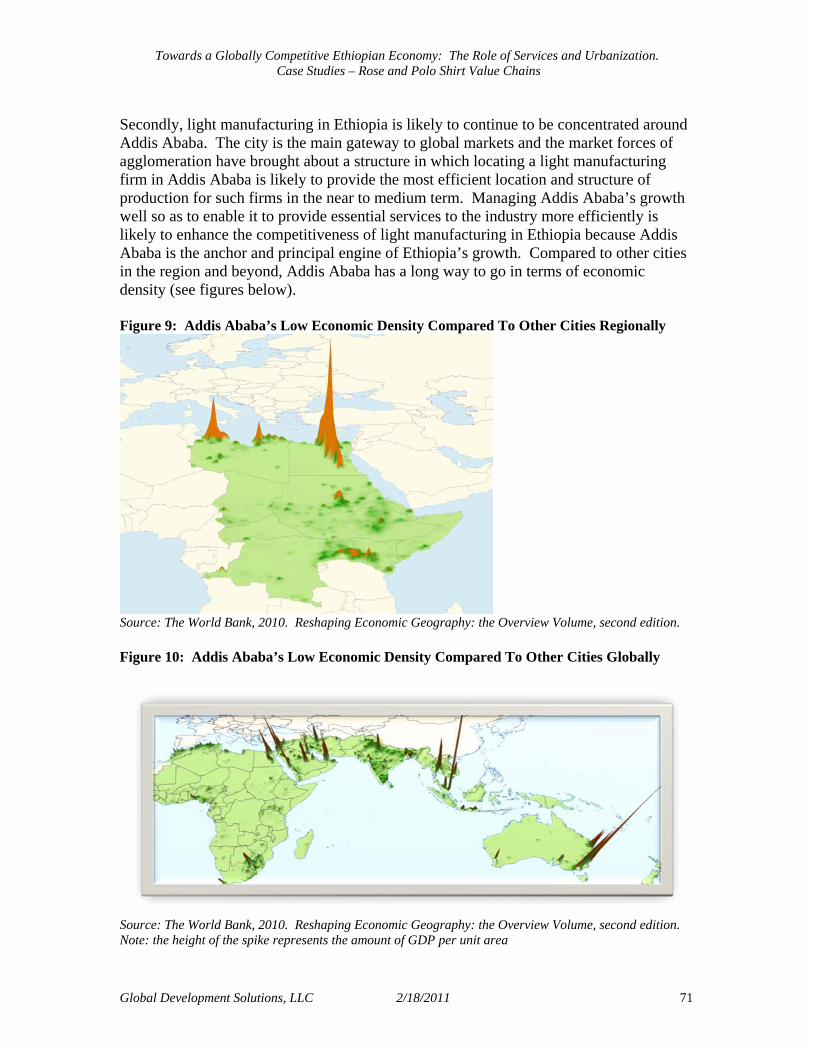

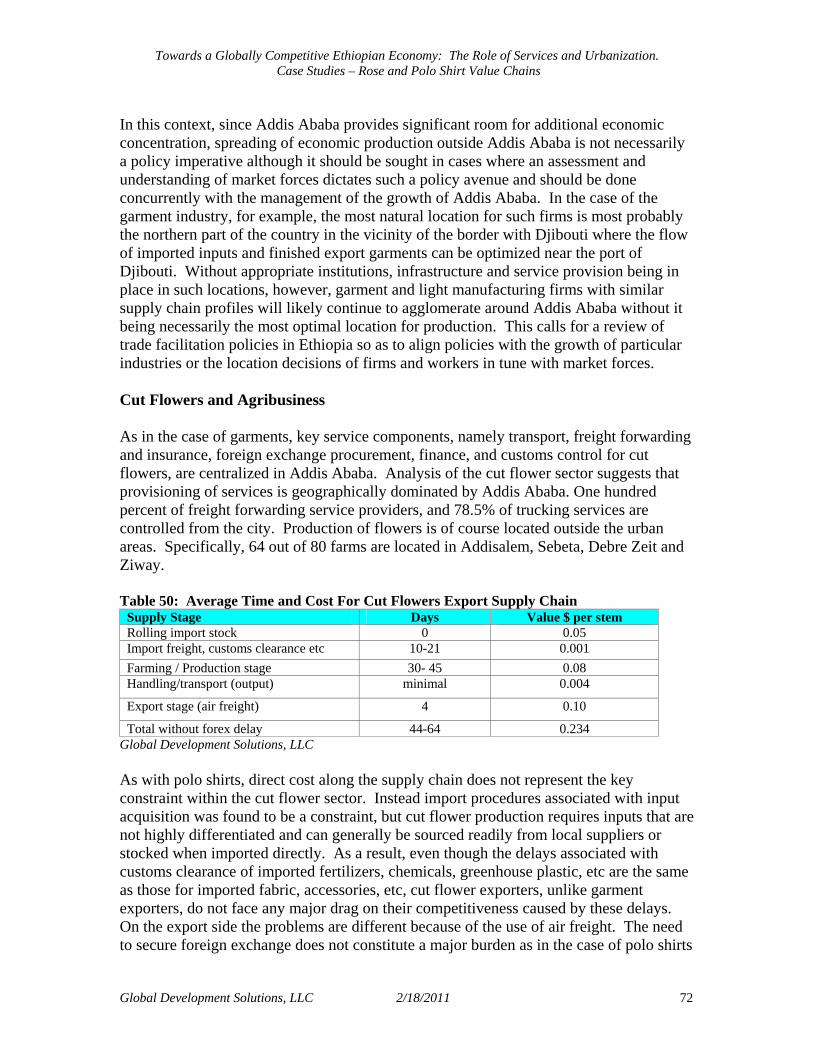

Towards a Globally Competitive Ethiopian Economy:...

78

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization Case Studies – Rose and Polo Shirt Value Chains Prepared for The World Bank Draft Final Prepared by Global Development Solutions, LLC 18 February, 2011

Transcript of Towards a Globally Competitive Ethiopian Economy:...

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization

Case Studies – Rose and Polo Shirt Value Chains

Prepared for

The World Bank

Draft Final

Prepared by

Global Development Solutions, LLC

18 February, 2011

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 2

Copyright Global Development Solutions, LLCTM

All Rights Reserved

Global Development Solutions, LLC

11921 Freedom Drive Suite 550

Reston, VA. 20190 Tel. +1 703 904-4373 Fax. +1 703 991-4056

E-mail: [email protected]

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 3

Table of Contents

I. Objectives and Approach of the Study.............................................................................................. 6

II. Background: Cut Flowers and Apparel – International Market Overview ................................. 8 1. Cut Flower Trade............................................................................................................................. 8 2. Apparel Trade .................................................................................................................................. 9

III. Ethiopia’s Services Value Chain and the Role of Urban Concentration (Addis Ababa) ....... 11 1. Objective ........................................................................................................................................ 11 2. The Service Value Chain - Background ......................................................................................... 11 3. Urbanization and the Role of Addis Ababa – Advantages and Disadvantages of Concentration.. 12 4. Transport/Trade Costs and Cities .................................................................................................. 14 5. Addis Ababa as an “Anchor” of Urban Economies – Its Growth and Activities in Nearby Towns18 6. Addis Ababa in Comparison with other Cities ............................................................................... 25 7. Addis Ababa as a Service Market Anchor/Leader – Strengths and Weaknesses............................ 28

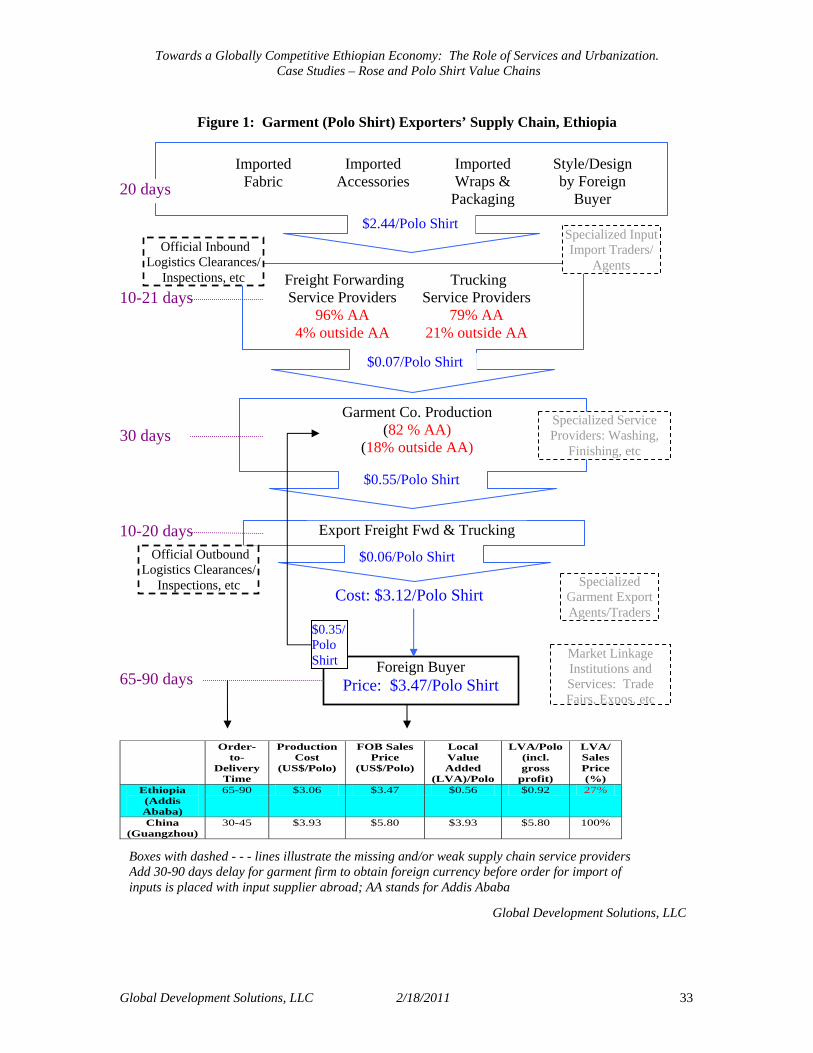

IV. Case Study 1: the Role of Services in the Ethiopian Garment Value Chain (Polo Shirts).... 32 1. The Garment Supply Chain ............................................................................................................ 32 2. Role of Services in the Import of Inputs – Garment Value Chain (Polo Shirts)............................. 34 3. Role of Services in Production – Garment Value Chain (Polo Shirts)........................................... 43 4. Role of Services in Exports – Garment Value Chain (Polo Shirts) ................................................ 45 5. The Contribution of Addis Ababa to the Garment Value Chain (Polo Shirts) ............................... 47

