Think Fundsindia - February 2017

9

Your post-budget strategy The markets cheered the 2017 Budget proposals with a sharp rally on Budget day. What made the market give it a thumbs-up? For one, Budget 2017 touches many people and industries in small ways. So it seeks to make maximum impact with minimum cost. Two, it appears to aim for macroeconomic stability than trigger immediate growth. It focuses on fiscal prudence, social and rural development and on stabilising slowing/weak sectors such as real estate and infrastructure. Three, it plans for better quality of spending, by slowing growth of revenue spending and improving capex spending. From an equity market perspective, the following proposals were significant: - Foreign Portfolio Investors (FPI) have received clarity on taxation – be it long-term capital gains tax or other indirect tax provisions. With the uncertainty removed, conditions augur well for more investments by FPIs. - Rural spending can be expected to keep consumption ticking. - Infrastructure spending and benefits to real estate can be expected to have ripple effects across multiple sectors including cement, steel and allied sectors and curtail any significant slowdown post demonetisation. What is the budget telling you? It is time to move to more regulated investment options that will also deliver returns. In the current low interest rate scenario, only mutual funds offer this. So here’s what you should do, post budget: - We believe that the markets are indeed factoring a turnaround in earnings. The budget provides scope for re-rating in certain sectors and that could in turn drive the markets. Having said that, as valuations are not at their best now, exposure to either large-cap/diversified funds or balanced funds would be the way forward. We would not hesitate to suggest partial deployment of lumpsum followed by SIPs in the above fund categories. - In the case of debt, while low inflation could provide some room for rate cuts, the case for investing in income accrual funds is higher today for investors looking to build long-term portfolios as the yield rally may be at its last stage. For a more detailed view on the budget read our detailed article inside. Vidya Bala Head – Mutual Fund Research FundsIndia.com February 2017 ■ Volume 07 ■ 02 Budget 2017 By the time this issue hits your inbox, I’m sure you'd have read a plethora of articles on the budget. Our own research team will provide a unique FundsIndia take on it - from the perspectives of investing and personal finance. The consensus opinion on the budget appears to be that this is a fine balancing act by the minister, emphasizing more on stability and continuity rather than on dramatic reform efforts. Time will tell if he and his team have gauged the impact of global trends accurately. Personally, I liked a couple of aspects about the budget - the committed push towards a digital economy, exemplified by the ban on cash transactions above Rs 3 lakh and the Aadhaar based payment method. Another laudable attempt was the effort to clean up the augean stables of political funding - by restricting cash contributions to a ceiling of Rs 2000 and creating electoral bonds as an alternative. The commitment shown by this government to clean-up the socio-political economy of the country is commendable. This steady budgetary effort by the minister is a welcome continuation in this regard. Happy investing! Srikanth Meenakshi Co-Founder & COO FundsIndia.com www.fundsindia.com

-

Upload

fundsindiacom -

Category

Business

-

view

10 -

download

2

Transcript of Think Fundsindia - February 2017

Your post-budget strategyThe markets cheered the 2017 Budget proposals with a sharp rally on Budgetday. What made the market give it a thumbs-up? For one, Budget 2017 touchesmany people and industries in small ways. So it seeks to make maximumimpact with minimum cost. Two, it appears to aim for macroeconomic stabilitythan trigger immediate growth. It focuses on fiscal prudence, social and ruraldevelopment and on stabilising slowing/weak sectors such as real estate andinfrastructure. Three, it plans for better quality of spending, by slowing growthof revenue spending and improving capex spending.

From an equity market perspective, the following proposals were significant:

- Foreign Portfolio Investors (FPI) have received clarity on taxation – be itlong-term capital gains tax or other indirect tax provisions. With theuncertainty removed, conditions augur well for more investments by FPIs.

- Rural spending can be expected to keep consumption ticking.

- Infrastructure spending and benefits to real estate can be expected to haveripple effects across multiple sectors including cement, steel and alliedsectors and curtail any significant slowdown post demonetisation.

What is the budget telling you?

It is time to move to more regulated investment options that will also deliverreturns. In the current low interest rate scenario, only mutual funds offer this.

