WHY INVEST IN TURKEY? · The convenient location has enabled Turkey to tap significant export...

20

WHY INVEST IN TURKEY? July 2019

Transcript of WHY INVEST IN TURKEY? · The convenient location has enabled Turkey to tap significant export...

WHY INVEST IN TURKEY? July 2019

Strategic Location

Robust Economy

Domestic market + EU

Business-friendly

Benign R&D Ecosystem

Opportunities

Favorable Demographics

Skilled workforce with cost advantage

Lucrative Incentives

Continuous reform process..

REFORMS

OPENfor BUSINESS

Why invest

in Turkey?10 reasons to invest in Turkey.

WHY

INVEST IN

TURKEY?

Real GDP Growth (Index: 2002=100)Ranking of Economies by GDP at PPP

100

120

140

160

180

200

220

240

260

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

Source: TurkStat, OECD, World Bank, IMF, PPP: Purchasing Power Parity

13TH

LARGEST

ECONOMY 5.5 4.0 3.9 2.8 2.1

Robust

EconomyTrack record growth and bright future with proven resilience.

Average Annual GDP Growth (%), 2003-2018

Turkey Poland Romania Czechia Hungary

2003 2018

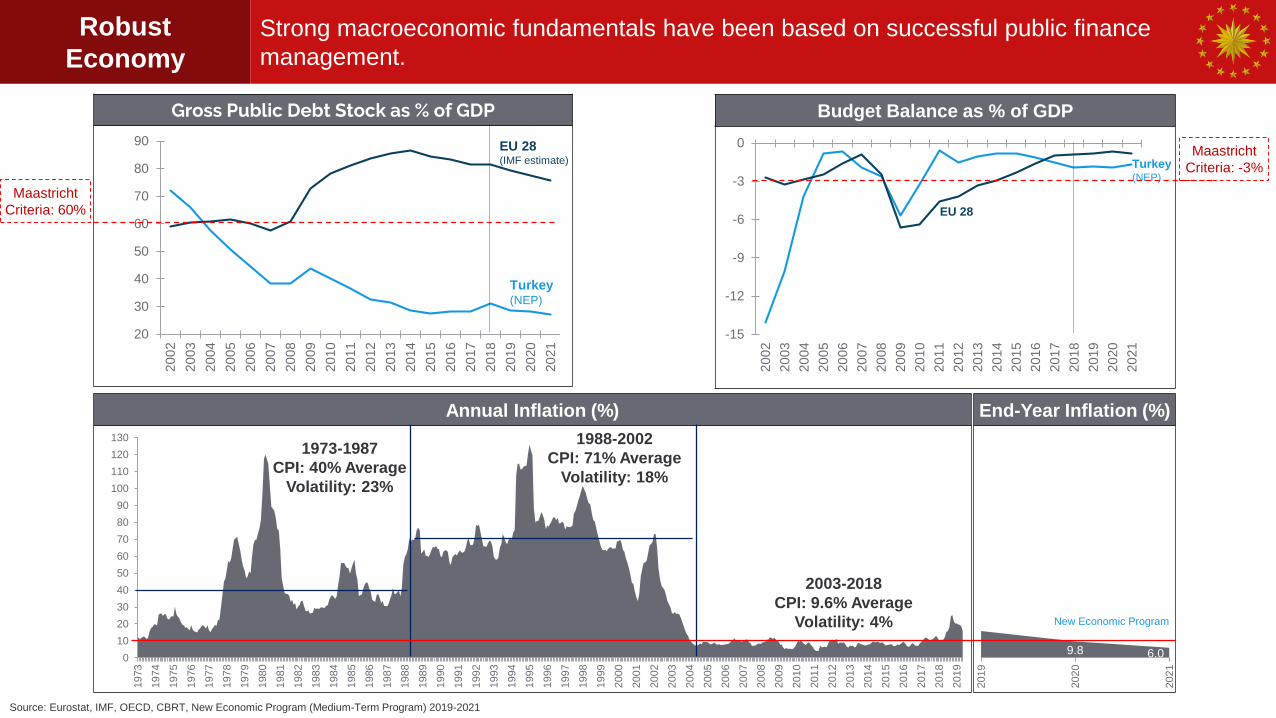

Budget Balance as % of GDPGross Public Debt Stock as % of GDP

Source: Eurostat, IMF, OECD, CBRT, New Economic Program (Medium-Term Program) 2019-2021

Robust

Economy

Strong macroeconomic fundamentals have been based on successful public finance

management.

-15

-12

-9

-6

-3

0

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

30

40

50

60

70

80

90

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

Turkey(NEP)

EU 28 (IMF estimate) Turkey

(NEP)

EU 28

Maastricht

Criteria: 60%

Maastricht

Criteria: -3%

End-Year Inflation (%)Annual Inflation (%)

