Andrew Hughes Hallett - Oesterreichische Nationalbank0b635ea0-2ff3-48ba-88d0-a8c1dbeaa04f/... ·...

26

Andrew Hughes Hallett

Transcript of Andrew Hughes Hallett - Oesterreichische Nationalbank0b635ea0-2ff3-48ba-88d0-a8c1dbeaa04f/... ·...

Andrew Hughes Hallett

vowi_tagung_2004 Seite 176 15.12.2004,08:32 schwarz rot

The European Economy

at the Cross Roads:

Structural Reforms,

Fiscal Constraints,

and the Lisbon Agenda1

1 IntroductionStructural reform is perhaps theleading economic policy issue inEurope. Indeed, it is widely arguedthat structural reform is a prerequi-site for a successful monetary union(Delors Committee, 1989). More-over since the European economiesappear to be less reformed in mar-ket flexibility terms than theirAmerican counterparts, efforts torestore economic performance vis-a‘-vis the U.S. economy have been as-sociated with the need for higherproductivity, lower costs and moreflexible labour markets in Europe.That has become known as the Lis-bon agenda.

1 Without implication, we thank Jacques Me«litz, JeanPisany-Ferry, Willem Buiter, Ken Kuttner, HansHelmut Kotz and conference participants in NewOrleans, Lisbon, Milan, Munich, Paris, Vienna,and Auckland for helpful comments. Financial sup-port from the EPRU Network, the Anniversary Fundof the Oesterreichische Nationalbank and CardiffUniversity is gratefully acknowledged.(E-mail: [email protected])

Andrew Hughes Hallett, Professor at the Vanderbilt University

Svend E. Hougaard Jensen, CEBR and SDU

Christian Richter, Loughborough University

vowi_tagung_2004 Seite 177 15.12.2004,08:32 schwarz rot

But structural reform also playsa key role in the context of EU en-largement, whether to the East orthrough the inclusion of the out-siders in the North. Here the issuehas generally been seen as a questionof whether, and at what pace, a lessreformed candidate country wouldbe able to meet a certain set of en-trance criteria before being allowedto join a more reformed union.2 Butthe reverse problem is equally im-portant: would more flexible econo-mies actually find it attractive toparticipate in a union of less flexibleeconomies?

This paper, then, has three ob-jectives. First, we examine the prop-osition that a flexible economy willfind it unattractive to be in a unionof economies whose markets are rel-atively unreformed or rigid. Thatproposition has three important cor-ollaries: a) that the more rigideconomies will want the more flexi-ble to join; b) that this incentivepattern reduces the chances of mar-ket reform, and could even encour-age candidates to move towards thelevel of the least flexible, once in;and c) it creates a distinction, interms of membership, between therelatively flexible Northern econo-mies, the less flexible Easterneconomies, and the relatively rigidmembers of the existing Europeancurrency union.

Second, we examine the proposi-tion that there may also be a linkagebetween fiscal discipline and struc-

tural reform which limits the re-forms being undertaken. This prop-osition would explain why, in theEuropean case, market reforms havebeen so widely discussed and advo-cated — but so seldom carried out.Agenda 2010 in Germany, labourmarket legislation in France, pensionreform in Italy, or the Lisbon proc-ess in general, are just four cases inpoint.

A third proposition is that struc-tural reforms are hindered by thefact that they typically involve largecosts up front, in the short run, andonly bring benefits in the longerterm. Politically sensitive policymakers may then worry that theshort-term costs will outweigh thelonger-term benefits — especially ifthe latter are rather uncertain. Toanalyse this proposition, we need touse numerical simulations in orderto gauge the size and speed of thereturns from a programme of struc-tural and market reforms.

These three propositions are fa-miliar. They have become part ofthe conventional wisdom aboutEurope; and similar propositionshave been derived in other contextsin the academic literature. For ex-ample, Hughes Hallett and Viegi(2003) find the same incentive pat-terns for membership and marketreforms in a model with monopolis-tic labour markets, with employ-ment and wage targets.3 Dellas andTavlas (2003) produce the same re-sult again using a New Keynesian

2 This point of view is derived from the analytic and empirical evidence for a negative link between economicperformance and (real) wage rigidity across many countries (Bruno, 1986). The same kind of link has beenexamined in both, the labour and product markets in Europe (Koedijk and Kremers, 1996), and in the transitioneconomies (Kaminski et al., 1996), where performance is measured in rates of growth and employment, andderegulation appears in competition policy, merger codes and the liberalisation of employment practices.

3 Similarly, they are also present in our earlier work with competitive labour markets (Hughes Hallett and Jensen,2001, 2003, 2004).

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

178 �

vowi_tagung_2004 Seite 178 15.12.2004,08:32 schwarz rot

model with representative house-holds, firms and asset markets — butlittle detail on the process of wageand price setting. And HM Treasury(2003, charts 6.3 and 6.4) find it intheir numerical simulations of flexi-bility in the U.K. government�s testsfor Economic and Monetary Union(EMU) membership. So our proposi-tions are evidently robust to differ-ent models, assumptions, or techni-ques of analysis. But no-one hasmanaged to analyse in any detailwhy these results emerge. It has notbeen possible to say, for example,whether the lack of structural re-form has been due to a problem oftiming (short-run costs versus long-run benefits); or whether it resultsfrom a mismatch of incentives; orwhether it is due to fiscal restric-tions which delay the reform proc-ess.

2 Methodology

In order to establish how a labourmarket reform could affect a coun-try�s decision to join a monetaryunion, as well as a decision by theexisting members whether to admita new member, we need a formalmodel of the incentives for eitherside to adopt a common currency.We have created such a model byadapting, and extending, a modelfirst suggested by Bayoumi (1994).4

Our approach is then to under-take a cost-benefit analysis of whetherthe adopting of a common currencyis net beneficial, by calculating forboth parties the changes in welfareif a candidate country does join,compared to the status quo if it does

not. The model has four main build-ing blocks: (1) production; (2)wages; (3) exchange rates; and (4)aggregate demand. The main macro-economic variables that enter theenlargement decision are:— The interrelationship of ag-

gregate demand betweencountriesThis is captured in the form ofexpenditure shares, denoted bythe parameter �ji, which is theproportion of country j�s incomespent on goods produced incountry i. The �ji parametersare subject to the normalisationsP

i �ji ¼ 1 andP

j �ji ¼ 1, toensure that total income is spentand that aggregate demand ex-hausts income spent on each good.

— The size of countriesA country is characterised as�large� if it has a �large impacton the union�, and �large� cantherefore be equated with beingopen with respect to the rest ofthe union. But the same econ-omy may not be large or openwith respect to the rest of theworld. Similarly, small meanshaving a small impact on theunion, and hence possibly closedwith respect to the union butnot necessarily with respect tothe rest of the world.

— The size of the underlyingdisturbancesWe consider both supply and de-mand disturbances. The discus-sion below shows how these dis-turbances affect the gains andlosses of membership; see equa-tions (1) and (2).

4 The technical details of this model are lengthy and certainly not original to us. The full framework and deriva-tion of results, is set out in Hughes Hallett and Jensen (2001, 2004). The results quoted here can be seen mostclearly in equations (1) and (2) below, which show the net gains (or costs) of EMU membership with partners ofdifferent degrees of market flexibility and reform.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

179�

vowi_tagung_2004 Seite 179 15.12.2004,08:32 schwarz rot

— The correlation between thedisturbances in differentcountriesFor the empirical implementa-tion we need standard deviationsfor the demand, supply andmonetary disturbances in theNorthern and Eastern countries,and the correlations of each ofthose individual country shockswith the corresponding averagefor the euro area countries.

— The costs of transactions be-tween different currenciesEach country has to choose itspreferred exchange rate regime.They can either opt for a mone-tary union with a single cur-rency, or they can choose sepa-rate currencies. In the latter casethere is a transactions cost be-tween the two currencies, imply-ing that, in value terms, goodsexported from country i shrinkby a factor ð1� �iÞ when theyarrive in country j. This is theusual Samuelson �iceberg� as-sumption. So rather than model-ling a separate transportationsector, we simply assume that afraction of a good shipped meltsaway in transit. For simplicity,we let �i ¼ � for all countries.

— The degree of rigidity inthe adjustment of nominalwagesTo incorporate wage rigidity, aso-called normal wage is definedto hold when there is full em-ployment, when there are noshocks, when the initial level ofprices is normalised at 1 for con-venience, and when the exchangerate is at its parity value. If thereis excess demand for labourwhen the wage is at its normalwage level, then wages will beraised until the excess demand

falls to zero. But if there is ex-cess supply of labour at the nor-mal wage, then wages remain atthis level and unemployment re-sults. Very importantly, we as-sume that employment would al-ways be at its full-employmentlevel if the exchange rate is flexi-ble.

— Factor mobility and wageprice flexibilityTo allow for different degrees offlexibility in different countries,we introduce a parameter, �i,which can vary between 0 and 1and which allows us to reachboth extremes and all points inbetween. We define �i ¼ 0 asfull downward rigidity in wagesin country i; and �i ¼ 1 as fullflexibility so that full employ-ment is always re-establishedafter a negative shock.

— AsymmetriesThere are four different types ofasymmetries: in wage/employ-ment responses; in country spe-cific shocks; in country size; andin degrees of market flexibility.

In the European Union with a singlemarket, no one can prevent the un-employed trying to leave one coun-try and seek employment in anothercountry. However, this is not thesame as saying that they actually domove in response to imbalances. In-deed, there is plenty of evidence oflow labour mobility in Europe, atleast compared to the U.S.A. (see,e.g., Begg, 1995, Obstfeld and Peri,1998). Here we simply assume thatsome initiative, of whatever kind, istaken to increase the degree of la-bour mobility such that enough flex-ibility is created to accept thesemovements in the excess supply oflabour. This requires that country j�smarkets have sufficient wage and

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

180 �

vowi_tagung_2004 Seite 180 15.12.2004,08:32 schwarz rot

price flexibility to absorb the addi-tional workers from country k, orto reemploy them at home. Andvice versa when the shocks hit coun-try j.

At this stage it may be helpful tohave a little intuition into why thesefactors are important for determin-ing the extent of the adjustmentcosts and welfare losses in a mone-tary union. The key point in thismodel is that all the costs are causedby rigidities in the labour marketsthat prevent wages, output and em-ployment from adjusting as theyshould to clear the goods and labourmarkets around the cycle. By pre-venting adjustment in one place,those rigidities cause spillovers ontoothers via their impact on trade.Consequently, the more flexible eachcountry�s labour market (�j, �k), thesmaller the adjustment needed athome or in other countries. Butgreater inflexibility means a greaterdisequilibrium (unemployment/infla-tion) at home; and consequentlyabroad too as price and quantitychanges are transmitted through ad-justments in trade and capital. Thusa higher �j value means that moreunemployed can migrate to countryk or can get employment at lowerwages at home in bad times; or that,more plausibly, wage rises will bemoderated by inflows of labour orattempts at output stabilisation inboom periods. Hence the costs fallwith �j and �k. But they rise withincreasing rigidity (�j,�k ! 0).

However, the costs will also fallwith the correlation between theshocks because there is then lessneed for each economy to adjustand absorb the unemployed fromabroad; or have their unemployedabsorbed when the domestic econ-omy is in a downturn; or to contain

wage inflation in an upturn — assum-ing, each time, that market flexibil-ity is incomplete (�j; �k < 1). But ifthe markets are completely flexible,�j ¼ �k ¼ 1 then there are no costsirrespective of the degree of correla-tion involved.

