Tax Capacity, Fiscal Federalism and Development · Tax Capacity, Fiscal Federalism and Development...

64

Tax Capacity, Fiscal Federalism and Development ",, (+-(0' '"/+,"-2, ' "'",-+2 ( "'', !' -(+ 1, 2015

-

Upload

nguyenthuan -

Category

Documents

-

view

216 -

download

0

Transcript of Tax Capacity, Fiscal Federalism and Development · Tax Capacity, Fiscal Federalism and Development...

Tax Capacity, Fiscal Federalism and Development

���� � �",,�

��(+ �-(0' �'"/�+,"-2, ���� �'� ��

�"'",-+2 (� �"'�'��, �!�'�

��-(��+ 1, 2015

��1�-"(' �'� ��/�%()&�'- �q ︎��1�-"(' ", ��'-+�% -( �(-! ,-�-� �'� ��('(&"�

��/�%()&�'-

OLS Coefficient: 5.72 (1.24)

010

2030

4050

Tota

l taxe

s / G

DP

7 8 9 10 11Log GDP per Capita in 2005

A. Total Tax Revenue to GDP

Source: Kleven, Kreiner, Saez (2015)

��1�-"(' �'� ��/�%()&�'- �

q ︎�+"-"��% *.�,-"(', "' -!� �"�%� (� ��/�%()&�'- �(+ )(%"�2&�$�+, �'� �����&"�,

5 !(0 �(�, � (/�+'&�'- ( �+(& +�","' �+(.'� 10% (� ��� "' -�1�, -( +�","' �+(.'� 40%”? (��,%�2 �'� ��+,,(' 2013)

6 0!�- ", -!� ()-"&�% "'/�,-&�'- "' -�1 �(%%��-"(' �'� ��&"'",-+�-"('?q ���"�"�'- -�1�-"(' +�*."+�, "'/�,-&�'-, "' ��)��"-2

(�%�&+(� �'� 2014)

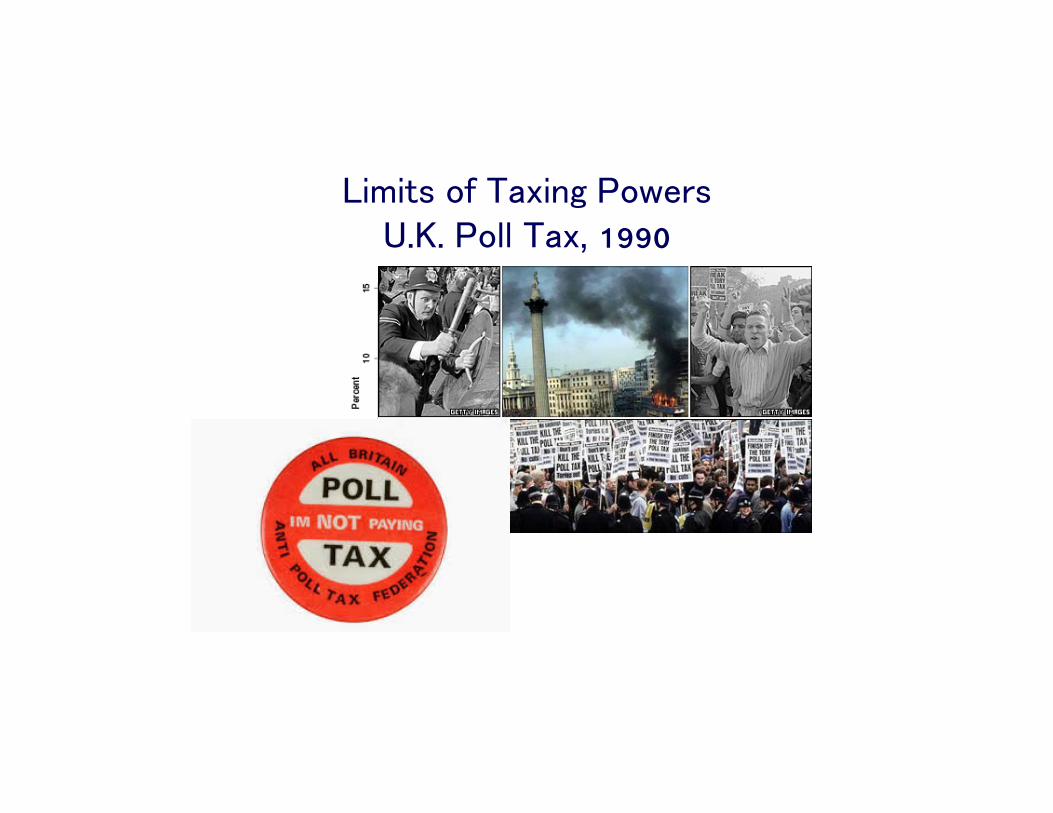

7 (0 ��' �/"��'�� �� �+(. !- -( ���+ (' )(%"�2 ��," 'q )(%"�2 '(- ��,�� (' �/"��'�� ��' (�-�' �( &(+� !�+& -!�' ((�

"&"-, (� ��1"' �(0�+, ��.�. �(%% ��1, 1990

��1�-"(' �'� ��/�%()&�'- �

q ︎�+"-"��% *.�,-"(', "' -!� �"�%� (� ��/�%()&�'- �(+ )(%"�2&�$�+, �'� �����&"�,

5 !(0 �(�, � (/�+'&�'- ( �+(& +�","' �+(.'� 10% (� ��� "' -�1�, -( +�","' �+(.'� 40%”?(��,%�2 �'� ��+,,(' 2013)

6 0!�- ", -!� ()-"&�% "'/�,-&�'- "' -�1 �(%%��-"(' �'� ��&"'",-+�-"('?q ���"�"�'- -�1�-"(' +�*."+�, "'/�,-&�'-, "' ��)��"-2

(�%�&+(� �'� 2014)

7 (0 ��' �/"��'�� �� �+(. !- -( ���+ (' )(%"�2 ��," 'q )(%"�2 '(- ��,�� (' �/"��'�� ��' (�-�' �( &(+� !�+& -!�' ((�

�.-%"'�

1. ��,"� ��--�+', �'� �+�'�,

2. �('��)-.�% �+�&�0(+$�) ��,"� ��('(&"� &(��%

�) ��1 ������� �))+(��!

3. �&)"+"��% "-�+�-.+�: �!�- �/� �� ��+'���) ��-!(�,: &(��%"-"�, �'� -��!'"��%"-"�,�) �/"��'��

4. �",��% ����+�%",& �'� �*."-2

5. �"+��-"(', �(+ �+��-"-"('�+, �'� �(%"�2&�$�+,

��1�-"(' �'� �",��% ��)��"-2 "' ��/�%()"' �(.'-+"�,

1. (0 �",��% ��)��"-2

2. ��/2 +�%"�'�� (' '�++(0 (�",-(+-"('�+2) -�1�, �, ())(,�� �+(��-��,�� ("'�(&�) -�1�,

q �+���, ,�%��-"/� �(',.&)-"(' �'� -.+'(/�+ -�1�,

q -�1 ��&"'",-+�-"('

0.1

.2.3

.4.5

Share

of ta

xes in G

DP

(1999)

6 7 8 9 10 11Log GDP per capita in 2000

High income in 2000 Mid income in 2000

Low income in 2000 Fitted values

A. Country-level taxes and income

0.1

.2.3

.4.5

5 y

ear

avera

ges o

f share

of ta

xes in G

DP

6 7 8 9 10 115 year averages of log GDP per capita

1900-39 1940-49 1950-69

1970-99 Fitted values

B. Global-level taxes and income

Figure 3: Tax revenue and GDP per capita

such tax allocations may encourage smuggling, this is a much easier propo-sition than collecting income taxes. The latter requires major investmentsin enforcement and compliance structures throughout the entire economy.We can thus obtain an interesting indication of fiscal-capacity investmentsby holding constant total tax revenue, and ask how large a share of it iscollected from trade taxes and income taxes, respectively.These shares are plotted against each other in Figure 4.4 Again, we report

the cross-sectional pattern for the year 2000, based on data from Baunsgaardand Keen (2005), and the time-series pattern over the last 100 years based onhistorical data from Mitchell (2007). The income-tax share is displayed onthe vertical axis, and the trade-tax share on the horizontal axis. We observea clear negative correlation: countries with a higher reliance on income taxestend to have less reliance on trade taxes. The left panel also shows a strikingpattern by income: high-income countries depend more on income taxes,while middle- and — in particular — low-income countries depend more ontrade taxes. The right panel of Figure 4 shows that the move from tradeto income taxes has also been a feature of the historical development of taxsystems. Again, the cross-sectional and time-series patterns look strikingly

4Other taxes not included in either trade or income taxes include indirect taxes suchas VAT, property and corporate taxes.

7

�"�!�+ �(.'-+"�, �(%%��- � &.�! %�+ �+ ,!�+� (� -!�"+ "'�(&� "' -�1�, -!�' �( )((+�+ �(.'-+"�,.

"'�(&�

��1

/���

-"&�

�%(��%

��1/�

��

��1�-"(' �'� �",��% ��)��"-2 "' ��/�%()"' �(.'-+"�,

1. (0 �",��% ��)��"-2

2. ��/2 +�%"�'�� (' '�++(0 (�",-(+-"('�+2) -�1�, �, ())(,�� �+(��-��,�� ("'�(&�) -�1�,

q -+���, ,�%��-"/� �(',.&)-"(' �'� -.+'(/�+ -�1�,

0.2

.4.6

.8Sh

are

of in

com

e ta

xes (

1999

)

0 .2 .4 .6Share of trade taxes (1999)

High income in 2000 Mid income in 2000Low income in 2000 Fitted values

A. Country-level income and trade taxes by GDP

0.2

.4.6

.85

year

ave

rage

s of s

hare

of in

com

e ta

x

0 .2 .4 .65 year averages of share of trade tax

1900-39 1940-49 1950-691970-99 Fitted values

B. Global-level income and trade taxes by time period

Figure 4: Income taxes and trade taxes

similar with a very similar slope of the regression lines.