0

10

20

30

40

50

60

70

80

90

100

110

120

130

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2003-2018

CPI: 9.6% Average

Volatility: 4%

1988-2002

CPI: 71% Average

Volatility: 18%

1973-1987

CPI: 40% Average

Volatility: 23%

9.8 6.0

2019

2020

2021

New Economic Program

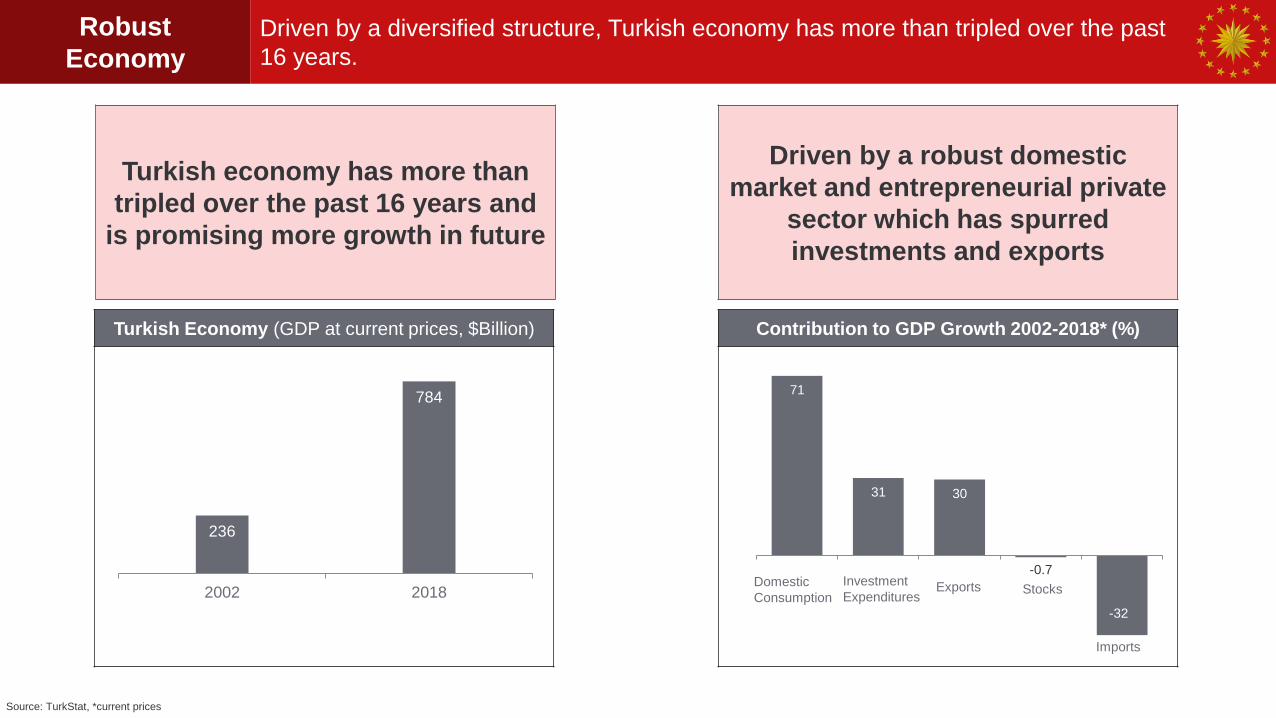

Contribution to GDP Growth 2002-2018* (%)

71

31 30

-0.7

-32

Turkish Economy (GDP at current prices, $Billion)

Turkish economy has more than

tripled over the past 16 years and

is promising more growth in future

Source: TurkStat, *current prices

Domestic

Consumption

Investment

Expenditures Stocks

Imports

Exports

236

784

2002 2018

Driven by a robust domestic

market and entrepreneurial private

sector which has spurred

investments and exports

Robust

Economy

Driven by a diversified structure, Turkish economy has more than tripled over the past

16 years.

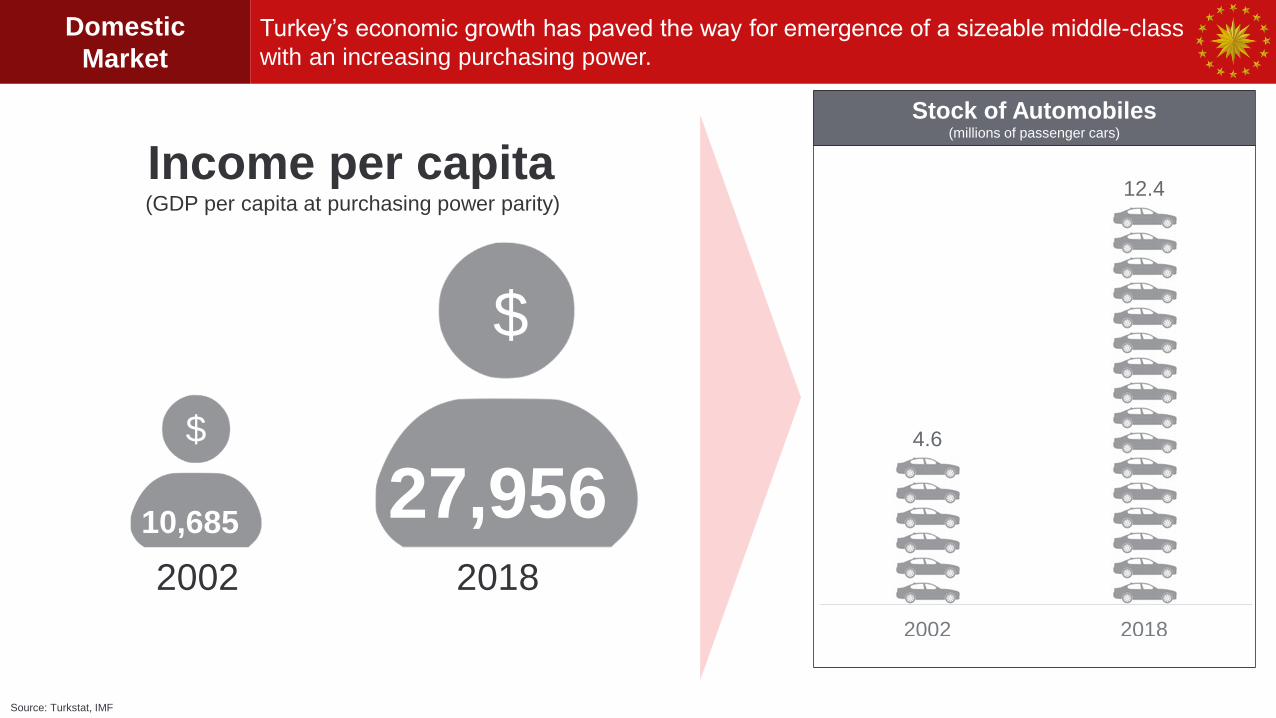

Stock of Automobiles(millions of passenger cars)

