University of Economics, Prague Faculty of Finance and ... · University of Economics, Prague...

133

University of Economics, Prague Faculty of Finance and Accounting Department of Banking and Insurance Field of study: Financial Engineering Interest Rate Modelling and Forecasting: Macro-Finance Approach Author of the Master Thesis: Bc. Adam Kuˇ cera Supervisor of the Master Thesis: doc. RNDr. Jiˇ r´ ı Witzany, Ph.D. Year of Defence: 2014

Transcript of University of Economics, Prague Faculty of Finance and ... · University of Economics, Prague...

University of Economics, Prague

Faculty of Finance and Accounting

Department of Banking and InsuranceField of study: Financial Engineering

Interest Rate Modelling and Forecasting:Macro-Finance Approach

Author of the Master Thesis: Bc. Adam Kucera

Supervisor of the Master Thesis: doc. RNDr. Jirı Witzany, Ph.D.

Year of Defence: 2014

Declaration of Authorship

The author hereby declares that the thesis ”Interest Rate Modelling and Fore-

casting: Macro-Finance Approach” was compiled independently by him, using

only the resources and literature properly marked and included in the attached

list of references.

Prague, May 27, 2014

Signature

Acknowledgments

The author is grateful to doc. RNDr. Jirı Witzany, Ph.D. for his comments

and support during writing the thesis. Equal thanks are admitted to all others

inspiring the author during his studies.

Abstract

The thesis compares various approaches to the term structure of interest rates

modelling. Several models are built, following two general frameworks: a dy-

namic Nelson-Siegel approach and an affine class of models. Based on an eval-

uation of dynamic properties of the estimated models, particularly in terms of

impulse-responses and a forecasting performance, effects of an explicit inclusion

of macroeconomic variables into the models are tested. The thesis shows, that

the benefit of such macro-finance extension of the models is varying in time, and

also differs for both approaches. However, it is shown that the models can be

considered as complementary, as the particular approaches are differently use-

ful under various macroeconomic conditions and financial markets situations.

Moreover, unusually long maturities are included into the term structure of

interest rates, and some of the models are shown to be able to forecast these

maturities as well, particularly in certain periods of time.

JEL Classification C38, C51, C58, E43, E47

Keywords Interest Rate, Yield Curve, Macro-Finance

Model, Affine Model, Nelson-Siegel

Author’s e-mail [email protected]

Supervisor’s e-mail [email protected]

Abstrakt

Diplomova prace porovnava ruzne prıstupy k modelovanı casove struktury

urokovych mer. V praci je sledovano nekolik modelu, odvozenych ze dvou

obecnych skupin: dynamicke interpretace Nelson-Siegel parametrizace, a afinnı

trıdy modelu. Na zaklade zhodnocenı dynamickych vlastnostı odhadnutych

modelu, vychazejıcıch zejmena z porovnanı impulse-response funkcı a predpoved-

nıch schopnostı modelu, je nasledne testovan prınos prımeho zahrnutı makroeko-

nomickych promennych do modelu. Prace ukazuje, ze prınos takoveho makro-

financnıho rozsırenı modelu se menı v case, a lisı se take pro obe skupiny

modelu. Nicmene je ukazano, ze modely lze povazovat za vzajemne se doplnujıcı,

jelikoz jednotlive prıstupy jsou odlisne uzitecne v ruznych makroekonomickych

a financnıch podmınkach. Pomocı nekterych modelu lze, zejmena v jistych

casovych obdobıch, zaroven predpovıdat i urokove mıry pro velmi dlouhe splat-

nosti.

Klasifikace JEL C38, C51, C58, E43, E47

Klıcova slova urokova mıra, vynosova krivka, makro-

financnı model, afinnı model, Nelson-Siegel

E-mail autora [email protected]

E-mail vedoucıho prace [email protected]

