Turkish Economy at Slides…

36

Turkish Economy at 35.5 Slides… Evaluation of 1H2014, Expectations for FY2014 & FY2015 'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR 1

Transcript of Turkish Economy at Slides…

Turkish Economy at 35.5 Slides…

Evaluation of 1H2014, Expectations for FY2014 & FY2015

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

1

» Investing in Turkey is like dating Don Juan…plenty of reasons for being attracted

(some irrational) but never a relief of confidence

» Alas, this will continue being the case in the period ahead

» If you are one of those who doesn't want to ‘lose the excitement in a

relationship’, then skip this report! For rather more ‘true love’ seekers (risk

conscious and realistic investors), the story I will tell will be addressing the risks

» In a nutshell I will tell you that: Conditions in the global economy will set to

change in the period ahead. But that is given for any given EM market. Thus

nothing we can change or control, but just have to live with. What will

differentiate a country in the period ahead will be its macro fundamentals and

political landscape. Turkey has low grades in both of the aforementioned fields,

with no short term structural improvement in the pipeline. But these

weaknesses are not the fruit of one day. So don’t blame FED, don’t blame

lobbies etc. Where we came is a part of the direction we took!

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

2

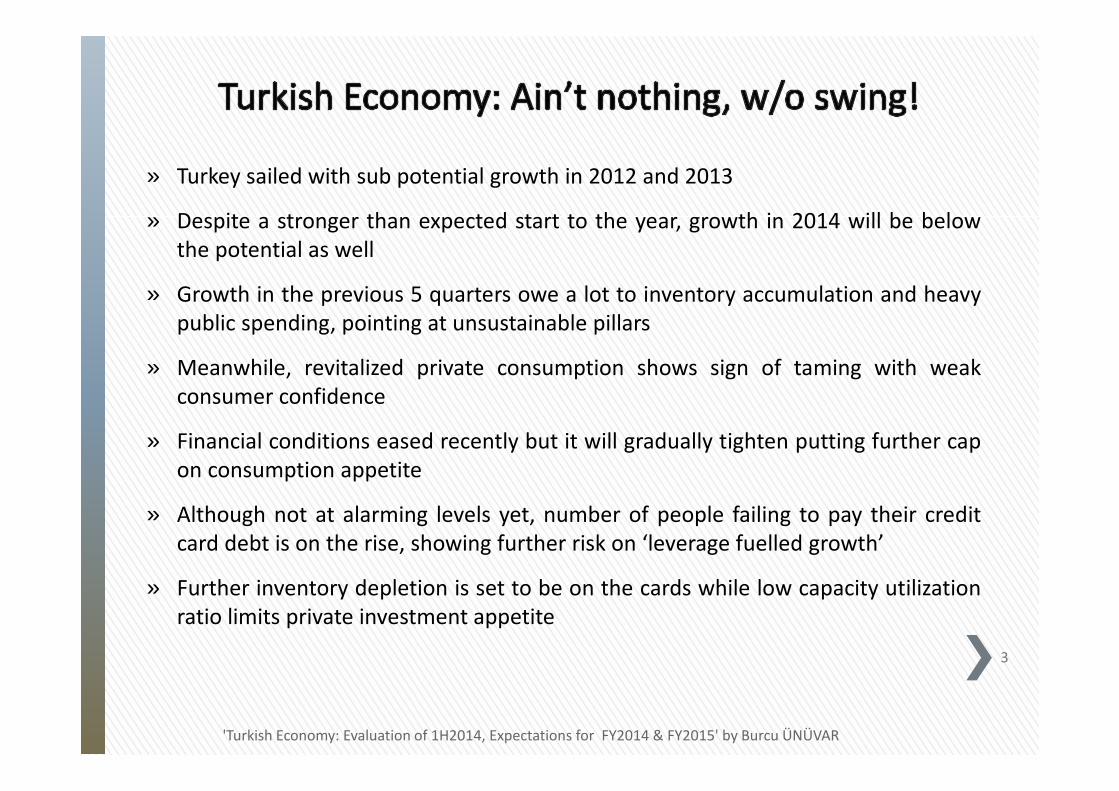

» Turkey sailed with sub potential growth in 2012 and 2013

» Despite a stronger than expected start to the year, growth in 2014 will be belowthe potential as well

» Growth in the previous 5 quarters owe a lot to inventory accumulation and heavypublic spending, pointing at unsustainable pillars

