Translated from the Lithuanian language HOLOCAUST IN LITHUANIAN

Upload

swedbank-ab-publCategory

view

218download

0

8/7/2019 The Lithuanian Economy, No.2, 9 March 2011

http://slidepdf.com/reader/full/the-lithuanian-economy-no2-9-march-2011 1/4

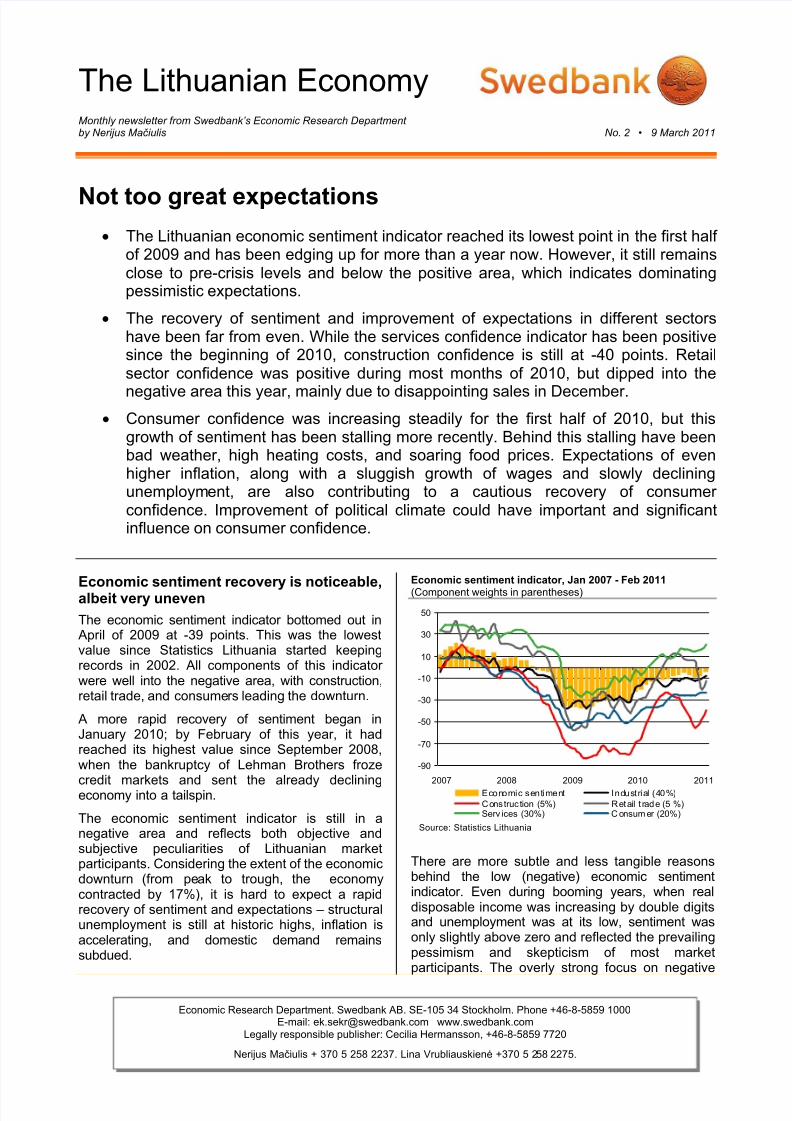

The Lithuanian EconomyMonthly newsletter from Swedbank’s Economic Research Department by Nerijus Mačiulis No. 2 • 9 March 2011

Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000E-mail: [email protected] www.swedbank.com

Legally responsible publisher: Cecilia Hermansson, +46-8-5859 7720

Nerijus Mačiulis + 370 5 258 2237. Lina Vrubliauskienė +370 5 258 2275.

Not too great expectations The Lithuanian economic sentiment indicator reached its lowest point in the first half

of 2009 and has been edging up for more than a year now. However, it still remainsclose to pre-crisis levels and below the positive area, which indicates dominatingpessimistic expectations.

