Transocean Ltd. William Kelly Lesya Kuzmyk Ceida Plasencia Rodrigo Polezel Alex Santos.

16

Transocean Ltd. William Kelly Lesya Kuzmyk Ceida Plasencia Rodrigo Polezel Alex Santos

-

Upload

keyla-balthrop -

Category

Documents

-

view

216 -

download

1

Transcript of Transocean Ltd. William Kelly Lesya Kuzmyk Ceida Plasencia Rodrigo Polezel Alex Santos.

Transocean Ltd.William KellyLesya KuzmykCeida PlasenciaRodrigo PolezelAlex Santos

Company Background

Transocean Ltd. is a corporation based in Switzerland that provides services, related equipment and crews for offshore drilling of oil and gas worldwide. They are the largest international provider of offshore contract drilling services, owning 136 offshore drilling units. They provide the following services:

• Contracted drilling services• Drilling Management Services• Integrated Services• Oil and Gas exploration

Where RIG Operates

Transocean LtdStock Price: $86.60Symbol: RIG52-Week High/Low: $41.95 - $94.44S&P 500: $1108.86

2008 A 2009 E 2010 EEPS 14.38 11.73 10.65

P/E Ratio 6.3 7.6 8.6S&P 500 $65.00 $50.00 $75.00

S&P 500 P/E 15.2 22.18 14.78Relative P/E 0.42 0.34 0.58

Porter's 5 Forces

RIG's Competition/New Entrants

• Main Competitors: Pride International Inc., Noble Corp., and Diamond Offshore Drilling.

• RIG has the largest drilling fleet in the industry, with a total of 136 mobile offshore drilling units and 10 new ultra-deepwater units under construction.

• RIG holds 19 of 23 world records for drilling in the deepest waters--drilling in 10,011 feet of water.

• RIG specializes in Harsh-Environment Drilling--not many other companies have the equipment and personnel to do so.• High start-up costs prevent new entrants (Moat).

The Market

• Transocean Ltd. (RIG)• P/E: 7.60• PEG ratio: 0.58 (5 year expected)• EPS: 11.73 (diluted)• Price to Book ratio: 1.44• Dividend Yield: N/A• Expected share price return: 10.8%• Profit Margin: 29.98%• Market Cap: 29,196.80 (US$ m)• Rating: Outperform (from Credit

Suisse on October 21, 2009)• Recommendation: 1.9 (1.0 strong

buy-5.0 sell)• Revenue: 12.09B (US$)

Diamond Offshore Drilling Inc.(DO)P/E: 9.91PEG ratio: 0.75 (5 year expected)EPS: 10.024Price to Book ratio: 3.74Dividend Yield: N/AProfit Margin: 38.26%Market Cap: 13.81B (US$)Rating: Buy (from Jesup & Lamont on October 23, 2009)Recommendation: 2.7 (1.0 strong buy-5.0 sell)Revenue: 3.64B (US$)

Noble Corp. (NE)P/E: 6.87PEG ratio: 0.63 (5 year expected)EPS: 6.328Price to Book ratio: 1.72Dividend Yield: 0.50%Profit Margin: 45.72%Market Cap: 11.36B (US$)Rating: Outperform (from RBC Capital Markets on October 26, 2009)Recommendation: 1.9 (1.0 strong buy-5.0 sell)Revenue: 3.61B (US$)

Supplier Power

• RIG contracts companies specialized in the construction of ships and offshore drilling units

• Companies engaged in the development of these rigs include Daewoo Shipbuilding and Marine Engineering Co. Ltd. (DSME), Hyundai Heavy Industries, Ltd., and Samsung.

