Sustained growth in a challenging environment Why not ... · 2 Topics Romania Macro picture Banking...

28

1 Sustained growth in a challenging environment Why not securitization? EFSE Annual Meeting 2007 Budva, Montenegro

Transcript of Sustained growth in a challenging environment Why not ... · 2 Topics Romania Macro picture Banking...

1

Sustained growth

in a challenging environment

Why not securitization?

EFSE Annual Meeting 2007 Budva, Montenegro

2

Topics

Romania� Macro picture

� Banking system

Banca Transilvania� Strategy and organization

� Key developments during 2006

� Why not thinking about securitization?

3

Romania

� Macro picture

� Banking system

4

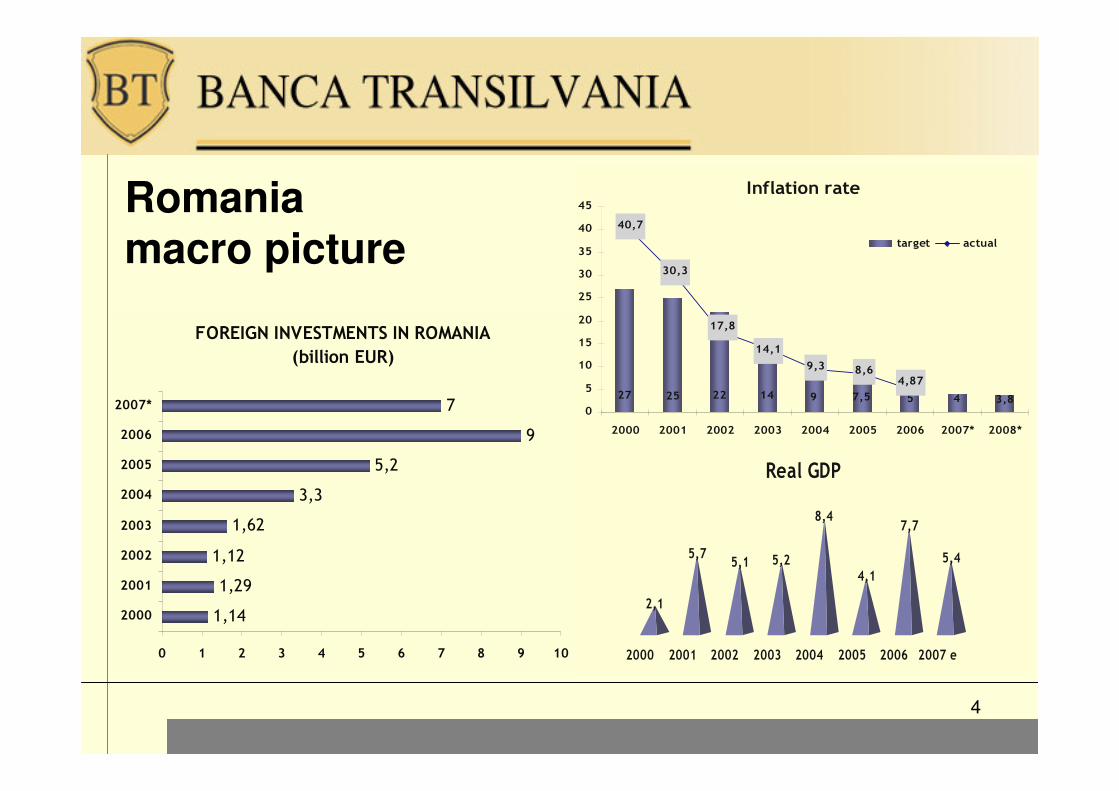

Romania macro picture

Inflation rate

27 25 22 14 9 7,5 5 4 3,8

17,8

14,1

40,7

30,3

9,3 8,64,87

0

5

10

15

20

25

30

35

40

45

2000 2001 2002 2003 2004 2005 2006 2007* 2008*

target actual

2,1

5,75,1 5,2

8,4

4,1

7,7

5,4

2000 2001 2002 2003 2004 2005 2006 2007 e

Real GDP

FOREIGN INVESTMENTS IN ROMANIA

(billion EUR)

1,14

1,29

1,12

1,62

3,3

5,2

9

7

0 1 2 3 4 5 6 7 8 9 10

2000

2001

2002

2003

2004

2005

2006

2007*

5

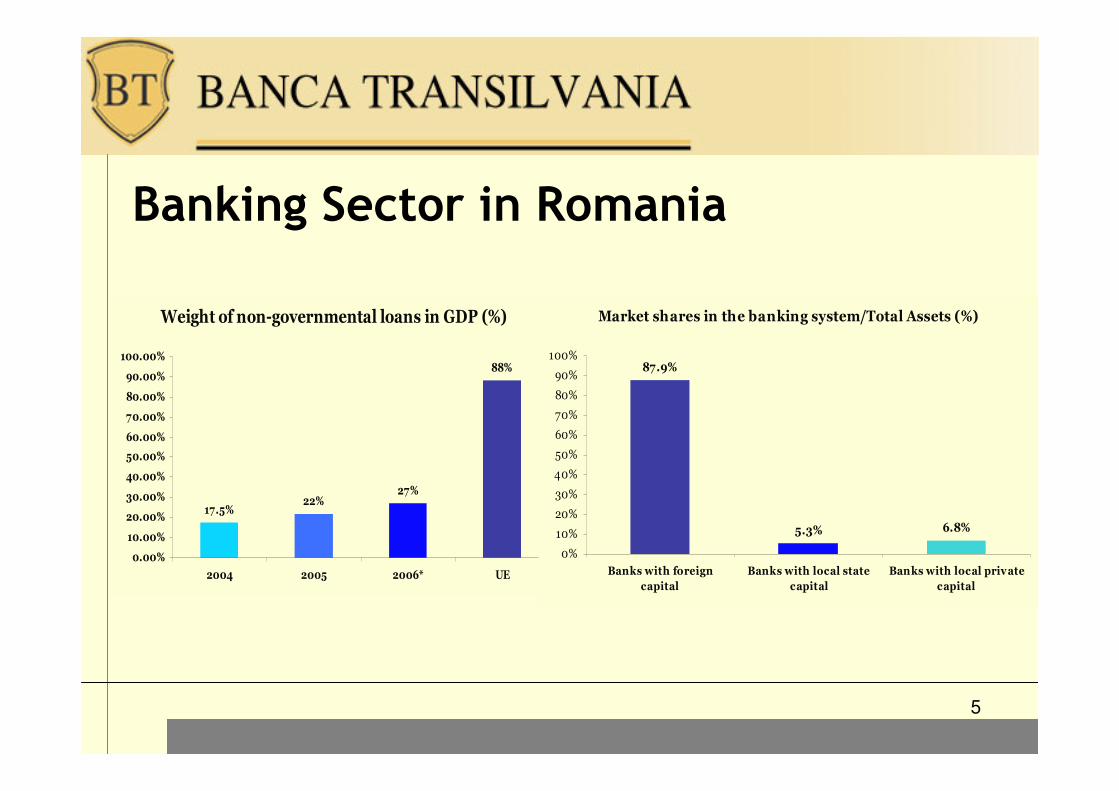

Banking Sector in Romania

Weight of non-governmental loans in GDP (%)

