WASBO Annual Conference 2015 1 - c.ymcdn.comc.ymcdn.com/sites/ · Imprest Accounts and Petty Cash...

46

WASBO Annual Conference 2015 1

Transcript of WASBO Annual Conference 2015 1 - c.ymcdn.comc.ymcdn.com/sites/ · Imprest Accounts and Petty Cash...

WASBO Annual Conference 2015 1

Presented by Holly Burlingame, CSBA

WASBO Instructor

WASBO Annual Conference 2015 2

Background: ◦ The WASBO Accounts Payable Manual was the

brainchild of Cory Plager and Denise Wolff.

◦ First introduced as a concept and a rough draft at the

WASBO Accounts Payable Conference in August 2014.

◦ Holly Burlingame, CSBA, was instrumental in compiling

and preparing the manual.

WASBO Annual Conference 2015 3

Others who contributed information, review, and

approval were:

Clark Fletcher, IRS Government Specialist

Scott Matheson, King County Cash Management

Carmen Smith, WA ST Department of Revenue

Kathie Collins, WA ST Dept. of Enterprise Services

Melanie Piccin, WA ST Dept. of Retirement Systems

WASBO Annual Conference 2015 4

Special thanks to Becky Montgomery for adding

the small schools perspective.

Special thanks to DeAnn Wagoner for her editing

skills.

WASBO Annual Conference 2015 5

GOALS:

Provide users with an understanding of school

accounts payable beyond data entry.

Provide a training tool for new employees

responsible for accounts payable functions.

Include essential information and resources

specific to accounts payable from RCW, WAC,

the Accounting Manual, IRS regulations, state

agency rules and regulations.

WASBO Annual Conference 2015 6

GOALS continued:

Provide 21st Century solutions for school

accounts payable processing.

Bring together the best practices in both small

and large school districts.

Be a companion to the WASBO Purchasing and

Warehouse Handbook.

WASBO Annual Conference 2015 7

Completed manual first released in March 2015 at

an Accounting and Budgeting Committee meeting.

Completed version can now be accessed on

WASBO’s web site.

Located under Resources/Publications

Or follow the link below:

http://c.ymcdn.com/sites/waasbo.site-ym.com/resource/resmgr/ABC_Committee/Accounts_Payable_Manual.pdf

