![Learning human behaviors and lifestyle by capturing ...let allocation (LDA) model [3]. The LDA can infer the function (LDA \topic") of a region (LDA \document") in a city, e.g., educational](https://static.fdocuments.us/doc/165x107/5f660a21498c6c339720e9c1/learning-human-behaviors-and-lifestyle-by-capturing-let-allocation-lda-model.jpg)

AN OVERVIEW OF INDIA January 2007 Information contained in this document is prepared by The Boston...

27

AN OVERVIEW OF INDIA January 2007 Information contained in this document is prepared by The Boston Consulting Group, Lda

-

Upload

jewel-shipwash -

Category

Documents

-

view

213 -

download

1

Transcript of AN OVERVIEW OF INDIA January 2007 Information contained in this document is prepared by The Boston...

AN OVERVIEW OF INDIA

January 2007

Information contained in this document is prepared by The Boston Consulting Group, Lda

- 2 -- 2 -Copyright BCG

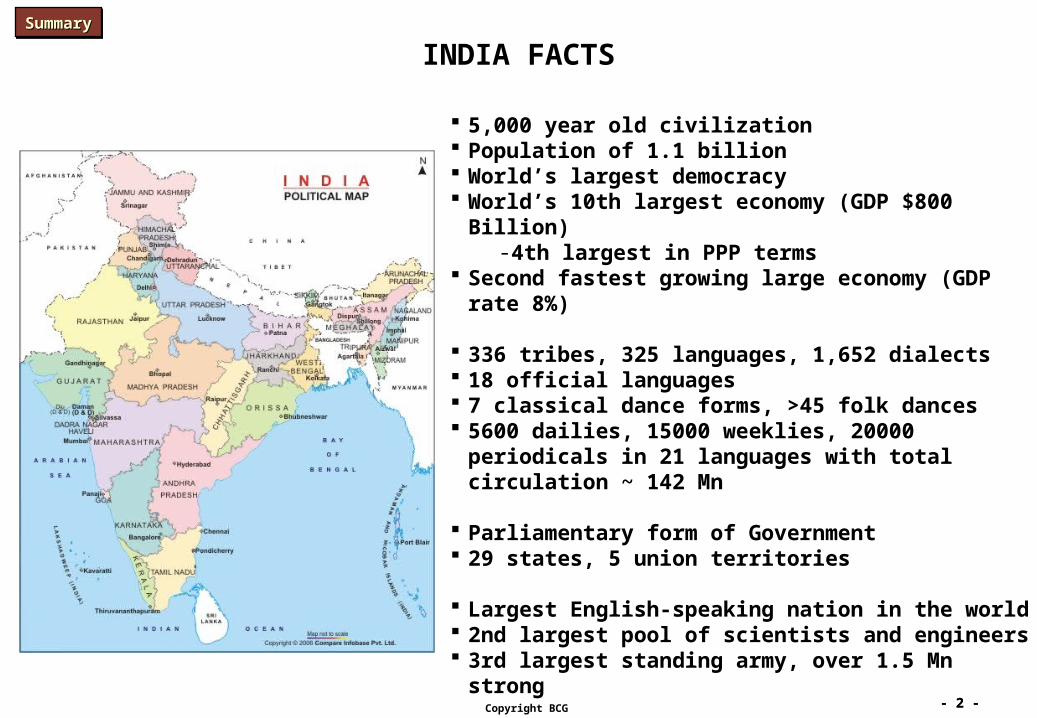

5,000 year old civilization Population of 1.1 billion World’s largest democracy World’s 10th largest economy (GDP $800 Billion)

-4th largest in PPP terms Second fastest growing large economy (GDP rate 8%)

336 tribes, 325 languages, 1,652 dialects 18 official languages 7 classical dance forms, >45 folk dances 5600 dailies, 15000 weeklies, 20000 periodicals in 21

languages with total circulation ~ 142 Mn

Parliamentary form of Government 29 states, 5 union territories

Largest English-speaking nation in the world 2nd largest pool of scientists and engineers 3rd largest standing army, over 1.5 Mn strong

INDIA FACTSSummarySummarySummarySummary

- 3 -- 3 -Copyright BCG

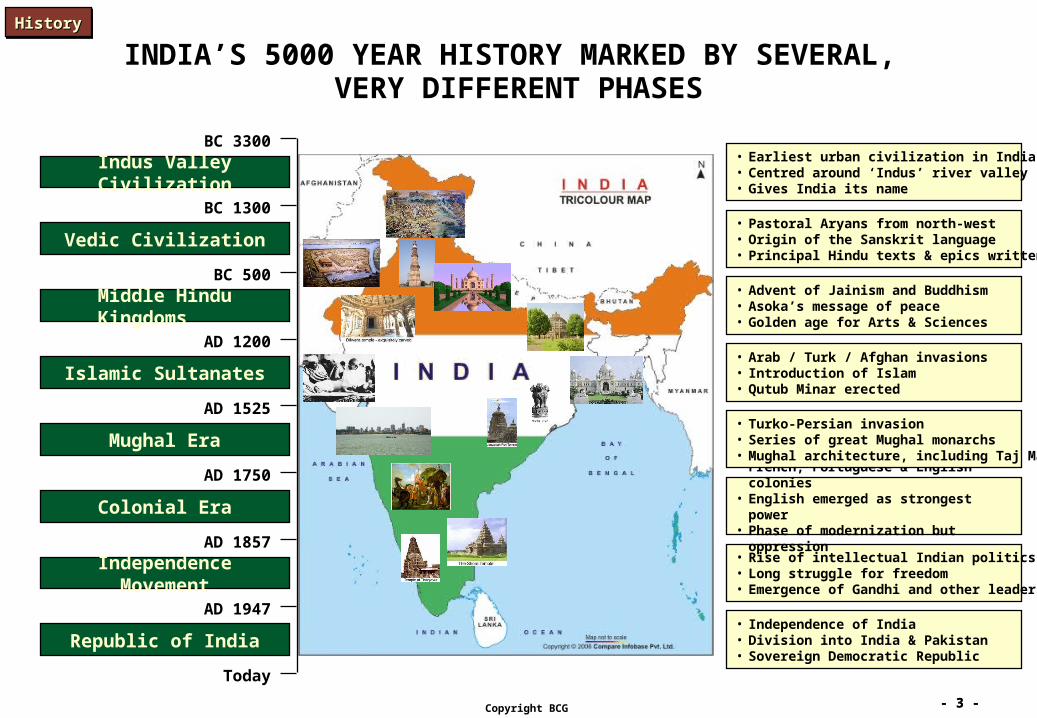

INDIA’S 5000 YEAR HISTORY MARKED BY SEVERAL, VERY DIFFERENT PHASES

Indus Valley Civilization

Vedic Civilization

Middle Hindu Kingdoms

Islamic Sultanates

Mughal Era

Colonial Era

Republic of India

Independence Movement

BC 3300

BC 1300

BC 500

AD 1200

AD 1525

AD 1750

AD 1857

AD 1947

Today

• Earliest urban civilization in India• Centred around ‘Indus’ river valley• Gives India its name

• Independence of India• Division into India & Pakistan• Sovereign Democratic Republic

• Rise of intellectual Indian politics• Long struggle for freedom• Emergence of Gandhi and other leaders

• French, Portuguese & English colonies• English emerged as strongest power• Phase of modernization but oppression

• Turko-Persian invasion• Series of great Mughal monarchs• Mughal architecture, including Taj Mahal

• Arab / Turk / Afghan invasions• Introduction of Islam• Qutub Minar erected

• Advent of Jainism and Buddhism• Asoka’s message of peace• Golden age for Arts & Sciences

• Pastoral Aryans from north-west• Origin of the Sanskrit language• Principal Hindu texts & epics written

HistoryHistoryHistoryHistory

- 4 -- 4 -Copyright BCG

ReligionsReligions

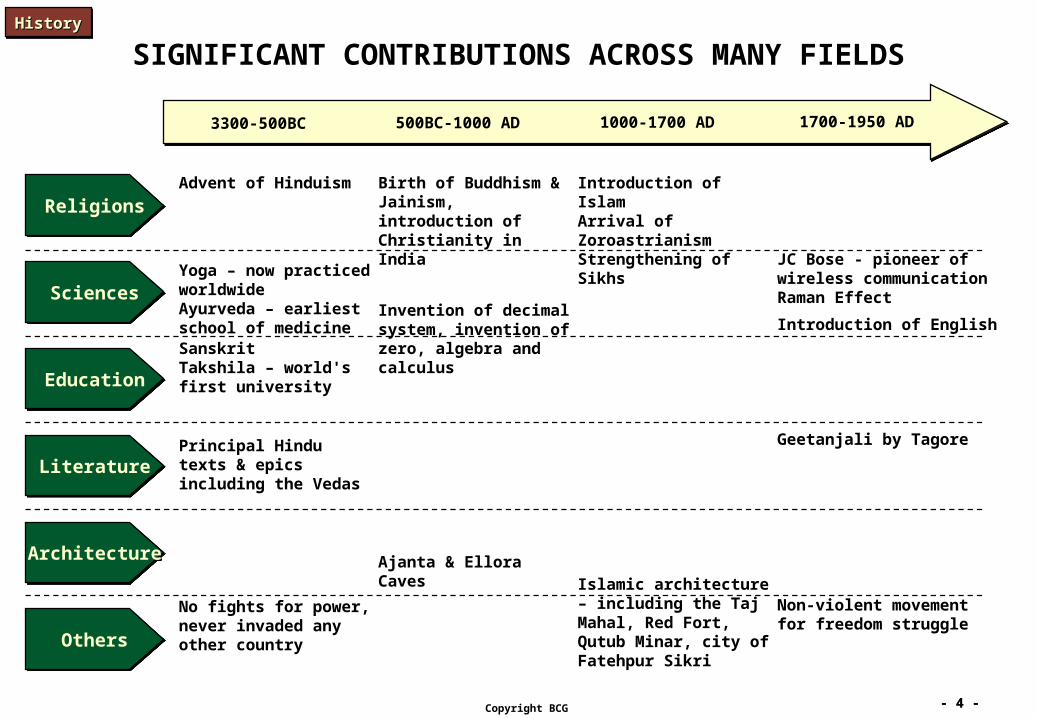

SIGNIFICANT CONTRIBUTIONS ACROSS MANY FIELDS

3300-500BC 500BC-1000 AD 1000-1700 AD 1700-1950 AD

Advent of Hinduism

Yoga – now practiced worldwideAyurveda – earliest school of medicineSanskritTakshila – world's first university

