Languages

Pages

Legal

ERT461 BIOSYSTEMS ENGINEERING DESIGN 1

ERT424 BIOPROCESS PLANT DESIGN 1

1

The Interest Rate Simple Interest Compound Interest Amortizing a Loan Compounding More Than Once per

Year

The Interest Rate Simple Interest Compound Interest Amortizing a Loan Compounding More Than Once per

Year

Which would you prefer -- $10,000 today $10,000 today or $10,000 in $10,000 in

5 years5 years?

TIMETIME allows you the opportunity to postpone consumption and earn

INTERESTINTEREST.

Why is TIMETIME such an important element in your decision?

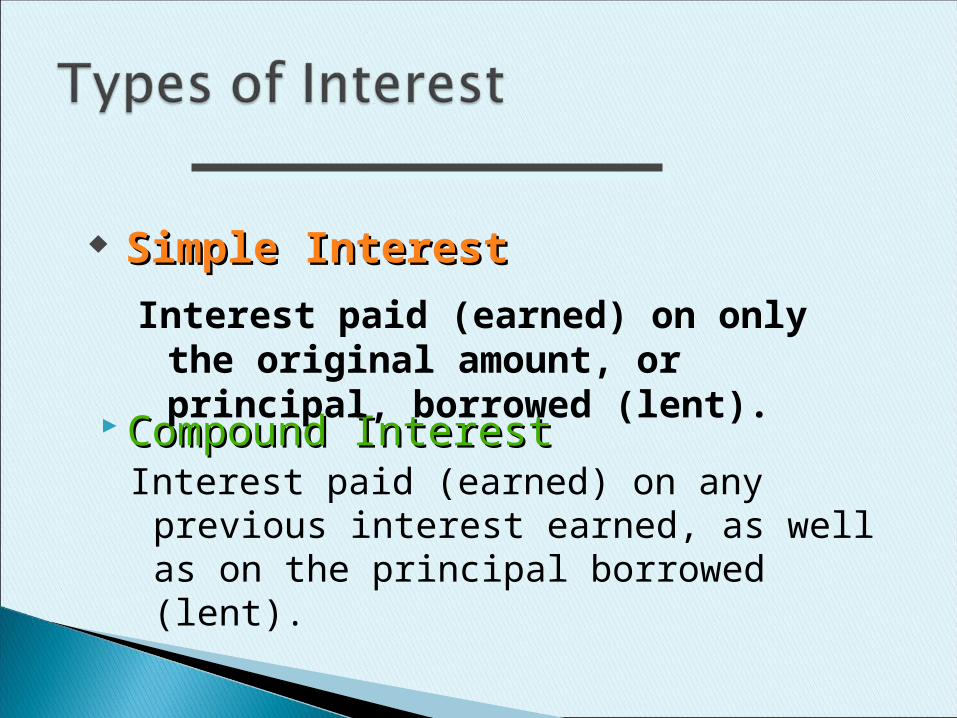

Compound InterestCompound InterestInterest paid (earned) on any previous

interest earned, as well as on the principal borrowed (lent).

Simple InterestSimple Interest

Interest paid (earned) on only the original amount, or principal, borrowed (lent).

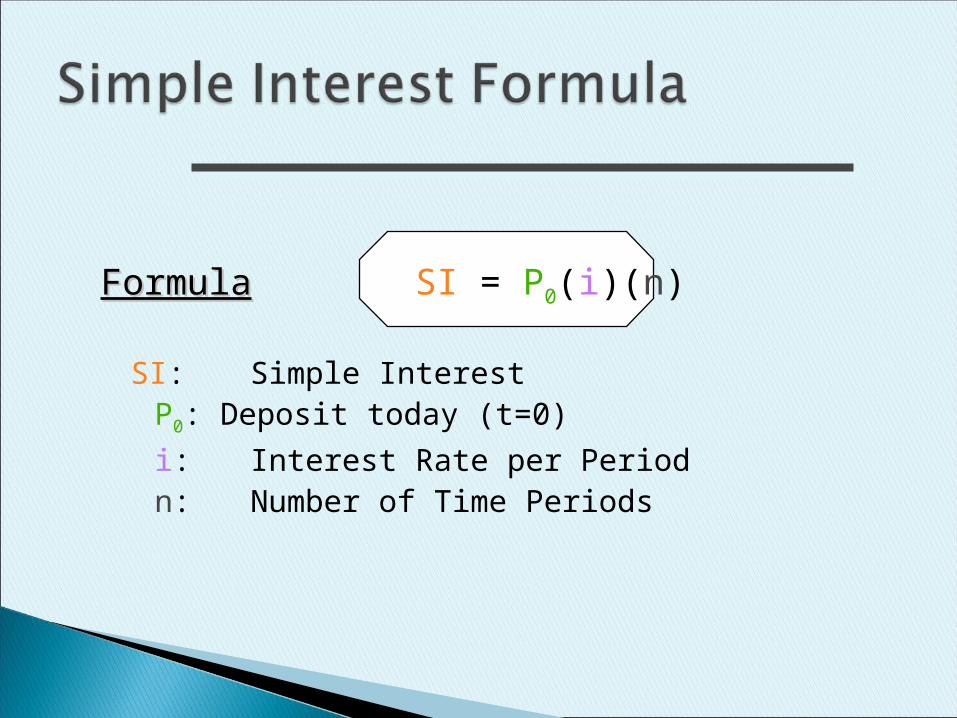

FormulaFormula SI = P0(i)(n)

SI: Simple InterestP0: Deposit today (t=0)

i: Interest Rate per Periodn: Number of Time Periods

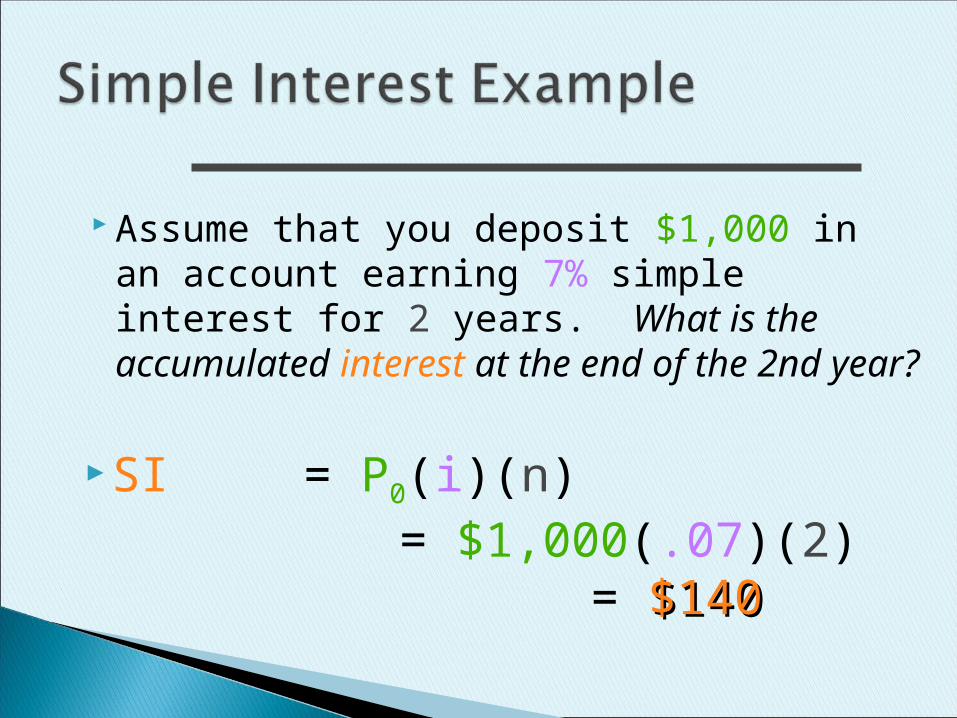

SI = P0(i)(n)= $1,000(.07)(2)

= $140$140

Assume that you deposit $1,000 in an account earning 7% simple interest for 2 years. What is the accumulated interest at the end of the 2nd year?

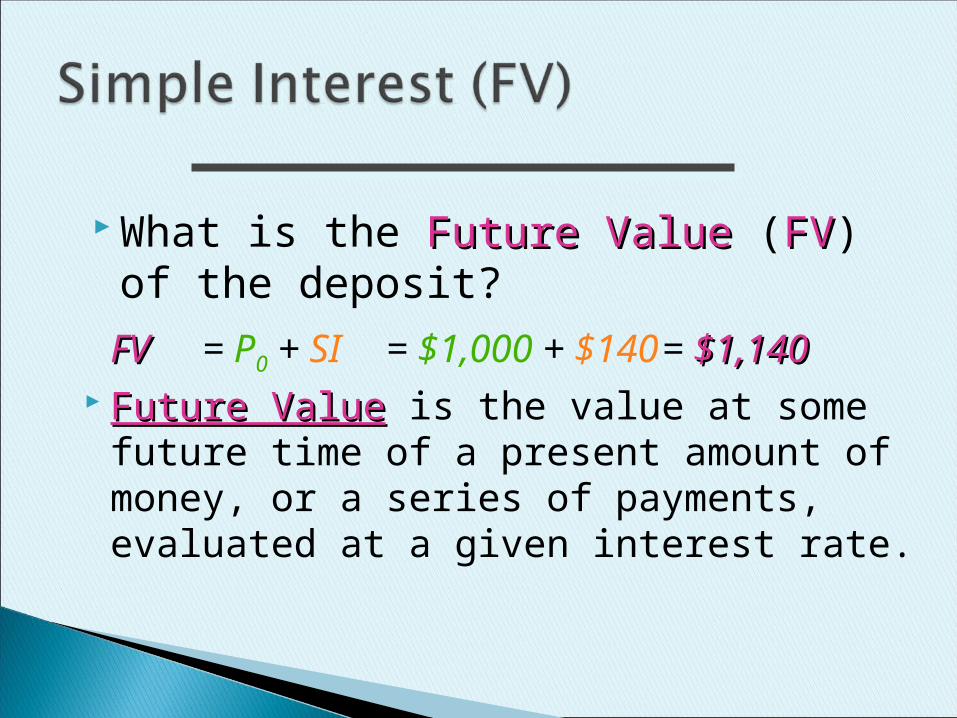

FVFV = P0 + SI = $1,000 + $140= $1,140$1,140

Future ValueFuture Value is the value at some future time of a present amount of money, or a series of payments, evaluated at a given interest rate.

What is the Future Value Future Value (FVFV) of the deposit?

The Present Value is simply the $1,000 you originally deposited. That is the value today!

Present ValuePresent Value is the current value of a future amount of money, or a series of payments, evaluated at a given interest rate.

What is the Present Value Present Value (PVPV) of the previous problem?

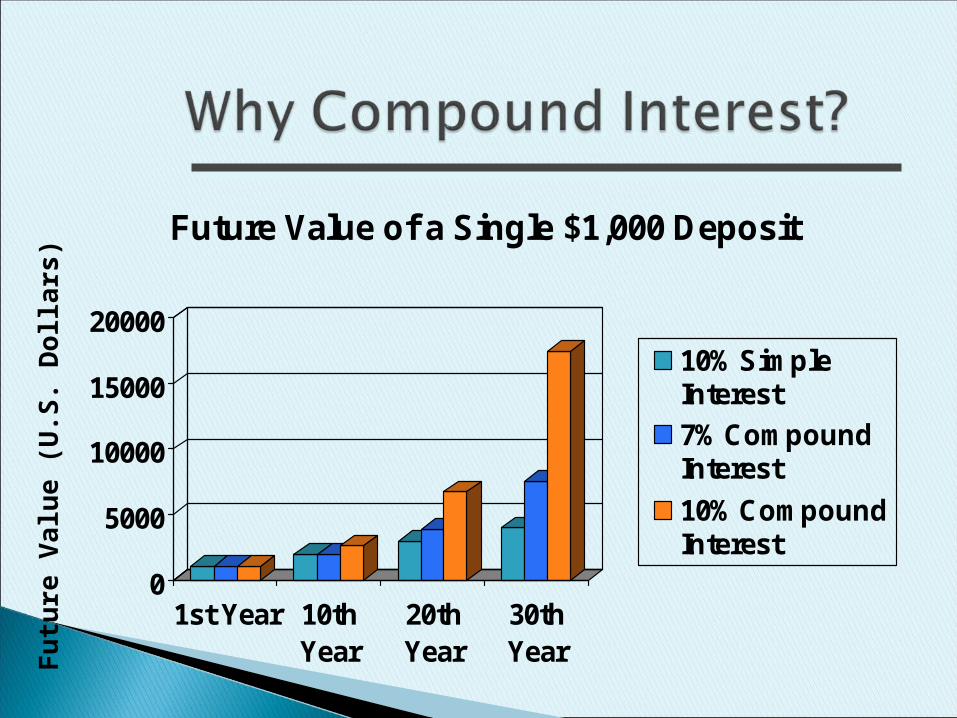

0

5000

10000

15000

20000

1st Year 10thYear

20thYear

30thYear

Future Value of a Single $1,000 Deposit

10% SimpleInterest

7% CompoundInterest

10% CompoundInterest

Fu

ture

Val

ue

(U.S

. Dol

lars

)