Figure 5 zooms in on the income tax, plotting the relationship between

the share of income taxes in total taxes and income per capita, in the current

cross section as well as the historical time series. The left panel separates

the observations into three groups by tax take: countries that raise more

than 25% of taxes in GDP, countries that raise 15-25% of taxes in GDP, and

countries that raise less than 15%. The countries in the high-tax group again

look markedly di�erent, raising much more of their tax revenues in the formof income taxes. The right panel again colors observations by time period.

A striking similarity between the historical situation of this sample of older

nations and the developing world today is again apparent.

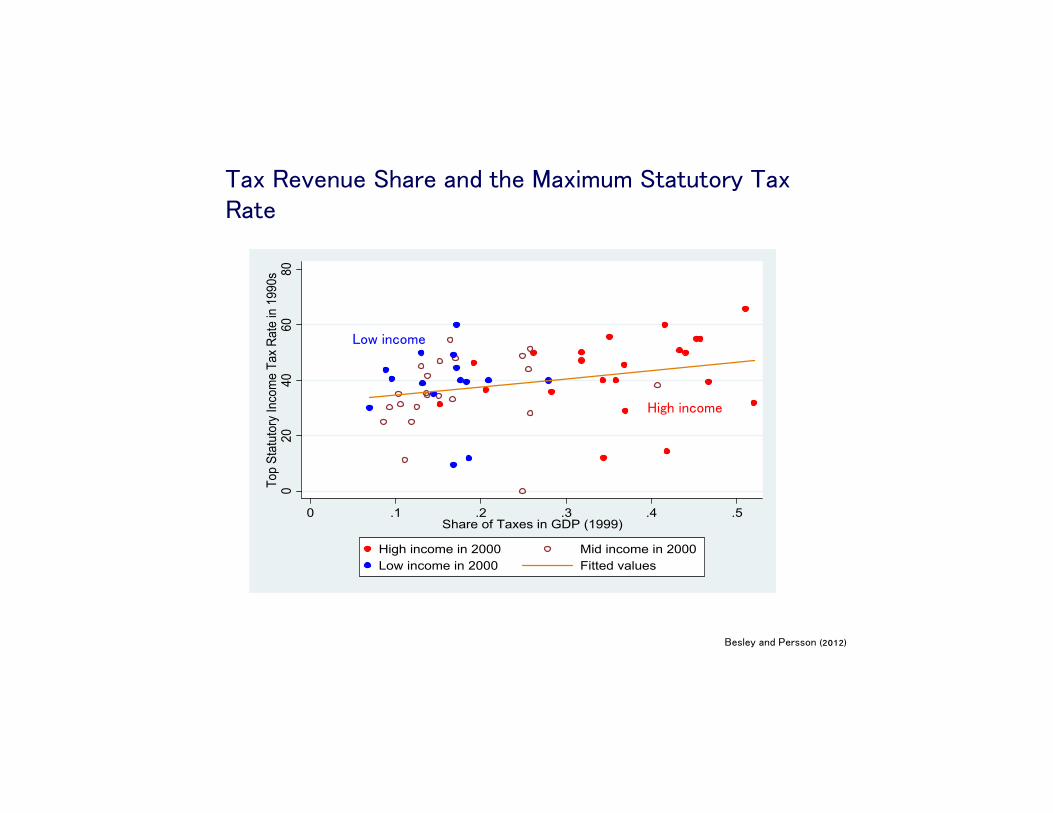

Finally, another indicator of fiscal capacity is the relation between statu-tory tax rates and actual tax take. Figure 6 shows some indication of this by

plotting the top statutory income tax rates in 1990s for the 67-country sam-

ple in Gordon and Lee (2005) against the share of total taxes in GDP from

Baunsgaard and Keen (2005) The figure shows that the distribution of thetop statutory rate is about the same amongst high-income and low-income

countries. Obviously, the figure does not take aspects such as coverage and

8

" !�+-"'�(&� �(.'-+"�, +�%2 &.�! &(+� (' "'�(&� -�1�, �, ())(,�� -( -+��� -�1�, -!�' �( )((+�+ �(.'-+"�,.

��,%�2 �'� ��+,,(' (2012)

��1�-"(' �'� �",��% ��)��"-2 "' ��/�%()"' �(.'-+"�,

1. (0 �",��% ��)��"-22. ��/2 +�%"�'�� (' '�++(0 (�",-(+-"('�+2) -�1�, �,

())(,�� �+(��-��,�� ("'�(&�) -�1�, q -+���, ,�%��-"/� �(',.&)-"(' �'� -.+'(/�+ -�1�,q �1)%�'�-"(' %"�, )�+-"�%%2 "' -�1 ��&"'",-+�-"('

3. � �(&)�%%"' +��,(' -!�- -!� �"���+�'�� "' -�1 ,!�+�, %"�, "' -�1 ��&"'",-+�-"(' (�, ())(,�� -( )(%"�2) �(&�, �+(& -!� +�%�-"(',!") ��-0��' -�1 +�-�, �'� -�1 +�-"(,

q �/�' 0"-! �(&)�+��%� ,-�-.-(+2 +�-�,, ��/�%()�� �(.'-+"�, +�",� &.�! &(+� +�/�'.� (�, � ,!�+� (� ���) -!�' ��/�%()"' �(.'-+"�,.

020

4060

80To

p St

atut

ory

Inco

me

Tax

Rate

in 1

990s

0 .1 .2 .3 .4 .5Share of Taxes in GDP (1999)

High income in 2000 Mid income in 2000Low income in 2000 Fitted values

Figure 6: Top statutory income tax rate and total tax take

progressivity into account. With this qualification, the fact that high-incomecountries raise much more tax revenue than low-income countries suggeststhat narrower tax bases driven by compliance di!culties are much biggerissues among low-income countries. This reinforces the earlier observationthat fiscal capacity is considerably less developed in poor countries.

Taken together, the cross-sectional and time series data suggest the fol-lowing five stylized facts confirmed in cross sectional and time series data:

Stylized Fact 1: Rich countries have made successive investments in theirfiscal capacities over time.

Stylized Fact 2: Rich countries collect a much larger share of their incomein taxes than do poor countries

Stylized Fact 3: Rich countries rely to a much larger extent on incometaxes as opposed to trade taxes than do poor countries.

Stylized Fact 4: High-tax countries rely to a much larger extent on incometaxes as opposed to trade taxes than do low-tax countries.

10

��1 ��/�'.� �!�+� �'� -!� ��1"&.& �-�-.-(+2 ��1 ��-�

" ! "'�(&�

(0 "'�(&�

��,%�2 �'� ��+,,(' (2012)

1. �(/�+'&�'- +�/�'.� ,!�+� "' ��� 0�, +","' (' �/�+� � -!+(. ! -!� 1990, �'� ��+%2 2000,q ��/��-,

q -�1 /,. (-!�+ ,(.+��, ('�-.+�% +�,(.+��,)

q � %(- (� /�+"��"%"-2 "' +�/�'.� �!�' �, ��+(,, �(.'-+"�,

q ,!"�-"' �(+-.'�, ��-�+ -!� 2008 �%(��% +���,,"('%

2. �!� �(&)(,"-"(' (� -�1�, !�, -"%-�� �0�2 �+(& -+��� -(0�+�, "'�"+��- -�1�,

��1�-"(' �'� �",��% ��)��"-2 "' ��+"��

5

7

9

11

13

15

17

19

21

2000 2001

2002 2003

2004 2005

2006 2007

2008 2009

2010 2011

2012 2013

Ghana Kenya Nigeria Sub-Saharan Africa (developing only)

���

�!�'�

��'2�

�" �+"�

�('��)-.�% �+�&�0(+$

q �+��"-"('�% %"-�+�-.+� (' -�1�-"('

q ��," ' (� ()-"&�% -�1

q ��&,�2 (1927): ()-"&�% �(',.&)-"(' -�1 '(- .'"�(+&

q ��1 ((�, ,.�! -!�- -!� &�+ "'�% +�/�'.� )�+ �(%%�+ ", �*.�% ��+(,, ((�,

q -�1 ((�, -!�- !�/� %(0 �%�,-"�"-2 (� ��&�'�/,.))%2 �- ����� +�-�,

q �(-� -!� �",-+"�.-"('�% "&)%"��-"(',

�)-"&�% '�(&� ��1

3 �(+'�+,-('�, (� ()-"&�% -�1 �+�&�0(+$ 5 '�"/"�.�% )+���+�'��,, �"+& -��!'(%( 2 �'� &�+$�-

,-+.�-.+�

6 ��/�'.� +�*."+�&�'- Ø �1( �'(.,: ,"&)%"�"�, (�#��-"/� �.'�-"('

7 �(�"�% 0�%��+� �.'�-"('

�(��+' �)-"&�% ��1 Ø �"�%��� "&)(+-�'- "'," !-, "'-( ��," ' (� -�1�,Ø �.- &(,- 0�+�/�+� (� %"&"-�� )+��-"��% +�%�/�'��

Ø �"++%��, (1971): &�+ "'�% -�1 +�-� (' +"�!�,- )�+,(' ", 3�+(

��1 �(&)%"�'��/�/�,"('

q �)-"&�% �/�,"(' ��)�'�, (' -�+&, (� �&�%� (%"$�%"!((� (� ��-��-"(' �'� )�'�%-2) �'� �--"-.�� -(0�+� +",$ (�%"' !�& � ��'�&( 1972)

q ��,�� (' ��('(&"� &(��% (� �+"&�

q � )�+,(' �(&&"-, � �+"&"'�% ��- "� -!� �1)��-�� .-"%"-2 -( !"& �1����, -!� .-"%"-2 !� �(.%� �- �2 .,"' !", -"&� �'� (-!�+ +�,(.+��, �- (-!�+ ��-"/"-"�,

q �+"&"'�%, -!�+��(+� �('’- !�/� � �"���+�'- ��,"� &(-"/�-"(', �+(& (-!�+,, �.- +�-!�+ !�/� �"���+�'-

��'��"-, �'� �(,-,.