By contrast, the costs of adjust-ment will rise with the size of theshocks (�2

j ; �2k), given a certain level

of intercountry correlations. Andthe size of the adjustments will risewith the size of the spillover effects,on one economy, from a disequili-brium in the other (�jk; �kj); andthe larger are the impacts of cyclicalfluctuations at home (�jj; �kk). Fi-nally, since the adjustments all haveto go through the labour market,the costs will be larger the largerthe share of labour in national in-come (�), affected by the residualrigidities.

We are now in a position to cal-culate the net effect of EMU mem-bership, for each country, under dif-ferent degrees of market flexibility.The key parameters will be �j and�k, defined above for country j andone of its partners or the union as awhole (k); also �2

j and �2k, the var-

iances of the corresponding supplyshocks, �j and �k in j and k, respec-tively, and the correlation betweenthem. In this part of the analysis,demand shocks play no particularrole (Hughes Hallett and Jensen,2001). The expected advantages forcountry j then turn out to be

E �UjÞ ¼ �jk���

� �jk 1� �j� �

þ �jjð1� �kÞ� �

�

� 0ð Þffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffi�2j � 2�j�k þ �2

k

qð1Þ

where � 0ð Þ is the distributionfunction of jointly normal distrib-

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

181�

vowi_tagung_2004 Seite 181 15.12.2004,08:32 schwarz rot

uted random variables, and� ¼ �= 2 1� �ð Þð Þ; where � is equalto the labour share in national in-come. Similarly, to answer the�would the euro area want country jin the union�, we insert the relevantparameter values into

E �UkÞ ¼ �kj���

� �kj 1� �kð Þ þ �kk 1� �j� �� �

�

� 0ð Þffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffiffi�2j � 2�j�k þ �2

k

qð2Þ

Details of how (1) and (2) arederived will be found in HughesHallett and Jensen (2001, 2004).However, the first term on the rightin the expression for E �Uj

� �de-

scribes the net trade benefits undera single currency; and the secondterm the expected adjustment costsgiven normally distributed supplyand demand shocks.

There is an asymmetry of behav-iour due to nominal wage rigiditieshere: if there is excess demand forlabour at the current wage rate,wages will increase until that excessdemand is eliminated. But if there isexcess supply at that level, thenwages remain as they are and unem-ployment rises. The extent to whichwages or unemployment actually risedepends on the elasticity of the de-mand for labour (� ); and on thepropensity for domestic labour tomigrate out (�j) or foreign labour tomigrate in (�k). Similarly, it also de-pends on the ability of wages in j tofall (�j) to re-absorb those whowould otherwise have been unem-ployed or who migrate out; and on

the ability of wages to rise moremoderately because of cost competi-tion, and stem the inflow of labourfrom, or the outflow of jobs to,country k.

3 Fiscal Policy and theNatural Rate of Output

There are other ways of adjustingthe economy in the face of real ornominal rigidities. Two obvious sug-gestions are fiscal policies whichsmooth the cycle, and fiscal policeswhich improve responses on thesupply side.5 These two possibilitiesdivide fiscal policy into two parts:short run adjustments (flexibility inthe short-run), and long run adjust-ments (flexibility in the long-run).The former, working through theeconomy�s automatic stabilisers,smooths aggregate demand shocks.The latter provides greater flexibilityin supply responses, and could in-clude changes in payroll taxes; inthe degree and cost of social sup-port, or in the extent of market de-regulation and price liberalisation.

3.1 Flexibility in the Short RunIf automatic stabilisers are operating,we can define �k to be the propor-tion of those who retain their jobs,or can be reemployed, as a result ofan expanding fiscal deficit in a pe-riod of low demand in country k("k < 0). Similarly �j is theproportion who retain their jobsin country j when "j < 0. Thus0 � �j; �k � 1 as before. The cost-benefit analysis of membership andstructural reform now proceeds ex-actly as in section 2.2. Equations (1)

5 Discretionary fiscal policies would also be possible, but typically suffer from variable lags and uncertain impacts.Taylor (2000) therefore recommends cyclical smoothing be left to the automatic stabilisers; and that discretionarypolicies be reserved for creating long-run improvements on the supply side. We adopt this convention throughoutthis paper.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

182 �

vowi_tagung_2004 Seite 182 15.12.2004,08:32 schwarz rot

and (2) now give the net benefits ofmembership, or of accepting newmembers, but with the new inter-pretation of �k and �j as the �em-ployment saving� consequences ofthe fiscal stabilisers. These �employ-ment saving� consequences may besignificant in practice. For example,Bayoumi and Masson (1995) esti-mate that fiscal redistribution (re-gional stabilisation) in the U.S.A.and Canada may contribute 30—40cents on the dollar to stabilising re-gional incomes — and hence similarproportions to employment saving.Hence we might expect �k and �j tobe around 0.3 or 0.4. In Europe,where there are no such redistribu-tive mechanisms in place (structuralfunds excepted), those parameterswould be at least 10—15 timessmaller (and perhaps zero) unlessthe domestic governments can insti-tute strong and effective fiscal poli-cies at that level. The conclusions,nevertheless, remain the same as be-fore:— Fiscal flexibility, defined to mean

strong budget multipliers andminimal restraints on the budget,can overcome the consequencesof rigidities elsewhere in theeconomy — and the costs of ad-justing in the labour markets inparticular.

— Individual governments are likelyto only want a union which hasat least as much, if not more,fiscal flexibility than themselves— and who have the freedom andtemperament to use that flexibil-ity. But they will want to mini-mise the cost of using fiscal poli-cy flexibly themselves.

— A �large� country will want toensure fiscal flexibility at homebefore joining; but a �small�country, including the current

candidates, would want the unionto accept the need for fiscal flex-ibility before agreeing to join.

Conversely, a lack of fiscal flexibilitywill bring greater costs to both par-ties — irrespective of where the in-flexibilities arise (�j ! 0 or �k ! 0,or both, in (1) and (2)); and irre-spective of whether they arise be-cause fiscal deficits are restricted bythe Stability Pact, or because debthas become too large. The point isthat fiscal restrictions in one countrywill impose costs on all, by increas-ing the amount of adjustment thatneeds to be undertaken to restoreequilibrium within each of the othercountries. Conversely, extra flexibil-ity in one country will benefit all,although it will benefit the homecountry most if �jj > �jk; k 6¼ j;holds in (1) and (2).

3.2 Flexibility in the Long RunWhat happens if policy makers cre-ate greater flexibility in the long runby lowering the natural rate of un-employment? As noted above, thesechanges would come from structuralreforms which reduce payroll taxes;or lower the cost and disincentiveeffects of social security; or whichmake institutional changes to liberal-ise markets, to improve competi-tion, skills and technology etc. Ourmodel shows that such changeswould make no difference to the netbenefits of union membership if itwere thought that those reformswould be undertaken whether ornot country j joined.

The reason is that structural ad-justments that alter the natural rateof unemployment or output capacitywould add a constant term of�yk > 0 and �yj > 0 to the rightof Uk or Uj respectively, where�yk > 0 represents an increase in

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

183�

vowi_tagung_2004 Seite 183 15.12.2004,08:32 schwarz rot

output capacity. Equations (1) and(2) show that such changes wouldmake no difference to the net bene-fits of union membership if such re-forms would be made anyway sincethese additional terms of �jk�ykand �kj�yj would, on average, can-cel out in (1) and (2). Only in thecase where the same reforms failedin the union, �yk < 0, but succeedoutside �yj � 0 would the costs ofmembership rise.

3.3 Could Fiscal Restrictions PreventStructural Reform?

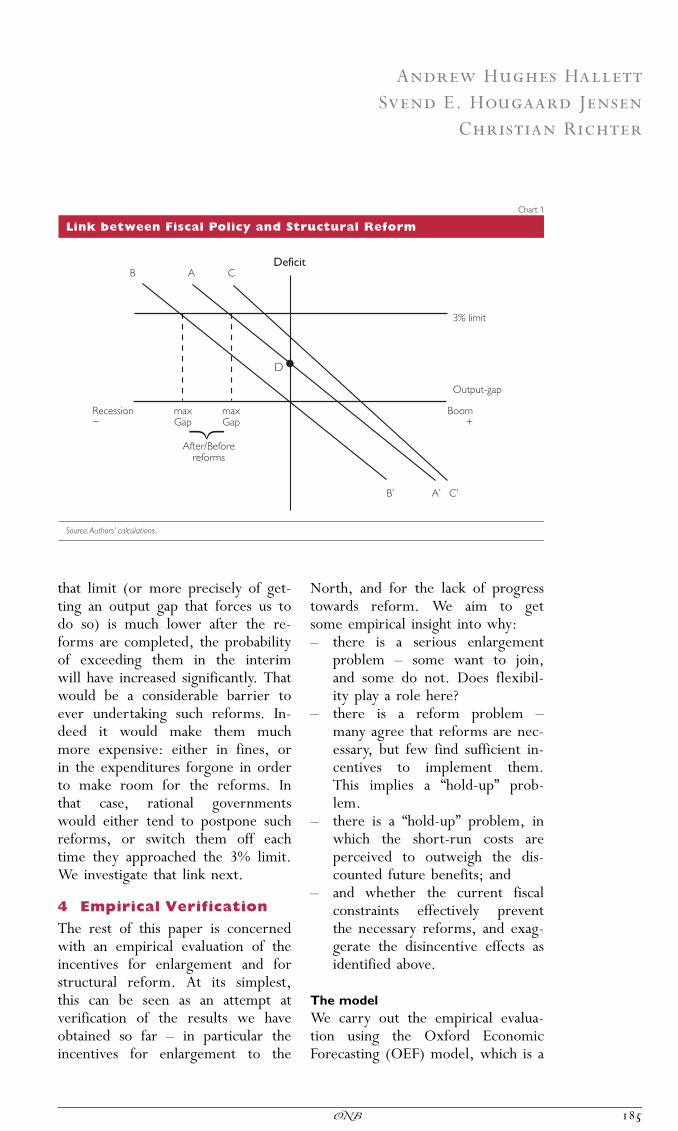

In the light of the previous section,we have to ask whether Europe�s fis-cal restrictions — such as those inthe Stability and Growth Pact —could prevent the necessary reformsbeing undertaken. One could imag-ine that any programme of structuralreform would entail additional pub-lic expenditures, and possibly lowerrevenues or larger output gaps whilethe reforms were being undertaken.Reform will put people out of workwhile the reforms are being carriedout, and it will take time beforethose people are reemployed. In-deed, many of them may need re-training or new skills. There willtherefore be additional unemploy-ment and other social benefits to bepaid in the interim, and extra re-training programmes to be paid for.At the same time, there may well benew infrastructure projects, develop-ment grants, support for new tech-nologies, etc. In each case, publicexpenditures will rise. But with un-employment temporarily higher andoutput lower, tax revenues will fall.Consequently, the fiscal deficit will

be larger, and the deficit ratio larger,than the trend position of either.

These changes will lead to chart1, which shows how the fiscal deficitratio could vary with different sizesof the output gap. The bold lineAA� shows the position before struc-tural reforms are undertaken.6 PointD is the structural deficit for thiseconomy; that deficit being positiveeven though the output gap is zero.

The reform programme would,presumably, be designed to eliminatethat structural deficit. That wouldget us to line BB�. But the argumentabove shows that we would have toreach that position via the line CC�,which represents a short term ad-justment phase. In fact, it is notclear exactly where CC� should lie,other than it must be above AA�and with a slope no less than AA�.Consequently, it could be a simplerightward shift from AA�; or a right-ward shift with steeper slope; or arightward shift for negative outputgaps only. Experience suggests thatit is probably one of the latter twopossibilities, since structural reformsduring boom periods are going tobe easier and cheaper to finance;meaning the unemployment/retrain-ing costs will be lower per unit out-put gap. In that case, the CC� linewill be as we show it.

