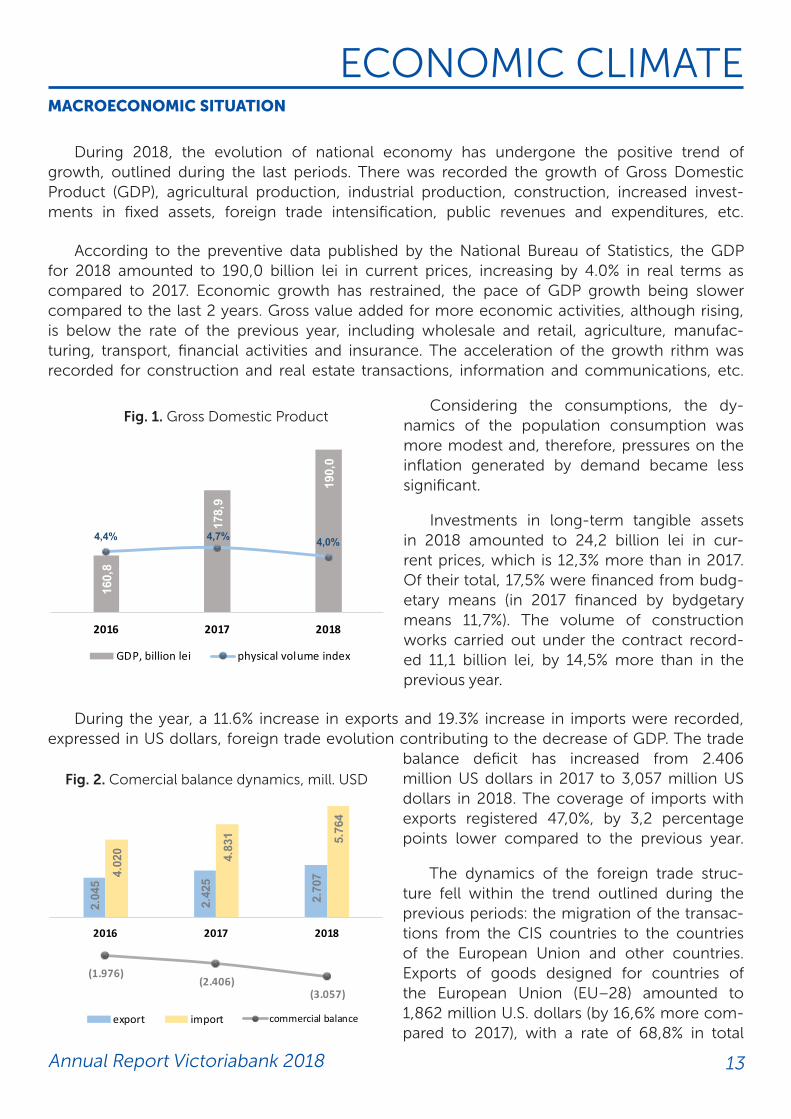

During 2018, the evolution of national economy has undergone the positive trend of growth, outlined during the last periods. There was recorded the growth of Gross Domestic Product (GDP), agricultural production, industrial production, construction, increased invest- ments in fixed assets, foreign trade intensification, public revenues and expenditures, etc.

According to the preventive data published by the National Bureau of Statistics, the GDP for 2018 amounted to 190,0 billion lei in current prices, increasing by 4.0% in real terms as compared to 2017. Economic growth has restrained, the pace of GDP growth being slower compared to the last 2 years. Gross value added for more economic activities, although rising, is below the rate of the previous year, including wholesale and retail, agriculture, manufac- turing, transport, financial activities and insurance. The acceleration of the growth rithm was recorded for construction and real estate transactions, information and communications, etc.

Considering the consumptions, the dy-namics of the population consumption was more modest and, therefore, pressures on the inflation generated by demand became less significant.

Investments in long-term tangible assets in 2018 amounted to 24,2 billion lei in cur-rent prices, which is 12,3% more than in 2017. Of their total, 17,5% were financed from budg-etary means (in 2017 financed by bydgetary means 11,7%). The volume of construction works carried out under the contract record-ed 11,1 billion lei, by 14,5% more than in the previous year.

During the year, a 11.6% increase in exports and 19.3% increase in imports were recorded, expressed in US dollars, foreign trade evolution contributing to the decrease of GDP. The trade

balance deficit has increased from 2.406 million US dollars in 2017 to 3,057 million US dollars in 2018. The coverage of imports with exports registered 47,0%, by 3,2 percentage points lower compared to the previous year.

The dynamics of the foreign trade struc-ture fell within the trend outlined during the previous periods: the migration of the transac-tions from the CIS countries to the countries of the European Union and other countries. Exports of goods designed for countries of the European Union (EU–28) amounted to 1,862 million U.S. dollars (by 16,6% more com-pared to 2017), with a rate of 68,8% in total

Fig. 1. Gross Domestic Product

Fig. 2. Comercial balance dynamics, mill. USD

160,

8

178,

9

190,

0

4,4% 4,7% 4,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

8,0%

9,0%

10,0%

11,0%

12,0%

13,0%

145,0

150,0

155,0

160,0

165,0

170,0

175,0

180,0

185,0

190,0

195,0

2016 2017 2018

Fig. 1 Gross Domestic Product

GDP, billion lei physical volume index

2.04

5

2.42

5

2.70

74.02

0 4.83

1 5.76

4

(1.976)(2.406)

(3.057)-4.000

-3.000

-2.000

-1.000

0

1.000

2.000

3.000

4.000

5.000

6.000

2016 2017 2018

Fig. 2 Trade balance dynamics, mil.USD

export import commercial balance

14 Annual Report Victoriabank 2018

ECONOMIC CLIMATE MACROECONOMIC SITUATION

exports (65,9% in 2017). CIS countries were present in thje Republic of Moldova’s exports with a share of 15.4% (in 2017 – 19,1%), which corresponds to a value of 416 million U.S. dollars. Exports of goods to these countries decreased by 10.1% compared to 2017, mainly due to the increase in volumes to the main partners: the Russian Federation and Belarus.

According to the information available for 9 months of 2018, revenues and expenditures of the national public budget have been increasing.

In 2018 the monetary aggregates recorded a positive dynamics. The main contribution to this development was mainly determined by the increase in sight deposits in national currency, sight deposits in foreign currency and money in circulation. The money supply (M3) recorded 83.2 billion lei, increasing in 2018 by 7.8%. In the structure of money supply, 25,3% goes to money in circulation and 33.8% to sight deposits.

The monetary policy implemented by the NBM ensured the decrease of the infla-tion rate compared to the previous year. The average annual inflation rate constituted 3,0%, compared to 6,6% recorded in 2017, being mainly conditioned by the evolution of pric-es for food and non-food goods. In 2018, the change in prices has been influenced by money supply growth, the evolution of the exchange rate, global energy and agricul-tural prices, regulated products and services prices, population income dynamics, etc.

The net supply of foreign currency from natural persons amounted to 2,1 billion US Dollars, recording the highest value in the past 5 years. Over 2/3 of the net currency offer is generated by the funds in EUR. Net sales of foreign currency to legal entities were fully covered from the account of the net supply of foreign currency from natural persons, as well as during 2016-2017.

The increase in the supply of currency in 2018 has been influenced, among others, by the increase in the volume of transfers through banks in the Republic of Moldova (on a net basis) by 5,6% compared to 2017, totalling 1,267 million USD. In the structure of transfers, the highest share is in EUR-47.3%, followed by that in USD-45,5% and in RUB – 7,2%.

During 2018, the national currency depre-ciated from 17,10 lei to 17,14 lei for 1 US dollar and has been appreciated from 20,41 lei to 19,52 lei for 1 EUR.

Fig. 3. Inflation and money supply

Fig. 4. Net transfers banking system, mln. USD

6,4%

6,6%

3,0%

10,2%9,4%

7,8%

5%

9,0%

6,5%6,5%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

2016 2017 2018

Fig.3 Inflation and money supply

average annual inflation money supply evolutioninflation target base rate

545

599

576

394 49

1 599

140

110 91

-4,4%

11,2%

5,6%

-6 ,0%

-1 ,0%

4,0 %

9,0 %

14, 0%

19, 0%

0

200

400

600

800

1.0 00

1.2 00

1.4 00

2016 2017 2018

Fig. 4 Net transfers banking system, mill.USD

USD EUR RUB evolution, %

1.0791.200

1.267

15Annual Report Victoriabank 2018

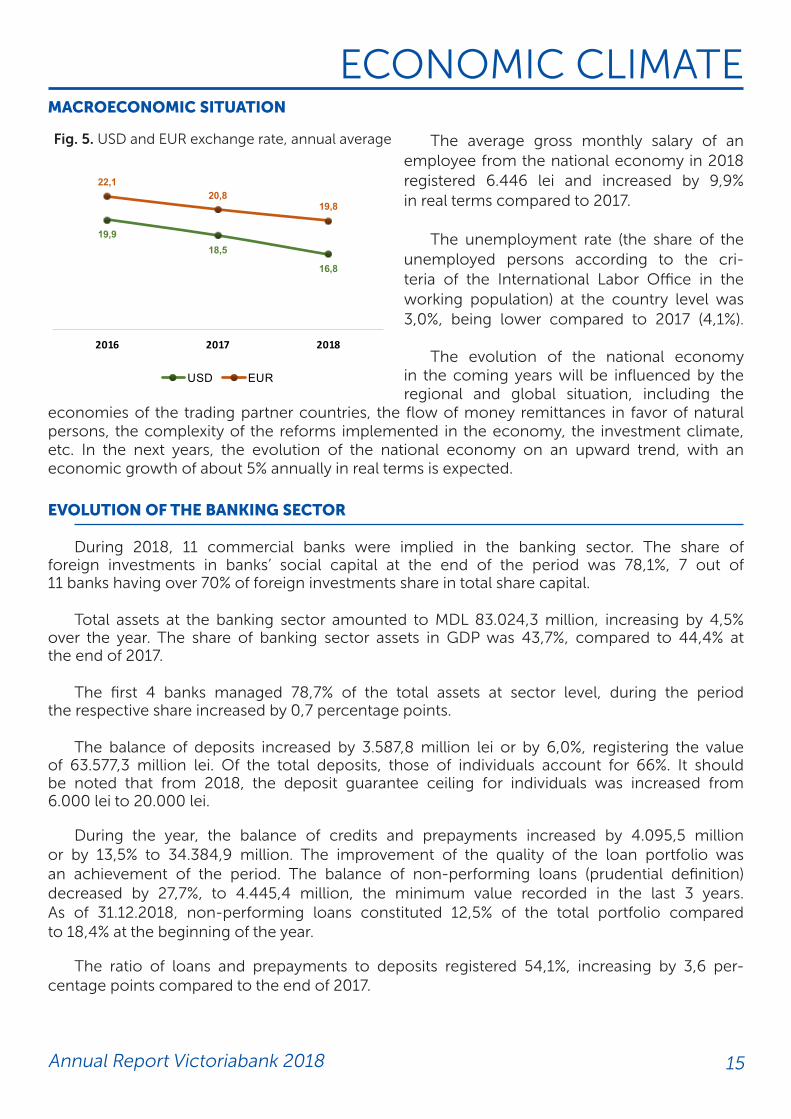

The average gross monthly salary of an employee from the national economy in 2018 registered 6.446 lei and increased by 9,9% in real terms compared to 2017.