WASBO Annual Conference 2015 8

Contents Overview

WASBO Annual Conference 2015 9

WASBO Annual Conference 2015 10

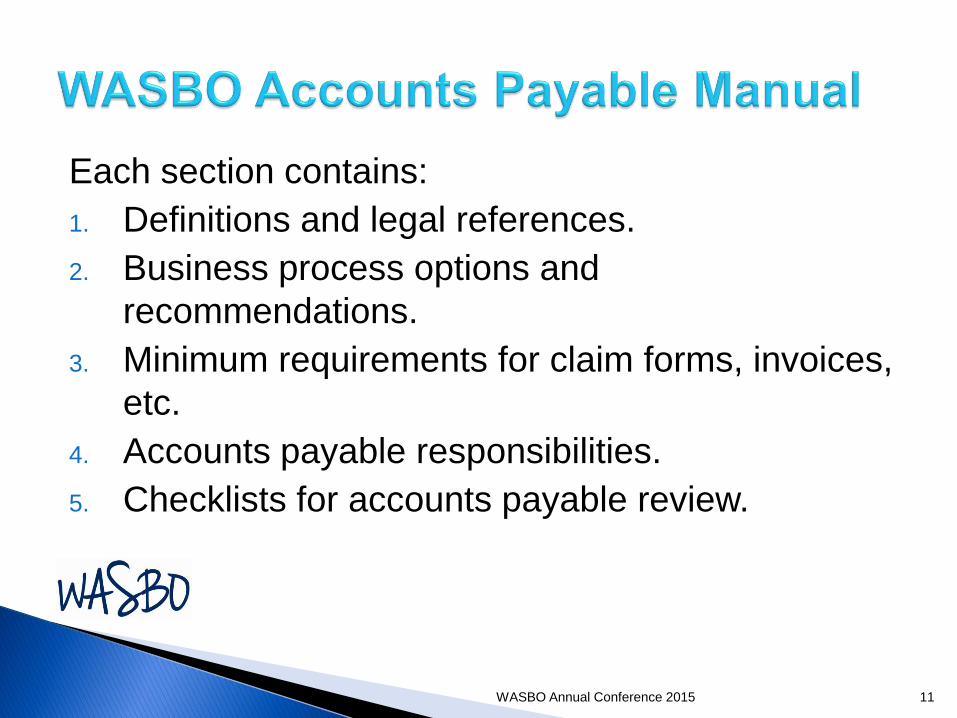

Each section contains:

1. Definitions and legal references.

2. Business process options and

recommendations.

3. Minimum requirements for claim forms, invoices,

etc.

