Valuing Government Guarantees in Toll Road Projects Luiz Brandão (PUC-Rio) Eduardo Saraiva (BNDES)...

40

Valuing Government Guarantees in Toll Road Projects Luiz Brandão (PUC-Rio) Eduardo Saraiva (BNDES) Jun 2007

-

Upload

harold-nichols -

Category

Documents

-

view

214 -

download

0

Transcript of Valuing Government Guarantees in Toll Road Projects Luiz Brandão (PUC-Rio) Eduardo Saraiva (BNDES)...

Valuing Government Guarantees in Toll Road

Projects

Luiz Brandão (PUC-Rio)

Eduardo Saraiva (BNDES)

Jun 2007

11th Real Option ConferenceBerkeley, June 2007

2

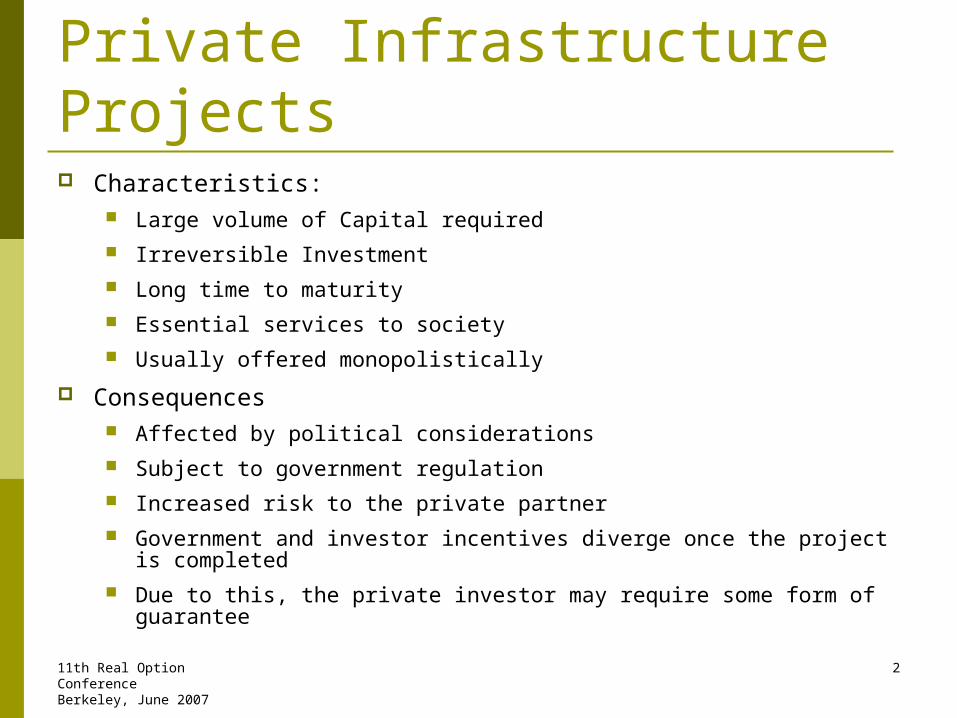

Private Infrastructure Projects Characteristics:

Large volume of Capital required Irreversible Investment Long time to maturity Essential services to society Usually offered monopolistically

Consequences Affected by political considerations Subject to government regulation Increased risk to the private partner Government and investor incentives diverge once the project is

completed Due to this, the private investor may require some form of guarantee

3

Risks Involved Construction Risk

Interest Rate Risk

Exchange Rate Risk

Political Risk

Environmental Risk

Traffic Risk

11th Real Option ConferenceBerkeley, June 2007

4

Stochastic Modeling of Traffic

Concession Period

Tra

ffic

De

man

d

Expected Traffic

11th Real Option ConferenceBerkeley, June 2007

5

Types of Government Guarantees

Grant

Concession Extension

Revenue Enhancement

Minimum Traffic Guarantee

Shadow Toll

Subordinate Loan

Exchange Rate Guarantee

Equity Guarantee

Debt Guarantee

Cost to Government

Impa

ct

on C

once

ssio

narie

Low High

High

6

Government Participation (PPP) Chile – Santiago – San Antonio Highway (1995)

$140 million dollar investment with Minimum Traffic Guarantee (MTG)

Mexico - CM-Toluca Highway (1992) $313 million dollar investment with MTG

Colombia –El Cortijo-El Vino (1996) MTG of 90%

Chile - Costanera Norte, Santiago (2005) $400 million dollar investment $80 million provided by governemnt, MTG of 80%

