Warren B Potts III Senior Director, Waters Corporation Trends_Fin… · Warren B Potts III Senior...

22

©2013 Waters Corporation 1 Pharmaceutical Trends Warren B Potts III Senior Director, Waters Corporation Confidential

-

Upload

phamkhuong -

Category

Documents

-

view

215 -

download

0

Transcript of Warren B Potts III Senior Director, Waters Corporation Trends_Fin… · Warren B Potts III Senior...

©2013 Waters Corporation 1

Pharmaceutical Trends

Warren B Potts III

Senior Director, Waters Corporation

Confidential

©2013 Waters Corporation 2

Pharmaceutical Industry What lies ahead

Continuing challenges caused by patent cliff

– Big pharma companies exposed to generic competition

– Growth of the biopharmaceuticals industry

Stricter regulations

– More emphasis on tighter quality control (QC)

– Demands for international harmonization

Increasing demands for profitability

– Demands for low price drug with high quality

The surge of rapidly growing markets

– Quality control is an increasingly critical topic

Confidential

©2013 Waters Corporation 3

Patent Cliff – an Example

Year Brand Name Manufacturer Generic Name

Sales ($m US)

2011 Lipitor Zyprexa

Pfizer Lilly

Atorvastatin Olanzapine

5,804 2,114

2012 Plavix Singulair Seroquel Actos Lexapro Diovan

SA/BMS Merck AZ Takeda Forest Novartis

Clopidogrel Montelukast Quetiapine Pioglitazone Escitalopram valsartan

5,020 3,824 3,549 2,914 2,591 1,585

2013 Cymbalta Lilly duloxetine 2,891

2014 Celebrex Nexium

Pfizer AZ

Celexocib esomeprazole

1,497 5,586

2015 Abilify BMS/Otsuka Aripirazole 4,077

2016 Crestor AZ Rosuvastatin 3,277

2019 Lyrica Pfizer pregabalin 1,571

Total $46,300

Confidential

©2013 Waters Corporation 4

Generics Industry

Grew to $84.8Bn [7.9%] in 2009

Represents worldwide

– 70% of prescriptions written

– 12% of sales revenue

Grow to $207.1B by 2025

– Growth outside mature markets

– >$150B losing patent protection

Difficult regulatory environment

– US Hatch-Waxman

o Can start before patent expires

o 180 days exclusivity

– ROW

o Start after patents expire

o No exclusivity period

46.4%

Confidential

©2013 Waters Corporation 5

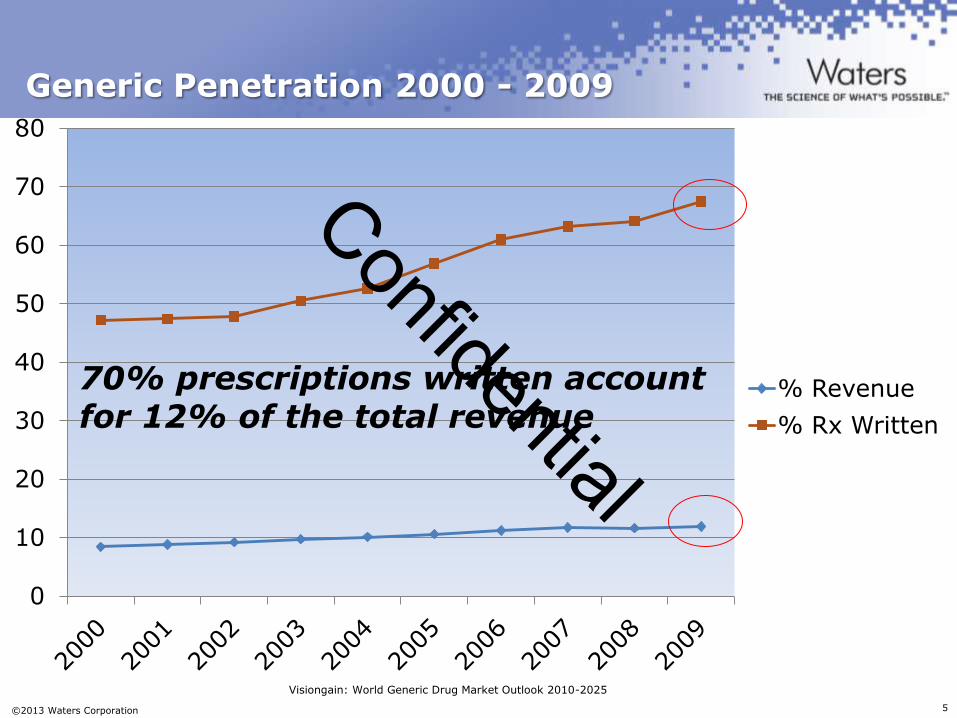

Generic Penetration 2000 - 2009

0

10

20

30

40

50

60

70

80

% Revenue

% Rx Written

Visiongain: World Generic Drug Market Outlook 2010-2025

70% prescriptions written account for 12% of the total revenue

Confidential

©2013 Waters Corporation 6

Global Generic Pharma Growth

0

50

100

150

200

250

An

nu

al

Sale

s (

$b

n)

CAGR 5.7%

Generic Pharma industry continues to sustain its growth Visiongain: World Generic Drug Market Outlook 2010-2025