So here’s what you should do, post budget:

- We believe that the markets are indeed factoring a turnaround in earnings.The budget provides scope for re-rating in certain sectors and that couldin turn drive the markets. Having said that, as valuations are not at their bestnow, exposure to either large-cap/diversified funds or balanced fundswould be the way forward. We would not hesitate to suggest partialdeployment of lumpsum followed by SIPs in the above fund categories.

- In the case of debt, while low inflation could provide some room for ratecuts, the case for investing in income accrual funds is higher today forinvestors looking to build long-term portfolios as the yield rally may be atits last stage.

For a more detailed view on the budget read our detailed article inside.

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

February 2017 � Volume 07 � 02

Budget 2017By the time this issuehits your inbox, I’msure you'd have read aplethora of articles on

the budget. Our own research teamwill provide a unique FundsIndiatake on it - from the perspectivesof investing and personal finance.

The consensus opinion on thebudget appears to be that this is afine balancing act by the minister,emphasizing more on stability andcontinuity rather than on dramaticreform efforts. Time will tell if heand his team have gauged theimpact of global trends accurately.

Personally, I liked a couple ofaspects about the budget - thecommitted push towards a digitaleconomy, exemplified by the banon cash transactions above Rs 3lakh and the Aadhaar basedpayment method. Anotherlaudable attempt was the effort toclean up the augean stables ofpolitical funding - by restrictingcash contributions to a ceiling ofRs 2000 and creating electoralbonds as an alternative.

The commitment shown by thisgovernment to clean-up thesocio-political economy of thecountry is commendable. Thissteady budgetary effort by theminister is a welcome continuationin this regard.

Happy investing!

Srikanth MeenakshiCo-Founder & COOFundsIndia.com

www.fundsindia.com

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

MORE SAVINGS, MORE HAPPINESS

• Long term wealth creation solution.• An Equity Linked Savings Scheme that aims to generate long term capital

appreciation by primarily investing in equity and related securities.

* Investors should consult their financial advisers if in doubt about whether the product is suitable for them.

This product is suitable for investors who are seeking*: Riskometer

Investors understand that their principal

will be at moderately

high risk

Low

Moderately

LowModeratelyHigh

High

Low High

Moderate

• Invest upto ₹ 1,50,000 & Save up to ₹ 46,350^

• ONE time investment for 3 years

• Earn tax free dividends+Tax free Returns#

To know more, visit www.iciciprumf.com or download the IPRUTOUCH app.

^Calculated at the highest tax slab rate applicable for FY 17 on investments u/s 80C. # Distribution of dividend is subject to approval from Trustees & availability of distributable surplus. As per the prevailing tax laws for FY 2017, returns earned after one year are tax-free. Android is a trademark of Google Inc. Apple logo is the trademark of Apple Inc. registered in the U.S. and other countries. App Store is a service mark of Apple Inc.

Invest in ICICI Prudential Long Term Equity Fund (Tax Saving)

This is a sponsored advertisement by ICICI Prudential Mutual Fund

www.fundsindia.com

With the budget being out, let us discuss what thebudget can do for the economy and markets andwhat cues you need to take from them for yourinvestments.

The following broadly sums up the actions intendedin the Budget proposal of 2017.

• Budget 2017 can be called popular, aiming to touchmany people and industries in small ways. It does notdole out largesse aimed at certain sections or to specificvote banks. To this extent, it can be called popular butnot populist

• It appears to aim for macroeconomic stability thantrigger immediate growth. It focuses on fiscal prudenceand social and rural development and on stabilisingslowing/weak sectors such as real estate andinfrastructure

• It plans for better quality of spending, by slowing thegrowth of revenue spending and improving capexspending; thus, trying to keep inflation at bay andgenerate more productive spending

While the budget does not seek to lift any one sector(other than support the slowing real estate), the budgetspending and reforms can be expected to have impact onvarious sectors.

