Substantiating an ABIL Deduction: An Analysis of the Key ... · Depuis plus de 25 ans, les...

48

canadian tax journal / revue fiscale canadienne (2010) vol. 58, n o 2, 229 - 76 229 Substantiating an ABIL Deduction: An Analysis of the Key Elements Maureen Donnelly and Allister Young* PRÉCIS Depuis plus de 25 ans, les contribuables canadiens contestent en appel les nouvelles cotisations établies en matière de perte déductible au titre d’un placement d’entreprise (PDTPE). La PDTPE est considérée comme l’une des matières du droit fiscal où les contestations et les litiges abondent et sur lequel l’incertitude pèse. Les contribuables qui font appel échouent deux fois plus souvent qu’ils ne réussissent. En 2001, le jugement rendu par la Cour canadienne de l’impôt dans l’affaire Gamus a permis d’y apporter quelques explications. En faisant allusion au nombre de dispositions techniques complexes qui entrent en ligne de compte lorsque les contribuables déduisent une PDTPE, le juge Bowman a relevé quatre éléments qui doivent converger pour que l’appelant obtienne gain de cause. Le présent article expose les résultats de l’analyse par les auteurs de ces quatre éléments essentiels dans les 240 affaires judiciaires rapportées qui forment la jurisprudence au Canada en matière de PDTPE. Pour chacun de ces éléments, une liste de questions supplémentaires est fournie pour aider les contribuables et leur conseiller à préparer leur dossier dans une affaire portant sur la PDTPE, ainsi qu’une revue des nombreuses affaires pertinentes. Deux autres outils sont offerts en annexe à l’article : un tableau qui présente les jugements de l’étude en fonction de la question abordée et de l’issue de l’instance ainsi qu’un organigramme qui illustre les questions qui, selon chaque situation de fait particulière, pourront nécessiter une réponse adéquate dans l’éventualité d’une contestation en matière de PDTPE. Même si le présent article n’offre aucune solution miracle ni aucune formule scientifique pour garantir la réussite des contribuables, les auteurs souhaitent tout de même aider les contribuables et leurs conseillers à réduire l’incertitude entourant cette matière complexe du contentieux fiscal. ABSTRACT For more than 25 years, Canadian taxpayers have been appealing reassessments of allowable business investment loss (ABIL) deductions. The ABIL is considered to be one of the most widely contested and frequently litigated areas in tax law, and one infused with uncertainty. Taxpayers’ appeals fail almost twice as often as they succeed. In 2001, some light was shed when the Tax Court of Canada issued its decision in the Gamus case. * Of the Faculty of Business, Brock University, St. Catharines, ON (e-mail: [email protected] and [email protected]). The authors are grateful for the comments provided by Alan Macnaughton and an anonymous reviewer.

Transcript of Substantiating an ABIL Deduction: An Analysis of the Key ... · Depuis plus de 25 ans, les...

canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2, 229 - 76

229

Substantiating an ABIL Deduction: An Analysis of the Key Elements

Maureen Donnelly and Allister Young*

P R É C I S

Depuis plus de 25 ans, les contribuables canadiens contestent en appel les nouvelles cotisations établies en matière de perte déductible au titre d’un placement d’entreprise (PDTPE). La PDTPE est considérée comme l’une des matières du droit fiscal où les contestations et les litiges abondent et sur lequel l’incertitude pèse. Les contribuables qui font appel échouent deux fois plus souvent qu’ils ne réussissent. En 2001, le jugement rendu par la Cour canadienne de l’impôt dans l’affaire Gamus a permis d’y apporter quelques explications. En faisant allusion au nombre de dispositions techniques complexes qui entrent en ligne de compte lorsque les contribuables déduisent une PDTPE, le juge Bowman a relevé quatre éléments qui doivent converger pour que l’appelant obtienne gain de cause. Le présent article expose les résultats de l’analyse par les auteurs de ces quatre éléments essentiels dans les 240 affaires judiciaires rapportées qui forment la jurisprudence au Canada en matière de PDTPE. Pour chacun de ces éléments, une liste de questions supplémentaires est fournie pour aider les contribuables et leur conseiller à préparer leur dossier dans une affaire portant sur la PDTPE, ainsi qu’une revue des nombreuses affaires pertinentes. Deux autres outils sont offerts en annexe à l’article : un tableau qui présente les jugements de l’étude en fonction de la question abordée et de l’issue de l’instance ainsi qu’un organigramme qui illustre les questions qui, selon chaque situation de fait particulière, pourront nécessiter une réponse adéquate dans l’éventualité d’une contestation en matière de PDTPE. Même si le présent article n’offre aucune solution miracle ni aucune formule scientifique pour garantir la réussite des contribuables, les auteurs souhaitent tout de même aider les contribuables et leurs conseillers à réduire l’incertitude entourant cette matière complexe du contentieux fiscal.

A B S T R A C T

For more than 25 years, Canadian taxpayers have been appealing reassessments of allowable business investment loss (ABIL) deductions. The ABIL is considered to be one of the most widely contested and frequently litigated areas in tax law, and one infused with uncertainty. Taxpayers’ appeals fail almost twice as often as they succeed. In 2001, some light was shed when the Tax Court of Canada issued its decision in the Gamus case.

* OftheFacultyofBusiness,BrockUniversity,St.Catharines,ON(e-mail:[email protected]@brocku.ca).TheauthorsaregratefulforthecommentsprovidedbyAlanMacnaughtonandananonymousreviewer.

230 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

Referring to the number of complex technical provisions that come into play when taxpayers claim an ABIL, Bowman j identified four elements that must converge if the appellant is to succeed. The purpose of this article is to present the results of the authors’ review of the 240 reported court cases that comprise Canada’s jurisprudence on abils in the context of the four essential elements. For each of these four elements, a further checklist of questions is provided to assist taxpayers and their advisers in preparing an ABIL case, along with a discussion of many of the relevant cases. An appendix to the article offers two additional tools: a table summarizing the cases by issue as well as by outcome, and a flowchart mapping the sequence of questions that, depending on the specific fact situation, may need to be answered when responding to an abil challenge. While there is no magic bullet or scientific formula that will guarantee taxpayers success, it is hoped that this article will be useful to taxpayers and their advisers in reducing the uncertainty in this complex area of tax litigation.

KEYWORDS: APPEALS n BUSINESS TRANSACTIONS n DEBTS n LOSSES n PURPOSE n TAX DEDUCTION

C O N T E N T S

Introduction 231Key Question 1: Did the Taxpayer Invest in Shares or Debt of a Corporation? 233

1. Was There an Investment in the Nature of Shares or Debt? 2352. Was the Investment Made by the Taxpayer (or by Some Other Person)? 2373. Was the Investment Made in a Corporation? 237

Key Question 2: Has the Debt Been Established To Be Bad? 2391. Did the Taxpayer Consider the Relevant Factors? 2412. Can the Taxpayer’s Determination Be Shown To Be Honest and Reasonable? 2413. Was the Determination Made by the Taxpayer Himself or Herself? 2434. Was the Determination Based on Past and Present Experience

(as Opposed to Future Possibilities)? 2445. Was the Taxpayer Required To Take Further Steps To Collect,

and If Yes, Were Those Steps Taken? 2446. Is There a Non-Arm’s-Length Relationship Between the Parties? 245

Key Question 3: Was the Property Issued by a “Small Business Corporation”? 2451. Can the Taxpayer Succeed When Corporate Documentation Contradicts

His or Her Stated Intention? 2482. In Determining the Principal Purpose of the Business, Whose Intention

Is Relevant? 2523. What Is the Relevant Time Period for the Determination of Principal Purpose? 2544. Was the Corporation Carrying On an Active Business? 255

Key Question 4: Was the Property Acquired for the Purpose of Earning Income? 2591. Where the Transaction Is in the Nature of Financial Assistance to a

Family Member’s Business, What Evidence Will the Courts Accept with Regard to Its Purpose? 260

2. Can the Taxpayer Establish Sufficient Nexus Between Himself or Herself and the Income? 264

Faint Hope 265Original Purpose 268Expectation Versus Right 269

Conclusion 272

substantiating an abil deduction n 231

INTRO DUC TIO N

Inthe2001caseofGamus v. The Queen,1theissuebeforetheTaxCourtofCanadawaswhethertheappellanthadsustainedanallowablebusinessinvestmentloss(ABIL)in1992.SheclaimedthatshehadsustainedabusinessinvestmentlossinrespectofaloanthatsheandherhusbandhadmadetoBIMPEnterprisesLtd.(“BEL”).Inar-rivingatadecisionintheappellant’sfavour,BowmanJnotedthecomplexityoftheABILprovisions2andsetoutalistoffouressentialcriteriaforasuccessfulABILclaim:

[AnABIL]involvesasomewhatcomplexinteractionofparagraphs3(d),38(c),39(1)(c),section50,subparagraph40(2)(g)(ii)andthedefinitionof“smallbusinesscorporation”insection248.

Here,fourelementsmustconvergeiftheappellantistosucceed:(a) BELmusthavebeenindebtedtotheappellantin1992(b) thedebtmusthavebecomeabaddebtinthatyear...(c) BELmusthavebeenasmallbusinesscorporation...(d) thedebtmusthavebeenacquiredforthepurposeofgainingorproducingin-

comefromabusinessorproperty.3

At theCanadianTaxFoundation’s2006annual conference,EdwinKroftwasaskedtocommentoncurrenttrendsandthehottopicsoftheday.Inhisremarks,helistedABILsasonetopicthatwouldcontinuetodominatethetaxlandscapeintermsofboththehighvolumeofcasesandthehighdegreeofuncertainty:“The

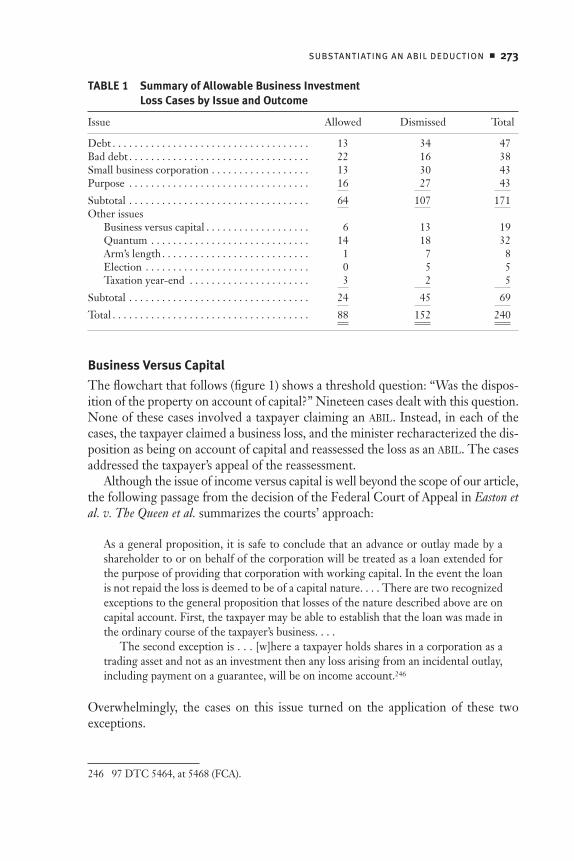

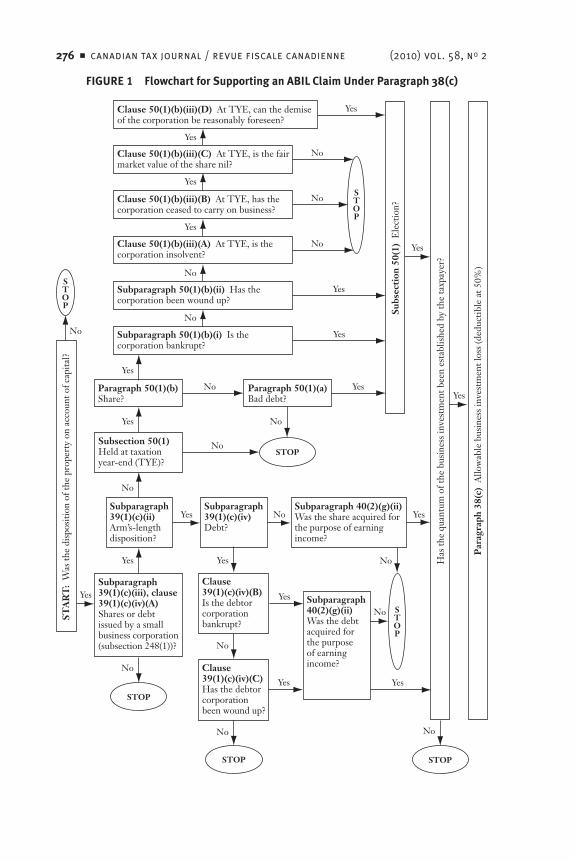

Appendix Classification of ABIL Cases and Flowchart for Evaluating ABIL Claims 272Business Versus Capital 273Quantum 274Arm’s Length 275Election 275Taxation Year-End 275

1 [2001]3CTC2342,atparagraph2(TCC).

