2010/11 Annual report

17

2010–2011 Our journey

-

Upload

lucrf-super -

Category

Documents

-

view

212 -

download

0

description

2010/11 Annual report

Transcript of 2010/11 Annual report

2010–2011

Our journey

Chairman & CEO Forward .............................................................................................................. 3

Our Trustee Board ........................................................................................................................ 4

Personal Financial Advice ............................................................................................................. 6

Member story – Claire .................................................................................................................. 8

Member story – Shaun ............................................................................................................... 10

Member story – Norm ..................................................................................................................12

Super as a long-term investment ................................................................................................. 14

Our awards ................................................................................................................................ 15

Investments ...........................................................................................................................................16

How the economy performed ....................................................................................................... 16

Annual Investment returns .......................................................................................................... 18

Pre-mixed investment options ..................................................................................................... 20

Asset class investment options ....................................................................................................22

Performance results ................................................................................................................... 24

Financial Statements and other information ..................................................................................................26

Enquiries and complaints ............................................................................................................ 26

Government supervision ............................................................................................................. 26

Identity fraud ............................................................................................................................. 26

Reserves policy .......................................................................................................................... 26

Contribution arrears – what to do .................................................................................................27

Indemnity insurance ....................................................................................................................27

Transfer of benefits to an Eliible Rollover Fund (ERF) ......................................................................27

Unclaimed money ........................................................................................................................27

Financial statements .................................................................................................................. 28

The past financial year has been a good one for LUCRF and its members with the Fund returning 9.92% to members accounts.

Members with transition to retirement pension accounts and allocated pension accounts achieved a return of 11.76%. The difference in the returns arises from the taxation advantages available to pension accounts.

As reported to members last year, LUCRF began to position its balanced fund a little more defensively from the beginning of the 2009/10 year. We continued this in the 2010/11 year. Our general view being that the circumstances in the US and Europe will contribute to continuing uncertainty in the near to medium term.

The recent dramatic volatility in the markets has caused members great concern and the number of members calling into our contact centre doubled during this period.

An important message coming out of this market uncertainty involves understanding and information. Members should seek an understanding of how their money is invested by LUCRF, and match their account investment profile with their personal needs.

LUCRF can help you do this as part of the Fund’s free advice service.

We offer a broad range of investment options for members and we have highly qualified staff available to talk with you over the phone, or in person. Please don’t hesitate to give us a call to talk to us about your account.

Thank you to our Board, our hardworking staff and our members who have travelled with us over the past year. We look forward to another successful year in 2011/12.

Greg Sword AM John Carlile CEO Chairman

Chairman & CEO forward

3

Greg Sword (left), John Carlile (right)

Table of contents

This Annual Report was issued by LUCRF Pty Ltd ABN 18 005 502 090 AFSL 258481 RSE Licence No L0002981 as Trustee for the Labour Union Co-operative Retirement Fund (LUCRF Super) ABN 26 382 680 883 RSE Reg R1067521

CommitteesThe Trustee Board has appointed four Committees that advise it. Members of each Board Committee at 30 June 2011 are detailed below:

Compliance & Audit CommitteeJohn Carlile, Ted Eftimiadis, Tim Kennedy*, Charlie Donnelly.

Membership Services CommitteeChristopher Brown, Caterina Cinanni, Jeff Doyle, Raymond Tanner*.

Investment CommitteeCharlie Donnelly, Tony O’Grady*, Tim Kennedy, Raymond Tanner.

Management CommitteeJohn Carlile, Gary Maas*, David O’Sullivan, Paul Richardson.

*Chairman

Trust DeedA copy of our Trust Deed and Rules is available by calling us on 1300 130 780 or sending an email request to [email protected]

Changes to the Trust DeedThe way in which the Fund is governed and controlled is established through a legal document

– the Trust Deed and Rules.

During the year, amendments were made to reflect changes to legislation and regulations affecting super and other operational matters such as enabling binding death benefit nominations.

5

Our trustee BoardLUCRF Pty Ltd is made up of:

• Five Member Representative Directors,

• Five Employer Representative Directors, and

• Two Independent Directors.

Member Representative DirectorsGeneral SecretaryNational Union of Workers Charlie Donnelly Deputy Chairman

Victorian Branch SecretaryNational Union of Workers Tim Kennedy

Legal OfficerNational Union of Workers Gary Maas

Lead OrganiserNational Union of Workers Caterina Cinanni

Assistant National SecretaryNational Union of Workers Paul Richardson (appointed 21st December 2010)

Executive DirectorLUCRF Pty Ltd Antony Thow (resigned 15th December 2010)

We would like to thank Antony for his contribution.

Employer Representative DirectorsJohn Carlile (Chairman) Consultant

Christopher Brown Consultant

Jeff Doyle CEO, Adecco Group

Raymond Tanner Consultant

Ted Eftimiadis Employee Relations Manager, Pacific Brands

Independent DirectorsDavid O’Sullivan Partner, IFS Legal

Tony O’Grady Consultant

Appointment to the BoardThe Fund’s Trust Deed and Rules sets out the procedure for appointing Directors. The General Secretary of the National Union of Workers nominates Member Representatives in writing.

Employer Representatives and Independent Directors are appointed on the recommendations of nominating committees.

The LUCRF Trustee Board From left to right: Tim Kennedy, John Carlile, Charlie Donnelly, Ted Eftimiadis, Christopher Brown, Jeff Doyle, Paul Richardson, Caterina Cinanni, Gary Maas, Tony O’Grady David O’Sullivan, Raymond Tanner.

7Wherever your path takes you, we’ll be here to help

• Commitment free

• Interested in travel, new car

• Thinking of first home

• Career development

Financial advice needs • Super co-contribution

• Budgeting for house, travel or new car

• Debt or savings help

Aged 18 to 24

• Have commitments, relationship/marriage

• Career orientated, education debt

• House, first mortgage

• Starting a family

Financial advice needs • Wealth creation

• Debt consolidation and savings plan

• Insurance

• Tax minimalisation

Aged 25 to 31

• Responsibility, financial commitments

• Busy work and home life

• Family holidays and education

• Career progression

Financial advice needs • Minimise debt, build wealth,

invest for future

• Tax minimisation strategy

• Estate planning

Aged 32 to 49

• Changing priorities, work/life balance

• Children moving, caring for elderly parents

• Reducing work hours, more time for you

• Mortgage paid off and have surplus income

Financial advice needs • Transition pension,

salary sacrifice

• Boost super and wealth protection

• Planning re: Centrelink and reducing tax

• Non super investments

Aged 50 to 63

• Enjoy what you’ve worked for and your family, travel, fulfil goals

• Pursuit of hobbies and social networking

• Renewed focus on life

• Helping with Grandchildren

• Volunteering or working part-time

Financial advice needs • Pension options

(LUCRF and Centrelink)

• Wealth protection and longevity

• Estate planning

• Structuring investments

• Tax efficiency

Aged 64 +

Personal financial advice you can trustWe can help you set and achieve your financial goals, regardless of which stage of life you are at. We can review your personal circumstances and develop a plan to suit your specific needs.