17.5%22%

27%

88%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

90.00%

100.00%

2004 2005 2006* UE

Market shares in the banking system/Total Assets (%)

87.9%

5.3% 6.8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Banks with foreign

capital

Banks with local state

capital

Banks with local private

capital

6

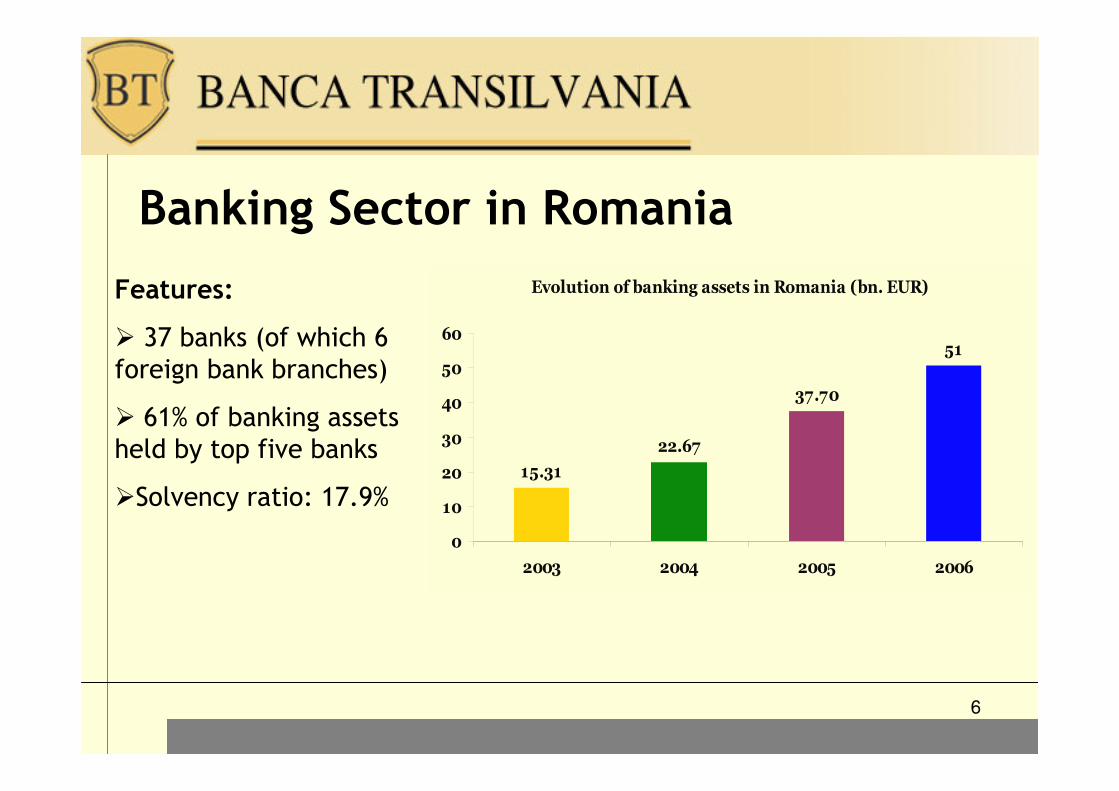

Banking Sector in Romania

Features:

� 37 banks (of which 6 foreign bank branches)

� 61% of banking assets held by top five banks

�Solvency ratio: 17.9%

Evolution of banking assets in Romania (bn. EUR)