» Meanwhile, revitalized private consumption shows sign of taming with weakconsumer confidence

» Financial conditions eased recently but it will gradually tighten putting further capon consumption appetite

» Although not at alarming levels yet, number of people failing to pay their creditcard debt is on the rise, showing further risk on ‘leverage fuelled growth’

» Further inventory depletion is set to be on the cards while low capacity utilizationratio limits private investment appetite

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

3

» Regular machinery renewals due, might create some action on the privateinvestment but it will not be aiming at expanding the capacity

» Public spending has already been on the stage since late 2012. With generalelections to come within coming 12 months (early elections also possible) more tocome on the public spending front

» Yet due to the relatively limited share of public spending in GDP compared toprivate spending, boosting the public spending can create only a rather limitedand temporary impact on the GDP…

» …but, it definitely carries the risk of hurting the fiscal front and inflation…a storywe will hear more often in 2015

» Europe’s recovery is still a day dream, while some of its members are strugglingwith recession as well as signs of stagnation

» Never-coming European recovery is good news on one hand for saving further richliquidity stance…

» …but it is also bad news for Turkey which expects to compensate weak domesticdemand and weak export demand of Eastern neighbors' by the European demand

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

4

» Although there is some rebalancing in the economy, it will not be enough todeliver a permanent improvement on the current account front

» Needless to say, exports will not be enough to elevate Turkey’s growth back to itspotential levels

» Weaker aggregate demand conditions will limit the pricing power of theproducers’ in 2015

» Yet, TL volatility and higher administrated prices are set to hurt the price settingdynamics. CBRT will not hit the inflation target in neither 2014 nor 2015

» Meanwhile, premature rate cuts of the Bank threatens the stability of themonetary policy outlook

» Taking her lessons from Bernanke’s 2013 August actions, I expect Yellen to besilent before her actions. Tightening will be gradual including indirect means

» Within this framework, EM countries with artificially low rates will be forced tocompensate their mistakes with behind the curve sharp rate hikes. One relief:CBRT is experienced in being behind the curve, that is almost the standard!

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

5

» GROWTH DYNAMICS

» INDUSTRIAL PRODUCTION OUTLOOK

» LEADING INDICATORS

» FOREIGN TRADE DYNAMICS

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

6

» 2014 kicked off with a 4.3% of growth YoY in 1Q2014, which was clearly too highcompared to my initial projections

» Following a volatile pattern, growth outlook sets to decline in the period ahead

» Data in hand suggest that FY2014 GDP growth will be around 3.3% higher than

my initial base case of 2.8% but lower than my best case of 4% (See previousreport: Something Happened On the Way to Tapering, December 2013)

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

7

Source: TurkStat

-15.0

-10.0

-5.0

0.0

5.0

10.0

15.0

1Q20

06

3Q20

06

1Q20

07

3Q20

07

1Q20

08

3Q20

08

1Q20

09

3Q20

09

1Q20

10

3Q20

10

1Q20

11

3Q20

11

1Q20

12

3Q20

12

1Q20

13

3Q20

13

1Q20

14

YoY GDP growth %, off calendar effect

• Turkey’s growth has not been a pre-planned one. Manufacturing growth has beenvolatile-weak while construction sector has been on the rise

• While the whole country looks like a construction yard, share of education in the

GDP fell compared to a decade ago, showing the ‘infertile investment taste’

• Current growth model creates temporary jobs for less educated part of theworkforce but stands very vulnerable to bubbles and financial shocks

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

8

Source: TurkStat

-5.5

-0.6

2.1

4.1

-8

-6

-4

-2

0

2

4

6

Agriculture Industry Construction Services

Change in the Share of the Sectors WithinEmployment, % Point, 2013-2004

Source: TurkStat

1.8%

1.9%

2.0%

2.1%

2.2%

2.3%

2.4%

2.5%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%19

98

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Share of Construction in GDP

Share of Education in GDP (r.a.)