Superannuation is now provided from a person’s first job to retirement, this is why members need to plan ahead and treat super as a long-term investment.

Advice regarding superannuation and pension options is generally free of charge. However, our advice is not limited to just super and pensions. We can advise you on a range of financial topics that should be considered at different times in your life, including:

• Budgeting

• Wealth creation

• Estate planning

• Investment choice

• Insurance needs

• Debt management

• Tax minimisation and much more.

Your financial advice requirements will change over time; from just starting out, to settling in to your retirement. Our Representatives can help you make the right decisions.

Read about the different life stages and situations of some of our members, over the next few pages:

• Claire running her own business and getting married

• Shaun working hard at his career and changing direction, and

• Norm transitioning from loyal full-time employee to relaxed retiree.

free Information seminarsThere are many factors you should consider when

making decisions about your financial arrangements,

including your super. Part of our commitment to you

is to help you to make the right decisions.

We provide information and support to

empower you to take control of your finances.

We run free information seminars around the

country that cover a broad range of topics.

Visit our website www.lucrf.com.au or

contact us on 1300 130 780 to find out more.

member story

Pointing you in the right direction

“What I’ve always loved about LUCRF is the fact that I can speak to a real person, someone who understands.Claire Turpin LUCRF Super member since 2005

In life it’s sometimes hard to know what is around the corner, especially when experiencing tough times.

However, LUCRF Super member Claire Turpin is a firm believer that everything happens for reason.

At just 27, Claire owns and runs her own business, a boutique clothing store, Simone Louise, based in Kellyville, New South Wales, along with husband, Brett.

Buying the business was a great achievement for the pair, who, Claire says, never thought it would be possible to own their own business, let alone at such a young age. But while the business is a dream come true, the road that led them to this point was less than smooth.

Claire joined LUCRF Super in 2005 while working in marketing for a publications company and took her super with her when she left. Her next role however was fraught with problems, and unbeknownst to Claire, her new employer was not paying her super.

“It was an extremely stressful and upsetting time,” recalls Claire. However, she says LUCRF Super was immensely supportive of her situation.

“What I’ve always loved about LUCRF is the fact that I can speak to a real person, someone who understands. I’ve had no reluctance in taking my super with me wherever I’ve gone as LUCRF Super is stable, reliable and easily accessible.”

Eventually Claire was forced to leave her job and found herself in need of work. When her mother-in-law, Kerry came to the rescue offering her work at one of her six Simone Louise stores, Claire had no idea that it would set wheels in motion, and eventually lead to owning her own store.

“It really did just start out as a retail-customer service role. But in time I began helping with buying and other duties essential to the business, and this past February we purchased the Kellyville store,” beams Claire.

Half way through their first year of business, every day presents new learnings and opportunities.

“While it hasn’t been easy, and a small business is a seven day a week commitment, it’s been a tremendous learning curve. I’ve gained confidence in my own abilities, from choosing stock to reflect my customers’ tastes and needs, to managing finances, and also managing three staff. I am lucky to have such a supportive network of friends, family and loyal staff around me. Kerry is a huge inspiration to me and what I can achieve. And I mean, really, what girl wouldn’t love to own their own clothing store!”

To say it has been a big year for Claire and Brett is an understatement. With their wedding last November, the purchase of the store in February – and everything that comes with being small business owners – the next step for the couple is to purchase their first family home, and perhaps even another store sometime in the future.

“If you had told me two years ago that the challenges I was going through would end up being one of the best things that happened to me, I would have laughed. But looking back it’s hard not to think that everything really does happen for a reason.”

9

Growing up in the western suburbs of Melbourne, Shaun Micallef fondly remembers his family trips down to Rye and Rosebud with his parents and two siblings.

Aspiring to his childhood heroes, David Beckham and Hulk Hogan, Shaun has always demonstrated poise and leadership qualities that have helped shape his work and family life.

Shaun is a dedicated father and a passionate Essendon supporter who enjoys Asian Cuisine and admires Richard Branson as he has been very successful in overcoming significant challenges and high risk business situations.

Shaun’s greatest achievements include raising his daughter and being able to successfully progress in his professional career.

After completing school, Shaun began working at Safeway as a trainee Department Manager, before working at their Distribution Centre as a ‘picker packer.’

He worked his way up the ladder and eventually his drive and ability to innovate and lead others

later enabled him to become a Dispatch Supervisor.

Recently, Shaun has had a change in career direction and is now the new Warehouse and Distribution Manager for Dexion Commercial.

Hungry for a new challenge, Shaun now enjoys the autonomy to make business decisions that affect the performance of the organisation.

The role is less hands on and requires the setup of new facilities, systems and processes that will help improve the organisation.

A member since 2010, Shaun decided to stay with LUCRF as he changed careers. Shaun feels that he is a valued part of the Fund and not just another number. LUCRF’s low fees, investment choices and excellent customer service helped cement his decision to take LUCRF with him to his new role.

“I try to keep up to date with my super. When you retire that’s what you look up to. As long as the returns are consistent with what I’m looking for, I have no reason to leave.”

Mapping the way

Shaun Micallef LUCRF Super member since 2010

“LUCRF makes me feel like a valued part of the Fund and not just another number

member story

11

Relaxed and friendly would be the best way to describe Norm Barrow.

Even when the Global Financial Crisis hit and affected his super balance, this didn’t dampen the spirits of Norm who retired in November 2007.

A loyal and hard-working employee of Ormiston Rubber for 50 years, Norm joined the company upon leaving school and worked his way up to Managing Director. His greatest achievement was keeping Ormiston running as a profitable business for so long.

A proud family man, Norm has been married for 43 years and has two children, whom have also been very successful in their chosen fields. His wife Faye was even awarded an Order of Australia medal for her good work and outstanding contribution to disability teaching.

Since retiring, Norm has had more time to focus on his health and fitness. He joined a gym for the first time, started playing tennis and enjoying long walks on the beach.

After working in an office environment and driving to and from work for such a long time, all this ex-ercise in retirement has greatly improved Norm’s health. In fact Norm, mentioned that the best thing about being retired was ‘not having to drive to work and being able to find time to do things’ that he couldn’t do before.

A typical day for Norm now involves walking his dog Millie, doing the daily crosswords, eating lunch with friends, going to the gym (or walking) and a little bit of housework.

