19704135 the BExA Guide to Letters of Credit UCP600 Update 2007

68

British Exporters Association The BExA Guide to Letters of Credit UCP600 – Update

-

Upload

michelesiciliano4467 -

Category

Documents

-

view

24 -

download

4

description

LC HOW TO UCP 600

Transcript of 19704135 the BExA Guide to Letters of Credit UCP600 Update 2007

British Exporters Association

The BExA Guide to Letters of Credit

UCP600 – Update

The BExA Guide to Letters of Credit - UCP600 – Update

1

Contents

Foreword

Introduction to the 2007 UCP600 updated guide

Chapter 1 What is a letter of credit?

Chapter 2 Why letters of credit are used and their limitations

Chapter 3 What the exporter wants

Chapter 4 What the exporter should look out for

Chapter 5 Amendments, How to Avoid Them and How to Obtain Them

Chapter 6 Presentation of documents

Chapter 7 What to do if presentation fails

Chapter 8 And fi nally, commercial realities … … …

Appendix 1 A checklist

Appendix 2 Swift Codes

Appendix 3 Contact details

Appendix 4 Introduction to the 2003 (UCP500) guide

The BExA Guide to Letters of Credit - UCP600 – Update

2

Foreword

The British Exporters Association has for many years prided itself on the work which it has done as a champion of the British exporting community. Much of this work has taken the form of lobbying successive Governments with the aim of ensuring that UK exports are effectively promoted - to the ultimate benefi t of the balance of payments and hence the British taxpayer. From time to time, however, the Association likes to do something for its members that does not require any input from Government. This guide represents one such opportunity.

There are any number of glossy brochures published on the subject of letters of credit. Most of them have one thing in common - they are published by banks! Now, there is nothing wrong with this; banks provide a service which traders require, and their brochures are excellent sources of information on this diffi cult subject. However, there does tend to be a certain slant to the advice which is offered in those brochures, perhaps not surprisingly.

It is my hope that this guide, written with the advice of bankers but essentially by exporters for exporters, will provide a clear and helpful reference work for those of our members who have an interest in getting paid through the mechanism of letters of credit. It is not a book of rules but more a summary of experience, much of it learned the hard way. It is offered to our members in the hope that reference to it will avoid others having to learn the same lessons in the same way!

Sir Richard NeedhamPresident of BExAOctober 2003

The BExA Guide to Letters of Credit - UCP600 – Update

3

Introduction to the 2007 UCP600 updated guide

Since the original BExA Letter of Credit guide was published in 2003 it has gained acceptance amongst users of letters of credit as a practical and readable introduction to a payment mechanism that is believed to be used to support about £350 billion of trade each year. If it has gained more readers amongst importers and exporters (the applicant and the benefi ciary of the letter of credit) than amongst bankers that is probably because bankers (who are paid to operate letters of credit) tend to be better trained in their operation than most other users of them. Of course, speaking from the point of view of the British exporter, this is something to be applauded. Whilst importers and exporters might develop a degree of competence in the subject, the bankers are the professionals and we should be grateful for their expertise; it is something for which we pay, after all.

So, why an updated guide? The International Chamber of Commerce has for some time been working on a revision of UCP500. It has been a major undertaking and is now published as Uniform Customs and Practice for Documentary Credits 2007 Revision (UCP600). It comes into effect on 1 July 2007 and the British Exporters’ Association decided to bring our original guide up to date, to refl ect what will become the new standard rules for the handling of letters of credit. Much of what was contained in the original guide continues to be true. Principles of prudence and common sense are not affected by a change in rules, after all. However, there are a number of changes which we felt should be incorporated in the guide and a complete revision and re-publication was thought to be the most effective way of doing this. Much of what has changed in UCP concerns the banks rather than the applicant or the benefi ciary directly. Indeed, in many respects the changes will only be apparent to the banks. Nonetheless, on the principle of ‘better to be up to date than out of date’ we decided to re-issue the guide.

Why the change?

UCP600 is the latest version of the rules for the handling of letters of credit published by the ICC. The fi rst was published in 1933. A major driver has been to simplify the rules and to reduce the scope for ambiguity in interpretation and avoid simple misunderstanding. Also, in view of the continuing high proportion of non-compliant fi rst presentations there is a need to assist benefi ciaries to prepare ‘better’ documents. To the extent that simplifi cation and added clarity reduce the number of rejections of documents as discrepant, that would obviously be welcome.

More than half of the questions formally answered by the ICC in connection with UCP500 related to seven articles, as follows:

Liability of Issuing and Confi rming Banks

Standard for Examination of Documents

Discrepant Documents and Notice

Unspecifi ed Issuers or Contents of Documents

Marine/Ocean Bill of Lading

Commercial Invoices

Transferable Credits

The articles covering these subjects have received particular attention in the revision.

The BExA Guide to Letters of Credit - UCP600 – Update

4

When does this happen?

UCP500 will continue to apply to letters of credit issued up to and including 30 June 2007. Letters of credit issued on or after 1 July 2007 should be subject to UCP600. It will be possible, but not necessary, to have a letter of credit that has already been issued subject to UCP500 amended to incorporate UCP600. This would be by means of a formal amendment (see Chapter 5). However, unless there are particular reasons to have the letter of credit amended, it would probably be better to allow current letters of credit to run off under UCP500.

A letter of credit issued ‘subject to: UCP current edition’ or similar will continue to be governed by the version of UCP that was current at the date of issue; if that was UCP500 the letter of credit will not automatically become subject to UCP600 on 1 July 2007.

Contributors

The 2003 guide was written with contributions from those named in the Introduction to the 2003 (UCP500) guide at Appendix 4 and most of what they wrote remains valid. This edition was revised with the assistance of:

Russell Brown of Deutsche BankJohn Clegg of ABC International BankDavid Meynall of Deutsche BankSusan Ross of Aon Trade CreditDavid Silverwood of RBS Ray Webb of Aon Forfaitingand I am grateful to them for their patience and understanding.

Three other BExA guides may also be found useful:

• 2004 Guide to On-Demand Contract BondsFor exporters who are obliged to provide bank bonds to support their export contracts. The guide covers the obligations and risks of the parties, includes sample wordings and offers advice in the event that the bond is called.

• 2005 Retention of TitleGetting our goods back if the buyer does not pay is a practical issue and our ability to do so depends upon the detail of the contract. The guide offers practical advice about retaining title and obtaining payment in diffi cult circumstances.

• 2007 Credit InsuranceExport credit insurance. This guide will be published in October 2007.

Richard HillBAE SYSTEMS plcChairman, BExAJune 2007

Copyright & disclaimer

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by other means, electronic, mechanical, pho-tocopying or otherwise without the prior permission of the British Exporters Association.

Whilst every reasonable effort has been made to ensure accuracy, information con-tained in this publication may not be comprehensive and readers should not act upon it without seeking professional advice from their usual professional advisers.

The BExA Guide to Letters of Credit - UCP600 – Update

5

Chapter 1 - What is a letter of credit?

Intention

A letter of credit is a written undertaking given by a bank on behalf of the customer to pay the exporter an amount of money within a specifi ed time frame provided that the exporter complies strictly with its terms and conditions. Payment will depend on the exporter presenting documents that conform to the terms laid down in the letter of credit. The customer’s aim is that he should get the goods that he has ordered, and the exporter’s aim is to receive payment for them.

Security

Generally speaking, a letter of credit is a safer way of obtaining payment than relying on open account payment terms. The essential point is that the payment undertaking is moved from the customer to a bank. It is commonly thought that this represents a more secure source of payment.