2 Unlessotherwisestated,statutoryreferencesinthisarticlearetotheIncomeTaxAct,RSC1985,c.1(5thSupp.),asamended(hereinreferredtoas“theAct”).Thedetailsoftherelevantprovisionsareaddressedbelowinthetextaswellasintheflowchartincludedintheappendix.Ingeneralterms,theyprovideasfollows:paragraph39(1)(c)definesataxpayer’s“businessinvestmentloss”forataxationyearasbasicallyalossarisingfromthedispositionofsharesordebtofasmallbusinesscorporation(SBC);subsection248(1)definesa“smallbusinesscorporation”tobeaCanadian-controlledprivatecorporationwhoseassetsareusedprincipallyinanactivebusinesscarriedonprimarilyinCanada;subsection50(1)appliestosuchdispositionswhentheyoccuratnon-arm’s-length;andsubparagraph40(2)(g)(ii)requiresthetaxpayertodemonstratethattheshareordebtwasacquiredforthepurposeofearningincome.Wheretheforegoingconditionsaremet,50percentofthelossamountbecomesanABILunderparagraph38(c).

Finally,paragraph3(d)permitsanABILtobedeductedalongwithotherlossesfromnon-capitalsourcesagainstallsourcesofdivisionBincome.

3 Supranote1,atparagraphs10-11.NotethatinGamus,theABILclaimwasbasedonabaddebt;therefore,thefourcriteriarelateonlytobaddebtcases.

232 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

ABILcaseskeepbeingheardbytheTaxCourt.Taxpayerssometimeswinandsome-timeslose.”4ThepurposeofthisarticleistoprovidetaxpayersandtheiradviserswithtoolstoassisttheminpreparinganABILcase.Tothatend,wehaveconductedareviewofthe240reportedcourtcasesthatcompriseCanada’sjurisprudenceonABILs.Inthebodyofthearticle,wepresentasummaryandanalysisofthecaselawusing Bowman J’s four-element test. After amending his wording, reproducedabove,toremovefact-specificreferencestotheGamuscase,wehaverecastthetestintheformoffourkeyquestions:

1. Didthetaxpayerinvestinsharesordebtofacorporation? 2. If the investment is debt, and not owed to a corporation with which the

debtorcorporationdoesnotdealatarm’slength,hasthedebtbeenestab-lishedtobebadasrequiredunderparagraph50(1)(a)?Iftheinvestmentisashare,hasthesharebecomeworthlessinthecircumstancesreferredtoinpara-graph50(1)(b),orhasitbeensoldatalossinanarm’s-lengthtransaction?

3. Wastheproperty(shareordebt)issuedbyasmallbusinesscorporationasdefinedinpartXVIIoftheAct?

4. Wasthepropertyacquiredbythetaxpayerforthepurposeofearningincomeasrequiredundersubparagraph40(2)(g)(ii)?

Foreachofthesefourquestions,weprovideafurtherseriesofsubquestionstoassisttaxpayersandtheiradvisersinrespondingtoanABILchallenge,alongwithadiscussionofmanyoftherelevantcases.Byourcount,over70percentofthecaseshadoneofBowmanJ’sfourelementsastheprimaryissue.(Thetaxpayerwassuc-cessfulin37percentofthe240cases.)GiventhecomplexityofthelegislationandthereportedpropensityofthetaxauthoritiestoscrutinizeABILclaims,5muchhasbeenwrittenonthetopic.6Inthisarticle,wehopetoaddtotheABILliteratureintwobasicways:first,toprovideacomprehensiveguidetotheABILjurisprudenceby

4 JohanneD’Auray,EdwinG.Kroft,andRogerE.Taylor,“CurrentCases,”inReport of Proceedings of the Fifty-Eighth Tax Conference,2006ConferenceReport(Toronto:CanadianTaxFoundation,2007),7:1-21,at7:16.

5 AccordingtoBrianPosthumus,“[a]necdotalevidencesuggeststhatmostindividualtaxreturnsfiledwithanABILdeductionareflaggedforpre-assessmentreview.Thevolumeofcaselawonthesubjectsuggeststhattheseclaimsarewidelycontestedandthoroughlyexamined.”BrianPosthumus,“TaxLossPlanningfortheOwnerManager—AnUpdateonClaimingAllowableBusinessInvestmentLosses,”in2008 Prairie Provinces Tax Conference(Toronto:CanadianTaxFoundation,2008),tab12,at2.

6 See,forexample,MaxWederandCarolynMacDonald,“AllowableBusinessInvestmentLosses:WhatToDoWhentheCRACalls,”in2009 British Columbia Tax Conference(Toronto:CanadianTaxFoundation,2009),tab7;DavidP.Webb,“BusinessInvestmentLosses,”in1993 Ontario Tax Conference(Toronto:CanadianTaxFoundation,1993),tab4A;JeffreyA.Nightingale,“SelectedSmallBusinessIssues,”in2002 Ontario Tax Conference(Toronto:CanadianTaxFoundation,2002),tab2;DavidW.Middleton,“TheDeductibilityofGuaranteePayments,”in1991 Ontario Tax Conference(Toronto:CanadianTaxFoundation,1991),tab2B;andPosthumus,supranote5.

substantiating an abil deduction n 233

summarizingalltherelevantcasestodate;and,second,toorganizethatjurispru-dencebyissue.Mostimportantly,wehopetoreducetheuncertaintyfacedbyABILclaimantsandtheiradviserswhenreassessed;thisarticlemaybearesourceforiden-tifyingpreviouscaseswithsimilarfactsandissues,thosecasesinwhichthetaxpayersucceeded,andthereasonsforthedecisionsinthetaxpayer’sfavour.

AnappendixtothearticleofferstwoadditionaltoolsforABILclaimantsandtheiradvisers:atablesummarizingthe240ABILcasesbyissueandbyoutcome;7and,todeconstructthe“complexinteraction”(toquoteBowmanJ)ofthenumerousprovi-sionsthatmakeuptheABILrules,aflowchartmappingthesequenceofquestionsthat—depending on the specific fact situation—may need to be answered whenrespondingtoanABILchallenge.

ThetransactionthatformsthebasisforanABILclaimbeginswhenanindividualadvancesfundsinexchangeforsharesordebtissuedbyacorporationthatisasmallbusinesscorporation(SBC).(ThedefinitionofanSBCwillbediscussedinalatersectionofthearticle.)Inalargenumberofcases,theABILclaimischallengedbe-cause,intheopinionofthetaxauthority,thetaxpayerhasfailedtoestablishoneormoreofthebasicelementsofthetransaction—

1. the“WHAT”of the transaction—that is, thenatureof the investmentasbeingeithersharesordebt;or

2. the“WHO”ofthetransaction—thatis,eithera. thatthedebt/sharewasheld,asalleged,bythetaxpayer(asopposedto

someotherperson),orb. thatthedebt/sharewasissued,asalleged,bythecorporation(asopposed

tosomeotherperson).

We will examine each of these elements in turn, beginning with our first keyquestion.

K E Y QUE S TIO N 1: DID THE TA X PAY ER IN V E S T IN SH A RE S O R DEBT O F A CO RP O R ATIO N?

Inanumberofcases,thetaxpayerisgenerallyunabletoprovidesufficientevidenceofthebasicfactsituationuponwhichtheABILclaimisfounded.Forexample:

n InKornelow v. MNR,althoughthetaxpayerpresentedmorethanadozendocu-mentsasexhibits,showingborrowings,guarantees,repayments,andmortgagesbetweenhimself,hiswife,hismother-in-law,andacorporation,“therewasnosatisfactorysubstantiation”ofhisclaimthatthecorporation“waslegallyindebtedtohimandthisindebtednessgaveriseto”theABIL.8

7 Weexplainintheappendixhowtheclassificationprocesswascarriedout.Thefulllistofthe240casesandtheclassificationgiventoeachisavailablefromeithertheauthorsortheCanadianTaxFoundationlibrary.

8 91DTC431,at433(TCC).

234 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

n InKatzenstein v. Canada,Mr.Katzenstein, appearingas agent forhiswife,offered“noexplanationastohowthebusinessinvestmentlossfigureswerearrivedat.”9

n IntheunfortunatecaseofChiarelli et al. v. R,althoughMs.Chiarelliwasrepre-sentedbyanagentwhowas“anaccountant,entrepreneurandformerauditorwithSpecialInvestigations,RevenueCanada,”thecourtfoundtheevidence“imprecise”ornotsupportedbycleardocumentation.10

n TheappellantinThibeault v. The Queenneededthecourt“tosubstituteforthefactsaninterpretationnotconsistentwithreality”andagainoffered“mereoralstatementsunsupportedbyanydocuments.”11

n Thetaxpayer inMcIntosh v. Ralsofailedasaresultofwoefully inadequateevidence:

ThereissimplynothingheretosupportthatthecorporationwasorcouldbeperceivedtobeindebtedtotheAppellantinanywaythatwouldsubstantiateabaddebt....

IfataxpayerisinvolvedinbusinessactivitiesandexpectstomakecertainclaimsundertheIncome Tax Act,hemustcometocourtpreparedtoprovide,atminimum,theessentialdocumentationforthecourttogivehimtheclaim.12

n InPeters v. MNR,“theAppellant’sevidence,suchasitisinthismatter,lacksanysubstantiationwhatsoeverandisincredible.”13

n Finally,inAllegritti v. R,thecourtdeniedtheABILclaimonthebasisthattheappellantshadonly“vaguememories”of the transactionbecause theirac-countanthad“workeditout.”14

9 [1993]1CTC2645,at2646(TCC).

10 [2001]3CTC2039,at2040(TCC).

11 2005DTC720,atparagraphs41and42(TCC).

12 [2003]3CTC2423,atparagraphs17and19(TCC).

13 93DTC422,at424(TCC).SeealsothedecisionoftheTaxCourtofCanadainAbrametz v. R,[2007]5CTC2157,atparagraph15:“Evenallowingforthebreakdowningoodrecordskeeping[sic]thatmayariseinthecircumstancesofafailingbusiness,itstrikesoneasoddthattheAppellantiswithoutthecorporate,bankingorlegalrecordstosubstantiatehisclaim.”TheFederalCourtofAppealdisagreed:“[T]heTaxCourtJudgereachedthatconclusion‘bywayofinference,’havingregardtothe‘weaknessoftheAppellant’stestimony’andtheabsenceofseeminglysimplelegaldocumentationtosubstantiatethetransferofthoseshares.Whileitisundoubtedlytruethattheappellant’stestimonywasconsiderablylessthancrystalclear,therecordcontainssignificantevidence,inadditiontotheappellant’stestimony,thatpointstotheconclusionthattheappellanttransferredhissharesofPlacidtoMr.Paulhus.”Abrametz v. Canada,2009FCA111,atparagraph41.(NotethatAbrametz’sappealforanABILwasdeniedowingtohisfailuretoprovidesufficientevidencetosubstantiatetheinvesteecorporationasanSBC.)AlsoseeIsaman v. The Queen,2003DTC994,atparagraph5(TCC):“[N]odocumentaryorotherevidenceexiststosupporthisassertion.”