4. Accounts payable responsibilities.

5. Checklists for accounts payable review.

WASBO Annual Conference 2015 11

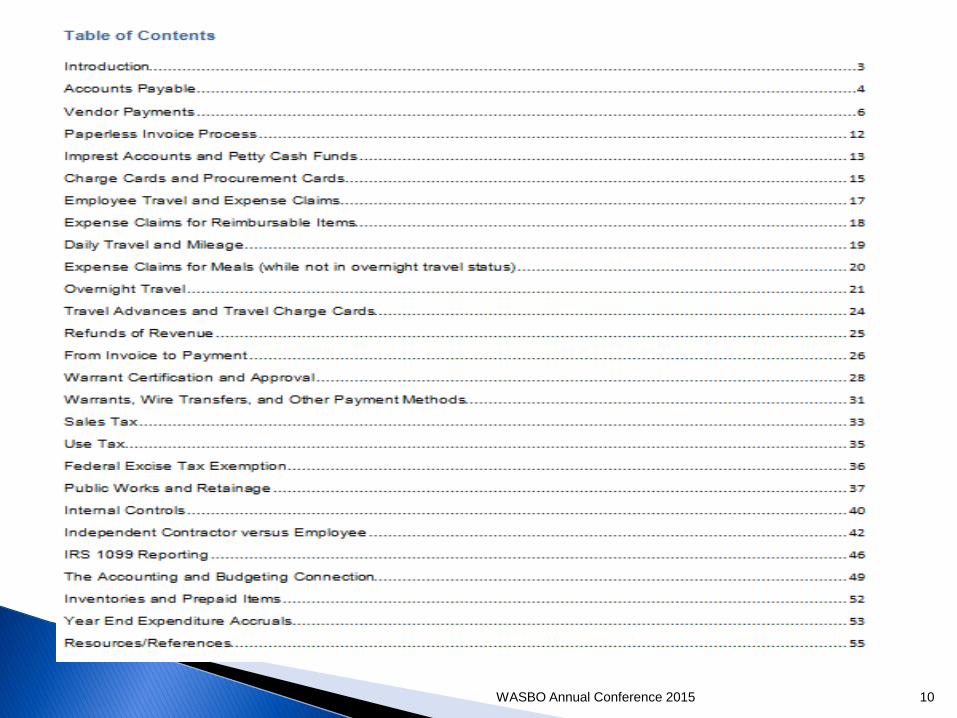

Table of Contents

Vendor Payments ……………………………………6

Paperless Invoice Process…………………………12

Imprest Accounts and Petty Cash Funds..……….13

Charge Cards and Procurement Cards ………….15

Employee Travel and Expense Claims …………..17

Expense Claims for Reimbursable Items ………..18

WASBO Annual Conference 2015 12

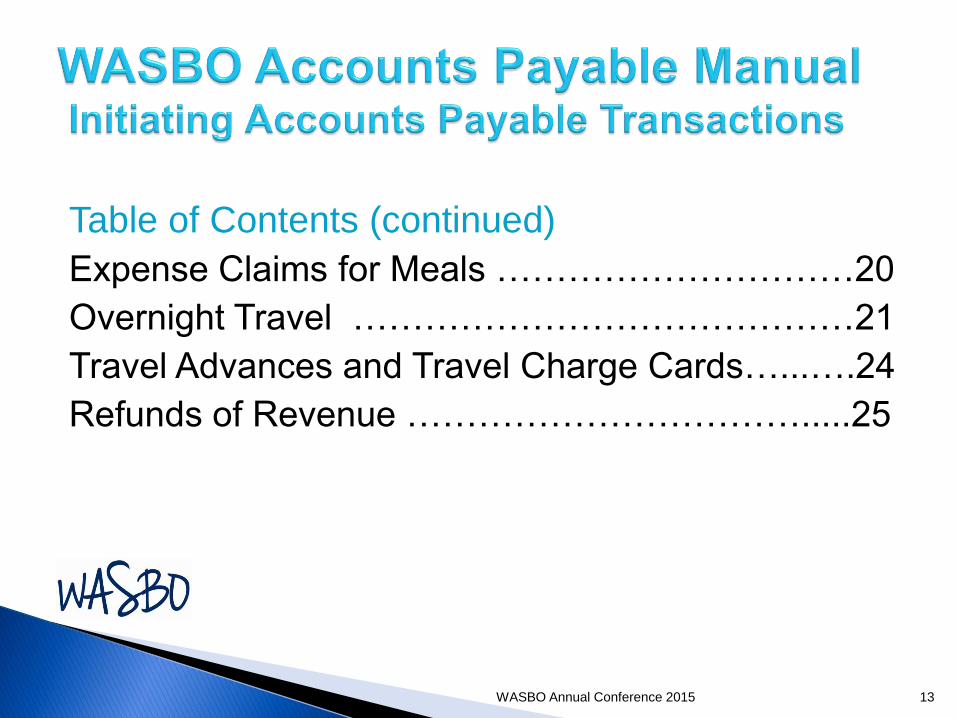

Table of Contents (continued)

Expense Claims for Meals …………………………20

Overnight Travel ……………………………………21

Travel Advances and Travel Charge Cards…...….24

Refunds of Revenue …………………………….....25

WASBO Annual Conference 2015 13

Table of Contents (continued)

