Think Fundsindia - September 2016

9

Seek transparency in other products too Many of you have the luxury of checking your fund performance almost every day. You know exactly how much your funds are returning and what your mutual fund expenses are. You call and ask us how we earn our income, whether we are unbiased in our recommendations and so on. Yes, transparency in the product provides you with a lot of information and allows you to raise a lot of questions. That empowers you as an investor. More power to you! But when you see this kind of transparency and feel encouraged to question more, how is it that some of you completely miss out on how other products operate, how they deliver and what they deliver? Let’s start with your home loan. While most of you would be on floating rates with your home loan, how is it that rates move up quickly but seldom come down (and are cut only if you ask)? This is not the case with your deposits, right? Have you ever questioned your bank on this? Let’s move to investment products. Many investors love money-back insurance policies. Do you know what their returns are? When so many of you are unhappy when your mutual fund performance temporarily dips a bit, how is it that a product that does not beat inflation (consistently) is lapped up by many? Take another popular investment-cum-insurance product – the ULIP. How many of you know exactly how much goes towards charges in your ULIP in the initial years, or how much is actually invested out of the money you pay as premium? Perhaps the lure of tax-savings closes gates on all legitimate questions that one ought to ask. Leave financial products. Let’s take the favourite investment of Indians - property. When a builder prices property how many of us ask him for the latest registered price of the property in that area? Do we ourselves take the pain to check such data? Would the builder or the agent or the local resident ever tell you that the actual rates are lower than what they have quoted? Does it not seem ironical that you check, recheck and question endlessly before starting a Rs 5,000 SIP and yet are willing to commit a cool Rs 50 lakh or even Rs 5 crore in the real estate market, where transparency is made a mockery of ? Seek transparency and answers everywhere! Vidya Bala Head – Mutual Fund Research FundsIndia.com September 2016 ■ Volume 06 ■ 09 Scourge of mis-selling Over the past month, Monika Halan at Mint, has been publishing a series of columns and articles about mis-selling at banks (you can read them here). She carried out a study which found that there are widely prevalent practices of selling inappropriate products to customers at these places. The products most sold are those where the benefits to the banks (by way of commissions) are far higher than those to the customers. This study captures this in a data analytic way using the technique of “mystery shopping” - the method of sending in customers with specific requirements, capturing their experiences, and cataloguing them in a data analysable manner. This is the first time such an exercise has been undertaken and one hopes that this catches the eyes of the regulators. The lesson here is that multi-purposing institutions is a bad idea. Banks are there to fulfil banking needs, not investment or insurance needs. Of course, investors with FundsIndia already knew this and that’s why they are counting on our services to guide them. They know that at FundsIndia, we don’t sell; we advise. Happy investing! Srikanth Meenakshi Co-Founder & COO FundsIndia.com www.fundsindia.com

-

Upload

fundsindiacom -

Category

Business

-

view

104 -

download

2

Transcript of Think Fundsindia - September 2016

Seek transparency in other products tooMany of you have the luxury of checking your fund performance almostevery day. You know exactly how much your funds are returning and whatyour mutual fund expenses are. You call and ask us how we earn our income,whether we are unbiased in our recommendations and so on. Yes,transparency in the product provides you with a lot of information andallows you to raise a lot of questions. That empowers you as an investor.More power to you!

But when you see this kind of transparency and feel encouraged to questionmore, how is it that some of you completely miss out on how other productsoperate, how they deliver and what they deliver?

Let’s start with your home loan. While most of you would be on floatingrates with your home loan, how is it that rates move up quickly but seldomcome down (and are cut only if you ask)? This is not the case with yourdeposits, right? Have you ever questioned your bank on this?

Let’s move to investment products. Many investors love money-backinsurance policies. Do you know what their returns are? When so many ofyou are unhappy when your mutual fund performance temporarily dips a bit,how is it that a product that does not beat inflation (consistently) is lappedup by many? Take another popular investment-cum-insurance product – theULIP. How many of you know exactly how much goes towards charges inyour ULIP in the initial years, or how much is actually invested out of themoney you pay as premium? Perhaps the lure of tax-savings closes gates onall legitimate questions that one ought to ask.

Leave financial products. Let’s take the favourite investment of Indians -property. When a builder prices property how many of us ask him for thelatest registered price of the property in that area? Do we ourselves take thepain to check such data? Would the builder or the agent or the local residentever tell you that the actual rates are lower than what they have quoted?