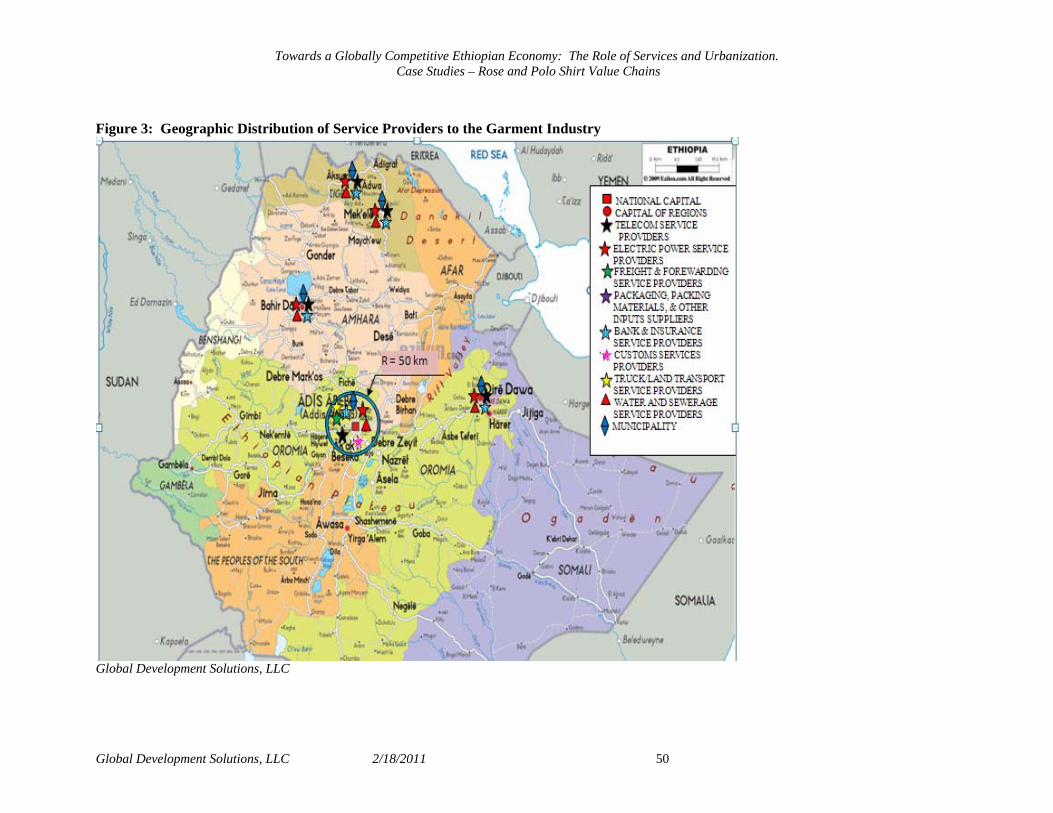

1. Geographic Distribution of the Garment Industry in Ethiopia .................................................. 47 2. Geographic Distribution of Service Providers to the Garment Industry in Ethiopia ................. 48

V. Case Study 2: the Role of Services in the Ethiopian Cut Flowers Value Chain (Roses) ............ 52 1. The Cut Flowers Supply Chain ...................................................................................................... 52 2. Role of Services in the Import of Inputs – Value Chain for Cut Flowers (Roses) .......................... 54 3. Role of Services in Production – Cut Flowers Value Chain (Roses) ............................................. 55 4. Role of Services in Exports – Cut Flowers Value Chain (Roses) ................................................... 57 5. The Contribution of Addis Ababa to the Value Chain for Cut Flowers (Roses)............................. 62

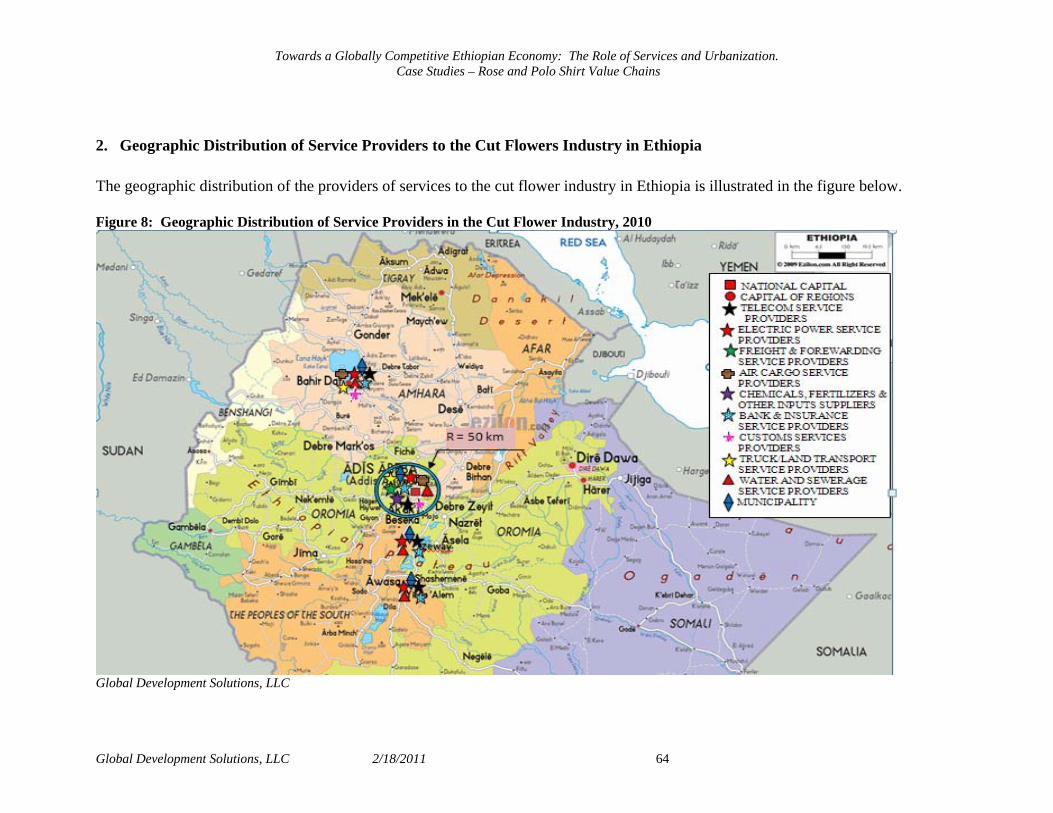

1. Geographic Distribution of the Cut Flowers Industry in Ethiopia............................................. 62 2. Geographic Distribution of Service Providers to the Cut Flowers Industry in Ethiopia ........... 64

VI. Conclusions ................................................................................................................................... 69

ANNEX 1: Power Consumption in Ethiopia (Domestic, Commercial and Industrial) ........................ 74

ANNEX 2: An Overview of the Financial Services in Ethiopia............................................................. 75

ANNEX 3: Commercial Banks and Insurance Companies in Ethiopia................................................ 78

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 4

List of Tables and Figures

Table 1: Cut Flowers Exports, Sub Saharan Africa, 2009 (US$ thousand) ................................... 8 Table 2: Employment Statistics for Ethiopian Cut Flower Sector ................................................. 9 Table 3: Apparel Exports, Sub-Saharan Africa, 2009 (US$ thousand)........................................ 10 Table 4: Employment Statistics for Ethiopia Apparel Sector....................................................... 10 Table 5: Business Services and the Manufacturing Value Chain................................................. 12 Table 6: Urbanization in Selected African Countries................................................................... 14 Table 7: African Cities, Comparative Data .................................................................................. 14 Table 8: Overall Growth of Towns .............................................................................................. 18 Table 9: Growth of Selected Larger Towns ................................................................................. 19 Table 10: Features of Selected Towns Close to Addis Ababa...................................................... 20 Table 11: Ten Largest Cities Ethiopia, 2007................................................................................ 20 Table 12: Number of Power Customers in Ethiopia..................................................................... 23 Table 13: Power Consumption Growth per Annum 2005/6 – 2008/9.......................................... 23 Table 14: Share of Addis Ababa in Power Consumption............................................................. 24 Table 15: Number of Enterprises and Employment in Addis Ababa and its Proximity............... 24 Table 16: Comparisons of Addis Ababa and Other Cities: Investment Climate Survey Data ..... 26 Table 17: Infrastructure Indicators in Select African Cities......................................................... 26 Table 18: Delays in Land Acquisition, Costs of Security and Theft by City ............................... 27 Table 19: Days Required to Process Lease for Urban Industrial land: Selected Countries.......... 27 Table 20: Doing Business International Ranking 2011................................................................ 28 Table 21: Addis Ababa and other African Cities, 2005 ............................................................... 30 Table 22: Addis Ababa as Primate City: Pros and Cons .............................................................. 31 Table 23: Cost of Services in the Ethiopian Export Polo Shirt, 2010 .......................................... 35 Table 24: Cost of Input Import Related Services as Share of Input Costs, 2010 ......................... 36 Table 25: Transportation and Handling Costs for Imported Inputs.............................................. 37 Table 26: Comparative Transport Cost ........................................................................................ 37 Table 27: Clothing and Accessories, Comparative Product Performance Table, 2007................ 38 Table 28: Storage Grace Period per Shipping Line...................................................................... 40 Table 29: Customs and Highway Inspection Points and Duration for Imported Cargo, Ethiopia 40 Table 30: Procedures and Time Lapse During Input Import Process, Ethiopia ........................... 41 Table 31: The Role of Services in the Polo Shirt Assembly Costs, Ethiopia............................... 43 Table 32: Commercial Banks in Ethiopia, 2010........................................................................... 44 Table 33: Sample Commercial Bank Rates in Ethiopia, 2010 ..................................................... 44 Table 34: The Role of Export Services in the Polo Shirt Garment Price, Ethiopia...................... 45 Table 35: Procedures and Time Lapse During the Garment Export Process, Ethiopia................ 46 Table 36: Service Providers to the Garment Industry .................................................................. 49 Table 37: Cities with Garment Firms, Ethiopia............................................................................ 51 Table 38: Cost of Services in the Ethiopian Export Roses, 2010................................................. 54 Table 39: Cost of Input Import Related Services, Share in Rose Production Input Costs, 2010 . 55 Table 40: The Role of Services in the Ex-Farm Rose Production Cost, Ethiopia........................ 56 Table 41: Breeders’ Varieties in Selected Cut-flower Producing Countries ................................ 56 Table 42: The Role of Export Services in Cut Flower Export Price, Ethiopia............................. 58 Table 43: Airfreight Cargo Fees. Addis Ababa - Europe ............................................................. 58 Table 44: Airlines Represented by Tradepath International PLC ................................................ 59 Table 45: Summary of Flower Export Handling Process and Duration....................................... 61 Table 46: Refer Trucks’ Service Supply for Cut Flower Exports ................................................ 62

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 5

Table 47: Geographic Distribution of Cut Flower Production in Ethiopia, 2010 ........................ 63 Table 48: Geographic Distribution of Service Providers for the Cut Flower Industry................. 65 Table 49: Average Time and Cost For Garment Export Supply Chain........................................ 70 Table 50: Average Time and Cost For Cut Flowers Export Supply Chain .................................. 72 Table 51: Power Consumption in Addis Ababa and Near Towns, 2005-2009 (kWh/year) ......... 74 Table 52: Key Characteristics of the Financial Sector in Ethiopia............................................... 75 Table 53: Commercial Banks in Ethiopia .................................................................................... 78 Table 54: Insurance Companies in Ethiopia................................................................................. 78 Figure 1: Garment (Polo Shirt) Exporters’ Supply Chain, Ethiopia............................................. 33 Figure 2: Geographic Distribution of Garment firms in Ethiopia ................................................ 48 Figure 3: Geographic Distribution of Service Providers to the Garment Industry....................... 50 Figure 4: Cut Flowers (Rose) Supply Chain, from Ethiopia to Dutch Auctions .......................... 53 Figure 5: Agricultural R&D Spending, Ethiopia, 1993-2008 ...................................................... 57 Figure 6: Export Airfreight Map for Cut Flowers, Ethiopia......................................................... 60 Figure 7: Distributions and Location of Cut Flower Farms in Ethiopia, 2010............................. 62 Figure 8: Geographic Distribution of Service Providers in the Cut Flower Industry, 2010......... 64 Figure 9: Addis Ababa’s Low Economic Density Compared To Other Cities Regionally .......... 71 Figure 10: Addis Ababa’s Low Economic Density Compared To Other Cities Globally ........... 71

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 6

I. Objectives and Approach of the Study In the global context, the competitiveness of Ethiopian producers is heavily influenced by the supply chains in which they operate, including the efficiency of the services sector. If ‘competitiveness’ is broadly defined to measure “the price at which goods are sold”, the two underpinning assumptions of this study, as per its terms of reference, are:

• Ethiopian producers cannot hope to sell goods competitively in the world market without having an efficient services sector – i.e. capturing a high share of the products sales price is contingent upon the ability of the national service sector to provide services competitively.