The unemployment rate (the share of the unemployed persons according to the cri-teria of the International Labor Office in the working population) at the country level was 3,0%, being lower compared to 2017 (4,1%).

The evolution of the national economy in the coming years will be influenced by the regional and global situation, including the

economies of the trading partner countries, the flow of money remittances in favor of natural persons, the complexity of the reforms implemented in the economy, the investment climate, etc. In the next years, the evolution of the national economy on an upward trend, with an economic growth of about 5% annually in real terms is expected.

EVOLUTION OF THE BANKING SECTOR

During 2018, 11 commercial banks were implied in the banking sector. The share of foreign investments in banks’ social capital at the end of the period was 78,1%, 7 out of 11 banks having over 70% of foreign investments share in total share capital.

Total assets at the banking sector amounted to MDL 83.024,3 million, increasing by 4,5% over the year. The share of banking sector assets in GDP was 43,7%, compared to 44,4% at the end of 2017.

The first 4 banks managed 78,7% of the total assets at sector level, during the period the respective share increased by 0,7 percentage points.

The balance of deposits increased by 3.587,8 million lei or by 6,0%, registering the value of 63.577,3 million lei. Of the total deposits, those of individuals account for 66%. It should be noted that from 2018, the deposit guarantee ceiling for individuals was increased from 6.000 lei to 20.000 lei.

During the year, the balance of credits and prepayments increased by 4.095,5 million or by 13,5% to 34.384,9 million. The improvement of the quality of the loan portfolio was an achievement of the period. The balance of non-performing loans (prudential definition) decreased by 27,7%, to 4.445,4 million, the minimum value recorded in the last 3 years. As of 31.12.2018, non-performing loans constituted 12,5% of the total portfolio compared to 18,4% at the beginning of the year.

The ratio of loans and prepayments to deposits registered 54,1%, increasing by 3,6 per- centage points compared to the end of 2017.

ECONOMIC CLIMATE MACROECONOMIC SITUATION

Fig. 5. USD and EUR exchange rate, annual average

19,918,5

16,8

22,120,8

19,8

10,0

12,0

14,0

16,0

18,0

20,0

22,0

24,0

2016 2017 2018

Fig. 5 USD and EUR exchange rate, annual average

USD EUR

16 Annual Report Victoriabank 2018

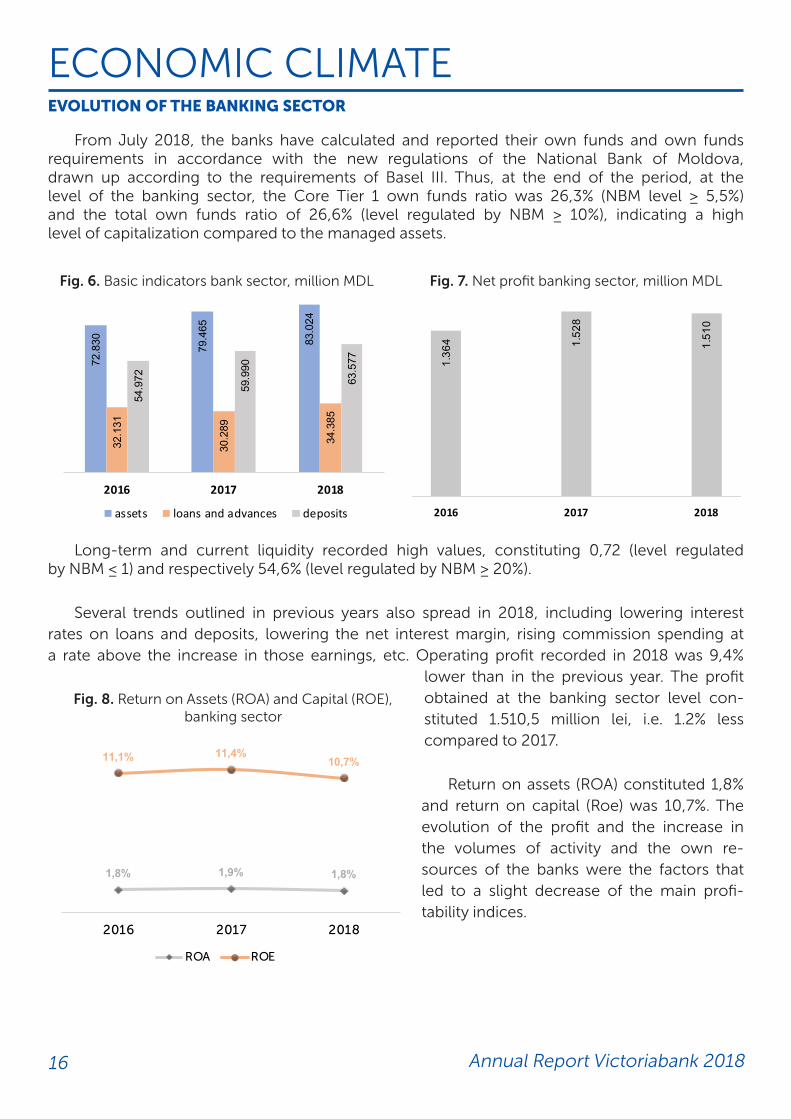

From July 2018, the banks have calculated and reported their own funds and own funds requirements in accordance with the new regulations of the National Bank of Moldova, drawn up according to the requirements of Basel III. Thus, at the end of the period, at the level of the banking sector, the Core Tier 1 own funds ratio was 26,3% (NBM level ≥ 5,5%) and the total own funds ratio of 26,6% (level regulated by NBM ≥ 10%), indicating a high level of capitalization compared to the managed assets.

Long-term and current liquidity recorded high values, constituting 0,72 (level regulated by NBM ≤ 1) and respectively 54,6% (level regulated by NBM ≥ 20%).

Several trends outlined in previous years also spread in 2018, including lowering interest rates on loans and deposits, lowering the net interest margin, rising commission spending at a rate above the increase in those earnings, etc. Operating profit recorded in 2018 was 9,4%

lower than in the previous year. The profit obtained at the banking sector level con-stituted 1.510,5 million lei, i.e. 1.2% less compared to 2017.

Return on assets (ROA) constituted 1,8% and return on capital (Roe) was 10,7%. The evolution of the profit and the increase in the volumes of activity and the own re- sources of the banks were the factors that led to a slight decrease of the main profi- tability indices.

ECONOMIC CLIMATE EVOLUTION OF THE BANKING SECTOR

Fig. 6. Basic indicators bank sector, million MDL Fig. 7. Net profit banking sector, million MDL

Fig. 8. Return on Assets (ROA) and Capital (ROE), banking sector

1,8% 1,9% 1,8%

11,1% 11,4%10,7%

0,0%

2,0%

4,0%

6,0%

8,0%

10,0%

12,0%

2016 2017 2018

Fig. 8 Rentabilitatea activelor (ROA) şi capitalului (ROE), sector bancar

ROA ROE

72.8

30 79.4

65

83.0

24

32.1

31

30.2

89

34.3

85

54.9

72

59.9

90

63.5

77

0

10.000

20.000

30.000

40.000

50.000

60.000

70.000

80.000

90.000

2016 2017 2018

Fig. 6 Key indicators banking sector, mill.lei

assets loans and advances deposits

1.36

4 1.52

8

1.51

0

0

200

400

600

800

1.000

1.200

1.400

1.600

1.800

2016 2017 2018

Fig. 7 Net profit banking sector, mill.lei

17Annual Report Victoriabank 2018

ACTIVITY PERFORMANCE OFB.C. ”VICTORIABANK” S.A.

EVOLUTION OF FINANCIAL RESULTS

According to the majority of activity indicators, B.C. ”Victoriabank” S.A. maintained its position on the market, ranking third among the banks in the Republic of Moldova.

Due to the fact that Transilvania Bank and the EBRD have become the main shareholders in B.C. ”Victoriabank” S.A. in January 2018, on 22.08.2018 the executive Board of the National Bank of Moldova decided to exclude the regime of intensive supervision of the Bank.

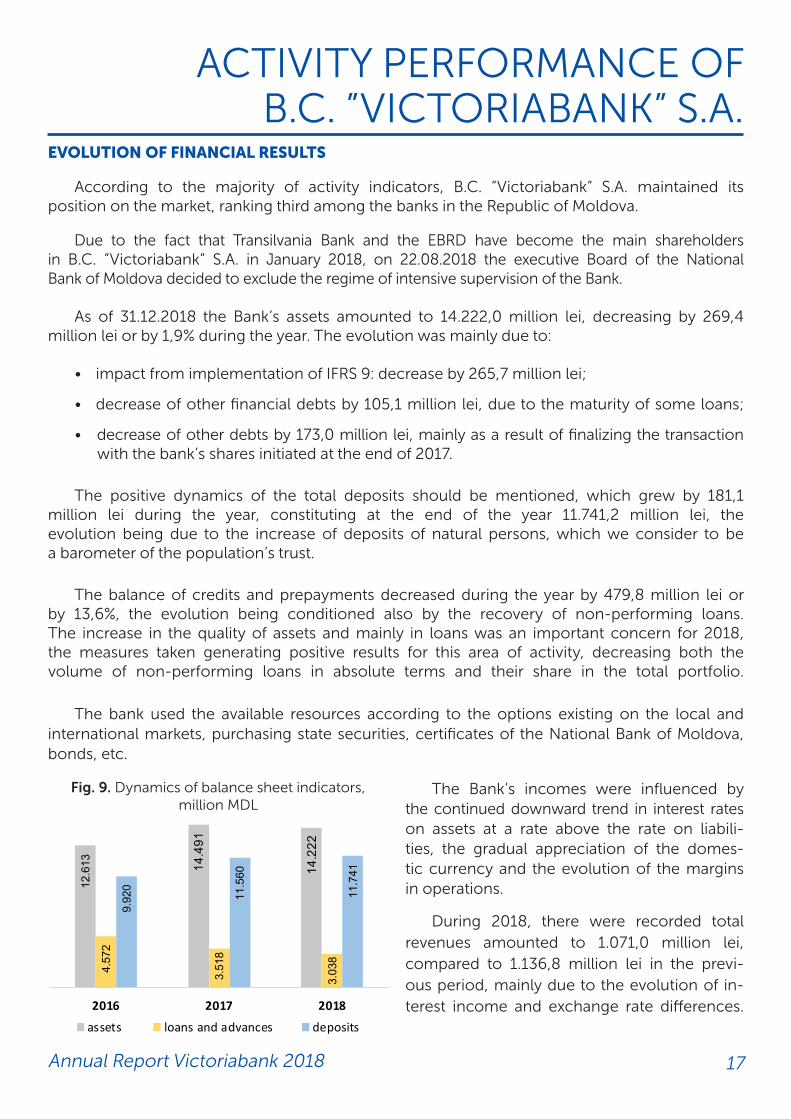

As of 31.12.2018 the Bank’s assets amounted to 14.222,0 million lei, decreasing by 269,4 million lei or by 1,9% during the year. The evolution was mainly due to:

• impact from implementation of IFRS 9: decrease by 265,7 million lei;

• decrease of other financial debts by 105,1 million lei, due to the maturity of some loans;

• decrease of other debts by 173,0 million lei, mainly as a result of finalizing the transaction with the bank’s shares initiated at the end of 2017.

The positive dynamics of the total deposits should be mentioned, which grew by 181,1 million lei during the year, constituting at the end of the year 11.741,2 million lei, the evolution being due to the increase of deposits of natural persons, which we consider to be a barometer of the population’s trust.

