The Accounting Information System. Study Objectives 1.Analyze the effect of business transactions on...

75

The Accounting The Accounting Information System Information System

-

Upload

brent-blair -

Category

Documents

-

view

216 -

download

0

Transcript of The Accounting Information System. Study Objectives 1.Analyze the effect of business transactions on...

The AccountingThe AccountingInformation SystemInformation System

Study ObjectivesStudy Objectives

1.1. Analyze the effect of business transactions Analyze the effect of business transactions on the basic accounting equation.on the basic accounting equation.

2.2. Explain what an account is and how it helps Explain what an account is and how it helps in the recording process.in the recording process.

3.3. Define debits and credits and explain how Define debits and credits and explain how they are used to record business they are used to record business transactions.transactions.

4.4. Identify the basic steps in the recording Identify the basic steps in the recording process.process.

Study ObjectivesStudy Objectives

5.5. Explain what a journal is and how it helps Explain what a journal is and how it helps in the recording process.in the recording process.

6.6. Explain what a ledger is and how it helps Explain what a ledger is and how it helps in the recording process.in the recording process.

7.7. Explain what posting is and how it helps Explain what posting is and how it helps in the recording process.in the recording process.

8.8. Explain the purposes of a trial balance.Explain the purposes of a trial balance.

5

Accounting Information SystemAccounting Information System

The system of collecting and processing The system of collecting and processing transaction data and communicating transaction data and communicating financial information to interested financial information to interested parties.parties.

Chapter OverviewChapter Overview

##11 Analyze the Effect of Analyze the Effect of

Business Transactions on the Business Transactions on the Basic Accounting Equation.Basic Accounting Equation.

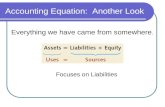

Assets = Liabilities + Stockholders’ EquityAssets = Liabilities + Stockholders’ Equity

Recall:Recall: must always balance!must always balance!

Accounting TransactionsAccounting Transactions

• Accounting Transactions:Accounting Transactions: economic events that economic events that must be recorded in the must be recorded in the financial statements.financial statements.

• Event must affect assets, Event must affect assets, liabilities or stockholders’ liabilities or stockholders’ equityequity

Accounting Transactions? Accounting Transactions?

Purchase computerPurchase computer

Is the financial position (assets, liabilities or Is the financial position (assets, liabilities or stockholders’ equity changed?stockholders’ equity changed?

YES!YES!

Accounting Transactions? Accounting Transactions?

Discuss product design Discuss product design with customerwith customer

Is the financial position (assets, liabilities or Is the financial position (assets, liabilities or stockholders’ equity changed?stockholders’ equity changed?

NO!NO!

Accounting Transactions? Accounting Transactions?

Pay rentPay rent

Is the financial position (assets, liabilities or Is the financial position (assets, liabilities or stockholders’ equity changed?stockholders’ equity changed?

YES!YES!

Transaction AnalysisTransaction Analysis

• Transaction Analysis:Transaction Analysis: the process of identifying the process of identifying the specific effects of economic events on the the specific effects of economic events on the accounting equation.accounting equation.

• Each transaction has a dual (double-sided) effectEach transaction has a dual (double-sided) effect

Transaction AnalysisTransaction Analysis

• If an individual asset is increased, there If an individual asset is increased, there must be a corresponding:must be a corresponding:– Decrease in another asset, Decrease in another asset, oror– Increase in a specific liability, Increase in a specific liability, oror– Increase in stockholders’ equityIncrease in stockholders’ equity

Transaction AnalysisTransaction Analysis

• Two or more items can be affectedTwo or more items can be affected

• Example: purchase computer for Example: purchase computer for $10,000 by paying $6,000 in cash and $10,000 by paying $6,000 in cash and signing a note for $4,000signing a note for $4,000

Let’s Practice!Let’s Practice!

Let’s practice transaction analysis Let’s practice transaction analysis with Sierra Corporation. . .with Sierra Corporation. . .

Event 1 – Investment of Cash Event 1 – Investment of Cash by Stockholdersby Stockholders

Oct. 1 - Owner invested $10,000 Cash in Oct. 1 - Owner invested $10,000 Cash in business in exchange for $10,000 of business in exchange for $10,000 of Sierra Corporation Common StockSierra Corporation Common Stock

Event 2 – Note Issued in Event 2 – Note Issued in Exchange for CashExchange for Cash

Oct. 1 – Sierra issued a 3-month, 12%, Oct. 1 – Sierra issued a 3-month, 12%, $5,000 Note Payable to Castle Bank. $5,000 Note Payable to Castle Bank.

