This time is different. - Ark Strategic Investmentsarkhedgefund.com/wp-content/uploads/pdfs/... ·...

39

This time is different. A contrarian, global macro fund designed to navigate precarious markets defined by the convergence of simultaneous corrections in multiple over-valued and co-linked asset classes. “Never doubt that a small group of contrarian, intelligent people can change the world; indeed, it’s the only thing that ever has.” -Margaret Mead

Transcript of This time is different. - Ark Strategic Investmentsarkhedgefund.com/wp-content/uploads/pdfs/... ·...

This time is different.

A contrarian, global macro fund designed to navigate precarious markets defined by the convergence of simultaneous corrections in multiple over-valued

and co-linked asset classes.

“Never doubt that a small group of contrarian, intelligent people can change the world; indeed, it’s the only thing that ever has.”

-Margaret Mead

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Thesis

• A False Market Recovery led by historically high deficit spending and misuse of central bank liquidity in the wake of the 2008 crisis.

• Multiple (6) Asset Bubbles sustained by the FED’s multi-trillion dollar QE printing experiment: 1) Real estate, 2) equities, 3) credit and 4) consumer spending. The popping of these four bubbles in 2008 led to massive growth in the two most damaging bubbles, namely: 5) government debt and 6) the U.S. dollar, whose eventual and collective collapse constitutes what we have consistently termed the “Aftershock.”

• All Bubbles Eventually Pop. The sequence of pending corrections/drawdowns will be part of a global economic depression marked by massive currency devaluations (Asia, the EU and eventually the US) and ultimate inflation (with attendant interest rate hikes).

• Precise Timing of the Correction is Impossible. Nevertheless, a debilitating correction/collapse is not only theoretical or probable but mathematically inevitable.

• Ark Investments was formed to actively prepare for and manage the Aftershock through a portfolio designed to meet three primary goals: 1) capital preservation, 2) reduced volatility and 3) absolute return.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Keep It Simple

• Despite an industry of complex strategies and a mystifying use of investment acronyms, behind the façade of the Wall Street mystique are surprisingly simple, historically confirmed, yet conventionally ignored market indicators.

• Decades of navigating the buy-and-sell side of public markets has convinced us of a growing trend of misinformation deliberately lacking context (and tilting more toward propaganda than objective data).

• Market cheerleaders outnumber fiduciaries in an industry naturally compelled to sell confidence in the very markets which sustain their profession (96% of broker recommendations are “buy/hold”). Increasingly rare are voices accepting simple yet unpopular realities, such as candid facts about inflated asset classes.

• Our approach is neither radical nor dramatic. We are not perma-bears spreading negativity. Rather, our objectives stem from a simple conviction:

Six years of quadrupling the money supply, doubling the debt and grossly inflating the core asset classes without stimulating real growth or full-time, wage-improved employment is a

recipe for a massive market fall.

It’s that simple.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Macros Matter: Key Facts

• Increasing the money supply (M0, M1, M2), when not accompanied by real GDP growth, mathematically (not theoretically) creates a correlative increase in inflation.

• Since 2008, the Federal Reserve has increased the money supply by roughly 400% (from $870B to over $4T in 2015) using QE printing policies—thus creating a dollar bubble.

• In the same short period, the U.S. has increased its debt level from $8T to $18T—creating a sovereign debt bubble in the U.S., where the debt-to-income ratio is 6-to-1.

• The combined debt and dollar bubbles have temporarily stimulated stock, bond, private credit and consumer spending bubbles without increasing GDP (compounding now at 1.8%, the lowest in over a century).

• The net result is an historically unprecedented perfect storm whereby:

1. Inflation is inevitable and will naturally induce higher interest rates, which trigger market corrections across the major asset classes, themselves all bubbles.