Now we can impose fiscal con-straints to see the consequences. Inchart 1 this is represented by theStability and Growth Pact�s (SGP)3% limit on the deficit ratio. It isimmediately obvious that any suchrestriction would interfere with theprocess of structural reform. Al-though the probability of exceeding

6 The European Commission (2002) has estimated the slope of this line to be approximately —0.5 for the euro areaas a whole, a bit steeper for countries with extensive social welfare programmes and a bit less steep elsewhere.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

184 �

vowi_tagung_2004 Seite 184 15.12.2004,08:32 schwarz rot

that limit (or more precisely of get-ting an output gap that forces us todo so) is much lower after the re-forms are completed, the probabilityof exceeding them in the interimwill have increased significantly. Thatwould be a considerable barrier toever undertaking such reforms. In-deed it would make them muchmore expensive: either in fines, orin the expenditures forgone in orderto make room for the reforms. Inthat case, rational governmentswould either tend to postpone suchreforms, or switch them off eachtime they approached the 3% limit.We investigate that link next.

4 Empirical Verification

The rest of this paper is concernedwith an empirical evaluation of theincentives for enlargement and forstructural reform. At its simplest,this can be seen as an attempt atverification of the results we haveobtained so far — in particular theincentives for enlargement to the

North, and for the lack of progresstowards reform. We aim to getsome empirical insight into why:— there is a serious enlargement

problem — some want to join,and some do not. Does flexibil-ity play a role here?

— there is a reform problem —many agree that reforms are nec-essary, but few find sufficient in-centives to implement them.This implies a �hold-up� prob-lem.

— there is a �hold-up� problem, inwhich the short-run costs areperceived to outweigh the dis-counted future benefits; and

— and whether the current fiscalconstraints effectively preventthe necessary reforms, and exag-gerate the disincentive effects asidentified above.

The modelWe carry out the empirical evalua-tion using the Oxford EconomicForecasting (OEF) model, which is a

)��$�3������5�-���������������2����������'���

�������

����� ��&�)��#,����������#$

�� ����

!E�+*&*�

�))&F

� � �

4(�5(�-,�5

�

�$ $..*)%0

&�8��5

&�8��5

�/�$�G�$/)�$�$/)�&.

��H �H �H

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

185�

vowi_tagung_2004 Seite 185 15.12.2004,08:32 schwarz rot

traditional multi-country economet-ric model (OEF, 2003). There aretwo reasons for selecting the OEFmodel. First, it is the only publicallyavailable model which contains a fullspecification of all the regions weare interested in: i.e., the Northern,Eastern and euro area countries.Second, unlike the OECD�s Interlinkand the IMF�s Multimod, the OEFmodel has a clear specification ofthe structural (supply-side) asymme-tries that can be exploited to illus-trate the analysis of this paper.

The OEF model contains a se-quence of theory based empiricalmodels covering all the OECDeconomies, 14 of the largest emerg-ing markets economies, and six trad-ing blocs covering the rest of theworld economy. These country mod-els are then linked by trade rela-tions, world prices for tradables, in-tercountry capital flows, and interestrate and exchange rate effects underdifferent possible exchange rate re-gimes.7

The countries covered specifi-cally include the U.S.A., Canada andJapan, plus China and Russia outsidethe EU; the euro area countries,and the U.K., Denmark and Swedenoutside the euro but in the EU; andPoland, Hungary and the Czech Re-public among the new accessioncountries. Each of these countrymodels is based on a traditional in-come-expenditure specification, plusa rather detailed supply-side specifi-cation to determine wages, prices,employment, and unit labour costs.

There is also a government sector toconduct fiscal policy. Total govern-ment revenues are collected from avariety of sources, and the govern-ment has a number of different out-lays. These fiscal policy variablesmay affect labour market behaviour.Although the specification of eachcountry is broadly similar, there areimportant differences both in thelevel of aggregation and in terms ofdifferent responses to shocks.

Since we are concerned aboutwage rigidities in general, and thesupply side in particular, we notehere the way in which wages andsalaries are set. The OEF model in-corporates short-run nominal andreal wage rigidities, which ensurethe existence of involuntary unem-ployment and monetary effects onthe real economy. In the long runthe employment equation solves fora constant level of real unit labourcosts, given by labour�s share in theproduction function, while the wageand price equations solve for thelevel of unemployment consistentwith this labour share. With verticalPhillips and aggregate supply curvesin the long run, monetary policy de-termines the inflation rate. Butstructural and supply-side policiesdetermine the unemployment rate.Structural unemployment is there-fore possible. Indeed, the equili-brium rate of unemployment is de-termined by the gap between the to-tal real cost of labour to employers,and the real value of post-tax wagesreceived by employees.

7 There is also a monetary sector in the model containing a monetary equilibrium and a Taylor rule. The exchangerate regimes are floating for the dollar, euro, pound, yen and other major currencies; but a single currencywithin the euro area, and a strict exchange rate targeting arrangement for Denmark (ERM-II), and for the acces-sion countries in Eastern Europe. It is important to note that the model also determines some world market varia-bles (such as oil and commodity prices) and the world aggregates (world GDP, industrial production) endoge-nously. A more detailed specification of each of the model�s expenditure blocs is provided in OEF (2003).

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

186 �

vowi_tagung_2004 Seite 186 15.12.2004,08:32 schwarz rot

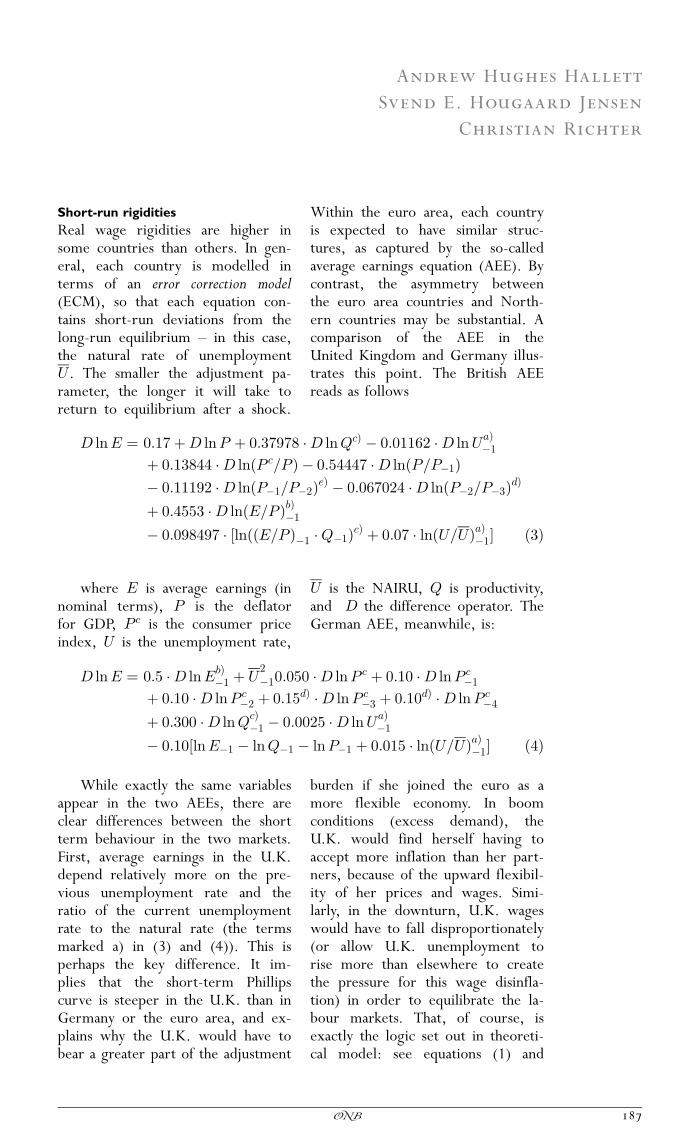

Short-run rigiditiesReal wage rigidities are higher insome countries than others. In gen-eral, each country is modelled interms of an error correction model(ECM), so that each equation con-tains short-run deviations from thelong-run equilibrium — in this case,the natural rate of unemploymentU. The smaller the adjustment pa-rameter, the longer it will take toreturn to equilibrium after a shock.

Within the euro area, each countryis expected to have similar struc-tures, as captured by the so-calledaverage earnings equation (AEE). Bycontrast, the asymmetry betweenthe euro area countries and North-ern countries may be substantial. Acomparison of the AEE in theUnited Kingdom and Germany illus-trates this point. The British AEEreads as follows

D lnE ¼ 0:17þD lnP þ 0:37978 �D lnQcÞ � 0:01162 �D lnUaÞ�1

þ 0:13844 �D lnðPc=P Þ � 0:54447 �D lnðP=P�1Þ� 0:11192 �D lnðP�1=P�2ÞeÞ � 0:067024 �D lnðP�2=P�3ÞdÞ

þ 0:4553 �D lnðE=P ÞbÞ�1

� 0:098497 � ½lnððE=P Þ�1 �Q�1ÞcÞ þ 0:07 � lnðU=UÞaÞ�1� ð3Þ

where E is average earnings (innominal terms), P is the deflatorfor GDP, Pc is the consumer priceindex, U is the unemployment rate,

U is the NAIRU, Q is productivity,and D the difference operator. TheGerman AEE, meanwhile, is:

D lnE ¼ 0:5 �D lnEbÞ�1 þ U

2

�10:050 �D lnPc þ 0:10 �D lnPc�1

þ 0:10 �D lnPc�2 þ 0:15dÞ �D lnPc

�3 þ 0:10dÞ �D lnPc�4

þ 0:300 �D lnQcÞ�1 � 0:0025 �D lnU

a�1

� 0:10½lnE�1 � lnQ�1 � lnP�1 þ 0:015 � lnðU=UÞaÞ�1� ð4Þ

While exactly the same variablesappear in the two AEEs, there areclear differences between the shortterm behaviour in the two markets.First, average earnings in the U.K.depend relatively more on the pre-vious unemployment rate and theratio of the current unemploymentrate to the natural rate (the termsmarked a) in (3) and (4)). This isperhaps the key difference. It im-plies that the short-term Phillipscurve is steeper in the U.K. than inGermany or the euro area, and ex-plains why the U.K. would have tobear a greater part of the adjustment

burden if she joined the euro as amore flexible economy. In boomconditions (excess demand), theU.K. would find herself having toaccept more inflation than her part-ners, because of the upward flexibil-ity of her prices and wages. Simi-larly, in the downturn, U.K. wageswould have to fall disproportionately(or allow U.K. unemployment torise more than elsewhere to createthe pressure for this wage disinfla-tion) in order to equilibrate the la-bour markets. That, of course, isexactly the logic set out in theoreti-cal model: see equations (1) and

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

187�

vowi_tagung_2004 Seite 187 15.12.2004,08:32 schwarz rot

(2). Interestingly, it is also the con-clusion reached in the six numericalsimulations conducted by the U.K.Treasury on this issue (HM Treasury,2003).

Second, once a disturbance hasset in, the German equation hasmore persistence, as reflected in ahigher coefficient on the previousperiod�s rate of change in averageearnings (term b)). Third, the U.K.has more supply side sensitivity(term c)) if there is a negative prod-uctivity shock. Fourth, Germany hasmore persistent accommodation ofprice rises, out to Pc

�4 instead ofP�2 (term d)). Note also that Pc,unlike P , has import prices in it,and hence implies an additionalsource of inflationary stickiness inGermany. Finally, P is influenced bycapacity utilisation which implies ex-tra market sensitivity in the Britishequation (term e)).

