the audit furcticn and uily rn. the - U.S. Government ... serves collaterally as the Director of the...

31

DCCUPI.ENT RESUME j5 - r E5 1944/1 1 k he Naval Audit Service Should Be Strenglthened. FGMsD-78-5; L-1l3411 9 s Novembe-r 11, 1977. 19 F. + 3 appendices 3 pp.). .zpoLt to the Conq-ess; by Robert F. Feller, Acting Comptroller J ne ra . issue- Area; Internal Aditing Systems- Sufficiency ct Federal Auditors and Coveraqe (201). Contact: Fllancial and General Management Studies iv. Dudqict Function: National Defense: Dartment c Deferse - iilitary (except procurement 6 contracts) (051).. qanization oncerned: Department o eense; Department c1 the i.avy A5sistant Secretaiy ct the Navy (Financial Fanaqement) ; Departmeat of the Navy: Naval Audit Service. Cn.qressionai elevance: Ccngress. Authtority: aiconai Security Act cf 1947, as amended. Acco:'nting dnld Auditinq Act of 1950, sec. 113. P.L. 93-365. 10 U.S.C. 125. Feaeral anaqement Circular 7-2. -1329CC (1970). DOD DJrectiv- 1100.4. by iaw, the head ci each Government agency must set up rd nair.tain systems of accounting and internal ccrtcl: of wl.ich internaJ audit is an integral Fart. In the Navy, internal Ud UtA.i is dolne y the aval Audit ervice under the direction of Mre Assistant SecretaLy of the Navy for Fin~.cial anagement, we dals serves as Comptroller. Findlngs/Conclusicns: The Navy .iuld ;iiuk: its internal audit stronger to kes:r top management betaur intornmd on how operations are conducted and rcomm ndat aons for imprcvement are carried out. The internal dudit trunrtlon is not placed niqh encugh i the Navy's LQaization to qrant auditors maximum independence in iconict i and reportin- on audit work. The current La:;Iz a ioal structure is inconsistent with the ccnptrcler -r.ral's audit standards which advocate that the audit tunction bt: fdCtU ut tte nighest practical level. he Lepartrent cf Dernse polcy rquires all nonmilitary oEiticns to be tilled Lt civcolians. contrary to this policy, te Audit Service is nt*,ad j ia m mllrary officer and it employs 34 other ilitary urLiceLs. 7h- aval Audit Sevice has been unatle to meet its audii q,cis rnd has a large audit backlog, due in Fart to the ;.ssve orkisoad and the use or audit resourct- on wcrk nct in k-eC i4 wii its primary missicn. The Navy's audit followup ystm does not provide assurance that all deticiencies id ntiied by audits arc promptly corrected. Cpportunities for cbVinqS ar- lost and inefficient and inetfective cierations c;nlinue. htcommtnations: The Secretary ot Lctense should use Nii re3zqadniZatlcn authority tc relocate the Nava'.l Audit Service ui;.er t=t stcre:tary or Uider secretary ot the avy and direct ~tn auit Stdt to r"por diLectly to that orticial. Tne Secretary or Derense should diiect the Secretary of the Navy to jill all ~ositlon, including the Dlrector, with prcfessicnally

Transcript of the audit furcticn and uily rn. the - U.S. Government ... serves collaterally as the Director of the...

DCCUPI.ENT RESUME

j5 - r E5 1944/1 1

k he Naval Audit Service Should Be Strenglthened. FGMsD-78-5;

L-1l34119s Novembe-r 11, 1977. 19 F. + 3 appendices 3 pp.).

.zpoLt to the Conq-ess; by Robert F. Feller, Acting Comptroller

J ne ra .

issue- Area; Internal Aditing Systems- Sufficiency ct Federal

Auditors and Coveraqe (201).

Contact: Fllancial and General Management Studies iv.

Dudqict Function: National Defense: Dartment c Deferse -

iilitary (except procurement 6 contracts) (051)..qanization oncerned: Department o eense; Department c1 the

i.avy A5sistant Secretaiy ct the Navy (Financial

Fanaqement) ; Departmeat of the Navy: Naval Audit Service.

Cn.qressionai elevance: Ccngress.

Authtority: aiconai Security Act cf 1947, as amended. Acco:'ntingdnld Auditinq Act of 1950, sec. 113. P.L. 93-365. 10 U.S.C.125. Feaeral anaqement Circular 7-2. -1329CC (1970). DOD

DJrectiv- 1100.4.

by iaw, the head ci each Government agency must set uprd nair.tain systems of accounting and internal ccrtcl: of

wl.ich internaJ audit is an integral Fart. In the Navy, internal

Ud UtA.i is dolne y the aval Audit ervice under the directionof Mre Assistant SecretaLy of the Navy for Fin~.cial anagement,

we dals serves as Comptroller. Findlngs/Conclusicns: The Navy.iuld ;iiuk: its internal audit stronger to kes:r top management

betaur intornmd on how operations are conducted andrcomm ndat aons for imprcvement are carried out. The internaldudit trunrtlon is not placed niqh encugh i the Navy's

LQaization to qrant auditors maximum independence in

iconict i and reportin- on audit work. The current

La:;Iz a ioal structure is inconsistent with the ccnptrcler

-r.ral's audit standards which advocate that the audit tunctionbt: fdCtU ut tte nighest practical level. he Lepartrent cf

Dernse polcy rquires all nonmilitary oEiticns to be tilled

Lt civcolians. contrary to this policy, te Audit Service is

nt*,ad j ia m mllrary officer and it employs 34 other ilitary

urLiceLs. 7h- aval Audit Sevice has been unatle to meet its

audii q,cis rnd has a large audit backlog, due in Fart to the

;.ssve orkisoad and the use or audit resourct- on wcrk nct ink-eC i4 wii its primary missicn. The Navy's audit followupystm does not provide assurance that all deticienciesid ntiied by audits arc promptly corrected. Cpportunities for

cbVinqS ar- lost and inefficient and inetfective cierations

c;nlinue. htcommtnations: The Secretary ot Lctense should use

Nii re3zqadniZatlcn authority tc relocate the Nava'.l Audit Service

ui;.er t=t stcre:tary or Uider secretary ot the avy and direct~tn auit Stdt to r"por diLectly to that orticial. Tne

Secretary or Derense should diiect the Secretary of the Navy to

jill all ~ositlon, including the Dlrector, with prcfessicnally

qualified civilians and improve te Audit Service's ability tocover its workload. Alternatives to te considered are tc: reducesiqnificantly the use c audit staff cn special requested andnonaFproprlated fund work and bring the audit wcrklcad and statecapability into balance; and strengthen the audit furcticn andrequire the Naval Audit Service to participate mote uily rn. theprocess. (Author/SW)

REPORT TO THE CONGRESS

o n BY THE COMPTROLLER GENERALII OF THE UNITED STATES

The Naval Audit ServiceShould Be Strengthened

The Navy could obtain greater managementbenefits from internal auditing by

--placing the audit function at a higherorganizational level,

--filling all military positions with quali-fied civilians,

--bringing the audit workload and staffcapability into balance,

- reducing the use of auditors on workthat is not fully productive, and

--strengthening the audit followup sys-tem.