11th Real Option ConferenceBerkeley, June 2007

7

Traffic Guarantees

Concession Period

Tra

ffic

De

man

d Expected

Floor

Government pays subsidy

CeilingGovernment receives excess revenues

11th Real Option ConferenceBerkeley, June 2007

8

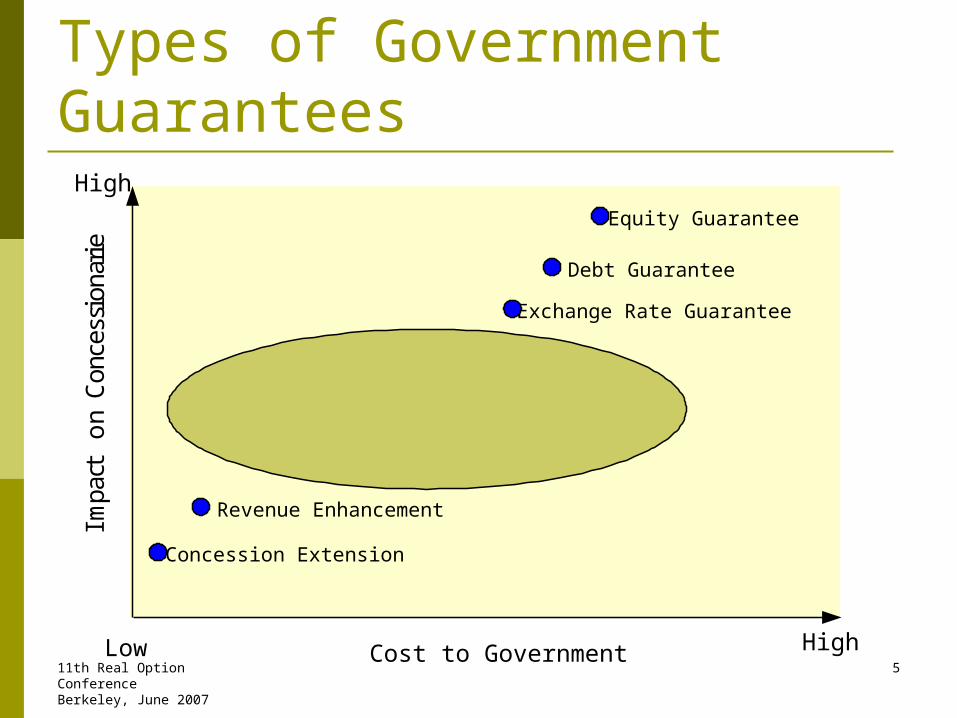

Level of Guarantees

Government retains revenuesgenerates by traffic above the

ceiling

Concessionaire receivesa subsidy proportional to traffic below the floor

Concession Period

Tra

ffic

De

man

d

11th Real Option ConferenceBerkeley, June 2007

9

Level of Guarantees

Concession Period

Tra

ffic

De

man

d

Concessionaire receivesa subsidy proportional to traffic below the floor

Government retains revenuesgenerates by traffic above the

ceiling

11th Real Option ConferenceBerkeley, June 2007

10

Level of GuaranteesT

raffi

c D

em

and

Government retains revenuesgenerates by traffic above the

ceiling

Concessionaire receivesa subsidy proportional to traffic below the floor

Concession Period

11th Real Option ConferenceBerkeley, June 2007

11

Level of Guarantees

Concession Period

Concessionaire receivesa subsidy proportional to traffic below the floor

Government retains revenuesgenerates by traffic above the

ceiling

Tra

ffic

De

man

d

The BR-163 Project

15

11th Real Option ConferenceBerkeley, June 2007

16

11th Real Option ConferenceBerkeley, June 2007

18

11th Real Option ConferenceBerkeley, June 2007

19

11th Real Option ConferenceBerkeley, June 2007

20

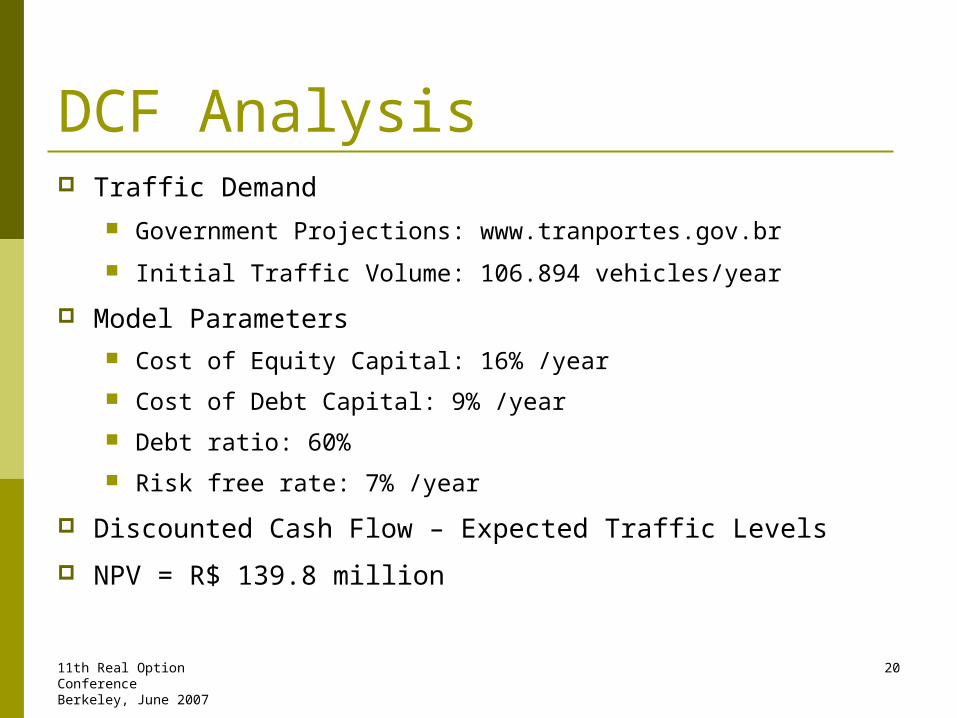

DCF Analysis Traffic Demand

Government Projections: www.tranportes.gov.br

Initial Traffic Volume: 106.894 vehicles/year

Model Parameters Cost of Equity Capital: 16% /year

Cost of Debt Capital: 9% /year

Debt ratio: 60%

Risk free rate: 7% /year

Discounted Cash Flow – Expected Traffic Levels

NPV = R$ 139.8 million

Projeção de Tráfego: (VHE)

Ano Ano PraçaCalendário Concessão 1 2 3 4 5 6 7 8 9 10 11