It is important to bear in mind that a letter of credit:

• Is separate from the contract to which it relates

• Requires that all parties deal only in documents

• Is not a contract between buyer and seller

• Is not a guarantee that the seller will defi nitely receive payment

• Is not a guarantee that the buyer will receive the goods he ordered

Confi rmation

Confi rmation of a letter of credit is an additional undertaking from another bank, the confi rming bank (usually the advising bank), to pay the exporter on presentation of correct documents in conformity with the letter of credit. To have value to the exporter the confi rming bank should be a bank based in the UK; it thus removes the political risk of waiting for payment from an overseas bank or one of its branches.

There are a number of advantages to the exporter in having a letter of credit confi rmed:

• He has the undertaking of two banks to pay

• The credit risk is reduced to that of the UK bank

• Country risk is eliminated after conforming documents have been presented (NB pre-delivery risk is still an issue; can the exporter produce the documents required?)

The principal disadvantage to the benefi ciary is the extra cost in the form of the confi rmation fee (which is generally paid by the exporter). The confi rmation of the letter of credit only adds to the security for the exporter if the documents (at step 10 below) can be produced.

The BExA Guide to Letters of Credit - UCP600 – Update

6

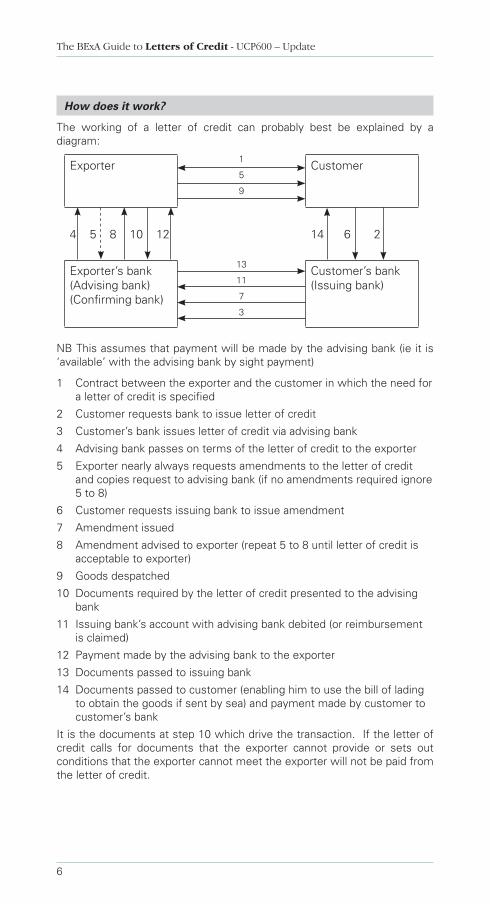

How does it work?

The working of a letter of credit can probably best be explained by a diagram:

Exporter1

5

9

Customer

4 5 8 10 12 14 6 2

Exporter’s bank(Advising bank)(Confi rming bank)

13

11

7

3

Customer’s bank(Issuing bank)

NB This assumes that payment will be made by the advising bank (ie it is ‘available’ with the advising bank by sight payment)

1 Contract between the exporter and the customer in which the need for a letter of credit is specifi ed

2 Customer requests bank to issue letter of credit

3 Customer’s bank issues letter of credit via advising bank

4 Advising bank passes on terms of the letter of credit to the exporter

5 Exporter nearly always requests amendments to the letter of credit and copies request to advising bank (if no amendments required ignore 5 to 8)

6 Customer requests issuing bank to issue amendment

7 Amendment issued

8 Amendment advised to exporter (repeat 5 to 8 until letter of credit is acceptable to exporter)

9 Goods despatched

10 Documents required by the letter of credit presented to the advising bank

11 Issuing bank’s account with advising bank debited (or reimbursement is claimed)

12 Payment made by the advising bank to the exporter

13 Documents passed to issuing bank

14 Documents passed to customer (enabling him to use the bill of lading to obtain the goods if sent by sea) and payment made by customer to customer’s bank

It is the documents at step 10 which drive the transaction. If the letter of credit calls for documents that the exporter cannot provide or sets out conditions that the exporter cannot meet the exporter will not be paid from the letter of credit.

The BExA Guide to Letters of Credit - UCP600 – Update

7

Whilst some of the documents required by the letter of credit will be produced by, and hence be within the control of, the exporter it is important to remember also those third party documents which are most commonly required, that is, those which are not produced by the exporter. These are generally (but there could be others):

• Transport documents, commonly bill of lading or air waybill

• Insurance document (policy or certifi cate)

• Certifi cate of Origin (which may require certifi cation and/or legalisation by an independent body such as a Chamber of Commerce or foreign embassy)

• Inspection Certifi cate

These are discussed in Chapter 6.

UCP600

Reference has already been made to UCP600. The whole document is important and should be considered essential reading for anyone working with letters of credit. Do not think of it as just something that the banks have to know. What follows is a brief commentary on some of the articles.

Article 1 - Application of UCP

UCP600 applies to any letter of credit where it is specifi cally included in the text of the letter of credit. The rules are binding on all parties unless expressly modifi ed or excluded by the letter of credit.

Article 2 - Defi nitions

Provides defi nitions of common letter of credit language, including defi nition of ‘honour’ and ‘negotiation’. It is worth noting that negotiation (ie the bank advancing value to the exporter before payment is due under the letter of credit) can be with or without recourse to the exporter – it is a matter for agreement between them in each case.

Article 3 - Interpretations

A letter of credit is irrevocable even if there is no indication to that effect.

A document can be signed by handwriting or by any mechanical or electronic method of authentication.

Branches of a bank in different countries are considered to be separate banks (but it would be unwise to have, for example, a London branch of the overseas opening bank confi rm the letter of credit).

Article 4 - Credits v Contracts

The letter of credit is a separate transaction from the contract of sale to which it relates. The banks will not be concerned with performance of the contract of sale and the performance of their undertakings will not be subject to claims by the customer regarding the contract of sale.

Article 5 - Documents v Goods/Services/Performances

Banks deal with documents, and not with goods, services and/or other performances to which the documents may relate.

Article 7 - Issuing Bank Undertaking

Provided that the correct documents are presented the issuing bank must honour the letter of credit if a nominated bank (ie the bank with which the letter of credit is available, see Article 12 below) does not do so. In fact, the issuing bank is irrevocably bound to honour the letter of credit at the time it

The BExA Guide to Letters of Credit - UCP600 – Update

8

is issued (hence ‘irrevocable’ letter of credit). Further, the issuing bank is obliged to reimburse the nominated bank; this is separate from its obligation to the benefi ciary.

Article 8 - Confi rming Bank Undertaking.

A confi rming bank has similar obligations to the benefi ciary and to another nominated bank. If a bank is authorised or requested by the issuing bank to confi rm a letter of credit but is not prepared to do so it must inform the issuing bank without delay and may advise the letter of credit without adding its confi rmation.

Article 9 - Advising of Credits and Amendments

By advising the letter of credit or an amendment the advising bank signifi es that it has satisfi ed itself as to the authenticity of the letter of credit or amendment and that the advice accurately refl ects the terms of the letter of credit or amendment, unless it specifi cally advises the benefi ciary that it has not been able to satisfy itself of the authenticity thereof.

Article 10 - Amendments

A letter of credit cannot be amended or cancelled without the agreement of the issuing bank (and confi rming bank, if any) and the benefi ciary.

