The Turkish economy and the evolution of the financial sector · The Turkish economy and the...

20

Matteo Ferrazzi, Unicredit Group Rome, 22 February 2011 The Turkish economy and the evolution of the financial sector

Transcript of The Turkish economy and the evolution of the financial sector · The Turkish economy and the...

Matteo Ferrazzi, Unicredit Group

Rome, 22 February 2011

The Turkish economy and the evolution of the financial sector

2

AGENDA

The Turkish economy

From crisis to solidity: the Turkish banking sector during the last decade

The Italian presence in Turkey

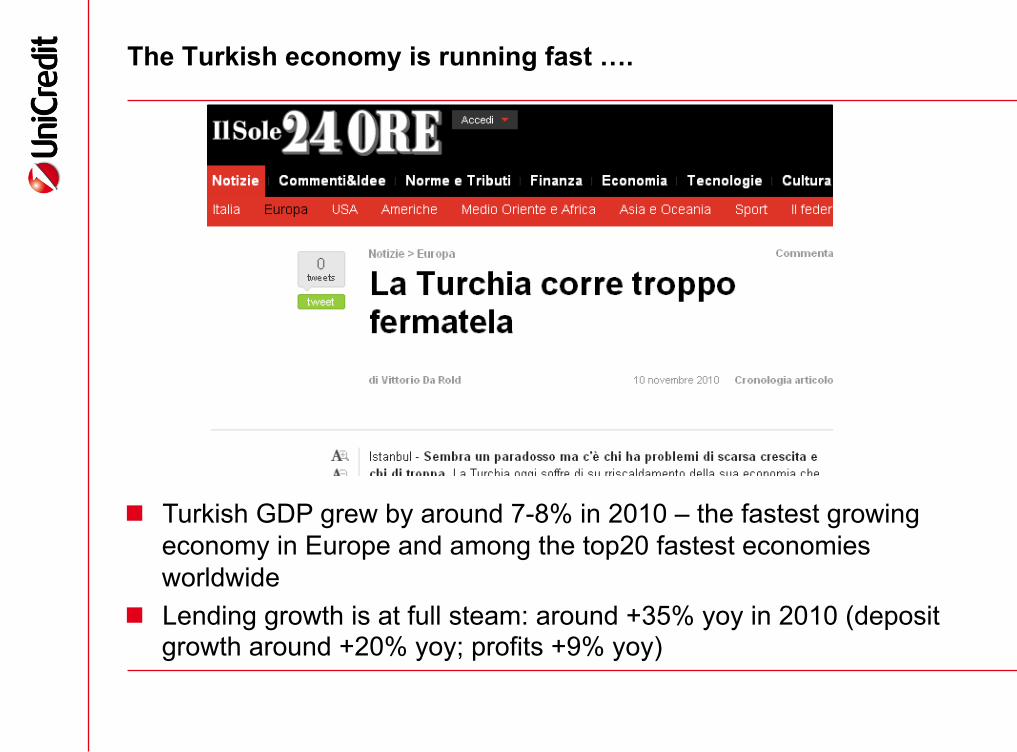

The Turkish economy is running fast ….

Turkish GDP grew by around 7-8% in 2010 – the fastest growing economy in Europe and among the top20 fastest economies worldwide

Lending growth is at full steam: around +35% yoy in 2010 (deposit growth around +20% yoy; profits +9% yoy)

4

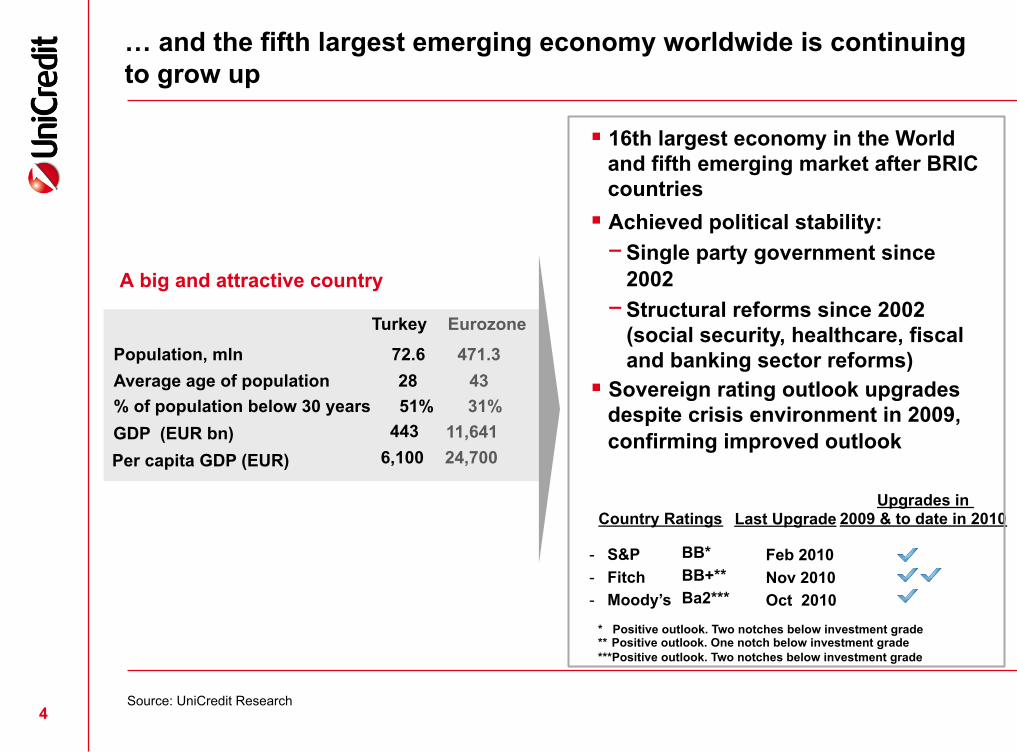

A big and attractive country Turkey

Population, mln 72.6 471.3

Per capita GDP (EUR) 6,100 24,700 GDP (EUR bn) 443

Average age of population 28 43 % of population below 30 years 51% 31%

11,641

16th largest economy in the World and fifth emerging market after BRIC countries

Achieved political stability: − Single party government since

2002 − Structural reforms since 2002

(social security, healthcare, fiscal and banking sector reforms)