Maximum coverage with minimum cost

The Budget proposes to reduce the direct tax impact ofalmost the entire universe of individuals filing returns,barring high net worth individuals with over Rs. 50 lakhincome. The impact is maximum for low-income taxpayers with taxable income of less than Rs. 5 lakh. It thusreaches out to almost the entire 3.7 crore tax filingindividuals. This move, prima facie, can be considered a

carrot for the salaried tax payer, probably hurt bydemonetisation. However, it is also meant to encouragethe non- tax-filing individual to come into the tax systemwith low, painless rates of tax. Whether this will achieve itspurpose, one must wait and watch. As such, the revenueforgone, at such low slabs, won’t hurt the government totry this out.

The other move, seeking to reduce the income tax rates of96% of domestic companies (MSMEs with turnover ofup to Rs. 5 crore) to 25% rate, from the present 30%, is afar significant one as it provides relief to many smallcompanies that do not enjoy much of the economies andbargaining power of their larger peers.

While there is no big bag stimulus to the economy fromthe above, one can expect the above measures to keepconsumption chugging. Seen together with the rural andagricultural spending, India’s consumption story does notappear to have many risks.

Focus on development and stability

The budget has focused on steady spending in key sectorsof social, rural and infrastructure development as shownin the table below. While infrastructure has receivedimpetus, agri boost in the form of higher agri credit andinternet waiver are also noteworthy.

"Through this Budget, the government has prodded individuals towards financial savings overphysical savings, by leaving more cash in the hands of individuals through reduction in the incometax rate of the lowest tax bracket individuals.”Nimesh Shah, MD & CEO, ICICI Prudential AMC

FundsIndia Views: Budget and after

Vidya Bala

In our 2017 outlook, we suggested that three key domestic developments (aside of externalfactors) would have a bearing on the markets. One being budget, the second being rate cuts andthe third being earnings growth.

www.fundsindia.com

Besides stable consumption from increased rural income,sectors such as auto, fertilizers and pesticides could alsoreceive a fillip.

The budget has also been a proactive one in terms ofproviding significant boost to the real estate space, as thesector is expected to bear the brunt of demonetisationand cleaning up.

Whether it is grant of infrastructure status for affordablehousing, 100% deduction of profits in case of affordablehousing with further leeway on carpet area, or longer timefor taxing notional income on unsold inventory, all ofthese provide the much-needed boost to this space.

But some points to be noted are that much of this wouldhelp smaller players and not much of listed entities. Also,more than viewing it as a direct benefit to real estate,investors need to look at the opportunity that will come byin allied sectors such as cement, steel and home fittings,that receive a chunk of their business from the realtysector.

Hence, the ripple effect of the support to this sector canbe expected to be felt in related industries.

Better quality of spending

The 2017 budget proposal also stands out for its moderatespending, suggesting that it is fiscal prudence that scores.The expenditure growth for FY-18 is projected at 7% ona year-on-year basis.

Here again, the growth is tilted towards capitalexpenditure (at 11% YoY) as opposed to revenueexpenditure (6% YoY).

below chart will tell you that the revenue spending growthis among the lowest in recent years. Even in the case ofallocation for MGNREGA, although it is at an all-timehigh, the hike is just 1% over revised estimates of FY-17.These numbers assume importance for 2 reasons: one,after a deterioration in the quality of spending from paycommission pay-outs in FY-17, the spending in FY-18 willensure that inflation is kept at bay.

More importantly, it has provided room for moreproductive capex spending, thus providing a multipliereffect on the economy, and some encouragement forprivate players to follow suit at some point.

Source: Government of India

The misses

While the above points talk of balance and positive impactto the economy there are some misses as well. While thebanking sector received some relief because of NPAprovisioning, not much has been budgeted for bankrecapitalisation. This could remain a sore point for severalpublic-sector banks still saddled with NPA issues,notwithstanding the liquidity from demonetisation. Whilethere are reforms aimed at skill development and alsolabour reforms, there seems no concrete move towardsbroad-basing of skills in a country that derives much ofits jobs from the IT sector. Protectionism policies in keyIT markets for India, while less harmful for IT companiesthemselves, may serve a blow for budding ITprofessionals. Not much thought appears to have gonetowards this.

What is the budget telling you?