Long-run rigiditiesIn the long run, structural rigiditiesaffect unemployment, and hencewages and economic performance.The equilibrium rate of unemploy-ment is determined by the �taxwedge� W, defined as the gap be-tween total cost of labour to em-ployers — including social securitycontributions — and the real value ofpost-tax wages received by employ-ees. ThuslnðUÞ ¼

�0 þ �1W þ �2 ln Pf=P� �

ð5Þ

where Pf are domestic fuel prices,P is the GDP deflator, and

W ¼ ln E 1þ �p þ Tpoc=Y WS� �

=P� �

� ln E 1� �a � �sð Þ=Pc½ � ð6Þ

where �p is the payroll tax rate,Tpoc is the personal sector other

contributions, Y WS are wages andsalaries, �a is the average personalincome tax rate, �s is the employeesocial security contribution rate, andE and Pc are as before. Rigiditiesmay therefore vary between coun-tries in the long run because the �coefficients in (5) differ; or becausethe components of the tax wedge(6) take different values in differentplaces. Structural unemploymentcreated in the short run can there-fore persist; and the choice of mon-etary regime may have long-run ef-fects through W if not throughother channels as well.

5 Economic and MonetaryUnion and StructuralReform

5.1 The Baseline SolutionWe turn now to the relative impor-tance of market inflexibilities inEMU. To judge that we have to cre-ate a counterfactual where there areno enlargements, no new flexibil-ities, and no additional fiscal con-straints. This baseline solution wouldtherefore not have any new econo-mies joining EMU; it will not havethe SGP�s 3% deficit limit imposedon those countries; and will nothave the current degree of labourmarket flexibility in Germany,France etc. increased.

It is important to stress that theprojections from such a scenario arenot of great interest in themselves.But they are necessary as a bench-mark against which the benefits ofan alternative scenario can be meas-ured: such as the United Kingdomjoins the euro; national fiscal policiesare restrained; or Germany makesher labour market more sensitive tomarket conditions. Consequently, itis not the baseline values themselveswhich matter, but whether the

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

188 �

vowi_tagung_2004 Seite 188 15.12.2004,08:32 schwarz rot

changes from that baseline can besaid to be favourable or unfavour-able.

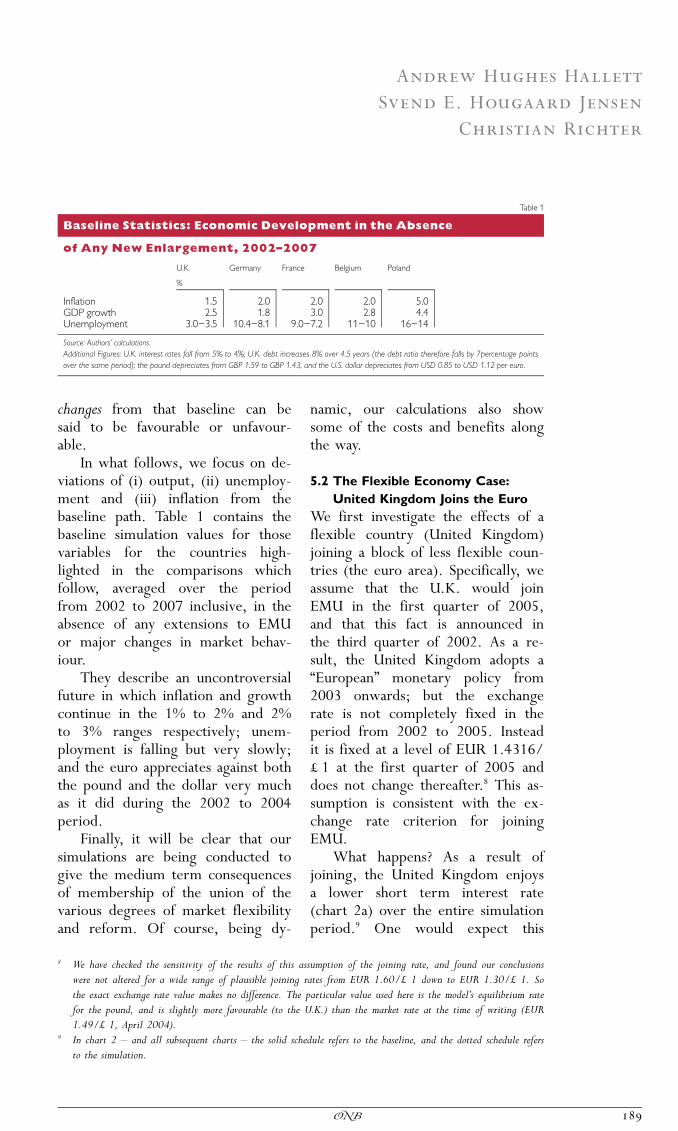

In what follows, we focus on de-viations of (i) output, (ii) unemploy-ment and (iii) inflation from thebaseline path. Table 1 contains thebaseline simulation values for thosevariables for the countries high-lighted in the comparisons whichfollow, averaged over the periodfrom 2002 to 2007 inclusive, in theabsence of any extensions to EMUor major changes in market behav-iour.

They describe an uncontroversialfuture in which inflation and growthcontinue in the 1% to 2% and 2%to 3% ranges respectively; unem-ployment is falling but very slowly;and the euro appreciates against boththe pound and the dollar very muchas it did during the 2002 to 2004period.

Finally, it will be clear that oursimulations are being conducted togive the medium term consequencesof membership of the union of thevarious degrees of market flexibilityand reform. Of course, being dy-

namic, our calculations also showsome of the costs and benefits alongthe way.

5.2 The Flexible Economy Case:United Kingdom Joins the Euro

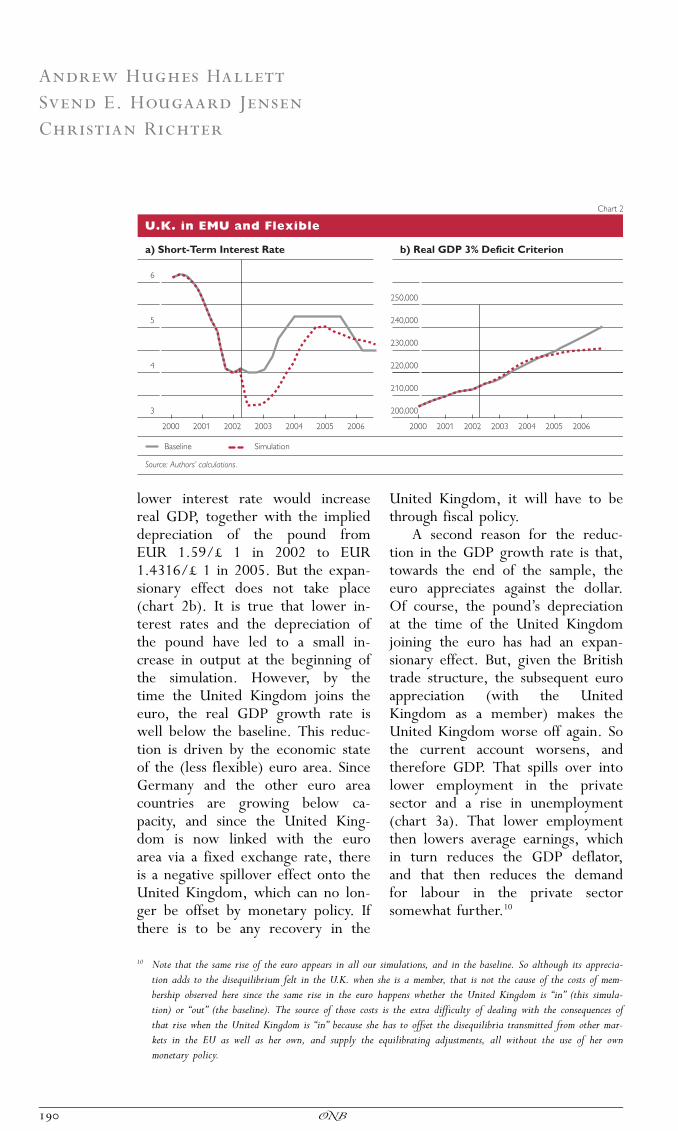

We first investigate the effects of aflexible country (United Kingdom)joining a block of less flexible coun-tries (the euro area). Specifically, weassume that the U.K. would joinEMU in the first quarter of 2005,and that this fact is announced inthe third quarter of 2002. As a re-sult, the United Kingdom adopts a�European� monetary policy from2003 onwards; but the exchangerate is not completely fixed in theperiod from 2002 to 2005. Insteadit is fixed at a level of EUR 1.4316/£ 1 at the first quarter of 2005 anddoes not change thereafter.8 This as-sumption is consistent with the ex-change rate criterion for joiningEMU.

What happens? As a result ofjoining, the United Kingdom enjoysa lower short term interest rate(chart 2a) over the entire simulationperiod.9 One would expect this

Table 1

Baseline Statistics: Economic Development in the Absence

of Any New Enlargement, 2002—2007

U.K. Germany France Belgium Poland

%

Inflation 1.5 2.0 2.0 2.0 5.0GDP growth 2.5 1.8 3.0 2.8 4.4Unemployment 3.0—3.5 10.4—8.1 9.0—7.2 11—10 16—14

Source: Authors� calculations.Additional Figures: U.K. interest rates fall from 5% to 4%; U.K. debt increases 8% over 4.5 years (the debt ratio therefore falls by 7percentage pointsover the same period); the pound depreciates from GBP 1.59 to GBP 1.43, and the U.S. dollar depreciates from USD 0.85 to USD 1.12 per euro.

8 We have checked the sensitivity of the results of this assumption of the joining rate, and found our conclusionswere not altered for a wide range of plausible joining rates from EUR 1.60/£ 1 down to EUR 1.30/£ 1. Sothe exact exchange rate value makes no difference. The particular value used here is the model�s equilibrium ratefor the pound, and is slightly more favourable (to the U.K.) than the market rate at the time of writing (EUR1.49/£ 1, April 2004).

9 In chart 2 — and all subsequent charts — the solid schedule refers to the baseline, and the dotted schedule refersto the simulation.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

189�

vowi_tagung_2004 Seite 189 15.12.2004,08:32 schwarz rot

lower interest rate would increasereal GDP, together with the implieddepreciation of the pound fromEUR 1.59/£ 1 in 2002 to EUR1.4316/£ 1 in 2005. But the expan-sionary effect does not take place(chart 2b). It is true that lower in-terest rates and the depreciation ofthe pound have led to a small in-crease in output at the beginning ofthe simulation. However, by thetime the United Kingdom joins theeuro, the real GDP growth rate iswell below the baseline. This reduc-tion is driven by the economic stateof the (less flexible) euro area. SinceGermany and the other euro areacountries are growing below ca-pacity, and since the United King-dom is now linked with the euroarea via a fixed exchange rate, thereis a negative spillover effect onto theUnited Kingdom, which can no lon-ger be offset by monetary policy. Ifthere is to be any recovery in the

United Kingdom, it will have to bethrough fiscal policy.