Sovereign rating outlook upgrades despite crisis environment in 2009, confirming improved outlook

Eurozone

- S&P - Fitch - Moody’s

Country Ratings Upgrades in

2009 & to date in 2010

BB* BB+** Ba2***

* Positive outlook. Two notches below investment grade ** Positive outlook. One notch below investment grade ***Positive outlook. Two notches below investment grade

Last Upgrade

Feb 2010 Nov 2010 Oct 2010

… and the fifth largest emerging economy worldwide is continuing to grow up

4 Source: UniCredit Research

5

AGENDA

The Turkish economy

From crisis to solidity: the Turkish banking sector during the last decade

The Italian presence in Turkey

6

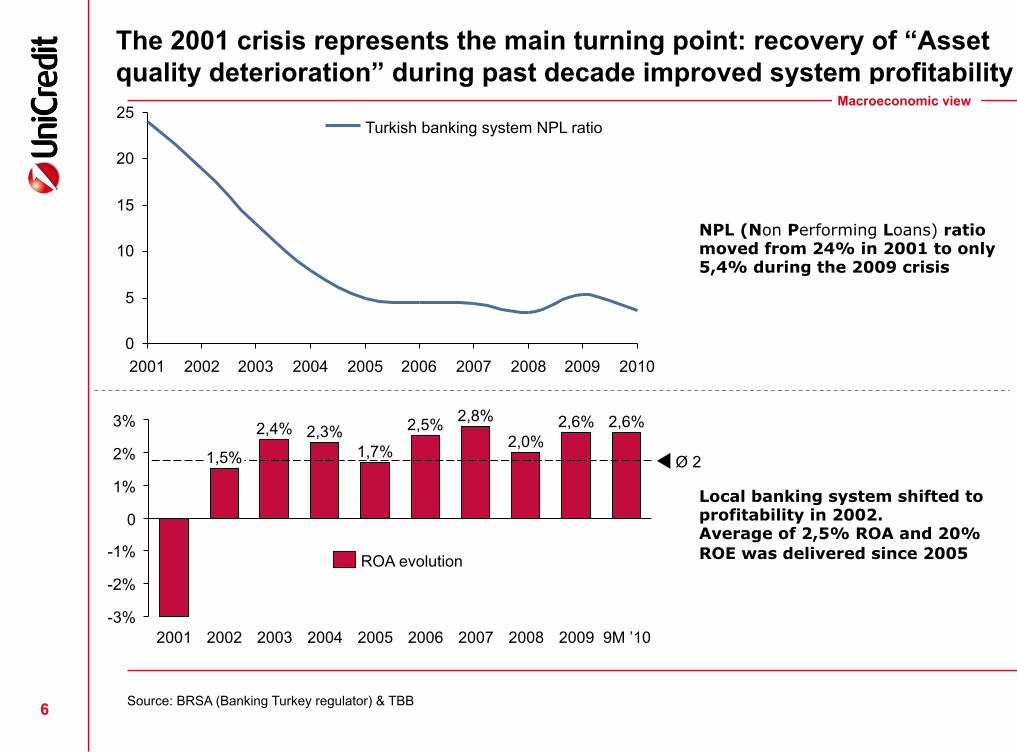

The 2001 crisis represents the main turning point: recovery of “Asset quality deterioration” during past decade improved system profitability

Turkey

Source: BRSA (Banking Turkey regulator) & TBB

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Turkish banking system NPL ratio

NPL (Non Performing Loans) ratio moved from 24% in 2001 to only 5,4% during the 2009 crisis

2,4%

2002

1,5%

2001

3%

2%

1%

0

-1%

-2%

-3%

Ø 2

9M ’10

2,6%

2009

2,6%

2008

2,0%

2007

2,8%

2006

2,5%

2005

1,7%

2004

2,3%

2003

Local banking system shifted to profitability in 2002. Average of 2,5% ROA and 20% ROE was delivered since 2005 ROA evolution

Macroeconomic view

7

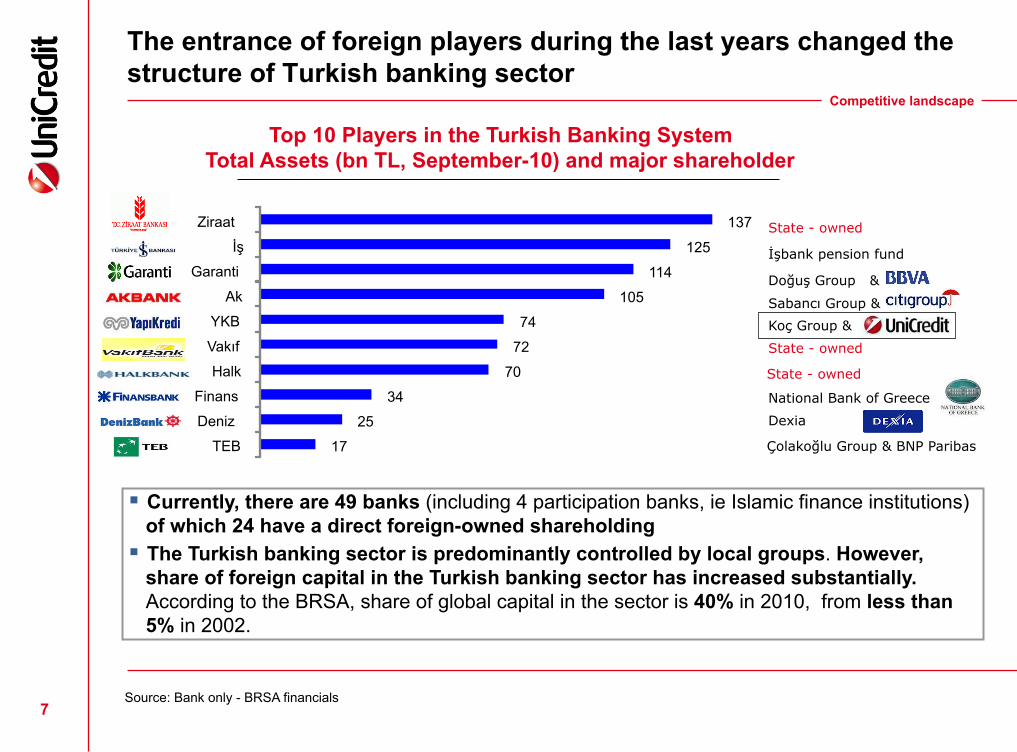

The entrance of foreign players during the last years changed the structure of Turkish banking sector