The balance of credits and prepayments decreased during the year by 479,8 million lei or by 13,6%, the evolution being conditioned also by the recovery of non-performing loans. The increase in the quality of assets and mainly in loans was an important concern for 2018, the measures taken generating positive results for this area of activity, decreasing both the volume of non-performing loans in absolute terms and their share in the total portfolio.

The bank used the available resources according to the options existing on the local and international markets, purchasing state securities, certificates of the National Bank of Moldova, bonds, etc.

The Bank’s incomes were influenced by the continued downward trend in interest rates on assets at a rate above the rate on liabili-ties, the gradual appreciation of the domes-tic currency and the evolution of the margins in operations.

During 2018, there were recorded total revenues amounted to 1.071,0 million lei, compared to 1.136,8 million lei in the previ-ous period, mainly due to the evolution of in-terest income and exchange rate differences.

Fig. 9. Dynamics of balance sheet indicators, million MDL

12.6

13 14.4

91

14.2

22

4.57

2

3.51

8

3.03

8

9.92

0

11.5

60

11.7

41

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000

2016 2017 2018

Fig. 9 Dynamics of balance sheet indicators, mill.lei

assets loans and advances deposits

18 Annual Report Victoriabank 2018

The total expenditures amounted to 1.028,4 million lei, by 173,6 million lei more than in 2017. The increase in expenditure was driven by the significant increase of those related to the impairment of assets, which increased compared to the previous year with 210,2 million lei, as a result of the fact that the Bank has applied a conservative approach regarding the formation of provisions for assets, reevaluating their risks and guarantees.

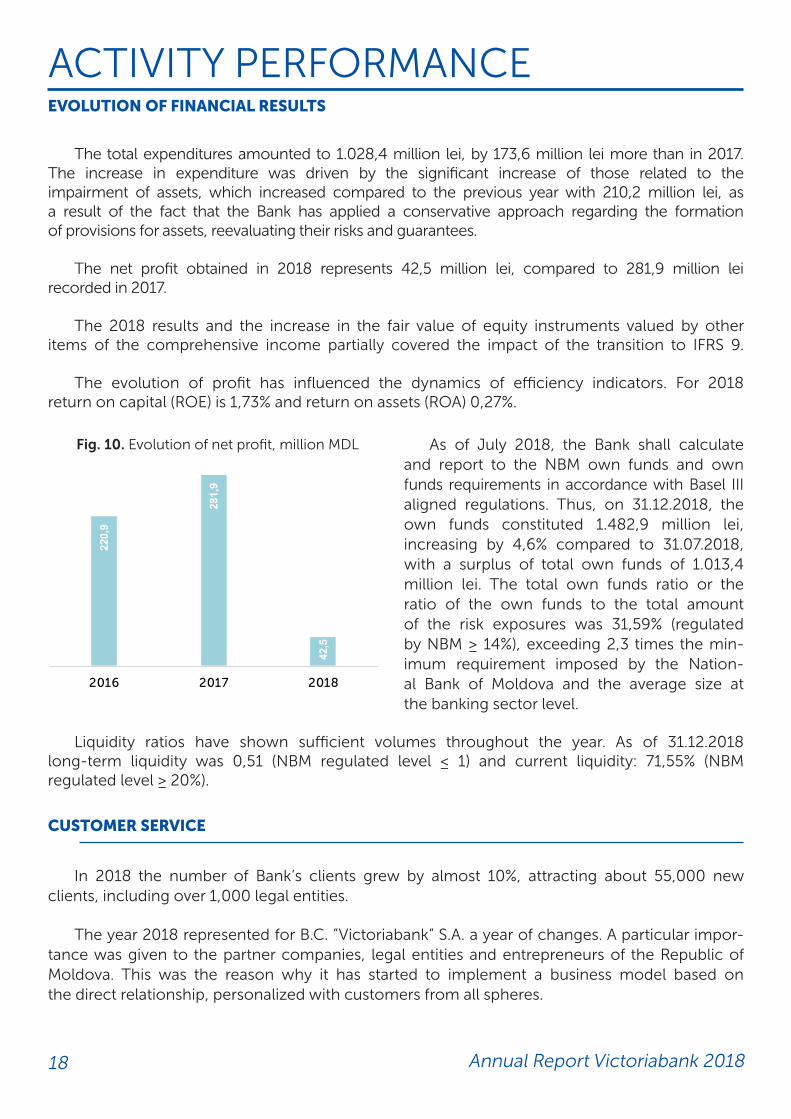

The net profit obtained in 2018 represents 42,5 million lei, compared to 281,9 million lei recorded in 2017.

The 2018 results and the increase in the fair value of equity instruments valued by other items of the comprehensive income partially covered the impact of the transition to IFRS 9.

The evolution of profit has influenced the dynamics of efficiency indicators. For 2018 return on capital (ROE) is 1,73% and return on assets (ROA) 0,27%.

As of July 2018, the Bank shall calculate and report to the NBM own funds and own funds requirements in accordance with Basel III aligned regulations. Thus, on 31.12.2018, the own funds constituted 1.482,9 million lei, increasing by 4,6% compared to 31.07.2018, with a surplus of total own funds of 1.013,4 million lei. The total own funds ratio or the ratio of the own funds to the total amount of the risk exposures was 31,59% (regulated by NBM ≥ 14%), exceeding 2,3 times the min-imum requirement imposed by the Nation-al Bank of Moldova and the average size at the banking sector level.

Liquidity ratios have shown sufficient volumes throughout the year. As of 31.12.2018 long-term liquidity was 0,51 (NBM regulated level ≤ 1) and current liquidity: 71,55% (NBM regulated level ≥ 20%).

CUSTOMER SERVICE

In 2018 the number of Bank’s clients grew by almost 10%, attracting about 55,000 new clients, including over 1,000 legal entities.

The year 2018 represented for B.C. ”Victoriabank” S.A. a year of changes. A particular impor-tance was given to the partner companies, legal entities and entrepreneurs of the Republic of Moldova. This was the reason why it has started to implement a business model based on the direct relationship, personalized with customers from all spheres.

ACTIVITY PERFORMANCEEVOLUTION OF FINANCIAL RESULTS

Fig. 10. Evolution of net profit, million MDL

220,

9

281,

9

42,5

0,0

50,0

100,0

150,0

200,0

250,0

300,0

2016 2017 2018

Fig. 10 Evoluţia profitului net, milioane lei

19Annual Report Victoriabank 2018

The new model offers a dedicated approach to corporate, corporate and SME environ-ments or to individual entrepreneurs such as peasant farms (GIs) and individual enterprises (IMs). Dedicated teams of relationship managers were created for each segment to sup-port this approach. Relationship Managers teams support the identification of credit and / or operational solutions for customers, focusing on increasing the quality of Bank services and increasing our customers / partners’ satisfaction in interacting with B.C. ”Victoriabank” S.A. For this purpose, credit flows have been modified and adapted; services provided by the branch offices have improved, as well as the interaction with the Bank through alternative channels, Internet Banking - VB24 Business. The launch of new products and the adaptation or improvement of existing ones began in 2018. The internet banking service - VB24 Business has been relaunched, with new design and functionality, i.e. an easier to use interface and more detailed information.

Considering the expertise of the new shareholder Banca Transilvania and that of the Bank of Entrepreneurs, B.C. ”Victoriabank” S.A. pays particular attention to the SME sector, supporting smaller customers with dedicated products. Starting from the needs of any start-up entrepre-neur, a package of services dedicated to them - First Free Year Account (”CPAG”) was launched. Benefiting from this package, newly established SMEs get a number of gratuities until they reach the age of 1 year after their foundation. This product helps customers save money that would have been paid as commissions for operations through the Bank.

At the same time, the first Credit Rapid (Quick Loan) Without Material Guarantees in the history of B.C. ”Victoriabank” S.A., designed namely for SMEs was launched. This product provides access to quick financing based on clear eligibility criteria and without the need for material guarantees. Being a credit issued for a 5-year term, small companies can benefit from a significant contribution to providing cash for the activity.

The relationship with the main shareholder, Banca Transilvania, as well as the increase of the economic exchanges and the Moldovan investments in Romania and the Romanian ones in Moldova, led to the creation of a dedicated office for relations with Romania, for partners with common interests in Moldova and Romania, who have business relations with Romanian partners. This office provides support to B.C. ”Victoriabank” S.A. in building strong relations with both, Banca Transilvania and with other clients and partners from Romania or Banca Transilvania’s clients with B.C. ”Victoriabank” S.A. or with partners in Moldova. The development of the relationship is also ensured by the currency transfers between B.C. ”Victoriabank” S.A. and Banca Transilvania at a reduced price of 10 EUR / transaction.

Wishing to bring the client more security and firmness in the process of fixing a decision in the financial and investment plan, in 2018 was launched the macroeconomic analysis and Forecast service. It provides clients and the general public with information on the latest macroeconomic and financial developments, the short and medium term prospects for the Republic of Moldova and the international sphere.

ACTIVITY PERFORMANCECUSTOMER SERVICE

20 Annual Report Victoriabank 2018

The electronic certificate was released for the convenience of the client and the constant concern about the rational use of resources. The electronic certificate, combined with the dotBank Informational freeware product, allows the customer to avoid periodic shifts in the Bank’s subdivisions to pick up certificates from the account, saving time, travel expenses, paper and supplies.

For the first time in the Republic of Moldova, an asset sales platform was launched in 2018 to facilitate the process of their recovery in a transparent and efficient way.

In the same year, the bank implemented the electronic food stamps, on the basis of the license issued by the Licensing Chamber. Thus, as a facility for both, employers and company employees, electronic food stamps are another step towards digitising banking services.

For Bank’s retail customers a new Web-banking version was launched. Moreover, a new application - VictoriaMobile with fingerprint authentication face ID options was launched, the availability of cash-in function in the bank’s ATMs was ensured, the list of organisations in favour of which payments can be made through remote service systems has been extended, the ”subscription to invoices” service through WebBanking and MobileWebBanking was imple-mented, etc.

In order to facilitate the access of individuals to purchase a home, B.C. ”Victoriabank” S.A. joined the state program ”Prima Casa” (first house). Besides the advantages offered by the state, the Bank offers even more advantages: free and discounted products, promotions, indi- vidual consulting etc.

Expanding the number and volume of remote operations has allowed to optimize the number of agencies. At the end of 2018, B.C. ”Victoriabank” S.A. managed the activity of 93 subdivisions, including 34 Subsidiaries and 59 Agencies.

We believe that optimization, similar to evolution, is a continuous process. The changes will continue in 2019 as well, by launching and promoting new products and services, conti- nuously improving the existing ones, in order to improve the customer experience in the interaction with B.C. ”Victoriabank” S.A.

WORK ON DEPOSIT ATTRACTION

The main source of financing the bank’s assets remains:

• attracting monetary resources;

• attracting new customers (economic agents) and increasing the deposits in current accounts of legal entities.