15.31

22.67

37.70

51

0

10

20

30

40

50

60

2003 2004 2005 2006

7

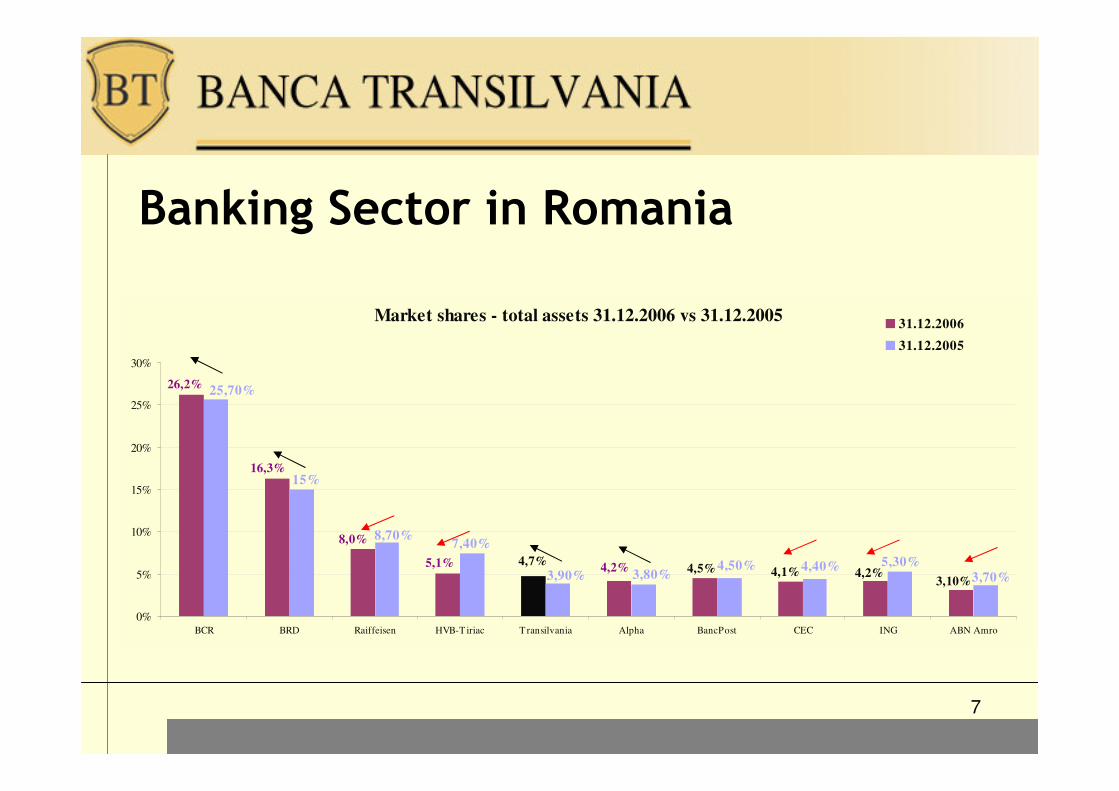

Market shares - total assets 31.12.2006 vs 31.12.2005

4,1%4,5%3,10%

4,2%4,2%

4,7%5,1%

8,0%

16,3%

26,2%

3,70%

5,30%4,40%4,50%3,80%

25,70%

15%

8,70%7,40%

3,90%

0%

5%

10%

15%

20%

25%

30%

BCR BRD Raiffeisen HVB-T iriac T ransilvania Alpha BancPost CEC ING ABN Amro

31.12.2006

31.12.2005

Banking Sector in Romania

8

Banca Transilvania

� Strategy and organization

� Key developments during 2006

� Why not thinking about securitization?

� Refinancing: own behalf & our clients

9

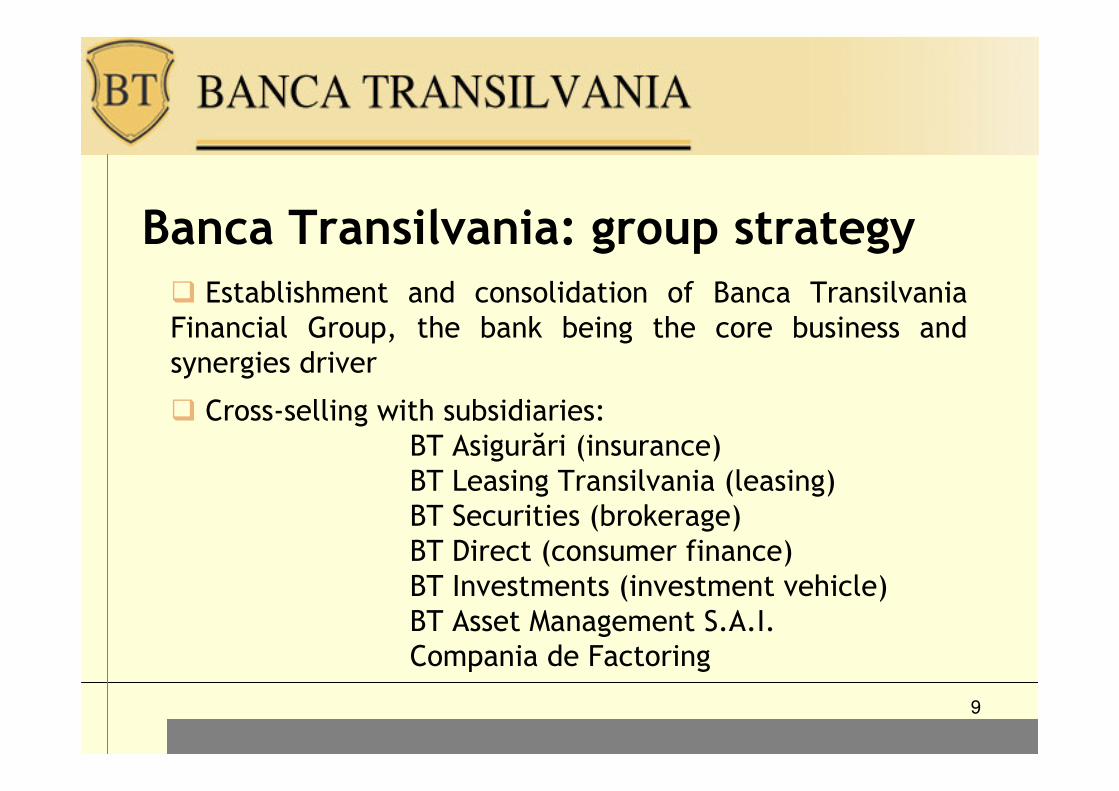

Banca Transilvania: group strategy

� Establishment and consolidation of Banca Transilvania Financial Group, the bank being the core business and synergies driver

� Cross-selling with subsidiaries:BT Asigurări (insurance)BT Leasing Transilvania (leasing)BT Securities (brokerage)BT Direct (consumer finance)BT Investments (investment vehicle)BT Asset Management S.A.I.Compania de Factoring