Source: Turkstat, IMF

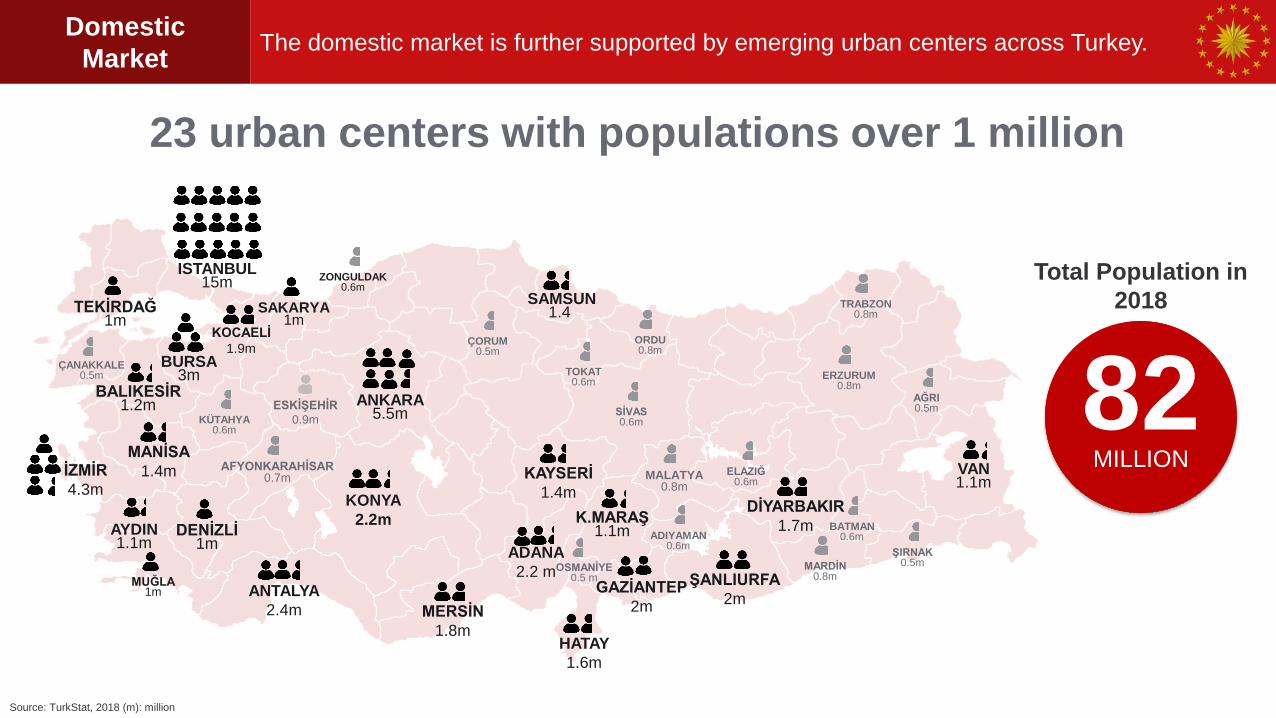

Domestic

Market

Turkey’s economic growth has paved the way for emergence of a sizeable middle-class

with an increasing purchasing power.

4.6

12.4

2002 2018

10,685

$

27,956

$

Income per capita(GDP per capita at purchasing power parity)

2002 2018

Source: TurkStat, 2018 (m): million

Domestic

MarketThe domestic market is further supported by emerging urban centers across Turkey.