Confidential

©2013 Waters Corporation 7

Generic Growth Driven Outside Traditional Markets

Traditional markets slowing

– US and Germany saturated

– Western EU and Japan slowing

Rapidly growing markets drive growth

– Latin America

– Russia

– India

– China

– Turkey

Opportunity for local companies as well as multi-nationals

Confidential

©2013 Waters Corporation 8

Market Comparison

Visiongain: World Generic Drug Market Outlook 2010-2025

Confidential

©2013 Waters Corporation 9

Trends in Generic Pharmaceuticals

Competitive pressures

– Reducing time to market

– Consistently manufacturing quality product

– Pricing pressures

Fiscal responsibility

– Manage expenses in increasingly competitive environment

– Differentiate on more than price

Global harmonization

– Drive to platform strategy

– Standardization on WW basis

– Consistent supply and technical support WW

Confidential

©2013 Waters Corporation 10

Trends in Generic Pharmaceuticals

Compliance and quality

– Risk based approaches

Focusing on innovation

– Drug delivery

– Diversifying portfolio through biosimilars

Continuous improvement philosophy

– Shorten development time/reduce time to market

– Operational excellence and quality product

Looking at new ways to engage value chain

– Vendor relationships focused on financial terms to partnership

Confidential

©2013 Waters Corporation 11

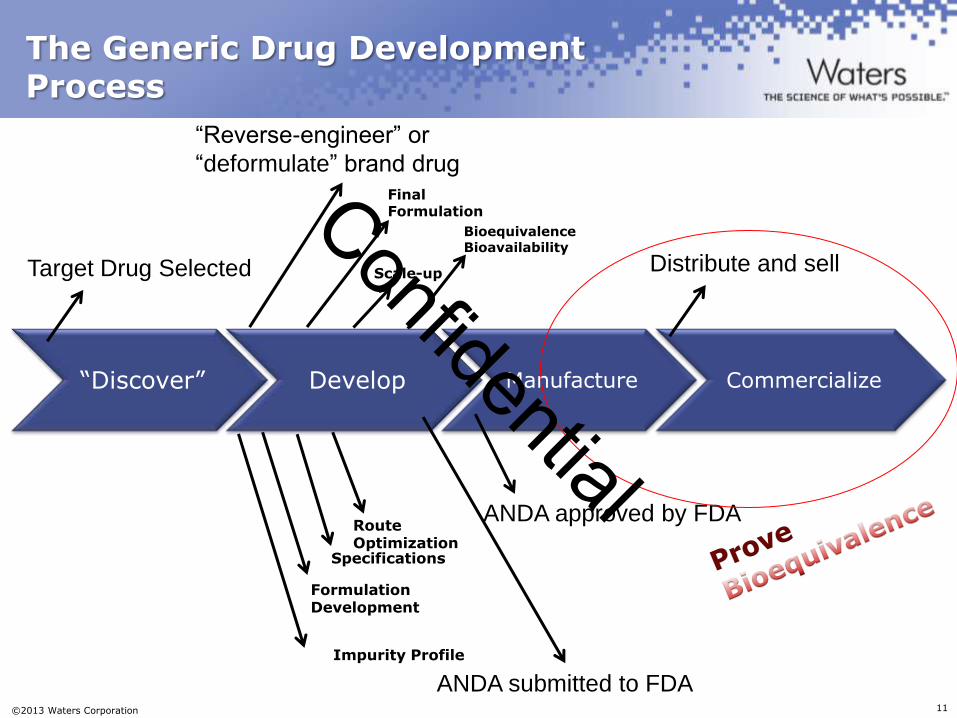

The Generic Drug Development Process

“Discover” Develop Manufacture Commercialize

Target Drug Selected

“Reverse-engineer” or

“deformulate” brand drug

Distribute and sell

ANDA submitted to FDA

ANDA approved by FDA

Impurity Profile

Formulation Development

Specifications

Route Optimization

Final Formulation

Scale-up

Bioequivalence Bioavailability

Confidential

©2013 Waters Corporation 12

QC Analysis Workflow Typical Tests

Finished Dosage

Form

Raw material

Intermediate and API

Assay

Content Uniformity

Dissolution

Impurities

Sterility

Preservatives

Physical tests

Purity

Identity

Impurities

Crystal form

Water content

Residual solvents

Prepare Samples

Acquire Data

Generate Report

Samples & Info

Product Release Confidential

©2013 Waters Corporation 13

QC Laboratory Challenges

Flexibility

Complexity

Instrument Robustness

Long Term reliability of Methods

Method transfer