An avid Essendon supporter since he was a little lad, Norm still enjoys going to the football with his daughter and watching sports on TV. He also loves music, especially Andre Rieu. When asked who he would invite for a dinner party, Norm said ‘Steve Martin, Hugh Grant and Meg Ryan!

Norm was happy to stay with LUCRF upon retiring and has recently opened a LUCRF Pension account. He cites the ‘strong performance, ease of access on the internet and advice of the consultants’ as the key things that have kept him connected to the Fund.

Missing his work mates has probably been the hardest part of his transition to retirement, although he still catches up with them as often as he can. A relaxed and healthy Norm agrees that retirement has been great so far and that you’ll know when you’re ready to retire’.

The ticket to a great retirement

Norm Barrow LUCRF Super member since 1998“LUCRF’s strong performance & personal advice has kept me connected with the Fund

member story

13

$120,000

$100,000

$80,000

$60,000

$40,000

$20,000

$0

$50,000 $50,000

$110,519

Account balance at 30/6/2004

Account balance at 30/6/2011

That’s a difference of $8,631

$101,888

Cash investment option Balanced (default) investment option

Assumptions: Starting income of $50,000, annually increased by 3%, 9% super contributions and starting account balance of $50,000.

Just as planning for the future and obtaining financial advice at different stages of life is important, it’s also essential to build your super savings for retirement. One way to do this is to invest in an option that achieves strong performance over time.

One of LUCRF Super’s objectives is to balance risk and return in order to maximise long-term returns for our members. We have investment strategies in place to reduce the impact that market extremes may have on your super or pension.

A word about our Balanced optionThe majority of our members are invested in the Balanced (default) option, which contains a mix of assets that provide a balance between risk and return.

The example below shows the difference between investing in the Balanced and Cash investment options over a 7 year period. This is based upon LUCRF Super’s actual returns during this period.

.

Super as a long-term investment Our awards

LUCRF Super is an award-winning Fund recognised for excellence in products and services by several independent ratings agencies. Our awards are outlined below:

AAA Rating LUCRF Super has again received an AAA rating by SelectingSuper, whose independent assessment rates the quality of a super fund by examining, reviewing, comparing and assessing funds to give a clear indication of their market position.

The AAA rating means that SelectingSuper considers the Fund to be of very high-quality, well managed, competitively priced and has a strong track record of demonstrated success with a range of useful features that is likely to appeal to its membership.

Platinum Rating LUCRF Super has been awarded a Platinum rating, the highest possible, for both our pension and super products, by SuperRatings, an independent ratings agency that assesses over 500 of Australia’s largest multi-employer super funds, personal super and pension funds. The prestigious platinum award is only given to funds that represent the “best value for money”. The criteria that help form the ratings include invest-ments, fees and charges, administration, advice, governance, insurance and qualitative overlay.

5 Apples LUCRF Super has received the highly regarded Chant West 5 Apples rating, the highest possible, for the Super and Pension products. Chant West is an independent specialist superannuation research and consultancy firm that provides an assessment of funds. The criteria that help form the ratings include investments, fees, insurance, administration, member services and employer services.

5 Star Rating LUCRF Pensions have been awarded five stars from one of Australia and New Zealand’s most comprehensive research service providers, CANSTAR CANNEX.

The five star status, which is the top rating possible, denotes outstanding value and was awarded based on factors including cost, management fees, transaction fees, member benefits, accessibility, functionality, insurance cover, income payment op-tions and retirement solutions. This award recog-nises our efforts to deliver high quality pension products and services to members.

Green Star RatingAlong with the National Union of Workers (NUW), we now hold a ‘4 Star Green Star – Office Interiors v1.1’ award from the Green Building Council of Australia which represents “Best Practice”, for the green-conscious fit out of our offices at 833 Bourke Street, Docklands, Melbourne.

Seven assessment areas were used to calculate the environmental impacts of each individual items used in the fitout (such as furniture, appliances and fittings), including: eco-preferred content, durability, and the product manufacturers product stewardship credentials.

Use of natural lighting was also another important factor, as well as proximity to public transport, cyclist facilities, energy saving technology such as sensor lights and waste minimisation.

Interiors

As can be seen above, the Balanced (default) option has provided superior returns for members during this period, despite the larger fluctuations in yearly returns. This can also be seen over the

long-term with our Balanced annual average return since inception of 10.02% (1978 to 2011). For more information about investments, please see pages 20-23.

15

Jargon Inflation – Upward price movement of goods and services in the economyAustralian 90 Day Bank Bill – Australia’s benchmark indicator for short-term interest ratesBudget deficits – when spending exceeds incomeQEII – A type of monetary policy, quantitative easing measures are intended to stimulate an economy through a central bank’s purchase of government bonds or other financial assetsTrade weighted index – Also known as the effective exchange rate, it is a weighted average of exchange rates of home and foreign currencies Liquidity – The degree to which an asset can be bought or sold in the market without affecting its priceCPI – Consumer Price Index.

How the economy performedPrepared by Towers Watson

Australian snapshot 2010/11 • The Australian economy grew at the inflation

adjusted rate of 1.0% (year to March 2011)

• The Reserve Bank of Australia (RBA) raised interest rates from 4.5% to 4.75% over the year

• The Australian share market performed strongly particularly during the first half of the financial year

• The Australian dollar rose significantly in value relative to the US dollar.

The Australian economy continued to grow coming out of the Global Financial Crisis and remained resilient throughout the financial year, withstanding natural disasters and rising global economic uncertainty.

Despite the Queensland floods and Cyclone Yasi at the start of 2011, the Australian economy still grew by 1% (inflation adjusted rate) for the year to March 2011. Inflation for the year to March was a manageable 3.3%, which enabled the official cash rate (interest rates) to remain steady at 4.75% since November 2010. In further positive news, the unemployment level decreased slightly from 5.1% to 4.9% over the financial year.

Global snapshotInternational economies have varied substantially between countries and continents. The US continued to battle slow economic recovery with a lower than expected growth rate and continuing levels of high unemployment at 9.2%. Meanwhile, China continued to show strong growth, with its economy recording 9.5% growth.

Inflation also increased to 6.4%, prompting the People’s Bank of China to implement measures to control inflation (e.g. raising interest rates). Although Japan was negatively impacted by the natural disasters earlier in 2011, the injection of liquidity to their economy has resulted in recent signs of stability.

In Europe, some economies grew (including Germany and France), whilst others such as Greece, Ireland, Italy, Spain and Portugal continued to struggle. The European Central Bank (EBC) increased interest rates by 0.25% to 1.25% in April in an effort to control inflation.

Australian sharesWhilst the Australian share market performed well overall, it experienced a volatile 12 months this financial year. Performance, although mostly positive, wavered as concerns regarding Greek debt escalated. The rise of the Australian dollar (A$) also held back offshore investors and com-pany earnings, resulting in higher levels of market instability. The S&P/ASX 300 accumulation index (Australian Stock Exchange) returned 11.9% over the 2010/11 financial year.