Principal Hindu texts & epics including the Vedas

No fights for power, never invaded any other country

Birth of Buddhism & Jainism, introduction of Christianity in India

Invention of decimal system, invention of zero, algebra and calculus

Ajanta & Ellora Caves

Introduction of IslamArrival of ZoroastrianismStrengthening of Sikhs

Islamic architecture – including the Taj Mahal, Red Fort, Qutub Minar, city of Fatehpur Sikri

SciencesSciences

EducationEducation

LiteratureLiterature

ArchitectureArchitecture

OthersOthers

JC Bose - pioneer of wireless communicationRaman Effect

Introduction of English

Geetanjali by Tagore

Non-violent movement for freedom struggle

HistoryHistoryHistoryHistory

- 5 -- 5 -Copyright BCG

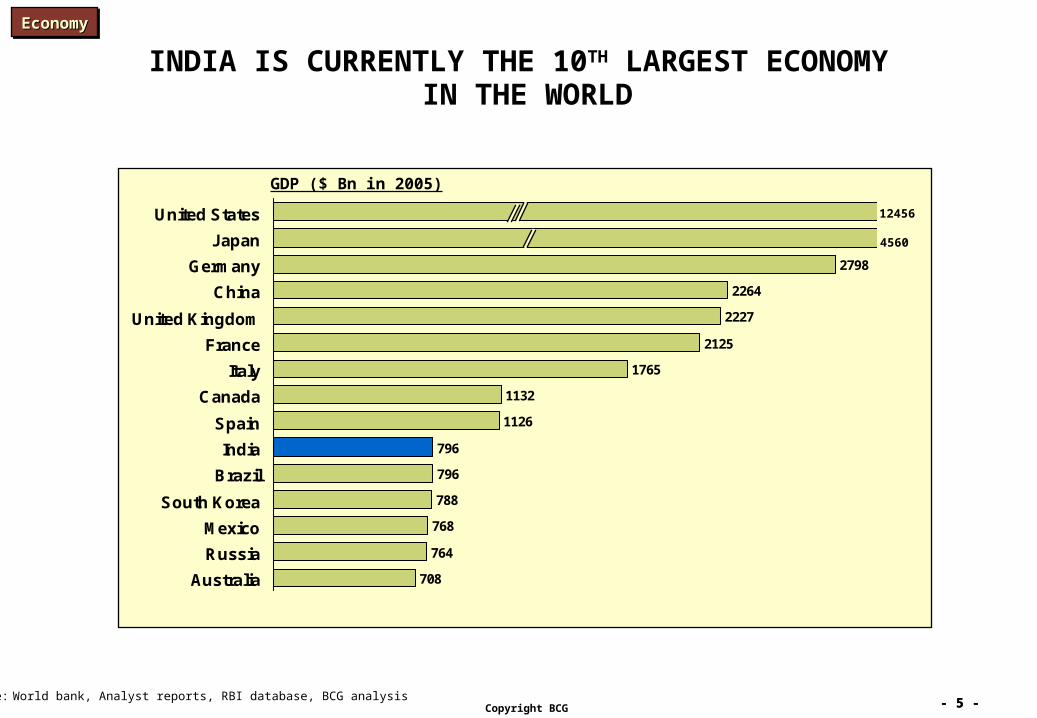

INDIA IS CURRENTLY THE 10TH LARGEST ECONOMY IN THE WORLD

708

764

768

788

796

796

1126

1132

1765

2125

2227

2264

2798

Australia

Russia

Mexico

South Korea

Brazil

India

Spain

Canada

Italy

France

United Kingdom

China

Germany

Japan

United States 12456

4560

Source: World bank, Analyst reports, RBI database, BCG analysis

GDP ($ Bn in 2005)

EconomyEconomyEconomyEconomy

- 6 -- 6 -Copyright BCG

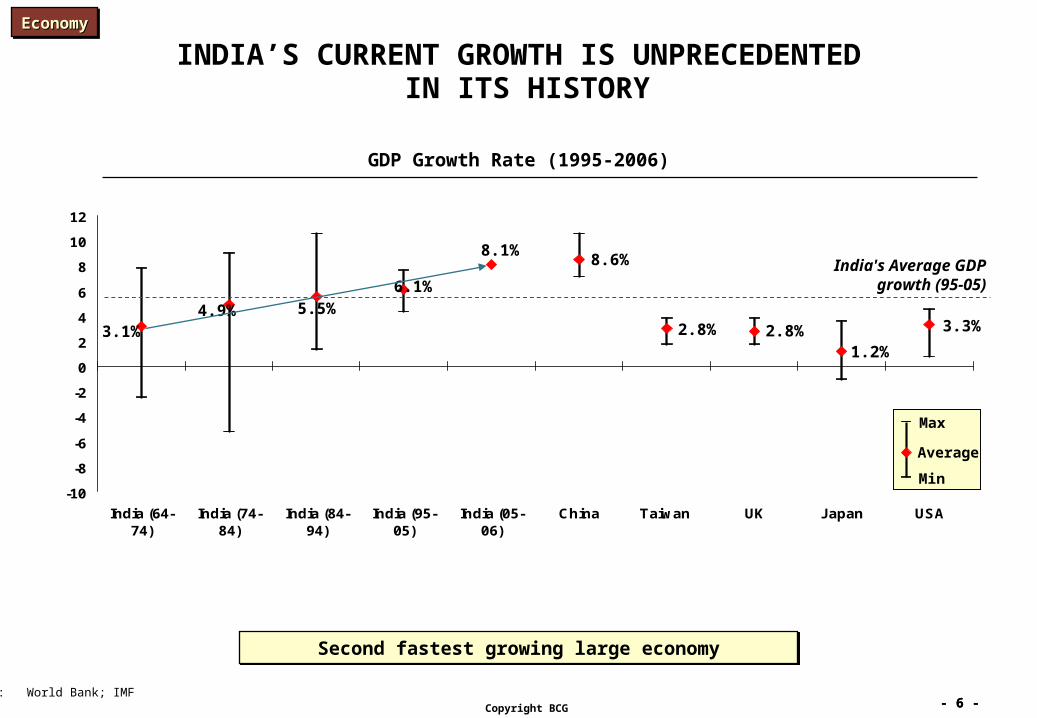

INDIA’S CURRENT GROWTH IS UNPRECEDENTED IN ITS HISTORY

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

India (64-74)

India (74-84)

India (84-94)

India (95-05)

India (05-06)

China Taiwan UK Japan USA

GDP Growth Rate (1995-2006)

India's Average GDP growth (95-05)

Max

Average

Min

4.9% 5.5%6.1%

8.6%

2.8% 2.8%1.2%

3.3%

Source: World Bank; IMF

Second fastest growing large economySecond fastest growing large economy

3.1%

8.1%

EconomyEconomyEconomyEconomy

- 7 -- 7 -Copyright BCG

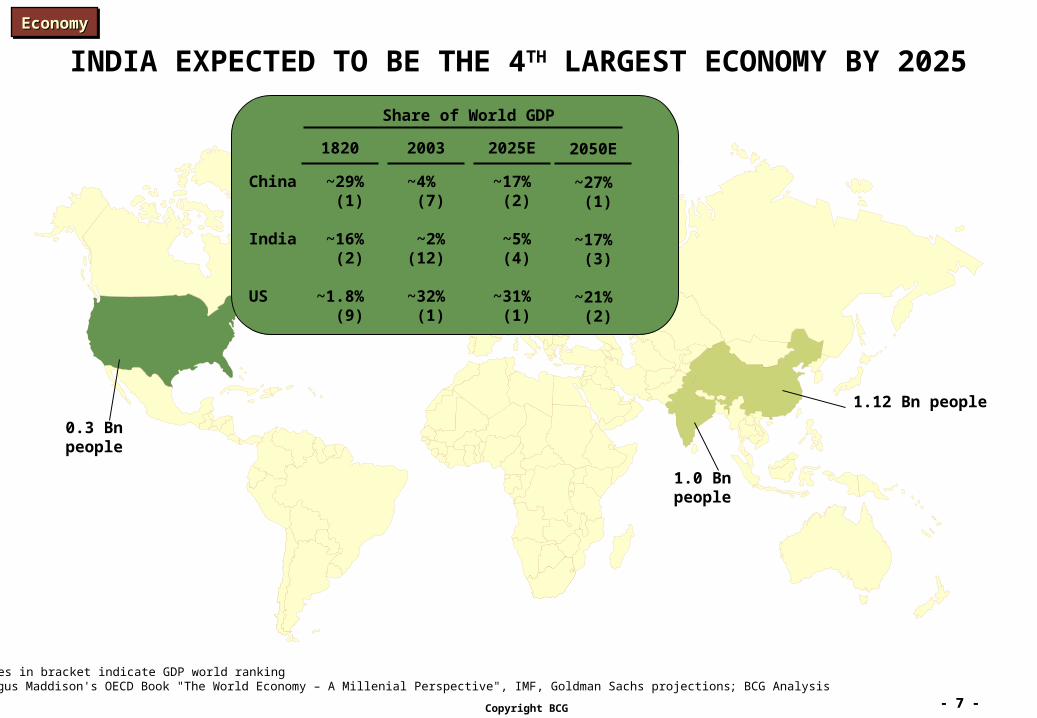

INDIA EXPECTED TO BE THE 4TH LARGEST ECONOMY BY 2025

Note: Figures in bracket indicate GDP world rankingSource: Angus Maddison's OECD Book "The World Economy – A Millenial Perspective", IMF, Goldman Sachs projections; BCG Analysis

1.12 Bn people

1.0 Bn people

China

India

US

~29%(1)

~16%(2)

~1.8%(9)

~4% (7)

~2% (12)

~32%(1)

~17%(2)

~5%(4)

~31%(1)

Share of World GDP

~27%(1)