2004 -3 12.894 11.215 10.391 9.072 7.116 7.116 7.116 7.116 7.116 5.570 5.241 89.9642005 -2 13.255 11.529 10.682 9.326 7.316 7.316 7.316 7.316 7.316 5.726 5.388 92.4832006 -1 13.626 11.852 10.981 9.587 7.520 7.520 7.520 7.520 7.520 5.887 5.538 95.0732007 0 14.008 12.184 11.289 9.856 7.731 7.731 7.731 7.731 7.731 6.052 5.694 97.7352008 1 16.062 13.959 13.267 11.827 9.550 9.550 9.550 9.550 9.550 7.600 7.246 117.7102009 2 17.679 15.457 14.773 13.326 10.927 10.927 10.927 10.927 10.927 8.743 8.364 132.9732010 3 19.079 16.753 16.070 14.616 12.092 12.092 12.092 12.092 12.092 9.695 9.304 145.9762011 4 20.340 17.903 17.242 15.772 13.123 13.123 13.123 13.123 13.123 10.533 10.110 157.5112012 5 21.501 18.989 18.307 16.822 14.046 14.046 14.046 14.046 14.046 11.269 10.848 167.9642013 6 22.589 19.982 19.280 17.773 14.904 14.904 14.904 14.904 14.904 11.957 11.511 177.6082014 7 23.618 20.907 20.210 18.663 15.691 15.691 15.691 15.691 15.691 12.582 12.128 186.5622015 8 24.590 21.788 21.077 19.509 16.428 16.428 16.428 16.428 16.428 13.182 12.694 194.9752016 9 25.146 22.121 21.377 19.735 16.626 16.626 16.626 16.626 16.626 13.364 12.857 197.7282017 10 25.710 22.461 21.675 19.960 16.833 16.833 16.833 16.833 16.833 13.568 13.019 200.5542018 11 26.262 22.818 22.002 20.202 17.050 17.050 17.050 17.050 17.050 13.755 13.196 203.4822019 12 26.832 23.173 22.327 20.450 17.266 17.266 17.266 17.266 17.266 13.951 13.372 206.4342020 13 27.396 23.550 22.646 20.701 17.483 17.483 17.483 17.483 17.483 14.167 13.555 209.4272021 14 27.979 23.929 22.994 20.964 17.726 17.726 17.726 17.726 17.726 14.373 13.739 212.6052022 15 28.557 24.326 23.348 21.234 17.968 17.968 17.968 17.968 17.968 14.593 13.931 215.8272023 16 29.175 24.749 23.712 21.511 18.216 18.216 18.216 18.216 18.216 14.830 14.133 219.1892024 17 29.772 25.172 24.094 21.811 18.475 18.475 18.475 18.475 18.475 15.069 14.341 222.6302025 18 30.391 25.604 24.478 22.117 18.752 18.752 18.752 18.752 18.752 15.316 14.555 226.2172026 19 31.019 26.058 24.882 22.428 19.025 19.025 19.025 19.025 19.025 15.574 14.787 229.8702027 20 31.678 26.523 25.285 22.753 19.329 19.329 19.329 19.329 19.329 15.842 15.015 233.7402028 21 32.336 26.994 25.714 23.094 19.619 19.619 19.619 19.619 19.619 16.117 15.251 237.5992029 22 33.016 27.485 26.154 23.446 19.938 19.938 19.938 19.938 19.938 16.407 15.500 241.6972030 23 33.709 28.005 26.620 23.806 20.267 20.267 20.267 20.267 20.267 16.707 15.763 245.9452031 24 34.410 28.530 27.090 24.187 20.613 20.613 20.613 20.613 20.613 17.021 16.027 250.3272032 25 35.149 29.093 27.580 24.571 20.965 20.965 20.965 20.965 20.965 17.352 16.314 254.881