Competitive landscape

Source: Bank only - BRSA financials

Top 10 Players in the Turkish Banking System Total Assets (bn TL, September-10) and major shareholder

İşbank pension fund

State - owned

Sabancı Group &

Doğuş Group &

Koç Group &

State - owned

National Bank of Greece

Dexia

Çolakoğlu Group & BNP Paribas

Currently, there are 49 banks (including 4 participation banks, ie Islamic finance institutions) of which 24 have a direct foreign-owned shareholding

The Turkish banking sector is predominantly controlled by local groups. However, share of foreign capital in the Turkish banking sector has increased substantially. According to the BRSA, share of global capital in the sector is 40% in 2010, from less than 5% in 2002.

State - owned

137 125

114 105

74 72

70 34

25 17

Ziraat İş

Garanti Ak

YKB Vakıf Halk

Finans Deniz

TEB

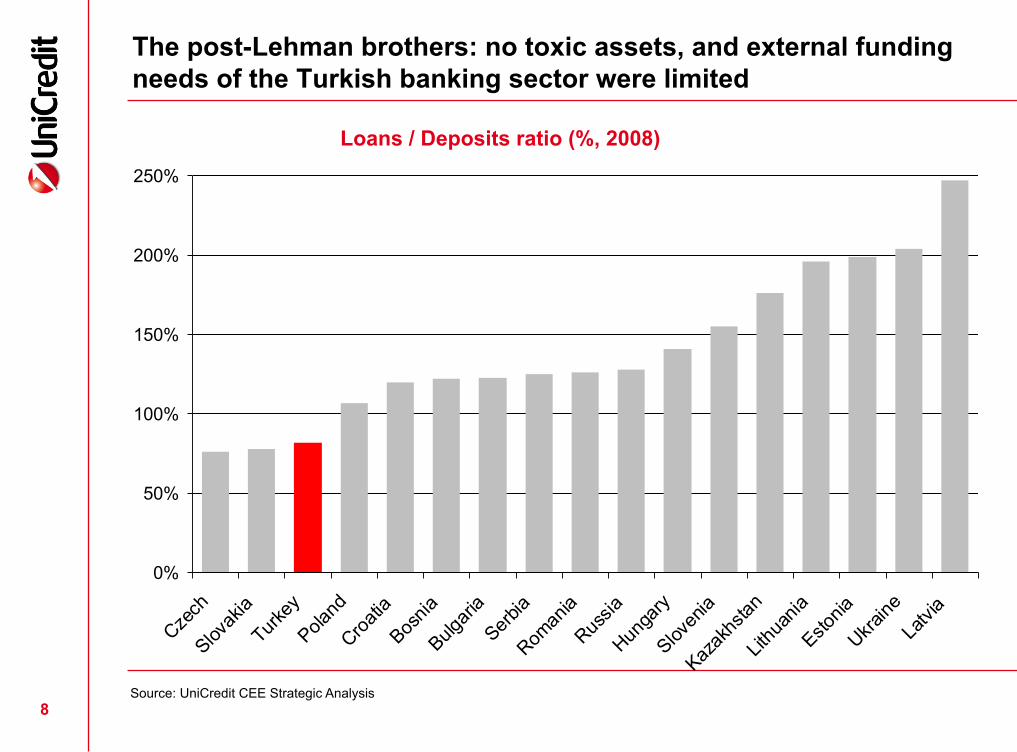

The post-Lehman brothers: no toxic assets, and external funding needs of the Turkish banking sector were limited

8

0%

50%

100%

150%

200%

250%

Czech

Slovakia

Turkey

Poland

Croatia

Bosnia

BulgariaSerbia

Romania

Russia

Hungary

Slovenia

Kazakhstan

Lithuania

Estonia

UkraineLatvia

Loans / Deposits ratio (%, 2008)

