Trade Finance - US Regulatory...

46

Trade Finance - US Regulatory Compliance prepared for: John Baranello Director TFCMC Americas Product Management Deutsche Bank AG, New York (212) 250-9604 [email protected] March 15, 2011

Transcript of Trade Finance - US Regulatory...

Trade Finance - US Regulatory Compliance prepared for:

John BaranelloDirectorTFCMC Americas Product ManagementDeutsche Bank AG, New York(212) [email protected]

March 15, 2011

1John Baranello

Deutsche Bank at a Glance

Our Company:• Deutsche Bank is a leading global investment bank with a strong and profitable private clients franchise. • Our businesses are mutually reinforcing.

Where we are now:• 80,456 employees in 72 countries • Unparalleled financial services throughout the world • A leader in Germany and Europe, the bank is powerful and growing in North America, Asia and key emerging markets.

History:• Deutsche Bank was founded in Berlin in 1870 to support the internationalization of business and to promote and facilitate trade relations between Germany, other European countries, and overseas markets.• Deutsche Bank is a leading global provider of financial services.

2John Baranello

AmericasArgentina Buenos AiresBrazil São PauloMexico Mexico City(a)

US New York

Europe / MEAAustria ViennaBelgium BrusselsCzech Republic PragueEgypt Cairo(a)

France ParisFinland Helsinki(a)

Germany DüsseldorfHamburgMunichStuttgart20 add. sales offices(a)

Hungary BudapestItaly MilanKazakhstan Almaty(a)

Netherlands AmsterdamNigeria Lagos(a)

Norway Oslo(a)

Poland WarsawPortugal Lisbon(a)

Russian Fed. MoscowSpain Barcelona

MadridSwitzerland ZurichSweden Stockholm(a)

Turkey IstanbulUAE Dubai(a)

UK London

Trade Finance global presence

CountriesAmericas 4Europe/MEA 22Asia 13

Total 39

LocationsAmericas 4Europe/MEA 46Asia 24

Total 72

Asia-PacificChina Beijing

Guangzhou (a)

Hong Kong Shanghai

India Bangalore Calcutta Chennai Mumbai New Delhi

Indonesia JakartaSurabaya

Japan TokyoKorea SeoulMalaysia Kuala LumpurPakistan Islamabad

KarachiLahore

Philippines ManilaSingapore SingaporeSri Lanka ColomboTaiwan TaipeiThailand BangkokVietnam Hanoi (a)

Ho Chi Minh City

Trade Finance – Global reach with Local Expertise

3

Share of MindWe are recognized leaders in the trade industry as we maintain leadership and membership roles in all the important

Trade and Regulatory Associations throughout the world.-Chairman of the BAFT - IFSA (Bankers Association for Foreign Trade -International Financial Services Association) NY / Metro Documentary Letter of Credit Committee-Chairman of the BAFT - IFSA Payments and Compensation Committee- Board of Director BAFT- IFSA- Member of the BAFT- IFSA National Documentary Letter of Credit Committee - Member of the BAFT- IFSA National US Regulatory Committee- Member of the US Regulatory, Trade Committees for BAFT- IFSA- Member of the SWIFT Cash and Treasury Committee- Rapertoire and member of the ICC (International Chamber of Commerce)-Trade and Regulatory resource for FIBA (Florida International Bankers Association)-Trade Resource for the International Cotton Institute of the American Cotton Shippers Association-Trade Resource for the FFEIC (Federal Financial Institutions Examination Council) and the Asociación Bancaria de Panamá-Recognized by the FBI as a Trade Finance Expert Witness-Our Trade Services team recognized as the Benchmark operation for all Trade Operations by the Federal Reserve for having exemplary US Regulatory Policies and Procedures.

4

Global Trade Finance

Counterparty

Political/ Country

Regulatory

Currency Rate

Commodity Rate

Contract Negotiation

Contract Signing Procurement Production Delivery Settlement

Non Acceptance of Contract

Non Acceptance

of Goods

Interest Rate

Trade Value Chain

Ris

ks

John Baranello4

WarrantyTermination

Rol

es

Issuing Bank Confirming Bank Advising Bank Negotiating Bank Transferring Bank Fronting Bank

Issuing Bank Confirming Bank Advising Bank Negotiating Bank

Paying Agent Remitting Bank Collecting Bank Presenting Bank

Issuing Bank Confirming Bank Advising Bank Fronting Bank Administrative Agent FDIC Insured

Mandated Lead Arranger

Agent

Documentary Letters of Credit

Import Export UCP 600 Experts Off-shore Issuance Confirmations Silent Confirmations Document Examination Negotiation Bankers’ Acceptances Deferred Payment Commodity Credit

Corporation Guarantee Programs

Back – to - Back

Global Trade Management

db-direct internet InfoTr@ck Supply Chain

Management Value added

Advising Bank Services

Document Creation

Document Management

Industry Leaders Expert Training

Financial Supply Chain Supplier Finance– Confirmed Payable– Pre-Shipment EIPP

Standby Letters of Credit

ISP98 / UCP500 / UCP 600 Experts

URDG 758 Experts Advance Payment Direct Payment Bid / Tender / Trade

Warranty Obligation Customs - Steamship Rental / Lease Performance /

Non Performance Counter –

Indemnifications Syndicated /

Revolving Facilities

Structured Trade & Export Finance

ECA Covered Finance Down Payment

Financing Pre-Export Finance Prepayment Finance Without Recourse

Financing Forfaiting Trade-Related Loans Distribution/Secondary

Market Trading A/R Financing Factoring

Collections Documentary Import / Export Clean Documents

against Payment Documents

against Acceptance

Direct Collections Avalisation of

Trade Acceptance URC 522 Experts

5

•The UCP 600,•The UCP 500, (….and 400 & 290)•URDG 758,•ISP 98,•ISBPED,•Incoterms 2010,•URC 522,•URR 525,•SWIFT,•The Back, Front, & Sides of Documents,•Atlas’s, Maps,•Internet…•Differing Local Commercial Law..

– Example: UCC Article V differs from State to State ■ Regulatory Compliance in the United States:

– US Department of the Treasury (“OFAC”)– US Department of Commerce (“BIS”)– Financial Crimes Enforcement Network (“FINCEN”)

– Patriot Act – Bank Secrecy Act (“BSA”)– Indicators of Suspicious Activity– Politically Exposed Persons (“PEPS”)– Suspicious Activity Reports (“SARS”)– Fraud

■ “Open Account”■ “KYC”■ US Persons….