The recovery of sentiment and improvement of expectations in different sectorshave been far from even. While the services confidence indicator has been positivesince the beginning of 2010, construction confidence is still at -40 points. Retailsector confidence was positive during most months of 2010, but dipped into the

negative area this year, mainly due to disappointing sales in December. Consumer confidence was increasing steadily for the first half of 2010, but this

growth of sentiment has been stalling more recently. Behind this stalling have beenbad weather, high heating costs, and soaring food prices. Expectations of evenhigher inflation, along with a sluggish growth of wages and slowly decliningunemployment, are also contributing to a cautious recovery of consumer confidence. Improvement of political climate could have important and significantinfluence on consumer confidence.

Economic sentiment recovery is noticeable,albeit very uneven

The economic sentiment indicator bottomed out inApril of 2009 at -39 points. This was the lowestvalue since Statistics Lithuania started keepingrecords in 2002. All components of this indicator were well into the negative area, with construction,retail trade, and consumers leading the downturn.

A more rapid recovery of sentiment began inJanuary 2010; by February of this year, it hadreached its highest value since September 2008,when the bankruptcy of Lehman Brothers froze

credit markets and sent the already decliningeconomy into a tailspin.

The economic sentiment indicator is still in anegative area and reflects both objective andsubjective peculiarities of Lithuanian marketparticipants. Considering the extent of the economicdownturn (from peak to trough, the economycontracted by 17%), it is hard to expect a rapidrecovery of sentiment and expectations – structuralunemployment is still at historic highs, inflation isaccelerating, and domestic demand remainssubdued.

Economic sentiment indicator, Jan 2007 - Feb 2011

(Component weights in parentheses)

-90

-70

-50

-30

-10

10

30

50

2007 2008 2009 2010 2011

Economic sentiment Industrial (40%)

Cons truc tion (5%) Retail t rade (5 %)Serv ices (30%) C onsum er (20%)

Source: Statistics Lithuania

There are more subtle and less tangible reasonsbehind the low (negative) economic sentimentindicator. Even during booming years, when realdisposable income was increasing by double digitsand unemployment was at its low, sentiment wasonly slightly above zero and reflected the prevailingpessimism and skepticism of most marketparticipants. The overly strong focus on negative

8/7/2019 The Lithuanian Economy, No.2, 9 March 2011

http://slidepdf.com/reader/full/the-lithuanian-economy-no2-9-march-2011 2/4

The Lithuanian Economy

Economic Research Department, Swedbank Nr 2 • 9 March 2011

2 (4)

news in the media and the ongoing upheavals inthe political arena are partly responsible for thislow-confidence phenomenon.