��1 �(&)%"�'��/�/�,"(' q (0 &.�! ,!(.%� �� �%%(��-�� -( ��-��-"'

�/�,"('? (��'�&( 1981)

Ø �*.�-� +�,(.+�� �(,- (� ��-��-"(' �'� -!� ,(�"�% ��'��"- (' -!� &�+ "'

» ���"-"('�% +�/�'.� ", '(- '�- �"' -( ,(�"�-2

» ��'��"-,: ��"-! "' (/�+'&�'-

�)-"&�% ��1 �2,-�&, �'� -!� ���!'(%( 2 (� ��1 �(%%��-"('

• �%�&+(� (2013) "'�(+)(+�-�, -�1 ��&"'",-+�-"(' "'-( ()-"&�% -�1 �+�&�0(+$– �(+'�+,-('� '(0 -��!'(%( 2 (� -�1 �(%%��-"('

– ��,� (� ��&"'",-�+"' /�+"(., -�1�, !�, �+"-"��% "&)%"��-"(', �(+ -!� ()-"&�% ,-+.�-.+� (� -�1 ,2,-�&,.Ø &�+ "'�% +�,(.+�� �(,- '(0 ��)�'�, (' ��,� (�

�(%%��-"('

Ø �)-"&�% -�1 ,2,-�& �*.�-�, -!� &�+ "'�% �1��,, �.+��' -( &�+ "'�% ��&"'",-+�-"/� �(,-

Ø �1�&)%�: ���Ø �"���+�'-"�-�� +�-�, �'� �1�&)-"(', "&)(,� &�+ "'�%

��&"'",-+�-"/� �(,-,

�'�%2-"��% �))+(��!�,

1. �" -�"�-.+�, &��+( �))+(��!: -�1 ��)��"-2 �'� ���(+- [�-(�!�,-"� �+('-"�+ �'�%2,", – �' �(+� �'� �!%�'�.+ ! 2015]

2. �"�+( �))+(��!:

Ø ��," ' �'� �/�%.�-� ("'�+�&�'-�%) )(%"�2 "''(/�-"(', "' � 0(+%� (� 0��$ -�1 �'�(+��&�'-

Ø �(%%��(+�-� (+�,��+�!�+,/)(%"�2 &�$�+,/)+��-"-"('�+,)

�"�+( ��1 ��,��+�!

Ø ��-�: ��&"'",-+�-"/� ��-� )+(/"�� � 0��%-! (� "'�(+&�-"(' "' -�1 +��(+�,

Ø �&)"+"��% ��-!(�,: �(.%� .,� -�1 ,�!��.%�, (+ -�1 +��(+&,, )+�/"(., �!�' �, "' -�1 +�-�, �'� �'�(+��&�'- -( �+��"�%2 �,-"&�-� "&)��-,

Ø �+�&�0(+$: �.�%"� �"'�'�� !�, � 0�%%-��/�%()�� -!�(+2 -!�- ��' �� �+(. !- -( ���+ "' ��," '"' )(%"�2

Ø �(%"�2: �-+(' "'-�+�,- �+(& )(%"�2 &�$�+, "' �--"' -�1�, +" !-

�&)"+"��% '/�,-" �-"(', "' -( ��-�+&"'�'-, (� ��1 ��)��"-2

1. ��1 �(%"�2

2. ��1 ��&"'",-+�-"('

3. ��1 �(&)%"�'��

�. �'�(+��&�'-

�. �(+�%�

��0 �/"��'�� (' �(&)%"�'��

q �'�(+��&�'-

1. �!"+�-)�+-2 "'�(+&�-"('– �&)%(2�+ ��)(+-"' /�"-!!(%�"' (��'&�+$)– �"-"3�', �, &('"-(+, (�+�3"%/�!"%�)– ���(.'-"' �"+&, (�+. .�2)

2. ���!'(%( 2 – �%��-+('"� �"%%"' &��!"'�,- �0�'��/��'3�'"�

3. �,2�!(%( 2– &(+�% ,.�,"(' (�'"-�� �"' �(&)– ��1 ,�%"�'��

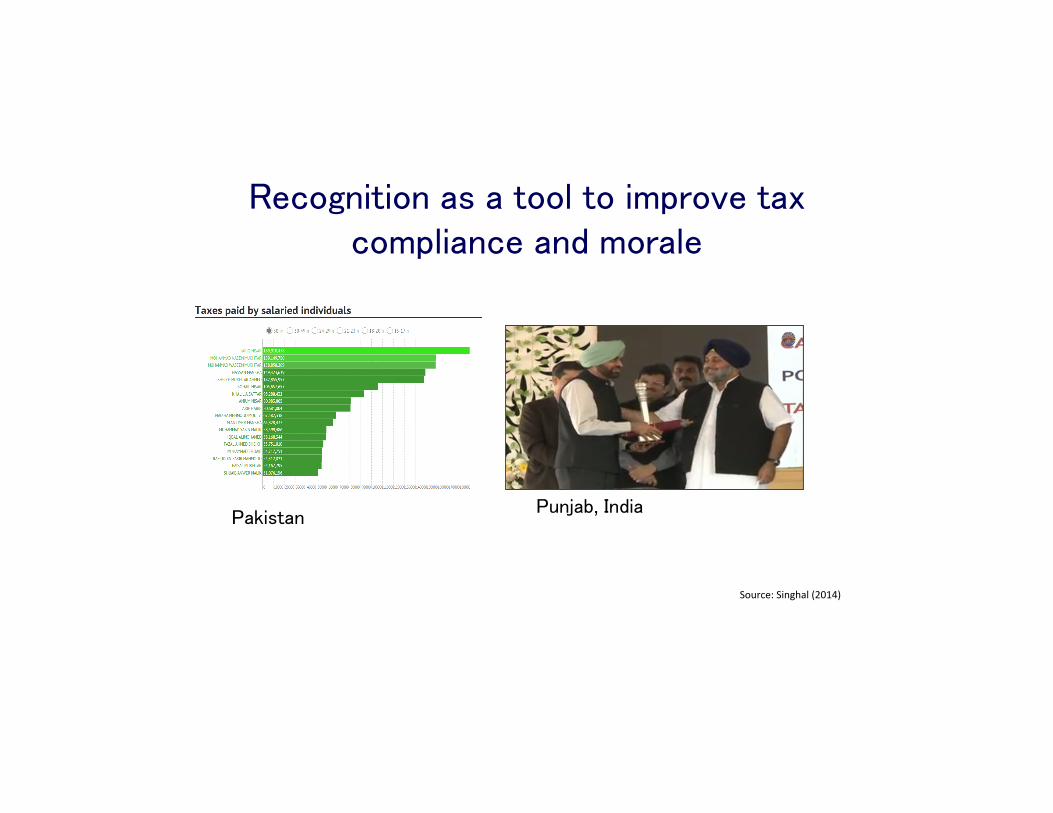

�!�&"' -�1 �(� �+, -( "&)+(/� �(&)%"�'��

�!�&"' - �!"%"))"'�,

“,"' "' �.'.�!,” – �"!�+, '�"�Source:Singhal(2014)

���( '"-"(' �, � -((% -( "&)+(/� -�1 �(&)%"�'�� �'� &(+�%�

�.'#��, '�"���$",-�'

Source:Singhal(2014)

��1 �'�(+��&�'-

�%�/�' ��. ��. (2009, 2011)

Ø ��'&�+$ �1)�+"&�'-: ��1 �/�,"(' +�-� ", �%(,� -( 3�+( �(+ "'�(&� ,.�#��- -( -!"+�-)�+-2 +�)(+-"' , �.- ,.�,-�'-"�% �(+ ,�%�-+�)(+-�� "'�(&�

Ø ��1 �'�(+��&�'- ", ,.���,,�.% "� �'� ('%2 "� /�+"�"��%� -!"+�-)�+-2 "'�(+&�-"(' !�, 0"�� �(/�+� �

��,�'- 0"�� �(/�+� � (� -!"+�-)�+-2 (+ (-!�+ "'�(+&�-"('Ø (0 ��' 0� �1)�'� -!"+�-)�+-2 "'�(+&�-"('?

Ø (0 ,!(.%� 0� ��," ' �.�"-,, ,�- )�'�%-"�,?

�!"+�-��+-2 ��)(+-"' : �/"��'�� �+(& ��'&�+$�(��1 -�$�: 50%)

Source: Kleven, Knudsen, Kreiner, Pedersen, Saez (2011) !