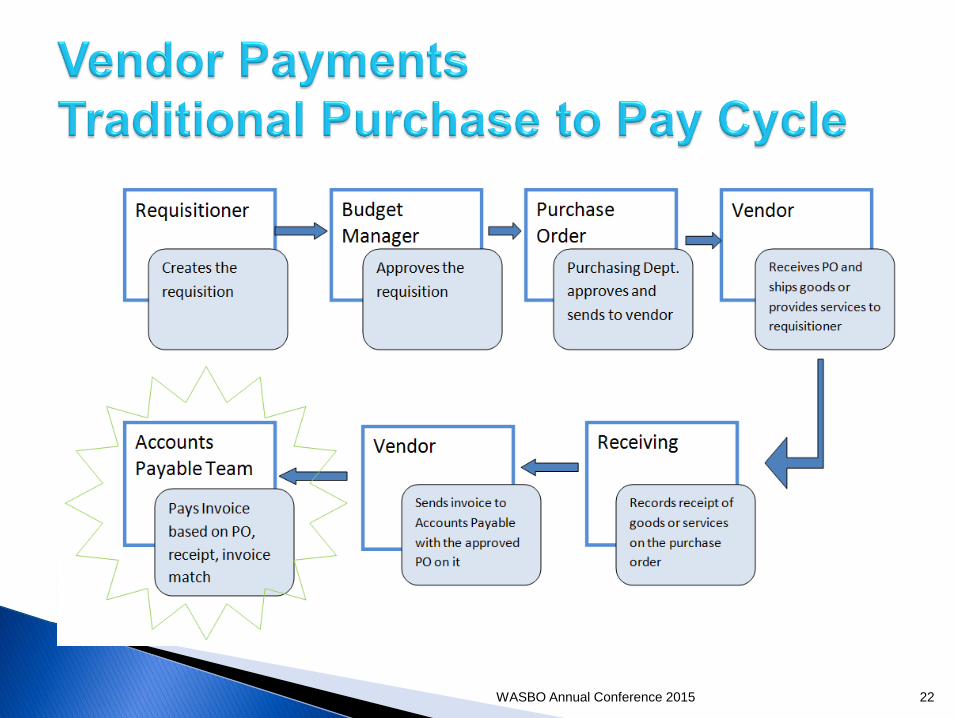

From Invoice to Payment………………………….26

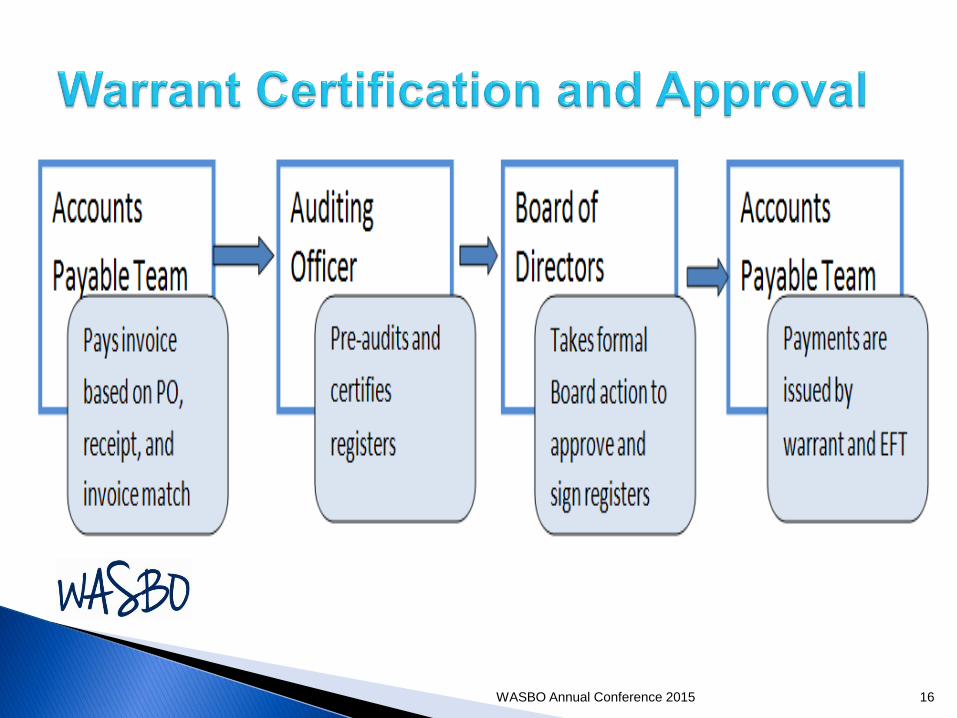

Warrant Certification and Approval……………….28

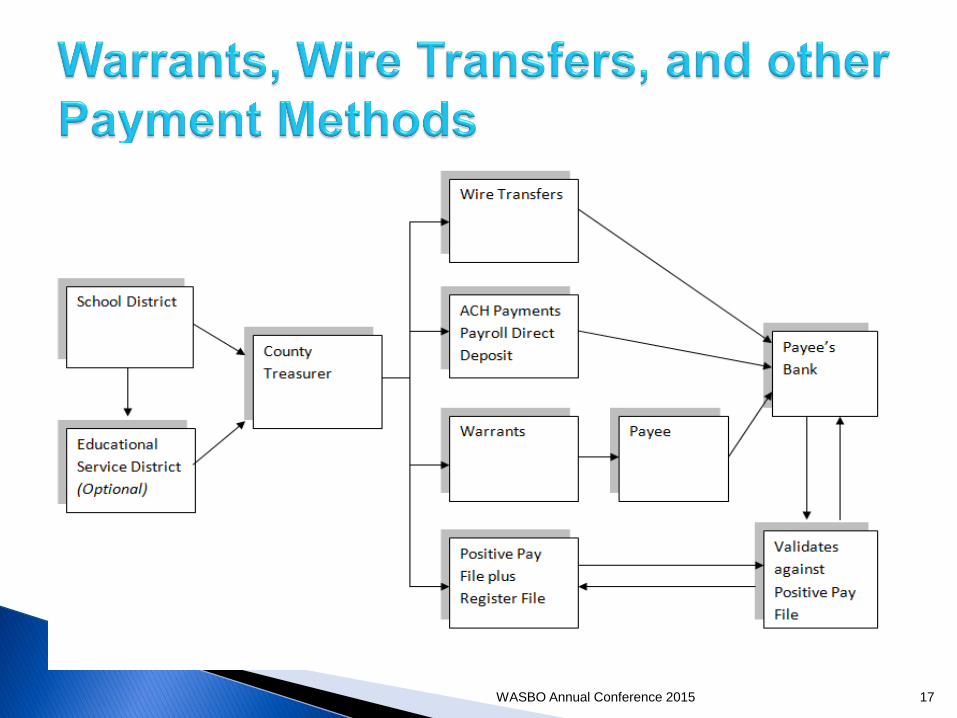

Warrants, Wire Transfers, and Other Payment

