VALUE CHAIN ROADMAP FOR PULSES - · PDF fileThis value chain roadmap was developed on the...

89

KENYA VALUE CHAIN ROADMAP FOR PULSES 2016-2020

Transcript of VALUE CHAIN ROADMAP FOR PULSES - · PDF fileThis value chain roadmap was developed on the...

KENYAVALUE CHAIN ROADMAP FOR PULSES2016-2020

KENYA Value Chain Roadmap foR PulsEs

KENYA Value Chain Roadmap foR PulsEs

This value chain roadmap was developed on the basis of the process, methodology and technical assistance of the International Trade Centre ( ITC ) within the framework of its Trade Development Strategy programme.

ITC is the joint agency of the World Trade Organization and the United Nations. As part of the ITC mandate of fostering sustainable development through increased trade opportunities, the Trade Development Strategy programme offers a suite of trade-related strategy solutions to maximize the development payoffs from trade. ITC-facilitated trade development strategies and roadmaps are oriented to the trade objectives of a country or region and can be tailored to high-level economic goals, specific development targets or particular sectors, allowing policymakers to choose their preferred level of engagement.

The views expressed herein do not reflect the official opinion of ITC. Mention of firms, products and product brands does not imply the endorsement of ITC. This document has not been formally edited by ITC.

The International Trade Centre ( ITC )

Street address : ITC, 54-56, rue de Montbrillant, 1202 Geneva, SwitzerlandPostal address : ITC Palais des Nations 1211 Geneva, SwitzerlandTelephone : + 41- 22 730 0111Postal address : ITC, Palais des Nations, 1211 Geneva, SwitzerlandEmail : [email protected] : http :// www.intracen.org

Layout: Jesús Alés – www.sputnix.es

v

[ KENYA Value Chain Roadmap foR pulSeS ]

aCknowledgments

This value chain roadmap was elaborated as a component of the ITC Supporting Indian Trade and Investment in Africa ( SITA ) project, a south-south trade and in-vestment initiative that aims to improve the competitiveness of select value chains through the provision of partnerships by institutions and businesses from India. SITA is funded by the United Kingdom Department for International Development ( DFID ).

The formulation of the value chain roadmap was led by the Ministry of Industrialization and Enterprise Development and EAGC with the technical assistance of ITC. This document represents the ambitions of the private and public sector stakeholders for the development of the sector. Stakeholders’ commitment and comprehensive collaboration have helped build consensus around a common vision that reflects the realities and limitations of the private sector, as well as of policymakers and trade-related institutions.

The document benefited particularly from the inputs and guidance provided by the members of the sector team.

Name Organization Position

� Mr. Gerald MASILA EAGC Executive Director � Mr. Samwel RUTTO EAGC Regional Manager, Structured

Trading Systems � Mr. Peter GITHINJI EAGC Regional Programs Coordinator � Ms. Davine MINAYO EAGC Program Officer � Mr. Wainaina KUNG’U – Independent Consultant � Dr. Ganga RAO ICRISAT Senior Scientist � Mr. Oswald MIRITI CGA Project Officer

Technical support and guidance from ITC was rendered through Rahul Bhatnagar, Aman Goel, Bharat Kulkarni, Carlos Griffin. Nzuki Waita provided valuable support as National SITA coordinator.

vi

foRewoRds

Mr. Julius Korir pRinCipal seCRetaRy, industRialisation

ministRy of industRialisation & enteRpRise deVelopment

The Ministry of Industrialization and Enterprise Development ( MoIED ) takes particular pleasure in welcoming the SITA Pulses Sector Strategy Roadmap and its detailed Plan of Action.

Pulses are an important source of supplementary protein to daily diets based on cereals and starchy food for predominantly vegetarian populations like the Indian sub-continent. They provide energy, essential minerals, vitamins and several compounds consid-ered beneficial for good health. In Sub-Saharan Africa as well as India, pulses play a vital role by being a source of livelihood for millions of people; and offer tremendous potential to contribute to the alleviation of malnutrition among resource-poor farmers.

Kenya is the seventh largest world producer of com-mon beans and ranks fourth in terms of world produc-tion of pigeon pea after India, Myanmar and Malawi. Besides this, the country has recently popularized the production and consumption of green grams.

However, despite Kenya’s growing exports of pulses in recent years, it still remains a small player in the global market only ranking 26 th in world exports with a little under US $ 50 million worth of pulses exported in 2013-2014. Kenyan pulses exports have been char-acterized by high volatility over the past decade, with sharp variations observed over short periods of time.

The Pulses Sector Roadmap responds to these con-straints by providing Kenya with a detailed Plan of Action ( PoA ) that will facilitate growth in the sector within the next 5-year period. Through the steps out-lined in the PoA, pulses stakeholders in Kenya will improve their capability to offer competitive products. The roadmap also supports the implementation of Kenya’s Industrial Transformation Program ( KITP ) that has identified Agro-processing and respective

value chains as priority sectors for further develop-ment given the country’s comparative advantage.

The Pulses Sector Roadmap has exceeded our ex-pectations, not only in the successful mobilization of sector stakeholders, but also in facilitating extensive and fruitful discussions between public and private sectors. Some 35 representatives attended two suc-cessive consultations, allowing for a realistic evalu-ation of the challenges and opportunities the sector currently faces and extensive debates as to define the best way forward. This inclusive approach ensured that all stakeholders were committed to the process and left with a clear understanding of each actor’s role.

Market led strategic orientations prioritized by the pulses sector stakeholders and embedded into a detailed implementation plan, provide a clear road map that can be leveraged to address constraints to trade, maximise value addition and support regional integration.

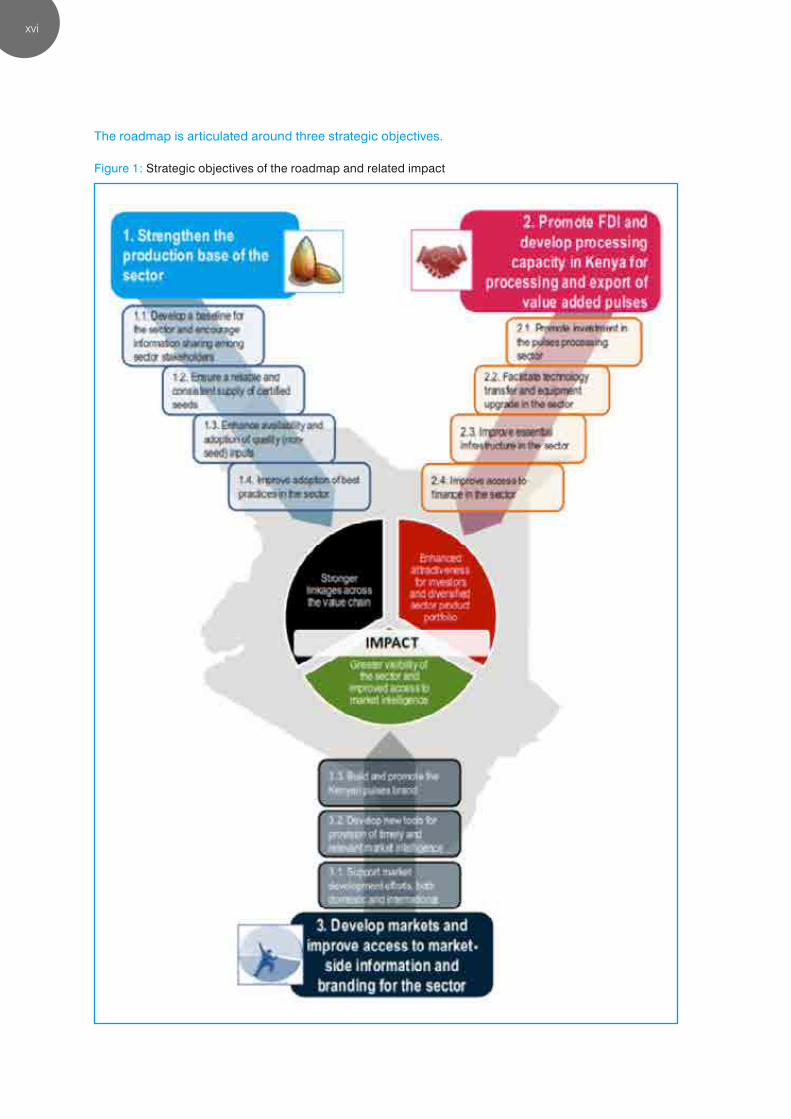

This roadmap is articulated around three strategic objectives :1. Strengthen the production base of the pulses

sector in Kenya2. Promote FDI and develop processing capacity

in Kenya.3. Develop markets and improve access to market

side information and branding for the pulses sector.

In order to maintain the momentum sparked by the consultations, the Ministry is taking steps towards es-tablishing an Apex Body for the Kenya pulses sector which will support the implementation of the opera-tional objectives defined in this Plan of Action.

vii

foRewoRds

Mr. GErAld MAKAu MAsilA exeCutiVe diReCtoR

easteRn afRiCa gRain CounCil

The Eastern Africa Grain Council ( EAGC ) is proud of its role as the Implementing Partner for the pulses value chain sector in the Supporting Indian Trade and Investment for Africa ( SITA ) project in Kenya and Tanzania.

EAGC is a regional, not-for-profit, membership-based organisation for the grain sector in Eastern and Southern Africa. The Council objective is to facili-tate efficient, structured and profitable trade in grain commodities and products for optimal benefits for all stakeholders – from producers to consumers.

In pursuit of our mandate, we provide a range of service and interventions aimed at developing and promoting structure grain trade including policy ad-vocacy to create and enabling environment for the grain sector to thrive, provision of market information through the regional agricultural trade intelligence network www.ratin.net, training and capacity build-ing of stakeholders on structured trading systems through our specialized training and capacity build-ing division the Eastern Africa Grain Institute ( EAGI ), grains post-harvest management, quality and safety assurance, warehousing, warehouse receipt systems and trade facilitation through the recently launched EAGC GSoko grain trading system.

As such, we are delighted by the SITA project which is bringing in the increased attention being afforded to the pulses sector in East Africa. Indeed, we see the pulses sector as a sleeping giant that once awoken, will play a significant role in socioeconomic develop-ment in Kenya, particularly in the context of Vision 2030. The facts truly speak for themselves ; global demand for pulses has been growing rapidly over the years and is forecasted to remain strong for the fore-seeable future, driven by growing populations, rising incomes and increased awareness of the nutritional value of pulses amongst consumers.

India which accounts for a quarter of all global im-ports of pulses, the European Union, the Middle East and North Africa region and China represent lucra-tive markets for pulses. Despite these opportunities in the global pulses market, Kenya accounts for just 0.5 % of global exports as recently as 2014, notwith-standing the increased domestic production. Limited awareness of the potential value of pulses in global markets, relatively weak domestic market linkages, low adoption of good agricultural practices and lim-ited value addition are just some of the stumbling blocks that will need to be addressed henceforth.

Given the need for clear strategic orientation for the pulses value chain in Kenya, the Kenya Value Chain Roadmap for Pulses has therefore been developed at an opportune moment. This Roadmap is the prod-uct of extensive consultations with public and private sector stakeholders, leading to unprecedented levels of cooperation among sector operators. Key private sector stakeholders and leading institutions facilitat-ed an exhaustive analysis of the sector. Market-led strategic interventions that have been prioritized by stakeholders are embedded into a detailed imple-mentation plan, ensuring that this Roadmap can be leveraged to address constraints to trade, maximize value addition and support regional integration, and eventually transform Kenya into a major player in the global pulses market.

EAGC has been privileged to participate in the devel-opment of this Roadmap and reaffirms its full com-mitment to spearhead its implementation in close collaboration with the Government of Kenya, ITC and other strategic partners. With the Roadmap in place, we urge all stakeholders to join forces and revamp the Pulses Sector in Kenya.

viii

Contents

acknowledgments v

ExEcutivE suMMArY xii

GlobAl PulsEs vAluE chAiN 17grown in many areas but dominated by a few large supply countries 17

larger number of exporters dominated by a small number of leading suppliers 19

dry peas, kidney beans and lentils dominate the trade of pulses 21

switch of import markets from the west to the east 22

strong indian demand keeps prices remunerative 25

AN EvolviNG vAluE chAiN iN NEEd of suPPort 27

CompetitiVe ConstRaints affeCting the Value Chain . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