Ease of Use

Right First Time

Removing Waste and variability

Interface with Manufacturing

Incorporating technology advances

– While maintaining workflow

Confidential

©2013 Waters Corporation 14

Resource Driven Challenges

People are are your most important assets

– Significant investment needed

Training

Using Multiple platforms

New technology

Ease of Use

New Molecules

– Emergence of Large Molecules

Institutional memory

– Staff Turnover

Avoiding Human Error

Limited Space

Confidential

©2013 Waters Corporation 15

Business Driven Challenges

Productivity

Asset Utilization

Reducing the cost of quality

Profitability

– Eliminate weekend work, OT, 3rd shift

Data processing/results crunching

– Excel?

Timeliness of results

– Releasing product

– Release manufacturing facilities

Documentation/data tracking/audit

Compliance

Confidential

©2013 Waters Corporation 16

Turning Challenges into Winning Strategy How to sustain growth and protect profitability

Take advantage of technology innovation and advances

– Enhance asset utilization and return of investment (ROI)

Make informatics a facilitating factor for productivity

Proactively work with regulatory organizations

– Compliance is a natural result of an effective streamlined workflow

– Should not burden productivity

Emphasis on efficient/effective QC strategies to enhance

productivity

Confidential

©2013 Waters Corporation 17

Why we built the ACQUITY UPLC H-Class

Designed for the QC Lab

Robustness and Reliability

Ease of Use

HPLC/UPLC capability

Smooth method transfer across existing LC platform

Solvent selection capability (up to 9)

Column switching capability (up to 6)

Different column temperature zones

Acquire Data Samples

Preparation Report

Release

Confidential

©2013 Waters Corporation 18

Managing your Laboratory Data

Comprehensive laboratory workflow and documentation solution

Integration of business and laboratory systems

Supports entire product lifecycle from research to manufacturing

Laboratory Instruments

Business Systems

Research QC Development

Sampling Testing Evaluation Release Reporting Request Manage Data

Confidential

©2013 Waters Corporation 19

Technology Adoption Barriers

Pharmaceutical companies risk adverse

– Highly regulated

o Is technology recognized by regulators and standard setters?