FGMSD-78-5 NOVEMBER 11, 1977

COMP'ROLLER GENERAL OF THE UNITED STATES

WASHINOTON. rC. I54

B-134192

To the President of the Senate and theSpeaker of the House of Representatives

This report, the fourth of a series on D)epartment ofDefense internal audit activities, describes how the Depart-ment of the Navy can improve its nternal auditing.

This survey is part of our current effort to expand andstrengthen internal audit activities of Government depart-ments and agencies. We made our review pursuant to the Budgetand Accounting Act, 1921 (31 U.S.C. 53), and the Accountingand Auditing Act of 1950 (31 U.S.C. 67). The act of 1950requires us to consider the effectiveness of any agency'sinternal controls, including internal audit, in determiningthe extent and scope of our examinations.

The report is being issued without agency comments.The Department of Defense did not comment within the 30 dayswe gave them or within the 60 day extension we allowed.

We are sending copies of this Leport to the ActingDirector, Office of Management and Budget, and to theSecretaries of Defense and the Navy.

ACTING Comptri neralof the United States

COMPTR')LLER GENERAL'S THE NAVAL AUDITREPORT TO THE CONGRESS SERVICE SHOULD BE

STRENGTHENED

DIGEST

By law, the head of each Government agencymust set up and maintain systems of account-ing and internal control, of which internalaudit is an ntegral part. In the Navy,internal auditin, is done by the Naval AuditService under the direction of the AssistantSecretary of the Navy for Financial Manage-ment, who also serves as Comptroller.

FINDINGS AND CONCLUSIONS

The Navy should make its internal auditstronger to keep top management betterinformed on how operations are conducted andrecommendations foc improvement are carriedout.

The internal audit function is not placedhigh enough in the Navy's organization togrant auditors maximum independence in con-ducting and reporting on audit work. Thecurrent organizational structure is incon-sistent with the Comptroller General's auditstandards which advocate that the auditfunction be placed at the highest practicallevel. (See pp. 3 to 6.)

Department of Defense policy requires allnonmilitary positions to be filled by civil-ians. Contrary to this policy, the AuditService is headed by a military officer andemploys 34 other milita- officers. (Seepp. 7 to 10.)

The Naval Audit Service r n unable tomeet its audit goals and - large auditbacklog. This is due in rt to the massiveworkload and the use of audit resources onwork that is not in keeping with its primarymission. (See pp. 11 to 16.)

FGMSD-78-5-tr W umon. 0to fiwtW d hould be not hoon.

i

The Navy's audit followu9 system does notprovide assurance that all deficienciesidentified by audits are promptly corrected.Opportunities for savings are lost and inef-ficierit and ineffective operations continue.(See pp. 17 to 19.)

RECOMMENDATIONS TO THESECRETARY OF DEFENSE

The Secretary of Defense should ust hisreorganization authority under 10 U.S.C. 125to relocate the Naval Audit Service underthe Secretary or Under Secretary of the Navyand direct the audit staff to report directlyto that official. (See p. 5.)

Also, the Secretary of Defense should directthe Secretary of the Navy to:

-- Fill all positions, including the Director,with professionally qualified civilians.(See p. 10.)

-- Improve te Audit Service's ability tocover its workload. Alternatives to beconsidered are to reduce significantly theuse of audit staff on special requestedand nonappropriated fund work and bringthe audit workload and staff capabilityinto balance. (See p. 16.)

-- Strengthen the audit followup function andrequire the Naval Audit Service to partici-pate more fully in the process. (Seep. 19.)

RECOMMENDATION TO THE CONGRESS

In order to assure that the greater auditindependence recommended is maintained in thefuture, we also recommend that the Congressamend the National Security Act of 1947, asamended, to place the internal audit functionsof the three military departments under theSecretary or Under Secretary of the respectivedepartments and have the internal auditorsreport directly to those officials. This rec-ommendation was made in a previous report(FGMSD-77-49, July 26, 1977).

ii

Because te Subcommittee on Legislation andNationa. Security, House Committee on Govern-ment Operations, requested a November 3, 1977,release date, this report is being issuedwithout agency comments. The Department ofDefense did not comment within the 30 daysGAO gave them or within the 0 day exten-sion GAO allowed.

aLir Sbli

iii

Contents

Page

DIGEST i

CHAPTER

INTRODUCTION 1Internal auditing in the Department

of the Navy 1Previous reviews and evaluations

of the Naval Audit Service 2Scope of review 2

2 THE INTERNAL AUDIT FUNCTION SHOULD BELOCATED AT A IGHER ORGANIZATIONALLEVEL 3GAO position on placement of audit 3Location of audit in the Navy 4Limitations on reporting 4Conclusions 5Recommendations to the Secretary

of Defense 5Recommendation to the Congress 6

3 MORE NAVAL AUDIT SEPVICE POSITIONSSHOULD BE CONVR¶D TO CIVILIAN 7Opportunity to realize savings 8Conclusions 9Recommendations 10

4 AUDIT STAFF COULD BE USED MOREEFFECTIVELY 11

Imbilance between workload andstaff 11

Current audit backlog 12Opportunity to improve audit

capability 13Conclusions 15Recommendations 16

5 NEED FOR MIORE EFFECTIVE FOLLOWUP OFAUDIT FINDINGS 17

Guidance on followup of findings 17Naval Audit Service followup is

spotty 17Conclusions 19Recommendations 19

APPENDIX

I Responsibilities of the Auditor Generalof the Navy/Director, Naval AuditService 20

II Organization chart of the Office of theAuditor General of the Navy 21

III Principal officials responsible foradministering activities discussed inthis report 22

ABBREVIATIONS

ADP automatic data processing

CPA certified public accountant

DOD Department of Defense

GAO Genetal Accounting Office

GSA General Services Administration

CHAPTER 1

INTRODUCTION

Section 113 of the Accounting and Auditing Act of 1950

made top management within each Federal agency responsible

for its internal auditing by providing that:

"The head of each executive agency shall establish and

maintain systems of accounting and internal control

designed to provide * * * effective control over and

accountability for all funds, property, and other assets

for which the agency is respunsible, including appro-

priate internal audit * * *."