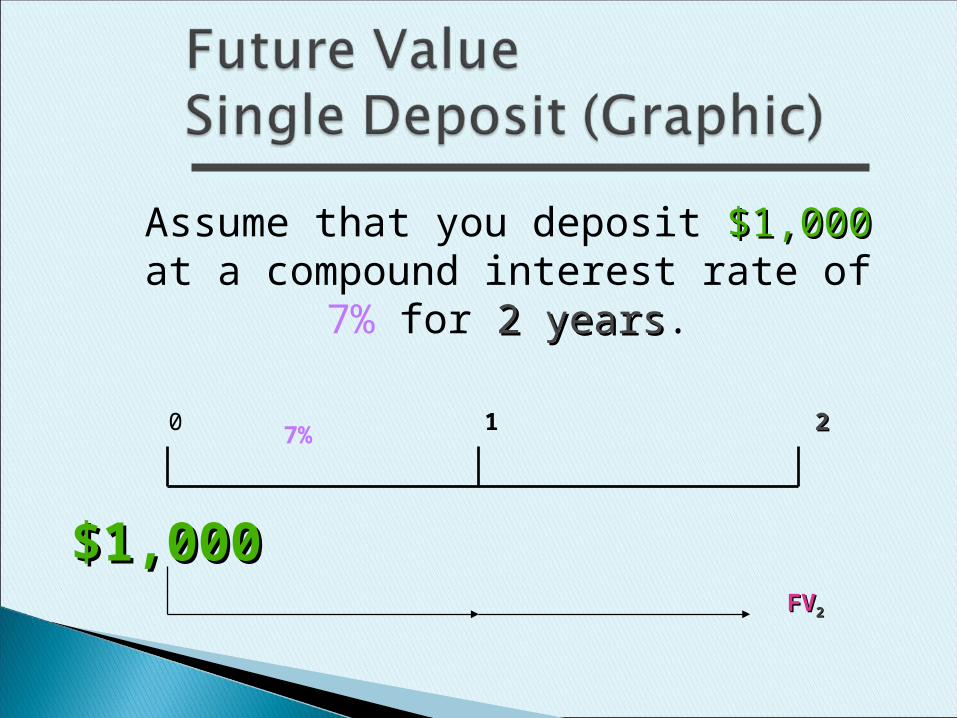

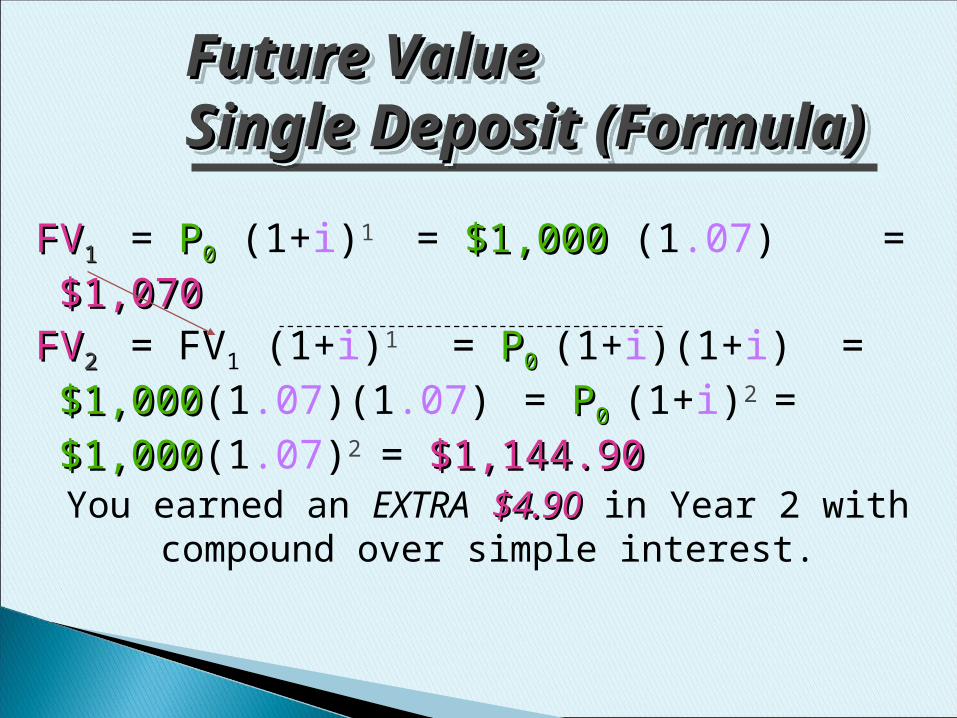

Assume that you deposit $1,000$1,000 at a compound interest rate of

7% for 2 years2 years.

0 1 22

$1,000$1,000FVFV22

7%

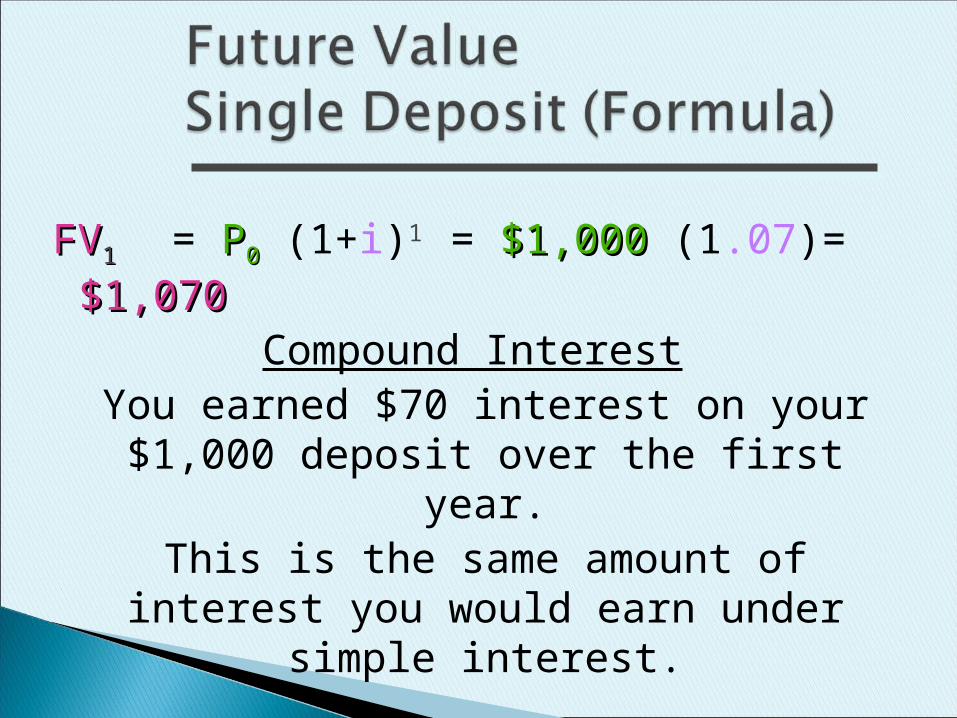

FVFV11 = PP00 (1+i)1 = $1,000$1,000 (1.07) = $1,070$1,070

Compound InterestYou earned $70 interest on your

$1,000 deposit over the first year.This is the same amount of interest

you would earn under simple interest.

FVFV11 = PP00 (1+i)1 = $1,000$1,000 (1.07) = $1,070$1,070

FVFV22 = FV1 (1+i)1 = PP0 0 (1+i)(1+i) = $1,000$1,000(1.07)(1.07)= PP00 (1+i)2 = $1,000$1,000(1.07)2

= $1,144.90$1,144.90You earned an EXTRA $4.90$4.90 in Year 2 with

compound over simple interest.

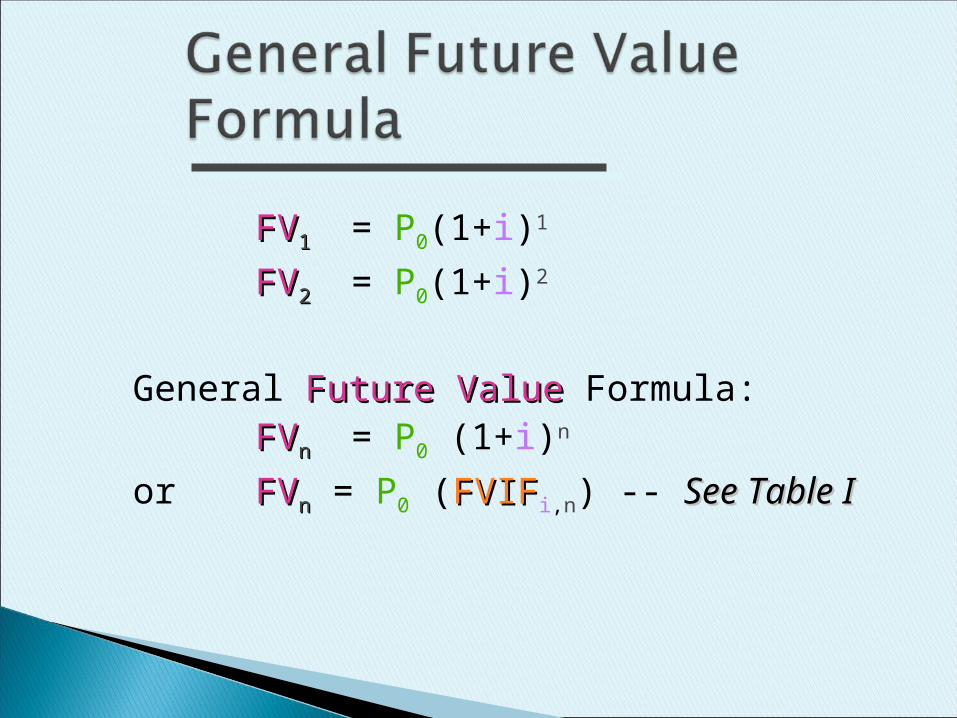

Future ValueFuture ValueSingle Deposit (Formula)Single Deposit (Formula)Future ValueFuture ValueSingle Deposit (Formula)Single Deposit (Formula)

FVFV11 = P0(1+i)1

FVFV22 = P0(1+i)2

General Future Value Future Value Formula:FVFVnn = P0 (1+i)n

or FVFVnn = P0 (FVIFFVIFi,n) -- See Table ISee Table I

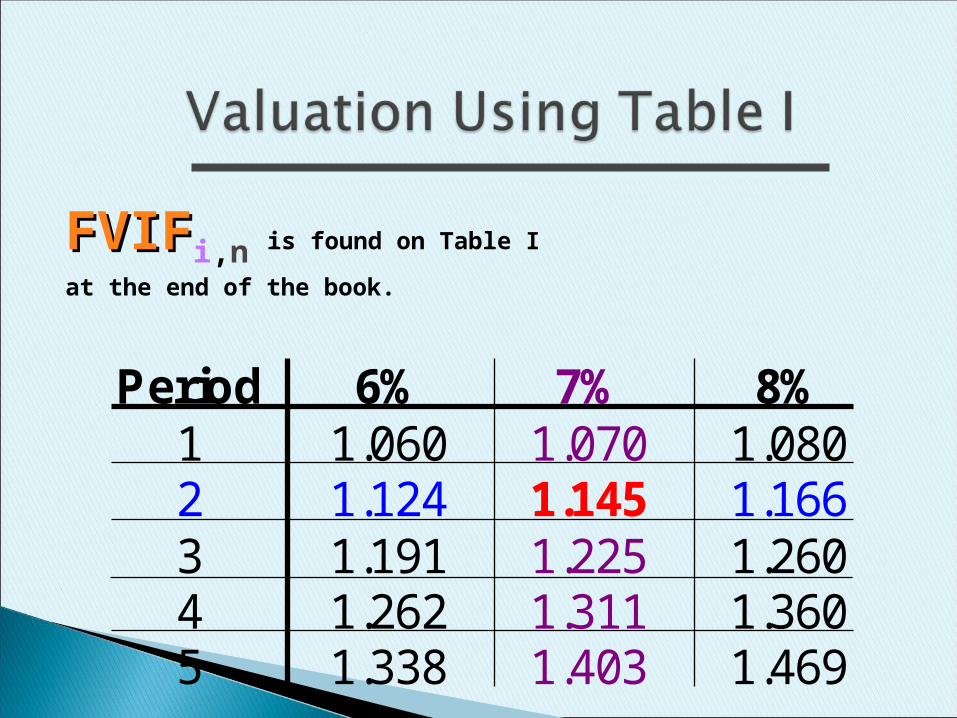

FVIFFVIFi,n is found on Table I

at the end of the book.