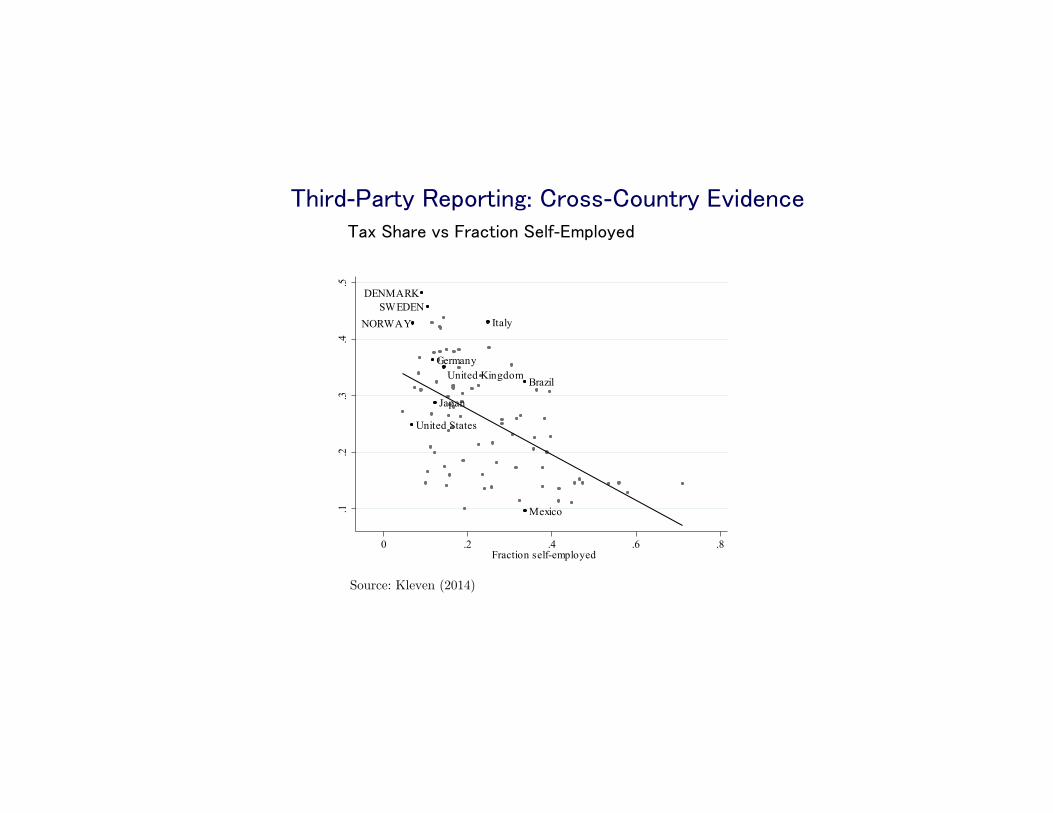

�!"+�-��+-2 ��)(+-"' : �+(,,-�(.'-+2 �/"��'����1 �!�+� /, �+��-"(' ��%�-�&)%(2��

Brazil

Germany

Italy

Japan

Mexico

United Kingdom

United States

DENMARK

NORWAYSWEDEN

.1.2

.3.4

.5

Tax

/ GD

P ra

tio

0 .2 .4 .6 .8Fraction self-employed

Source: Kleven (2014) !

���!'(%( 2 �'� ��1 �(&)%"�'��: �%��-+('"� �"%%"' ���!"'�, �'� ��� ��/�'.�,

�(%%��(+�-"(' 0"-! �0�'�� ��/�'.� �.-!(+"-2 (���)�&&��"�-� *.�,-"(': �!�- ", -!� "&)��- (� ���, ('

-�1 +�/�'.�?

�+(���+ *.�,-"(': (0 ��' -!� (/�+'&�'- �'�(.+� � �(&)%"�'��?

��-�

1. �.�+-�+%2 ��� ���%�+�-"(',, �+(& 2012 -!+(. ! 2014

2. 2. ��� +� ",-+�-"(' ��-�

��� ����")-

��� ��()-"('

��� ���!"'�, %�� -( !" !�+ ��� ��/�'.�,

��� +�/�'.�, "'�+��,�� �2 5.4%

�.-, -( ��--�+ .'��+,-�'� 0!�-’, .'��+%2"' -!", "&)��-, 0� ,�- .) � &2,-�+2-,!())�+ ,-.�2

Ø �( 0!�- �1-�'- �+� &��!"'�, ��"' .,��?

Ø ��' �(',.&�+, �'�(.+� � &(+� .,� �?

�2,-�+2 �!())�+ �-.�2: ��," '

q 129 /","-, -( ���-��-"/� +�-�"% ,!(), "' �" �%"q �.+�!�,�, �+(& � &�'. (� ,&�%% ((�,: -��, �(����, ,(�), ,-�)%�,, �-�., /�%.�� ��-0��' ��� 500–���1000.

q �' �&������ �1)�+"&�'-: "' (('%2) !�%� (� -!�,� /","-,, ,�%��-�� �- +�'�(&, 0� ,)��"�"��%%2 �,$�� �(+ � +���")-.

�2,-�+2 ,!())�+: ��,.%-,

1. �!�' .')+(&)-��, -!� �+��-"(' (� ).+�!�,�, +���"/"' ���, ", %(0, �- 4 21 )�+��'-.

2. ��+�%2 �,$"' �(+ � +���")- �!�' �, -!", ,.�,-�'-"�%%2: "'�+��,�, -!� �!�'��, (� +���"/"' � +���")- �2 42 )�+��'-� � )("'-, Ø ,.�,-�'-"�% ,�()� �(+ �(',.&�+, �, �.�"-(+,

3. �+�%"&"'�+2 +�,.%-, �+� ,. �,-"/� ��� ", ��"' )�+-"�%%2 )�,,�� -!+(. ! -( �(',.&�+,. Ø �,-"&�-�� "&)��- (' )+"�� ", ��� 111, �, � �"',- � &��' )+"�� (� ��� 1300 0"-!(.- +���")-,.

Ø �('��+': �(&)�-"-"/� �+"' �

�(,- (� ���+�,,"' �/�,"(' &�2 �� /�+2 %(0

– �(',.&�+, �, -�1 �.�"-(+, (��+"-(&" 2013) – �'-"--�1 �/�,"(' )+( +�& �+(& ��( ��.%(, �+�3"% - �(-� �",��% ��.%",-� - -!�- �+��-�� &('�-�+2 +�0�+�, �(+ �(',.&�+, -( �,$ �(+ +���")-,.

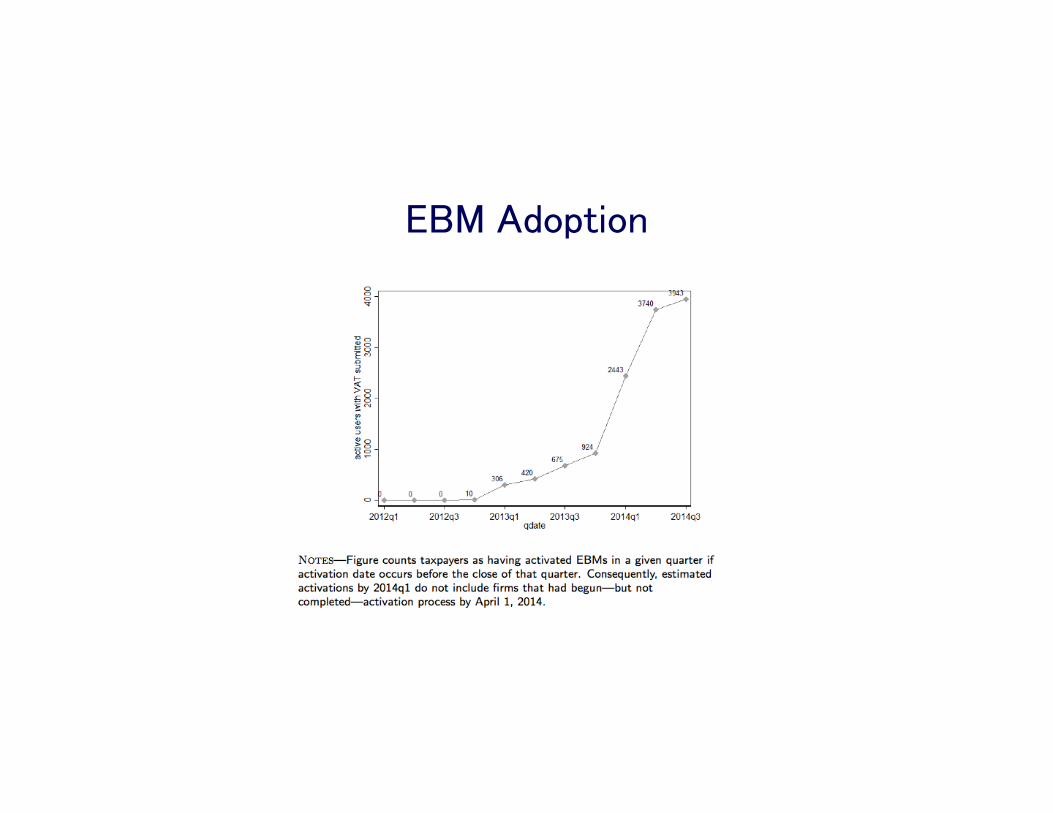

• ��,,"/� ��-�: 1 &"%%"(' �"+&,, 40 &"%%"(' )�()%�, �'� 2.7 �"%%"(' +���")-,!