Source: UniCredit CEE Strategic Analysis

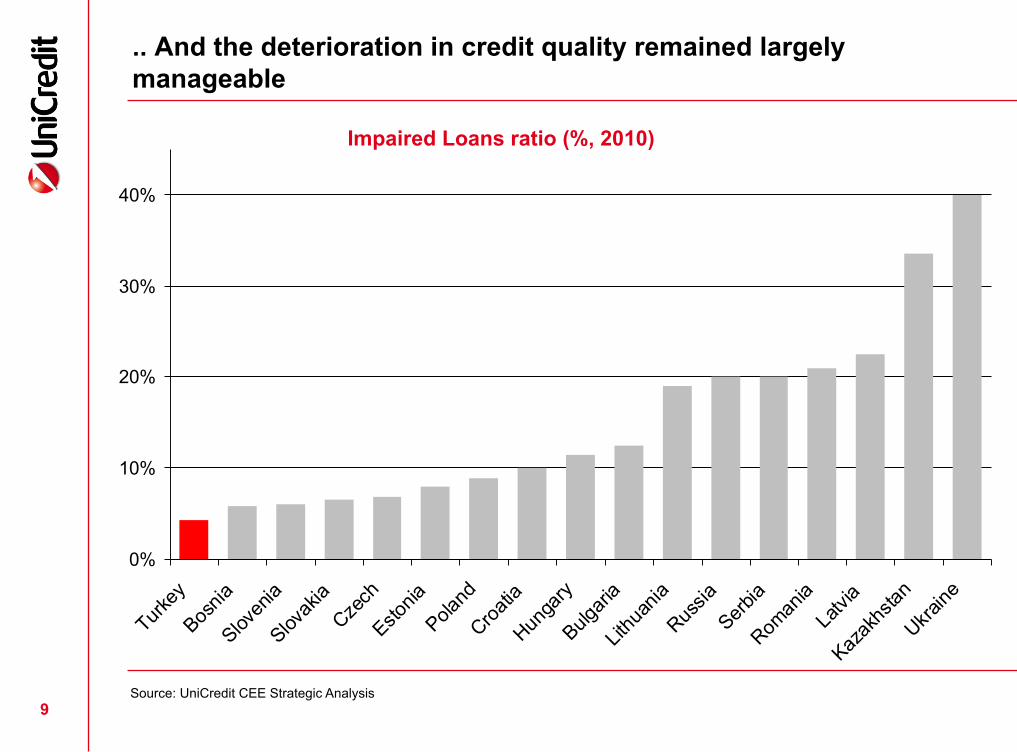

.. And the deterioration in credit quality remained largely manageable

9

0%

10%

20%

30%

40%

Turkey

Bosnia

Slovenia

SlovakiaCzech

Estonia

Poland

Croatia

Hungary

Bulgaria

Lithuania

RussiaSerbia

RomaniaLatvia

Kazakhstan

Ukraine

Impaired Loans ratio (%, 2010)

Source: UniCredit CEE Strategic Analysis

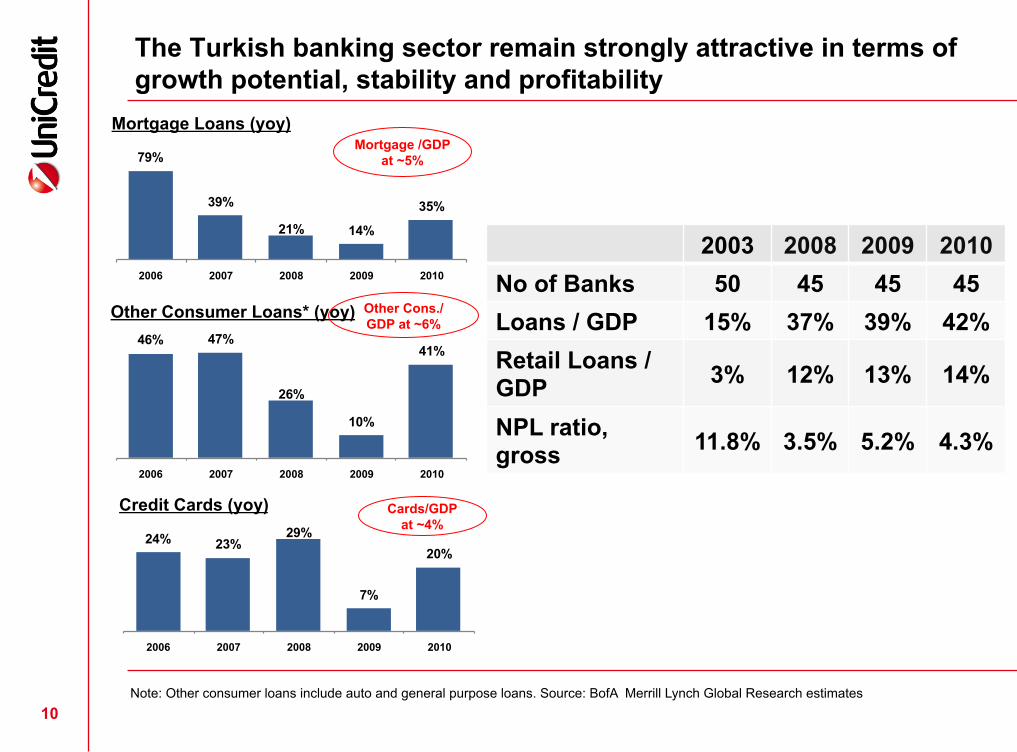

79%

39%

21% 14%

35%

2006 2007 2008 2009 2010

46% 47%

26%

10%

41%

2006 2007 2008 2009 2010

24% 23%29%

7%

20%

2006 2007 2008 2009 2010

The Turkish banking sector remain strongly attractive in terms of growth potential, stability and profitability

10

Mortgage Loans (yoy)

Other Consumer Loans* (yoy)

Credit Cards (yoy)

2003 2008 2009 2010 No of Banks 50 45 45 45 Loans / GDP 15% 37% 39% 42% Retail Loans / GDP 3% 12% 13% 14%

NPL ratio, gross 11.8% 3.5% 5.2% 4.3%

Mortgage /GDP at ~5%

Cards/GDP at ~4%

Other Cons./GDP at ~6%

Note: Other consumer loans include auto and general purpose loans. Source: BofA Merrill Lynch Global Research estimates 10