• Despite sailing higher than my call in the first five months of the year, slow-downsignals in the manufacturing industry became more visible as of June

• Following the first quarter GDP growth of 4.3% YoY, data in hand suggest a GDP

growth of some 2.5% YoY in 2Q2014

• A slight recovery might come in 3Q2014 only to be followed by furtherdeterioration in 4Q2014

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

9

Source: TurkStat

-30-25-20-15-10

-505

10152025

2006

Q1

2006

Q3

2007

Q1

2007

Q3

2008

Q1

2008

Q3

2009

Q1

2009

Q3

2010

Q1

2010

Q3

2011

Q1

2011

Q3

2012

Q1

2012

Q3

2013

Q1

2013

Q3

2014

Q1

Quarterly Manufacturing Growth, YoY %Change

Quarterly GDP Growth, YoY % Change

• After delivering positive contribution to GDP growth for 4 consecutive quarters,we saw a limited inventory depletion in 1Q2014

• Weak consumer confidence hints that, weaker demand to come shall be met viafurther inventory depletion rather than new production, which will cast its shadowover the growth in the short term

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

10

Source: TurkStatSource: TurkStat

-4

-2

0

2

4

6

8

10

2010

-I

2010

-II

201

0-III

2010

-IV

2011

-I

2011

-II

201

1-III

2011

-IV

2012

-I

2012

-II

201

2-III

2012

-IV

2013

-I

2013

-II

201

3-III

2013

-IV

2014

-I

Contribution of Inventory to GDP, % point

68

70

72

74

76

78

80

1 2 3 4 5 6 7 8 9 10 11 12

Consumer Confidence Index 2013 2014

months

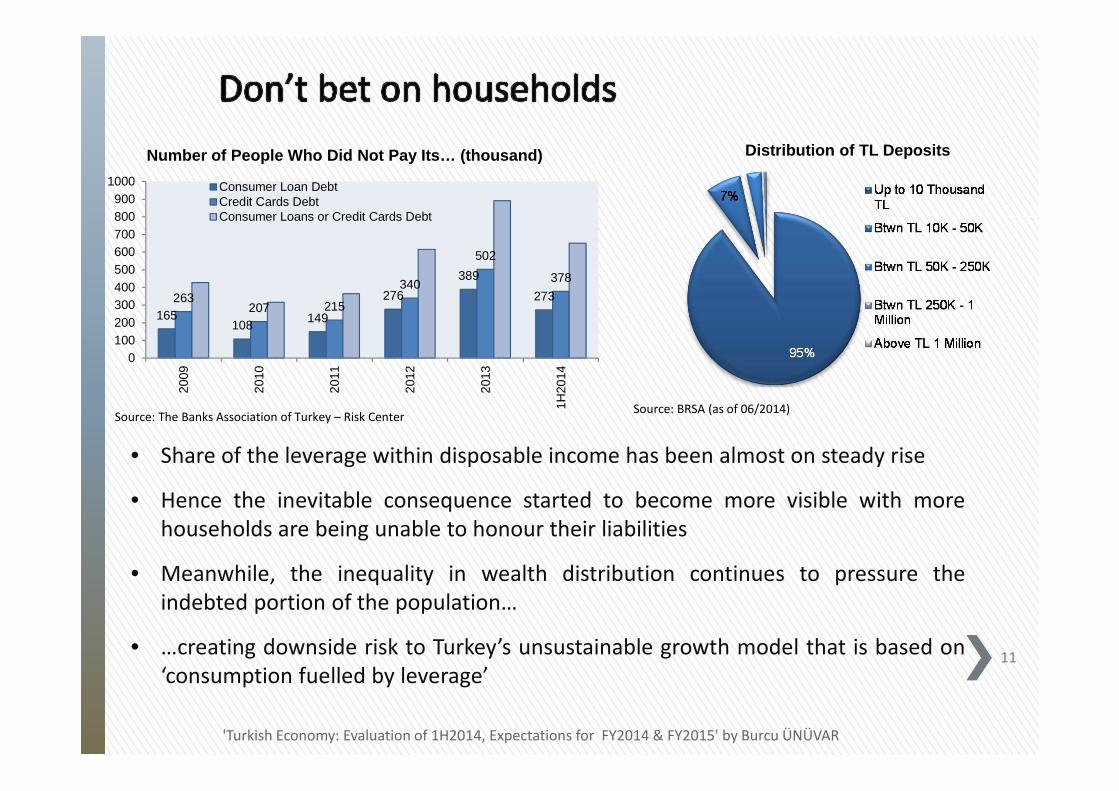

• Share of the leverage within disposable income has been almost on steady rise

• Hence the inevitable consequence started to become more visible with morehouseholds are being unable to honour their liabilities

• Meanwhile, the inequality in wealth distribution continues to pressure theindebted portion of the population…

• …creating downside risk to Turkey’s unsustainable growth model that is based on‘consumption fuelled by leverage’