Trade Finance Practitioner Concerns:

Then:

UCP 290

Now:

6John Baranello

The Laws and Regulations of the United States apply to all United States Persons….

■ And you are "a U.S. Person" if…– You are a(n):

– Individual, Corporation, United States Government, Bank located in the United States or, – Located outside the United States if Controlled-in-Fact by a United States concern– You are a company liable to U.S. law– A U.S. citizens in or outside the USA as well as non U.S. citizens staying in the USA– You are an individual or economic entity, located in the USA, especially financial institutions, their subsidiaries,

branches, agencies, representatives and all their directors, staff etc. – Note: This definition includes both the singular and plural,

■ You are Controlled-in-Fact by a United States concern:– Owns substantial stock, appoints officers and / or– Controls:

– general policies, or,– the day-to-day operations of foreign concern,

■ You are a Foreign Division or entity of a U.S. Concern.■ Not the Head Office or any Foreign Branch of a Branch of a Foreign Bank in the United States.

– US Laws apply only to DBNY

■ Article 37d of the UCP 600 – Article 18d of the UCP 500:– The Applicant shall be bound by and liable to indemnify a bank against all obligations and responsibilities imposed by

foreign laws and usages.

7John Baranello

Methods of Payment

Domestically or Internationally Buyers and Sellers basic objectives: ■ Buyers - want to receive the goods they order on time, in good condition and….

■ Pay as late as possible.

■ Sellers - want to hold title to their goods for as long as possible and….

■ Control their own payment fate.

In order of Safety for the Seller: ■ Payment in Advance – (Most Favorable)

■ Confirmed Letter of Credit■ Unconfirmed Letter of Credit ■ Documentary Collection■ Open Account

■ Consignment – (Least Favorable)

Commercial Objectives

ICC Rules Based

8

The International Chamber of Commerce (“ICC”)

Is the world business organization championing the global economy as a force for economic growth, jobs creation and prosperity.The ICC was established in 1919, with the primary objective of facilitating the flow of international trade at a time when nationalism and protectionism posed serious threats to the world trading system. This private international organization fosters self-regulation in business practices. It was in that spirit that the Uniform Customs and Practice for Documentary Credits (commonly called “UCP”) were first introduced – to alleviate the confusion caused by individual countries’ promoting their own national rules on letter of credit practice.

•The UCP600, which has been in effect since July 2007, is the sixth revision of the rules for documentary letter of credit since they were first promulgated in 1933. •ICC Publication No. 590 (ISP98 ) are rules specific for Standby Letters of Credits, have been in effect since January 1999.•URDG 758 are the new Uniform Rules for Demand Guarantees replacing the URDG 458 on July 1, 2010.

ICC rules offer: Harmonization versus differing customs. Common understanding of terms and intentions. The ability to rely on a set of contractual rules that establish substantial uniformity in practice, to reduce the need for

practitioners to cope with a plethora of often conflicting national regulations. A platform in which to conduct business between countries with widely divergent economic and judicial systems.The adoption and use of international publications and rules helps to avoid disputes and, where these arise, leads to much greater predictability in their outcome.It is important to note that the work of the ICC represents the work of a private international organization, not a governmental body. Since its inception, the ICC has insisted on the central role of self-regulation in business practice. These rules, formulated entirely by experts in the private sector, have validated that approach.

John Baranello8

9John Baranello

Letter of CreditA Letter of Credit (Documentary or Standby) is a written undertaking given by a Bank (Issuing Bank) to the Beneficiary - on the instruction of the Applicant (Issuing Banks Client) to pay the Beneficiary at sight or at a determinable future date - up to a stated amount of money - within a defined period of time.

This undertaking is conditional upon the Beneficiary’s documentary compliance of the terms and conditions stated in the Letter of Credit.

Beneficiary looks to a bank to receive payment for their goods, services or performance – not their client.

Reasons a Bank needs to substitute its own credit for the credit of its Client…■ New economic relationship■ The credit of the buyer / applicant is weak or unknown ■ Economic and political conditions are uncertain■ Security ■ Convince beneficiary capital has been allocated in their favor, and provide for a,■ Clear, defined, rules based path to payment■ Local law demands:

– Recognition– Control– Tariffs

10

Documentary Letter of Credit

Documentary (“Commercial”) Letter of Credit:■ Used as the Primary means to Finance the Buying and Selling of Goods, Services or Performance.

Standby Letter of Credit / Guarantee:■ Generally used as a Secondary means of payment. Something may have gone wrong. Financial assurance is “guaranteed” or is on “standby”, and is available from a Bank or Guarantor

– Assures the beneficiary of the performance of their customer's obligation– Bank / Guarantor stands behind monetary obligations of its client– Bank / Guarantor strengthens the credit worthiness of its client– Can be used as a primary means of payment when issued as a “direct pay” or “direct draw” letter of credit– Easy for the Beneficiary to draw. Documents are simple to create and usually in Beneficiary’ control– Capital Adequacy Reserves– More Expensive to Issue & Maintain than a Commercial Letter of Credit

Choice of Governing Rules:■ UCP 500 - UCP 600 - ISP 98 – URDG 758 ■ UCC Article 5 (U.S. Regional Law)

Some examples for the use of Standby’s or Guarantees are:■ Support importer’s open account purchases■ Cover brokerage firm’s margin requirements■ Serve as Bid, Performance, and/or Warranty Bonds in the construction and service industries■ Tender, Advance Payment, Performance, Payment, Retention Money, Warranty - Guarantee■ Provide insurer’s agent worldwide reimbursement of claims paid■ Enable corporations that are issuing commercial paper to gain a better rate■ Provide security for mortgages, leases and rent payments, and,■ Entice good grades in school!

John Baranello10

11John Baranello

Documentary Letter of Credit Advising Procedure- Export Letter of Credit

Applicant(Buyer)

Contract1

2

Issuing Bank

Letter of Credit Application

Beneficiary(Seller)

Issuing Bank issues the letter of credit at the request of its client (applicant of the letter of credit), or, on its own behalf.

Irrevocably bound to honour beneficiaries complying documents.