11

AGENDA

The Turkish economy

From crisis to solidity: the Turkish banking sector during the last decade

The Italian presence in Turkey

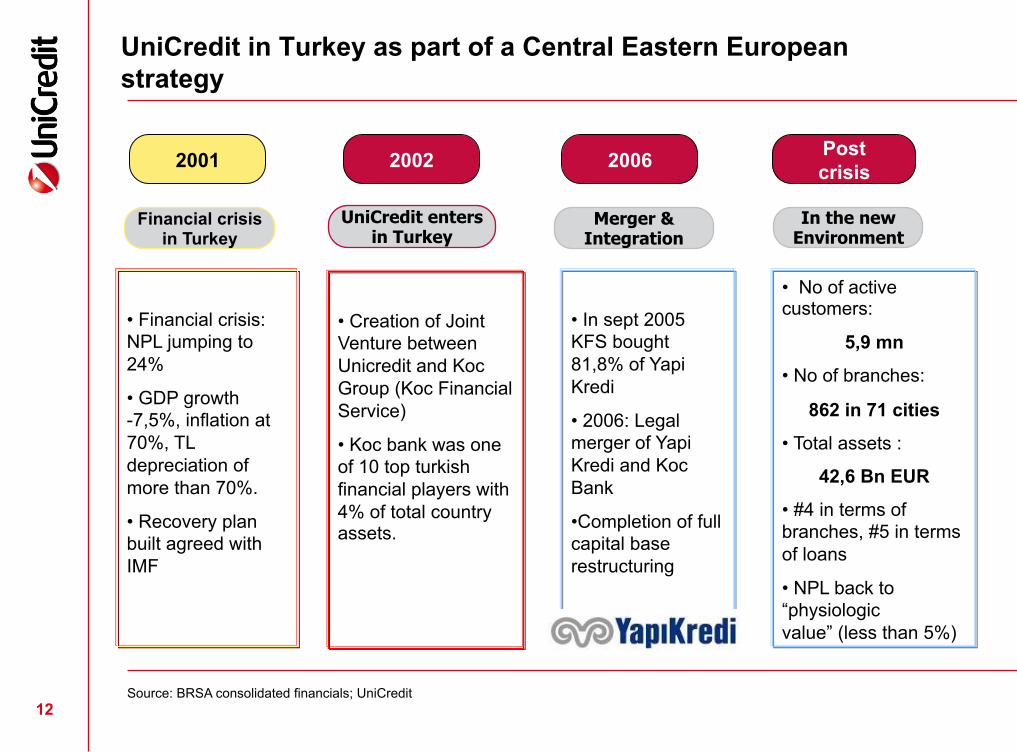

UniCredit in Turkey as part of a Central Eastern European strategy

2006

Post crisis

Merger &

Integration In the new

Environment

• In sept 2005 KFS bought 81,8% of Yapi Kredi

• 2006: Legal merger of Yapi Kredi and Koc Bank

• Completion of full capital base restructuring

2002

UniCredit enters in Turkey

• Creation of Joint Venture between Unicredit and Koc Group (Koc Financial Service)

• Koc bank was one of 10 top turkish financial players with 4% of total country assets.

• No of active customers:

5,9 mn

• No of branches:

862 in 71 cities

• Total assets :

42,6 Bn EUR

• #4 in terms of branches, #5 in terms of loans

• NPL back to “physiologic value” (less than 5%)

12 Source: BRSA consolidated financials; UniCredit

2001

Financial crisis in Turkey

• Financial crisis: NPL jumping to 24%

• GDP growth -7,5%, inflation at 70%, TL depreciation of more than 70%.

• Recovery plan built agreed with IMF

13

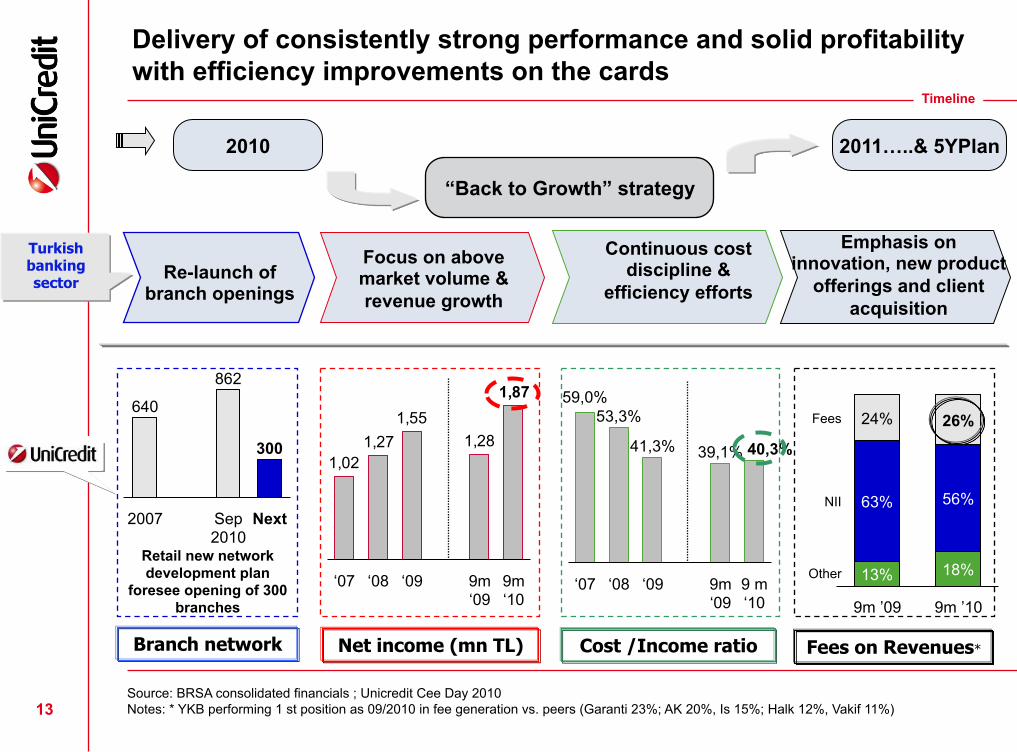

2010

“Back to Growth” strategy

Delivery of consistently strong performance and solid profitability with efficiency improvements on the cards

Re-launch of branch openings

Focus on above market volume & revenue growth

Continuous cost discipline &

efficiency efforts

Emphasis on innovation, new product

offerings and client acquisition

1,87

1,281,55

1,271,02

9m ‘10

9m ‘09

‘09 ‘08 ‘07 ‘09

53,3%

‘07

59,0%

41,3%

‘08 9m ‘09

39,1% 40,3%

9 m ‘10

Net income (mn TL) Cost /Income ratio Fees on Revenues* Branch network

862

2007

640

Next Sep 2010

300

Retail new network development plan

foresee opening of 300 branches

Other

Fees

NII

13%

24%

63%

26%

56%

18%

9m ’10 9m ’09

2011…..& 5YPlan

Source: BRSA consolidated financials ; Unicredit Cee Day 2010 Notes: * YKB performing 1 st position as 09/2010 in fee generation vs. peers (Garanti 23%; AK 20%, Is 15%; Halk 12%, Vakif 11%)