supply-side issues 43

Business environment issues 46

market entry issues 47

development issues 47

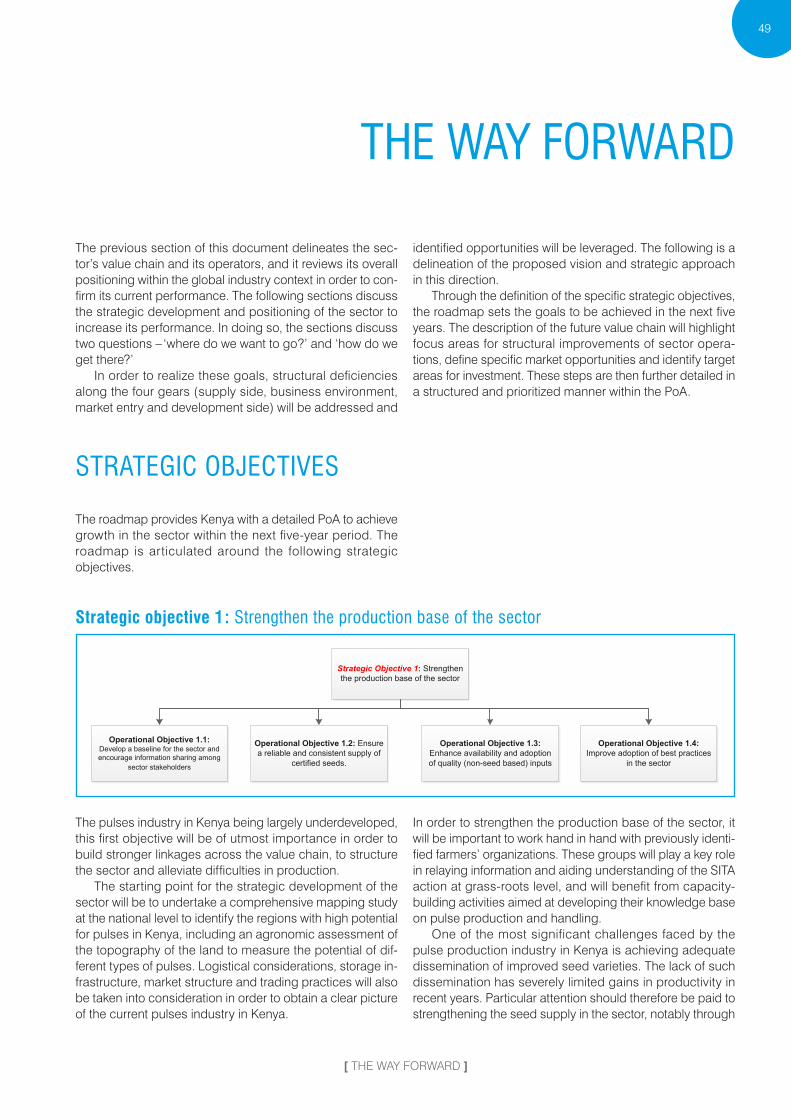

thE wAY forwArd 49

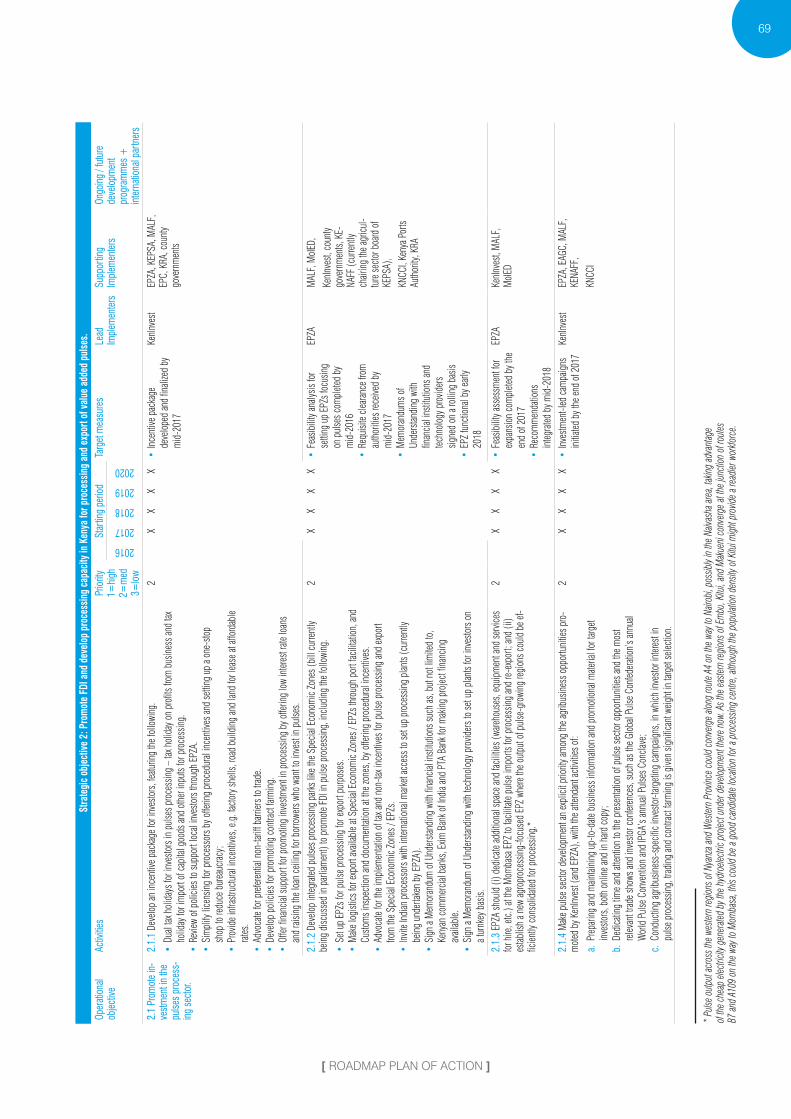

stRategiC oBjeCtiVes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

leVeRaging pRoduCt diVeRsifiCation and maRket oppoRtunities . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

leVeRaging inVestment to sCale up opeRations and ClimB the Value addition laddeR . . . . . . . . 55

pulse trading and processing 56

agribusiness inputs and services 56

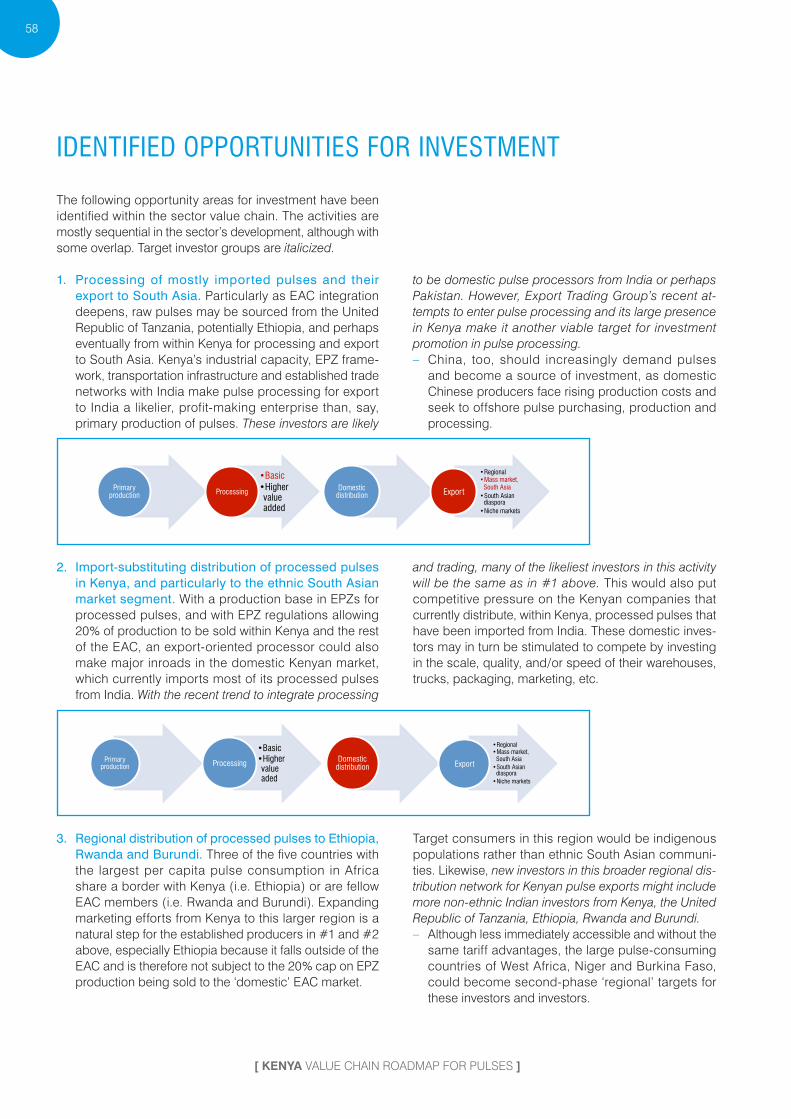

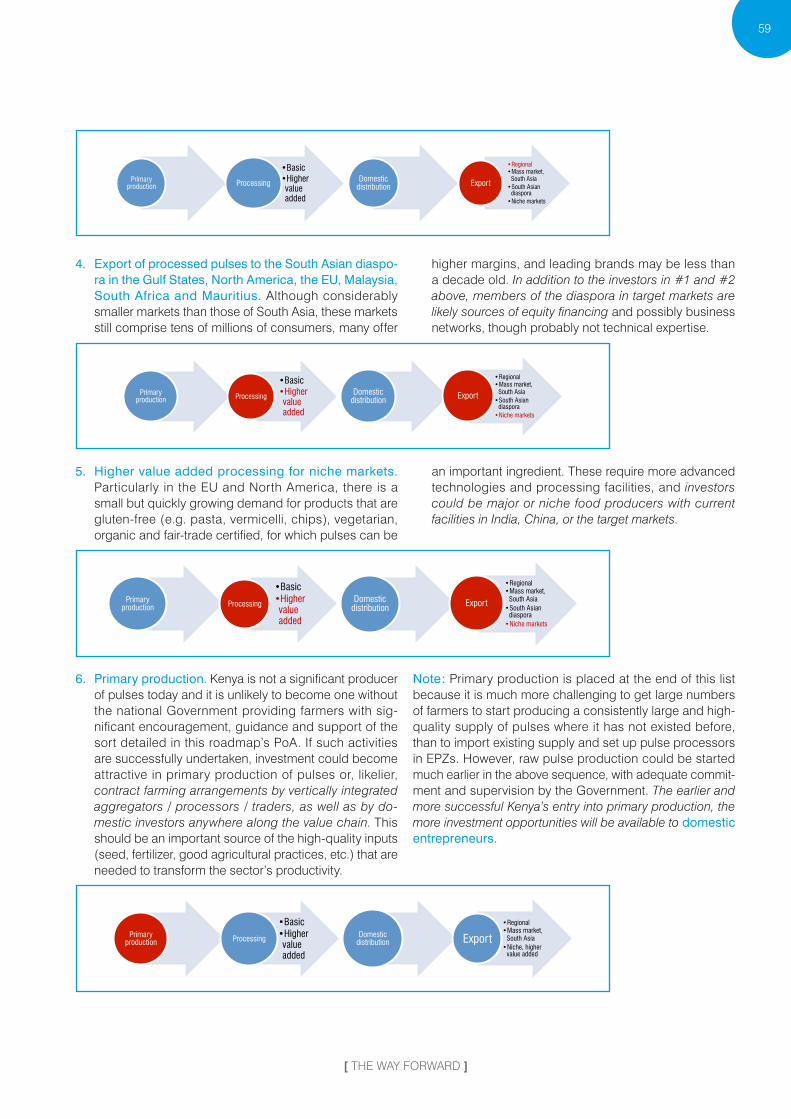

identified oppoRtunities foR inVestment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

MoviNG to ActioN 61

pRioRity aCtions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

roAdMAP PlAN of ActioN 65

appendix: kenya’s policies and trade agreements in a nutshell 74

References 81

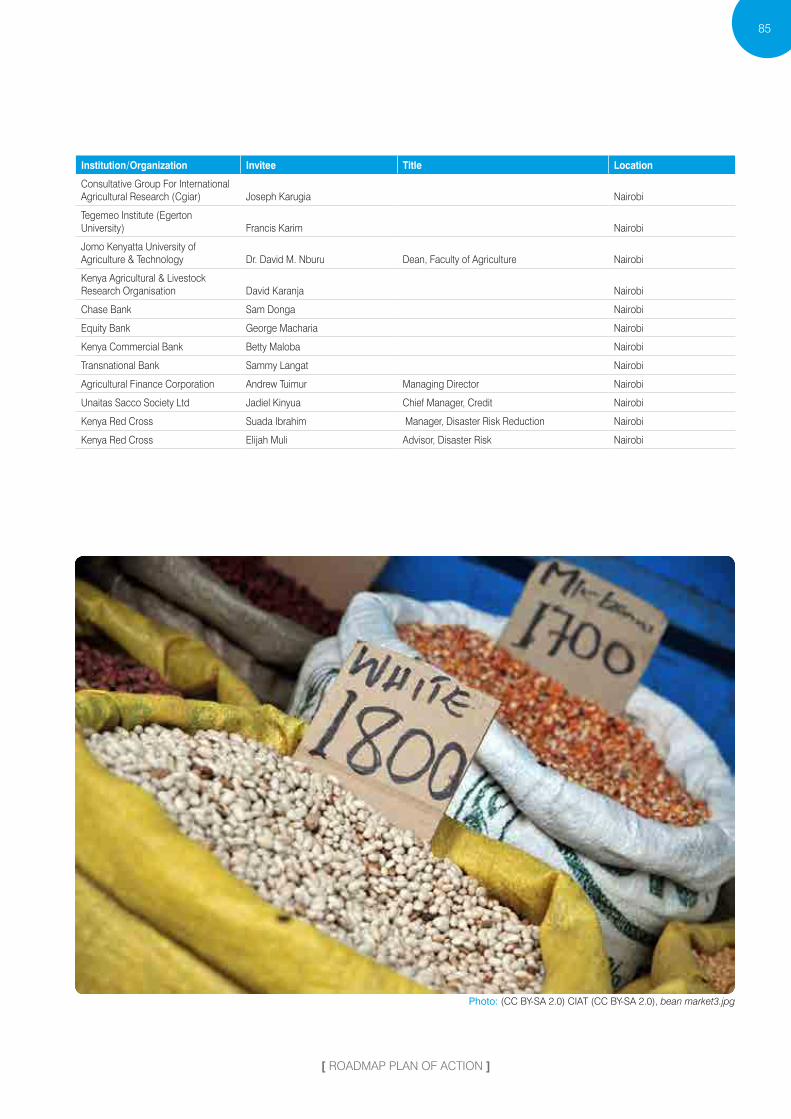

annex 1: list of invited participants 83

ix

[ KENYA Value Chain Roadmap foR pulSeS ]

figuRes

figure 1 : strategic objectives of the roadmap and related impact xvi

figure 2 : global pulses production and area harvested, 2003–2013 17

figure 3 : pulses production by region, average 2009–2013 18

figure 4 : share of pulse varieties in global production ( % ) – 2004 and present 18

figure 5 : exports of pulses, 2004–2014 ( us $ billions ) 19

figure 6 : exports of pulses by region or regional group, 2004–2014 ( us $ billions ) 20

figure 8 : kenyan production of pulses, 1961–2013 27

figure 9 : production of pulses in kenya, 2000–2013 29

figure 10 : production of pulses in kenya by subsector, 2000–2013 ( thousands of tons ) 29