The Budget proposal of 2017 may hold positives andsome negatives for your personal finances.However, webelieve there are some cues from the proposal thatsuggests that investing in financial assets linked tomarkets would be compelling now. Let us look atwhat they are:

FPI to hold steady: Foreign Portfolio Investors (FPIs)arethe large stakeholders in the Indian stock markets. Thebudget had alleviated their key fears. One, capital gains taxcontinues to remain exempt if held for over one year.Two, certain indirect transfer provisions caused difficulties(by way of taxation) for FPIs when there was transfer ofstake of investors of India-based funds located abroadbut investing in India-based companies. The budget nowproposes that such indirect tax provisions will not apply to

“If one can say that all the bank credit to a particular case moves under one umbrella and thereforeit becomes easier and faster to resolve, then maybe it is useful. But we should first figure what willbe our method of resolution. Only then we should decide on the form of it.”Chanda Kochhar, MD and CEO, ICICI Bank

www.fundsindia.com

www.fundsindia.com

certain categories of FPIs that include sovereign wealthfunds, central banks, mutual funds and banks. Theremoval of uncertainty on these aspects together withhigh fiscal prudence (if the debt to GDP ratiorecommended by the FRBM committee is followed, itcould result in India receiving a higher credit rating fromIMF), can make India a favoured destination for FPIs.

Move away from physical assets and cash: Apart fromthe many moves to curb cash transactions and also digitisethem there are some subtle hints from the budget thatsuggests that it is good for you to move from physicalassets to cash and that it is prudent to move to regulatedinvestment options. Some of them are as follows:

- That the loss on income from house property is to berestricted to Rs 2 lakh for set off (and can only becarried forward) is a hint that treating property as ameans of ‘investment’ for tax purposes is not aprudent one any more

- While the proposal to provide long-term capital gainsstatus to land and property after 2 years of holdinginstead of 3 years might seem positive; what it also tellsyou is that you have a chance to liquidate your physicalassets faster and make the shift to financial assets

- A draft bill to curtail illicit deposit schemes means thatthe government is serious about taking away highyielding-high risk unregulated schemes from the publicdomain.

Now view the above together with low bank interest rates,stagnant gold prices and a more transparent and lessrigged real estate market. They all mean that youropportunities for building wealth lies more in asset classessuch as equity and debt instruments and in products suchas mutual funds.

What you should do

While the massive rally on budget day may be a hasty one,we believe that the markets are indeed factoring aturnaround in earnings. The budget provides scope forre-rating in certain sectors and that could in turn drive themarkets. Having said that, as valuations are not at theirbest now, exposure to either large-cap/diversified fundsor balanced funds would be the way forward. We wouldnot hesitate to suggest partial deployment of lumpsumfollowed by SIPs in such funds.

As for debt, we believe that while low inflation couldprovide some room for rate cut, the case for investing inincome accrual funds is higher today for investors lookingto build long-term portfolios as the yield rally may be at itslast stage.

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

Where dividends come from

A fund can declare dividends only from realised profits –profits generated by actually selling instruments andbooking profits, or receiving dividend on shares andinterest on debt instruments. The paper profit (unsold)from the instruments is not considered realised profits.The decision on when to declare dividends and theamount of it is the fund manager’s call. That call dependson the state of the debt or equity market, and newopportunities to redeploy booked profits. Since marketsare unpredictable, this realised profit component is notsteady.

Dividend versus growth numbers

There is only one portfolio for a fund. A fund does notmaintain a separate dividend plan portfolio and a growthplan portfolio. To the scheme portfolio itself, whether youhold the dividend plan or growth is immaterial. Thereturns numbers for a fund shown are for the portfolioitself – or how the stocks or bonds that the fund heldreturned. When websites or funds show returns, they areshowing the performance of the fund, and not the plan.Where websites list dividend plans separately (very fewshow it distinctly like that), they assume reinvestment ofdividend when they show the returns.

Because you see the dividend and growth plans returningthe same, you conclude that the dividend plan will giveyou extra returns and more units due to the lower NAVcompared to growth option. Wrong. It does not matterhow many units you have. A lower NAV is not better thanor worse than a higher NAV. The NAV represents theper-unit value of your investment in the fund and isindependent of the fund’s portfolio itself. A fund pays youdividend by deducting it from your NAV and giving it to

you. This effectively translates into you booking profits inyour fund.