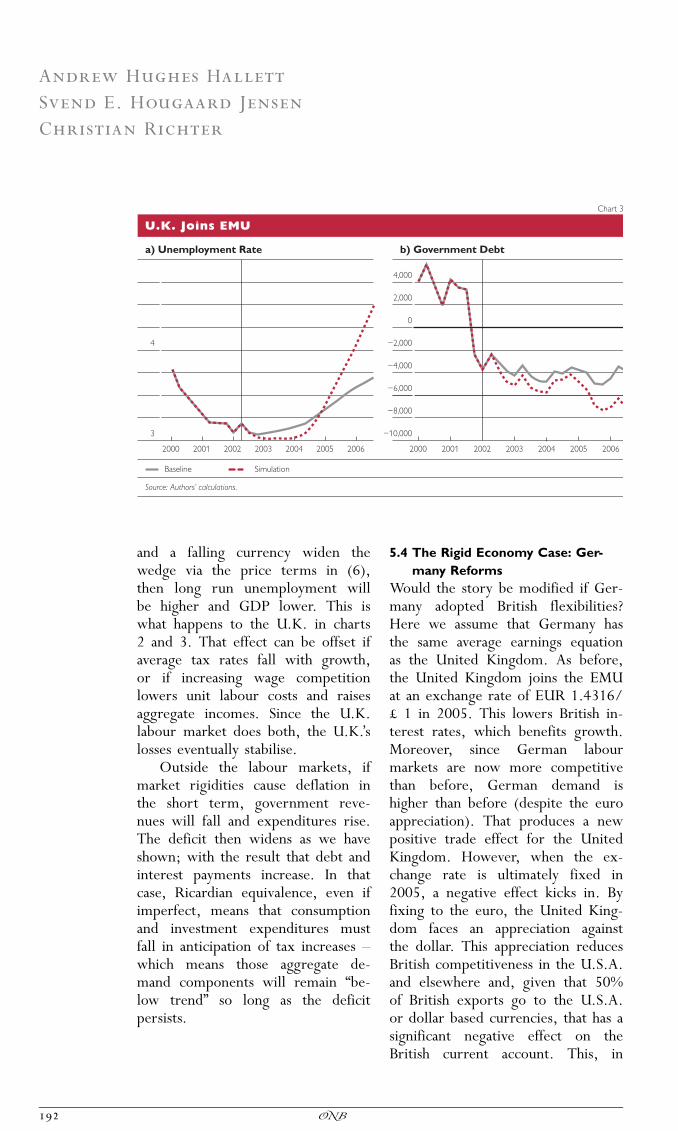

A second reason for the reduc-tion in the GDP growth rate is that,towards the end of the sample, theeuro appreciates against the dollar.Of course, the pound�s depreciationat the time of the United Kingdomjoining the euro has had an expan-sionary effect. But, given the Britishtrade structure, the subsequent euroappreciation (with the UnitedKingdom as a member) makes theUnited Kingdom worse off again. Sothe current account worsens, andtherefore GDP. That spills over intolower employment in the privatesector and a rise in unemployment(chart 3a). That lower employmentthen lowers average earnings, whichin turn reduces the GDP deflator,and that then reduces the demandfor labour in the private sectorsomewhat further.10

�?@?�����0������5��6�3��

�

�

!

�������

�������� ��!��������������

��:

��:

�!:

��:

��:

�:

"������������������#���$�������

����� � &�)��#,����������#$

� �� �� �! �� �� � � �� �� �! �� �� �

��.$+*%$ �*&(+��*)%

10 Note that the same rise of the euro appears in all our simulations, and in the baseline. So although its apprecia-tion adds to the disequilibrium felt in the U.K. when she is a member, that is not the cause of the costs of mem-bership observed here since the same rise in the euro happens whether the United Kingdom is �in� (this simula-tion) or �out� (the baseline). The source of those costs is the extra difficulty of dealing with the consequences ofthat rise when the United Kingdom is �in� because she has to offset the disequilibria transmitted from other mar-kets in the EU as well as her own, and supply the equilibrating adjustments, all without the use of her ownmonetary policy.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

190 �

vowi_tagung_2004 Seite 190 15.12.2004,08:32 schwarz rot

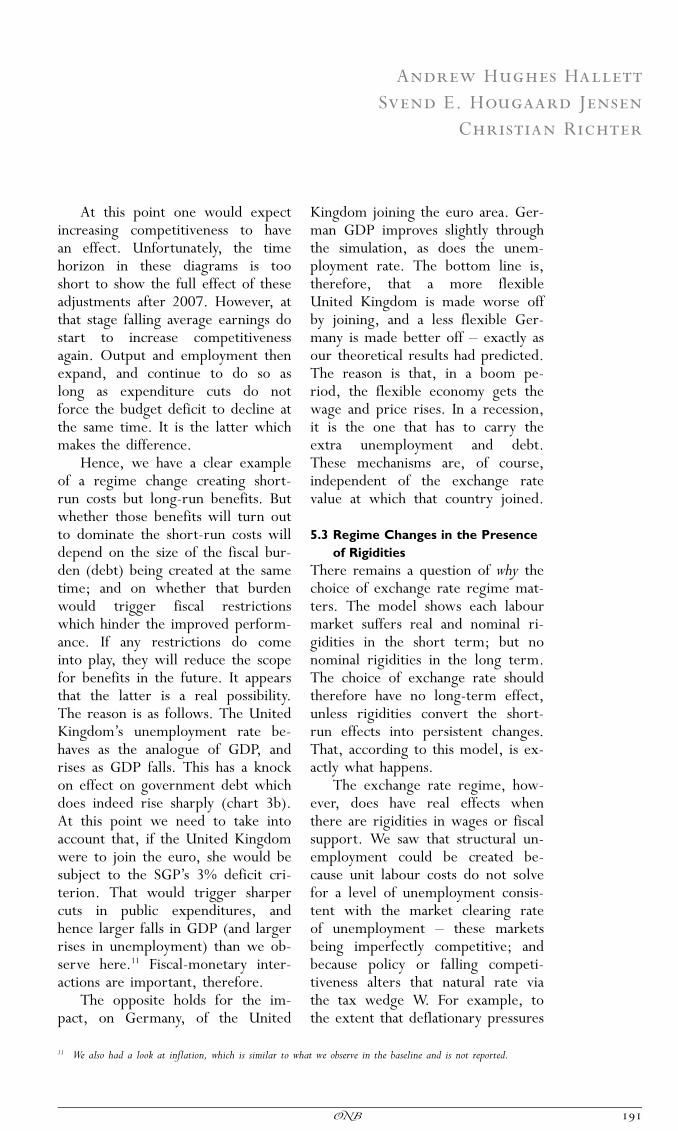

At this point one would expectincreasing competitiveness to havean effect. Unfortunately, the timehorizon in these diagrams is tooshort to show the full effect of theseadjustments after 2007. However, atthat stage falling average earnings dostart to increase competitivenessagain. Output and employment thenexpand, and continue to do so aslong as expenditure cuts do notforce the budget deficit to decline atthe same time. It is the latter whichmakes the difference.

Hence, we have a clear exampleof a regime change creating short-run costs but long-run benefits. Butwhether those benefits will turn outto dominate the short-run costs willdepend on the size of the fiscal bur-den (debt) being created at the sametime; and on whether that burdenwould trigger fiscal restrictionswhich hinder the improved perform-ance. If any restrictions do comeinto play, they will reduce the scopefor benefits in the future. It appearsthat the latter is a real possibility.The reason is as follows. The UnitedKingdom�s unemployment rate be-haves as the analogue of GDP, andrises as GDP falls. This has a knockon effect on government debt whichdoes indeed rise sharply (chart 3b).At this point we need to take intoaccount that, if the United Kingdomwere to join the euro, she would besubject to the SGP�s 3% deficit cri-terion. That would trigger sharpercuts in public expenditures, andhence larger falls in GDP (and largerrises in unemployment) than we ob-serve here.11 Fiscal-monetary inter-actions are important, therefore.

The opposite holds for the im-pact, on Germany, of the United

Kingdom joining the euro area. Ger-man GDP improves slightly throughthe simulation, as does the unem-ployment rate. The bottom line is,therefore, that a more flexibleUnited Kingdom is made worse offby joining, and a less flexible Ger-many is made better off — exactly asour theoretical results had predicted.The reason is that, in a boom pe-riod, the flexible economy gets thewage and price rises. In a recession,it is the one that has to carry theextra unemployment and debt.These mechanisms are, of course,independent of the exchange ratevalue at which that country joined.

5.3 Regime Changes in the Presenceof Rigidities

There remains a question of why thechoice of exchange rate regime mat-ters. The model shows each labourmarket suffers real and nominal ri-gidities in the short term; but nonominal rigidities in the long term.The choice of exchange rate shouldtherefore have no long-term effect,unless rigidities convert the short-run effects into persistent changes.That, according to this model, is ex-actly what happens.

The exchange rate regime, how-ever, does have real effects whenthere are rigidities in wages or fiscalsupport. We saw that structural un-employment could be created be-cause unit labour costs do not solvefor a level of unemployment consis-tent with the market clearing rateof unemployment — these marketsbeing imperfectly competitive; andbecause policy or falling competi-tiveness alters that natural rate viathe tax wedge W. For example, tothe extent that deflationary pressures

11 We also had a look at inflation, which is similar to what we observe in the baseline and is not reported.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

191�

vowi_tagung_2004 Seite 191 15.12.2004,08:32 schwarz rot

and a falling currency widen thewedge via the price terms in (6),then long run unemployment willbe higher and GDP lower. This iswhat happens to the U.K. in charts2 and 3. That effect can be offset ifaverage tax rates fall with growth,or if increasing wage competitionlowers unit labour costs and raisesaggregate incomes. Since the U.K.labour market does both, the U.K.�slosses eventually stabilise.

Outside the labour markets, ifmarket rigidities cause deflation inthe short term, government reve-nues will fall and expenditures rise.The deficit then widens as we haveshown; with the result that debt andinterest payments increase. In thatcase, Ricardian equivalence, even ifimperfect, means that consumptionand investment expenditures mustfall in anticipation of tax increases —which means those aggregate de-mand components will remain �be-low trend� so long as the deficitpersists.

5.4 The Rigid Economy Case: Ger-many Reforms

Would the story be modified if Ger-many adopted British flexibilities?Here we assume that Germany hasthe same average earnings equationas the United Kingdom. As before,the United Kingdom joins the EMUat an exchange rate of EUR 1.4316/£ 1 in 2005. This lowers British in-terest rates, which benefits growth.Moreover, since German labourmarkets are now more competitivethan before, German demand ishigher than before (despite the euroappreciation). That produces a newpositive trade effect for the UnitedKingdom. However, when the ex-change rate is ultimately fixed in2005, a negative effect kicks in. Byfixing to the euro, the United King-dom faces an appreciation againstthe dollar. This appreciation reducesBritish competitiveness in the U.S.A.and elsewhere and, given that 50%of British exports go to the U.S.A.or dollar based currencies, that has asignificant negative effect on theBritish current account. This, in

�?@?�;���-��0�

�

!

������!