14 [1997]2CTC2114,atparagraph9(TCC).AlsounsuccessfulonsimilargroundswerethetaxpayersinBurkart et al. v. The Queen,98DTC1328(TCC),andKaupas v. R,[2004]1CTC3025(TCC).

substantiating an abil deduction n 235

In all of these cases, the court lacked sufficient evidence to determine whattransaction(s)(ifany)tookplacethatcouldformthefoundationforanABILclaim.Thereareanumberofothercases inwhichtheevidencewastherebut ledtoaconclusionthatwasinconsistentwiththeclaim.Thesecasestendtofallintothreetypesofscenarios,givingrisetothree,morespecific,subquestions:

1. Wasthereaninvestmentinthenatureofsharesordebt? 2. Wastheinvestmentmadebythetaxpayer(orbysomeotherperson)? 3. Wastheinvestmentmadeinacorporation?

1. Was There an Investment in the Nature of Shares or Debt?

AnumberofABILclaimsarechallengedonthegroundsthatwhatthetaxpayerre-ceivedinreturnforfundsadvancedtoaqualifyingcorporation—the“WHAT”ofthetransaction—waspropertyotherthantherequiredsharesordebt:

n Bhaganididnothavesharesordebt—hehadajudgmentagainsthim.15

n McHalehadguaranteedadebtbutnotactuallypaidanythingatthetimeinquestion.16

n Monacohadpurchasedrightsnotshares.17

n Barker’sconsiderationwasachoseinaction(areleasefromaguarantee).18

n Dastousagreedtoforgoprofessionalfees.19

InGrant et al. v. The Queen,thecourtfoundthatthetaxpayerhad

clearlyputsomemoneyintotheprojectbutitisunclearhow.Certainlyitwasnotbywayofaloantoorsubscriptionforsharesofanyofthecorporateentitiesthatseemedtobefloatingaround.20

Again,thereistherecurringthemeofinadequatedocumentation.InBullas v. The Queen,theFederalCourtofAppealagreedthatMr.Bullas“wasunabletoproduceadequaterecordsorotherevidence”ofhisinvestment.21

PoorrecordkeepingdoesnotnecessarilyresultindenialofanABILclaim,buthowhopefulshouldataxpayerbeinthisregard?Consider,forexample,Chandan v.

15 Bhagani v. R,[2004]4CTC2367(TCC).

16 McHale v. MNR,92DTC1781(TCC).

17 Monaco v. R,[2000]2CTC2277(TCC).

18 Barker v. R,[2002]3CTC2055(TCC).

19 Dastous v. R,[2004]3CTC2264(TCC).SeealsoSandner et al. v. MNR,93DTC901(TCC),wherethetaxpayermistakenlybelievedthathehadincurredindebtedness“tantamounttopayment”onaloanguaranteewhenthebankregisteredajudgmentagainsthisland.

20 (2000),54DTC1985,atparagraph32(TCC).

21 2002DTC7043,atparagraph1(TCC).

236 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

The Queen.22Despite“abysmal”recordkeeping,sobad“thattheappellantdidnotknowwhattheformofhisinvestmentwas,”23thecourtwasconvincedthat

losseswereobviouslyincurred.Thisisnotacasewherethereisdoubtastowhetheranymoneywasinvested.24

Thetaxpayer,abusdriverbyoccupation,succeededlargelybecausehecouldproducethird-partydocumentstosupporthistestimony,becausehisstorywas“plausible”enoughtoestablishaprimafaciecase,and,mostsignificantly,becausetheCrownpresentednocontradictoryevidence.WoodsJclarifiedthecourt’sapproachregard-ingtheissueofrecords:

Counselalsoreferredtodecisionsthatemphasizetheimportanceofrecord-keeping....Ataxpayerisrequired...tokeepappropriaterecordssothattheincometaxreturnscanbeverifiedandataxpayerwhofailstokeepadequaterecordsmayhavetheirclaimsdisallowed.Aclaimforadeductionisnotnecessarilytobedenied,however,becausethetaxpayerfailedtokeepadequaterecords.Therequirementisthataprima faciecasebeestablishedand,inmyview,thatiswhattheappellanthassucceededindoing.25

Bowman J subsequentlyaffirmed this approach inBenjamin v. The Queen andofferedanevenmorehopefulpicturefortaxpayerscomingbeforethecourtwithinadequaterecordswherecredibleoraltestimony(eveninconsistenttestimony)ispresented:

Here,theappellantinadditiontohisowntestimonycalledtheothertwoshareholderswhobothtestifiedthattheappellantloaned$50,000tothecompany.Theywerecred-iblewitnesses and I accept their testimony.Counsel for the respondentpointed tosome inconsistencies in their testimony.Onesaid that the$50,000waspaid to thecompanyinonelumpsum,theappellantsaidhepaiditintwoandthethirdwasun-certain.Itisnotsurprisingthattheremightbesomelapsesofmemoryaftertenyears.Farfromdetractingfromtheappellant’stestimonythesediscrepanciesenhanceit.Itprovesthatthethreedidnotgettogetherandconcoctaconsistencyinthedetailsoftheirstory.Iamnotpreparedtoattributetothesewitnessessuchadegreeofingenuitythattheyconcoctedinconsistenciestomaketheirstorylookcredible.26

22 2005TCC685.

23 Ibid.,atparagraph8.

24 Ibid.,atparagraph26.

25 Ibid.,atparagraph34.Ontheissueoftaxpayeronus,seealsoGregory v. R,[1999]1CTC2279,atparagraph6(TCC):“CounselfortheRespondentarguedthattheappealshouldbedismissedbecausetheAppellanthadnotprovenwithaprecisepapertrail....Counseliscorrect...butsomecredencemustbegiventotheverybelievableswornanduncontradictedevidenceoftheAppellanthimselfplusthecorroboratingdocuments.WhiletheonusofproofisontheAppellant,itisonlyacivilonus.IamsatisfiedthattheAppellantdischargedtheonusonhimandshiftedtheonustotheRespondent.”

26 2006DTC2265,atparagraph10(TCC).

substantiating an abil deduction n 237

2. Was the Investment Made by the Taxpayer (or by Some Other Person)?

Althoughtheformoftheinvestmentmaybeestablishedasdebtorshares,thestum-blingblock in the casemaybe establishing the “WHO”of the transaction—inparticular,establishing the identityof the investoras the taxpayer.Often, familymembersorotherrelatedpersonsareinvolved.InWierbicki v. The Queen,27forex-ample,anothercasewheremanyoftherequiredelementswereunsupported,someoftheindebtednessappearedmorelikelytobeowedtothetaxpayer’swifeandotheramountstohismother-in-law.ThetaxpayersinBeaulac v. The Queen28andYiouroukis v. The Queen29were foundtobeassertingclaimsbasedon loans thatweremorelikelytakenoutbytheirspouses.In817254 v. The Queen,theidentitiesofthebor-rowerandthelenderwerefoundnottobeasclaimed.30Bycontrast,considerAir Rock Drilling Co. Ltd. et al. v. The Queen.31Eventhoughtheappellantwasfoundnottobeinfactashareholderofthedebtorcorporation(“CPI”),andtherecordkeepingwas“sloppyandinaccurate,”thecourtallowedtheclaimonthebasisthat“AirRockwasanindirectbutequitableshareholderofCPI.”32

3. Was the Investment Made in a Corporation?

Theother“WHO”ofthetransaction—theidentityoftheinvestee—isoftenthebasis foranABILchallenge.Taxpayersmostoftenlosethesecaseswhentheyarefoundtohaveadvancedfundstootherindividualspersonallyinthehonestbeliefthatthefundswillthenfindtheirwayintostartuporstrugglingbusinesscorpora-tions.33InBrand v. The Queen,34althoughthetaxpayerhadadvancedfundstohissonanddaughter,credibletestimonyandsupportingdocumentaryevidenceledtothefindingthatthechildrenhadinfactreceivedtheloansintrustfortheircorpora-tions.This“intrust”argumentfailedinMackay v. The Queen,35wheredocumentary

27 2000DTC6243(FCA).

28 2000DTC2218(TCC). 29 99DTC333(TCC). 30 98DTC1192(TCC).Thecourtdescribedthetestimonyofthesoleshareholderas

“reprehensible,scandalousandoutrageous”(at1196). 31 99DTC617(TCC). 32 Ibid.,atparagraph51.PerhapsthisdecisioncanbebestexplainedbythefactthatbothAir

Rockanditsowners(theappellantindividuals)wereallatarm’slengthwithCPI. 33 See,forexample,Marceau v. The Queen,2005DTC446(TCC);Wieler v. R,[2001]3CTC

2142(TCC);St. Martin v. R,[1998]4CTC2656(TCC);McDonald v. The Queen,98DTC2223(TCC);Shoeman v. The Queen,2004DTC2500(TCC);Crane v. The Queen,99DTC3521(TCC);andStern v. The Queen,2004DTC3260(TCC).

34 2005DTC1249(TCC). 35 2006DTC3653(TCC).InTurcotte v. R,[2000]2CTC2369(TCC),thetaxpayerwasableto

produceevidencethattheindividualintowhosehandsthefundswerepaidwasactingasamandataryforthecorporation,notwithstandinganotarizedloancontractshowingthisindividual,andnotthecorporation,astheborrowingparty.Thecourtdoubtedtheauthenticityofthis“irregular”document.

238 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

evidence contradicted the appellant’s testimony as to what she believed she waspurchasing.

Alternatively,thebarriertotheclaimmaybethattherecipiententityisinsomeotherlegalform,asinMarkovzki v. The Queen36(atrust),Jones v. R37(ajointventure),andSmilovici v. R38(apartnership).InYau v. R,39ontheotherhand,thetaxpayerwasreassessed,likeSmilovici,onthebasisthathehadadvancedfundstoapartnershipatatimewhenthecorporationdidnotexist.UnlikeSmilovici,Yauwonhisappealbecausehehadcorroboratingdocumentaryevidence:hehadsuedtorecoverthedebt,andthejudgmentnamednotonlythepartnersbutalsothesubjectcorpora-tion.InEynan v. R, thetaxpayer“statedthatsheinvested$40,000 inhorseswithSilverUnicornInc.”40Moreaccurately,sheboughtpartialownershipinthehorsesdirectly,andnotsharesinthecorporation.

ThedecisionsinHuneault v. R41and,fiveyearslater,Chambly Radios Communi-cations Cellulaires v. The Queen42provideaninterestingcomparisonwheretwocaseswithsimilarfactsproduceoppositeoutcomes.Inbothcases,theministerconsideredthattheappellanthadloanedfundstoanindividualwithwhomtheappellanthadabusinessrelationship,andnottoacorporation.InHuneault,theappellantmadea loantoaMr.Gauthier,whowasthesoleshareholderofastrugglingbusiness,JanréLtée.Althoughthecourtunderstoodthemotivationfortheformofthetrans-action,precedentseemedtorequirethattheformofthetransactiondeterminetheoutcome:

AsJanréLtéewasonthepointofbankruptcyitishighlylikelythattheappellantandMr.GauthierdeliberatelyagreedtomakealoantoMr.Gauthierdirectlysothelattercouldcontrolwherethemoneywent.Iftheloanhadbeenmadetothecompanydir-ectly,inviewofthefactthattherewasalreadyapetitionpendingtoappointaninterimreceiver,Mr.Gauthierwouldhavelostcontrolofit.