~17%(3)

~21%(2)

1820 2003 2025E 2050E

0.3 Bn people

EconomyEconomyEconomyEconomy

- 8 -- 8 -Copyright BCG

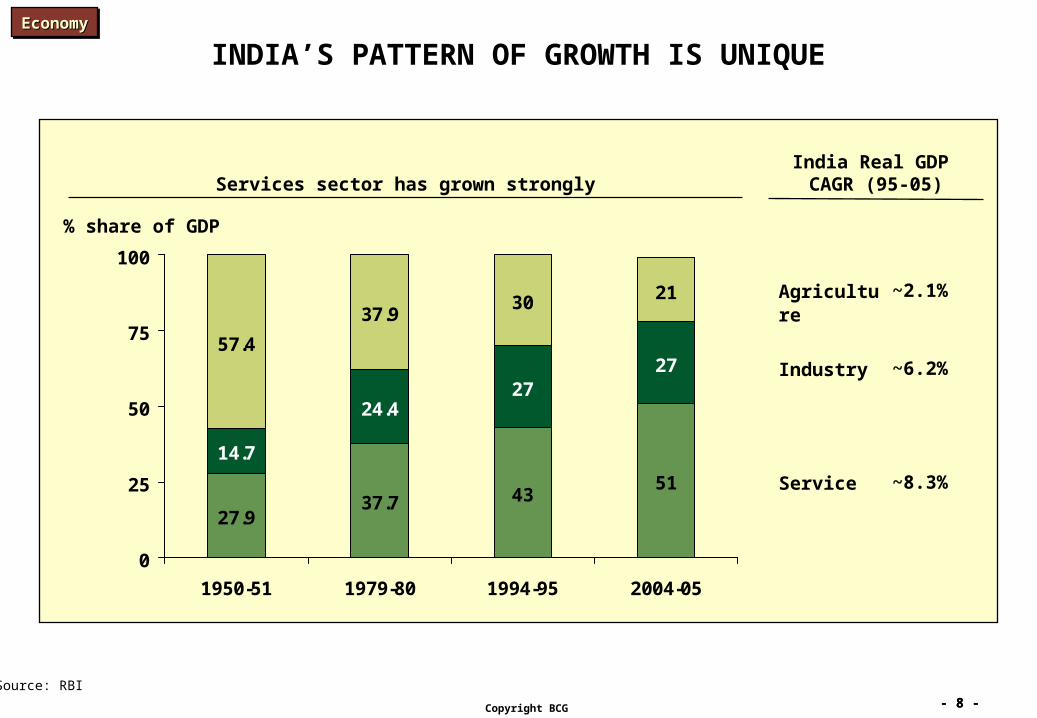

INDIA’S PATTERN OF GROWTH IS UNIQUE

India Real GDP CAGR (95-05)

~8.3%

~6.2%

~2.1%

Industry

Service

Agriculture

Services sector has grown strongly

Source: RBI

% share of GDP

27.937.7 43

51

14.7

24.427

2757.4

37.930 21

0

25

50

75

100

1950-51 1979-80 1994-95 2004-05

EconomyEconomyEconomyEconomy

- 9 -- 9 -Copyright BCG

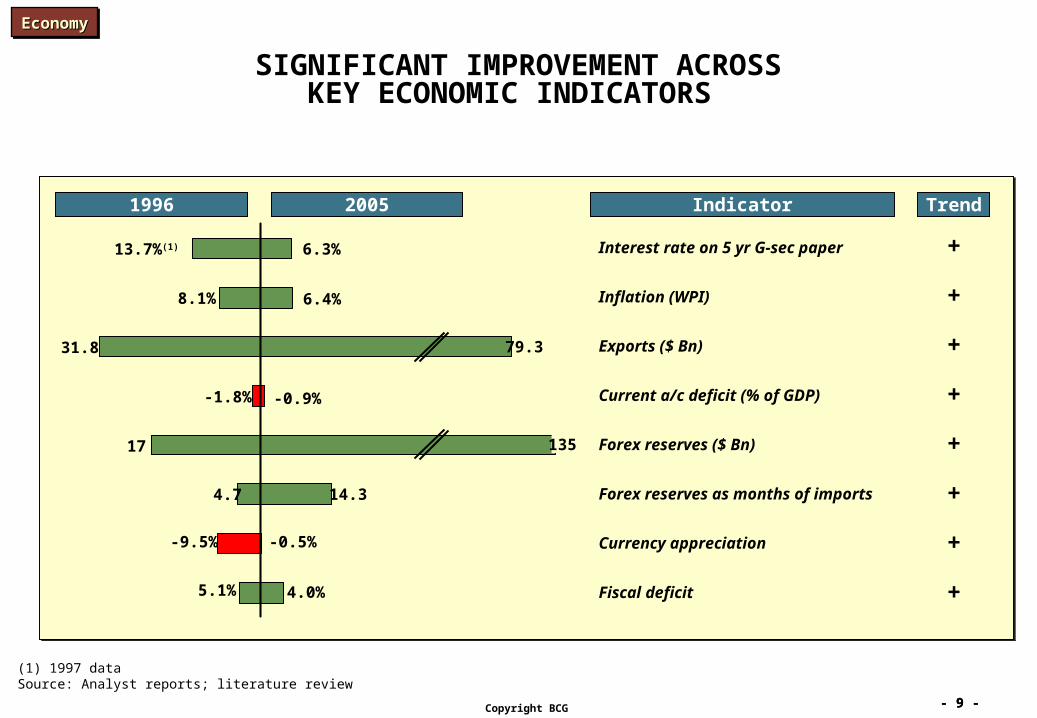

SIGNIFICANT IMPROVEMENT ACROSSKEY ECONOMIC INDICATORS

Interest rate on 5 yr G-sec paper

Inflation (WPI)

Exports ($ Bn)

Forex reserves ($ Bn)

Forex reserves as months of imports

Currency appreciation

Current a/c deficit (% of GDP)

Fiscal deficit

(1) 1997 dataSource: Analyst reports; literature review

Indicator

+

+

+

+

+

+

+

+

Trend

13.7%(1) 6.3%

8.1% 6.4%

31.8 79.3

17

4.7

-9.5%

14.3

-1.8% -0.9%

5.1% 4.0%

1996 2005

135

-0.5%

EconomyEconomyEconomyEconomy

- 10 -- 10 -Copyright BCG

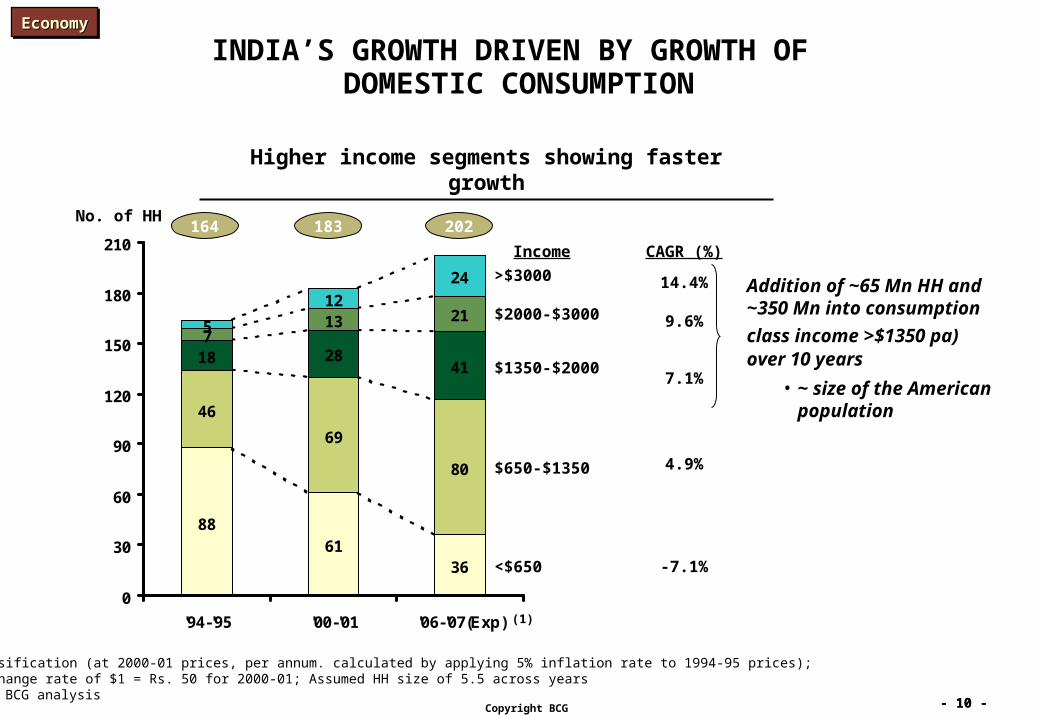

INDIA’S GROWTH DRIVEN BY GROWTH OF DOMESTIC CONSUMPTION

8861

36

46

69

80

18 2841

713 21

5

12

24

0

30

60

90

120

150

180

210

'94-'95 '00-'01 '06-'07(Exp)

Higher income segments showing faster growth

<$650

$650-$1350

$1350-$2000

$2000-$3000

>$3000

Expected figures Note: Income classification (at 2000-01 prices, per annum. calculated by applying 5% inflation rate to 1994-95 prices);

Assumed exchange rate of $1 = Rs. 50 for 2000-01; Assumed HH size of 5.5 across yearsSource: NCAER, SOI; BCG analysis

(1)

-7.1%

4.9%

7.1%

9.6%

14.4%

CAGR (%)