The terms of the original letter of credit will remain in force until you communicate your acceptance of an amendment to the advising bank. If you present documents which comply with the letter of credit and any not yet accepted amendment you will be accepting the amendment.

Partial acceptance of an amendment is not allowed and would be regarded as rejection of the amendment. You must accept or reject an advice of amendments in whole; you cannot, for example, accept items 1 and 3 but reject item 2.

A provision in an amendment saying that it will become effective unless rejected within a certain time limit would be disregarded. However, a clause in the original letter of credit to the effect that any amendments issued shall become effective if not rejected within x days might be a way around this. You would be wise to reject such a clause in a letter of credit.

Article 12 - Nomination

By nominating a bank to accept a draft or incur a deferred payment undertaking, an issuing bank authorises that nominated bank to prepay or purchase a draft accepted or a deferred payment undertaking incurred by that nominated bank.

Article 14 - Standard for Examination of Documents

Banks must examine a presentation of documents to determine, on the basis of the documents alone, whether or not the documents appear on their face to constitute a complying presentation.

A document presented but not required by the credit will be disregarded and may be returned to the presenter.

Data in a document, when read in context with the credit, the document itself and international standard banking practice, need not be identical to, but must not confl ict with, data in that document, any other stipulated document or the credit.

In documents other than a commercial invoice the description of the goods or services, if stated, may be in general terms not confl icting with their description in the credit. (See Article 18 – Commercial Invoice).

The BExA Guide to Letters of Credit - UCP600 – Update

9

The banks (issuing and advising/confi rming) each have up to fi ve banking days, following the day of receipt of the documents, to examine the documents and determine whether to take up or refuse the documents and to inform the party from which they received the documents accordingly. It used to be the case that the bank had to do this within a reasonable time, not to exceed to seven banking days. Of course, a reasonable time would sometimes be less than seven or fi ve banking days, but now the concept of a reasonable time has gone.

Unless otherwise specifi ed in the letter of credit presentations of documents which include transport documents, eg bill of lading, air waybill, must be made no later than 21 days following the date of shipment as described in those documents (but not later than the expiry date of the letter of credit, ie the expiry date stands regardless of the 21 days allowed for presentation of transport documents).

The addresses of the benefi ciary and the applicant need not be the same as those shown in the letter of credit but must be in the same countries as those shown in the letter of credit. The exception is when the address of the applicant is to appear as part of consignee or notify party details on a transport document. Contact details (fax, telephone, email and the like) stated as part of the benefi ciary’s and the applicant’s address will be disregarded.

Article 16 - Discrepant Documents, Waiver and Notice

If a nominated, confi rming or issuing bank refuses to honour or negotiate a presentation of documents it must give a single notice to the presenter of the documents.

The notice must state:

i. that the bank is refusing to honour or negotiate;

ii. each discrepancy; and

iii. what the bank is doing with the documents (holding them, requesting a waiver from the applicant or further instructions from the presenter, returning them or acting in accordance with instructions from the presenter).

This notice must be given by telecommunication or by other expeditious means, no later than the fi fth banking day following the day of presentation.

If the issuing or confi rming bank fails to comply with the terms of Article 16 it cannot then claim that the documents are discrepant.

Article 18 - Commercial Invoice

The invoice:

• must appear to have been issued by the benefi ciary,

• must be made out in the name of the applicant,

• must be in the same currency as the letter of credit, and

• need not be signed.

The description of the goods or services must correspond with that appearing in the letter of credit.

Article 20 - Bill of Lading

Even if the letter of credit prohibits transhipment, banks will accept a bill of lading which indicates that transhipment will take place as long as the

The BExA Guide to Letters of Credit - UCP600 – Update

10

relevant cargo is shipped in a container, a trailer or LASH barge as evidenced by the bill of lading, provided that the entire ocean carriage is covered by the same bill of lading.

Article 27 - Clean Transport Document

Banks will only accept a clean transport document ie one that does not contain any reference to a defective condition of the goods or their packaging. The word ‘clean’ does not need to appear, even if the letter of credit requires the transport document to be ‘clean on board’.

Article 28 - Insurance Document and Coverage

These must be issued and signed by an insurance company, an underwriter or their agents or their proxies. Cover notes will not be accepted.

An insurance document may contain reference to any exclusion clause.

Article 32 - Instalment Drawings or Shipments

If drawings and/or shipments by instalments within given periods are stipulated in the letter of credit and any instalment is not drawn and/or shipped within the period allowed for that instalment, the letter of credit ceases to be available for that and any subsequent instalments.

Bank inspection of documents

Finally, a few words on what has become known as the doctrine of strict compliance. UCP600 says that banks must examine all documents stipulated in the letter of credit to ascertain whether or not they appear, on their face, to be in compliance with the terms and conditions of the letter of credit. Further, data in a document, when read in context with:

• the letter of credit,

• the document itself, and

• international standard banking practice,

need not be identical to, but must not confl ict with, any other document or the letter of credit (Article 14). You should bear in mind that the concept of international standard banking practice is wider than that enshrined in ICC publication no 645, ‘International Standard Banking Practice (ISBP).

ICC publication no 645, ‘International Standard Banking Practice (ISBP) for the examination of documents under documentary credits’ was published in January 2003 with the aim of explaining how the rules set out in UCP500 were to be applied. Its Foreword says that the result of the use of ISBP ‘should be a signifi cant reduction in the number of documents refused for discrepancies on fi rst presentation’. ISBP is to be updated to bring it into line with the substance and style of UCP600.

In the meantime, whilst it is not uncommon for exporters to complain that examining banks are unthinking in their consideration of the documents presented, we should not lose sight of who is to benefi t from presenting documents which comply with the terms of the letter of credit – the exporter. It therefore is in our interest to do everything that we reasonably can to make sure that our documents are accepted on fi rst presentation. Our fate is in our own hands and one purpose of this guide is to try to improve our success in this regard.

The BExA Guide to Letters of Credit - UCP600 – Update

11

Chapter 2 - Why letters of credit are used and their limita-

tions

Why use letters of credit

Your customer promises to pay you – why do you want a letter of credit? Now, your customer may have every intention of paying you but, when payment is due, be unable to do so. Of course, he may not have every intention of paying you. So, we have two good reasons why you might want a letter of credit. Other possibilities include:

• It may be that it is the normal practice of your customer’s country to provide (and require) letters of credit for overseas payments.

• It may be that the establishment of a letter of credit is the only way in which your customer can obtain foreign currency with which to pay you. In this case it is quite possible that the central bank of your customer’s country will require a local currency payment to be made by your customer to buy the supply of foreign currency, or to satisfy another requirement, perhaps to obtain an import licence.

• A letter of credit provides a good way of demonstrating the customer’s commitment that an overseas payment is to be made (and, incidentally, the contract in respect of which the letter of credit is opened can usefully demonstrate that there is a genuine reason for your customer’s purchase of foreign currency).

• It is not unknown for some countries to require the involvement of a local bank in the payment mechanism for a signifi cant import. This might be for no other reason than to provide fee income for that bank.

Where you use credit insurance to protect your export contracts, you will fi nd from time to time that your credit insurer will require you to obtain a letter of credit to secure payment as a condition of approving cover on a customer with a low credit rating or perhaps for any customer in a particular country. The essential point is that the letter of credit represents a payment undertaking issued by a bank rather than the customer. The bank probably represents a better credit risk than your customer and should have an interest in maintaining its good name for meeting its obligations. It is likely, therefore, to pay you in accordance with the terms of the letter of credit.