Lower compounding in dividend

The amount you invest and how it grows is what isimportant. In routinely getting dividends, you are routinelybooking profits and forgoing compounding benefits. Inthe growth plan, your returns remain with the fund and itcompounds - you are allowing the returns you earn to stayinvested which in turn make returns. That is whatcompounding is all about. As you take out your returns inthe dividend option, you lose this because only your initialinvestment stays.

Here is an illustration, assuming an investment of Rs10,000 in Birla Sun Life Frontline Equity (used forillustrative purposes only) in February 2011. You see howthe worth of your investment in the dividend option, evenincluding the dividend received, is much lower than thegrowth option. Further, once you receive the interest,you’d need to take care not to spend it all. And if you wereto reinvest this dividend, why go for the dividend optionat all?

Dividend: 460.2 units Growth: 117.5 units

Year NAV Dividend Value NAV Dividend Totalincl. Div. Value

2011 21.73 575.24 10,575 85.14 0 10,0002012 19.54 690.29 10,258 81.30 0 9,5492013 22.56 920.39 12,568 101.16 0 11,8822014 20.86 1,104.46 12,890 102.92 0 12,0882015 31.00 2,416.01 19,972 167.91 0 19,7222016 23.08 1,274.74 17,602 151.99 0 17,8522017 24.94 0.00 18,458 182.46 0 21,431

"The plans laid out by the Finance Minister in the Union Budget for 2016-17 are ambitious but theactual implementation may be difficult and will be keenly watched."C Rangarajan, Ex-chairman, PMEAC

Why the growth option is superior

Bhavana Acharya

We always recommend you go for the growth option when investing rather than dividend. Manyof you may wonder why. To understand why, you need to understand where dividends comefrom and what happens to your returns when dividends are paid.

www.fundsindia.com

NAVs as on the 1st Feb of that year. All values in Rs.

Unpredictable dividend

The surplus that an equity fund generates differs frommonth to month depending on the market, the calls thefund takes, and the dividend it receives from stocks itholds.

A debt fund is a bit more certain of its surplus since itknows the interest that accrues. Even then, the surpluswill fluctuate as the instruments it holds change and thecalls the fund takes.

If there is no certainty on the exact surplus, your dividendcan be neither fixed nor guaranteed. The table above is anexample of how dividends vary. For debt funds, you’repaying tax on dividends.

The dividend is taxed at 28.8%, which the AMC deductsfrom the NAV along with the dividend. So not only is yourdividend going to reduce compounding, you’re hurting

your returns further by paying this tax.

Thus, relying on dividend for income is not a good idea ifyou need a certain cash flow each month. The best way forregular cash flows is to go for the growth option andwithdraw from your funds systematically. This is especiallytrue with debt funds, for those in the 10% and 20% taxbrackets.

Those in the 30% tax bracket will have to pay only aslightly higher tax for three years, after which indexationbenefits significantly reduce tax outgo. For long-terminvestments, the growth option is the only way to get thebest return. The longer you stay invested, the greater isthe compounding and the more your returns.

Bhavana AcharyaAnalyst – Mutual Fund Research

FundsIndia.com

www.fundsindia.com

"A very workmen-like Budget. Got some clear indications about how to broaden the tax base inIndia, developments around improving transparency, efficiency, these are all good things."Adrian Mowat, Chief Asian & Emerging Market Strategist, JP Morgan