figure 11 : kenyan production of dry beans, 2000–2013 30

figure 12 : kenyan production of cowpeas, 2000–2013 31

figure 13 : kenyan production of pigeon peas, 2000–2013 32

figure 14 : Current value chain 34

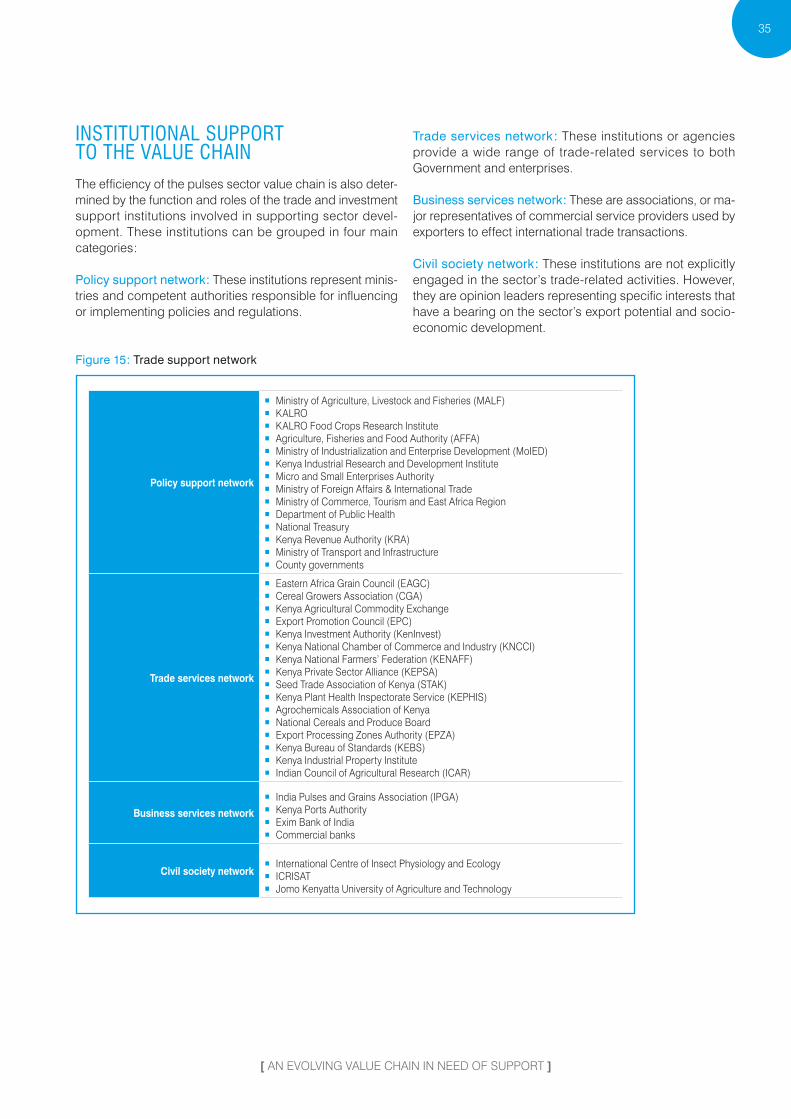

figure 15 : trade support network 35

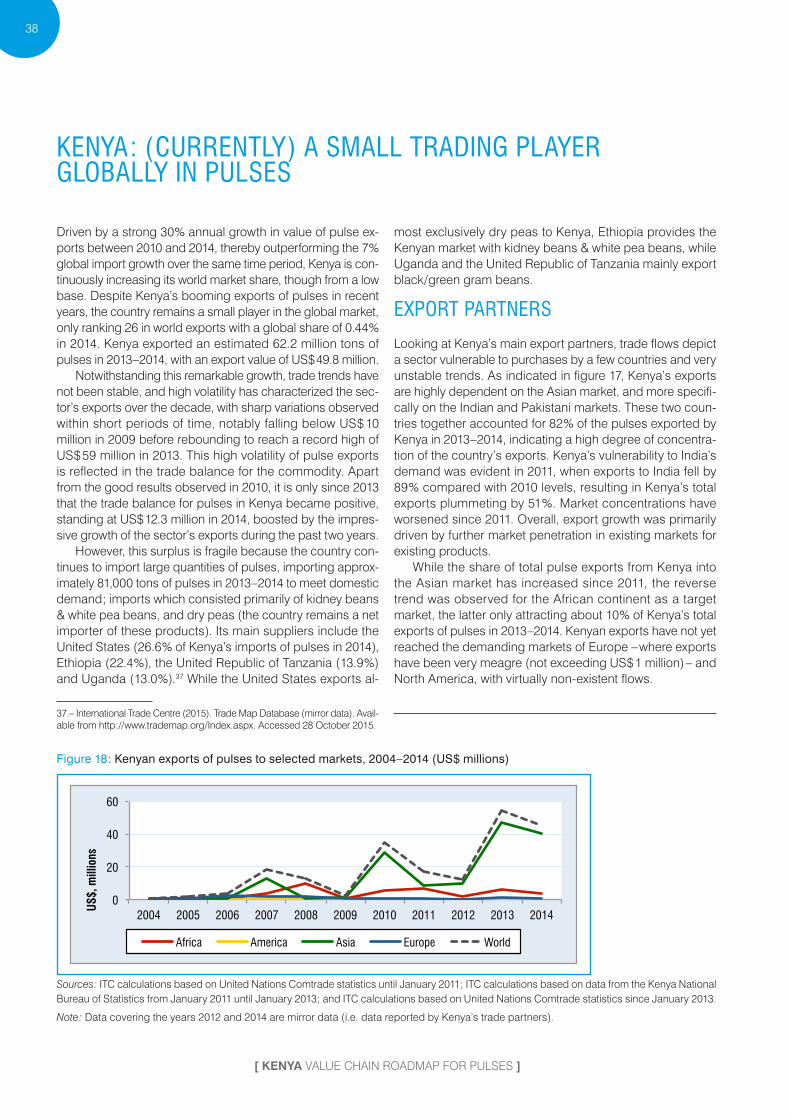

figure 18 : kenyan exports of pulses to selected markets, 2004–2014 ( us $ millions ) 38

figure 19 : kenya’s export basket of pulses, 2004–2014 ( us $ thousands ) 39

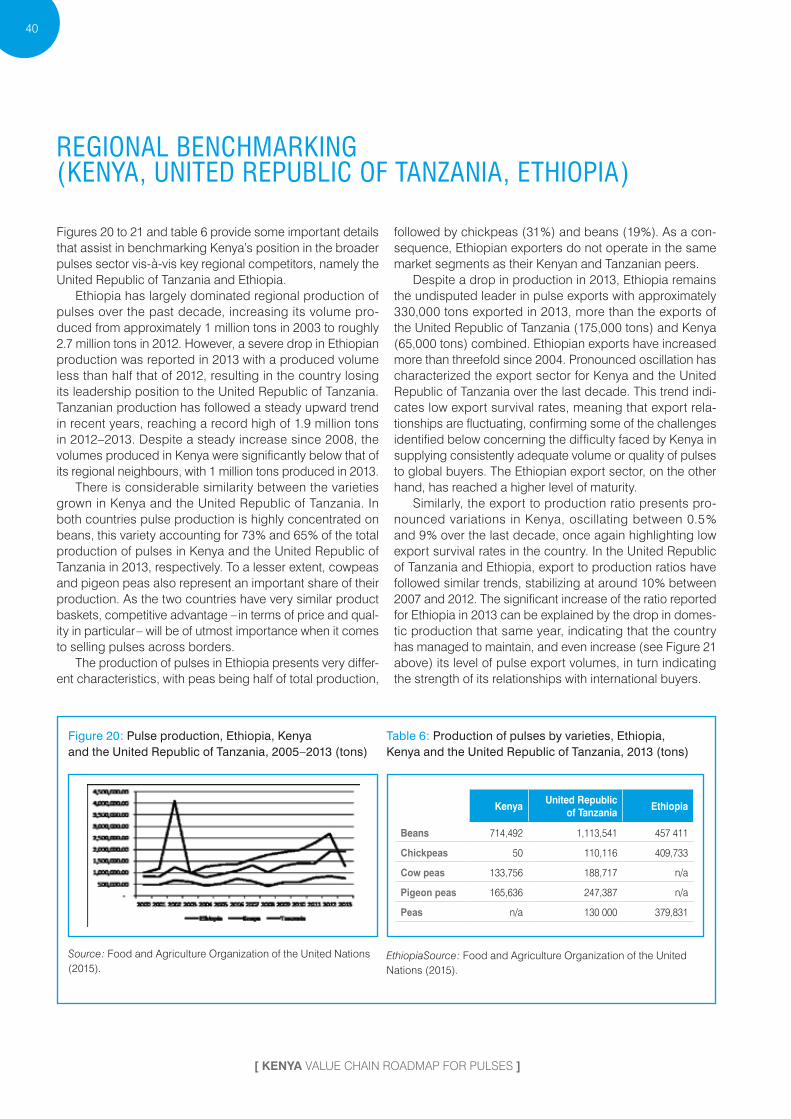

figure 20 : pulse production, ethiopia, kenya and the united Republic of tanzania, 2005–2013 ( tons ) 40

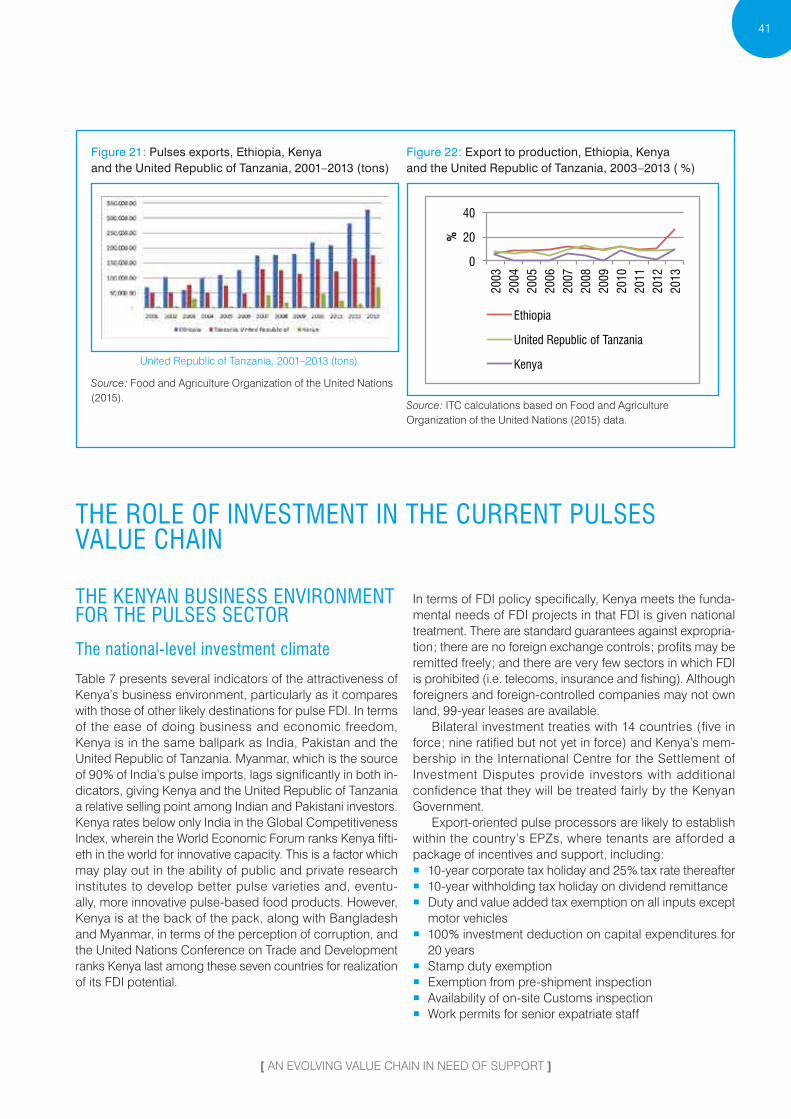

figure 21 : pulses exports, ethiopia, kenya and the united Republic of tanzania, 2001–2013 ( tons ) 41

figure 22 : export to production, ethiopia, kenya and the united Republic of tanzania, 2003–2013 ( % ) 41

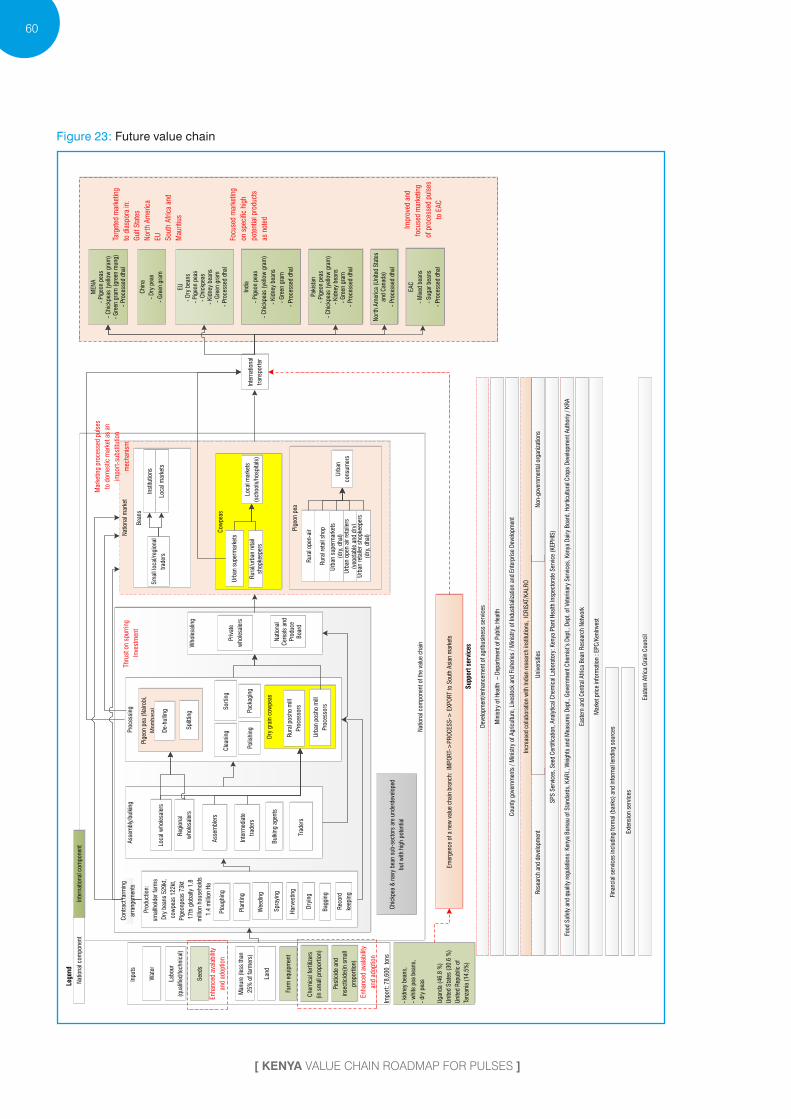

figure 23 : future value chain 60

x

taBles

table 1 : top 10 exporters of pulses ( harmonized system ( hs ) 0713 ), 2014 20

table 2 : pulse varieties with international supply >us $ 1 billion, 2014 21

table 3 : world-leading importers of pulses ( hs 0713 ) 22

table 4 : pulse production, trade and consumption of india, 2013–2014 to january 2015 ( tons ) 23

table 5 24

table 6 : production of pulses by varieties, ethiopia, kenya and the united Republic of tanzania, 2013 ( tons ) 40

table 7 : the investment climate in kenya and possible competitors for pulse investment 42

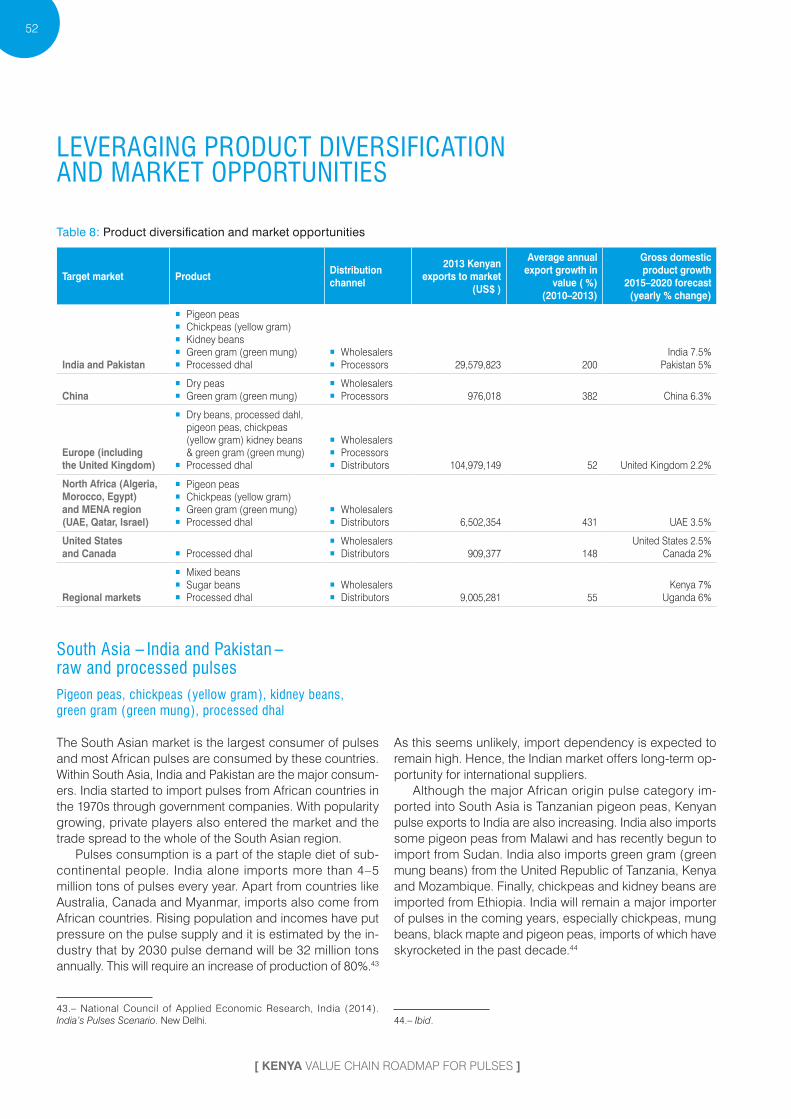

table 8 : product diversification and market opportunities 52

table 9 : Value chain segments needing fdi and likely sources 57

table 10 : the priority actions to kick-start implementation 61

xi

[ KENYA Value Chain Roadmap foR pulSeS ]

aCRonyms

The following abbreviations are used :