What a letter of credit provides, in short, is risk mitigation. It does not remove risk. It offers a more secure means of payment, in most cases, than relying on your customer’s promise to pay. It does not guarantee that you will be paid. It is not a guarantee of payment. Receipt of the advice that a letter of credit has been issued in your favour is merely a stage in the process, not the time for heaving a sigh of relief that all is well.

Their limitations

It would be as well to mention some of the reasons for this note of caution. Exporters working with an experienced customer, through two respected banks, do not obtain total protection. It is not ‘buyer beware’ but the exporter who must be continually alert to the fact that his working capital remains exposed until payment is irrevocably made to his bank account. This section considers some of the issues which can frustrate payment and what might be done to lessen their impact or prevent these diffi culties arising. It does not address clerical or documentary errors which remain the greatest source of delays in ensuring that payment is made under a letter of credit.

The BExA Guide to Letters of Credit - UCP600 – Update

12

You might have a perfectly good letter of credit and still not be paid, because, for example:

• the letter of credit is opened by a bank in your customer’s (or other overseas) country and political events or shortage of hard currency might prevent the bank paying you

• the opening or advising bank becomes insolvent and cannot pay you

• the opening bank refers your documents to your customer for approval before paying you

• you present documents to the bank which do not comply with those required by the letter of credit

• you present documents to the bank which do comply with those required by the letter of credit but you are too late in presenting them

• you are unable to present documents to the bank which comply with those required by the letter of credit

There are circumstances outside the control of all the parties to a letter of credit which may frustrate the contract and the ability of the customer to honour its legal obligations. An exporter might face the risk of an export embargo being enforced either by its own government or the United Nations.

During the Argentinian invasion of the Falkland Islands, the British government imposed an export embargo on goods to Argentina. Similarly, it was agreed through the United Nations that exports to both Kuwait and Iraq should be suspended after the invasion of the former by the latter in 1990. Exporters were faced with the prospect of payments to be made under letters of credit being frozen by the Argentinian and Iraqi authorities. Those companies which had not shipped their goods were unable to do so and there-fore were not in a position to present the correct documentation to the advising bank to secure payment even under a letter of credit which had been confi rmed.

Similar situations can arise when the customer’s country imposes an import embargo which might be a refl ection of economic and political instability. Exporters can only really protect themselves against the losses arising from such events by insuring their contract from the date of contract.

From the perspective of a British exporter the risk of the advising bank’s insolvency should be very much a theoretical risk only, unless the branch of an overseas bank is used as the advising party. The failure of the advising bank though would mean the customer having to cancel the existing letter of credit and making new arrangements for it to be advised by a new bank. In dealing with the branch or subsidiary of an overseas bank which fails, the exporter will be faced with problems similar to that of the failure of an opening bank and will not be protected in the event that the letter of credit has been confi rmed by it.

Remember BCCI? A British exporter was left out of pocket when BCCI, the advis-ing bank for a letter of credit from Taiwan, stopped trading during the period between presentation of the documents (and after it had received funds from the Taiwan bank) but before the exporter had been paid.

It is important not to accept confi rmation by the branch or subsidiary of the opening bank. Confi rmation only makes sense if credit enhancement takes place and that is unlikely when a branch confi rms its parental undertaking.

Confi rmation

You can avoid the worst effects of some of these potential problems by having the letter of credit confi rmed, in the UK or, perhaps, in the EU. This

The BExA Guide to Letters of Credit - UCP600 – Update

13

adds the confi rming bank’s commitment to pay you. It is perfectly possible to have, say, a bank in Germany confi rm a third country letter of credit – the disadvantage in doing so in comparison to a UK confi rmation is that you are merely replacing one political risk with another, not removing the political risk. Now, it may be argued that the political risk of having a German bank confi rm the letter of credit for a UK company is much less than the political risk of the third country bank being able to pay; this is probably so. In that you can be fairly selective in which bank you ask to confi rm we can perhaps disregard the risk that the confi rming bank will also become insolvent (though there is still that risk).

The exporter can also arrange ’silent confi rmation’ of the letter of credit. This is a third party undertaking to pay given by a bank or other fi nancial institution not involved in issuing or advising the letter of credit. Such an arrangement is not contemplated by UCP600, and although most banks will be prepared to consider such a ‘confi rmation’, you should be aware that each request will be considered on a case by case basis. If agreed, the silent confi rmation will be designed to refl ect the specifi c terms and conditions of the letter of credit to which it relates.

With a confi rmation the exporter might assume that all that is now required is for the necessary documentation to be presented to the bank for payment to be made. It is important to remember that if an amendment is requested the confi rming bank is not bound to confi rm that amendment, whether the amendment is originally requested by the exporter or the buyer.

We are therefore left with those issues which could be outside your control (and remain so, notwithstanding that you might have had the letter of credit confi rmed). For example, if one of the documents which you are required to present in order to be paid out of the letter of credit is a bill of lading demonstrating shipment of your goods to the customer’s country and you are unable to ship, a UK bank confi rmation will be of no value to you. You will not be paid.

The FOB trap

In contracts concluded on FOB terms (Incoterms 2000) the customer may have advised that it has nominated a vessel to which the goods are to be delivered. Up to this point the exporter will have incurred manufacturing costs, local transportation costs and will now incur warehousing and other costs until such time as the goods are moved. It is important to remember that contractually the exporter, having signed an FOB contract, is clearly responsible for costs until the goods pass over the ship’s rail at the port of shipment of the nominated vessel. What happens if the vessel either arrives later than the last date for shipment permitted in the letter of credit, or does not arrive at all?

This ‘FOB trap’ has been exploited effectively by government buyers in the past which have insisted on FOB terms but then failed to provide the vessel as contracted.

It is worth noting that UCP600 now provides for the possibility of a charterer to sign a charter party bill of lading (Article 22ai), thus creating another opportunity for your customer to interfere with your payment mechanism.

Credit insurance

It is possible to remove the political risks relating to inability to ship (eg a UN resolution preventing despatch, or the ceasing of diplomatic relations and closure of an embassy prior to the signature of a certifi cate which was to have been issued by the embassy) by insuring your export contracts with a

The BExA Guide to Letters of Credit - UCP600 – Update

14

credit insurer (eg AIG, Atradius, Coface, Ducroire Delcredere, Euler Hermes, Exporters). These are termed pre-delivery risks and you would need to buy cover from the date of contract or the date of receipt of the letter of credit, not just from the date of despatch. Thus, if you are unable to ship for political reasons, whilst you would still not be able to draw on the letter of credit you would be able to claim on your insurance for the net costs (ie after resale of your goods) you have incurred in manufacturing the unshipped equipment.

Open account terms

There are circumstances when open account terms (eg 30 days from the date or the end of the month of despatch) are, for practical reasons, a more sensible option than payment out of a letter of credit. For example:

• Short delivery times might not allow the time necessary for the procedures related to a letter of credit

• Low margins might not be able to absorb the costs associated with a letter of credit or those costs would make your terms uncompetitive

• Long manufacturing times will add considerably to the cost of a letter of credit opened at the start of the process – it might be an option to have the letter of credit opened when the exporter notifi es the customer that the goods will be ready for shipment in the near future (of course this carries the risk that the letter of credit will not be opened)

There is no such thing as total protection

It has to be recognised that it is not possible to protect against every contingency. However, by ensuring that the original contract is unambiguous, that solvent and competent banks are involved in the letter of credit transaction and that insurance is applied effectively, an exporter will minimise the risk of loss when working beneath the umbrella of a letter of credit. There are times when the exporter will feel very exposed with no help available from his bank or insurer but, by contracting prudently and seeking advice, these occasions should be rare.