In 1972 we issued a booklet entitled "Standards for

Audit of Governmental Organizations, Programs, Activities &

Functions." These standards recognized the growing informa-

tion needs of public officials, legislators, and the general

public, and established a framework for full-scope examina-

tions of Government programs by independent and objective

auditors. In August 1974 we incorporated the standards in acevised policy statement entitled 'Internal Auditing in Fed-eral Agencies." In 1973 the General Services Administration(GSA) issued Federal Management ircular 73-2, setting forthpolicies to be followed by agencies in audits of Federaloperations and programs.

The Department of Defense (DOD) and its component mili-tary departments and agencies have joined with the Congress,our office, and GSA in recognizing the importance of and theneed for (1) internal audit, (2) performance standards for awide range of audit services, and (3) policies for implemen-tation and guidance of internal audit organizations.

INTERNAL AUDITING IN THEDEPARTMENT OF THE NAVY

The Naval Audit Service is the internal audit organiza-tion of the Department of the Navy. It is headed by theAuditor General of the Navy, who is a member of the militaryand serves collaterally as the Director of the Naval AuditService. In fiscal year 1976 the Audit Service reported over$177 million of potential savings. Of this amount $64.4 mil-lion was recovered by major claimants and reapplied in otherprograms. Compared with total annual costs of audit opera-tions of about $13 million, these recovered savings representa return on investment of 4.9 to 1.

1

The Naval Audit Service Headquarters is located in FallsChurch, Virginia. The operating elements of the organizationare located in four regional offices: northeast region,Camden, New Jersey; capital region, located with Headquartersin Falls Church, Virginia; southeast region, Virginia Beach,Virginia; and the western region, San Diego, California.

PREVIOUS REVIEWS AND EVALUATIONSOF THE NAVAL AUDIT SERVICE

The Naval Audit Service's operations were discussed inour reports issued in AIarch 1968 and in January 1970(B-132900). These reor,:ts contained recommendations forimproving internal audit operations in DOD, including co-ordination and overall control of the total audit effort.Also, a Blue Ribbon Defense Panel convened by the Presidentin 1970 as part of a comprehensive study of DOD managementprocedures made several recommendations for improving theNaval udit Service's organizational structure and its in-ternal audit operations.

SCOPE OF REVIEW

Our survey of the internal audit activities of the NavalAudit Service was conducted during the period August 1976 toMarch 1977. Site visits were made to the southeast and west-ern regions and meetings were held with appropriate officialsat the capital region and Naval Audit Service Headquarters.We wanted to know whether the internal audit functions of theNaval Audit Service were being performed in accordance withour audit standards and were being effectively and efficientlycarried out.

The Audit Service enjoys a high level of competence andprofessionalism among its staff. Generally, internal auditpolicies, plans, and operations comply with the requirementsof an effective internal audit system. However, we believethat the independence and effectiveness of the Naval AuditService can be enhanced as discussed in succeeding chapte-

2

CHAPTER 2

THE INTERNAL AUDIT FUNCTION SHOULD BE LOCATED

AT A HIGHER ORGANIZATIONAL LEVEL

The Naval Audit Service is not placed high enough in the

Navy's organization to insure that its auditors have maximumindependence in reporting on the results of audit work.

Government agencies, if they are to receive the fullbenefits of internal auditing, must locate their audit func-

tions at a sufficiently high organizational level to insurethat auditors are insulated against internal agency pressuresso they can conduct their auditing objectively and reporttheir conclusions completely without fear of censure or repri-

sal. In our opinion, the present organizational placement ofthe Naval Audit Service does not provide this assurance.

GAO POSITION ON PLACEMENT OF AUDIT

We have consistently advocated that

-- the positions of internal auditors in an organizationshould be such that they are independent of the offi-cials who are responsible for the operations the audi-tors review and

-- to provide an adequate degree of independence, inter-nal auditors should be responsible to the highestpractical organizational level, preferably to the

agency head or to a principal official reportingdirectly to the agency head.

These principles are emphasized in our standards for govern-mental auditing and in our statement on internal auditing inFederal agencies.

We have also pointed out that, for internal auditing tobe of maximum usefulness, the internal auditor should be freeto determine the scope and character of the audit and thecontent of the audit report. Navy auditors have not beenfree to do this, in our opinion, because they are not totallyindependent of officials who are responsible for some of theoperations they review.

3

LOCATION OF AUDIT IN THE NAVY

Organizationally the Naval Audit Service is under theAssistant Secretary of the Navy (Financial Management), whoalso serves as Comptroller of the Navy and senior automaticdata processing (ADP) policy official for the Navy. TheAssistant Secretary, as Comptroller, is responsible for budg-eting, accounting, progress anI statistical reporting, pro-viding financial assistance to defense contractors, internalauditing, and for the management information system andrelated management functions within the Department of theNavy. As the senior ADP policy official for the Navy, he isrequired to

--implement the ADP program within the Department ofthe Navy,

-- approve the acquisition of ADP equipment by contrac-tors,

-- establish criteria for the validation of data process-ing requirements, and

-- issue procedures for the review and approval of theNavy's ADP resources.

LIMITATIONS ON REPORTING

As a result of the organiza ional placement of the NavalAudit Service, the Assistant Secretary f the Navy (FinancialManagement) has been able to place limitations on reportingof the Audit Service. Placement of the Auditor General ascoequal to some management positions within the Office of theComptroller of the Navy has caused dissention when in-housedisagreements arise over audit findings. Using his authority,the Assistant Secretary has promulgated a "working agreement"for his staff as a solution.

In April 1975 the Assistant Secretary established spe-cial procedures for resolving in-house disagreements on auditreports. He reported that, in the past, audit reports hadsometimes included recommended changes to the Navy Comptrol-ler's policies and procedures which were not fully concurredin by management. The Assistant Secretary reasoned that thispractice of publishing audit reports showing unresolved dis-agreements within the Comptr-ller organization would no doubtconfuse field activities as to the correct guidance to fol-low--the Audit Service or the Comptroller. Under the specialprocedures, any management responses from the Office of Bud-gets and Reports; Assistant Comptroller, Financial Management

4

Systems; and General Counsel sections of the Comptroller'sorganization which expressed disagreement with audit findingsor recommendations are to be referred to the Deputy Comptrol-ler for resolution before publication. This can and doesgive the Deputy the power to limit disclosure of controver-sial findings.