Total

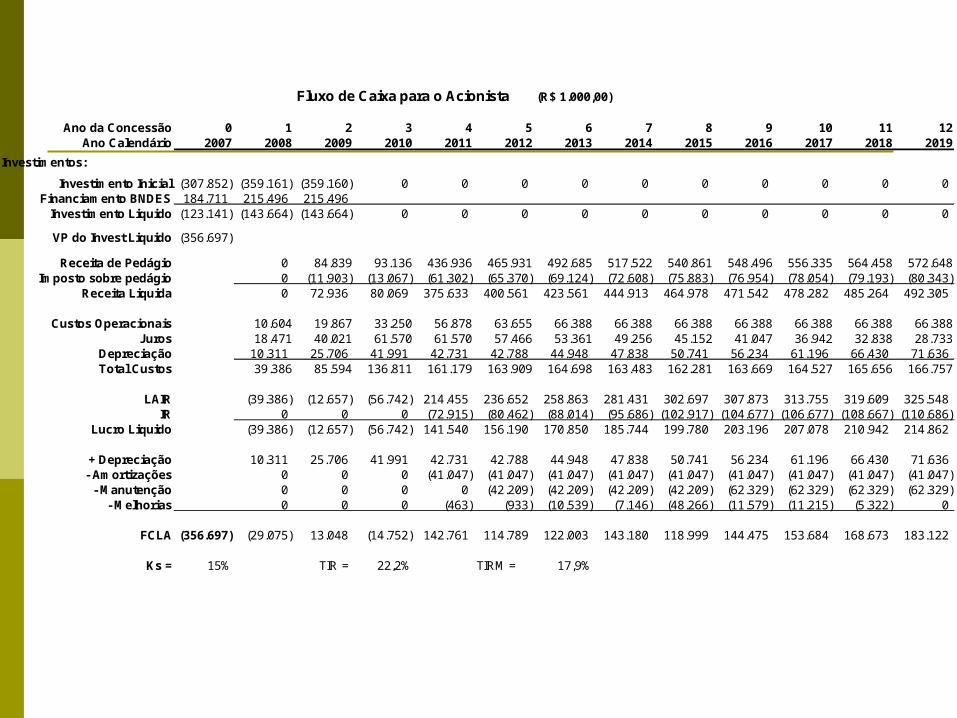

Fluxo de Caixa para o Acionista (R$ 1.000,00)

Ano da Concessão 0 1 2 3 4 5 6 7 8 9 10 11 12Ano Calendário 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Investimentos:

Investimento Inicial (307.852) (359.161) (359.160) 0 0 0 0 0 0 0 0 0 0Financiamento BNDES 184.711 215.496 215.496

Investimento Liquido (123.141) (143.664) (143.664) 0 0 0 0 0 0 0 0 0 0

VP do Invest Liquido (356.697)

Receita de Pedágio 0 84.839 93.136 436.936 465.931 492.685 517.522 540.861 548.496 556.335 564.458 572.648Imposto sobre pedágio 0 (11.903) (13.067) (61.302) (65.370) (69.124) (72.608) (75.883) (76.954) (78.054) (79.193) (80.343)

Receita Liquida 0 72.936 80.069 375.633 400.561 423.561 444.913 464.978 471.542 478.282 485.264 492.305

Custos Operacionais 10.604 19.867 33.250 56.878 63.655 66.388 66.388 66.388 66.388 66.388 66.388 66.388Juros 18.471 40.021 61.570 61.570 57.466 53.361 49.256 45.152 41.047 36.942 32.838 28.733

Depreciação 10.311 25.706 41.991 42.731 42.788 44.948 47.838 50.741 56.234 61.196 66.430 71.636Total Custos 39.386 85.594 136.811 161.179 163.909 164.698 163.483 162.281 163.669 164.527 165.656 166.757

LAIR (39.386) (12.657) (56.742) 214.455 236.652 258.863 281.431 302.697 307.873 313.755 319.609 325.548IR 0 0 0 (72.915) (80.462) (88.014) (95.686) (102.917) (104.677) (106.677) (108.667) (110.686)

Lucro Liquido (39.386) (12.657) (56.742) 141.540 156.190 170.850 185.744 199.780 203.196 207.078 210.942 214.862