12John Baranello

Export Documentary Letter of Credit Advising Procedure

Applicant (Buyer)

Contract

Issuing Bank

1

2 Letter of Credit Application

3 Letter of Credit Issuance via

SWIFTAdvising Bank

Beneficiary(Seller)

Advising BankAdvises the credit and any amendment without any undertaking to honour or negotiate, signifying that it has satisfied itself as to the apparent authenticity of the credit or amendment and that the advice accurately reflects the terms and conditions of the credit or amendment received.

( Could be our Client and direct LC to us )

( Could be our Client and direct LC to us )

13

Trade Transactions are Reviewed for Compliance with:

Department of the Treasury: Office of Foreign Assets Control (OFAC): OFAC Country Sanction Programs OFAC List-Based Sanctions Programs SDN List

Bureau of Industry and Security US Department of Commerce: Denied Person Unverified List Entity List Debarred List Anti-boycott Compliance

Others: KYC Politically Exposed Persons FFIEC - Bank Secrecy Act Anti-Money Laundering Examination Manual, 2010 European Union List

14

OFAC, is a Division of the US Department of the Treasury, administers and enforces economic and trade sanctions based on US foreign policy and national security goals against targeted foreign countries, terrorists, international narcotics traffickers, and those engaged in activities related to the proliferation of weapons of mass destruction….

■ As part of its enforcement efforts, OFAC publishes a list of individuals and companies owned or controlled by, or acting for or on behalf of, targeted countries. It also lists individuals, groups, and entities, such as terrorists and narcotics traffickers designated under programs that are not country-specific. Collectively, such individuals and companies are called "Specially Designated Nationals" or "SDNs." Their assets are blocked and U.S. persons are generally prohibited from dealing with them.

■ Many of the sanctions are based on United Nations or other international mandates, are multilateral in scope, and involve close cooperation with allied governments.

■ OFAC acts under Presidential wartime and national emergency powers as well as under the authority granted by specific legislation to impose controls on transactions and to "freeze” or “block" assets under U.S. jurisdiction

15

OFAC Sanctioned Entities…...

■ Anti Terrorism Sanctions

■ Counter Narcotics Trafficking Sanctions

■ Diamond Trading

■ Nonproliferation

■ Blocked Persons

■ Certain Countries

■ Certain Named Ocean Vessels….

Vessels…

The Casablanca, Celtic, Cotty, Huntsland, Violet or West or Rose

Islands, Sand Swan, and the Ravens…

All fly the flag of…Cuba

The Pilot, Police 1, 2, or 3, Sky Sea, and the Antara…

All fly the flag of…..Iran

16John Baranello

The United States Department of Commerce...The Bureau of Industry and Security (“BIS”)■ The mission of the (BIS) is to:

– Advance U.S. national security, foreign policy, and economic interests

■ BIS’s activities include:– Regulating the export of sensitive goods and technologies in an effective and efficient manner – Enforcing export control– Public safety laws– Cooperating with and assisting other countries on export control and strategic trade issues– Assisting U.S. industry to comply with international arms control agreements– Monitoring the viability of the U.S. defense industrial base and seeking to ensure that it is capable of satisfying U.S.

national and homeland security needs– Requires us to enforce export controls on dual use goods and technology (primarily commercial goods which

have potential military applications) not only to fight proliferation, but also to pursue other national security, short supply, and foreign policy goals (such as combating terrorism)

– Requires us to enforce sanctions against imports and exports of goods and services to certain Denied / Embargoed Persons

■ During the mid-1970's the United States adopted two laws that seek to counteract the participation of U.S. citizens in other nation's economic boycotts or embargoes. These "antiboycott" laws are the 1977 amendments to the Export Administration Act (EAA) and the Ribicoff Amendment to the 1976 Tax Reform Act (TRA). – The antiboycott laws were adopted to encourage, and in specified cases, require U.S. firms to refuse to

participate in foreign boycotts that the United States does not sanction.– They have the effect of preventing U.S. firms from being used to implement foreign policies of other nations

which run counter to U.S. policy.

17

Requirements…..Concerned with United States Commerce■ The export of goods or services from the United States and the import of goods or services into the United States are

activities in United States commerce ■ In addition, the action of a domestic concern in specifically directing the activities of its controlled in fact foreign

subsidiary, affiliate, or other permanent foreign establishment is an activity in United States commercePrimary Impact■ The Arab League boycott of Israel is the principal foreign economic boycott which impacts U.S. persons■ Each of the following is currently a member of the Arab League:■ Algeria, Bahrain, Iraq, Jordan, Lebanon, Libya, Mauritania, Morocco, Oman, Qatar, Saudi Arabia, Somalia, Sudan,

Tunisia, United Arab Emirates, Yemen, Egypt, Palestine, Comoros, Syria, Djibouti, Kuwait

There are actually three levels of boycott:■ Primary boycott:

– Examples:– Syria refuses to trade with Israel– Kuwait asks a U.S. Company not to ship Israeli goods to Kuwait– …In these examples, U.S. persons may comply, but must report their receipt.

■ Secondary boycott:– Example: Syria refuses to trade with anyone who does business with Israel and develops a "blacklist" of those

trading with Israel

■ Tertiary boycott:– Example: Syria refuses to trade with anyone who does business with names on Syria’s "blacklist"

For the Secondary and Tertiary boycotts, U.S. persons may not comply and must report receipt of requests to comply to the United States Department of Commerce

18

Bank Secrecy Act / Anti-Money Laundering Examination Manual………..updated 2010Trade Finance practitioners must review all documentation to detect:

■ Items shipped that are inconsistent with the nature of the customer’s business (e.g., a steel company that starts dealing in paper products, or an information technology company that starts dealing in bulk pharmaceuticals).

■ Customers conducting business in higher-risk jurisdictions.

■ Customers shipping items through higher-risk jurisdictions, including transit through noncooperative countries.

■ Customers involved in potentially higher-risk activities, including activities that may be subject to export/import restrictions (e.g., equipment for military or police organizations of foreign governments, weapons, ammunition, chemical mixtures, classified defense articles, sensitive technical data, nuclear materials, precious gems, or certain natural resources such as metals, ore, and crude oil).

■ Obvious over- or under-pricing of goods and services.

■ Obvious misrepresentation of quantity or type of goods imported or exported.

■ Transaction structure appears unnecessarily complex and designed to obscure the true nature of the transaction.