Further,intaxmattersformtakesonsomeimportance.InthisconnectionIwouldrefertotheFederalCourtofAppealjudgmentinFriedberg v. R(1991),92D.T.C.6031(Fed.C.A.),at6032:

Intaxlaw,formmatters.Ameresubjectiveintention,hereaselsewhereinthetaxfield,isnotbyitselfsufficienttoalterthecharacterizationofatransactionfortaxpurposes.Ifataxpayerarrangeshisaffairsincertainformalways,enor-moustaxadvantagescanbeobtained,eventhoughthemainreasonforthesearrangementsmaybetosavetax(seeThe Queen v. Irving Oil91DTC5106,per

36 98DTC2040(TCC).

37 [1996]2CTC2246(TCC).

38 [2006]1CTC2578(TCC).

39 [2005]3CTC2124(TCC).

40 [2001]2CTC2140,atparagraph3(TCC)(emphasisadded).

41 [1998]3CTC2788(TCC).

42 2003TCC3957.

substantiating an abil deduction n 239

Mahoney,J.A.).Ifataxpayerfailstotakethecorrectformalsteps,however,thetaxmayhavetobepaid.43

SimilarlyinChambly,thefundswereadvancednottothecorporationbutdelib-erately to its individualowner, so that theycouldbeused topayemployeesandavoidseizurealongwiththeothercorporateassets.AlthoughtheCrownarguedthatthetransactionhadtobe“understoodinitsliteralsenseandnotinlightoftheintentionbehindit,”TardifJ,allowingtheappeal,explained:

Iagreewiththiscontention,althoughIdonotbelievethatitwarrantssucharigidinterpretation.

Thecontextandallofthecircumstancesmustnotbeoverlookedinassessingthenatureofatransaction.Anoverlyconservativeandrigidapproachcouldoftenparalyzetheordinarycourseofbusiness.Itwouldthenbenecessarytocallonexpertsinordertodraftalladministrativedocuments.44

K E Y QUE S TIO N 2: H A S THE DEBT BEEN E S TA BLISHED TO BE B A D?

TheFederalCourtofAppealhaditsfirstopportunitytodeterminewhetheradebthasbecomebadintheABILcontextinits2003hearingofRich v. The Queen.45TheministerhaddisallowedanABILclaimedbyLarryRich,anaccountant(infact,afellowoftheaccountingprofession),inhis1995taxreturn.ThelossrelatedtoadebtowedtoRichbyacorporationknownasDMS,ofwhichheowned25percentandofwhichhis son (whoalsoowned25percent)was themanager.46Rich senior (thetaxpayerinthecase)consideredthedebttobebad,largelyonthebasisofanex-change of letters: he wrote to DMS asking when he might expect repayment, towhichhissonresponded,probablynever.TheTaxCourtofCanadadisagreedwiththetaxpayer’spositionthatthedebtwasthenestablishedtobeabaddebtandcon-cludedthatheshouldhavemadea“concreteeffort”tocollect.47Richappealed.

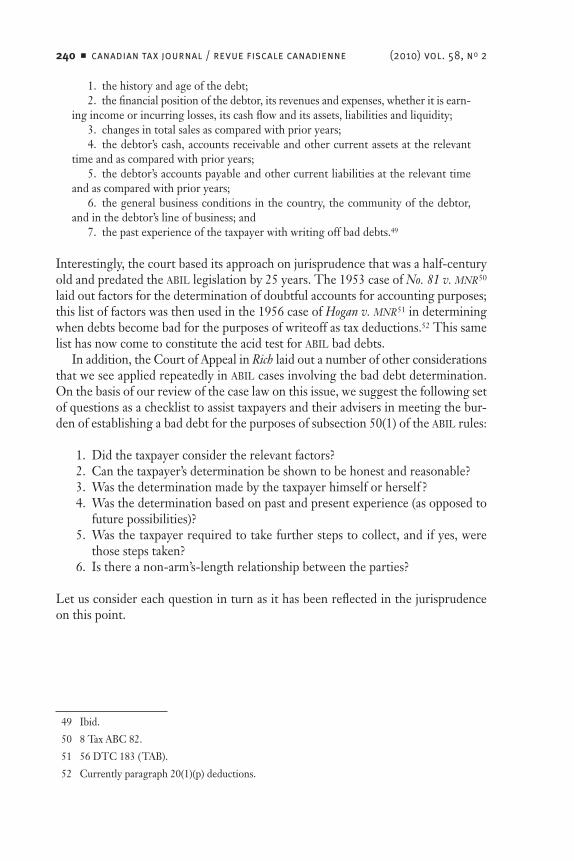

Inamajoritydecision,theFederalCourtofAppealfoundinfavourofthetax-payer.Writingforthemajority,RothsteinJsetoutalistofsevenfactorsthatinthecourt’sopinion“usuallyshouldbetakenintoaccountindeterminingwhetheradebthasbecomebad.”48Thislistoffactorshasbeenheavilyrelieduponinmanycases.Itincludes:

43 Huneault,supranote41,atparagraphs29-30.

44 Supranote42,atparagraphs29-30.

45 2003DTC5115(FCA).

46 Theson’sfather-in-lawownedtheother50percent.

47 Rich v. R,[2002]1CTC2224,atparagraph29(TCC).Therewasalsoanissueofpurposeundersubparagraph40(2)(g)(ii),discussedinalatersectionofthisarticle.

48 Supranote45,atparagraph13.

240 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

1. thehistoryandageofthedebt;2. thefinancialpositionofthedebtor,itsrevenuesandexpenses,whetheritisearn-

ingincomeorincurringlosses,itscashflowanditsassets,liabilitiesandliquidity;3. changesintotalsalesascomparedwithprioryears;4. thedebtor’scash,accountsreceivableandothercurrentassetsattherelevant

timeandascomparedwithprioryears;5. thedebtor’saccountspayableandothercurrentliabilitiesattherelevanttime

andascomparedwithprioryears;6. thegeneralbusinessconditionsinthecountry,thecommunityofthedebtor,

andinthedebtor’slineofbusiness;and7. thepastexperienceofthetaxpayerwithwritingoffbaddebts.49

Interestingly,thecourtbaseditsapproachonjurisprudencethatwasahalf-centuryoldandpredatedtheABILlegislationby25years.The1953caseofNo. 81 v. MNR50laidoutfactorsforthedeterminationofdoubtfulaccountsforaccountingpurposes;thislistoffactorswasthenusedinthe1956caseofHogan v. MNR51indeterminingwhendebtsbecomebadforthepurposesofwriteoffastaxdeductions.52ThissamelisthasnowcometoconstitutetheacidtestforABILbaddebts.

Inaddition,theCourtofAppealinRichlaidoutanumberofotherconsiderationsthatweseeappliedrepeatedlyinABILcasesinvolvingthebaddebtdetermination.Onthebasisofourreviewofthecaselawonthisissue,wesuggestthefollowingsetofquestionsasachecklisttoassisttaxpayersandtheiradvisersinmeetingthebur-denofestablishingabaddebtforthepurposesofsubsection50(1)oftheABILrules:

1. Didthetaxpayerconsidertherelevantfactors? 2. Canthetaxpayer’sdeterminationbeshowntobehonestandreasonable? 3. Wasthedeterminationmadebythetaxpayerhimselforherself ? 4. Wasthedeterminationbasedonpastandpresentexperience(asopposedto

futurepossibilities)? 5. Wasthetaxpayerrequiredtotakefurtherstepstocollect,andifyes,were

thosestepstaken? 6. Isthereanon-arm’s-lengthrelationshipbetweentheparties?

Letusconsidereachquestioninturnasithasbeenreflectedinthejurisprudenceonthispoint.

49 Ibid.

50 8TaxABC82.

51 56DTC183(TAB).

52 Currentlyparagraph20(1)(p)deductions.

substantiating an abil deduction n 241

1. Did the Taxpayer Consider the Relevant Factors?

AlthoughRothsteinJcautionedthatthelistoffactors“isnotexhaustiveand,indif-ferent circumstances,one factoror anothermaybemore important,”53 it seemsquiteclearthatacompletefailuretoaddressanyofthefactorsmaywellbefataltothetaxpayer’scase.Indismissingthetaxpayer’sappealinBarrie v. The Queen,theTaxCourtobserved,“NotoneofthefactorssummarizedbyRothsteinJA,inRich v. CanadawasseriouslyconsideredbyMr.Barrie.”54

2. Can the Taxpayer’s Determination Be Shown To Be Honest and Reasonable?

LiketheruleondoubtfulaccountssetoutinHogan,thereis“nonecessitythatadebtbeabsolutelyirrecoverable”55aslongasthetaxpayeracted“honestlyandrea-sonably”inmakingthebaddebtdetermination.56Injudgingthereasonablenessofthetaxpayer’sdetermination,thecasesrefertothestandardofa“prudentbusiness-man,”57a“pragmaticbusinessman,”58ora“goodfaithobjectiveassessment.”59Thetaxpayer’spositiononthereasonablenessofhisorherdeterminationwillbebut-tressedif“solid,competent,professionalaccountingrecords”canbepresentedinevidence.60

Thosetaxpayerswhocontinuetoadvancefundstoadeadbeatdebtormayhavedifficultyestablishingthemselvesbeforethecourtaseitherreasonableorprudent.Moreoftenthannot,continuingtolendmoneyundersuchcircumstancesdealsafatalblowtothecase.InGiahinejad v. R,forexample,thecourtseemedtobegoingaboveandbeyondinhelpingthetaxpayertoprovehercase,butwasunabletoig-noreher“totalfailuretoshowthatthedebtwentbad.”61

53 Supranote45,atparagraph13.

54 2004DTC2176,atparagraph37(TCC).SeealsoLitowitz v. The Queen,2005DTC1469(TCC).

55 Berretti v. MNR,86DTC1719,at1722(TCC).

56 Theissueofwhetherthetaxpayerhadanhonestandreasonablebeliefintheuncollectibilityofthedebtisaddressedin,forexample,Kyriazakos v. The Queen,2007DTC373(TCC);Deck et al. v. The Queen,2002DTC1371(TCC);andAnjalie Enterprises Ltd. v. The Queen,95DTC216(TCC).

57 Flexi-Coil Ltd. v. The Queen,96DTC6350(FCA);Netolitzky v. The Queen,2006DTC2953(TCC).

58 Campbell v. The Queen,2000DTC2528(TCC);Roy c. R,[2004]2CTC2519(TCC);Orlando v. The Queen,99DTC1201(TCC).

59 AsinNetolitzky,supranote57.

60 Rich,supranote47,atparagraph22(TCC).SeealsoCackirovski v. R,[2003]2CTC2155(TCC),ontheneedforrecords.However,recallBenjamin v. The Queen,supranote26,wherethelackofrecordswasnotfataltothetaxpayer’scase.

61 [2002]1CTC2141,atparagraph10(TCC).Certainlyataxpayerwho“lent”moneyneverexpectingtogetitbackisdoomed;see,forexample,Kronstal v. R,[1998]4CTC2844(TCC).