23 urban centers with populations over 1 million

ISTANBUL15m

ANKARA5.5m

İZMİR

4.3m

BURSA3m

ANTALYA

2.4m

ADANA

2.2 m

KONYA

2.2m

ŞANLIURFA

2mGAZİANTEP

2m

KOCAELİ

1.9m

MERSİN

1.8m

DİYARBAKIR

1.7m

HATAY

1.6m

MANİSA

1.4m KAYSERİ

1.4m

SAMSUN1.4

BALIKESİR1.2m

K.MARAŞ1.1m

VAN1.1m

AYDIN1.1m

TEKİRDAĞ1m

DENİZLİ1m

SAKARYA1m

82MILLION

MUĞLA1m

ESKİŞEHİR

0.9m

MARDİN0.8m

TRABZON0.8m

MALATYA0.8m

ORDU0.8m

ERZURUM0.8m

AFYONKARAHİSAR0.7m

SİVAS0.6m

ADIYAMAN0.6m

TOKAT0.6m

ZONGULDAK0.6m

BATMAN0.6m

ELAZIĞ0.6m

KÜTAHYA0.6m

ÇANAKKALE0.5m

AĞRI0.5m

ÇORUM0.5m

OSMANİYE0.5 m

ŞIRNAK0.5m

Total Population in

2018

Source: Eurostat, Population as of 2017, Ministry of Economy

* In ratification process

Access to

in 27 countries

with Free Trade

Agreements

Customs

Union with the

EU allows

direct access

to the EU

Market+

+

Free Access

to

945million consumers

Domestic

Market + EUDomestic market + EU market + Free Trade Area

355million in

FTA Area

82million in

Turkey

510million

in EU

Strategic

Locationto manufacture, export and manage…

Production base for MENA

Its largest production facility worldwide

Exporting 85% of its production

Exporting 77% of its production

67 countries

80 countries

60 countries

30 countries

89 countries

72 countries

80 countries

63 countries

PROXIMITY TO

MAJOR

MARKETS1.5 billion people and $24T GDP

in Europe, MENA and Central

Asia at 4 hour flight-distance

CONNECTIVITYTurkish Airlines connects you to 255

destinations in 122 countries

MANUFACTURING

& EXPORT HUB

FOR

MULTINATIONALS

AS WELL AS

MANAGEMENT

HUB FOR

MULTINATIONALS

25 countries

Strategic

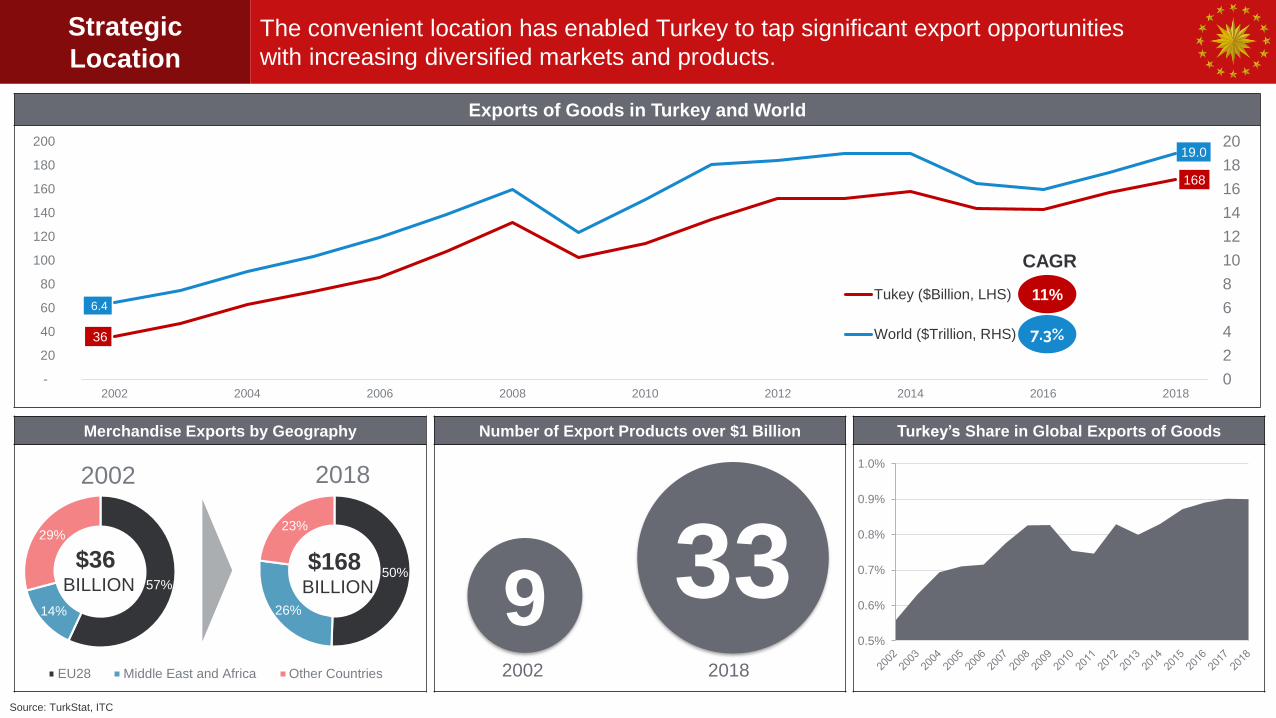

Location

The convenient location has enabled Turkey to tap significant export opportunities

with increasing diversified markets and products.

Merchandise Exports by Geography

Exports of Goods in Turkey and World

Source: TurkStat, ITC

36

168

6.4

19.0

0

2

4

6

8

10

12

14

16

18

20

-

20

40

60

80

100

120

140

160

180

200

2002 2004 2006 2008 2010 2012 2014 2016 2018

Tukey ($Billion, LHS)