Period 6% 7% 8%1 1.060 1.070 1.0802 1.124 1.145 1.1663 1.191 1.225 1.2604 1.262 1.311 1.3605 1.338 1.403 1.469

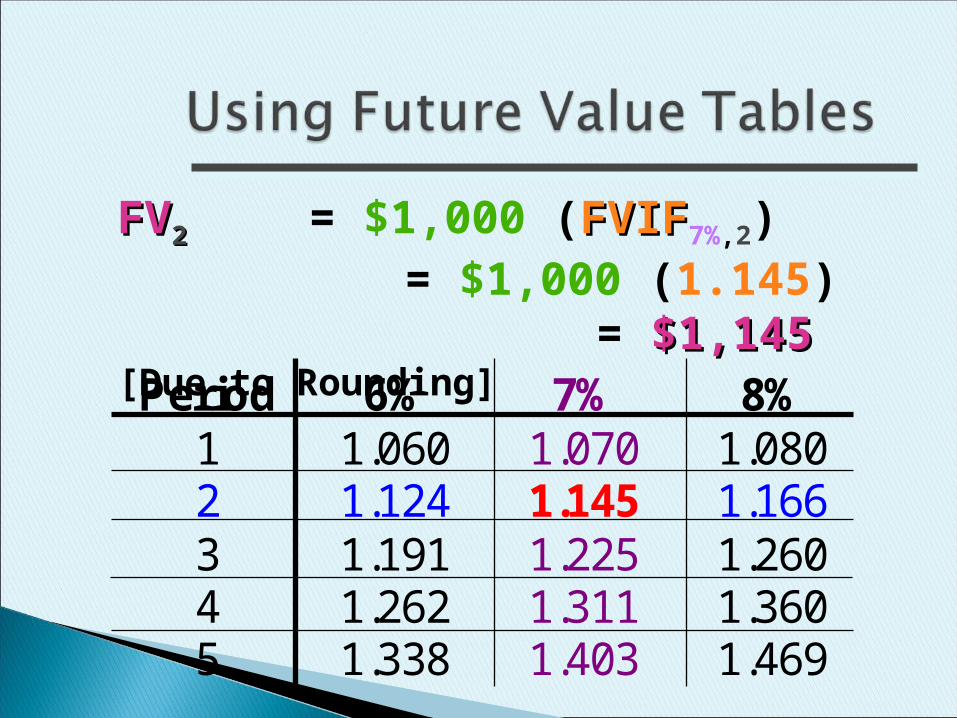

FVFV22 = $1,000 (FVIFFVIF7%,2)= $1,000 (1.145)

= $1,145$1,145 [Due to Rounding]

Period 6% 7% 8%1 1.060 1.070 1.0802 1.124 1.145 1.1663 1.191 1.225 1.2604 1.262 1.311 1.3605 1.338 1.403 1.469

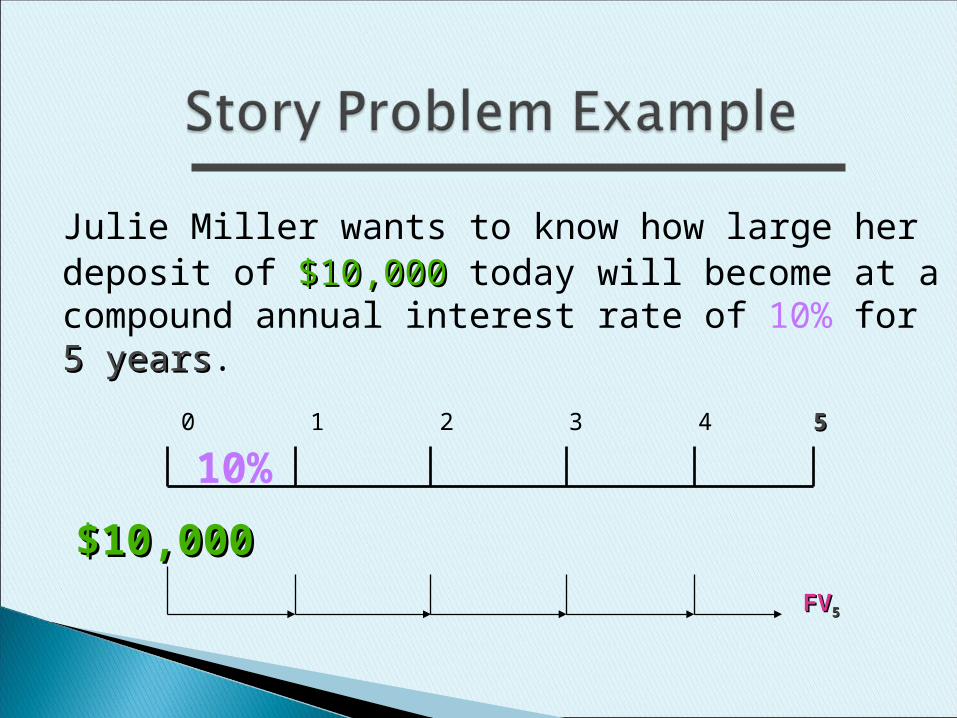

Julie Miller wants to know how large her deposit of $10,000$10,000 today will become at a compound annual interest rate of 10% for 5 5 yearsyears.

0 1 2 3 4 55

$10,000$10,000FVFV55

10%

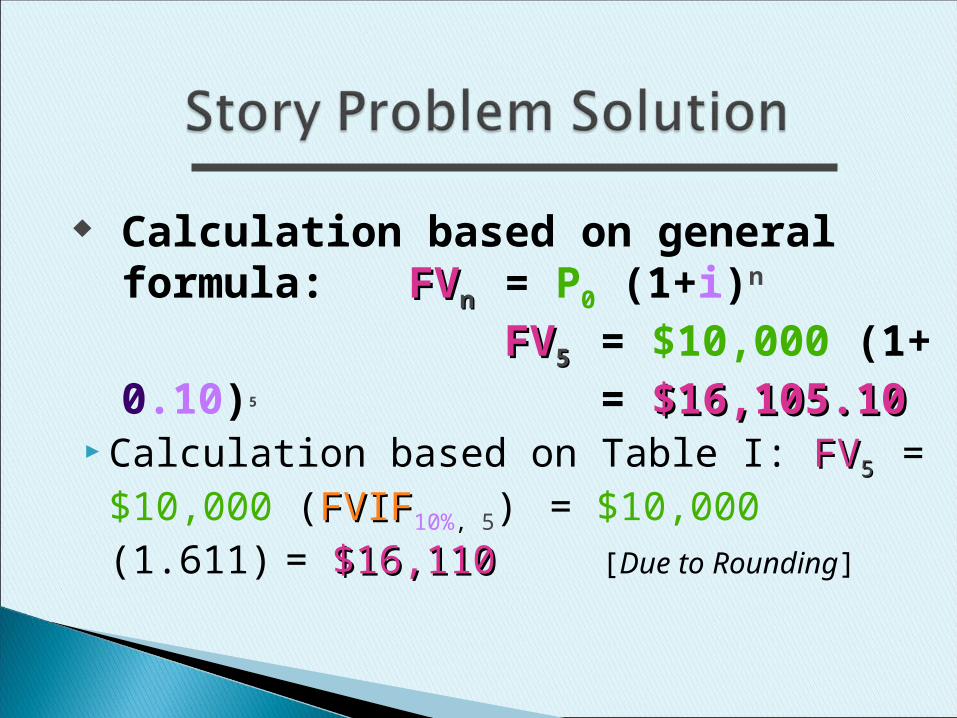

Calculation based on Table I:FVFV55 = $10,000 (FVIFFVIF10%, 5)

= $10,000 (1.611)= $16,110$16,110 [Due to

Rounding]

Calculation based on general formula:FVFVnn = P0 (1+i)n

FVFV55 = $10,000 (1+ 0.10)5

= $16,105.10$16,105.10

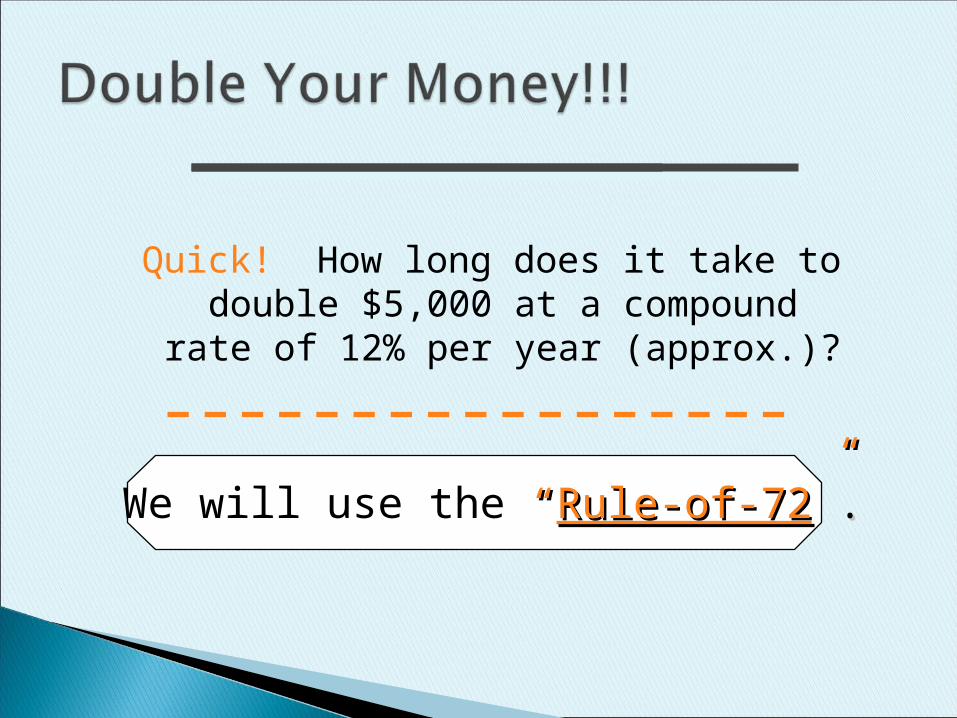

We will use the ““Rule-of-72Rule-of-72””..

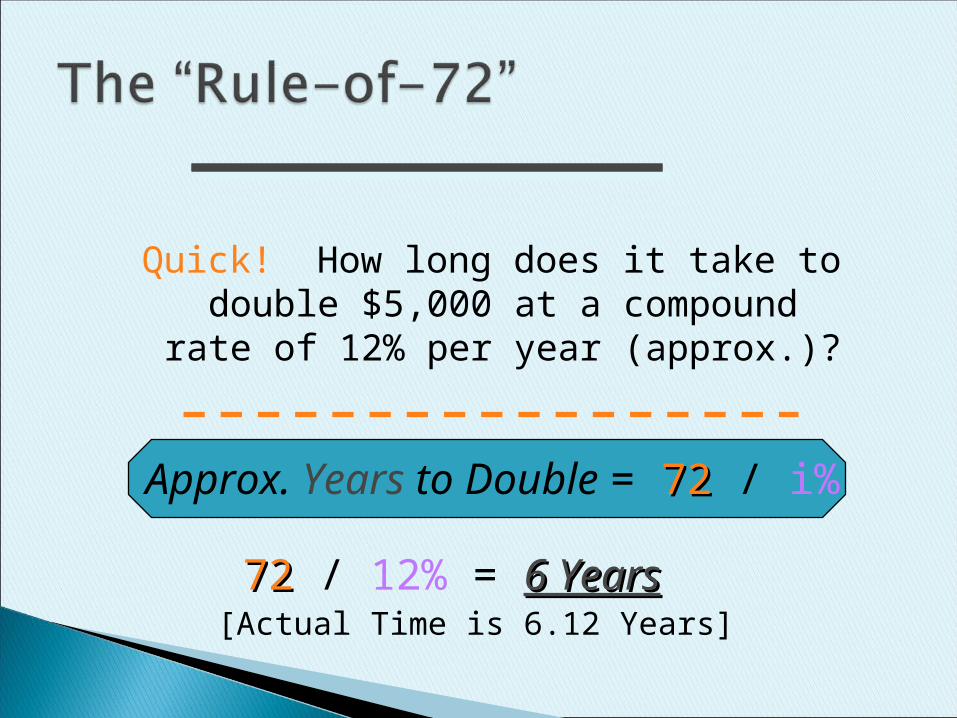

Quick! How long does it take to double $5,000 at a compound rate

of 12% per year (approx.)?

Approx. Years to Double = 7272 / i%

7272 / 12% = 6 Years6 Years[Actual Time is 6.12 Years]

Quick! How long does it take to double $5,000 at a compound rate

of 12% per year (approx.)?

Estimating Cost/Benefit for Engineering Projects

Incremental Cash Flows

Developing Cash Flow Statements

Generalized Cash Flow Approach

21

Elements of Investment Decision

• Identification of Investment Opportunities

• Generation of Cash Flows

• Measures of Investment Worth

• Project Selection

• Project Implementation

• Project-Control/Post-Audit

Our focus in this chapter is to

develop the format of after-tax cash flow statements.