Methods …………………………………………..31

WASBO Annual Conference 2015 14

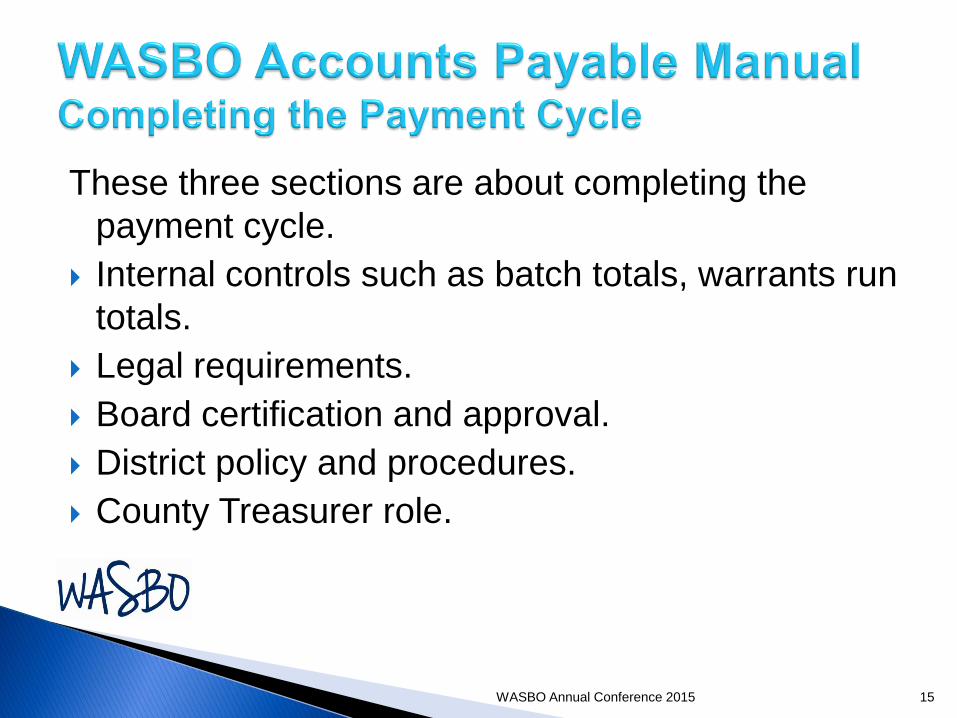

These three sections are about completing the

payment cycle.

Internal controls such as batch totals, warrants run

totals.

Legal requirements.