+ Depreciação 10.311 25.706 41.991 42.731 42.788 44.948 47.838 50.741 56.234 61.196 66.430 71.636 - Amortizações 0 0 0 (41.047) (41.047) (41.047) (41.047) (41.047) (41.047) (41.047) (41.047) (41.047)

- Manutenção 0 0 0 0 (42.209) (42.209) (42.209) (42.209) (62.329) (62.329) (62.329) (62.329) - Melhorias 0 0 0 (463) (933) (10.539) (7.146) (48.266) (11.579) (11.215) (5.322) 0

FCLA (356.697) (29.075) 13.048 (14.752) 142.761 114.789 122.003 143.180 118.999 144.475 153.684 168.673 183.122

Ks = 15% TIR = 22,2% TIRM = 17,9%

11th Real Option ConferenceBerkeley, June 2007

23

NPV Distribution – no guarantees

-0,75-0,75

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% > -,2844 ,6596

Mean=139003,5 Mean=139003,5

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,200

0,400

0,600

0,800

1,000

1,200

1,400

1,600

Mean=139003,5

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

24

NPV Distribution with 30% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,2809 ,6495

Mean=138883,3

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,200

0,400

0,600

0,800

1,000

1,200

1,400

1,600

Mean=138883,3

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

25

NPV Distribution with 40% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,2863 ,6541

Mean=139630,7

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,200

0,400

0,600

0,800

1,000

1,200

1,400

1,600

Mean=139630,7

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

26

NPV Distribution with 50% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,2855 ,6621

Mean=150563,9

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=150563,9

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

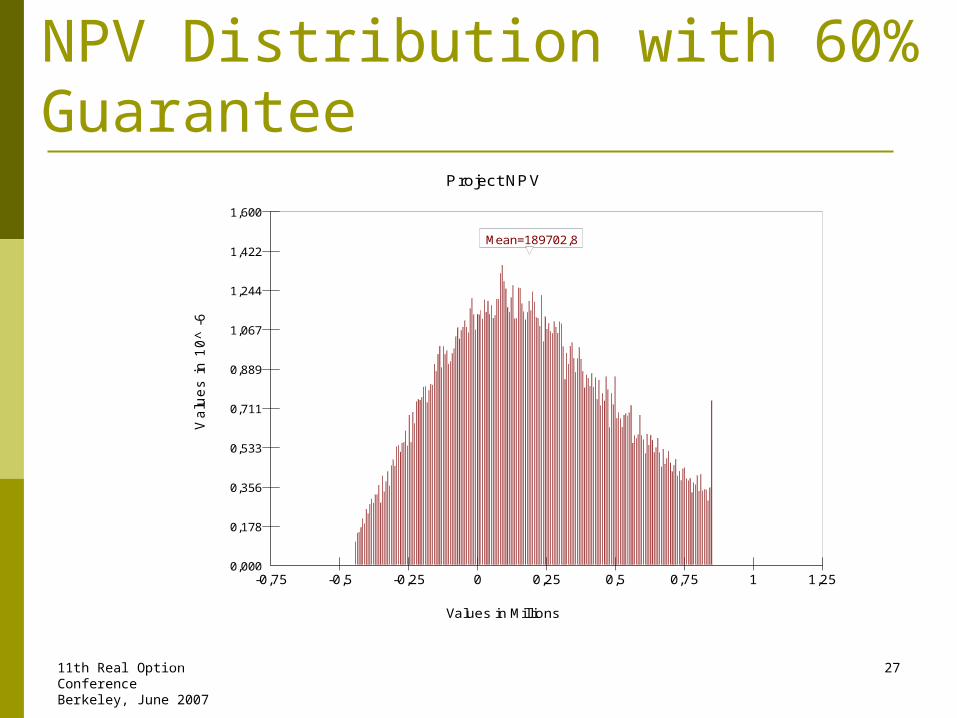

27

NPV Distribution with 60% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,2851 ,728

Mean=189702,8

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=189702,8

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

28

NPV Distribution with 65% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,277 ,7838