ACTIVITY PERFORMANCECUSTOMER SERVICE

21Annual Report Victoriabank 2018

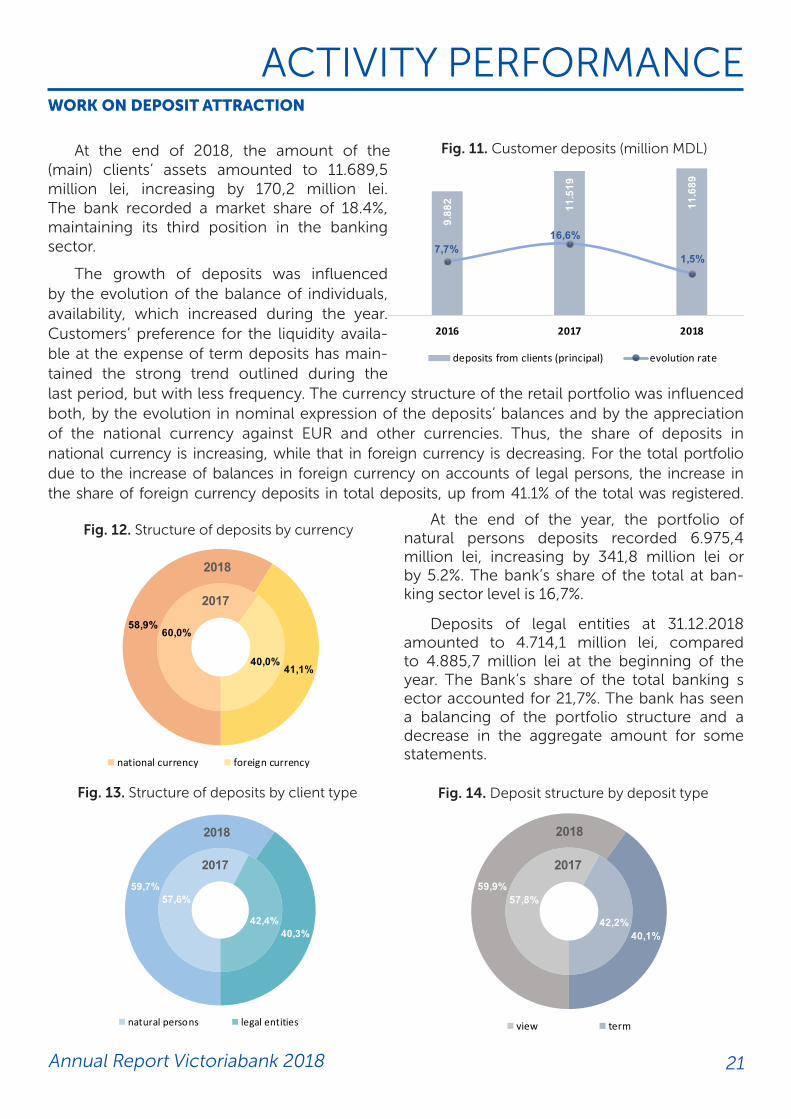

At the end of 2018, the amount of the (main) clients’ assets amounted to 11.689,5 million lei, increasing by 170,2 million lei. The bank recorded a market share of 18.4%, maintaining its third position in the banking sector.

The growth of deposits was influenced by the evolution of the balance of individuals‚ availability, which increased during the year. Customers’ preference for the liquidity availa- ble at the expense of term deposits has main-tained the strong trend outlined during the last period, but with less frequency. The currency structure of the retail portfolio was influenced both, by the evolution in nominal expression of the deposits’ balances and by the appreciation of the national currency against EUR and other currencies. Thus, the share of deposits in national currency is increasing, while that in foreign currency is decreasing. For the total portfolio due to the increase of balances in foreign currency on accounts of legal persons, the increase in the share of foreign currency deposits in total deposits, up from 41.1% of the total was registered.

At the end of the year, the portfolio of natural persons deposits recorded 6.975,4 million lei, increasing by 341,8 million lei or by 5.2%. The bank’s share of the total at ban- king sector level is 16,7%.

Deposits of legal entities at 31.12.2018 amounted to 4.714,1 million lei, compared to 4.885,7 million lei at the beginning of the year. The Bank’s share of the total banking s ector accounted for 21,7%. The bank has seen a balancing of the portfolio structure and a decrease in the aggregate amount for some statements.

ACTIVITY PERFORMANCEWORK ON DEPOSIT ATTRACTION

Fig. 11. Customer deposits (million MDL)

Fig. 12. Structure of deposits by currency

Fig. 13. Structure of deposits by client type Fig. 14. Deposit structure by deposit type

57,6%

42,4%

59,7%

40,3%

Fig. Structura depozite după tip client

persoane fizice persoane juridice

2018

2017

57,8%

42,2%

59,9%

40,1%

Fig. Structura depozite după tip depozit

vedere termen

2018

2017

9.88

2 11.5

19

11.6

89

7,7%16,6%

1,5%

-2 0,0%

-1 0,0%

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

60, 0%

70, 0%

0

2.0 00

4.0 00

6.0 00

8.0 00

10. 000

12. 000

14. 000

2016 2017 2018

Fig. Customer deposits (mill.lei)

deposits from clients (principal) evolution rate

60,0%

40,0%

58,9%

41,1%

Fig. Structure of deposits by currency

national currency foreign currency

2018

2017

57,6%

42,4%

59,7%

40,3%

Fig. Structure of deposits by client type

natural persons legal entities

2018

2017

57,8%

42,2%

59,9%

40,1%

Fig. Deposit structure by deposit type

view term

2018

2017

22 Annual Report Victoriabank 2018

Interest expense on client deposits amounted to 238 million lei, which is 13,0% less, compared to the previous year.

The interest rates on attracted deposits, both in national currency and in foreign currency decreased during the year, considering the demand and supply of resources, the dynamics of the exchange rate, inflation and monetary policy rates.

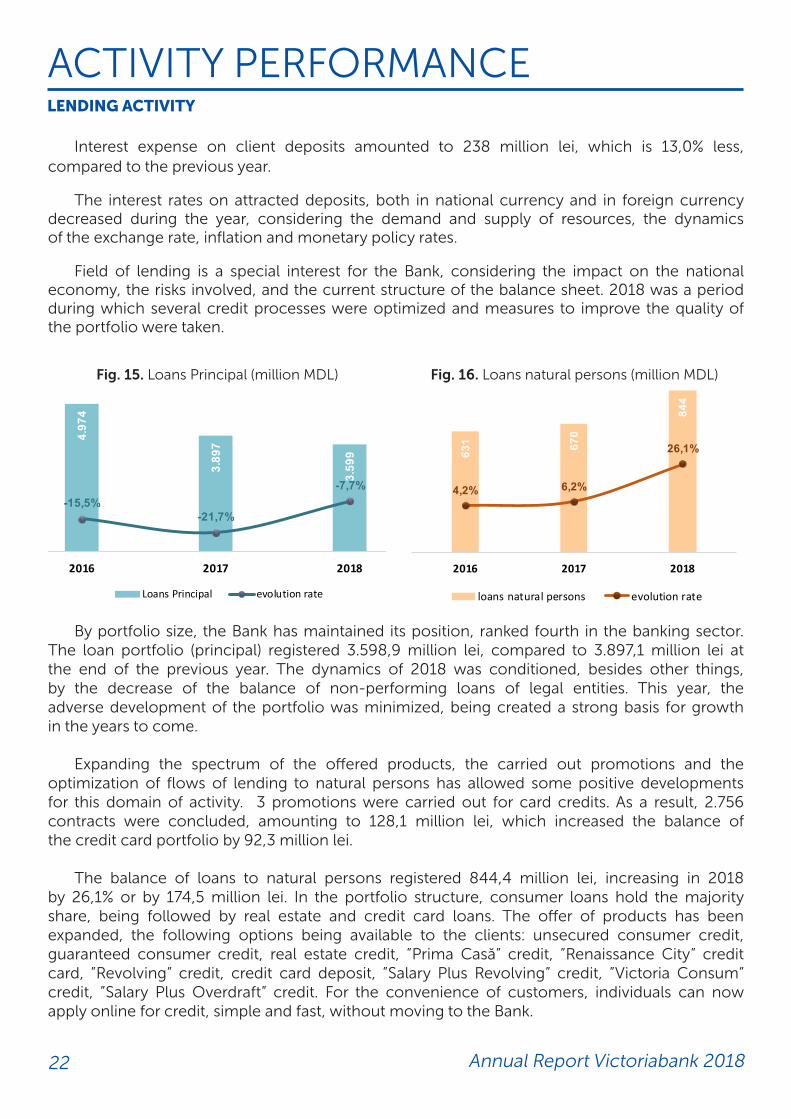

Field of lending is a special interest for the Bank, considering the impact on the national economy, the risks involved, and the current structure of the balance sheet. 2018 was a period during which several credit processes were optimized and measures to improve the quality of the portfolio were taken.

By portfolio size, the Bank has maintained its position, ranked fourth in the banking sector. The loan portfolio (principal) registered 3.598,9 million lei, compared to 3.897,1 million lei at the end of the previous year. The dynamics of 2018 was conditioned, besides other things, by the decrease of the balance of non-performing loans of legal entities. This year, the adverse development of the portfolio was minimized, being created a strong basis for growth in the years to come.

Expanding the spectrum of the offered products, the carried out promotions and the optimization of flows of lending to natural persons has allowed some positive developments for this domain of activity. 3 promotions were carried out for card credits. As a result, 2.756 contracts were concluded, amounting to 128,1 million lei, which increased the balance of the credit card portfolio by 92,3 million lei.

The balance of loans to natural persons registered 844,4 million lei, increasing in 2018 by 26,1% or by 174,5 million lei. In the portfolio structure, consumer loans hold the majority share, being followed by real estate and credit card loans. The offer of products has been expanded, the following options being available to the clients: unsecured consumer credit, guaranteed consumer credit, real estate credit, ”Prima Casă” credit, ”Renaissance City” credit card, ”Revolving” credit, credit card deposit, ”Salary Plus Revolving” credit, ”Victoria Consum” credit, ”Salary Plus Overdraft” credit. For the convenience of customers, individuals can now apply online for credit, simple and fast, without moving to the Bank.

ACTIVITY PERFORMANCELENDING ACTIVITY

Fig. 15. Loans Principal (million MDL) Fig. 16. Loans natural persons (million MDL)

4.97

4

3.89

7

3.59

9

-15,5%-21,7%

-7,7%

-3 0,0%

-2 0,0%

-1 0,0%

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

0

1.0 00

2.0 00

3.0 00

4.0 00

5.0 00

6.0 00

2016 2017 2018

Fig. Loans Principal (mill.lei)

