140513 Commodity Strategy report - Macro Research...

51

Trading Strategy Commodity strategy report, May 13, 2014 A Commodity bust in slow motion In the midst of an unsynchronised commodity bust Supply wave is here after a decade of oil, gas and mining capex flurry Supply dynamics favour nickel, zinc and aluminium over copper and iron ore Supply disruptions hindered oil price gravidity but pressure increases

Transcript of 140513 Commodity Strategy report - Macro Research...

Trading Strategy

Commodity strategy report, May 13, 2014

A Commodity bust in slow motion

In the midst of an unsynchronised commodity bust

Supply wave is here after a decade of oil, gas and mining capex flurry

Supply dynamics favour nickel, zinc and aluminium over copper and iron ore

Supply disruptions hindered oil price gravidity but pressure increases

Contents

Summary and trading case 3

This commodity cycle in perspective 5

A mining bust in slow motion 8

Precious metals: gold value in the eye of the beholder 21

Western world steel rising from the ashes 25

Crude oil and natural gas – the boom of 21st century 29

Is a new bull market coming in commodities? 35

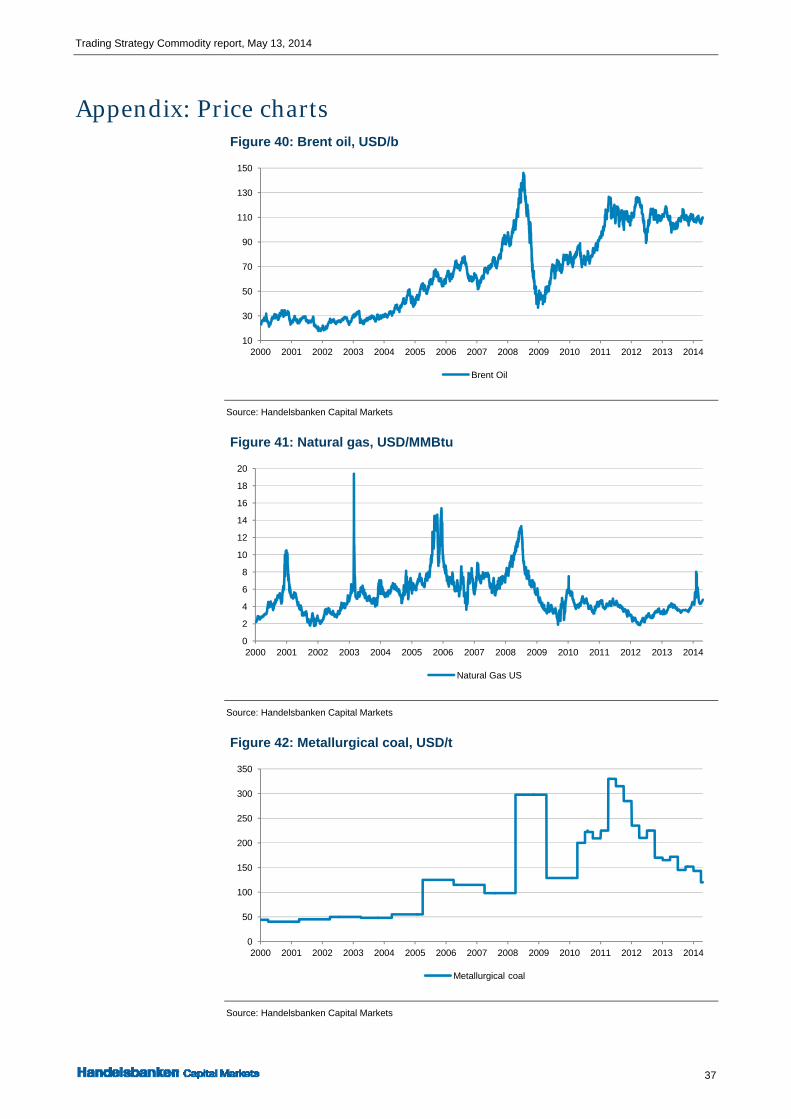

Appendix: Price charts 37

Appendix: Production and consumption charts 42

Disclaimers 50

Martin Jansson +46 (0)87012343 [email protected]

This report has been prepared solely on raw data

from Bloomberg and the Raw Materials Group,

and shows how the timing differences between the

decision to expand and production coming on

stream have a significant impact on metal prices.

We conclude that the wave of copper and iron ore

supply set to hit the market will suppress prices,

while aluminium, nickel and zinc have already

taken the pain. Oil production is reallocated from

ME to US, and pressure on OPEC will increase as

supply disruptions ease in ME.

Trading Strategy Commodity report, May 13, 2014

3

Summary and trading case We have analysed the last decade of booming commodity prices. After digging into 1,500 mining projects,

drilling down into the US shale revolution, and looking at years of supply disruptions in the Middle East, we

conclude that we are in the midst of an unsynchronised commodity bust, where supply will take the lead after

years of tracking intense commodity consumption in China. We expect that oil, iron ore, copper, zinc,

aluminium and nickel will all be priced on the marginal cost of production in the coming years.

Commodity prices no longer walk in tandem, conclusions: The step change in Chinese commodity demand is petering out. As the nation’s intensity of

commodity consumption normalises, we expect metal, oil and gas prices to be increasingly determined by supply dynamics, as supply has few other barriers to entry than capital and time on hand.

Zinc and nickel were filled with low hanging capex fruit, mostly brownfield expansions, even before the financial crisis, and are better balanced markets. These are also the first to hit a supply deficit again, starting with the nickel rally this year. Zinc supply is likely to become an issue, but our supply analysis indicates no shortage emerging until 2016.

Copper and iron ore have needed larger and more time-consuming greenfield projects to match demand. The current ballooning project pipeline will likely push prices of these commodities lower. In contrast to iron ore, copper projects have a high incentive price, meaning the price dive should be followed by a rebound back to current levels within a few years.

Aluminium is set to remain in a tight, flat range as the main input material; bauxite is not a hard rock mined raw material. It is in constant and abundant supply, meaning that bauxite prices have not come up as a result of the deficits that have driven the mining industry.

Falling input costs from lower iron ore prices work in steel producers’ favour and should help the bleeding steel industry to expand margins ahead, even though steel prices are set to fall by 10%. As a general topic ahead, we believe that we will see a relative power shift, where upstream stands to lose ground to downstream players.

The booming US shale production will likely continue to push worldwide energy costs down. Crude oil is set to fall in a scenario in which supply disruptions in the Middle East ease, but oil prices will have to remain relatively high to globalise the shale revolution and to bridge depleting US shale wells.

The platinum group metals stand out as being late-cycle in demand, where consumption intensity has yet to peak, while mining them is becoming increasingly complicated for various reasons.

Table 1: Price assumptions between now and 2018e

Source: Handelsbanken Capital Markets

Spot Low 2018 Low/spot 2018/spot

Iron ore 102 80 80 -22% -22%

Brent oil 108 90 95 -17% -12%

Copper 6 855 5 500 6 700 -20% -2%

Platinum 1 434 1 350 1 550 -6% 8%

Aluminium 1 773 1 800 2 000 2% 13%

Palladium 807 700 950 -13% 18%

Nickel 18 500 18 500 22 000 0% 19%

Zinc 2 050 2 000 2 500 -2% 22%

The mining spending

cycle is just about to

overshoot

Nickel is the first out

of the red; zinc next

in line to rally

Iron ore and copper

stand to lose

Lack of bottlenecks

keeps aluminium flat

Steel prices to fall on

lower iron ore

Oil set to fall when

supply disruptions

ease

PGMs to outperform

everything in the

long run

Trading Strategy Sector report, May 13, 2014

4

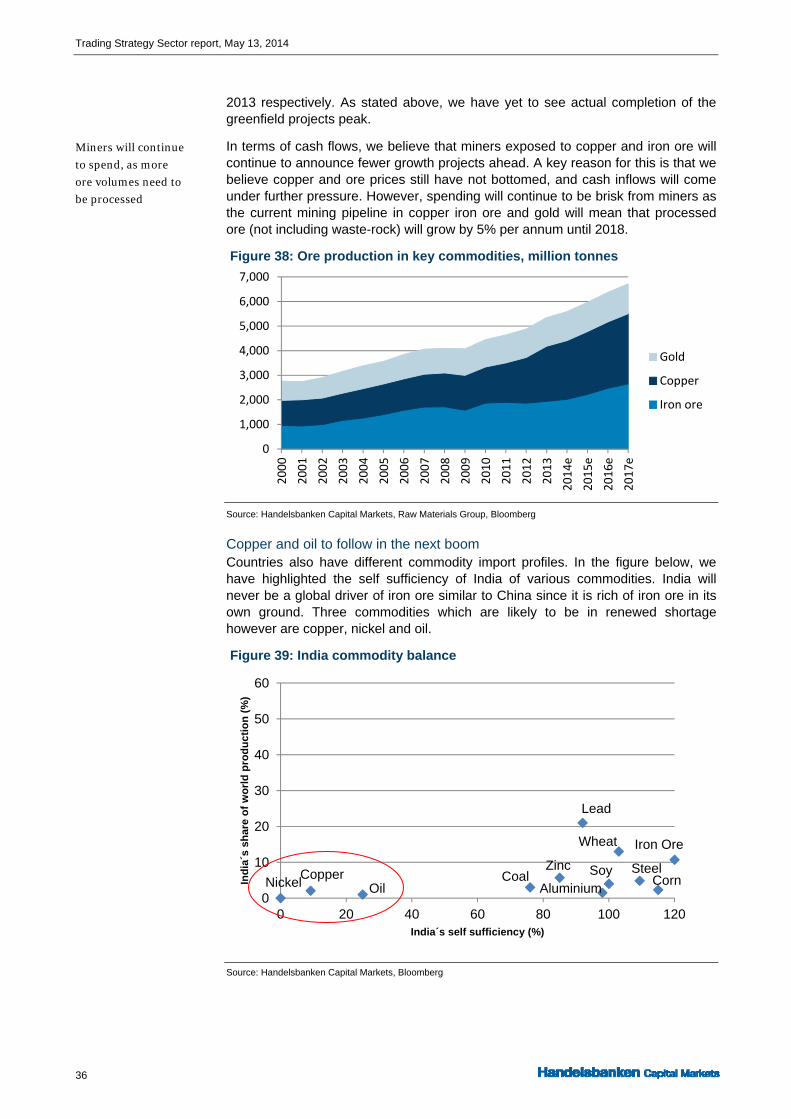

Mining project pipeline As a basis for this report, we have analysed the mining project pipeline consisting of more than 1,500 projects completed during the past decade or set to be completed until 2018. In the current pipeline we see the strongest annual supply growth in iron ore (7%), followed by copper (5%), aluminum (5%), zinc (4%) nickel (3%) and PGMs (0%). For the sake of supply/demand balances, we assume consumption growth of 4% for copper, iron ore, nickel, and zinc, and 5% for aluminium; growth rates in the past decade have amounted to 2.8 % for copper, 7.5% for iron ore, 5.5% for aluminium, 5.1% for zinc and 3.7% for nickel. Few macroeconomic analyses indicate that the coming five years will hold stronger commodity demand than during the past decade of strong Chinese growth featuring high commodity intensity.