Event 3 – Purchase of Office Event 3 – Purchase of Office Equipment for CashEquipment for Cash

Oct. 2 – Sierra acquired office equipment Oct. 2 – Sierra acquired office equipment by paying $5,000 cash to Superior Sales Co.by paying $5,000 cash to Superior Sales Co.

Event 4 – Receipt of Cash in Event 4 – Receipt of Cash in Advance from CustomerAdvance from Customer

Oct. 2 – Sierra received a $1,200 Oct. 2 – Sierra received a $1,200 cash advance from R. Knox, a client.cash advance from R. Knox, a client.

Event 5 – Services Rendered for Event 5 – Services Rendered for CashCash

Oct. 3 – Sierra received $10,000 in cash Oct. 3 – Sierra received $10,000 in cash from Copa Co. for advertising services from Copa Co. for advertising services performedperformed

Event 5 – Services Rendered, Event 5 – Services Rendered, WHAT IFWHAT IF these were performed these were performed

“on account”?“on account”?

Later, when $10,000 is collected from Later, when $10,000 is collected from customer…customer…

Event 6 – Payment of RentEvent 6 – Payment of Rent

Oct. 3 – Sierra paid its office rent for the month Oct. 3 – Sierra paid its office rent for the month of October in cash, $900.of October in cash, $900.

Event 7 – Purchase of Insurance Event 7 – Purchase of Insurance Policy with CashPolicy with Cash

Oct. 4 – Sierra paid $600 for a one-year insurance Oct. 4 – Sierra paid $600 for a one-year insurance policy that will expire next year on Sept. 30.policy that will expire next year on Sept. 30.

Event 8 – Purchase of Supplies Event 8 – Purchase of Supplies on Crediton Credit

Oct. 5 – Sierra purchases a three-month supply of Oct. 5 – Sierra purchases a three-month supply of advertising materials on account from Aero Supply for advertising materials on account from Aero Supply for $2,500.$2,500.

Event 9 – Hiring of New Event 9 – Hiring of New EmployeesEmployees

Oct. 9 – Sierra hired four new Oct. 9 – Sierra hired four new employees to begin work on Oct. 15.employees to begin work on Oct. 15.

Accounting transaction Accounting transaction has has NOTNOT occurred! occurred!

Event 10 – Payment of DividendEvent 10 – Payment of Dividend

Oct. 20 – Sierra paid a $500 dividend.Oct. 20 – Sierra paid a $500 dividend.

Event 11 – Payment of Cash for Event 11 – Payment of Cash for Employee SalariesEmployee Salaries

Oct. 26 – Paid employees working two Oct. 26 – Paid employees working two weeks, who have earned $4,000 in salaries. weeks, who have earned $4,000 in salaries.

Summary of TransactionsSummary of Transactions

Assets =Assets = LLiabilities ies ++ E Equityity

##22 Explain what an account is and Explain what an account is and

how it helps in the recording how it helps in the recording process.process.

• Account:Account: individual accounting individual accounting record of increases and decreases in a record of increases and decreases in a specific Asset, Liability, or specific Asset, Liability, or Stockholders’ Equity item.Stockholders’ Equity item.

AccountAccount

• Consists of three parts:Consists of three parts:

–Title of the accountTitle of the account

–Left sideLeft side, the , the debitdebit side, side, Dr.Dr.

–Right sideRight side, the , the creditcredit side, side, Cr.Cr.

• We call this the T - accountWe call this the T - account

The T AccountThe T Account

##33 Define debits and credits and Define debits and credits and

explain how they are used to explain how they are used to record business transactions.record business transactions.

• Recall Debit means leftRecall Debit means left

• thus, entry on thus, entry on left side is debitingleft side is debiting

• Recall Credit means rightRecall Credit means right

• thus, entry on thus, entry on right side is creditingright side is crediting

ExExamplesles

52

Total the Balances on T-AccountTotal the Balances on T-Account

DebitDebitTitle of AccountTitle of Account

CreditCredit

Total Debits Total Debits >> Credits, then you Credits, then you

have a Debit have a Debit Balance!Balance!