• Each drilling unit costs an average of $283.5 million• Newbuilds such as the ultra-deepwater drill

ships are contracted for about $500,000/day

• The Brand Power• Safe, effective and efficient • Known for their deep water and

harsh environment explorations• "The largest offshore driller"• Owns patented structure and

• Oil from one company's rig is no different than another's; buyers will look for the best price and contract terms

• Dependable Buyers• Set contracts from several months

to multiple years• Contracts with 41 different

companies from the NOC, IOC and independents such as Shell, Chevron, BP

Buyer PowerAverage

Condition Drilling

Ultra Deep/Harsh Environment

Drilling

Buyer has more control over

prices

RIG has more control over

prices

More substitutes available

Little-to-no substitutes available

Less dependent Very dependent

Low brand power Stong brand power

Threat of Substitute Products• To access natural gas and oil resources located under the

ocean, use of drilling rigs is necessary • No viable alternative process

• Transocean specializes in and derives large bulk of revenue from deep water rigs• Very few companies possess technology, expertise and

resources to create such specialized rigs • As a result, primary substitute product threat faced by

Transocean lies with jackups and medium depth rigs• Much easier for competitors to create own rigs that can

accomplish same objectives at low depths• Constitute smaller percentage of Transocean's revenue;

minimal threat faced

SWOT Analysis

Strengths

• Dominant position in the ultra-deepwater (+4,000 feet) industry with a 35% market share.

• Stronger cash flows in following years due to lower capex• Low debt obligations• Recent development of technologically enhanced Enterprise-

Class drillships• Newbuild program includes three rigs that reach depth

12,000 feet

Contract Backlog• Strong contract backlog of deepwater rigs, which contributes to 70% of

its revenue

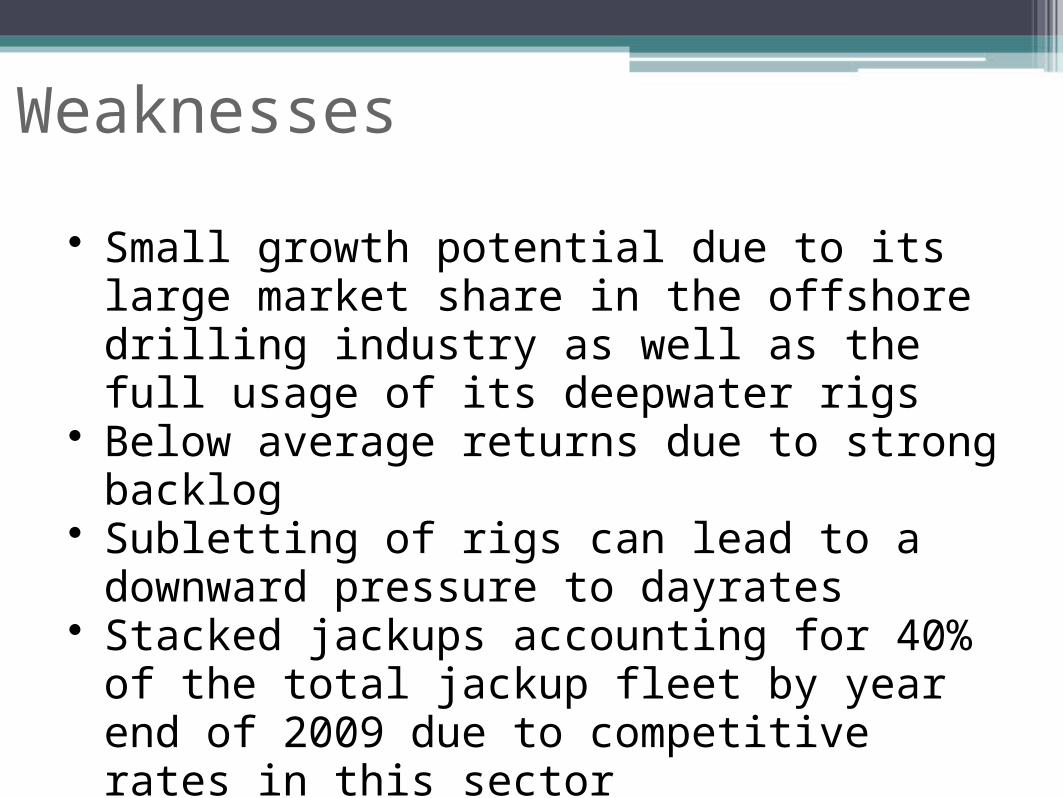

Weaknesses

• Small growth potential due to its large market share in the offshore drilling industry as well as the full usage of its deepwater rigs