242 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

ReferringtotheAppellantnotbeingabletorecovertheloansin1997,ontheevidencebeforeme,IcouldnotpossiblyfindthatthesedebtsowingtotheAppellantbythenumberedcompanywerebaddebtsatanytimein1997.EvenonDecember1,1997,theAppellantissuedachequetothecompany...andthenagainonDecember28,sheissuedanevenbiggercheque....Shewasstillinvestingmoneyinthiscompanyinthelastmonthoftheyearand,indeed,inthelastthreeorfourdaysoftheyear.Icannotfind,therefore,thatthecompanywasinsolventorunabletopayherloanswhenshewasstilllendingmoneyattheendoftheyear.Onthatbasisalone,theAppellant’sap-pealcannotsucceed.62

Thejurisprudenceonthisquestionincludesanumberofcaseswheretheminis-teracknowledgedthatanABILhadbeenincurredbythetaxpayerasaresultofadebtgonebadbutcontestedthetaxpayer’sviewastowhen—thatis,inwhichtaxa-tionyear—thesubjectdebtinfactwentbad.63Earl v. MNR64involvedanABILclaimforthe1984taxationyear.Thetaxpayerarguedthathedidnotknowofthedemiseofthedebtorcorporationbecausehehadbeenseriouslyillforseveralyears.Thecourt relied heavily on the right of the taxpayer himself to make the necessarydetermination:

Barringclearevidence to thecontrary, theyearselectedbyanAppellantas that inwhichheand he aloneaccordingtotheAct,establishedthatadebtbecamebad,shouldbetheoneacceptedbytheMinister.65

Onceagain,however,thetaxpayer’spositionmustbeshowntobereasonableinthecircumstancesandconsistentwiththeevidence.InGilhooly v. MNR,66theABILwasclaimedinthetaxationyearinwhichthedebtorcorporationwasdissolved;theministerreassesseditasanABILoftheimmediatelyprecedingtaxationyear,whichwastheyearofthetaxpayer’spersonalbankruptcy.Thetaxpayer’sfailuretoshowtheloanreceivableasanassetwasarguedasevidencethatithadbeenestablishedbyhimtohavebecomeabaddebtinthatyear.TaylorJagreedonthebasisthatthetaxpayer’spositionwasunreasonable:“[T]herationaleuponwhichMr.Gilhoolybasedhiscontention...completelyescapesme.”67Similarly,inRichardson v. MNR,theappellantclaimedthedebtsasbeingbad,butinthecourt’sview,“hisactionsandwordsbeliedthisbothinhisevidenceandwrittenargument.”68

62 Giahinejad,supranote61,atparagraph8.

63 Inadditiontothecasesdiscussedbelow,seeÉ. Lavoie v. Canada,[1994]1CTC2294(TCC),andLee v. MNR,90DTC1738(TCC).

64 89DTC221(TCC).

65 Ibid.,atparagraph10(emphasisadded).

66 87DTC4(TCC).

67 Ibid.,at6.Othercaseswheretheminister’sdeterminationwonoutasmorereasonableoverthatofthetaxpayerincludeMacKenzie & Fiemann Ltd. v. MNR,[1989]2CTC2133(TCC),andMacMillan v. R,98DTC3465(TCC).

68 93DTC258,at260(TCC).

substantiating an abil deduction n 243

Insomeinstances,itappearsthatthetaxpayersoughttoclaimanABILonadebtthataroseinastatute-barredyear.InDuncan v. MNR,69thebusinesswasfoundtohaveinfactceasedoperationin1973,beforetheenactmentoftheABILlegislation.InTardif v. The Queen,70theministersuccessfullyarguedthatthelosshadoccurredinayearwithalowercapitalgain/lossinclusionratethantheoneclaimedinthetaxpayer’sfilings.

3. Was the Determination Made by the Taxpayer Himself or Herself?

Itseemsclearthatthetaxpayerisnotobligedtoseekthird-partyadvice.InNetolitzky v. The Queen,whentheCrownarguedthatthetaxpayer“oughttohaveobtainedanindependentassessmentoftheamountofthelossandofthecompany’spotentialresalevalue,”thecourtdisagreed,referringtosuchanexpectationas“anunwar-rantedexpansionofthedutyimposedonthetaxpayer”bythelegislation.71

Whileitissettledthatthetaxauthoritycannotsubstituteitsownjudgmentforthat of the taxpayer,72 there is some apparent confusion around the question ofwhetherthestandardforthedeterminationtobereasonableisasubjectiveoranobjectivetest.AccordingtotheFederalCourtofAppealinRich,“theCourtisnottosecond-guessthebusinessacumenoftaxpayers.”73ThatstatementconfirmsthejudgmentoftheTaxCourtinDeck et al. v. The Queen,wherethecourtheldthat“thedeterminationofwhenadebtbecomesabaddebt isasubjectiveonetobemadebythe[creditor]”74asthepartymostfamiliarwithallthefacts.However,thisisnotonallfourswiththemorerecentcaseofKyriazakos v. The Queen,75wherethecourtforgavethetaxpayer’sfailuretoconductarevieworinanywayinvestigatethedebtor’sfinancesbecauseifshehad,shewouldhaveseenthatthefinancialsitu-ation was hopeless. The court’s description of its reasoning is rather enigmatic:“[Thetaxpayer]actedreasonablybasedonwhatshedidnotknow”!76ConsideralsoLitowitz v. The Queen,wherethestandardisambiguouslyexpressedas“areasonableperson,suchasMr.Litowitz.”77

69 86DTC1549(TCC).

70 2006DTC2895(TCC).Theissuewaswhetherthegone-baddatefellin1999orDecember2000.

71 Netolitzky,supranote57,atparagraph13.

72 See,forexample,thewordsofBowmanJinLitowitz,supranote54,atparagraph4:“Theremustbeanelementofcommonsenseandreasonablenessbutsomedeferencemustbepaidtothebusinessman’sjudgement.”

73 Supranote45,atparagraph10.

74 Deck,supranote56,atparagraph13.Thecasereportreads“debtor”;however,itisobviousthattheintendedreferencewas“thecreditor.”

75 Supranote56.

76 Ibid.,atparagraph18.

77 Litowitz,supranote54,atparagraph10.

244 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

4. Was the Determination Based on Past and Present Experience (as Opposed to Future Possibilities)?

Forthemostpart,“possiblerecoveryinthefutureisnotper seabar”tothetaxpayer’scase.78InMonaghan v. The Queen,79forexample,thecourtacceptedtheappellant’sdeterminationthatthedebthadbecomebadasofDecember31,1986eventhough,sixmonthslater,alargeinjectionofcapitalandachangeinleadershiphadturnedthe company into a successful profit-making business once again. On the otherhand,theFederalCourtofAppealinRichdidallowthat

[i]fthereissomeevidenceofaneventthatwillprobablyoccurinthefuturethatwouldsuggest that thedebt iscollectibleonthehappeningof theevent, the futureeventshouldbeconsidered.[However,if]futureconsiderationsareonlyspeculative,theywouldnotbematerialinanassessmentofwhetherapastduedebtiscollectible.80

5. Was the Taxpayer Required To Take Further Steps To Collect, and If Yes, Were Those Steps Taken?

Generally,thetaxpayerisrequiredtotakestepsinpursuitofcollectiononlywhencollectionisreasonablypossible.ThisistheprinciplesetoutbytheFederalCourtofAppealinRich.Othercasesmayusesomewhatdifferentvocabularytoexpressbasicallythatsametest—forexample,“Thereisalimittohowmuchthetaxpayerisexpectedtodo.”81Bycontrast,theTaxCourtin2002hadexpressedtheopinionthatthetaxpayerdidindeedneedtoexhaustallmeansofcollection,82and,accord-ingtothecourtinDeck,“adebtisonlybadwhenithasbeenproveduncollectible.”83More recently, in Kyriazakos, the court provided the following “continuum-of-hope”approachontheissueofwhenfurtherstepsarerequired:

If...thesituationisfoundtobehopeless,thennostepsatallarerequired.Attheotherendofthespectrum,ifthereview,conductedreasonablyandhonestly,suggestsconsiderablehopeforrepayment,Iwouldsuggestsomevigorouspursuitofcollectionshouldbeexpectedbeforewritingoffthedebt.Thegreyareaofcourseiswherethereviewleadstoaconclusionthathopeofcollectionliessomewherebetweenfutileandlikely.Insuchcases,IgleanfromprinciplesinRichthatthecreditor,whilecertainlynotexhaustingallremedies,shouldmakesomeeffortatcollectionbeforebeingabletosay,thedebtisbad.84

78 Berretti,supranote55,at1722.Onthisprinciple,seealsoLitowitz,supranote54,andHoule v. MNR,90DTC1247(TCC).

79 95DTC920(TCC).

80 Supranote45,atparagraph14.

81 Netolitzky,supranote57,atparagraph15.

82 Campbell,supranote58.

83 Deck,supranote56,atparagraph13(emphasisadded).

84 Kyriazakos,supranote56,atparagraph14.

substantiating an abil deduction n 245

Thetaxpayer’sdilemmais,ofcourse,howmucheffortisenough?InKeating v. The Queen,85forexample,theministercontendedthattheappellanttooknostepstorecoverherdebt.Thecourtagreedbutfoundherlackofefforttobereasonableinthecircumstances:

[T]heAppellanthadnoobligationtotakestepstocollectwhenfacedwiththeimmin-entthreatofforeclosureproceedingsagainstherhome....

IbelievethataccordingtotheprinciplesinRich,thepredominantconsiderationisstilltheabilityofthedebtortorepaythedebtinwholeorinpart.ThereisnothinginthefactswhichwouldindicatethatVisualSynergycouldhavepaidanyportionofthatdebtin1998oratanytimethereafter.86

6. Is There a Non-Arm’s-Length Relationship Between the Parties?

Theburdenofestablishingthereasonablenessofthebaddebtdeterminationmaybemademoreonerousinthecontextofanon-arm’s-lengthrelationship.Howmuchmoreonerousisunclear.RecallthatinRichthetaxpayerhadadvancedfundstokeepafloatwhatwasessentiallyhisson’sbusiness,ownedbythetaxpayerhimself,hisson,andhis son’s father-in-law.TheTaxCourtnoted in its judgment the suggestionthat,innon-arm’s-lengthcircumstances,thecourtmaybewelladvisedtobe“doublyvigilant.”87Themajoritydecisionof theFederalCourtofAppealalsosuggestedthatanon-arm’s-lengthrelationshipmay justify“closer scrutiny.”Further,whileEvansJdissentedfromthemajoritydecision,heagreedthatcaseswithrelatedpar-ties,inparticularfamilymembers,requireacloserlook:

Itisadmirablethatparentshelptheirchildrentobecomeestablishedintheircareers.However,whenparentsaskothertaxpayerstosharetheburdenofassistingachild’sstrugglingbusinessbydeductingfromtheirownincomepartofaloanasabaddebt,theycanexpectthetaxauthoritiesandthecourtstoexaminetheclaimwithcare.88

K E Y QUE S TIO N 3: WA S THE PRO PERT Y ISSUED BY A “ SM A LL BUSINE SS CO RP O R ATIO N ” ?

Paragraph39(1)(c)requiresthatthepropertyuponwhichthebusinessinvestmentlossisclaimedbeeither“ashareofthecapitalstockofasmallbusinesscorporation”89or

85 2005DTC743(TCC).

86 Ibid.,atparagraphs15-16.

87 Supranote47,atparagraph21;seealsoTaylor,infranote164.TheTaxCourtinRichexpresseditsreservationsaboutapplyingsuchastringentstandardinthecircumstancesofthecasebeforethecourt(paragraph22).Theissueofinvestmentsinthebusinessesoffamilymemberswillbediscussedatlengthinalatersectionofthearticleinthecontextofthesubparagraph40(2)(g)(ii)purposerequirement.