Loans Principal evolution rate

631 67

0

844

4,2% 6,2%

26,1%

-2 0,0%

-1 0,0%

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

60, 0%

70, 0%

0

100

200

300

400

500

600

700

800

900

2016 2017 2018

Fig. Loans natural persons (mill.lei)

loans natural persons evolution rate

23Annual Report Victoriabank 2018

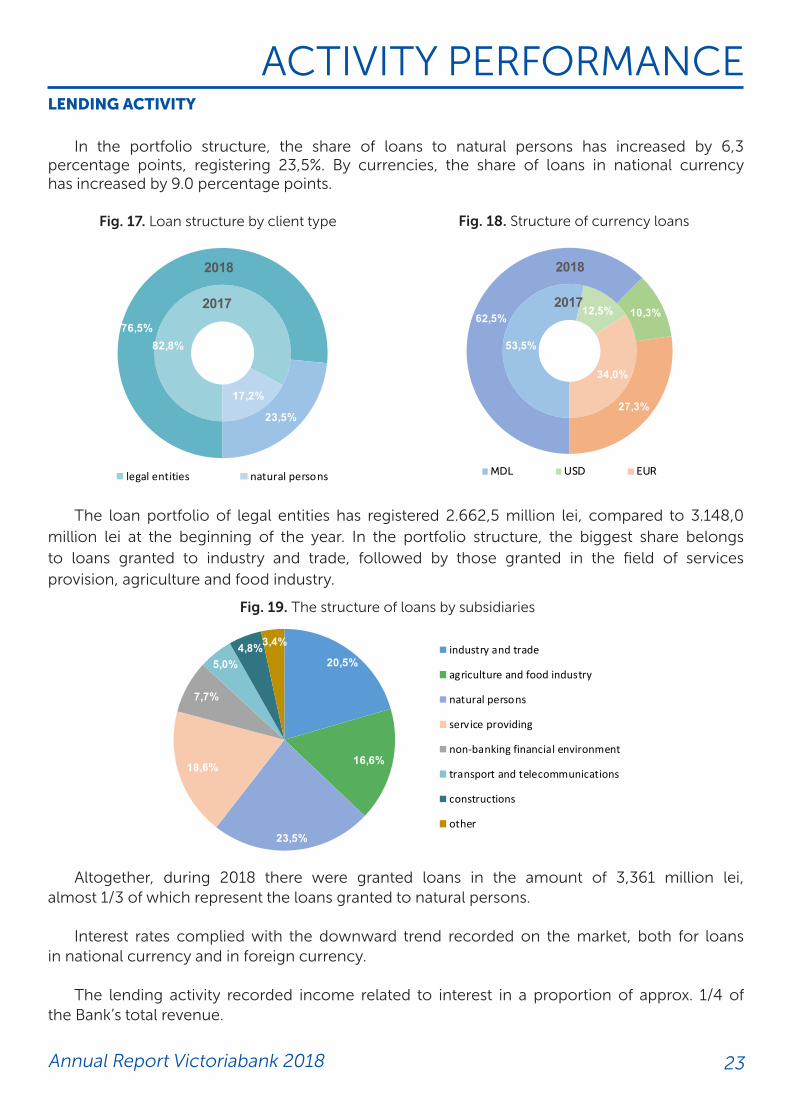

In the portfolio structure, the share of loans to natural persons has increased by 6,3 percentage points, registering 23,5%. By currencies, the share of loans in national currency has increased by 9.0 percentage points.

The loan portfolio of legal entities has registered 2.662,5 million lei, compared to 3.148,0 million lei at the beginning of the year. In the portfolio structure, the biggest share belongs to loans granted to industry and trade, followed by those granted in the field of services provision, agriculture and food industry.

Altogether, during 2018 there were granted loans in the amount of 3,361 million lei, almost 1/3 of which represent the loans granted to natural persons.

Interest rates complied with the downward trend recorded on the market, both for loans in national currency and in foreign currency.

The lending activity recorded income related to interest in a proportion of approx. 1/4 of the Bank’s total revenue.

ACTIVITY PERFORMANCELENDING ACTIVITY

Fig. 17. Loan structure by client type Fig. 18. Structure of currency loans

Fig. 19. The structure of loans by subsidiaries

53,5%

12,5%

34,0%

62,5% 10,3%

27,3%

Fig. Structura credite pe valute

MDL USD EUR

2018

2017

82,8%

17,2%

76,5%

23,5%

Fig. Loan structure by client type

legal entities natural persons

2018

2017

20,5%

16,6%

23,5%

18,6%

7,7%

5,0%4,8%3,4%

Fig. Loans structure by branches

industry and trade

agriculture and food industry

natural persons

service providing

non-banking financial environment

transport and telecommunications

constructions

other

24 Annual Report Victoriabank 2018

2019 is a year with important objectives in the lending activity: the growth of the loan portfolio and its quality, attracting new customers and strengthening partnerships with current customers, increasing market share for loans issued to natural persons and legal entities, expanding the range of products and services, completion of initiated projects and imple- mentation of new projects.

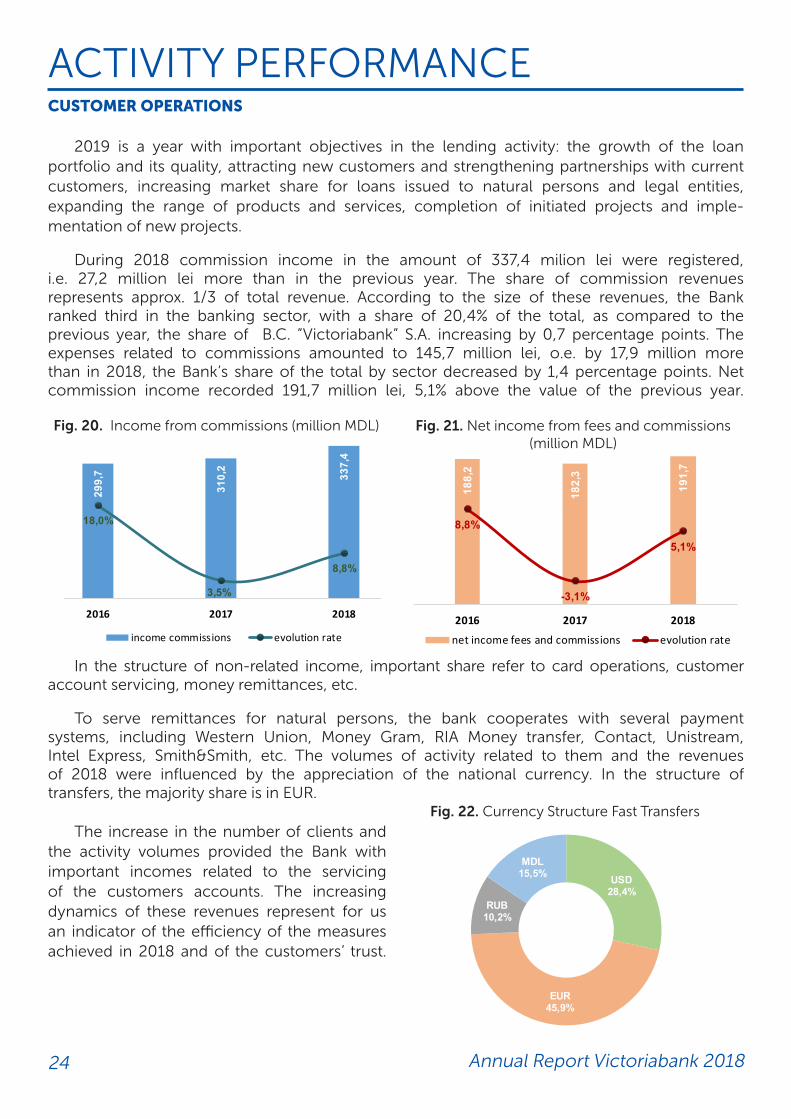

During 2018 commission income in the amount of 337,4 milion lei were registered, i.e. 27,2 million lei more than in the previous year. The share of commission revenues represents approx. 1/3 of total revenue. According to the size of these revenues, the Bank ranked third in the banking sector, with a share of 20,4% of the total, as compared to the previous year, the share of B.C. ”Victoriabank” S.A. increasing by 0,7 percentage points. The expenses related to commissions amounted to 145,7 million lei, o.e. by 17,9 million more than in 2018, the Bank’s share of the total by sector decreased by 1,4 percentage points. Net commission income recorded 191,7 million lei, 5,1% above the value of the previous year.

In the structure of non-related income, important share refer to card operations, customer account servicing, money remittances, etc.

To serve remittances for natural persons, the bank cooperates with several payment systems, including Western Union, Money Gram, RIA Money transfer, Contact, Unistream, Intel Express, Smith&Smith, etc. The volumes of activity related to them and the revenues of 2018 were influenced by the appreciation of the national currency. In the structure of transfers, the majority share is in EUR.

The increase in the number of clients and the activity volumes provided the Bank with important incomes related to the servicing of the customers accounts. The increasing dynamics of these revenues represent for us an indicator of the efficiency of the measures achieved in 2018 and of the customers’ trust.

ACTIVITY PERFORMANCECUSTOMER OPERATIONS

Fig. 20. Income from commissions (million MDL) Fig. 21. Net income from fees and commissions (million MDL)

Fig. 22. Currency Structure Fast Transfers

USD28,4%

EUR45,9%

RUB10,2%

MDL15,5%

Fig. Structura valutară transferuri rapide

299,

7

310,

2

337,

4

18,0%

3,5%

8,8%

0,0 %1,0 %2,0 %3,0 %4,0 %5,0 %6,0 %7,0 %8,0 %9,0 %10, 0%11, 0%12, 0%13, 0%14, 0%15, 0%16, 0%17, 0%18, 0%19, 0%20, 0%21, 0%22, 0%23, 0%24, 0%25, 0%26, 0%27, 0%28, 0%29, 0%30, 0%31, 0%32, 0%33, 0%34, 0%35, 0%

0,0

50, 0

100 ,0

150 ,0

200 ,0

250 ,0

300 ,0

350 ,0

400 ,0

2016 2017 2018

Fig. Revenue from commissions(mill.lei)

income commissions evolution rate

188,

2

182,

3

191,

7

8,8%

-3,1%

5,1%

-7 ,0%-6 ,0%-5 ,0%-4 ,0%-3 ,0%-2 ,0%-1 ,0%0,0 %1,0 %2,0 %3,0 %4,0 %5,0 %6,0 %7,0 %8,0 %9,0 %10, 0%11, 0%12, 0%13, 0%14, 0%15, 0%16, 0%17, 0%18, 0%19, 0%20, 0%21, 0%22, 0%23, 0%24, 0%25, 0%

0,0

50, 0

100 ,0

150 ,0

200 ,0

250 ,0

2016 2017 2018

Fig. Net income from fees and commissions(mill.lei)

net income fees and commissions evolution rate

25Annual Report Victoriabank 2018

ACTIVITY PERFORMANCEBANKING CARD ACTIVITY

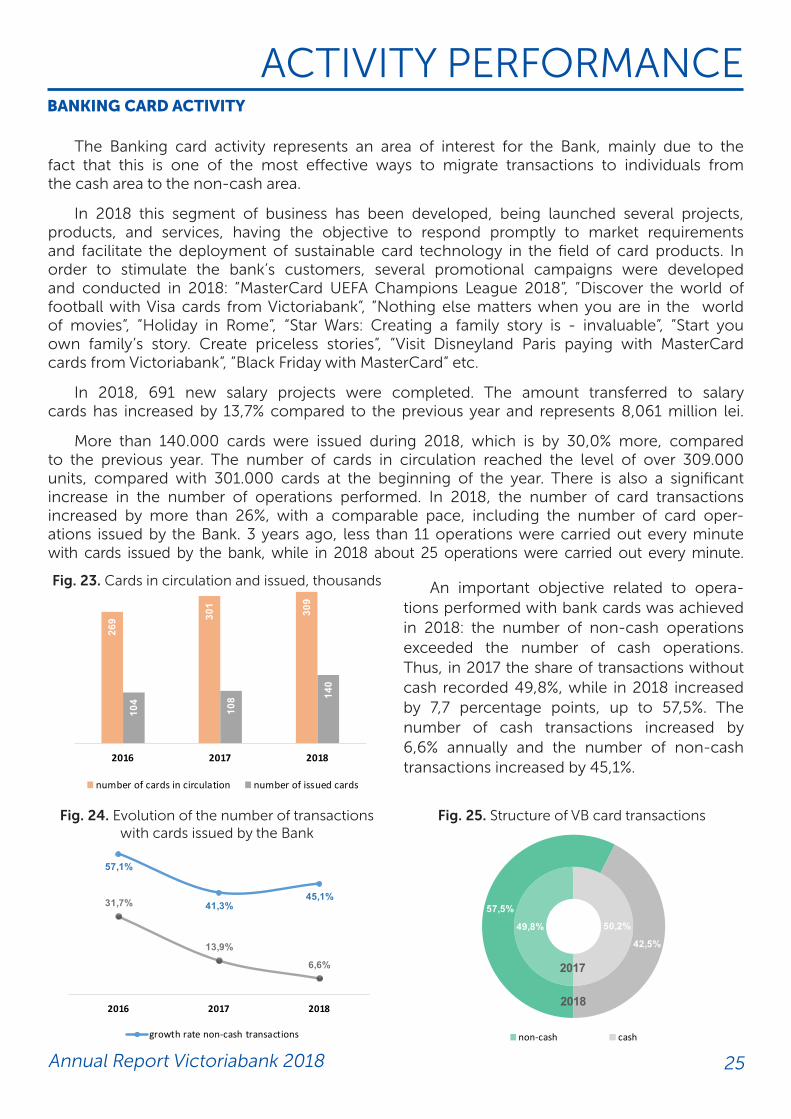

The Banking card activity represents an area of interest for the Bank, mainly due to the fact that this is one of the most effective ways to migrate transactions to individuals from the cash area to the non-cash area.