Does it not seem ironical that you check, recheck and question endlesslybefore starting a Rs 5,000 SIP and yet are willing to commit a cool Rs 50lakh or even Rs 5 crore in the real estate market, where transparency is madea mockery of?

Seek transparency and answers everywhere!

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

September 2016 � Volume 06 � 09

Scourge of mis-sellingOver the past month,Monika Halan atMint, has beenpublishing a series of

columns and articles aboutmis-selling at banks (you can readthem here). She carried out a studywhich found that there are widelyprevalent practices of sellinginappropriate products tocustomers at these places. Theproducts most sold are thosewhere the benefits to the banks (byway of commissions) are far higherthan those to the customers.

This study captures this in a dataanalytic way using the technique of“mystery shopping” - the methodof sending in customers withspecific requirements, capturingtheir experiences, and cataloguingthem in a data analysable manner.This is the first time such anexercise has been undertaken andone hopes that this catches the eyesof the regulators.

The lesson here is thatmulti-purposing institutions is abad idea. Banks are there to fulfilbanking needs, not investment orinsurance needs. Of course,investors with FundsIndia alreadyknew this and that’s why they arecounting on our services to guidethem. They know that atFundsIndia, we don’t sell; weadvise.

Happy investing!

Srikanth MeenakshiCo-Founder & COOFundsIndia.com

www.fundsindia.com

This is a sponsored advertisement by ICICI Prudential Mutual Fund

www.fundsindia.com

FundsIndia Strategies: How to play the debt fund space

The most popular category chosen by many investorsseems to be the ‘dynamic bond’ fund category; what withthis space sporting returns in double digits. With bank FDrates at 7-7.5 per cent, this category’s double-digit returnsover 1, 3 and 5-year time-frames do seem far superior.

But, while dynamic bonds hold potential to deliverbetter-than-FD returns, we would like you to be aware ofthe following:

• The double-digit returns that you see now may notsustain over the long term. In other words, do not lookat the returns prevailing now and expect the same overthe next 5 years.

• While taking exposure to dynamic bond funds, youshould also take some exposure to another debtcategory called income accrual funds, or, simply,income funds. These funds are known to deliversteadier returns with lesser volatility.

Before we move on to showing you why you shouldbalance between the two categories we mentioned, let usquickly bring out the distinction between them.

Dynamic bond and income funds

Dynamic bond funds play on the interest rate cycle andmostly take exposure to government securities, also calledgilts, along with some exposure to corporate bonds. Asthe name suggests, they dynamically manage their averagematurity to ensure they gain from rate movements.

For instance, in a falling rate scenario, they anticipate suchfalls and go for long-term gilts, and thus gain from a pricerally when yields fall. Similarly, in times of rising interestrates, they reduce their average maturity and stay inshort-term instruments to reduce volatility and getreturns. The key risk here is the interest rate. If they get

the rate movement wrong, their returns drop.

Income accrual funds, on the other hand, predominantlybuy and hold short-term and medium-term corporatebonds and other corporate instruments and simply gainfrom the interest (coupon rate) that accrues from thosebonds. They do not try to actively time their entry and exitbased on interest rate.

Their acumen would lie in finding the right opportunitieswith good rates but without much credit risk. Hence, therisk here, if there is any, would be credit risk – that is, therisk of entering into poor quality bonds. But then there aretimes that the quality of the debt instrument they holdimproves and is re-rated by credit rating agencies; thusproviding gains, if the instrument is listed.

Within the income accrual category – you may choose totake lower risks and stick to funds that hold high-quality(AAA-rated) instruments or decide to go with funds(called credit opportunities funds) that take higher risksto get a higher coupon rate.

Historical data suggests that income accrual funds maynot provide periods of high returns like dynamic bondfunds, but they do not see sharp swings in their returnseither. In other words, they provide steadier returns acrosstime-frames and are not dependent on rate cycles.

Having a combination of these two categories of funds will ensurethat you play both these risks – interest rate risk and credit risk -in a balanced manner.

What to expect

The table below tells you the kind of returns that dynamicbond funds and income funds delivered as a category,when their returns were rolled daily for 1-year time-framesover three years.

www.fundsindia.com

Vidya Bala

With the interest rates of bank Fixed Deposits (FDs) moving south, we have seen increasedinterest in debt funds. If you have made a switch from FDs to debt funds now, we believe it isa good move.Debt funds not only ensure that you have low reinvestment risk (case in point being the fall inFD rates now if you have deposits maturing soon), but also provide better post-tax returns,especially for holding periods of three years or more.