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

11

Source: The Banks Association of Turkey – Risk Center

Number of People Who Did Not Pay Its… (thousand)

165108 149

276

389

273263207 215

340

502

378

0100200300400500600700800900

100020

09

2010

2011

2012

2013

1H20

14

Consumer Loan DebtCredit Cards DebtConsumer Loans or Credit Cards Debt

Distribution of TL Deposits

Source: BRSA (as of 06/2014)

• Real Sector Confidence Index shows that private investment appetite will betamed in the coming 12 months as well…

• …casting its shadow over the contribution of private investment to GDP growth in2015

• Yet given the high inventory and weak consumer confidence, I guess no one issurprised (or not that many)

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

12

Source: CBRT, TurkStat

-50

-30

-10

10

30

50

70

-50

-40

-30

-20

-10

0

10

20

200

7Q

1

200

7Q

3

200

8Q

1

200

8Q

3

200

9Q

1

200

9Q

3

201

0Q

1

201

0Q

3

201

1Q

1

201

1Q

3

201

2Q

1

201

2Q

3

1Q

201

3

3Q

201

3

1Q

201

4

3Q

201

4

12M Ahead Investment Expenditures (RSCIIndex)Real Private Investment Growth (YoY, %,r.a.)

• Despite losing some steam,adjusted time series showsthat public spending is still onthe table

• Public consumption rose by4.4% QoQ (adjusted series) in1Q2014

• Meanwhile public investmentrose by 5.6% QoQ (adjustedseries) in 1Q2014 vs privateinvestment that fell by 2.8%QoQ (adj.)

• Can public demandcompensate the weakening ofprivate demand? Can NOT!

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

13

Source: TurkStat *Data adjusted for seasonality and calendar effect

Source: TurkStat *Data adjusted for seasonality and calendar effect

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

1Q20

10

2Q20

10

3Q20

10

4Q20

10

1Q20

11

2Q20

11

3Q20

11

4Q20

11

1Q20

12

2Q20

12

3Q20

12

4Q20

12

1Q20

13

2Q20

13

3Q20

13

4Q20

13

1Q20

14

Public Consumption, QoQ % Chng* (l.a.)

Household Spending, QoQ % Chng.*

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

1Q20

10

2Q20

10

3Q20

10

4Q20

10

1Q20

11

2Q20

11

3Q20

11

4Q20

11

1Q20

12

2Q20

12

3Q20

12

4Q20

12

1Q20

13

2Q20

13

3Q20

13

4Q20

13

1Q20

14

Public Investment, QoQ % Chng.*

Private Investment, QoQ % Chng.*

• One shall remember that the share of public spending (consumption + investment)in GDP is limited at roughly 15-16%

• Said in another way, private spending adds the lion’s share to the GDP

• Due to its rather limited share in Turkey’s GDP pie, one shall conclude that raising

the public spending can NOT save the growth stand alone but it will for sure risk

the fiscal front as well as the inflation outlook

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

14

Source: TurkStat

0%

20%

40%

60%

80%

100%

120%

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Share of Private Spending in GDP

Source: TurkStat

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2012

-I

2012

-II

2012

-III

2012

-IV

2013

-I

2013

-II

2013

-III

2013

-IV

2014

-I

PrivateInvestment

Public Investment

Contribution to GDP, % Point

• Net exports added 2.7 pp to the headline GDP growth in 1Q2014 vs 2.1 ppcontribution of private consumption of the households, pointing at rebalancing

• While weak consumer confidence points at a slow-down in the HH consumption,recovery in European growth is expected to serve as a buffer to compensate theweakness

• Yet, I shall warn you: Stronger European demand might ease the pain but it will

NOT be the panacea against sub-potential growth

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

15

Source: TurkStat, Author’s Own Calculations

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

201

0-I

201

0-I

I

201

0-I

II

201

0-I

V

201

1-I

201

1-I

I

201

1-I

II

201

1-I

V

201

2-I

201

2-I

I

201

2-I

II

201

2-I

V

201

3-I

201

3-I

I

201

3-I

II

201

3-I

V

201

4-I

Net Exports, % Point Contribution to GDP

Private Consumption, % Point Contribution to GDP

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

16

Source: TurkStat, Author’s Own Calculations

• Unexpected gold trade in the recent years distorted the trade picture of thecountry

• Focusing on the exports excluding gold – which is more meaningful for the GDPcontribution – one shall see that, share of Europe has been in fact more or lessstabilized

• Said in another way, when gold exports are excluded, the recent rise in Europe’sshare within Turkey’s total export pie stands rather limited…

• …thus, not big enough to compensate the growth loss that shall come from theexpected deterioration in private demand

1H2014 1H2013 YoY Diff.