164 183 202No. of HH

Income

Addition of ~65 Mn HH and ~350 Mn into consumption

class income >$1350 pa) over 10 years

• ~ size of the American population

EconomyEconomyEconomyEconomy

- 11 -- 11 -Copyright BCG

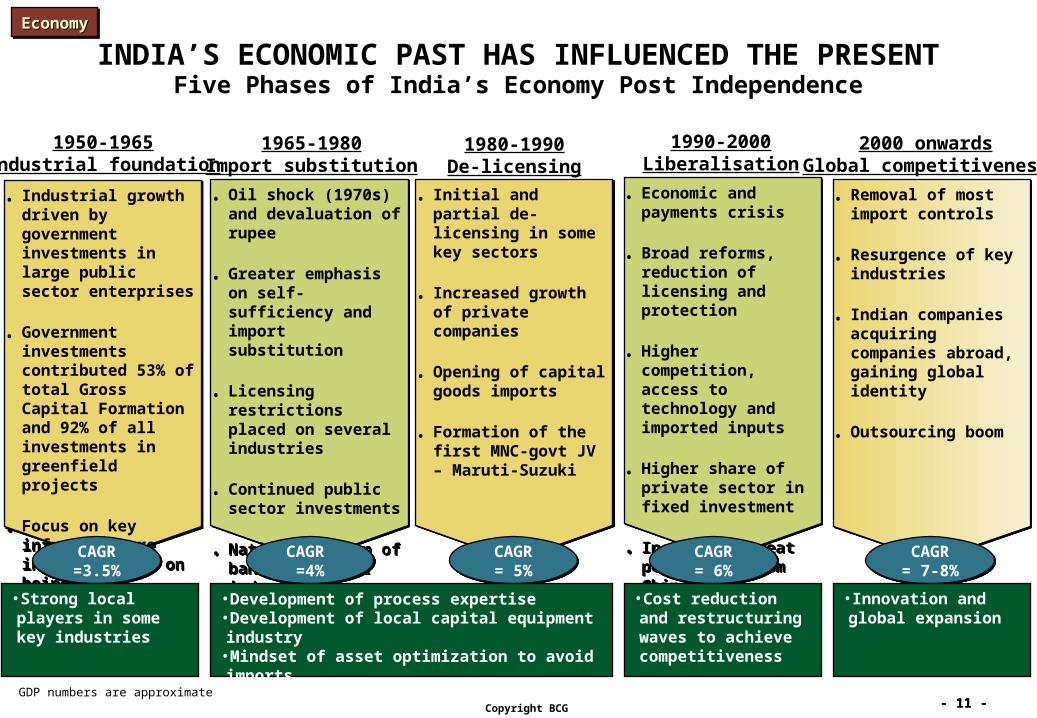

INDIA’S ECONOMIC PAST HAS INFLUENCED THE PRESENTFive Phases of India’s Economy Post Independence

• Initial and partial de-licensing in some key sectors

• Increased growth of private companies

• Opening of capital goods imports

• Formation of the first MNC-govt JV – Maruti-Suzuki

• Initial and partial de-licensing in some key sectors

• Increased growth of private companies

• Opening of capital goods imports

• Formation of the first MNC-govt JV – Maruti-Suzuki

1980-1990De-licensing

CAGR= 5%

CAGR= 5%

• Oil shock (1970s) and devaluation of rupee

• Greater emphasis on self-sufficiency and import substitution

• Licensing restrictions placed on several industries

• Continued public sector investments

• Nationalization of banks and other industries

• Oil shock (1970s) and devaluation of rupee

• Greater emphasis on self-sufficiency and import substitution

• Licensing restrictions placed on several industries

• Continued public sector investments

• Nationalization of banks and other industries

1965-1980Import substitution

CAGR =4%

CAGR =4%

• Industrial growth driven by government investments in large public sector enterprises

• Government investments contributed 53% of total Gross Capital Formation and 92% of all investments in greenfield projects

• Focus on key infrastructure industries and on being self-sufficient

• Industrial growth driven by government investments in large public sector enterprises

• Government investments contributed 53% of total Gross Capital Formation and 92% of all investments in greenfield projects

• Focus on key infrastructure industries and on being self-sufficient

1950-1965Industrial foundation

CAGR=3.5%CAGR=3.5%

•Strong local players in some key industries

•Development of process expertise•Development of local capital equipment industry•Mindset of asset optimization to avoid imports•Focus on flexibility rather than scale

• Economic and payments crisis

• Broad reforms, reduction of licensing and protection

• Higher competition, access to technology and imported inputs

• Higher share of private sector in fixed investment

• Increased threat perception from China

• Economic and payments crisis

• Broad reforms, reduction of licensing and protection

• Higher competition, access to technology and imported inputs

• Higher share of private sector in fixed investment

• Increased threat perception from China

1990-2000Liberalisation

CAGR= 6%

CAGR= 6%

•Cost reduction and restructuring waves to achieve competitiveness

• Removal of most import controls

• Resurgence of key industries

• Indian companies acquiring companies abroad, gaining global identity

• Outsourcing boom

• Removal of most import controls

• Resurgence of key industries

• Indian companies acquiring companies abroad, gaining global identity

• Outsourcing boom

2000 onwardsGlobal competitiveness

CAGR= 7-8%CAGR= 7-8%

•Innovation and global expansion

Note: GDP numbers are approximate

EconomyEconomyEconomyEconomy

- 12 -- 12 -Copyright BCG

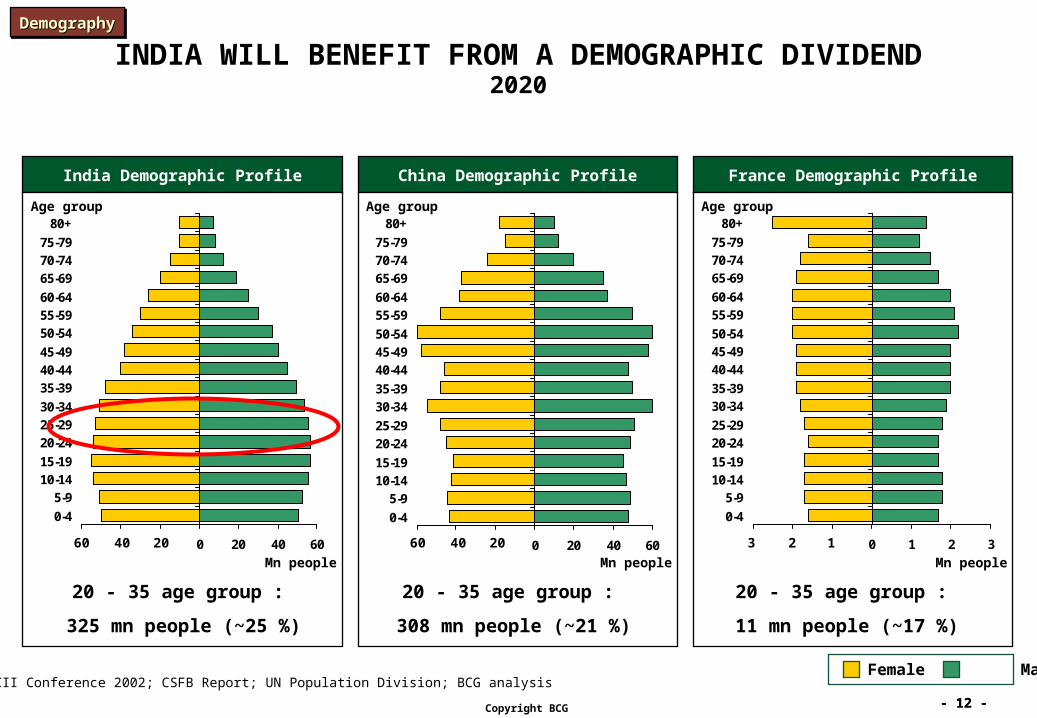

INDIA WILL BENEFIT FROM A DEMOGRAPHIC DIVIDEND2020

India Demographic Profile China Demographic Profile France Demographic Profile

-60 -40 -20 0 20 40 60

0-4

5-910-1415-19

20-2425-2930-34

35-3940-4445-49

50-5455-5960-64

65-6970-7475-79

80+

Mn people

Age group

Female Male

-60 -40 -20 0 20 40 60

0-4

5-910-1415-19

20-2425-29

30-3435-39

40-4445-4950-54

55-5960-64

65-6970-7475-79

80+

Mn people

Age group

-3 -2 -1 0 1 2 3

0-4

5-910-1415-19

20-2425-29

30-3435-39

40-4445-4950-54

55-5960-64

65-6970-7475-79

80+

Mn people

Age group

204060204060 123

Source: CII Conference 2002; CSFB Report; UN Population Division; BCG analysis

20 - 35 age group :

325 mn people (~25 %)

20 - 35 age group :

308 mn people (~21 %)

20 - 35 age group :

11 mn people (~17 %)

DemographyDemographyDemographyDemography

- 13 -- 13 -Copyright BCG

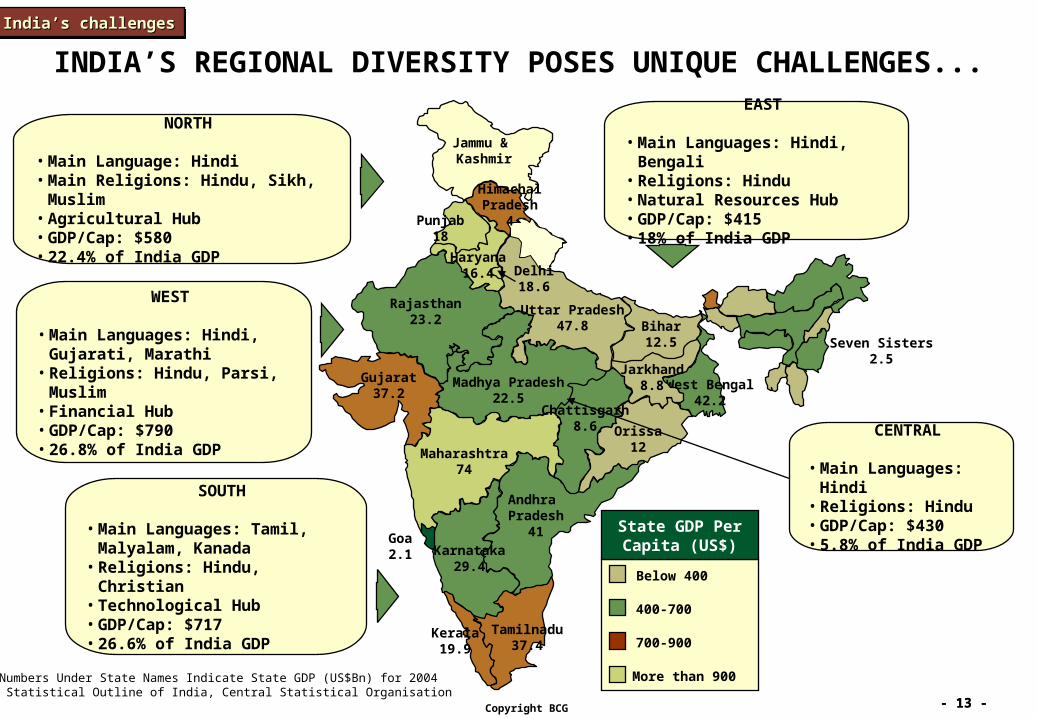

INDIA’S REGIONAL DIVERSITY POSES UNIQUE CHALLENGES...