Board certification and approval.

District policy and procedures.

County Treasurer role.

WASBO Annual Conference 2015 15

WASBO Annual Conference 2015 16

WASBO Annual Conference 2015 17

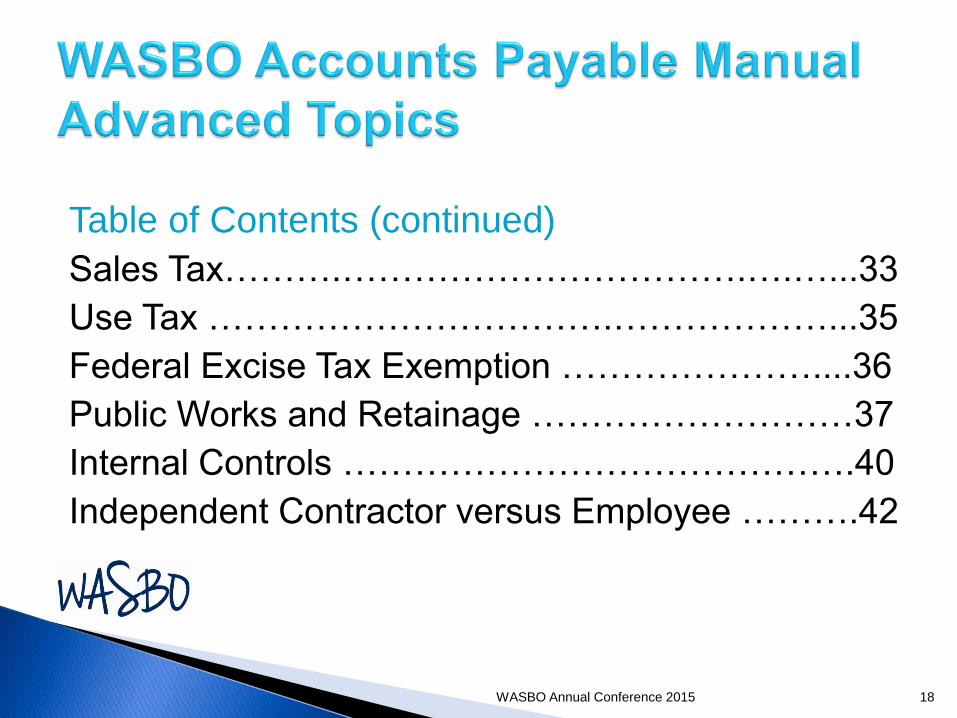

Table of Contents (continued)