■ Customer directs payment of proceeds to an unrelated third party.

■ Shipment locations or description of goods not consistent with letter of credit.

■ Significantly amended letters of credit without reasonable justification or changes to the beneficiary or location of payment. Any changes in the names of parties also should prompt additional OFAC review.

19John Baranello

Indicators of Suspicious Letter of Credit ActivitySuspicious activities or transactions may present themselves in many different forms. The scenarios listed below are considered

to be "Red Flags" that you should be aware of and alert to for possible money laundering activities in Trade Finance:

– Letter of Credit does not provide for a description of the goods, services or technology being furnished,– Transactions that have no apparent business or lawful purpose, are not expected of a particular customer, and the Bank

knows no reasonable explanation for the transaction after examining the available facts,– Changing the Letter of Credit beneficiary name and address just before payment is to be made, including requests for

assignment of proceeds or transfer at the time documents are presented,– Changing the Letter of Credit place of payment,– Standby Letter of Credit fails to reference underlying project or contract, or designates an unusual beneficiary,– A freight-forwarding firm is listed as the products final destination,– The shipping route and destination appears to be abnormal for the product…– Transactions which appear to lack reasonable economic substance or intent,– Inadequate or unreliable information / documentation provided by the client to support a transaction,– Transactions for which the source of funds is not readily apparent and / or is otherwise suspicious,– Unusual transactions involving inherently risky industries or geographical areas where the client typically does not do

business,– Transactions or business opportunities that seem "too good to be true“ or that can not pass the "Smell test“– Transactions which appear to be inconsistent with the clients financial status,– Transactions which appear unnecessarily or unusually easy to complete,– Pricing inconsistent with previous transactions,– Identify trends and patterns,– "…Know, suspect or have reason to suspect unlawful activity…“

20John Baranello

FINCEN – Financial Crimes Enforcement NetworkTo safeguard the financial system from the abuses of financial crime, including terrorist financing, money laundering,

and other illicit activity….

The USA PATRIOT Act

On October 26, 2001, President Bush signed into law: the United and Strengthening America Act by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism

■ This law, known as the USA Patriot Act of 2001, imposes certain requirements with respect to correspondent bank accounts held by foreign banks in the United States

■ Title III of the Act, the International Money Laundering Abatement and Anti-Terrorist Financing Act of 2001, contains a number of sections that have anti-money laundering and anti-terrorism financing implications for financial institutions

■ This act enhances America’s ability to combat money laundering and terrorist activities. Some of the major requirements of the act include:– Requiring the implementation of AML Compliance programs, – AML compliance training for employees,– Establishing standards for Customer Identification Programs – “CIP”– Delineating Enhanced due diligence and information to be collected on Private Bank and Correspondent Bank

relationships for non-U.S. persons,– Prohibiting U.S. banks from maintaining relationships with shell banks– Providing for increased information sharing between and among financial institutions, law enforcement, and

regulatory agencies

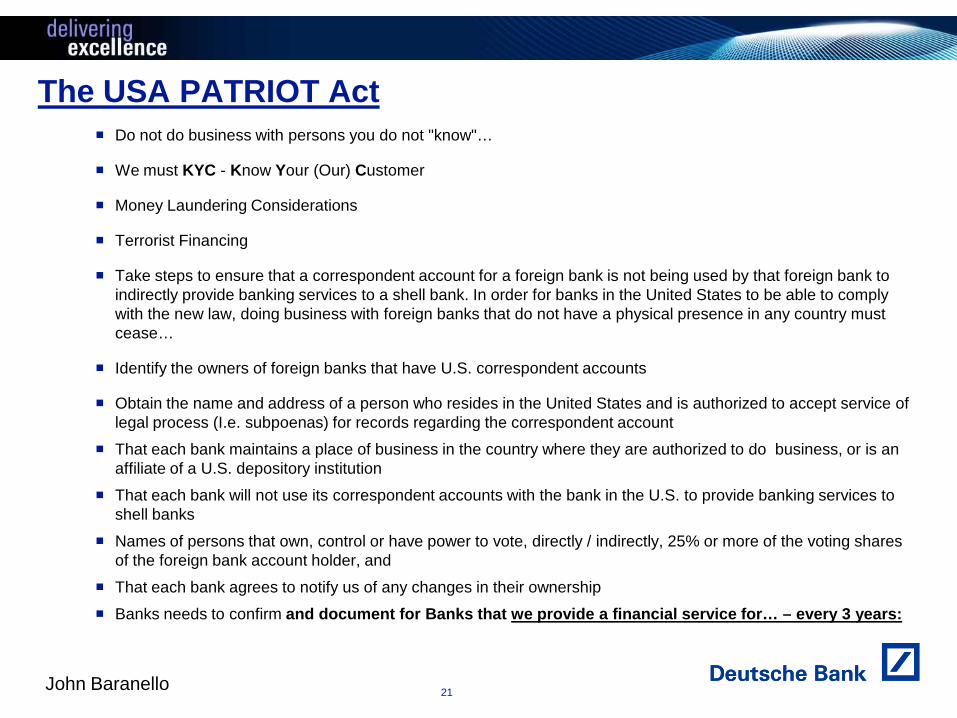

21John Baranello

The USA PATRIOT Act■ Do not do business with persons you do not "know"…

■ We must KYC - Know Your (Our) Customer

■ Money Laundering Considerations

■ Terrorist Financing

■ Take steps to ensure that a correspondent account for a foreign bank is not being used by that foreign bank to indirectly provide banking services to a shell bank. In order for banks in the United States to be able to comply with the new law, doing business with foreign banks that do not have a physical presence in any country must cease…

■ Identify the owners of foreign banks that have U.S. correspondent accounts

■ Obtain the name and address of a person who resides in the United States and is authorized to accept service of legal process (I.e. subpoenas) for records regarding the correspondent account

■ That each bank maintains a place of business in the country where they are authorized to do business, or is an affiliate of a U.S. depository institution

■ That each bank will not use its correspondent accounts with the bank in the U.S. to provide banking services to shell banks

■ Names of persons that own, control or have power to vote, directly / indirectly, 25% or more of the voting shares of the foreign bank account holder, and

■ That each bank agrees to notify us of any changes in their ownership

■ Banks needs to confirm and document for Banks that we provide a financial service for… – every 3 years:

22

Certification Regarding Correspondent Accounts For Foreign Banks – “Patriot Act Certificate”

The information contained in this Certification is sought pursuant to Sections 5318(j) and 5318(k) of Title 31 of the United States Code, as added by sections 313 and 319(b) of the USA PATRIOT Act of 2001 (Public Law 107-56).