World ($Trillion, RHS) 7.3%

57%

14%

29%

2002

EU28 Middle East and Africa Other Countries

50%

26%

23%

2018

Number of Export Products over $1 Billion

9 332002 2018

Turkey’s Share in Global Exports of Goods

$36 BILLION

$168 BILLION

0.5%

0.6%

0.7%

0.8%

0.9%

1.0%

11%

CAGR

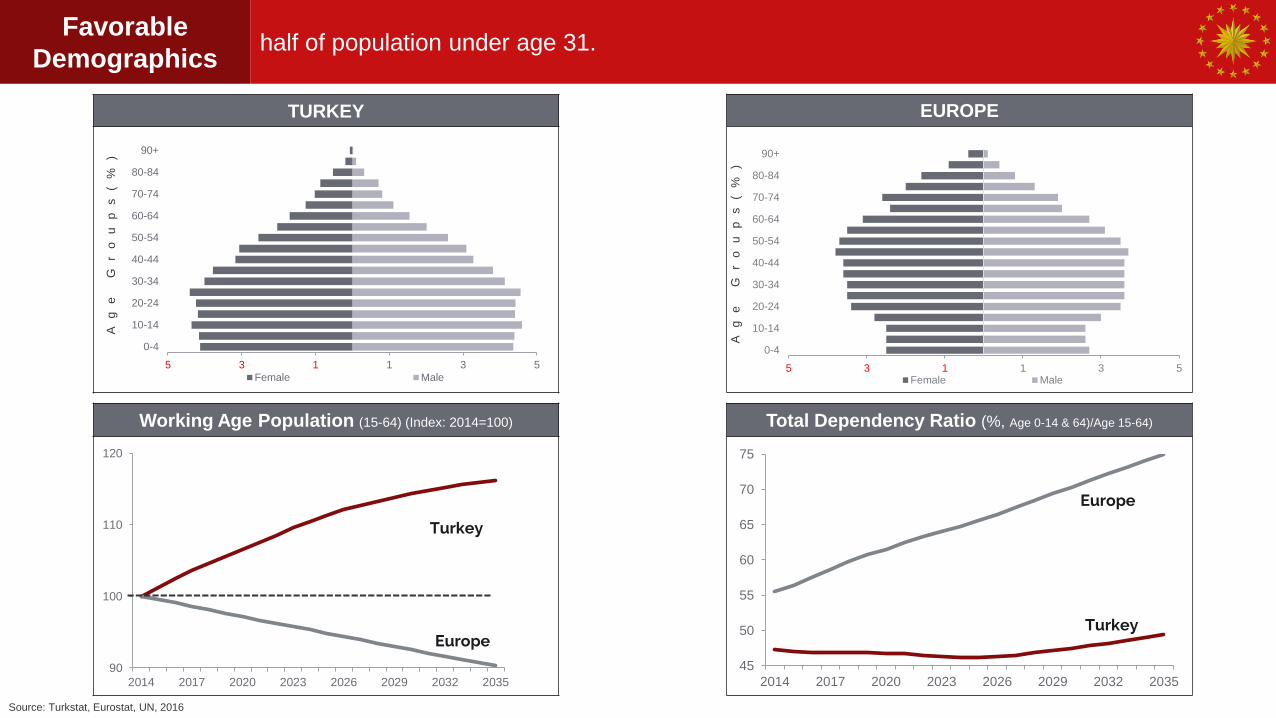

Working Age Population (15-64) (Index: 2014=100) Total Dependency Ratio (%, Age 0-14 & 64)/Age 15-64)

45

50

55

60

65

70

75

2014 2017 2020 2023 2026 2029 2032 2035

Europe

Turkey

90

100

110

120

2014 2017 2020 2023 2026 2029 2032 2035

Europe

Turkey

TURKEY EUROPE

5 3 1 1 3 5

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90+

Female Male5 3 1 1 3 5

0-4

10-14

20-24

30-34

40-44

50-54

60-64

70-74

80-84

90+

Female Male

Source: Turkstat, Eurostat, UN, 2016

Ag

e

Gr

ou

ps

(%

)

Ag

e

Gr

ou

ps

(%

)

Favorable

Demographicshalf of population under age 31.

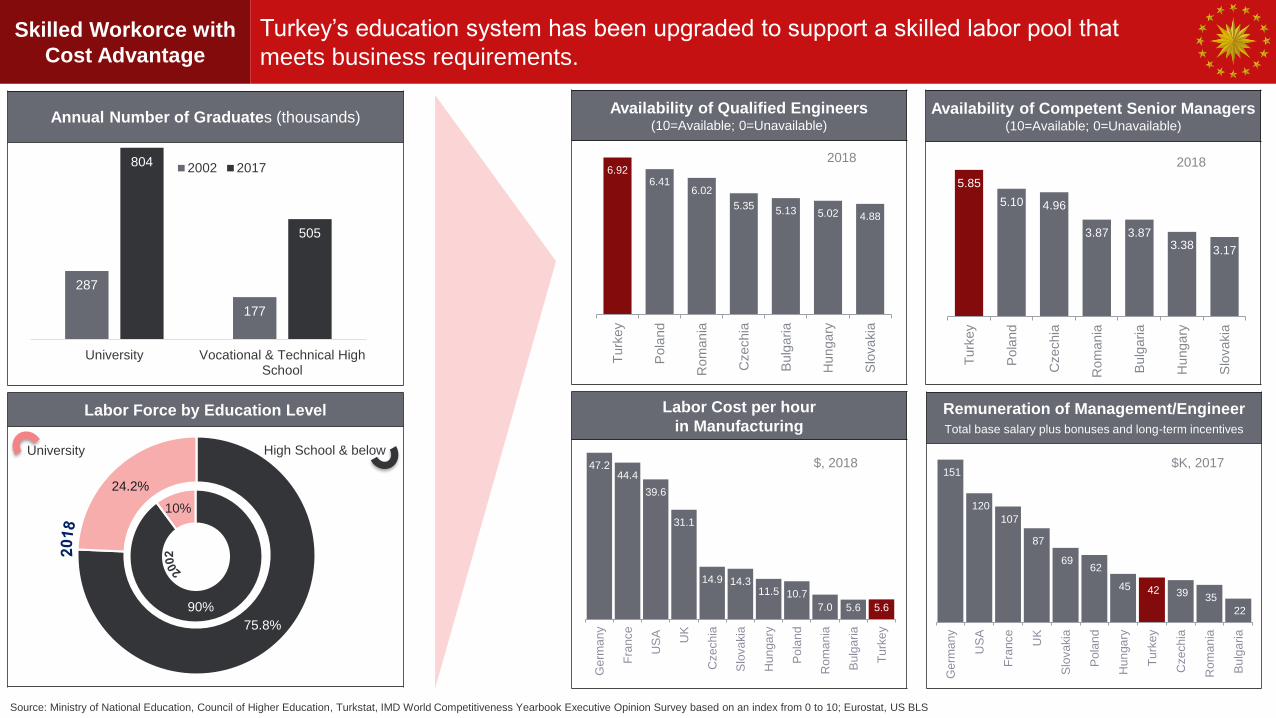

Labor Force by Education Level

75.8%

24.2%

90%

10%

Availability of Competent Senior Managers (10=Available; 0=Unavailable)

Availability of Qualified Engineers(10=Available; 0=Unavailable)

6.926.41

6.02

5.35 5.13 5.02 4.88

Turk

ey

Pola

nd

Ro

man

ia

Czechia

Bulg

aria

Hu

nga

ry

Slo

vakia

Annual Number of Graduates (thousands)

Source: Ministry of National Education, Council of Higher Education, Turkstat, IMD World Competitiveness Yearbook Executive Opinion Survey based on an index from 0 to 10; Eurostat, US BLS

Skilled Workorce with

Cost Advantage

Turkey’s education system has been upgraded to support a skilled labor pool that

meets business requirements.