One such case occurred during a fiscal year 1976 reviewof the Navy Finance Information System. The Assistant Comp-troller of the Navy for Financial Management Systems did notconcur with a finding which reported that he had exceeded hisapproval authority for contracting for automatic data process-ing services. In a memorandum to the Deputy Comptroller, theAuditor General stated that a full disclosure of this find-ing was in consonance with their other activities in the ADPworld and should be reported to insure the proper handlingof these matters by other auditable activities. After dis-cussing the matter with the Deputy Comptroller, the AuditorGeneral directed that the controversial fincing be removedfrom the final report.

CONCLUSIONS

Under the current organizational arrangement, the AuditService is too far removed from the highest organizationallevel of the Navy to insure maximum audit independence andeffectiveness and appropriate management attention to auditfindings.

The Assistant Secretary of the Navy (Financial Manage-ment) is responsible for all bdgeting, accounting, progressand statistical reporting, management information systems,and ADP programs within the Department of the Navy. Theinclusion of the internal audit function 'with these otherresponsibilities has resulted in unnecessary limitations onreporting of the Naval Audit Service. Further, it can con-tribute to the appearance of impaired independence since oneindividual is responsible not only for the performance of theaudit but also for the day-to-day operations of some of theorganizations audited.

Audit independence in the Department of the Navy wouldbe enhanced and audit results improved by placing the auditstaff directly under the Secretary or the Under Secretary.

RECOMMENDATIONS TO THE SECRETARY OF DEFENSE

We recommend that, to improve the effectiveness of inter-nal auditing in the Department of the Navy and to help insuremaximum audit independence in accordance with our standards,

5

the Secretary of Defense place the Naval Audit Service underthe Secretary or Under Secretary of the Navy and direct thestaff to report directly to that official.

RECOMMENDATION TO THE CONGRESS

In order to assure that the greater audit independencerecommended is maintained in the future, we also recommendthat the Congress amend the National Security Act of 1947, asamended, to place the internal audit functions of the threemilitary departments under the Secretary or Under Secretaryof the respective departments and have the internal auditorsreport directly to those officials. This recommendation wasmade in a previous report (FGMSD-77-49, July 26, 1977).

6

CHAPTER 3

MORE NAVAL AUDIT SERVICE AUDIT POSITIONS

SHOULD BE CONVERTED TO CIVILIAN

The positions of Director and Deputy Director of theNaval Audit Service and most audit positions currently filledwith military personnel should be filled with qualified civil-ians.

DOD Directive 1100.4 states that the military servicesshould employ civilians in positions which

-- do not require military incumbents for reasons of law,training, security, discipline, rotation, or comb treadiness;

-- do not require a military background for successfulperformance of the duties involved; and

-- do not entail unusual hours not normally associated orcompatible with civilian employment.

DOD Directive 1100.9 states that management positions inprofessional support activities should be designated as mili-tary or civilian according to the following criteria.

Military--when required by law, when the positionrequires skills and knowledge acquired primarily throughmilitary training and experience, and when experiencein the position is essential to enable officer personnelto assume responsibilities necessary to maintain combat-related support and proper career development.

Civilian--when the skills required are usually foundin the civilian economy and continuity of managementaid experience is essential and can be better providedby civilians.

The Assistant Secretary of Defense (Manpower and ReserveAffairs), in an October 1976 article for the Defense Manage-ment Journal, stated that

"Defense Department policy is.that each position befilled by a civilian unless it can be proven that amilitary person is required. As a result, the burdenof proof is on the Services to show that each positionprogrammed as a military space can only be filled bya military person."

7

DOD policy notwithstanding, the Navy has followed thepractice of appointing high-ranking military officers to thepositions of Director, Deputy Di:ector, and District OfficeDirector(s) of the Naval Audit Service. Because militaryofficers are subject to periodic rotation, there have beenmany incumbents. Sinca 1970, the Audit Service has had fourdifferent military directors.

At the end of fiscal year 1976, tne Naval Audit Serviceemployed 35 military personnel, many of whom were in highlevel policy and management positions. Based on discussionswith Audit Service officials, there appears to be no auditwhich specifically requires military staffing. However, theAuditor General and several of the military staff believethat, as a result of the diversity of the work performed,the audit experience generally makes officers more effectivein accomplishing their responsibilities at subsequent dutystations than are officers of comparable rank not previouslyassigned to the Audit Service. Also, audit officials believethat, as a result of their training and background, militarypersonnel are more oriented toward combat-related functionsand art thus better able to audit these areas than civiliansof comparable grade.

While there may be some advantage to appointing a smallnumber of military staff to positions as management internsor in training positions, military personnel are not neededto audit combat-related functions. Other defense audit agen-cies have for a long time successfully reviewed combat-relatedfunctions without military staffing. In our opinion, auditsof combat-related or tactical functions are not unique. Theaudits are conducted by comparing peformance with standardsprescribed by both military and civilian personnel. In thiskind of audit, auditors review reported accomplishments, com-pare them to the prescribed standards, and determine whetherthe standards have been met. Military personnel are not nec-essarily better able to do this than civilians. For instance,using these and other generally accepted auditing techniques,it is not necessary for uditors to know how to shoot a rifleto determine whether the rifle has been accurately fired, orweil maintained.

OPPORTUNITY TO REALIZE SAVINGS

Public Law 93-365, dated August 5, 1974, states that:

"It is the sense of Congress that the Department ofDefense shall use the least costly form of manpower * * *consistent with military requirements and other needs ofthe Department * * *."