AffA Agriculture, Fisheries and Food Authority

AGMArKNEt Agricultural Marketing Information Network

cAGr Compound Annual Growth RatecGA Cereal Growers AssociationEAc East African CommunityEAGc Eastern Africa Grain CouncilEPc Export Promotion CouncilEPZ Export Processing ZoneEPZA Export Processing Zones AuthorityEu European UnionfAo Food and Agriculture Organization

of the United Nationsfdi Foreign Direct Investmentha HectareshaNPv Helicoverpa armigera

Nucleopolyhedrosis virushg Hectogramshs Harmonized SystemicAr Indian Council of Agricultural ResearchicrisAt International Crops Research Institute

for the Semi-Arid TropicsiPGA India Pulses and Grains Associationitc International Trade Centre

KAlro Kenya Agricultural & Livestock Research Organization

KEbs Kenya Bureau of StandardsKENAff Kenya National Farmers’ FederationKeninvest Kenya Investment AuthorityKEPhis Kenya Plant Health Inspectorate ServiceKEPsA Kenya Private Sector AllianceKNcci Kenya National Chamber of Commerce

and IndustryKrA Kenya Revenue AuthorityMAlf Ministry of Agriculture, Livestock

and FisheriesMENA Middle East and North AfricaMoiEd Ministry of Industrialization and

Enterprise DevelopmentPoA Plan of ActionPPP Public–Private PartnershiprAtiN Regional Agricultural Trade Intelligence

NetworksitA Supporting Indian Trade and Investment

in AfricasMs Short Message ServicestAK Seed Trade Association of KenyauAE United Arab Emirates

Photo: (CC BY-SA 2.0) CIAT (CC BY-SA 2.0), A climbing bean Aarmer.Ap

g

xii

exeCutiVe summaRy

the goal of Kenya’s Pulses value chain roadmap

the goal of Kenya’s Pulses value chain roadmap is to set the sector on the course of strategic develop-ment by addressing constraints in a comprehensive manner and defining concrete opportunities that can be realized through the specific steps detailed in its Plan of Action ( PoA ). Kenya’s pulses sector has recently shown signs of development, with booming exports in recent years as well as promising signs of diversification. While they were traditionally grown for sustenance, pulses have now become an important source of income for small Kenyan farmers. Nonetheless, the sector is still largely underdeveloped and exports are currently characterized by high volatility and a low level of survivability of trade relationships.

Efforts to address persistent constraints along the value chain must be made if the country is to compete on the international stage. The industry must build stronger linkages across the value chain, develop its knowledge base and attract investment in order to reach a higher – and sus-tainable – growth path and value addition. This will require addressing gaps in input supply, skills, market structure and institutional support. The PoA responds to these require-ments by setting three strategic objectives.

1. Strengthen the production base of the sector.a. Develop a baseline for the sector and encourage

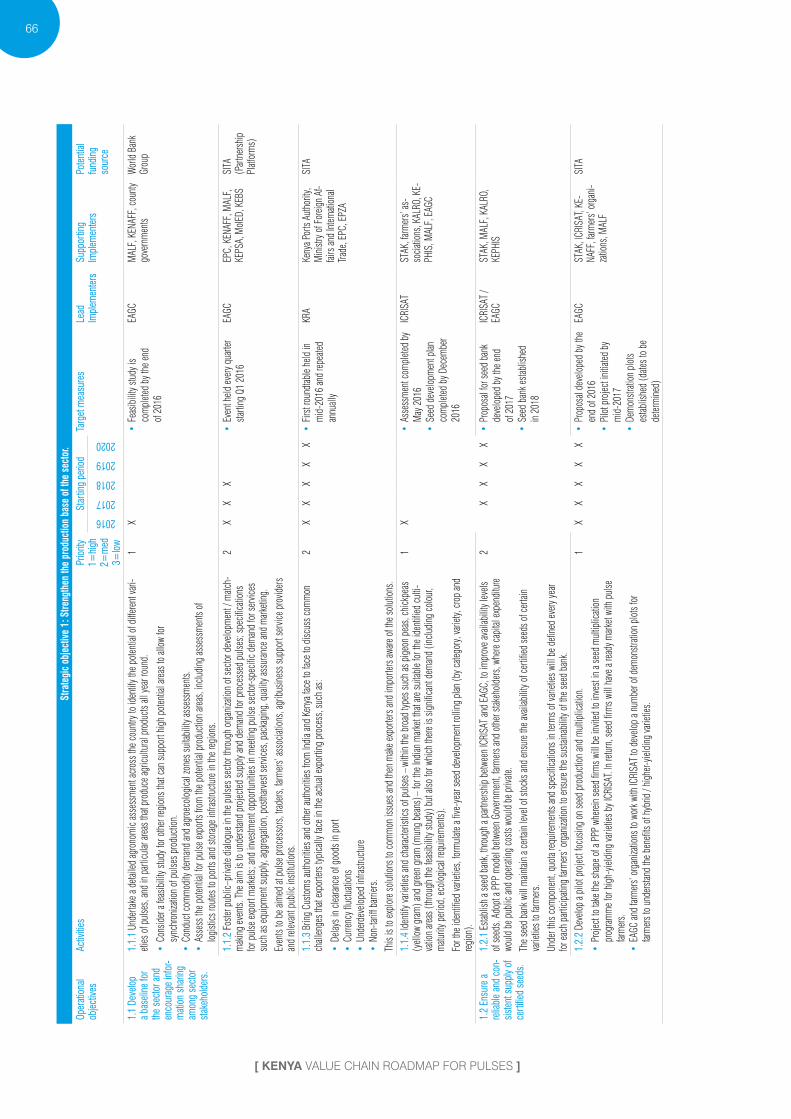

information sharing among sector stakeholders.b. Ensure a reliable and consistent supply of certified

seeds.c. Enhance the availability and adoption of quality

( non-seed ) inputs.d. Improve adoption of best practices in the sector.

2. Promote foreign direct investment ( FDI ) and develop processing capacity in Kenya for processing and export of value added pulses.a. Promote investment in the pulses processing sector.b. Facilitate technology transfer and equipment upgrade

in the sector.c. Improve essential infrastructure in the sector.d. Improve access to finance in the sector.

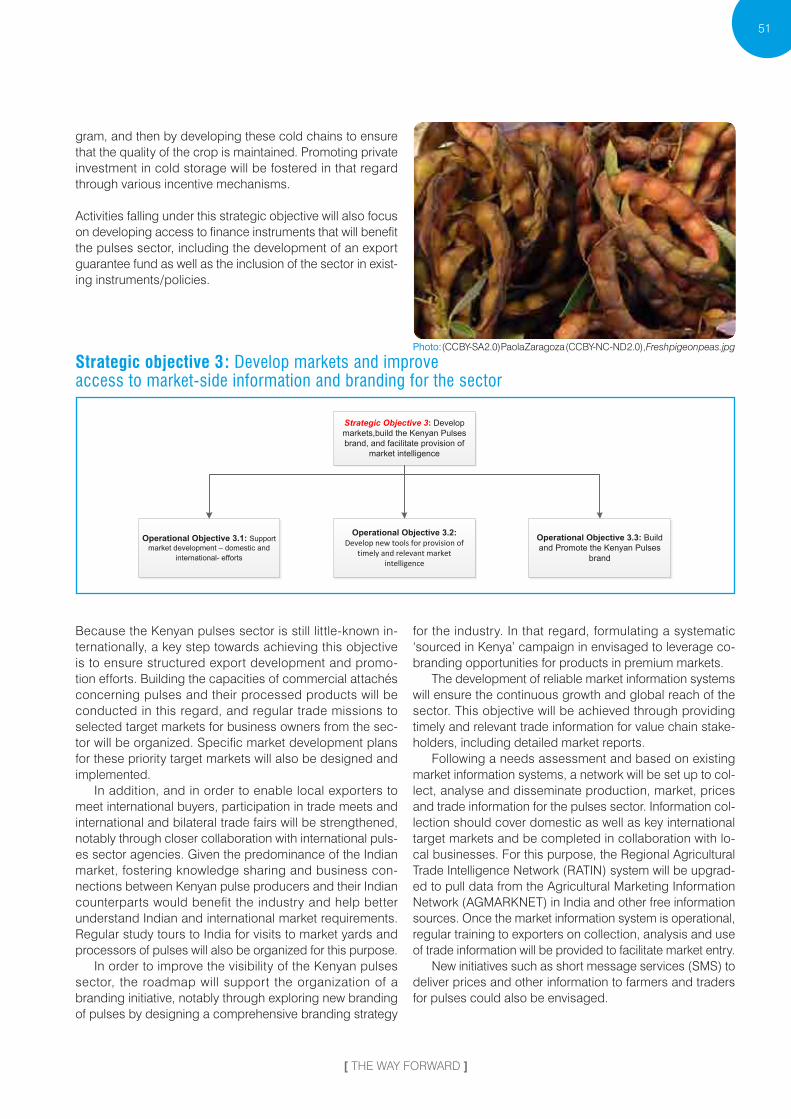

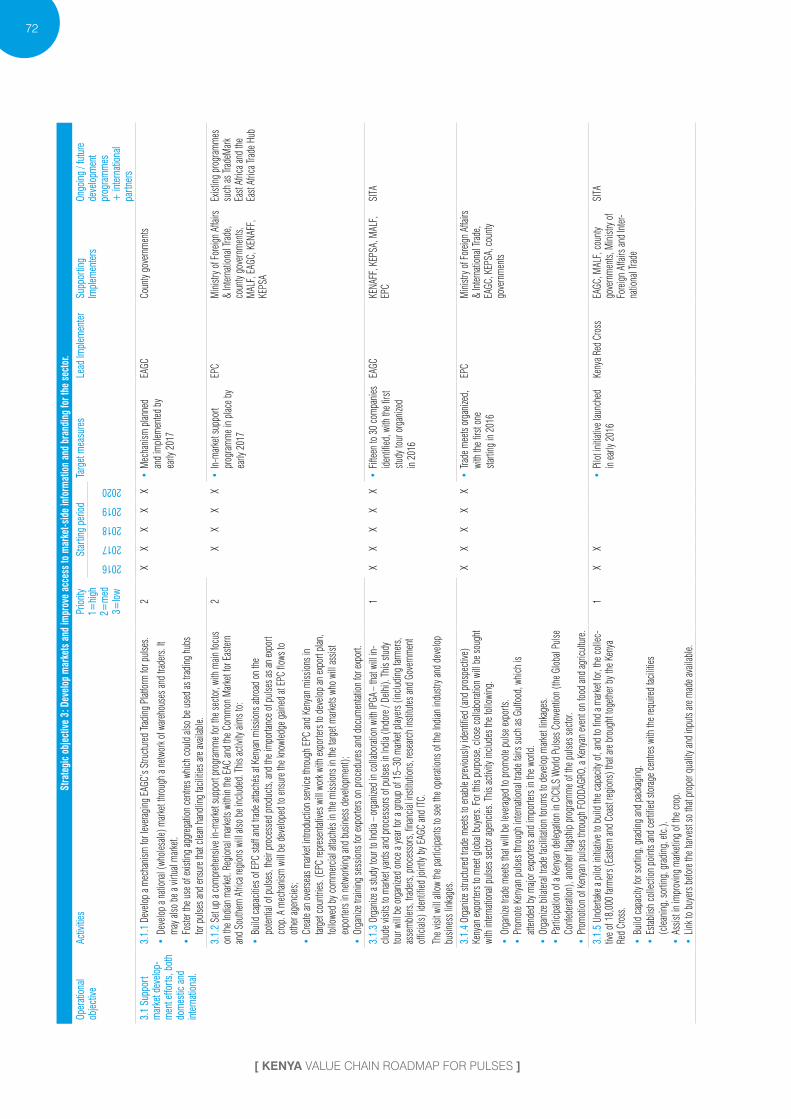

3. Develop markets and improve access to market-side information and branding for the sector.a. Support market development efforts, both domestic

and international.b. Develop new tools for provision of timely and rel-

evant market intelligence.c. Build and promote the Kenyan pulses brand.

Usually intercropped with maize, sugar cane and coffee, and grown entirely by smallholder farmers, pulses have historically received little attention from support institutions in Kenya, which tended to focus more on cash crops such as maize.

Due to their hardiness and resistance to drought, which makes them ideal for Kenya’s often sporadic rainfall, and also being an important food source due to their high protein content and relatively low cost when compared with meat, pulses have gained in popularity among farmers. In 2013, Kenyan farmers were cultivating pulses on 1.47 million hectares ( ha ) of land, involving roughly 1.8 million households and producing 1 million tons of pulses. Domestic production is largely dominated by the production of dry beans ( 715,000 tons ), followed by pigeon peas ( 166,000 tons ), and cowpeas ( 134,000 tons ). Despite periods of fluctuation the volume produced, as

Photo: (CC BY-SA 2.0) CIAT (CC BY-SA 2.0), A climbing bean Aarmer.Ap

g

xiii

[ KENYA Value Chain Roadmap foR pulSeS ]

well as the area harvested and yields, has progressed over the past decade, making Kenya the fourth top producer of pulses in Africa

after Nigeria, the United Republic of Tanzania and Ethiopia, and number 17 in the world ( Food and Agriculture

Organization of the United Nations ( FAO ) ).

Despite these recent positive developments, the sector remains largely underdeveloped, in

particular compared with other African produc-ers such as the United Republic of Tanzania and Ethiopia, and vertical and horizontal business linkages tend to be undeveloped and informal because trade is based on temporary relationships with limited use of contracts. More generally, the indus-try appears to be relatively unstructured and poorly organized, partly resulting from low levels of cooperation among the different actors and a lack of trust among the different stakeholders op-erating in the sector. Farmers’ groups and cooperatives in the pulses sector also appear to be weak or non-existent, in turn contributing to the overall lack knowledge of the potential of pulses in

Kenya.

The most significant challenge at the mo-ment is achieving adequate dissemination

of improved seed varieties because most farms use their own beans for seed or buy from

local markets. Lack of such dissemination has severely limited productivity gains and has greatly

hindered the development of the supply chain, further complicated by farmers’ reluctance to pay the high cost of

certified seeds. Improved bean varieties could, for example, yield from 1,500 to 2,500 kg / ha, whereas the majority of farmers

use seeds that yield approximately 400 kg / ha. In addition to the low quality of seeds, other inputs such as fertilizers, insecticides and pesticides

appear to be used by only a small proportion of the sector’s farmers.

The low adoption of improved agricultural practices also significantly hinders the performance of the sector. In particular, postharvest practices suffer from a number of problems including inappropriate handling, inadequate storage methods and facilities, and common pest infestation, resulting in a higher than necessary inci-dence of spoilage. These factors are further complicated by slow transport caused by an inadequate road system. International buyers have also highlighted the uneven quality of Kenyan products – which is a major limiting factor for the export of pulses from Kenya – due to a lack of quality certification and standardization mechanisms as well as a lack of knowledge about specific markets’ requirements in terms of quality standards.

xiv

Another key issue affecting the capacity of the industry is the limited knowledge base of pulse producers and exporters. Market information appears to be a major constraint for Kenyan producers and exporters because very little information is available on issues such as pulse varieties and types, the calendar of different pulses globally, market requirements, and price fluctuation and movements, among others. This lack of knowledge impacts the development of pulse exports in Kenya. Building capacity on these issues will allow the industry to identify international business op-portunities while mitigating some of the costs and risks for new market development, ultimately resulting in greater competitiveness.