���%��!&� !��������

�:

�:

0�:

0�:

0:

0�:

0�:

"���'���!������"�

����� � &�)��#,����������#$

� �� �� �! �� �� � � �� �� �! �� �� �

��.$+*%$ �*&(+��*)%

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

192 �

vowi_tagung_2004 Seite 192 15.12.2004,08:32 schwarz rot

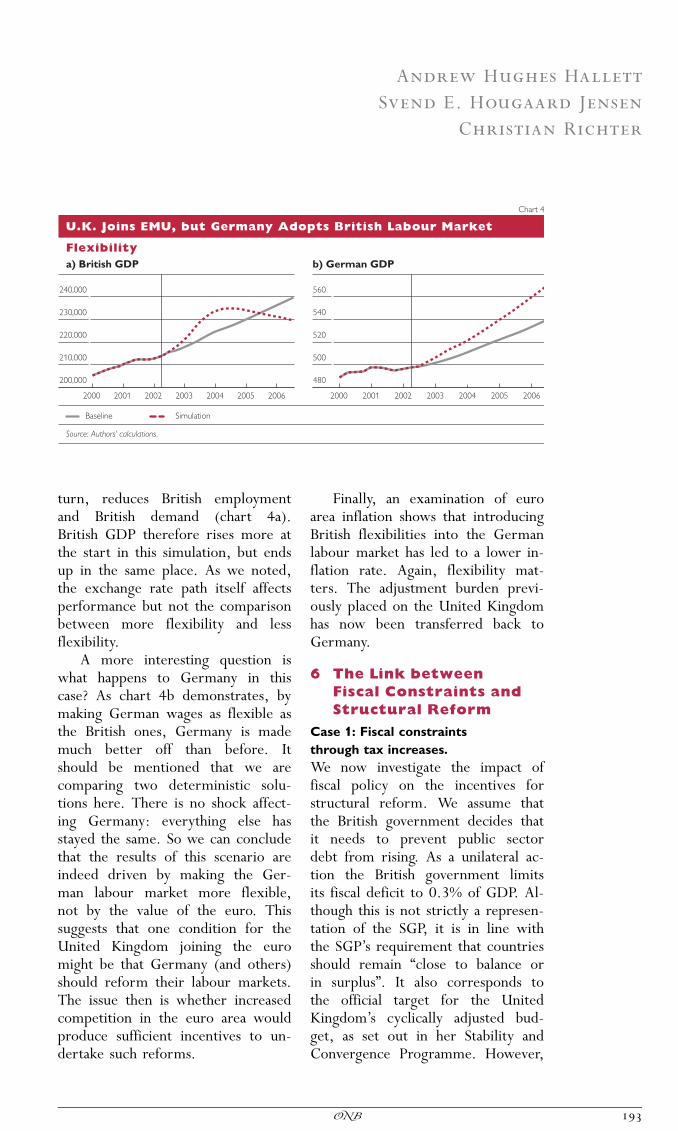

turn, reduces British employmentand British demand (chart 4a).British GDP therefore rises more atthe start in this simulation, but endsup in the same place. As we noted,the exchange rate path itself affectsperformance but not the comparisonbetween more flexibility and lessflexibility.

A more interesting question iswhat happens to Germany in thiscase? As chart 4b demonstrates, bymaking German wages as flexible asthe British ones, Germany is mademuch better off than before. Itshould be mentioned that we arecomparing two deterministic solu-tions here. There is no shock affect-ing Germany: everything else hasstayed the same. So we can concludethat the results of this scenario areindeed driven by making the Ger-man labour market more flexible,not by the value of the euro. Thissuggests that one condition for theUnited Kingdom joining the euromight be that Germany (and others)should reform their labour markets.The issue then is whether increasedcompetition in the euro area wouldproduce sufficient incentives to un-dertake such reforms.

Finally, an examination of euroarea inflation shows that introducingBritish flexibilities into the Germanlabour market has led to a lower in-flation rate. Again, flexibility mat-ters. The adjustment burden previ-ously placed on the United Kingdomhas now been transferred back toGermany.

6 The Link betweenFiscal Constraints andStructural Reform

Case 1: Fiscal constraintsthrough tax increases.We now investigate the impact offiscal policy on the incentives forstructural reform. We assume thatthe British government decides thatit needs to prevent public sectordebt from rising. As a unilateral ac-tion the British government limitsits fiscal deficit to 0.3% of GDP. Al-though this is not strictly a represen-tation of the SGP, it is in line withthe SGP�s requirement that countriesshould remain �close to balance orin surplus�. It also corresponds tothe official target for the UnitedKingdom�s cyclically adjusted bud-get, as set out in her Stability andConvergence Programme. However,

�?@?�;���-��0��3����������%���-�.���-��)�3����0��$�

5��6�3����

��:

�!:

��:

��:

�:

�������

���(����������

�

��

��

�

��

"�����!������

����� � &�)��#,����������#$

� �� �� �! �� �� � � �� �� �! �� �� �

��.$+*%$ �*&(+��*)%

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

193�

vowi_tagung_2004 Seite 193 15.12.2004,08:32 schwarz rot

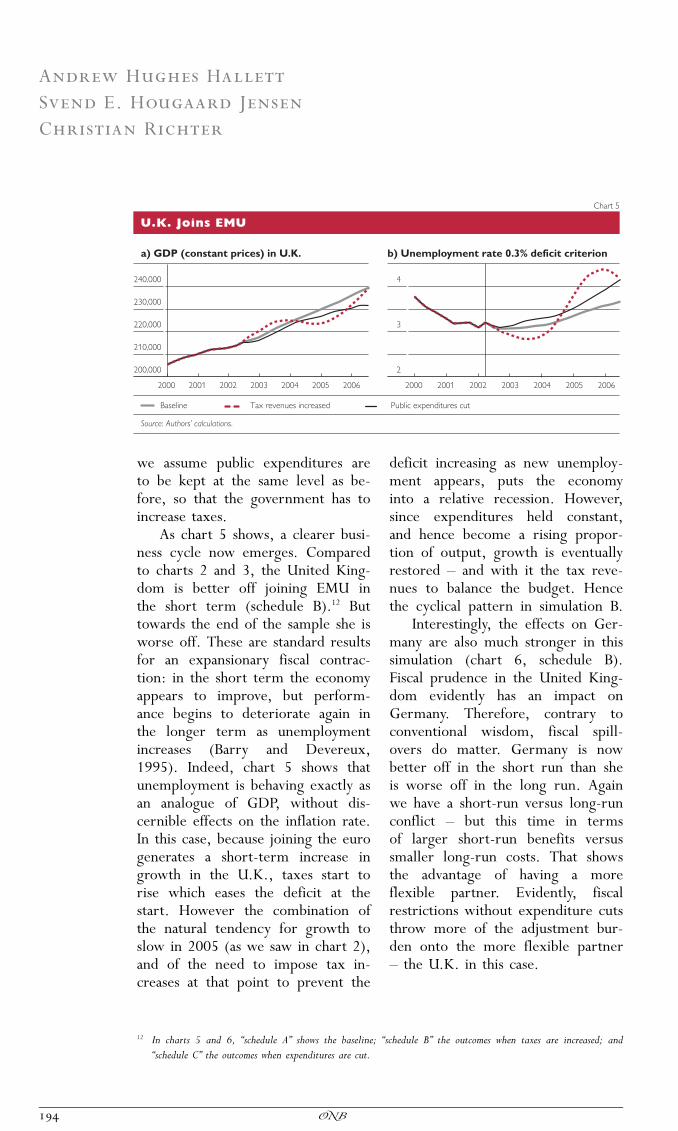

we assume public expenditures areto be kept at the same level as be-fore, so that the government has toincrease taxes.

As chart 5 shows, a clearer busi-ness cycle now emerges. Comparedto charts 2 and 3, the United King-dom is better off joining EMU inthe short term (schedule B).12 Buttowards the end of the sample she isworse off. These are standard resultsfor an expansionary fiscal contrac-tion: in the short term the economyappears to improve, but perform-ance begins to deteriorate again inthe longer term as unemploymentincreases (Barry and Devereux,1995). Indeed, chart 5 shows thatunemployment is behaving exactly asan analogue of GDP, without dis-cernible effects on the inflation rate.In this case, because joining the eurogenerates a short-term increase ingrowth in the U.K., taxes start torise which eases the deficit at thestart. However the combination ofthe natural tendency for growth toslow in 2005 (as we saw in chart 2),and of the need to impose tax in-creases at that point to prevent the

deficit increasing as new unemploy-ment appears, puts the economyinto a relative recession. However,since expenditures held constant,and hence become a rising propor-tion of output, growth is eventuallyrestored — and with it the tax reve-nues to balance the budget. Hencethe cyclical pattern in simulation B.

Interestingly, the effects on Ger-many are also much stronger in thissimulation (chart 6, schedule B).Fiscal prudence in the United King-dom evidently has an impact onGermany. Therefore, contrary toconventional wisdom, fiscal spill-overs do matter. Germany is nowbetter off in the short run than sheis worse off in the long run. Againwe have a short-run versus long-runconflict — but this time in termsof larger short-run benefits versussmaller long-run costs. That showsthe advantage of having a moreflexible partner. Evidently, fiscalrestrictions without expenditure cutsthrow more of the adjustment bur-den onto the more flexible partner— the U.K. in this case.

�?@?�;���-��0�

��:

�!:

��:

��:

�:

�������

�������)#�������&��#�������%�*�

�

!

�

"��%��!&� !��������������+���#���#�������

����� � &�)��#,����������#$

� �� �� �! �� �� � � �� �� �! �� �� �

��.$+*%$ ��8��$3$%($.�*% �$�.$" �(�+* �$85$%"*�(�$.� (�

12 In charts 5 and 6, �schedule A� shows the baseline; �schedule B� the outcomes when taxes are increased; and�schedule C� the outcomes when expenditures are cut.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

194 �

vowi_tagung_2004 Seite 194 15.12.2004,08:32 schwarz rot

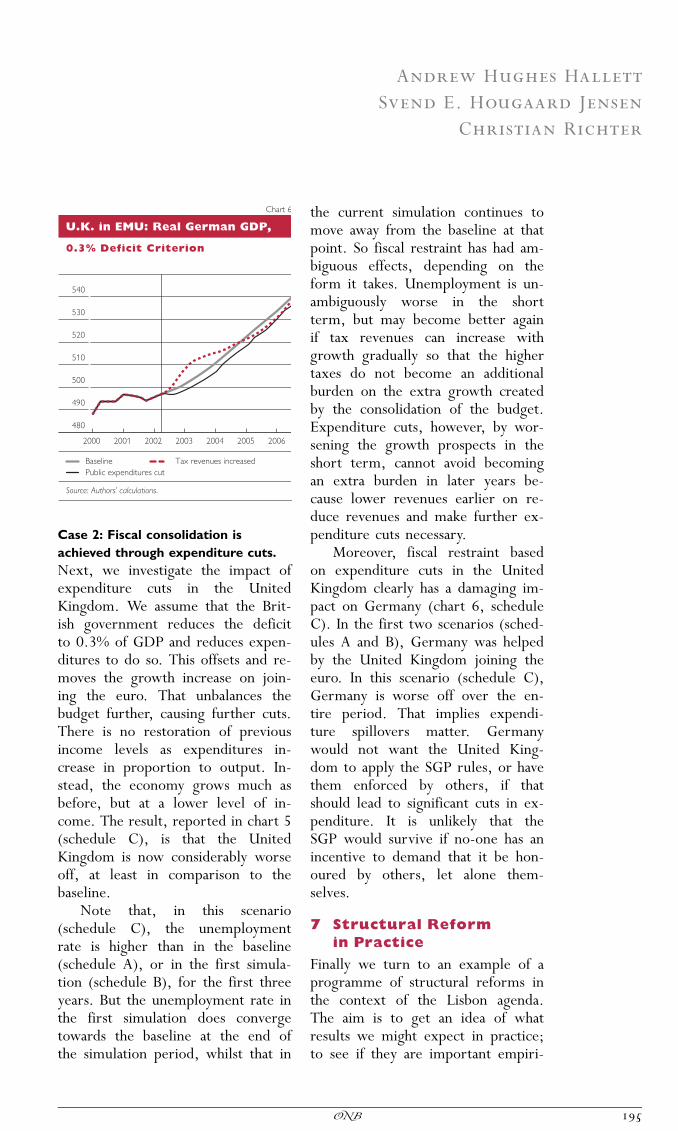

Case 2: Fiscal consolidation isachieved through expenditure cuts.Next, we investigate the impact ofexpenditure cuts in the UnitedKingdom. We assume that the Brit-ish government reduces the deficitto 0.3% of GDP and reduces expen-ditures to do so. This offsets and re-moves the growth increase on join-ing the euro. That unbalances thebudget further, causing further cuts.There is no restoration of previousincome levels as expenditures in-crease in proportion to output. In-stead, the economy grows much asbefore, but at a lower level of in-come. The result, reported in chart 5(schedule C), is that the UnitedKingdom is now considerably worseoff, at least in comparison to thebaseline.