88 Supranote45,atparagraph35.

89 Subparagraph39(1)(c)(iii).

246 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

“adebtowingtothetaxpayerbyaCanadian-controlledprivatecorporation...thatis...asmallbusinesscorporation.”90Thedefinitionofa“smallbusinesscorpora-tion,”containedinsubsection248(1),isthusakeyelementofanABILclaim.Agreatmanycasesinvolvethegovernment’schallengeofanABILdeductiononthegroundthattheissuingentitywasnotanSBCbydefinition—thatis,wasnotaCanadian-controlledprivatecorporation(CCPC)whoseassetsareusedprincipallyinanactivebusinesscarriedonprimarilyinCanada.91

Acomprehensivetreatmentoftheconceptandjurisprudenceofcorporatecontrolisbeyondthescopeofthisarticle;however,thereareseveralABILcaseswherethetaxpayer’sclaimwaschallengedonthegroundthatthecorporationinwhichtheshareswereheldorbywhichthedebtwasowedwasnotaCCPCasdefinedinsubsection125(7).InRandhawa et al. v. The Queen,92thescantevidenceprofferedindicatedthatfundshadbeenadvancedinUSdollarstoaUScorporation(andwereinfactbeingrepaidbyaninmateinaUSprison).InBilodeau v. R,theissuewaswhetherthecor-porationwasprivatewhentwopubliccorporationsactingtogetherheldthevotingpower to elect theboardofdirectors.93Survivance (La) c. R94had an interestingoutcome,arguablyinconsistentwithlegislativeintent.Theappellant,apubliccor-poration,soldsharesinitssubsidiarytoaprivatecorporationandclaimedanABILbasedonthefactthat,pursuanttosubsection256(9),thesubsidiarywasdeemedtobeownedbytheCCPCatthebeginningofthedayofthesharesale,withtheeffectthatthedispositionoccurredatatimewhenthesubsidiarywascontrolledbyaCCPCandnotbyapubliccorporation.TheFederalCourtofAppealagreedandcouldfindnoexpressprovisiontothecontrary.95

Taxpayerswhomaybeabletosubstantiatethataninvestmentwasinfactmadecannotalwaysverifythenatureoractivitiesofthecorporationinwhichtheinvest-mentwaslost.Longerich v. The Queen96providesanexample.Thetaxpayer,actingonhisownbehalf,submittedthat“althoughhedidnothavesharesinthesecompanies

90 Clause39(1)(c)(iv)(A).

91 Wecategorized43casesunderthisissue.

92 2001DTC382(TCC).SeealsoLabell v. R,[2000]4CTC2495(TCC),andRobertson v. The Queen,2002DTC3834(TCC).

93 [2000]1CTC2888(TCC).Acasewithsimilarfactsarisingtodaywouldbesubjecttoparagraph(b)ofthedefinitionof“Canadian-controlledprivatecorporation”insubsection125(7).ThisprovisionreversestheruleinSilicon Graphics Limited v. The Queen,2002DTC7112(FCA).SeealsoStriefel v. R,[1999]3CTC2684(TCC),wherethecorporation,previouslyanSBC,hadbeenacquiredbyapubliccompanytwoyearsbeforetheABIL-claimyear.

94 [2007]1CTC189(FCA).

95 Ibid.,atparagraph62:“[S]ubsection256(9)statesaruleofgeneralapplicationastothetimeatwhichcontrolisacquired,andthisruleappliesforthepurposesoftheActunlessitisexpresslyoverridden.Ihavefoundnoprovisionthatwouldshieldtheappellantfromtheapplicationofthisrule.”

96 2004DTC2980(TCC).

substantiating an abil deduction n 247

theamountsheadvancedrepresentedadebteventhoughtherewasnoloandocu-mentationandno interestpayable.”97Hemade the investment“believing itwasmadewiththetwoCanadiancorporations. . .andthattheyweresmallbusinesscorporations.”98Infact,thefundswerebeingfunnelledtoaHongKongcorporationandclearlycouldnotbetracedtoaninvestmentinanactivebusinessinCanada.ThetaxpayerthenwentontoarguethatsincethetwoCanadiancorporationshadlostthemonieshehadadvancedtothem,theywereinfactcarryingonanactivebusinessinCanada—thatis,thebusinessofdefraudingtheirinvestors.AlthoughthisargumentfailedforthetaxpayerinLongerich,itisnotwithoutsubstance,asshownbythe2004decisioninJohnston v. The Queen.99TheFederalCourtofAppealwasunabletoconcludethattheTaxCourthaderredinacceptingtheappellant’ssub-missionthatthecorporation“wasintheactivebusinessofdefrauding,”usinganelaboratepyramidschemewithover200participants.Theillegalnatureofthebusi-nessdidnothindertheinvestor’sABILclaim:

Thefactthatsuchactivitieswerecriminaldoesnotpreventthemfrombeingcharacter-izedasa“business”forincometaxpurposes.DuringtheperiodinquestionWSLhademployees,premises,warehousesandinventoryandwasengagedinbuyingandsellingmerchandise.Italsohadmoney,albeitadvancesfrompersonsenteringjointventures.Theseassetswereusedtoperpetratefraudonthosepersons.Iconclude,therefore,thatWSLwasusingitsassetsinthebusinessofenticinganddefraudingco-venturers.100

Asnotedabove,theassetsofanSBCmustbeusedprincipallyinanactivebusi-nesscarriedonprimarilyinCanada.Accordingly,theFederalCourtofAppealinFillion v. Canada101hadnotroubledismissingtheABILclaimofataxpayerwhohadbought sharesof a companyallof the assetsofwhichwere located inMali andwhichcarriedonallofitsactivitiesthere.

An“activebusiness”isdefined,inpart,tobe“anybusinesscarriedonbyatax-payerresidentinCanada...otherthanaspecifiedinvestmentbusiness”;a“specifiedinvestmentbusiness” (SIB) isdefined tobe abusiness the “principalpurpose”ofwhichistoderiveincomefromproperty.102MostofthejurisprudenceintheSBCcategoryinvolvestheclaimbytheministerthattheissuingcorporation,althoughaCCPC,wasinfactanSIB.Theassessmentmosttypicallyallegesthatthecorporation’sprincipalpurposewastoproduceincomefromproperty;mostoftenthetaxpayer’s

97 Ibid.,atparagraph2.

98 Ibid.

99 2000DTC1864(TCC).

100 Ibid.,atparagraph62.SeealsoLangille v. The Queen,2009DTC1103(TCC),wherethetaxpayer,anotherindividualdefraudedbyWSL,wasalsosuccessfulonthesameissue.

101 58DTC6579(FCA).

102 Seesubsection248(1),thedefinitionof“activebusiness,”andsubsection125(7),thedefinitionof“specifiedinvestmentbusiness.”

248 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

responseisthatthecorporation’sprincipalpurposewasinsteadeithertoearnincomefromabusinessortobuyandresellpropertytoproducecapitalgain.Inarecentcaseonthisissue,Glynn v. R,103theappellanthadinheritedahouse,whichshethentransferredtoapreviouslydormantcorporation(“TOI”).Whenthetaxpayer’sstatedintention of using the house as a bed and breakfast failed to materialize,104 TOIrentedthehouseoutinstead.Afterfiveyearsofrentalincomeasitssolesourceofrevenue,TOIsoldthehouseandceasedoperating.TheappellantclaimedanABILofapproximately$36,000.Thecourt’sanalysisfocusedontheprincipalpurposeofthecorporationandbeganbystatingthatthetestfordeterminingprincipalpurpose“isgenerally considered as being what the corporation actually does and what itssourceofincomeis.”105Inthediscussionthatfollows,wewillexaminetheextenttowhichthisstatementaccuratelyexpressestheapproachtakeninthecaselaw.ThecourtinGlynnseemstobesayingthatwherethecorporationengagesinactivitythatgenerallyproduces incomefromproperty,andthatactivity in factproducesincomefromproperty,thecorporationwillbecarryingonaSIBandnobusinessinvestmentlosswillbeallowed.Whilethiswouldbeaharshtest,itwouldalsobeaneasyonetoapply.

InlightoftheSBCrequirementsandtherelatedcaselaw,adviserswillneedtoconsiderthefollowingquestions:

1. Canthetaxpayersucceedwhencorporatedocumentationcontradictshisorherstatedintention?

2. In determining the principal purpose of the business, whose intention isrelevant?

3. Whatistherelevanttimeperiodforthedeterminationofprincipalpurpose? 4. Wasthecorporationcarryingonanactivebusiness?

1. Can the Taxpayer Succeed When Corporate Documentation Contradicts His or Her Stated Intention?

Havingreviewedtheprecedentcaselaw,itseemstousthattheprincipalpurposetestisnotasharsh,norisitnearlyaseasytoexpressortoapply,assuggestedbythecourtinGlynn.The1992judgmentinEd Sinclair Construction & Supplies Ltd. et al. v. MNR106addressedtheissueofabusiness’sprincipalpurposeinapplyingtheSIBdefinitionunderthesmallbusinessdeductionprovisions.Whenaskedtoweighthe taxpayer’s testimonyagainst thehardevidenceof thecorporation’sactivities,BowmanJcitedwithapprovaltheapproachtakeninanearlierTaxCourtdecision:

103 [2007]3CTC2172(TCC).

104 Thechangeinintentionwasattributedto“achangeinparentalresponsibilitiesfortheappellantandherspouse.”Ibid.,atparagraph5.

105 Ibid.,atparagraph13.

106 92DTC1163(TCC).

substantiating an abil deduction n 249

Indeterminingthe“principalpurpose”ofabusinesscarriedonbyacorporationthestatedobjectofthepersonwhocarriesitonisnotnecessarilytheonly,oreventhemostimportant,criterion.Ofcriticalimportanceiswhatthecorporationinfactdoesandwhatitssourcesofincomeare.107

Thecorporation’sfinancialstatementsrevealedthat“ineachyear,mortgagesre-ceivableandrentalpropertiesmadeupwelloverfiftypercentofthevalueofthecompany’sassets”and“theprincipalportionoftherevenuesoftheAppellantwasderivedfromrentalsandinterest”;accordingly,BowmanJconcludedthat“theprin-cipalpurposeofthebusinessofProsperousInvestments...wastoderiveincomefromproperty.”108

InGascoigne v. R,109 thecourtdidnotacceptthetaxpayer’stestimonythatthemainintentionofthecorporation,Triwest,wastosellpropertiesandthattheprop-ertieswererentedoutonlytosubsidizetheoperationuntilsalescouldbemade.Instead, the court found the contradicting documentation more persuasive: thepropertiesweretreatedforaccountingpurposesasfixedassets;rentalincomewasgenerated;disposalswerereportedascapitalgains;and,onthetaxreturn,Triwest’sbusinesswasspecifiedas“rentals.”Thedocumentedevidencespokemoreloudlyofthecorporation’sprincipalpurposethanthetaxpayer’sassertions.

TheintentionofTriwestasmanifestedbytheactionsofthedirectingminds,includingtheappellant,mustbeassessedonthebasisofeventsastheyunfoldedandbyresortingtowhatthecorporationdid,includinglookingatthemannerofreportingincometotheMinisteronaconsistentbasisandhowaccountingwasdoneforinternalpurposes.110

InGill et al. v. MNR,111thetaxpayersinvestedinacorporation,Homebank,whichconstructeda17-unit stripmallwith the intentionof selling itonce itwas fullyleased.Homebankwentintoreceivershipsoonafterlistingthepropertyforsale.Theinvestmentwent“bad”fiveyearsafterthelandhadbeenpurchasedandthreeyearsafterconstructionhadbeencompleted.Onceagain,thecourtallowedthefi-nancialresultsandfinancialstatementstostandasevidenceforthecorporation’sprincipalpurposeandtotrumpthetaxpayers’testimonyastowhytheyenteredintotheinvestment.

TheonlyincomeearnedbyHomebankwastherentalincomefromthetenantsintheshoppingplaza,interestsontherentaldepositsandamanagementfee....Further-more,thefinancialstatementsofHomebanklistedthepropertyasafixedcapitalassetandtheaccording[sic]depreciation(amortization)wasdeducted.112

107 Ibid.,at1165,referringtoBen Barbary Co. v. MNR,[1989]1CTC2364(TCC).108 Sinclair Construction,supranote106,at1166.109 1996CarswellNat2839.110 Ibid.,atparagraph24.111 98DTC2048(TCC).112 Ibid.,atparagraph30.