2. The pending correction will not be cyclical or conventional in scope, but rather characteristic of an economic collapse in which traditional buy-and-hold value investing or MPT diversification will be ineffective to preserve capital, generate returns or manage risk.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

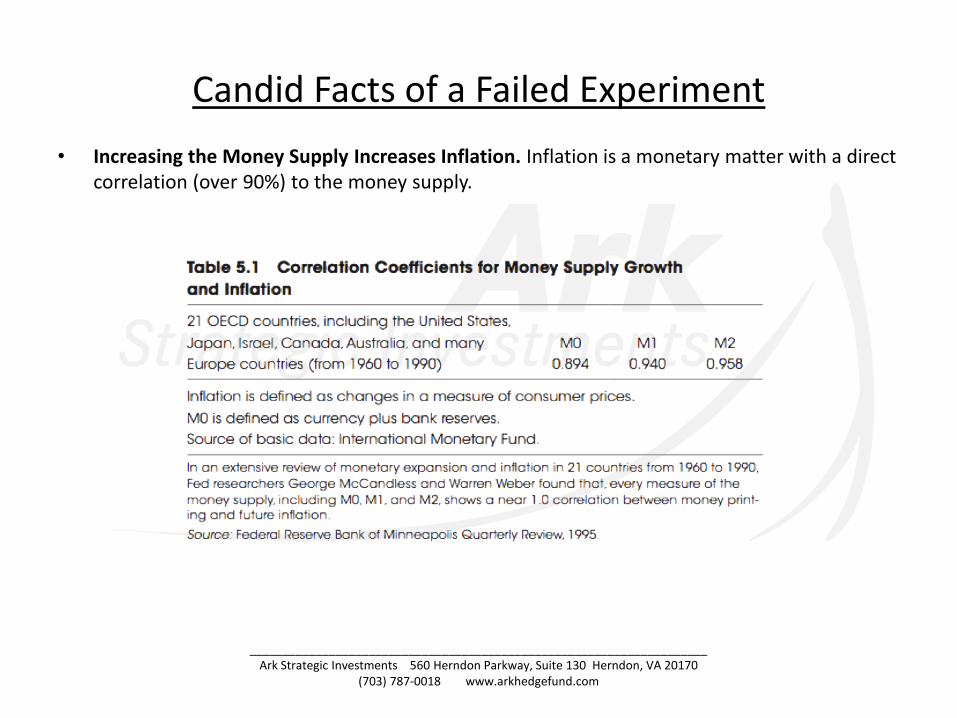

Candid Facts of a Failed Experiment

• Increasing the Money Supply Increases Inflation. Inflation is a monetary matter with a direct correlation (over 90%) to the money supply.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Candid Facts of a Failed Experiment (cont.)

• Neo-Keynesian Growth Premise. The Fed experiment was led by the New Monetarist notion that aggressive monetary policies (ZIRP, QE, Sovereign Balance Sheet Expansion) are justified if and when such policies lead to increased growth, productivity and employment.

• Failed Experiment by All Measures. Despite six years of inflating the money supply and the national debt, there has been weak GDP growth, Depression-level unemployment, and languishing household income.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Candid Facts of a Failed Experiment (cont.)

Sentier Research Household Income Index (HII)

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Common Sense

• An S&P that rises by 30% in the same year earnings are 3% is a bubble.

• A Dow that increases 7-fold (in real terms) since 1980 while GDP increases less than 3-fold is a bubble.

• An over-bought, thinly-traded and yield-compressed bond market driven by a nearly zero-percent interest rate policy whereby a central bank drives demand is a bubble.

• A real estate market in which: 1) the real drivers are low rates rather than population or wage growth, 2) nearly half the purchasers are cash buyers, 3) a third of the mortgages are FHA underwritten, and 4) new household formation is actually down by well over 60%, is not a recovery, but a re-inflated bubble led by a QE-inflated stock market.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