International sharesGlobal share markets recorded strong gains over the 2010/11 financial year. A reduced risk appetite for shares and falling investor sentiment, resulting from uncertainty over the Greek debt crisis, stabilised in late June as measures to reduce the Greek budget deficit, were approved by the Greek parliament.

A major development during the year was the strengthening of the Australia dollar (A$), which reached historical highs of 109 US cents in May, and closed the financial year at 107.08 US cents (up from 84.08 US cents). The A$ also rose against its other major trading partners, as measured by the Trade weighted index, finishing the year at 77.8 (up from 67.3 the previous year).

PropertyThe Australian property market, as measured by the S&P/ASX300 Property Accumulation Index, returned 5.9% over the year, and performed poorly compared to the last financial year where the Index had returned 20.3%.

InvestmentsCash and fixed interestThe Australian fixed interest market performed well over the 2010/11 financial year. The Australian 90 Day Bank Bill Index returned 2.2% for the financial year, while the All Maturities (UBSA Composite Bond Index) returned 5.6% for the year.

Global fixed interest, as measured by the Barclays Global Aggregate Index (hedged to A$) returned 6.9%, outperforming the Australian fixed interest market.

Looking forwardIn the short-term, increased uncertainty in global markets is likely as the US approaches the end of the second term of its quantitative easing (QEII) initiatives and continues to raise the government debt ceiling. European economic conditions are likely to vary greatly, as elevated debt issues are expected to remain unresolved.

In a number of advanced economies, especially the US and UK, high levels of economic slack and unemployment may prevent core inflation rates from rising for a number of years. However, strong growth in emerging economies will drive wage and price growth in these countries, with possible spill-over effects for the developed world, especially from the commodity sector.

China is expected to experience a lower level of growth in their economy over the next few years. There are indications that Brazil, is also expecting lower economic conditions ahead.

Note: This investment commentary does not constitute advice. All investment figures quoted relate to before-tax performance of the relevant industry benchmark.

17

19Annual investment returnsUpdating your balanceAt the end of each financial year, we calculate our declared rates which represent the final return on investment (ROI) for our members. This percentage (positive if your option has made money, negative if it has not) is then applied to your balance and adjusted accordingly.

This process takes a couple of months after 30 June and once finalised, we send you a statement outlining how your account balance has performed over the course of the year (or since you joined if you are a relatively new member).

Rollovers and other benefit paymentsWhere you request to rollover your balance to other superannuation or pension funds, full or partial benefit payments (commutations) and Death and Total & Permanent Disablement payments, you will receive the latest rates (post date of receipt of the benefit payment request) and then the net cash rate to the date of payment.

Authorised early release paymentsCompassionate (APRA approved) and financial hardship payments will receive the most recent rate and then the net cash rate to the date of payment.

Note: The net cash rate is the after-tax rate determined by LUCRF Super.

InvestmentsAt 30 June 2011, the following investment exceeded 5% of the Fund’s total assets:

Members Equity – Cash Management Accounts ......................5.39%

DerivativesThe Trustee has authorised the use of forward foreign exchange contracts to partially hedge the Fund’s international investments. Futures and options may also be used to manage the Fund’s investment portfolio. Derivatives are used to control risk and are not used to leverage the Fund or to speculate.

Investment optionsLUCRF Super and LUCRF Pensions offered nine investment options for members to choose from during the 2010/11 financial year.

These are classified as either Pre-mixed or Asset Class options.

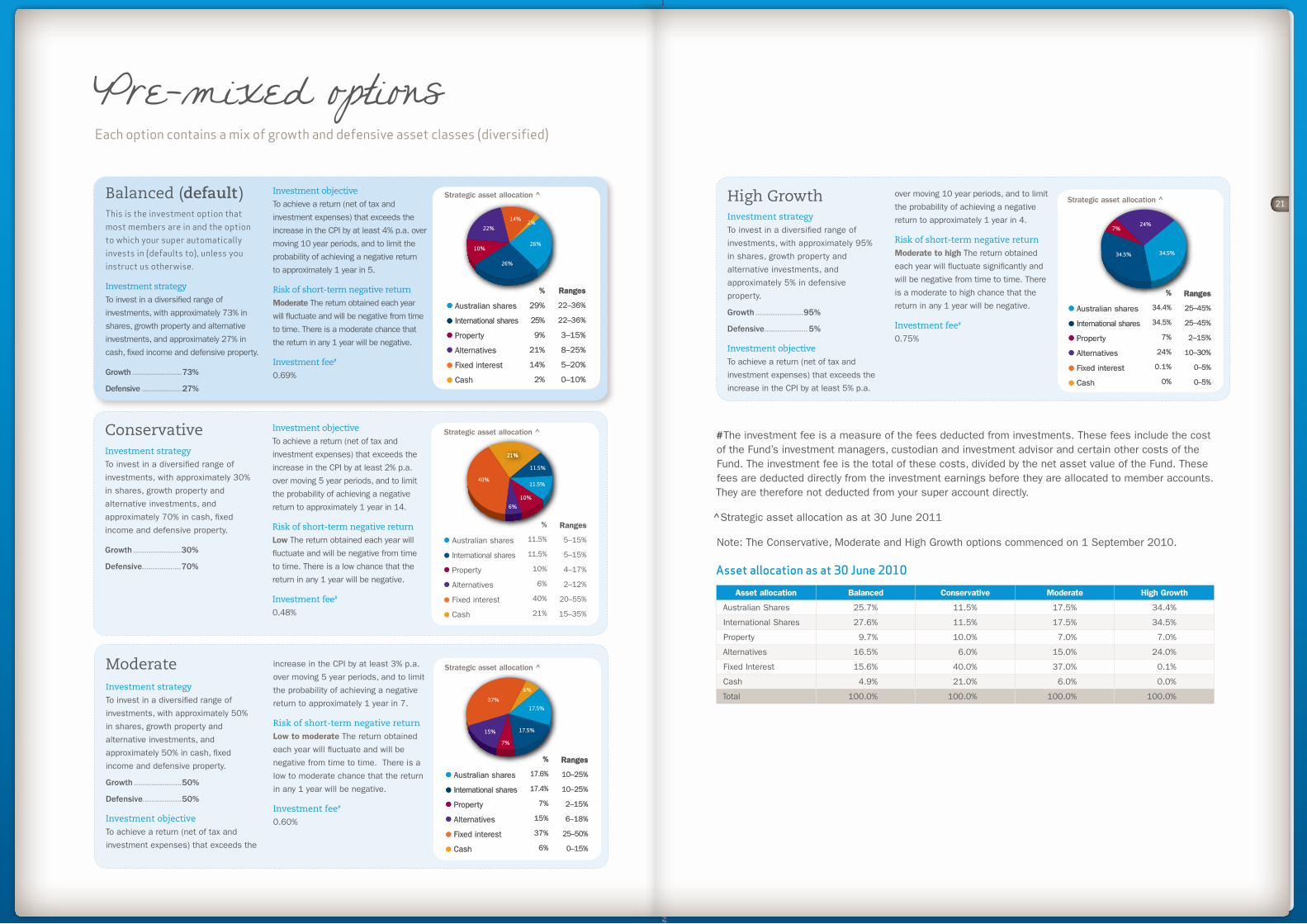

Pre-mixed optionsOur pre-mixed options are made up of a blend of asset classes and are known as diversified options. Each choice has a different amount of growth and defensive types of assets that spread the risk. The pre-mixed options are:

• Balanced (default)

• Conservative

• Moderate, and

• High Growth

Asset class optionsOur asset class specific options are just that, options that invest solely in one asset class. The asset class options are:

• Cash

• Indexed Shares

• Australian Shares

• International Shares, and

• Property

We introduced the Conservative, Moderate and High Growth options on 1 Sept 2010. Information regarding the offer of these pre-mixed options was notified to members in our previous MySuper and MyPension newsletters and the 2009/10 Annual Report.

The Balanced optionLUCRF’s Balanced (default) investment option is diversified in its mix of growth and defensive asset classes.

This option provides a broad range of investments with the majority in shares, property, fixed income and alternatives. It is designed to offer both growth and protection over the long-term.

Our approach for the Balanced option is to allow the Fund to provide a measure of stability when the markets are volatile and to capture growth as the markets rise. Since the Fund’s inception, our Balanced option has produced an average annual return to members of 10.02% (1978 to 2011).

Whilst past investment returns are no guarantee of future investment performance, our history over more than 30 years show that despite investment markets moving up and down, our Balanced option has provided members with a healthy return over the long-term.

Investment ManagersAcorn Capital Alliance Bernstein Apostle Asset Management Limited Arrowstreet Capital LP Aviva Bell Asset Management Limited Bridgewater Associates Inc. Colonial First State Asset Management (Australia) Limited Commonwealth Bank of Australia DFA Australia (Dimensional) GSAM Ixis Loomis Sayles JF Capital Partners Ltd JPM Chase Bank, National Association (Sydney Branch) Karara Capital Limited Lazard Asset Management Pacific Co. Macquarie Investment Management Limited ME Portfolio Management Pty Ltd

MFS Investment Management Northcape Capital Pty Ltd Palisade Investment Partners Limited Perpetual Investment Management Limited PIMCO Australia Pty Ltd QIC Limited Schroder Investment Management Australia Ltd Stone Harbor Investment Partners LP Super Loans Trust Vanguard Investments Australia Ltd Vianova Asset Management Pty Ltd

Investment advisors and consultants Arcadia Funds Management Limited Bell Asset Management Limited Sovereign Investment Research Pty Ltd Thomas Murray (Australasia) Pty Ltd Towers Watson

List of key LUCRF Super service providers (as at 30 June 2011)AuditorPricewaterhouseCoopers

BankersCommonwealth Bank of Australia JP Morgan Chase Bank

CustodianJP Morgan Chase Bank

Legal AdvisorsDLA Phillips Fox Holding Redlich Ryan Carlisle Thomas Lawyers

Group InsurerOne Path

Tax AdvisorErnst & Young

Asset Allocation ConsultantTowers Watson

Investments (continued)

21

26%

14%22%

10%

2%

26%

21%21%

11.5%

11.5%

10%6%

40%

37%6%

17.5%

17.5%

7%

15%

34.5%34.5%

24%7%

Pre-mixed optionsEach option contains a mix of growth and defensive asset classes (diversified)

#The investment fee is a measure of the fees deducted from investments. These fees include the cost of the Fund’s investment managers, custodian and investment advisor and certain other costs of the Fund. The investment fee is the total of these costs, divided by the net asset value of the Fund. These fees are deducted directly from the investment earnings before they are allocated to member accounts. They are therefore not deducted from your super account directly.

^Strategic asset allocation as at 30 June 2011

Note: The Conservative, Moderate and High Growth options commenced on 1 September 2010.

Asset allocation as at 30 June 2010 Asset allocation Balanced Conservative Moderate High Growth