Note that, in this scenario(schedule C), the unemploymentrate is higher than in the baseline(schedule A), or in the first simula-tion (schedule B), for the first threeyears. But the unemployment rate inthe first simulation does convergetowards the baseline at the end ofthe simulation period, whilst that in

the current simulation continues tomove away from the baseline at thatpoint. So fiscal restraint has had am-biguous effects, depending on theform it takes. Unemployment is un-ambiguously worse in the shortterm, but may become better againif tax revenues can increase withgrowth gradually so that the highertaxes do not become an additionalburden on the extra growth createdby the consolidation of the budget.Expenditure cuts, however, by wor-sening the growth prospects in theshort term, cannot avoid becomingan extra burden in later years be-cause lower revenues earlier on re-duce revenues and make further ex-penditure cuts necessary.

Moreover, fiscal restraint basedon expenditure cuts in the UnitedKingdom clearly has a damaging im-pact on Germany (chart 6, scheduleC). In the first two scenarios (sched-ules A and B), Germany was helpedby the United Kingdom joining theeuro. In this scenario (schedule C),Germany is worse off over the en-tire period. That implies expendi-ture spillovers matter. Germanywould not want the United King-dom to apply the SGP rules, or havethem enforced by others, if thatshould lead to significant cuts in ex-penditure. It is unlikely that theSGP would survive if no-one has anincentive to demand that it be hon-oured by others, let alone them-selves.

7 Structural Reformin Practice

Finally we turn to an example of aprogramme of structural reforms inthe context of the Lisbon agenda.The aim is to get an idea of whatresults we might expect in practice;to see if they are important empiri-

�?@?�����0�>����������������

?�=���'������������

��

�!

��

��

�

�#

��

������

����� � &�)��#,����������#$

� �� �� �! �� �� �

��.$+*%$ ��8��$3$%($.�*% �$�.$"�(�+* �$85$%"*�(�$.� (�

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

195�

vowi_tagung_2004 Seite 195 15.12.2004,08:32 schwarz rot

cally, and whether they are in linewith the analytic reasoning set outearlier. The example we have takenis the German government�s Agenda2010. The German economy is animportant candidate for reform, and�Agenda 2010� is a good example ofa portfolio of measures currently inthe process of being implemented.Indeed, Chancellor Schro‹der hadstaked his own career on thesemeasures being adopted by the endof 2003.

The measures themselves fallinto five broad categories:— Employment generation with

training- increasing the number of ap-

prenticeships, and liberalisingthe training laws;

- an apprentice preparationscheme;

- training schemes at the La‹nderor local level (human capital);

- subsidies for those in appren-ticeship schemes (Jump Plus).

— Investment creation through sub-sidies and infrastructure- subsidised loans for capital to

employ newly engaged em-ployees;

- subsidised loans for those whoprovide apprentice places.

— Direct demand measures of theKeynesian kind- loan subsidies to those who

employ new people in thebackward regions or from thepool of long-term unem-ployed;

�������>�����������'���������-A�2�����������3�����3��!=

��

�!

��

��

�

�#

�������

�����������

�

#

�

"��%��!&� !��������

�� �� �! �� �� � �� �� �� �! �� �� � ��

���

��

���

���

��

��

�

#���������������

����� � &�)��#,����������#$

�� �� �! �� �� � ��

��.$+*%$ �*&(+��*)%

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

196 �

vowi_tagung_2004 Seite 196 15.12.2004,08:32 schwarz rot

- wage subsidies for the newlyself employed.

— Tax cuts to increase labour supply- raising income tax thresholds,

lowering the basic rate;- subsidies to contributions to

private pension schemes;- reductions in pension (social

security) contributions paid byemployees.

— Labour costs and supply-sidemeasures- deregulation of the master

craftsman market;- discounts/tax breaks on social

security contributions;- suspension of some hiring/fir-

ing costs;

- reduction in compensation forredundancy, in unemploymentbenefits, and a requirementthat the unemployed acceptjob offers even if at a lowerwage.

These measures are all designed toaffect the supply or demand for la-bour directly, without affecting thecosts of employment or the flexibil-ity of markets to excess supply orexcess demand. The exception ofcourse is the last group of measures.We have therefore simulated a rep-resentative measure from each groupin the German component of theOEF model.13 Charts 7 to 10 displaythe results.

�������>�����������'���������-A�2�����������3�����3�� =

��

��

�

��

�������

����������� "��%��!&� !��������

�

�

�

�

0�

0�

�� �� �! �� ���� �� �! �� ��

��

��

�

#�

#

#���������������

����� � &�)��#,����������#$

��.$+*%$ �*&(+��*)%

�� �� �! �� ��

13 We have ignored the conventional direct demand measures (the third group) as being of little interest in thiscontext.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

197�

vowi_tagung_2004 Seite 197 15.12.2004,08:32 schwarz rot

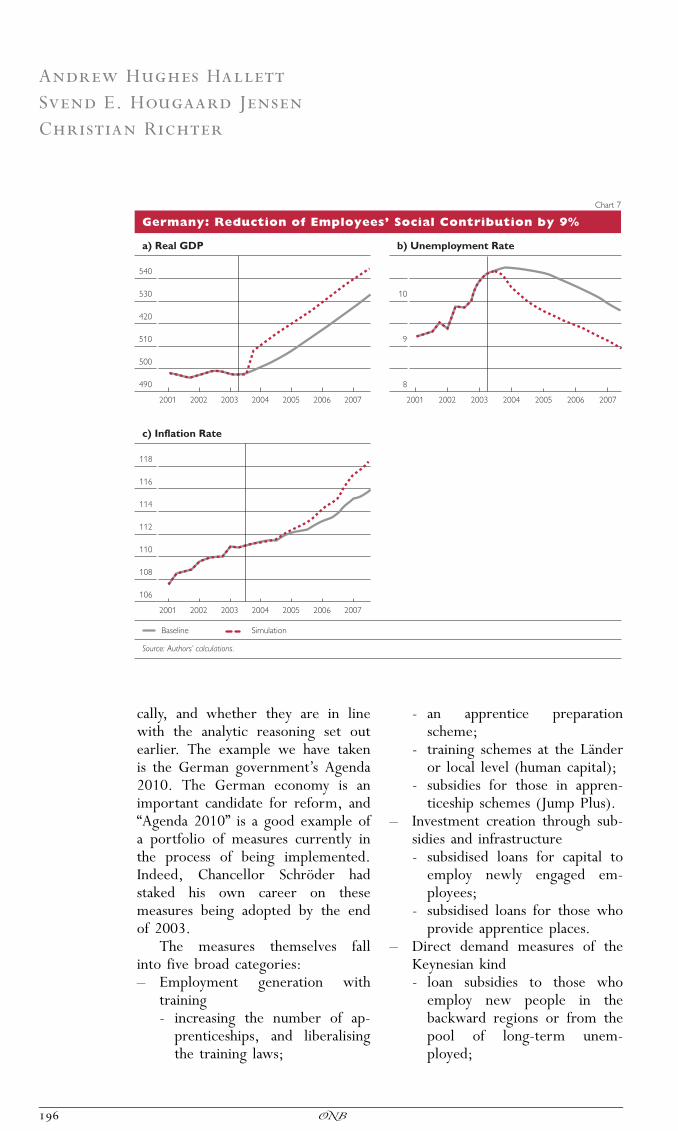

Chart 7 shows the income, em-ployment and inflation consequencesto be expected from a reduction inthe employees� social security contri-butions of 9%. The change is intro-duced in early 2003, and we reportfive years of results. It is clear thatsuch a change would lead to a smallimprovement in national income: up2.5% over five years, but no long-term increase in the growth rate.Unemployment drops from 10% to9%, and the inflation rate is slightlyhigher (0.5 percentage point) over afive-year period. These may be con-sidered welcome changes perhaps,but they are small.

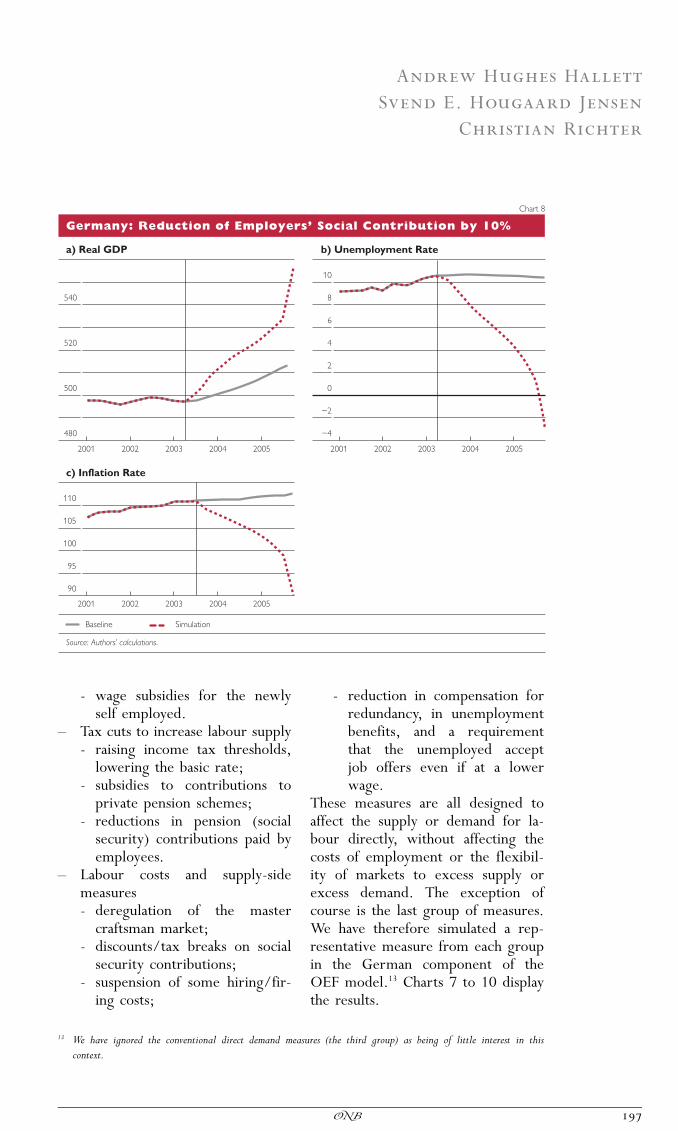

Chart 8 shows the effect of re-ducing the employers� social securitycontributions (non-wage costs) by10%. The simulated outcomes areclearly unsatisfactory after three years

because the change is too large forthe behaviour modelled to be a reli-able guide. But the first three yearsprovide an indication of the likelydirection of that change. Here GDPhas risen 7% within three years, un-employment has dropped markedly,and prices have fallen by about 6%each year. Significant changes there-fore, and in the right direction.