10

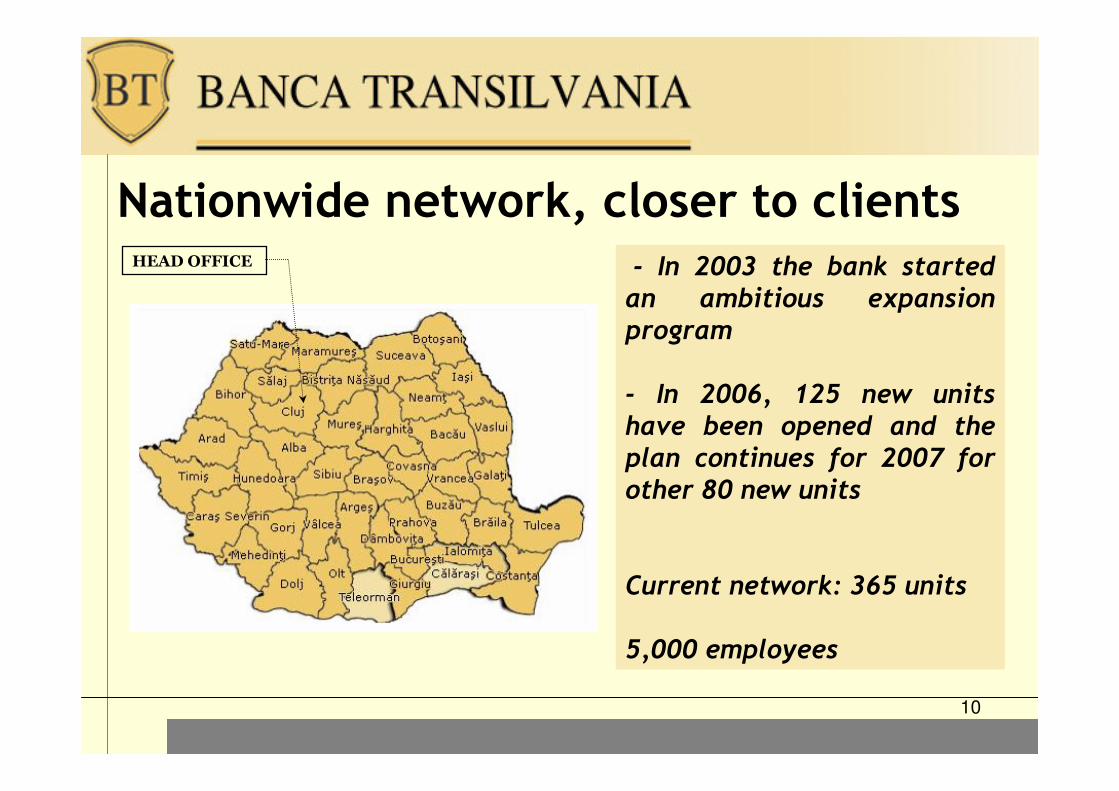

Nationwide network, closer to clients

- In 2003 the bank started an ambitious expansion program

- In 2006, 125 new units have been opened and the plan continues for 2007 for other 80 new units

Current network: 365 units

5,000 employees

HEAD OFFICE

11

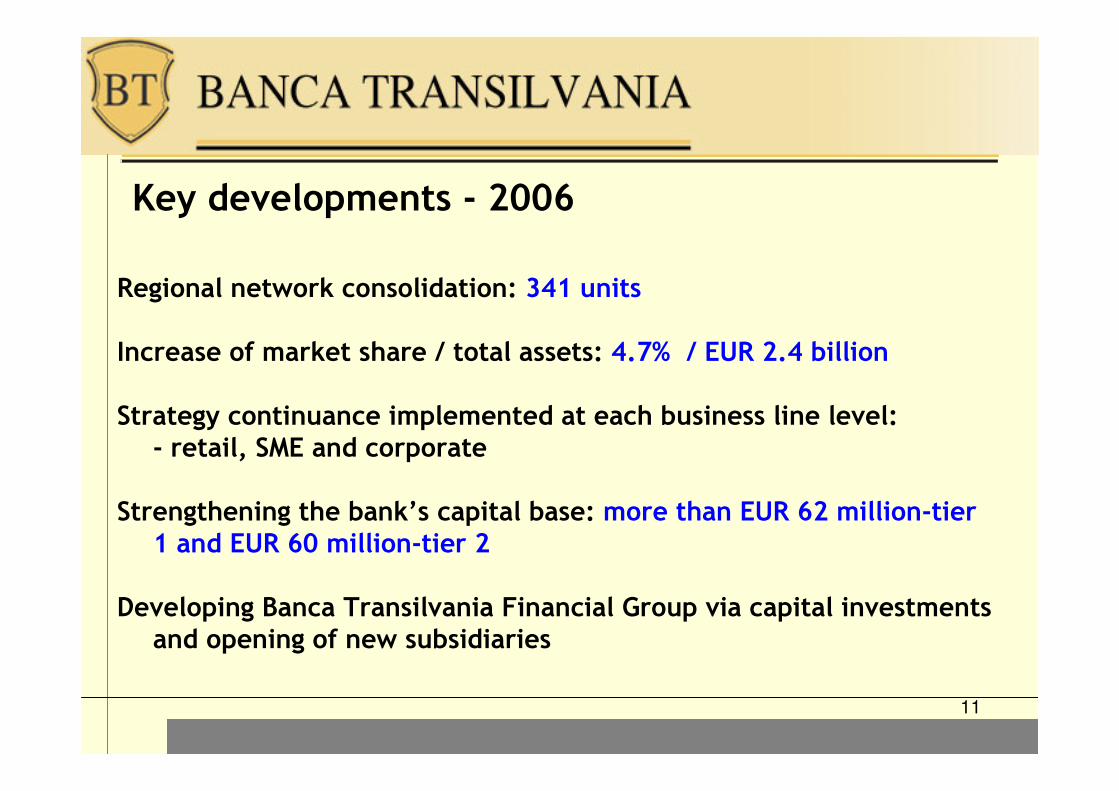

Key developments - 2006

Regional network consolidation: 341 units

Increase of market share / total assets: 4.7% / EUR 2.4 billion

Strategy continuance implemented at each business line level: - retail, SME and corporate

Strengthening the bank’s capital base: more than EUR 62 million-tier 1 and EUR 60 million-tier 2

Developing Banca Transilvania Financial Group via capital investments and opening of new subsidiaries