Contents

List of Tables viii

List of Figures x

Acronyms xii

1 Introduction 1

2 Basic Definitions and Notations 3

2.1 Bond Market, Yield and Interest Rate . . . . . . . . . . . . . . 3

2.2 Term Structure of Interest Rates . . . . . . . . . . . . . . . . . 9

2.3 Term Structure Models . . . . . . . . . . . . . . . . . . . . . . . 13

2.4 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

3 Description of Models 20

3.1 Factors and Principal Component Analysis . . . . . . . . . . . . 20

3.2 Random Walk . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

3.3 Dynamic Nelson-Siegel Approach . . . . . . . . . . . . . . . . . 23

3.4 Affine Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

4 Estimation 39

4.1 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

4.2 Random Walk . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

4.3 Dynamic Nelson-Siegel Approach . . . . . . . . . . . . . . . . . 50

4.4 Affine Models . . . . . . . . . . . . . . . . . . . . . . . . . . . . 60

5 Performance Evaluation 68

5.1 In-Sample Characteristics . . . . . . . . . . . . . . . . . . . . . 68

5.2 Predictive Performance . . . . . . . . . . . . . . . . . . . . . . . 72

5.3 Comparison with Similar Studies . . . . . . . . . . . . . . . . . 79

Contents vii

6 Conclusion 84

Bibliography 89

A Estimated Parameters I

B Predictions XXIX

List of Tables

2.1 Latent-Factors-Only Models . . . . . . . . . . . . . . . . . . . . 17

2.2 Macro-Finance Models . . . . . . . . . . . . . . . . . . . . . . . 18

3.1 Dynamic Nelson-Siegel Models . . . . . . . . . . . . . . . . . . . 30

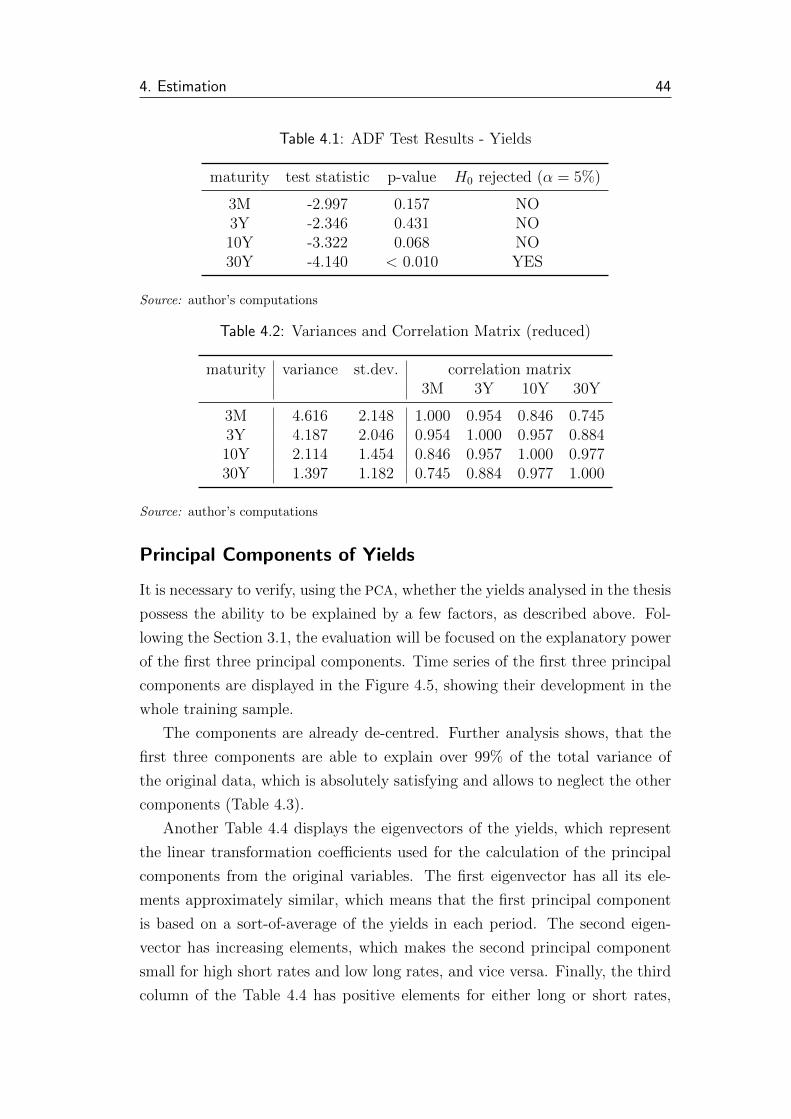

4.1 ADF Test Results - Yields . . . . . . . . . . . . . . . . . . . . . 44

4.2 Variances and Correlation Matrix (reduced) . . . . . . . . . . . 44

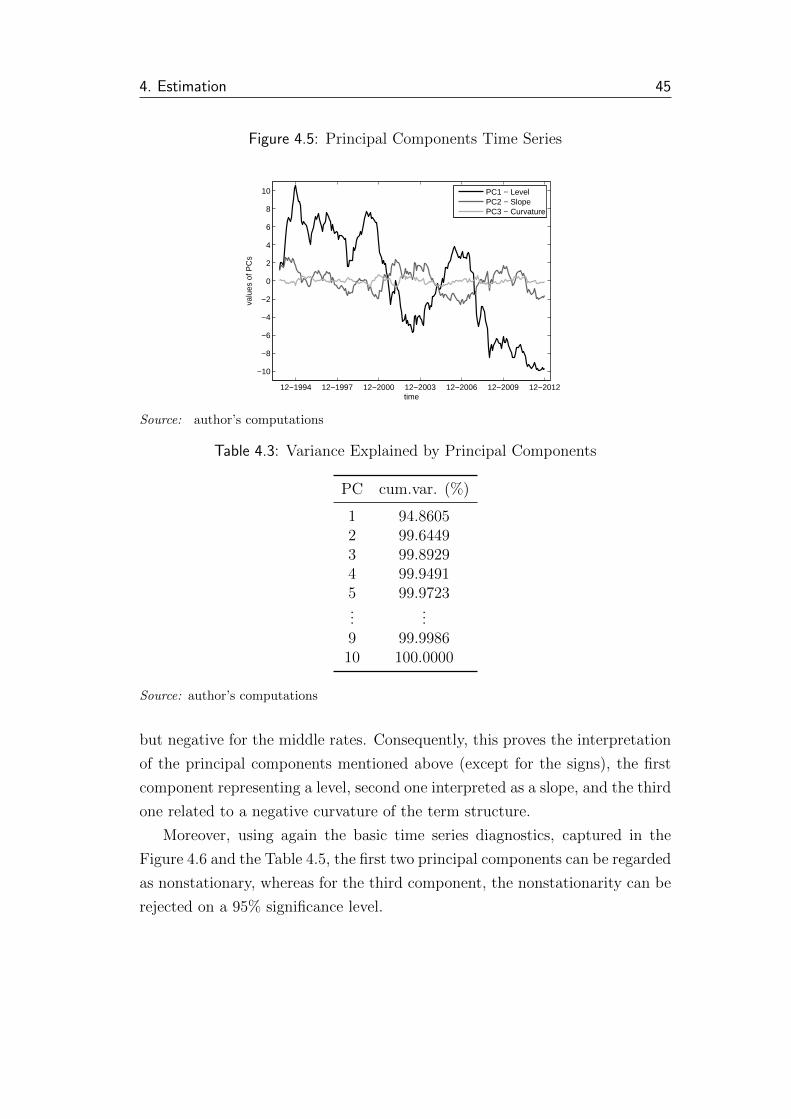

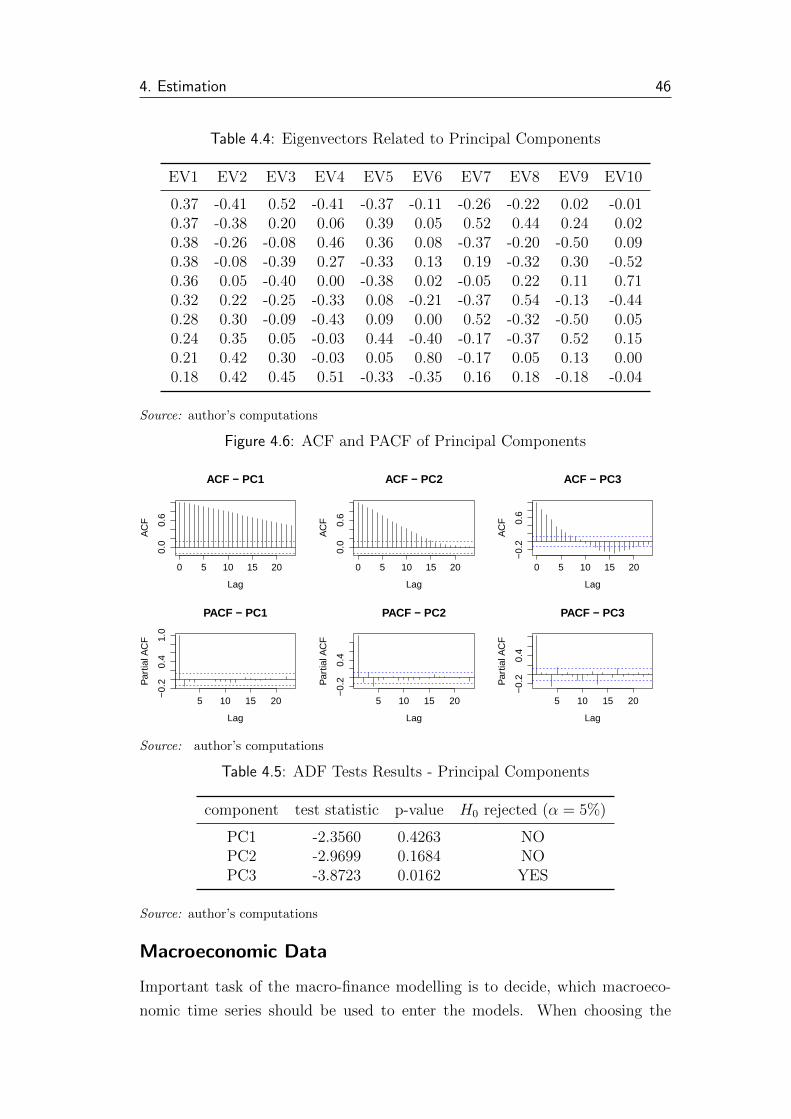

4.3 Variance Explained by Principal Components . . . . . . . . . . 45

4.4 Eigenvectors Related to Principal Components . . . . . . . . . . 46

4.5 ADF Tests Results - Principal Components . . . . . . . . . . . . 46

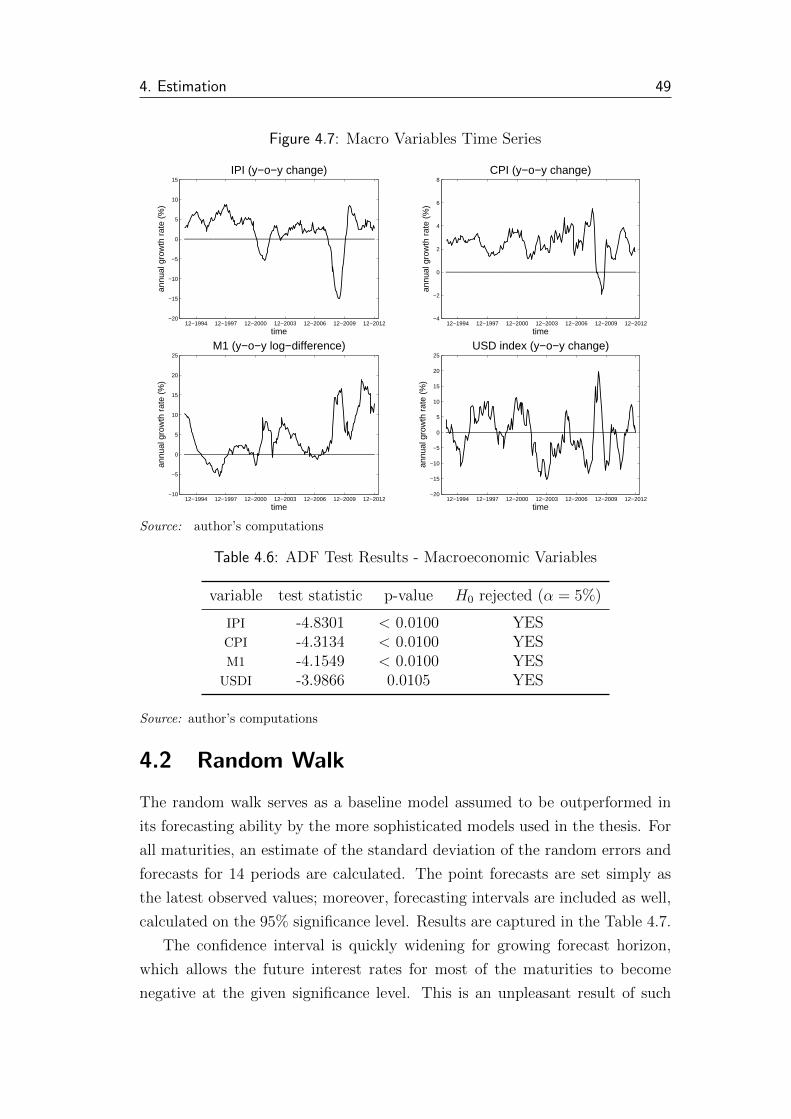

4.6 ADF Test Results - Macroeconomic Variables . . . . . . . . . . 49

4.7 Random Walk Estimation & Forecasts . . . . . . . . . . . . . . 51

4.8 Nelson-Siegel RSS for Various λ Values . . . . . . . . . . . . . . 52

4.9 ADF Test Results - Latent Factors (βs) . . . . . . . . . . . . . . 54

4.10 NS-L-A Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . 57

4.11 NS-L-B Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . 58

4.12 NS-M-A Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . 59

4.13 NS-M-B Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . 60

4.14 AF-L Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

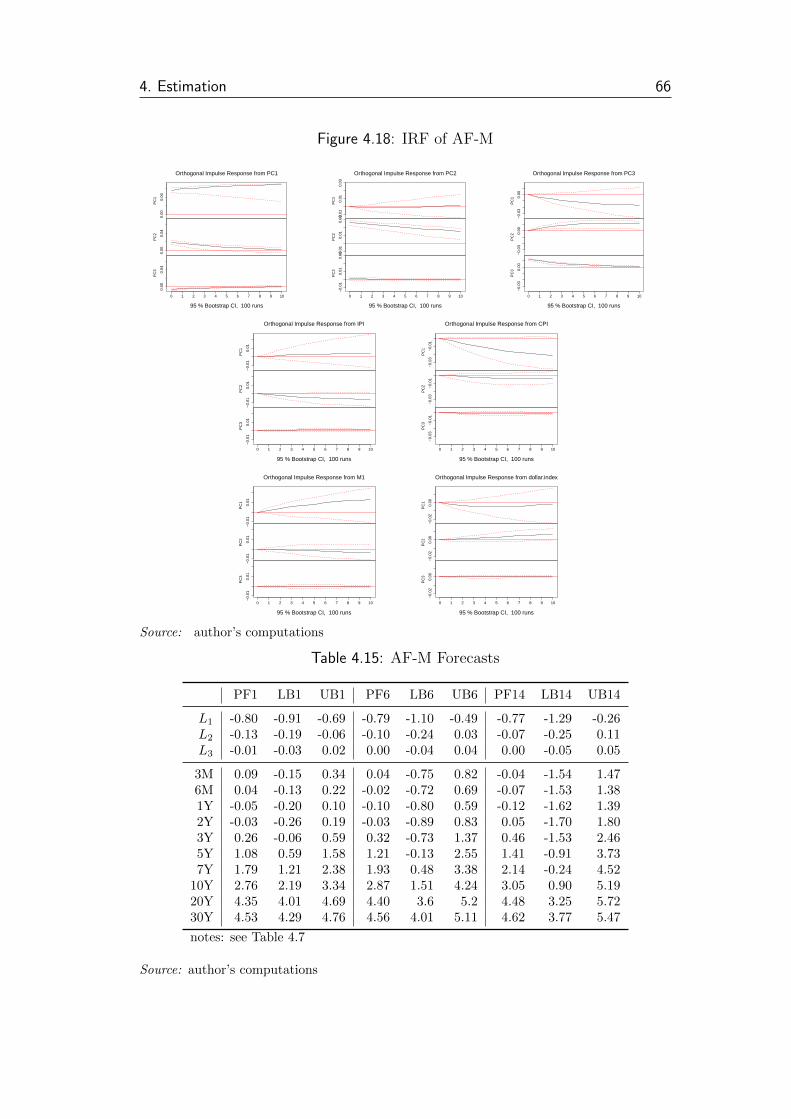

4.15 AF-M Forecasts . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

5.1 In-Sample Fit Results . . . . . . . . . . . . . . . . . . . . . . . . 69

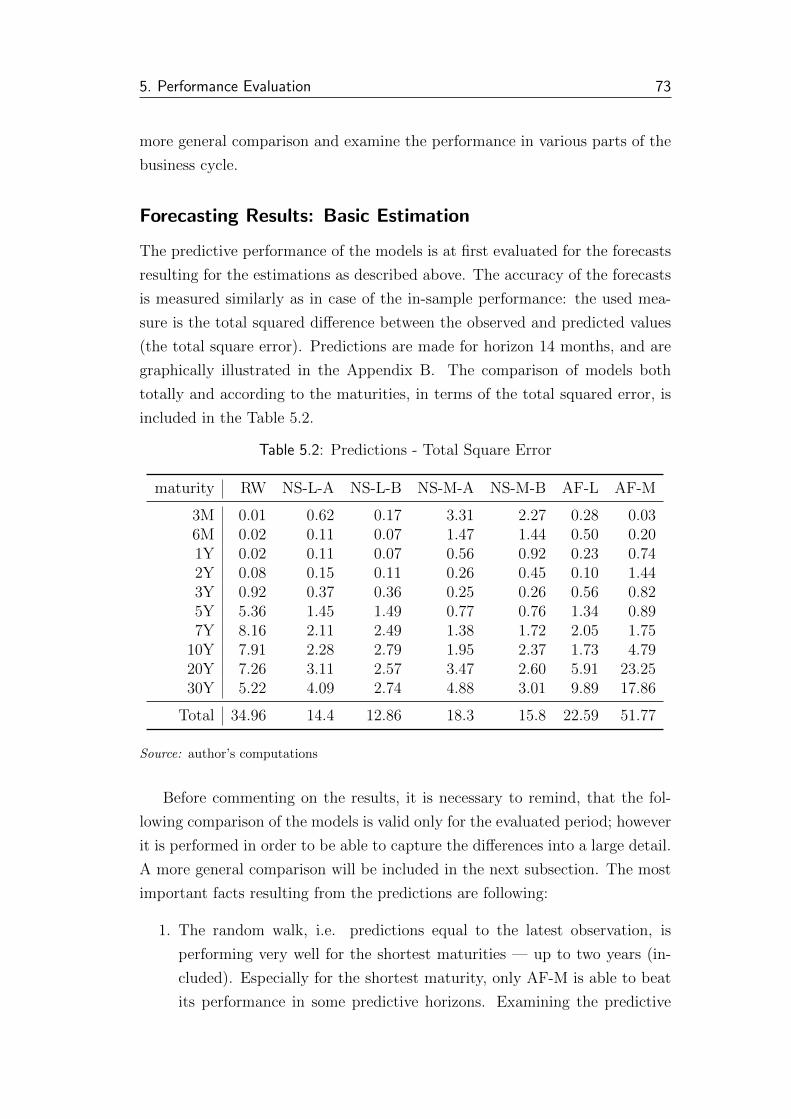

5.2 Predictions - Total Square Error . . . . . . . . . . . . . . . . . . 73

5.3 Prediction Rankings - Random Walk . . . . . . . . . . . . . . . 75

5.4 Prediction Rankings - NS-L-A . . . . . . . . . . . . . . . . . . . 75

5.5 Prediction Rankings - NS-L-B . . . . . . . . . . . . . . . . . . . 76

5.6 Prediction Rankings - NS-M-A . . . . . . . . . . . . . . . . . . . 76

5.7 Prediction Rankings - NS-M-B . . . . . . . . . . . . . . . . . . . 77

5.8 Prediction Rankings - AF-L . . . . . . . . . . . . . . . . . . . . 77

List of Tables ix

5.9 Prediction Rankings - AF-M . . . . . . . . . . . . . . . . . . . . 78

5.10 Predictions - RMSE . . . . . . . . . . . . . . . . . . . . . . . . . 79

A.1 Estimation results for equation beta1A: . . . . . . . . . . . . . . II

A.2 Estimation results for equation beta2A: . . . . . . . . . . . . . . II

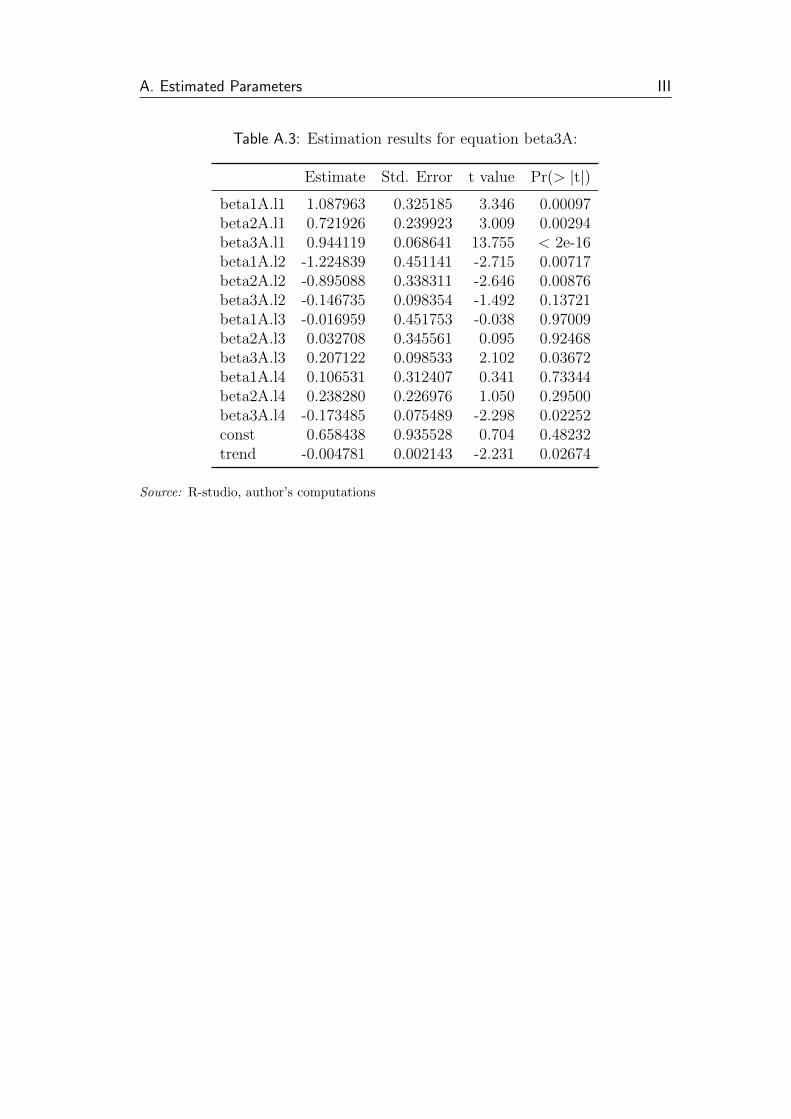

A.3 Estimation results for equation beta3A: . . . . . . . . . . . . . . III

A.4 Estimation results for equation beta1B: . . . . . . . . . . . . . . V

A.5 Estimation results for equation beta2B: . . . . . . . . . . . . . . V

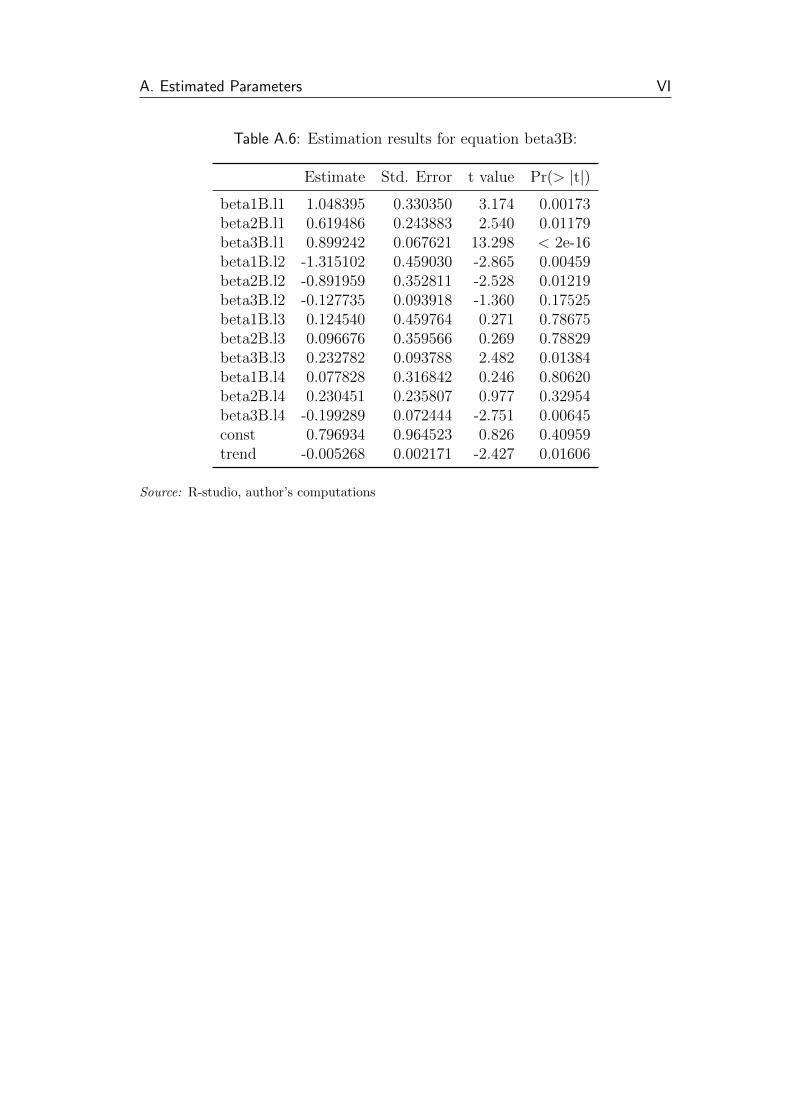

A.6 Estimation results for equation beta3B: . . . . . . . . . . . . . . VI

A.7 Estimation results for equation beta1A: . . . . . . . . . . . . . . IX

A.8 Estimation results for equation beta2A: . . . . . . . . . . . . . . X

A.9 Estimation results for equation beta3A: . . . . . . . . . . . . . . XI

A.10 Estimation results for equation IPI-A: . . . . . . . . . . . . . . . XII

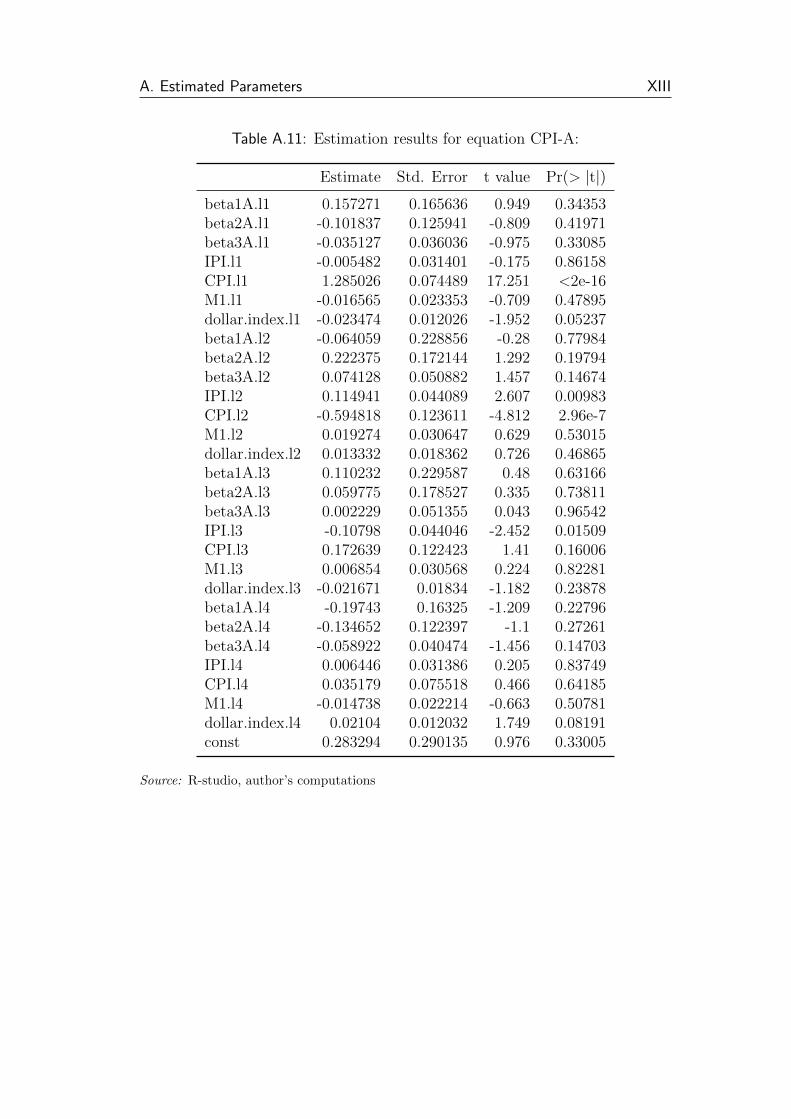

A.11 Estimation results for equation CPI-A: . . . . . . . . . . . . . . XIII

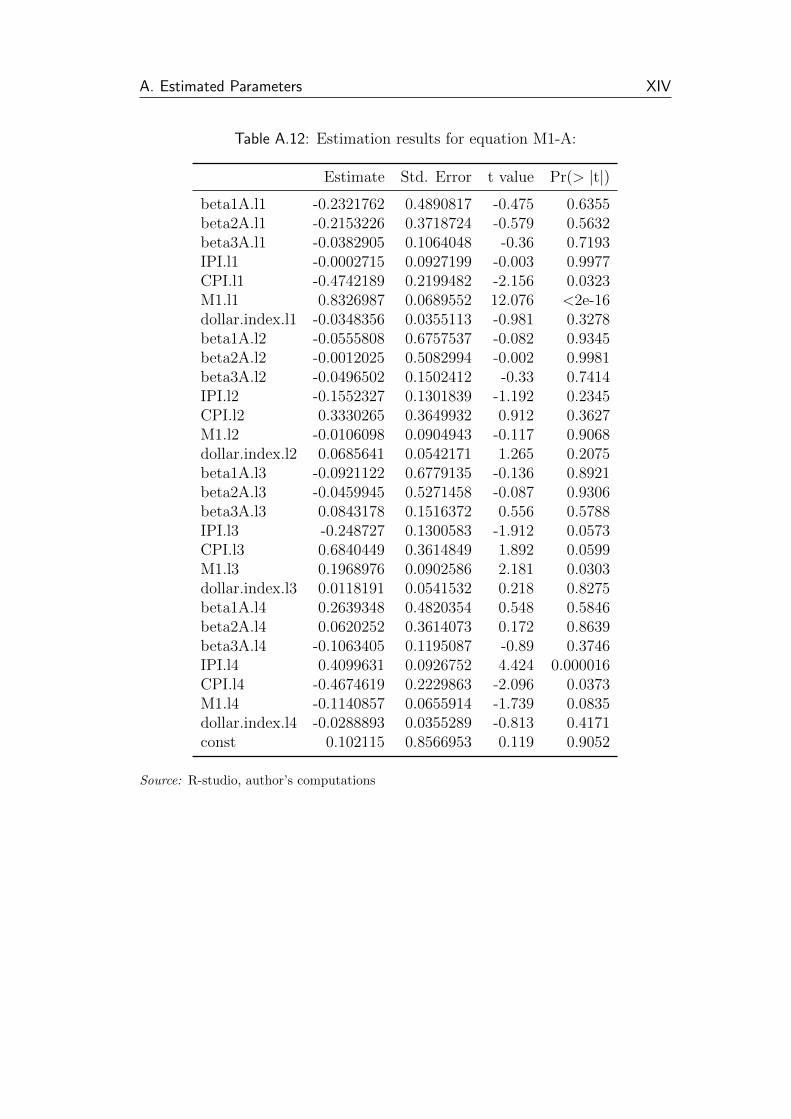

A.12 Estimation results for equation M1-A: . . . . . . . . . . . . . . . XIV

A.13 Estimation results for equation USDI-A: . . . . . . . . . . . . . XV

A.14 Estimation results for equation beta1B: . . . . . . . . . . . . . . XVIII

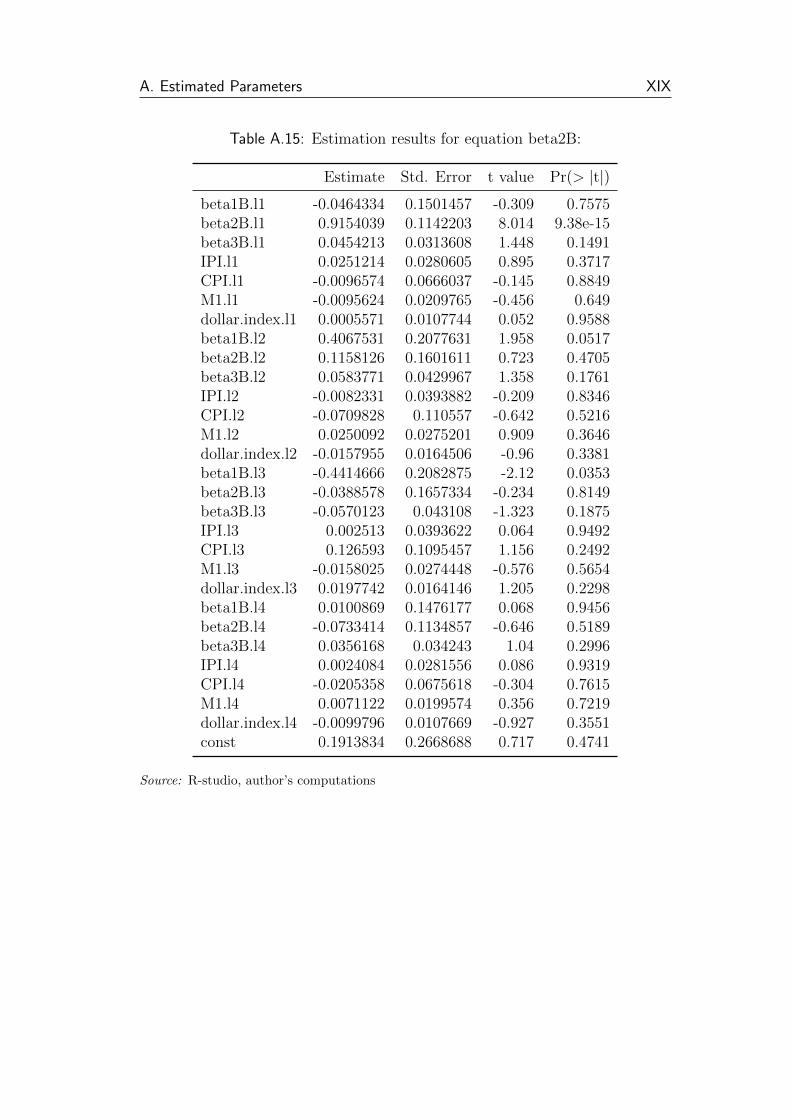

A.15 Estimation results for equation beta2B: . . . . . . . . . . . . . . XIX

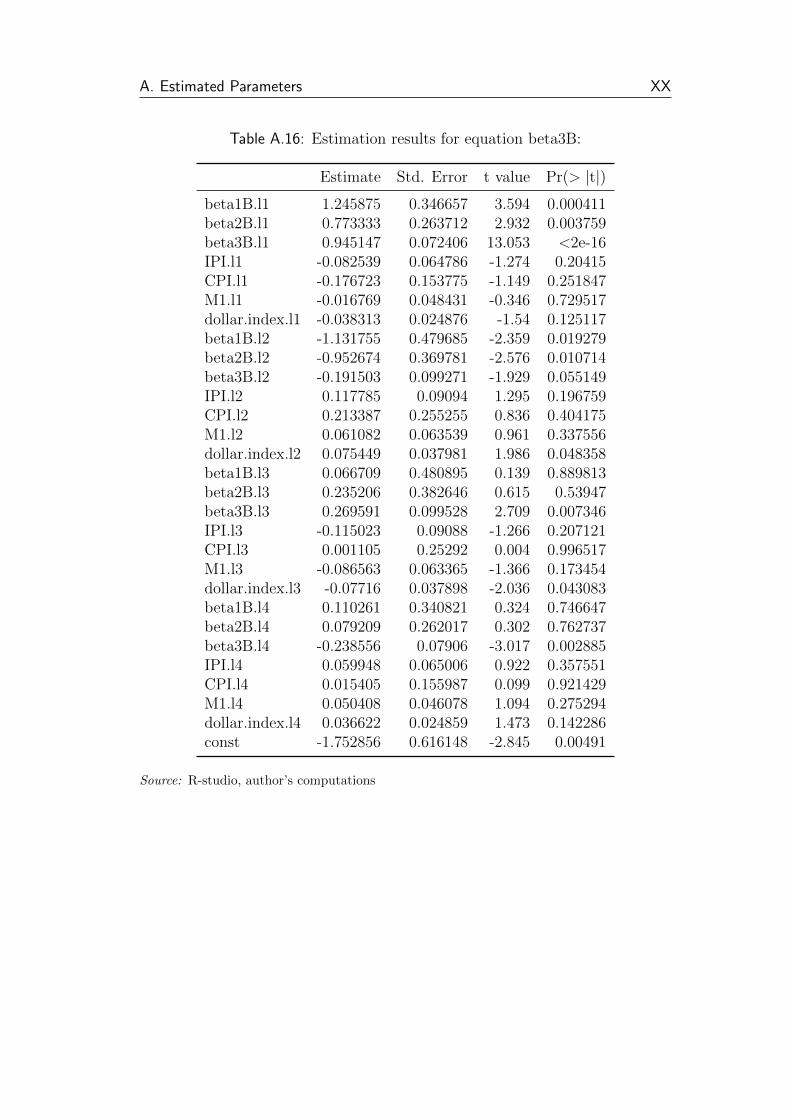

A.16 Estimation results for equation beta3B: . . . . . . . . . . . . . . XX

A.17 Estimation results for equation IPI-B: . . . . . . . . . . . . . . . XXI

A.18 Estimation results for equation CPI-B: . . . . . . . . . . . . . . XXII

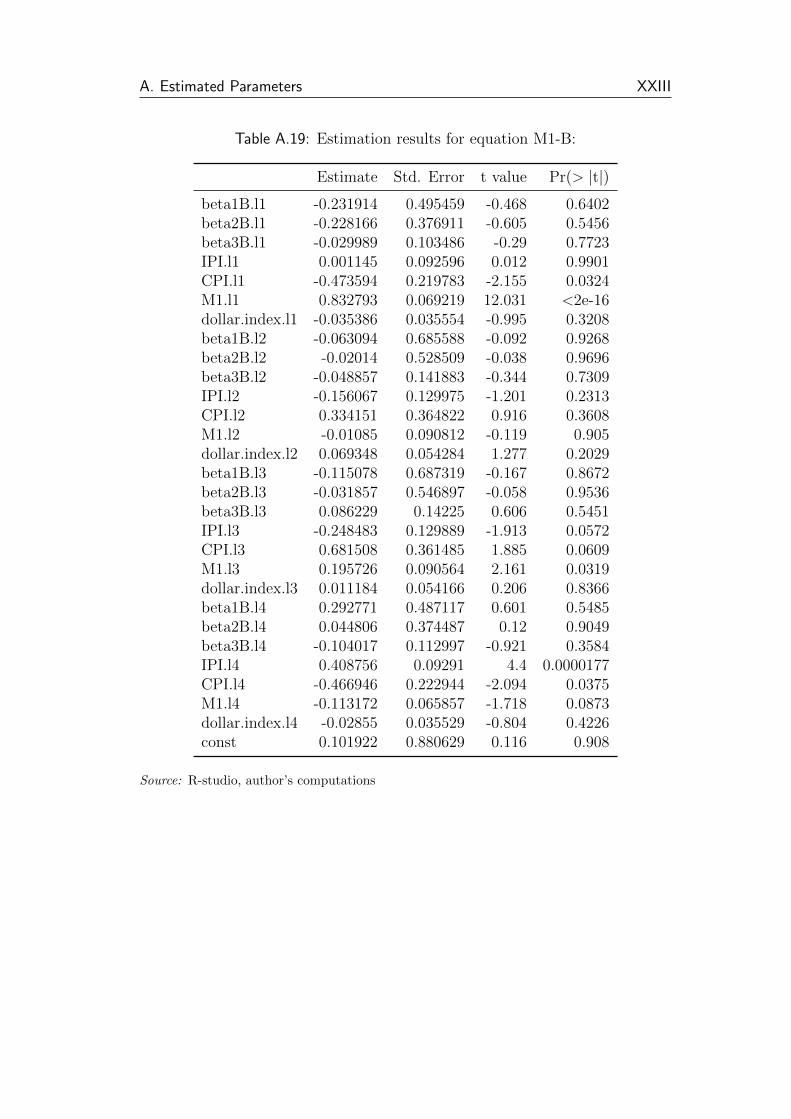

A.19 Estimation results for equation M1-B: . . . . . . . . . . . . . . . XXIII

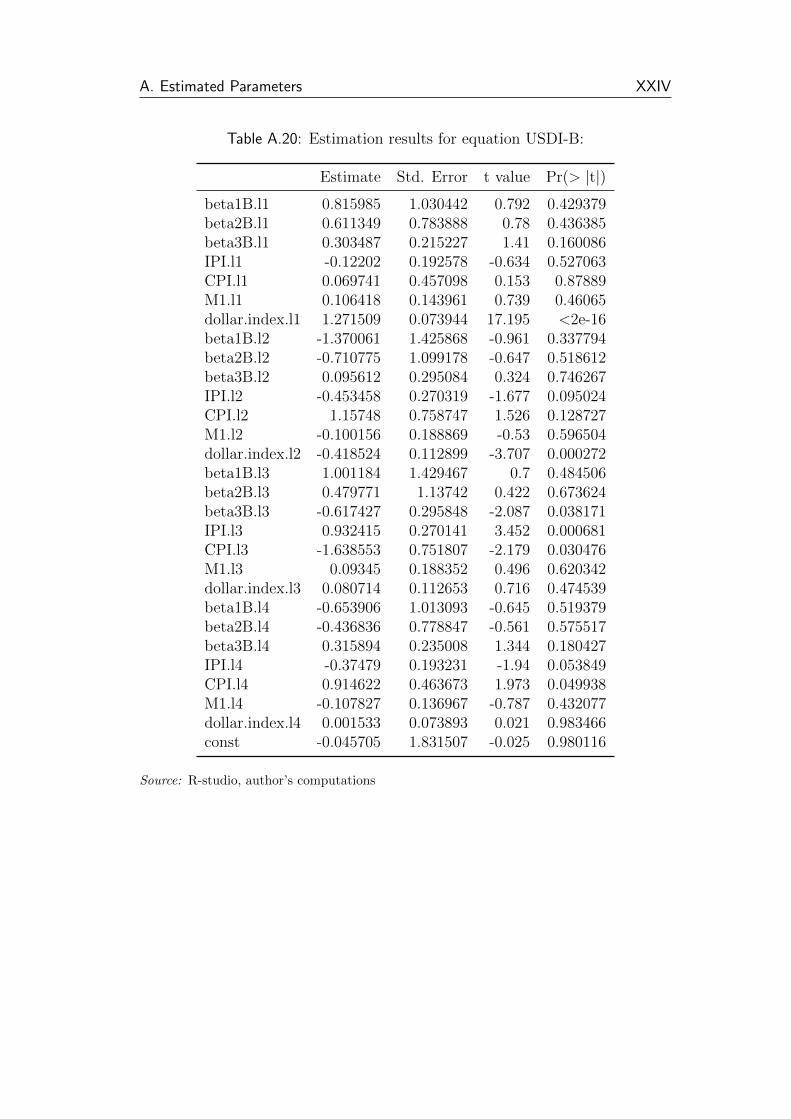

A.20 Estimation results for equation USDI-B: . . . . . . . . . . . . . XXIV

List of Figures

3.1 Relationship of the Factors . . . . . . . . . . . . . . . . . . . . . 21

3.2 Inclusion of the Factors in the Models . . . . . . . . . . . . . . . 22