Below 400

400-700

700-900

More than 900

State GDP Per Capita (US$)

NORTH

• Main Language: Hindi• Main Religions: Hindu, Sikh, Muslim• Agricultural Hub• GDP/Cap: $580• 22.4% of India GDP

EAST

• Main Languages: Hindi, Bengali• Religions: Hindu• Natural Resources Hub• GDP/Cap: $415• 18% of India GDP

WEST

• Main Languages: Hindi, Gujarati, Marathi

• Religions: Hindu, Parsi, Muslim• Financial Hub• GDP/Cap: $790• 26.8% of India GDP

SOUTH

• Main Languages: Tamil, Malyalam, Kanada

• Religions: Hindu, Christian• Technological Hub• GDP/Cap: $717• 26.6% of India GDP

Andhra Pradesh

41

Karnataka29.4

Gujarat37.2

Madhya Pradesh22.5

Chattisgarh8.6

Maharashtra74

Orissa12

Rajasthan23.2

West Bengal42.2

Delhi18.6

Seven Sisters2.5

Goa2.1

Punjab18

Haryana16.4

Note: Numbers Under State Names Indicate State GDP (US$Bn) for 2004Source: Statistical Outline of India, Central Statistical Organisation

Uttar Pradesh47.8

Kerala19.9

Tamilnadu37.4

Jarkhand8.8

Bihar12.5

CENTRAL

• Main Languages: Hindi• Religions: Hindu• GDP/Cap: $430• 5.8% of India GDP

HimachalPradesh

4

Jammu & Kashmir

India’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 14 -- 14 -Copyright BCG

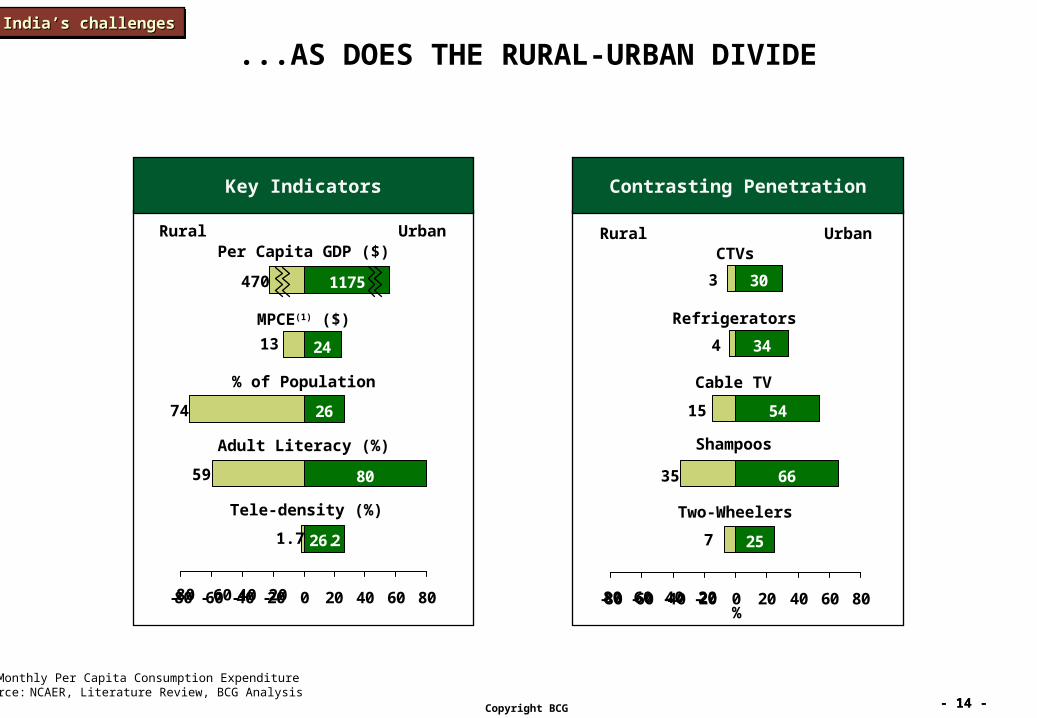

...AS DOES THE RURAL-URBAN DIVIDE

Key Indicators Contrasting Penetration

30

34

54

66

25

-80 -60 -40 -20 0 20 40 60 80%

80 60 40 20

Rural UrbanCTVs

Refrigerators

Shampoos

Cable TV

Two-Wheelers

24

26

80

26.2

1175

-80 -60 -40 -20 0 20 40 60 80 80 60 40 20

Rural UrbanPer Capita GDP ($)

MPCE(1) ($)

% of Population

Adult Literacy (%)

Tele-density (%)

1.7

59

74

13

470

7

35

15

4

3

(1) Monthly Per Capita Consumption ExpenditureSource: NCAER, Literature Review, BCG Analysis

BackupIndia’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 15 -- 15 -Copyright BCG

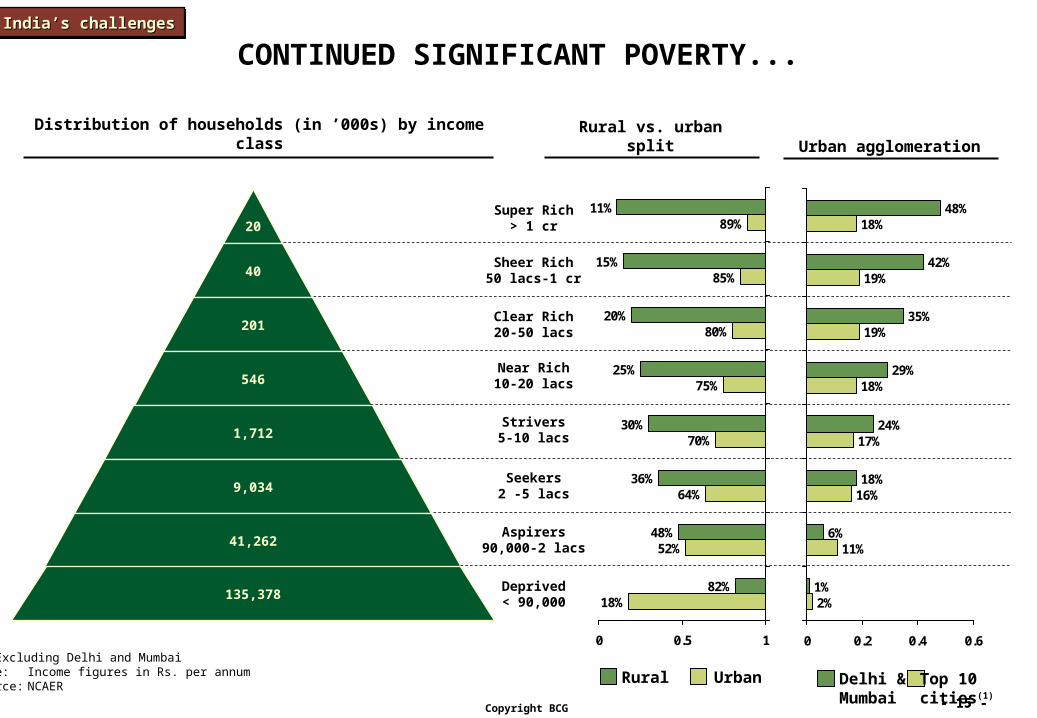

CONTINUED SIGNIFICANT POVERTY...

Distribution of households (in ’000s) by income class Rural vs. urban split

18%

52%

64%

70%

75%

80%

85%

89%

82%

48%

36%

30%

25%

20%

15%

11%

0 0.5 1

20

40

201

546

1,712

9,034

41,262

135,378Deprived< 90,000

Aspirers90,000-2 lacs

Seekers2 -5 lacs

Strivers5-10 lacs

Near Rich10-20 lacs

Clear Rich20-50 lacs

Sheer Rich50 lacs-1 cr

Super Rich> 1 cr

UrbanRural

2%

11%

16%

17%

18%

19%

19%

18%

1%

6%

18%

24%

29%

35%

42%

48%

0 0.2 0.4 0.6

Top 10cities(1)

Delhi &Mumbai

Urban agglomeration

(1) Excluding Delhi and MumbaiNote: Income figures in Rs. per annumSource: NCAER

India’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 16 -- 16 -Copyright BCG

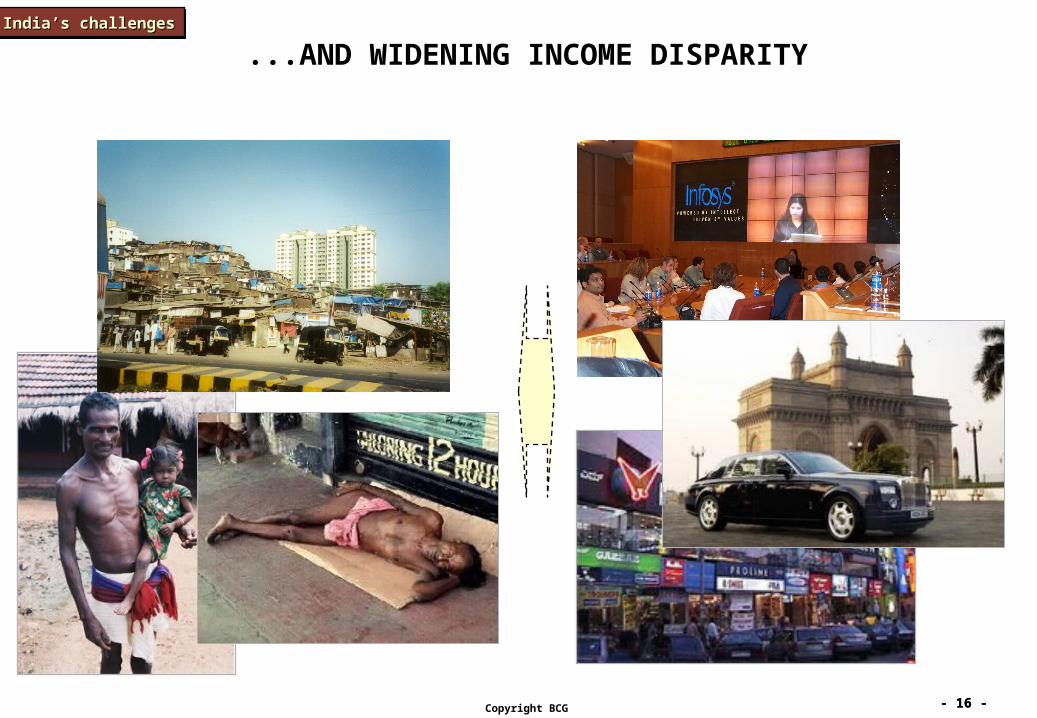

...AND WIDENING INCOME DISPARITYIndia’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 17 -- 17 -Copyright BCG