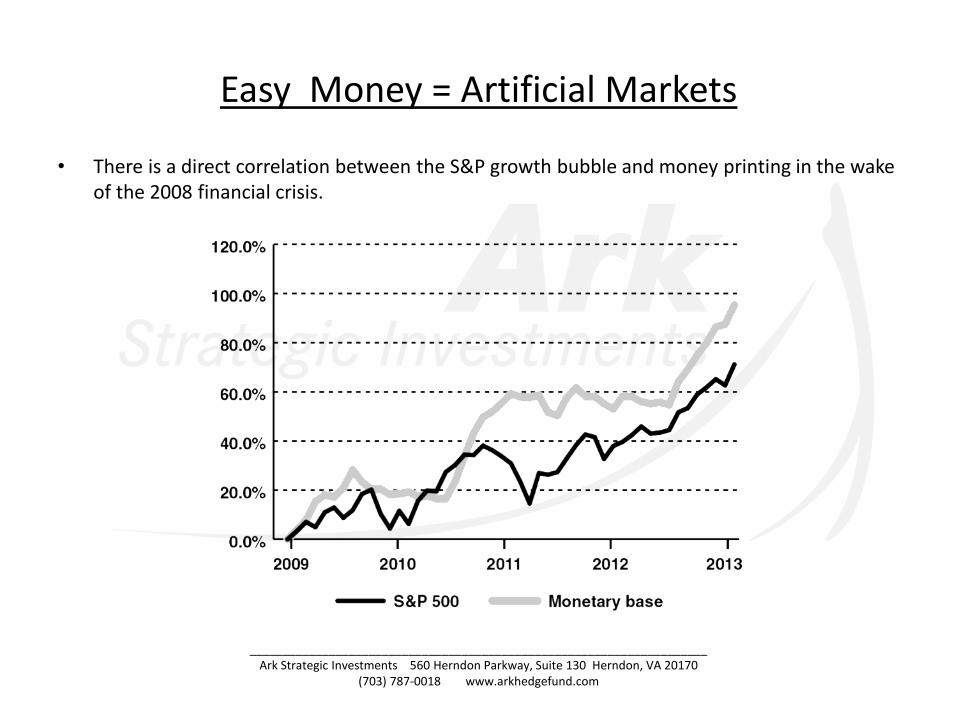

Easy Money = Artificial Markets

• There is a direct correlation between the S&P growth bubble and money printing in the wake of the 2008 financial crisis.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

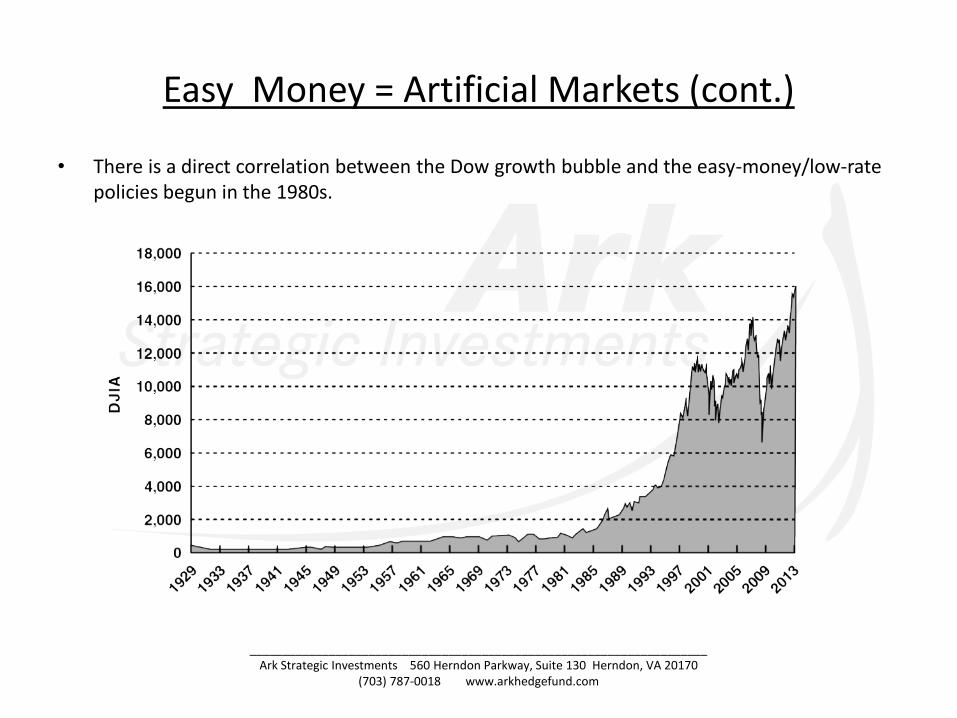

Easy Money = Artificial Markets (cont.)