– )+( +�& "'�+��,�� +�/�'.� +�)(+-�� "' +�-�"% ,��-(+, �2 &(+� -!�' 22% ((/�+ �(.+ 2��+ )�+"(�).• '( +�,"�.�% �����- (� �"+& �1"-, �'� �&)%(2&�'-

�(',.&�+ �--�'-"(' �'� )�+-"�")�-"('

39

Figure 2: Number of Receipts Reported Electronically to the Tax Authority – Timeline of Program Implementation

Notes: The figure shows the total number of receipts (millions of receipts) – with and without a SSN – electronically reported to the tax authority by month by establishments in Sao Paulo. The vertical lines highlight the key dates for the implementation of the NFP program. Between Oct.07 (Phase-in begins line) and May.08 (Phase-in ends line) 8 groups of sectors were phased-in in the policy of submitting receipts electronically to the tax authority. The possibility of inserting a SSN in the receipt for tax rebate purposes was introduced along with the electronic submission of receipts. The first lottery based on the purchases with SSN receipts was introduced in Dec.2008.

Figure 3: Consumer Participation

.

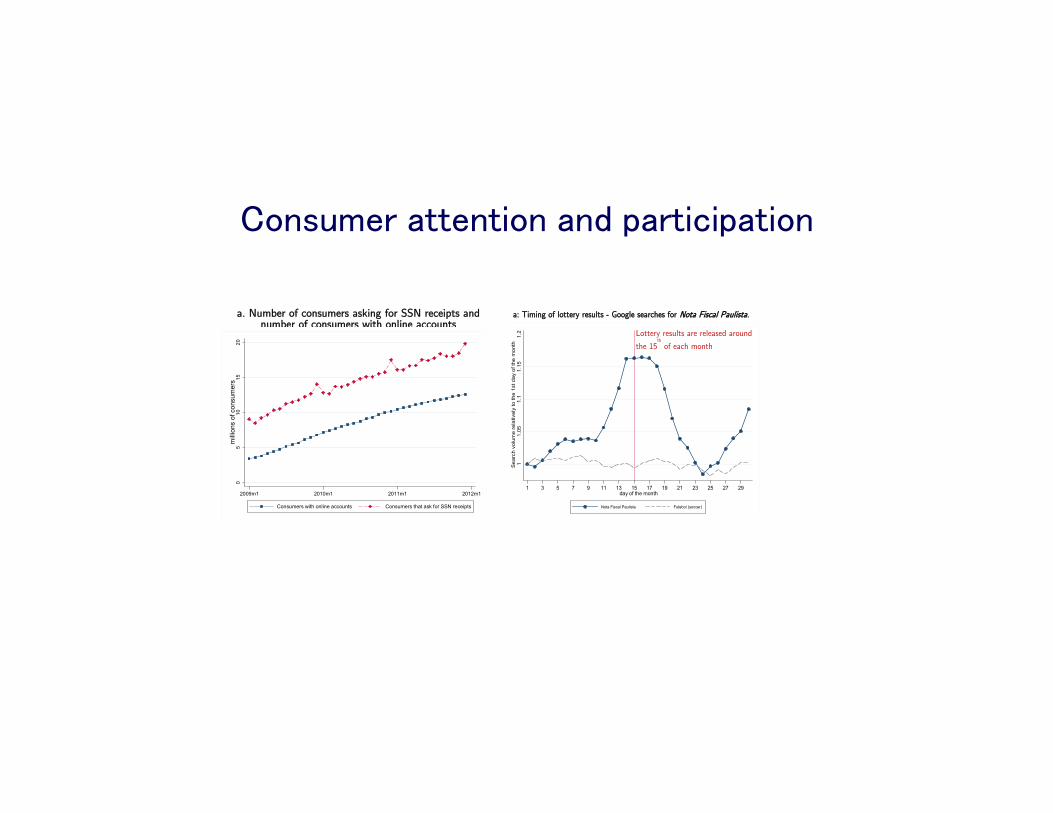

Notes: The dashed line in Figure 3a displays total number of consumers asking for SSN receipts each month, and the solid line is

the total number of consumers that had set up online account at the tax authority’s website between Jan. 2009 and Dec. 2011. Any person holding a Brazilian SSN is eligible to ask for receipts. In order to collect rewards and opt in for lotteries consumers need to enroll online. Figure 3b shows the average monthly expenditure by consumers with online accounts between Jan. 2009 and Dec. 2011. Monthly expenditure is the sum of the total value of SSN receipts by individual. The spikes of expenditure around December of each year follows the seasonal variation in consumption due to Christmas shopping.

Phase-in begins

Phase-in ends

first lottery

010

020

030

040

050

0m

illio

ns o

f rec

eipt

s

2007m1 2007m7 2008m1 2008m7 2009m1 2009m7 2010m1 2010m7 2011m1 2011m7

05

1015

20m

illio

ns o

f con

sum

ers

2009m1 2010m1 2011m1 2012m1

Consumers with online accounts Consumers that ask for SSN receipts20

030

040

050

060

0A

vera

ge m

onth

ly e

xpen

ditu

re in

US

$2009m1 2010m1 2011m1 2012m1

a. Number of consumers asking for SSN receipts and number of consumers with online accounts

b: Average expenditure in SSN receipts per month by consumers with online accounts.

40

Figure 4: Are Consumers Paying Attention to the Rewards Schedule?

a: Timing of lottery results - Google searches for Nota Fiscal Paulista.

b: Timing of tax rebate disbursements - Rewards requested for deposit in consumers’ bank accounts

Notes: Figure 4a displays the search volume from Google Trends website for Google searches with terms related to ”nfp” or ”nota fiscal paulista” or ”nota paulista” pooled by day of the month from IPs addresses in the state of Sao Paulo between Oct. 2007

and Dec. 2011. It also displays searches for “futebol” (soccer in Portuguese) pooled by day of the month from IPs addresses in the state of Sao Paulo for the same time period. The lottery results are released around the 15th of each month marked by the solid

vertical line. In Figure 4b each data point is the total amount in millions of US$ requested for direct deposit in consumer’s bank accounts. As described in section II.B, the tax authority does a biannual disbursement of the tax rebates: every April and October. The disbursement dates are marked by vertical lines in the x-axis.

11.

051.

11.

151.

2S

earc

h vo

lum

e re

lativ

ely

to th

e 1s

t day

of t

he m

onth

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29day of the month

Nota Fiscal Paulista Futebol (soccer)

020

4060

8010

0

Rew

ards

req

uest

ed fo

r ba

nk a

ccou

nt d

epos

its(m

illio

ns U

S$)

2009m4 2009m10 2010m4 2010m10 2011m4 2011m10

two annual disbursements of tax rebates: April and October

Lottery results are released around

the 15th

of each month

��)(+-�� ��/�'.� �!�' �,���-�"% /, �!(%�,�%�

41

Figure 5: Compliance Effect – Retail vs. Wholesale a. Raw data: reported revenue changes

b. Difference coefficients for 6-month time bins - Log reported revenue by sector

Notes: Figure 5a shows reported revenue changes for retail and wholesale sectors. Each line is defined by the reported revenue by all establishments aggregated by retail or wholesale scaled by the average monthly reported revenue in 2004 for each sector group. The figure plots the raw data, so there are spikes around December of each year follows the seasonal variation in consumption due to Christmas shopping. The vertical lines highlight the key dates for the implementation of the NFP program: phase-in of sectors begins in Oct.07 and ends in May.08, and the first lottery based on the purchases with SSN receipts was introduced in Dec.2008. Figure 5b plots regression coefficients from estimating specification (1) using a sample of 210 sectors between Jan 2004 and Dec 2011. The sector sample has 24,990 observations. The difference in differences (DD) coefficient displayed in the figure is estimated using the specification (2) where the DD variable is defined by the interaction between a dummy for retail sectors and a dummy that equals 1 for time periods after Oct 2007. Standard errors are clustered by sector.

0.5

11.

52

2.5

3

2005m1 2005m11 2006m9 2007m7 2008m5 2009m3 2010m1 2010m11 2011m9

Retail Wholesale

16.8

1717

.217

.417

.6D

iffer

ence

in L

og R

epor

ted

Rev

enue

Jan

.04-

Mar

.04

Apr

.04-

Sep

.04

Oct

.04-

Mar

.05

Apr

.05-

Sep

.05

Oct

.05-

Mar

.06

Apr

.06-

Sep

.06

Oct

.06-

Mar

.07

Apr

.07-

Sep

.07

Oct

.07-

Mar

.08

Apr

.08-

Sep

.08

Oct

.08-

Mar

.09

Apr

.09-

Sep

.09

Oct

.19-

Mar

.10

Apr

.10-

Sep

.10

Oct

.10-

Mar

.11

Apr

.11-

Sep

.11

Oct

.11-

Dec

.11

DD coef. = 0.22*** [0.042]

�(,- (� ���+�,,"' �/�,"(' &�2 �� /�+2 %(0

– �'"-�� �"' �(&• �--�+, �+(& ��� (�%%,0(+-! �-.�% 2014)

• !--),://000. (/..$/ (/�+'&�'-/'�0,/!&+�-,��.+�,-+��(+�--�1-+�/�'.�,-�2-�+��$"' -�(0'-('--�1-�(� �+,

��1 �(%"�2

�+��"-"('�% +��(&&�'��-"(', �+(& -!� -�1 -!�(+2 %"-�+�-.+�:

Ø �,� )+( +�,,"/� "'�(&� -�1�, �'� ���

Ø �( '(- .,� �"���+�'-"�-�� �(',.&)-"(' -�1�,, ��)"-�% -�1�,, �'� -�1�, (' -.+'(/�+, -+���, �'� "'-�+&��"�-� ((�,

�!�,� -!�(+�-"��% +�,.%-, �'�+�%%2 �,,.&�:

Ø ��+���- -�1 �'�(+��&�'- (��&"'",-+�-"(' �(,-%�,,)

Ø �.%% ,�- (� -�1 "',-+.&�'-, �/�"%��%� -( )(%"�2 &�$�+,

�)-"&�% ��1 �(%"�"�,

�"�&('�-�"++%��, (1971): �,,.&"' )�+���- �'�(+��&�'-, ('%2 )+(�.�-"(' ���"�"�'- -�1 "',-+.&�'-, ,!(.%� �� .,��

�+(�.�-"(' "'���"�"�'- -�1 )(%"�2 "' ��/�%()"' �(.'-+"�, .�"*."-(.,:

Ø �"'"&.& ��1 ��!�&�, (���) 0!�+��2 �"+&, �+� -�1�� (' �"-!�+ )+(�"-, (+ -.+'(/�+ ��)�'�"' (' 0!"�! -�1 %"��"%"-2 ", %�+ �+

�.+'(/�+ -�1�, �+� )+(�.�-"(' "'���"�"�'-, �.- &�2�� !�+��+ -( �/���?