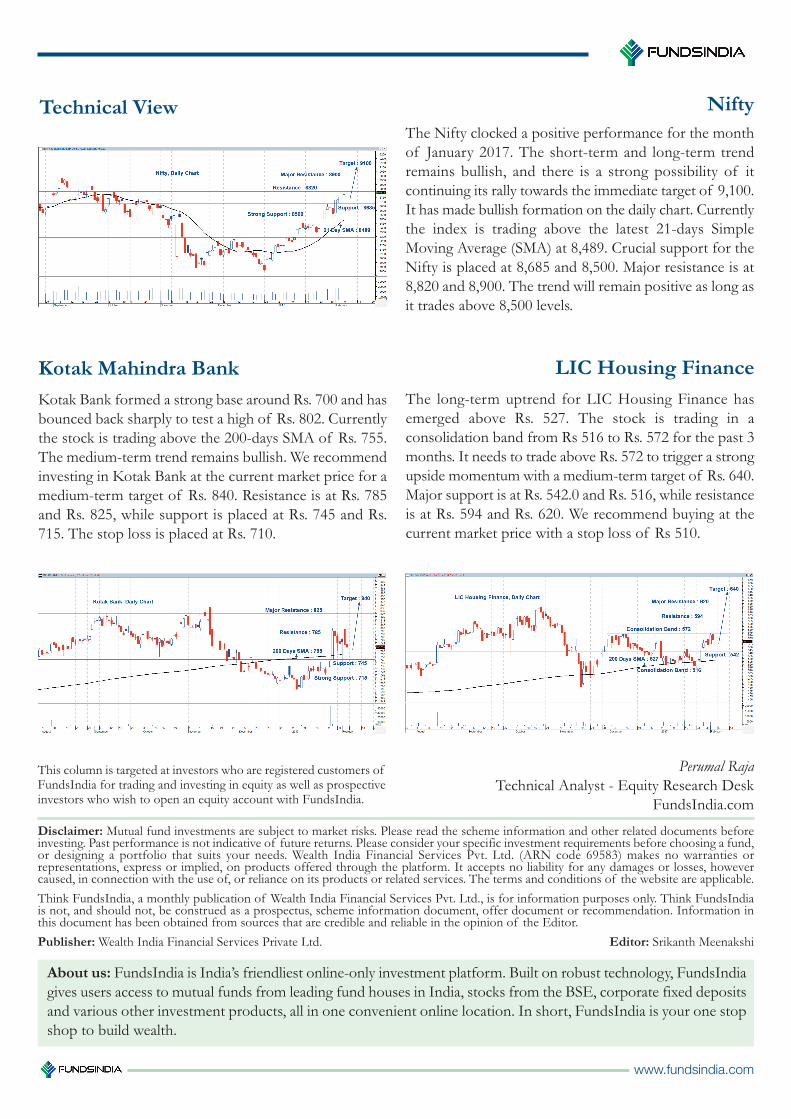

Kotak Mahindra BankKotak Bank formed a strong base around Rs. 700 and hasbounced back sharply to test a high of Rs. 802. Currentlythe stock is trading above the 200-days SMA of Rs. 755.The medium-term trend remains bullish. We recommendinvesting in Kotak Bank at the current market price for amedium-term target of Rs. 840. Resistance is at Rs. 785and Rs. 825, while support is placed at Rs. 745 and Rs.715. The stop loss is placed at Rs. 710.

This column is targeted at investors who are registered customers ofFundsIndia for trading and investing in equity as well as prospectiveinvestors who wish to open an equity account with FundsIndia.

The Nifty clocked a positive performance for the monthof January 2017. The short-term and long-term trendremains bullish, and there is a strong possibility of itcontinuing its rally towards the immediate target of 9,100.It has made bullish formation on the daily chart. Currentlythe index is trading above the latest 21-days SimpleMoving Average (SMA) at 8,489. Crucial support for theNifty is placed at 8,685 and 8,500. Major resistance is at8,820 and 8,900. The trend will remain positive as long asit trades above 8,500 levels.

Perumal RajaTechnical Analyst - Equity Research Desk

FundsIndia.com

LIC Housing FinanceThe long-term uptrend for LIC Housing Finance hasemerged above Rs. 527. The stock is trading in aconsolidation band from Rs 516 to Rs. 572 for the past 3months. It needs to trade above Rs. 572 to trigger a strongupside momentum with a medium-term target of Rs. 640.Major support is at Rs. 542.0 and Rs. 516, while resistanceis at Rs. 594 and Rs. 620. We recommend buying at thecurrent market price with a stop loss of Rs 510.