• There is a direct correlation between the Dow growth bubble and the easy-money/low-rate policies begun in the 1980s.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Easy Money = Artificial Markets (cont.)

• The grossly oversized, highly illiquid bond market, driven by low rates since the 1980s and the recent artificial demand of government support is a bubble poised for inevitable collapse.

• These are not hyperbolic predictions. They are asset bubbles with a mathematically and historically corroborated evolution. When the easy money “pops,” the markets they inflated will do the same thing.

Growth in the Size of the U.S. Bond Market Since 1980

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

History Repeats Itself…

• Markets driven by promiscuous credit and collective risk denial instead of real productivity and earnings are bubbles. Think of 1929, or Japan in 89, the dot-com collapse of 2000, or the sub-prime burst in 2008.

• 2008 was a culmination of false confidence in an unregulated derivatives market whose lack of fundamental value was misunderstood by the wire houses, rating agencies, investors, central bankers and industry “experts.” This conventional lack of wisdom brought markets to a crisis. The response was money creation unlike any before in history.

• The post-2008 policy of printing money to cure or sustain structurally broken and over-valued markets became an addictive medication rather than a cure, resulting in the creation of even larger bubbles to revive or support past ones. This policy has inflated the U.S. money supply and equity and debt markets to unprecedented and unsustainable levels.

• QE gave temporary relief for the 2008 sickness, but the medicine is now a poison, having resulted in what is a familiar yet repeated (as well as collective) pattern of false confidence and misunderstood valuation of the very markets QE was intended to save. And once again, “expert” conventional lack of wisdom—from the wire houses to the Federal Reserve—is overlooking the obvious: new bubbles don’t solve structural problems. To the contrary, new bubbles just make old problems bigger.

Yet despite history’s capacity for repeating itself…

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

…This Time, It’s Different. It’s Worse.

Why?

Because now we are facing a currency and debt bubble.

The Fed printed more new money in 2013 than in its entire history up to 2007.

The national debt was already very high at $9.5 trillion in 2008. Since then we’ve nearly doubled it.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

…This Time, It’s Different. It’s Worse. (cont.)

• We’ve seen bubbles before, from the dot-com craze (1990s), to the housing rush (2000s), from the tulip revolution (1600s) in Holland or the South Seas stock bubble (1700s) to the crash of the Nikkei in Japan (1980s) or land booms in Florida (1920s). But none of those bubbles, including the recent sub-prime bubble, shared the greater and implicit dangers of the current environment, which is composed of numerous, co-linked bubbles, culminating in sovereign debt and currency bubbles, for which there is no safety net, no further bailout, no new medicine. Bluntly:

The Fed can’t afford to “bail out” the next collapse. It will need to “print” more money and hence the momentarily strong USD, like all the “QE-made” currencies will experience inevitable devaluation leading to inflation.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

… and When a Currency Bubble Pops

• Inflation arrives,

• Interest rates rise,

• And markets continue to dive.

It’s that simple. It’s that certain.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

And It’s Global

• Central banks propping up markets via money creation (QE) is not just an American phenomenon. The Japanese invented QE in the wake of the NIKKEI collapse in ’89. The QE playbook has been modified and passed around by the major central banks of the world since then, in the U.S., the UK, the Eurozone and China. Net result?

Debt and currency devaluation is now a global problem, and thus a global source of additional bubbles which add to

the scope of the Aftershock.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

And It’s Global (cont.)

• Since 2009, money supply in the UK is up over 350%, in the EU over 200%, and in a non-transparent China (where the debt-to-GDP level is at least above 200%) money supply has increased by more than 500%.