Australian Shares 25.7% 11.5% 17.5% 34.4%

International Shares 27.6% 11.5% 17.5% 34.5%

Property 9.7% 10.0% 7.0% 7.0%

Alternatives 16.5% 6.0% 15.0% 24.0%

Fixed Interest 15.6% 40.0% 37.0% 0.1%

Cash 4.9% 21.0% 6.0% 0.0%

Total 100.0% 100.0% 100.0% 100.0%

% Ranges

Australian shares 29% 22–36%

International shares 25% 22–36%

Property 9% 3–15%

Alternatives 21% 8–25%

Fixed interest 14% 5–20%

Cash 2% 0–10%

% Ranges

Australian shares 17.6% 10–25%

International shares 17.4% 10–25%

Property 7% 2–15%

Alternatives 15% 6–18%

Fixed interest 37% 25–50%

Cash 6% 0–15%

% Ranges

Australian shares 34.4% 25–45%

International shares 34.5% 25–45%

Property 7% 2–15%

Alternatives 24% 10–30%

Fixed interest 0.1% 0–5%

Cash 0% 0–5%

26%

14%22%

10%

2%

26%

21%21%

11.5%

11.5%

10%6%

40%

37%6%

17.5%

17.5%

7%

15%

34.5%34.5%

24%7%

26%

14%22%

10%

2%

26%

21%21%

11.5%

11.5%

10%6%

40%

37%6%

17.5%

17.5%

7%

15%

34.5%34.5%

24%7%

26%

14%22%

10%

2%

26%

21%21%

11.5%

11.5%

10%6%

40%

37%6%

17.5%

17.5%

7%

15%

34.5%34.5%

24%7%

^Strategic asset allocation as at 30 June 2011

Note: the asset allocation was the same at 30 June 2010

23

100%

100%

100%

100%

50%

50%

100%

100%

100%

100%

50%

50%

100%

100%

100%

100%

50%

50%

100%

100%

100%

100%

50%

50%

100%

100%

100%

100%

50%

50%

Asset Class optionsEach option invests in a single asset class

Performance results

25

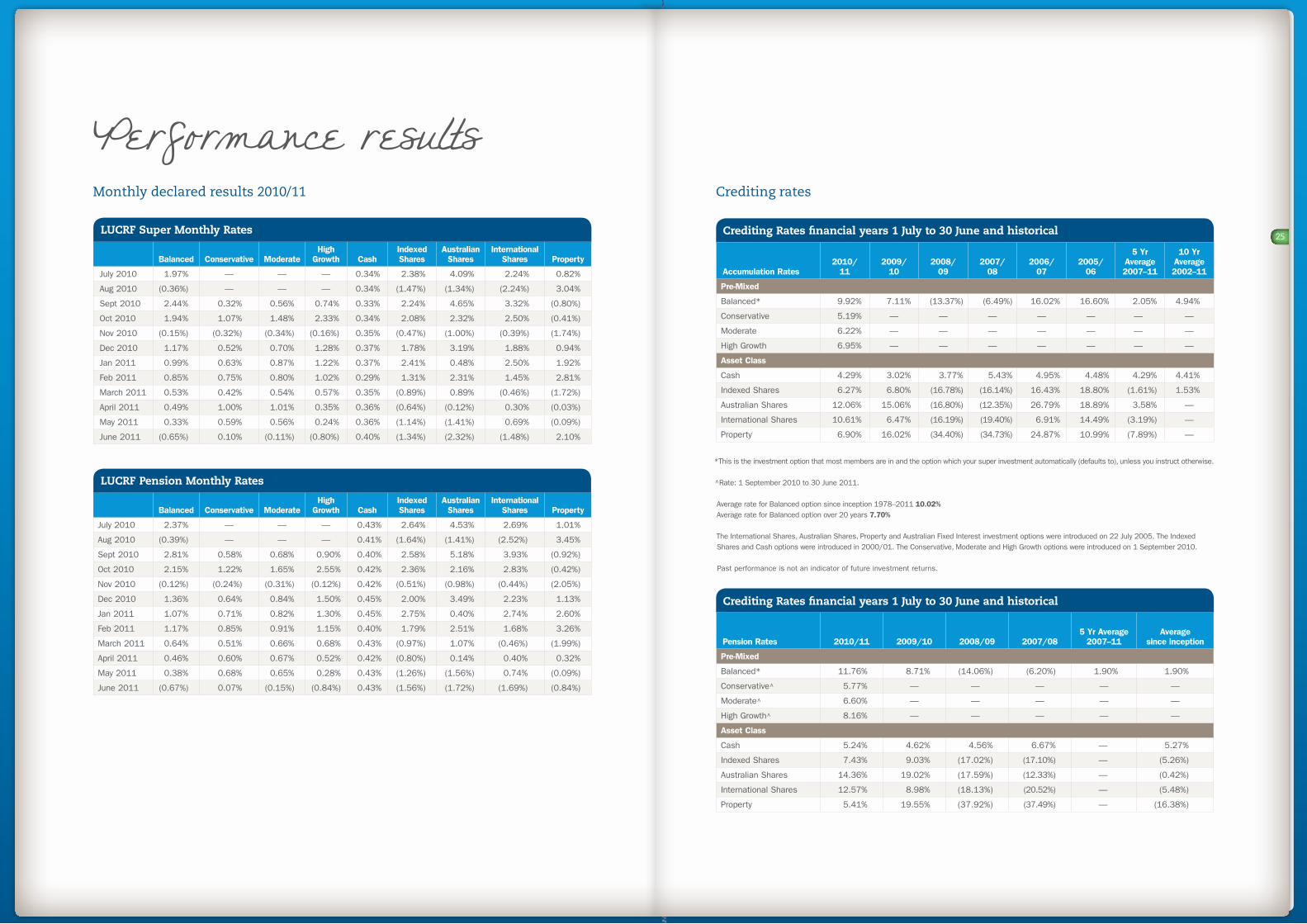

Monthly declared results 2010/11

*This is the investment option that most members are in and the option which your super investment automatically (defaults to), unless you instruct otherwise.

^Rate: 1 September 2010 to 30 June 2011.

Average rate for Balanced option since inception 1978–2011 10.02% Average rate for Balanced option over 20 years 7.70%

The International Shares, Australian Shares, Property and Australian Fixed Interest investment options were introduced on 22 July 2005. The Indexed Shares and Cash options were introduced in 2000/01. The Conservative, Moderate and High Growth options were introduced on 1 September 2010.

Past performance is not an indicator of future investment returns.

Crediting rates

Balanced Conservative ModerateHigh

Growth CashIndexed Shares

Australian Shares

International Shares Property

July 2010 1.97% — — — 0.34% 2.38% 4.09% 2.24% 0.82%

Aug 2010 (0.36%) — — — 0.34% (1.47%) (1.34%) (2.24%) 3.04%

Sept 2010 2.44% 0.32% 0.56% 0.74% 0.33% 2.24% 4.65% 3.32% (0.80%)

Oct 2010 1.94% 1.07% 1.48% 2.33% 0.34% 2.08% 2.32% 2.50% (0.41%)

Nov 2010 (0.15%) (0.32%) (0.34%) (0.16%) 0.35% (0.47%) (1.00%) (0.39%) (1.74%)

Dec 2010 1.17% 0.52% 0.70% 1.28% 0.37% 1.78% 3.19% 1.88% 0.94%

Jan 2011 0.99% 0.63% 0.87% 1.22% 0.37% 2.41% 0.48% 2.50% 1.92%

Feb 2011 0.85% 0.75% 0.80% 1.02% 0.29% 1.31% 2.31% 1.45% 2.81%

March 2011 0.53% 0.42% 0.54% 0.57% 0.35% (0.89%) 0.89% (0.46%) (1.72%)

April 2011 0.49% 1.00% 1.01% 0.35% 0.36% (0.64%) (0.12%) 0.30% (0.03%)

May 2011 0.33% 0.59% 0.56% 0.24% 0.36% (1.14%) (1.41%) 0.69% (0.09%)

June 2011 (0.65%) 0.10% (0.11%) (0.80%) 0.40% (1.34%) (2.32%) (1.48%) 2.10%

LUCRF Super Monthly Rates

Balanced Conservative ModerateHigh

Growth CashIndexed Shares

Australian Shares

International Shares Property

July 2010 2.37% — — — 0.43% 2.64% 4.53% 2.69% 1.01%

Aug 2010 (0.39%) — — — 0.41% (1.64%) (1.41%) (2.52%) 3.45%

Sept 2010 2.81% 0.58% 0.68% 0.90% 0.40% 2.58% 5.18% 3.93% (0.92%)

Oct 2010 2.15% 1.22% 1.65% 2.55% 0.42% 2.36% 2.16% 2.83% (0.42%)

Nov 2010 (0.12%) (0.24%) (0.31%) (0.12%) 0.42% (0.51%) (0.98%) (0.44%) (2.05%)