Mean=226474,3

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=226474,3

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

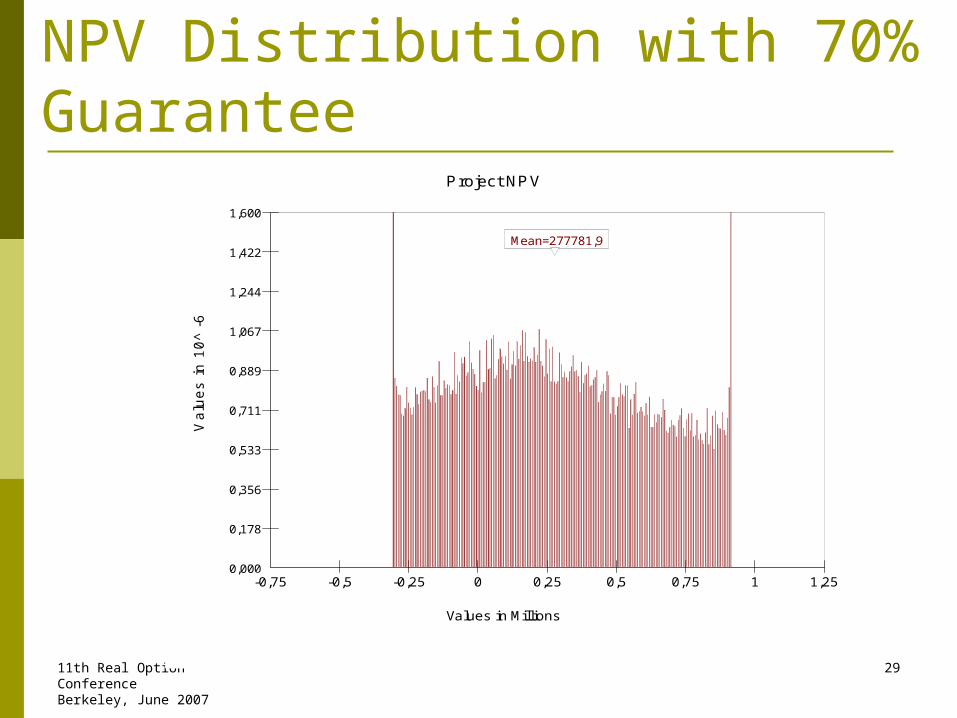

29

NPV Distribution with 70% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,2511 ,8585

Mean=277781,9

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=277781,9

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

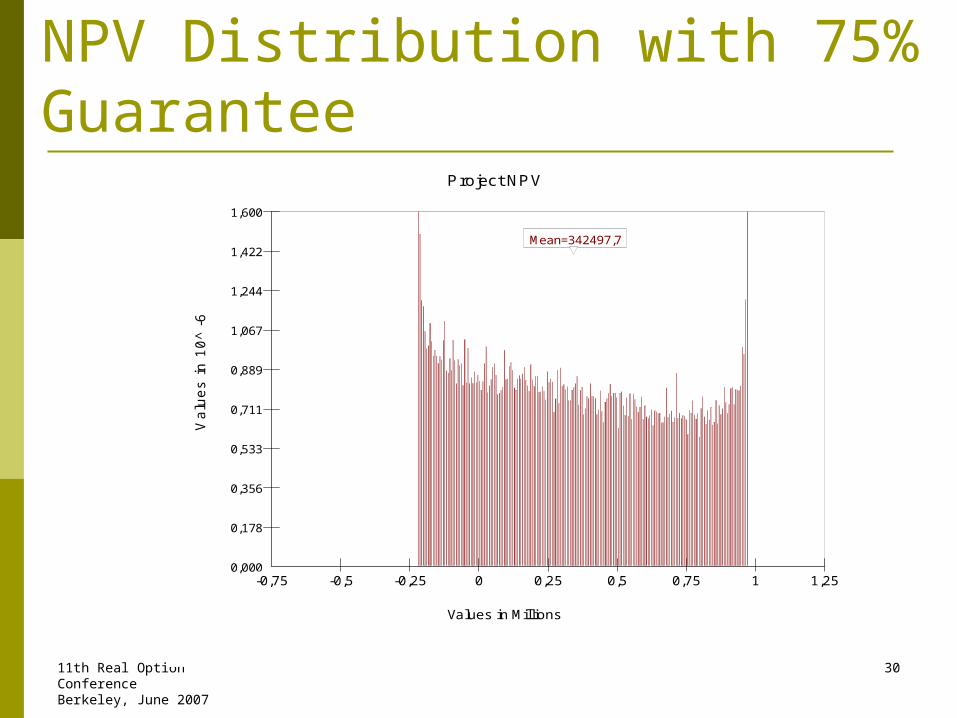

30

NPV Distribution with 75% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,1958 ,9409