In 2018 this segment of business has been developed, being launched several projects, products, and services, having the objective to respond promptly to market requirements and facilitate the deployment of sustainable card technology in the field of card products. In order to stimulate the bank’s customers, several promotional campaigns were developed and conducted in 2018: ”MasterCard UEFA Champions League 2018”, ”Discover the world of football with Visa cards from Victoriabank”, ”Nothing else matters when you are in the world of movies”, ”Holiday in Rome”, “Star Wars: Creating a family story is - invaluable”, ”Start you own family’s story. Create priceless stories”, ”Visit Disneyland Paris paying with MasterCard cards from Victoriabank”, ”Black Friday with MasterCard” etc.

In 2018, 691 new salary projects were completed. The amount transferred to salary cards has increased by 13,7% compared to the previous year and represents 8,061 million lei.

More than 140.000 cards were issued during 2018, which is by 30,0% more, compared to the previous year. The number of cards in circulation reached the level of over 309.000 units, compared with 301.000 cards at the beginning of the year. There is also a significant increase in the number of operations performed. In 2018, the number of card transactions increased by more than 26%, with a comparable pace, including the number of card oper-ations issued by the Bank. 3 years ago, less than 11 operations were carried out every minute with cards issued by the bank, while in 2018 about 25 operations were carried out every minute.

An important objective related to opera-tions performed with bank cards was achieved in 2018: the number of non-cash operations exceeded the number of cash operations. Thus, in 2017 the share of transactions without cash recorded 49,8%, while in 2018 increased by 7,7 percentage points, up to 57,5%. The number of cash transactions increased by 6,6% annually and the number of non-cash transactions increased by 45,1%.

Fig. 23. Cards in circulation and issued, thousands

Fig. 24. Evolution of the number of transactions with cards issued by the Bank

Fig. 25. Structure of VB card transactions

269 30

1

309

104

108 14

0

0

50

100

150

200

250

300

350

2016 2017 2018

Fig. Cards in circulation and issued, thousands

number of cards in circulation number of issued cards

57,1%

41,3%45,1%31,7%

13,9%

6,6%

0,0 %

10, 0%

20, 0%

30, 0%

40, 0%

50, 0%

60, 0%

2016 2017 2018

Fig. Evolution of the number of transactions with cards issued by the

Bank

growth rate non-cash transactions

49,8% 50,2%

57,5%

42,5%

Fig. Structure of VB card transactions

non-cash cash

2018

2017

26 Annual Report Victoriabank 2018

FOREIGN EXCHANGE ACTIVITY

The foreign currency assets of B.C. ”Victoriabank” S.A. were concentrated in the correspond-ent banks from category A and have been reduced to the maximum balances held in the banks in Russia, the Ukraine and Belarus, by setting protectionist exposure limits and associating increased risk levels. Thus, in addition to the corresponding banks with which we have been working for many years (Bank of New York Mellon, DZ Bank AG, Intesa SanPaolo), business relations with Banca Transilvania were initiated as part of the integration process with the group.

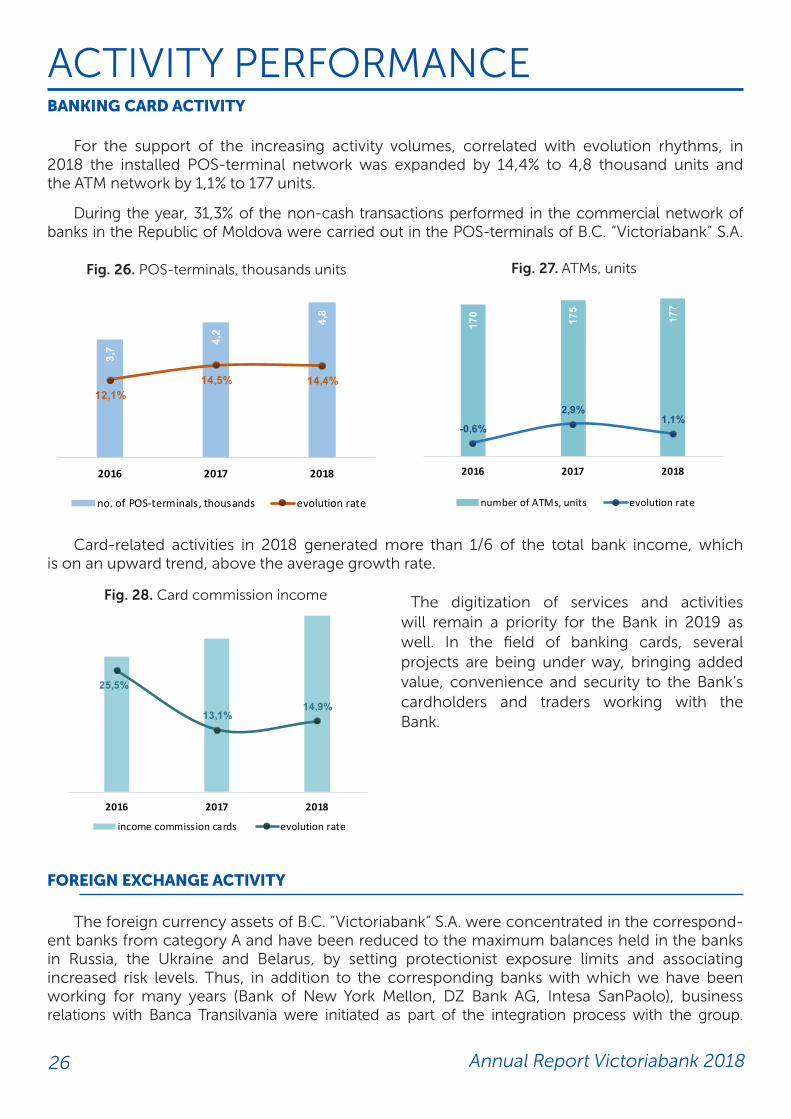

For the support of the increasing activity volumes, correlated with evolution rhythms, in 2018 the installed POS-terminal network was expanded by 14,4% to 4,8 thousand units and the ATM network by 1,1% to 177 units.

During the year, 31,3% of the non-cash transactions performed in the commercial network of banks in the Republic of Moldova were carried out in the POS-terminals of B.C. ”Victoriabank” S.A.

Card-related activities in 2018 generated more than 1/6 of the total bank income, which is on an upward trend, above the average growth rate.

The digitization of services and activities will remain a priority for the Bank in 2019 as well. In the field of banking cards, several projects are being under way, bringing added value, convenience and security to the Bank’s cardholders and traders working with the Bank.

ACTIVITY PERFORMANCEBANKING CARD ACTIVITY

Fig. 26. POS-terminals, thousands units

Fig. 28. Card commission income

Fig. 27. ATMs, units

3,7

4,2

4,8

12,1%14,5% 14,4%

0,0 %

5,0 %

10, 0%

15, 0%

20, 0%

25, 0%

30, 0%

0,0

1,0

2,0

3,0

4,0

5,0

6,0

2016 2017 2018

Fig. POS-terminals, thousands units

no. of POS-terminals, thousands evolution rate

170

175

177

-0,6%

2,9%1,1%

-3 ,0%

2,0 %

7,0 %

12, 0%

17, 0%

22, 0%

27, 0%

0

20

40

60

80

100

120

140

160

180

200

2016 2017 2018

Fig. ATMs, units

number of ATMs, units evolution rate

25,5%

13,1%14,9%

0,0 %

5,0 %

10, 0%

15, 0%

20, 0%

25, 0%

30, 0%

35, 0%

40, 0%

0

20. 000

40. 000

60. 000

80. 000

100 .000

120 .000

140 .000

160 .000

180 .000

200 .000

2016 2017 2018

Fig. Card fee income

income commission cards evolution rate

27Annual Report Victoriabank 2018

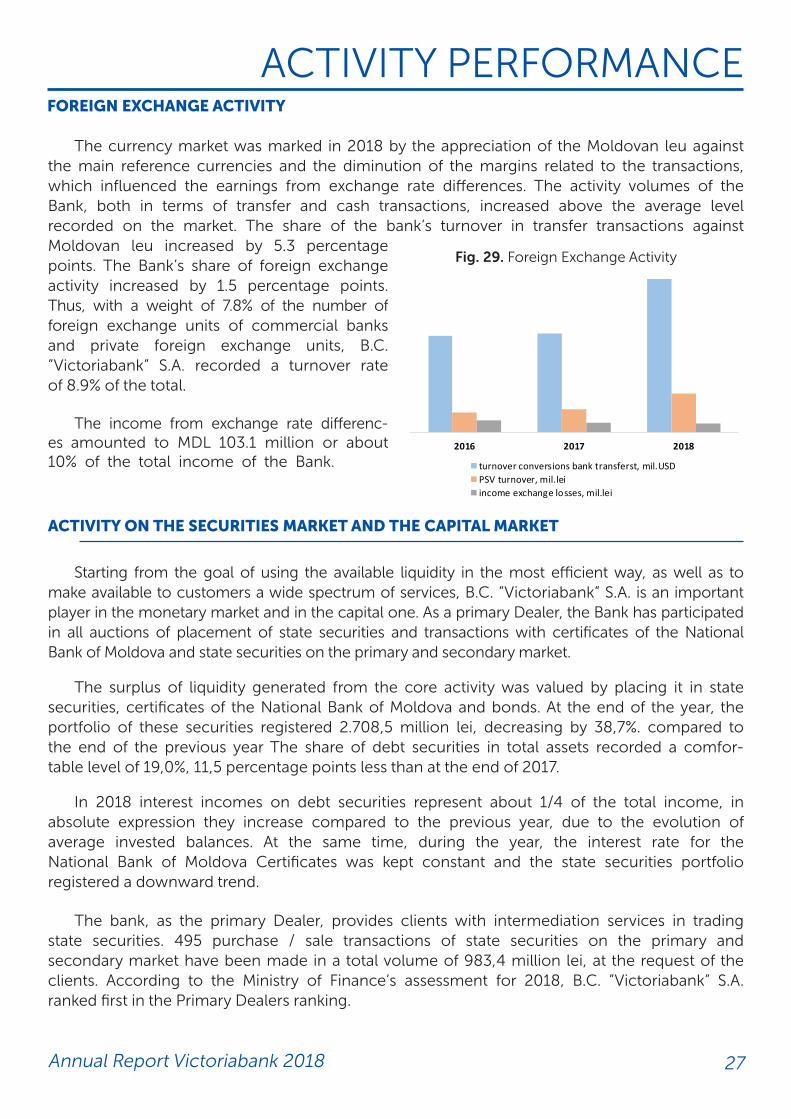

The currency market was marked in 2018 by the appreciation of the Moldovan leu against the main reference currencies and the diminution of the margins related to the transactions, which influenced the earnings from exchange rate differences. The activity volumes of the Bank, both in terms of transfer and cash transactions, increased above the average level recorded on the market. The share of the bank’s turnover in transfer transactions against Moldovan leu increased by 5.3 percentage points. The Bank’s share of foreign exchange activity increased by 1.5 percentage points. Thus, with a weight of 7.8% of the number of foreign exchange units of commercial banks and private foreign exchange units, B.C. ”Victoriabank” S.A. recorded a turnover rate of 8.9% of the total.