250 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

Similarly,inCapogreco v. R,113therealityoftheresultssimplyovershadowedthetaxpayer’sclaimofanactivebusiness.Thetaxpayerarguedthat“itnotonlyhadrentalincomebutthatitalsointendedtoobtainothercompaniesandotherbusi-nessestooccupythepremises.”114CounselfortheministerreliedonGill,andthecourtagreed.

Theonlyincomeearnedbythecorporationtherewasrentalincome,andtheprincipalpurposeofthecorporationwastoderiveincomefromproperty.Thesamecanbesaidofthecaseatbar....

[T]heCompanyinquestioninthiscaseleasedabuildingandtheonlysourceofincomewasrentalincome.Itwascarryingona“specifiedinvestmentbusiness”andnotanactivebusiness.115

Ontheotherhand,anumberoftaxpayershavebeenabletosuccessfullycontra-dicttherealityoftheirresults.InGeropoulos v. R,116thetaxpayerwasa25percentshareholderinacorporation(Woodstock)thatwasincorporatedtopursueashoppingmalldevelopment.Whentheprojectfailedtomaterializeowingtotherejectionofarezoningapplication,Woodstockwasrenderedinsolvent.ThetaxpayerclaimedanABILforfundshehadloanedtothecorporation.Thegovernmentrejectedthe“activebusiness”designationonthebasisthat,althoughthepartiestookstepstoputabusinessinplace,“nobusinessassuchmaterialized.”ThecourtreadilyacceptedtestimonyofWoodstock’s“desire”andwhatitwasorwasnot“lookingfor,”eventhoughtherewascontradictorydocumentaryevidence,andconcluded:

WhileitisafactthattheCo-Ownersagreementspeaksofholdingtheprojectforin-vestmentpurposes,Butcher’stestimony,whichIaccept,clearlynegatesthatintentionvis-à-visWoodstock.117

ItmightbearguedthattheresultinGeropouloscanbedistinguishedfrommanyoftheothercasesonthispoint,onthebasisthattheWoodstockpropertyneverproducedanyrentalincome.Consider,then,thecaseofFautley v. R.118Thetaxpayer,Fautley, transferredhishome tohis corporation,FautleyTowersLtd., and thenenteredintoanagreementtogiveaMr.Peelanoptiontobuy.Peelcouldnotraisethemoneytobuy,soinsteadhecontinuedtooccupythehomeandpayrent.Theminister’spositionwassimplyput:therewasnoactivebusiness,and“theearningofrentsfromtheProperty[was]anindicatorthattheCompanywasoperatinga

113 [2001]4CTC2326(TCC).

114 Ibid.,atparagraph47.

115 Ibid.,atparagraphs36and38.

116 [1998]3CTC2384(TCC).

117 Ibid.,atparagraph21.ButcherwasanotherWoodstockshareholder.

118 [2002]3CTC2098(TCC).

substantiating an abil deduction n 251

specifiedinvestmentbusiness.”119Thiscouldbeasimplecaseofestablishingprincipalpurpose,aswesawinthecasesdiscussedabove,onthebasisof“whatthecorporationactuallydoesandwhatitssourceofincomeis.”120Infact,thecourtwaspersuadedbythetaxpayer’stestimonythat

therentreceiptsweremerelypartofthedealwithPeelandthemainthrustofthatagreement was to sell the Property and moreover that the overall activities of theCompanyweretodeveloppropertiesandnottoholdsameforrental.121

Inresponsetothetaxpayer’sappealinBarrette c. La Reine,122theCrownreliedonthecourttoagainconstructtheinvesteecorporation’sprincipalpurposefromwhatthecorporationdidandwhatitssourceofincomewas.Essentially,theCrown’spositionwasthat,becausetheonlyincomedeclaredbythecorporation(Diese)wasrentalincome,thecorporationwasengagedinaSIB.However,thecourtwasnotinclinedtoagree.Despitethedocumentedevidence—thecorporation’ssoleassetwasthebuildingsshownonthefinancialstatementsascapitalproperty,capitalcostallow-ancewasclaimed,andthecompany’saccountantstatedonthetaxreturnthatDiesewasengagedintherentalofproperty—andeventhoughthecourtfoundthedetailsofattemptstosellthepropertyforaprofittobe“somewhatvague,”123theCrown’sfailuretospeaktothe“trueintentionofthetaxpayer”wasfataltoitscase.Instead,thecourtembracedthepositionofoneofthefourequalshareholders,whowasbyoccupationarealestateagentandwhosubmittedherownversionofthefinancialstatements.ArchambaultJconcluded:

IampersuadedthatiftheaccountanthadbeenproperlyapprisedofthetrueintentionofDiese,hewouldnothavedescribeditsprincipalactivityashedid.Hewouldnothaveenteredthebuildinginthestatementasacapitalasset,andhewouldnothaveclaimedacapitalcostallowance.Itismyopinionthatthefinancialstatementpreparedbythejointshareholderwholocatedthebuilding,negotiateditspurchase,andplayedaleadershiproleinDiesehasamoresignificantprobativevaluethanthesimplede-scriptionmadebytheaccountantinthefinancialstatements.124

Unfortunately,theaboveanalysisfailstoprovideadefinitiveanswertotheques-tionweposed at thebeginningof this section. It appears that the taxpayer cansucceedwhencorporatedocumentationcontradictshisorherstatedintention—but,thenagain,maybenot.Thebest-casescenarioariseswhenthetaxpayer,the

119 Ibid.,atparagraph6.

120 Glynn,supranote103,atparagraph13.

121 Supranote118,atparagraph6.

122 2004TCC437.

123 Ibid.,atparagraph36.

124 Ibid.,atparagraph34.

252 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

paperwork,and theobjective indicatorsaremutuallycorroborativeofabusinessintention,astheywere,forexample,inBelzile v. The Queen.125Thetaxpayerandanunnamedpartytogetherownedthreeseparatecorporations;theoneinquestionwasreferredtoas“9005.”Inthemid-1990s,eachofthethreecorporationsbuiltamulti-unitapartmentbuilding.Twoofthecorporationssoldtheirbuildingsrightaway;however,9005wasunabletosellits8-unitbuildingand,accordingtothetaxpayer,renteditoutinthemeantimeto“stemthelosses.”Thisfactsituationisreminis-centofGascoigneandhisinvestmentinTriwest,discussedabove.126However,inBelzile,thebuildingwaslistedasinventory(notafixedasset),andthecorporationidentified itsactivityas“construction.”The9005corporationwasheld tobeanactivebusiness.

TheappellanttestifiedinastraightforwardandhonestmannerandIaccepthisversionofthefacts.Thiswasnothisfirstbusinessofthiskind,anditisclearfrom9005’sarti-clesthatitseconomicactivitywasconstruction,asitwaswiththeothercorporationsthattheappellantestablishedearlier.9005’sfinancialstatement...statesthatthecor-poration’sinventoryconsistedofarentalbuildingintendedforresale.While9005’sincomewas fromrentalsofproperty, thecorporationexperiencedonly losses.Theincome,andtheadvancesmadebytheappellant,merelyservedtokeepeverythinginorderuntilthesaleofthebuilding,whichspecialcircumstancesmadedifficult.9005neverchangedvocationsandtheintentionwasalwaystosellthebuilding.127

2. In Determining the Principal Purpose of the Business, Whose Intention Is Relevant?

Returningtothe2007Glynndecision,weseethecourtapplyinganoft-citedpas-sagefromthe1990caseofMayon Investments Inc. et al. v. MNR.128AlthoughMayonwasnotanABILcase,itrequiredaninterpretationofthe“principalpurpose”testundertheSIBdefinitionforthepurposesofthesmallbusinessdeduction.AccordingtoBruléJ,“theprincipalpurposeofwhichistoderiveincomefromproperty”inrespectofthebusinessofacorporationmeansthat

thesourceofrevenue,thenatureoftheassetsheldandthe purpose of the corporationaretoderiveincomefromproperty.129

Isthepurposeofthecorporationindeedthesameasthepurposeofitsbusiness?Andareeitherorbothofthesethesameastheintentionofthetaxpayer?Althoughtheanswerisunclear,perhapsthereisamethodtobedetectedinthecasesonthis

125 2006DTC2540(TCC).

126 Seesupranote109andtherelatedtext.

127 Supranote125,atparagraph19.

128 91DTC364(TCC).

129 Ibid.,at369(emphasisadded).

substantiating an abil deduction n 253

issue.Generally,wherethetaxpayeriseitherthesoleshareholder,oneofasmallgroupofrelatedshareholders,130orthe“directingmind”oftheinvesteecorporation,nodistinctionisseentoexistasbetweentheintentionofthetaxpayer,thecorpora-tion,and/orthecorporation’sbusiness.Compare,forexample,thecasesofGascoigneandGill,bothdiscussedabove.InGascoigne,thetaxpayer,acharteredaccountant,wasoneofthreeshareholdersinTriwest.Thecourthadnotroublereceivinghisevidenceregarding“the intentionofTriwestasmanifestedby theactionsof thedirectingmindsincludingtheappellant.”131Similarly,inGeropoulos,wheretheap-pellantwasoneofthreeshareholdersinWoodstock(andanothershareholderwashisbrother),thecourtspokeoftheintentionsoftheappellantandthoseofWood-stockasbeingoneandthesame.132Theapproachwasarguably takenfurther inBelzile,wherethetaxpayer(alawyer)ownedtheinvesteecorporation,9005,withoneotherperson,withwhomhealsoownedtwoothercorporations.Thecourt’sanalysisinarrivingatthe“principalpurpose”of9005appearedtoincludeconsider-ationoftheactivitiesoftheothertwoassociatedcorporations.133

Incontrast,considerGill.134Theappellants(“SG”and“IG”)werenotrelatedtothe investee corporation (“Homebank”). Together they owned 16 percent ofHomebank;thecontrollinginterestwasheldbyaMr.andMrs.Benet.AlthoughtheBenetswerenotbeforethecourt,BruléJconsiderednotonlytheirintentionsre-gardingHomebank,butalso,“asanaside,”evidenceoftheirbusinessactivities:

[I]tisthe“principalpurpose”ofthebusinessandnotnecessarilythe“principalpur-pose”of the individual taxpayer thatmustbeconsidered indeterminingwhetheracorporationisa“specifiedinvestmentbusiness.”SGandIGhada16%interestintheoperations of Homebank. Mr. Benet and his wife held the controlling interest of52%....Anyinquiryintothe“principalpurpose”ofthecorporationwouldhavetoconsidertheintentionofMr.andMrs.Benet.Mr.Benetwasthedriving forcebehindhisowncorporation,Sampuran,aswell asHomebank.The“principalpurpose”ofHomebank,asanentireentity,mustbeconsidered.TheMinisterdidnotmakeanyinquiriesintotheintentionofMr.BenetwithrespecttoHomebank.TheCourtbe-lievesthattheprofitmadeonSampuran’ssaleofapreviousshoppingdevelopmentisrelevanttothecaseathand.135

PerhapsthemostdifficultcasetoreconcileonthispointisBarrette.136Theap-pellants,BarretteandBerard,bothbuildinginspectors,eachownedone-quarterof

130 Inthiscontext,themeaningof“related”isnotnecessarilyasdefinedintheAct.

131 Supranote109,atparagraph124.

132 Supranote116,atparagraph21.

133 Supranote125,atparagraphs16-20.

134 Supranote111.

135 Ibid.,atparagraph33(emphasisadded).

136 Supranote122.

254 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

thecorporationknownasDiese.Anadditionalone-quarterwasownedbyBerard’ssister-in-law,Beaudry,arealestateagent.ThecourteasilyequatedtheprincipalpurposeofDiesewiththeintentionsofBarretteandBerard:

Itisimportant...todeterminetheprincipalpurpose,which,obviously,dependsonthe true intention of the taxpayer.137

ThecourtthenturnedtoBeaudry,againnotapartytotheaction,todeterminetheprincipalpurposeofDiese’sbusiness.