Mean=342497,7

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=342497,7

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

31

NPV Distribution with 80% Guarantee

1,251,25

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% -,107 1,0369

Mean=427200

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=427200

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

32

NPV Distribution with 85% Guarantee

-0,75-0,75

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% ,0286 1,1164

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

Mean=526444,6 Mean=526444,6

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=526444,6

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

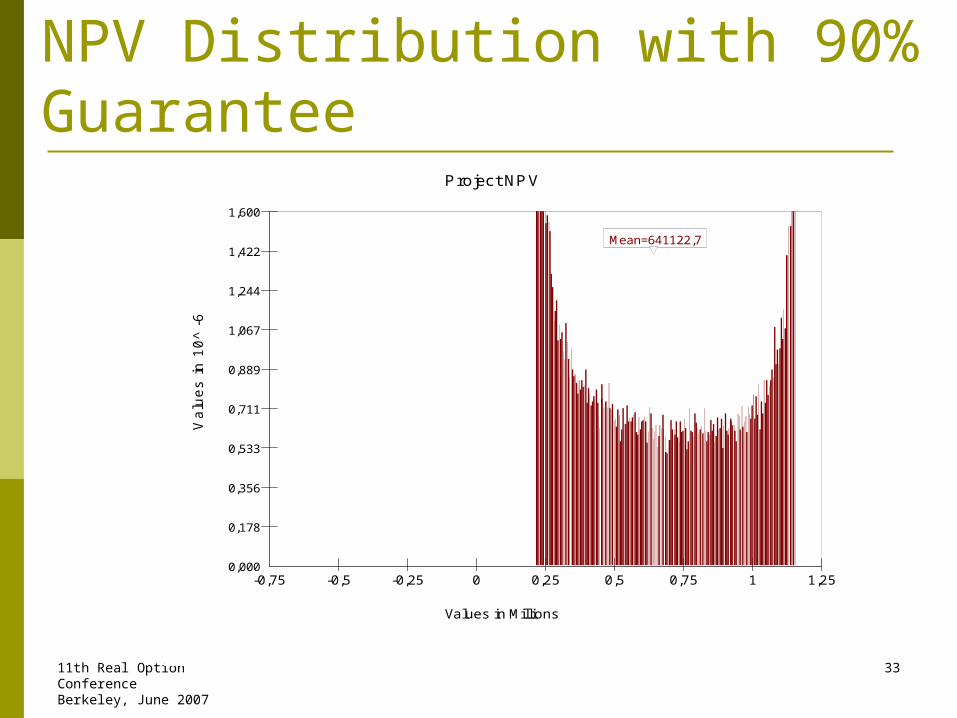

33

NPV Distribution with 90% Guarantee

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

5% 90% 5% ,2153 1,1592

Mean=641122,7

Project NPV

Val

ues

in 1

0^ -

6

Values in Millions

0,000

0,178

0,356

0,533

0,711

0,889

1,067

1,244

1,422

1,600

Mean=641122,7

-0,75 -0,5 -0,25 0 0,25 0,5 0,75 1 1,25

11th Real Option ConferenceBerkeley, June 2007

34

Effect of Guarantee on Project

0

200

400

600

800

20% 30% 40% 50% 60% 70% 80% 90%

Traffic Guarantee (%)

R$

Mill

ion

s

NPV w/o Guarantee

NPV w/ Guarantee

11th Real Option ConferenceBerkeley, June 2007

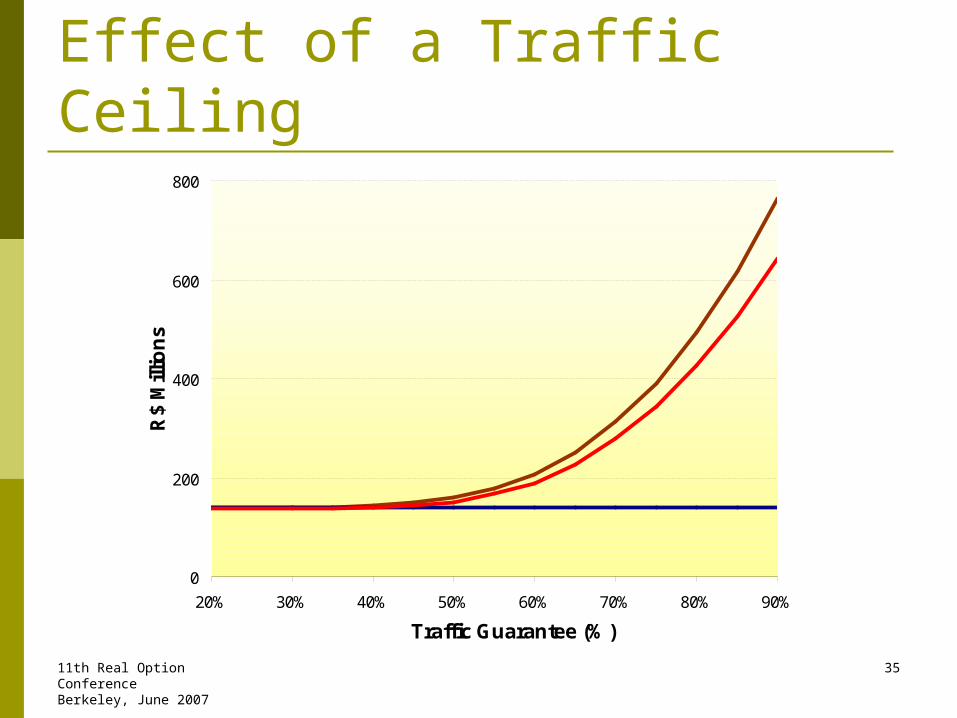

35

Effect of a Traffic Ceiling

0

200

400

600

800

20% 30% 40% 50% 60% 70% 80% 90%

Traffic Guarantee (%)