The income from exchange rate differenc-es amounted to MDL 103.1 million or about 10% of the total income of the Bank.

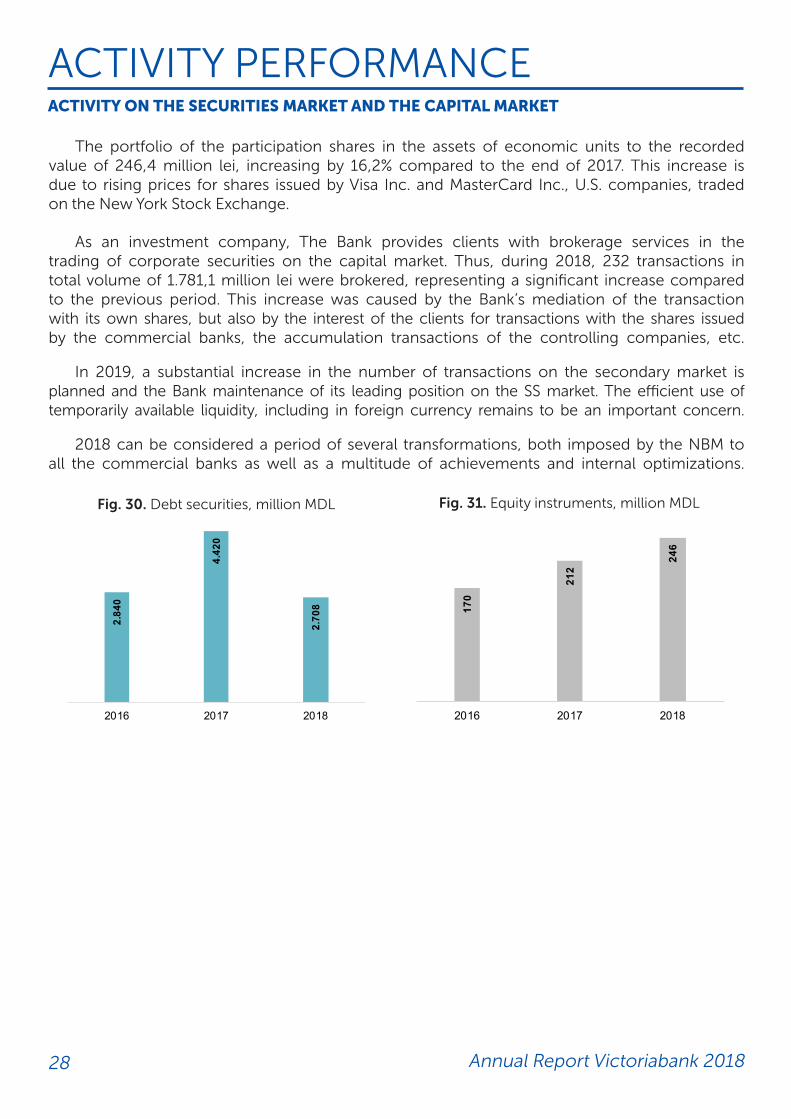

ACTIVITY ON THE SECURITIES MARKET AND THE CAPITAL MARKET

Starting from the goal of using the available liquidity in the most efficient way, as well as to make available to customers a wide spectrum of services, B.C. ”Victoriabank” S.A. is an important player in the monetary market and in the capital one. As a primary Dealer, the Bank has participated in all auctions of placement of state securities and transactions with certificates of the National Bank of Moldova and state securities on the primary and secondary market.

The surplus of liquidity generated from the core activity was valued by placing it in state securities, certificates of the National Bank of Moldova and bonds. At the end of the year, the portfolio of these securities registered 2.708,5 million lei, decreasing by 38,7%. compared to the end of the previous year The share of debt securities in total assets recorded a comfor- table level of 19,0%, 11,5 percentage points less than at the end of 2017.

In 2018 interest incomes on debt securities represent about 1/4 of the total income, in absolute expression they increase compared to the previous year, due to the evolution of average invested balances. At the same time, during the year, the interest rate for the National Bank of Moldova Certificates was kept constant and the state securities portfolio registered a downward trend.

The bank, as the primary Dealer, provides clients with intermediation services in trading state securities. 495 purchase / sale transactions of state securities on the primary and secondary market have been made in a total volume of 983,4 million lei, at the request of the clients. According to the Ministry of Finance’s assessment for 2018, B.C. ”Victoriabank” S.A. ranked first in the Primary Dealers ranking.

ACTIVITY PERFORMANCEFOREIGN EXCHANGE ACTIVITY

Fig. 29. Foreign Exchange Activity

0

200

400

600

800

1.0 00

1.2 00

1.4 00

1.6 00

1.8 00

2.0 00

2016 2017 2018

Fig. Foreign Exchange Activity

turnover conversions bank transferst, mil.USDPSV turnover, mil.leiincome exchange losses, mil.lei

28 Annual Report Victoriabank 2018

The portfolio of the participation shares in the assets of economic units to the recorded value of 246,4 million lei, increasing by 16,2% compared to the end of 2017. This increase is due to rising prices for shares issued by Visa Inc. and MasterCard Inc., U.S. companies, traded on the New York Stock Exchange.

As an investment company, The Bank provides clients with brokerage services in the trading of corporate securities on the capital market. Thus, during 2018, 232 transactions in total volume of 1.781,1 million lei were brokered, representing a significant increase compared to the previous period. This increase was caused by the Bank’s mediation of the transaction with its own shares, but also by the interest of the clients for transactions with the shares issued by the commercial banks, the accumulation transactions of the controlling companies, etc.

In 2019, a substantial increase in the number of transactions on the secondary market is planned and the Bank maintenance of its leading position on the SS market. The efficient use of temporarily available liquidity, including in foreign currency remains to be an important concern.

2018 can be considered a period of several transformations, both imposed by the NBM to all the commercial banks as well as a multitude of achievements and internal optimizations.

ACTIVITY PERFORMANCEACTIVITY ON THE SECURITIES MARKET AND THE CAPITAL MARKET

Fig. 30. Debt securities, million MDL Fig. 31. Equity instruments, million MDL

2.84

0

4.42

0

2.70

8

0

500

1.0 00

1.5 00

2.0 00

2.5 00

3.0 00

3.5 00

4.0 00

4.5 00

5.0 00

2016 2017 2018

Fig. Titluri de datorie, mil.lei

170

212

246

0

50

100

150

200

250

300

2016 2017 2018

Fig. Instrumente de capital propriu, mil.lei

29Annual Report Victoriabank 2018

STRATEGIC OBJECTIVES FOR 2019DEVELOPMENT STRATEGY

The change of the shareholder structure B.C. ”Victoriabank” S.A. and the strategic partner-ship between the EBRD and Banca Transilvania, constituted in this respect, have had significant impact on the strategic objectives of the Bank. The new shareholders set out to continue the growth of B.C. ”Victoriabank” S.A. and to contribute to the consolidation of the banking and business environment in Moldova. Thus, several priorities were set:

• Support the private business environment in the Republic Of Moldova, especially the SME sector;

• Developing a wide range of products and services for individuals;

• Aligning the organizational structure and corporate governance of the Bank with those of Banca Transilvania Financial Group;

• Involvement in personal and professional development of people with entrepreneurial spirit from the Republic of Moldova.

Our mission is to develop the business of customers and the bank by offering quality and innovative services and products.

Our goal: to become number ONE, among the banks of the Republic of Moldova, due to the interest we have towards people and business.

The strategic objectives of the Bank:

Employees:our priority

Operational efficiency

Digital initiatives

Boosting the Retail and SME segment

Strengthening the position on the banking market in Moldova

Besides the mission, the purpose and strategic objectives are set and pursued the goals related to current activity, which refers to the profitability of the Bank, volumes of activity and their evolution, expenditure management, asset quality, management, human resources, etc.

30 Annual Report Victoriabank 2018

PERSONNEL MANAGEMENTVictoriabank’s Human Resources Management Policy and strategy is oriented towards

achieving the following strategic goals:

• Supporting the bank’s business strategy by providing the necessary human resources for continuity and increased financial profitability.

• Continuous development of employees‚ skills based on training paths.

• Improving the transparency of human resources activities and processes.

• Promoting the image of the employer as well as taking a leading position among the top employers.

• Developing an active corporate culture by developing team spirit and aligning the employee’s personal values with company values.

• Motivating bank employees and maintaining talents.

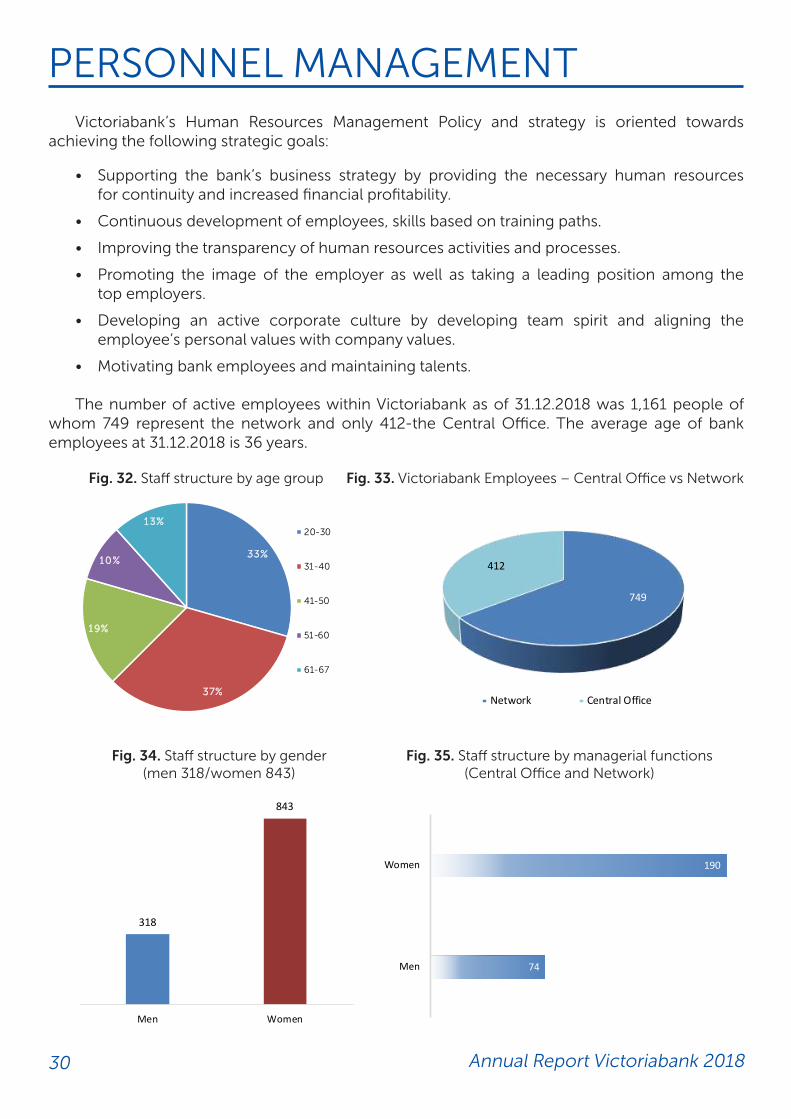

The number of active employees within Victoriabank as of 31.12.2018 was 1,161 people of whom 749 represent the network and only 412-the Central Office. The average age of bank employees at 31.12.2018 is 36 years.