Technical View Nifty

Disclaimer: Mutual fund investments are subject to market risks. Please read the scheme information and other related documents beforeinvesting. Past performance is not indicative of future returns. Please consider your specific investment requirements before choosing a fund,or designing a portfolio that suits your needs. Wealth India Financial Services Pvt. Ltd. (ARN code 69583) makes no warranties orrepresentations, express or implied, on products offered through the platform. It accepts no liability for any damages or losses, howevercaused, in connection with the use of, or reliance on its products or related services. The terms and conditions of the website are applicable.Think FundsIndia, a monthly publication of Wealth India Financial Services Pvt. Ltd., is for information purposes only. Think FundsIndiais not, and should not, be construed as a prospectus, scheme information document, offer document or recommendation. Information inthis document has been obtained from sources that are credible and reliable in the opinion of the Editor.Publisher:Wealth India Financial Services Private Ltd. Editor: Srikanth Meenakshi

About us: FundsIndia is India’s friendliest online-only investment platform. Built on robust technology, FundsIndiagives users access to mutual funds from leading fund houses in India, stocks from the BSE, corporate fixed depositsand various other investment products, all in one convenient online location. In short, FundsIndia is your one stopshop to build wealth.

www.fundsindia.com

1. Name state government behind the “Digital Dakiya”scheme for the encouragement of cashlesstransactions.

2. X was the first district in the country to have a highspeed rural broadband network. Name X and stateto which is belongs.

3. What is India’s GDP growth forecast rate for FY 17,as per the IMF’s updated “World Economic Outlook(WEO)” report?

4. Where is India’s first cashless island located? Namethe island and its state.

5. Name the entity that launched the “Wave N Pay”contactless card?

Please click here to submit your answers.

Answers for January 2017 Investment Quiz:

1. Rajiv Gandhi International Airport (RGIA),Hyderabad 2. Punjab 3. V.K. Sharma 4.Majuli (Assam) 5. Chhattisgarh

Note : Due to a technical error, last month's quiz linklead readers to an earlier quiz. Due to this mismatch,there is no winner for this month’s quiz. We apologisefor the inconvenience caused.

FundsIndia Select Funds

Investment Quiz

Equity funds - Moderate risk

These are equity-oriented funds that will seek to generate inflation - beating returns and limit downside risks. Therecommended holding period for these funds is at least five years .

Birla SL Frontline Equity Fund (Growth) Invesco India Growth Fund (Growth)BNP Paribas Equity Fund (Growth) Kotak Select Focus Fund (Growth)Franklin India Bluechip Fund (Growth) Mirae Asset India Opportunities Fund (Growth)Franklin India Prima Plus Fund (Growth) SBI BlueChip Fund (Growth)ICICI Pru Focused Bluechip Equity Fund (Growth) SBI Magnum Equity Fund (Growth)Invesco India Dynamic Equity Fund (Growth) UTI Equity Fund (Growth)

What is FundsIndia Select Funds: This is a listing of mutual funds that we think are most investment worthy fora regular investor. We review this list on a quarterly basis. Do note, however, that past performance is not a guaranteeof future results. Please consider your specific investment requirements before designing a portfolio that suits yourneeds. Please click here for a complete listing of our preferred funds.

www.fundsindia.com

Q & A

Q: Of late, I see several such FMP NFOs coming up, with“hold for 39 months and get 4-year indexation benefit” andso on. It would be great if you could share how pastclosed-ended FMPs have performed. That will explaindetails like post-tax, have FMPs done better than bank FDsor equity funds (since it is 3+ year tenure).

Please also explain where we are currently in the interestrate cycle. That will help to choose whether to opt forFMPs or open-ended debt funds.

A: You can look up the performance of past FMPs onaggregator websites. But past FMP performance is notcomparable. Looking at past FMP returns will not tell youwhat new FMPs will deliver, either. FMPs launched indifferent periods lock into different coupon rates and hencetheir returns become hard to compare. Nor would it beright to do so. We are in a falling interest rate scenario now. That meansFMPs launched now will lock into low rates. On the otherhand, open-ended debt funds will benefit from capitalappreciation in the price of their debt instruments as yieldsfall. Hence the returns of open-end medium-term debtfunds will be higher than FMPs.

Vidya Bala Head – Mutual Fund Research

FundsIndia.com