22

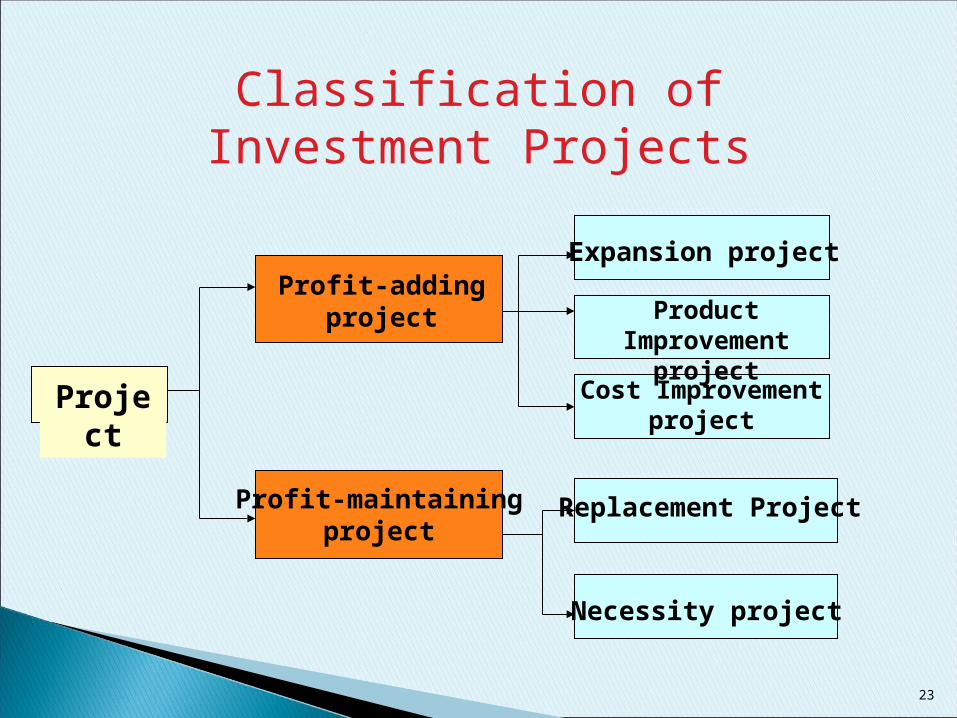

Classification of Investment Projects

Project

Profit-addingproject

Profit-maintainingproject

Expansion project

Product Improvement project

Necessity project

Replacement Project

Cost Improvementproject

23

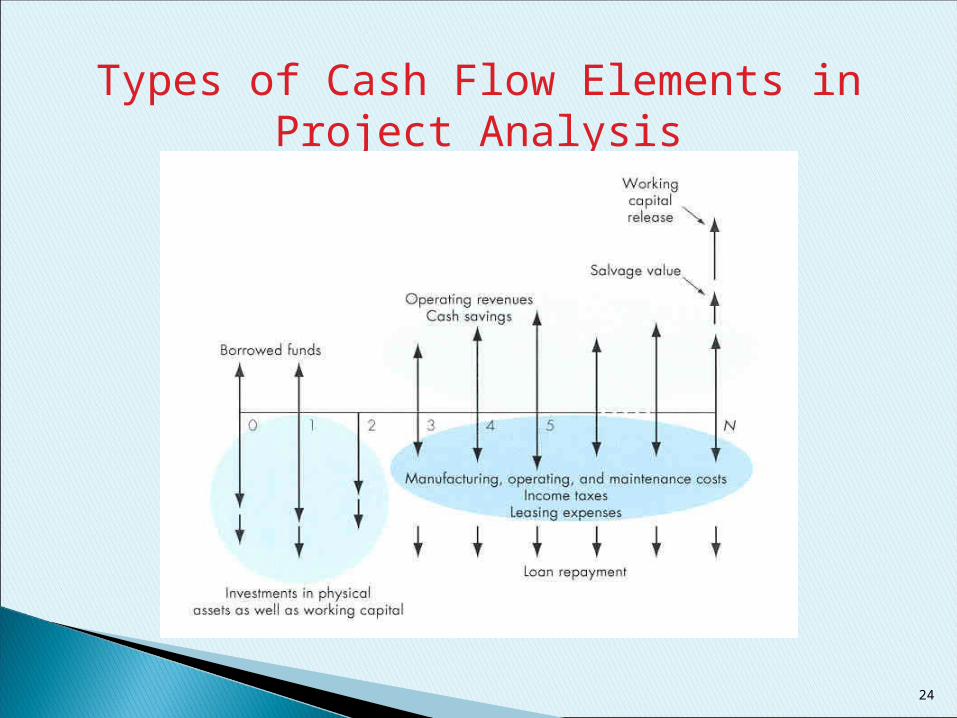

Types of Cash Flow Elements in Project Analysis

24

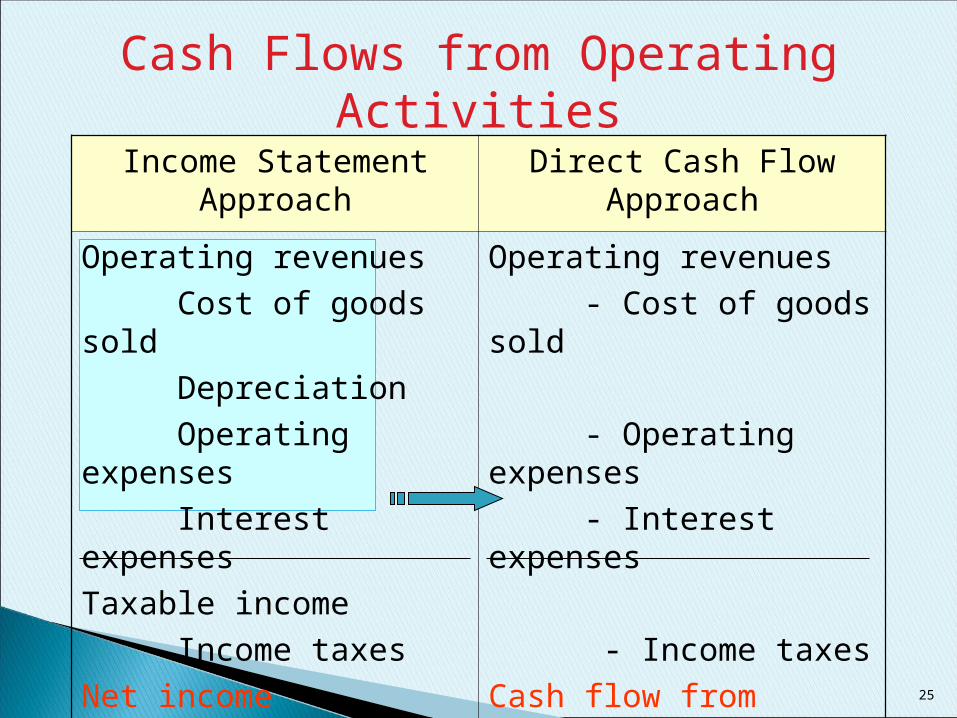

Income Statement Approach Direct Cash Flow Approach

Operating revenues

Cost of goods sold

Depreciation

Operating expenses

Interest expenses

Taxable income

Income taxes

Net income

+ Depreciation

Operating revenues

- Cost of goods sold

- Operating expenses

- Interest expenses

- Income taxes

Cash flow from operation

Cash Flows from Operating Activities

25

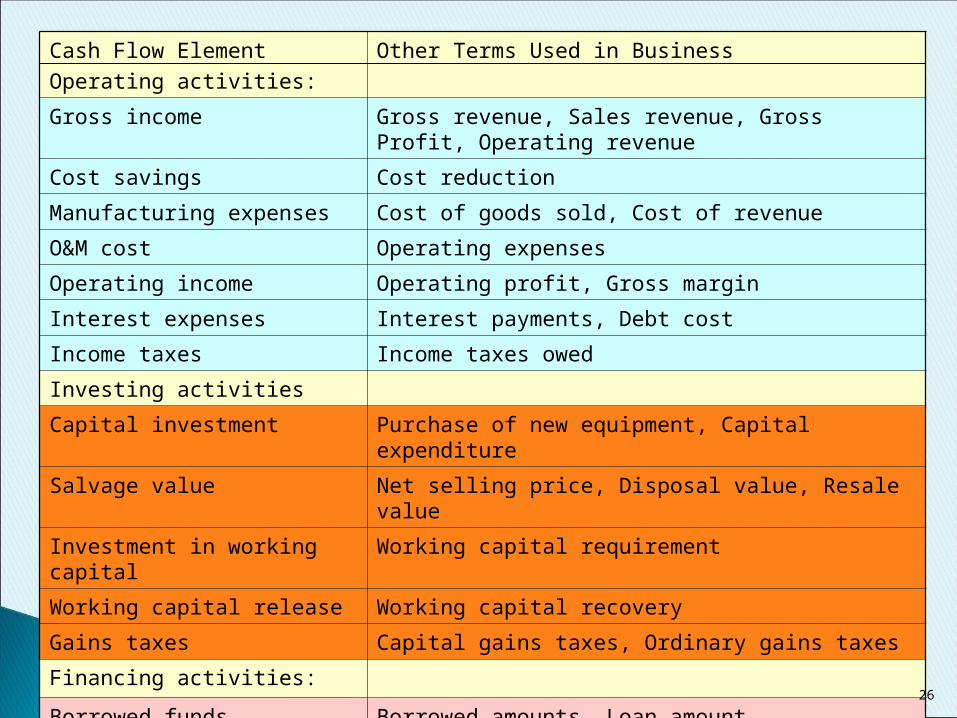

Cash Flow Element

Operating activities:

Other Terms Used in Business

Gross income Gross revenue, Sales revenue, Gross Profit, Operating revenue

Cost savings Cost reduction

Manufacturing expenses Cost of goods sold, Cost of revenue

O&M cost Operating expenses

Operating income Operating profit, Gross margin

Interest expenses Interest payments, Debt cost

Income taxes Income taxes owed

Investing activities

Capital investment Purchase of new equipment, Capital expenditure

Salvage value Net selling price, Disposal value, Resale value

Investment in working capital Working capital requirement

Working capital release Working capital recovery

Gains taxes Capital gains taxes, Ordinary gains taxes

Financing activities:

Borrowed funds Borrowed amounts, Loan amount

Principal repayments Loan repayment

26

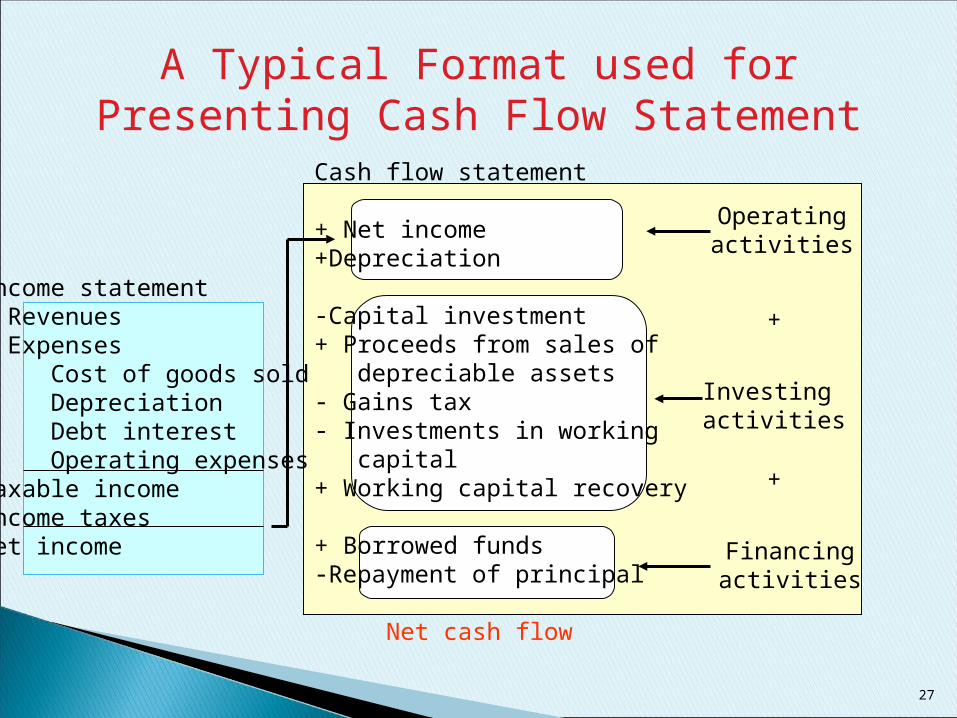

A Typical Format used for Presenting Cash Flow Statement

Income statement Revenues Expenses Cost of goods sold Depreciation Debt interest Operating expensesTaxable incomeIncome taxesNet income

Cash flow statement

+ Net income+Depreciation

-Capital investment+ Proceeds from sales of depreciable assets- Gains tax- Investments in working capital+ Working capital recovery

+ Borrowed funds-Repayment of principal Net cash flow

Operatingactivities

Investing activities

Financingactivities

+

+

27

defines depreciation as the ‘allocation of the depreciable amount of an asset over its estimated life’.