Near & Middle East 21.4% 20.8% 0.7%

EU28 + Other Europe 53.8% 52.0% 1.8%

Near & Middle East 22.2% 24.0% -1.8%

EU28 + Other Europe 53.8% 49.6% 4.3%

Excluding the Export of Precious Metals

Including the Export of Precious Metals

% Share In Total Exports

• European recovery continues to be a day dream

• When we go rather detailed in the data, we see that our trading partners’ growthprojections are being revised downward (Germany contraction, Italy recession,France stagnation wow wow wow!)…

• …pointing at negative divergence and risking the upside potential of theirexpected contribution to Turkey’s export demand (ja, naturlich!)

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

17

Countries 1H2014 2013 2012 2014 2015Germany 1 1 1 0.2 0.1Iraq 2 2 2 n.a. n.a.UK 3 3 4 0.4 0.2Italy 4 5 7 -0.3 0.0France 5 6 8 -0.3 -0.1USA 6 7 9 -1.1 0.1Russia 7 4 10 -1.1 -1.3

Revision in IMF's Growth Call July vs April, % Point

Rank in Turkey's Export Markets

Source: TurkStat, IMF

• Private sector companies signal for falling competitiveness in countries bothwithin and outside EU

• Latest reading of the graph might have been heavily influenced by the recentpolitical tension with both Western and Eastern neighbors and might tame a bit.But since political tension is not set to decline in the ST, a recovery is not realistic

• Meanwhile low value added export goods of Turkey are open to increasingcompetitive pressure, being another factor to cast shadow over exports’contribution

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

18

Source: CBRT

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

04-1

205

-12

06-1

207

-12

08-1

209

-12

10-1

211

-12

12-1

201

-13

02-1

303

-13

04-1

305

-13

06-1

307

-13

08-1

309

-13

10-1

311

-13

12-1

301

-14

02-1

403

-14

04-1

405

-14

06-1

407

-14

Countries Within EU

Countries Outside EU

Competitive Power - Balance

Sour - 2015 Sweet and Sour - 2015

» Annual GDP growth: 2.7%

» Budget Deficit / GDP: 2.6%

» Primary Balance / GDP: 0.3%

» Story:

Private spending tames whilepublic spending stands positivebut under control. Ambiguity onthe political front continues butdoes not turn into a full-fledgedcrisis. Then the drive will beshaky but manageable.

» Annual GDP growth:1.5%

» Budget Deficit / GDP: 3.2%

» Primary Balance / GDP: -0.5%

» Story:

Domestic political tension risesdelivering instability, whileterror in southern neighbourscontinue. In that case Turkeycan not differentiate in FED’snormalization period and stepsahead as the weak chain of theEM

» Annual GDP growth: 4%

» Budget Deficit / GDP: 2.2%

» Primary Balance / GDP: 0.5%

» Story:

Harmony between Presidentialoffice and the ruling partysupport the stability attractingexternal savings to the countrydespite FED’s normalizationsteps

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

19

Sweet -2015

» BALANCE of PAYMENTS

» CURRENT ACCOUNT BALANCE

» REAL EFFECTIVE EXCHANGE RATE

20

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

• Rebalancing in 1Q2014 helped to improve the CAD outlook, with the deficitstepping back by USD 12.9 bn in 1H2014 compared to 1H2013

• Meanwhile, 1H2014 portfolio investment is also down by USD 15 bn YoY

• Hence the picture in hand shows lower CAD but also weaker financing

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

21

Source: CBRT

12,934

-14,943-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

Current Account Deficit Portfolio Investments (net) (selected items)

1H2014 - 1H2013, USD mn

• Private sector is the fat boy of Turkey’s balance of payments picture, while itsstrong roll-over ability serves as a limited relief

• Savings that fell short of the investment need of the country pushes externalborrowing almost as the mandatory way to finance private investment

• Yet, recent data in hand challenges the generally accepted rhetoric of ‘growthcreating leverage’ (see above graph on the right)

• So it is time to question the efficiency of borrowing-investment relationship andpossible course of private sector roll-over

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

22

Source: CBRT, BRSA, Undersecretariat of Treasury

-200000-150000-100000-50000

050000

100000150000200000250000

Hou

seho

lds

CB

RT

Ba

nks

Pu

blic

Se

ctor

Non

Ba

nkin

gP

riva

te S

ecto

r

May.14 May.13

0

100

200

300

400

500

600

700

800

900

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

1Q

201

4-

An

n.