8

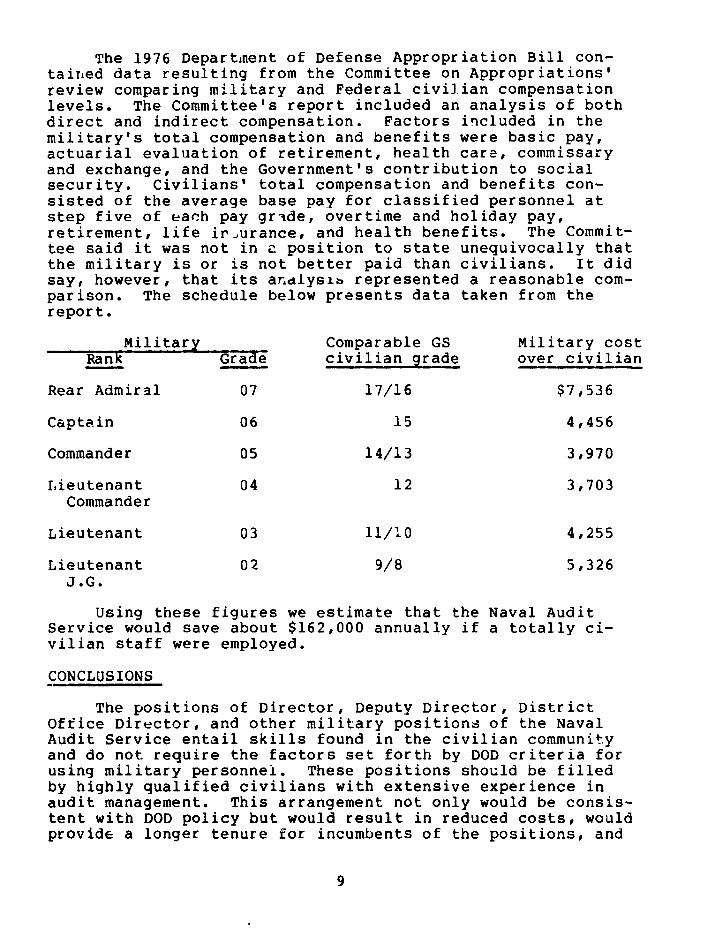

The 1976 Department of Defense Appropriation Bill con-taired data resulting from the Committee on Appropriations'review comparing military and Federal civilian compensationlevels. The Committee's report included an analysis of bothdirect and indirect compensation. Factors included in themilitary's total compensation and benefits were basic pay,actuarial evaluation of retirement, health care, commissaryand exchange, and the Government's contribution to socialsecurity. Civilians' total compensation and benefits con-sisted of the average base pay for classified personnel atstep five of each pay grade, overtime and holiday pay,retirement, life ir,urance, and health benefits. The Commit-tee said it was not in a position to state unequivocally thatthe military is or is not better paid than civilians. It didsay, however, that its andlyslb represented a reasonable com-parison. The schedule below presents data taken from thereport.

Military Comparable GS Military costRank Grade civilian grade over civilian

Rear Admiral 07 17/16 $7,536

Captain 06 15 4,456

Commander 05 14/13 3,970

Lieutenant 04 12 3,703Commander

Lieutenant 03 11/10 4,255

Lieutenant 02 9/8 5,326J.G.

Using these figures we estimate that the Naval AuditService would save about $162,000 annually if a totally ci-vilian staff were employed.

CONCLUSIONS

The positions of Director, Deputy Director, DistrictOffice Director, and other military positions of the NavalAudit Service entail skills found in the civilian communityand do not require the factors set forth by DOD criteria forusing military personnel. These positions should be filledby highly qualified civilians with extensive experience inaudit management. This arrangement not only would be consis-tent with DOD policy but would result in reduced costs, wouldprovide a longer tenure for incumbents of the positions, and

9

would result in greater continuity of management policiesand procedures.

An Advisory Committee to the American Institute ofCertified Public Accountants reached similar conclusions in1970. In an analysis of the audit function in DOD, pre-pared for the Blue Ribbon Defense Panel and included as anappendix to the panel's July 1970 report to the President,the committee recommended that the head and most of thestaff of each of the audit groups in DOD (including theNaval Audit Service) be civilians with expertise in auditmanagement. The committee pointed out that the-se recom-mended changes

"* * * would provide a longer period of tenure for thehead of the audit group, assuring greater continuityof audit policy and direction than is likely to beattained under the present arrangement of having thegroup headed by a military officer who usually has hadlittle or no professional experience in internal audit-ing * * *."

The committee further concluded that the recommended changeswould provide more attractive career opportunities for profes-sional auditors and would improve the likelihood of attract-ing and retaining highly competent people.

RECOMMENDATIONS

To enhance career opportunities for professional audi-tors and to attract and retain competent people, we recommendthat the Secretary of Defense direct the Secretary of theNavy to

--redesignate as civilian the positions of Director,Deputy Directors, and directors of district officesof the Naval Audit Service and, as they become avail-able, fill these positions with qualified civilianpersonnel and

--as they become open, staff other military positionswith qualified civilian personnel.

10

CHAPTER 4

AUDIT STAFF COULD BE USED MORE EFFECTIVELY

The Naval Audit Service has not met its audit goals andhas accumulated a large audit backlog. This is due in partto its workload and the us- of audit time on work that iseither not consistent with the Audit Service's primary mis-sion or is not sufficiently productive to warrant allocationof scarce audit staff resources.

The Audit Service's primary responsibility is to providethe Navy at all levels with an independent and objectiveinternal audit service which evaluates the effectiveness ofthe Navy's control and management of resources. Implicit inits mission statement is the mandate that the Audit Serviceis (or should be) primarily concerned with the managementand control of funds appropriated by the Congress.

IMBALANCE BETWEEN WORKLOAD AND STAFF

In 1974 the Assistant Secretary of Defense (Comptroller)placed special emphasis on increasing the effectiveness ofinternal auditing in the Department of Defense. A jointstudy group was formed consisting of representatives fromeach DOD audit organization. The first area reviewed was theworkload of the internal audit organizations within DOD.

The study group compared Naval Audit Service resourceswith its identified workload and concluded that the AuditService did not have sufficient resources to achieve tiennialaudit coverage of activities--the cycle established by DODInstruction 7600.3. Based on personnel strength as ofJune 30, 1974, and the percentage of time directly attrib-utable to audit during fiscal year 1974, the study groupreported that the Audit Service would require 6.2 years ofconcentrated effort to perform a complete audit of all Navyentities. At four Naval Audit Service offices the studygroup noted that audit cycles ranged from 8 to 15 years asshown in the following schedule:

11

No. of yearsDirect man-hours requireda - _FY974 to complete

workload EroSL m onecycleAviation Supply Office 157,250 10,40) 15.1Naval Air Statioil, Alameda 88,500 8,400 10.5Naval Air Station, Norfolk 60,600 6,10( 9.9Ships Parts Control Center 98,500 11,700 8.4

In February 1976 the Naval Audit Se ice completed aStaffing study which was conducted primaiLly to determinethe personnel resources needed to meet its projected work-load requirements, including the elimination of the currentaudit backlog, through fiscal year 1980. The recommendedtarget manpower strength and yearly staff increases neededto achieve it are presented in the following schedule.

Fiscal ear

Target 729 729 729 729 729Staffing a/572 590 633 680 729Shortfall 157 139 96 49 -a/Actual fiscal year 1976 ending strength.