According to the matching concept, revenues should be matched with expenses in order to determine the accounting profit.

The cost of the asset purchased should be spread over the periods in which the asset will benefit a company.

The assets are acquired or constructed with the intention of being used and not with the intention for resale.

regards assets as depreciable when they◦ Are expected to be used in more than one

accounting period.◦ Have a finite useful life, and◦ Are held for use in the production or supply of

goods and services, for rental to others, or for administrative purposes.

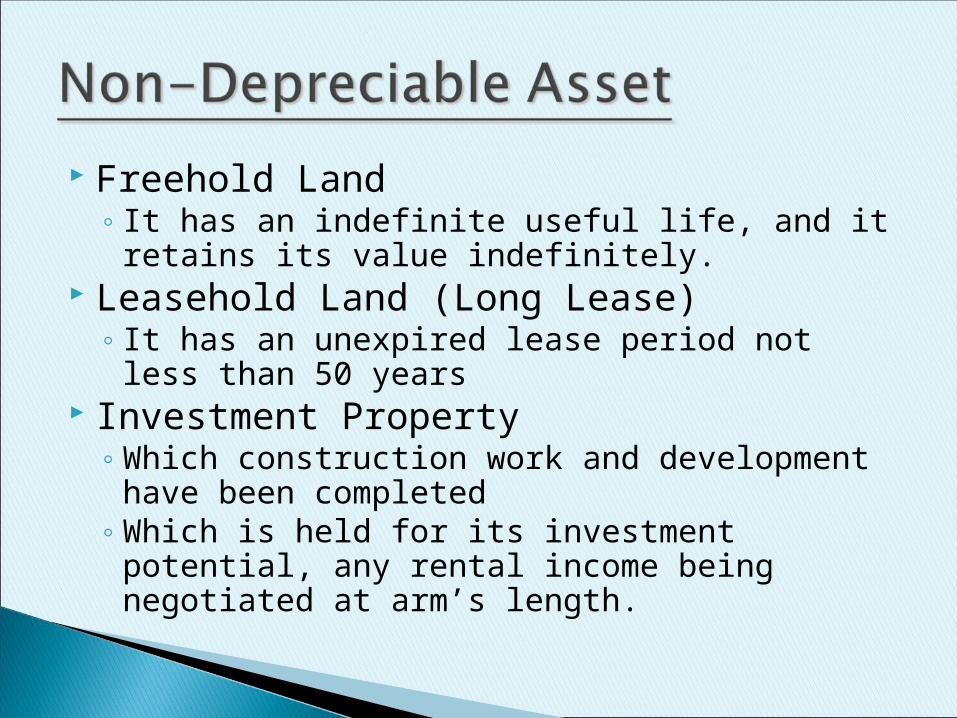

Freehold Land◦ It has an indefinite useful life, and it retains its

value indefinitely. Leasehold Land (Long Lease)

◦ It has an unexpired lease period not less than 50 years

Investment Property◦ Which construction work and development have

been completed◦ Which is held for its investment potential, any

rental income being negotiated at arm’s length.

Freehold Land◦ It has an indefinite useful life, and it retains its

value indefinitely. Leasehold Land (Long Lease)

◦ It has an unexpired lease period not less than 50 years

Investment Property◦ Which construction work and development have

been completed◦ Which is held for its investment potential, any

rental income being negotiated at arm’s length.

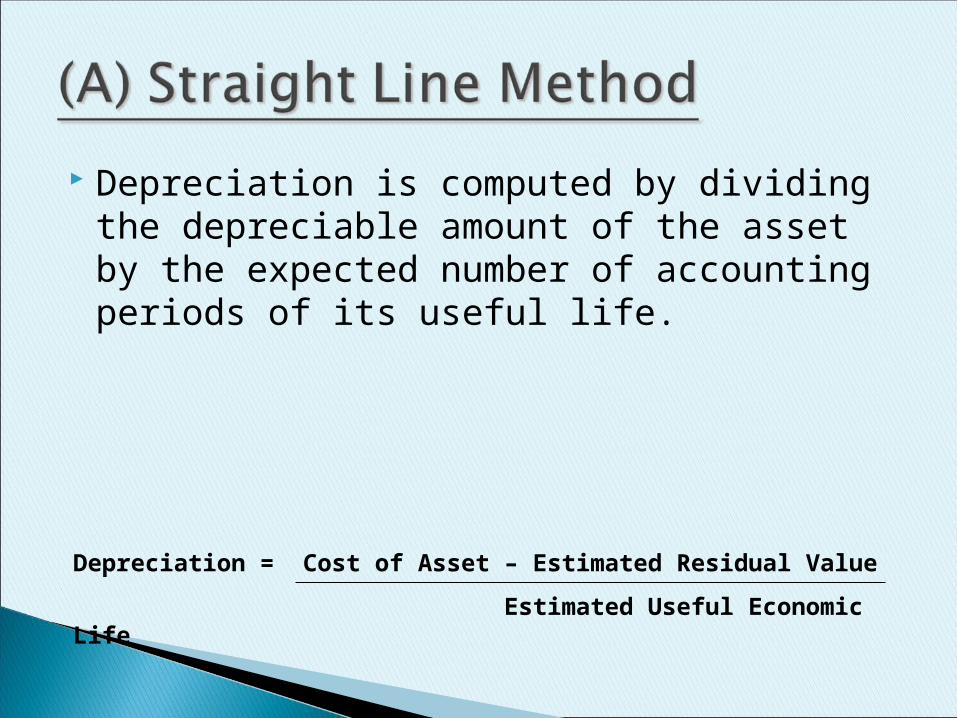

Depreciation is computed by dividing the depreciable amount of the asset by the expected number of accounting periods of its useful life.

Depreciation = Cost of Asset – Estimated Residual Value

Estimated Useful Economic Life

Useful economic life is not equal to physical life

It is the period over which the present owner intends to use the asset

It is the amount received after disposal of the asset

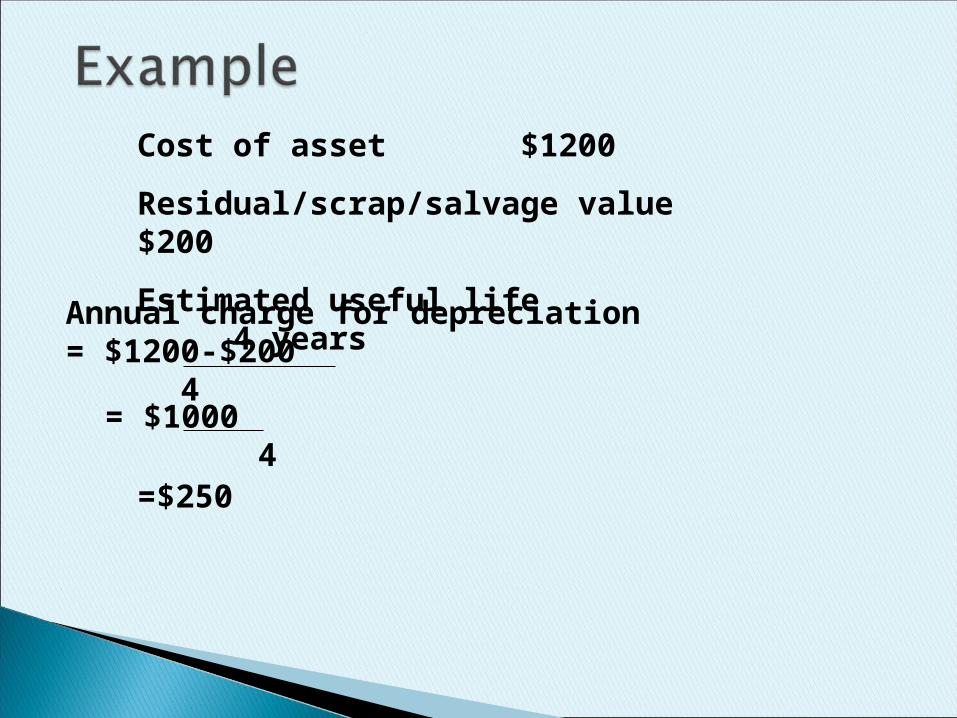

Cost of asset - Residual value = Total amount to be depreciated

Cost of asset $1200

Residual/scrap/salvage value $200

Estimated useful life 4 years

Annual charge for depreciation= $1200-$200

4= $1000 4=$250

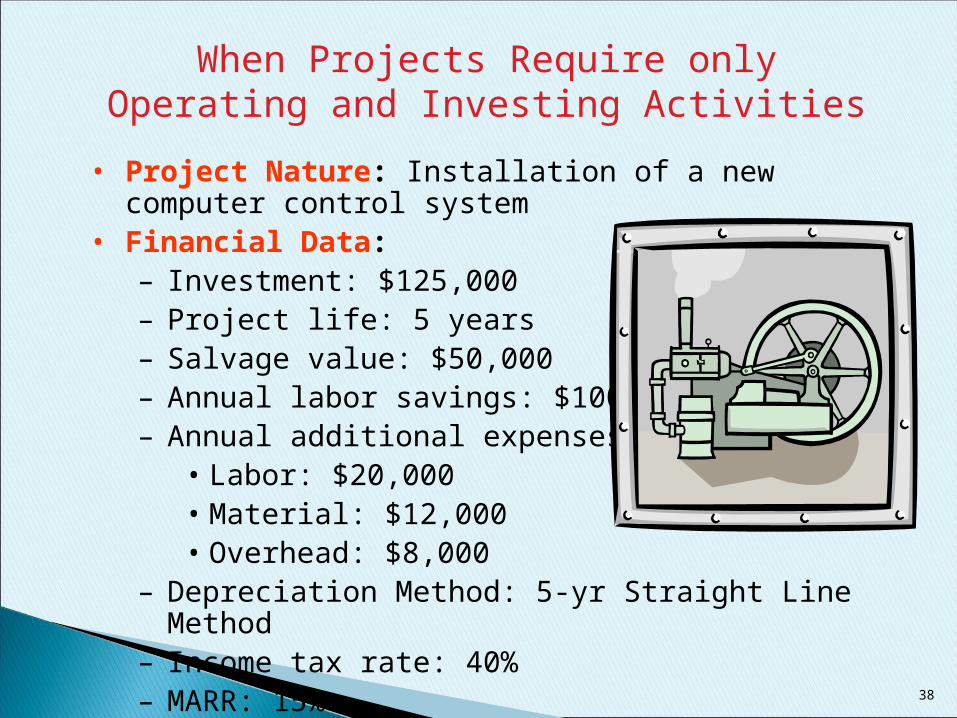

When Projects Require only Operating and Investing Activities

• Project Nature: Installation of a new computer control system • Financial Data:

– Investment: $125,000– Project life: 5 years– Salvage value: $50,000– Annual labor savings: $100,000– Annual additional expenses:

• Labor: $20,000• Material: $12,000• Overhead: $8,000

– Depreciation Method: 5-yr Straight Line Method– Income tax rate: 40%– MARR: 15%

38

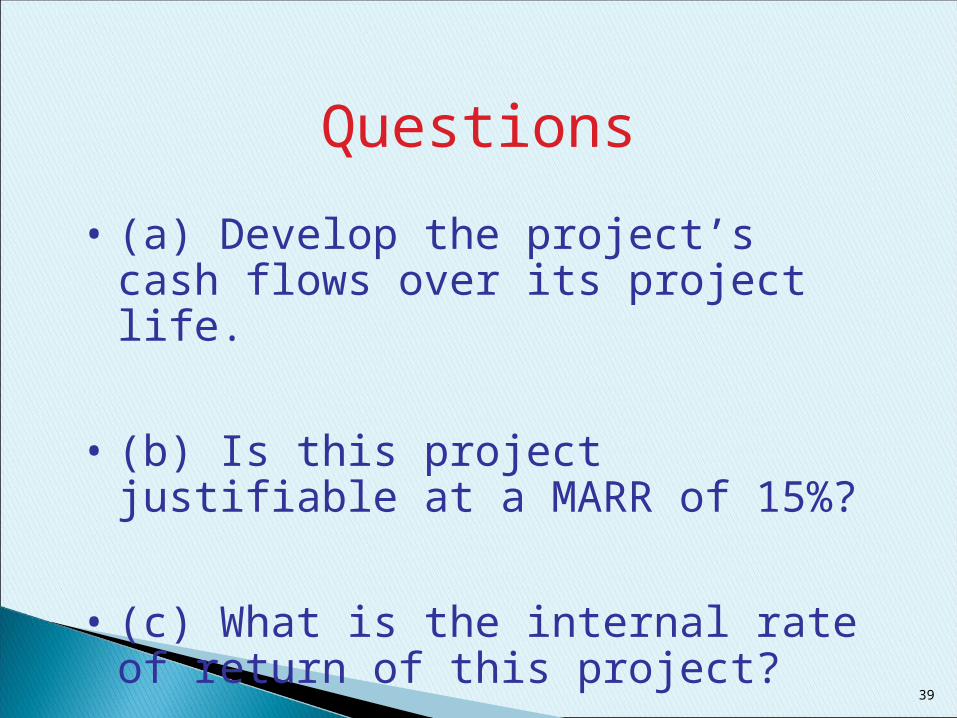

Questions

• (a) Develop the project’s cash flows over its project life.