3.3 Slope - Factor Loading for Various λ Values . . . . . . . . . . . 25

3.4 Curvature - Factor Loading for Various λ Values . . . . . . . . . 26

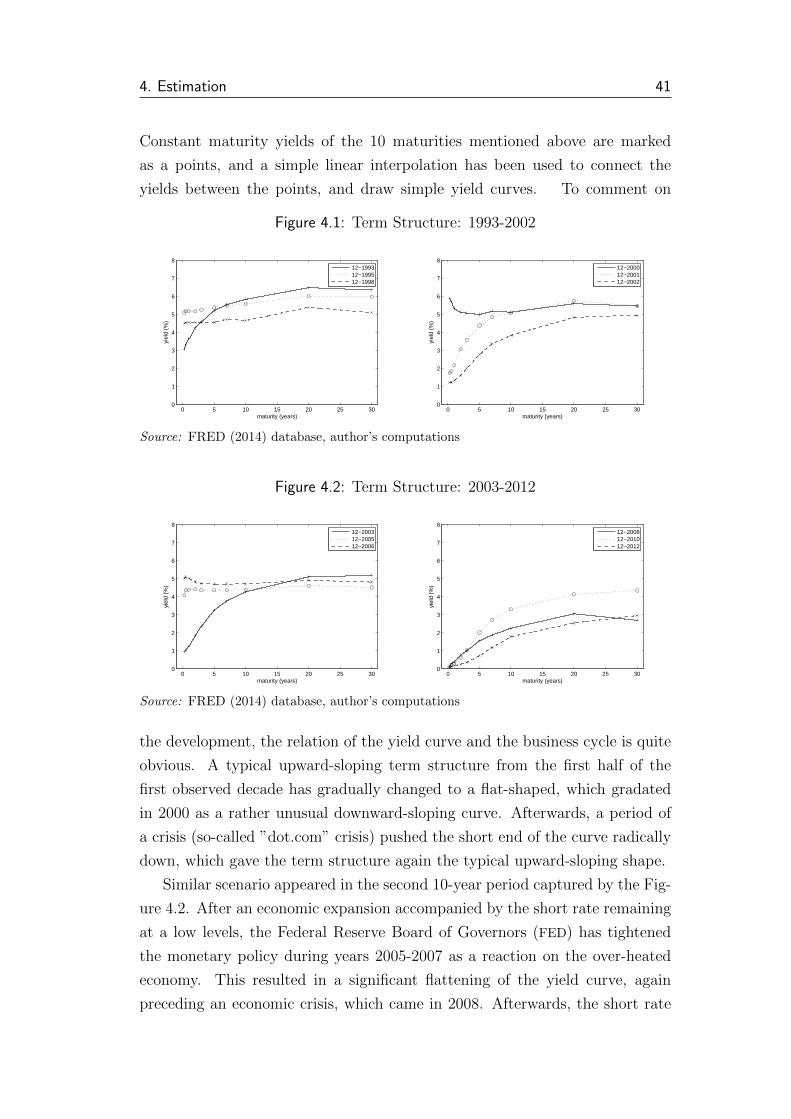

4.1 Term Structure: 1993-2002 . . . . . . . . . . . . . . . . . . . . . 41

4.2 Term Structure: 2003-2012 . . . . . . . . . . . . . . . . . . . . . 41

4.3 Yields Time Series . . . . . . . . . . . . . . . . . . . . . . . . . 42

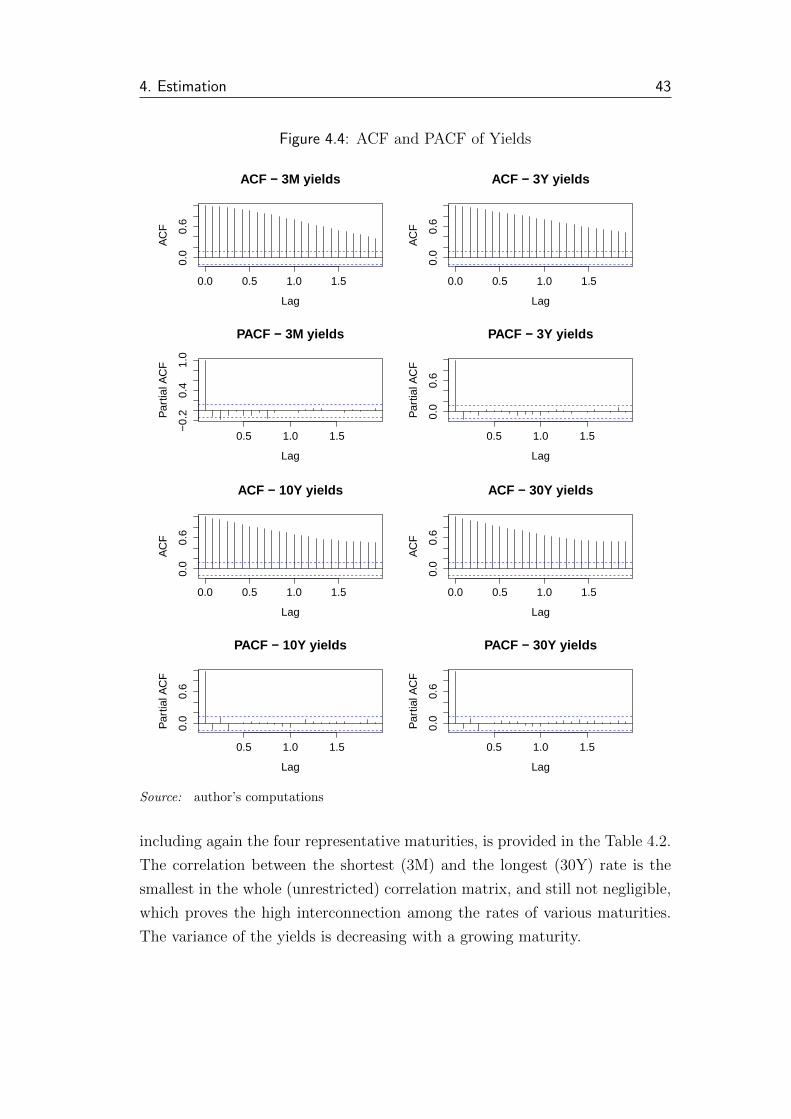

4.4 ACF and PACF of Yields . . . . . . . . . . . . . . . . . . . . . 43

4.5 Principal Components Time Series . . . . . . . . . . . . . . . . 45

4.6 ACF and PACF of Principal Components . . . . . . . . . . . . 46

4.7 Macro Variables Time Series . . . . . . . . . . . . . . . . . . . . 49

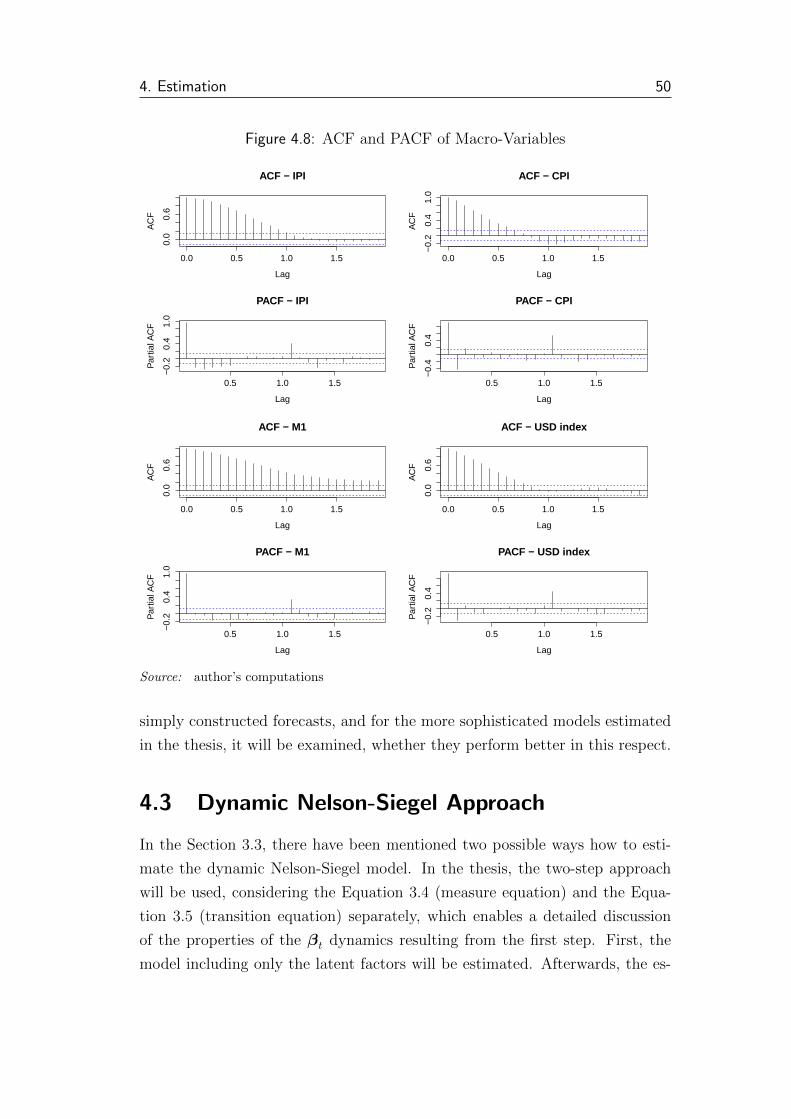

4.8 ACF and PACF of Macro-Variables . . . . . . . . . . . . . . . . 50

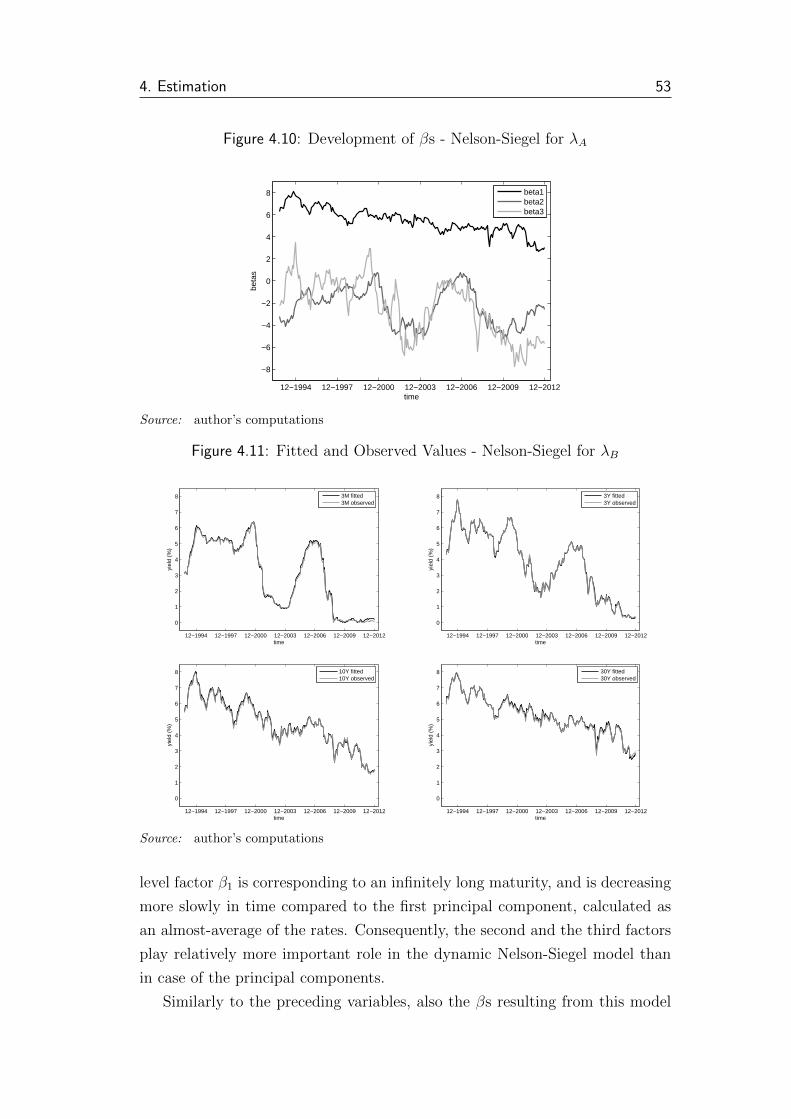

4.9 Fitted and Observed Values - Nelson-Siegel for λA . . . . . . . . 52

4.10 Development of βs - Nelson-Siegel for λA . . . . . . . . . . . . . 53

4.11 Fitted and Observed Values - Nelson-Siegel for λB . . . . . . . . 53

4.12 Development of βs - Nelson-Siegel for λB . . . . . . . . . . . . . 54

4.13 IRF of NS-L-A and NS-L-B . . . . . . . . . . . . . . . . . . . . 58

4.14 IRF of NS-M-A and NS-M-B: part 1 . . . . . . . . . . . . . . . 60

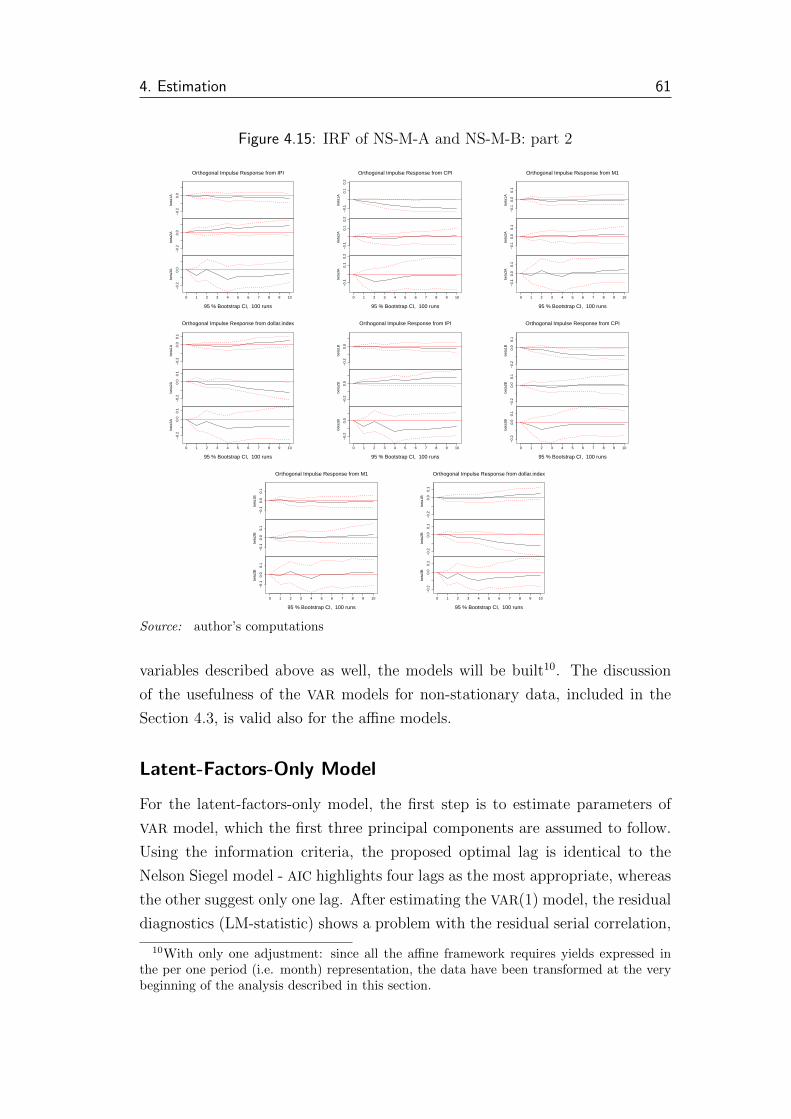

4.15 IRF of NS-M-A and NS-M-B: part 2 . . . . . . . . . . . . . . . 61

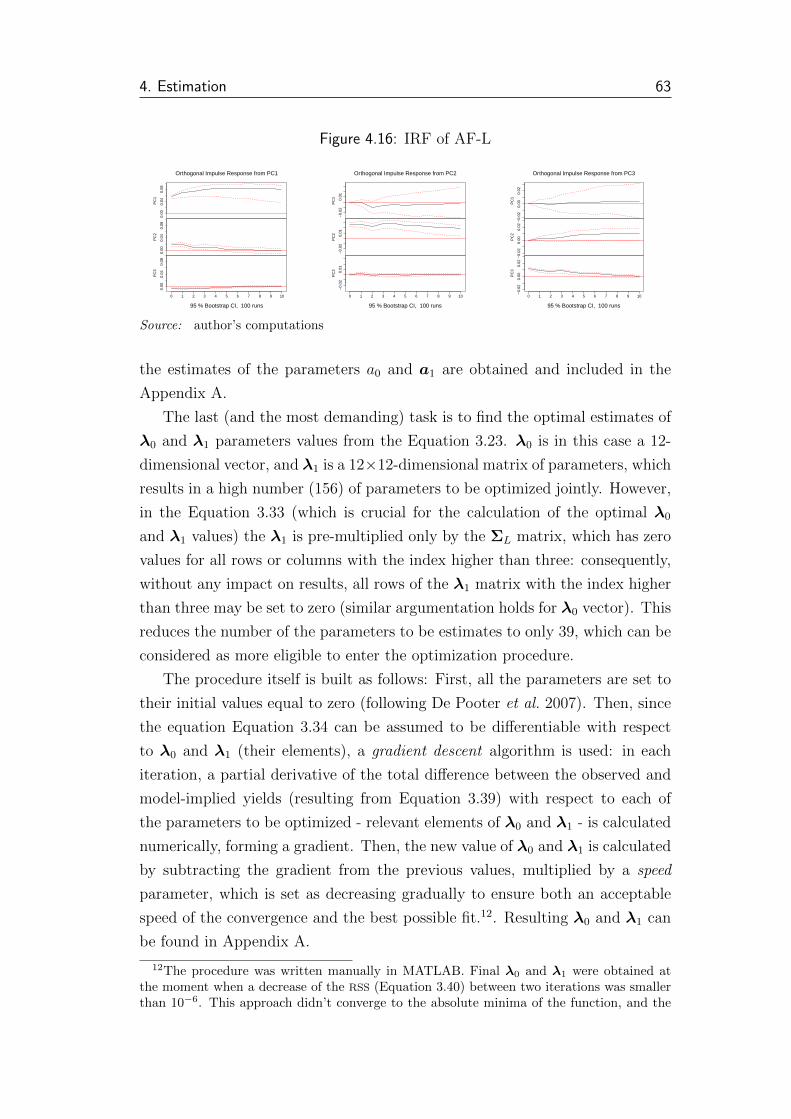

4.16 IRF of AF-L . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 63

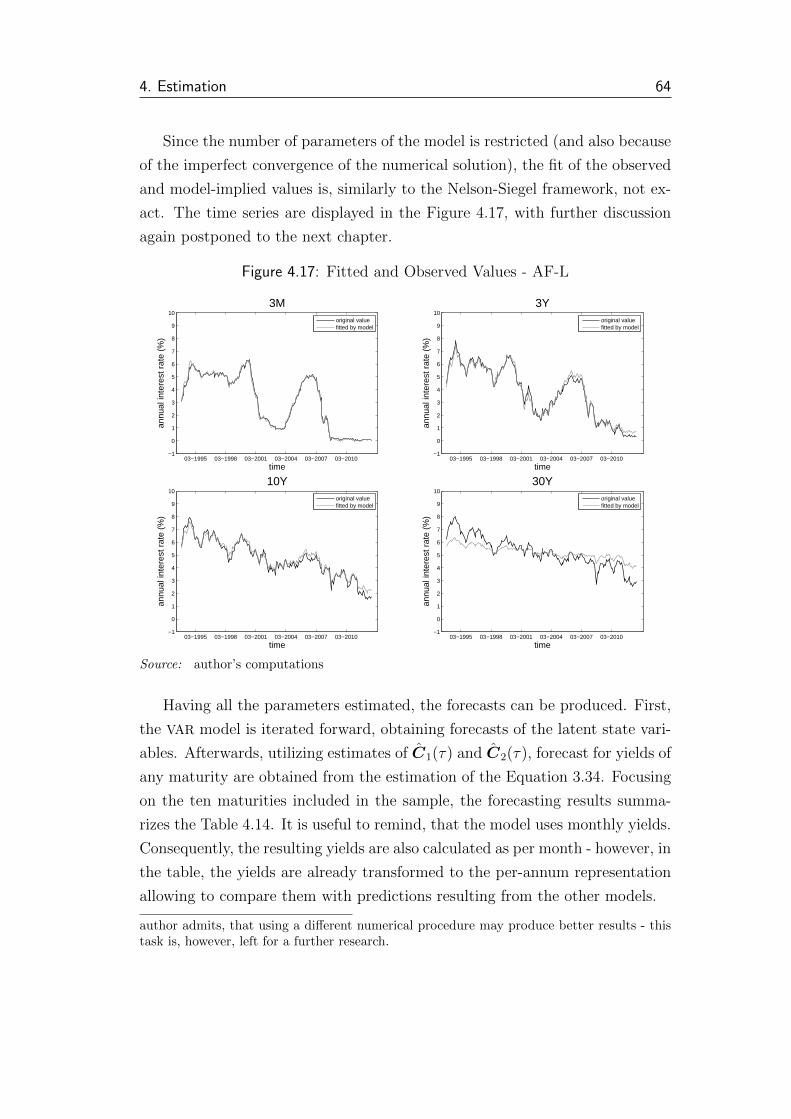

4.17 Fitted and Observed Values - AF-L . . . . . . . . . . . . . . . . 64

4.18 IRF of AF-M . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66

4.19 Fitted and Observed Values - AF-M . . . . . . . . . . . . . . . . 67

5.1 3M Yields Forecasting: One Month Prediction Horizon . . . . . 79

5.2 3M Yields Forecasting: Six Months Prediction Horizon . . . . . 80

5.3 3M Yields Forecasting: One Year Prediction Horizon . . . . . . 80

5.4 3Y Yields Forecasting: One Month Prediction Horizon . . . . . 81

List of Figures xi

5.5 3Y Yields Forecasting: Six Months Prediction Horizon . . . . . 81

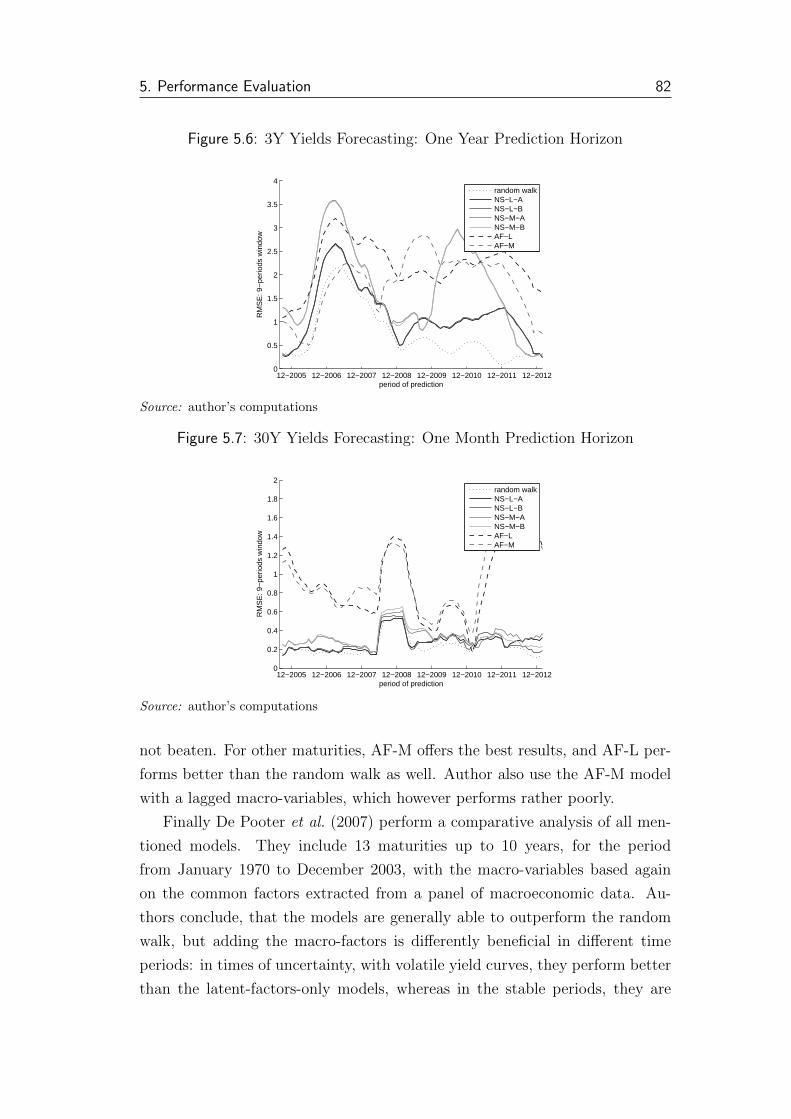

5.6 3Y Yields Forecasting: One Year Prediction Horizon . . . . . . 82

5.7 30Y Yields Forecasting: One Month Prediction Horizon . . . . . 82

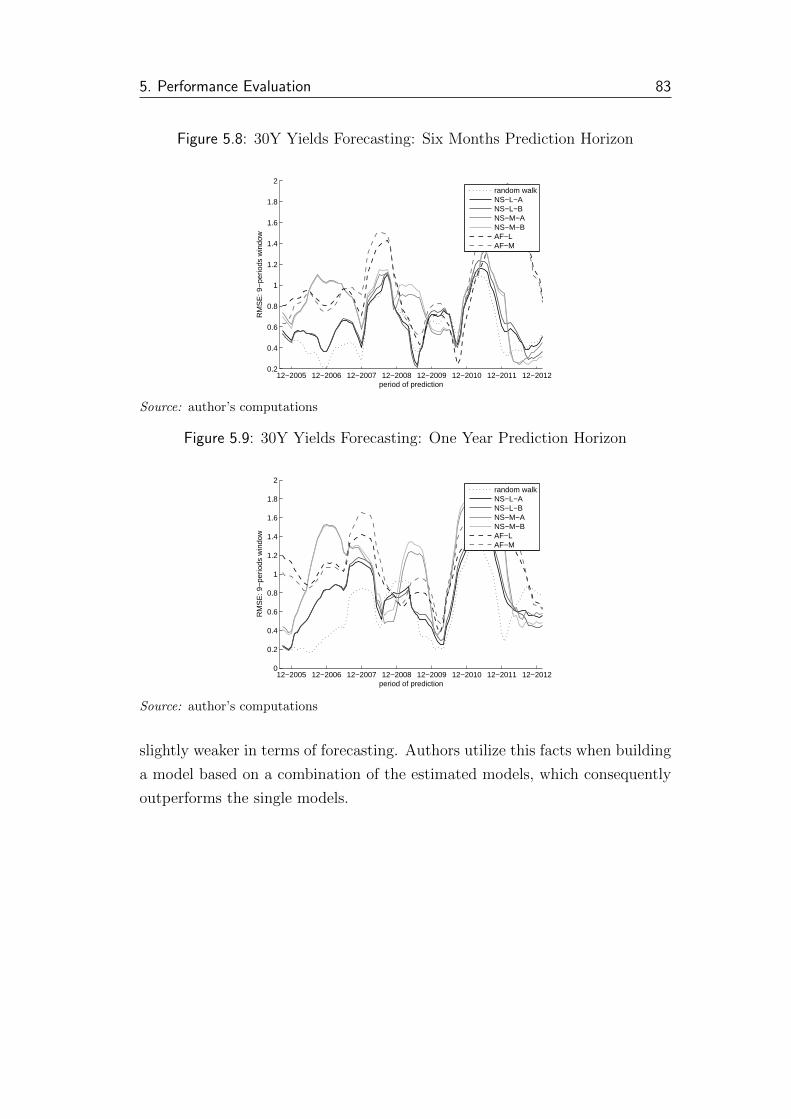

5.8 30Y Yields Forecasting: Six Months Prediction Horizon . . . . . 83

5.9 30Y Yields Forecasting: One Year Prediction Horizon . . . . . . 83

A.1 NS-L-A estimation results . . . . . . . . . . . . . . . . . . . . . I

A.2 NS-L-B estimation results . . . . . . . . . . . . . . . . . . . . . IV

A.3 NS-M-A estimation results - latent variables . . . . . . . . . . . VII

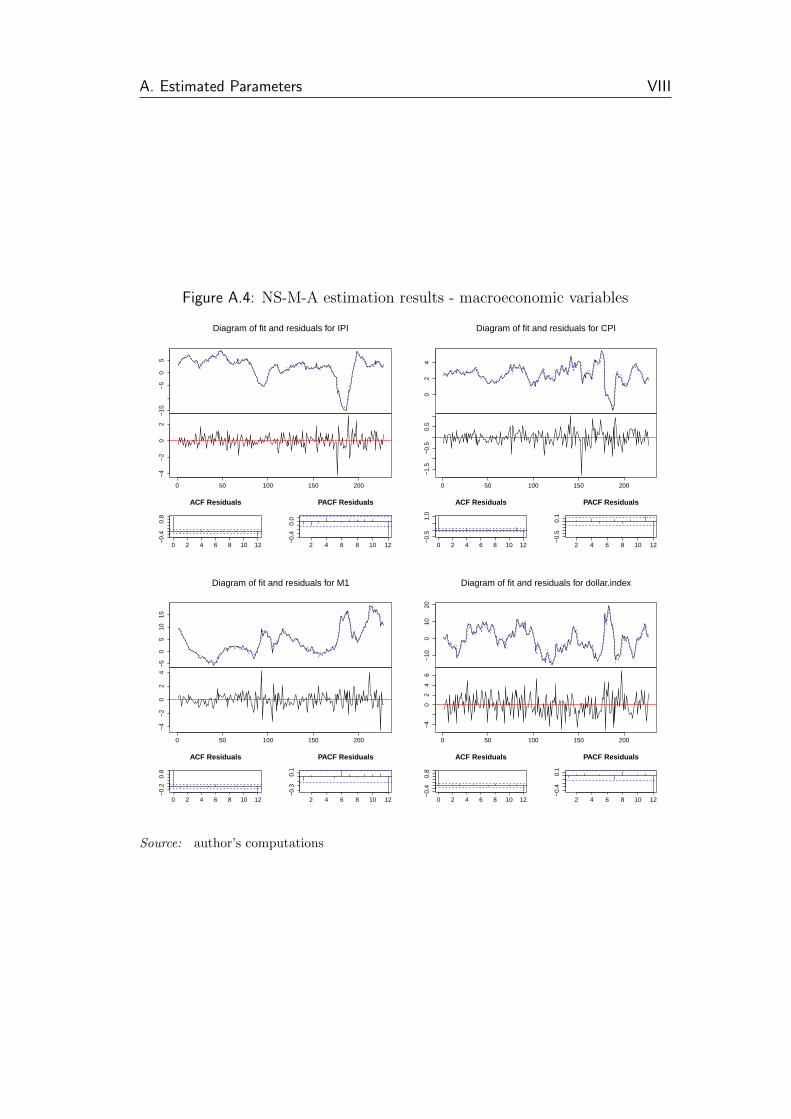

A.4 NS-M-A estimation results - macroeconomic variables . . . . . . VIII

A.5 NS-M-B estimation results - latent variables . . . . . . . . . . . XVI

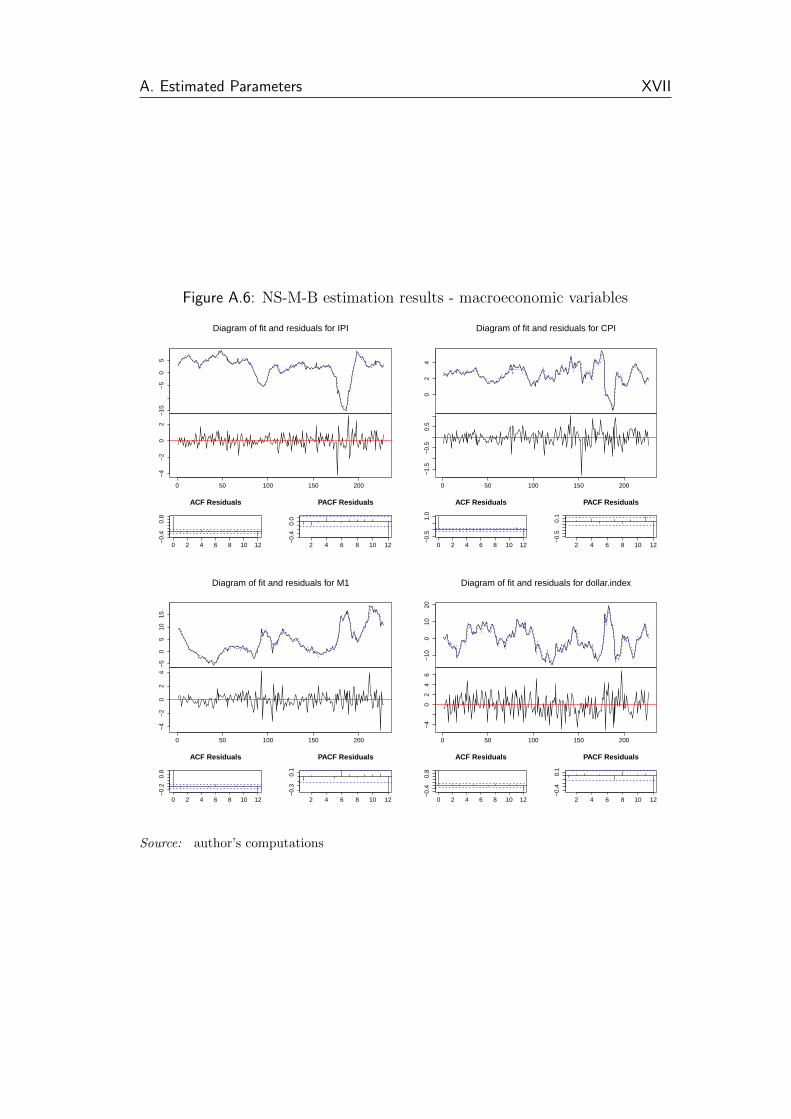

A.6 NS-M-B estimation results - macroeconomic variables . . . . . . XVII

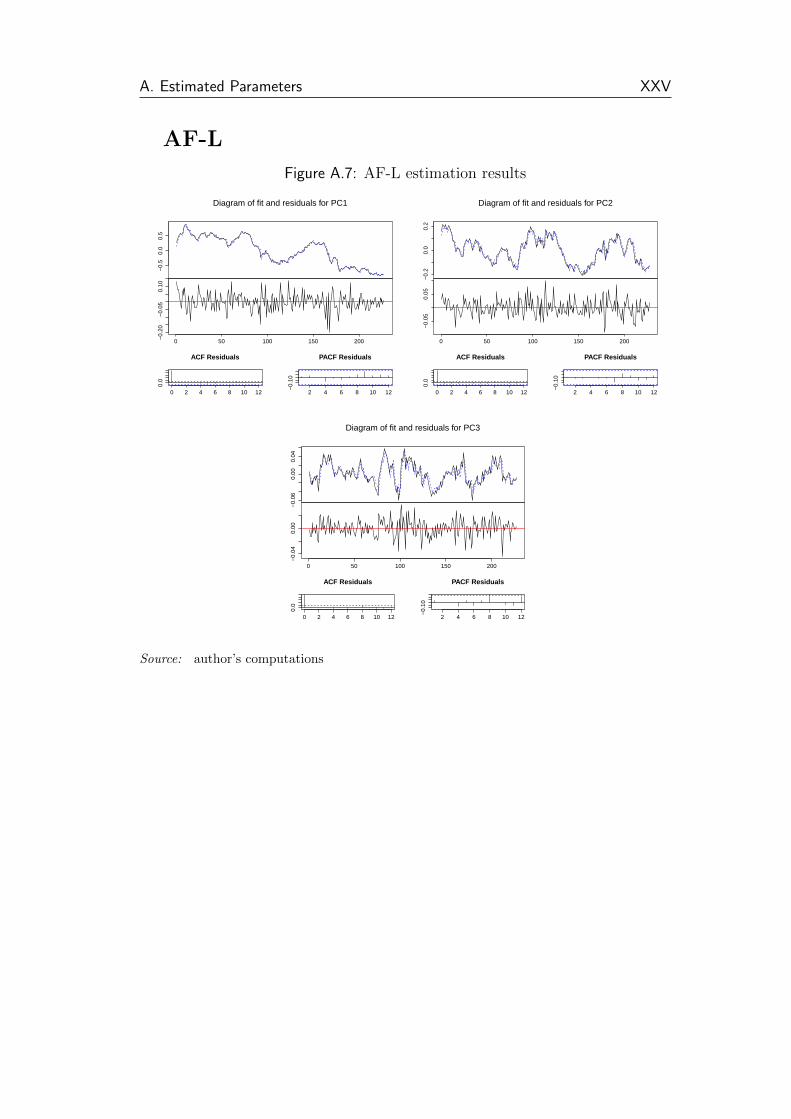

A.7 AF-L estimation results . . . . . . . . . . . . . . . . . . . . . . XXV

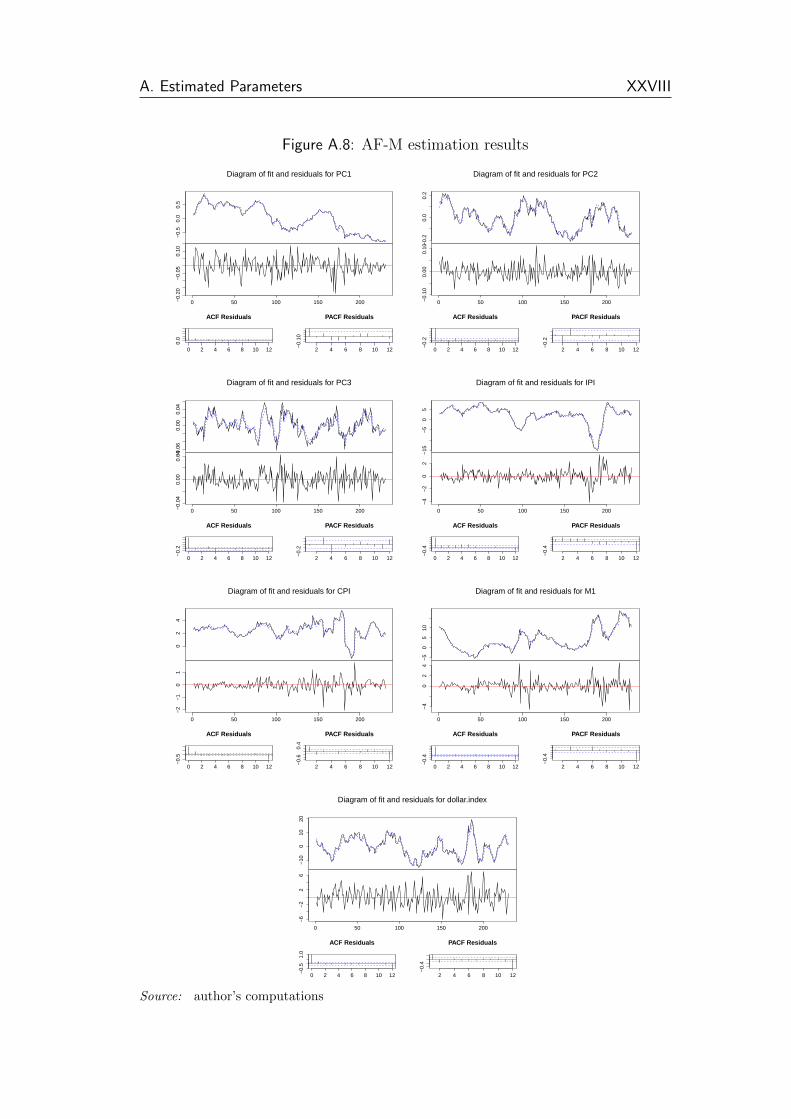

A.8 AF-M estimation results . . . . . . . . . . . . . . . . . . . . . . XXVIII

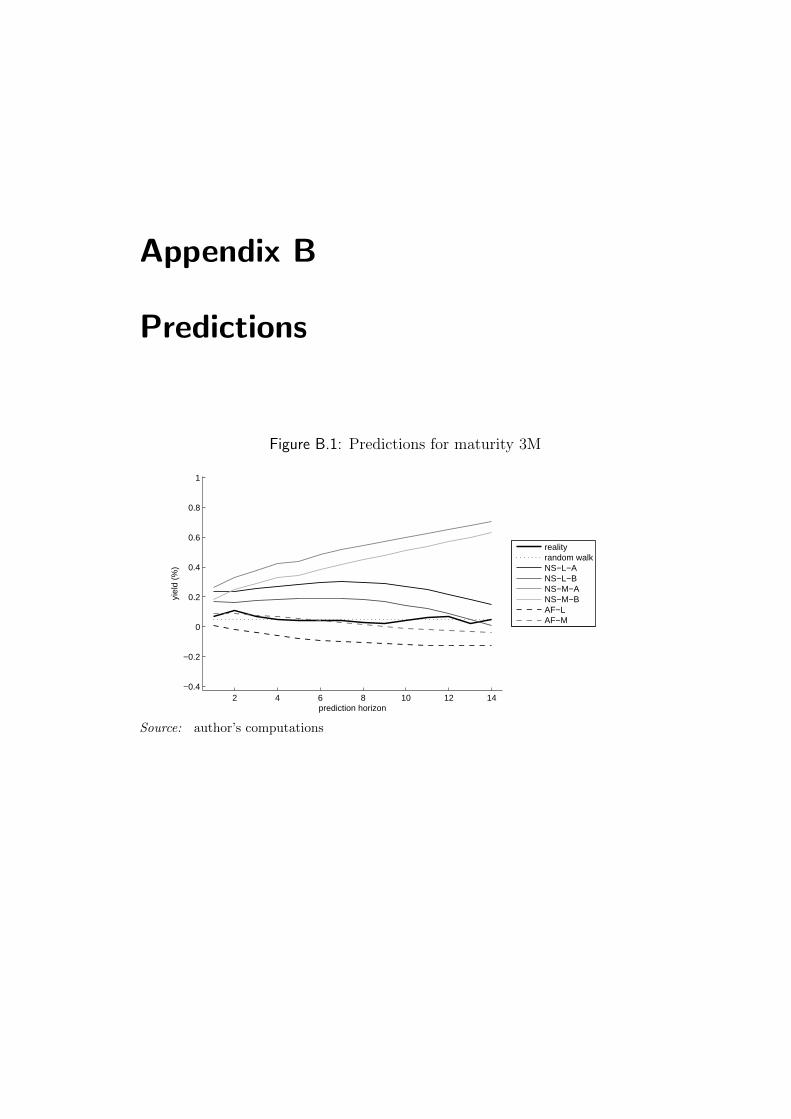

B.1 Predictions for maturity 3M . . . . . . . . . . . . . . . . . . . . XXIX

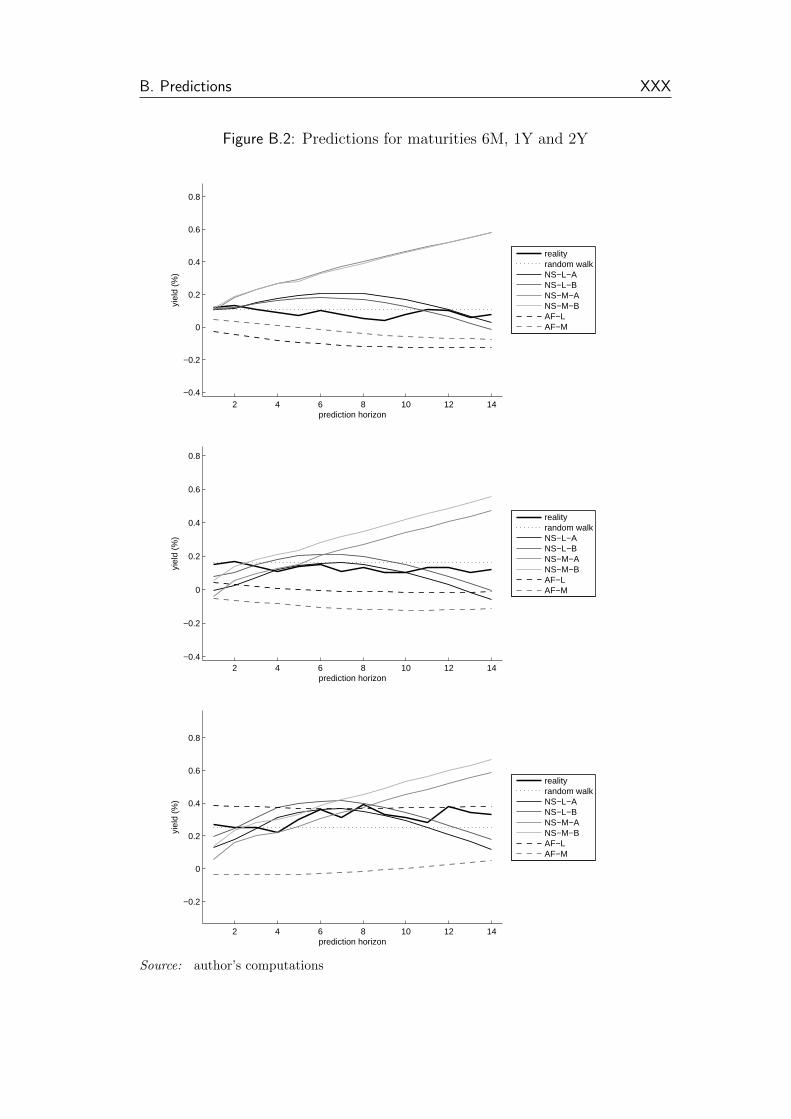

B.2 Predictions for maturities 6M, 1Y and 2Y . . . . . . . . . . . . XXX

B.3 Predictions for maturities 3Y, 5Y and 7Y . . . . . . . . . . . . . XXXI

B.4 Predictions for maturities 10Y, 20Y and 30Y . . . . . . . . . . . XXXII

Acronyms

ACF Autocorrelation Function

ADF Augmented Dickey-Fuller

AIC Akaike Information Criterion

CPI Consumers Price Index

DSGE Dynamic Stochastic General Equilibrium

FED Federal Reserve Board of Governors

HJM Heath-Jarrow-Morton Model

HQIC Hannah-Quinn Intormation Criterion

IPI Industrial Production Index

IRF Impulse-Response Function

LMM LIBOR Market Model

M1 Monetary Aggregate M1

OLS Ordinary Least Squares

PACF Partial Autocorrelation Function

PCA Principal Component Analysis

RMSE Root Mean Square Error

RSS Residual Sum of Squares

SIC Schwarz Information Criterion

USDI U.S. Dollar Index

VAR Vector Autoregression

Chapter 1

Introduction

The global financial crisis, which completely broke out at the moment the large

investment bank Lehman Brothers declared bankruptcy in September 2008, has

fully shown a large weakness of both macroeconomic models used in the central

banks and the approach of the financial markets players to the asset valuation

and the risk management: in their models, the areas of macroeconomics and

finance were not explicitly considered as interconnected. The problem has

been known already before the crisis, but only the huge collapse attracted

the necessary attention to it. Consequently, so-called macro-finance models,

incorporating both financial principles and the macroeconomic dynamics, are

becoming increasingly popular. The expected benefit of such models can be

well illustrated in terms of the pre-crisis situation. An explicit inclusion of the

macroeconomic dynamics into the models underlying the investment and risk-

management decisions could maintain a reasonable level of the risk-aversion on

the global markets, as the banks and hedge funds would be possibly able to

identify the pre-crisis boom as related to the over-heated economy and hence

very unstable. On the other hand, enlarging the macroeconomic models used

in central banks by the financial assets valuation principles might help the