It should not be thought, after reading the last few paragraphs, that a letter of credit has no value. It is a very valuable tool but it does not exist in isolation from the world around it. In most cases you will depend upon other documents and the actions of third parties to make it work. Making it work as you require involves considerable care and attention on the part of the exporter. That means that when the advice of the letter of credit arrives, the next stage of the work begins.

What happens if your buyer goes bust before despatch? Can you still draw down on the letter of credit? In theory ‘yes’ because the letter of credit is an independent instrument. In practice, you may not be able to access this benefi t. If the terms of delivery are FOB, this means that your customer is obliged to nominate the vessel and pay the freight. Which carrier will agree to provide a shipping service to a company that is already bust? Similar problems will be apparent with all delivery terms except DDP – and even DDP will require signature confi rming delivery, and this assumes that the insolvency practitioner managing your customer’s affairs is continuing to trade. The letter of credit only really covers the insolvency risk of your customer from the moment that documents are successfully presented.

The BExA Guide to Letters of Credit - UCP600 – Update

15

Chapter 3 - What the exporter wants

The exporter’s interests

It is a useful rule to bear in mind that no one will look after the exporter’s interests like the exporter. The customer will have his own interests at heart (which may or may not coincide with the exporter’s) and it would be unwise to expect the banks involved to put the exporter’s interests above their own. In short, if you want a job doing properly, you have to do it yourself.

It is not enough simply to receive a letter of credit. You need to ensure that it is written in such a way that you will be in a position to provide the documents required by the letter of credit, and which comply with its terms, to receive payment from the paying bank. It is important that the number of documents required by the letter of credit which are to be produced by third parties is kept to a minimum (and ideally all documents, except the transport and insurance documents, should be capable of being produced by the exporter).

To confi rm or not to confi rm?

Probably the fi rst decision for the exporter when negotiating a contract where payment is to be by letter of credit is whether he wants the letter of credit confi rmed. There are two points of view here.

The case for confi rmation

For the best security, it is essential for the letter of credit to be confi rmed by a UK based bank and payable in the UK. This ensures that you can deal directly with the bank responsible for checking the documents and, if in order, paying you. A letter of credit available with the advising bank but not confi rmed by them will enable the advising bank to check the documents but only pay the exporter if it holds funds of the issuing bank which could be debited or receives funds from a named reimbursing bank. The documents would have to be presented through the advising bank to the overseas issuing bank for them to check the documents and pay, or not, as the case may be. Once you have made the decision to require a letter of credit, it is much simpler and more effi cient to deal with a paying bank in London than a bank in the customer’s country, although the confi rmation of a letter of credit will result in an additional cost to you.

It is essential that you select the right confi rming bank for the letter of credit. Different banks have different appetites for risk. Some are very cautious and others more bullish. If the advising bank or your house bank will not confi rm a letter of credit, you may be able to arrange a silent confi rmation with a third party bank or fi nancial institution.

Whilst talking to prospective confi rming banks, you should ask them which local banks in your customer’s country would be acceptable to them as issuing banks. There are many issuing banks that do not represent an acceptable risk to UK confi rming banks. It is important to identify a local bank with which both your customer and the prospective UK confi rming bank can work. Good correspondent relations between the opening bank and the advising/confi rming bank can be very important in the operation and success of a letter of credit transaction, and may signifi cantly affect the bank charges. It will often be the case that the customer will have only one bank; that bank will probably only be willing to use one of its usual

The BExA Guide to Letters of Credit - UCP600 – Update

16

correspondent banks to advise letters of credit – it may have only one corresponding bank in the UK. If feasible (and acceptable to your customer) you should investigate using a reputable and reliable banking group with offi ces in both the UK and your customer’s country: this can lead to advantages in terms of speed and effi ciency, and may even mean a reduction in the overall charges payable by you and your customer.

Sometimes the issuing bank will not be willing to request a bank to confi rm its letter of credit. You should check this possibility with a UK bank with branches or other presence in your customer’s country. If this proves to be the case your bank may well be able to advise you how to overcome the problem and whether you should request any specifi c wording to be included in the letter of credit when issued to ensure you can still enjoy the advantage of a confi rmation, albeit ’silent’ in this case. With a silent confi rmation, the issuing bank is unaware of the existence of the confi rming bank. The confi rming bank contracts with you to pay you only if the issuing bank does not honour its agreement to pay – eg within 30 days of acceptance of conforming documents. In all probability, the letter of credit would need to be available by negotiation by any bank.

The case against

That is the case for confi rmation; get the documents right and to the UK bank in time and you will be paid by the UK bank. The other point of view is that confi rmation is not necessary, or is necessary only in some circumstances. Either the extra cost of the confi rmation is too much to bear in the price or perhaps the fact that you will be asking a UK bank to confi rm your customer’s bank’s undertaking to pay will not be regarded favourably by your customer. In any case, there will be confi rmation fees to pay.

Credit insurance

One method of mitigating the risks of non-payment under an unconfi rmed letter of credit is to insure your export receivables. In the UK the main export credit insurers are AIG, Atradius, Coface, Ducroire Delcredere, Euler Hermes and Exporters. They offer insurance of export contracts either from the date of contract (pre-credit risk) or from the date of despatch and invoice of the goods or invoicing for the services (credit risk). They tend to look for a spread of risk (wanting to cover all your exports rather than only those to the more risky markets of the world) but this does not necessarily mean that the insurance cost need be prohibitive. The premium rate per £100 of business will tend to fall if a good spread of business is insured; the insurer earns enough on the ‘good’ markets to allow for the lower overall premium rate also to be applied to the more challenging markets.

The terms of cover vary between insurers. Some offer full non-payment cover, treating the letter of credit as a means of payment (which it is), while others provide only political risk cover (such as for shortage of foreign exchange) in letter of credit transactions. You are recommended to seek advice from an insurance broker as to the best option for your export trade.

The BExA Guide to Letters of Credit - UCP600 – Update

17

If insurance starts at the date of contract then you would be protected from the risks associated with your inability to produce the documents necessary to allow you to be paid from a letter of credit because of events outside your control which occur before you ship. This cover is generally suitable for exporters who make goods to order; a claim is calculated after the goods are re-sold or otherwise disposed of. Unless your customer is a government, pre-credit risk insurance would not protect you against the failure by your customer to have the letter of credit opened. If your goods are not made to order then you may feel comfortable with this risk – if you are unable to supply the goods to your customer they can be used for another order.

The insurer will usually be content to exclude from cover the payment risk where you hold a confi rmed letter of credit. This allows the exporter to choose when to seek confi rmation and to compare the confi rmation fee with the insurance premium for the credit or payment risk.

When to ask for a letter of credit

How do you know whether payment by means of a letter of credit should be requested? This will depend upon:

• The territorial conditions – eg as advised by Croner’s, D&B, Coface@rating, your bankers.

• Any credit insurer’s security requirements for the country.

• The creditworthiness of your customer (and/or your credit insurer’s view of your customer).

Getting the letter of credit right

Regardless of whether the letter of credit is confi rmed you will need to ensure that the letter of credit refl ects the terms of the export contract.

The letter of credit should be valid for the duration of the despatch period under the contract plus the agreed time for presentation of the documents. The contract of sale should stipulate the documents to be presented and the letter of credit terms should refl ect the contract’s requirements. This is important; in the case of a discrepancy between the terms of the contract and those of the letter of credit the exporter will have a contractual obligation to fulfi l, but the bank (advising, opening or confi rming) will refer only to the terms of the letter of credit. There should be no confl ict between the two.