• (b) Is this project justifiable at a MARR of 15%?

• (c) What is the internal rate of return of this project?

39

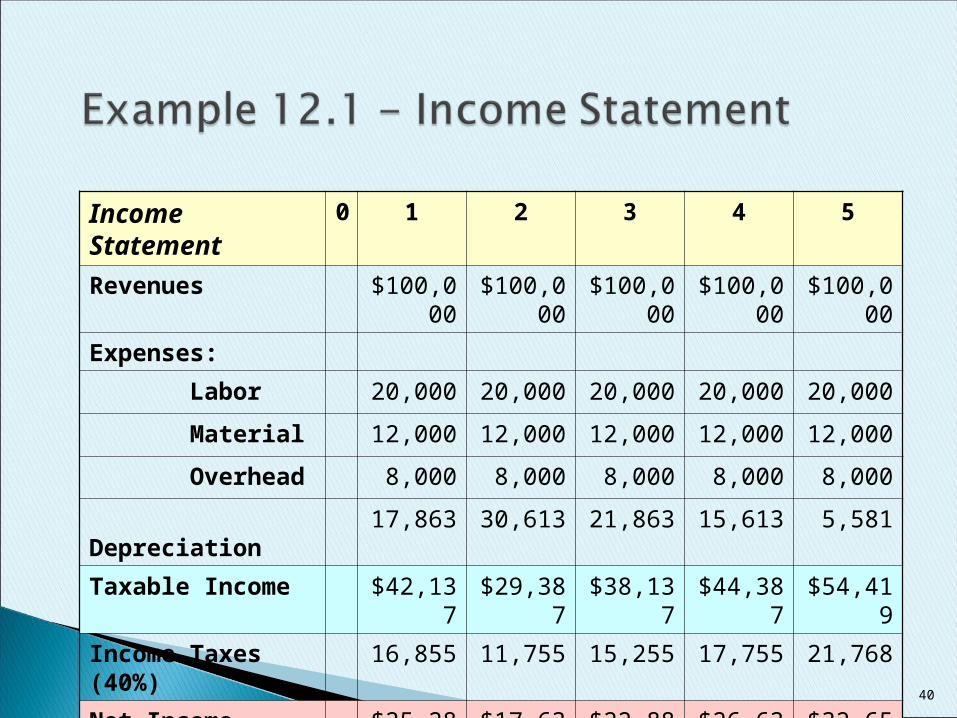

Income Statement 0 1 2 3 4 5

Revenues $100,000 $100,000 $100,000 $100,000 $100,000

Expenses:

Labor 20,000 20,000 20,000 20,000 20,000

Material 12,000 12,000 12,000 12,000 12,000

Overhead 8,000 8,000 8,000 8,000 8,000

Depreciation 17,863 30,613 21,863 15,613 5,581

Taxable Income $42,137 $29,387 $38,137 $44,387 $54,419

Income Taxes (40%) 16,855 11,755 15,255 17,755 21,768

Net Income $25,282 $17,632 $22,882 $26,632 $32,651

40

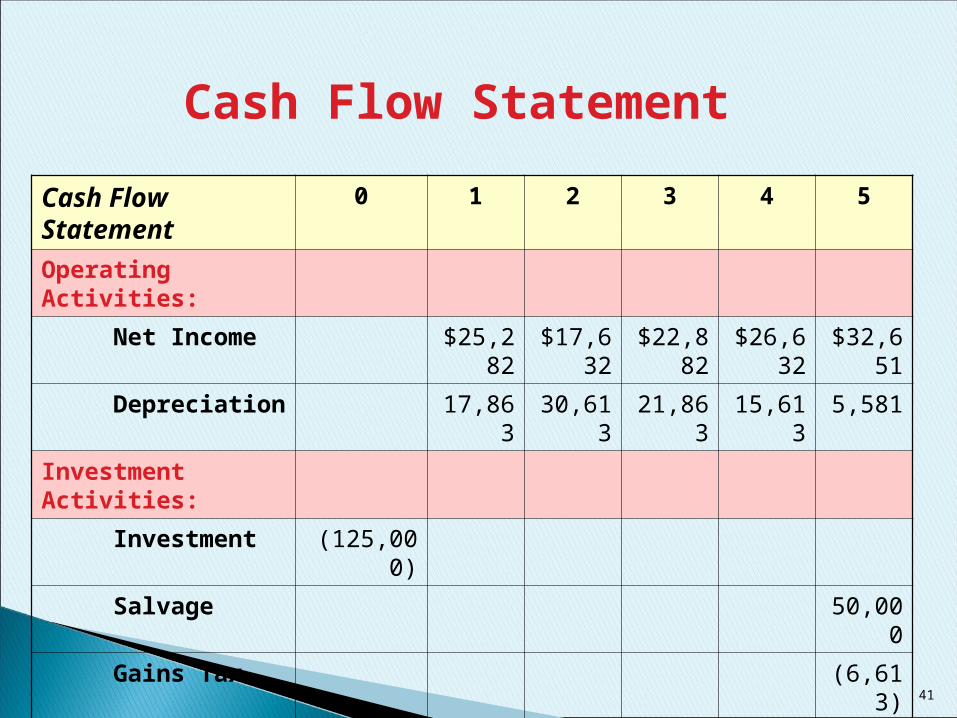

Cash Flow Statement

Cash Flow Statement 0 1 2 3 4 5

Operating Activities:

Net Income $25,282 $17,632 $22,882 $26,632 $32,651

Depreciation 17,863 30,613 21,863 15,613 5,581

Investment Activities:

Investment (125,000)

Salvage 50,000

Gains Tax (6,613)

Net Cash Flow ($125,000) $43,145 $48,245 $44,745 $42,245 $81,619

41

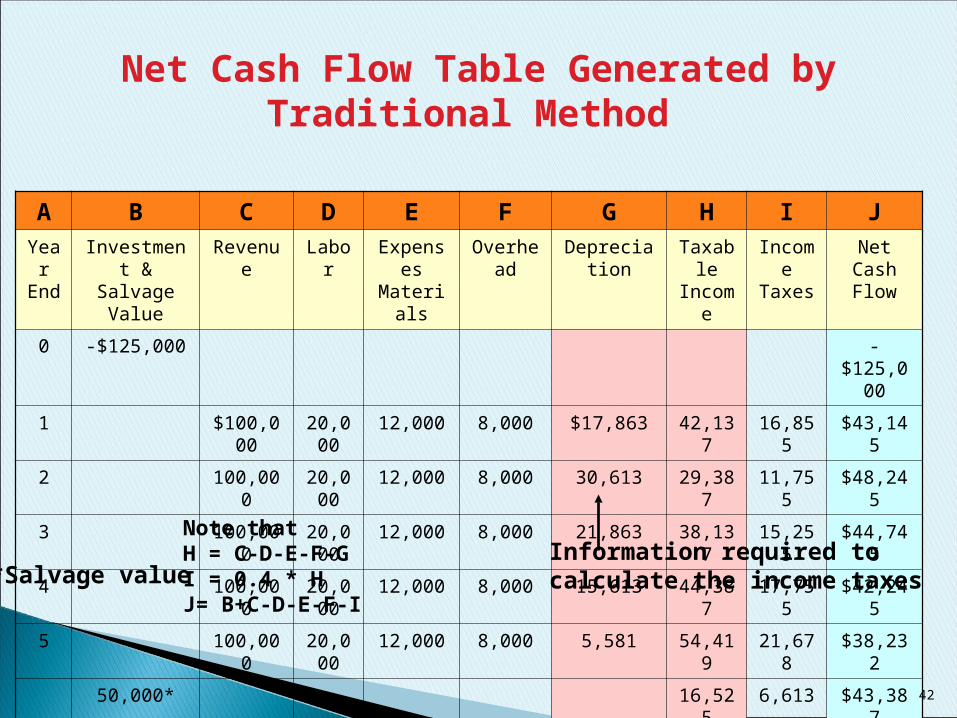

Net Cash Flow Table Generated by Traditional Method

A B C D E F G H I J

Year End

Investment & Salvage Value

Revenue Labor Expenses Materials

Overhead Depreciation

Taxable Income

Income Taxes

Net Cash Flow

0 -$125,000 -$125,000

1 $100,000 20,000

12,000 8,000 $17,863 42,137 16,855 $43,145

2 100,000 20,000

12,000 8,000 30,613 29,387 11,755 $48,245

3 100,000 20,000

12,000 8,000 21,863 38,137 15,255 $44,745

4 100,000 20,000

12,000 8,000 15,613 44,387 17,755 $42,245

5 100,000 20,000

12,000 8,000 5,581 54,419 21,678 $38,232

50,000* 16,525 6,613 $43,387

Information required tocalculate the income taxes*Salvage value

Note thatH = C-D-E-F-GI = 0.4 * HJ= B+C-D-E-F-I

42

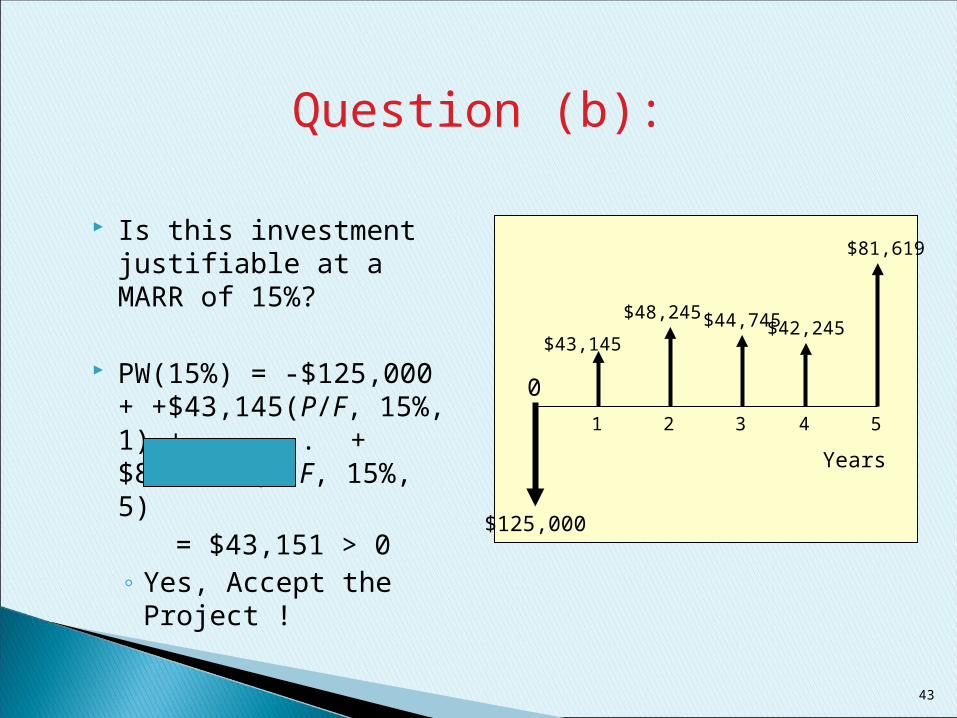

Is this investment justifiable at a MARR of 15%?

PW(15%) = -$125,000 + +$43,145(P/F, 15%, 1) + . . . . + $81,620 (P/F, 15%, 5)

= $43,151 > 0 ◦ Yes, Accept the

Project !

Question (b):

0

1 2 3 4 5

$125,000

$43,145

$48,245 $44,745 $42,245

$81,619

Years

43

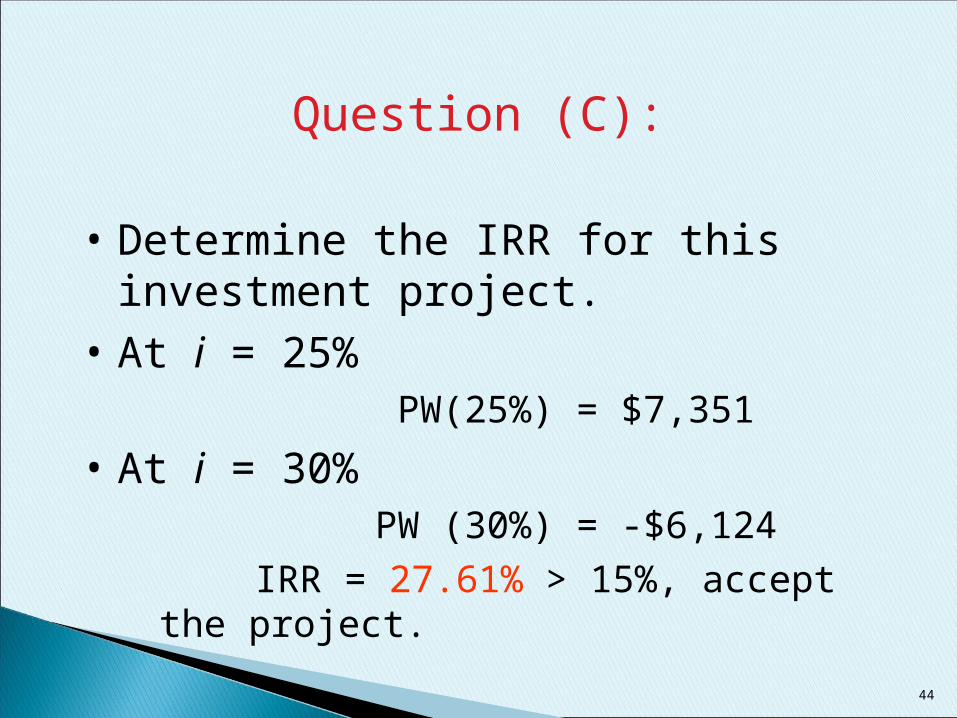

Question (C):

• Determine the IRR for this investment project.