– Cost of change

o Investment in technology and potential cost to change filings

– How easy is it to migrate organizationally?

o Acceptance and usage

Many companies, many approaches

– Is there a monograph?

– Start in development

– Prioritize marketed products by volume

– Focus on areas with lower regulatory hurdles

Confidential

©2013 Waters Corporation 20

New Technology Batch Release of Polypellets

Background

– Polypellet (MUPS) manufacturing for Omeprazole

Production

o Three stages of HPLC analysis

• Assay of individual polypellet batches

• Assay of blended polypellets

• Finished product

New technology

– UPLC reduced from 25 mins per run to 2 mins per run

(same resolution)

– Solvent consumption reduced significantly

– HPLC total wait time for a single in-process was 5 hours!

– UPLC total wait time is 30 minutes

Impact

– Release 6 batches in 6 hours, instead of 2 batches per day

– Production of Omeprazole capsules increased from 25

million per month to 40 million per month

Confidential

©2013 Waters Corporation 21

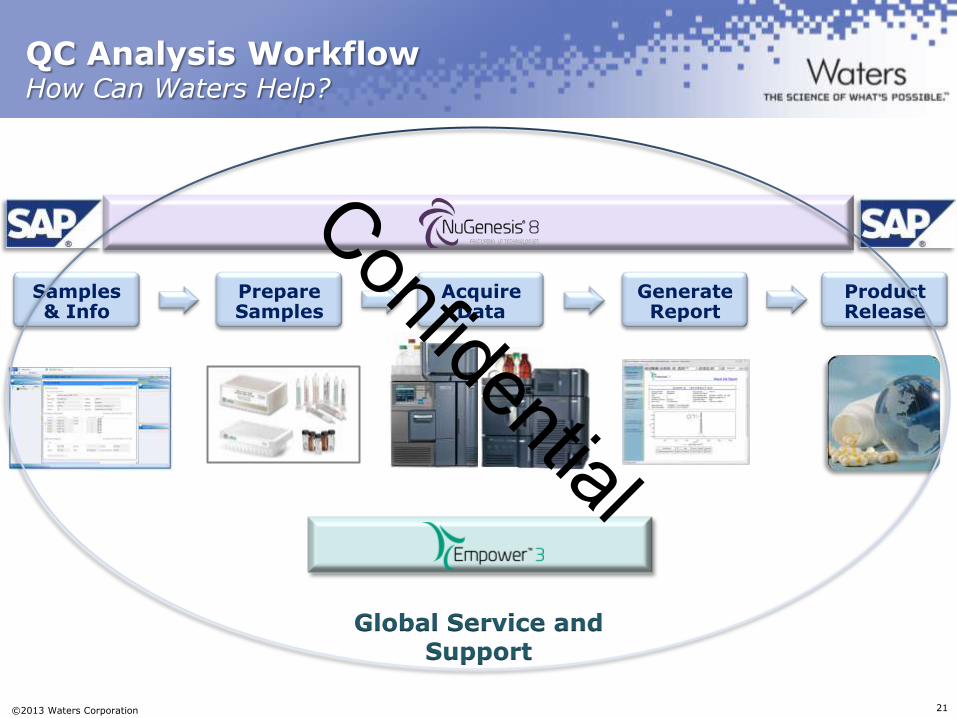

QC Analysis Workflow How Can Waters Help?

Global Service and Support

Prepare Samples

Acquire Data

Generate Report

Samples & Info

Product Release

Confidential

©2013 Waters Corporation 22

Summary

Generic business will continue to grow

Regulations, quality, margins will continue to put pressure on business

Technology adoption will be required for business efficiency

Picking the right company to partner with will make the attainment of the business goals easier

Confidential