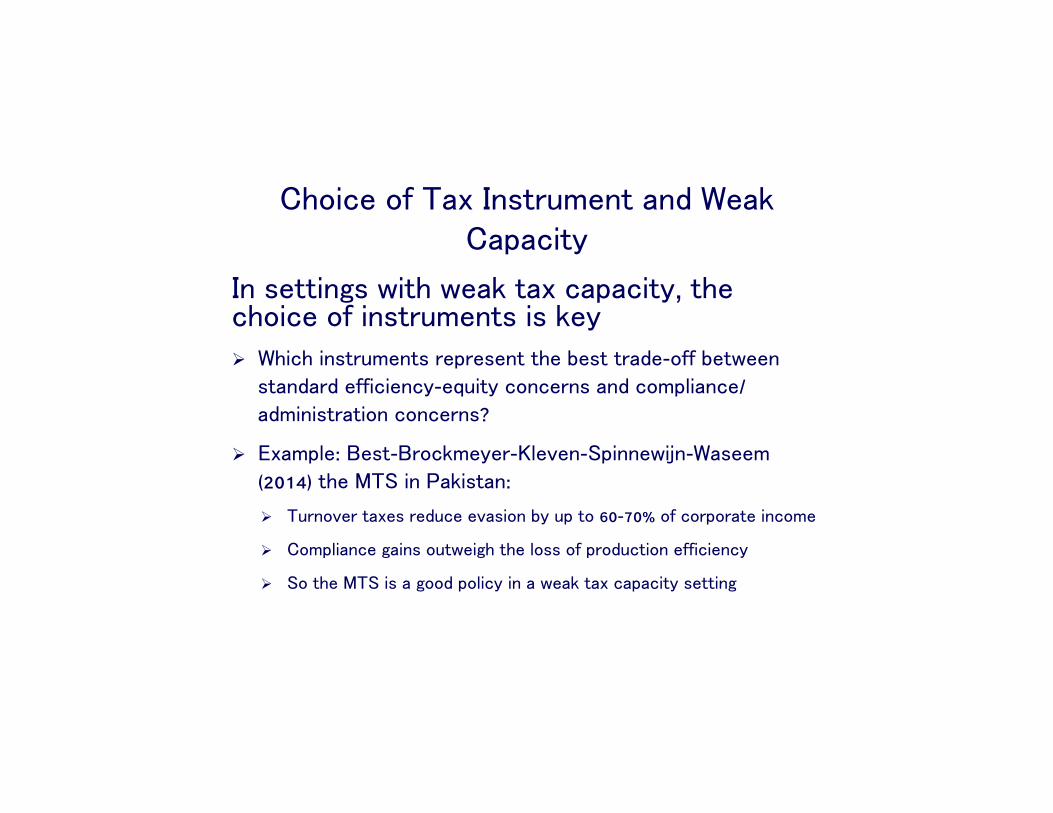

�!("�� (� ��1 ',-+.&�'- �'� ���$ ��)��"-2

' ,�--"' , 0"-! 0��$ -�1 ��)��"-2, -!� �!("�� (� "',-+.&�'-, ", $�2Ø �!"�! "',-+.&�'-, +�)+�,�'- -!� ��,- -+���-(�� ��-0��'

,-�'��+� ���"�"�'�2-�*."-2 �('��+', �'� �(&)%"�'��/��&"'",-+�-"(' �('��+',?

Ø �1�&)%�: ��,--�+(�$&�2�+-�%�/�'-�)"''�0"#'-��,��& (2014) -!� ��� "' ��$",-�':

Ø �.+'(/�+ -�1�, +��.�� �/�,"(' �2 .) -( 60-70% (� �(+)(+�-� "'�(&�

Ø �(&)%"�'�� �"', (.-0�" ! -!� %(,, (� )+(�.�-"(' ���"�"�'�2

Ø �( -!� ��� ", � ((� )(%"�2 "' � 0��$ -�1 ��)��"-2 ,�--"'

��2 �,,(',

1. �!"+�-)�+-2 "'�(+&�-"('

– 0"-!!(%�"' ("'�(&�) – -��!'(%( 2 (���)• �(',.&�+,

2. ��%"�'�� �'� �+�&"' – �(+�%�: '(+&, �'� �.,"'�,, -�1 (��' %���,!)– ��,,� "'

��2 ��$��0�2, Ø ��-!�+ -!�' +�%2 (' -+�',)%�'-"' ��/�%()�� �(.'-+2

,(%.-"(',, 0� �1�&"'� �(.'-+2-,)��"�"� )(%"�"�,

Ø �!�%%�' "' �.- �(��%�:

- ��-�: " !-*.�%"-2 ��-� [�. . ��&"'",-+�-"/� ��-�]

- ��," ': �+��"�%� +�,��+�! ��," ' [���,, *.�,"-�1)�+"&�'-,]

- �/�%.�-"(': �" (+(., �/�%.�-"(' -��!'"*.�,

- �(%%��(+�-"(': �' � �&�'- ��-0��' )(%"�2 &�$�+, �'� +�,��+�!�+,

��+- ��",��% ����+�%",& �'� �*."-��%�

��/�%()&�'-

�!�- ", �",��% ����+�%",&?

v �-�+- 0"-! � �(&&(' ���"'"-"(' (� � ����+�% ,2,-�&

v � ).�%"� ,��-(+ 0"-! �(-! ��'-+�%"3�� �'� ����'-+�%"3�� %�/�%, (� ���","('-&�$"' "' 0!"�! �!("��, &��� �- ���! %�/�% �+� ��-�+&"'�� �2 -!� ��&�'�, (� +�,"��'-, (� +�,)��-"/� #.+",�"�-"(', (��-�, 1972)

v �(-�: -!", 0"%% �%,( �� )(%"-"��% (%(��% �%��-"(',) (+ ��&"'",-+�-"/� ().�%"� ,�+/�'- ,�%��-"(', )�2, 0(+$ �('�"-"(',)

v ��,"� )+"'�")%� (� �",��% ����'-+�%"3�-"(': -!� )+(/","(' (� ).�%"� ,�+/"��, ,!(.%� �� �- -!� %(0�,- %�/�% (� (/�+'&�'- -!�- "'-�+'�%"3�, -!� (,)�-"�%) ��'��"-, �'� �(,-,

&)%�&�'-�-"(' ",,.�,: �",��% ����+�%",& �'� ����'-+�%"3�-"('

v �",��% ����'-+�%"3�-"(' ", -!� -+�',��+ (� �('-+(% (/�+ �1)�'�"-.+�, � � +�/�'.�, �+(& -!� ��'-�+ -( %(0�+ %�/�%, (� (/�+'&�'-

– �1)�'�"-.+�: ,�+/"�� ��%"/�+2 – !��%-!��+�, ��.��-"(', ,(&� "'�+�,-+.�-.+�

– ��/�'.�,: "'�+��,� -+�',)�+�'�2 �'� ,-��"%"-2 (� -+�',��+,, -+�',��+ )(0�+ -( �(%%��- �'� ,�- -�1�,

v �'�%2,", (� -!� "&)��- (� �",��% ����+�%",& &.,- ���(.'- �(+ )(%"-"��% �'� ��&"'",-+�-"/� ,-+.�-.+�,

�-!�+ �"&�',"(', (� ����'-+�%"3�-"('