This Certification should be completed by any foreign bank that maintains a correspondent account with any U.S. bank or U.S. broker-dealer in securities (a covered financial institution as defined in 31 C.F.R. 103.175(f)). An entity that is not a foreign bank is not required to complete this Certification.

A foreign bank is a bank organized under foreign law and located outside of the United States (see definition at 31 C.F.R. 103.11(o)). A bank includes offices, branches, and agencies of commercial banks or trust companies, private banks, national banks, thrift institutions, credit unions, and other organizations chartered under banking laws and supervised by banking supervisors of any state (see definition at 31 C.F.R. 103.11 (c))*.

A Correspondent Account for a foreign bank is any account to receive deposits from, make payments or other disbursements on behalf of a foreign bank, or handle other financial transactions related to the foreign bank.

*A “foreign bank” does not include any foreign central bank or monetary authority that functions as a central bank, or any international financial institutions or regional development bank formed by treaty or international

John Baranello22

23John Baranello

Export Documentary Letter of Credit Advising Procedure –Final Stage

Applicant(Buyer)

Contract

Issuing Bank

1

2 Letter of Credit Application

3 Letter of Credit Issuance via

SWIFT

4 Letter of Credit Advised

Advising Bank

Beneficiary(Seller)

Advising BankAdvises the credit and any amendment without any undertaking to honour or negotiate, signifying that it has satisfied itself as to the apparent authenticity of the credit or amendment and that the advice accurately reflects the terms and conditions of the credit or amendment received.

24

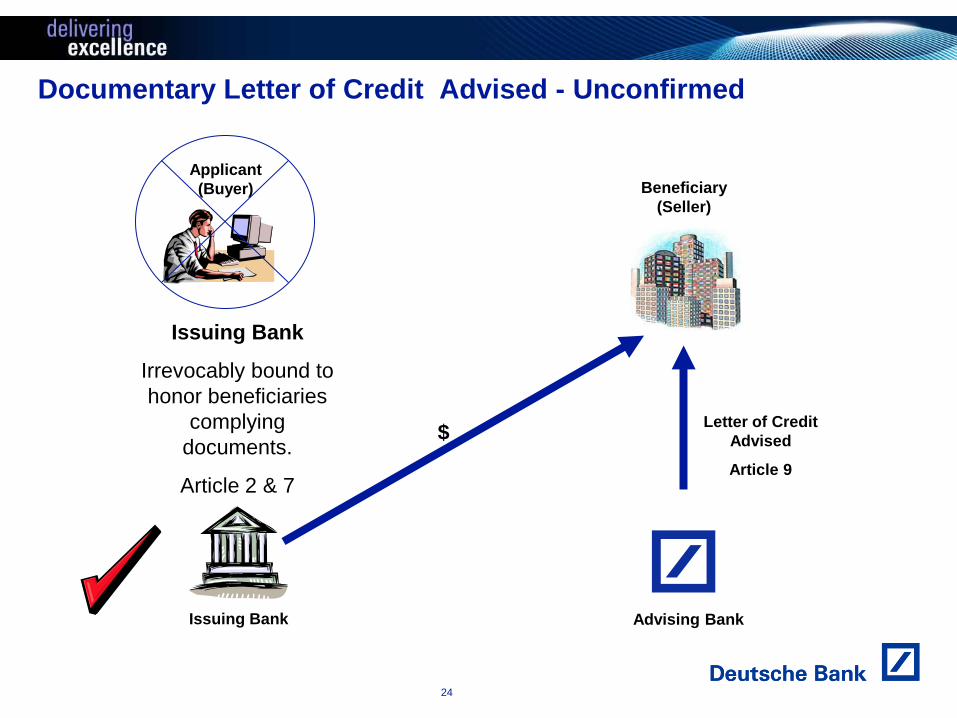

Documentary Letter of Credit Advised - Unconfirmed

Issuing Bank

Letter of Credit Advised

Article 9

Advising Bank

Beneficiary(Seller)

Issuing Bank

Irrevocably bound to honor beneficiaries

complying documents.

Article 2 & 7

$

Applicant(Buyer)

25John Baranello

Documentary Letter of Credit - Confirmed

Applicant (Buyer)

Contract

Issuing Bank

1

2 Letter of Credit Application

3 Letter of Credit Issued via SWIFT

4

Confirming Bank

Beneficiary(Seller)

Confirming Bank Irrevocably bound to honour beneficiaries complying documents. Assumes Issuing Bank risk

Letter of Credit Advised

& Confirmed

26

Documentary Letter of Credit – “Silent” Confirmation

Advising Bank

“Silent Confirmer”

Beneficiary(Seller)

“Silent” Confirming Bank:

Commits to honor beneficiaries complying documents by direct arrangement detailing assumed risks.

Not requested by Issuing Bank to add confirmation.

Issuing Bank is not made aware of this arrangement. $

Issuing Bank

27page 27

Documentary Payment Processing

Goods1

2

Documents

Beneficiary(Seller)

Nominated Bank

Applicant(Buyer)

28John Baranello

Shipping Documents

Transport Documents:Marine Bill of Lading (Document of Title)

Air Way Bill

INVOICEBill Of Sale

DraftPayment Instrument

Certificate of OriginInspection Certificate

Phytosanitary Certificate

Packing/Weight List

29

Trade Transactions are Reviewed for Compliance with:

Department of the Treasury: Office of Foreign Assets Control (OFAC): OFAC Country Sanction Programs OFAC List-Based Sanctions Programs SDN List

Bureau of Industry and Security US Department of Commerce: Denied Person Unverified List Entity List Debarred List Anti-boycott Compliance

Others: KYC Politically Exposed Persons FFIEC - Bank Secrecy Act Anti-Money Laundering Examination Manual, 2010 European Union List

30

Documentary Payment Processing – Non Discrepant DrawingPayable with the Nominated / Confirming Bank

Goods1

2

Documents

Beneficiary(Seller)

Applicant (Buyer)

Sight Payment / Confirmed

A presentation is payable by the drawee on its determination that the documents constitute a complying presentation.