• The global economy, like the bubbles which define it, is highly linked (Brazil, for example, exports to China, which exports to the U.S., which in turn exports to the EU, which in turn supports emerging markets, etc). When any or a part (or all) of these inter-linked economies suffer a recession or currency crash, the entire cycle of geographies and markets suffer.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Why This Isn’t Obvious to All?

• Human Nature: It’s human as well as market nature to collectively turn away from negative evidence and collectively buy into positive spin.

• Boring: Most investors don’t have the time or interest to sift past endless opinions and look at the cold math and history of bubbles, inflation and market collapse. Topics like debt-to-GDP ratios, QE policies, inflation correlations and CPI flaws are boring, time consuming and ultimately disturbing.

• Denial/Self-Interest: Many market professionals prefer denial to deeper analysis, as denial allows for the selling of confidence in the very markets that sustain their livelihoods. At a time when investors need candid voices revealing blunt yet unpopular dangers, we are left with televised fluff and wirehouse salesmanship rather than a sober analysis from objective fiduciaries. CNN, in short, is far more soothing and popular, than Minsky, Graham, Friedman, von Mises or even Adam Smith. Today, Panglossian optimism is embraced with greater ease than unpopular facts. Our greatest bubble is a “groupthink” bubble.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

The Counter-Theories(Our responses are italicized)

• Banks are keeping this printed money in excess reserves and thus it won’t “escape” into the velocity of the economy and cause inflation. (Money—M1—is in fact in the economy, doubling since 2008, and thus not “on reserve.”)

• Falling asset prices (deflation) will counteract/dilute the inflation threat posed by the Fed’s money supply increase. (Deflation, like inflation, is caused by changes (viz. reduction) in the money supply, not falling asset prices, which today are the result of weak demand and oversupply, not deflation, as this term is correctly intended/used.)

• The government and banks will write off the debt in the future to avoid catastrophe. (Forgiving debt does not make the money already spent disappear. If I owe you $20.00 and you forgive the debt, the $20.00 is still “out there.”)

• The Fed knows what it’s doing, and is printing just the right amount of money to safely avoid inflation. (This is the same Fed that gave us [and failed to predict] the housing bubble in 2006 and the sub-prime bubble in 2008; it is no wiser today than it was then. Furthermore, the Fed can’t undo all its purchases of low-rate/yielding bonds and MBS, as there are no buyers for them; if there were, the Fed wouldn’t be doing the buying itself. In essence, the Fed has made itself a badly collateralized bank.)

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

The Counter-Theories

• The USD is the world reserve currency, and “too important to fail.” (The dollar is a fiat currency backed not by gold, but by trust. Once confidence is lost—which could be caused by any number of events—the relative strength and importance of the dollar won’t prevent a global dumping of the currency, as has happened before. And yes, relative to other currencies [Yen, Euro etc], the USD may be the best patient in the ICU, but it will still be a very sick patient…)

• We’re fine, or else we’d already have inflation. (There are lag factors which slow the arrival of inflation, the most alarming of which is how much is at stake. The markets and the Fed have more at stake in propping the USD and markets than at any other time in history. Candor about real and pending market implosions and inflation today would be like pulling the finger out of a dyke. Hence the current and ubiquitous Panglossian groupthink we see with an eerie and increasing frequency in the financial media. Furthermore, we do have inflation. The CPI is an intentionally broken measure of inflation and if adjusted accurately—like the SGS Alternate—places current inflation above 10%. One feels this already at the toll booths, the tuition bill and the grocery store.)

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

How/When Will the Rain Come?

• After leverage and concentration risk, the next biggest risk to any portfolio is timing risk. In short, no one can precisely time a market shift. That being said, you don’t need a weatherman to tell you exactly when it’s going to rain if thunder clouds fill the horizon. You simply need an umbrella, or—in the storm we anticipate—an Ark.

• We see a dark horizon. What will trigger the rain? Any number of possible scenarios:

– A slowdown in China’s tremendously fragile, bubble-driven growth, or…

– Political or economic tipping points in emerging markets in Asia, the Middle East, Russia, North Africa, or…

– A deepening recession in the EU, threats to the petrodollar arrangement, a gold-buy panic…

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

How/When Will the Rain Come? (cont.)