Sight or tenor?

You will normally want to be paid immediately following presentation of compliant documents – at sight – unless you have agreed otherwise with the customer. The letter of credit will show clearly whether or not payment is at sight. If the letter of credit states ‘payment at 30 days from the date of the bill of lading’ for example, you will have to wait 30 days before you are paid. On the other hand, a confi rming bank may agree to discount the amount due and pay you immediately. Check this possibility with the banks at an early stage. At the same time, check the banks’ costs for this discount; they can vary considerably and they will come out of your profi t margin unless you are able to build them into your contract price (together with the other letter of credit fees). It pays to shop around with the confi rming or advising bank and with other banks, fi nancial institutions or forfaiters.

When do you want the letter of credit?

You will certainly want the letter of credit to be issued, with terms and conditions acceptable to you, well before shipment, particularly if you are

The BExA Guide to Letters of Credit - UCP600 – Update

18

exporting to a new customer. If you have to start a manufacturing process shortly after contract signature but before the letter of credit is issued in order to meet a shipping deadline, you must think very carefully about the implications of undertaking costs which may not be recoverable from the customer, under a contract for which you have no means of payment in place.

Expect the unexpected

Bear in mind that despite all forward planning, a letter of credit is rarely issued with all terms and conditions acceptable fi rst time around. There is nearly always something that needs changing. The point is, all this takes time and you should take this into account when setting the date you want the letter of credit in your hands and in good order.

Begin at the beginning

Leading exporters advise that the time to start making sure that the letter of credit is right is at the time of quotation. We all know that only a proportion of quotations end up as fi rm contracts, but it is important for this stage to be right – what value is a contract if there is no hope of getting paid?

Your sales team will need to have a requirement written into their procedures that they should check with the credit department before making quotations for export sales. They will need to offer the potential customer a price that will refl ect the payment terms (to include the cost of credit and any risk protection premium/fee as well as the freight and insurance and other overhead costs).

The quotation must clarify:

• the time period for making delivery,

• the terms of delivery,

• the credit period (including when the credit period starts), and

• any security for payment such as a letter of credit.

It is important that, at the stage of quotation, the responsibilities for payment for any changes or extensions to the letter of credit are clear. The person who will have responsibility for ensuring that the funds are drawn from the letter of credit will need to be given the opportunity to comment on any quotation where payment is to be by letter of credit. This person must have the tools and authorities for getting the letter of credit into a workable document.

Will you get the transport documents you need?

When supplying goods to unfamiliar countries, it is imperative that your forwarding agent and/or shipping line has sight of the letter of credit in its entirety at the earliest opportunity. It may be that the shipping line is unable to comply with one or more of the documentary requirements, in which case you might need either to change your shipping line, or request an amendment. Your shipping line’s clear understanding of the terms of the letter of credit and its conditions is critical to the success of your presentation of documents and hence being paid.

It all takes time

It is important to know something about your customer’s country and its requirements. The salesman is likely to have discussed with the production manager and shipping department how much time is needed for production and delivery. It would be wise to spend time at this stage thinking about what sort of documentation will be needed to fulfi l the terms of any quotation

The BExA Guide to Letters of Credit - UCP600 – Update

19

that becomes a fi rm contract. Documents that require any form of authentication by a Chamber of Commerce or similar authority will add to your costs.

For example, inspection by SGS or Cotecna may be necessary for the customer’s country – you can check this in Croner’s. Even if you do not make reference to either body, or provision for pre-export inspection in your contract, it will be necessary in order for you to be able to be paid from the letter of credit. You may wish to consider, therefore, subscribing to Croner’s export guide in order to maintain your knowledge of which countries require what.

Many African and South American countries require inspection, and some Far Eastern countries are increasingly requiring it.

It is important that, when the letter of credit arrives, you have planned to be able to produce the documents required.

In Bangladesh and India, experienced exporters will know that a customer paying using a letter of credit will often require a number of documents which we might believe to be excessive. These may take some time to assemble and will add to your costs.

The letter of credit wording should refl ect the terms stated in the contract of sale (and possibly follow the wording of the quotation). This will need to be checked.

What part does the sales contract play?

One of the main purposes of a written contract is to set out, clearly and unambiguously, what each party to it is supposed to do, and when, in order to get the job done to everyone’s satisfaction. There is no reason why the contract should not also set out the requirement for a letter of credit and its contents. There are a vast number of possibilities as to what a letter of credit can say; the wording is crucial for its successful use so it is clearly necessary to spell out in the contract exactly what should appear in the letter of credit. It may be that there are commercial pressures operating against the wish to include the details (and even a specimen of the wording) of the letter of credit in the contract – we can imagine the salesman’s response ‘… but we don’t want to upset the customer by spelling out the details of the payment arrangement…’. It may be that your negotiations with the customer in the course of settling the wording of the contract have been particularly long and stressful. In these circumstances there is usually everything to be said for spelling out the details. Remember, you have a right to be paid.

It may be easier said than done to get the right things agreed but it would be foolish to hope that the customer or his bank, or even the exporter’s bank, will look after the exporter’s interests. Only the exporter can be truly responsible for ensuring that he is paid; he is neglecting his duty (and his shareholders) if he does not try his best to achieve this.

The exporter should therefore arrange for at least the following items to be spelled out in the contract:

Names and addresses of the banks which will issue and advise the letter of credit

Details of the proposed opening bank should be cleared with the exporter’s bank just in case there are any problems between the two. It is useful if the

The BExA Guide to Letters of Credit - UCP600 – Update

20

two banks have a “correspondent” relationship. The exporter’s bank will expect the letter of credit to state that it is governed by UCP600. In order to ensure more speedy and effi cient processing it is benefi cial if the letter of credit is issued using SWIFT: the Society for Worldwide Interbank Financial Telecommunications, a secure system for passing messages, payment instructions, etc., between banks internationally.

When the letter of credit is to be opened

Many exporters leave it too late before requiring the letter of credit to be opened, with the result that there is too little or no time to correct the inevitable mistakes, and the value of the letter of credit is largely lost. The surest way in which to require a letter of credit to be opened is to have a clause in the contract called an effectiveness clause and to include a reference to the letter of credit in it. Such a clause delays the coming into effect of the signed contract until the items specifi ed in the clause have been complied with. If one such item is receipt of a letter of credit with the details as specifi ed in the contract (or in a form approved by the exporter) then the customer has an incentive, when requested by the exporter, to correct the mistakes which will inevitably appear.

All dates in the contract will need to be expressed as periods from the date of contract effectiveness to ensure that pressure on the parties is maintained. Other items which can be referred to in the effectiveness clause might include issue of an export licence, an import licence and receipt of a down payment. There will need to be an end-stop date so that if any of the items is not procured by then, either party will have certain rights, one of which may be the ability to get out of any obligations early before further problems arise.

If you are using credit insurance, take care to read any conditions requiring letter of credit security: is the letter of credit required to be opened “before despatch” or must it be ’at date of contract’?

Documents: who issues them and who signs them

The law books are full of cases involving the use of documents which one side says were wrong. Several principles should be followed by the exporter to reduce the risk of becoming the latest interesting case for debate in the courts.

The best arrangement is for the documents to be produced and signed by the exporter only, because they are then within his control. If they are to be provided by an independent third party, it is necessary to ensure by checking fi rst that the documents as specifi ed can be made available within the requisite time-scale.