The current stage of maturity of the sector is hindering Kenya’s ability to fully capitalize on the industry’s strong global growth. Driven by rising incomes and population, and greater awareness of the health properties of pulses, the global pulses sector is projected to see stable demand and consumption trends in the long term. In line with the upward trend in global production, the growth path of pulse exports globally has been significant : pulse exports doubled in 2003 in comparison with the previous 20 years.1 The major importers of this commodity are concentrated in South Asia, China, Europe, and the Middle East and North Africa ( MENA ) region, India alone capturing nearly a quarter of the world imports.

In such favourable circumstances, and despite Kenyan’s booming exports of pulses in recent years, the country remains a small player in the global market, only ranking 26 in world exports, with US $ 49.8 million worth of pulses exported in 2013–2014. Kenyan exports have been characterized by high volatility over the past decade, with sharp variations observed within short periods of time, also reflecting the low level of survivability of export relationships. Besides, the sector is extremely vulnerable to imports from India and Pakistan, which together account for 82 % of the pulses exported by Kenya. This also highlights the fact that Kenyan firms are not taking advantage of the preferential market access Kenya benefits from in many countries2 as these markets remain largely untapped. Although South Asia, China, Europe and the MENA region offer the maximum potential for pulse exports, market characteristics and sensitivities vary from one region to another, forcing exporters to be fully aware of market requirements while exploring these opportunities.

Although signs of product diversification have recently been observed, it ap-pears to be difficult, at this stage of maturity of the sector, to add value to pulse products in Kenya. More than half of Kenya’s pulse exports are comprised of kidney beans and white pea beans, with most exports of pulses consisting of raw products with extremely limited value added by processors. Kenya’s product diversification is nevertheless promising, providing that concerted actions are taken to expand further and promote long survival rates. Extra efforts also need to be made to penetrate new markets and to unlock the production of more pulse varieties.

Kenya has to catch up with its competitors to become a major player in the global pulses market. In order to achieve a greater level of competitiveness, the sector must build stronger linkages across the value chain with the view to structuring the

1.– Food and Agriculture Organization of the United Nations ( 2005 ). Pulses : Past Trends and Future Prospects. Summary of paper con-tributed by FAO to the 4th International Food Legumes Research Conference, New Delhi, 18–22 October. Available from http : // www.fao.org / fileadmin / templates / est / COMM_MARKETS_MONITORING / Pulses / Documents / PulsesStudy.pdf.2.– Kenya is a signatory state of the Common Market for Eastern and Southern Africa Free Trade Area, a Member State of the East African Community ( EAC ), and has recently signed the EU–EAC Economic Partnership Agreement.

xv

[ KENYA Value Chain Roadmap foR pulSeS ]

sector and alleviating difficulties in production, promoting FDI in the pulse process-ing sector, and ensuring structured export development and promotion efforts.

The roadmap responds to these needs by providing Kenya with a detailed PoA that will facilitate growth in the sector within the next five-year period. Through the steps outlined in the PoA, stakeholders will improve their ability to offer competitive products. To this end, improved competitiveness must be tied to further penetration of current markets in the short term, expansion into new markets in the medium term, and the development of new products in the longer term. Particularly promising prospects for sectoral development may lie within the following market opportunities and products.

Target market Product Distribution channel

India and Pakistan

� Pigeon peas � Chickpeas ( yellow gram ) � Kidney beans � Green gram ( green mung ) � Processed dhal

� Wholesalers � Processors

China � Dry peas � Green gram ( green mung )

� Wholesalers � Processors

Europe ( including the United Kingdom of Great Britain and Northern Ireland )

� Dry beans, processed dhal, pigeon peas, chickpeas ( yellow gram ) kidney beans & green gram ( green mung )

� Processed dhal

� Wholesalers � Processors � Distributors

North Africa ( Algeria, Morocco, Egypt ) and MENA region ( United Arab Emirates ( UAE ), Qatar, Israel )

� Pigeon peas � Chickpeas ( yellow gram ) � Green gram ( green mung ) � Processed dhal

� Wholesalers � Distributors

United States of America and Canada � Processed dhal � Wholesalers � Distributors

Regional markets

� Mixed beans � Sugar beans � Processed dhal

� Wholesalers � Distributors

The roadmap was the result of extensive consultations with public and private sector stakeholders, leading to unprecedented levels of cooperation among sector operators. Key private sector stakeholders and leading institutions facilitated an exhaustive analysis of the sector. Market-led strategic orientations, prioritized by stakeholders and embedded into a detailed implementation plan, provide a clear roadmap that can be leveraged to address constraints to trade, maximize value addi-tion and support regional integration. In addition, the inclusive approach ensured that all stakeholders were committed to the process and left with a clear understanding of each actor’s role.

xvi

The roadmap is articulated around three strategic objectives.

Figure 1 : Strategic objectives of the roadmap and related impact

[ GLOBAL PULSES VALUE CHAIN ]

17

gloBal pulses Value Chain

Pulses play an important role in farming systems worldwide. They have proved to be ideal crops for achieving improve-ments in nutrition and health conditions, reducing poverty through higher food security and enhancing ecosystem re-silience, particularly in developing countries.

Trade trends for this crop are determined by importing countries’ local production and by production in exporting countries, both of which are affected by weather conditions, disease management, price increases of other crops ( as farmers can be compelled to move towards a higher rent crop ) and countries’ trade policies ( such as export incen-tives ). The following trends characterize the sector.

gRown in many aReas But dominated By a few laRge supply CountRies

Fuelled notably by increasing demand from India and other developing countries, annual global production of pulses has seen unprecedented growth over the past decade with an average of 70 million tons produced yearly since 2009. Production grew at a sustainable average annual growth rate of 2.1 % over the period 2003–2013, from 59.5 million

tons in 2003 to 73.2 million tons in 2013 ( FAO ), indicating the excellent health of the sector ( see figure 2 ). According to the FAO Statistics Division, about 74 % of pulses are used for hu-man consumption and 20 % for feed use, with the remainder being used as seed.

increasing cultivated area but weak productivity growthThe progression of global production goes hand in hand with a significant increase in the area cultivated over the past five years. The average area under cultivation has gone up to 80 million ha since 2010, an encouraging sign considering that the area under cultivation stagnated at approximately 70 million ha between 1990 and 2003 ( see figure 2 ). Yields also continuously increased globally over the past decade, from 0.82 tons / ha in 2003 to 0.9 tons / ha in 2013, but significant discrepancies between developed and developing countries have been observed. For example, Canada reported yields well above 1.5 tons / ha, whereas the largest producer, India, is producing less than 1 ton / ha. This gap can be explained by differences in input use, technology and infrastructure. Owing to low and stagnant yields in developing countries, pulse production did not grow as rapidly as that of cereals and oilseeds.

Figure 2 : Global pulses production and area harvested, 2003–2013

50

60

70

80

90

50

60

70

80

90

2003

20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

Hect

ares

, mill

ions

US$,

mill

ions

Area cultivated Production

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

18

[ KENYA Value Chain Roadmap foR pulSeS ]

Figure 3 : Pulses production by region, average 2009–2013

Africa 22%

Americas 20%

Asia 45%

Europe 9%

Oceania 4%

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

Figure 4 : Share of pulse varieties in global production ( % ) – 2004 and present

31

20

14

7 6 6 5

13

17

24

16

9 9 6 6

11

0

5

10

15

20

25

30

35

Dry beans Dry peas Chickpeas Dry broad beans

Cow peas Lentils Pigeon peas

Others

2004 Present

Source : FAOSTAT ( 2015 ).

In spite of their relatively low yields, developing countries are the largest producers of pulses, accounting for around 70 % of global production, with India leading the way. With its large vegetarian population that is largely dependent on pulses, wheat and milk as its major sources of protein, India remains by far the largest producing country, alone account-ing for 25 % ( or 18.3 million tons ) of world production in 2013 ( FAO ). It is followed by Canada ( 8.3 % ), Myanmar ( 7.1 % ),

China ( 6.1 % ) and Nigeria ( 4.1 % ), which together account for more than half of global output. Pulses of African origin have gained significant importance in recent years, from 12.2 million tons produced over the period 2004–2008, or 20 % of global production, to 15.4 million tons between 2009 and 2013, or 22 % of total production ( see figure 3 ).

[ GLOBAL PULSES VALUE CHAIN ]

19

the medium-to-long term outlook is promising

Supported by an anticipated growth in yields to reach an av-erage of 1.6 tons / ha by 2050 ( Alexandratos and Bruinsma, 2012, p. 121 ), pulse production is expected to grow in the long term and is forecast to reach 100 million tons by 2050. Driven by rising incomes and population, and greater aware-ness of the health properties of pulses, the sector is pro-jected to see stable demand and consumption trends in the long term. The FAO ( Alexandratos and Bruinsma, 2012, p. 47 ) further anticipates that ‘for the future, no major chang-es are foreseen in per capita consumption of pulses, with the average of the developing countries remaining at 7-8 kg’.

shift in consumption patterns

Significant changes have been observed in global con-sumption, and therefore production, of pulses over the past decade. Dry beans, which include Phaseolus species ( kid-ney beans, lima beans and tepary beans ) and Vigna spe-cies ( adzuki beans, mung beans and black gram ) used to be the largest category of pulses grown globally until 2004, contributing about 31 % of total pulse production. The share of dry beans has gone down significantly and now repre-sents 17 % of global pulse production. This variety has pro-gressively been replaced by dry peas as the leading variety over the past decade, going up from 20 % to 24 % of global production. One major reason that can be identified is the significant reduction of production of black beans in China. Chickpeas, representing 16 % of global production, stand as the third-largest grown variety, followed by cowpeas ( 9 % ) and broad beans ( 9 % ) ( see figure 4 ).

laRgeR numBeR of expoRteRs dominated By a small numBeR of leading supplieRs

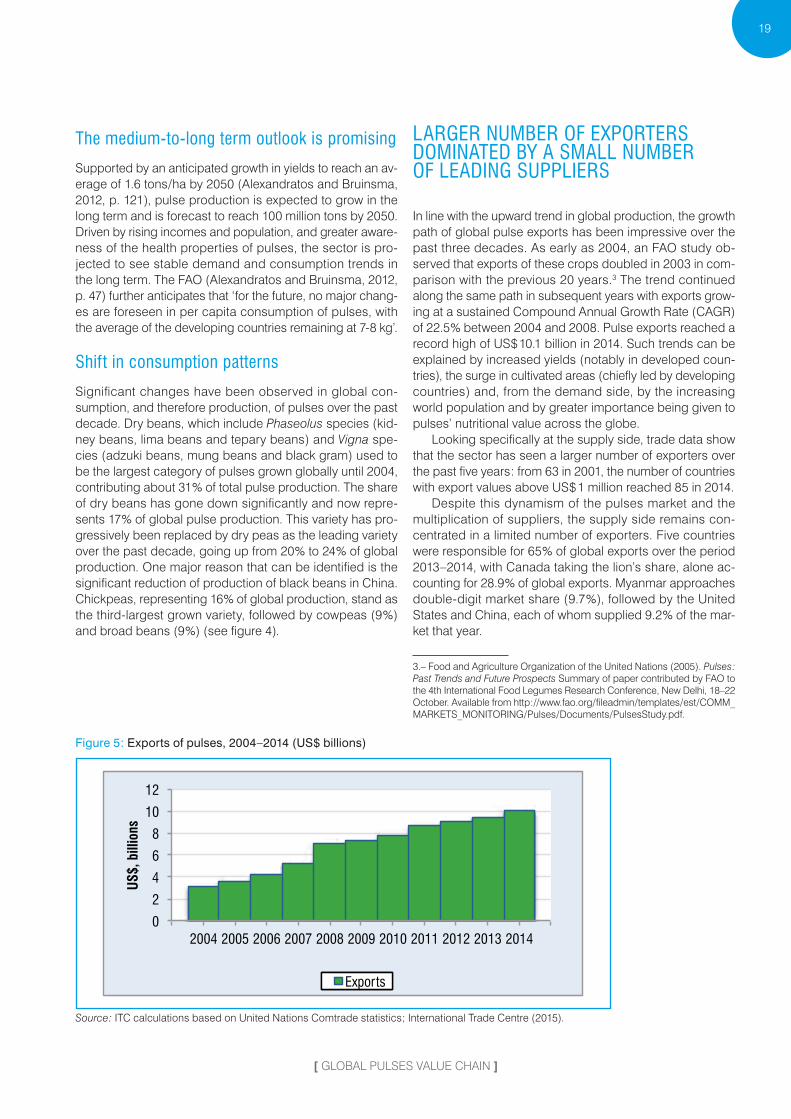

In line with the upward trend in global production, the growth path of global pulse exports has been impressive over the past three decades. As early as 2004, an FAO study ob-served that exports of these crops doubled in 2003 in com-parison with the previous 20 years.3 The trend continued along the same path in subsequent years with exports grow-ing at a sustained Compound Annual Growth Rate ( CAGR ) of 22.5 % between 2004 and 2008. Pulse exports reached a record high of US $ 10.1 billion in 2014. Such trends can be explained by increased yields ( notably in developed coun-tries ), the surge in cultivated areas ( chiefly led by developing countries ) and, from the demand side, by the increasing world population and by greater importance being given to pulses’ nutritional value across the globe.

Looking specifically at the supply side, trade data show that the sector has seen a larger number of exporters over the past five years : from 63 in 2001, the number of countries with export values above US $ 1 million reached 85 in 2014.

Despite this dynamism of the pulses market and the multiplication of suppliers, the supply side remains con-centrated in a limited number of exporters. Five countries were responsible for 65 % of global exports over the period 2013–2014, with Canada taking the lion’s share, alone ac-counting for 28.9 % of global exports. Myanmar approaches double-digit market share ( 9.7 % ), followed by the United States and China, each of whom supplied 9.2 % of the mar-ket that year.

3.– Food and Agriculture Organization of the United Nations ( 2005 ). Pulses : Past Trends and Future Prospects Summary of paper contributed by FAO to the 4th International Food Legumes Research Conference, New Delhi, 18–22 October. Available from http : // www.fao.org / fileadmin / templates / est / COMM_MARKETS_MONITORING / Pulses / Documents / PulsesStudy.pdf.

Figure 5 : Exports of pulses, 2004–2014 ( US $ billions )

0

2

4

6

8

10

12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

US$,

bill

ions

Exports

Source : ITC calculations based on United Nations Comtrade statistics ; International Trade Centre ( 2015 ).