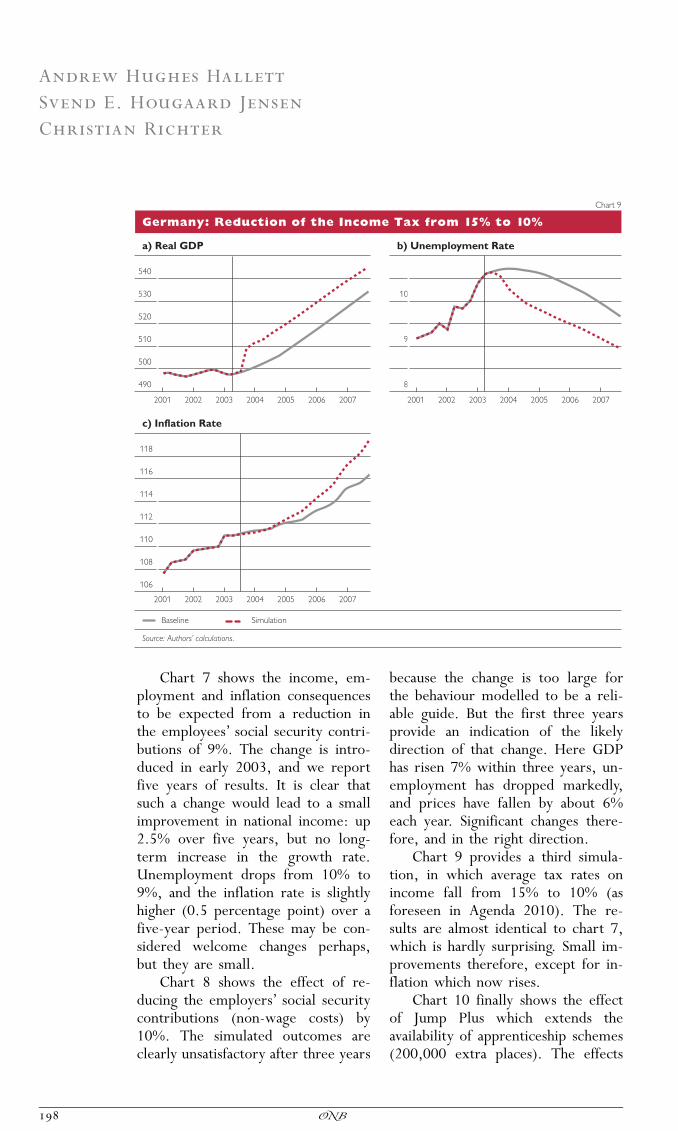

Chart 9 provides a third simula-tion, in which average tax rates onincome fall from 15% to 10% (asforeseen in Agenda 2010). The re-sults are almost identical to chart 7,which is hardly surprising. Small im-provements therefore, except for in-flation which now rises.

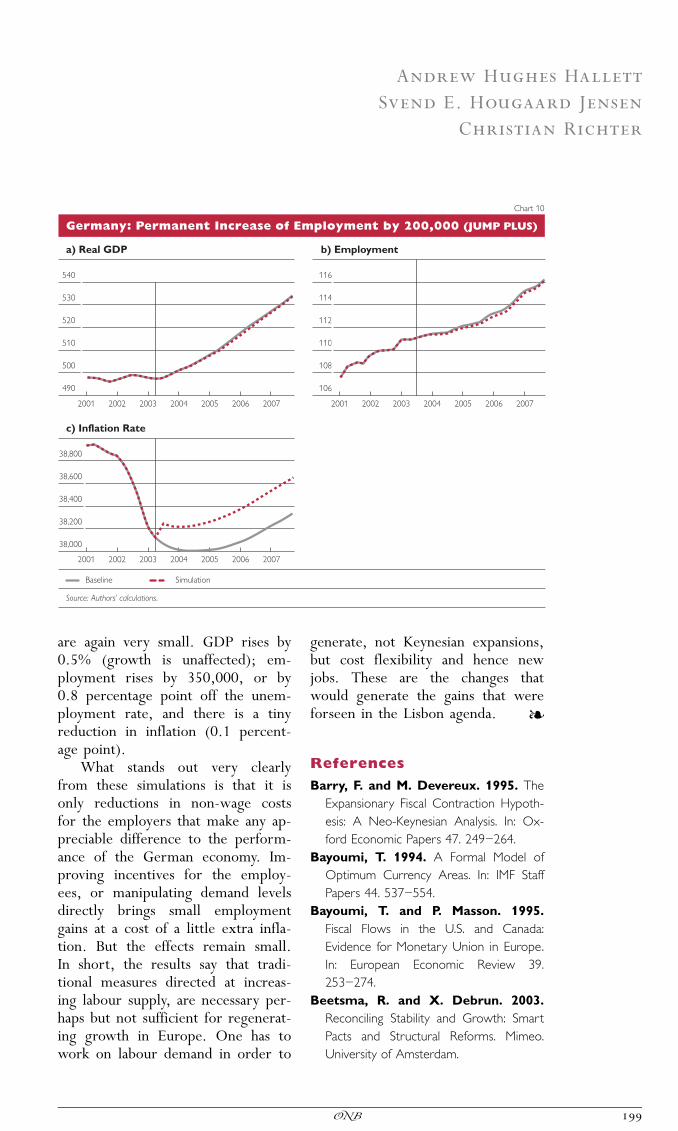

Chart 10 finally shows the effectof Jump Plus which extends theavailability of apprenticeship schemes(200,000 extra places). The effects

�������>�����������'����&������,�6�'���� "=��� =

��

�!

��

��

�

�#

������#

����������� "��%��!&� !��������

�

#

�

�� �� �! �� �� � �� �� �� �! �� �� � ��

���

��

���

���

��

��

�

#���������������

����� � &�)��#,����������#$

��.$+*%$ �*&(+��*)%

�� �� �! �� �� � ��

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

198 �

vowi_tagung_2004 Seite 198 15.12.2004,08:32 schwarz rot

are again very small. GDP rises by0.5% (growth is unaffected); em-ployment rises by 350,000, or by0.8 percentage point off the unem-ployment rate, and there is a tinyreduction in inflation (0.1 percent-age point).

What stands out very clearlyfrom these simulations is that it isonly reductions in non-wage costsfor the employers that make any ap-preciable difference to the perform-ance of the German economy. Im-proving incentives for the employ-ees, or manipulating demand levelsdirectly brings small employmentgains at a cost of a little extra infla-tion. But the effects remain small.In short, the results say that tradi-tional measures directed at increas-ing labour supply, are necessary per-haps but not sufficient for regenerat-ing growth in Europe. One has towork on labour demand in order to

generate, not Keynesian expansions,but cost flexibility and hence newjobs. These are the changes thatwould generate the gains that wereforseen in the Lisbon agenda. §

References

Barry, F. and M. Devereux. 1995. TheExpansionary Fiscal Contraction Hypoth-esis: A Neo-Keynesian Analysis. In: Ox-ford Economic Papers 47. 249—264.

Bayoumi, T. 1994. A Formal Model ofOptimum Currency Areas. In: IMF StaffPapers 44. 537—554.

Bayoumi, T. and P. Masson. 1995.Fiscal Flows in the U.S. and Canada:Evidence for Monetary Union in Europe.In: European Economic Review 39.253—274.

Beetsma, R. and X. Debrun. 2003.Reconciling Stability and Growth: SmartPacts and Structural Reforms. Mimeo.University of Amsterdam.

�������>����������&�����-���'�����������3��� �B;�0���)�2C

��

�!

��

��

�

�#

�������

����������� "��,!&� !���

��

���

���

��

��

�

�� �� �! �� �� � �� �� �� �! �� �� � ��

����� � &�)��#,����������#$

!�:�

!�:

!�:�

!�:�

!�:

#���������������

��.$+*%$ �*&(+��*)%

�� �� �! �� �� � ��

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

199�

vowi_tagung_2004 Seite 199 15.12.2004,08:32 schwarz rot

Begg, I. 1995. Factor Mobility and Re-gional Disparities in the European Union.In: Oxford Review of Economic Policy11. 96—112.

Bruno, M. 1986. Aggregate Supply andDemand Factors in OECD Unemploy-ment: An Update. Economica 53. 35—52.

Dellas, H. and G. Tavlas. 2003. WageRigidity and Monetary Union. In: TheEconomic Journal. Forthcoming.

Delors Committee. 1989. Report onEconomic and Monetary Union in theEuropean Community. Office of the Pub-lications of the European Communities.Luxembourg.

European Commission. 2002. PublicFinances in EMU — 2002. EuropeanEconomy, Reports and Studies 3/2002.European Commission. Brussels.

Frankel, J. A. and A. K. Rose. 1998.The Endogeneity of the Optimum Cur-rency Area Criterion. In: The EconomicJournal 108. 1009—1025.

HM Treasury. 2003. Modelling Shocksand Adjustment Mechanisms in EMU. In:U.K. Membership of the Single Currency:An Assessment of the Five EconomicTests. HMSO. London, U.K. Command5776.

Hughes Hallett, A. and S. E. H. Jen-sen. 2001. Currency Unions and the In-centive to Reform: Are Market Mecha-nisms Enough? In: North AmericanJournal of Economics and Finance 12.139—155.

Hughes Hallett, A. and S. E. H. Jen-sen. 2003. On the Role of Labour Mar-ket Reform for the Enlargement of aMonetary Union. In: CESifo EconomicStudies 49(3). 355—379.

Hughes Hallett, A. and S. E. H. Jen-sen. 2004. On the Enlargement of Cur-rency Unions: Incentives to Join and In-centives to Reform. In: Beetsma, R., C.Favero, A. Missale, V. A. Muscatelli, P. Na-tale and P. Tirelli (eds.). Monetary Policy,Fiscal Policies and Labour Markets: Mac-roeconomic Policymaking in the EMU.

Cambridge University Press. Cambridge.U.K.

Hughes Hallett, A. and L. Piscitelli.2002. Does Trade Cause Convergence?In: Economics Letters 75. 165—170.

Hughes Hallett, A. and N. Viegi.2003. Labour Market Reform and Mon-etary Policy in EMU: Do AsymmetriesMatter? In: Journal of Economic Integra-tion 18. 726—749.

Kaminski, B., Z. K. Wang and L. A.Winters. 1996. Export Performance inTransition Economies. In: Economic Policy23. 423—467.

Koedijk, K. and J. Kremers. 1996.Market Opening, Regulation and Growthin Europe. In: Economic Policy 23.445—467.

Obstfeld, M. and G. Peri. 1998. Re-gional Nonadjustment and Fiscal Policy.In: Begg, D. J. Von Hagen, C. Wyploszand K. Zimmerman (eds.). EMU: Pros-pects and Challenges for the Euro. BasilBlackwell. Oxford, U.K.

OEF. 2003. The New OEF WindowsWorld Model Software. Oxford, U.K.

Saint-Paul, G. 2004a. Did European La-bour Markets Become More Competitivein the 1990s? Evidence from EstimatedWorker Rents. Discussion Paper 4327.Centre for Economic Policy Research.London.

Saint-Paul, G. 2004b. Why Are Euro-pean Countries Diverging in their Unem-ployment Experiences? Discussion Paper4328. Centre for Economic and BusinessResearch. London.

Sibert, A. 1999. Monetary Integrationand Economic Reform. In: The EconomicJournal 109. 78—92.

Sibert, A. and A. Sutherland. 2000.Monetary Regimes and Labour MarketReform. In: Journal of International Eco-nomics 51. 421—435.

Taylor, J. 2000. Discretionary Fiscal Poli-cies. In: Journal of Economic Perspectives14. 1—23.

Andrew Hughes Hallett

Svend E. Hougaard Jensen

Christian Richter

200 �

vowi_tagung_2004 Seite 200 15.12.2004,08:32 schwarz rot

vowi_tagung_2004 Seite 201 15.12.2004,08:32 schwarz rot