12

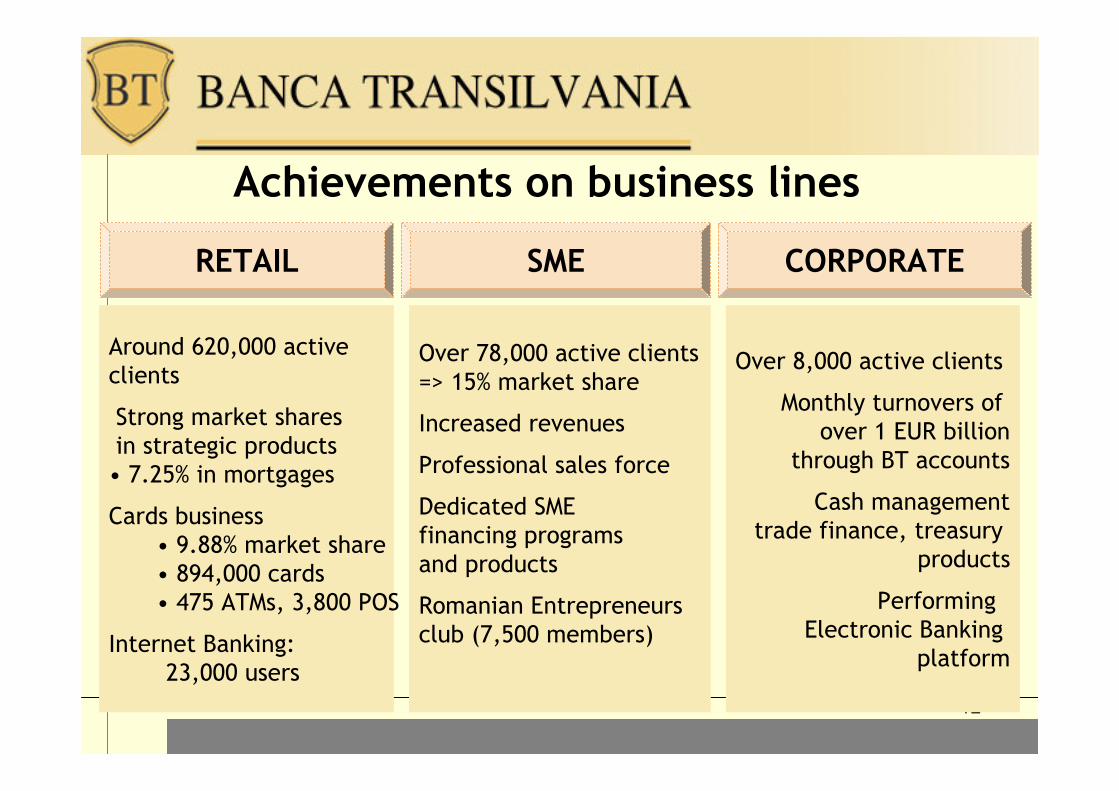

Achievements on business lines

RETAIL SME CORPORATE

Around 620,000 active clients

Strong market sharesin strategic products• 7.25% in mortgages

Cards business• 9.88% market share • 894,000 cards• 475 ATMs, 3,800 POS

Internet Banking: 23,000 users

Over 78,000 active clients=> 15% market share

Increased revenues

Professional sales force

Dedicated SME financing programs and products

Romanian Entrepreneurs club (7,500 members)