“The strong historical outperformance of mid-caps is causing investors to incrementally allocatehigher capital to mid-cap stocks and funds. This may be the reason for its continued outperformanceas it is being backed by flows.”Vinit Sambre, Fund Manager, DSP BlackRock Investment Managers.

www.fundsindia.com

While dynamic bond funds at present appear to havedelivered high returns, in reality they did not do so steadily.The average 1-year rolling returns given below show that,in reality, income funds outperformed.

Clearly, while dynamic bond funds have the potential todeliver very high 1-year returns as they are currently doing,they are also much more volatile as you can see from thehigher standard deviation and lower returns.

Over a 3-year return period too (when rolled daily overfive years), income funds as a category delivered about 8.3per cent on an average, while dynamic bond funds were ata more modest 7.8 per cent. While good funds from thesecategories would have delivered way higher for you; the

point to note here is that income accrual providesopportunities across rate cycles and generates more steadyreturns as a result of its strategy.

Among FundsIndia’s Select Funds we would go withHDFC Medium Term Opportunities for a low-riskincome accrual strategy, and with Reliance Regular Savings-Debt or Franklin India Income Builder if you are lookingfor higher risk income strategies. In the dynamic bondspace, Birla Sun Life Dynamic Bond and UTI DynamicBond are in our list at this point. All these need a 3-yearplus view. With dynamic bond funds, returns may taperoff a bit post 12-18 months. Still, post the capital gainsindexation benefit after three years, they will likely beatFDs by a mile.

“We believe that the consumer discretionary space will see escalation in growth in the coming 12-18months. The second theme we believe is that the public capex is picking up and sooner than laterwe will see a pickup on the industrial side.”Pankaj Tibrewal, Fund Manager with Kotak Asset Management Company.

Category Avg. rolling 1-year Avg. std. dev Best 1-year rolling Worst 1-yearrolling returns return return

Dynamic Bond funds 8.4% 4.0% 21.3% -4.6%

Income funds (includingcredit Opportunity funds) 9.0% 1.8% 16.8% 0.8

Rolling returns over 3 years ending August 16, 2016. Only funds with track record over this period were considered.

Vidya BalaHead – Mutual Fund Research

FundsIndia.com

One-year returns for dynamic bond & income funds

Should you choose the dividend option or the growth option?“Should I go for growth option or take out the dividendsin my fund?” - is a question frequently asked by many ofyou, when venturing into mutual fund investments. Wehave already discussed how dividends are paid out andhow your NAV reacts in a previous article.

We also summarized what to choose. This week, weelaborate on which option to go for, based on your cashflow need.

Which one to choose?

Two key factors will determine what is appropriate optionis for you:

1. Cash requirement and time frame

2. Tax efficiency

Most people base their decisions on tax efficiency. Whileit is a key deciding criterion, let us look at how otherfactors too play a role in choosing between dividendand growth.

Equity funds

Let’s take on the easy one first. Equity funds are meantfor the long term. Your reason for choosing an equityfund must be to build wealth towards some goal which isperhaps at least few years away.

That simply means you should stay invested in the fundand not take the cash out (unless you will invest thedividends back diligently) to help compounding work foryou.

Since, long-term capital gains are free of tax, the solutionhere is simple: As a general principle, go for growth or dividendreinvestment in equity funds.

But there are exceptions: One, in case of theme fundsor sector funds that you hold tactically, you may wish toeither opt for dividend payouts or book profits as thefortunes of themes can take a turn after one good cycle.

Two, in case of ELSS, given that your money is locked in,you may wish to go for a dividend payout if you are in sayyour 50s and are a bit averse to risk and want some profitsin cash during the lock-in.

Young investors should allow their tax saving fund togrow with growth option.

Debt funds

This category gets a bit tricky because the dividend suffersdividend distribution tax (DDT). DDT is nothing but thetax on the dividend.

While it is not deducted on your dividend directly in yourhands, it is reduced from your NAV.

Given this tax component, dividend payout and dividendreinvestment can be tax inefficient. Let us look at whetheryou need to opt for it.