Nominated / Confirming Bank

$3

31

Documentary Payment Processing - Unconfirmed Letter of Credit

Applicant (Buyer)

Goods

Issuing Bank

1

3 Documents

2

Documents

$4

$

5

Beneficiary(Seller)

Advising Bank

32John Baranello

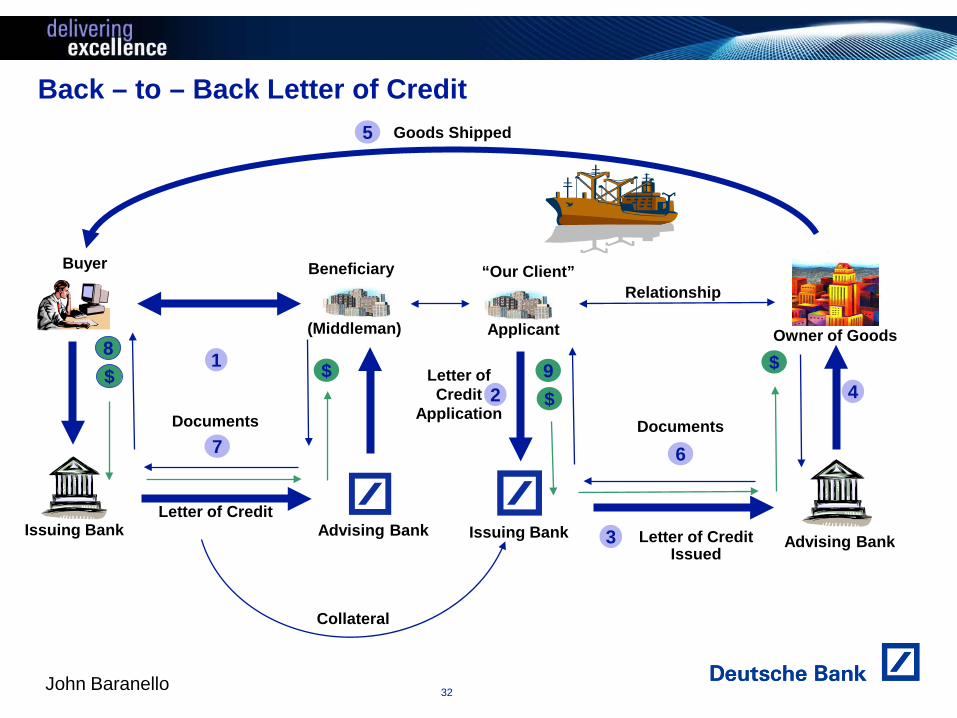

Back – to – Back Letter of Credit

Buyer

Issuing Bank Advising Bank

Beneficiary

Issuing Bank

2Letter of Credit

Application

3 Letter of Credit Issued

4

Advising Bank

Owner of Goods

“Our Client”

Goods Shipped

1

5

Collateral

Letter of Credit

(Middleman)8

DocumentsDocuments7 6

Relationship

$ 9$

$$

Applicant

33

Supplier

Purchase Order

Goods Delivered

Day 2 Day 30 Day 60

Payment TermsProduce & ShipGoods

ApprovedPayables File

Notification of Maturity date

DiscountRequest

ProcessRequest

DiscountedPayment

Debit SettlementPayment

Invoice

1

2

3

4 5

67

8

9

Buyer

Day 1

Day 60 Day 30

Trade Value Chain

Principal

Financial Supply Chain Solution – Supplier Advanced Funds

FSC

34John Baranello

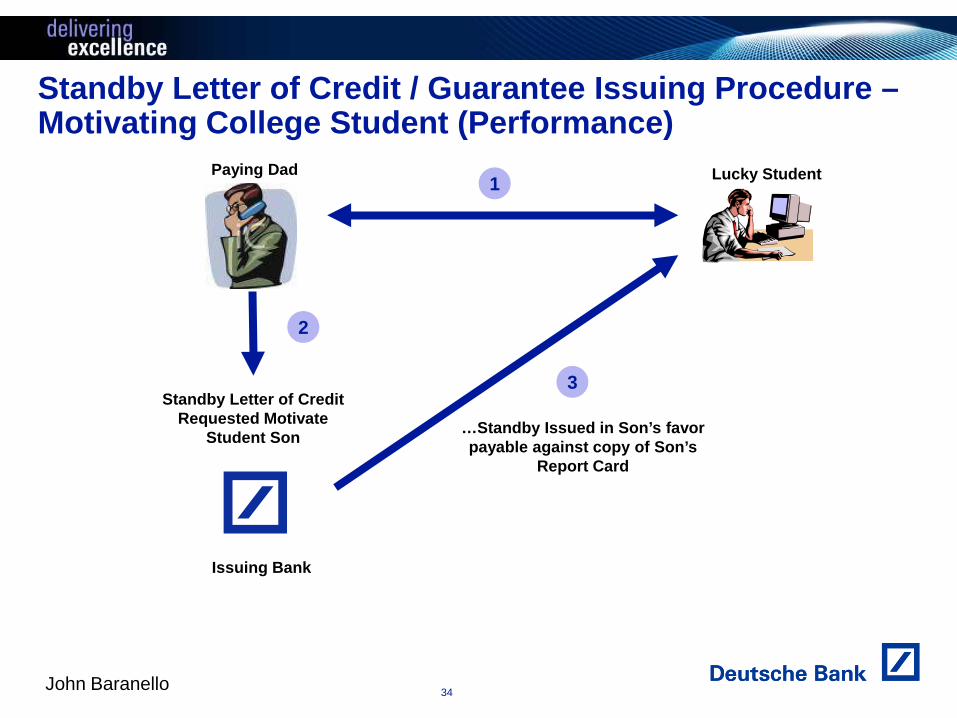

Standby Letter of Credit / Guarantee Issuing Procedure –Motivating College Student (Performance)