R$

Mill

ion

s

NPV w/o Guarantee

NPV w/ Guarantee

NPV w/ Ceiling

11th Real Option ConferenceBerkeley, June 2007

36

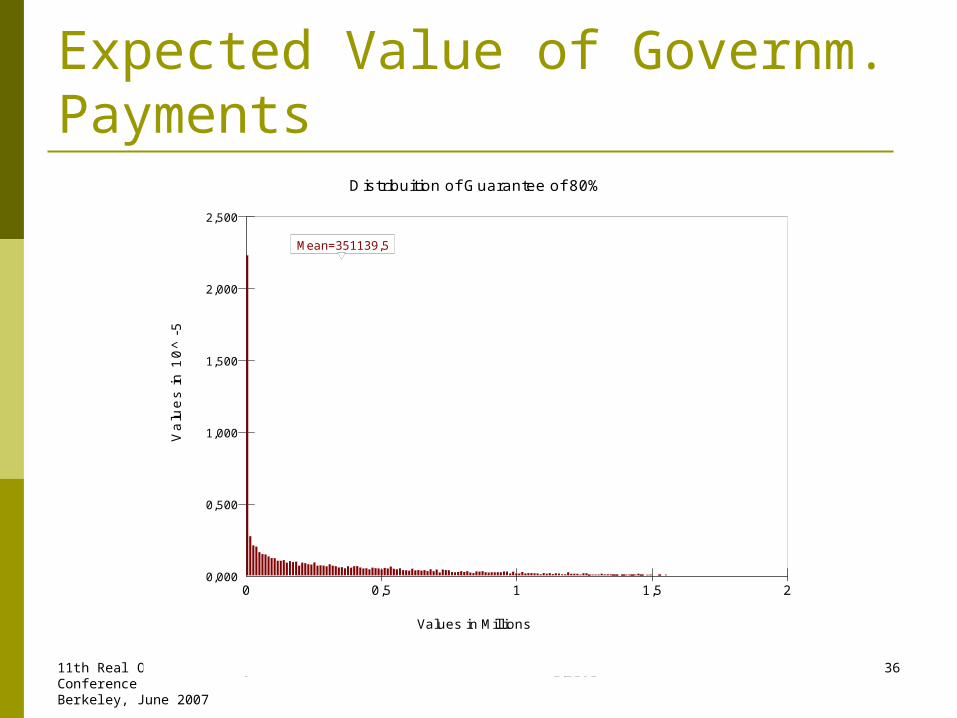

Expected Value of Governm. Payments

00

0 0,5 1 1,5 2

75,1% 5% > 0 1,2161

Mean=351139,5

Distribuition of Guarantee of 80%

Va

lue

s in

10

^ -5

Values in Millions

0,000

0,500

1,000

1,500

2,000

2,500

Mean=351139,5

0 0,5 1 1,5 2

11th Real Option ConferenceBerkeley, June 2007

37

NPV with Guarantee Caps

0

200

400

600

800

20% 30% 40% 50% 60% 70% 80% 90%

Traffic Guarantee (%)

R$

Mill

ion

s

NPV w/o Guarantee

No Cap

400M Cap

600M Cap

11th Real Option ConferenceBerkeley, June 2007

38

Expected Value of Payments w/ Caps

-100 0 100 200 300 400 500 600 700

5% 90% 5% 0 600

Mean=259243,5

80% Guarantee with 600M Cap

Va

lue

s in

10

^ -5

Values in Thousands

0,000

0,200

0,400

0,600

0,800

1,000

1,200

Mean=259243,5

-100 0 100 200 300 400 500 600 700-50 75 200 325 450

5% 90% 5% 0 400

Mean=201896

80% Guarantee with 400M Cap

Va

lue

s in

10

^ -5

Values in Thousands

0,000

0,200

0,400

0,600

0,800

1,000

1,200

1,400

1,600

1,800

2,000

Mean=201896

-50 75 200 325 450

11th Real Option ConferenceBerkeley, June 2007

39

Conclusions Valuation of government guarantees require the use of

option pricing methods.

The effect of different levels of support on the value and the risk of the project can be measured.

The expected cost and its probability distribution can also be estimated through real option analysis.

Setting caps to outlays from guarantees can be an effective way to limit government liability

Other forms of supports can also be modeled with this approach.

Valuing Government Guarantees in Toll Road

Projects

Luiz Brandão (PUC-Rio)

Eduardo Saraiva (BNDES)

Jun 2007