Over 8,000 active clients

Monthly turnovers of over 1 EUR billion

through BT accounts

Cash managementtrade finance, treasury

products

Performing Electronic Banking

platform

13

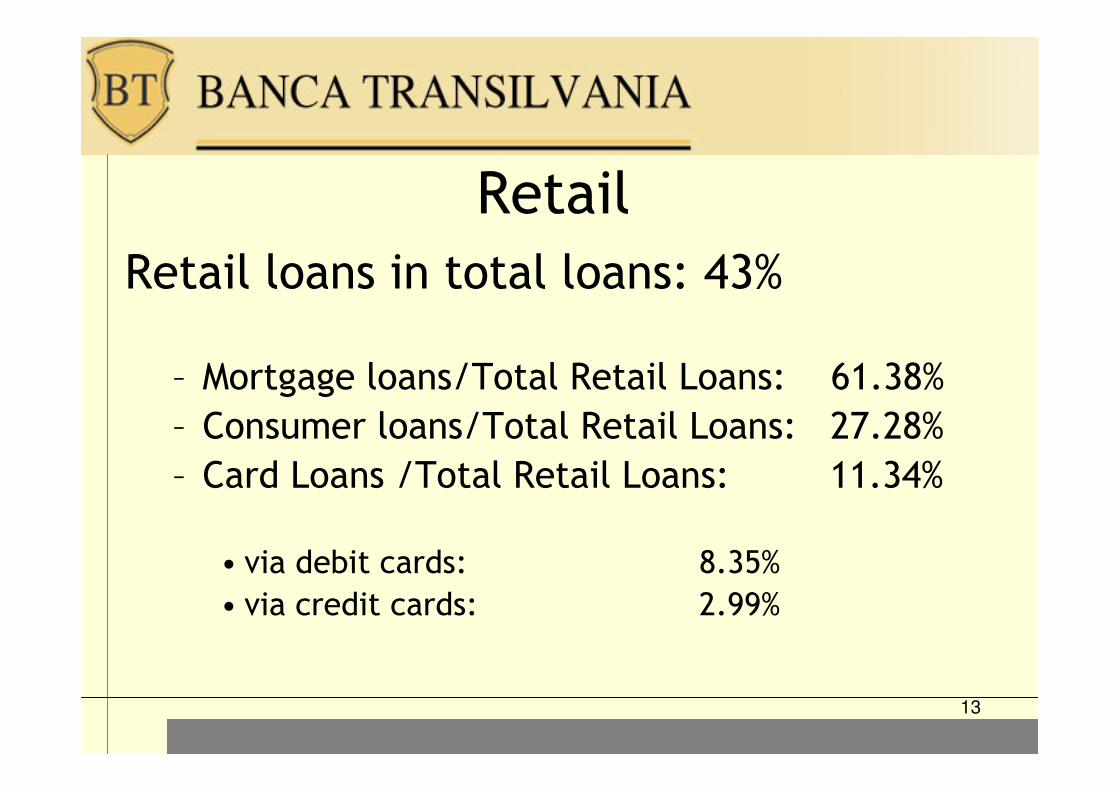

Retail

Retail loans in total loans: 43%

– Mortgage loans/Total Retail Loans: 61.38%

– Consumer loans/Total Retail Loans: 27.28%

– Card Loans /Total Retail Loans: 11.34%

• via debit cards: 8.35%

• via credit cards: 2.99%

14

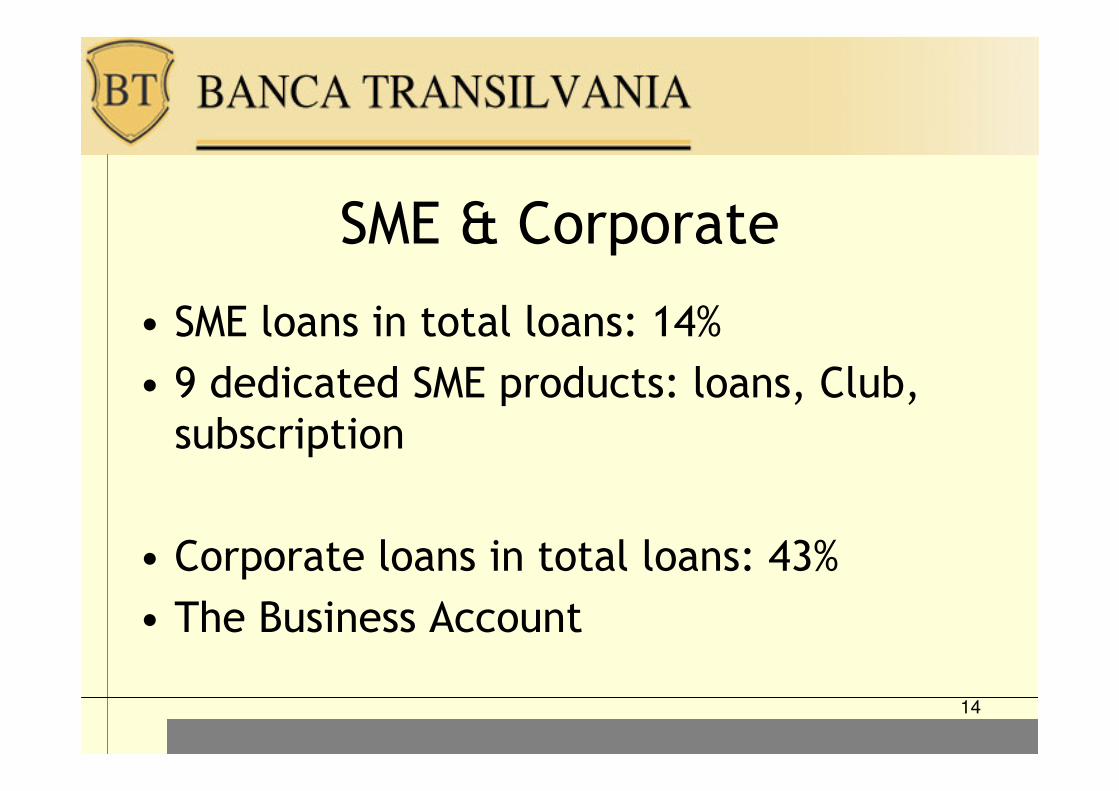

SME & Corporate

• SME loans in total loans: 14%

• 9 dedicated SME products: loans, Club, subscription

• Corporate loans in total loans: 43%

• The Business Account

15

Decembrie 2005 Decembrie 2006

403

621

Decembrie 2005 Decembrie 2006

105

215

Loans (EUR Mio.)

Staff increase

+170 (94%) +31 (15%)

105% 54%

SME Corporate

16

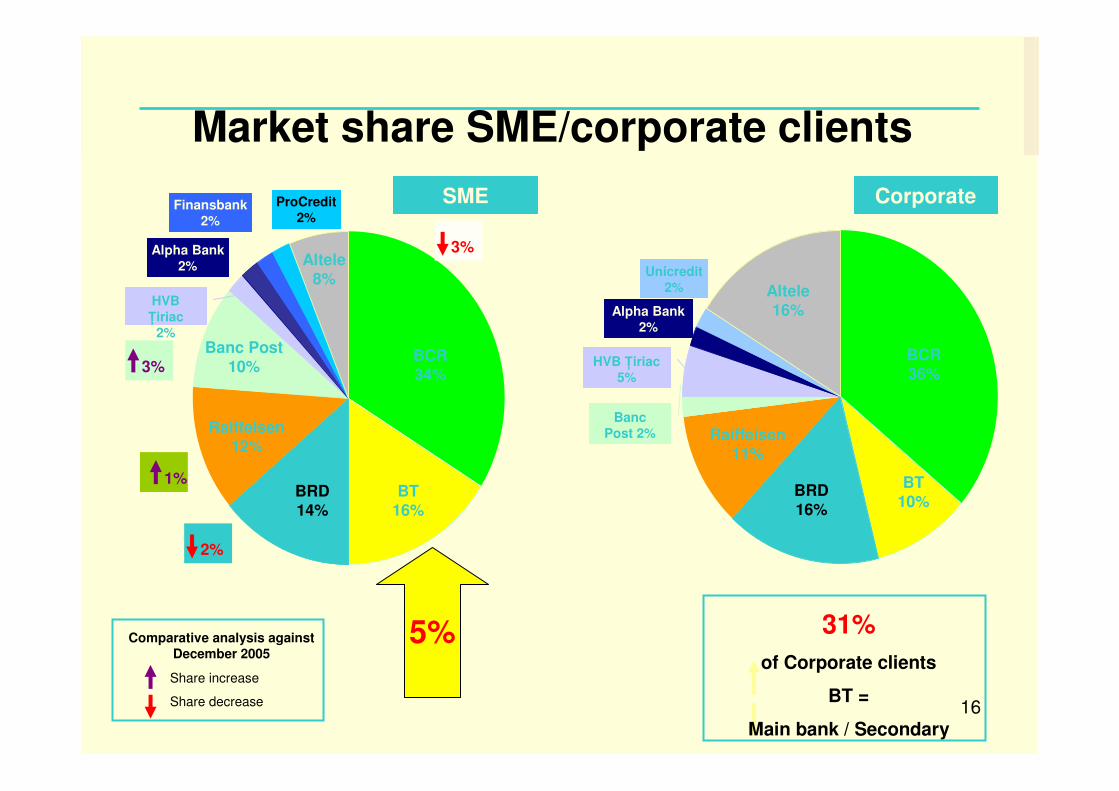

Market share SME/corporate clients

BCR 34%

BT 16%

BRD 14%

Raiffeisen 12%

Banc Post 10%

Altele8%

2%

1%

3%

3%

HVB

łiriac

2%

Alpha Bank

2%

Finansbank

2%

ProCredit

2%

BCR 36%

BT 10%

BRD 16%

Raiffeisen 11%

Altele16%

HVB łiriac

5%

Alpha Bank

2%

Unicredit

2%

Banc

Post 2%

SME Corporate

Share increase

Share decrease

Comparative analysis against

December 2005

31%

of Corporate clients

BT =

Main bank / Secondary

5%

17

�Why not thinking about securitization?

18

a. True sale?