The worst arrangement for the exporter is for a document to be provided or signed by the customer or someone acting for him because this removes the safeguard to the exporter which a letter of credit can provide, and gives the customer the chance to delay payment for his own reasons which may have nothing to do with the exporter’s performance of the contract. ISBP article 4 states that a credit should not require a document that is to be issued or countersigned by the customer, but if it does, the exporter must bear the risk of failure.

Safe achievability of dates

A letter of credit must specify certain dates and periods such as the expiry date for presentation of documents. If the period for presentation of shipping documents is not specifi ed UCP600 sets a maximum of 21 days

The BExA Guide to Letters of Credit - UCP600 – Update

21

from the date of shipment (Article 14c). It therefore makes sense for the exporter to propose his own dates and periods for agreement with the customer and inclusion in the contract so that they can then appear in the letter of credit. Delays, particularly by third parties, are common so safety margins should always be included when agreeing dates. It should be remembered that short journeys by sea can be completed before the paperwork is ready – a delay in presenting the bills of lading and other documents to the bank (even within the 21 days) could lead to the goods being held at the port of discharge with costs of storage (demurrage) being incurred for the consignee. In these circumstances it is worth considering avoiding sea transport (where the original bill of lading has to be presented by the consignee in order to take delivery) and instead choosing alternative methods of transport such as road transport.

Attention to detail

The purpose behind getting all the details clearly spelled out in the contract is that these will provide a fi rm basis for getting the letter of credit put right when it is issued. Once the exporter accepts the letter of credit, it must be remembered that to be paid he has to comply exactly with its requirements even if they are wrong or even impossible. The English Courts have developed the doctrine of ’absolute compliance’ with the requirements of the letter of credit. ‘Almost’ right will not do, so even the most trivial of differences between the wording of the letter of credit and the wording of documents could permit a bank to withhold payment. This is not to say that exact literal compliance in all circumstances is required, but to be safe the exporter should work on the basis of providing documents which do comply absolutely with the terms of the letter of credit.

Some exporters believe that their relationship with their bank will ensure that this harsh doctrine will not be applied in their case. They should not rely on this belief because the interests of the bank and the exporter are different, and the bank will expect the exporter to comply with the wording of the letter of credit.

One British exporter received a letter of credit covering the 10% advance payment under the contract as well as payments for the balance of the contract price. The docu-ments required for the advance payment were:• Commercial invoice for the value of the advance payment, and• Copy of customer’s receipt for the advance payment guarantee.Now, whether it was wise for the exporter to provide the customer with the advance payment guarantee before the advance payment was received might provide the mate-rial for a separate discussion. The advance payment guarantee was given for a value of £12,800,000.00. The contract price was £128,000,032.00. The bank initially refused to pay the advance payment because the advance payment guarantee was not for the same amount as the advance payment (£12,800,003.20). They agreed to pay after the exporter pointed out that the letter of credit did not require the advance payment guarantee to be for the same amount as the advance payment. The point is that for the sake of £3.20 a payment of £12.8 million nearly failed.

There is no substitute for the most intense attention to detail:

• when setting out the requirements in the contract,

• when approving the letter of credit at the beginning,

• when preparing the documentation for presentation and payment.

The BExA Guide to Letters of Credit - UCP600 – Update

22

Summary

• Request a confi rmed letter of credit (or arrange confi rmation yourself) or consider insuring the payment risk

• Consider insuring the pre-credit risk

• Choose the right UK bank to confi rm or consider silent confi rmation

• Pay very close attention to all the conditions of the letter of credit – the banks will

• Make sure the letter of credit works for you

• Ensure the letter of credit payment terms refl ect those in the export contract

• Are you happy with deferred payment terms? Can you discount for cash on a non-recourse basis?

• Have you included ALL letter of credit costs in your price?

• Identify which local banks are acceptable to your confi rming bank (remember that if the same banking group handles the transaction at both ends this may be quicker and cheaper)

The BExA Guide to Letters of Credit - UCP600 – Update

23

Chapter 4 - What the exporter should look out for

Before the letter of credit is issued

Fees

There is no rule as to who (exporter or customer) pays for the cost of the letter of credit. The only certainty is that the banks involved will request fees for opening, advising (the original and any amendments), confi rming and paying. The most common arrangement is that the customer will pay the costs of the opening bank and the exporter will pay the costs of any other bank involved.

Confi rmation charges

The largest single letter of credit cost for the exporter is the fee charged by the confi rming bank for confi rming the letter of credit. The custom is for the confi rmation fee to be charged from the date the letter of credit is advised to you, to the date the fi nal drawing is paid. The bank may calculate this fee on the value of the letter of credit, but more commonly calculates it quarterly on the undrawn balance outstanding at the beginning of each period; the fee may be charged either in advance or in arrears.

Some banks may agree to charge confi rmation fees for the fi rst quarter and then monthly thereafter. Always consider the timing of your deliveries as to whether or not they may run into a new quarter by a small margin of days, as this could have a signifi cant effect on your confi rming fees.

One way to reduce this fee is to shop around when selecting a confi rming bank – fees will vary one from another. This might not always be possible; certainly your ability to drive a bargain with a confi rming bank will to a degree depend upon the size of your business. You may fi nd it is the case that a UK bank with a long standing and mature presence in the country or region of your customer will tend to charge less than another bank with less experience in the country. On the other hand, however, it might be the case that you will get a better deal overall if you put all your letter of credit confi rmations to one bank.

Another way to reduce the confi rmation fee is to delay the point at which your UK bank adds its confi rmation until close to the date of shipment. This runs the risk, of course, that by that time the circumstances of the customer’s country or the bank’s relationship with the opening bank may have deteriorated such that the cost of confi rmation has risen from the estimate at the time of the contract or that it is no longer possible to obtain a confi rmation, at any price. This might suggest that it would be unwise to delay the confi rmation; if it is needed it should be obtained as soon as possible.

The important thing in all of this is always to seek to understand your risks so that you can manage them properly and cost effectively. Although you can’t afford to take unnecessary or unacceptable risks, neither can you afford to incur unnecessarily high costs. You will often fi nd that there is a balance to be struck between the cost and the value of the service you receive from the confi rming bank.

The preferred local bank

Your customer may resist your suggestions for acceptable local banks to issue the letter of credit. You should try to give him as wide a range as possible, and, if you are to have the letter of credit confi rmed, this may require you to go to a number of UK banks acceptable to you, who between

The BExA Guide to Letters of Credit - UCP600 – Update

24

them cover four or fi ve local banks. You will fi nd the Bankers Almanac helpful in this respect. If you are not going to seek confi rmation then the decision is one for you (or your credit insurer): are you content to take the risk on the local issuing bank? If the customer insists on a particular bank opening the letter of credit and you cannot fi nd a UK bank willing to confi rm that bank’s letter of credit you should think very carefully indeed as to why this might be and consider the risk of taking the letter of credit without confi rmation. If your credit insurer also is unwilling to give cover on the basis of a letter of credit issued by that bank you have a very clear indication that you should not be willing to take the risk.

In doing so, you would have to be able to answer the question:

’What do I know about this bank that makes me comfortable with their risk when my bank (and credit insurer) is not?’