• For Ethiopian goods and services to be competitive at home and abroad, it is vital that Addis Ababa’s economy stays vibrant and competitive – i.e. Addis Ababa plays an “anchor” role in linking producers in rural areas and towns with national and international buyers by the virtue of its centrality (geographic and otherwise) in the national supply chain of goods and services.

Against this background, the purpose of this study is to assess the competitiveness of the Ethiopian economy at the national and the sub-national level particularly as it relates to the role of services. For the assessment at the national level, the study will use the Integrated Value Chain Analysis (IVCA) methodology for two products: (1) cut flowers (horticulture), using roses as a proxy for developments in the processed agricultural products sector; and (2) polo shirts (garments) as a proxy for developments in the light manufacturing sector. By following cut flowers (roses) and garments (polo shirts) from production all the way to the market delivery stage, the IVCA will assess the relevance of the service sector along the products’ supply and value chains including the role of services along three product value chain points:

a) Import of inputs; b) Production of exportable goods; and c) Export of finished goods.

Informed by the IVCA findings at the national level, including information on the geographic location of activities along the rose and polo shirts value chains, the report will assess the role of services at the sub-national level by examining the role played by Addis Ababa as a provider of services to the manufacturing sector. The report follows a case study approach and is organized in six chapters. This introductory chapter is followed by Chapter II which introduces the cut flowers and apparel sectors in the context of the Ethiopian economy by providing background information on the level of employment and exports generated by these two sectors. A brief discussion of international trade and other developments in these sectors is also provided in this chapter. Chapter III discusses the service value chain and the role of urbanization and urban concentrations, and the relevance of Addis Ababa on national competitiveness. Chapters IV and V provide case studies on the role of services in the cut flower and garment sectors at the national level using two proxy products: roses and polo shirts. A sub-national level discussion is also presented in each case study chapter

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 7

by assessing the role and relevance of Addis Ababa as the country’s key urban center, and the source of many vital services to firms in the selected product value chains. The study ends with Chapter VI which provides concluding remarks.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 8

II. Background: Cut Flowers and Apparel – International Market Overview

1. Cut Flower Trade In 2009, the world trade in cut flowers was worth roughly US$7 billion. As the world’s leading hub for cut flower trade, the Netherlands maintained its leadership position by exporting roughly half of all cut flowers traded in the world in 2009 (US$3.6 billion). Other major exporting countries include Colombia (US$1 billion in 2009), and Ecuador (US$500 million); on an annual basis, these three countries combined export roughly three quarters of the world’s cut flowers. The largest importers of cut flowers are Germany, the Netherlands, and the United Kingdom, each of which import, on average, US$1 billion worth of cut flowers annually. France, Italy, Russia and Japan make up the bulk of the remaining cut flower imports. Sub-Saharan Africa is a significant region in the global cut flower trade by the virtue of having three big exporters of cut flowers, namely: Kenya, Zimbabwe and Ethiopia (see table below).1 Table 1: Cut Flowers Exports, Sub Saharan Africa, 2009 (US$ thousand)

Exporters Exported value in

2005

Exported value in

2006

Exported value in

2007

Exported value in

2008

Exported value in

2009 % of World

% of Africa

'World $5,617,103 $ 6,811,428 $ 7,121,896 $ 7,705,355 $7,305,167 100% Africa $ 346,263 $ 1,134,251 $ 636,271 $ 804,636 $1,012,821 14% 'Kenya $ 242,561 $ 274,946 $ 313,412 $ 445,996 $ 421,484 6% 42% 'Zimbabwe $ 33,658 $ 765,230 $ 201,056 $ 185,772 $ 334,117 5% 33% 'Ethiopia $ 12,128 $ 25,137 $ 68,827 $ 104,740 $ 131,518 2% 13% 'Nigeria $ - $ 4,585 $ 9,905 $ 67,725 7% 'South Africa $ 24,408 $ 22,064 $ 25,439 $ 28,412 $ 26,467 3% Tanzania $ 9,282 $ 7,791 $ 8,812 $ 13,428 $ 14,075 1% Global Development Solutions LLC from ITC/Comtrade data. Ethiopia is an increasingly important player in the regional and global market for cut flowers. In 2005, the country exported US$12 million worth of cut flowers. By 2009, its cut flower exports increased by tenfold to US$131 million, which represented 13% of African exports and 2% of world exports. In the first ten month of 2010 alone, Ethiopia exported an estimated US$250 million of cut flowers.2 The industry employs roughly 35,000 people – mostly women (80%) employed on temporary basis (80%).

1 North African countries do not export cut flowers in any significant numbers. Sub-Saharan Africa export figures are therefore roughly equal to export figures of the continent as a whole. 2 www.floracultureinternational.com

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 9

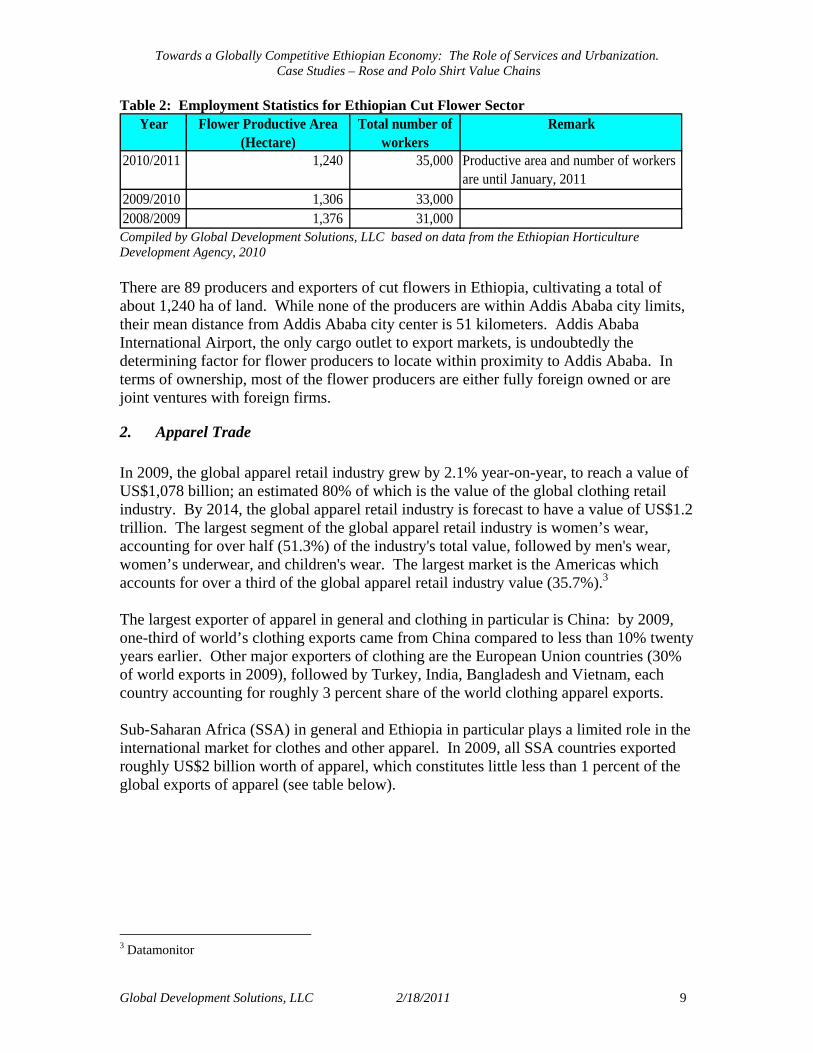

Table 2: Employment Statistics for Ethiopian Cut Flower Sector Year Flower Productive Area

(Hectare)Total number of

workersRemark

2010/2011 1,240 35,000 Productive area and number of workers are until January, 2011

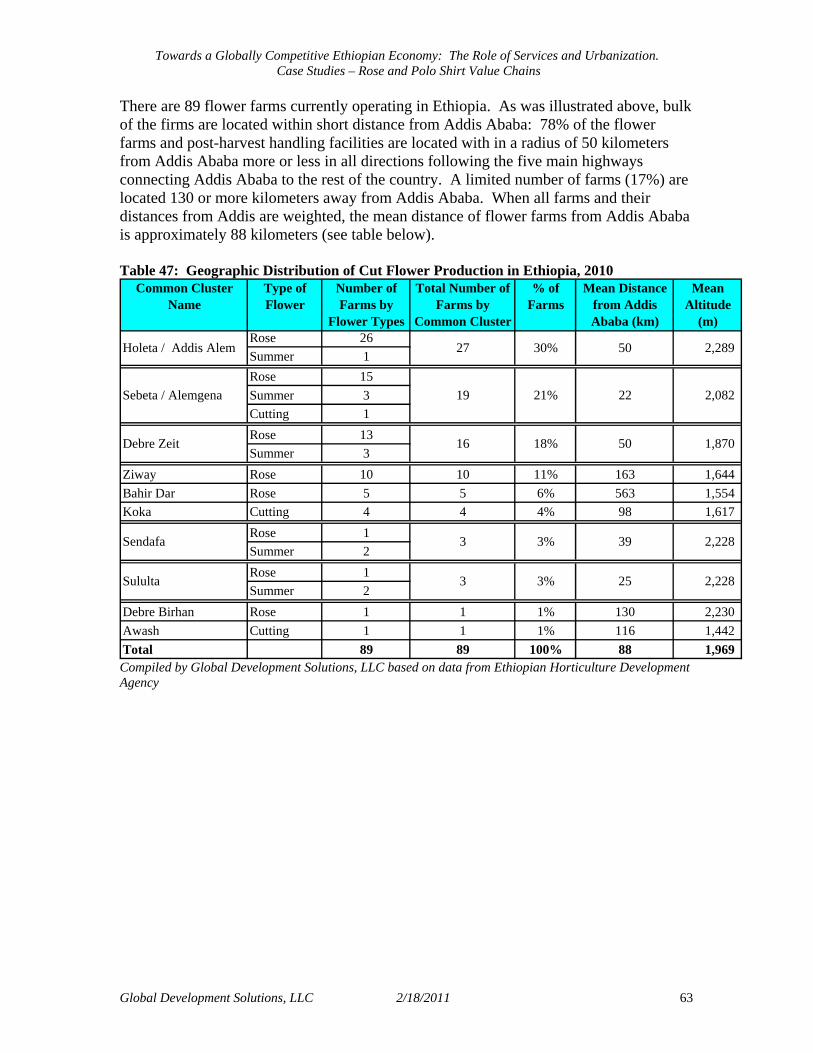

2009/2010 1,306 33,000 2008/2009 1,376 31,000 Compiled by Global Development Solutions, LLC based on data from the Ethiopian Horticulture Development Agency, 2010 There are 89 producers and exporters of cut flowers in Ethiopia, cultivating a total of about 1,240 ha of land. While none of the producers are within Addis Ababa city limits, their mean distance from Addis Ababa city center is 51 kilometers. Addis Ababa International Airport, the only cargo outlet to export markets, is undoubtedly the determining factor for flower producers to locate within proximity to Addis Ababa. In terms of ownership, most of the flower producers are either fully foreign owned or are joint ventures with foreign firms.