19

150%

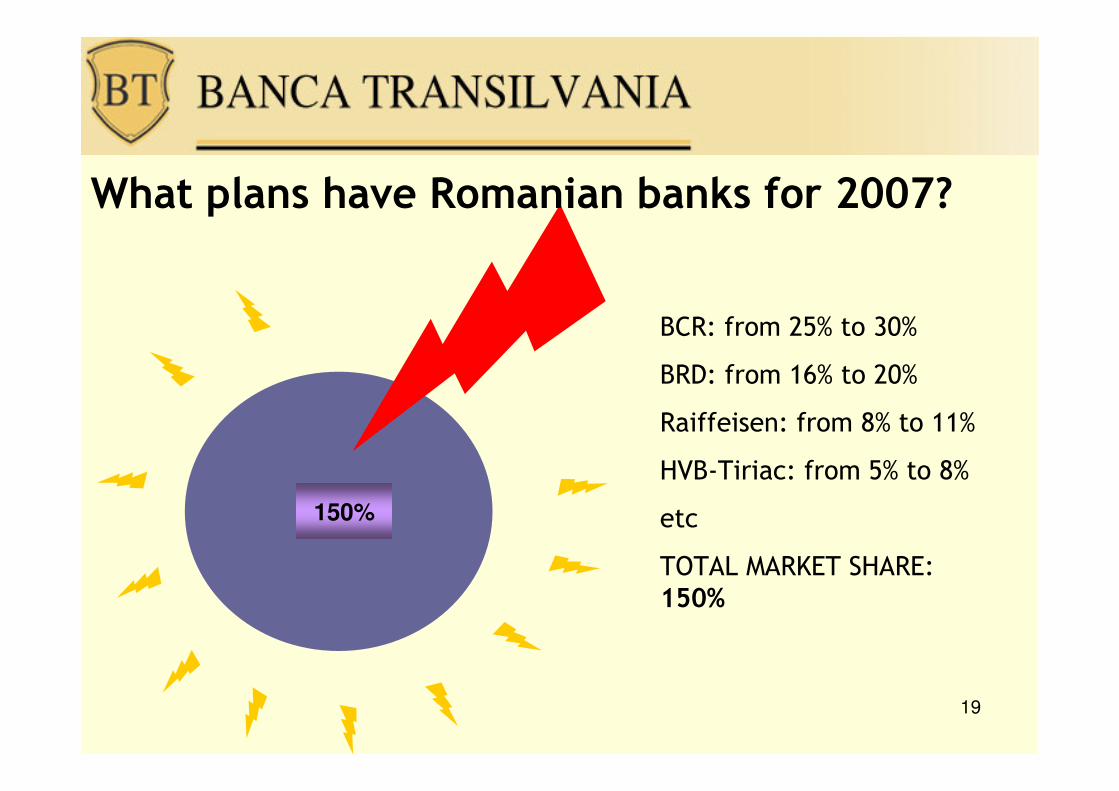

What plans have Romanian banks for 2007?

BCR: from 25% to 30%

BRD: from 16% to 20%

Raiffeisen: from 8% to 11%

HVB-Tiriac: from 5% to 8%

etc

TOTAL MARKET SHARE: 150%

20

Fight for additional market share will diminish the chances for a “true sale” securitization

21

b. Credit risk?

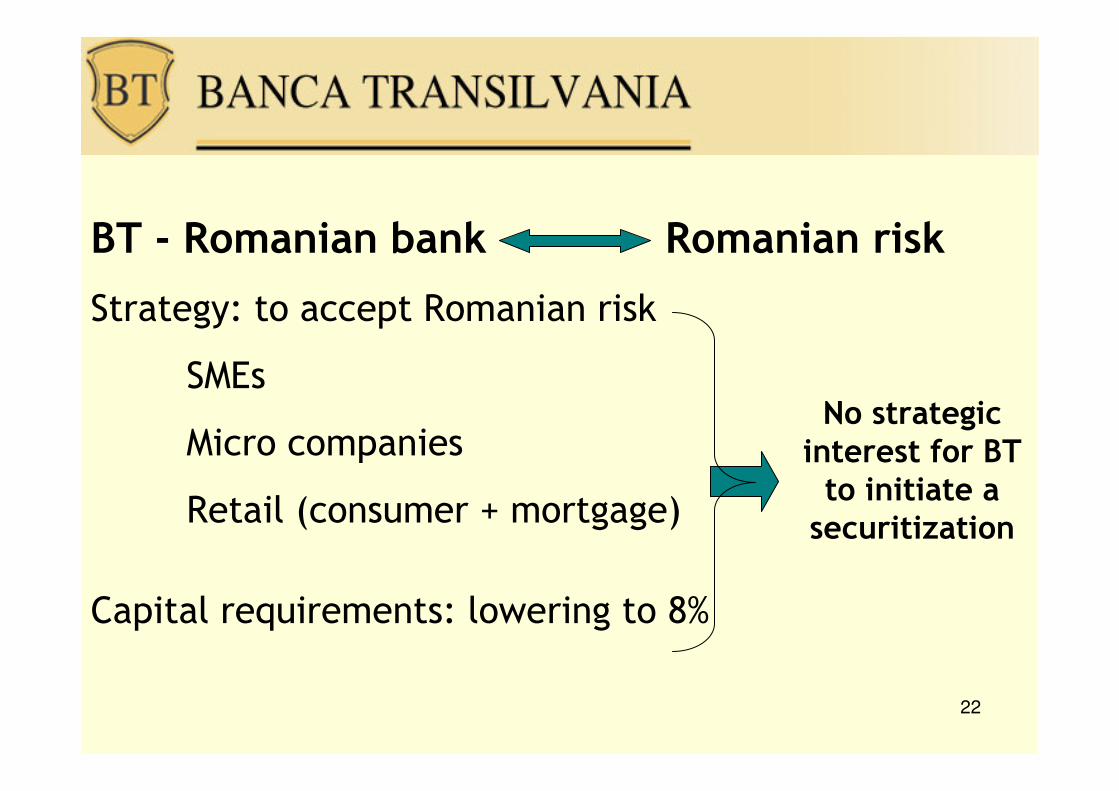

22

BT - Romanian bank Romanian risk

Strategy: to accept Romanian risk

SMEs

Micro companies

Retail (consumer + mortgage)

Capital requirements: lowering to 8%

No strategic interest for BT to initiate a

securitization

23

c. Cost of funding?