Standby Letter of CreditRequested Motivate

Student Son

Issuing Bank

…Standby Issued in Son’s favor payable against copy of Son’s

Report Card

1

3

Lucky StudentPaying Dad

2

35John Baranello

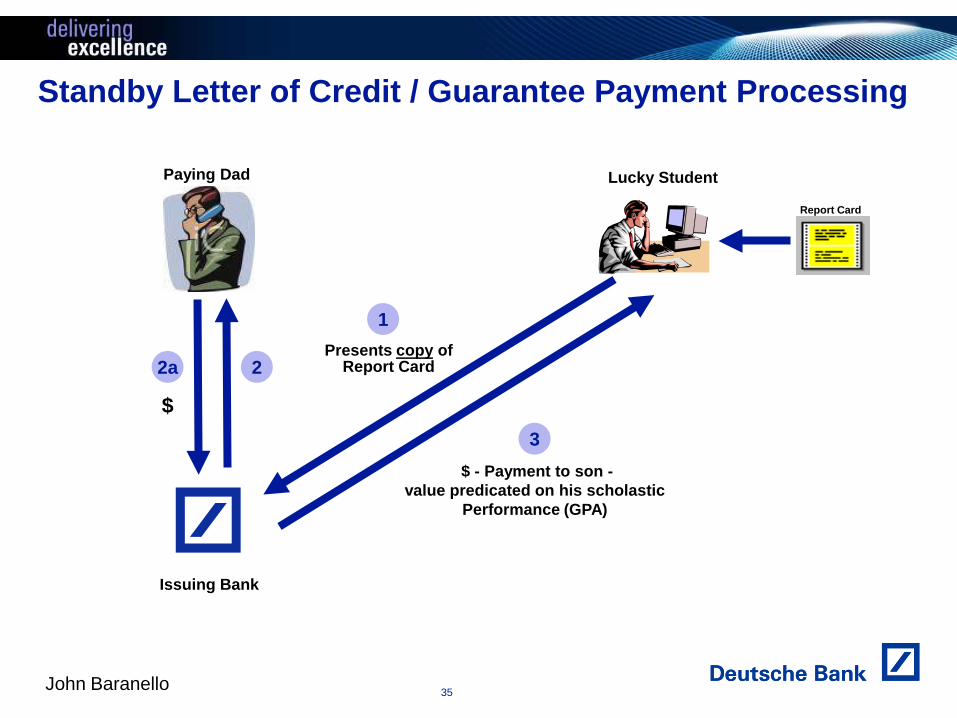

Standby Letter of Credit / Guarantee Payment Processing

Lucky Student

Issuing Bank

2Presents copy of

Report Card

$

2a

$ - Payment to son -value predicated on his scholastic

Performance (GPA)

3

Paying Dad

1

Report Card

36John Baranello

Standby Letter of Credit / Guarantee Payment ProcessingTrading Partners Letter head

Signed and dated Certificate stating:“The undersigned, a purportedly authorised signatory of: (Trading Partner)

• In the case of a Tender Guarantee: the supporting statement could state: •The Applicant (Our Client) has withdrawn its offer during the tender period,

or, while it was declared the successful bidder, The Applicant did not sign the contract corresponding to its offer and/or failed to provide the guarantee(s) requested in the call for tenders.

• In the case of a Performance Guarantee: the supporting statement could state: The Applicant (Our Client) is in breach of its obligations with respect to the underlying relationship because [of late

delivery] [the contract’s performance was not completed by the due date] [there was a shortfall in the quantity of the goods supplied under the contract] [the delivered works are defective] etc.

• In the case of a Payment Guarantee: the supporting statement could state: The Applicant (Our Client) has not fulfilled its contractual payment obligations.

Therefore, the attached draft for: (Currency and value) represents funds due us in accordance with: (the terms and conditions of contract number: , proforma invoice number: , lease agreement, etc….) . and represented by Letter of Credit Number….”.

________________________________________(Trading Partners Authorised Signature)

37

•Issued by the ICC•Effective July 2010 •Replaces the URDG 458•Internationally acclaimed•Consists of 35 articles •Reflects International practice in the use of demand guarantees•Sets out the liabilities and responsibilities of the parties to a demand guarantee•Shares Independence and Documentary nature with the UCP 600 and ISP 98•Details vital phases in the lifecycle of a demand guarantee•Offers model guarantee and counter-guarantee forms

URDG 758 – Uniform Rules for Demand Guarantees

John Baranello37

38

•Independent vs. Dependent

Financial undertaking needed to be independent from underlying transaction

Payment against documents only

•Dependent was not permitted, with some exceptions

•Reason: May be called upon to determine events or facts outside of the documents presented.

•US financial institutions generally could not enter into suretyship transactions as reflected in the National Bank Act

•Concern over Safety and Soundness of US financial institutions

•If the surety is required to pay or perform due to the principal's failure to do so, the law will usually give the surety a right of subrogation, allowing the surety to "step into the shoes of" the principal and use his (the surety's) contractual rights to recover the cost of making payment or performing on the principal's behalf, even in the absence of an express agreement to that effect between the surety and the principal.

•Office of the Comptroller of the Currency – Dissuaded US Banks in issuing dependant guarantees with some exceptions

•Development of Standby Letter of Credit Practice

•Only recently were US banks generally permitted to issue ordinary dependant financial guarantees, but were reluctant to do so.

History of US Law...

John Baranello38

39

•Uniform Commerctial Code, Article 5 (revised) law would apply•US Law is consistent with the United Nations Convention on Independent Guarantees and Standby Letters of Credit•Revised UCC Section 5-116(a) provides that: the jurisdiction whose law is chosen need not bear any relation to the transaction•Revised UCC Section 5-116(e) permits the choice of any forum in which any disputes are to be litigated•URDG 758 - Documentary based – Independent – Tenor and amount limited

US Financial Institutions can enter into Independant Documentary Guarantee Transactions....

John Baranello39

40

Side – by – Side……..