monetary authority to synchronize its policy steps with the financial markets

situation, and to react on the economic reality swiftly, not ex post.

During the last fifteen years, a large progress in the macro-finance modelling

has been done, with the most important milestones mentioned throughout the

further text. The thesis compares the most frequent approaches to the term

structure modelling, both with and without an explicit inclusion of the macroe-

conomic variables. Through the models specification, estimation, and results

evaluation, the work intends to contribute to the macro-finance field in a few

1. Introduction 2

respects, reacting on some weaknesses of preceding studies:

First, most of the models are estimated using a data sample starting far

before 1990, usually covering most of the second half of the 20th century. How-

ever, since the models include global macroeconomic relations resulting from

behaviour of the economic subjects (most importantly the central banks in this

case), it is sometimes argued that such a long horizon could provide models not

resisting the Lucas Critique. Consequently, the thesis examines, whether it is

possible to estimate the models using only on the recent data, for which the cen-

tral banks objective functions can be considered as stable under the paradigm

of the inflation targeting. Second, the models rarely include maturities longer

than ten years. The thesis consequently examines, whether the models are

able to fit and predict also the longest part of the yield curve. Third, it can be

expected that individual models produce different results, in terms of their per-

formance, under various macroeconomic and financial markets conditions. For

this reason, the performance of the models is analysed also dynamically over a

certain period of time, allowing to examine the strength of various models in

different parts of the business cycle.

When performing the analysis, the thesis is structured in the following way:

The second chapter provides necessary basis. It starts with a definition of

the core terms and the notation used thorough the work, simultaneously ex-

plaining both theory and mathematics of the basic fixed income instruments

— bonds. It also introduces motivations and approaches related to the in-

terest rates modelling. The theoretical part is finished with an outline of the

quantitative methods used in the thesis.

The third chapter starts with a discussion of the factors underlying the

interest rate dynamics. Then it describes in a detail two general frameworks of

the term structure models — a dynamic Nelson-Siegel approach and affine-class

models. The theoretical background behind each of the groups is explained,

and the models are then built in both latent-factors-only and macro-finance

forms. For each model, an approach used for its estimation is also outlined.

The fourth chapter covers description of the used data and the estimation

of the models. Figures and tables are extensively used in order to illustrate

results of the estimations. The fifth chapter describes the properties of the

estimated models, both in terms of impulse-response functions and a predictive

performance. Moreover, the development of the accuracy of models in time is

inspected. The chapter also includes a comparison of the results with similar

studies. Finally, the last chapter summarizes findings of the thesis.

Chapter 2

Basic Definitions and Notations

2.1 Bond Market, Yield and Interest Rate

The thesis deals with a dynamic behavior and relationship of both macroeco-

nomic and financial variables. A brief and concise description of the variables

is the necessary first step, together with the introduction of the notation used

throughout the work.

The financial instruments underlying the topic of the thesis are bonds. A

bond can be defined as ”any interest-bearing or discounted government or cor-

porate security that obligates the issuer to pay the bondholder a specified sum of

money, usually at specific intervals, and to repay the principal amount of the

loan at maturity.” (Downes & Goodman 1998, pg. 59). An important special

type of bonds is a zero-coupon bond, which pays no cash flow except for the

principal amount at the maturity of the bond. Zero-coupon bonds are almost

always traded with a discount, i.e. with their price smaller than the principal

amount, whereas coupon-bearing bonds can be traded for a price either below

or above the principal amount.

The bond market is a place where a bond demand and a bond supply

meet. The demand side is formed by investors motivated to obtain a return

from the amount they are offering to fund-seekers creating the bond supply.

Such definition is valid for the primary bond market, where the bonds are

underwritten. Nevertheless, a secondary market also exists, where the supply

of bonds is formed by the subjects that are re-selling the bonds once purchased,

i.e. investors exiting the bond market. From a simplified point of view, the

secondary bond supply may be considered as a negative bond demand, therefore

it is possible to describe both bond markets together.

2. Basic Definitions and Notations 4

Generally, a motivation of the investors is to realize a yield. They enter the

bond market only if the yield resulting from the bond purchase, after adjusting

for the risk related to the investment, is higher then a risk-adjusted yield of

different investment opportunities. Contrary, the fund seekers enter the bond

market in order to minimize their costs of funding: to get the lowest possible

interest rate. The terms yield and interest rate can not be considered as equiv-

alent terms — basically not because of the method of their calculation, but