2. Apparel Trade In 2009, the global apparel retail industry grew by 2.1% year-on-year, to reach a value of US$1,078 billion; an estimated 80% of which is the value of the global clothing retail industry. By 2014, the global apparel retail industry is forecast to have a value of US$1.2 trillion. The largest segment of the global apparel retail industry is women’s wear, accounting for over half (51.3%) of the industry's total value, followed by men's wear, women’s underwear, and children's wear. The largest market is the Americas which accounts for over a third of the global apparel retail industry value (35.7%).3 The largest exporter of apparel in general and clothing in particular is China: by 2009, one-third of world’s clothing exports came from China compared to less than 10% twenty years earlier. Other major exporters of clothing are the European Union countries (30% of world exports in 2009), followed by Turkey, India, Bangladesh and Vietnam, each country accounting for roughly 3 percent share of the world clothing apparel exports. Sub-Saharan Africa (SSA) in general and Ethiopia in particular plays a limited role in the international market for clothes and other apparel. In 2009, all SSA countries exported roughly US$2 billion worth of apparel, which constitutes little less than 1 percent of the global exports of apparel (see table below).

3 Datamonitor

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 10

Table 3: Apparel Exports, Sub-Saharan Africa, 2009 (US$ thousand) Exporters Exported

value in 2006 Exported value

in 2007 Exported value

in 2008 Exported

value in 2009 % of World % of SSA

'World $ 340,626,012 $ 383,678,608 $ 408,126,132 $ 359,532,180 100% Africa $ 8,959,393 $ 10,325,969 $ 11,525,187 $ 10,267,308 2.9% Sub Saharan Africa $ 2,539,483 $ 2,970,069 $ 3,022,420 $ 2,014,444 0.6% 'Mauritius $ 771,922 $ 884,065 $ 843,054 $ 552,645 27.4% 'Madagascar $ 347,450 $ 502,897 $ 888,173 $ 461,626 22.9% 'Lesotho $ 418,649 $ 413,895 $ 370,149 $ 303,433 15.1% 'Kenya $ 279,255 $ 286,231 $ 288,419 $ 215,847 10.7% 'South Africa $ 171,282 $ 157,512 $ 168,305 $ 159,969 7.9% 'Swaziland $ 150,204 $ 48,059 $ 133,546 $ 99,888 5.0% Tanzania $ 29,181 $ 69,128 $ 76,678 $ 70,205 3.5% 'Malawi $ 43,047 $ 34,919 $ 27,637 $ 31,489 1.6% 'Zimbabwe $ 61,394 $ 79,677 $ 49,328 $ 25,326 1.3% 'Botswana $ 148,941 $ 347,636 $ 30,835 $ 21,976 1.1% 'Côte d'Ivoire $ 17,352 $ 15,623 $ 20,116 $ 16,823 0.8% 'Senegal $ 5,891 $ 6,255 $ 7,657 $ 12,840 0.6% 'Ethiopia $ 8,196 $ 10,927 $ 10,753 $ 7,904 0.4%' ki $ 2 4Global Development Solutions LLC from ITC/Comtrade data.

Ethiopia exports roughly US$7 million - US$10 million worth of apparel each year. Although exports have increased significantly from earlier periods (US$4 million in 2002), the country remains an insignificant player in the global (and regional) apparel trade. Even at these comparatively low export volumes, however, the Ethiopian textile and apparel sector is a major contributor to the country’s industrial production: for the year ending in June 2010, the sector accounted for 7 percent of the country’s industrial production. The sector employs an estimated 9,746 workers who work mostly in small firms (see table below). Table 4: Employment Statistics for Ethiopia Apparel Sector

Company SizeEstimated Number of

Companies% of Companies

by SizeNumber ofEmployees

Ave Number of Employees

Small 397 91.1% 1,961 5 Medium 7 1.6% 343 49 Large 32 7.3% 7,442 233 Total 436 100.0% 9,746 Source: Central Statistical Authority

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 11

III. Ethiopia’s Services Value Chain and the Role of Urban Concentration (Addis Ababa)

1. Objective This section is a preliminary analysis of urbanization in Ethiopia, examining the following issues:

• The extent to which Addis Ababa is an ‘anchor’ for the development of urban economies in Ethiopia, the rate of growth of productive activity over time in and around the city, and the correlation between its growth and the concentration of new enterprises in some geographic proximity.

• The contribution of Addis Ababa compared with similar cities in other

developing countries to assess whether the City of Addis Ababa has a disproportionately high importance for urban market linkages that take place, especially the balance of advantage and disadvantage of concentration and centralization within a single city, and whether a more decentralized structure of value added is a sustainable solution.

• The areas where Addis Ababa is weakest compared to other similar Cities and

the reasons for this – whether it is due to the market structure and/or the policy/regulatory environment, and ways to improve competitiveness of Addis Ababa.

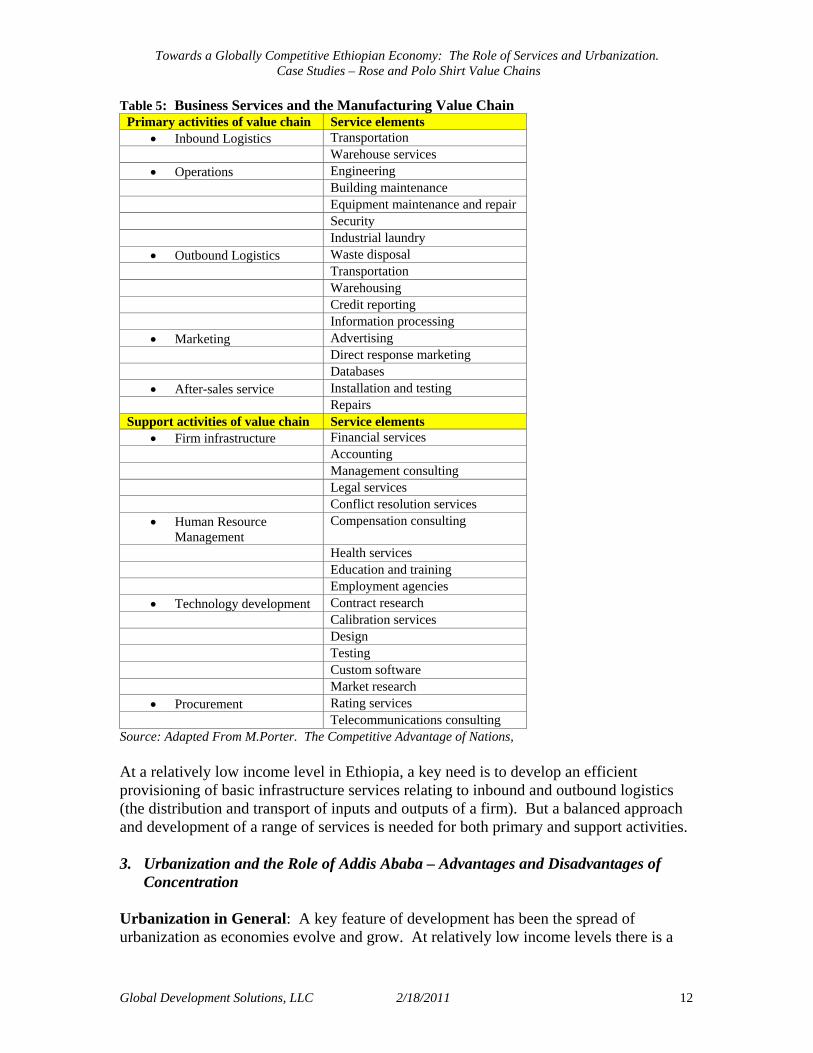

This analysis serves as the background to the value chain analysis of two products, roses and polo shirts. The roses and polo shirt VCAs explore at the business process level the opportunities for cost reduction in services, for investment entry and expanded supply of each product, and for increasing domestic value added by rationalizing or expanding services in Ethiopia. In the process, the VCAs also identify the geographical location of activity in order to provide information to assess the role of the prime city, Addis Ababa, as a provider of services in two important activities. 2. The Service Value Chain - Background The importance of services can be illustrated by reference to the original value-chain model developed by Porter, which comprises five stages of Primary Activities of which most are service activities – Production, Inbound Logistics, Outbound Logistics, Marketing and Sales and After-Sale Service. Operations in turn require service activities such as equipment maintenance. In addition, all Primary Activities are supported by a range of Support Activities covering Firm Infrastructure (that is Finance and Planning), Human Resource Management, Technology Development and Procurement, which have service elements. The table below lists some of the key business services associated with different stages of the manufacturing value chain.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 12

Table 5: Business Services and the Manufacturing Value Chain Primary activities of value chain Service elements

• Inbound Logistics Transportation Warehouse services

• Operations Engineering Building maintenance Equipment maintenance and repair Security Industrial laundry

• Outbound Logistics Waste disposal Transportation Warehousing Credit reporting Information processing

• Marketing Advertising Direct response marketing Databases

• After-sales service Installation and testing Repairs Support activities of value chain Service elements

• Firm infrastructure Financial services Accounting Management consulting Legal services Conflict resolution services

• Human Resource Management

Compensation consulting

Health services Education and training Employment agencies

• Technology development Contract research Calibration services Design Testing Custom software Market research

• Procurement Rating services Telecommunications consulting

Source: Adapted From M.Porter. The Competitive Advantage of Nations, At a relatively low income level in Ethiopia, a key need is to develop an efficient provisioning of basic infrastructure services relating to inbound and outbound logistics (the distribution and transport of inputs and outputs of a firm). But a balanced approach and development of a range of services is needed for both primary and support activities. 3. Urbanization and the Role of Addis Ababa – Advantages and Disadvantages of

Concentration Urbanization in General: A key feature of development has been the spread of urbanization as economies evolve and grow. At relatively low income levels there is a

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 13

strong association between the growth of GDP and the rise in the urban population as workers move off the land into manufacturing or service employment in urban areas. The strength of this association tends to weaken once a country reaches middle-income level. Globally urban centers in most countries take a major share of economic activity. The top 100 cities for example are said to contribute 25% of world output and this concentration is also found in the least urbanized of regions such as sub-Saharan Africa. For example, Luanda with 0.2% of the land area of Angola contributes roughly 30% of GDP, and Nairobi and Lagos with around 1% of the land area of Kenya and Nigeria, respectively, contribute around 20% of GDP. Theories based on the ‘New Economic Geography’ combined with the principles of internal and external scale economies explain the reasons for the concentration of activity. That is, where firms choose to locate is determined by the interaction between resource endowments (which determine labor costs), market size (which has a bearing on internal economies of scale), external benefits (the scale of which will be determined by the linkages between firms) and trade (transport, distribution and related services) costs. The key prediction is that where trade costs are very high there will be a tendency for firms to locate close to the market for their goods, whilst at the lowest levels of trade cost differences in labor costs between countries are likely to be the key determinant of location. At intermediate trade cost, it is likely that the influence of external benefits relative to other factors will be greatest, leading to a tendency for firms to cluster close to each other in a few countries, and locate within regions in a process of agglomeration. Once an industrial center becomes established it will take either a major reduction in trade costs (so that imports take a rising share of domestic demand) or a significant rise in wage, land rents or congestion costs (so new centers in the same country become competitive) to create a significant process of dispersal to satellite towns. However these disadvantages emerge later and hence the initial link between increased urbanization and growth. The inflow of firms and workers widens the market and attracts firms from the same industry as a result of range of potential agglomeration effects such as:

• A pool of skilled labor that firms can draw on; • A set of specialist intermediate suppliers; • Sharing of equipment and services; and • Knowledge spillovers through copying and the transfer of skills between firms.