1. You need some cash flows from your debt fund:In this case, you can choose the dividend payout orthe Systematic Withdrawal Plan (SWP) undergrowth option.

Look at the table below. The SWP is a clear winnerfor those in the 10 per cent and 20 per cent taxbrackets. But please ensure that you do not end uppaying exit load. Opt for SWP post the exit loadperiod if you wish to avoid the load.

When you need cash flows

Redemption date 10-20% tax 30% taxbracket bracket

- Is less than 3 years Opt for SWP Opt forfrom date of purchase payout dividend

- Is more than 3 years Opt for SWP Opt for SWPfrom date of purchase

Those in the 30 per cent tax bracket, can go fordividend payout, if you intend to hold the fund forless than three years.

But if you are invested for more than 3 years andredeem post that, then growth option makes sense,since you will get capital gains indexation benefit.

In such cases, go for SWP for regular cash flows.Each such redemption will get capital gain

www.fundsindia.com

“The corporate bond market in India was virtually non-existent; this is a signal… that we shouldget ready to tap available resources, either through retail or corporate bond markets.”Umesh Revankar, Director, Shriram Group

indexation benefit if your investment is more than3 years old.

Remember, switching between options will alsounnecessarily entail capital gains tax if you haveprofits. Hence, get your investment time frame rightwhen you start your investment.

2. You don’t need cash flows from your debt fund:In this case, dividend payout and SWP are notneeded since you have no cash flow need.

You therefore have 2 options – to go for growth ordividend reinvestment. Look at the table below -growth option scores in most cases, except whenyou are in the 30 per cent tax bracket and redeem inless than 3 years.

This will be true in case of liquid funds orultra-short-term funds that you may park for a shortwhile. In that case you will suffer DDT of 28.33 per cent(including surcharge and cess) on the dividend reinvested.

This will be slightly lower than the income tax slab of 30.9per cent (including cess).

Consider your fresh investments through the aboveroutes. But if you make your switches now, do take intoaccount the exit load and the capital gains, (will vary foreach fund) if any, you may suffer on the fund now.

When you don’t need cash flows

Redemption date 10-20% tax 30% taxbracket bracket

- Is less than 3 years Opt for Opt forfrom date of purchase growth dividend

reinvest

- Is more than 3 years Opt for Opt forfrom date of purchase growth growth

Mutual Fund Research DeskFundsIndia.com

www.fundsindia.com

“Job creation, wage growth and availability of credit at cheaper rate are the reasons for consumerconfidence coming back. Business confidence comes out of stable and non- obstructive system.”Anand Radhakrishnan, CIO, Franklin Templeton Investments

Index 1 Year 5 Years 10 Years

Nifty 50 10.2 11.9 9.9

S&P BSE Sensex 8.2 11.3 9.3

Nifty Freefloat Midcap 100 17.6 16.0 13.6

Nifty Freefloat Smallcap 100 19.4 13.1 8.7

Nifty 100 10.8 12.8 10.6

Nifty 500 12.3 13.1 10.3

Nifty Bank 15.4 15.7 15.7

Nifty Energy 26.3 4.7 6.0

Nifty FMCG 12.4 17.6 15.4

Nifty Infrastructure -0.6 1.1 1.9

Nifty IT -9.1 14.1 9.0

Returns (in per cent as of August 31, 2016) for less than one yearis on an absolute basis, and for more than one year on acompounded annual basis.

Equity Performance Snapshot

Did you know?With FundsIndia's Money Mitr, you can get instant fundrecommendations for SIPs for various life goals, such asretirement, your child's wedding, building wealth, andtax-saving investments. You can also getrecommendations for lump sum investments in minutes!Login to your FundsIndia account and click on the MoneyMitr tab to give it a shot today!

www.fundsindia.com

Q: What strategy should I follow for investing in debt funds? Should it be in a lump sum or through SIPs?According to me, it should be lump sum if I want to take advantage of post 3-year period indexation benefits.SIPs would not be suitable if we are looking at it as a replacement for bank FDs. Please advise.

A: It depends on the purpose for investing. If you are investing specifically in debt and have a reasonable sum todeploy, it can be via a lump sum. However, if you are looking at investing for the long term and in that, you want anallocation of some amount to debt, use the SIP method. The method of investing is more to do with whether youare using debt for asset allocation (with equity) or simply investing in debt.