because of the economic motivation related to them. Consequently, as notes

Choudhry (2011), the terms yield curve and term structure of interest rates, as

defined below, are in general not exactly the same and a precise description of

them is necessary for an exact specification of the subject of the thesis.

Yield

Yield (in general) represents a rate of an increase or a decrease of resources that

a subject (investor) holds for purposes other than consumption. It is usually

expressed as relative change during a period of time. Investors want to invest

their resources into such an asset, real or financial, that offers maximal yield

within given risk category — alternatively, the investor wants to maximize

the risk-adjusted yield. One of the possibilities, where to invest, is the bond

market. Investors enter the bond market having an intuition about the yield

they want to achieve (required yield), which is usually different from the actual

yield realized on the market — an investor confirms a trade only if his required

yield is lower or the same as the observed market yield. The required yield is

a function of many variables, with the most important being:

time factor ρ — the ”core” compensation required by the investors for post-

poning their consumption into the future

expected inflation E [π] — included as the investor is concerned with the real

yield regardless to the changes of the price level

risk premium ξ — required for the uncertainty related to the investment; it may

be further split into:

� market risk premium ξM — related to the fact, that market condi-

tions may change, which would have an impact on the price of the

bond

2. Basic Definitions and Notations 5

� liquidity risk premium ξL — related to the risk that investor will not

be able to sell the bond on the secondary market without any costs

(time, transaction costs)

� credit risk premium ξC — reflecting the fact there is non-zero prob-

ability the counter-party will not be able to meet its obligations

related to the bond

Individual required yield yreq is then a function of the variables mentioned

above:

yreq = f (ρ, ξM , ξL, ξC , E [π]) (2.1)

The function 2.1 is unique for each investor. Moreover, it differs among various

instruments, since these are related to different risks and time dimension. To

make the analysis simple and consistent, the study focuses on a single instru-

ment: government bonds1. However, there will be bonds of various maturities

used in the thesis — the variance in the required yield for bonds differing only

in their maturity is often called term premium. The individual demand for

bonds is then determined by the difference between the required yield and the

yield observed on the bond market, together with other factors: individual

wealth, income, taxation, institutional factors (law enforcement, political sta-

bility, etc.). Moreover, the demand for bonds is also influenced by the yields

on alternative markets – a stock market, a foreign currencies market, and a

real assets (commodities, real estate,...) market. The aggregate bond demand

is then the sum of all individual demands.

Let Pc,t(τ) be a price2 of a coupon-bearing bond at a time t, maturing at

time T = t+ τ , with n coupon payments with rates c1, c2, . . . cn paid at times

t1, t2, . . . tn. If the bond is held until its maturity, its yield (yytm) per one

period is a function of the variables (parameters):

yytm = f (Pc,t(τ), t, τ, ci, ti) for i=1...n (2.2)

1It can be assumed that results of the thesis might be generalized for the whole bondmarket (particularly also corporate or municipal bonds), in case the higher risk premium ishandled properly.

2In the study, price will be always expressed as a percentage of the nominal value – it isnot necessary to deal with either the nominal value of the bond or the absolute value of thecoupons.

2. Basic Definitions and Notations 6

and can be defined as a solution of the following equation.

Pc,t(τ) =n∑i=1

ci

(1 + yytm)ti−t+

1

(1 + yytm)τ(2.3)

Usually, a few simplifications may be used: all the coupons are assumed to

be identical c = c1 = c2 = ... = cn, paid in regular periods starting one period

after t with the last coupon paid with maturity. If the maturity is expressed

in years, the period between two coupon payments is equal to τ/n. The price

can be consequently expressed in a simpler way:

Pc,t(τ) =n∑i=1

c

(1 + yytm)iτn

+1

(1 + yytm)τ(2.4)

The bond price can be further split into a so-called clean price and the accrued

interest. However, since only the zero coupon bonds will be analysed in the

further work, it is not necessary to describe the general coupon bonds into more

detail. The Equation 2.4 implicitly assumes that the interest period is identical

with the coupon period. However, it can be also convenient to express the

Pc,t(τ) using an infinitely small interest period, i.e. continuous compounding:

Pc,t(τ) =n∑i=1

ce−yytmiτn + e−yytmτ (2.5)

In case the coupon rate c = 0, the bond is called zero-coupon bond, denoted

as Pt(τ)(omitting the c subscript), and the yield to maturity can be expressed

directly from either Equation 2.4:

yytm = Pt(τ)−1τ − 1 (2.6)

or Equation 2.5:

yytm = − lnPt(τ)

τ(2.7)

Generally, the bonds with various maturities, having all other parameters

identical, have to be considered as different bonds, since the inputs to the

Equation 2.1 are not the same - their yields differ in the term premium. The

function of yield to maturity with respect to the maturity is then called a yield

curve, which will be described in detail below.

2. Basic Definitions and Notations 7

Interest Rate

The fund seekers, which form the supply side of the bond market, are trying