The special benefits from urban location stem from closeness to consumers and economies of scale in infrastructure and service provision. Manufacturing, for example, requires physical infrastructure like transport, power and water, and services like wholesale warehousing, finance, consultancy or advertising, and considerable economies of scale can be achieved through expanding existing urban supply networks. In addition, since service support is frequently based on face-to-face contact, it is efficient to have service facilities located relatively close to producers. Manufacturing requires more land than services and so it tends to be located in the outskirts of a city where saving in land rents is greater than the higher transport costs due to location further from the distribution point. The link between manufacturing and services has become increasingly close in most countries over the last few decades with the emergence of specialist service

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 14

suppliers who undertake activities that might earlier have been conducted in-house by a manufacturing firm. To get an indication of how Addis Ababa compares in terms of the level of urban concentration, the table provides some comparisons with other African cities, in relation also to infrastructure development. Table 6: Urbanization in Selected African Countries

Country Agglomeration Index 2000

Urban Pop 2000 %

Urban Pop 2005 %

Road Density km/100 km2

Rail density km/100 km2

Ethiopia 11.9 14.9 16.0 3.6 0.1 Gambia 44.0 49.1 53.9 37.4 Na Ghana 34.1 44.0 47.8 21.0 0.4 Kenya 25.4 19.7 20.7 11.1 0.5 Mozambique 24.1 30.7 34.5 Na 0.4 Tanzania 28.2 22.3 24.2 8.9 0.4 Zambia 30.8 34.8 35.0 12.3 0.3 Zimbabwe 33.4 33.8 35.9 25.1 0.8

World Development Report 2009 Ethiopia remains less urbanized than a number of other African countries while at the same time indicators of infrastructural development which are related to service efficiency, that is road and rail density, are also lagging well behind those of the comparator countries, a fact that is likely to result in relatively high transport costs within value chains. While Ethiopia as a whole is less urbanized than others, as shown in the table below Addis Ababa is the most densely populated amongst the capital cities of this group of African countries, although it apparently also has a relative urban welfare level higher than the other comparators except for Nairobi. Thus, despite the categorization as ‘incipient urbanizer’ and problems such as unemployment (see below) Addis Ababa is shown here as relatively well developed as the primate city in Ethiopia. Table 7: African Cities, Comparative Data

City Pop/km² (latest Census)

Area km² Welfare measure/country average (1995-2006) %

Addis 4,574 530 197 Accra 1,121 2,593 182 Nairobi province 3,133 684 244 Banjul 4,060 88 183 Maputo 1,631 602 192 Dar es Salaam 1,793 1,393 188 Lusaka 64 21,898 170

World Development Report 2009 4. Transport/Trade Costs and Cities General Experience: One of the major cost components in service value chains (see Table 6) is transport, or more broadly, transport logistics, consisting of transport costs, warehousing, freight forwarding and border-related costs.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 15

Trade volumes outside a central area are highly sensitive to transport costs. One finding by the World Bank suggests that a 10% increase in trade costs reduces the volume of trade by 20%. In the case of intermediate goods, the effect is even greater. Trade volume in itself also affects costs because large trade flows tend to reduce trade costs through economies of scale. Transport costs are a determinant of the extent of urban agglomeration. High transport costs tend to confine economic activity at a relatively low level within a small geographical center or area. As costs fall, longer distance supply becomes feasible and activity spreads geographically, dependent on the location of key supplies and markets. However at lower levels of transport cost, location of certain types of business may return to the Center, now attracted by the advantages of concentration rather than the location of suppliers and markets. In other words low transport costs tend to encourage agglomeration. As the economy grows more new businesses can optimally locate close to existing production. Transport costs thus become a key to urbanization, manufacturing and services. As more facilities and services are provided centrally in larger cities, smaller communities become less attractive. A fall in transport costs thus indirectly allows more efficient sharing of facilities and services in the center. Improving transport infrastructure thus leads to more concentration of economic activity. To attract a business away from the advantages of being close to a major center it has to have access to outside centers or hubs that are within a reasonable distance of the major center. These firms may follow the available transport corridors. The significance of transport costs for location is also influenced by the value-to-weight ratio of goods being transported. Thus where transport costs per km-ton are relatively high there may still be scope for trade in high-value goods since they face low transport costs as a percent of value. This turns out to be the case for the high-value good (roses) and the medium value good (polo shirts) in Ethiopia, discussed below. With low percentage transport and handling costs high value goods may be located close to supply sources, or concentrated within urban centers even where transport costs per km-ton are high. Transport costs are also sensitive to the structure (eg degree of monopoly) of the transport industry. Costs tend to be inflated by monopolistic transport providers resulting from the naturally large scale and high threshold investment costs of much transport infrastructure. There has been a tendency for monopoly power to increase through concentration of ownership of infrastructure. For example according to the World Bank, in 1980s the top 20% of the world’s carriers controlled 26% of the global port slot capacity while by 1992 this had increased to 42% and by 2003, to 58%. Regulating market structure thus becomes important for developing countries who wish to increase or rationalize the percent of domestic value added in both exports and imports, especially where facilities are foreign owned or controlled. Similarly, improving trade facilitation and regional coordination are also needed. In the case of a landlocked country (such as Ethiopia) there

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 16

may be an additional problem because transport to the only available port is outside its control. Although Ethiopia’s transport industry is competitive, one of the problems noted by the World Bank is that it is of low capacity and therefore competition is likely to be limited, resulting in increased costs, and potential collusive practices. Transport and Trade Costs in Ethiopia: The Port of Djibouti in the North handles 98% of Ethiopia’s export and import needs, of which over 97% is transported by road. The registered vehicle fleet in Ethiopia is small, less than four vehicles per 1,000 people compared to Kenya (18 vehicles/1,000 people) and Zimbabwe (45 vehicles/1,000 people).4 Walking and head loading remain the main transport modes in rural areas. The combined fleet of the public and private sectors has been inadequate for the size of the population while the fleet is also aging. Ethiopia’s transport infrastructure consists of: a) an all-weather road network of 44,000 km in 2008 (compared to 25,000 km in 1997) plus community roads of about 70,000 km; b) a railway line (781 km) from Addis Ababa to Djibouti (of which 709 km lies within Ethiopia); and, c) air transport facilities including four international airports, five major domestic airports, and more than 30 other domestic runways and airstrips. The proportion of the road network classified as in good condition has risen to 66% from 23% in 1977, with road density per 1,000 inhabitants increasing slowly. The average distance to all weather roads (km) has fallen steadily over time to 11 km in 2008, but a large majority of the population still live more than 2 km from an all-weather road. Despite considerable efforts to expand the road network over the past few decades, the country still has one of the lowest road densities in Africa (see Table 7). Addis Ababa is not excessively large compared with other African capitals but it has nonetheless started to face congestion, low infrastructure utilization, and relatively weak traffic management. The Government is planning to introduce an urban mass-transit system involving electric trams and buses. It is also introducing concession arrangements for management of the Ethiopia-Djibouti railway which is being rehabilitated. The government is also proposing the construction of new railways and upgrading of some domestic airports to international airport standard. Outside Addis Ababa there have been reductions in time spent on travel and transport. The most significant impact reported as a result of World Bank assistance has been the reduction in travel time and costs of travel on a number of roads. On one road (Daleti to Oda Bildigilu) the freight rate fell following upgrading in 2004 from about ETB 83 per quintal to ETB 20 per quintal - less than a quarter of the previous rate, while the new road provided significant opportunities for the diversification of agriculture, and a significant increase in percent of marketed crops (30% to 50%). However, key constraints remain in the quality and quantity especially of feeder roads, and to some extent the main road network (weak capacity for road maintenance is contributing to an increase in inland transport costs). 4 The age of registered vehicle fleets varies across countries – relatively new in Ethiopia and relatively old in Zimbabwe.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 17

Aside from actual transportation services, the broader area of transport and trade is an important constraint in Ethiopia. The overall cost of trading across borders is the number one problem facing businesses. Ethiopia ranks only 157th out of 185 countries according to the World Bank’s ‘Doing Business’ index for 2011 in terms of ease of cross border trade. Although the VCAs have not shown high transport costs in relation to total value according to the Doing Business report, the average time required in Ethiopia for exporting is 44 days at $1,890 per container, and for importing, 45 days at $2,993 per container, with relatively heavy documentation requirements. This provides a potential for arbitrary controls which fuel delay and increase costs. With the only port of Djibouti being outside Ethiopia, there are likely to be additional potential costs associated with port handling and customs that cannot be easily controlled by Ethiopian authorities. Despite the long distances and less than adequate road conditions, high value goods such as cut flowers may face relatively low transport costs as a proportion of value. The high value of roses allows the use of air freight which avoids the potential difficulties of surface transport. Polo shirts (Section 7) also face relatively low transport costs as percent of border value. The total transport and handling cost of import of inputs and export of outputs comprise only about 4% of combined import and export value of polo shirts. The relatively low importance of transport and handling costs for these two products has two conflicting implications for the growth of cities such as Addis Ababa. On the one hand it favors geographical concentration of production, gaining economies in infrastructure and service provision; on the other hand, it makes it less important to concentrate close to urban services. The key cost consideration is more likely to be nearness to urban distribution points and markets (in the case of polo shirts). For roses the optimal location of production is clearly outside urban areas but with proximity to air transport and refrigeration services, which are likely to be urban-based. The above considerations suggest that for these types of products Ethiopia’s main doing-business problem of cross-border trade is not a cash cost issue – i.e. the actual cost of transport and handling. Instead it is the implicit cost of delay, especially for perishables like roses (e.g. if refrigeration services fail). In the case of non-perishables such as polo fabrics, the cost of delay shows up not in transport but in finance of excessive inventories and is one reason why the cost of finance is relatively high. Securing of finance is also a lengthy process. Time required for order-to-delivery (excluding time for securing finance) are about double those of China and may thereby exclude some Ethiopian products from world markets altogether (see Section 7). The cost of delays may thus be not the result of poor services as much as the result of regulatory constraints such as border documentation. Regarding transport costs themselves, while the proportion of all-weather road has significantly increased, reductions in cost have been achieved and serious attempts made at institution building, but several key issues remain.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 18

• Urban congestion in Addis Ababa is significant while other towns are small and currently unable to reap agglomeration economies. Thus, transport costs overall may be higher than necessary.

• The national transport fleet appears to be underdeveloped in relation to the scale of trade flow.

• Transport costs within Ethiopia are likely to be relatively high because of the distance of most of the population from road access, and the remaining poor road conditions, partly due to overloading of trucks, leading to breakdowns, especially with the long distances traveled to and from the available port, and excessive damage to roads from overweight loads.