CURRENT AUDIT BACKLOG

The Audit Service backlog is made up of four distinctareas. These are:

-- Activities on the periodic inventory listing whichare one or more years behind schedule.

-- Activities on the periodic inventory listing whichhave never been audited.

--Activities not planned for audits.

-- Navy ships.

In arriving at the projected manpower needs above, auditofficials considered only the first two backlog areas.As of October 1976, agency figures showed that, forapproximately 30 percent (161) of the activities on the peri-odic inventory list, audit coverage is one or more yearsbehind schedule. There are also 164 activities on the peri-odic inventory list which have never been audited. Audit

12

officials have projected that this combined backlog for 325activities can be eliminated by fiscal years 1980 or 1981,but only if the Audit Service is permitted to attain thestaffing level recommended in its study.

As noted, Audit Service officials did not consider shipsor activities at which audits were not planned in their back-log statistics. Excluded were 475 active duty ships and 60reserve force ships. The list of entities not planned foraudits contains approximately 1,300 small activities thathave never been audited and that would require an estimated106 additional staff years to audit. This list was also ex-cluded from the Audit Service's statistics. We believe thatby not including ships and entities not planned for audits,the Audit Service has seriously understated its backlog andthe staffing level required to meet its workload requirements.

OPPORTUNITY TO IMPROVE AUDIT CAPABILITY

With the audit workload greater than staff capability,it is imperative that the Audit Service be prudent in uti-lizing its staff resources. The audit staff does severalkinds of work which either are not consistent with its primarymission or are not sufficiently productive to warrant alloca-tion of scarce staff resources. This work includes specialrequest audits and audits of activities supported by nonappro-priated funds.

The use of audit staff for these secondary efforts causesa drain on scarce audit resources and impairs the Audit Serv-ice's ability to carry out its primary mission.

Special request audits

The Naval Audit Service spends a considerable amount ofstaff time on audits specifically requested by commanders ofnaval installations and activities. These special auditsare generally limited in scope to examination of a specificproblem in response to a request frcm some management level.In fiscal years 1975 and 1976, the Audit Service spent 50,960staff-hours on special request audits with limited reportutilization and distribution and 71,136 staff-hours on spe-cial request audits with normal report utilization and dis-tribution. The value of this combined service was about $2.6million, computed on the basis of the Audit Service's averagecost per staff-hour.

Requests for audit assistance are handled on a case-by-case basis. Before acceptance, each request is investigatedto ascertain

13

-- the size and scope of the job and manpower require-ments,

-- the impact on audits in progress or scheduled, and

-- whether action within the purview of audit is actuallyrequired, or whether assistance from a source otherthan audit would be more appropriate.

In our 1968 report entitled "Internal Audit Activitiesin the Department of Defense" (B-132900), we noted that, inperforming special request audits, DOD's internal audit orga-nizations were limiting their reporting function and wereperforming as internal review groups rather than as internalaudit organizations.

Audits of nonappropriatedfund activities

The Naval Audit Service devotes a large amount of stafftime to audits of activities which are operated primarilyfor the benefit of military personnel and their dependents.In fiscal years 1975 and 1976, it spent 66,976 staff-hoursin auditing nonappropriated fund activities. The value ofthis service was about $1.4 million, computed on the basisof the Audit Service's average cost per staff-hour. TheAudit Service estimates it will spend 30,875 staff-hours(valued at about $650,000) in making these audits in fiscalyear 1977. The Audit Service is not reimbursed by theaudited activities for the cost of this work.

There are several levels of audit inspection and reviewapplied to Navy's nonappropriated fund activities. They in-clude the local command, the immediate superior in command,the Bureau of Naval Personnel, certified public accountants(CPAs), and the Naval Audit Service. According to NavalAudit Service Instruction 7520.7A, a 2 -year cycle has beendesignated for coverage of nonappropriated fund activitiesby the Audit Service. Although the Audit Service is not ableto meet the 2-year cycle, the audit coverage of nonappropri-ated funds is, on a cyclical basis, relatively greater thanthe coverage of appropriated funds.

A report issued on October 30, 1972, by a special subcom-mittee of the House Armed Services Committee discussed auditsupport provided to nonapropriated fund activities. Thesubcommittee noted that the three military department auditagencies are funded by appropriated funds and that their pri-mary mission is to conduct audits to evaluate the effective-ness with which commanders utilize appropriated-fund resources.

14

Tr Subcommittee recommended that the secretary of each mili-department establish an audit staff directly under him

t audit all nonappropriated funds.

A its of the Navy Relief Society

During the past few years, the Audit Service has per-formed semiannual audits of the Navy Relief Society Head-quarters, a nonappropriated fund activity. These examinationscovered transactions shown in the books and records of theSociety. The audit for the year ended December 31, 1975,took about 750 direct staff-hQurs. The audit, completed inSeptember 1976 for the 6-month period ended June 30, 1976,took about 500 direct staff-hours. Because of other workloadrequirements, the present Auditor General has requested thatthe Navy Relief Society utilize CPA firms for these audits.

CuNCLUSIONS

The Naval Audit Service has not been able to cover itsestablished workload--there is a large imbalance between itsworkload and the Audit Service's ability to meet it. It isimportant that the two be brought into balance so that theAudit Service can reduce its backlog and improve its auditcoverage. Internal audit staffs should be of an adequate sizeto perform required audits within established time frames.

The Naval Audit Service devotes a substantial amount ofstaff time to marginally productive and nonmission-relatedaudit work and to special request and nonappropriated fundaudits. If these types of efforts were reduced, the AuditService would have additional staff time available each yearfor carrying out its primary mission and reducing the currentaudit backlog.

The Audit Service's policy of conducting audits on spe-cific problems, some with reporting limited to the requestingofficials, results in reduced effectiveness of the auditingand reporting functions of a central audit agency. Thesetypes of efforts appear to be within the scope of internalreview responsibilities for which a capability already existsat command levels.

The Audit Service has devoted too large an amount ofstaff time for audits of nonappropriated fund activities.Using internal auditors to review nonappropriated fund ac-tivities is questionable from a management viewpoint becausethese audits represent a free service provided at the tax-payers' expense to activities which were set up to be largelyself-supporting.

15

RECOMMENDATIONS

We recommend that the Secretary of Defense direct theSecretary of the Navy to improve the Audit Service's abilityto cover its workload. Among the alternatives to be consid-ered are:

-- Assess the minimum required workload of the NavalAudit Service and the capability of the audit staffto perform that work and take action to bring thetwo into balance,

-- Significantly reduce the number of special requestaudits performed, and

-- Reduce audits of nonappropriated fund activities.