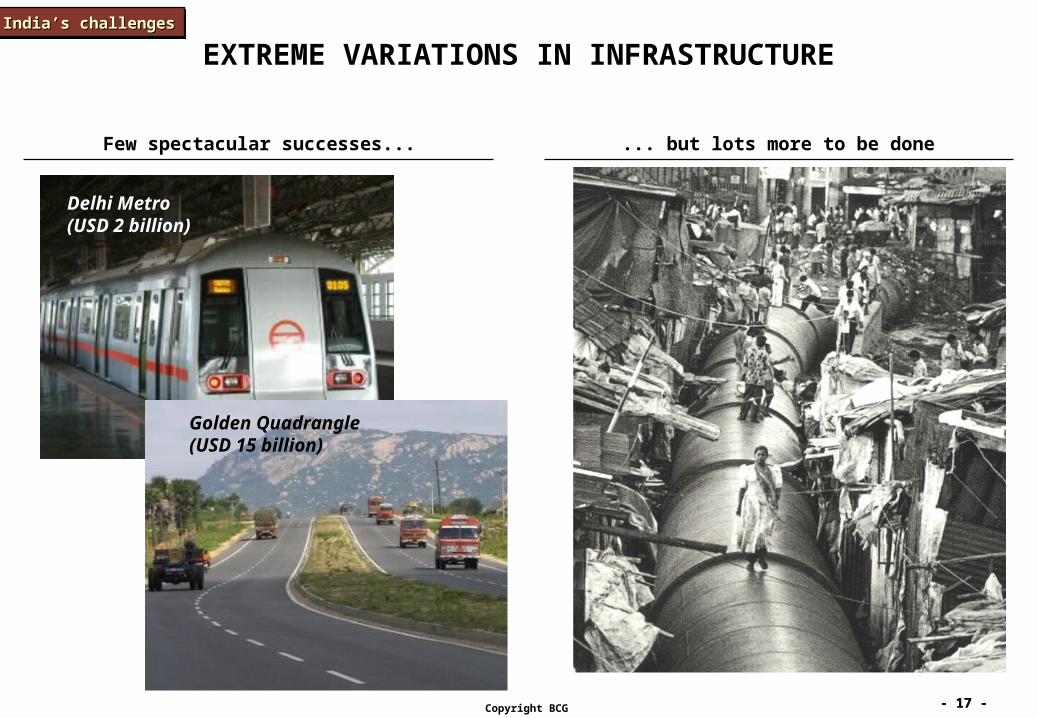

EXTREME VARIATIONS IN INFRASTRUCTURE

Few spectacular successes... ... but lots more to be done

Delhi Metro(USD 2 billion)

Golden Quadrangle(USD 15 billion)

India’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 18 -- 18 -Copyright BCG

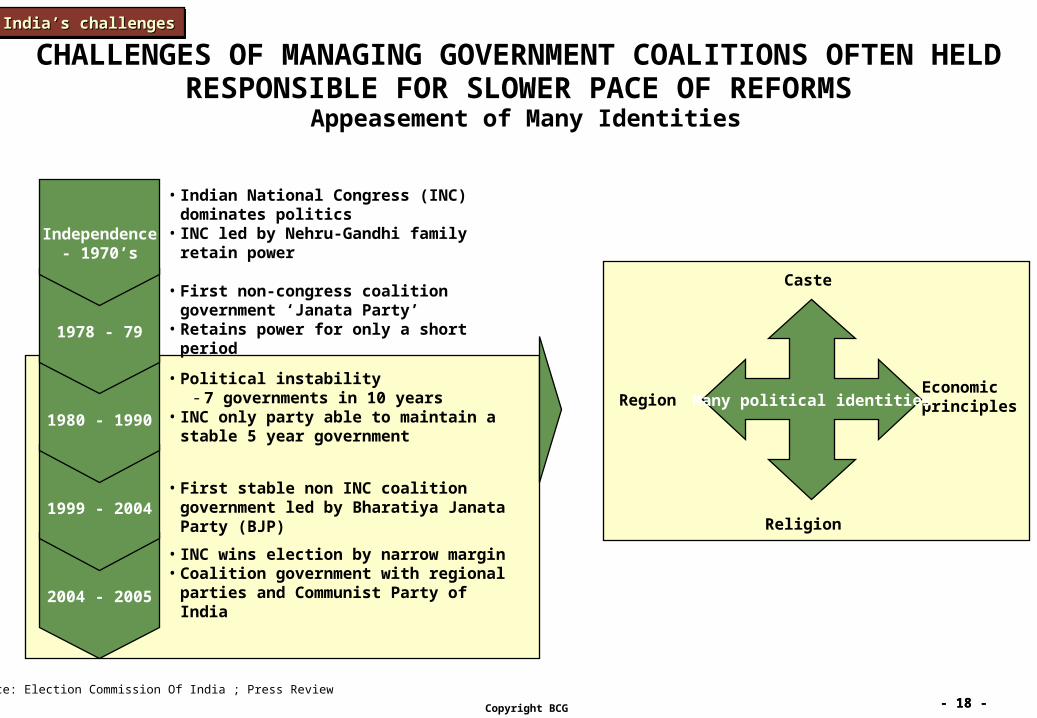

CHALLENGES OF MANAGING GOVERNMENT COALITIONS OFTEN HELD RESPONSIBLE FOR SLOWER PACE OF REFORMS

Appeasement of Many Identities

2004 - 2005

1999 - 2004

1980 - 1990

1978 - 79

Independence- 1970’s

• Indian National Congress (INC) dominates politics

• INC led by Nehru-Gandhi family retain power

• First non-congress coalition government ‘Janata Party’

• Retains power for only a short period

• Political instability- 7 governments in 10 years

• INC only party able to maintain a stable 5 year government

• First stable non INC coalition government led by Bharatiya Janata Party (BJP)

• INC wins election by narrow margin• Coalition government with regional parties

and Communist Party of India

Source: Election Commission Of India ; Press Review

Caste

Region

Religion

EconomicprinciplesMany political identities

India’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 19 -- 19 -Copyright BCG

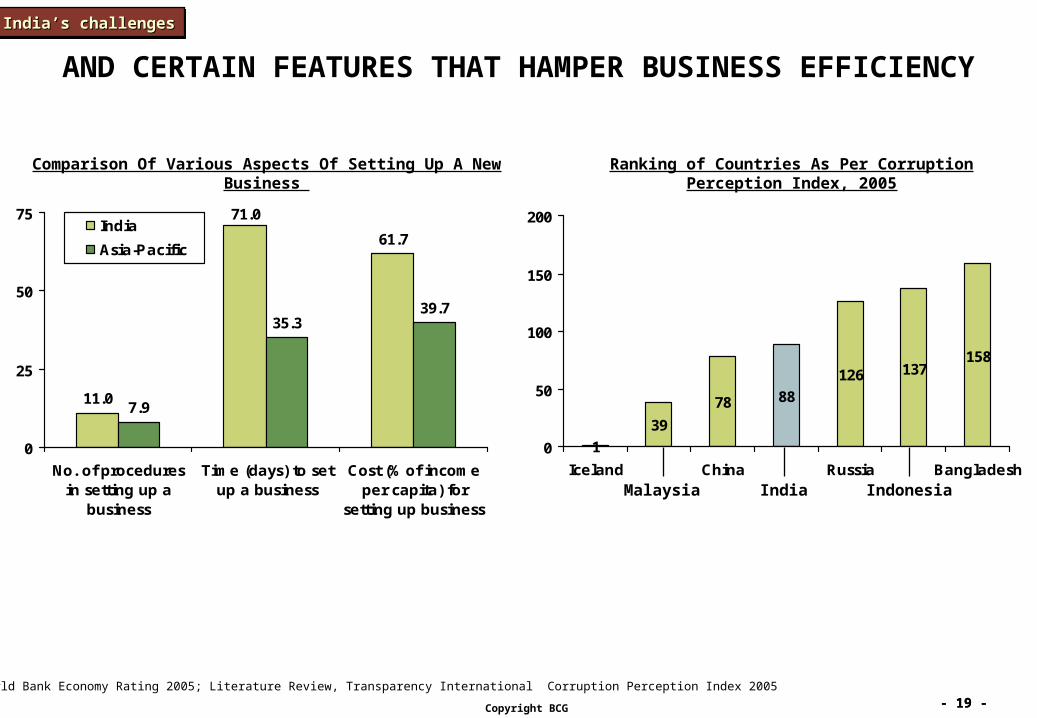

AND CERTAIN FEATURES THAT HAMPER BUSINESS EFFICIENCY

Comparison Of Various Aspects Of Setting Up A New Business

11.0

71.0

61.7

7.9

35.339.7

0

25

50

75

No. of proceduresin setting up a

business

Time (days) to setup a business

Cost (% of incomeper capita) for

setting up business

India

Asia-Pacific

Source: World Bank Economy Rating 2005; Literature Review, Transparency International Corruption Perception Index 2005