• At i = 25% PW(25%) = $7,351

• At i = 30% PW (30%) = -$6,124

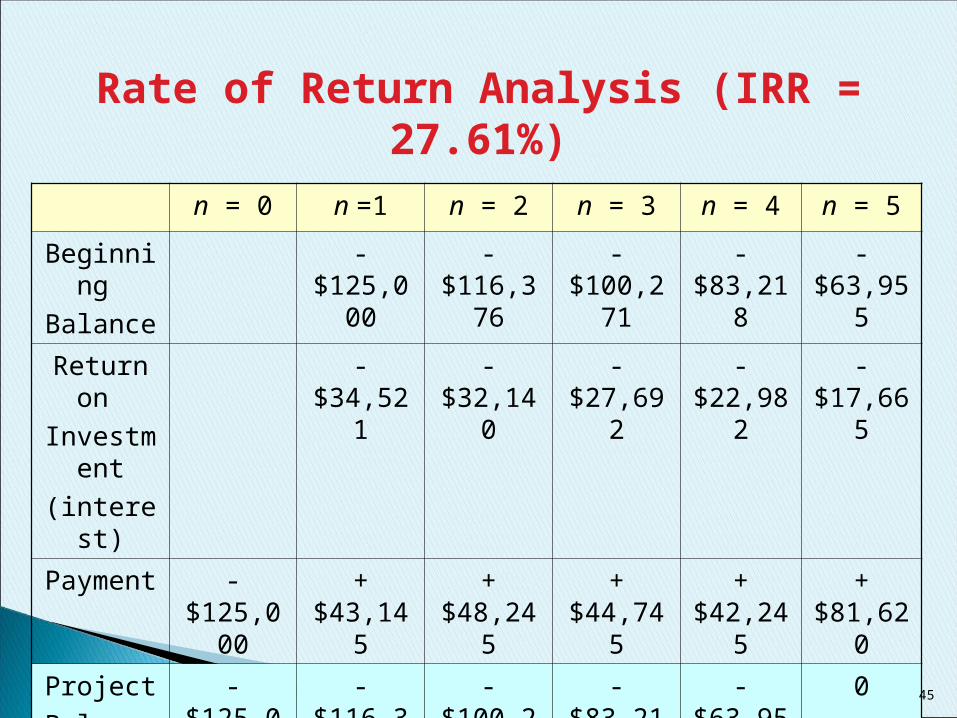

IRR = 27.61% > 15%, accept the project.

44

Rate of Return Analysis (IRR = 27.61%)

n = 0 n =1 n = 2 n = 3 n = 4 n = 5

Beginning

Balance

-$125,000

-$116,376

-$100,271

-$83,218 -$63,955

Return on

Investment

(interest)

-$34,521 -$32,140 -$27,692 -$22,982 -$17,665

Payment -$125,000

+$43,145 +$48,245 +$44,745 +$42,245

+$81,620

Project

Balance

-$125,000

-$116,376

-$100,271

-$83,218 -$63,955 0

45

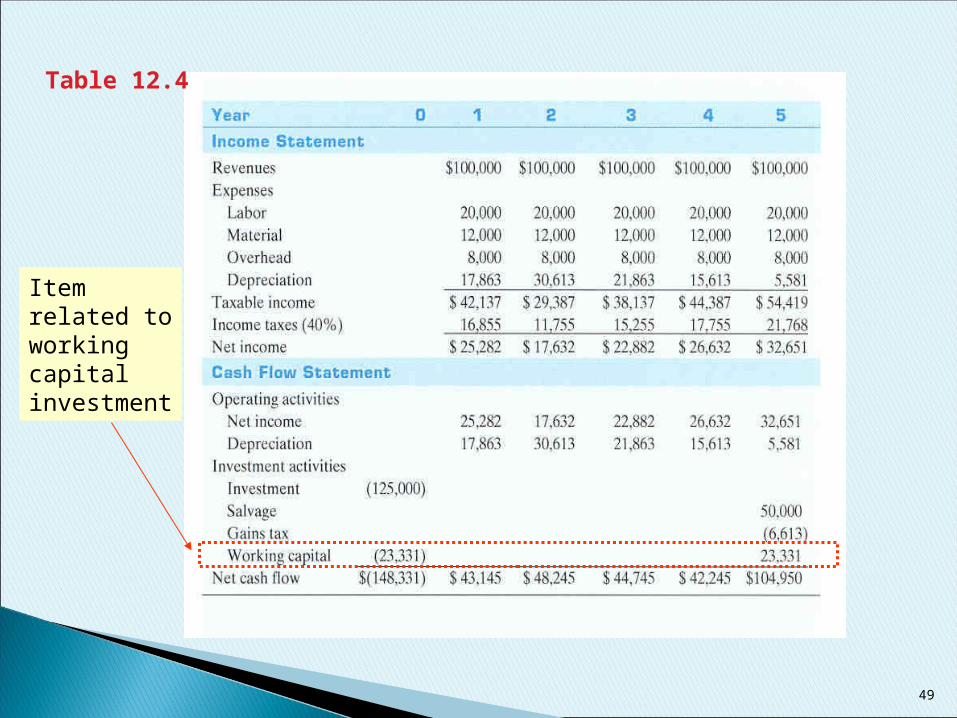

Working capital means the amount carried in cash, accounts receivable, and inventory that is available to meet day-to-day operating needs.

How to treat working capital investments: just like a capital expenditure except that no depreciation is allowed.

46

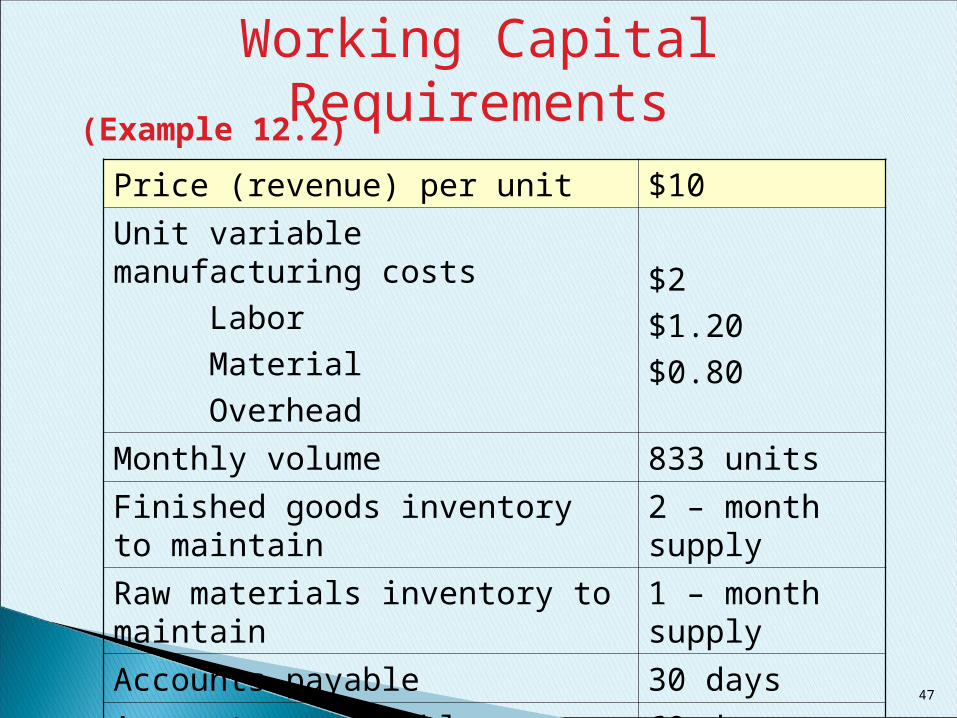

Working Capital Requirements

Price (revenue) per unit $10

Unit variable manufacturing costs

Labor

Material

Overhead

$2

$1.20

$0.80

Monthly volume 833 units

Finished goods inventory to maintain 2 – month supply

Raw materials inventory to maintain 1 – month supply

Accounts payable 30 days

Accounts receivable 60 days

(Example 12.2)

47

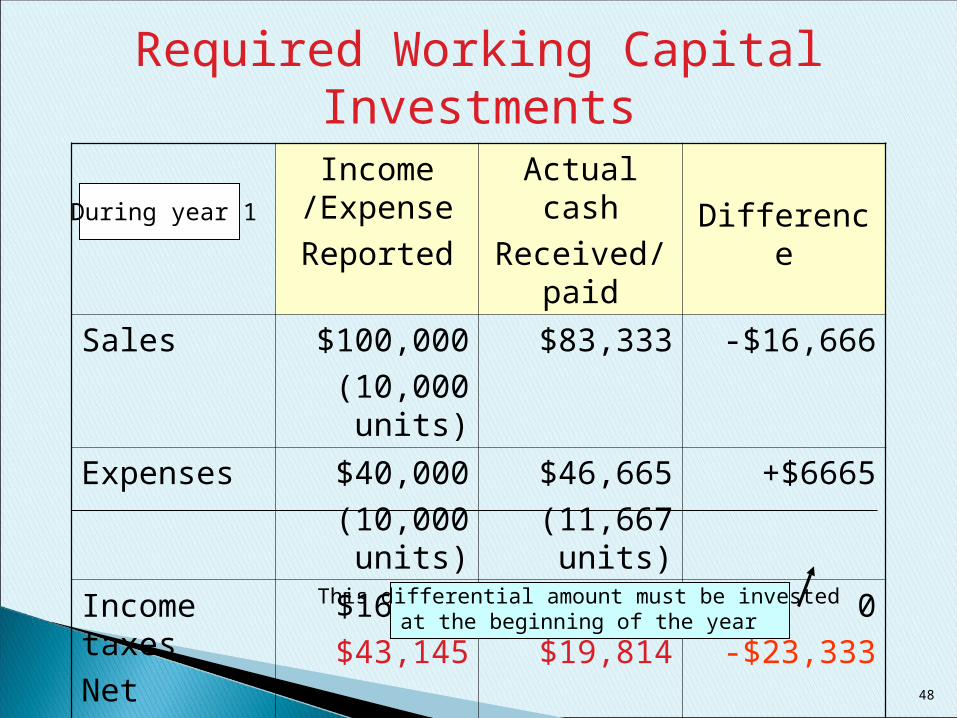

Income /Expense

Reported

Actual cash

Received/paid Difference

Sales $100,000

(10,000 units)

$83,333 -$16,666

Expenses $40,000

(10,000 units)

$46,665

(11,667 units)