Figure 1: Production growth projections for metals

Source: Handelsbanken Capital Markets

Trading case in the commodities universe

Brent: Put ratio spread. Buy 1 * June 2015 102 put, Sell 2 * June 2015 90 put

Premium = Pay USD 1.60

Max profit = USD 10.40

Breakeven = USD 100.40 and USD 79.60

Aluminium: Strangle. Sell 1 * June 2015 1,775 put, Sell 1 * June 2015 2,025 call

Premium = Receive USD 161/t

Breakeven = USD 1,614 and USD 2,186

Zinc: Call ratio spread. Buy 1 * June 2016 2,140 call, Sell 2 * June 2016 2,425 call

Premium = USD 0

Max profit = USD 285/t

Break even = USD 2,710/t

Copper:

A) Knock In Call, Buy 1 * Jun 2015 KI 6,000 call with 5,800 barrier

Premium = USD 70 (vs. USD 1000 for vanilla call)

B) Short copper outright

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2014

2015

2016

2017

2018

YoY

cha

nge

IO Cu Al Zn Ni PGM:s Demand @ 4 %

More than 1,500

mining projects

analysed

We assume

consumption growth

of 4-5%

Trading Strategy Commodity report, May 13, 2014

5

This commodity cycle in perspective Extractive industries are boom/bust industries and are by nature caught in a constant struggle between

supply and demand dynamics. After two decades with buyers having the upper hand in pricing and

commodity prices being under pressure, China emerged as the largest single commodity consumer ever in

the early 2000s. With few barriers to entry other than capital and time on hand, resource industries

responded by expanding; this report digs into the supply side of the equation.

The third commodity boom in a century Since the late 19th century, there have been three golden periods of strong economic growth and high demand for minerals. The first commenced in the late 1800s with the industrial revolution in Europe and the USA. That cycle had many similarities with what is playing out in China today, with urbanisation and rapidly rising standards of living as main drivers. The second boom occurred after the Second World War with the reconstruction of Europe and the strong economic development in Korea and Japan. In 1950-1973, crude oil prices were effectively controlled by the Seven Sisters and remained nearly constant in real terms. The second boom ended along with the oil crisis in 1980. From the first oil crises in 1973-1974 until the early 1980s, oil prices skyrocketed, largely as a result of increased market control by the newly formed OPEC price cartel.

In 1980, real oil prices also started to decline after a decade of intensive exploration and new discoveries of reserves in non-OPEC countries such as Angola (today an OPEC member), Mexico, Norway, the former Soviet Union and the UK. All these new sources reduced the market control of OPEC from 53% in 1974 to 30% in 1985. The following two decades (1980s and 1990s) of depressing oil prices and, in total, three decades of depressing metal prices (1973-2003) had important consequences and forms the booming period of 2000s, when China entered the stage as the largest commodity-buying nation in history.

Figure 2: Real prices of crude oil and copper 1950-2013

Source:Bloomberg, Macrobond, Handelsbanken Capital Markets

China has echoes of

the industrial

revolution in Europe

and the US

In 1980, oil prices

started to decline

after non-OPEC

discoveries

Current boom came

after two decades of

price deflation and

low industry

spending

Trading Strategy Sector report, May 13, 2014

6

The Chinese derivatives and upstream/downstream mismatch

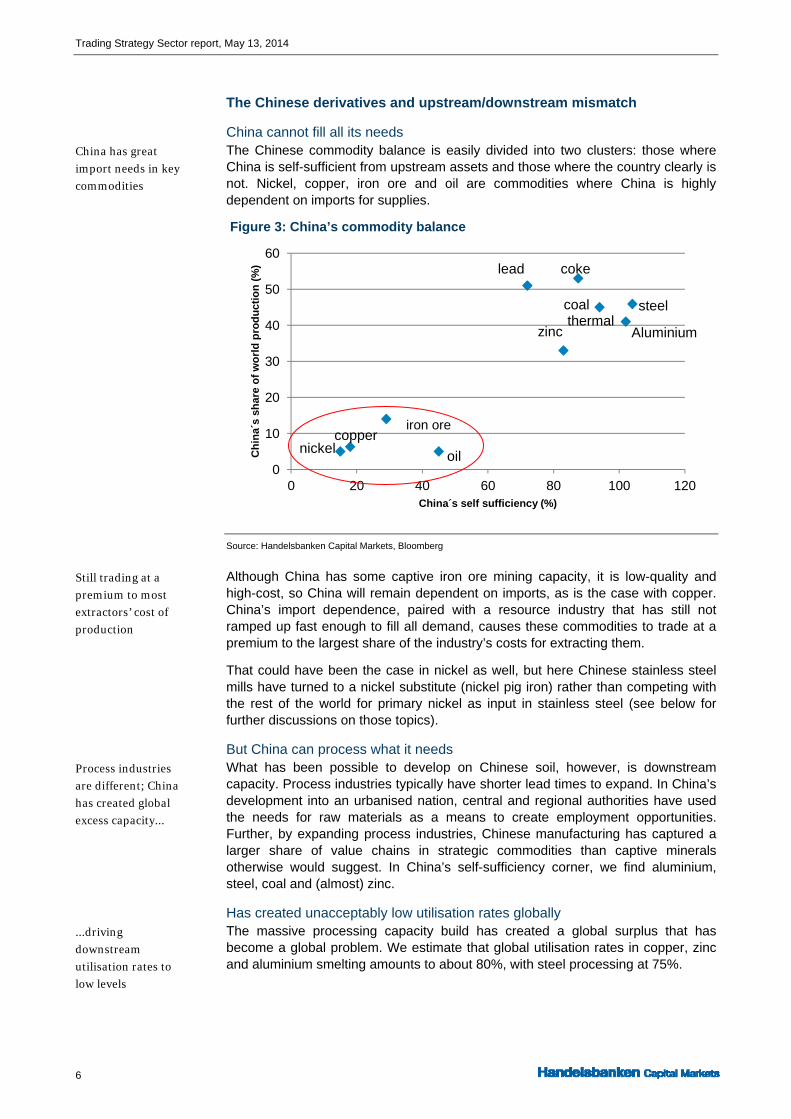

China cannot fill all its needs The Chinese commodity balance is easily divided into two clusters: those where China is self-sufficient from upstream assets and those where the country clearly is not. Nickel, copper, iron ore and oil are commodities where China is highly dependent on imports for supplies.

Figure 3: China’s commodity balance

Source: Handelsbanken Capital Markets, Bloomberg

Although China has some captive iron ore mining capacity, it is low-quality and high-cost, so China will remain dependent on imports, as is the case with copper. China’s import dependence, paired with a resource industry that has still not ramped up fast enough to fill all demand, causes these commodities to trade at a premium to the largest share of the industry’s costs for extracting them.

That could have been the case in nickel as well, but here Chinese stainless steel mills have turned to a nickel substitute (nickel pig iron) rather than competing with the rest of the world for primary nickel as input in stainless steel (see below for further discussions on those topics).

But China can process what it needs What has been possible to develop on Chinese soil, however, is downstream capacity. Process industries typically have shorter lead times to expand. In China’s development into an urbanised nation, central and regional authorities have used the needs for raw materials as a means to create employment opportunities. Further, by expanding process industries, Chinese manufacturing has captured a larger share of value chains in strategic commodities than captive minerals otherwise would suggest. In China’s self-sufficiency corner, we find aluminium, steel, coal and (almost) zinc.

Has created unacceptably low utilisation rates globally The massive processing capacity build has created a global surplus that has become a global problem. We estimate that global utilisation rates in copper, zinc and aluminium smelting amounts to about 80%, with steel processing at 75%.

0

10

20

30

40

50

60

0 20 40 60 80 100 120

Ch

ina´

s sh

are

of

wo

rld

pro

du

ctio

n (

%)

China´s self sufficiency (%)

iron ore

steel

copper

oil

zinc Aluminium

nickel

lead coke

coalthermal

China has great

import needs in key

commodities

Still trading at a

premium to most

extractors’ cost of

production

Process industries

are different; China

has created global

excess capacity...

...driving

downstream

utilisation rates to

low levels

Trading Strategy Commodity report, May 13, 2014

7

Lack of market concentration creates lack of industry discipline The upstream resources markets are fragmented. On aggregate, no single commodity is concentrated to the extent that supply could be controlled to alter the supply/demand equation. The implication of a lack of concentration combined with the lack of differentiating factors in end products (commodities) means that there is a lack of industry discipline; hence, each operator always strives to optimise its own outcome.

The exception here is oil, where OPEC controls 36% of production, enabling the cartel to act as one single producer. Iron ore was on the verge of becoming concentrated in 2010 when BHP Billiton and Rio Tinto, two of the top iron pre-producers in the world, attempted to merge their Australian iron ore assets. However, the transaction was axed after anti-competition complaints from regulators and top customers, including China, as the combined entity would have controlled over 30% of global seaborne trade in iron ore.

Figure 4: Market concentration in various minerals, percent

Source: Handelsbanken Capital Markets, Raw Materials Group

The highest market concentration is found among the platinum group metals (PGMs). The main reason for that relative concentration is geological. PMGs are mined in Russia and at harsh conditions in South Africa. Shafts deeper than 3,500 metres with temperatures of up to 70°C and high rock pressure keep many miners from entering the space. Among the most fragmented markets is coal. 75 % of all coal is mined in Asia or FSU. Coal is easy to mine and abundant; low mechanisation has made it easy for smaller and less sophisticated miners to enter the market. Copper and iron ore are the most capital-intensive metallic minerals. Important barriers to entry here are access to funding and complicated infrastructural requirements, an increasingly important factor as miners must go more remote as the lowest hanging fruits are gone.

Commodities have a cost of carry and lack forward-looking abilities In a fragmented industry with commoditised end products and long lead times between the commencement of production and actual output, the supply side should be predictable, as the barriers for every project are known. Given that commodities have a cost of carry and that spot pricing rarely factors in future events, long-term prices will be set by supply. As presented above, we believe that we are on the downward slope of a supply-driven commodity downturn peaked in 2011. As prices fall, spending from resource companies dries up as cash flow yields crumble, paving the way for the next boom, which will occur once demand again exceeds supply from an under-invested industry.

Upstream markets

are fragmented and

lack industry

discipline

Coal most

fragmented, PMG:s

most concentrated

Extractive industries

are boom/bust

industries

Trading Strategy Sector report, May 13, 2014

8

A mining bust in slow motion The mining industry has now spent more than a decade on heavy investments. The theme “China buys what

China needs” has been the driver. With high price premiums over the marginal cost of production,

investments in many mining projects have displayed an irresistible internal rate of return (IRRs) on paper.