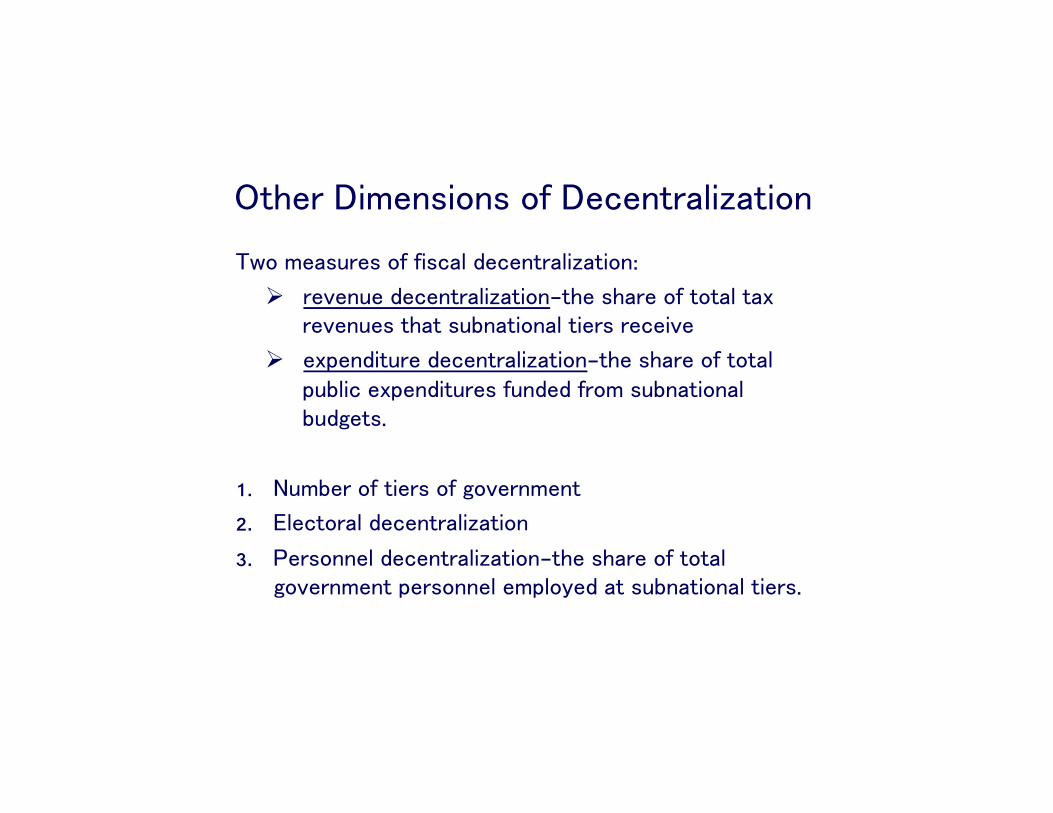

�0( &��,.+�, (� �",��% ����'-+�%"3�-"(':

Ø +�/�'.� ����'-+�%"3�-"('—-!� ,!�+� (� -(-�% -�1 +�/�'.�, -!�- ,.�'�-"('�% -"�+, +���"/�

Ø �1)�'�"-.+� ����'-+�%"3�-"('—-!� ,!�+� (� -(-�% ).�%"� �1)�'�"-.+�, �.'��� �+(& ,.�'�-"('�% �.� �-,.

1. �.&��+ (� -"�+, (� (/�+'&�'-

2. �%��-(+�% ����'-+�%"3�-"('

3. ��+,(''�% ����'-+�%"3�-"('—-!� ,!�+� (� -(-�% (/�+'&�'- )�+,(''�% �&)%(2�� �- ,.�'�-"('�% -"�+,.

14

4Table 6.1 Median Levels of Decentralization Measures by Geographic Region, 1995 (percentage)

Decentralization Number of Sub-Saharan Latin Middle Eastern Former WesternMeasure Observations Africa East Asia South Asia America East Europe Soviet Union Europe

Number of tiers 164 4 4 4 3 3.5 3 4 3Percent elected 155 33.3 35.4 33.3 62.5 0.0 83.3 33.3 69.0Subnational share

of publicexpenditure 67 4.7 10.8 37.6 9.6 8.4 16.9 27.6 24.1

Subnational shareof total taxrevenue 53 4.0 6.5 N/A 6.7 6.3 7.3 24.2 13.4

Subnational shareof publicemployment 90 23.1 41.0 50.0 20.8 35.8 26.4 35.4 48.4

Stipulatedautonomy 133 6.9 11.8 20.0 23.5 0.0 8.3 15.4 33.0

Residual authority 133 3.8 5.9 20.0 22.2 0.0 16.7 7.7 23.8Federal 164 4.8 5.2 28.6 14.8 5.3 9.1 7.1 23.8

Sources: Daniel Treisman, Defining and Measuring Decentralization: A Global Perspective (Los Angeles: University of California, 2002);D. Elazar, Federal Systems of the World: A Handbook of Federal, Confederal and Autonomy Arrangements, 2nd ed. (London: Longman, 1994);S. Saideman, D. Lanoue, M. Campenni, and S. Stanton, “Democratization, Political Institutions, and Ethnic Conflict: A Pooled Time-SeriesAnalysis, 1985–1998,” Comparative Political Studies 35 (1) (2002): 103–129.

07_Connerley_Ch6.qxd 4/19/10 3:21 PM Page 144

�"&�',"(', (� ����+�%",&

' )+��-"��, -+�&�'�(., �+(,,-'�-"('�% /�+"�-"(' "' !(0 ����'-+�%"3�-"(' � �����

1. � �'�� – �1)�',"/� ����'-+�%"3�-"(' ��+(,, �%% �"&�',"(', "' -!� 1990,, �(&)+(&",�� �2 0��$ (0'-,(.+�� +�/�'.�,, ,�+/"�� ��%"/�+2, �",��% +�,)(',"�"%"-2

2. ��&�(�"� – �(&&.'�% �%��-"(',, %"--%� "'��)�'��'- +�/�'.� �('-+(%, !��/2 +�%"�'�� (' "'-�+ (/�+'&�'-�% -+�',��+,

3. �!"%� – )(%"-"��% ����'-+�%"3�-"(' �.- ��'-+�%"3�� +�/�'.�,

4. �(%"/"� – +�/�'.� ,!�+"' 0"-! &.'"�")�%"-"�, (+.%� ��,��) �.- ��'-+�%"3�� ��&"'",-+�-"('

�(�%,: -( 0!�- �'�?

1. �.�%"� ,�+/"�� ��%"/�+2/��('(&"� +(0-! ('�"�)2. ��&(�+�-"3�-"('3. �-��"%"-2 (�(%.&�"�/��&�(�"�)

�(%(&�"� – ����'-+�%"3�-"(' ,��' �, � 0�2 -( +��,-��%",! ,-��"%"-2 �'� )��"�2 +���% "',.+ �'�2

v �(%"-"��% – &�2(+�% �'� .��+'�-(+"�% �%��-"(',v �",��% – -+�',��++�� "&)(+-�'- �",��% +�/�'.�,

��&�(�"� – +�,-(+� �"-"3�' -+.,- "' (/�+'&�'- ��-�+ �+&�� �1-�'��� �+&�� �('�%"�-

v �",�+�-"('�+2 "'-�+ (/�+'&�'-�% -+�',��+, �%%(��-�� .,"' ������� �(+&.%�

v ��+/"��, )+"(+"-"3�� -!+(. ! %(��% )�+-"�")�-"('

��,"� -!�(+2v �+��"-"('�% -!�(+2 (� �",��% ����+�%",& )+(/"��, � �'�+�% ������� �+�&�0(+$ �(+ �,," '"' �.'�-"(', -( �"���+�'- %�/�%, (� (/�+'&�'- �'� �(+ -!� �))+()+"�-� �",��% "',-+.&�'-, +�*."+�� (�., +�/� 1959; ��-�, 1972, 1999)

v ��'-+�% (/�+'&�'- +�,)(',"�"%"-2

v ��+-�"' "'�-"('�%" ).�%"� ((�, %"$� '�-"('�% ����',�

v "'�(&� +��",-+"�.-"('

v ����'-+�%"3�� %�/�%, (� (/�+'&�'- )+(/"�� (%(��%) ((�, �'� ,�+/"��, -!�- &�-�! +�,"��'-,’ )+���+�'��,v .'�/�' ����'-+�%"3�� )+(/","(' ��,"+��%� �, "- "&)+(/�, ��('(&"�

0�%��+� (+�%�-"/� -( .'"�(+& %�/�%, (� ,.�! ,�+/"��,)

�",��% ',-+.&�'-, "' � ����+�% �2,-�&

v �+"&�+2 ,(.+��, (� (/�+'&�'- �"'�'�� �+� -�1 (�'� ���-) "',-+.&�'-,

– �.�,-"(' "' -!� �('-�1- (� ����+�% ,2,-�&: 0!"�! -�1�, �+� ��,- ,."-�� �(+ .,� �- ���! %�/�% (� (/�+'&�'- (-�1-�,," '&�'- )+(�%�&)?

– '��� -( �",-"' .",! ��-0��' ��&"'",-+�-"(' (�(%%��-"(') �'� )(%"�2 (,�--"' -�1 +�-�,, �'� -�1 ��,�)

v (0�+ %�/�%, (� (/�+'&�'-, !�/� �' ���"-"('�% ,(.+��: "'-�+ (/�+'&�'-�% +�'-,

��1�-"(' "' ����+�% �2,-�&

• ' -!� �('-�1- (� -�1�-"(', -!� $�2 ",,.� "' -!� ��," ' (� -�1�, ", -!� �� +�� (� &(�"%"-2 (� -�1�� .'"-, (0(+$�+,, �"+&, �-�.) �- -!� ��'-+�% �'� %(0�+ %�/�%,

– �(�"%� .'"-, ��' �/("� -!� -�1 �2 +�%(��-"' -( %(0�+ -�1 #.+",�"�-"('

• ��'�+�% �('�%.,"(': %(0�+ %�/�%, (� (/�+'&�'- ,!(.%� �/("� -�1"' &(�"%� .'"-, – �� -!�2 )�()%�, �"+&, (+ ((�,. – ��1"' -!�,� .'"-, �+��-�, � 0�%��+� %(,, �, -!�2 ��' �/("� -!� -�1

�2 �!�' "' %(��-"('

�.+",�"�-"('�% �(.'��+"�,

• �!�- ,!(.%� -!� �( +�)!"� �(.'��+"�, ��?