20

[ KENYA Value Chain Roadmap foR pulSeS ]

Table 1 : Top 10 exporters of pulses ( Harmonized System ( HS ) 0713 ), 2014

HS 0713 – Dried vegetables, shelled

ExportersExports

2013–2014( US $ millions )

CAGR Share in world exports

CAGR2010–2014 ( % )

Average2011–2012 ( % )

Average2013–2014 ( % )

World 9 776 6.8 100 100

1 Canada 2 789 8.7 23.4 28.6

2 Myanmar 943 4.2 9.4 9.7

3 United States 894 5.8 8.4 9.2

4 China 892 -1.8 11.1 9.2

5 Australia 796 8.9 10.9 8.2

6 India 283 1.9 2.4 3.0

7 Argentina 274 4.0 5.2 2.8

8 Ethiopia 263 20.4 1.9 2.7

9 Turkey 227 -3.1 2.6 2.3

10 Egypt 220 33.0 1.2 2.2

15 United Republic of Tanzania 132 17.8 1.0 1.4

23 Kenya 50 6.8 0.2 0.5

Source : International Trade Centre ( ITC ) calculations based on United Nations Comtrade statistics ; International Trade Centre ( 2015 ).

Figure 6 : Exports of pulses by region or regional group, 2004–2014 ( US $ billions )

0

2

4

6

8

10

12

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

2014

US$,

bill

ions

America Asia Europe Africa Oceania

Source : International Trade Centre ( 2015 ).

pulses of african origin are gaining market share

The African continent produces several varieties of puls-es that are in high demand in consuming countries, chief among which is India. Pulses like mung beans, chickpeas ( yellow gram variety ), pigeon peas and kidney beans are already being exported to India from Africa, with

major exporters including Ethiopia, the United Republic of Tanzania, Malawi, Kenya, Mozambique, Madagascar, Uganda and, more recently, Sudan. African origin pulses were first introduced by the State Trading Corporation of India. Subsequently, some private players have entered the market and are exporting to the South Asia region. Further, Indian buyers and processors are increasingly looking at

[ GLOBAL PULSES VALUE CHAIN ]

21

African origin due to logistical convenience, availability of raw materials for processing and low processing costs. Indian importers have also been trying to look for alterna-tive origins to diversify the import from Myanmar.

Pulses of African origin are gaining market share. Among the top 20 exporters of pulses, Ethiopia and the United Republic of Tanzania achieved significant growth rates in exports between 2010 and 2014, with a CAGR of exports in value of 20.4 % and 17.8 %, respectively. With US $ 50 mil-lion worth of pulses exported over the period 2013–2014, Kenya’s share in world exports is roughly 0.5 %, a significant progression compared with the 0.2 % share the country re-ported for the period 2011–2012.

The major African origin pulse category imported in South Asia is Tanzanian pigeon peas, imported to the level of 22 % of the total imports of pigeon peas in India. In addi-tion to pigeon peas, the United Republic of Tanzania also exports chickpeas to India. To a lesser extent, Mozambique, Malawi and Sudan are also supplying the Indian market with this variety of pulse. Mung beans of African origin are also being exported to India from the United Republic of

Tanzania, Kenya and Mozambique. Finally, Ethiopia appears to be a major supplier of kidney beans to the Indian market. These imports are expected to continue growing in the long term given shortfalls in domestic production.

dRy peas, kidney Beans and lentils dominate the tRade of pulsesWhile all varieties experienced strong growth over the past five years, the expansion of dry peas and kidney beans & white pea beans exports is especially notable, with a CAGR of 10 % over the period 2010–2014. Canada is by far the top exporter of dry peas and lentils, whereas Myanmar and Australia are the most important exporters of urd, mung, black / green gram beans and chickpeas, respectively. China still largely dominates exports of kidney beans & white pea beans but its market share is declining.

Table 2 provides information on pulse varieties whose international supply, on average for 2013–2014, was above US $ 1 billion.

Table 2 : Pulse varieties with international supply >US $ 1 billion, 2014

Dry peas ( HS 071310 ) Kidney beans & white pea beans ( HS 071333 ) Lentils ( HS 071340 )

Exporter

Average 2013-2014

( US $ millions )CAGR

2010–2014 Exporter

Average 2013-2014

( US $ millions )CAGR

2010–2014 Exporter

Average 2013-2014

( US $ millions )CAGR

2010–2014

World 2 134 10 % World 1 991 10 % World 1 907 3 %

Leading and growing Leading and growing Leading and growing

Canada 1 194 12 % Argentina 195 2 % Canada 1 220 7 %

United States 265 9 % United States 181 20 % Australia 197 16 %

Russian Federation 103 29 % Ethiopia 166 42 %

United States 147 1 %

Australia 73 3 % Egypt 164 51 % Sri Lanka 15 8 %

Ukraine 46 7 % Canada 146 4 % Egypt 12 16 %

Leading but declining Leading but declining

China 577 -5 % Turkey 181 -3 %

UAE 34 -17 %

Urd, mung, black / green gram beans ( HS 071331 ) Chickpeas ( HS 071320 )

ExporterAverage 2013-2014

( US $ millions )CAGR

2010–2014 ExporterAverage 2013-2014

( US $ millions )CAGR

2010–2014

World 1 006 0 % World 1 093 6 %

Leading and growing Leading and growing

China 196 6 % Australia 298 8 %

Indonesia 26 28 % Mexico 157 16 %

Egypt 20 27 % Russian Federation 88 103 %

United States 9 6 % United States 48 3 %

Malawi 8 134 % Argentina 38 20 %

Leading but declining Leading but declining

Myanmar 588 -3 % India 264 -1 %

Australia 48 -22 % Canada 44 -10 %

Ethiopia 34 -3 %

22

[ KENYA Value Chain Roadmap foR pulSeS ]

Table 3 : World-leading importers of pulses ( HS 0713 )

0713 – Dried vegetables, shelled

ImportersImports

2013–2014( US $ millions )

CAGR Share in world imports

CAGR2010–2014 ( % )

Average2011–2012 ( % )

Average2013–2014 ( % )

World 10 255 6.6 100 100

1 India 2 488 9.5 22.0 24.2

2 China 554 11.8 5.2 5.5

3 Egypt 437 8.4 4.6 4.3

4 Bangladesh 403 3.5 2.9 3.9

5 United States 400 14.0 4.5 3.9

6 Turkey 323 10.5 2.7 3.2

7 Pakistan 320 -0.5 4.3 3.2

8 Italy 314 10.6 2.8 3.1

9 Spain 271 3.0 3.0 2.7

10 Algeria 270 2.4 2.7 2.7

Source : ITC calculations based on United Nations Comtrade statistics ; International Trade Centre ( 2015 ).

switCh of impoRt maRkets fRom the west to the eastThe dynamic of pulse imports has dramatically changed over the past 10 years. The major importers of this com-modity are now concentrated in South Asia, China, Europe and the MENA region. Europe, once the major importer of pulses, has reported a significant decline in its imports over the years, while China, Central Asian countries, and most importantly India, are gaining importance in world mar-kets. The South Asia region, which includes India, Pakistan, Bangladesh, Sri Lanka, Nepal and Bhutan, accounts for the largest consumption and is the fastest-growing pulse-consuming region, with an increase in imports of than more than 250 % growth in the past 10 years.

The market for pulses appears to be a vibrant one, with an annual growth of imports of 6.6 % between 2010 and 2014, driven by booming Indian demand that reported an impressive CAGR for imports of 9.5 % over the period. In 2014, the global market for the commodity was valued at ap-proximately US $ 10.3 billion of imports, India alone capturing nearly a quarter of world imports. Other important markets, but far behind India, include China, Egypt, Bangladesh and the United States, each accounting for approximately 4 % to 5 %. With double-digit CAGRs for imports of pulses be-tween 2010 and 2014, it is to be noted that China, the United States, Turkey and Italy have experienced strong expansions as target markets.

despite being the world’s largest producer of pulses, india has emerged as the largest importer of pulses in the worldIndian imports increased dramatically over the past decade, from US $ 446 million in value in 2004 to US $ 2,685 million in 2014. Domestic production of pulses has proven insufficient to supply booming demand fuelled by an increasing popu-lation, sustained economic growth and rapid urbanization. The situation has forced the country to import increasing quantities of pulses from the rest of world to bridge this wid-ening gap ( see table 4 ). India imported more than 4 million tons of pulses in 2014, including chickpeas, pigeon peas, mung beans, lentils and dry peas, with major imports com-ing from Canada ( accounting for 37.4 % of India’s imports of pulses in 2014 ), Myanmar ( 29.8 % ), Australia ( 7.1 % ) and the United States ( 6.3 % ) ( ITC Trade Map Database, 2015 ).

India’s high import dependency led the Government of India to ban the export of pulses ( except kabuli chana ( chick-peas ) ), including processed pulses, in 2006. This has led to some structural changes, and processing plants are being relocated to places such as Dubai and Singapore, mostly to ensure supply to the large South Asian diaspora that had been importing processed dhal from India. Indian au-thorities have also permitted duty-free import of pulses into the country, contributing to the sharp increase in imports.

With a growing population expected to reach 1.7 billion by 2030 – from the current 1.2 billion – the Indian pulse re-quirement for the year 2030 is estimated at 32 million tons, implying that India would have to increase its production by an unlikely 80 % in order to meet domestic demand. Indian import dependency for pulses is consequently expected to rise significantly, offering a long-term opportunity for inter-national suppliers.

[ GLOBAL PULSES VALUE CHAIN ]

23

Table 4 : Pulse production, trade and consumption of India, 2013–2014 to January 2015 ( tons )

2013–2014 2014–2015 January 2015

Production 19.78 18.4 18.43

Import 3.04 3.41 4.1

Total availability 22.82 21.81 22.53

Export 0.34 0.23 0.19

Domestic availability 22.48 21.58 22.34

Source : Indian Directorate of Economics and Statistics.

significant contraction of european demand

Once the most important market for pulses with about 45 % of the world’s pulse imports handled in 2004, Europe has now slipped to second position, standing at approximately 22 % of total imports with an average import of about 2.2 million tons every year ( FAO ).

Several factors can explain this fall in imports, includ-ing an inadequate level of product innovation adapted to modern life, a small home supply of pulses and competition from cheaper low-quality imports. An important factor when it comes to the European market for pulses is that pulses are consumed in many different ways in the various European Union ( EU ) countries, due to different regional food habits and traditions, and to differences in the supplies of grain legumes. Although dry beans are the most consumed pulse in the EU, it is important to keep in mind that preferences between varieties vary from one country to another.

A significant amount of pulse imports were for animal feed because the production of meat and dairy products in most EU countries is to a large degree dependent on pro-tein feed imports. However, a shift from pulses to soybeans, mainly imported from Latin America, has been observed during the past several years.

Despite the recent loss of market share, pulse demand could rebound in Europe with recent increases in preferenc-es for vegan and gluten-free diets, offering exciting export opportunities. As discussed above, pulses have significant nutritional and health advantages for consumers and their cultivation has a positive impact on agriculture and the en-vironment. If Europe is a slow market, trends in consump-tion of pulses could change, especially if awareness-raising campaigns about the benefits of pulses are improved and if the food industry and professional organizations take up the challenge to incorporate grain legumes in novel, convenient and healthy food products.

pulses are seeing an increase in demand from the non-traditional processed food sector, namely with an increasing drive towards gluten-free diets

The pulses industry is estimated to be worth over US $ 100 billion at the retail level. With greater awareness of coeliac disease and gluten sensitivity, the demand for gluten-free products is on the rise, resulting in a significant change in dietary patterns in the past few years. Benefiting from these developments, pulses such as yellow peas, lentils and chickpeas are gaining recognition as the ‘new and im-proved’ heart of healthy foods and new processed products made from lentils and chickpeas – such as pasta, noodles and chips – have been developed.

Change in consumption patterns in China

With a growing population of 1.35 billion, China has recently shown an impressive rise in demand for pulses to become the second major importer in Asia and the third-largest mar-ket in the world.

China reported a CAGR of imports of 11.8 % between 2010 and 2014, its share in world imports rising from less than 1 % ( average for the years 2003–2004 ) to 5.5 % ( aver-age for 2013–2014 ) over the past decade. Once a net ex-porter of cheap, low quality pulses such as black beans, China, with its economic resurgence and growing middle class, is now importing some of those very same commodi-ties, the result of shifting demands and a rapidly changing society. Increasing production costs in local agriculture have led to a loss of competitiveness of the pulses sector, result-ing in a contraction of production and exports. The 2013 flooding that partially destroyed crops has also contributed to the drop in black bean exports from China.

The country is importing significant quantities of dry peas, consumed in various forms including starch, vermicelli and snack food. The increasing influence of Western culture and food habits in China has contributed to this change in consumption patterns with a new demand for processed pulses that were not traditionally consumed. Recent invest-ments in processing factories confirm this trend, resulting in

24

[ KENYA Value Chain Roadmap foR pulSeS ]

a sharp increase in imports of dry peas by China in recent years. Although the carry-over stock kept imports to a level of 700,000–800,000 tons in 2014, imports are expected to rebound to an average of 1 million tons every year.

the mena region is a traditional importer of pulses, which feature prominently in regional cuisine

The MENA region has high population growth rates and many countries are seeing sustainable growth in food ser-vice and retail sales. Consumers in the MENA region are increasingly using supermarkets for food purchases, which has in turn led to an increase in demand for processed puls-es such as canned pulses and pulse flours. The extraordi-nary growth in the hospitality industry in countries such as Morocco, Egypt and Israel, and the city of Dubai ( UAE ), cou-pled with the introduction of new cuisines, is also pushing

demand for pulses such as chickpeas, lentils, peas and beans to new levels. Demand for pulses is on the rise among both traditional consumers and new markets in this region.

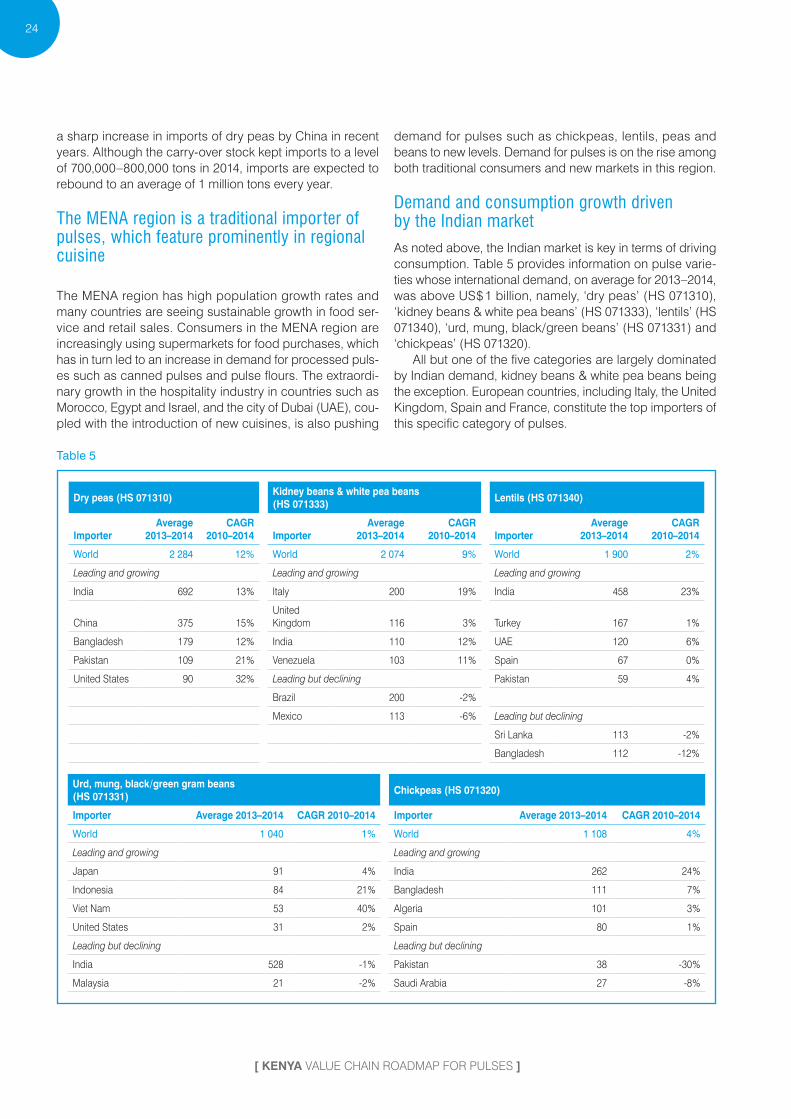

demand and consumption growth driven by the indian marketAs noted above, the Indian market is key in terms of driving consumption. Table 5 provides information on pulse varie-ties whose international demand, on average for 2013–2014, was above US $ 1 billion, namely, ‘dry peas’ ( HS 071310 ), ‘kidney beans & white pea beans’ ( HS 071333 ), ‘lentils’ ( HS 071340 ), ‘urd, mung, black / green beans’ ( HS 071331 ) and ‘chickpeas’ ( HS 071320 ).