However, we maintain that the price cycle for metals such as zinc and nickel peaked in 2006-07 and that

copper and iron ore are merely lagging that trend. In our view, the lag is due to commodities filling demand

on brownfield investments, while copper and iron ore will continue to see price deflation as projects come on

stream. As argued and illustrated below, we believe we are in a commodity bust that is playing out in

unsynchronised slow motion and that there is more downside in key commodities, while aluminium, zinc

and nickel have already passed bottom levels.

Working through base metals, iron ore supply side; this is what we expect The entrance of China as a commodity consumer caused a commodity boom across all assets, although more in some than others. We have examined the mining expansion pipelines for the coming five years for iron ore, coking coal, copper, nickel and zinc (precious metals are discussed in later sections). We draw the following four conclusions:

Iron ore is likely to see prices decline towards USD 80/tonne, as the project pipeline is too large to be absorbed at current prices

Copper is likely to see prices decline to USD 5,500/tonne, as abundant supplies will need to be absorbed before there is any renewed shortage

Zinc is in ample supply and is likely to trade at prices of USD 2,100/tonne, +/- USD 200, for the coming two years, only to see prices rise thereafter on an emerging supply shortage

Nickel has entered a period of supply shortage after Indonesia banned exports of nickel ore to China. Prices are likely to drift towards USD 25,000/tonne without the NPI industry in China before it falls back as these levels will trigger new supply.

Aluminium has moved close to, or into deficit this year after some major producers suspended operations due to poor profitability. This action has lifted the price, but any sustained price rallies will trigger capacity to come back on stream, though we foresee a flat, tight trading interval of USD 1,800-2,000/tonne during coming years.

Chinese metal consumption normalising History suggests that a country’s consumption of metal typically grows in line with per capita income until that figure reaches USD 15-20,000. China now has more than 1.3 billion inhabitants. The country’s urbanisation rate has exploded, with the coastal areas setting the pace. Chinese incomes, property prices and standards of living now resemble those of many other developed economies. The western parts of China are still less developed, but with a large share of China now urbanised, the intensity of commodity usage has drifted lower. In Figure 5 we illustrate how China’s consumption growth of various metals and oil has fallen below one as a ratio to GDP growth, meaning commodity demand is now growing slower than the economy in general. As China now aims to curb structural and investment spending in an attempt to develop a more dynamic, consumer-driven economy, it is likely that the intensity of commodity consumption will continue to cool.

Four high-conviction

conclusions

The intensity of

commodity usage

has drifted lower in

China

Trading Strategy Commodity report, May 13, 2014

9

Figure 5: Chinese consumption intensity of commodities

Source: Handelsbanken Capital Markets, Bloomberg, Macrobond

Difference in competitive position mapped in the cash-cost curve Miners have few or no competitive advantages in what they produce, but rather in where, how and with what they produce it. Miners’ operating expenses are fixed at 70-80%, which means that miners will always operate at close to full capacity. Differentiating factors for cash costs in a mine are head grades, geology, mining method, FX and, not least, the occurrence of by-products.

The cash-cost curve of a metal is illustrated in a bar chart with aggregated output from all mines in the respective universe. The width of each bar represents the annual output from a specific mine, while the height of the same bar illustrates the cash costs for extracting the metal from the same mine. The mines furthest to the right in the supply curve are those with the poorest finances; as the least competitive miners, they should be the first to close once prices fall.

The steeper the cash-cost curve, the higher the fall Early in a mining cycle, when demand and prices rise, brownfield projects show the easiest and fastest profitability because they are low-cost and quick to complete. To the extent that brownfields are not sufficient to meet demand, miners start greenfield projects. These are typically larger, more costly and take longer to complete, as infrastructure spending is always required, but greenfields have the benefit of often being large-scale and cost-efficient to operate; hence, a newly-built mine may well end up in the first (most competitive) quartile on the cash-cost curve.

In boom markets and early in the bust of a metal cycle, cash-cost curves tend to be steeper. High-cost swing producers earn a decent living from the supply deficit that makes their output needed and defines the marginal pricing of the metal. Through the cycle, and as more and larger greenfield projects lower down in the cash-cost curve are completed, high-cost mines tend to constitute abundant supply and fall victim to the early stage of a bust. As these mines are forced to close, very small changes in excess supply will mean sharp drops in prices as the cash-cost curve flattens out and excess returns diminish.

Greenfields larger and completion lagging A mining boom typically commences with the number of completed brownfields rising and ends with the number of completed greenfields declining. Our study clearly indicates that we are on the verge of seeing greenfield declines materialising. Here, we illustrate 1,458 mining projects that were completed between 2000 and 2013:

There is no industry

discipline; miners

will always operate

at full capacity

A mining boom

starts with

brownfield

expansions

Cash-cost curves

tend to be steep;

swing producers

make money

Brownfield

expansions are

quicker to respond

Trading Strategy Sector report, May 13, 2014

10

Figure 6: Completed mining projects, 2000-13

Source: Handelsbanken Capital Markets, Raw Materials Group

The charts illustrate the dynamics of brownfields being early to complete and generally being lower in value than greenfields. Shorter lead times in completing brownfield projects mean that the trend in completing such projects is better matched with the price cycle. Completed brownfield expansions rose in 2004 and in 2010, while the completed number of greenfields has been rising over the past two years of declining metal prices, after a slow start.

The average size of a brownfield project is currently USD 430m versus greenfield projects with an average total spending of USD 787m; this compares with respective costs of USD 75m and USD 143m 10 years ago. In 2013, finalised copper greenfield projects accounted for 50% of mining spending in finalised projects, up from 20% in all other years since 2000. Gold accounts for a steady 20%, without any trend over the period. Nickel has had a few substantial greenfield projects with huge budget overruns and reached 30% of greenfield spending in 2010 as a high mark. Iron ore accounts for less than 15% of finalised projects, as these are larger in size and take longer to develop; most greenfield projects are still to be completed and the spending flurry has not yet occurred.

Figure 7: Indexed commodity prices, 2000-14

Source: Handelsbanken Capital Markets, Bloomberg

0

5

10

15

20

25

30

0

10

20

30

40

50

60

70

80

90

100

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Bill

ion

US

D

Capex finished greenfield Capex finished brownfields

Number of finished greenfield Number of finished brownfield

Brownfields better

matched with the

price cycle

Finalisation of

copper greenfields

accounted for 50% of

mining investments

in 2013

Iron ore and copper

prices lagging

Trading Strategy Commodity report, May 13, 2014

11

Iron ore: a bust in the making

Excess capacity is coming on stream Global iron ore markets currently produce about 1.9 billion tonnes, with more than 60% of that volume seaborne (i.e. exported from producing countries to consuming countries). China is by far the largest buyer of seaborne ore. Although there is a pick-up in demand from most regions in the world, we believe that China will remain the driver of iron ore demand in the coming five years, as in excess of 60% of seaborne demand comes from China. The growth rate that we assume in seaborne growth ahead is 4%, which is well in line with what the China Iron and Steel Association (CISA) expects in China.

In our estimates, an iron ore surplus will materialise by 2015. We base this on a conservative iron ore supply scenario, where we just assess the number of iron ore projects that have already obtained financing and necessary permits and are in the process of being completed.

When looking at the pipeline of iron ore projects, we note that this surplus would last through to 2020. Assuming that high prices linger for a few years more, we note that a number of still-unfunded projects could intrude into the market and kill prices.

Figure 8: Mismatch between iron ore supply and demand

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

Prices should approach USD 80/tonne The cash-cost curve for iron ore displays the typical steepness in the fourth quartile of a commodity that has not reached excessive supply volumes. The low-grade and small-scale Chinese mines generally have higher costs, while traditional iron ore regions Brazil and Australia are found in the lower quartiles.

Our analysis of 40 new iron ore projects shows an average cash cost of USD 48/tonne (after deducting USD 20 and USD 7 respectively for a pellets premium and lump premiums over fines, and adding shipping costs to China from site), meaning that large new greenfield projects end up in the first and second quartiles. The average production cost in China is close to USD 120 USD/tonne and the cash-cost for current supply excluding Chinese producers is USD 63/tonne. New iron ore supply will be dominated by Australia, with 57% of new supply coming from that country by 2018. Brazil's share of new supply will be steady, ranging between 17-22% during the next five years.

0

0

0

1

1

1

1

1

2

2

2

Mt Iron ore

Demand 4% CAGR

Production

Financed new supply

Not Financed new supply

Seaborne iron ore

demand at 4% CAGR

ahead

Iron ore to go into

surplus in 2015

It could last through

to 2020

Fourth-quartile

mines have high

cash-costs

New projects will

end up in the first

and second quartiles

Trading Strategy Sector report, May 13, 2014

12

Besides Chinese, Brazilian and Australian mines, a large number of high-cost mines refine and sell higher-grade products such as iron pellets. These miners, including LKAB, live off the premiums for the higher value added that they deliver.

Figure 9: Iron ore supply cash-cost curve, 2013 and 2018 (seaborne growth)

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

The impact of new capacity expansions will be that high-cost swing producers that have decent earnings at current prices (the 2014 average to May has been USD 120/tonne) will be forced to close and prices will fall along the cash-cost curve. In the assumption above of a 4% CAGR in the consumption of seaborne ore, demand will be lower than two billion tonnes, meaning that iron ore industries are heading for severe supply abundance in the coming years. Judging from the cash-cost curve above, that would imply iron ore prices in the range of USD 80/tonne.

Chinese steel mills will be happy to see local ore mines go bust The current volume of Chinese iron ore imports are approaching 800 million tonnes per annum and sourcing from domestic mines amounts to 220 million tonnes. At the latest 12-month price of USD 125/tonne, the value of these imports stands at USD 100bn; in addition, Chinese steel plants spend another USD 30bn on locally sourced ore. Assuming that the Chinese mines are scrapped in our price scenario, the Chinese would increase their dependence on seaborne markets, which may seem somewhat counterintuitive for Chinese consumers to applaud.

However, Chinese mines produce low-grade ore high in impurities. With the steel fleet being upgraded and modernised in China, the need for higher-quality feed rises. Additionally, the total bill for Chinese ore consumption would fall from USD 130bn to USD 90bn as iron ore prices decline to USD 80/tonne. Chinese mines have played a role not only as local sourcers, but they have also helped keep prices at a level where iron ore miners worldwide have run head-over-heels to create a future surplus in ore markets.