287

177

804

505

University Vocational & Technical HighSchool

2002 2017

University High School & below

Labor Cost per hour

in Manufacturing

5.85

5.10 4.96

3.87 3.873.38 3.17

Turk

ey

Pola

nd

Czechia

Ro

man

ia

Bulg

aria

Hu

nga

ry

Slo

vakia

47.244.4

39.6

31.1

14.9 14.311.5 10.7

7.0 5.6 5.6G

erm

an

y

Fra

nce

US

A UK

Czech

ia

Slo

va

kia

Hun

ga

ry

Po

lan

d

Ro

ma

nia

Bu

lga

ria

Tu

rke

y

2018 2018

Remuneration of Management/Engineer

Total base salary plus bonuses and long-term incentives

151

120

107

87

69 62

45 42 39 35

22

Ge

rma

ny

US

A

Fra

nce

UK

Slo

va

kia

Po

lan

d

Hun

ga

ry

Tu

rke

y

Czech

ia

Ro

ma

nia

Bu

lga

ria

$K, 2017$, 2018

FDI Regulatory Restrictiveness Index, 2018

Personal Data

Protection

Law

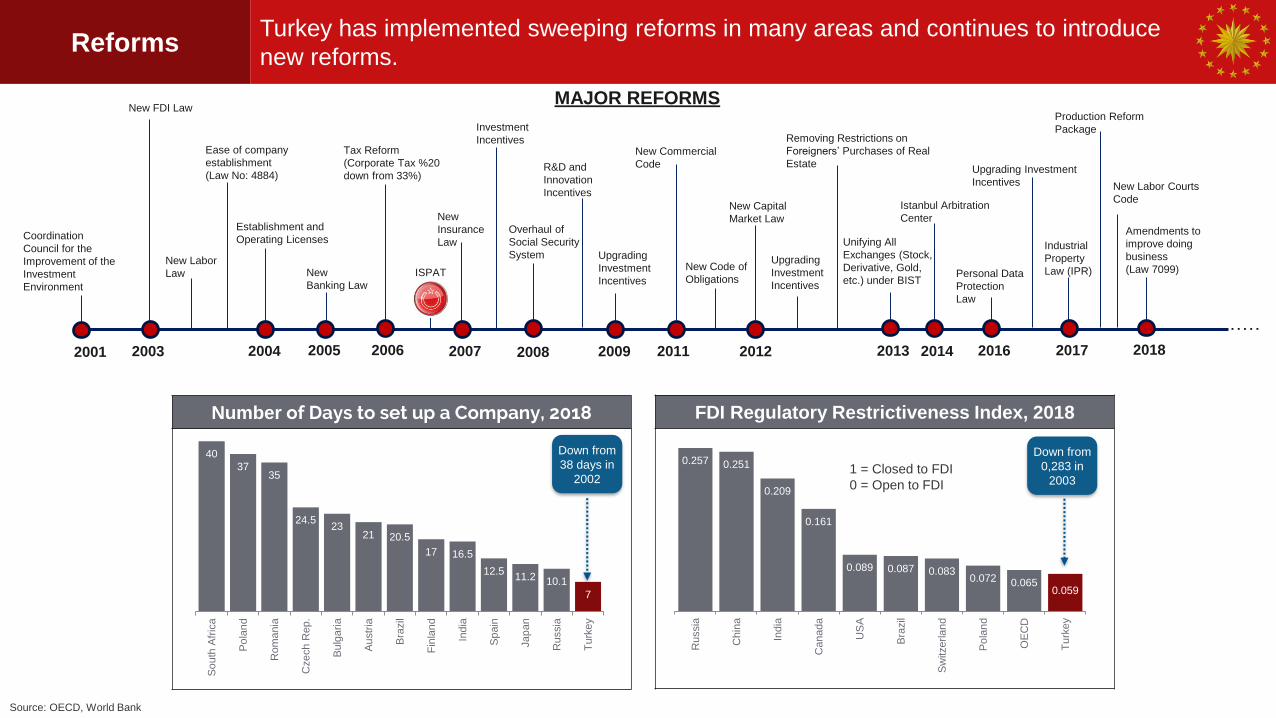

MAJOR REFORMS

0.257 0.251

0.209

0.161

0.089 0.087 0.0830.072 0.065

0.059

Russia

Chin

a

India

Canada

US

A

Bra

zil

Sw

itzerlan

d

Po

lan

d

OE

CD

Tu

rkey

1 = Closed to FDI

0 = Open to FDI

Source: OECD, World Bank

2006

Tax Reform

(Corporate Tax %20

down from 33%)

2003

New FDI Law

……

ISPAT

2005

New

Banking Law

2008

Overhaul of

Social Security

System

2011

New Commercial

Code

New Code of

Obligations

2012

New Capital

Market Law

New Labor

Law

2014

Istanbul Arbitration

Center

Ease of company

establishment

(Law No: 4884)

Investment

Incentives

R&D and

Innovation

Incentives

2009

Upgrading

Investment

Incentives

Upgrading

Investment

Incentives

2016

Upgrading Investment

Incentives

2007

New

Insurance

Law

Establishment and

Operating Licenses

2004

Removing Restrictions on

Foreigners’ Purchases of Real

Estate

2013

Unifying All

Exchanges (Stock,

Derivative, Gold,

etc.) under BIST

2001

Coordination

Council for the

Improvement of the

Investment

Environment

2017

Industrial

Property

Law (IPR)

Production Reform

Package

Down from

0,283 in

2003

ReformsTurkey has implemented sweeping reforms in many areas and continues to introduce

new reforms.