Sales Tax……….…………………………….….…...33

Use Tax …………………………….………………...35

Federal Excise Tax Exemption …………………....36

Public Works and Retainage ………………………37

Internal Controls …………………………………….40

Independent Contractor versus Employee ……….42

WASBO Annual Conference 2015 18

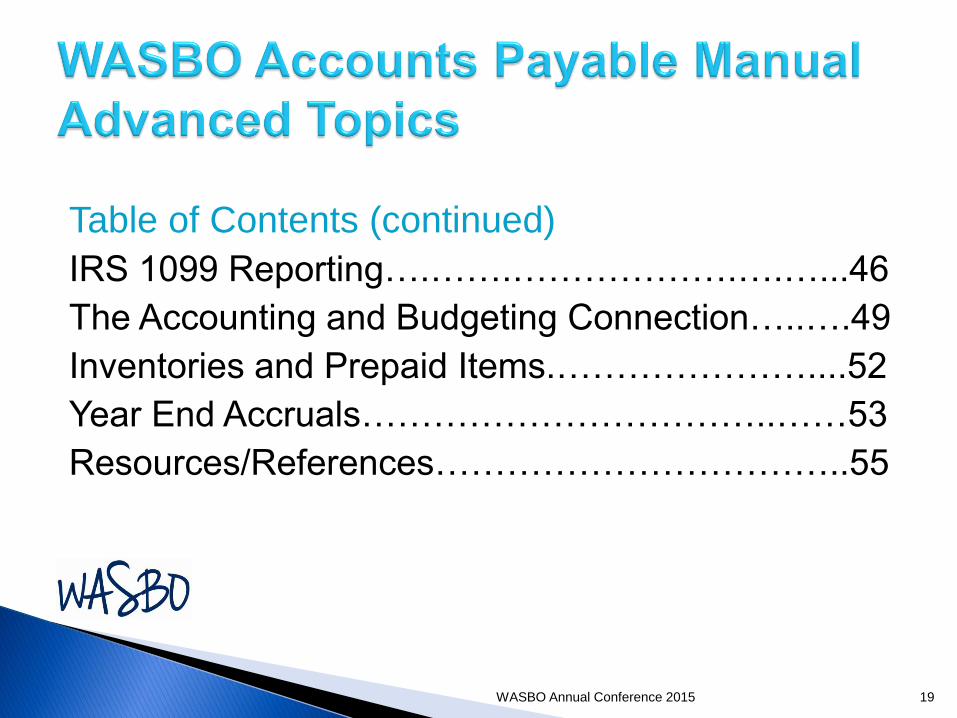

Table of Contents (continued)

IRS 1099 Reporting….…….……………….….…...46

The Accounting and Budgeting Connection…..….49

Inventories and Prepaid Items.…………………....52

Year End Accruals……………………………..……53

Resources/References……………………………..55

WASBO Annual Conference 2015 19

Vendor Payment Section

WASBO Annual Conference 2015 20

Sections:

1. Definition of a Vendor W9, UBI numbers, etc.

Employees as vendors (or not)

2. New Vendors Internal controls over new vendors

Maintaining your vendor data base

Tips

WASBO Annual Conference 2015 21

WASBO Annual Conference 2015 22

Vendor Invoice Section:

1. Defines what a vendor invoice is (original, copy,

fax, electronic image, data file, etc.)

2. Minimum requirements of any invoice:

description, detailed pricing, sales tax, freight,

etc.

3. Three-way match: PO to invoice to receiving

document in the traditional purchase to pay

cycle.

WASBO Annual Conference 2015 23

Accounts Payable vendor invoice audit checklist:

Three-way match complete

Invoice is not a duplicate

Total is correct

Shipping and handling are correct

Sales tax added at the correct rate

Is this a public works contract requiring retainage

to be held?

WASBO Annual Conference 2015 24

Accounts Payable checklist continued:

Current charges with no brought-forward

balances.

Purchase order encumbrance sufficient to cover

the current invoice or within the district’s allowed

variance (example: ten percent over

encumbrance).

Invoice pricing matches quote or bid.

WASBO Annual Conference 2015 25

Accounts Payable checklist continued:

Account code is correct per the district chart-of-

accounts and state account code requirements of

program, activity, and object.

Determine the fiscal year for processing.

WASBO Annual Conference 2015 26

Exceptions/alternatives to the three-way match:

1. Direct payments such as small purchases

without a PO.

2. Prepayments for registration fees and deposits.

Examples: sporting event entrance fees and

deposits for event facility.

WASBO Annual Conference 2015 27

Prompt Payments

Section on how to calculate a prompt payment

discount such as 2/10, net 30.

Tools for determining whether a discount makes

economic sense.

Late Payments

Maximum allowed is 1% per month under

Washington State law.

How to calculate late payments.

WASBO Annual Conference 2015 28

Correcting vendor invoices.

Managing and taking vendor credits.

WASBO Annual Conference 2015 29

Paperless Invoice Processing

WASBO Annual Conference 2015 30

This section answers the following questions:

Original invoice?

What is an original invoice?

Who can tell the difference between an original

and a copy?

Why do we care?

What is acceptable as a source document in the

21st century?

WASBO Annual Conference 2015 31

Invoices are received in your district by the following

methods:

1. Vendor emails an image of an invoice (KCDA).

2. Vendor uploads an invoice to a district’s vendor

portal (new technology developing).