Timeline

Turkish banking sector

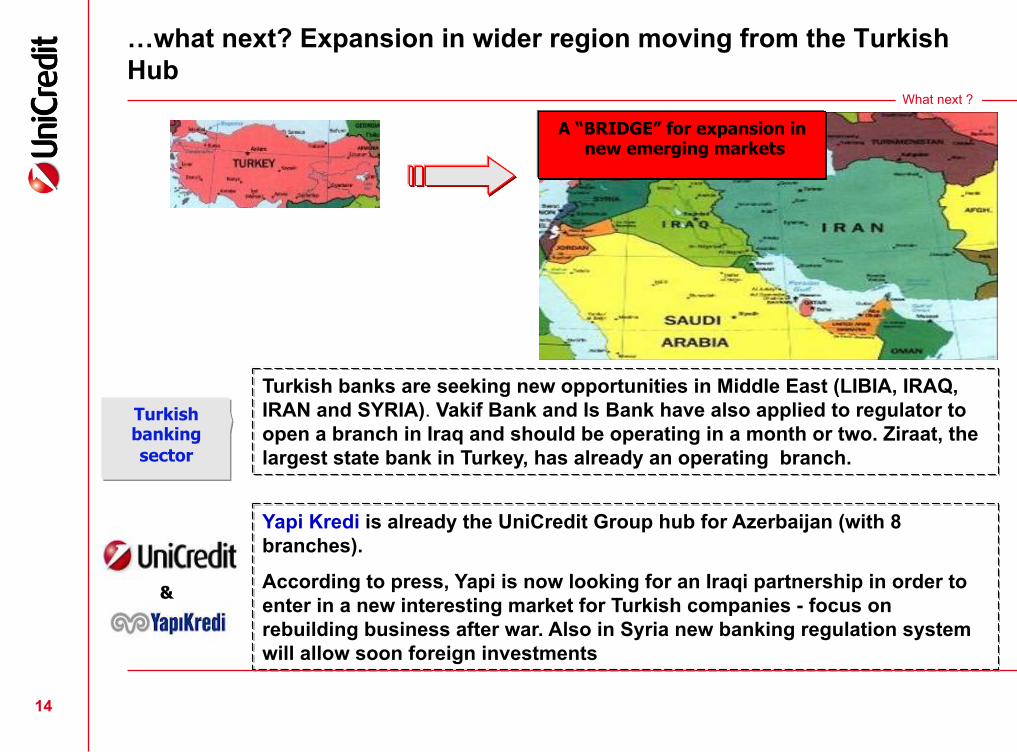

…what next? Expansion in wider region moving from the Turkish Hub

Yapi Kredi is already the UniCredit Group hub for Azerbaijan (with 8 branches).

According to press, Yapi is now looking for an Iraqi partnership in order to enter in a new interesting market for Turkish companies - focus on rebuilding business after war. Also in Syria new banking regulation system will allow soon foreign investments

14

Turkish banks are seeking new opportunities in Middle East (LIBIA, IRAQ, IRAN and SYRIA). Vakif Bank and Is Bank have also applied to regulator to open a branch in Iraq and should be operating in a month or two. Ziraat, the largest state bank in Turkey, has already an operating branch.

What next ?

A “BRIDGE” for expansion in new emerging markets

&

Turkish banking sector

Matteo Ferrazzi Tel. +39.334.6569238 [email protected]

ANNEX

17

What next ?

Source: BofA Merrill Lynch Global Research estimates

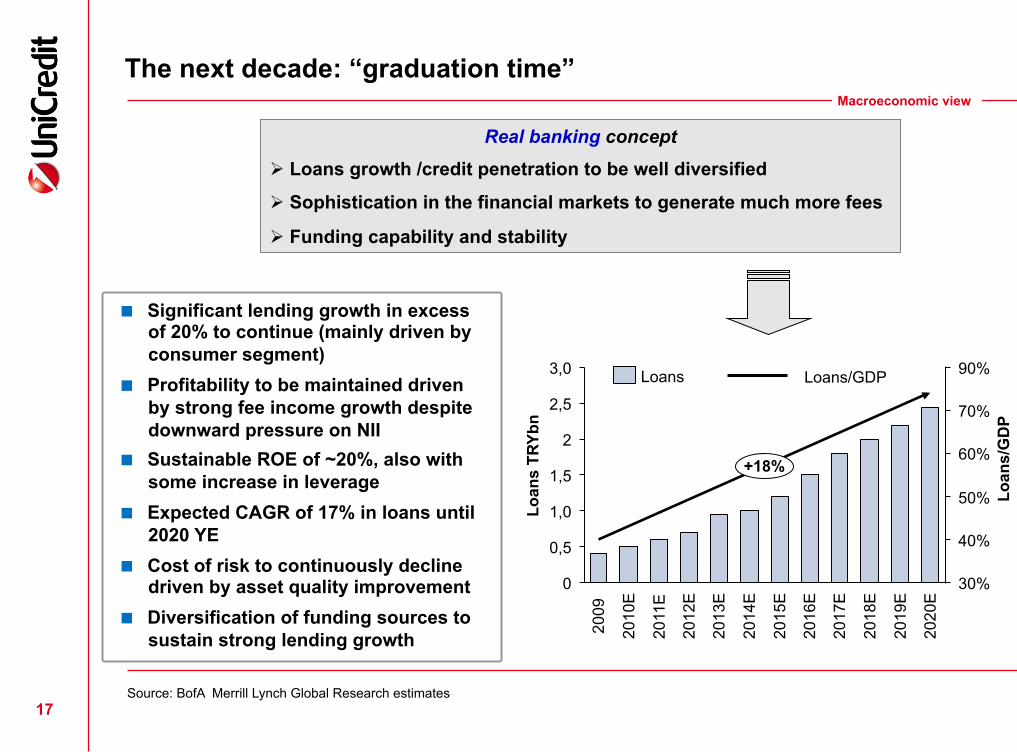

The next decade: “graduation time”

Real banking concept

Loans growth /credit penetration to be well diversified

Sophistication in the financial markets to generate much more fees

Funding capability and stability

Significant lending growth in excess of 20% to continue (mainly driven by consumer segment)

Profitability to be maintained driven by strong fee income growth despite downward pressure on NII