to find the cheapest way how to finance their needs. The cost of borrowing

the funds (i.e. price of the free funds) is represented by the interest rate. The

bigger the interest rate is, the more costly it is for a borrower to get funds, and

the more profitable it is for a creditor to provide them.

In case of the coupon bond paying n coupons, it is useful to split the cash

flows and replicate the bond by a set of n zero-coupon bonds (the one with

the longest maturity including also the notional), which are sold to n investors.

Since each of the investor faces different maturity, they require different yields

- put differently, the fund seeker pays different interest rate for each single

cash-flow. The price of the bond, i.e. the amount the fund-seeker obtains

when issuing the bond, is correspondingly determined as the future cash flows

discounted by individual interest rates:

Pc,t(τ) =c[

1 + rt(1τn

)] 1τn

+ . . .+c[

1 + rt

((n−1)τn

)] (n−1)τn

+1 + c

[1 + rt (τ)]τ(2.8)

Pc,t(τ) =n∑i=1

c[1 + rt

(iτn

)] iτn

+1

(1 + rt(τ))τ(2.9)

where rt(iτn

)is the interest rate set in the time t for an amount repayable in

time t+ iτn

, i = 1 . . . n.

Obviously, the Equation 2.9 is very similar to the Equation 2.4. However,

the forces changing the bond supply are different. The borrowers will indi-

vidually calculate interest rate they are willing to pay, depending on costs of

different funding resources (bank loans, shares etc.), and their credit capacity

related to their real investments opportunities. The bond will be issued only if

its realization on the market is not more expensive than the acceptable interest

rate.

In case of a zero-coupon bond, the Equation 2.9 (plugging 0 for c) allows

an analytical expression of rt(τ), which is equal to the right-hand side of the

Equation 2.6:

rt(τ) = Pt(τ)−1τ − 1 (2.10)

2. Basic Definitions and Notations 8

The same holds for continuous compounding and Equation 2.7:

rt(τ) = − lnPt(τ)

τ(2.11)

For purpose of construction of various interest rate models, it is necessary

to present also the concept of an instantaneous spot interest rate rt. It can

be defined as an interest rate of a loan or a bond repayable after an infinitely

small period:

rt = limτ→0

rt(τ) (2.12)

Another common step is to define the forward rate ft(T1, T2), which can be

expressed as interest rate set in time t, for period beginning at time T1 = t+ τ1

and ending at T2 = t + τ2, i.e. τ2 > τ1. In order to ensure no arbitrage

possibilities on the market, following equation must be fulfilled:

(1 + rt(τ2))τ2 = (1 + rt(τ1))

τ1 (1 + ft(T1, T2))(τ2−τ1) (2.13)

ft(T1, T2) =

[(1 + rt(τ2))

τ2

(1 + rt(τ1))τ1

]τ2−τ1− 1 (2.14)

Similarly for continuous compounding:

eτ2rt(τ2) = eτ1rt(τ1)e(τ2−τ1)ft(T1,T2) (2.15)

ft(T1, T2) =τ2rt(τ2)− τ1rt(τ1)

τ2 − τ1(2.16)

Also for the forward rate, the instantaneous version can be defined as a rate

for an infinitely short period between T1 a T2:

ft(T1) = limT2→T1

ft(T1, T2) (2.17)

For T1 equal to t, the forward rate is identical to the spot rate. Since

both forward rates and bond prices (zero-coupon bonds with notional equal

to one currency unit) are given directly by the spot interest rates (and vice

versa), knowledge only one of these three sets of variables provides knowledge

of all of them. For this reason, focusing directly on the continuous compound-

ing (discrete-time compounding would provide equivalent form) and combining

equations 2.11 and 2.15, following relationships between forward rates and bond

prices can be expressed in terms of k forward rates (respectively k− 1 forward

2. Basic Definitions and Notations 9

rates and a spot rate):

Pt(τ) = e−[τ1ft(t,T1)+(τ2−τ1)ft(T1,T2)+...+(τ−τk−1)ft(Tk−1,Tk)] (2.18)

In case the k will grow infinitely for fixed τ , i.e. the length of the (Tj−1, Tj)

intervals will became infinitesimally small and all the forward rates in the Equa-

tion 2.18 will become instantaneous, the price of a bond can be expressed as:

Pt(τ) = e−∫ t+τt ft(s)ds (2.19)

2.2 Term Structure of Interest Rates

As has been described in the previous section, a price of a bond Pc,t(τ) is deter-

mined by the interaction of the bond demand, i.e. investors maximizing their

yield to maturity yytm, and the bond supply — fund seekers minimizing their

costs represented by a set of interest rates {rt(τi)}ni=1. However, an individual

subject does not influence the price significantly, as he or she can be assumed to

be a price-taker. From his point of view, the market prices are given, implying

both yields and interest rates of various maturities.

The term structure of interest rates is a function of rt(τ) with respect to

τ — the maturity. The interest rates of various maturities usually differ, and

the graphic representation of the term structure can consequently reach vari-

ous shapes - it can be upward-sloping, flat, downward-sloping, or even partly

upward- and partly downward-sloping. The theoretical background of various

shapes will be explained below.

Similarly to the term structure of interest rates, the yield curve can be

expressed as a function o yield (yytm) with respect to the maturity of the bond.

Generally, the yield curve and the term structure of interest rates are different:

a bond with a price Pc,t(τ) implies whole set {rt(τi)}ni=1 related to the cash flows

resulting from the bond, whereas the single yield for the investor is determined

directly. Consequently, the yield (and resulting yield curve) is also influenced

by the structure of the cash flows, and can be seen as a sort of average of the

situation over the whole term structure. For this reason, it is more suitable to

use the term structure of interest rates, since each interest rate is related to

single cash flow.