Private Sector Investment, Current Prices, Reindexed

2002=100Private Sector FX Liabilities

Private Investment, Fixed Prices, Reindexed 2002=100

Source: CBRT, TurkStat

Short FX Position, USD mn

• Normalization steps in FED’s policy will tame the appetite of the global capital but one shall not expect to see a dry-up

• As global liquidity becomes more selective, domestic pull side factors will be more important for each country

• Turkey has a loaded risk agenda with external political tension, domestic political tension, possible early elections, low growth and high inflation

• Since we are not exactly the ‘best candidate’, portfolio inflows will ease and roll-over performance of the private sector and banking sector will moderate

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

23

Source: CBRT

0%

100%

200%

300%

400%

500%

600%

700%

01-0

4

06-0

4

11-0

4

04-0

5

09-0

5

02-0

6

07-0

6

12-0

6

05-0

7

10-0

7

03-0

8

08-0

8

01-0

9

06-0

9

11-0

9

04-1

0

09-1

0

02-1

1

07-1

1

12-1

1

05-1

2

10-1

2

03-1

3

08-1

3

01-1

4

06-1

4

LT Roll-Over Ratio for the Banks, Annualized

16% 18% 19% 20%

8%

19%

35%29%

84%

49%

37%

13%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2010 2011 2012 2013 1H2013 1H2014

FDI

Net Portfolio Investment

Credits Excluding GovernmentShare in Financing

Source: CBRT

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

24

• Shape of the global liquidity will be the same for everyone and it is out of our control

• EM currenciess will all be affected but diverge according to their own macro health and political agenda.

• In this matter, I see risk of further pressure over TL in 2015 (weaker in averagethan year end)…

• …which means that CBRT will not sleep tight (more on that in the coming chapter)

Source: OECD

70

75

80

85

90

95

100

08.1

3

09.1

3

10.1

3

11.1

3

12.1

3

01.1

4

02.1

4

03.1

4

04.1

4

05.1

4

06.1

4

07.1

4

Turkey India Indonesia South Africa

Real Effective Exchange Rate Index: RelativeConsumer Price Indeces, 2010=100

-25,000

-20,000

-15,000

-10,000

-5,000

0

5,000

10,000

15,000

20,000

2006

2007

2008

2009

2010

2011

2012

2013

1H20

13

1H20

14

Total Reserve Change,USD mnBanks' FX Assets, Chng,USD mnOfficial Reserves, Chng,USD mn

Change in the Reserves, (-) is accumulation

Source: CBRT

» PRICE DYNAMICS

» MONETARY POLICY

» REACTION FUNCTION

25

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

• Let’s get it straight: CBRT is unsuccessful in inflation targeting and shows no sign ofimprovement

• The Bank clearly denies the bad inflation outlook, becoming more and more

professional in finding excuses but also less and less credible

• 2014 is not an exception either. CBRT blames the food prices for high inflation

although core indicator excl. food also sails high

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

26

Source: TurkStat

0

2

4

6

8

10

12

01.1

0

03.1

0

05.1

0

07.1

0

09.1

0

11.1

0

01.1

1

03.1

1

05.1

1

07.1

1

09.1

1

11.1

1

01.1

2

03.1

2

05.1

2

07.1

2

09.1

2

11.1

2

01.1

3

03.1

3

05.1

3

07.1

3

09.1

3

11.1

3

01.1

4

03.1

4

05.1

4

07.1

4

CPI, YoY % Chng.

I-Type Indicator (excl. Food), YoY % Chng.

• Rest of 2014 and 2015 will give a bumpy inflation ride

• I expect to see higher administrated prices after the general elections tocompensate the public spending, which will pressure the inflation

• Consumer inflation shall end up around 8.5-8.8% in 2014 and 7-7.5% in 2015

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

27

Source: CBRT, Author’s Own Calculations

-2.00

-1.00

0.00

1.00

07/1

4

08/1

4

09/1

4

10/1

4

11/1

4

12/1

4

01/1

5

02/1

5

03/1

5

04/1

5

05/1

5

06/1

5

07/1

5

Food Alc.Tob Sub-Segment ClothHousing Furnishings TransportComm. Recr. EducationHotels. Misc. Health

Base Year Effect on Consumer Prices, % Point

• CBRT is talented in building handsome sentences with fancy words whiledescribing its monetary policy

• Yet the reality is usually rather more simple and sometimes it bites!