Q: There is a bit of confusion around fund categorization in debt funds. Birla SL Dynamic Bond Fund islisted under ‘Debt funds – long term’ in the FundsIndia Select Funds list, but it is categorized as ‘Debt –Short-term funds’ when you open its page. Similarly, in your blog post, UTI Dynamic Bond Fund wasmentioned as a ‘Dynamic Bond’ fund but it is categorized as ‘Debt – Income funds’ in its page. Why is thisdiscrepancy coming in?

A: That’s a very valid question! BSL Dynamic Bond has the CRISIL Short Term Bond index as its benchmark. Hence,it is classified into the short-term category by our data service provider (they go by the benchmark mentioned in theScheme Information Document). Secondly, there is no separate classification between dynamic bond funds and incomefunds for most data providers (since dynamic bond funds have the CRISIL Composite Bond as their index). Theclassification you see in the fund pages is from our data service providers. When we, at research, do our analysis, wemake our own classifications based on average maturity, credit risk, strategy, and so on. Therefore, I would suggest thatfor advisory purpose, you go with the ‘long-term’ research classification. To sum up, ignore the classification in theexplorer page and go with what is said in the Select Funds list.

Vidya BalaHead - Mutual Fund Research

FundsIndia.com

Q & A

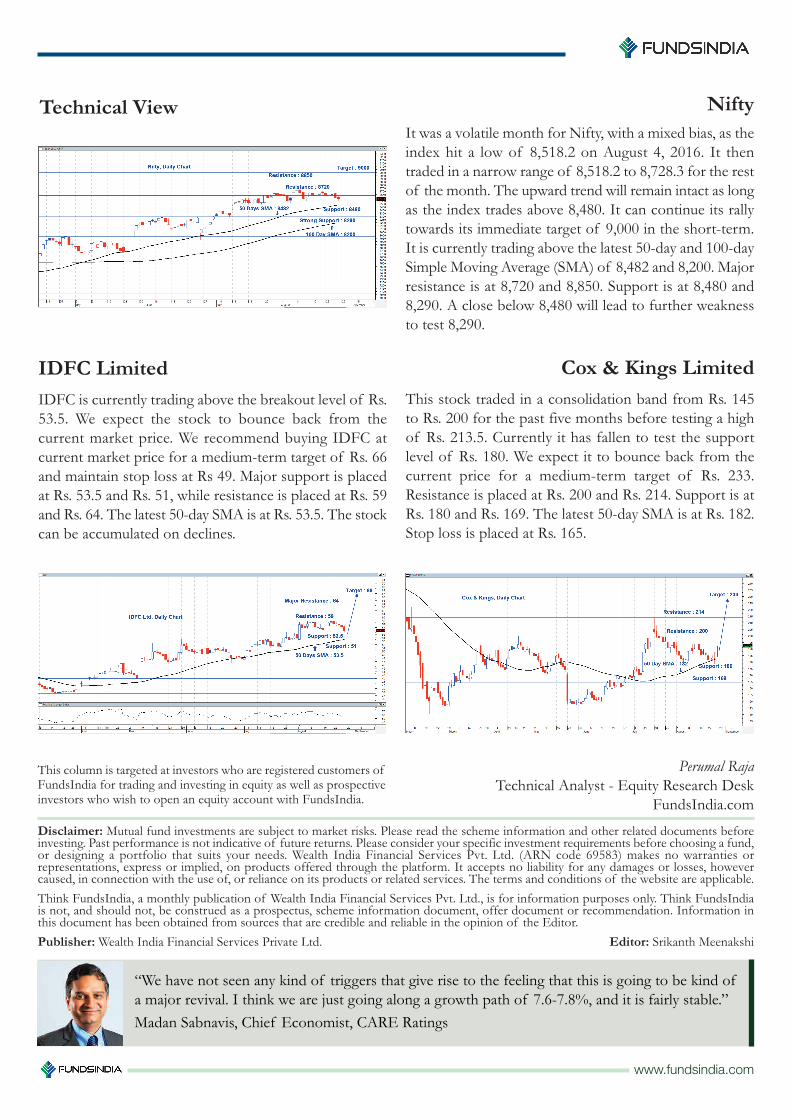

IDFC LimitedIDFC is currently trading above the breakout level of Rs.53.5. We expect the stock to bounce back from thecurrent market price. We recommend buying IDFC atcurrent market price for a medium-term target of Rs. 66and maintain stop loss at Rs 49. Major support is placedat Rs. 53.5 and Rs. 51, while resistance is placed at Rs. 59and Rs. 64. The latest 50-day SMA is at Rs. 53.5. The stockcan be accumulated on declines.