• ��2 ",,.�: �)"%%(/�+,, �2 0!"�! 0� &��' -!� ���+.�% (� ��'��"-, �+(& �'2 ('� #.+",�"�-"('’, ).�%"� ((�, -( "-’, '�" !�(+,. – "'�+��,� -!� ()-"&�% ,"3� (� � #.+",�"�-"('– '-+(�.��, !�-�+( '(., )+���+�'��, �'� +��.��, ��('(&"�

0�%��+�.

• �1",-"' �(.'��+"�, %�+ �%2 !",-(+"��%%2 �'� �.%-.+�%%2 ��-�+&"'��– �(.-! �.��', ��-� ���$ -( -!� &"��%� (� -!� 20-! ��'-.+2

(�(!',(' 2015)– �'"-�� �-�-�,: +"/�+, 0�+� .,�� -( ��&�+��-� �(.'��+"�,.

�.+",�"�-"('�% �(.'��+"�,

• �+ .��%2 � &.�! &(+� +�-"('�% &�) 0(.%� )+(���%2 �'-�"%

1. ,(&� ��"+%2 ,"3���%� +� "('�% (/�+'&�'-, -!�- �1-�'� (/�+ �'/"+('&�'-�% +�,(.+��,

2. ,&�%%�+ %(��% (/�+'&�'-, -!�- �%%(0 +(.), (� +�,"��'-, -( ��-�+&"'� ,�+/"��, (� +�%�/�'�� &�"'%2 -( -!�&,�%/�, (��-�, 1999)

�",��% ����+�%",& "' �(.-! �.��': ��2 ,,.�,

1. �-!'"�"-2 �"/�+,"-2

2. '-�+'�%/�+&�� �('�%"�-

3. '�*."-"�, ��+(,, #.+",�"�-"(', (,-�-�,, �(.'-"�,,..)

v �-!'"� �"/�+,"-2:v �/"��'�� ", (/�+0!�%&"' -!�- �-!'"� �"/�+,"-2 %(0�+, ).�%"� ((�,

1. �"�+(�+��"- %(�' ����.%- +�-�, "' ��+. (��+%�', 2002)

2. �.'�"' �(+ )+(�.�-"/� ).�%"� ((�,—��.��-"(', +(��,, ,�0�+, �-�. "' -!� �'"-�� �-�-�, (�%�,"'�, ��*"+ �'� ��,-�+%2, 1999)

3. )+"&�+2 ,�!((% �.'�"' –���"%"-"�,, &�"'-�'�'�� "' +.+�% ��'2� (�" .�% �'� �. �+-2 2004)

�/�+%�): (��% �(/�+'�'�� �'"-, �'� �-!'"� �",-+"�.-"('

�&)"+"��% ��,-

v �!�- ", -!� +�%�-"(',!") ��-0��' ).�%"� ,�+/"�� )+(/","(' �'� -!� �-!'"� �(&)(,"-"(' �- -!� �(.'-2 %�/�%?

v (0 �(�, %(��% ).�%"� ,�+/"�� )+(/","(' �"���+ ��+(,, �(.'-"�,/)�2�&,/�(&�, 0"-! �"���+�'- �-!'"� �(&)(,"-"('?

v �-!�+ ���-(+, &�--�+: )�+-��)"-� "'�(&�, '�-.+�% +�,(.+�� ��,�, � � �",-+"�.-"(', �-�,…

• ,,.� ", -!� %��$ (� ��-�

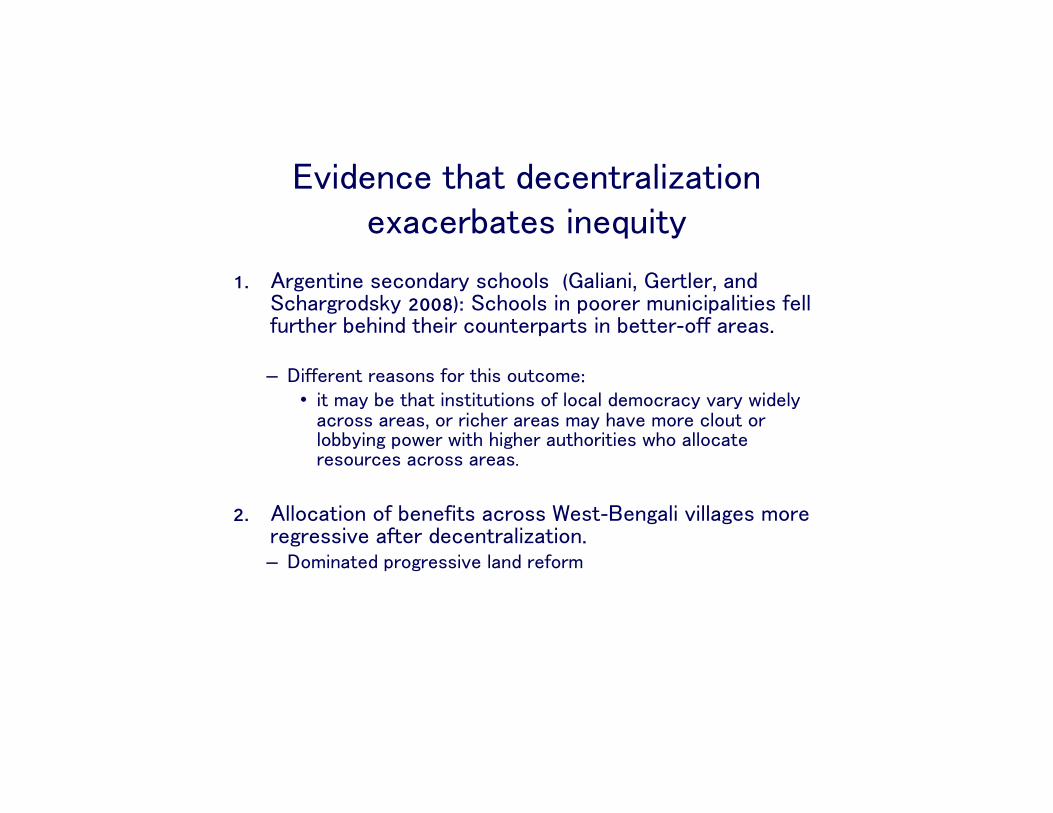

�/"��'�� -!�- ����'-+�%"3�-"(' �1���+��-�, "'�*."-2

1. �+ �'-"'� ,��('��+2 ,�!((%, (��%"�'", ��+-%�+, �'� ��!�+ +(�,$2 2008): ��!((%, "' )((+�+ &.'"�")�%"-"�, ��%% �.+-!�+ ��!"'� -!�"+ �(.'-�+)�+-, "' ��--�+-(�� �+��,.

– �"���+�'- +��,(', �(+ -!", (.-�(&�: • "- &�2 �� -!�- "',-"-.-"(', (� %(��% ��&(�+��2 /�+2 0"��%2 ��+(,, �+��,, (+ +"�!�+ �+��, &�2 !�/� &(+� �%(.- (+ %(��2"' )(0�+ 0"-! !" !�+ �.-!(+"-"�, 0!( �%%(��-� +�,(.+��, ��+(,, �+��,.

2. �%%(��-"(' (� ��'��"-, ��+(,, ��,--��' �%" /"%%� �, &(+� +� +�,,"/� ��-�+ ����'-+�%"3�-"('. – �(&"'�-�� )+( +�,,"/� %�'� +��(+&

��.��-"('�% +�,(.+��, /�+2 ��+(,, ,-�-�, �'� ��+(,, �(.'-"�, 0"-!"' ,-�-�,

��.��-"('�% +�,(.+��, /�+2 ��+(,, ,-�-�, �'� ��+(,, �(.'-"�, 0"-!"' ,-�-�,

�+�-�1",-"' "'�*."-"�, '('--+"/"�% "' �(.-! �.��': )(/�+-2 �'� ��.%- %"-�+��2 +�-�,

��+(,, ,-�-�,

,,.�, "' -!� ��," ' (� '-�+ (/�+'&�'-�% �+�'-,

1. �� +�� (� +��",-+"�.-"(' 1. �%(�$ +�'-, /, &�-�!"' +�'-,2. �",-�'�� &��,.+�,

2. �('�"-"('�% /, .'�('�"-"('�%

3. �",��% �",�")%"'�- )�+/�+,� "'��'-"/�, �(+ �",��% ��!�/"(+ - (0'-,(.+�� +�/�'.�, /,. “�+��” &('�2

���",-+"�.-"(' �((%,• ���",-+"�.-"(' -( (��,�- "'�*."-"�, ����'-+�%"3�� ,2,-�&

1. �%(�$ +�'-, • �.+� "'�(&� �����- �- -!� %(��% %�/�%• �%2)�)�+ �����- – �(�, %(��% ,)�'�"' +",� �2 -!� ,�&� �&(.'- (� -!� -+�',��+? �( %(��% �.-!(+"-"�, +��.�� -�1 �.+��',?

2. ��-�!"' +�'-,• �+"�� �'� "'�(&� �����-, �- -!� %(��% %�/�% • '��'-"/"3�, ).�%"� ,�+/"�� )+(/","(' (' -!� &�+ "'• �-+(' �+ �",��% �",�")%"'� (?)

���",-+"�.-"(' �((%,

• �(',"��+�-"(',1. �('�"-"('�%"-2

• (0 &.�! �",�+�-"(' ,!(.%� %�(�% �.-!(+"-"�, !�/�?

2. �+"-�+"� • �().%�-"(': -+�',��+, ��,�� (' #.+",�"�-"(', ,!�+� (�

)().%�-"('

• '�(&� )�+ ��)"-�

• �(�"�% 0�%��+� (.-�(&�,: ��.��-"(', !��%-!, )(/�+-2