Sustainable ROE of ~20%, also with some increase in leverage

Expected CAGR of 17% in loans until 2020 YE

Cost of risk to continuously decline driven by asset quality improvement

Diversification of funding sources to sustain strong lending growth 20

12E

2011

E

2010

E

2009

2016

E

+18%

2017

E

2013

E

3,0

2

2014

E

2019

E

2015

E

90%

70%

60%

0,5

1,5

30%

50%

0

1,0

2020

E

40%

2018

E

2,5

Loans Loans/GDP

Loan

s/G

DP

Loan

s TR

Ybn

Macroeconomic view

38.6%56.6%78.5%

141.5%

0%

40%

80%

120%

160%

2003 2004 2005 2006 2007 2008 2009

Hungary Poland MU16 Turkey

52.3%

31.9%25.8%17.3%

0%

10%

20%

30%

40%

50%

60%

2003 2004 2005 2006 2007 2008 2009

Hungary Poland MU16 Turkey

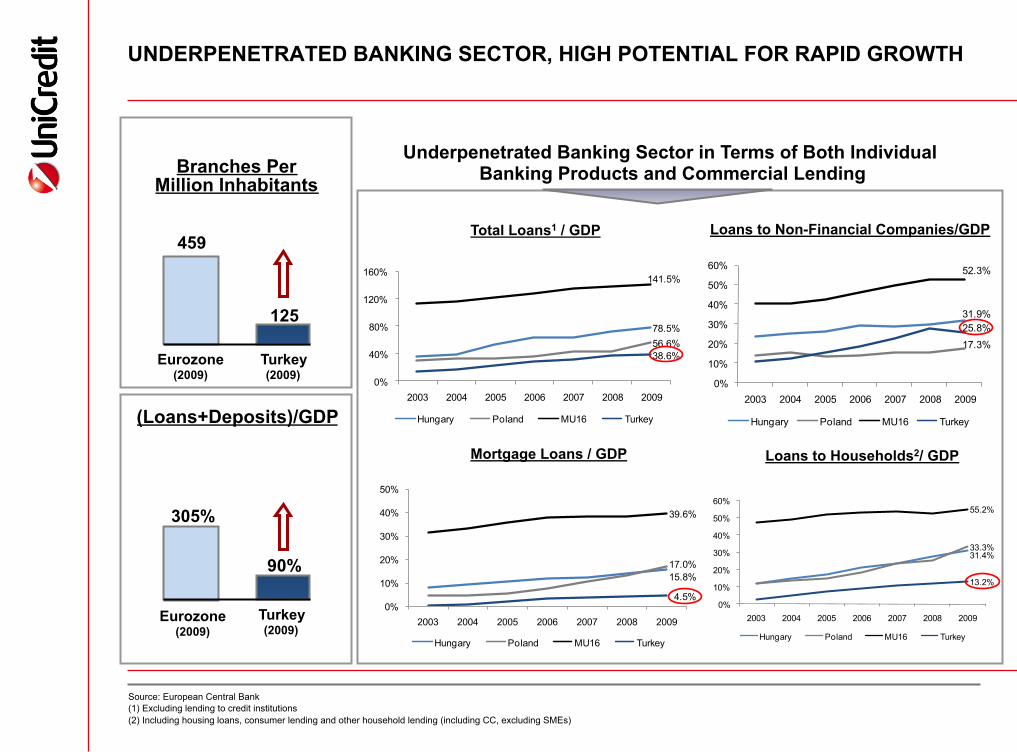

Branches Per Million Inhabitants

UNDERPENETRATED BANKING SECTOR, HIGH POTENTIAL FOR RAPID GROWTH

Eurozone (2009)

125

459

Turkey (2009)

90%

305%

(Loans+Deposits)/GDP

Turkey (2009)

Eurozone (2009)

Underpenetrated Banking Sector in Terms of Both Individual Banking Products and Commercial Lending

Source: European Central Bank (1) Excluding lending to credit institutions (2) Including housing loans, consumer lending and other household lending (including CC, excluding SMEs)

Loans to Non-Financial Companies/GDP

18

Mortgage Loans / GDP

Total Loans1 / GDP

Loans to Households2/ GDP

39.6%

17.0%15.8%

4.5%0%

10%

20%

30%

40%

50%

2003 2004 2005 2006 2007 2008 2009

Hungary Poland MU16 Turkey

55.2%

33.3%31.4%

13.2%

0%

10%

20%

30%

40%

50%

60%

2003 2004 2005 2006 2007 2008 2009

Hungary Poland MU16 Turkey

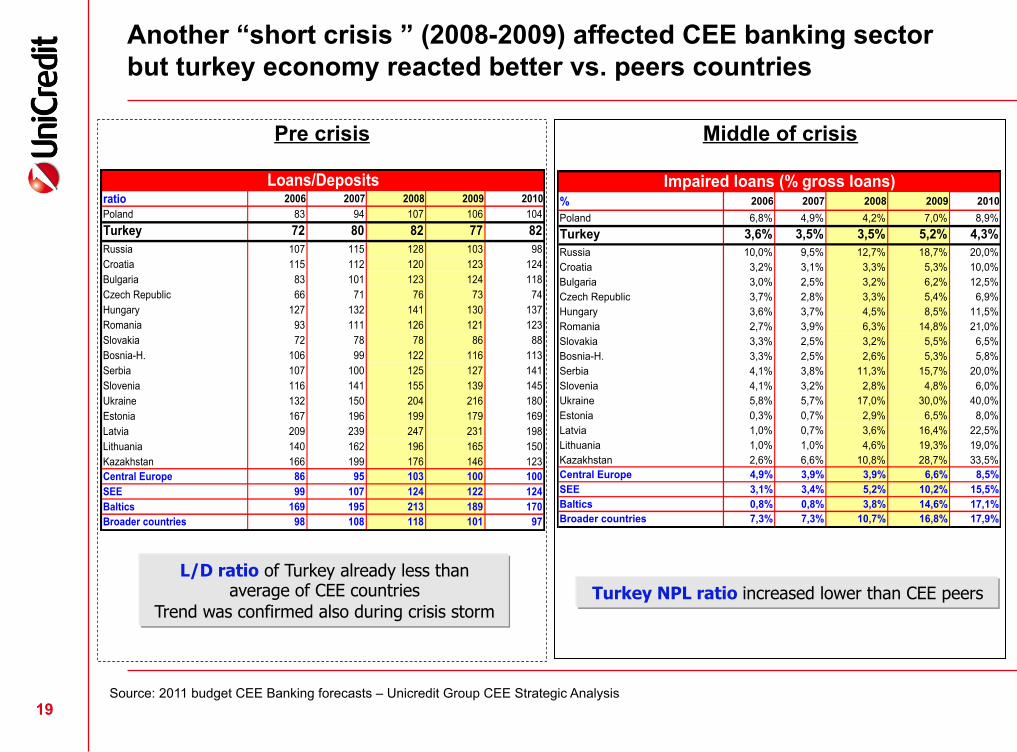

Another “short crisis ” (2008-2009) affected CEE banking sector but turkey economy reacted better vs. peers countries