Both terms — the yield curve and the term structure of interest rates — are

similar only in two cases: when the interest rate is the same for all maturities

2. Basic Definitions and Notations 10

(both the term structure and the yield curve are absolutely flat), and when the

bonds used for its construction are zero-coupon bonds. The former condition is

purely theoretical, but the latter can be often met, since the zero-coupon bonds

are often used in this way. For this reason, the terms will be used equivalently

in further text, always assuming they refer to the term structure of interest

rates (or yields) constructed from the zero coupon bonds.

Yield Curve Theories

During the time, there were many attempts to offer a theoretical explanation for

the shapes of the term structure of interest rates. The most important theories,

examining the yield curve from different points of view, are the expectations

hypothesis, the liquidity preference hypothesis, the market segmentation hy-

pothesis and the preferred habitat hypothesis. Concise and brief description of

them can be found in Cox et al. (1985), which is followed also below:

The expectations hypothesis3 considers the current observed forward rates as

an unbiased estimator of the future spot rates. After plugging the Equation 2.19

into the Equation 2.11, it becomes obvious that the rt(τ) is an average of the

forward rates over the period until maturity τ . Consequently, the upward-

sloping term structure of interest rates is explained by the expected growth of

the (instantaneous) spot rates; similarly for the other possible shapes of the

yield curve. However, this explanation coincides with the empirical fact that

the yield curve is upward-sloping most of the time, which would provide sys-

tematic error to the expectations. Moreover, the expectation hypothesis does

not incorporate any difference in risk among various maturities (i.e. assumes

zero term premium). These facts imply that the forward rates cannot be an

unbiased estimator of the future spot rates under the real probability measure4,

and the pure expectations hypothesis is insufficient.

Basic principles of the liquidity preference hypothesis have been stated al-

ready in the work of Hicks (1946), who improved the expectations hypothesis

by the risk related to various maturities. Due to the risk aversion, the in-

vestors require a positive risk premium ξ as entering the Equation 2.1, which

makes the bond price relatively smaller. Consequently, as obvious from the

Equation 2.19, this is equivalent with the instantaneous forward rates being

3Various types of the expectation hypothesis are described for example in Malek (2005).4Nevertheless, the forward rates can be used as an estimate of the future spot rates

assuming we are in a risk-neutral world, e.g. the expected value is given under the risk-neutral measure.

2. Basic Definitions and Notations 11

relatively higher than the expected spot rates. Since the long-term bonds are

related to a relatively higher risk accepted by the investors, they demand a

higher risk premium. Because of this, the long-term yields are relatively higher

than the short-term, which sufficiently explains the prevailing upward slope of

the yield curve.

Different point of view offers the market segmentation hypothesis, mentioned

by Culberison (1957). It assumes that the investors on markets of bond of var-

ious maturities are strictly different, not moving between the markets. The

supply and demand for these bonds are therefore not related among the mar-

kets, and there is no reason for the yields to be equal. This hypothesis does

not directly explain, why the term structure of interest rates is usually upward-

sloping, however, it can offer an intuition why the interest rates for various

maturities can be distinctly different (which is useful especially at the times of

financial crises).

Finally, the preferred habitat hypothesis, introduced by Modigliani & Sutch

(1966), joins all the other theories together, using the positive aspect of each of

them. It is able to both explain the prevailing positive slope of the yield curve

and offer a reasoning for its different shapes. All the theories are, rather than

competing, together forming a complex view on the mechanisms underlying the

shape of the term structure of interest rates.

Term Structure Construction

An important issue related to the analysis of the term structure of interest

rates is its construction. Since the yield curve (as a continuous function of the

maturity) is not fully observed and there can be identified only a small number

(usually not more than 20) of points — yields of zero bonds of several maturities

— on the market, the problem has to be handled properly. It is necessary

to use mathematical and/or statistical techniques to fit these observed values

with a continuous function, preferably defined on (0,∞). The most common

approaches to the zero-bond yield curve construction, described into more detail

for example in Filipovic (2009), are:

Bootstrapping is based on the coupon bond prices observed on market, be-

ginning with a calculation of one-year interest rate rt(1) from one-year

(zero-coupon) bond. The rate is then inserted into the Equation 2.9 for

a two-year coupon bond, leaving the two-year interest rate rt(2) the only

unknown variable. The process is recursively repeated, obtaining interest

2. Basic Definitions and Notations 12

rates of higher maturities based on the knowledge of the rates of shorter

maturities. The approach is, however, producing an output which may

be biased, because the coupon-bond and zero-coupon-bond markets are

not perfect substitutes, particularly due to different cash-flows structure

resulting from the bonds. This restricts the bootstrapping to be used as

a theoretical tool rather than practical.

Interpolation can be considered as purely mathematical method. Using polyno-

mial interpolation, single polynomial function is used to fit all observed

maturities (poles), which may, however, offer unsatisfactory results par-

ticularly for both extremely short and long maturities. A different method

is the spline interpolation, which uses polynomials of lower orders on mul-

tiple sub-intervals. Most frequently used are either a cubic spline func-

tion, creating function continuous up to its second order, or a B-spline

interpolation, with splines constructed as a weighed sum of recursively

defined base-spline functions.

Nelson-Siegel approach, defined by Nelson & Siegel (1987) and sometimes used

in its extended version offered by Svensson (1994), is perhaps the most

frequently used method for the yield curve construction, mainly for its

relative simplicity. The approach is based on a specific functional form

including four parameters, which can be used for fitting the observed

yields. The method is described into detail in the Section 3.3, together

with the most common estimation technique.

Stochastic interest rates models represent distinctly different approach. Com-

pared to the static character of the previous methods, the interest rate

models try to capture dynamics if interest rates, typically focusing on the

short rate dynamics in continuous time. The model is first specified, and

a bond price is derived, defined as a function of the maturity and various

parameters (capturing dynamics of the latent factors, i.e. usually drift,

volatility and the mean-reversion level of the short rate). After the model

is calibrated on the observed bond prices, it can be used to price bonds

of any maturity, which is equivalent to the calculation of the entire term

structure (see the Equation 2.11). Stochastic models will be in the thesis

represented by an affine-class model, described in the Section 3.4

2. Basic Definitions and Notations 13

2.3 Term Structure Models

Purposes for Term Structure Modelling

To be able to describe and classify various models of the terms structure of

interest rates, it is first necessary to distinguish between two different general

motivations for the interest rates modelling, as each of them requires a different

approach:

1. Financial assets valuation. Time t value V (t) of any financial asset

(typically a financial derivative) can be determined as an expected value

of an uncertain future value V (T ) discounted to the present:

V (t) =EP [V (T )]

eτyreq(2.20)

where τ = T − t is the time to maturity of the asset and the P subscript

denotes the expectations under the real probability measure. It is difficult

to model yreq, since it is from its definition individual for each investor and

depends on particular instrument, maturity, time, market situation etc.

Moreover, the determination of the expected value EP [V (T )] is equally

demanding. For this reason, so-called risk-neutral valuation has been de-

veloped. This approach is built on an assumption, that the market is

arbitrage-free and complete, which ensures there exists a unique measure

(risk-neutral), equivalent to the original. Under this new measure, the

expected rate of return of assets is equal to the risk-free rate. Conse-

quently, instead of expressing the expected future value under the real

probability measure P and discounting by a risk-adjusted rate yreq, the

risk-neutral probability measure Q is used and the value of the instrument

is obtained as the expected future value under this risk-neutral measure

discounted simply by the risk-free rate, which is assumed to be equal to

the instantaneous interest rate rt.5

V (t) =EQ [V (T )]

eτrt(2.21)

Assuming the risk-free interest rate is not fixed, but floating over time,

5Relation of the original real-world and the equivalent risk-neutral measures is basedon Girsanov theorem and related use Radon-Nikodym derivative, which are described forexample in Musiela & Rutkowski (2005), and will be used also in the Section 3.4.

2. Basic Definitions and Notations 14

the Equation 2.21 can be generalized into the form:

V (t) = EQ

[V (T )

e∫ Tt rsds

](2.22)

More precisely, instead of using an abstract ”discount factor” approach,

it is better to talk about a so-called numeraire. Numeraire is an asset in

terms of which the values of other assets are computed. Typical example

of a numeraire is the money market account M(t), having at the time

t = 0 value M(0) = 1, which is accrued by the risk-free instantaneous

interest rate, using continuous compounding. The value of the money

market in time t > 0 is then:

M(t) = 1 ∗ e∫ t0 rsds (2.23)

Under the risk-neutral measure, the original asset V (t) expressed in terms

of the numeraire (i.e. discounted by the money market account, there-

fore called also as a discounted process) has to be a martingale. For this

reason, the term risk-neutral measure is sometimes replaced by a term

equivalent martingale measure. Utilizing properties of martingales, ex-

pected future value of the discounted process is equal to its present value

(still under the risk-neutral measure Q):

V (t)

e∫ t0 rsds

= EQ

[V (T )

e∫ T0 rsds

](2.24)

which is equivalent to the Equation 2.22.

Specifically for the bond, it is useful to utilize the fact that the value of

any bond at maturity is equal to its notional (i.e. V (T ) = P (T ) = 1 in

terms of relative price). In order to maintain consistency in the notation

throughout the thesis, the time t price of a zero-coupon bond maturing

at the time T = t+ τ , with τ standing for time to maturity of the bond,

will be henceforth noted Pt(τ). The Equation 2.22 then simplifies into

the form:

Pt(τ) = EQ

[e−

∫ t+τt rsds

](2.25)

Obviously, in case of bonds, the stochastic evolution of the instanta-

neous interest rate rt is the only variable to be modelled in order to

2. Basic Definitions and Notations 15

capture dynamics of bond prices. Through the relationship captured in

the Equation 2.11, the whole term structure can be simply derived from

the calculated bond prices of various maturities.

2. Portfolio management. The previous approach observes the actual sit-

uation on the market, according to it models the risk-neutral dynamics of

the interest rates, and determines the value of a derivative, a bond or the

term structure of interest rates. Contrary to it, modelling of interest rates

for portfolio management purposes is based on an analysis of the mar-

kets in the context of their historical development and, moreover, offers

predictions of the future development. Where the risk-neutral approach

considers the whole market as an arbitrage-free system, the portfolio ap-

proach focuses on individual financial assets and tries to determine, which

of them should be included into (or excluded from) the portfolio, in order

to maximize future value of the portfolio, or, respectively, to minimize loss

resulting from holding particular instruments. The portfolio management

requires an analysis of the real-world probability dynamics of the vari-

ables. Instead of calibrating the models on the actual data, an estimation

of the time series parameters, typically using autoreggresive models in-

cluding the Vector Autoregression (VAR), is a frequent approach to term

structure modelling under this motivation. Consequently, the continu-

ous dynamics is for the estimation purposes often replaced by a discrete

specification of the models.

Since the aim of the thesis is to model the real dynamics of the interest

rates, rather than to price financial assets, the latter motivation can be picked

as the crucial for the thesis.

Interest Rates Models Classification

In order to be able to evaluate the results of the performance comparison of the

models introduced in Chapter 3 correctly, it is necessary to classify the models

first. As points out Rudebusch (2008), the term structure of interest rates can

be generally modelled in three ways:

From the financial point of view, modelling the short rate as a function of latent

factors, and longer rates through an introduction of the risk premium.

2. Basic Definitions and Notations 16

Focusing on the macroeconomic relations only, which considers the short rate to

be a product of the macroeconomic dynamics, and the long rates to be

given by expectations of the short rates.6

Combination of both, which yields the macro-finance models.

Detailed classification of the models is outlined in the Table 2.1 and Ta-

ble 2.2, following De Pooter et al. (2007), Filipovic (2009), Witzany (2012),

Malek (2005) and Stork (2012). The classification already follows the fact that

the thesis is focused on capturing the real-world dynamics. The first family

of models, latent-factors-only models, is divided into two groups. Statistical

models7 capture the development of yields of various maturities without a di-

rect inclusion of relationships between various maturities, which is what the

no-arbitrage models focus on, employing the no-arbitrage condition, when ex-

pressing the longer rates in terms of the short rate.8

Short rate models, as a category within the no-arbitrage models, are try-

ing to capture the dynamics of the instantaneous interest rate, which is then

used to determine bond prices directly from the Equation 2.25. The short

rate dynamics is given specified as a function of several latent factors — state

variables. A frequent approach is to set the short rate itself as the only one

latent factor, whose dynamics is then given explicitly by a certain stochastic

differential equation. However, particularly for the purposes of the forecast-

ing, more then one factor approach is often used (usually two or three factors

are included). Moreover, for computational purposes, the functional form is

usually set as affine. An affine three-factor model is further described in the

Section 3.4. Second category within the no-arbitrage class are so-called term-

structure models, which focus on the forward rates, either instantaneous as uses

Heath-Jarrow-Morton Model (HJM) developed by Heath et al. (1992), or for a

given periodicity, as captures LIBOR Market Model (LMM) based on Brace

et al. (1997).

It is necessary to note, that the borders between the models classes are

not strict: Dynamic Nelson-Siegel approach has also its no-arbitrage version,

6Since these models are purely macroeconomic, not considering the interest rate as afinancial variable, they will not be further discussed.

7Represented by the dynamic Nelson-Siegel model introduced by Diebold & Li (2006) andfurther described in the Section 3.3.

8Sometimes, the no-arbitrage models are considered to be only a sub-group of the shortrate models, specific in their ability to fit the observed data perfectly, thanks to enough freeparameters. Such classification is meaningful for purposes of the risk-neutral calibration, butnot for capturing the real-world dynamics. For this reason, the no-arbitrage models will inthe thesis include all models utilizing the no-arbitrage conditions.

2. Basic Definitions and Notations 17

some of the models (for instance Ho & Lee 1986 or Hull & White 1990) can

be considered as part of either HJM framework or a as short rate model. How-

ever, the classification offered here still offers a view on the basic characteristic

properties of the models.

Table 2.1: Latent-Factors-Only Models

Group Category Type Example

Statistical Dynamic Nelson-Siegel

No-ArbitrageShort Rate

One-Factor Vasicek (1977)Multi-Factor Fong & Vasicek (1991)

Term StructureCont. Compound. HJM

Simple Compound. LMM

Source: author’s own

The second family of the models are the macro-finance models, which, in

contrast with the latent-factors-only models, explicitly include macroeconomic

variables when modelling the interest rates dynamics. Rudebusch (2008) rec-

ognizes three possible approaches to their construction:

1. First, following the work of Ang & Piazzesi (2003) as a cornerstone in this

field, an affine no-arbitrage latent-factors-only model in a discrete-time

specification is modified. This modification is made quite simply: the

vector containing the latent state variables, which is assumed to follow a

VAR process, is enriched by the observed macroeconomic variables.

2. Second, a Dynamic Stochastic General Equilibrium (DSGE) model serves

as basis. In this model, the stochastic discount factors is directly derived

from the households’ optimization problem. This group of models is

distinctly different from the others, since it uses purely macroeconomic

framework to derive values of financial variables, whereas in the all other

cases, the originally financial models are extended by the macroeconomic

variables.

3. Third, the dynamic Nelson-Siegel approach, as mentioned above, may be

utilized, as proposed by Diebold et al. (2006). The way of the macro-

variables inclusion is similar to the approach followed in the first point:

the vectors of macroeconomic and latent variables are merged to ensure

the joint dynamics within the VAR process.

2. Basic Definitions and Notations 18

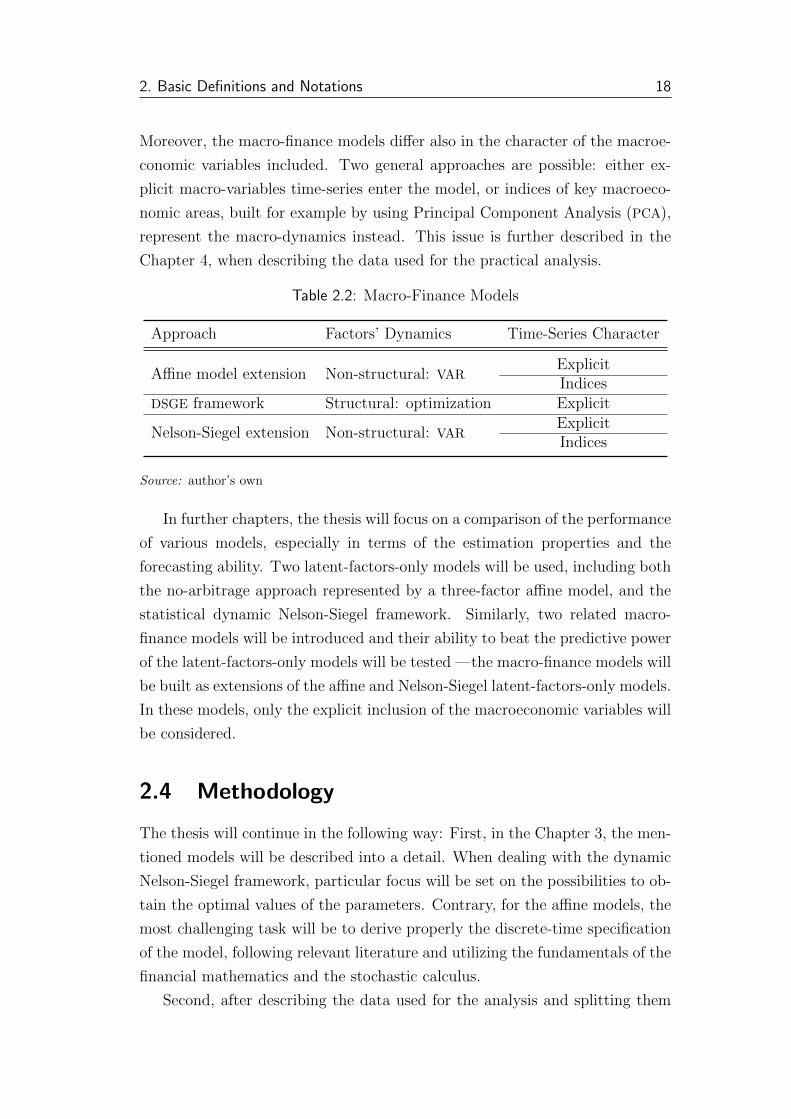

Moreover, the macro-finance models differ also in the character of the macroe-

conomic variables included. Two general approaches are possible: either ex-

plicit macro-variables time-series enter the model, or indices of key macroeco-

nomic areas, built for example by using Principal Component Analysis (PCA),

represent the macro-dynamics instead. This issue is further described in the

Chapter 4, when describing the data used for the practical analysis.