All but one of the five categories are largely dominated by Indian demand, kidney beans & white pea beans being the exception. European countries, including Italy, the United Kingdom, Spain and France, constitute the top importers of this specific category of pulses.

Table 5

Dry peas ( HS 071310 )Kidney beans & white pea beans( HS 071333 )

Lentils ( HS 071340 )

ImporterAverage

2013–2014CAGR

2010–2014 ImporterAverage

2013–2014CAGR

2010–2014 ImporterAverage

2013–2014CAGR

2010–2014

World 2 284 12 % World 2 074 9 % World 1 900 2 %

Leading and growing Leading and growing Leading and growing

India 692 13 % Italy 200 19 % India 458 23 %

China 375 15 %United Kingdom 116 3 % Turkey 167 1 %

Bangladesh 179 12 % India 110 12 % UAE 120 6 %

Pakistan 109 21 % Venezuela 103 11 % Spain 67 0 %

United States 90 32 % Leading but declining Pakistan 59 4 %

Brazil 200 -2 %

Mexico 113 -6 % Leading but declining

Sri Lanka 113 -2 %

Bangladesh 112 -12 %

Urd, mung, black / green gram beans( HS 071331 )

Chickpeas ( HS 071320 )

Importer Average 2013–2014 CAGR 2010–2014 Importer Average 2013–2014 CAGR 2010–2014

World 1 040 1 % World 1 108 4 %

Leading and growing Leading and growing

Japan 91 4 % India 262 24 %

Indonesia 84 21 % Bangladesh 111 7 %

Viet Nam 53 40 % Algeria 101 3 %

United States 31 2 % Spain 80 1 %

Leading but declining Leading but declining

India 528 -1 % Pakistan 38 -30 %

Malaysia 21 -2 % Saudi Arabia 27 -8 %

Photo: (CC BY-SA 2.0) CC0 Public Domain, beans-228870.Apg

[ GLOBAL PULSES VALUE CHAIN ]

25

stRong indian demand keeps pRiCes RemuneRatiVeThe increasing international demand for pulses has driven up the price of the commodity. Average prices have been rising, suggesting a shortfall of supply. India being the larg-est importer of pulses, the Indian market situation and crop positions significantly affect global prices. Importantly, con-sumption patterns in India indicate a strong preference for

low-cost varieties and the use of substitutions as prices go up ( e.g. if the price of chickpeas goes up, the import shifts to yellow peas ). Further, the major demand for pulses is gen-erated from countries that have higher population growth rates. Countries like India, with its high population growth rate and rising per capita income, is keeping the prices of pulses up. If the average price of imports by India is gener-ally lower than the global average, Indian demand neverthe-less plays a major role in keeping prices remunerative.

box 1 : global trends

• World demand for pulses is reaching an all-time high, exacer-bated by nutritional demand for a substitute protein across the world as people shift from traditional sources like meat due to dietary needs and preferences.

– Production of pulses has seen unprecedented growth over the past decade.

– Global production of pulses reached 73.2 million tons in 2013.

– Although the area cultivated has significantly increased, pro-ductivity remains low, especially in developing countries.

– South Asia is the biggest pulse producing region in the world, accounting altogether for 25 % of world pulse production.

– Pulses of African origin have gained significant importance in recent years, currently accounting for roughly 20 % of global production.

– Dry peas constitute 24 % of the world’s pulse production, followed by dry beans ( 17 % ), chickpeas ( 16 % ), dry broad beans and cowpeas ( 9 % each ), lentils and pigeon peas ( 6 % each ), and others.

• Pulse exports are dominated by a small number of leading suppliers.

– The major exporter of pulses in 2011 was Canada ( 28.9 % share of world exports ), followed by Myanmar ( 9.7 % ), China and the United States ( with approximately 9.2 % share of world exports each ).

– The total value of Canada’s pulse exports in 2014 amounted to about US $ 2.8 billion.

– Pulses of African origin are gaining market share.• Switch of import markets from the West to the East.

– International demand and consumption growth are now driven by the Indian market, which in turn keeps pulse prices remunerative.

– Pulses of African origin are gaining market share. – Significant contraction of European demand, once the lead

importer. – Other key markets include China and the MENA region. – Dry peas, kidney beans and lentils dominate the trade in

pulses.

Photo: Kiyo (CC BY-NC 2.0), Kidney Beans.Apg

an eVolVing Value Chain in need of suppoRt 4

box 2 : the sector’s socioeconomic importance to kenya

Endowed with over 569,000 square kilometres of land, Kenya boasts a wide range of ecological regions and plant life. The country straddles the equator, it enjoys areas of both temperate and tropical climate, and its 475 endemic plant species include a variety of pulses.*

Production of pulses began to increase following Kenya’s independ-ence. From 1960 to 1982, output more than doubled to 568,000 tons per year, due in large part to the growth of dry bean production.** Continuing to grow through 1993, production fell off in the mid-1990s. Nevertheless, growth has picked up again in recent years.

Today, pulses are an important food source for the Kenyan population due to their nutritional value, high protein content and relatively low cost when compared with meat.*** Pulses are gaining in popularity among farmers due to their hardiness and resistance to drought, which makes them ideal for Kenya, where rainfall is sporadic because it is governed by the erratic movement of the intertropical convergence zone.**** Further complicating the matter, weather has been particu-larly unpredictable in recent years due to climate change. This has led many farmers to abandon wheat production in favour of pulses, which mature quickly and can thrive with limited rainfall.*****

Figure 8 : Kenyan production of pulses, 1961–2013

275 370

450

700

482

758

0

200

400

600

800

1.000

1961 1971 1981 1991 2001 2013

Tons

, tho

usan

ds

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

* Wambugu P.W. and Muthamia Z.K. (2009). Country Report on the State of Plant Genetic Resources for Food and Agriculture: Kenya, p. 19. Kenya Agricultural Research Institute; National Genebank of Kenya.

** Food and Agriculture Organization of the United Nations (2015). Statistics database. Available from http://faostat3.fao.org/download/T/*/E. Accessed 5 August 2015.

*** Katungi, E., Farrow. A., Chianu. J., Sperling. L., and Beebe. S. (2009). Common Bean in Eastern and Southern Africa: A Situation and Outlook Analysis. International Centre for Tropical Agriculture.

**** Pereira, Charles (1996). The role of agricultural research in the development of Kenya before independence. In Review of Kenyan Agricultural Research, Vol. 1, p. 9.

***** Njagi, Kagondu (2013). As wheat yields fall in Kenya, farmers turn to beans. Thomson Reuters Foundation, 25 April.

4.– Information source for the value chain – consultations and desk research, prominently using the following source : Dalipagic, Ian and Elepu, Dr. Gabriel ( 2014 ). Agricultural Value Chain Analysis in Northern Uganda : Maize, Rice, Groundnuts, Sunflower and Sesame. Action Against Hunger / ACF International.

28

[ KENYA Value Chain Roadmap foR pulSeS ]

A wide array of actors works together throughout the sector in order to produce and sell pulses on both domestic and international markets. Vertical business linkages tend to be undeveloped and informal.5 Trade is based on temporary relationships and most actors do not use contracts.

ReseaRCh and deVelopment

The pulses sector had historically received little attention from research and support institutions, which tended to focus more on crops such as maize. In recent years, in-stitutions including the Kenya Agricultural and Livestock Research Organization ( KALRO ), local universities, non-governmental organizations and other local research or-ganizations have begun to engage more with the sector, producing higher-yield crop varieties that cater to local conditions. Regional institutions such as the Association for Strengthening Agricultural Research in Eastern and Central Africa and its Eastern and Central Africa Bean Research Network have also played a role.

In the bean subsector, a number of disease- and pest-resistant varieties have been developed. KALRO, the International Crops Research Institute for the Semi-Arid Tropics ( ICRISAT ), the University of Nairobi and Winrock International meanwhile have developed a number of high-yielding varieties of pigeon pea that are adapted to local conditions and resistant to diseases. ICRISAT in particular has been actively promoting the use of enhanced pigeon pea varieties in Eastern province.

inputs

The value chain’s main inputs are labour and seeds, which are mainly domestic. Most farms use their own beans for seed or buy from local markets ; improved varieties are generally only used where there is Government or donor intervention. It is estimated that 75 % of cowpea seeds and 95 % of pigeon pea seeds come from farm retention or neighbouring households. Certified and improved seeds, where used, may come from local businesses supplied by the Kenya Seed Company Ltd ( cowpeas ) and ICRISAT ( pi-geon peas ), the latter of which contracts local farmers to generate the certified seeds.

Supplying certified pulse seeds is perceived as quite risky, as self-pollinated seeds can easily be retained and used to achieve similar yields.6 This limits greater devel-opment of the supply chain, which is further complicated by farmers’ reluctance to pay the high cost of certified seeds.7 Additionally, there is only a limited commercial mar-ket for minor crop seeds, making it difficult for suppliers

5.– Ibid. : p. 124.6.– Ibid, : p. 118.7.– Ibid, : p, 153.

to achieve economies of scale. Where there is a shortage of seed due to a poor harvest, supplies are either bought from neighbouring regions at markets or supplied by the Government or donors.8 Other inputs such as fertilizers, in-secticides and pesticides are only used by a small propor-tion of the sector’s farmers. Some farmers do use manure.

pRoduCtion

The next step in the value chain is production, which is undertaken on smallholder farms and characterized by ploughing, planting and weeding.9 Planting and harvesting are accomplished by manual labour, while oxen ploughs and hoes are often used in ploughing and weeding. Beans are grown during both the short and long rains periods ( September / December and February / June respectively ).10 Pigeon pea is planted at the beginning of the short rains.11 The short- and medium-duration varieties are harvested as fresh vegetable from February to April, while the long dura-tion variety is usually harvested as dry grain between August and September.

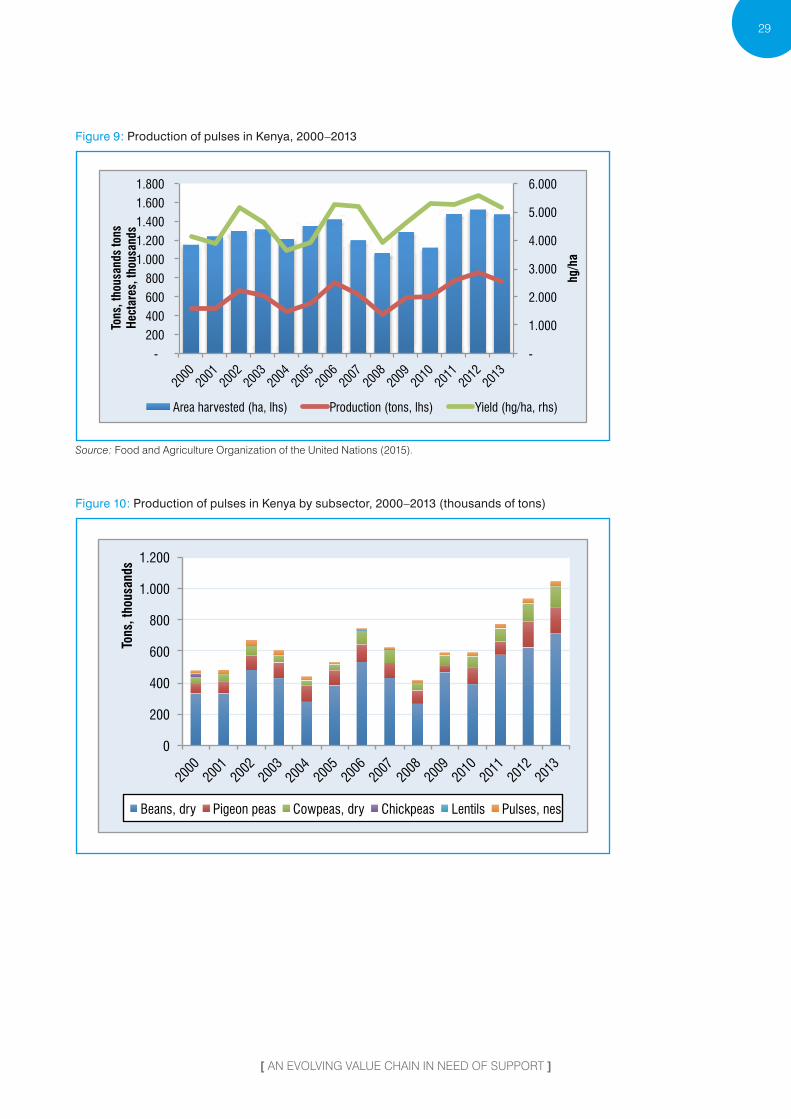

Kenyan farmers currently cultivate pulses on 1.47 million ha of land. All three metrics – area harvested, production volume, and yield – have grown between 2000 and 2013, despite periods of fluctuation.

According to the FAO, Kenya is the seventeenth top producer of pulses worldwide – and number four in Africa after Nigeria, the United Republic of Tanzania and Ethiopia – involving roughly 1.8 million households in the production of pulses in general. Kenyan farms produced more than 1 million tons of pulses in 2013, including dry beans ( 715,000 tons ), pigeon peas ( 166,000 tons ), and cowpeas ( 134,000 tons ). As illustrated in figure 10, production growth since the turn of the century ( 6.2 % CAGR from 2000 to 2013 ) has been driven largely by increased cultivation of dry beans, pigeon peas and cowpeas, which have grown by a CAGR of 6.1 %, 7.4 % and 10.1 % respectively over the past decade. The production of lentils, while small, has grown by 8.0 % per annum.

8.– Ibid. : p, 118.9.– Ibid. : p. 134.10.– Ibid. : p. 119.11.– Ibid. : p. 134.