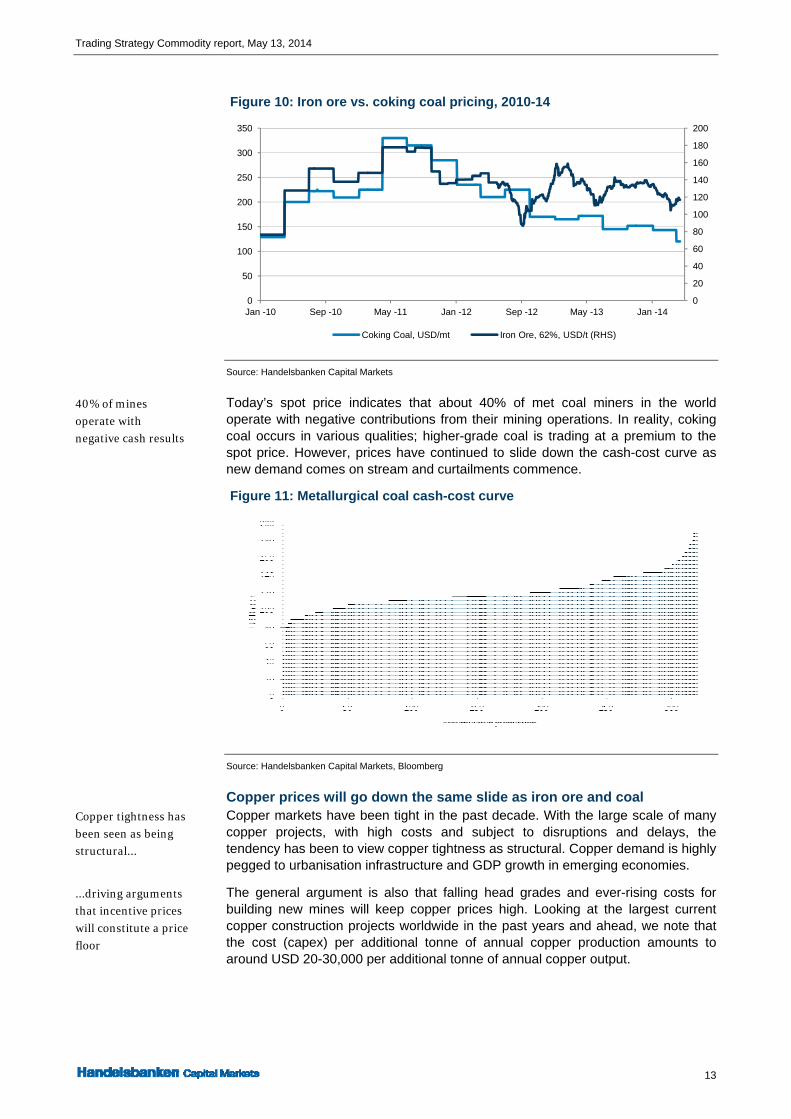

Metallurgical coal price has already collapsed Metallurgical coal, which is used in blast furnaces in the steel-making process, has gone through a price bust similar to what we expect to see for iron ore. Met coal mining is typically done in non-complex open mines, and expansions to meet demand in the past decade have been faster than for iron ore. In the past three years, coking coal prices have been under severe structural pressure: prices fell to multi-year lows after the supply wave hit the markets. Looking ahead in 2014, some 13 million metric tonnes of incremental met coal supply will hit the market, representing 4.5% of seaborne trade.

Prices could trend

down the curve to

USD 80-90/tonne

Chinese steel mills

have will need to

turn to more

imports…

…but will save USD

40bn by doing so

Met coal price has

already collapsed

Trading Strategy Commodity report, May 13, 2014

13

Figure 10: Iron ore vs. coking coal pricing, 2010-14

Source: Handelsbanken Capital Markets

Today’s spot price indicates that about 40% of met coal miners in the world operate with negative contributions from their mining operations. In reality, coking coal occurs in various qualities; higher-grade coal is trading at a premium to the spot price. However, prices have continued to slide down the cash-cost curve as new demand comes on stream and curtailments commence.

Figure 11: Metallurgical coal cash-cost curve

Source: Handelsbanken Capital Markets, Bloomberg

Copper prices will go down the same slide as iron ore and coal Copper markets have been tight in the past decade. With the large scale of many copper projects, with high costs and subject to disruptions and delays, the tendency has been to view copper tightness as structural. Copper demand is highly pegged to urbanisation infrastructure and GDP growth in emerging economies.

The general argument is also that falling head grades and ever-rising costs for building new mines will keep copper prices high. Looking at the largest current copper construction projects worldwide in the past years and ahead, we note that the cost (capex) per additional tonne of annual copper production amounts to around USD 20-30,000 per additional tonne of annual copper output.

0

20

40

60

80

100

120

140

160

180

200

0

50

100

150

200

250

300

350

Jan -10 Sep -10 May -11 Jan -12 Sep -12 May -13 Jan -14

Coking Coal, USD/mt Iron Ore, 62%, USD/t (RHS)

40% of mines

operate with

negative cash results

Copper tightness has

been seen as being

structural...

...driving arguments

that incentive prices

will constitute a price

floor

Trading Strategy Sector report, May 13, 2014

14

Figure 12: Capex (‘000 USD) per additional tonne of annual production

Source: Handelsbanken Capital Markets, Bloomberg

Assuming an average 15-year depreciation term, we would need to add USD 1,300-2,000/tonne of production costs to cover both capex and operating costs. With this argument, it would be fair to assume that copper miners will build new mines only if prices remain above USD 6,000-6,700/tonne. Over time, this is a fair assumption. The incentive price point where miners spend is highly relevant for pricing as long as supply is tight; but when excess supply emerges, the marginal level of suffering swings into focus. As that happens, the relevant questions are which mines will close and when.

Industry participants have taken action, but it is not enough Comparing the pipeline of the 2011 copper cash-cost curve at the price-cycle peak (looking forward to 2018) to the current cash-cost curve, we note that projects have been put on hold. The pipeline has decreased by 1.6m tonnes of copper, which is equivalent to 20% of the 2011 pipeline. Projects scrapped or postponed are large-scale ones, including Rieko Diq, Tampakan and Olympic Dam.

Figure 13: Copper pipeline to 2018 planned in 2011 (scrapped in red)

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

A 20% decrease in the pipeline is substantial; however, the main issue as we see it is that the projects scrapped are those furthest from generating cash flow (i.e. greenfield projects that have not been started or have barely begun). Hence, although these scrapped projects do wonders for production in 2017e-18e, they do

0

5

10

15

20

25

30

Lum

wan

a

Pin

to V

alle

y

Mic

hiqu

illa

y

Kan

suki

Toq

uepa

la

Kan

sans

hi S

ulfid

e

Bue

navi

sta

Min

e

Put

hep

Peb

ble

Sen

tinel

Nok

omis

Ant

amin

a

Los

Bro

nces

Inca

de

Oro

Eag

le

La G

ranj

a

Que

llave

co

Esp

eran

za E

xpan

sion

Las

Bam

bas

Can

aria

co N

orte

Tam

paka

n

Sie

rra

Gor

da

El T

esor

o

Rek

o di

q

Aqu

a R

ica

Frie

da R

iver

Cob

re P

anam

a

Oyu

Tol

goi

Ant

ucoy

a

Gal

ore

Cre

ek

Tor

omoc

ho

When excess supply

emerges, cash-cost

curves set prices

Copper projects have

been scrapped

…but projected

output from those

were too far out to

matter now

Trading Strategy Commodity report, May 13, 2014

15

little to mitigate the supply wave in 2014e-15e. Rather than smoothing booms and busts, the scrapped projects may well pave the way for the next copper price boom by limiting supply. But before we see any such boom, we believe that there is all the reason in the mining world to see a copper price bust.

The problem is at the top of the cash-cost curve As with iron ore, the fourth quartile of the copper cash-cost curve is steep and the marginal cost of copper production rises fast. As in most mine segments, capex for new greenfields is high due to more remotely-located mineral deposits with poor infrastructure. However, operating expenses are quite similar to those mines operating today and relative cash costs are determined by factors such as the occurrence of by-products. Hence, for copper and iron ore, new mines do not end up solely in the fourth quartile; new mines do not push the cost-curve higher, they merely extend it, making the slope of the curve flatter (new projects in green below).

Figure 14: Copper supply cash-cost curve, 2013 and 2018

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

Copper surplus between 2014 and 2017; price decline expected Copper demand averaged 2.8% growth in the past decade, primarily driven by China. Comparing the supply growth in 2014-18, we see copper swinging into surplus in 2014. Based on the cash-cost curves above, we expect copper prices to decline to USD 5,500/tonne in 2015 and 2016.

Figure 15: Copper surplus mounting after decades of spending

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

10

12

14

16

18

20

22

24

26

Mt Copper

New mine supply

Demand 4% CAGR

Production

The slope of the 4th

quartile copper cash

cost curve is steep

making downside

high

Copper expected at

USD 5,500/tonne

Trading Strategy Sector report, May 13, 2014

16

In the current pipeline, we see this surplus lingering beyond 2018. As noted above, the copper industries have been responsive in scrapping expansion plans. Unlike in iron ore, surplus in copper is not structural but more temporary in nature; as copper prices decline, we expect that postponed projects will aid the supply/demand balance and that incentive pricing again will be a reasonable floor for long-term assumptions, which we expect to be some USD 6,700/tonne from 2018 and onwards.

The Chinese copper financing trade has merely delayed the price decline A topic that normally emerges parallel to discussions of lower growth in Chinese copper consumption is the Chinese copper financing trade (CCFT). In the CCFT, copper is used as collateral when cheap loans are imported from offshore financial markets to mainland China. There are various estimates on how large these copper positions are and how much copper is actually tied up in these trades.

Our understanding is that a borrower must have a warehouse warrant of some type in China, meaning that the maximum tonnage that can be tied up in this trade is a million tonnes of copper. The inventory build in Chinese bonded warehouses coincides with copper markets moving from contango to backwardation, as selling pressure occurs when physical holders hedge positions on the future curve to eliminate copper price risk in the trade.

Figure 16: Imports push copper curve from contango to backwardation

Source: Handelsbanken Capital Markets, Bloomberg

The Chinese State Administration for Foreign Exchange (SAFE) has expressed that this type of asset-backed currency inflow should cease. If and when this occurs, excess supply is likely to be released and have a one-off effect on prices. Our view is that the CCFT has delayed the slide in copper prices, as markets without this artificially-created demand would have been exposed to higher tonnage on the supply side. This demand has most likely contributed to delaying the impending growth of supply.

Nickel has been sliding down the curve for two years Along with copper, nickel is one of the strategic commodities where China has insufficient amounts of domestic reserves to fill its needs; thus, China is a major importer of nickel. In recent years, China has expanded its imports of low-grade iron ore with high nickel content, primarily from Indonesia and to some extent from the Philippines. This ore has become the main feedstock in Chinese stainless steel production and has substituted refined nickel as input. The nickel ore from

Surplus mounts in

2014-17

Chinese copper

financing trade plays

its part

Could tie up to a

million tonnes of

copper

Price risk on the

downside if CCFTs

are banned

Nickel pig iron killed

nickel prices

Trading Strategy Commodity report, May 13, 2014

17

Indonesia contains 1.8-2% nickel and 15-20% iron, which is ideal for the electric arc furnaces common in Chinese stainless steel manufacturing.