Fig. 32. Staff structure by age group

Fig. 34. Staff structure by gender (men 318/women 843)

Fig. 35. Staff structure by managerial functions (Central Office and Network)

Fig. 33. Victoriabank Employees – Central Office vs Network

74

190

Barbati

Femei

33%

37%

19%

10%

13%20-30

31-40

41-50

51-60

61-67

318

843

Barbati Femei

749

412

Network Central Office

318

843

Men Women

74

190

Men

Women

31Annual Report Victoriabank 2018

PERSONNEL MANAGEMENTThe development of the bank’s network called for a special approach to human resources

policy. The main task was to give employees the opportunity to benefit from functional mobi-lity, to manifest themselves as subsidiary managers or RM. Internal recruitment, particularly from the Central Office, has been managed to ensure work in new open agencies.

Throughout 2018, the bank continued to hire and develop staff, preparing it for the changes that had been made in terms of adhering to Banca Transilvania Financial Group, as well as the new business model of the bank.

Loyalty and motivation actions including employees’ financial incentives have been under- taken on the basis of criteria to boost performance and productivity.

Measures to increase revenue through the granting of FOOD STAMPS, as well as projects to streamline operations with clients have led to the reduction of staff turnover in the area of the money collectors and to an increase in their productivity.

MAJOR ACHIEVEMENTS IN 2018

• Employee performance evaluation.

• E_Learning online PLATFORM (launching online courses for employees: Communica- tion and negotiation; Finance and accounting, Leadership; Management, Marketing, Personal Development; Project Management, Sales, Englis; Microsoft Office etc.)

• Optimizing staff-related administrative processes.

• Correlation of the remuneration strategy and compensation with the bank’s strategy.

• FOOD STAMPS for employees (45 lei/working day).

32 Annual Report Victoriabank 2018

RISK MANAGEMENTThe objective of B.C. ”Victoriabank” S.A. in 2018 with regard to the risk management is the

integration of the average risk appetite in the decision-making process by promoting an appropriate alignment of assumed risks, available capital and performance targets while tak-ing into account the tolerance of both financial risks and non-financial ones. In determining the appetite and risk tolerance, the Bank takes into account all the risks to which it is exposed due to the specific nature of its activities, being predominantly influenced by credit risk.

The risk management within the Bank is an integral part of all decision-making and business processes. In this sense, the management:

• Evaluates continuously the risks to which the Bank activity is or may be exposed, which may affect the achievement of its objectives and takes actions regarding any change in the conditions under which it operates;

• Ensures the existence of an adequate framework for managing the activity of the Bank, taking into account both the internal factors (complexity of the organizational structure, nature of the activities carried out, staff quality and level of staff turnover) and the exter- nal factors (macroeconomic factors, changes in the competitive environment in the banking sector, technological advances). The risk management framework includes internal regulations applicable to the Bank and each branch, limits and controls that ensure the identification, assessment, monitoring, mitigation and reporting of risks related to the activities carried out.

• Identifies the risks: The exposure to the risks inherent in the business through daily operations and transactions (including lending operations, asset management and other specific activities) is identified and aggregated through the implemented risk management infrastructure.

• Assesses/measures risks: The Bank assesses the identified risks by specific models and methods of calculation such as a system of indicators and related limits, a methodology for assessing the risk events able to generate losses, credit risk provisioning methodology, estimates of future developments of asset value, etc.

• Monitors and controls risks: Policy and procedures implemented for an effective risk management have the ability to temper the risks inherent in the business. There have been implemented procedures to control and approve the limits of decision and trans-actioning per person/product, etc. These limits are monitored daily/weekly/monthly.

• Reports risks: For specific risk categories, regular and transparent reporting mecha-nisms have been set up so that the governing body and all relevant units receive timely, accurate, concise, understandable and meaningful reports and can share information relevant for the identification, measurement or assessment and monitoring of risks.

The main risk categories, to which the Bank is exposed, are:

• Credit risk

• Liquidity risk

• Operational risk

• Market risk

33Annual Report Victoriabank 2018

• Interest risk from non-trading book activities

• Reputational risk

• Risk associated with excessive use of leverage

• Strategic risk

• Risk of compliance

During the course of 2018, the overall risk level calculated on the basis of indicators varied between low and high.

Credit risk

The framework of credit risk management is updated and improved from time to time. It is designed to cover all credit exposures in the banking activity and includes the following basic components:

• A risk assessment system for new credit products/significant changes in existing products;

• Credit granting methodology that ensures the creation of a healthy loan portfolio;

• Integrated customer relationship management systems, both for corporate and individual loans;

• Risk-based pricing methodology;

• An efficient process of active loan portfolio management that includes an adequate r eporting system;

• Limits of focusing on customer/group of customers/on products/sectors/guarantors/ types of collateral;

• Methodology for early detection of actual or potential increases in the credit risk (early warning signals);

• Processes applied regularly and consistently to establish appropriate loss adjustments in accordance with the applicable credit risk accounting regulations.

The methodologies used for the credit risk assessment are in particular to:

a) include a robust process designed to equip the Bank with the ability to identify the level, nature and determinants of credit risk at the time of initial recognition of exposure due to lend-ing, and ensure that subsequent changes in the credit risk can be identified and quantified;

b) include criteria that take due account of the impact of forward-looking information, including macroeconomic factors;

c) include a process for assessing the adequacy of inflows and significant assumptions related to the chosen method of determining the level of expected loss from lending;

RISK MANAGEMENT

34 Annual Report Victoriabank 2018

RISK MANAGEMENTd) take into account relevant internal and external factors that may affect estimates of

expected losses from lending;

e) ensure that the estimates of expected credit loss incorporate adequately the forward- looking information, including macroeconomic factors, which have not already been taken into account when calculating the adjustments for losses measured at the individual exposure level;

f) involve a process for assessing the overall adequacy of loss adjustments in accordance with relevant accounting regulations, including a regular review of loss patterns expected from lending.

The credit risk management at the Bank level is implemented by:

• Organizing a proper system of rules and procedures in the relevant field, able to create the regulatory framework, which when being applied in the lending process, allows avoiding or minimizing the triggering of risks; developing/improving the procedural framework of credit risk management (strategy, policies, credit risk management rules); continuous improvement of the approval/lending activities;

• Maintaining an adequate process of management, control and monitoring of credits;

• In the organizational structure of the Bank - there are directors and committees playing a role in supervising and managing the credit risk.

Liquidity risk

The aim of liquidity risk management is to obtain the expected returns on assets by capitaliz-ing on temporary liquidity surpluses and to allocate efficiently the resources attracted from cus-tomers in the context of a proper management consciously assumed and adapted to market conditions and the current legislative framework. Liquidity management is performed at the centralized level and aims at combining prudential requirements with profitability requirements.

For managing the liquidity risk, the Bank applies a number of principles, including liquid-ity crisis simulations, with different probabilities and severities, based on which the potential Bank vulnerabilities related to the liquidity position are analyzed, potential adverse effects and ways of their prevention/mitigation are determined. The liquidity risk management, as an element of the Bank strategy, is the task of the Asset and Liability Management Committee.

For the sound management of liquidity risk, the Bank continuously seeks to attract liquidity through treasury operations, external financing, etc., taking into account various factors such as the issuer’s rating, maturity and size of the issue and the markets on which it is traded.

The operational liquidity management is also performed throughout the day so as to ensure all settlements/payments assumed by the Bank, in its own name or on behalf of customers, in lei or currency, on account or in cash within the legal, mandatory internal limits.

The Bank also takes account of a liquidity reserve to cover the additional need for liquidity that may occur over a short period of time under stressful conditions, tested from time to time on the basis of different crisis scenarios.

During the course of 2018, the Bank recorded very good levels of liquidity indicators, thus demonstrating a solid position, enjoying more than comfortable liquidity.

35Annual Report Victoriabank 2018

Operational risk

Operational risk is the risk that practices, policies and internal systems of the institution are not adequate to prevent a loss due to market conditions or operational difficulties.

For the purpose of identifying, assessing, monitoring and mitigating the Bank’s operational risk, the Bank assesses products, processes and systems aimed at developing new markets, products and services as well as significant changes in existing ones and executing excep- tional transactions for determining the associated risk levels and measures to eliminate/mitigate them at accepted levels.

In order to reduce the risks inherent in the operational activity of the Bank, it is necessary to monitor continuously the controls implemented at different levels, to evaluate their effec- tiveness, and to introduce methods for reducing the effects of operational risk events.

The Bank strategy for mitigating exposure to operational risks is based mainly on the permanent compliance of the regulatory documents with the legal regulations and market conditions, on the staff training, efficiency of the internal control systems (organization and performance), continuous improvement of the IT solutions and consolidation of the infor- mation security systems of the Bank, use of complementary means of risk mitigation (execution of specific risk insurance policies, application of measures to limit and mitigate the effects of identified operational risk incidents such as standardization of current activity, evaluation of products, processes and systems to determine those significant with regard to the inherent operational risk), use of recommendations and conclusions resulting from controls performed by internal and external controlling bodies in the field of operational risks, updating of continuity plans and their regular review and testing.

The operational risk assessment process is closely correlated with the global risk manage-ment process. Its result is an integral part of the processes of operational risk monitoring and control and it is constantly compared to the risk appetite set out in the risk management strategy.

Market risk

Market risk is the risk of recording losses related to the on and off-balance sheet positions due to unfavorable market fluctuations in the prices of financial instruments and equity securities held for trading, interest rates and foreign exchange rates.

For managing the market risk, the Bank applies a number of rules, including stress tests, which assess the impact of possible sudden and unexpected changes in interest rates and/or market fluctuations in the exchange rate on own funds, being included in the regular reports to the Asset and Liability Management Committee.

In order to diminish the market risks inherent in operations, the Bank has adopted a prudential approach in order to protect the Bank profit from market fluctuations in prices, interest rates, exchange rates, which are all exogenous, external and independent factors. The Bank applies a set of principles that refer to the quality, maturity, diversity and degree of risk of component elements.

RISK MANAGEMENT

36 Annual Report Victoriabank 2018

The market risk analysis is carried out starting from three risk subcategories mentioned below, aimed at combining prudential requirements with profitability requirements:

Interest rate and price risk. The management of this risk is adapted and adjusted to the conditions of the financial and banking market of the Republic of Moldova and international markets and to the general economic and political context.

Currency risk. This is the risk of recording losses related to the on and off-balance sheet positions due to unfavorable market fluctuations in exchange rates. The Bank applies a number of rules and limits regarding operations/positions sensitive to exchange rate fluctuations, way of performance, recording, and the impact of exchange rates on the Bank assets and liabilities.