Dec 2010 1.36% 0.64% 0.84% 1.50% 0.45% 2.00% 3.49% 2.23% 1.13%

Jan 2011 1.07% 0.71% 0.82% 1.30% 0.45% 2.75% 0.40% 2.74% 2.60%

Feb 2011 1.17% 0.85% 0.91% 1.15% 0.40% 1.79% 2.51% 1.68% 3.26%

March 2011 0.64% 0.51% 0.66% 0.68% 0.43% (0.97%) 1.07% (0.46%) (1.99%)

April 2011 0.46% 0.60% 0.67% 0.52% 0.42% (0.80%) 0.14% 0.40% 0.32%

May 2011 0.38% 0.68% 0.65% 0.28% 0.43% (1.26%) (1.56%) 0.74% (0.09%)

June 2011 (0.67%) 0.07% (0.15%) (0.84%) 0.43% (1.56%) (1.72%) (1.69%) (0.84%)

LUCRF Pension Monthly Rates

Accumulation Rates 2010/

112009/

102008/

092007/

082006/

072005/

06

5 Yr Average 2007–11

10 Yr Average 2002–11

Pre-Mixed

Balanced* 9.92% 7.11% (13.37%) (6.49%) 16.02% 16.60% 2.05% 4.94%

Conservative 5.19% — — — — — — —

Moderate 6.22% — — — — — — —

High Growth 6.95% — — — — — — —

Asset Class

Cash 4.29% 3.02% 3.77% 5.43% 4.95% 4.48% 4.29% 4.41%

Indexed Shares 6.27% 6.80% (16.78%) (16.14%) 16.43% 18.80% (1.61%) 1.53%

Australian Shares 12.06% 15.06% (16.80%) (12.35%) 26.79% 18.89% 3.58% —

International Shares 10.61% 6.47% (16.19%) (19.40%) 6.91% 14.49% (3.19%) —

Property 6.90% 16.02% (34.40%) (34.73%) 24.87% 10.99% (7.89%) —

Pension Rates 2010/11 2009/10 2008/09 2007/085 Yr Average

2007–11Average

since inception

Pre-Mixed

Balanced* 11.76% 8.71% (14.06%) (6.20%) 1.90% 1.90%

Conservative^ 5.77% — — — — —

Moderate^ 6.60% — — — — —

High Growth^ 8.16% — — — — —

Asset Class

Cash 5.24% 4.62% 4.56% 6.67% — 5.27%

Indexed Shares 7.43% 9.03% (17.02%) (17.10%) — (5.26%)

Australian Shares 14.36% 19.02% (17.59%) (12.33%) — (0.42%)

International Shares 12.57% 8.98% (18.13%) (20.52%) — (5.48%)

Property 5.41% 19.55% (37.92%) (37.49%) — (16.38%)

Crediting Rates financial years 1 July to 30 June and historical

Crediting Rates financial years 1 July to 30 June and historical

Enquiries and complaintsEnquiries and complaints can be made in writing or verbally. If you wish to make a complaint in writing, please address correspondence to:

LUCRF Super Complaints Officer PO Box 211 North Melbourne VIC 3051

Complaints can be made by a Fund member, a previous member, a non-member spouse (re: Family Law split agreement), or from a dependant (beneficiary/ies) or legal personal representative of a deceased member. Responses from the Fund will be dealt with promptly and certainly within 90 days as required by legislation.

If you are not satisfied with our response or han-dling of a complaint, you may be entitled to lodge a complaint with the Superannuation Complaints Tribunal (SCT), which is a free service.

Superannuation Complaints Tribunal Locked Bag 3060, Melbourne VIC 3001 Telephone: 1300 884 114 Website: www.sct.gov.au

If your complaint is outside the jurisdiction of the SCT and you are not satisfied with the han-dling of your complaint, or you have not received a response within 90 days, you may be able to take your complaint to the Financial Ombudsman Service, which is also a free service.

Financial Ombudsman Service GPO Box 3, Melbourne VIC 3001 Telephone: 1300 780 808 Website: www.fos.org.au

The Australian Securities and Investment Service (ASIC) also has an infoline on 1300 300 630 which you may use to make a complaint and ob-tain information about your rights.

Government supervisionLUCRF Pty Ltd is the Trustee of the Labour Union Co-operative Retirement Fund (LUCRF Super) and complies with the requirements of the

Superannuation Industry (Supervision) Act 1993, the Corporations Act 2001 and other relevant legislation.

The Australian Prudential Regulation Authority (APRA) has approved LUCRF Pty Ltd as the holder of a Registrable Superannuation Entity Licence (L0002981) and LUCRF Super as a Registrable Superannuation Entity (R1067521).

An Australian Financial Services Licence was also granted to LUCRF Pty Ltd (AFSL No. 258481) by the Australian Securities Investment Commission (ASIC) which enables general superannuation advice to be provided. The Trustee is also approved to operate a non-cash payment facility (clearing house).

Identity fraudYou may have heard of identity fraud. It is when someone steals (or tricks you into providing) your personal details to commit financial fraud. While this seems to mainly occur with bank accounts (where certain undesirable people will use your personal details to access your accounts via phone, internet or writing bad cheques), your super could also be a target.

If you receive calls or emails requesting your personal details, please be aware that responding to this could leave you open to fraud. You should never provide your personal details to anyone.

Visit the ASIC MoneySmart website at www.moneysmart.gov.au for useful superannuation information and scam updates.

Reserves policyThe Trustee maintains three reserves. This makes no difference to the fees or charges you pay as a member of LUCRF Super.

Trustee ReserveThe difference between fees charged to members and the administration and investment expenses incurred in the management of the Fund are credited to the Trustee Reserve. This reserve is maintained to supplement funds required to meet future Trustee expenses.

Fund Administration ReserveThe after-tax value of any insurance rebate received and tax benefit received in the payment of insurance premiums are both credited to this reserve.

Earnings at the cash rate on reserve balances and on assets that support unpaid liabilities that cannot be directly referable to a member investment choice are also credited to this reserve. It is maintained to meet additional significant expenses of LUCRF Super and LUCRF Pensions.

Fund Operational Risk ReserveThis reserve is funded through rounding of the crediting rate process. It is maintained to meet unfunded liabilities as they arise during the administration and operation of the Fund.

Contribution arrears – what we doLegislation requires employers to pay contributions by certain due dates. When an employer fails to do this (once aware), the Fund endeavours to resolve these situations within a reasonable period.

The Fund identifies and follows up overdue contributions in writing (letter and email), phone calls or may also perform site visits to advise employers of arrears.

Indemnity insuranceThe Fund has taken out insurance to indemnify the Directors and legally responsible officers from loss resulting from any claim or wrongful act by the Trustee or any other party. The Directors are not indemnified against penalties or fine imposed by law as a result of negligence or dishonest conduct.