Extraneous documents

Your customer may require you to provide a document under the letter of credit that you have never heard of. Check with your bank if they are familiar with it and if there is anything for you to worry about. Such documents, for example a Phytosanitary Certifi cate issued by the UK Forestry Commission stating that the packing materials do not contain disease, are diffi cult (nearly impossible) to obtain and should not be a requirement of the letter of credit. You may of course agree to send your customer this certifi cate separately as it is required in certain countries to demonstrate satisfactory treatment of wooden packing materials, and your agreement to do so may be included in your contract. In this case a satisfactory compromise could well be that you agree to include in the documents to be presented under the letter of credit your written statement confi rming that the relevant certifi cate has been or will be sent to the importer. It is quite easy to draft such a document but it is advisable to seek guidance from your bank to ensure that it is acceptable.

When the letter of credit should be issued and what

happens if it isn’t

You should make clear at the earliest stage, (include it in your bid), your requirements for the timing of the issue of the letter of credit. You should generally want it, with terms and conditions acceptable to you, shortly following contract signature. Thirty days is quite reasonable and is the period of time that is typically given for the issue of any related advance payment guarantees. This is where the effectiveness clause of the contract comes into play.

A contract signed without a payment structure in place will lead to diffi culties later on. Furthermore, unless you have included an effectiveness clause in your contract (that relieves you from the obligation to do anything under the contract until the letter of credit is in place), you may be obliged to begin work on the contract, spend money, and manufacture perhaps specifi cally for this customer, without an acceptable payment structure in place. If the letter of credit does not materialise and you have manufactured goods specifi cally for this customer with limited or no potential to be sold elsewhere, what do you do? Do you ship and hope he pays you effectively on open account terms because you have been assured everything will be put right (in which case why didn’t the letter of credit appear?), or do you sit tight?

The BExA Guide to Letters of Credit - UCP600 – Update

25

Bear in mind that the customer may hold your advance payment bond or performance bond and cash it if you fail to perform even though the letter of credit has not been opened or is in an unacceptable format. This illustrates the need for any bond wording to state that the bond comes into effect only when the contract comes into effect (or when a satisfactory letter of credit has been received if there is no proper effectiveness clause in the contract). Just as the letter of credit is separate from the contract of sale, so is the bond separate.

It may be that sitting tight or lack of action is the best option in these grim circumstances. If the customer really needs your equipment, he will fi nd a way to pay for it and while the goods are under your control, you have a degree of leverage.

In straightforward contracts which do not require export and import licences, down payments or bonds etc, a simpler alternative to an effectiveness clause is to state in the proforma invoice that delivery time is calculated as x weeks from receipt of an acceptable letter of credit. This may be more acceptable to your customer. In addition this option would enable the exporter to include less of a margin in his delivery time, possibly making his quotation more attractive in terms of delivery. Comparisons between competitors are often made on this basis.

Expiry date of the letter of credit

Some customers are renowned for trying to get exporters to agree to accept a letter of credit with a shorter expiry date than is required to cover the payment plan. They will often quote their ’rules’ and ‘procedures’ as justifi cations. Again, be very careful before agreeing to this. You would be taking a signifi cant risk by not insisting that all your payments are covered by the letter of credit. Clearly, however, there is a balance to be struck between insistence and losing your competitive edge by quoting an unrealistic delivery time that compares badly with that of your competitors.

Third party shippers

During contract negotiation you should ascertain whether or not all the equipment you are proposing to supply is to be shipped by you or whether another company will ship some of it direct to the customer. In these cases it may be important for your customer to understand that equipment will be exported from a country other than the UK. This may have import licence and customs duties implications and the letter of credit will need to recognise this fact. In particular, it should not specify shipment only from a UK port if the third party is an overseas company.

Benefi ciary of the letter of credit

The exporter is the benefi ciary of the letter of credit. When the letter of credit is issued the benefi ciary’s details will probably be extracted from the contract by the customer and made available to the issuing bank. It is a good idea to ensure always that the letter of credit includes any specifi c reference that would help the letter of credit, when it arrives at your company’s offi ces, to reach the right person in your organisation as quickly as possible.

Whilst in smaller companies this may not be an issue, in larger companies with many different departments, the company’s standard address may not be suffi cient to guarantee prompt arrival on the right person’s desk. Therefore request your customer to include the appropriate contact name in the details together with a telephone number.

The BExA Guide to Letters of Credit - UCP600 – Update

26

Very shortly after the letter of credit is issued

Letter of credit terms and conditions

Do these agree with what the contract says? If not, make a list of the differences with a view to requesting amendments from the customer. You should tell the advising and the confi rming bank (if there is one).

Shipment/expiry dates and third party shippers

Check the shipment date, expiry date and clauses that allow third parties as shipper and more than one shipment, if you are not intending to ship everything in one go. UCP600 provides (Article 32) that if there is to be more than one shipment, each with related dates for presentation of documents, and any one date is missed then the letter of credit ceases to be available for that and all subsequent shipments and drawings. If you have a series of shipping dates you may wish to have the following words ‘Article 32 of UCP600 does not apply to this credit’ added as a condition of the letter of credit. This would have the effect of removing the provisions of Article 32.

Mode of transport

Check that the letter of credit requires you to ship by the appropriate means of transport: sea, overland or air, or in some cases a combination. A ‘by air’ option can be useful if you are unable to ship everything by sea and need to make a second shipment which must arrive quickly. This should be discussed at contract negotiation.

If you have agreed a third party as shipper, you must obviously be allowed to make partial shipments, as well as from the third party shipper’s port of loading, but check the letter of credit just in case this has not been followed through. You may be manufacturing or sourcing from several locations and in any case, the shipping department will have a view.

One last point on shipment. Check that the destination port is attainable from the UK. Some ocean vessels cannot reach smaller ports and not all intercontinental fl ights land at every airport in a particular country.

Seek advice

Speak to your bank for guidance on what they will expect to see on the shipping documents based on the letter of credit’s clauses and, if necessary, your freight forwarder who can advise on the appropriateness of the destination ports and what information can be included on the relevant shipping document to satisfy the letter of credit.

Typing errors

Check the letter of credit for typing errors, particularly with respect to your details as benefi ciary, your customer and such key information as the description of the goods. If there are any discrepancies, check with your advising/confi rming bank to ascertain if the discrepancies will necessitate an amendment to the letter of credit. One way to avoid an amendment is to include the information in all documents exactly as spelt in the letter of credit, even if incorrect, but this can cause further problems; having to perpetuate spelling mistakes in a series of documents can not only be tiresome, it can lead to inconsistencies and other errors. It is not always necessary to have amendments for typing errors that are not material, but it would be a commercial decision as to whether to insist on an amendment or not; some customers do not take favourably to requests for long lists of largely irrelevant amendments. Your bank should advise on whether the error is material for payment in their view.

The BExA Guide to Letters of Credit - UCP600 – Update

27

Documents issued/signed by third parties/end-users

If under the contract an end-buyer will have to sign or issue a certifi cate, does the letter of credit give the end-buyer’s name or refer only to “end-buyer”? If the latter, check with your advising/confi rming bank for guidance. Some banks like the name to be included in the letter of credit so that the name in the relevant document tallies. Clearly, this provides a further opportunity for inconsistency and error.

21 days for presenting shipping documents?

Check whether or not you have been given at least 21 days to present shipping documents. Although Article 14c of UCP600 is clear that a time limitation of 21 days is the norm (but in any event not later than the expiry date of the letter of credit), poor wording in the letter of credit may create a doubt as to whether or not the intention of the issuing bank is to change this condition. Therefore, check with your advising/confi rming bank for guidance. If the time for presentation is less, or the expiry date is the same as the latest shipment date, this may not necessitate an amendment, but would require the exporter to be more effi cient and timely with presentation of documents. Again, this will be down to logistics and commercial decision-making.

Bills of exchange