16

CHAPTER 5

NEED FOR MORE EFFECTIVE FOLLOWUP OF AUDIT FINDINGS

The Navy's audit followup system does not provide assur-ance that all deficiencies identified by internal audits arepromptly corrected.

Internal auditing, regardless of how well it is done, isuseless unless prompt and effective action is taken to cor-rect deficiencies identified. In our opinion, the true mea-sure of an internal audit organization's effectiveness is itssuccess in bringing about needed improvements. To insurethat appropriate management action is taken on audit recom-mer.dations, there must be an effective audit followup systemwhich promptly apprises top management of the adequacy ofcorrection action.

GUIDANCE .. FOLLOWUP OF FINDINGS

General Services Administration's Federal Management Cir-cular 73-2 sets forth policies to be followed in the audit ofFederal operations and programs by executive departments andestablishments. The circular requires agencies to designateofficials responsible for following up on audit recommenda-tions, and to submit periodic reports to agency managementon actions taken on audit recommendations.

Our guidance on internal auditing in ederal agenciesrecognizes that rimary responsibility for action and follow-up on audit recommendations rests with management. Still,reporting a finding, observation, or recommendation shouldnot end an internal auditor's concern with the matter. Heshould ascertain whether his recommendations have receivedserious management consideration and whether satisfactorycorrective actions have been taken.

NAVAL AUDIT SERVICE FOLLOWUP IS SPOTTY

The Audit Service does not have a formal system that caneffectively track the progress of findings and recommendationsafter reports are issued. Significant findings and recom-mendations in certain audit reports are selected for the at-tention of the cognizant assistant secretaries, the UnderSecretary, and the Secretary of the Navy. These selectedaudit cases require senior Navy and Marine Corps officialsto provide management's position on

17

--the adequacy of the corrective actions taken or plannedby managemenc,

-- the propriety of the target dates for completion ofunfinished corrective actions, and

-- the reasons for nonconcurrence with any audit recom-mendations.

There have been only 10 such cases since 1972. Also, theAudit Service conducts followup reviews as requested by man-agement or as directed by the Assistant Secretary of the Navy(Financial Management). In certain instances the AuditorGeneral personally apprises management of the audit situationthrcugh letters. Still, these followup actions by the AuditService have not been good enough.

The Audit Service has not est.blished a formal followupsystem because it has not been directed to do so. Departmentof Defense Instruction 7600.3, amended November 28, 1975,specifies that an independent office should be assigiedresponsibility for monitoring actions taken on audit findingsand recommendations, but does not designate the internal auditorganization as this independent office. Navy instructionsclearly require managers to monitor corrective actions but donot specifically require the Audit Service followup on itsown reports.

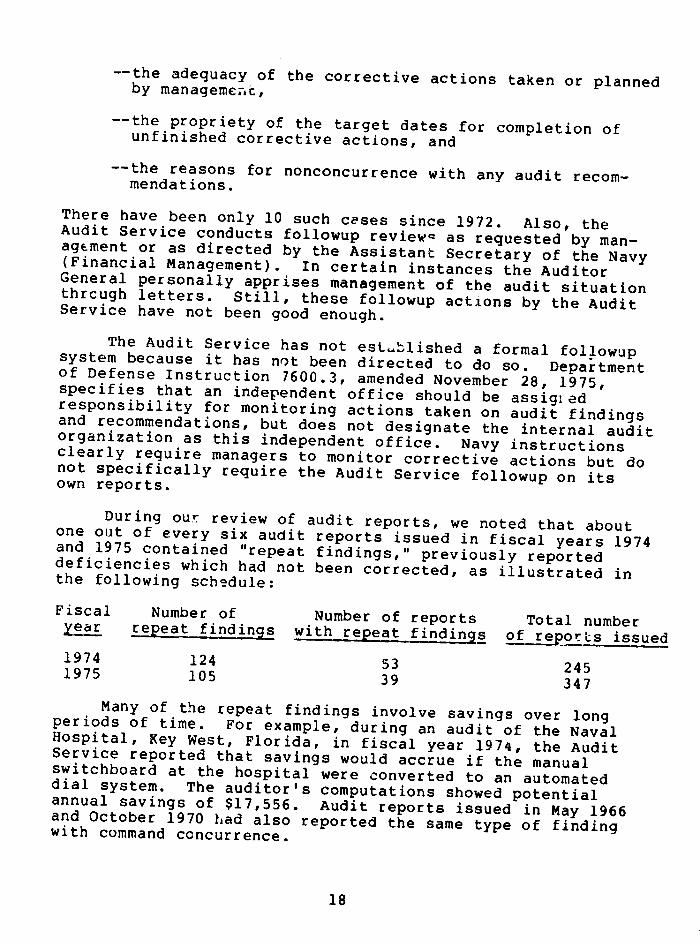

During our review of audit reports, we noted that aboutone out of every six audit reports issued in fiscal years 1974and 1975 contained "repeat findings," previously reporteddeficiencies which had not been corrected, as illustrated inthe following schedule:

Fiscal Number of Number of reports Total numberyear repeat findings with repeat findings of reports issued

1974 124 53 2451975 105 39 347

Many of the repeat findings involve savings over longperiods of time. For example, during an audit of the NavalHospital, Key West, Florida, in fiscal year 1974, the AuditService reported that savings would accrue if the manualswitchboard at the hospital were converted to an automateddial system. The auditor's computations showed potentialannual savings of $17,556. Audit reports issued in May 1966and October 1970 had also reported the same type of findingwith command concurrence.

18

Another example occurred during audits of the NavalRegional Medical Center, Portsmouth, Virginia. In fiscalyear 1974, the Audit Service reported that the Medical Centerwould realize savings thLough increased use of Federalsources of supply to satisfy material requirements. The audi-tors reviewed some procurement items and compared the costof similar items in Federal supply sources showing that theycould have ben purchased at a savings of about $90,900.This condition had also been reported in a previous auditreport issued in October 1970 with command concurring.

CONCLUSIONS

The Navy's audit followup should be strengthened to helpinsure prompt evaluation of all crrective actions taken inresponse to audit recommendations and to provide reports ofthese evaluations to top management.

The large number of repeat findings indicates the inade-quacy of both management's implementation of audit recommenda-tions and its present procedures for audit followup. Ineffect, Naval Audit Service's appraisals have not effectivelyinsured appropriate followup actions by management. To cor-rect this situation, the Audit Service should establish aformal followup system--thus permitting auditors who are al-ready located in the field and who are familiar with reportedconditions to evaluate the adequacy of corrective actionstaken and to verify that all significant weaknesses have beencorrected. The results of these evaluations should be sum-marized and reported to appropriate top management levels irthe Navy.