Table 2.2: Macro-Finance Models

Approach Factors’ Dynamics Time-Series Character

Affine model extension Non-structural: VARExplicitIndices

DSGE framework Structural: optimization Explicit

Nelson-Siegel extension Non-structural: VARExplicitIndices

Source: author’s own

In further chapters, the thesis will focus on a comparison of the performance

of various models, especially in terms of the estimation properties and the

forecasting ability. Two latent-factors-only models will be used, including both

the no-arbitrage approach represented by a three-factor affine model, and the

statistical dynamic Nelson-Siegel framework. Similarly, two related macro-

finance models will be introduced and their ability to beat the predictive power

of the latent-factors-only models will be tested —the macro-finance models will

be built as extensions of the affine and Nelson-Siegel latent-factors-only models.

In these models, only the explicit inclusion of the macroeconomic variables will

be considered.

2.4 Methodology

The thesis will continue in the following way: First, in the Chapter 3, the men-

tioned models will be described into a detail. When dealing with the dynamic

Nelson-Siegel framework, particular focus will be set on the possibilities to ob-

tain the optimal values of the parameters. Contrary, for the affine models, the

most challenging task will be to derive properly the discrete-time specification

of the model, following relevant literature and utilizing the fundamentals of the

financial mathematics and the stochastic calculus.

Second, after describing the data used for the analysis and splitting them

2. Basic Definitions and Notations 19

into training and testing samples, PCA will be used to reduce the dimensionality

of the yields. Afterwards, the models themselves will be estimated, using several

techniques:

� time series analysis, utilizing the Box & Jenkins (1970) methodology,

particularly the reduced-form VAR;

� Ordinary Least Squares (OLS) method;

� and numerical iterative methods.

Third, the estimations will be evaluated. The features of the estimations

themselves will be described, using Residual Sum of Squares (RSS) to compare

the models in terms of their ability to fit the observed values, and Impulse-

Response Function (IRF) to depict the qualitative properties of the estimations.

The estimations will be also used to construct predictions, and the forecasting

performance will be compared by calculating the total squared predictive error.

Finally, all the models will be re-estimated for a shorter data samples, and

the time development of the forecasting ability will be inspected. In this case,

the Root Mean Square Error (RMSE) will be used as the quantitative measure.

At the end, the results will be compared with outcomes of similar studies.

In the thesis, MATLAB and R-Studio are used when estimating the models

and producing the forecasts, as well as for construction of various charts.

Chapter 3

Description of Models

3.1 Factors and Principal Component Analysis

One of the biggest difficulties related to the yield curve modelling and fore-

casting seems to be the fact, that it is necessary to capture the dynamics of

many maturities (usually 10-15). This might be, due to the resulting over-

parametrization of a model, quite a problematic task. The common approach

is to model the dynamics of several latent (i.e. unobservable) factors, and de-

rive relations of the yields to these factors. For purposes of the financial assets

valuation, the task can be well simplified by calibrating a one-factor model,

typically Vasicek (1977) or Hull & White (1990) model. Since the dynamics

of rates of longer maturities are given by the no-arbitrage condition (applied

under a risk-neutral probability measure) in these cases, the model is able to

capture the dynamics using only one source of uncertainty – the short rate.

However, for purposes of a dynamic real-world analysis (as an opposite to

the risk-neutral pricing) and particularly forecasting, this approach might be

considered as inefficientRather than fitting the observed market situation, the

model should in this case also incorporate the exact relationship between the

yield curve shifts and changes of the factors driving these movements — since

various parts of the term structure have a different sensitivity to changes of

various underlying factors, it is necessary to allow multiple sources of the risk

to enter the models. It has been shown by Litterman & Scheinkman (1991)

that three factors are perfectly able to explain the dynamics of the whole yield

curve. The nature of these factors can be obtained by the PCA of yields, which

allows an elegant reduction of the dimension1 while setting a useful basis for

1It is implied directly by the nature of the PCA, that there does not exits any linear

3. Description of Models 21

building macro-finance models. The logic can be illustrated by the Figure 3.1.

Figure 3.1: Relationship of the Factors

Source: author’s own.

Representation of the entire yield curve by the three factors — principal

components (usually called Level, Slope and Curvature of the yield curve) —

can be considered as distinctively accurate. Litterman & Scheinkman (1991)

have shown that the three factors are able to explain more than 98% of the

total variance.2 The use of level, slope and curvature as the factors underlying

the yield curve movements is therefore beneficial in two ways:

� Only three variables are modelled, which solves the over-parametrization

problem.

� The new variables are tightly related to real macroeconomic and financial

factors driving the dynamics of the term structure.

The latter has been illustrated by Diebold & Li (2006), who have shown that

the level (the first component) is reflecting long-term inflation expectations,

whereas the slope (the second component) is connected to the real activity

and short-term inflation and growth expectations. The third component is

sometimes believed (Kollar 2011) to be related to the expectations of economic

growth and inflation in the medium time horizon.

Assuming the market is efficient, as defined by Fama (1970), market prices

(i.e. also bond yields ) should always capture all relevant available informa-

tion, including development of the macroeconomic variables. Consequently, for

purposes of the financial assets pricing, capturing dynamics of the latent fac-

tors (level, slope and curvature) is perfectly sufficient. However, such approach

does not include the particular relations of the macroeconomic variables and

transformation of the original variables incorporating more information (i.e. variance ofthe original data) than the first principal component, and a linear transformation with thetransformation vector orthogonal to the vector of the first transformation, which would beable to include more information than the second principal component, etc.

2A similar analysis will be performed also in the practical part of the thesis.

3. Description of Models 22

the term structure of interest rates. This can be a shortcoming for economic

subjects — typically central banks or governments — assessing an impact of

particular monetary or fiscal policy steps on the interest rates of various ma-

turities. This is where the macro-finance models are particularly useful, when

adding the macroeconomic variables directly into the models - their explicit

inclusion allows a simple analysis of the impact of monetary (or fiscal) policy

steps on the interest rates and its further propagation into the whole economy.

The difference between the latent-factors-only and the macro-finance models is

depicted by the Figure 3.2.

Figure 3.2: Inclusion of the Factors in the Models

Source: author’s own.

Four different models will be introduced in the following text, focusing on

their nature, derivation and an approach to their estimation and construction

of predictions.

Random walk will serve as a simple baseline, which the other models will be

assumed to outperform.

Dynamic Nelson-Siegel model, i.e. a model based on a specific utilization of the

Nelson-Siegel framework, will be estimated in two ways:

1. A simple dynamic version of the Nelson-Siegel representation of the

yield curve, including only the latent variables.

2. A macro-finance model explicitly including macro-variables into the

vector of factors driving the movements of the term structure of

interest rates.

Affine model, based on the no-arbitrage assumption, will be also built in two

forms, following the same logic:

1. An affine model including the three latent factors only.

3. Description of Models 23

2. And again its macro-finance extension with macro-variables included

in the vector of the factors — state variables.

3.2 Random Walk

To be able to assess the performance of both latent-factors-only and macro-

finance models, it is necessary to introduce a simple model serving as a baseline.

The yields of most maturities can be regarded as nonstationary, as will be shown

in the Section 4.1. For this reason, a random walk could be regarded as the most

simple baseline. Moreover, considering the random walk as a process the prices

are assumed to follow under the efficient market hypothesis (in compliance with

Fama 1965), testing the ability of other models to outperform the random walk

will implicitly create a naıve test of the market efficiency itself.3

The random walk (without a constant) can be written as:

rt (τ) = rt−1 (τ) + at,τ (3.1)

where at,τ represents a white noise process, i.e.

E [at,τ ] = 0

var [at,τ ] = σ2a,τ

cov [at,τ , as,τ ] = 0 for s 6= t

Predictions resulting from the random walk are very simple to obtain - they

are equal to the latest observation:

E [rt+1 (τ)] = E [rt (τ)] + E [at+1,τ ] = rt (τ) (3.2)

3.3 Dynamic Nelson-Siegel Approach

Basic Description

A pivotal work in this area is Diebold & Li (2006). Authors try to react on poor

results of no-arbitrage models in terms of predictive performance, assuming that

3It is, however, necessary to note, that the author is not aiming at proving or refusing thehypotheses of Eugene Fama, which are definitely going far behind the extent of the thesis.

3. Description of Models 24

leaving the no-arbitrage restrictions (used in the Section 3.4 when constructing

the affine model) may lead to more accurate forecasts.

The first step to take when building the model is to describe the basic

Nelson-Siegel framework, based on the work of Nelson & Siegel (1987). Authors

offered a statistical approach to the estimation of the term structure of interest

rates, which quickly became popular, mainly for its relative simplicity. The

main building block of the framework is a representation of the yield curve as

a function of the maturity in the following form:

r (τ) = β1 + β2

(1− e−λτ

λτ

)+ β3

(1− e−λτ

λτ− e−λτ

)(3.3)

where τ = T − t represents the time to maturity and β1, β2, β3 and λ are the

parameters to be estimated. Later, the Equation 3.3 was extended by Svensson

(1994), including an extra term to enhance the flexibility of the function when

fitting the term structure; however, the original form is often considered to be

flexible enough, which will be assumed also henceforth. The resulting estimated

term structure does not fit the observed values exactly — consequently the

bond prices implied by the Nelson-Siegel estimation may slightly deviate from

the observed ones. However, the specific exponential form of the function as

defined by the Equation 3.3 ensures substantial flexibility, which makes the

approach attractive.4

The three indexed beta parameters are of a special interest,5 since they can

be (and often are) considered as representatives of the main characteristics of

the term structure of interest rates — the latent factors:

� β1 is common for all maturities, so it represents the level of the term

structure.

� The expression directly following β2 (i.e. its factor loading) is decreasing

with growing maturity (approaching 1 with the maturity decreasing to

0, respectively going to 0 with the maturity approaching +∞), assuming

λ is positive. Positive β2 therefore implies short maturities being bigger

than the long ones and vice versa — and β2 can be therefore interpreted

as a negative slope of the term structure. The development of the β2

4Compared to the restricted ability of Vasicek (1977) or Cox et al. (1985) models to fitthe observed term structure of interest rates (Malek 2005).

5Whereas λ is set in order to ensure either an optimal shape of the yield curve or the bestfit of the original and model-implied yields, as will be described below.

3. Description of Models 25

factor loading, for maturities between 0 and 15 and various values of

lambdλ a, is outlined by the Figure 3.3

Figure 3.3: Slope - Factor Loading for Various λ Values

0 1 2 5 10 20 30

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

maturity

fact

or lo

adin

g

0.10.20.512510100

Source: author’s own.

� The β3 factor loading is positive for positive λ and approaches zero for

maturities reaching either 0 or +∞. The maturity, for which the factor

loading is in its maximum, depends on the value of λ: with growing λ,

the maturity in which the maximum is obtained is decreasing. Conse-

quently, the third expression can be considered as a location of a ”hump”

in the term structure, whereas the β3 itself represents extent of the cur-

vatures. Setting the λ positive, yields of medium maturities will be rel-

atively higher than the short or long rates. Possible values of the factor

loading are illustrated by the Figure 3.4.

The interpretation of the β parameters is very close to the interpretation

of the first three principal components of the yield curve, as explained above.

Nelson-Siegel parametrization consequently offers an elegant and simple ap-

proach how to use the benefits of the Litterman & Scheinkman (1991) findings

in practice. The favourable properties of the Nelson-Siegel representation con-

firm also Diebold & Li (2006), when noting that this approach keeps the key

properties of the term structure, mostly in terms of implied forward rates and

the ability to fit well many possible shapes of the yield curve observed at the

market.

When fitting the yield curve on the observed data, one of the frequent

approaches is to estimate separately the β parameters, using OLS and assuming

3. Description of Models 26

Figure 3.4: Curvature - Factor Loading for Various λ Values

0 1 2 5 10 20 30−0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

maturity

fact

or lo

adin

g

0.10.20.512510100

Source: author’s own.

the λ parameter to be fixed, then evaluate the accuracy of the fit, and find such

a λ maximizing the accuracy (can be measured by R-square of the OLS or by

the information criterion of the model).

Dynamic Version and Macro-Finance Extension

Diebold & Li (2006) introduced a new view on the Nelson-Siegel function.

Considering the β parameters as time-varying latent factors, the dynamics of

the yield curve can be derived from the dynamics of these latent factors. The

model is described by two equations (Diebold et al. 2006):

rt (τ) = β1,t + β2,t

(1− e−λτ

λτ

)+ β3,t

(1− e−λτ

λτ− e−λτ

)+ εr,t (τ) (3.4)

βt = α+ Γβt−1 + εβ,t (3.5)

where βt is a 3× 1 vector consisting of βt,1, βt,2 and βt,3; the scalar error terms

of the yields εr,t (τ) are forming a m × 1 vector error term εr,t (where m is

number of maturities τ in the sample), which is believed to follow N (0,Σr)

distribution with Σr being a m ×m covariance matrix; εβ,t is a 3 × 1 vector

error term related to the stochastic process of βt, assumed to follow aN (0,Σβ)

distribution (with Σβ of a dimension 3 × 3), and α and Γ are a 3 × 1 vector,

respectively a 3× 3 matrix of parameters.

The Equation 3.5 is simply a representation of a three-dimensional VAR

process with one lag, which can be considered as the most simple way how to

3. Description of Models 27

capture the development of βt, and will be used also in the thesis. One benefit of

the VAR model used in the Equation 3.5 is that the construction of the resulting

macro-finance model is very simple. The 3 × 1 vector of latent variables βt

including the latent factors level, slope and curvature can be enriched by a k-

dimensional vector θt including k macroeconomic variables, to form a (3 + k)×1

vector (henceforth denoted ηt). The original three-dimensional VAR process

will be modified into a (3+k)-dimensional (following Diebold et al. 2006):

[βt

θt

]= µ+ Φ

[βt−1

θt−1

]+ εη,t (3.6)

ηt = µ+ Φηt−1 + εη,t (3.7)

where µ, Φ and εη,t are similar to α, Γ and εβ,t, differing only in their dimen-

sions.

The macro-variables included in the vector θ do not influence the yields

directly (i.e. they are not included in the Equation 3.4), but only through

the impact on the development of the latent β factors, which then govern the

yields themselves. The macroeconomic variables are considered as exogenous,

and the macro-finance relationship is therefore only one-sided6, lacking the

reverse causality in the direction from the interest rates to the macroeconomic

variables. This simplification can reduce the performance of the model, as

a consequence of an omission of some transition channels, nevertheless the

simplicity of resulting model can be beneficial in terms of a robustness and a

good estimation performance, especially when focusing on the predictive power.

Estimation and Forecasting

Diebold & Li (2006), or similarly Kollar (2011) for the Czech yield curve,

proceed in the following way: First, for each period, the Nelson-Siegel function

is fitted on the observed maturities — i.e. the parameters of the Equation 3.4

are estimated for each period separately; β coefficients are allowed to vary,

whereas λ is kept fixed. Afterwards, the estimated β parameters, representing

the latent factors — level, slope and curvature — enter the model capturing

their dynamics: a reduced-form VAR model defined in the Equation 3.5 is

estimated, using a least-squares method. After an evaluation of the error term

6Which will be followed also in all other models included in the thesis

3. Description of Models 28

of the model in terms of diagnostic tests, properties of the estimated model can

be analysed, typically using IRF, to comment on the dynamics implied by the

model.

Different approach present Diebold et al. (2006), using the very nature of

the described model — it is a typical representative of a State-Space model

in the most basic form. Observed values are determined by unobservable (la-

tent) factors, which are following VAR(1) process. Following the methodology

of these models (for example in Pichler 2007), the Equation 3.4 can be called a

measurement equation, since it represents the process how the latent factors are

related to the measurable variables (yields); consequently, εr,t is a measurement

error. The Equation 3.5 is a state (transition) equation, which describes be-

havior of the latent variables, and includes the state equation errors εβ,t. Since

the relationship is linear, the two steps can be jointly estimated by Kalman

filter (Kalman 1960), which is a special method for constructing and using the

likelihood function in the State-Space models framework, even when the least

squares methods are not applicable (Pichler 2007).

The macro-finance extension is then constructed rather easily. The β pa-

rameters enter the Equation 3.6 instead of the original one, regardless to which

of the two approaches to the estimation is used - no change of the estimation

methods is necessary. A shock into a macroeconomic variable (either external

or resulting from a policy-making process) is directly (with a one-period lag)

propagated into the other macroeconomic variables and simultaneously into

the latent factors, which can be well depicted by the IRF. The latent factors

then directly determine the new shape of the yield curve.

After the models are estimated, the forecasts can be constructed by step-by-

step iterating the β (or η in the macro-finance model) vector through the transi-

tion equation 3.5 (respectively 3.7), utilizing the fact that E [εβ,t] = E [εη,t] = 0.

The forecasts of the yields themselves then result from the measure Equa-

tion 3.4.

It is useful to describe, returning to the start of the estimation, how to

obtain the fixed λ parameter. Since the parameter determines the maturity in

which the curvature factor is maximal (see Figure 3.4), Diebold & Li (2006)

simply argue the optimal λ should ensure the largest curvature for maturities

2-3 years, which are, according to the authors, the most appropriate from the

empirical point of view. More specifically, the authors find such a λ maximizing

the curvatureβ3 factor loading for 30 months maturity.

However, because the data scope analysed in the thesis includes quite vari-

3. Description of Models 29

able shapes of the yield curve (particularly after the 2009 crisis), as well as

a different ”hump” location for different periods, the approach to set λ as

mentioned above could be considered as unreasonable. Instead, λ may be de-

termined so that it ensures an optimal fit of estimated and observed values.

The procedure can be described in the following way:

1. An arbitrary λ1 is chosen.

2. For each period t, the β vector is obtained by a simple OLS method, using

the maturities in the given period as the observations:

βt =(XTX

)−1XTrt (3.8)

where:

βt =

β1,t

β2,t

β3,t

,

rt =

rt (τ1)

rt (τ2)...

rt (τm)

,

X =

1 1−e−λ1τ1

λ1τ11−e−λ1τ1

λ1τ1− e−λ1τ1

1 1−e−λ1τ2

λ1τ21−e−λ1τ2

λ12− e−λ1τ2

......

...

1 1−e−λ1τm

λ1τm1−e−λ1τm

λ1τm− e−λ1τm

with m = number of maturities in the sample.

3. Then, the difference between the estimated and observed values (residuals

et) is calculated as:

et = rt − rt = rt −Xβt (3.9)

4. Finally, returning to λ, the numerical methods are used to find its optimal

value, i.e. minimizing the residual sum of squares (RSS) over all periods:

minλ

n∑t=1

etTet (3.10)

where n is the number of the periods included in the sample.

3. Description of Models 30

To conclude, there will be multiple models belonging to the dynamic Nelson-

Siegel family estimated in the Section 4.3, and their results will be compared.

The different approaches are captured by the Table 3.1.

Table 3.1: Dynamic Nelson-Siegel Models

model name type λ setting