New Labor Courts

Code

2018

Amendments to

improve doing

business

(Law 7099)

Number of Days to set up a Company, 2018

Internationally-

minded

people

40

3735

24.523

21 20.5

17 16.5

12.511.2 10.1

7

So

uth

Afr

ica

Po

lan

d

Rom

ania

Cze

ch R

ep.

Bu

lga

ria

Au

str

ia

Bra

zil

Fin

lan

d

India

Sp

ain

Jap

an

Russia

Turk

ey

Down from

38 days in

2002

International Tax Competitiveness, 2018(Index=100 as most competitive)

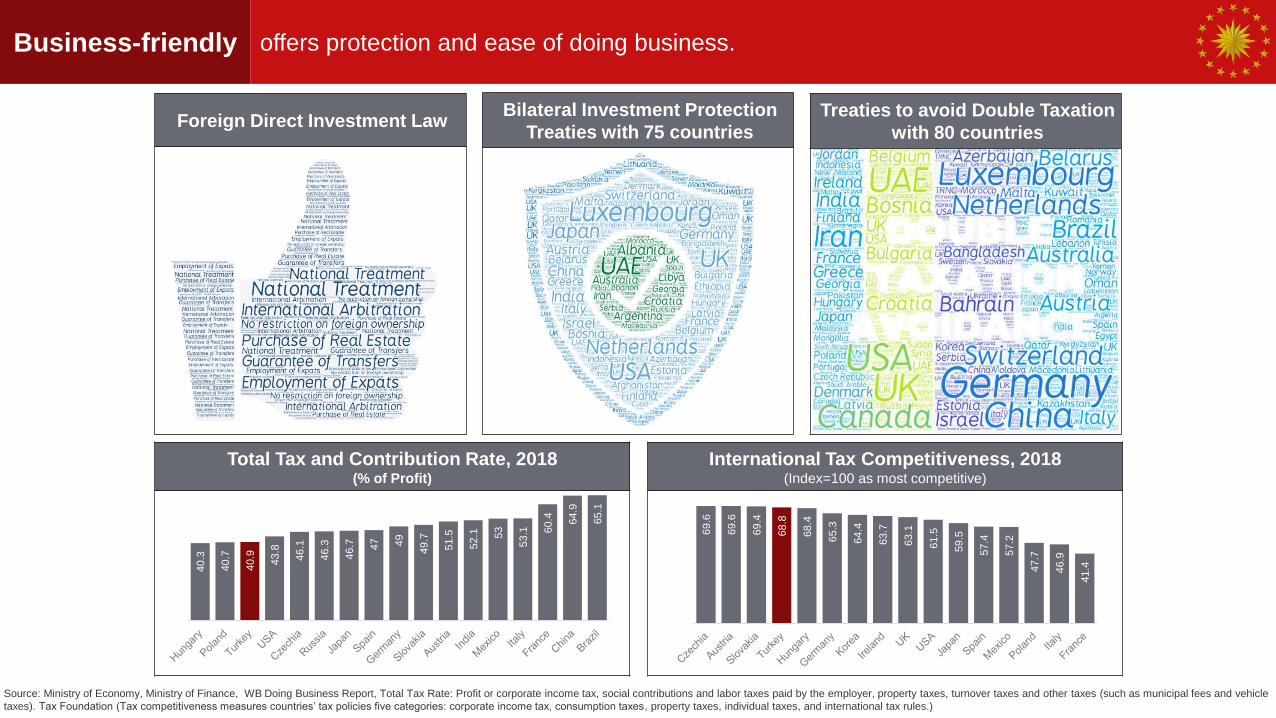

Bilateral Investment Protection

Treaties with 75 countries

Source: Ministry of Economy, Ministry of Finance, WB Doing Business Report, Total Tax Rate: Profit or corporate income tax, social contributions and labor taxes paid by the employer, property taxes, turnover taxes and other taxes (such as municipal fees and vehicle

taxes). Tax Foundation (Tax competitiveness measures countries’ tax policies five categories: corporate income tax, consumption taxes, property taxes, individual taxes, and international tax rules.)69.6

69.6

69

.4

68.8

68.4

65.3

64.4

63.7

63.1

61.5

59.5

57.4

57

.2

47.7

46.9

41.4

Foreign Direct Investment Law

Total Tax and Contribution Rate, 2018(% of Profit)

40.3

40.7

40.9

43.8

46.1

46.3

46.7 47 49

49.7

51.5

52.1 53

53.1 6

0.4 64.9

65.1

Business-friendly offers protection and ease of doing business.

Treaties to avoid Double Taxation

with 80 countries

R&D and Innovation Incentives

Tax deduction & exemption +

Employment Incentives

Payroll & Training support +

Manufacturing Incentives

Tax deduction & exemption +

Technology Development Zones

To support R&D

Tax deduction & exemption+

Exclusive Zones

Free Zones

Tax deduction & exemption +

Organized Industrial Zones

Developed infrastructure

Academia

Industry

Incentives for Service Exporters

Tax deduction for exporting

services in;

E n g i n e e r i n g

A r c h i t e c t u r e

D e s i g nS o f t w a r e

Medical Reporting

Accounting

Call Center

D a t a c e n t e r

EDUCATION

H e a l t h c a r e

Lucrative

IncentivesInvestors are offered lucrative incentives in many ways.

Selected Foreign Companies conducting R&D in Turkey

Increasing R&D Spending ($ Billion, PPP)Number of Researchers (thousands)

Source: OECD, Eurostat, Turkstat, PPP: Purchasing Power Parity

0

5

10

15

20

Turkey

Romania

Poland

0

20

40

60

80

100

120

140

160

180

200

220 Turkey

Romania

Poland

Benign R&D

EcosystemR&D incentives are further supported by a favorable ecosystem..