Transfer of benefits to an Eligible Rollover Fund (ERF)If no contributions have been received by LUCRF Super for over 12 months and a member account is below $500, the Trustee may elect to roll over the benefit to an ERF.

An ERF is a fund that can receive benefits from other superannuation funds for members who cannot be contacted or who do not respond to letters regarding payment of their benefits.

If a benefit is transferred to an ERF, any insurance cover will cease and all rights of membership of LUCRF Super cease. An ERF is not generally considered a suitable long-term investment vehicle for super.

The ERF nominated by the Trustee is called Australia’s Unclaimed Super Fund (AUSfund). If you need to contact AUSfund, call 1300 361 798 or write to:

AUSfund PO Box 2468, Kent Town SA 5071 Website: www.unclaimedsuper.com.au

Unclaimed moneyThe Trustee of LUCRF Super is required to transfer your entire benefit to the ATO as unclaimed money in certain circumstances. This will occur within four months of the end of each half-calendar year if:

• You reach the eligibility age of 65 years, your account has been inactive for two years or more and we have not had contact with you for five years; or

• You have died and the Trustee is unable to locate a beneficiary in order to pay your benefit (after reasonable endeavour); or

• You were in Australia as a temporary resident and you have not claimed your benefit after six months from your visa expiry or cancellation date; or

• You are a lost member of the Fund (because two items of mail we sent to you have been retuned and undelivered) and:

• The balance of your account is below $200, or

• We have not received any contributions for you within five years and it will not be possible to pay a benefit to you in the future.

Note: The Trustee relies on ASIC relief to the effect that it is not obligated to issue an exit statement to departed former temporary residents when a benefit is transferred to the ATO, however the information can be obtained upon request.

Financial StatementsAnd other information

27

Contact the ATO directly to claim your benefit.

Statement of financial position as at 30 June

2011 2010

$’000 $’000 $’000 $’000

Investments

Money Market Deposits and Other Investments $236,663 $267,720

Fixed Interest $57,883 $64,635

Australian Equities $1,646,264 $822,834

International Equities $710,504 $1,095,573

Derivatives $2,782 $9,110

Real Estate Investments $253,675 $2,907,771 $230,208 $2,490,080

Other assets

Cash at Bank $2,283 $2,982

Contributions Receivable $10,172 $15,000

Sundry Receivable $971 $836

Accrued Income $10,346 $7,292

Outstanding (Sales) Settlements $804 $2,581

Provision for Deferred Income Tax $16,150 $40,726 $21,046 $49,737

Total assets $2,948,497 $2,539,817

Less

Income Tax Payable ($16,433) ($7,153)

Benefits Payable ($1,509) ($1,516)

Outstanding (Purchases) Settlements ($7,512) ($4,988)

Sundry Payables ($6,391) ($4,239)

($31,845) ($17,896)

Net assets available to pay benefits $2,916,652 $2,521,921

Represented by: Liability for Accrued Benefits

Allocated to Members Accounts $2,892,454 $2,503,744

Investment Reserve $ $

Operational Risk Reserve $3,293 $1,396

Admin Guarantee Reserve (APRA) $500 $500

Expense Reserve $20,405 $2,916,652 $16,280 $2,521,920

Statement of change in net assets as at 30 June

2011 2010

$’000 $’000 $’000 $’000

Net assets available to pay benefits at start of year $2,521,920 $2,214,986

Interest Income $16,233 $13,834

Dividend Income $134,707 $63,546

Net Property Income $863 $669

Change in Market Value $129,820 $94,278

Other Investment Income $5,532 $287,155 $2,633 $174,960

Contribution revenue

Employer Contributions $255,946 $234,630

Member Contributions $13,782 $18,503

Transfer from Other Funds and Co-Contributions $89,606 $359,334 $75,997 $329,130

Other revenue

Other Revenue $654 $1,073

Group Life Proceeds $11,289 $11,943 $10,327 $11,400

Opening net assets plus revenue $3,180,352 $2,730,476

Less expenses and outgoings

Benefits paid and Payable ($161,243) ($126,425)

Group Life Premiums ($14,104) ($12,998)

Superannuation Surcharge Tax ($3) ($4)

Administration Expenses ($13,969) ($13,849)

Direct Investment Expenses ($22,493) ($18,231)

Income Tax Expenses ($51,888) ($263,700) ($37,049) ($208,556)

Net assets available to pay benefits at end of year $2,916,652 $2,521,920

Reconciliation of interest paid to member accounts for the year ended 30 June

2011 2010 2009

$’000 $’000 $’000

Investment Revenue $283,868.00 $174,959.00 ($319,360.00)

Other Income $1,559.00 $523.00 $.00

Tax Benefit on Administration & Investment Expenses $6,967.00 $6,479.00 $6,869.00

Insurance Rebate $654.00 $551.00 $500.00

Administration Fee Collected $11,899.00 $11,797.00 $12,013.00

$304,947 $194,309 ($299,978)

Outgoings

Administration Expenses ($13,969.00) ($13,849.00) ($18,387.00)

Member Benefit Protection ($1,634.00) ($1,747.00) ($3,841.00)

Direct Investment Expenses ($20,767.00) ($18,231.00) ($15,866.00)

Tax Credit (Payable) out of Investment Income ($20,194.00) ($7,350.00) $36,465.00

Movement from (to) Reserves ($4,802.00) ($4,136.00) $1,133.00

Total paid as interest to members $243,581 $148,996 ($300,474)

If you wish to obtain a copy of the auditor’s report and the full audited accounts, please contact us after 25 August 2011.

Financial Statements 2010/11

29

A big thank you !

To our members Claire, Shaun and Norm for sharing the story

of their journey with us.

31

Contact LUCRF Super

1300 130 780

This Annual Report dated August 2011 is issued by LUCRF Pty Ltd ABN 18 005 502 090 AFSL 258481 RSE Licence L0002981 as Trustee for the Labour Union Co-operative Retirement Fund (LUCRF Super) ABN 26 382 680 883 RSE Reg. R1067521. The information contained in this report is general in nature only and should be read in conjunction with your Annual Statement. It does not take into account your fi nancial situation, objective or needs, so you should look at your own fi nancial position and requirements before making a decision. Should you require advice that addresses your personal circumstances, please call us to speak to a qualifi ed LUCRF Representative. For more information on LUCRF Super, call 1300 130 780 or access our website www.lucrf.com.au for a copy of our Member guide (combined Product Disclosure Statement and Financial Services Guide), which should be considered before making a decision about the Fund.

LU

CR

F0

03

02

_2

60

81

1

Web: www.lucrf.com.au

E-mail: [email protected]

Post: PO Box 211 North Melbourne VIC 3051

Fax: (03) 9326 6907

An award-winning fund