• Pass through from the currency depreciation to inflation is still considerable…

• …hence despite initial attempts for denial, periods of currency depreciation endsup with rate hikes, almost without exception

• I expect currency to give hard times to CBRT in 2015 as well, making the Bank

regret for the rate cuts that are delivered between May-July this year

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

28

Source: CBRT

3

4

5

6

7

8

9

10

11

-5

0

5

10

15

20

25

01.1

1

03.1

1

05.1

1

07.1

1

09.1

1

11.1

1

01.1

2

03.1

2

05.1

2

07.1

2

09.1

2

11.1

2

01.1

3

03.1

3

05.1

3

07.1

3

09.1

3

11.1

3

01.1

4

03.1

4

05.1

4

07.1

4

Non Domestic PPI, YoY % Chng (l.a.)

Domestic PPI, YoY % Chng

One Week Repo Rate

1.9

2.0

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

4

5

6

7

8

9

10

11

12

1310

.11

12.1

1

02.1

2

04.1

2

06.1

2

08.1

2

10.1

2

12.1

2

02.1

3

04.1

3

06.1

3

08.1

3

10.1

3

12.1

3

02.1

4

04.1

4

06.1

4

08.1

4

Funding Cost (%,simple, l.a.)

Eq. Weighted Bask

Source: CBRT, TurkStat

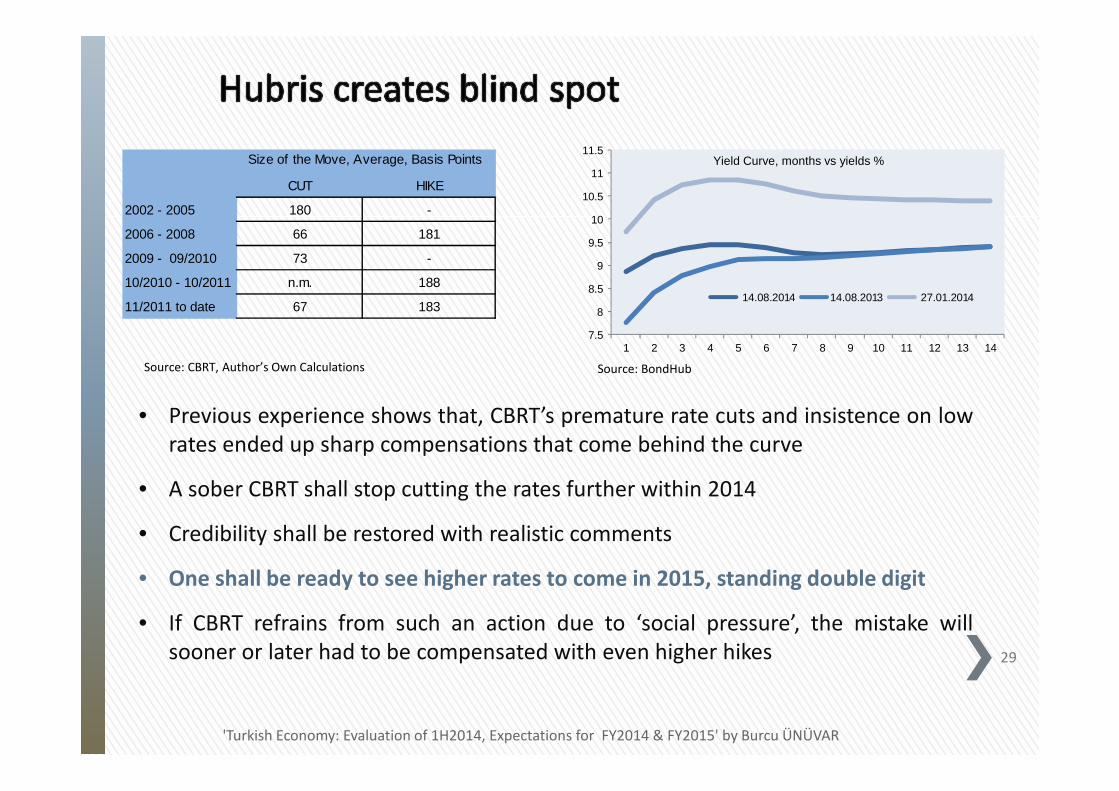

• Previous experience shows that, CBRT’s premature rate cuts and insistence on lowrates ended up sharp compensations that come behind the curve