Figure 17: China nickel import by source

Source: Handelsbanken Capital Markets, Bloomberg

The nickel pig iron from Indonesia has had two main effects on global markets:

The substitution of refined nickel has caused mine supply to exceed demand, leading to nickel prices falling to USD 14,000, where 30% of miners are cash-cost negative

Chinese stainless steel producers enjoy a cost benefit of approximately 10% over western-world stainless steel producers from low cost feed

Hence, nickel prices collapsed in what seems like typical excess supply but in fact, substitution played a major role in creating this supply/demand imbalance.

Indonesians want a greater piece of the pie In January 2014, the Indonesian government imposed a ban of exports of unrefined nickel ore. The aim is to force miners to build nickel smelting and refineries in Indonesia in order to maintain their mining licences, thus giving the Indonesia a larger share of the value chain. The export ban has been discussed for some time and most Chinese pig iron producers held ore stocks of up to six months of production. Nevertheless, Chinese steel producers are eating through their stockpiles of ore, and they are now left with the option to either buy refined nickel or source scrap from global markets. While nickel pig iron is priced in local Asian markets, refined nickel is priced on the LME, meaning that nickel prices should find a new equilibrium as the stainless industry in China is reshaped (discussed further below).

Tight supply to drive prices higher The supply pipeline in nickel is tight. In recent years nickel pig iron-based stainless steel production has deteriorated the interest to spend on new expansions.

Ban on ore exports

from Indonesia

Tightening refined

nickel markets

Trading Strategy Sector report, May 13, 2014

18

Figure 18: Nickel among the tightest metals ahead

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

We expect that refined nickel consumption will start eating into inventories at LME already in 2014, as stockpiled Indonesian ore in China is consumed and the market moves from surplus to deficit. With nickel pig iron moving largely out of the picture, nickel sourcing will occur to a greater extent from refined nickel or scrap, driving prices higher.

Zinc is the metal where a rally may be looming Zinc as a metal constitutes 3-4% of the total value of mined metals. Being minor and often mined in smaller mines with few economies of scale, it has not attracted interest from major miners. Prices have been in steady decline since the peak in 2006 and with inventories being high, the pipeline has become somewhat muted. In addition to this, we expect that a number of mines will be depleted in the coming years, mitigating the expansions that we know of.

Figure 19: Zinc has a few more years before reaching a deficit

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

At current prices, we see little fundamental downside in zinc prices but rather expect balanced markets throughout 2014 and into 2015. In 2016, the world’s second largest zinc mine, Century in Australia (owned by Chinese Minmetals), will be depleted, and we believe that this will be the spark that ignites a zinc deficit which is set to drive prices higher.

0

0.5

1

1.5

2

2.5

3

Mt Nickel

New mine supply

Demand 4% CAGR

Production

5

7

9

11

13

15

17

19

21

23

Mt Zinc

New mine supply

Demand 4% CAGR

Production

Driving prices higher

Zinc pipeline is

somewhat muted

May cause supply

squeeze in 2016

Trading Strategy Commodity report, May 13, 2014

19

Figure 20: The zinc supply cash-cost curve, 2014 and 2018

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

Based on the shape of the cash-cost curve, we expect zinc prices to drift towards USD 2.500/tonne in 2016-18. A word of caution here is that China appears to be close to self-sufficient in zinc and we have little information about the Chinese zinc industry. Based on our understanding from better-known zinc mines, we believe that USD 2,500/tonne zinc in mines with lead by-products would make high economic sense; in our view, such price levels would spark investments in mine expansions.

Aluminium: capacity closures to keep supply balanced In contrast to base metals and iron ore, aluminium is produced from bauxite, which is not is a hard rock mined metal and hence is not subject to the same supply deficits in various parts of the cycle as other metal commodities are. Rather than adding capacity in mining, expanding capacity in bauxite extraction is simple. The supply/demand balance is determined by downstream capacity relative to demand. As a consequence, aluminium was only doubled during the last cycle, where as other base metals five folded and iron ore eight folded.

Figure 21: Capacity reductions keep markets balanced

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

Demand for aluminium has been running at close to 6% CAGR in the past decade, which is higher than for other base metals as a result of low price inflation compared to other metals. Three of the major global aluminium producers have in

0 20001000 40003000 60005000 80007000 9000

US

D/t

on

Accumulated production

-2000

-1000

0

1000

2000

3000

5

15

25

35

45

55

65

75

Mt Aluminium

New supply

Demand 5% CAGR

Production

Trading Strategy Sector report, May 13, 2014

20

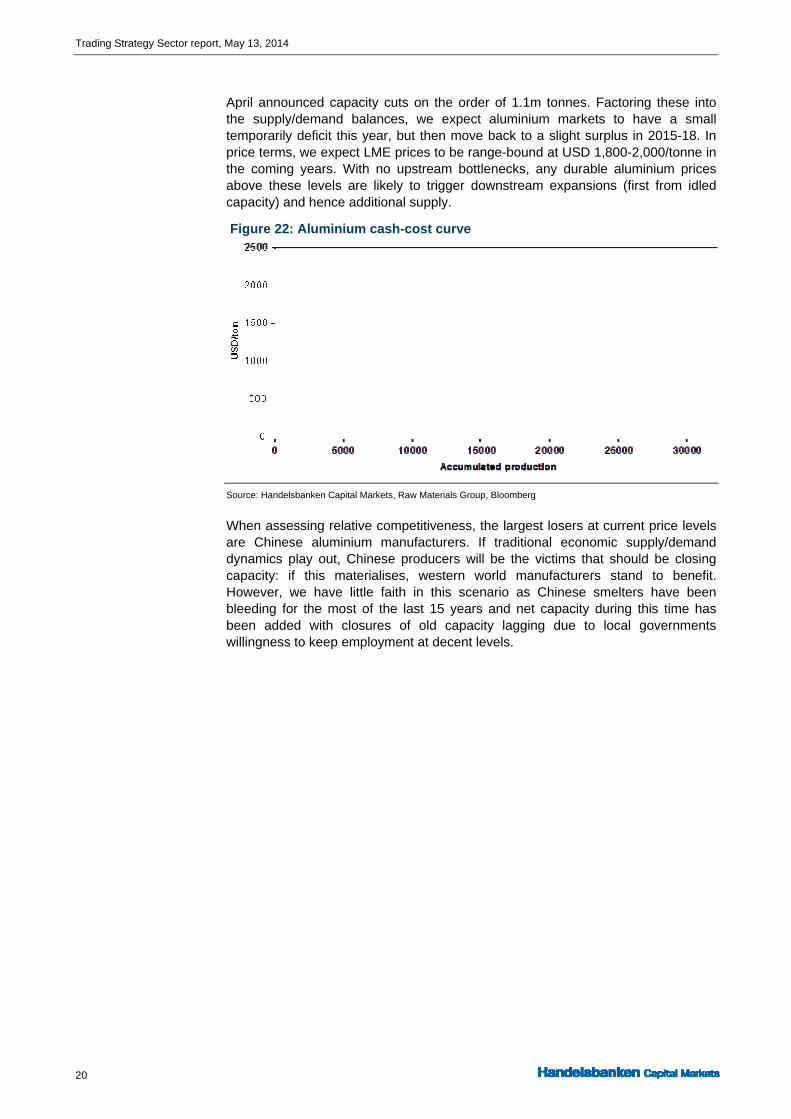

April announced capacity cuts on the order of 1.1m tonnes. Factoring these into the supply/demand balances, we expect aluminium markets to have a small temporarily deficit this year, but then move back to a slight surplus in 2015-18. In price terms, we expect LME prices to be range-bound at USD 1,800-2,000/tonne in the coming years. With no upstream bottlenecks, any durable aluminium prices above these levels are likely to trigger downstream expansions (first from idled capacity) and hence additional supply.

Figure 22: Aluminium cash-cost curve

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

When assessing relative competitiveness, the largest losers at current price levels are Chinese aluminium manufacturers. If traditional economic supply/demand dynamics play out, Chinese producers will be the victims that should be closing capacity: if this materialises, western world manufacturers stand to benefit. However, we have little faith in this scenario as Chinese smelters have been bleeding for the most of the last 15 years and net capacity during this time has been added with closures of old capacity lagging due to local governments willingness to keep employment at decent levels.

Trading Strategy Commodity report, May 13, 2014

21

Precious metals: gold value in the eye of the beholder The value of gold is based solely on perception, in our view, as industrial usage is second to speculation as a

driver of price. Although silver may have a higher share of industrial usage than gold, the metal trends tend

to mirror those of gold. The low industrial usage and high level of investment demand make these metals

directional, and this direction appears to be down. However, platinum group metals (PGMs) are to a greater

extent priced on supply/demand fundamentals, and with supply being constrained, we believe that these will

continue to be the star performers among precious metals.

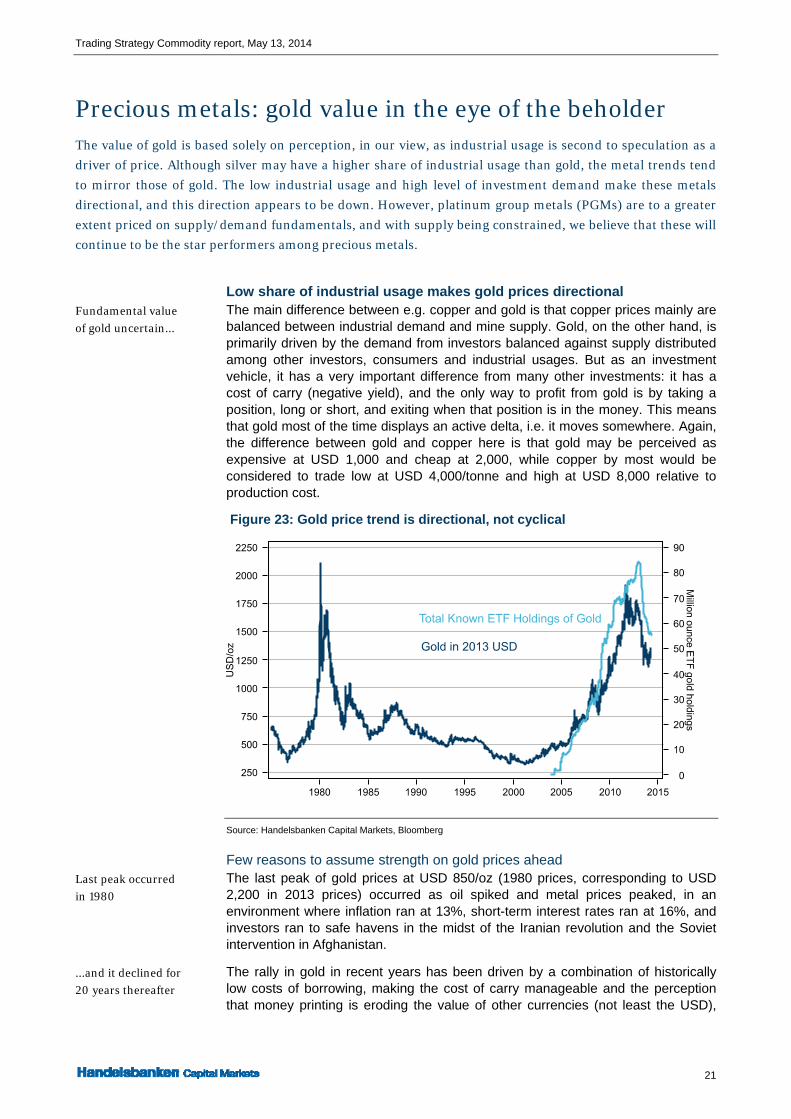

Low share of industrial usage makes gold prices directional The main difference between e.g. copper and gold is that copper prices mainly are balanced between industrial demand and mine supply. Gold, on the other hand, is primarily driven by the demand from investors balanced against supply distributed among other investors, consumers and industrial usages. But as an investment vehicle, it has a very important difference from many other investments: it has a cost of carry (negative yield), and the only way to profit from gold is by taking a position, long or short, and exiting when that position is in the money. This means that gold most of the time displays an active delta, i.e. it moves somewhere. Again, the difference between gold and copper here is that gold may be perceived as expensive at USD 1,000 and cheap at 2,000, while copper by most would be considered to trade low at USD 4,000/tonne and high at USD 8,000 relative to production cost.