+$6665

Income taxes

Net amount

$16,855

$43,145

$16,855

$19,814

0

-$23,333

During year 1

Required Working Capital Investments

This differential amount must be investedat the beginning of the year

48

Table 12.4

Item related toworkingcapitalinvestment

49

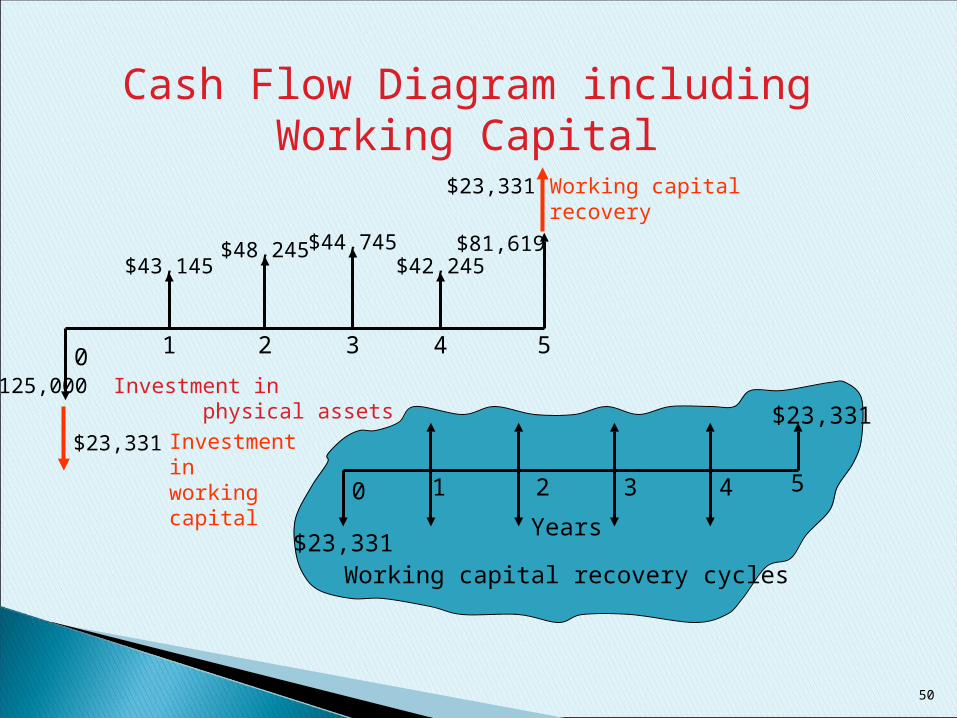

Cash Flow Diagram including Working Capital

0 1 2 3 4 5

$23,331Years

$23,331

Working capital recovery cycles

0 1 2 3 4 5

$43,145$48,245 $44,745

$42,245$81,619

Working capitalrecovery

$23,331

$125,000 Investment in physical assets

$23,331 Investment inworking capital

50

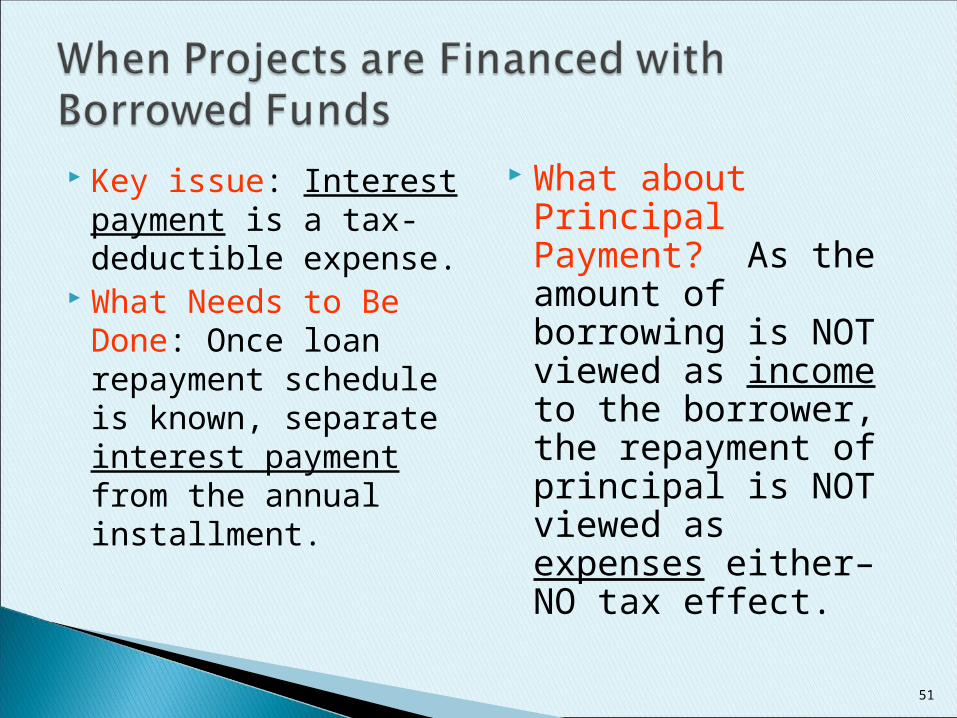

Key issue: Interest payment is a tax-deductible expense.

What Needs to Be Done: Once loan repayment schedule is known, separate interest payment from the annual installment.

What about Principal Payment? As the amount of borrowing is NOT viewed as income to the borrower, the repayment of principal is NOT viewed as expenses either– NO tax effect.

51

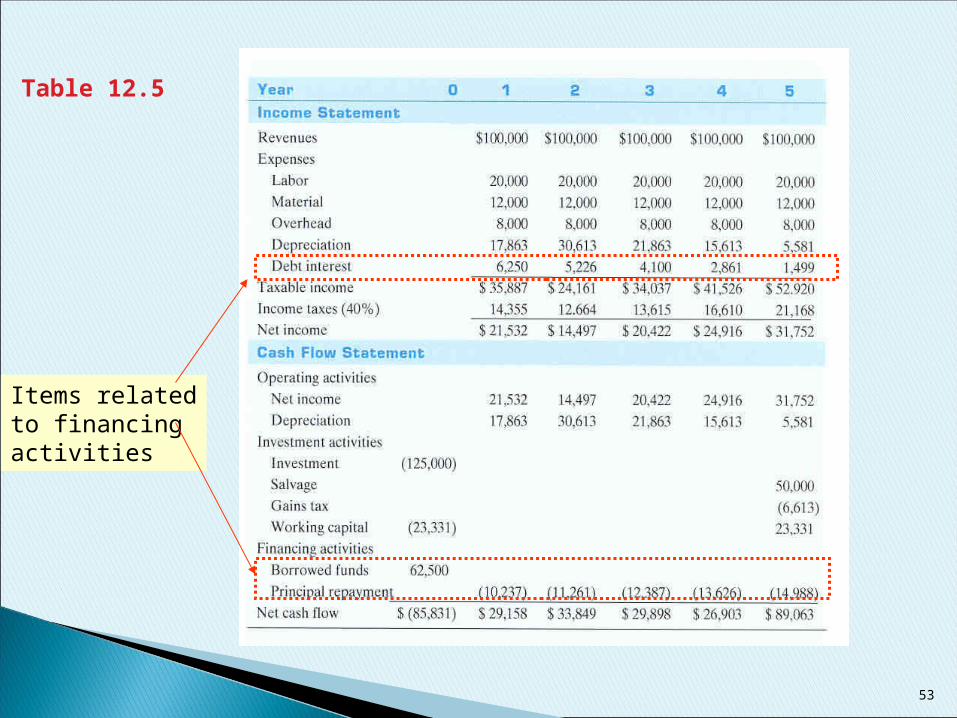

Loan Repayment Schedule (Example 12.4)

End of

Year

Beginning

Balance

Interest Payment

Principal Payment

Ending

Balance

1 $62,500 $6,250 $10,237 $52,263

2 52,263 5,226 11,261 41,002

3 41,002 4,100 12,387 28,615

4 28,615 2,861 13,626 14,989

5 14,989 1,499 14,988 0

Amount financed: $62,500, or 50% of total capital expenditureFinancing rate: 10% per yearAnnual installment: $16,487 or, A = $62,500(A/P, 10%, 5)

$16,487

52

Items relatedto financingactivities

Table 12.5

53

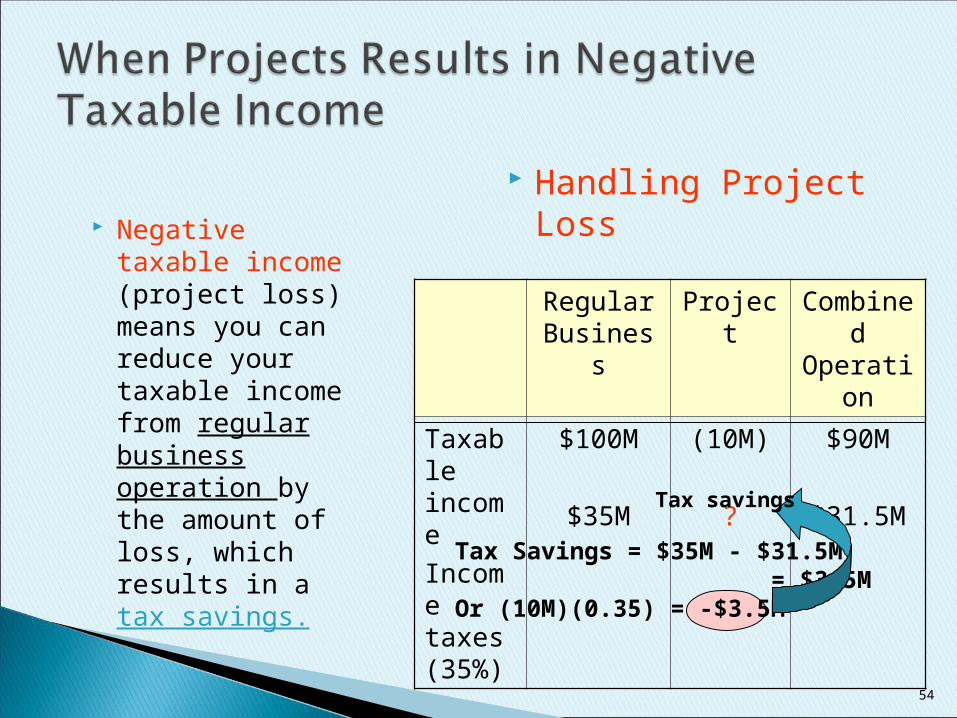

Negative taxable income (project loss) means you can reduce your taxable income from regular business operation by the amount of loss, which results in a tax savings.

Handling Project Loss

Regular Business

Project Combined Operation

Taxable income

Income taxes (35%)

$100M

$35M

(10M)

?

$90M

$31.5M

Tax Savings = $35M - $31.5M = $3.5MOr (10M)(0.35) = -$3.5M

Tax savings

54

When to Use: When undertaking a project does not change a company’s marginal tax rate.

Pros: The cash flows can be generated more quickly.

Cons: The process is less intuitive and not commonly understood by business people.

55

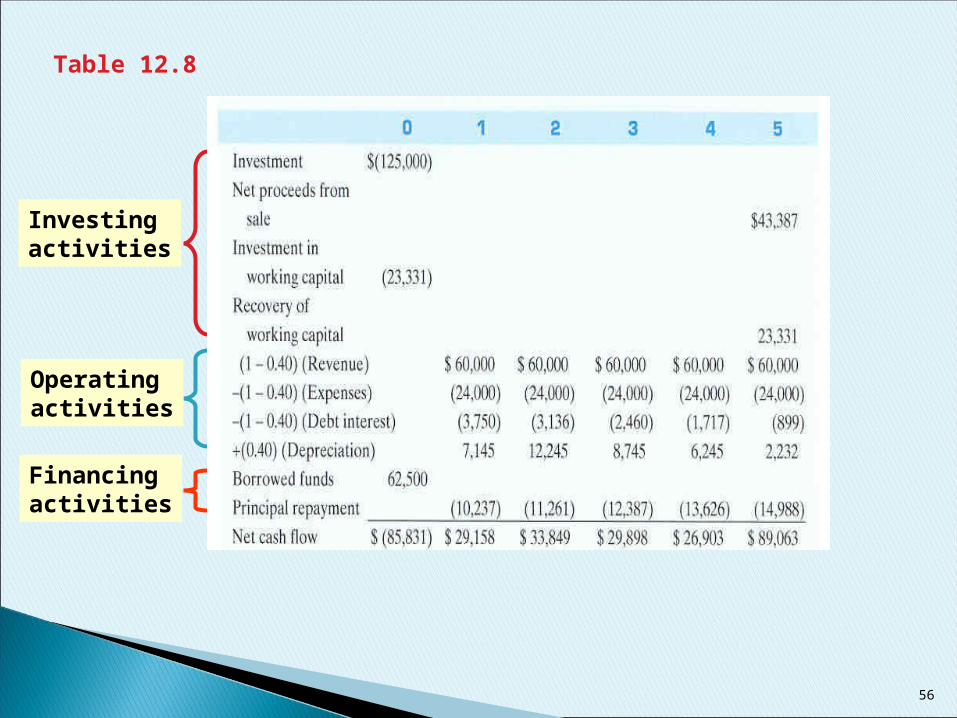

Table 12.8

Investing activities

Operatingactivities

Financingactivities

56

Summary

• Identifying and estimating relevant project cash flows is perhaps the most challenging aspect of engineering economic analysis. All cash flows can be organized into one of the following three categories:

1. Operating activities.2. Investing activities3. Financing activities.

57

•Cash Items

1. New investment and disposal of existing assets

2. Salvage value (or net selling price)

3. Working capital

4. Working capital release

5. Cash revenues/savings

6. Manufacturing, operating, and maintenance costs.

7. Interest and loan payments

8. Taxes and tax credits

58

• Non-cash items1. Depreciation expenses2. Amortization expenses

• The income statement approach is typically used in organizing project cash flows. This approach groups cash flows according to whether they are operating, investing, or financing functions.

• The generalized cash flow approach to organizing cash flows can be used when a project does not change a company’s marginal tax rate. The cash flows can be generated more quickly and the formatting of the results is less elaborate than with the income statement approach. However, the generalized approach is less intuitive and not commonly understood by business people.

59

Top Related