But the ultimate triggers will be time and interest rate moves.

– As time passes, the positive investor psychology paid for by the easy money of QE and deficit-spending (in the US and around the world) will lose its mythical appeal. The bond market, and not the central banks, will begin to set rates and price risk, and thus rates will rise. This will be an obvious sign of rain.

– As rates rise, markets will fall. And just as Hemingway described poverty as “starting slowly then coming all at once,” so too will the stock and bond markets collapse, as investors slowly, then “all at once,” realize they’ve been living in a series of bubbles.

– The central banks won’t be able to stop this inflation-led deluge using their old tricks—inflation can’t be cured by more inflation. That is the Aftershock.

The rain is coming…

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

And When Did Noah Build the Ark?

Before the rain.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Our Approach

• Candor

• Educate, rather than pitch

• Active management that preserves and grows capital with reduced volatility

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

What’s In the Ark?

• Ark Investments is not a tail-risk/black-swan fund seeking to perform exclusively in the wake of an Aftershock.

• Actively managed to operate before, during, and after a high-inflation/interest-rate driven market collapse.

• Tracks macro and micro economic indicators signaling entry and exits points.

• Uses a range of asset classes and instruments (equities, credits, currencies and hard assets via direct shares, ETF’s, indexes, CDS etc.)

• Avoids buy-and-hold strategies in conventional, correlation-sensitive asset classes.

• Favors carefully timed/signaled positions in those sectors and asset classes which have opportunistic (“Pre-Rain” and “Post-Rain”) upside and manageable duration risk.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

What’s in the Ark (cont.)

• Ultimate bias for those asset classes which excel in highly inflationary markets.

• “Ride” current QE markets/bubbles that still have risk adjusted upside until our signals suggest otherwise.

• Avoid and/or short (depending on market signals) those currencies, sectors and commodities adversely impacted by inflationary moves or exhibit high market beta (correlation) in declining markets.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

And Gold?

• The hardest bubbles to see are the ones you’re in and the ones to come.

• Ultimately, we never liked gold as an asset class (too volatile, regulated and intervened).

• But in times of crisis, we love gold. We see gold as the next big bubble, yet...

– “Buy Gold” advertisements/stores are everywhere, which skeptical minds would rightly interpret as the sign of an over-bought bubble; so why buy a bubble?

– Since 2000, the price of gold has soared 300%, despite recent corrections; so why buy a bubble?

– Conventional wisdom is skeptical of gold—it has no application and is speculative—so why buy its bubble?

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

And Gold? (cont.)

• Because this bubble still has a long way to go.

– Gold performs when stock, bond and currency markets weaken and inflation and interest rates climb.

– Yet even during a decade of record high stock and bond prices, a still strong dollar, low reported inflation and nearly zero-percent interest rates, we’ve seen gold increase dramatically (revealing just how nervous our “recovery” really is).

– Given gold’s strong performance in conditions adverse to its demand, consider how gold will perform when Aftershock conditions are ideal for gold, i.e. when stock, bond and currencies collapse and inflation and interest rates climb?

– Gold, which has a limited supply and moves quickly and powerfully, will have an immense national and global demand pull (and price climb) as markets correct in the coming storm.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

And Gold? (cont.)

• Does this mean we are a gold-bug fund or a gold-only trade? Not at all. We keep emotion to the side and the numbers and facts before us, and they point toward gold as a key, yet not predominant, part of any pending portfolio.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Strategy

• The Ark Fund uses a global macro approach with minimal leverage to prepare for and invest in markets before, during and after the Aftershock.

• In pre-Aftershock markets still characterized by Fed-policy sustained asset classes, the Ark Fund will engage in appropriate equity and fixed income sectors/positions, typically aiming to carefully ride QE-driven markets in sectors/regions where some upside remains.

• As conditions suggest the approach of the Aftershock (i.e. obvious rate and gold valuation changes and other key and proprietary indicators), the Ark Fund will make strategic allocations from more traditional equity and credit positions into carefully screened foreign currencies and precious metals, as well as to a broader diversification of assets, including, but not limited to specific hard assets.