Figure 23: Gold price trend is directional, not cyclical

Source: Handelsbanken Capital Markets, Bloomberg

Few reasons to assume strength on gold prices ahead The last peak of gold prices at USD 850/oz (1980 prices, corresponding to USD 2,200 in 2013 prices) occurred as oil spiked and metal prices peaked, in an environment where inflation ran at 13%, short-term interest rates ran at 16%, and investors ran to safe havens in the midst of the Iranian revolution and the Soviet intervention in Afghanistan.

The rally in gold in recent years has been driven by a combination of historically low costs of borrowing, making the cost of carry manageable and the perception that money printing is eroding the value of other currencies (not least the USD),

Fundamental value

of gold uncertain...

Last peak occurred

in 1980

...and it declined for

20 years thereafter

Trading Strategy Sector report, May 13, 2014

22

and making gold the ultimate hedge against central banks’ relentless stimulus. The main problem with these arguments is that they are based on a value of gold that only can be anchored in history; it has been more expensive before. With interest rates most likely pointing higher and gold being more directional in its pricing than fundamental, we struggle to see good arguments for gold to trend higher from here, but rather expect that deflation will continue. From the peak in 1980, it took 20 years before prices bottomed.

A gold price bust will have implications on the mining industry Gold is of importance for the mining industry as gold mining accounts for some 15% of total spending in the industry, third behind copper and iron ore. The strong price trend in the past decade paired with a brisk appetite from equity investors has turned gold into the most explored-for mineral in the mining universe in recent years. Despite this, new discoveries are of low grade and the average cash costs for mining gold have increased by 350% in a decade due to larger ore production, only to keep metal output flat.

Figure 24: Cash cost of mining gold has rocketed since 2002

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

The result of low-quality gold mining is that high gold prices have contributed to longer lead times for equipment, spare parts and skilled people. A declining gold price would hence ease some of the cost pressures on the rest of the mining industry, as a larger number of gold mines would cease operations. In copper mining, however, gold and silver account for 10% of the value of the copper mining universe, and an easing of cost pressures would most likely be more than mitigated by lower value of by-product credits.

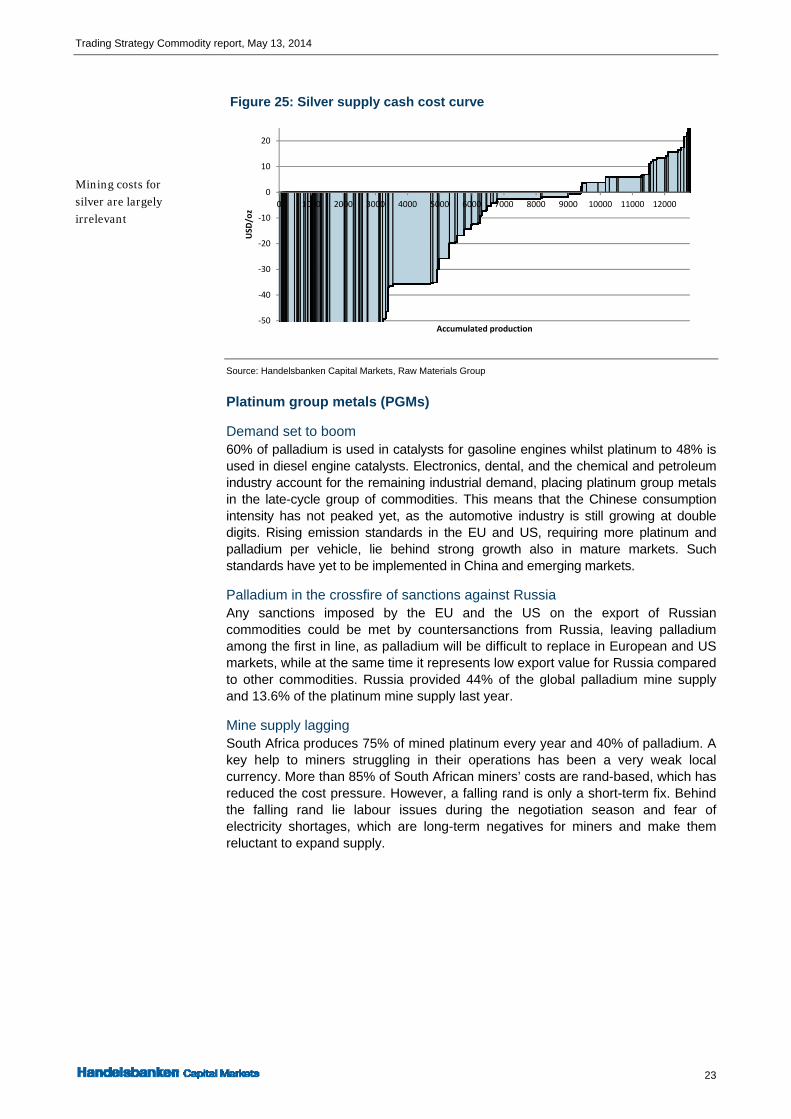

Silver tends to follow gold and cash costs are less relevant The price trend of silver tends to map that of gold. A main difference, however, is that silver is mined in dedicated mines to a lesser extent than gold, and more often occurs as a by-product from other mines. Hence, a silver cash-cost curve displays mines that are largely cash-cost negative. Therefore, by defining a zinc and lead mine with by-product credits from silver as a silver mine, the proceeds from selling silver and lead most often cover all operating expenses and, hence, the implicit cost for the silver production is negative.

This also means that the silver price will depend on output to a lesser extent than any other metals, but rather tends to look more like gold, where perception is a key driver.

0

200

400

600

800

1000

1200

1400

1600

1800

2000

0 10 20 30 40 50 60 70 80 90 100

US

D/o

z

%

2012

2007

2002

Opportunistic gold

mining has driven

production costs

higher

…and caused cost

inflation in the

mining industry

Silver tends to follow

gold

Trading Strategy Commodity report, May 13, 2014

23

Figure 25: Silver supply cash cost curve

Source: Handelsbanken Capital Markets, Raw Materials Group

Platinum group metals (PGMs)

Demand set to boom 60% of palladium is used in catalysts for gasoline engines whilst platinum to 48% is used in diesel engine catalysts. Electronics, dental, and the chemical and petroleum industry account for the remaining industrial demand, placing platinum group metals in the late-cycle group of commodities. This means that the Chinese consumption intensity has not peaked yet, as the automotive industry is still growing at double digits. Rising emission standards in the EU and US, requiring more platinum and palladium per vehicle, lie behind strong growth also in mature markets. Such standards have yet to be implemented in China and emerging markets.

Palladium in the crossfire of sanctions against Russia Any sanctions imposed by the EU and the US on the export of Russian commodities could be met by countersanctions from Russia, leaving palladium among the first in line, as palladium will be difficult to replace in European and US markets, while at the same time it represents low export value for Russia compared to other commodities. Russia provided 44% of the global palladium mine supply and 13.6% of the platinum mine supply last year.

Mine supply lagging South Africa produces 75% of mined platinum every year and 40% of palladium. A key help to miners struggling in their operations has been a very weak local currency. More than 85% of South African miners’ costs are rand-based, which has reduced the cost pressure. However, a falling rand is only a short-term fix. Behind the falling rand lie labour issues during the negotiation season and fear of electricity shortages, which are long-term negatives for miners and make them reluctant to expand supply.

‐50

‐40

‐30

‐20

‐10

0

10

20

0 1000 2000 3000 4000 5000 6000 7000 8000 9000 10000 11000 12000

USD

/oz

Accumulated production

Mining costs for

silver are largely

irrelevant

Trading Strategy Sector report, May 13, 2014

24

Figure 26: PMGs: New supply, demand and production

Source: Handelsbanken Capital Markets, Raw Materials Group, Bloomberg

While most other metals have experienced strong mine supply growth during the past five years as a natural consequence of high prices and miners expanding production, as revenues are ploughed back in to operations, PGMs differ. Miners have been reluctant to invest in South Africa, which suffers from an unstable political climate, labour issues and technically-challenging deep ore bodies. For Russian miners, PGMs are valuable bimetals to nickel production. They had a significant contribution to profitability during recent quarters when nickel traded below USD 18,000/tonne but they are not the primary target in expansion plans. Nickel prices have suffered from rising substitution by nickel pig iron in recent years, and mine expansions have not been on the agenda for Russian miners. Nickel investments might surface in the wake of the Indonesian export ban, but it will take years for Russian miners to complete any expansion plans, leaving PGMs exposed to South Africa’s struggling mining industry and strong global demand.

Figure 27: Cash cost of PGM mines in South Africa and Zimbabwe

Source: Handelsbanken Capital Markets, Raw Materials Group

0

100

200

300

400

500

600

700

ton Demand 5% CAGR

Production

New supply

0

200

400

600

800

1000

1200

1400

1600

1800

0 1000 2000 3000 4000 5000 6000

USD

/4E oz

Accumulated production

PGM basket price 1174 USD

Avg cash cost 800 USD

Trading Strategy Commodity report, May 13, 2014

25

Western world steel rising from the ashes Although steel markets will not be a quick fix, we argue that industry margins will rise from current levels.

Based on our assumption that iron ore prices will continue to deflate, and as input costs are likely to remain a

key driver of the nominal price of steel, we argue that we will see lower steel prices ahead. As this

materialises, we see a lesser scope for global trade in steel and we expect that price negotiations will leave

more room for margin expansion in carbon steel. In stainless, we believe that higher nickel prices and less

price competition from Chinese nickel pig iron producers will enable higher base prices in western world

stainless steel producers.

No quick fix in carbon steel Steel markets have suffered from excess capacity since after the global financial crisis as demand has not returned to pre-crisis levels. Steel intensity in China has peaked and demand in western Europe has not returned to pre-crisis levels.