• Below average returns due to strong backlog• Subletting of rigs can lead to a downward

pressure to dayrates• Stacked jackups accounting for 40% of the total

jackup fleet by year end of 2009 due to competitive rates in this sector

Opportunities• Due to the recession, investment in oil production and

exploration has experienced an overall reduction• With the likelihood of oil prices increasing within the

next few years due to sustained demand, utilization of rigs is likely to increase• With higher oil prices, incentive explore for oil located in

the deepest, harshest territories will increase• These will increasingly require deep-water capable rigs,

which Transocean has an advantage in

• May seek to acquire competitors, maintain technological dominance

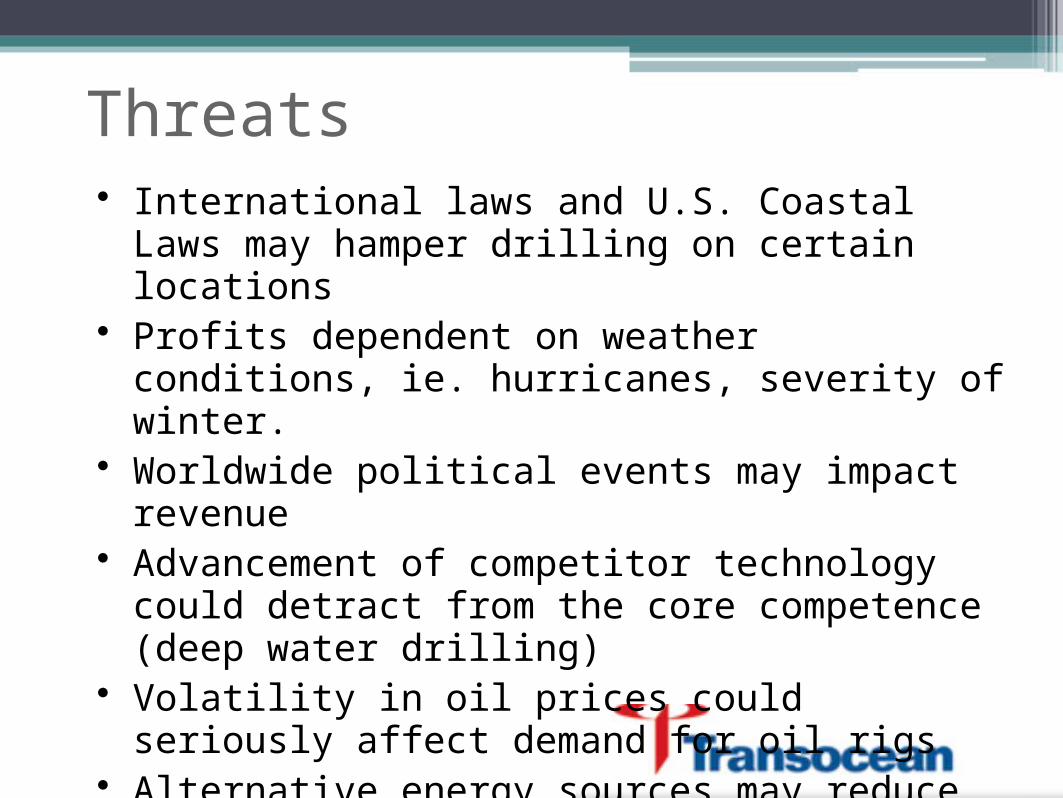

Threats• International laws and U.S. Coastal Laws may

hamper drilling on certain locations• Profits dependent on weather conditions, ie.

hurricanes, severity of winter.• Worldwide political events may impact revenue• Advancement of competitor technology could detract

from the core competence (deep water drilling)• Volatility in oil prices could seriously affect demand

for oil rigs• Alternative energy sources may reduce future

demand for oil rig utilization