Pre crisis Middle of crisis

L/D ratio of Turkey already less than average of CEE countries

Trend was confirmed also during crisis storm

% 2006 2007 2008 2009 2010Poland 6,8% 4,9% 4,2% 7,0% 8,9%Turkey 3,6% 3,5% 3,5% 5,2% 4,3%Russia 10,0% 9,5% 12,7% 18,7% 20,0%Croatia 3,2% 3,1% 3,3% 5,3% 10,0%Bulgaria 3,0% 2,5% 3,2% 6,2% 12,5%Czech Republic 3,7% 2,8% 3,3% 5,4% 6,9%Hungary 3,6% 3,7% 4,5% 8,5% 11,5%Romania 2,7% 3,9% 6,3% 14,8% 21,0%Slovakia 3,3% 2,5% 3,2% 5,5% 6,5%Bosnia-H. 3,3% 2,5% 2,6% 5,3% 5,8%Serbia 4,1% 3,8% 11,3% 15,7% 20,0%Slovenia 4,1% 3,2% 2,8% 4,8% 6,0%Ukraine 5,8% 5,7% 17,0% 30,0% 40,0%Estonia 0,3% 0,7% 2,9% 6,5% 8,0%Latvia 1,0% 0,7% 3,6% 16,4% 22,5%Lithuania 1,0% 1,0% 4,6% 19,3% 19,0%Kazakhstan 2,6% 6,6% 10,8% 28,7% 33,5%Central Europe 4,9% 3,9% 3,9% 6,6% 8,5%SEE 3,1% 3,4% 5,2% 10,2% 15,5%Baltics 0,8% 0,8% 3,8% 14,6% 17,1%Broader countries 7,3% 7,3% 10,7% 16,8% 17,9%

Impaired loans (% gross loans)ratio 2006 2007 2008 2009 2010Poland 83 94 107 106 104Turkey 72 80 82 77 82Russia 107 115 128 103 98Croatia 115 112 120 123 124Bulgaria 83 101 123 124 118Czech Republic 66 71 76 73 74Hungary 127 132 141 130 137Romania 93 111 126 121 123Slovakia 72 78 78 86 88Bosnia-H. 106 99 122 116 113Serbia 107 100 125 127 141Slovenia 116 141 155 139 145Ukraine 132 150 204 216 180Estonia 167 196 199 179 169Latvia 209 239 247 231 198Lithuania 140 162 196 165 150Kazakhstan 166 199 176 146 123Central Europe 86 95 103 100 100SEE 99 107 124 122 124Baltics 169 195 213 189 170Broader countries 98 108 118 101 97

Loans/Deposits

Turkey NPL ratio increased lower than CEE peers

Source: 2011 budget CEE Banking forecasts – Unicredit Group CEE Strategic Analysis 19

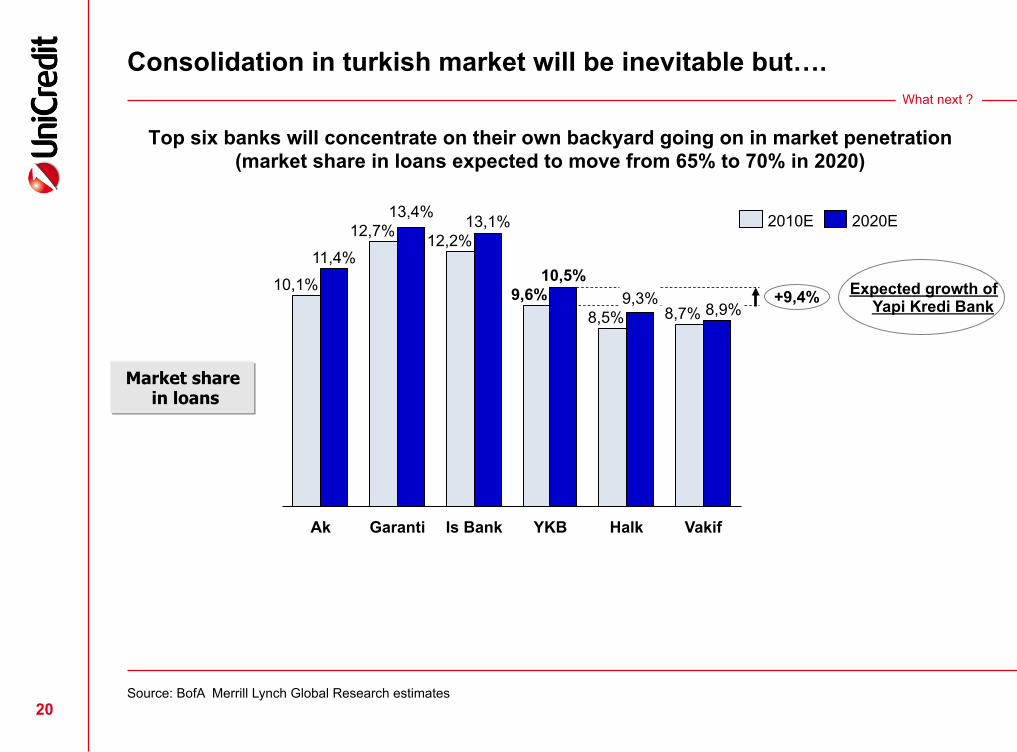

Consolidation in turkish market will be inevitable but….

Top six banks will concentrate on their own backyard going on in market penetration (market share in loans expected to move from 65% to 70% in 2020)

20

11,4%

12,7%

Ak

10,1% 9,6%

Is Bank Garanti

13,1% 12,2%

13,4%

8,9% +9,4%

Vakif

8,7%

Halk

9,3% 8,5%

YKB

10,5%

2010E 2020E

Expected growth of Yapi Kredi Bank

Source: BofA Merrill Lynch Global Research estimates

Market share in loans

What next ?