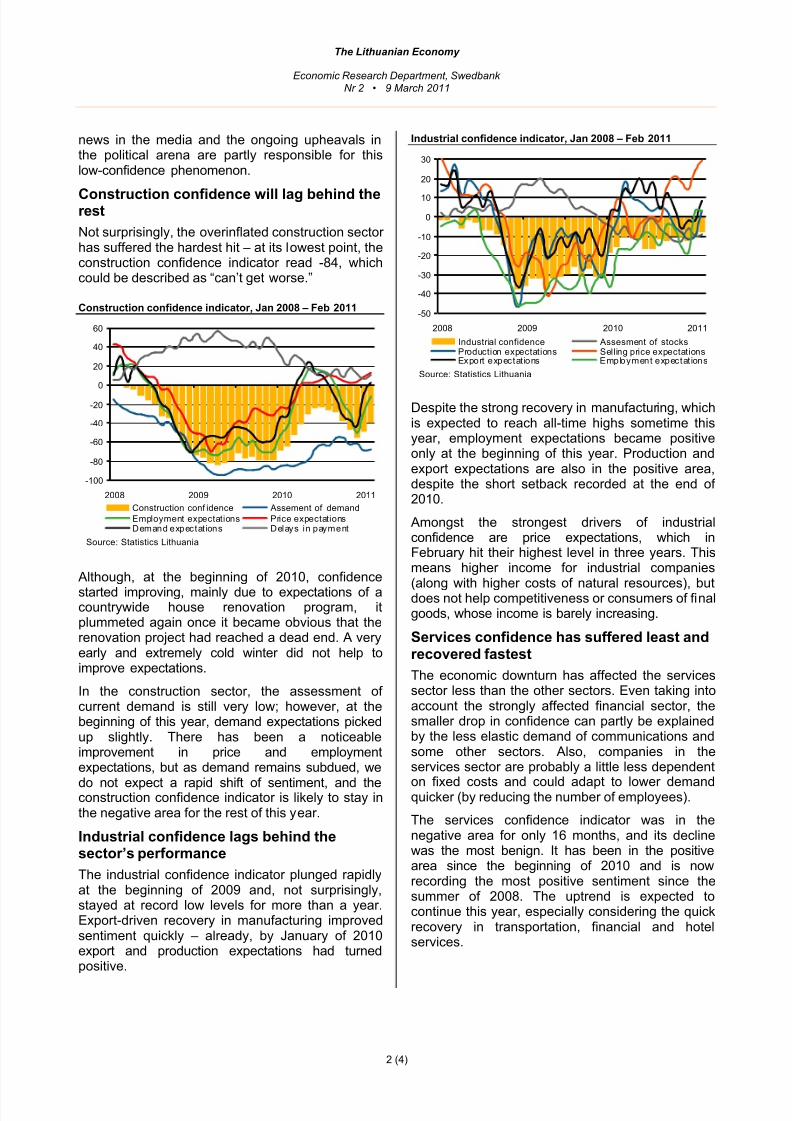

Construction confidence will lag behind therest

Not surprisingly, the overinflated construction sector has suffered the hardest hit – at its lowest point, theconstruction confidence indicator read -84, whichcould be described as “can’t get worse.”

Construction confidence indicator, Jan 2008 – Feb 2011

-100

-80

-60

-40

-20

0

20

40

60

2008 2009 2010 2011

Construction conf idence Assement of demand

Employment expectations Price expectationsDemand expectat ions Delays in payment

Source: Statistics Lithuania

Although, at the beginning of 2010, confidence

started improving, mainly due to expectations of acountrywide house renovation program, itplummeted again once it became obvious that therenovation project had reached a dead end. A veryearly and extremely cold winter did not help toimprove expectations.

In the construction sector, the assessment of current demand is still very low; however, at thebeginning of this year, demand expectations pickedup slightly. There has been a noticeableimprovement in price and employmentexpectations, but as demand remains subdued, we

do not expect a rapid shift of sentiment, and theconstruction confidence indicator is likely to stay inthe negative area for the rest of this year.

Industrial confidence lags behind thesector’s performance

The industrial confidence indicator plunged rapidlyat the beginning of 2009 and, not surprisingly,stayed at record low levels for more than a year.Export-driven recovery in manufacturing improvedsentiment quickly – already, by January of 2010export and production expectations had turnedpositive.

Industrial confidence indicator, Jan 2008 – Feb 2011

-50

-40

-30

-20

-10

0

10

20

30

2008 2009 2010 2011

Industrial confidence Assesment of stocksProduction expectations Selling price expectationsExport expectat ions Employment expectat ions

Source: Statistics Lithuania

Despite the strong recovery in manufacturing, whichis expected to reach all-time highs sometime thisyear, employment expectations became positiveonly at the beginning of this year. Production andexport expectations are also in the positive area,despite the short setback recorded at the end of 2010.

Amongst the strongest drivers of industrialconfidence are price expectations, which inFebruary hit their highest level in three years. Thismeans higher income for industrial companies

(along with higher costs of natural resources), butdoes not help competitiveness or consumers of finalgoods, whose income is barely increasing.