3. Vendor provides a district with a customer

portable to upload invoices (FSA, Fisher

Scientific, Pitney Bowes)

WASBO Annual Conference 2015 32

Rather than images, you may also be receiving your

“invoices” by software data files:

1. Upload from purchasing card software.

2. Upload from utility management systems.

Districts may already be receiving up to 50% of

their invoices in an electronic format.

WASBO Annual Conference 2015 33

Still getting paper invoices in the US Mail? Here’s

an example of adopting a paperless accounts

payable process for those invoices:

1. Scan invoice on a desktop scanner.

2. Image is named and filed on desktop or server.

3. Image is routed to user for receipt verification.

4. On-line receiving is verified.

WASBO Annual Conference 2015 34

5. Invoice image is viewed on one computer

monitor and second monitor is used to enter

invoice data into accounts payable data entry

screens.

6. The scanned invoice image is then attached to

the accounts payable record within the district’s

software.

7. The invoice image is viewed by a drill-down of

the transaction on fiscal reports run to the

screen.

WASBO Annual Conference 2015 35

Technology is available today.

Need to meet the Requirements for Destruction of Non-Archival Paper Records After Imaging with Secretary of State (details on their website).

Paper invoices are thrown away!

Scanned images of invoices are your source document.

When your auditor selects an accounts payable transaction for audit, print a copy or email the scanned image. FYI – SAO is already paperless!

WASBO Annual Conference 2015 36

Charge Cards and Purchasing Cards

WASBO Annual Conference 2015 37

This section garnered a lot of interest from many

who previewed the manual.

Defines purchasing cards, credit cards, travel and

fuel cards.

Legal references.

Best practices.

Some duplication with the Purchasing Handbook.

Focuses on payment processing and auditing side

in Accounts Payable.

WASBO Annual Conference 2015 38

Best Practices to mitigate risk and alleviate

workload in AP: Upload the district’s chart-of-accounts into the bank

software.

Assign default account codes for each cardholder.

Utilize the on-line approval process available in bank

software.

Upload monthly spending activity into the district’s

software.

Upload monthly spending activity in detail, including

merchant’s name.

WASBO Annual Conference 2015 39

Accounts Payable checklist:

Verify that all cardholders with current transactions

have submitted the required reconciliations.

Verify all appropriate signatures or on-line

approvals are included.

Verify the account codes are correct per the

district’s chart-of-accounts, person responsible,

and state account code requirements of program,

activity and object.

WASBO Annual Conference 2015 40

Accounts Payable checklist continued:

Verify that original, itemized receipts are attached

for every transaction.

Verify that the items purchased have a clear

district purpose.

Verify that any merchandise shipments went to a

district location.

Verify that sales tax has been paid, if due, and add

use tax if not.

WASBO Annual Conference 2015 41

Accounts Payable checklist continued:

Verify that federal excise tax has not been

charged on gas credit cards.

Determine the fiscal year for processing.

WASBO Annual Conference 2015 42

Future Training and Updates

WASBO Annual Conference 2015 43

WASBO Accounts Payable Conference ◦ Scheduled for August 5, 2015

◦ In depth training on various sections of the manual

◦ Presentations from content experts from state agencies

Update sections prior to each year’s AP

Conference based on: ◦ Content expert review

◦ User feedback

WASBO Annual Conference 2015 44

Available for your use now.

Use for training new staff.

Use as a handy reference for experienced staff.

Use in conjunction with your own district

procedures.

Use to create your own district procedures.

Send suggestions, additional information, or

concerns in writing to the WASBO office at:

WASBO Annual Conference 2015 45

Questions?

WASBO Annual Conference 2015 46

![Samburu County 3rd June Outstanding Imprest Register 030614[1]-1](https://static.fdocuments.us/doc/165x107/55cf94f9550346f57ba5ae60/samburu-county-3rd-june-outstanding-imprest-register-0306141-1.jpg)