RECOMMENDATIONS

To increase he effectiveness of the Navy's audit fol-lowup system, we recommend that the Secretary of Defensedirect the Secretary of the Navy to:

-- Require the Audit Service to make more followup re-views to determine whether appropriate correctiveaction has been taken on all significant audit find-ings.

-- Instruct other Navy activities to prepare writtenreports as to the actions taken on audit recommenda-tions and require the Audit Service to evaluate thereports to determine whether appropriate correctiveactions have been taken.

-- Require the Audit Service to periodically report theresults of its followup evaluations in summary formto top management officials.

19

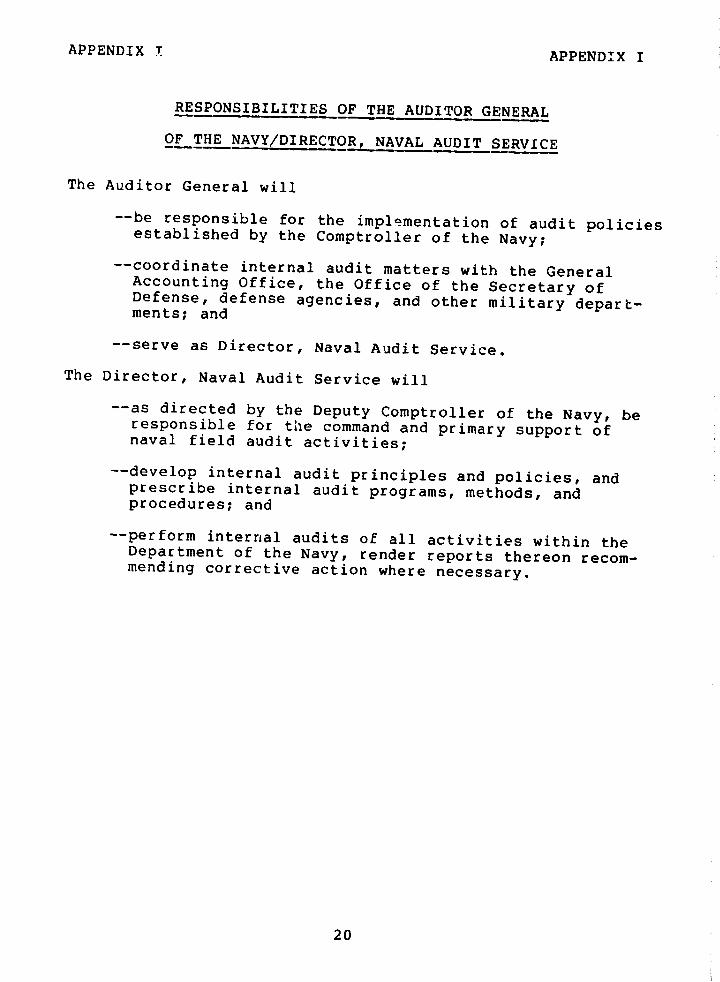

APPENDIX T APPENDIX I

RESPONSIBILITIES OF THE AUDITOR GENERAL

OF THE NAVY/DIRECTOR, NAVAL AUDIT SERVICE

The Auditor General will

--be responsible for the implementation of audit policiesestablished by the Comptroller of the Navy;

--coordinate internal audit matters with the GeneralAccounting Office, the Office of the Secretary ofDefense, defense agencies, and other military deparL-ments; and

-- serve as Director, Naval Audit Service.

The Director, Naval Audit Service will

-- as directed by the Deputy Comptroller of the Navy, beresponsible for the command and primary support ofnaval field audit activities;

--develop internal audit principles and policies, andprescribe internal audit programs, methods, andprocedures; and

-- perform internal audits of all activities within theDepartment of the Navy, render reports thereon recom-mending corrective action where necessary.

20

APPENDIX II APPENDIX II

U.

I-II~~~~I00z Iv cW aMur2

!--Y C

I I

I IF

I)-'-

z

>LU

-%~~~~~~-;

2w~~ 8O 1-

> ,F t>

z ~irO aLA.3

.- Io IwZ ~ ~ 0 wU

z>~~mo

I o 5~~~~~~

cc~~~~c

> "2>~ i-'"

@~~~~~~~~~~~ 0

I - I U.

0

M.~~~~Eo~~~~~~~~

w CC0 > aZ wt at~MW 0< LU 4 .- I C

Ur ,

U~~~~~~~~~~~~..

0~~~~~~~~~~

I~~~~~~I

c ~ ~ ~ ~~~~~~~~~~Z

O~~~~~~~~~

z z o21 2

LU I I I I 'a ZZ cu. o~~~ , . c

UjrU

CC

~~~R% otW~~~FX~ ~~Lr 4c

w ~~~~35 6m OL 0,

C w~~~~

APPENDIX III APPENDIX III

PRINCIPAL OFFICIALS

RESPONSIBLE FOR ADMINISTERING

ACTIVITIES DISCUSSED IN THIS REPORT

Tenure of officeFrom To

DEPARTMENT OF DEFENSE

SECRETARY OF DEFENSE:Harold Brown Jan. 1977 PresentDonald H. Rumsfeld Nov. 1975 Jan. 1977William P. Clements, Jr. Nov. 1975 Nov. 1975

(acting)James R. Schlesinger July 1973 Nov. 1975

DEPARTMENT OF THE NAVY

SECRETARY OF THE NAVY:W. Graham Claytor, Jr. Feb. 1977 PresentG. D. Penisten Feb, 1977 Feb. 1977

(acting)David R. MacDonald Jan. 197/ Feb. 1977

(acting)J. W. Middendorf June 1974 Jan. 1977J. W. Middendorf Apr. 1974 June 1974

(acting)John Warner May 1972 Apr. 1974

ASSISTANT SECRETARY OF THE NAVY(FINANCIAL MANAGEMENT)/COMPTROLLEROF THE NAVY:

Rear Adm. J. R. Ahern May 1977 Present(acting)

G. D. Penisten Oct. 1974 May 1977Rear Adm. S. H. Moore Apr. 1974 Oct. 1974

(acting)Robert D. Nesen May 1972 Apr. 1974

AUDITOR GENERAL OF THE NAVY/DIRECTOR, NAVAL AUDIT SERVICE:

Rear Adm. P. H. Engel May 1975 PresentRear Adm. J. E. Forrest July 1972 May 1975

(91163)

22