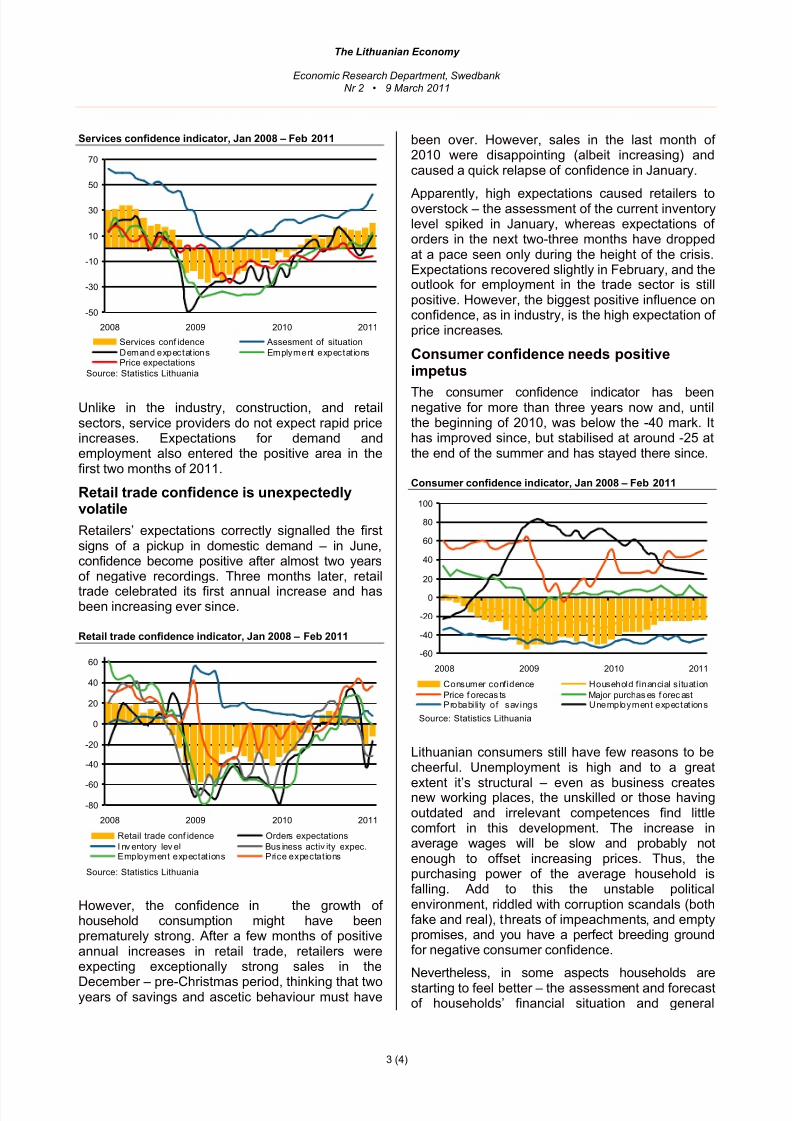

Services confidence has suffered least andrecovered fastest

The economic downturn has affected the servicessector less than the other sectors. Even taking intoaccount the strongly affected financial sector, thesmaller drop in confidence can partly be explainedby the less elastic demand of communications andsome other sectors. Also, companies in theservices sector are probably a little less dependent

on fixed costs and could adapt to lower demandquicker (by reducing the number of employees).

The services confidence indicator was in thenegative area for only 16 months, and its declinewas the most benign. It has been in the positivearea since the beginning of 2010 and is nowrecording the most positive sentiment since thesummer of 2008. The uptrend is expected tocontinue this year, especially considering the quickrecovery in transportation, financial and hotelservices.

8/7/2019 The Lithuanian Economy, No.2, 9 March 2011

http://slidepdf.com/reader/full/the-lithuanian-economy-no2-9-march-2011 3/4

The Lithuanian Economy

Economic Research Department, Swedbank Nr 2 • 9 March 2011

3 (4)

Services confidence indicator, Jan 2008 – Feb 2011

-50

-30

-10

10

30

50

70

2008 2009 2010 2011

Services conf idence Assesment of situation

Demand expectat ions Emplyment expectat ionsPrice expectations

Source: Statistics Lithuania

Unlike in the industry, construction, and retailsectors, service providers do not expect rapid priceincreases. Expectations for demand andemployment also entered the positive area in thefirst two months of 2011.

Retail trade confidence is unexpectedlyvolatile

Retailers’ expectations correctly signalled the firstsigns of a pickup in domestic demand – in June,confidence become positive after almost two yearsof negative recordings. Three months later, retail

trade celebrated its first annual increase and hasbeen increasing ever since.