• In longer-term, post-Aftershock markets, the Ark Fund will exit (and take profits from) those assets, in particular gold, which will have run the course of their own cycles and have reached the risk of over-value and subsequent correction(s). Ultimately, the Ark Fund expects to move the majority of its assets into a deep value strategy, seeking effectively to “bottom-feed” via direct equity investments made possible from the immense upside potential created by an expected and significant downward re-pricing of post-Aftershock assets.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Risk Management

• Risk Management is based on numerous factors, most notably tracking, anticipating and reacting to key macro and asset specific indicators developed by the Ark Fund’s expert management, which has written (and traded) extensively on these matters.

• The Ark Fund was launched in part on the premise that various market complexities [driven primarily by 1) derivative over-leverage and 2) misguided monetary policies have made traditional market risk models inadequate for modeling, measuring and anticipating sudden market shocks. Consequently, conventional risk management tools will not be key indicators.

• Although the Ark Fund will use regression models and VaR tools, risk management will rely more particularly on the experience of the Portfolio Manager and the macro indicators developed, studied and employed from direct experience.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Risk Management (cont.)

• The Ark Fund operates with a risk management committee that meets weekly and includes the Portfolio Manager and key analysts with extensive market experience. The committee gives particular attention to counterparty and operational risks during the market cliff.

• Although no absolute restrictions are anticipated, the Ark Fund expects to use minimal leverage, with average net exposures typically no greater than 60% and gross exposures at no point greater than 200%. The Ark Fund does not foresee significant use of leverage except under special circumstances prior to the Aftershock. Because the Ark Fund is not seeking to outperform market averages in the pre Aftershock environment, the need for leverage is greatly reduced; the Fund expects to use minimal to no leverage thereafter, as the Fund anticipates minimal to no availability of leverage under expected market conditions in the post-Aftershock environment.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

In Summary

• Macro conditions (misunderstood or ignored by the majority of market professionals) point to a convergence of numerous and co-linked asset bubbles.

• These asset bubbles were inflated by an historically unmatched combination of exaggerated deficit and money supply increases— “The New Monetarism.”

• New Monetarism is theoretically justified by increasing productivity (GDP) and employment, neither of which has occurred.

• All bubbles pop.

• These popping asset bubbles culminate with the popping of the two largest and most dangerous bubbles: the U.S. debt bubble and the U.S. dollar bubble. There is no safety net.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

In Summary (cont.)

• The collapse of the stock and bond markets, and the inevitable inflation, interest rate climb, and global currency disasters portended by these bursting asset classes is mathematical rather than theoretical.

• This time is different. With a 400% increase in the money supply and a debt-to-income ratio of 6-to-1, market collapse will come. Traditional buy-and-hold strategies will not enjoy traditional and cyclical market recoveries, because the markets are no longer traditional, but grossly distorted, and there will be no more funds left at the central banks to “bail out” the next crisis, which we’ve made bigger than the last one.

• Active management by those versed in distorted, over-valued markets is essential to navigating and profiting in the macro-driven conditions of today and tomorrow.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Team

Robert Wiedemer – Managing Director

In 2006 Mr. Wiedemer wrote the landmark book that predicted the 2008 financial crisis and its aftermath, America’s Bubble Economy, published by John Wiley. As Paul Farrell, Senior Investment Columnist at Dow Jones MarketWatch, said “In short, America’s Bubble Economy's prediction, though ignored, was accurate.” Kiplinger’s chose it as one of the best business books of 2006.His following book, Aftershock, was published by John Wiley in November 2009. It was chosen by Smart Money magazine as one of the five best investment books of 2009. Aftershock Second Edition was published in August 2011 and became a New York Times and Wall Street Journal Bestseller. Both books have sold over 750,000 copies.