• A sober CBRT shall stop cutting the rates further within 2014

• Credibility shall be restored with realistic comments

• One shall be ready to see higher rates to come in 2015, standing double digit

• If CBRT refrains from such an action due to ‘social pressure’, the mistake willsooner or later had to be compensated with even higher hikes

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

29

Source: CBRT, Author’s Own Calculations

CUT HIKE

2002 - 2005 180 -

2006 - 2008 66 181

2009 - 09/2010 73 -

10/2010 - 10/2011 n.m. 188

11/2011 to date 67 183

Size of the Move, Average, Basis Points

7.5

8

8.5

9

9.5

10

10.5

11

11.5

1 2 3 4 5 6 7 8 9 10 11 12 13 14

14.08.2014 14.08.2013 27.01.2014

Yield Curve, months vs yields %

Source: BondHub

» MACRO PROJECTIONS FOR 2015

» SCENARIO WORK

30

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

31

Growth Outlook Sour Sweet-Sour Sweet

GDP (TL bn) 1910 1931 1950

GDP ($ billion) 823 862 898

GDP Grow th (real, %, YoY) 1.5 2.7 4.0

Central Government Budget

Budget Balance (%of GDP) -3.20 -2.60 -2.20

Primary Balance (% of GDP) -0.50 0.30 0.50

International Trade

Current Account Balance (% of GDP) -5.4 -6.5 -7.5

Price Dynamics

CPI (%, YoY, end of period) 7.5 7.3 6.7

Foreign Exchange

$/TL Exchange Rate (year-end) 2.450 2.300 2.150

Projections for 2015

Source: Mind and Mood of Burcu ÜNÜVAR

» GLANCE AT THE POLITICAL LANDSCAPE

32

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

» Turkish politics have been suffering an unbalanced game played between a strongpolitical party in the office vs weak and fragmented opposition

» After Mr. Erdogan, who has been the Prime Minister for more than anuninterrupted decade, was elected as the next President, one of the biggestquestion marks is about his successor

» His successor will be taking AKP to the next general elections scheduled mid 2015

» AKP will not be facing a strong opposition from outside as the results of thePresidential election left a ticking bomb to the hands of two leading oppositionparties

» Main opposition party CHP is already created its internal storm on the back of theunsuccessful presidential election results

» Hence before the next general elections, the challenge to AKP does not come fromthe opposition but from its internal dynamics

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

33

» Where does to-be-veteran-President Abdullah Gül fit into this picture ? From hisearlier comments, we aknow that he thinks ‘he is too young to quit active politics’

» Meanwhile there will be many deputies within AKP who will not be able to run forthe Parliament again, due to a internal legislation of the AKP banning the office formore than 3 terms. Will Turkish politics be able to find them a new seat?

» While fresh blood circulation shall be welcomed, markets will definitely be missingMr Babacan (who can be replaced in September or in the next general electionseven if AKP wins) who has been seen as the guarantee of sober economy policiesin Turkey

» A populist candidate to replace Mr Babacan (populist means someone whobelieves that there is a global interest rate lobby who is after Turkey, or whobelieves that Master Yoda exists while in fact ‘there is no spoon’…yes it can goreally that surrealist) will hurt the investment appetite

» If that will be the case, one shall not be surprised to see rating agencies

downgrading Turkey right after the Cabinet revision

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

34

• AKP knows that with deterioration in the economy and higher number of peoplebeing dissatisfied, general elections had to be timed carefully

• Meanwhile having the ‘musical chairs’ – that is more candidates than number of

available posts- rings the bells for possible tension within the ruling party, whichhas been deemed as a source of stability by the investors

• Within this picture, Turkey might be facing earlier general elections around March

2015

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR

35

Source: PEW

Country Satisfaction - TURKEY

0%

20%

40%

60%

80%

100%

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Dissatisfied Satisfied

Burcu ÜNÜVAR

Economist – Lecturer at Yasar University

Views expressed in this report are mine and do not reflect those of the institutions that I work with or have any work affiliation.

36

'Turkish Economy: Evaluation of 1H2014, Expectations for FY2014 & FY2015' by Burcu ÜNÜVAR