Over 100 R&D centers

by foreign companies

Hungary Hungary

Source: Turkstat, Ministry of Industry and Technology, Sasad, OSD, SBB; export values as of 2018, market values as of 2017, defence industry value as of 2018

Opportunities Turkey offers abundant opportunities in a variety of sectors.

AUTOMOTIVEMACHINERY &

ELECTRICAL EQP.AEROSPACE &

DEFENCE ENERG

Y INFRASTRUCTUR

E

FINANC

E

OPPORTUNITIES

AGROFOOD

–Largest TV & white goods

producer in Europe

–Market: $38 billion

–Export: $25 billion

–$19 billion defense spending

–Industry: $8.7 billion

–Export: $2.2 billion

–Air passengers: 210 million

–Market: $66 billion

–Growing demand

–Energy corridor

–Untapped renewables

–15th largest manufacturer

–1.6 million vehicle produced

-Market: $24 billion

–Export: $32 billion

–$127 billion PPP contracts

(2003-2018)

–More opportunities in

transport, energy, health

–Robust growth with double

digits

–Islamic finance to grow

–Istanbul Financial Center

–Market: $80 billion

Export: $17 billion

–Export to around 200

countries

Number of Foreign Companies in Turkey (‘000)FDI Inflows ($ Billion)

Source: CBRT, Ministry of Industry and Technology, Team Analysis *Geographic (adjusted) and sectoral breakdown of cumulative gross inflows of equity FDI from 2003 to 2018

15

209

1973-2002 (30 years) 2003-2018 (16 years)

5.6

65.5

2002 2018

EU68.6%

USA8.8%

Asia21.5%

Other1.1%

Geographic Breakdown of Investments*

Finance33.7%

Manufacturing24.1%

Energy11.7%

Information & Communication Services 8.1%

Wholesale & Retail Trade

6.4%

Transport & Storage

4.5%

Construction 3.1%

Others 8.4%

SectoralBreakdown of Investments*

Foreign Direct

Investment (FDI)

Turkey’s value has been appreciated by foreign investors with increasing FDI inflow to

Turkey.

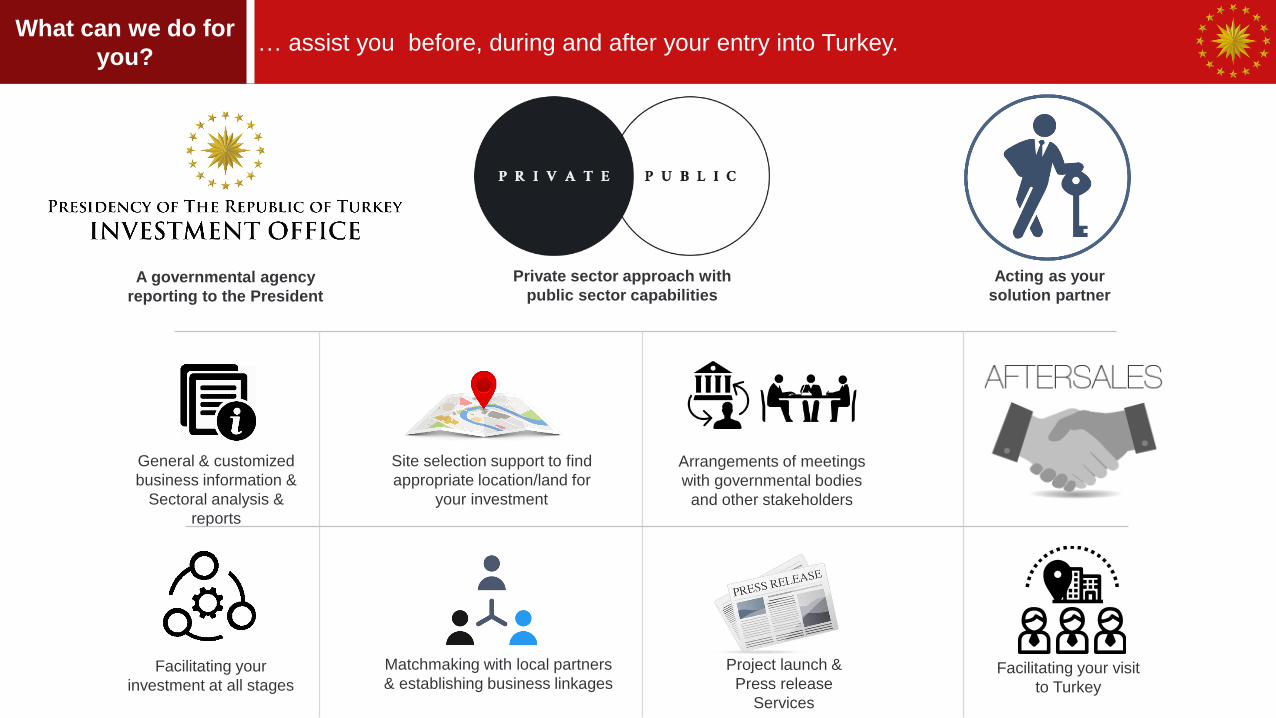

What can we do for

you?… assist you before, during and after your entry into Turkey.

A governmental agency

reporting to the President

Private sector approach with

public sector capabilities

Acting as your

solution partner

General & customized

business information &

Sectoral analysis &

reports

Site selection support to find

appropriate location/land for

your investment

Arrangements of meetings

with governmental bodies

and other stakeholders

Matchmaking with local partners

& establishing business linkages Facilitating your

investment at all stages

Project launch &

Press release

Services

Facilitating your visit

to Turkey