This column is targeted at investors who are registered customers ofFundsIndia for trading and investing in equity as well as prospectiveinvestors who wish to open an equity account with FundsIndia.

It was a volatile month for Nifty, with a mixed bias, as theindex hit a low of 8,518.2 on August 4, 2016. It thentraded in a narrow range of 8,518.2 to 8,728.3 for the restof the month. The upward trend will remain intact as longas the index trades above 8,480. It can continue its rallytowards its immediate target of 9,000 in the short-term.It is currently trading above the latest 50-day and 100-daySimple Moving Average (SMA) of 8,482 and 8,200. Majorresistance is at 8,720 and 8,850. Support is at 8,480 and8,290. A close below 8,480 will lead to further weaknessto test 8,290.

Perumal RajaTechnical Analyst - Equity Research Desk

FundsIndia.com

Cox & Kings LimitedThis stock traded in a consolidation band from Rs. 145to Rs. 200 for the past five months before testing a highof Rs. 213.5. Currently it has fallen to test the supportlevel of Rs. 180. We expect it to bounce back from thecurrent price for a medium-term target of Rs. 233.Resistance is placed at Rs. 200 and Rs. 214. Support is atRs. 180 and Rs. 169. The latest 50-day SMA is at Rs. 182.Stop loss is placed at Rs. 165.

Technical View Nifty

Disclaimer: Mutual fund investments are subject to market risks. Please read the scheme information and other related documents beforeinvesting. Past performance is not indicative of future returns. Please consider your specific investment requirements before choosing a fund,or designing a portfolio that suits your needs. Wealth India Financial Services Pvt. Ltd. (ARN code 69583) makes no warranties orrepresentations, express or implied, on products offered through the platform. It accepts no liability for any damages or losses, howevercaused, in connection with the use of, or reliance on its products or related services. The terms and conditions of the website are applicable.Think FundsIndia, a monthly publication of Wealth India Financial Services Pvt. Ltd., is for information purposes only. Think FundsIndiais not, and should not, be construed as a prospectus, scheme information document, offer document or recommendation. Information inthis document has been obtained from sources that are credible and reliable in the opinion of the Editor.Publisher:Wealth India Financial Services Private Ltd. Editor: Srikanth Meenakshi

“We have not seen any kind of triggers that give rise to the feeling that this is going to be kind ofa major revival. I think we are just going along a growth path of 7.6-7.8%, and it is fairly stable.”Madan Sabnavis, Chief Economist, CARE Ratings

www.fundsindia.com

1. Who has been appointed as the new independentdirector on the board of India Post Payment Banks(IPPB)?

2. Which bank launched the mobile app ‘iMobileSmartKeys’?

3. Who has been appointed as the new Governor ofthe Reserve Bank of India (RBI)?

4. Which state has become the first Indian state to ratifyGST Constitution Amendment Bill?

5. What is the current repo rate as per the RBI’s recentlyreleased third bi-monthly monetary policy review forFY 2016-17?

Please click here to submit your answers. You'll bedirected to a Google Form where you can enter theanswers to this month's quiz.

Answers for August 2016 Investment Quiz:

1. State Bank of India (SBI) 2. 15 per cent 3 Rs. 1,601crore 4. Michel Barnier 5. ICICI Bank and Axis Bank

The winner of the August 2016 Investment Quiz isVineeth Vannadil Puthiyaveettil.

www.fundsindia.com

FundsIndia Select Funds Investment QuizDebt Funds – Long Term

These funds invest in a mix of gilt, long-term corporatebonds as well as short-term papers with varying time frames.The recommended holding period is over two years.

Birla SL Dynamic Bond Fund (G)

BNP Paribas Medium Term Income Fund(G)

HDFC Medium Term Opportunities Fund(G)

UTI Dynamic Bond Fund (G)

Please click here for a complete listing of our preferredfunds.

@FundsIndiaWe’re happy to announce that we have now launched themuch awaited equity investing feature on the FundsIndia appfor Android. Just update your app to take advantage of thisnew feature.

We’ve also redesigned the FundsIndia iOS app to improvethe user experience. Do let us know what you think of thesechanges at [email protected].