5. Addis Ababa as an “Anchor” of Urban Economies – Its Growth and Activities in Nearby Towns

Addis Ababa and Smaller Town Growth: Ethiopia had an almost entirely rural economy up until relatively recently. Only since the 1960s have new urban centers started to emerge outside Addis Ababa and some older towns such as Asmara (now part of Eritrea), Gonder, Dire Dawa, Debre Zeyt, and Debre Markos. The newer towns included Akaki, Arba Minch, Awasa, Bahir Dar, Jijiga, and Shashemene, whose populations more than tripled between 1965 and 1975 due to rural-urban migration. Bahar Dar was a planned city with several industrial units located therein, and Akaki and Aseb became industrial towns. Jijiga and Shashemene developed communications and services as a part of its development strategy. More modest growth was recorded in the older towns. Overall, the rate of urban growth declined between 1975 and 1987. This was partly due to 1975 land reforms which provided incentives and opportunities for the rural population to stay put combined with restrictions on travel, lack of employment, housing shortages, and social unrest in some towns. Rural-urban migration was also restricted by an official registration system. Significant urban migration restarted during 1988-91 especially to Addis Ababa, as a result of war, causing incipient congestion problems and unemployment. Addis Ababa has a current population (in 2010) of over 3.0 million which, while relatively large compared to other African cities, is still less than 5% of the total population of the country. Its growth rate has been moderate in comparison to smaller towns as is reflected in its declining share of the total population in urban areas from 41% to 35% over 1994 to 2007. The total urban population outside Addis Ababa grew at about 3.9 % per annum from 1994 to 2007 while the population of Addis Ababa grew at 2.0% in that period. Table 8: Overall Growth of Towns

1984* 1994 2007 130 towns above 10,000 population 3,117,130 5,173,117 7,775,623 Urban population excluding Addis Ababa 1,704,555 3,060,380 5,036,072 Addis Ababa % share of total 45.3% 40.8% 35.2%

Compiled by Global Development Solutions, LLC *excludes some towns shown in 1994 and 2007.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 19

Thus while the total absolute population size of Addis Ababa rose by about 620,000 between 1994 and 2007, the urban population outside Addis Ababa rose by about 1,300,000. Excluding the smallest towns, 50 towns with population above 30,000 in 2007 achieved a growth rate of about 3.1% per annum over a period between 1994 and 2007. Addis Ababa’s share in the total population of these 50 towns correspondingly also fell steadily from 50% in 1994 to 43% in 2007. Table 9: Growth of Selected Larger Towns

1984 1994 2007 1994-2007

Growth rate 50 towns above 30,000 population 2,661,783 4,220,868 6,308,213 3.2% Addis Ababa population 1,412,575 2,112,737 2,739,551 2.0% Addis Ababa % total 53.1% 50.1% 43.4%

Compiled by Global Development Solutions, LLC The group of towns outside Addis Ababa with population above 100,000 in 2007 grew at 4.1 % per annum over 1994-2007, faster than both the total urban population (towns above 10,000), and the population of towns with more than 30,000. The fastest growing towns were Jijiga, an Eastern regional capital with a population of approximately 125,000 (in 2007) which grew at over 6% per annum between 1994 and 2007. Mekele, a regional capital in the North about 400 miles from Addis Ababa grew at about 6.4% making it the fastest growing Ethiopian city with a population above 100,000 (215,000 in 2007). Mekele has an airport that meets international standards, and a number of heavy industrial plants that originated in the public sector. Shashemene with a population of 100,000 has been another fast growing town at 5% per annum over 1994-2007. It is located 150 miles South of Addis Ababa, close to the town of Awasa with a population of about 160,000 in 2007. Nazret about 70 miles South East of Addis Ababa with a population of 220,000 grew at about 4.2% per annum between 1994 and 2007. There is no obvious correlation between Addis Ababa and surrounding towns in these figures, nor a pattern from the point of view of location-based advantage and international competitiveness. The four fastest growing towns with a population of over 100,000 are relatively far geographically from Addis Ababa,. These towns are to the North near the Eritrean border, to the South on the road to Kenya, and to the West close to the Somali border. To benefit from international trade, they would have to be located either close to Addis Ababa or on the main route between Addis Ababa and Djibouti in the North East. Rather they are mostly administrative capitals. On the other hand none of the towns that do have trade location-based advantages have shown impressive size or growth up to 2007. Debre Zeyt, the largest town in proximity to Addis Ababa (30 miles away with a population of about 100,000 in 2007) grew little faster than Addis Ababa itself at a rate of 2.4% from 1994 to 2007. The towns of Dese with a population of 130,000 and Kembolcha (60,000), both with good location-based advantages on the transit route to Djibouti, have also shown modest size and/or growth. Few towns appear to be flourishing on the North Easterly route to Djibouti despite the fact that it is now the

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 20

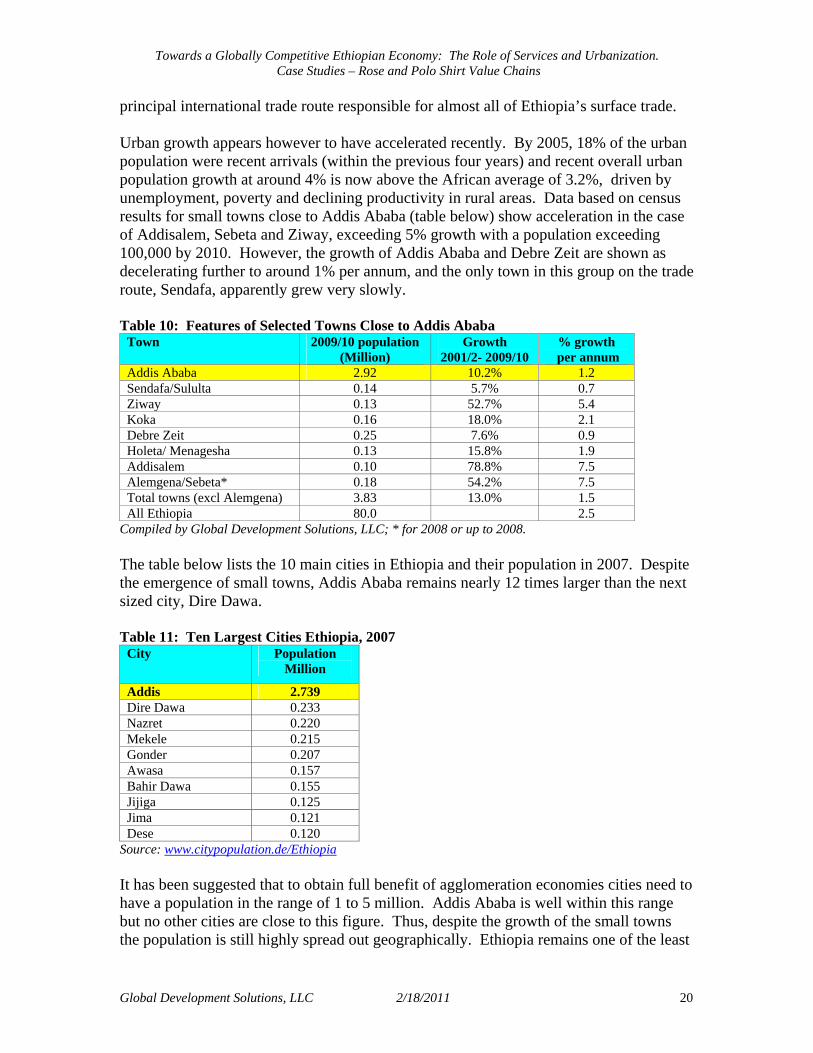

principal international trade route responsible for almost all of Ethiopia’s surface trade. Urban growth appears however to have accelerated recently. By 2005, 18% of the urban population were recent arrivals (within the previous four years) and recent overall urban population growth at around 4% is now above the African average of 3.2%, driven by unemployment, poverty and declining productivity in rural areas. Data based on census results for small towns close to Addis Ababa (table below) show acceleration in the case of Addisalem, Sebeta and Ziway, exceeding 5% growth with a population exceeding 100,000 by 2010. However, the growth of Addis Ababa and Debre Zeit are shown as decelerating further to around 1% per annum, and the only town in this group on the trade route, Sendafa, apparently grew very slowly. Table 10: Features of Selected Towns Close to Addis Ababa

Town 2009/10 population (Million)

Growth 2001/2- 2009/10

% growth per annum

Addis Ababa 2.92 10.2% 1.2 Sendafa/Sululta 0.14 5.7% 0.7 Ziway 0.13 52.7% 5.4 Koka 0.16 18.0% 2.1 Debre Zeit 0.25 7.6% 0.9 Holeta/ Menagesha 0.13 15.8% 1.9 Addisalem 0.10 78.8% 7.5 Alemgena/Sebeta* 0.18 54.2% 7.5 Total towns (excl Alemgena) 3.83 13.0% 1.5 All Ethiopia 80.0 2.5

Compiled by Global Development Solutions, LLC; * for 2008 or up to 2008. The table below lists the 10 main cities in Ethiopia and their population in 2007. Despite the emergence of small towns, Addis Ababa remains nearly 12 times larger than the next sized city, Dire Dawa. Table 11: Ten Largest Cities Ethiopia, 2007

City Population Million

Addis 2.739 Dire Dawa 0.233 Nazret 0.220 Mekele 0.215 Gonder 0.207 Awasa 0.157 Bahir Dawa 0.155 Jijiga 0.125 Jima 0.121 Dese 0.120

Source: www.citypopulation.de/Ethiopia It has been suggested that to obtain full benefit of agglomeration economies cities need to have a population in the range of 1 to 5 million. Addis Ababa is well within this range but no other cities are close to this figure. Thus, despite the growth of the small towns the population is still highly spread out geographically. Ethiopia remains one of the least

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 21

urbanized economies in Africa. The World Bank ‘Agglomeration Index’ score for Ethiopia (see Table 6) is well below that of other African countries and low even in relation to the country’s low income per capita. Its urban population share is only 18% and its road and rail density is also very low (Table 6). It is described in the World Development Report 2009 as an ‘incipient urbanizer.’ One of the reasons for the underdevelopment of the Ethiopian minor towns is probably associated with the presence up to 1991 of Asmara, the main city of what is now Eritrea, with a current population of about 600,000, which along with the port of Massawa, constituted a key component of Ethiopia’s trade infrastructure for about fifty years. The urban profile of Ethiopia may yet have to fully adjust for the trade disruption resulting from the secession of Eritrea. Overall, there has in the past generally been only weak inducement to migrate to all towns including Addis Ababa. The small towns are as yet nowhere near the level of activity of Addis Ababa. The need for more vigorous small town development was taken up in the Plan for Accelerated Sustained Development to End Poverty (PASDEP) 2005/6–2009/10 which aimed to develop some of the smaller urban centers. Economic Activity in Addis Ababa and Smaller Towns: According to the sparse data available, while up to about 2004 urban economic activity overall grew slowly, more recently data show that urban-based activity has accelerated. Even during the slow growth period up to 2004, banking and insurance, transport and communication, and construction grew at over 7% per annum. Manufacturing growth lagged behind at or below 3%. Further analysis by the World Bank shows that over 1999 to 2005, growth in value added in industry of almost 3% per annum was eroded by productivity falling by 0.6% per annum, whereas in transport and communications a significant increase in productivity has occurred, with output increasing despite little growth in employment. These trends are consistent with the gradual emergence of Addis Ababa as a services center while manufacturing remained relatively stagnant. However, even with the acceleration in activity, especially in services, urban job growth seems to have slowed overall, and the urban unemployment rate rose. New income earning opportunities are typically in the informal microenterprise sector, and generally represent very low paying jobs. According to the World Bank the urban labor market is segmented into three categories, namely, a privileged high wage public sector; a small private formal sector; and a large informal economy, which is more ‘survivalist’ than entrepreneurial. Thus main sources of formal urban employment have been in Government and parastatal enterprises. The unemployment rate in Addis was around 24% in 2005, well above the national average of 13.5 % and that of the next largest city Dire Dawa at 18%. More recent unemployment data for 2006 put the Addis unemployment rate at 29%. Ethiopia’s low overall urbanization ratio suggests that economies of agglomeration have yet to be realized across the country, but at the same time Addis Ababa is, in absolute terms, a medium-sized city by African standards (and one of the largest for a landlocked

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 22

economy) and diseconomies of concentration are emerging (such as congestion). A key issue therefore is whether scale economies can still be pursued in Addis Ababa or whether decentralization is a better strategy. More data is needed to arrive at a clear picture of the nature of the urban economy and the extent of private sector capacity and growth, but to the extent that the public sector continues to account for the bulk of urban formal employment and much of the private expansion is in the microenterprise, informal sector, which is the least susceptible to scale economies, this would usually suggest rather limited urban agglomeration externalities, despite the growth of services. One indicator of the rate of growth of economic activity in Addis Ababa and the townships near to Addis Ababa is the growth of commercial and industrial power consumption. The increase in power customers can be used as a proxy for business start-ups (although some new customers will be shifting from self-generation to the grid). The table below gives the number of business power customers 2005/06 to 2008/09 nationally and in Addis Ababa and surrounding small towns. There was a roughly parallel growth in the number of customers over 2005/6 to 2008/9 between Addis Ababa and its nearby towns but somewhat lower than for the country as a whole. For the commercial area (of which services would comprise a significant proportion) the total number of customers grew nationally by 11.6% per annum between 2005/6 and 2008/9. Similarly, Addis Ababa grew by 8.2% per annum, and Addis Ababa plus nearby towns also grew 8.2%. For low-voltage industrial customers (SMEs) Ethiopia showed 16.4% growth, Addis Ababa 14% and Addis Ababa plus nearby towns 14.4%. For high voltage industrial customers, Ethiopia showed 8.5% annual growth, Addis Ababa 27.5%, and Addis Ababa plus nearby towns 13% per annum. Thus the Addis Ababa region generally showed a smaller increase in the number of customers than Ethiopia as a whole for commercial and low voltage establishments, partly because of the rural electrification drive. Only in the case of high voltage customers did the Addis Ababa area growth exceed the rest of the country. The drive for rural electrification may cause consumption to migrate to more distant areas from Addis Ababa and its nearby towns, which is consistent with the finding on the fastest growth of population which has been in towns more remote from Addis Ababa, and off the main transit routes, such as Jijiga, Mekele and Awasa.