52

Total the Balances on T-AccountTotal the Balances on T-Account

DebitDebitTitle of AccountTitle of Account

CreditCredit

Total Credits Total Credits >> Debits, then you Debits, then you

have a Credit have a Credit Balance!Balance!

Normal Balances Normal Balances for Assets and Liabilitiesfor Assets and Liabilities

Normal Balances Normal Balances for Stockholders’ Equityfor Stockholders’ Equity

Normal Balances Normal Balances for Expenses and Revenuesfor Expenses and Revenues

52

DebitsDebits

Increase assets Increase assets and expenses and expenses

Decrease Decrease liabilities, liabilities, common stock, common stock, revenuesrevenues

53

CreditsCredits

Decrease assets and Decrease assets and expensesexpenses

Increase liabilities, Increase liabilities, common stock, common stock, revenuesrevenues

Expansion of Basic EquationExpansion of Basic Equation

Let’s ReviewLet’s ReviewWhat is the normal balance for the What is the normal balance for the

following accounts?following accounts?

Cash?Cash?

Service Revenue?Service Revenue?

Accounts Receivable?Accounts Receivable?

Accounts Payable?Accounts Payable?

Common Stock?Common Stock?

Salaries Expense?Salaries Expense?

DebitDebit

CreditCredit

DebitDebit

CreditCredit

CreditCredit

DebitDebit

Let’s ReviewLet’s ReviewWhat is the normal balance for the What is the normal balance for the

following accounts?following accounts?

Dividends?Dividends?

Service Revenue?Service Revenue?

Taxes Payable?Taxes Payable?

Building?Building?

Prepaid Insurance?Prepaid Insurance?

Rent Expense?Rent Expense?

DebitDebit

DebitDebit

CreditCredit

CreditCredit

DebitDebit

DebitDebitMore

52

Let’s Review Using Let’s Review Using Sierra’s TransactionsSierra’s Transactions

Oct. 1 - Owner invested $10,000 Cash in Oct. 1 - Owner invested $10,000 Cash in business in exchange for $10,000 of business in exchange for $10,000 of Sierra Corporation Common StockSierra Corporation Common Stock

CashCash Common StockCommon Stock

10,00010,000 10,00010,000

52

Let’s Review Using Let’s Review Using Sierra’s TransactionsSierra’s Transactions

CashCash Note PayableNote Payable

5,0005,000 5,0005,000

Oct. 1 – Sierra issued a 3-month, 12%, Oct. 1 – Sierra issued a 3-month, 12%, $5,000 Note Payable to Castle Bank. $5,000 Note Payable to Castle Bank.

52

Let’s Review Using Let’s Review Using Sierra’s TransactionsSierra’s Transactions

Office EquipmentOffice Equipment CashCash

5,0005,000 5,0005,000

Oct. 2 – Sierra acquired office equipment Oct. 2 – Sierra acquired office equipment by paying $5,000 cash to Superior Sales Co.by paying $5,000 cash to Superior Sales Co.

5,0005,000

10,00010,000

##44 Identify the Basic Steps in Identify the Basic Steps in

the Recording Process.the Recording Process.

1.1.AnalyzeAnalyze

2.2. JournalizeJournalize

3.3.PostPost

Recording Process Step 1Recording Process Step 1

Analyze each transaction and Analyze each transaction and effect on accountseffect on accounts

Recording Process Step 2Recording Process Step 2

Enter transaction information in a journal, Enter transaction information in a journal, a process called journalizinga process called journalizing

Recording Process Step 3Recording Process Step 3

Transfer (post) the journal information Transfer (post) the journal information to the appropriate accounts in the ledgerto the appropriate accounts in the ledger

##55 Explain what a journal is and Explain what a journal is and

how it helps in the recording how it helps in the recording process.process.

• An accounting record where the An accounting record where the transactions are initially recorded in transactions are initially recorded in chronological order.chronological order.