Figure 28: Global steel capacity utilisation

Source: Handelsbanken Capital Markets, World Steel Association

In terms of utilisation ahead, we see no easing. According to Eurfer, net additions of steel capacity may amount to some 10% of total global capacity until 2016. China has initiated closures of environmentally hazardous capacity, but according to Hebei Steel, the net trend is that total capacity in China is still growing.

With freight costs being a fraction of total steel prices, abundant supplies in China have been exported elsewhere in the past few years, with total exported volumes amounting to some 50 million tonnes annually, corresponding to 7% of produced materials. China produces 50% of all steel globally, and these exports of excess capacity have been sufficient to pressure steel margins in the rest of the world.

The main problem with low capacity utilisation in steel is the high operating leverage due to the high level of fixed costs. As in mining, markets are fragmented and no companies act for the betterment of the general industry. The cash cost curve in steel is flat and cost savings have been eaten up by price pressure, as the positive leverage from gaining volumes has been, and still is in many cases, better than holding onto the savings. A steel plant with 3 million tonnes in capacity operating at 75% utilisation, and with fixed costs of SEK 2bn while trying to save SEK 0.5bn, would be better off giving away all savings through price pressure and increasing utilisation to 85% than it would if it held onto the savings (no price reductions) and maintained volumes. This creates substantial issues for steel producers in the

65%

70%

75%

80%

85%

Jan -11 Jul -11 Jan -12 Jul -12 Jan -13 Jul -13 Jan -14

Steel utilisation rates

too low

Steel capacity is most

likely still growing

China exports 7% of

produced volumes

Operating leverage

remains a challenge

Trading Strategy Sector report, May 13, 2014

26

current market. The cure for the above is higher utilisation and hence a better pricing position between steel sellers and buyers.

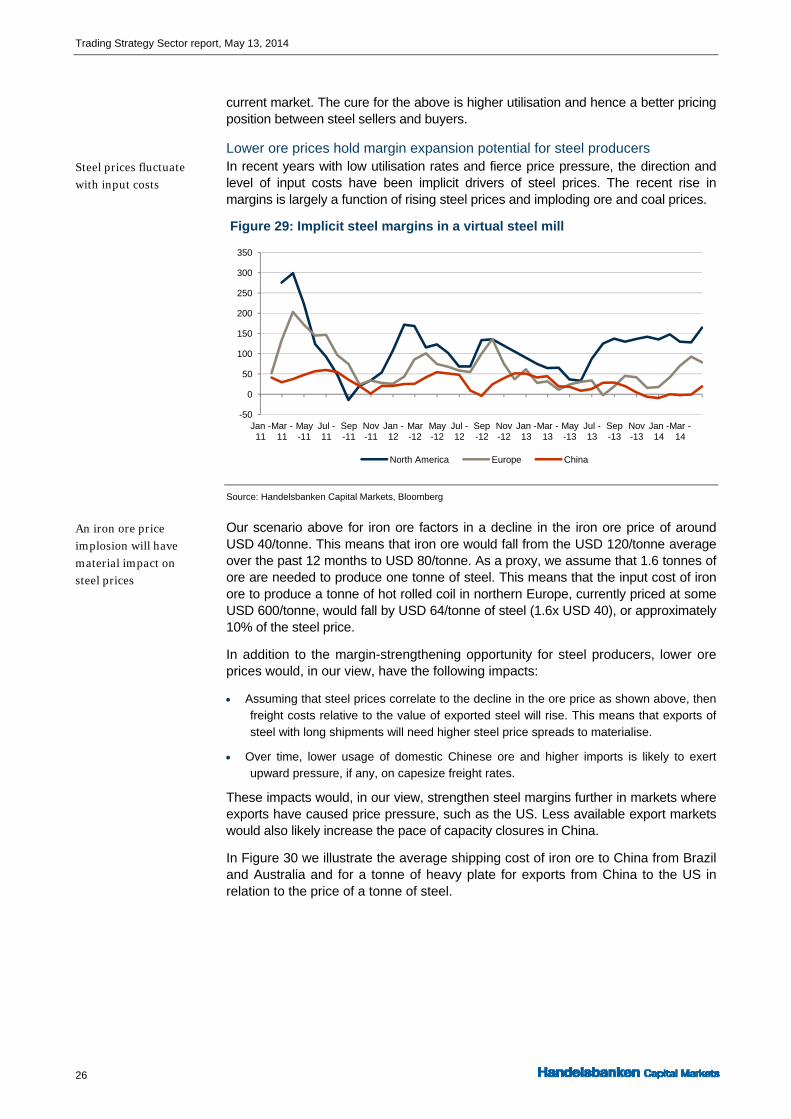

Lower ore prices hold margin expansion potential for steel producers In recent years with low utilisation rates and fierce price pressure, the direction and level of input costs have been implicit drivers of steel prices. The recent rise in margins is largely a function of rising steel prices and imploding ore and coal prices.

Figure 29: Implicit steel margins in a virtual steel mill

Source: Handelsbanken Capital Markets, Bloomberg

Our scenario above for iron ore factors in a decline in the iron ore price of around USD 40/tonne. This means that iron ore would fall from the USD 120/tonne average over the past 12 months to USD 80/tonne. As a proxy, we assume that 1.6 tonnes of ore are needed to produce one tonne of steel. This means that the input cost of iron ore to produce a tonne of hot rolled coil in northern Europe, currently priced at some USD 600/tonne, would fall by USD 64/tonne of steel (1.6x USD 40), or approximately 10% of the steel price.

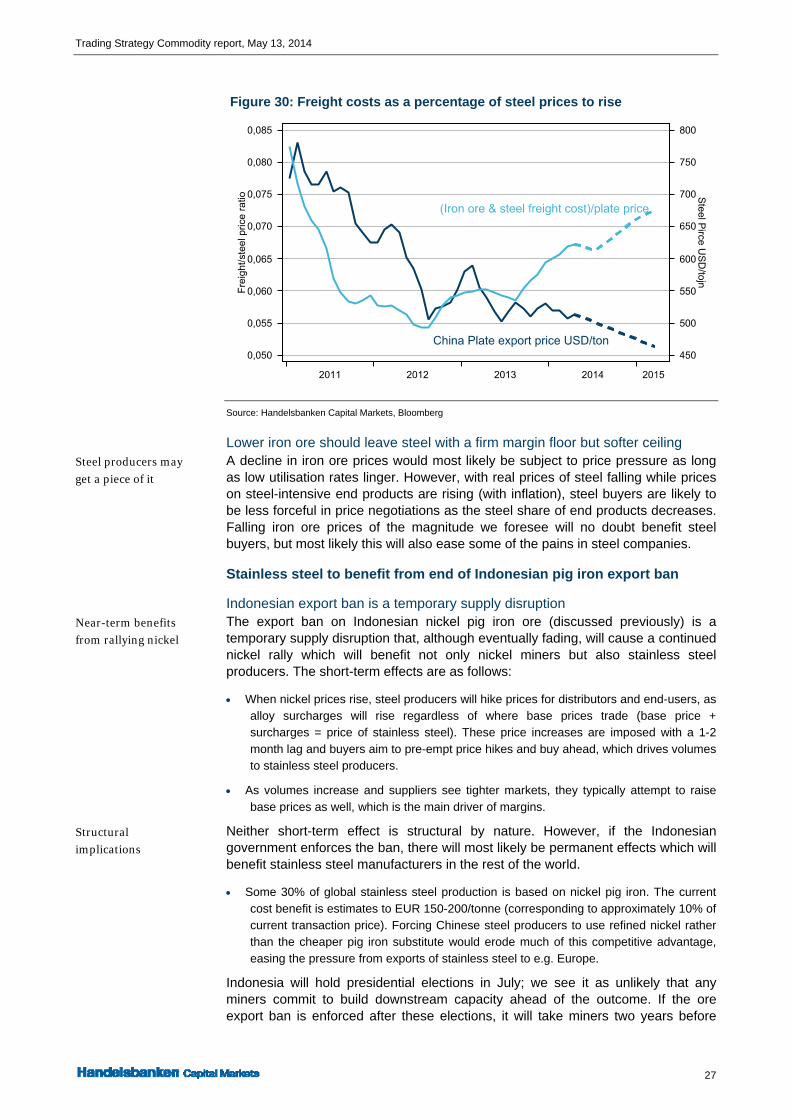

In addition to the margin-strengthening opportunity for steel producers, lower ore prices would, in our view, have the following impacts:

Assuming that steel prices correlate to the decline in the ore price as shown above, then freight costs relative to the value of exported steel will rise. This means that exports of steel with long shipments will need higher steel price spreads to materialise.

Over time, lower usage of domestic Chinese ore and higher imports is likely to exert upward pressure, if any, on capesize freight rates.

These impacts would, in our view, strengthen steel margins further in markets where exports have caused price pressure, such as the US. Less available export markets would also likely increase the pace of capacity closures in China.

In Figure 30 we illustrate the average shipping cost of iron ore to China from Brazil and Australia and for a tonne of heavy plate for exports from China to the US in relation to the price of a tonne of steel.

-50

0

50

100

150

200

250

300

350

Jan -11

Mar -11

May -11

Jul -11

Sep -11

Nov -11

Jan -12

Mar -12

May -12

Jul -12

Sep -12

Nov -12

Jan -13

Mar -13

May -13

Jul -13

Sep -13

Nov -13

Jan -14

Mar -14

North America Europe China

Steel prices fluctuate

with input costs

An iron ore price

implosion will have

material impact on

steel prices

Trading Strategy Commodity report, May 13, 2014

27

Figure 30: Freight costs as a percentage of steel prices to rise

Source: Handelsbanken Capital Markets, Bloomberg

Lower iron ore should leave steel with a firm margin floor but softer ceiling A decline in iron ore prices would most likely be subject to price pressure as long as low utilisation rates linger. However, with real prices of steel falling while prices on steel-intensive end products are rising (with inflation), steel buyers are likely to be less forceful in price negotiations as the steel share of end products decreases. Falling iron ore prices of the magnitude we foresee will no doubt benefit steel buyers, but most likely this will also ease some of the pains in steel companies.

Stainless steel to benefit from end of Indonesian pig iron export ban

Indonesian export ban is a temporary supply disruption The export ban on Indonesian nickel pig iron ore (discussed previously) is a temporary supply disruption that, although eventually fading, will cause a continued nickel rally which will benefit not only nickel miners but also stainless steel producers. The short-term effects are as follows:

When nickel prices rise, steel producers will hike prices for distributors and end-users, as alloy surcharges will rise regardless of where base prices trade (base price + surcharges = price of stainless steel). These price increases are imposed with a 1-2 month lag and buyers aim to pre-empt price hikes and buy ahead, which drives volumes to stainless steel producers.

As volumes increase and suppliers see tighter markets, they typically attempt to raise base prices as well, which is the main driver of margins.

Neither short-term effect is structural by nature. However, if the Indonesian government enforces the ban, there will most likely be permanent effects which will benefit stainless steel manufacturers in the rest of the world.