Demand Guarantee•Irrevocable Undertaking•ICC issued Rules Based•Recognized Internationally including the US•Independent of the underlying Relationship•Issued by Guarantor•At request of Instructing Party•In favor of Beneficiary•Guarantor deal with documents and not with goods, services or performances to which the documents may relate•Provide for payment against complying documentary demand•Finite Expiration•Finite Amount•Defined Payment / Documentary Rejection Process•Transferrable / Assignable

Standby Letter of Credit•Irrevocable Undertaking•ICC issued Rules / Articles Based•Recognized Internationally including the US•Separate from sale / contract •Issued by Issuing Bank•At request of Applicant •In favor of Beneficiary•Banks deal with documents and not with goods, services or performances to which the documents may relate•Honor complying documentary presentation•Finite Expiration•Finite Amount•Defined Payment / Documentary Rejection Process•Transferrable / Assignable

John Baranello40

41John Baranello

Foreign Guarantee Issued - Supported by Our Guarantee

GuaranteeRequested To Support

(Foreign) Financial Arrangement

Issuing Bank

Counter GuaranteeIssued in Favor of Our

Foreign Correspondent / Branch

Counter Guarantee Received

Our Client

Guarantee Received

Guarantee Issued Countered by our Guarantee

1 2

Trading Partner

Cross border business arrangement

Business can be conducted

42

John Baranello

Fraud / ScamKey Phrases / Buzz Words

■ Banking Coordinates■ Buy-Sell■ "Cash" Wire Transfer■ C&F ASWP■ Comfort Letter■ "Conditional" Swift Payment■ CUSIP Number■ Cutting House■ X % Performance Bond■ Validation of the MCC

(Master Collateral Commitment)■ Verbiage■ With Full Bank Responsibility■ Zero-Coupon Letter of Credit

■ Discounting L/C’s

■ Due 1, 5, or 10 years and 1 day

■ First-cut Paper

■ Fresh-cut paper

■ Foreign Bank Advice

■ Good, clean, cleared funds

■ Good, clean, cleared funds of non-criminal origin

■ ICC Investment Program

■ ICC Promissory Notes

■ ICC 322 Program

■ ICC 3039/3034

■ International Certificate of Deposit (ICD)

■ Irrevocable Bank Purchase Order (IBPO)

43

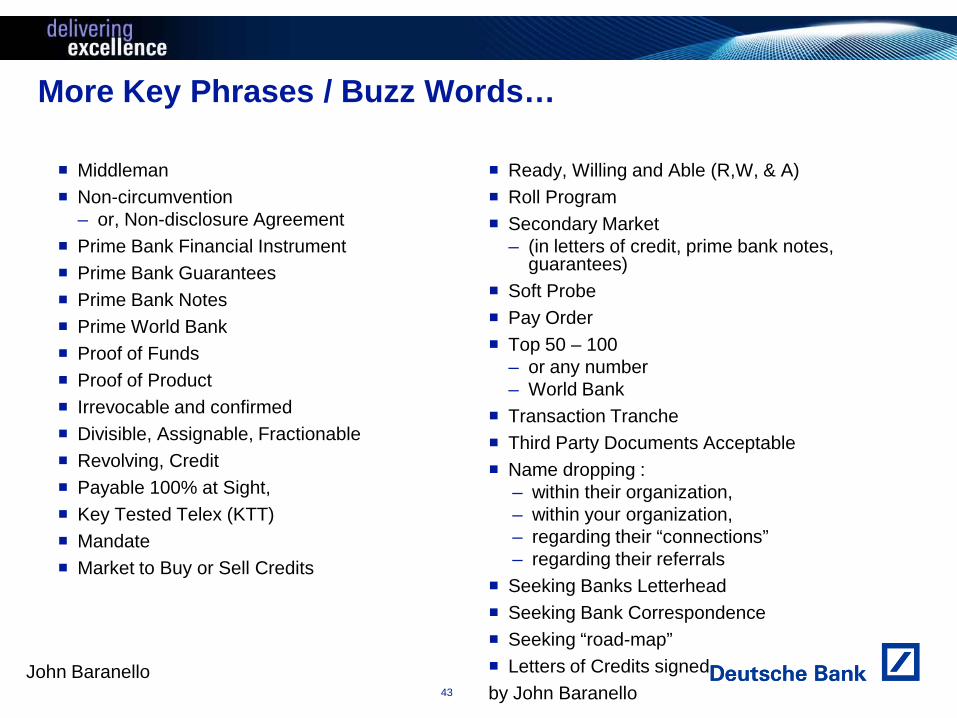

John Baranello

More Key Phrases / Buzz Words…

■ Middleman■ Non-circumvention

– or, Non-disclosure Agreement■ Prime Bank Financial Instrument■ Prime Bank Guarantees■ Prime Bank Notes■ Prime World Bank■ Proof of Funds■ Proof of Product■ Irrevocable and confirmed ■ Divisible, Assignable, Fractionable■ Revolving, Credit ■ Payable 100% at Sight,■ Key Tested Telex (KTT)■ Mandate■ Market to Buy or Sell Credits

■ Ready, Willing and Able (R,W, & A)■ Roll Program■ Secondary Market

– (in letters of credit, prime bank notes, guarantees)

■ Soft Probe■ Pay Order■ Top 50 – 100

– or any number – World Bank

■ Transaction Tranche■ Third Party Documents Acceptable■ Name dropping :

– within their organization, – within your organization,– regarding their “connections”– regarding their referrals

■ Seeking Banks Letterhead■ Seeking Bank Correspondence■ Seeking “road-map”■ Letters of Credits signed by John Baranello

44John Baranello

United States Regulatory Websites….

■ U.S. Department of Commerce:– http://www.bis.doc.gov/about/index.htm

■ U.S. Department of The Treasury Office of Foreign Assets Control (OFAC)– www.TREAS.GOV/ofac/index.html

■ Financial Crimes Enforcement Network (FINCEN)– http://www.fincen.gov/

The information contained herein is strictly for informational purposes only and does not constitute and shall not be construed to constitute anycontractual or non-contractual obligation or liability of Deutsche Bank AG or any of its affiliates, including Deutsche Bank Trust Company Americas(collectively "Deutsche Bank"), nor shall this [brochure/presentation]or the content herein be construed as advice, an offer or a solicitation of anynature whatsoever nor is this brochure or its contents intended to be relied upon by any person. Deutsche Bank makes no representation as to theaccuracy, completeness, or timeliness of such information. Deutsche Bank shall not be held liable for the authentication of or compliance with theinformation contained herein nor does Deutsche Bank assume any obligation to update any such information. No part of this brochure may be copiedor reproduced in any way without the prior written consent of Deutsche Bank. Copyright © 2010 Deutsche Bank AG. All Rights Reserved.

John BaranelloDirectorDocumentary Trade Product Management

Deutsche Bank AGGlobal Transaction Banking60 Wall StreetNew York, NY 10005

Telephone +1 (212) 250-9604, Fax +1 (212) 797-0780E-Mail: [email protected]

Documentary Trade Contact….

John Baranello45