• For each transaction journal shows the For each transaction journal shows the debit and creditdebit and credit

58

Journals Help Recording ProcessJournals Help Recording Process

• Discloses in one place the complete effect Discloses in one place the complete effect of a transactionof a transaction

• Provides a chronological record of Provides a chronological record of transactionstransactions

• Helps prevent or locate errors because debit Helps prevent or locate errors because debit and credit amounts can be readily comparedand credit amounts can be readily compared

58

Computerized SystemsComputerized Systems

• Journals are kept as Journals are kept as data filesdata files

• Accounts are recorded in computer Accounts are recorded in computer databasedatabase

JournalizingJournalizing

• Complete entry consists of:Complete entry consists of:– Date of transactionDate of transaction– Accounts titles and dollar amounts to be Accounts titles and dollar amounts to be

debited and crediteddebited and credited– Brief explanationBrief explanation

• Let’s use the first three Sierra transactions . . .Let’s use the first three Sierra transactions . . .

Examample

Date Debit Credit

GENERAL JOURNAL

Account Titles and Explanations

2005 Oct. 1 Cash 10,000 Common Stock 10,000 (Invested cash in business) 1 Cash 5,000

Notes Payable 5,000 (Issued 3-month, 12% note payable for cash) 2 Office Equipment 5,000 Cash 5,000 (Purchased office equipment for cash)

##66 Explain what a ledger is and Explain what a ledger is and

how it helps in the recording how it helps in the recording process.process.

• Ledger is the entire group of accounts Ledger is the entire group of accounts maintained by a companymaintained by a company

•Keeps all the information about current Keeps all the information about current account balances and changes in specific account balances and changes in specific account balancesaccount balances

• Ledger contains all the asset, liability, & Ledger contains all the asset, liability, & stockholders’ equity accountsstockholders’ equity accounts

General LedgerGeneral Ledger

Most businesses computerize these files!Most businesses computerize these files!

Chart of AccountsChart of Accounts• List of company accountsList of company accounts• Number and type used depends upon size Number and type used depends upon size

and complexity of businessand complexity of business• Small business might use 20 to 30 accountsSmall business might use 20 to 30 accounts• Large business could use thousands Large business could use thousands

worldwideworldwide• Computerized systems assign number Computerized systems assign number

sequence to each unique account and groupsequence to each unique account and group

Chart of AccountsChart of Accounts

Note: In the Sierra examples we used the red accountsNote: In the Sierra examples we used the red accounts

##77 Explain what posting is and Explain what posting is and

how it helps in the recording how it helps in the recording process.process.

• Procedure of transferring Procedure of transferring journal entries to ledger is journal entries to ledger is called postingcalled posting

Recall:Recall: Basic Steps in the Recording Process.Basic Steps in the Recording Process.

1.1. Analyze the transaction, identify the type of Analyze the transaction, identify the type of accounts involved?accounts involved?

2.2. Journalize, debit or credit what?Journalize, debit or credit what?

3.3. PostPost

Let’s use some of Sierra’s data to demonstrate Let’s use some of Sierra’s data to demonstrate the recording process . . .the recording process . . .

Posting in Data File or Paper FilesPosting in Data File or Paper Files

GENERAL JOURNALGENERAL JOURNAL

Account Titles and ExplanationsAccount Titles and Explanations

2005 2005 Oct. 1 Cash Oct. 1 Cash 10,000 10,000 Common Stock Common Stock 10,000 10,000

BalanceAcct 1010 Account CASH

Date

Acct 3010 Account COMMON STOCKDate

Balance

debit

debit

credit

credit

debit

debit

credit

credit

ref

ref

Oct 1

Oct 1

GJ 1

GJ 1

10,000 10,000

10,00010,000

##88 Explain the purposes of a trial Explain the purposes of a trial

balance.balance.• Lists all the accounts and their balances at a Lists all the accounts and their balances at a given time.given time.

• Proves mathematical equality of debits Proves mathematical equality of debits and credits after posting.and credits after posting.

• Useful in the preparation of financial Useful in the preparation of financial statements.statements.

• Does not tell you ledger is correct!Does not tell you ledger is correct!

Sierra CorporationTrial Balance

October 31, 2005

Debit Credit Cash $15,200Advertising Supplies 2,500Prepaid Insurance 600Office Equipment 5,000Notes Payable $ 5,000Accounts Payable 2,500Unearned Service Revenue 1,200Common Stock 10,000Dividends 500Service Revenue 10,000Salaries Expense 4,000Rent Expense 900 $28,700 $28,700