Some 30% of global stainless steel production is based on nickel pig iron. The current cost benefit is estimates to EUR 150-200/tonne (corresponding to approximately 10% of current transaction price). Forcing Chinese steel producers to use refined nickel rather than the cheaper pig iron substitute would erode much of this competitive advantage, easing the pressure from exports of stainless steel to e.g. Europe.

Indonesia will hold presidential elections in July; we see it as unlikely that any miners commit to build downstream capacity ahead of the outcome. If the ore export ban is enforced after these elections, it will take miners two years before

Steel producers may

get a piece of it

Near-term benefits

from rallying nickel

Structural

implications

Trading Strategy Sector report, May 13, 2014

28

downstream capacity has been installed. However, as these decisions to build are taken it is likely that Chinese stainless steel mills commence calibrating their production to use scrap and refined nickel. Such a restructuring of the Chinese stainless steel industry will create a new equilibrium in refined nickel markets but also likely lay the foundation for less meagre stainless steel markets in Europe as the export incentive ease for the Chinese.

Trading Strategy Commodity report, May 13, 2014

29

Crude oil and natural gas – the boom of 21st century Optimists say the conditions are right for a truly global unconventional oil business. Sustained high oil prices

give drillers every incentive to unlock more supply. This is what happened in the US, where forecasts for 2015

predict the US will be vying with Russia and Saudi Arabia to be the world’s largest producer. However, we

remain cautious: the rest of the world is not the US.

US shale oil: the production boom of the 21st century Technology improvements come stepwise in the extractive industries. The technology for extracting unconventional oil and gas has advanced rapidly, which by itself makes today’s unconventional resources the conventional ones of tomorrow. It also vouches for increasing production simultaneously, as prices fall when improvements in technology lower production costs.

Global impact from local booms One of the most visible success signs of recent times is illustrated in the figures below. Higher natural gas output from a significant lower number of rigs verifies the improved efficiency looked for by commodity-producing industries. The impact of this is already being felt outside the US, although the US export ban on crude oil remains intact. A rising gas supply at low cost has substituted demand for US coal, which instead has been exported elsewhere, particularly to Europe, putting pressure on coal and electricity prices.

Figure 31: Gas output vs. rigs US coal exports, nat. gas production

Source: Handelsbanken Capital Markets, Bloomberg

The US crude oil miracle We are witnessing one of the greatest production booms of modern times. After 40 years of declining production, the US managed to implement new technology and reverse the negative trend of crude oil output. US production is growing even faster than Russia’s did between 2000 and 2005, and is predicted to add another million barrels per day during 2014 to rise again by nearly the same amount in 2015 and reach 9.3m b/d. The world balance has changed and will continue to do so quickly. Many non-OPEC countries have increased production, and only one of the world’s five biggest oil producers today is an OPEC member.

The US, Canada and Mexico now produce more oil than the top three OPEC countries, Saudi Arabia, Iraq and Iran. OPEC, whose politics are largely a consequence of what Saudi Arabia can afford given the country represents 30% of

Technology

advancing rapidly

US gas boom putting

pressure on coal and

electricity prices in

Europe

Only one of the

world’s five biggest

oil producers is an

OPEC member

Trading Strategy Sector report, May 13, 2014

30

the cartel’s production, has seen its power wane. OPEC´s ambition to stabilise the price lies behind the fluctuating production in Saudi Arabia. North Sea production is declining fast, as it has been doing for a decade. Recent years have seen more bucks but less of a bang in that region.

Figure 32: World oil map is changing fast (US forecast from EIA)

Source: Handelsbanken Capital Markets, Bloomberg

Not repeated elsewhere The sceptics say, however, that the oil production rise will be short-lived and concentrated in North America. The success in the US is accredited to a few small independent oil companies run by managers with a superhuman tolerance for risk. That sort of development will not be seen in Europe, the home of eco-warriors, and it will not be repeated easily in China, Russia or Latin America, which all lack the fleet of service companies that have done the grunt work in the US. For those reasons, significant production from unconventional sources outside North America is probably a decade away. In addition, the structurally steep decline rates of shale oil wells means a greater number of them need to be drilled to maintain merely flat production – a strong argument that growth rates will slow significantly in a few years.

Lower imports affect exporters of light, sweet oil

The rising US production corresponds to lower import needs. Most new American wells, such as those in the Bakken shale oil field, produce light, sweet crude that can be easily refined into gasoline. Lower US imports affect west African exporters in the first place, as they produce similar qualities. On the other hand, the US still has a strong need for sour, dense qualities, which are produced by Saudi, Canada and Venezuela. These countries still keep their positions as crude exporters.

Significant shale oil

production outside

North America is a

decade away

America’s new wells

producing light,

sweet crude

Trading Strategy Commodity report, May 13, 2014

31

Figure 33: US crude output, imports US crude imports from West Africa

Source: Handelsbanken Capital Markets, Bloomberg

Incentive price only matters when supply is tight The IEA says a breakeven oil price of USD 64/barrel is required to make tight oil projects feasible. That is the lower end of North American unconventional oil reserves. The high end is represented by oil sands, with a supply cost in a wide range between USD 50-90/barrel. In general, USD 80-85/barrel would make most sources in North America viable. Today’s marginal cost of non-OPEC production worldwide is USD 104/barrel, strongly supported by ultra deepwater projects. It would thus be natural to assume that oil producers only will expand capacity if prices remain above the USD 100 mark. Over time, this is a fair assumption. The incentive price where producers spend is highly relevant for pricing as long as supply is tight, but when actual excess supply emerges, the marginal level of suffering swings into focus, and as that happens, the relevant question is what OPEC can sustain.

Supply disruption hindered price gravidity Concerns about Iran, oil thieves in Nigeria, disintegration in Iraq and civil war in Libya have all fuelled the price of oil during the last three years. Exports from these countries are down by about 3 million barrels per day. This loss is almost exactly compensated by increased production in the US, which has led to stability in the oil price without any strategically voluntary cutbacks from OPEC. Now, these problems are starting to ease.

Iraq has already increased exports from its southern regions and reached record levels in February post the American intervention in 2003.

Incentive price

where producers

spend is only

relevant as long as

tightness remains

Supply disruptions

are compensated by

US rising production

Iraq has already

increased exports

Trading Strategy Sector report, May 13, 2014

32

Figure 34: Crude production OPEC supply disruptions

Source: Handelsbanken Capital Markets, Bloomberg

Negotiations with Iran had a breakthrough in November 2013 when an interim deal struck over its nuclear programme and exports started to edge higher. Easing of sanctions so far does not include oil, but a long-term deal is scheduled to be finalised by July 20. If oil sanctions ease, then Iran’s oil exports could begin a slow recovery.

Libya seems more hopeful. Exports are hindered by strikes and threats from rebels seeking self-rule for Libya’s eastern regions to sell oil independently of Tripoli. Rebels agreed to surrender two oil ports to the government on April 6. The two remaining export facilities they control will be handed over shortly. It is unlikely that 2014 will end without a solution being found, and Libya will then have the opportunity to secure much needed oil export income. Of the three trouble spots, it is Libya that can quickest achieve exports that influence the price and Libya is therefore the one to watch more closely.

OPEC will come under pressure OPEC’s situation is hereby set to deteriorate rapidly. The members of the cartel that have not been affected by supply disruptions or sanctions have been able to benefit from high production and high prices when exports from three members have involuntarily ceased. If Libya, Iran and Iraq return to exporting oil at pre-disruption levels, it remains to be seen how interested Saudi Arabia is in cutting production to hand over income to Iraq, which is still officially outside OPEC’s joint production quota, and Iran, with whom relations have been mixed throughout OPEC’s history.

Putin gave some relief Recent good news out of Libya has been counteracted by the rising risk premium due to the escalation of violence in Ukraine. Any change in the situation with Russia will override news flow in MENA given Russia’s larger portion of the crude export market. At the same time, growing public discontent and lack of investment are taking their toll on Venezuelan oil output, which has dropped from 2.7 million barrels per day in 2013 to 2.5 million in 2014.

Saudi Arabia to set floor at USD 91 The potentially rising supply on the world export market comes at the same time as shifting demographics and fuel efficiency in developed economies and China’s cooling economic growth affecting the demand side of the price equation. Given last year’s civil unrest in the MENA region, it has been increasingly important for budgets to be balanced so that cherished social benefits are maintained as these governments traditionally have had low taxes and high levels of subsidies for food

Supply disruptions

equal to US boom

If oil sanctions ease

on Iran, exports

could begin a slow

recovery in H2 2014

It is unlikely that

2014 will end

without Libya back

in exports

OPEC’s situation is

set to deteriorate

rapidly

Russia risk premium

overrides news flow

in MENA

Saudi will maintain a

fiscal balance at

Brent price of more

than USD 91

Trading Strategy Commodity report, May 13, 2014

33

and fuel. Saudi will maintain a fiscal balance at a Brent price of more than USD 91. These levels will be more important if OPEC comes under pressure as we expect.

Figure 35: Oil price for fiscal breakeven in MENA from IMF

Source: Handelsbanken Capital Markets, Bloomberg, IMF

Natural gas Even though the US and Canada have the most developed fields in unconventional gas, other nations are about to catch up. China, Argentina and Australia are all set to be among significant future producers. China has huge shale gas reserves and has entered into an agreement with the US to share technological know-how.

The development of shale resources is however subject to a lengthy learning curve. It took the United States 35 years to move from discovery to production. However, this will go much faster for the followers. Europe is only at the start of this process. European deposits appear to be deeper than in the US and hence more technically challenging. Land ownership is also much more fragmented and there is less incentive for European residents to support nearby drilling. A ban on the industry is already in place in France, Bulgaria and North Rhine Westphalia in Germany.

Regional gas market will normalise in slow motion Given the high transport barriers in intercontinental natural gas markets stemming from the high cost of transportation and the need for board-breaking infrastructure solutions, a wide spread between regional gas prices has established. The price divergence has widened after the Fukushima accident, but Japan’s nuclear regulators are about to review a possible restart of 17 nuclear reactors. This is a slow process and will likely not impact gas prices in 2014. However, the election of pro-nuclear Yoichi Masuzoe as Tokyo Governor could accelerate the process.

As infrastructure for exporting natural gas is built in the US for imports in Europe, prices will start to narrow. The expected surge in liquefied natural gas to Europe during and after 2015 will reduce Russia’s flows and stranglehold on Europe’s gas supply. Russia currently supplies 30% of the Continent’s gas needs.

China, Argentina and

Australia are all set

to be significant

future producers

It took the United

States 35 years to

move from discovery

to production

High transport

barriers in

intercontinental

natural gas markets

Russia is supplying

30% of Europe’s gas

needs

Trading Strategy Sector report, May 13, 2014

34

Figure 36: Regional gas prices have diverged

Source: Handelsbanken Capital Markets, Bloomberg

Trading Strategy Commodity report, May 13, 2014

35