24

Initial costs for the first deal: significant

Profile of loan portfolio: higher risk = higher margins

Currency structure of loan portfolio

Funding costs: (relatively) lower after EU accession

Insufficient cost reduction

25

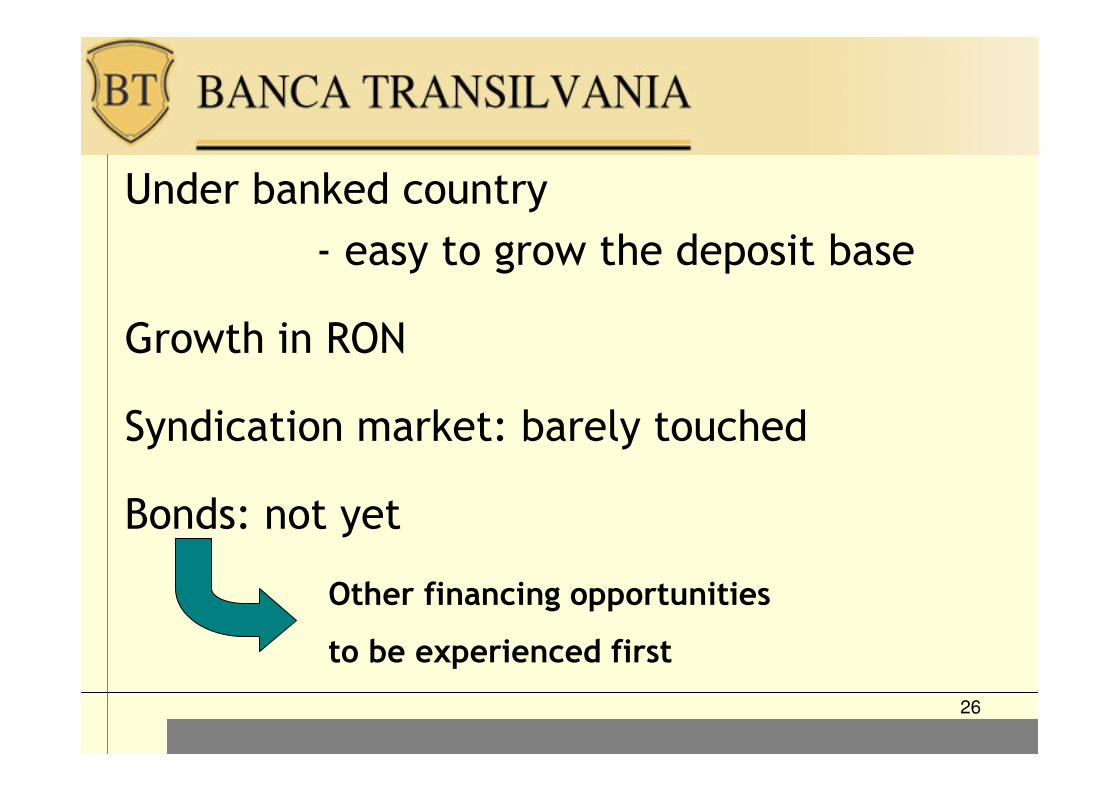

d. Asset – liability management?

26

Under banked country

- easy to grow the deposit base

Growth in RON

Syndication market: barely touched

Bonds: not yet

Other financing opportunities

to be experienced first

27

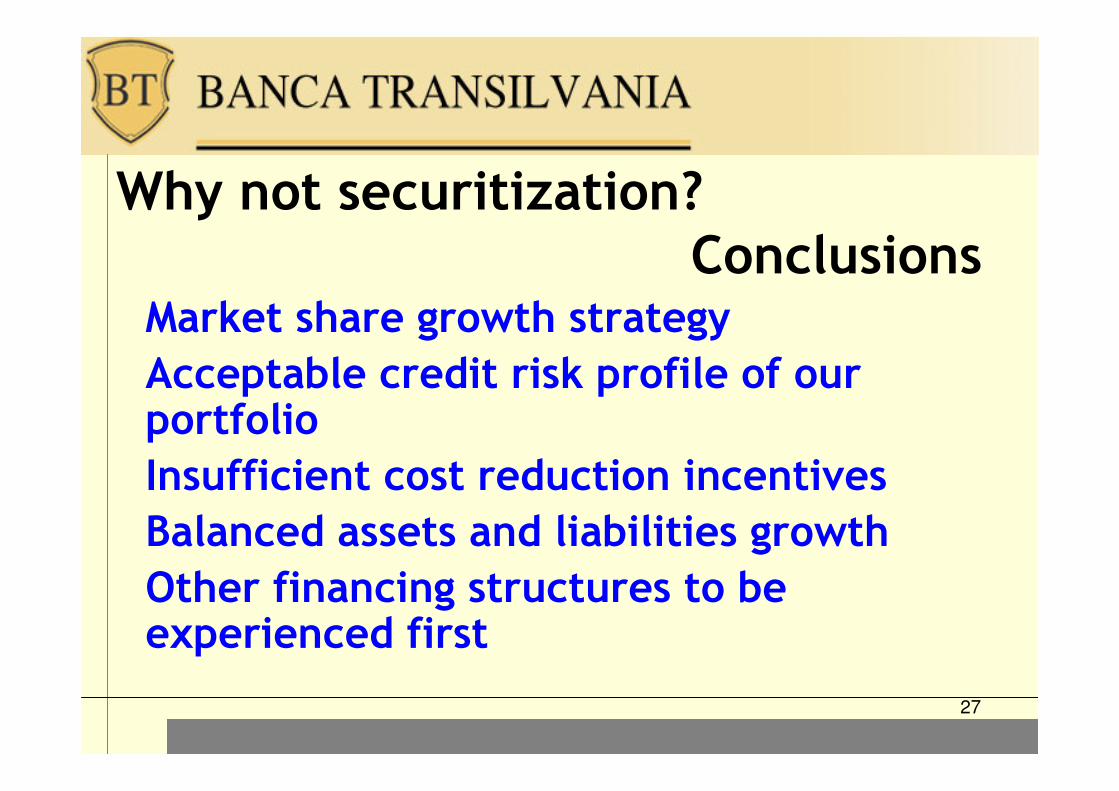

Why not securitization?Conclusions

Market share growth strategy

Acceptable credit risk profile of our portfolio

Insufficient cost reduction incentives

Balanced assets and liabilities growth

Other financing structures to be experienced first

28

Thank you!

Banca Transilvania S.A.

8, Baritiu St., 400027 Cluj-Napoca, Romania

Ph: + 40 264 407 150

Fax: + 40 264 407 179

E-mail: [email protected]