[ AN EVOLVING VALUE CHAIN IN NEED OF SUPPORT ]

29

Figure 9 : Production of pulses in Kenya, 2000–2013

-

1.000

2.000

3.000

4.000

5.000

6.000

- 200 400 600 800

1.000 1.200 1.400 1.600 1.800

2000

20

01 20

02 20

03 20

04

2005

20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

hg/h

a

Tons

, tho

usan

ds to

ns

Hect

ares

, tho

usan

ds

Area harvested (ha, lhs) Production (tons, lhs) Yield (hg/ha, rhs)

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

Figure 10 : Production of pulses in Kenya by subsector, 2000–2013 ( thousands of tons )

0

200

400

600

800

1.000

1.200

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

Tons

, tho

usan

ds

Beans, dry Pigeon peas Cowpeas, dry Chickpeas Lentils Pulses, nes

30

[ KENYA Value Chain Roadmap foR pulSeS ]

0

200

400

600

800

1.000

2000

20

01

2002

20

03

2004

20

05

2006

20

07

2008

20

09

2010

20

11

2012

20

13

Tons

, tho

usan

ds

Beans, dry Chick peas Cow peas, dry Pigeon peas Lentils Pulses, nes

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

Figure 11 : Kenyan production of dry beans, 2000–2013

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

-

200

400

600

800

1.000

1.200

2000

20

01 20

02 20

03 20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

Hg/h

a

Tons

, tho

usan

ds

hect

ares

, tho

usan

ds

Area harvested (ha, lhs) Production (tons, lhs) Yield (hg/ha, rhs)

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

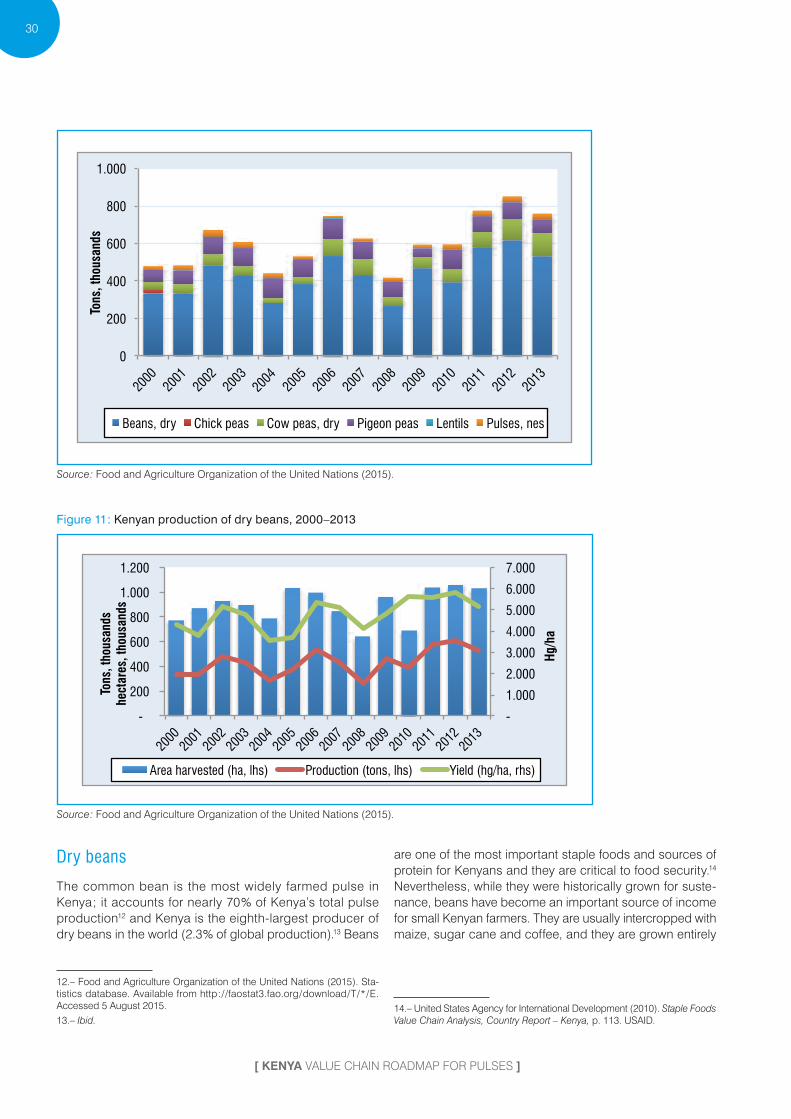

dry beans

The common bean is the most widely farmed pulse in Kenya ; it accounts for nearly 70 % of Kenya’s total pulse production12 and Kenya is the eighth-largest producer of dry beans in the world ( 2.3 % of global production ).13 Beans

12.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Accessed 5 August 2015.13.– Ibid.

are one of the most important staple foods and sources of protein for Kenyans and they are critical to food security.14 Nevertheless, while they were historically grown for suste-nance, beans have become an important source of income for small Kenyan farmers. They are usually intercropped with maize, sugar cane and coffee, and they are grown entirely

14.– United States Agency for International Development ( 2010 ). Staple Foods Value Chain Analysis, Country Report – Kenya, p. 113. USAID.

[ AN EVOLVING VALUE CHAIN IN NEED OF SUPPORT ]

31

by smallholder farmers.15 Roughly 1.5 million households are engaged in bean cultivation.

Farmers cultivated dry beans on over 1 million ha in 2013, up from 770,000 in 2000.16 Dry beans are produced mainly in the Rift Valley ( 33 % ), Eastern province ( 24 % ), Nyanza ( 185 ), Western province ( 12 % ) and Central province ( 12 % ).17 While production has been unsteady due to reliance on the variable rainfall, consumption has been growing in double digits since the turn of the century. As such, Kenya often imports beans in order to fill the deficit and meet do-mestic demand. It should also be noted that while yields have improved by 20 % since 2000, they are still well below the levels achieved throughout the rest of the world ( 2013 : 7,850 hectograms ( hg ) / ha ).18

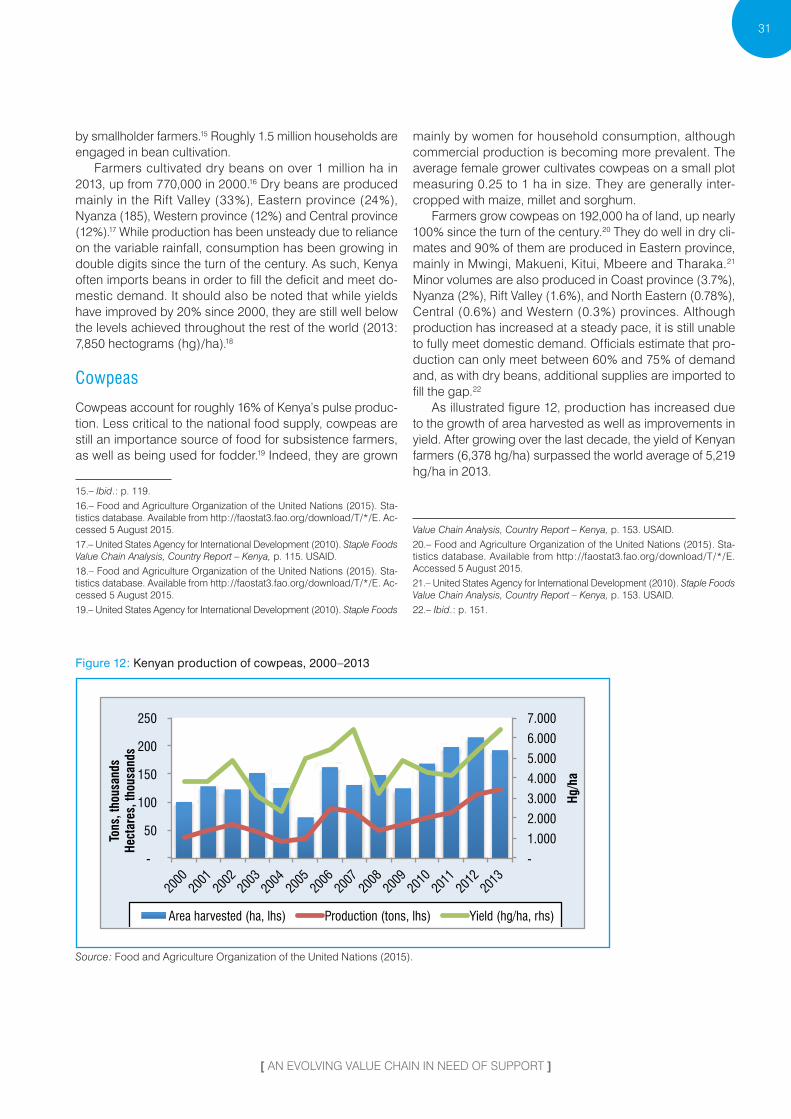

Cowpeas

Cowpeas account for roughly 16 % of Kenya’s pulse produc-tion. Less critical to the national food supply, cowpeas are still an importance source of food for subsistence farmers, as well as being used for fodder.19 Indeed, they are grown

15.– Ibid. : p. 119.16.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Ac-cessed 5 August 2015.17.– United States Agency for International Development ( 2010 ). Staple Foods Value Chain Analysis, Country Report – Kenya, p. 115. USAID.18.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Ac-cessed 5 August 2015.19.– United States Agency for International Development ( 2010 ). Staple Foods

mainly by women for household consumption, although commercial production is becoming more prevalent. The average female grower cultivates cowpeas on a small plot measuring 0.25 to 1 ha in size. They are generally inter-cropped with maize, millet and sorghum.

Farmers grow cowpeas on 192,000 ha of land, up nearly 100 % since the turn of the century.20 They do well in dry cli-mates and 90 % of them are produced in Eastern province, mainly in Mwingi, Makueni, Kitui, Mbeere and Tharaka.21 Minor volumes are also produced in Coast province ( 3.7 % ), Nyanza ( 2 % ), Rift Valley ( 1.6 % ), and North Eastern ( 0.78 % ), Central ( 0.6 % ) and Western ( 0.3 % ) provinces. Although production has increased at a steady pace, it is still unable to fully meet domestic demand. Officials estimate that pro-duction can only meet between 60 % and 75 % of demand and, as with dry beans, additional supplies are imported to fill the gap.22

As illustrated figure 12, production has increased due to the growth of area harvested as well as improvements in yield. After growing over the last decade, the yield of Kenyan farmers ( 6,378 hg / ha ) surpassed the world average of 5,219 hg / ha in 2013.

Value Chain Analysis, Country Report – Kenya, p. 153. USAID.20.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Accessed 5 August 2015.21.– United States Agency for International Development ( 2010 ). Staple Foods Value Chain Analysis, Country Report – Kenya, p. 153. USAID.22.– Ibid. : p. 151.

Figure 12 : Kenyan production of cowpeas, 2000–2013

-

1.000

2.000

3.000

4.000

5.000

6.000

7.000

-

50

100

150

200

250

2000

20

01 20

02 20

03 20

04

2005

20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

Hg/h

a

Tons

, tho

usan

ds

Hect

ares

, tho

usan

ds

Area harvested (ha, lhs) Production (tons, lhs) Yield (hg/ha, rhs)

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

32

[ KENYA Value Chain Roadmap foR pulSeS ]

Figure 13 : Kenyan production of pigeon peas, 2000–2013

- 1.000 2.000 3.000 4.000 5.000 6.000 7.000

-

50

100

150

200

250

2000

20

01 20

02 20

03 20

04 20

05 20

06 20

07 20

08 20

09 20

10 20

11 20

12 20

13

Hg/h

a

Tons

, tho

usan

ds

Hect

ares

, tho

usan

ds

Area harvested (ha, lhs) Production (tons, lhs) Yield (hg/ha, rhs)

Source : Food and Agriculture Organization of the United Nations ( 2015 ).

pigeon peas

Pigeon peas accounted for 9.7 % of total pulse production in 2013.23 The peas are rich in protein and can be eaten fresh or dry ; the leaves and hulls can be used to feed livestock ; and the stems can be used for firewood.24 In addition, pi-geon peas are able to fix atmospheric nitrogen into the soil, especially pertinent given that soils in semi-arid regions tend to be deficient in nitrogen.

Pigeon peas are grown by smallholder farms ranging in size from 0.2 to 1.4 ha for both sustenance and income.25 It has been estimated that they are cultivated by up to 100 % of farming families in certain areas, and roughly two-thirds of these sell a portion of their produce. They are intercropped with both grains and other legumes such as beans, green gram and cowpeas. All varieties of pigeon pea are grown in Kenya, including those of short ( 100–120 days to mature with determinate growth habit ), medium ( 150–200 days with indeterminate growth habit ) and long duration ( more than 200 days with indeterminate growth habit ) maturities.

Pigeon peas are cultivated on 144,000 ha of land.26 This is a decline of 16 % from the area under cultivation in 2000. They are grown in arid and semi-arid climates, and 99 % of Kenyan cultivation occurs in Eastern province,27 with 80 %

23.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Ac-cessed 5 August 2015.24.– United States Agency for International Development ( 2010 ). Staple Foods Value Chain Analysis, Country Report – Kenya, p. 126. USAID.25.– Ibid. : p. 127.26.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Ac-cessed 5 August 2015.27.– United States Agency for International Development ( 2010 ). Staple Foods Value Chain Analysis, Country Report – Kenya, p. 128. USAID.

concentrated in Machakos ( 33 % of national production ), Makueni ( 25 % ) and Kitui ( 22 % ).

Despite a decline in area under cultivation between 2000 and 2013, production has increased by 12 % over the same period due to a 33 % increase in yield.28 Even so, and despite these improvements, yields remain well below the world av-erage of 7,509 hg / ha in 2013.

Chickpeas

At 25 %, chickpeas have the highest protein content of any pulse.29 Nevertheless, they are a relatively less important crop in Kenya, accounting for only 0.01 % of total pulse pro-duction. They are grown in the same areas as cowpeas and pigeon peas ( Eastern province ).30

ColleCtion and distRiBution

Once harvested, the majority of pulse crops are retained for consumption at home or sold to other households or locally at markets. The remainder is sold to both local and regional wholesalers, assemblers, brokers, agents and traders. While similar, each of the three main subsectors is characterized by slightly different distribution mechanisms in which the goods are assembled and sold throughout wholesale and retail channels.

28.– Food and Agriculture Organization of the United Nations ( 2015 ). Sta-tistics database. Available from http : / /faostat3.fao.org / download / T / * / E. Ac-cessed 5 August 2015.29.– United States Agency for International Development ( 2010 ). Staple Foods Value Chain Analysis, Country Report – Kenya, p. 157. USAID.30.– Ibid. : p. 158.

Photo: (CC BY-SA 2.0) CIAT (CC BY-SA 2.0), bean market5.Apg

[ AN EVOLVING VALUE CHAIN IN NEED OF SUPPORT ]

33

dry beans

It is estimated that 60 % of the beans produced are con-sumed by the household and the remaining 40 % are sold.31 While some are sold directly by the producers to wholesal-ers, retailers and households, beans are also consolidated by farm gate agents ( either farmers or local traders ) and regional traders who transport the goods to traders and wholesalers in urban centres. Wholesalers include both in-dividuals and institutions such as the National Cereals and Produce Board, and they tend to be present at multiple lev-els of the value chain. Most wholesalers do not operate full-time, instead engaging in parallel activities or moving away from beans during off-seasons. Wholesalers sell the goods to domestic retailers while also engaging in export. Retailing meanwhile is conducted by local traders in markets and shops. Mixed wholesaling and retailing is quite common.

pigeon peas

Pigeon peas can be sold as fresh vegetables, dry grain or dhal. Roughly 60 % of the crop is used for dry grain while 40 % is used as a vegetable.32 While 62 % of dry grain

31.– Ibid. : p. 12032.– Ibid. : p. 135.

harvests are sold, that percentage falls to only 10 % for vege-table peas. The high level of household consumption is due to pigeon peas’ relative sweetness and cheapness when compared to alternatives, as well as the fact that they are harvested during times of staple food shortage.