1

39

78

126 137158

88

0

50

100

150

200

Iceland China Russia Bangladesh

Ranking of Countries As Per Corruption Perception Index, 2005

Malaysia India Indonesia

India’s challengesIndia’s challengesIndia’s challengesIndia’s challenges

- 20 -- 20 -Copyright BCG

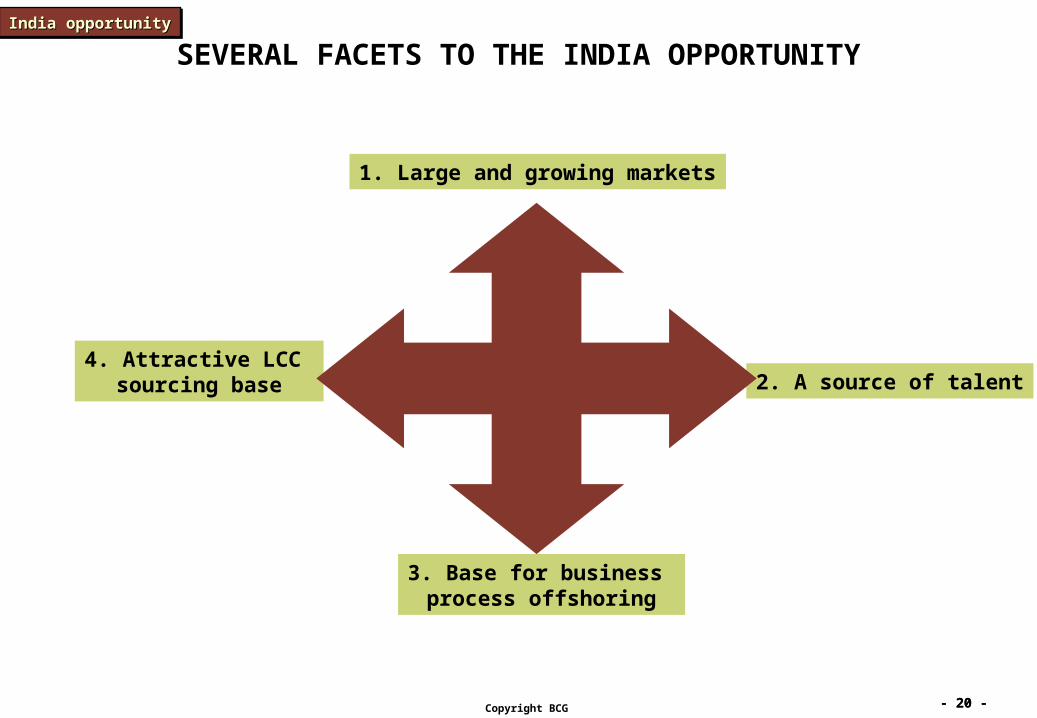

SEVERAL FACETS TO THE INDIA OPPORTUNITY

1. Large and growing markets

2. A source of talent

3. Base for business process offshoring

4. Attractive LCC sourcing base

India opportunityIndia opportunityIndia opportunityIndia opportunity

- 21 -- 21 -Copyright BCG

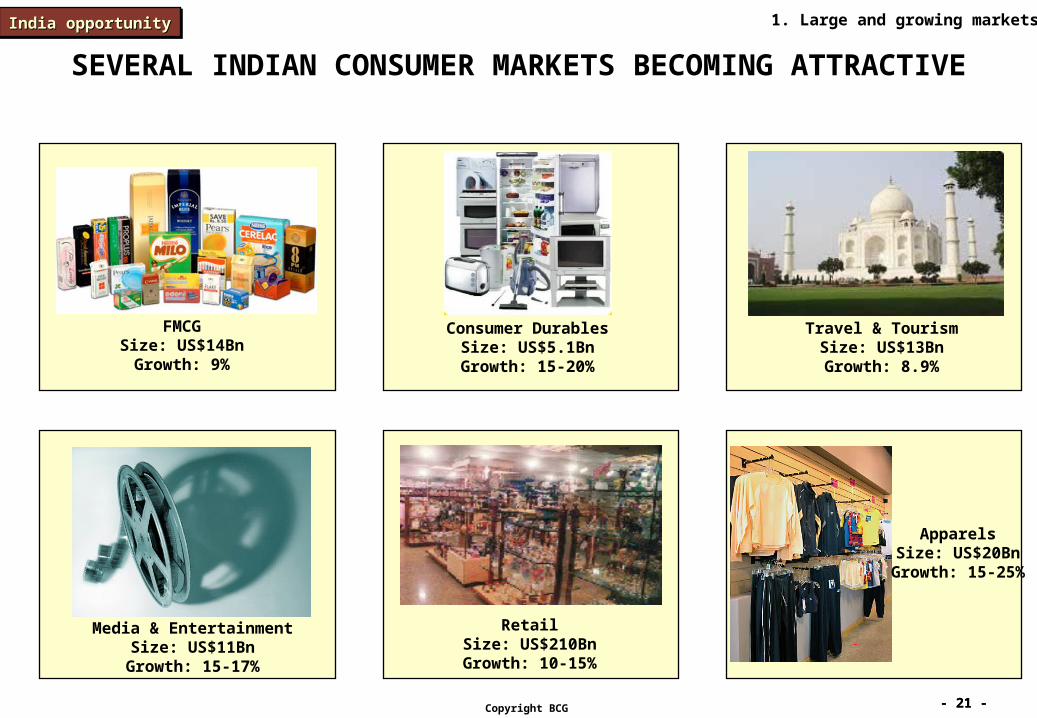

SEVERAL INDIAN CONSUMER MARKETS BECOMING ATTRACTIVE

FMCGSize: US$14Bn

Growth: 9%

Media & EntertainmentSize: US$11BnGrowth: 15-17%

Consumer DurablesSize: US$5.1BnGrowth: 15-20%

RetailSize: US$210BnGrowth: 10-15%

ApparelsSize: US$20BnGrowth: 15-25%

Travel & TourismSize: US$13BnGrowth: 8.9%

1. Large and growing marketsIndia opportunityIndia opportunityIndia opportunityIndia opportunity

- 22 -- 22 -Copyright BCG

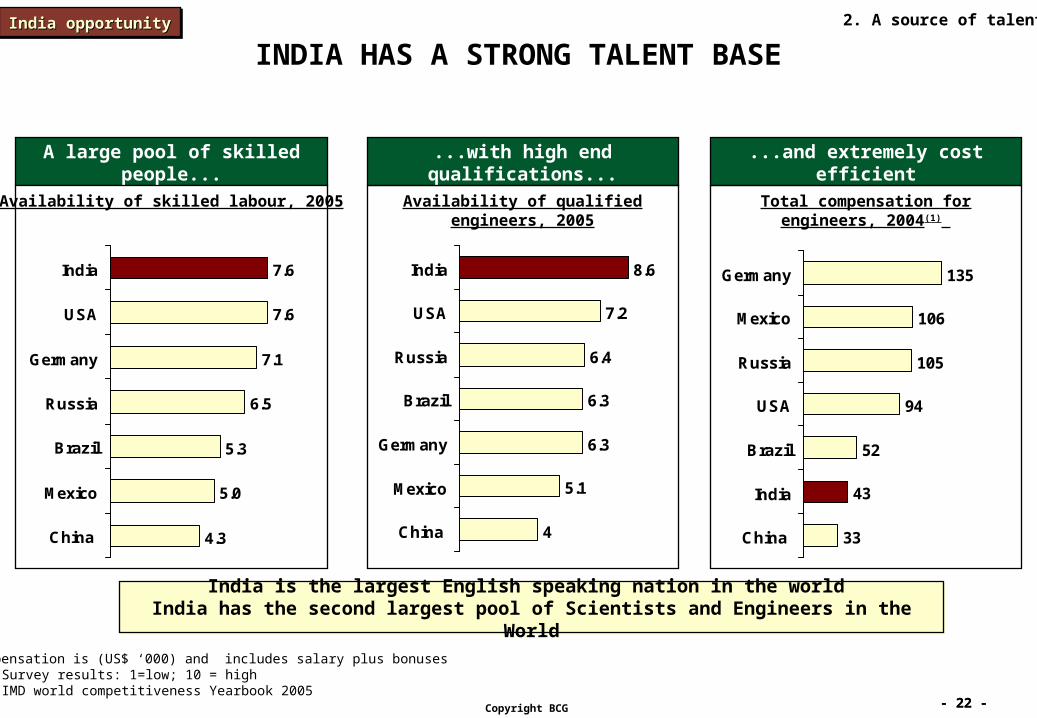

INDIA HAS A STRONG TALENT BASE

(1) Compensation is (US$ ‘000) and includes salary plus bonusesNote: Survey results: 1=low; 10 = highSource: IMD world competitiveness Yearbook 2005

...with high end qualifications...

4

5.1

6.3

6.3

6.4

7.2

8.6

China

Mexico

Germany

Brazil

Russia

USA

India

...and extremely cost efficient

33

43

52

94

105

106

135

China

India

Brazil

USA

Russia

Mexico

Germany

Availability of qualified engineers, 2005

India is the largest English speaking nation in the world India has the second largest pool of Scientists and Engineers in the World

India is the largest English speaking nation in the world India has the second largest pool of Scientists and Engineers in the World

A large pool of skilled people...