Aftershock has also received widespread international interest. It has become a bestseller in Korea and has also been translated into Chinese and Japanese. Aftershock and America’s Bubble Economy have been the subject of articles in the major press including the Wall Street Journal, Financial Times, The New York Hedge Fund Journal, Euromoney, Barrons, Reuters, AP, and others. Mr. Wiedemer also co-founded MacroView Investment Management, a Registered Investment Advisor with over $200 million in assets. MacroView focuses on separately managed accounts with varying objectives, but are generally managed in a conservative manner with significant holdings of gold and the goal of a higher Sharpe ratio.

Mr. Wiedemer’s fourth book, The Aftershock Investor, was released in September 2012 and is a Wall Street Journal Bestseller. The Aftershock Investor Second Edition was released in October 2013 and Aftershock Third Edition was released in April 2014.Robert Wiedemer speaks to groups of investors, financial analysts and economists including the New York Hedge Fund Roundtable, SIFMA, CFA Societies, the World Bank, the Army’s Training and Doctrine Command, and the National Press Club. He is a frequent commentator on TV, including CNBC and Fox Business News. Mr. Wiedemer holds an MS-Marketing from the University of Wisconsin - Madison.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Team

David Wiedemer, Ph.D – Managing Director

David Wiedemer, Ph.D is the co-author of the landmark book, America’s Bubble Economy, published in 2006. The book predicted the Great Recession and the popping of the housing, private credit, stock and consumer spending bubbles. His series of predictions were contrary to most major economists and government officials. His analysis provided the macroeconomic basis for the economic analysis and predictions contained in the book.

Mr. Wiedemer also co-wrote the bestseller Aftershock, now in its third edition, where he again provided the economic analysis underlying their accurate financial and economic predictions. Aftershock became a New York Times and Wall Street Journal Bestseller. Mr. Wiedemer also co-wrote The Aftershock Investor. The second edition was released in October 2013. Both books have sold over 750,000 copies.

Mr. Wiedemer also co-founded MacroView Investment Management, a Registered Investment Advisor with over $200 million in assets. MacroView focuses on separately managed accounts with varying objectives, but are generally managed in a conservative manner with significant holdings of gold and the goal of a higher Sharpe ratio.

Mr. Wiedemer holds a Ph.D in economics from the University of Wisconsin - Madison and a BA from the University of Pennsylvania.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Team

Matthew Piepenburg – Managing Director

With over 20 years experience as the GC and, later, CIO of a Single Family Office (J.HowardJohnson), as well as the Managing Director of a Multi-Family-Office (Massey Quick & Co), Mr. Piepenburg has overseen the allocation of over $5B in investable assets over a full range of portfolios and alternative investment vehicles. He has lead the quantitative and qualitative due diligence on hundreds of diverse hedge fund managers and strategies and has developed a unique expertise as to the best practices and diverse strategies of the world’s premier investment funds. This expertise has informed an equally strong understanding of macro forces and their essential role in selecting the most efficient and timely strategies for long term asset preservation and growth. Mr. Piepenburg graduated with the highest honors from Brown University (magna cum laude, phi beta kappa) and holds a Masters and Law degree from Harvard and the University of Michigan. Fluent in French and German, he is the author of numerous international white papers on macro conditions, asset classes and global risk management strategies.

_____________________________________________________________________Ark Strategic Investments 560 Herndon Parkway, Suite 130 Herndon, VA 20170

(703) 787-0018 www.arkhedgefund.com

Terms

• Domestic Fund: Ark Strategic Investments, LP (the “Fund”)

• Fund’s General Partner: Ark Strategic Investment Partners, LLC

• Auditor: McGladrey

• Prime Broker: BTIG (Goldman Sachs, Custodian)

• Administrator: Gemini Fund Services

• Legal Counsel: Alston & Bird LLP, New York, New York

• Investor Type: Accredited Investor ( “3(c)1 Fund”)

• Investment Minimum: $500,000.00

• Fee Structure: 1.5 and 20. (Management Fee of 1.5%; Performance Allocation of 20%)

• Redemption/Liquidity Rights: Requests allowed Monthly with 60 day liquidity

• Other Notes: Foreign and US tax-exempt investors have the option of an off-shore fund arrangement via a master-feeder structure.