Retail trade confidence indicator, Jan 2008 – Feb 2011

-80

-60

-40

-20

0

20

40

60

2008 2009 2010 2011

Retail trade conf idence Orders expectations

I nv entory lev el Bus iness activ ity expec.Employment expectations Price expectations

Source: Statistics Lithuania

However, the confidence in the growth of household consumption might have beenprematurely strong. After a few months of positiveannual increases in retail trade, retailers wereexpecting exceptionally strong sales in the

December – pre-Christmas period, thinking that twoyears of savings and ascetic behaviour must have

been over. However, sales in the last month of 2010 were disappointing (albeit increasing) andcaused a quick relapse of confidence in January.

Apparently, high expectations caused retailers tooverstock – the assessment of the current inventorylevel spiked in January, whereas expectations of orders in the next two-three months have droppedat a pace seen only during the height of the crisis.Expectations recovered slightly in February, and theoutlook for employment in the trade sector is stillpositive. However, the biggest positive influence onconfidence, as in industry, is the high expectation of price increases.

Consumer confidence needs positiveimpetus

The consumer confidence indicator has beennegative for more than three years now and, untilthe beginning of 2010, was below the -40 mark. Ithas improved since, but stabilised at around -25 atthe end of the summer and has stayed there since.

Consumer confidence indicator, Jan 2008 – Feb 2011

-60

-40

-20

0

20

40

60

80

100

2008 2009 2010 2011

Consumer confidence Household financial situation

Price f orecas ts Major purchas es f orec astProbabi li ty of savings Unemployment expectat ions

Source: Statistics Lithuania

Lithuanian consumers still have few reasons to becheerful. Unemployment is high and to a great

extent it’s structural – even as business createsnew working places, the unskilled or those havingoutdated and irrelevant competences find littlecomfort in this development. The increase inaverage wages will be slow and probably notenough to offset increasing prices. Thus, thepurchasing power of the average household isfalling. Add to this the unstable politicalenvironment, riddled with corruption scandals (bothfake and real), threats of impeachments, and emptypromises, and you have a perfect breeding groundfor negative consumer confidence.

Nevertheless, in some aspects households arestarting to feel better – the assessment and forecastof households’ financial situation and general

8/7/2019 The Lithuanian Economy, No.2, 9 March 2011

http://slidepdf.com/reader/full/the-lithuanian-economy-no2-9-march-2011 4/4

The Lithuanian Economy

Economic Research Department, Swedbank Nr 2 • 9 March 2011

4 (4)

economic conditions are improving, andunemployment expectations are dropping rapidly.Consumer confidence is likely to be increasing thisyear, but it would take a strong impetus to push it

into the positive area. Amongst the strongestanchors of current expectations are rising consumer prices (and future increases are well reflected ininflation expectations). This affects mostlyhouseholds of lower-than-average income, wherealmost half of the consumer basket consists of expenses on food and transport – two groups of products most affected by upheavals North Africaand the Middle East.

The government has few tangible instruments toboost consumer confidence – public finances arestill strained, and there is no room to cut taxes or increase social benefits. However, a more positive

rhetoric and fewer pointless clashes between thegovernment and the opposition wouldn’t hurt.

At the end of the day, the linkage between theeconomy and political climate is stronger than whatis often realized. Building household confidence byfocusing on growth oriented policies could make adifference between a slow and a fast recovery inLithuania.

Nerijus Maciulis

SwedbankEconomic Research Department

SE-105 34 StockholmPhone +46-8-5859 [email protected]

Legally responsible publisher Cecilia Hermansson, +46-8-5859 7720.

Nerijus Mačiulis, +370 5 2582237.Lina Vrubliauskienė, +370 5 268 4275.

Swedbank’s monthly newsletter The Lithuanian Economy is published as a service to our customers. We believe that we have used reliable sources and methods in the preparationof the analyses reported in this publication. However, we cannot guarantee the accuracy or completeness of the report and cannot be held responsible for any error or omission in theunderlying material or its use. Readers are encouraged to base any (investment) decisionson other material as well. Neither Swedbank nor its employees may be held responsible for losses or damages, direct or indirect, owing to any errors or omissions in Swedbank’smonthly newsletter The Lithuanian Economy.