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 23

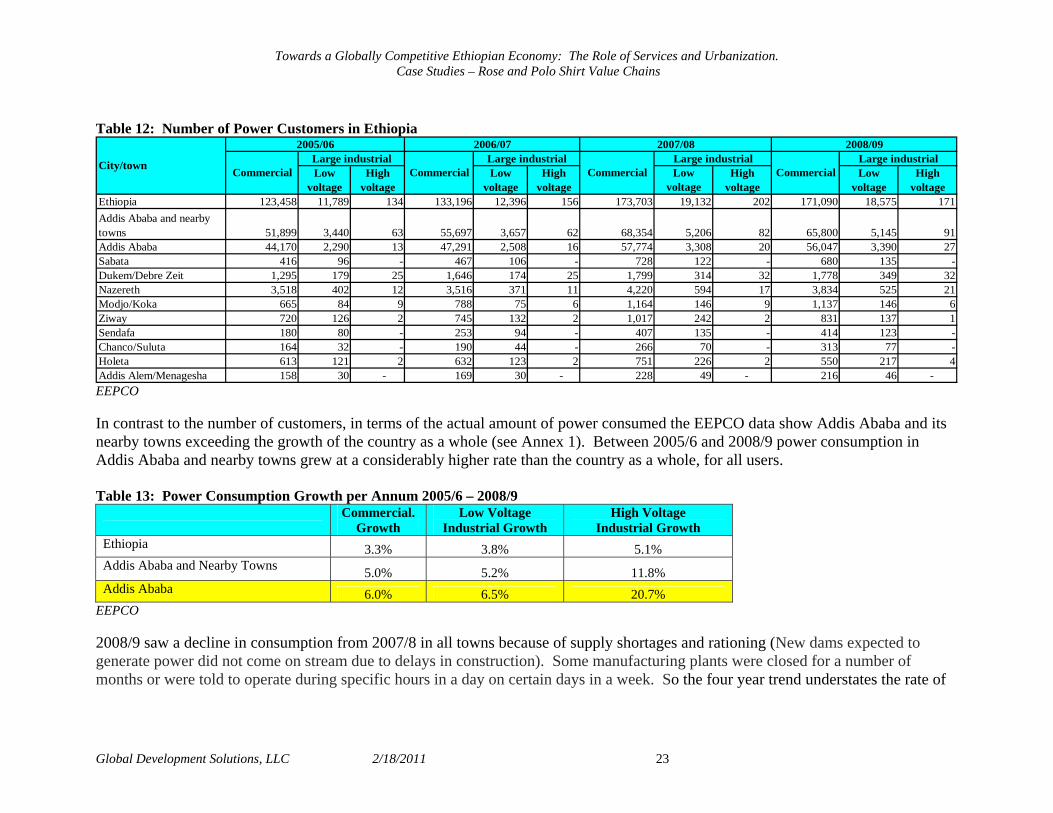

Table 12: Number of Power Customers in Ethiopia

Low voltage

Ethiopia 123,458 11,789 134 133,196 12,396 156 173,703 19,132 202 171,090 18,575 171Addis Ababa and nearby towns 51,899 3,440 63 55,697 3,657 62 68,354 5,206 82 65,800 5,145 91Addis Ababa 44,170 2,290 13 47,291 2,508 16 57,774 3,308 20 56,047 3,390 27Sabata 416 96 - 467 106 - 728 122 - 680 135 - Dukem/Debre Zeit 1,295 179 25 1,646 174 25 1,799 314 32 1,778 349 32Nazereth 3,518 402 12 3,516 371 11 4,220 594 17 3,834 525 21Modjo/Koka 665 84 9 788 75 6 1,164 146 9 1,137 146 6Ziway 720 126 2 745 132 2 1,017 242 2 831 137 1Sendafa 180 80 - 253 94 - 407 135 - 414 123 - Chanco/Suluta 164 32 - 190 44 - 266 70 - 313 77 - Holeta 613 121 2 632 123 2 751 226 2 550 217 4Addis Alem/Menagesha 158 30 - 169 30 - 228 49 - 216 46 -

Large industrialCommercial Commercial Commercial CommercialLow

voltageHigh

voltageLow

voltageHigh

voltageHigh

voltageLow

voltageHigh

voltage

Large industrial Large industrial Large industrialCity/town

2005/06 2006/07 2007/08 2008/09

EEPCO In contrast to the number of customers, in terms of the actual amount of power consumed the EEPCO data show Addis Ababa and its nearby towns exceeding the growth of the country as a whole (see Annex 1). Between 2005/6 and 2008/9 power consumption in Addis Ababa and nearby towns grew at a considerably higher rate than the country as a whole, for all users. Table 13: Power Consumption Growth per Annum 2005/6 – 2008/9

Commercial. Growth

Low Voltage Industrial Growth

High Voltage Industrial Growth

Ethiopia 3.3% 3.8% 5.1% Addis Ababa and Nearby Towns 5.0% 5.2% 11.8% Addis Ababa 6.0% 6.5% 20.7%

EEPCO 2008/9 saw a decline in consumption from 2007/8 in all towns because of supply shortages and rationing (New dams expected to generate power did not come on stream due to delays in construction). Some manufacturing plants were closed for a number of months or were told to operate during specific hours in a day on certain days in a week. So the four year trend understates the rate of

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 24

growth overall. Two of the small towns near Addis Ababa (Debre Zeyt and Sabata) have rapidly increased their high voltage consumption, the main users of which are industries such as cement, glass, sugar and metal products. Otherwise the available data show the nearby small towns as decreasing their share while Addis Ababa’s overall share is increasing, as shown in the table below. Table 14: Share of Addis Ababa in Power Consumption

Year 2005/06 2008/09 City/town Industrial Industrial

Commer- cial

Low

voltage High

Voltage

Commer- cial

Low

voltage High

Voltage Addis Ababa and near towns as % of nation 60% 55% 38% 63% 54% 42% Addis Ababa as % of nation 53% 40% 8% 56% 42% 7% Near towns excluding Addis Ababa as % of nation 7% 15% 30% 7% 11% 35%

EEPCO This result is not consistent with a significant decentralization of economic activity from Addis Ababa to its surrounding towns, but seems to support the conclusion based on population growth that economic activity is if anything migrating to more distant cities, and not necessarily on the optimal trade transit routes. To back up findings based on power usage and population some data were also collected from the Statistical Agency on enterprise and employment growth which were available for non-commercial enterprises provides some data for Addis Ababa and nearby towns (see table below). Table 15: Number of Enterprises and Employment in Addis Ababa and its Proximity

Note 1) Data for Addis Alem, Holeta/Menagesha and Koka are subsumed in the nearest township, but not identified. 2) the employment in the table does not include commercial entities and self employed. Source: Central Statistics Agency (CSA), compiled by Global Development Solutions, LLC., 2010. According to the table both formal employment and number of establishments have recently been growing at a remarkably rapid pace. In Addis Ababa there was a recorded

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 25

53% rise (23% per annum) in the number of establishments, and 82% increase (35% per annum) in employment over 2005/6 to 2007/8, far exceeding the growth of power usage or population. Data on growth in the seven nearby towns is patchy but seems to have been lower than Addis Ababa, which is contrary to the indications based on population growth. Sebeta shows the highest level of activity but a relatively low rate of growth. Sendafa has just recently established three medium scale green field production facilities. Ziway shows a rapid rate of increase but again from a very low starting point. Taking together the available data on urban population, employment and output, it seems likely that there has been an acceleration in urban output growth and that Addis Ababa is maintaining its position as the manufacturing and services hub even if its population is increasing relatively slowly. The evidence we have available is, however, insufficient to suggest that other nearby towns have ‘taken off’ as satellites of Addis Ababa, but instead activity seems to have migrated more to distant cities like Makele, Jijiga, Shashemene and Awasa. This is the basis on which the Government has adopted a Plan for Accelerated Sustained Development to End Poverty (PASDEP) 2005/6–2009/10, in order to develop smaller urban centers through a range of measures including:

• Support for municipal authorities; • Infrastructure urban investment; • Improvements to the licensing and regulatory system to allow easier access to

land • Increased availability of land for urban development.

Despite some growth in smaller towns, there seems to be an absence of a critical mass in these towns to warrant support for an internationally oriented service industry. Transport costs remain elevated partly because there is little economic activity and no towns of significant size near the border with Djibouti which could, for example, act as export free zones, or special economic zones that can minimize transport costs on import and export. There is thus a need to support both the existing expansion of services within Addis Ababa, and to encourage the expansion of other urban centers. For low income ‘incipient urbanizers’ like Ethiopia, the World Bank (World Development Report 2009) recommends a policy towards urbanization of spatial neutrality - improving the operation of land markets and the provision of basic public services - rather than one that favors specific locations to allow market forces based on agglomeration effects to determine which urban centers would grow most rapidly. 6. Addis Ababa in Comparison with other Cities The following section provides a comparison of key indicators associated with urbanization among several cities including Addis Ababa. Based on investment climate survey data, some preliminary comparisons of business conditions are provided in the table below. Amongst the differences in the business environment between cities both in Africa and elsewhere (table below) are the following:

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 26

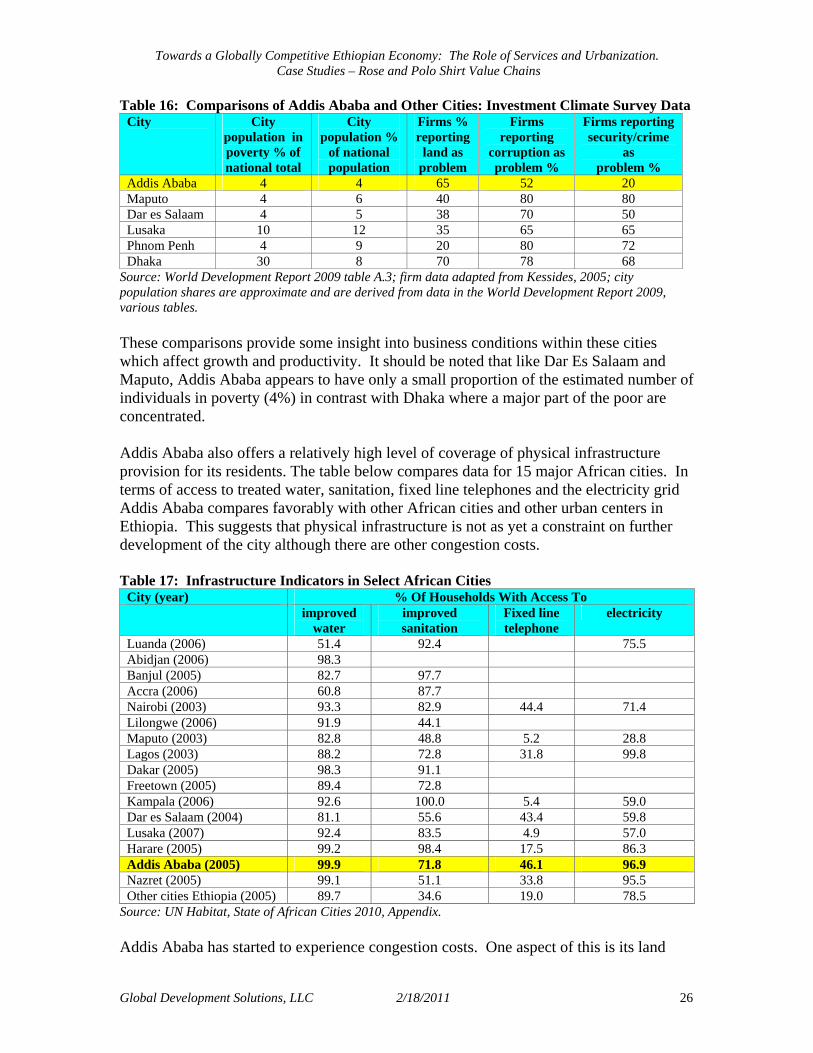

Table 16: Comparisons of Addis Ababa and Other Cities: Investment Climate Survey Data City City

population in poverty % of national total

City population %

of national population

Firms % reporting

land as problem

Firms reporting

corruption as problem %

Firms reporting security/crime

as problem %

Addis Ababa 4 4 65 52 20 Maputo 4 6 40 80 80 Dar es Salaam 4 5 38 70 50 Lusaka 10 12 35 65 65 Phnom Penh 4 9 20 80 72 Dhaka 30 8 70 78 68

Source: World Development Report 2009 table A.3; firm data adapted from Kessides, 2005; city population shares are approximate and are derived from data in the World Development Report 2009, various tables. These comparisons provide some insight into business conditions within these cities which affect growth and productivity. It should be noted that like Dar Es Salaam and Maputo, Addis Ababa appears to have only a small proportion of the estimated number of individuals in poverty (4%) in contrast with Dhaka where a major part of the poor are concentrated. Addis Ababa also offers a relatively high level of coverage of physical infrastructure provision for its residents. The table below compares data for 15 major African cities. In terms of access to treated water, sanitation, fixed line telephones and the electricity grid Addis Ababa compares favorably with other African cities and other urban centers in Ethiopia. This suggests that physical infrastructure is not as yet a constraint on further development of the city although there are other congestion costs. Table 17: Infrastructure Indicators in Select African Cities

City (year) % Of Households With Access To improved

water improved sanitation

Fixed line telephone

electricity

Luanda (2006) 51.4 92.4 75.5 Abidjan (2006) 98.3 Banjul (2005) 82.7 97.7 Accra (2006) 60.8 87.7 Nairobi (2003) 93.3 82.9 44.4 71.4 Lilongwe (2006) 91.9 44.1 Maputo (2003) 82.8 48.8 5.2 28.8 Lagos (2003) 88.2 72.8 31.8 99.8 Dakar (2005) 98.3 91.1 Freetown (2005) 89.4 72.8 Kampala (2006) 92.6 100.0 5.4 59.0 Dar es Salaam (2004) 81.1 55.6 43.4 59.8 Lusaka (2007) 92.4 83.5 4.9 57.0 Harare (2005) 99.2 98.4 17.5 86.3 Addis Ababa (2005) 99.9 71.8 46.1 96.9 Nazret (2005) 99.1 51.1 33.8 95.5 Other cities Ethiopia (2005) 89.7 34.6 19.0 78.5

Source: UN Habitat, State of African Cities 2010, Appendix. Addis Ababa has started to experience congestion costs. One aspect of this is its land

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 27

market which is reported as working much less effectively than in comparable cities, and only in Dhaka does a higher proportion of firms report accessing land as a problem (see table below). Two-thirds of firms in Addis see land as a constraint on their development compared with 35%-40% in Maputo, Dar es Salaam and Lusaka. Much of the problem in Addis appears to have been the extreme delay in land acquisition (around one and half years from agreement to sell). However, in contrast with other cities Addis has the reported advantage of being a relatively safe urban environment with corruption appearing to be relatively less significant than in other cities. The table below gives the investment climate comparative survey data on key business constraints in the selected cities. These are: average days of delay in land acquisition and the average share of security costs and of losses due to theft in total sales. Table 18: Delays in Land Acquisition, Costs of Security and Theft by City Delay in land

acquisition (days) Cost of security (%

of sales) Losses due to theft (% of

sales) Addis Ababa 538 0.9 0.4 Maputo 38 Na Na Dar es Salaam Na 3.1 Na Lusaka 233 4.1 5.9 Phnom Penh Na 20.2 2.9 Dhaka Na Na 0.6

Source: Adapted from Kessides, 2005. Reform of the urban land market in Addis Ababa remains an issue. The 2006 Investment Climate survey ranked access to land as a lesser concern overall (5th out of the 10 main constraints faced by firms) but for service firms it remained the second biggest constraint. For medium size service firms (which would tend to include formal sector long distance transport firms) 73% report land as a major constraint. The Government has introduced a program for the reform of the urban land market with measures to improve procedures for land registration, reform the system of land leases and regularize compensation payments. Progress on these reforms is important in achieving the full benefits of urban agglomeration. Alternatively, more recent data on time required to process a lease for urban land shows more days required in Ethiopia than elsewhere in East Africa. However, Ethiopia is just below the average for sub-Saharan Africa as a whole for leasing public land, and a little above it for private land (see table below). Table 19: Days Required to Process Lease for Urban Industrial land: Selected Countries

Country Private land Public land Ethiopia 75 145 Kenya 65 110 Tanzania 65 80 Uganda 55 75 Republic of South Africa 45 300 Average Sub-Saharan Africa 60 150

Source: Adapted from UN Habitat, The State of African Cities 2010 The World Bank ‘Doing Business’ reports also provide information on a number of constraints that relate the efficiency of the urban sector because they are either under the

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 28

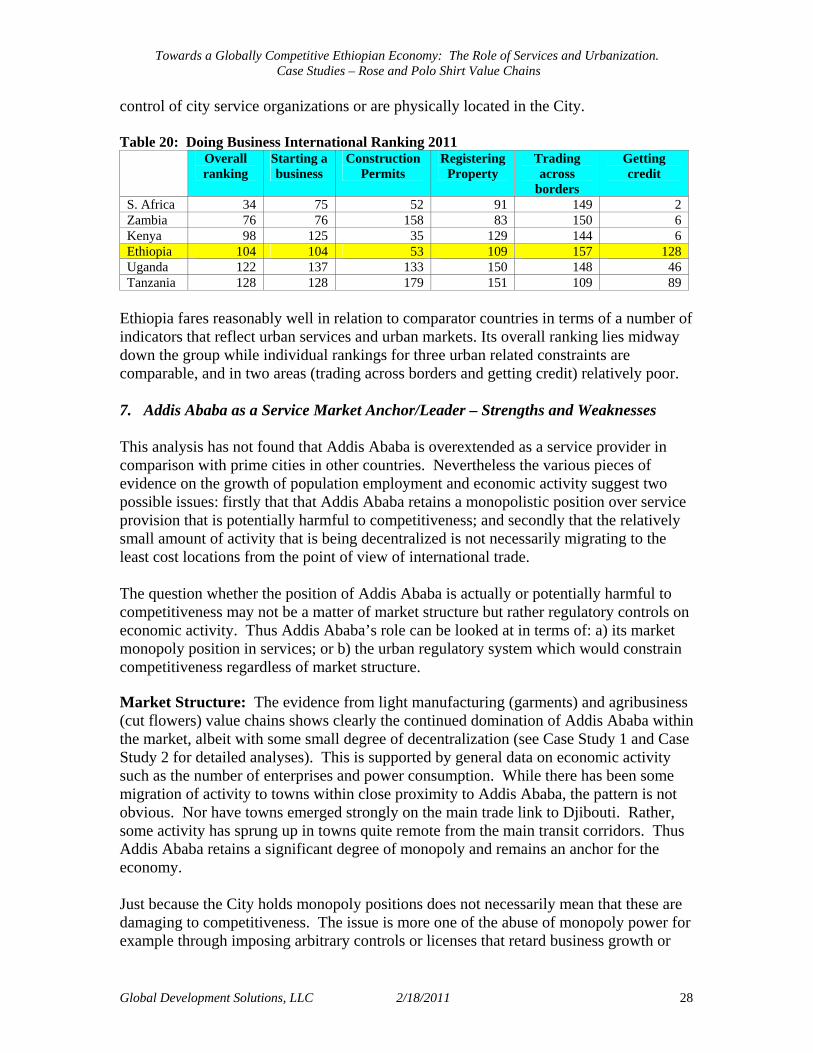

control of city service organizations or are physically located in the City. Table 20: Doing Business International Ranking 2011

Overall ranking

Starting a business

Construction Permits

Registering Property

Trading across

borders

Getting credit

S. Africa 34 75 52 91 149 2 Zambia 76 76 158 83 150 6 Kenya 98 125 35 129 144 6 Ethiopia 104 104 53 109 157 128 Uganda 122 137 133 150 148 46 Tanzania 128 128 179 151 109 89

Ethiopia fares reasonably well in relation to comparator countries in terms of a number of indicators that reflect urban services and urban markets. Its overall ranking lies midway down the group while individual rankings for three urban related constraints are comparable, and in two areas (trading across borders and getting credit) relatively poor. 7. Addis Ababa as a Service Market Anchor/Leader – Strengths and Weaknesses This analysis has not found that Addis Ababa is overextended as a service provider in comparison with prime cities in other countries. Nevertheless the various pieces of evidence on the growth of population employment and economic activity suggest two possible issues: firstly that that Addis Ababa retains a monopolistic position over service provision that is potentially harmful to competitiveness; and secondly that the relatively small amount of activity that is being decentralized is not necessarily migrating to the least cost locations from the point of view of international trade. The question whether the position of Addis Ababa is actually or potentially harmful to competitiveness may not be a matter of market structure but rather regulatory controls on economic activity. Thus Addis Ababa’s role can be looked at in terms of: a) its market monopoly position in services; or b) the urban regulatory system which would constrain competitiveness regardless of market structure. Market Structure: The evidence from light manufacturing (garments) and agribusiness (cut flowers) value chains shows clearly the continued domination of Addis Ababa within the market, albeit with some small degree of decentralization (see Case Study 1 and Case Study 2 for detailed analyses). This is supported by general data on economic activity such as the number of enterprises and power consumption. While there has been some migration of activity to towns within close proximity to Addis Ababa, the pattern is not obvious. Nor have towns emerged strongly on the main trade link to Djibouti. Rather, some activity has sprung up in towns quite remote from the main transit corridors. Thus Addis Ababa retains a significant degree of monopoly and remains an anchor for the economy. Just because the City holds monopoly positions does not necessarily mean that these are damaging to competitiveness. The issue is more one of the abuse of monopoly power for example through imposing arbitrary controls or licenses that retard business growth or

Towards a Globally Competitive Ethiopian Economy: The Role of Services and Urbanization. Case Studies – Rose and Polo Shirt Value Chains

Global Development Solutions, LLC 2/18/2011 29