4.3

5.0

5.3

6.5

7.1

7.6

7.6

China

Mexico

Brazil

Russia

Germany

USA

India

Availability of skilled labour, 2005 Total compensation for engineers, 2004(1)

2. A source of talentIndia opportunityIndia opportunityIndia opportunityIndia opportunity

- 23 -- 23 -Copyright BCG

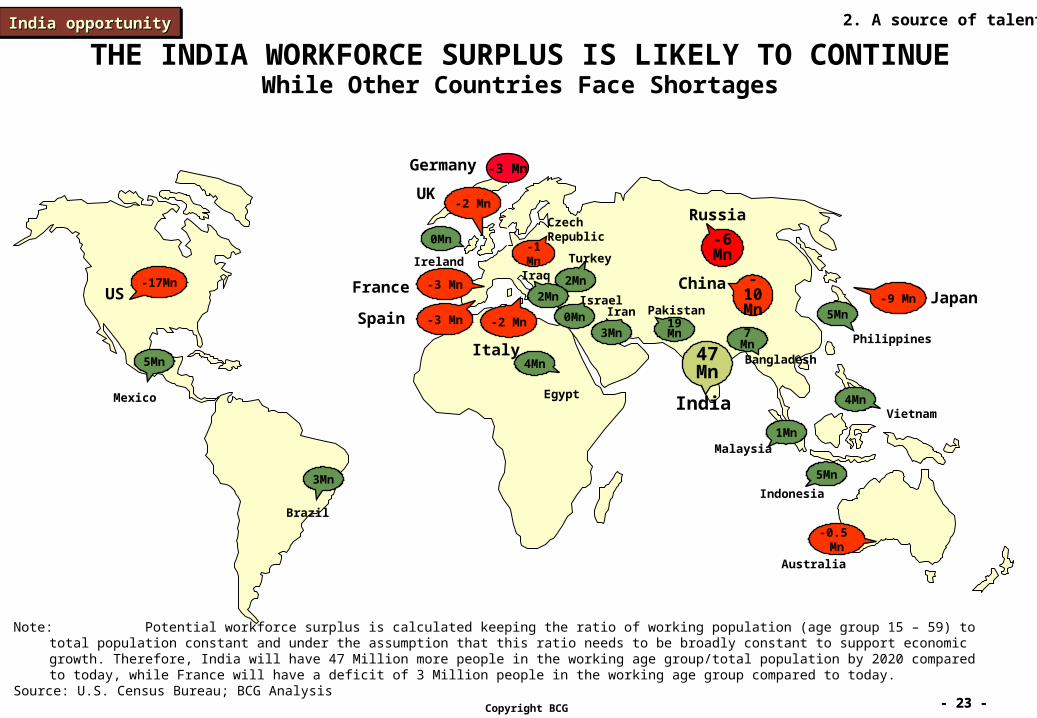

47Mn

19Mn 7

Mn

3Mn

5Mn

3Mn

India

Bangladesh

PakistanIran

Brazil

Mexico

Philippines

5Mn

4MnVietnam

2Mn

Turkey

Potential surplus population in working age group (2020)

-10Mn

China

-6Mn

Russia

5Mn

Indonesia

1MnMalaysia

0Mn

Ireland

Israel0Mn

THE INDIA WORKFORCE SURPLUS IS LIKELY TO CONTINUEWhile Other Countries Face Shortages

Iraq

2Mn

-1Mn

CzechRepublic

Note: Potential workforce surplus is calculated keeping the ratio of working population (age group 15 – 59) to total population constant and under the assumption that this ratio needs to be broadly constant to support economic growth. Therefore, India will have 47 Million more people in the working age group/total population by 2020 compared to today, while France will have a deficit of 3 Million people in the working age group compared to today.

Source: U.S. Census Bureau; BCG Analysis

4Mn

Egypt

-17MnUS

-2 MnUK

-2 Mn

Italy

-3 MnFrance-9 Mn Japan

-0.5 Mn

Australia

-3 MnSpain

-3 MnGermany

2. A source of talentIndia opportunityIndia opportunityIndia opportunityIndia opportunity

- 24 -- 24 -Copyright BCG

SEVERAL FIRMS HAVE OUTSOURCED OPERATIONS TO INDIASelect Examples

Industrial Goods Consumer/Services/Hi-TechFinancial Services

3. Base for business process off-shoringIndia opportunityIndia opportunityIndia opportunityIndia opportunity

- 25 -- 25 -Copyright BCG

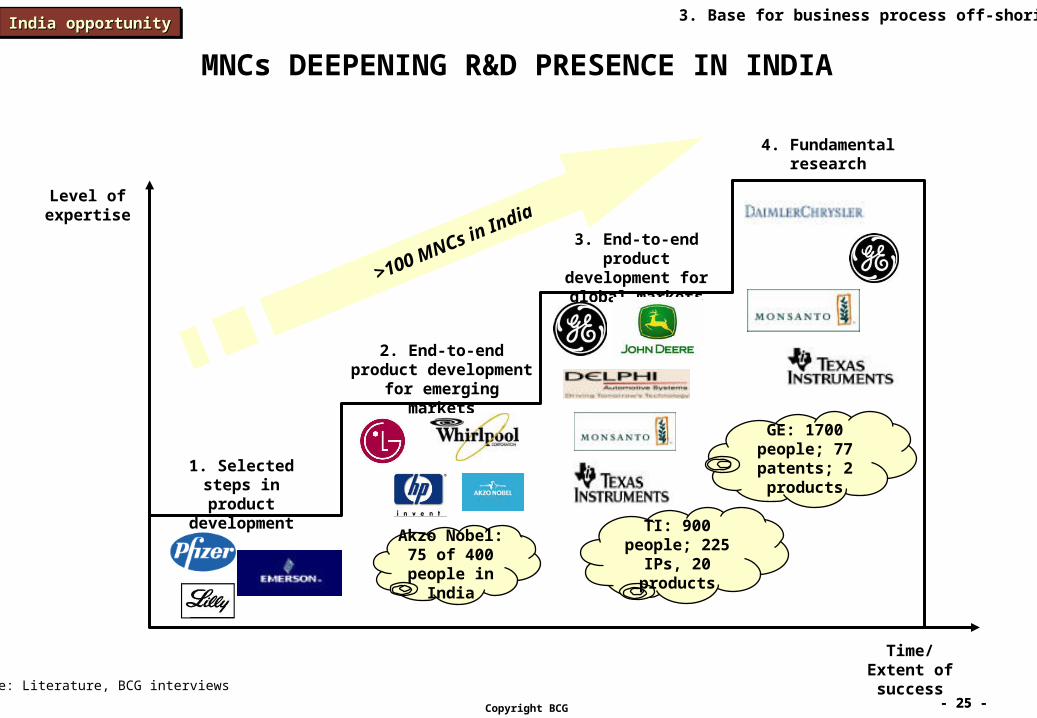

MNCs DEEPENING R&D PRESENCE IN INDIA

>100 MNCs in IndiaLevel of

expertise

1. Selected steps in product

development

2. End-to-end product development for

emerging markets

3. End-to-end product development for global markets

4. Fundamental research

TI: 900 people; 225 IPs, 20 products

GE: 1700 people; 77 patents; 2

products

Time/Extent of success

Akzo Nobel: 75 of 400 people in

India

Source: Literature, BCG interviews

3. Base for business process off-shoringIndia opportunityIndia opportunityIndia opportunityIndia opportunity

- 26 -- 26 -Copyright BCG

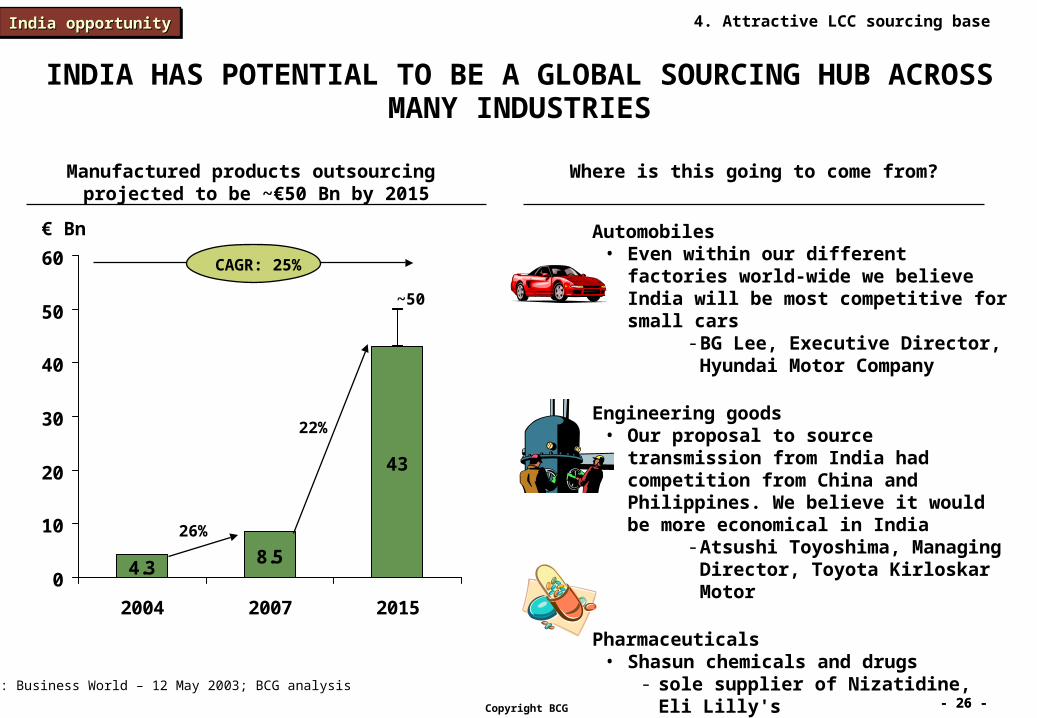

INDIA HAS POTENTIAL TO BE A GLOBAL SOURCING HUB ACROSS MANY INDUSTRIES

Source: Business World – 12 May 2003; BCG analysis

Automobiles• Even within our different factories world-

wide we believe India will be most competitive for small cars

- BG Lee, Executive Director, Hyundai Motor Company

Engineering goods• Our proposal to source transmission from

India had competition from China and Philippines. We believe it would be more economical in India

- Atsushi Toyoshima, Managing Director, Toyota Kirloskar Motor

Pharmaceuticals• Shasun chemicals and drugs

- sole supplier of Nizatidine, Eli Lilly's ~€190 Mn anti ulcer drug

- 60% of Knoll Pharma's global requirement of Ibuprofen

€ Bn

4.38.5

43

0

10

20

30

40

50

60

2004 2007 2015

26%

22%

~50

CAGR: 25%

Manufactured products outsourcing projected to be ~€50 Bn by 2015

Where is this going to come from?

4. Attractive LCC sourcing baseIndia opportunityIndia opportunityIndia opportunityIndia opportunity

- 27 -- 27 -Copyright BCG

JUST ANOTHER DAY IN INDIA...