Giventheirprofessionalexperienceasbuildinginspectors,theAppellantsdidnothavetheknowledgerequiredforspeculation,nordidtheyhavetheknowledgerequiredforcommercialleasing.TheyreliedonMs.Beaudry,whowastheveritableinstigatorofthisprojectandthepersonwhodirectedit,atleastattheoutset.HerintentionissignificantforthepurposeofdeterminingtheintentofDieseinthepursuitofthisproject.138

3. What Is the Relevant Time Period for the Determination of Principal Purpose?

Establishing the relevant timeperiod for theprincipalpurposedetermination isrelativelystraightforward.Asageneral rule, thecasesconsiderboththeoriginalpurposeofthebusinessandthatmanifestedinthetaxationyearsatissue,assug-gestedinInterpretation BulletinIT-73R6:

Theprincipalpurposeofacorporation’sbusinessmust be determined annuallyafterallthefactsrelatingtothatbusinesscarriedonbythatcorporationinthatyearhavebeenconsideredandanalyzed.Includedinthisevaluationshouldbesuchthingsas:

(a) the purpose for which the business was originally commenced;(b) thehistoryandevolutionofitsoperations,includingchanges in its mode of oper-

ation and purpose of existence;and(c) themannerinwhichthebusinessisconducted.139

In both Gascoigne and Glynn, the principal purpose of the corporation hadchangedover time; inneither casedid thiswork to the taxpayer’s advantage. InBelzile,thecourtfoundthat

9005neverintendedtoderiverentalincomeonceitcompletedthebuildinginques-tion,and...thisfactremainedtruethroughouttheyearsinwhich9005ownedthebuilding,includingtheyearinissue.Therewasnochangeofdirection.140

137 Ibid.,atparagraph28(emphasisadded).

138 Ibid.,atparagraph33.

139 IT-73R6,“TheSmallBusinessDeduction,”March25,2002,paragraph14(emphasisadded),quotedinBelzile,supranote125.

140 Belzile,supranote125,atparagraph18.

substantiating an abil deduction n 255

4. Was the Corporation Carrying On an Active Business?

Oftenthetaxpayerisfacedwiththeargumentthatthecorporation’sbusinessisnotbeingcarriedon,eitherbecauseitnevercommencedorbecauseithadalreadyceased.Foranexampleoftheformer,considerBoulanger et al. v. The Queen.141Thetaxpayers,BoulangerandDufour,claimedanABILrelatingtoamortgageextendedtoanum-beredcompany,referredtoas“170663.”Thecorporationhadacquiredthreelotsoflandtoconstructanautomotivebusiness.Anoverallplanwasdeveloped,abuildingpermitobtained,surveysprepared,andmeetingsheldwithengineersandarchitectswhopreparedplans for abuilding;however,whenbankfinancingwasdenied, aportion(almosthalf )ofthelandwassoldofftoaconstructioncompany,leavingtheundevelopedlandandthereceivablefromtheconstructioncompanyas170663’sonlyassets.Inlightofthissequenceofevents,thequestionforthecourtwaswhetherthecorporationhadstartedthebusiness,andifso,whetherthatbusinesswasactive.

TheTaxCourtconfirmedtheminister’sassessmentonthebasisthat

expensesrelatingtopreliminarystagesinestablishingabusinessthatdoesnotexistdonotgiverisetoabusinesslossifthosestepsdonotgobeyondtheprojectstage....Thepurposeofall[thecorporation’s]...activitieswastoestablishthestructureofthebusinessitself,whichultimatelyneversawthelightofday.142

Inconsideringthetaxpayers’appeal,theFederalCourtofAppealreliedheavilyonthewordsofDesjardins J inthe2001Hudondecisionandherdescriptionoftheproblem:

[A]toneendofthespectrumtherearebusinesseswhichhavenotbegunoperationsandattheothertherearedormantbusinesses,whileinbetweentherearemanyactiv-ities“whicharesignsthatacompanyisoperatingandwhichshouldfallwithinthespectrumoftheconceptofcarryingonbusiness,eventhough,forexample,theactivitiesare carried on for the purpose of reaching an agreement which eventually is notreachedoreventhoughtheydonotresultintheearningofincome.”143

Thecourt foundthat theappellants’proposedbusiness lackedanorganizationalstructureandotherkeyindiciaofanactivebusinesswereabsent—employees,marketresearch,cost-benefitanalysis,andtheability“toconductanymajortransactionwithrespecttothetypeofbusinessitwassupposedtocarryon.”144Thefactthattherewasnoincomefromtheallegedlyactivebusinesswasdescribedasrelevantbutnotinitselfdeterminative.145

141 2003DTC1277(TCC).

142 Ibid.,atparagraphs23and24.

143 Boulanger et al. v. The Queen,2004DTC6192,atparagraph5(FCA),quotingfromHudon et al. v. The Queen,2001DTC5630,atparagraph62(FCA).

144 Boulanger,supranote143,atparagraph6.

145 Ibid.,atparagraph7.

256 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

ThetaxpayerinO’Neill v. The Queen146sufferedasimilarfatein2000.TheTaxCourtconcludedthat“themoneywasspentingoodfaithwiththehopeandexpect-ationthatsomewheredowntheroadtheAppellantandhispartnerwouldbeinapositiontocommencethebusinessandtoearnaprofitfromit,butthatmomenthadnotyetarrived.”147O’Neillandhispartnerco-ownedacorporation(“C&C”)andhadpurchasedanaircraftwiththeplantostartupahuntinglodgebusiness.Theplanewouldbeusedtoflypatronsinandoutoftheremoteproperty.Althoughtheappellantalreadyhadoccupancyrightstothelandandhadbuiltacabinonit,keyindiciawereabsentwhenthecompany’sonlyasset,theplane,wasdestroyedinacrash.Therewasnowrittenplan,nocompanybankaccount,nobusinesslicence(infact,noknowledgeofthelicencerequirements),nomarketresearch,nodrawingsfortheplannedexpansionoftheexistingcabin,norevenuefromitsoccupancy,andnostaff.Tothesubmissionthatthepurchaseoftheaircraftputtheappellantandhispartnerinbusiness,thecourtresponded:

TheCourtdoesnotaccepttheargumentofcounselfortheAppellantthatatthetimetheBeaveraircraftwaslost,theAppellanthadreachedsuchastageofdevelopmentinitsenterprisethatitcouldhavebeenreferredtoasa“business”byanyreasonabledef-initionofthattermascontemplatedbytheAct.Itisnotananswertothisdeficiencytosaythatthisbusinesswaslikeanyotherandthatitstartedslowly,inanunsophisti-catedmannerandatapaceatwhichthedeveloperscouldaffordwithoutborrowinglargesumsofmoney.Thequestionasalwaysis,wasthereabusinessattherelevanttime?Inthecaseatbar,wasthereaplan?Didtheyhavetherequisiteequipment?Didtheyhavetherequisitelicence?Weretheypreparedandabletocarryonthebusinessofoutfittingatthetimethattheplanewaslost?TheCourtmustfindconclusivelythattheywerenot.148

At the other end of the spectrum are those cases where, in the tax assessor’sopinion,thebusinessthatwasbeingcarriedonhasceased.Consider,forexample,Proulx-Drouin v. The Queen.149In1990,thetaxpayeractedasguarantorforadebtowedbyherhusband’sconstructioncompany(“Société”)andpledgedherhomeascollateral.SociétéhadbeenformedtorenovateandexpandacommercialpropertyontheTrans-CanadaHighway inorder tomeet therequirementsofanexistingtenant.ThetenantwentbankruptandSociétéwasnotgettingpaid.By1996,Sociétéwasindefaultontheloan.Thetaxpayerwascalledonherguarantee,Sociétéwasdissolved,andthehomewassold.Onher1997taxreturn,thetaxpayerclaimedanABILinrespectofherlossontheguarantee.Forherclaimtosucceed,theapplica-tionofsubsection39(12)requiredthatthecorporationwhosedebtwasguaranteedwasanSBC“atanytimeinthe12monthsbeforethetimeanamountfirstbecame

146 2000DTC2631(TCC).

147 Ibid.,atparagraph158.

148 Ibid.,atparagraph154.

149 Proulx-Drouin v. The Queen,2005DTC487(TCC).

substantiating an abil deduction n 257

payablebythetaxpayer.”Onthefacts,theTaxCourtdeterminedthattherelevanttimeperiodwasthe12monthsprecedingMarch5,1996(thedatethatthebankfilednoticeof itsclaimagainstProulx-DrouinasSociété’sguarantor).150Proulx-Drouin’s husband testified that in 1995, although Société no longer carried onconstructionactivities (whichhad long since ceased), the companycontinued tocarryonanactivebusiness,providingmanagementservicestotworelatedcorpor-ations owned by him, his wife, and other family members. However, the courtfoundthatthedocumentaryevidencedidnotsubstantiatehisclaim:

ThereisnodisinterestedevidenceofSociétécarryingonabusinessafter1995.De-positsofchequesintoabankaccountarenotproofofthecarryingonofabusiness,inparticularwhenthemakerofthecheque,thepayeeofthechequeandthepersoninwhoseaccountthechequeisdepositeddonotdealwitheachotheratarm’slength.TothisareaddedthefactsthatSociété’sfinancialstatementsandincometaxreturnfor1995shownogrossoranyincomeandnotaxreturnhasbeenfiledforanytaxationyearafter1995.151

Anotherfatalfactorthatindicatesthecessationofactivebusinessistheabsenceofbusinessassets.InYaworowski v. R,152theappellantandhiswifehadoperatedamotelbusinesslocatedonahighway,butbytheyearinquestion(1996),thehigh-wayhadbeenrerouted,thecompanyhadbecomedormant,andtheappellant’sonlyinvestmentconsistedofexpensesheincurredinmaintainingthemotelproperty,inwhichhethenlived.TheTaxCourtfoundthat

[t]he evidence is quite clear that the Appellant’s operation does not constitute thecarryingonofanactivebusiness.Thecorporationhadceasedbusinessbefore1990.Therewerenosalesreportedinthefinancialstatementforthatyear.Therewasnoopeninginventoryandnopurchases.In1992,thetaxpayerhimself,astheprepareroftheincometaxreturnforthecorporation,describeditasinactive.In1995,thecorpor-ationwasdissolved.Theevidenceisquiteclearthatnoneoftheremainingassetswereused inabusiness,but ratherwerebeingusedpersonallyby theAppellantandhisfamily.153

InCraig v. R,154theassetsofthetaxpayer’scorporationhadbeenseizedbyitslandlord.Althoughthetaxpayerhadretainedlawyerstodefeattheseizureandwascontinuingtolookforalternatepremises,theTaxCourtheldthatthiswasnotsuf-ficienttoconstitutecarryingonanactivebusiness:

150 Ibid.,atparagraph30.Foranotherexampleoftheapplicationofthe12-monthruleinsubsection39(12),seeArmstrong v. R,97DTC3263(TCC).

151 Proulx-Drouin,supranote149,atparagraph32.

152 [2000]3CTC2665(TCC).

153 Ibid.,atparagraph4.

154 [2003]2CTC2033(TCC).

258 n canadian tax journal / revue fiscale canadienne (2010) vol. 58, no 2

WhenonlytheseactivitiesarecarriedonhowcanonesaythatallorsubstantiallyallofthefairmarketvalueoftheassetswereusedprincipallyinanactivebusinesscarriedonprimarilyinCanada.Thereferenceistoassetsbeingusedandinthepresentcasebecauseoftheseizureitwasimpossibletousetheassetsinthebusiness.155

ComparethedecisioninVogel v. The Queen.156VogelclaimedanABILonhis1988taxreturn;however,theministerconsideredthecorporationtobeinactiveonthebasisthatithadnoreportedincomeandnosignificantexpenses.Thetaxpayer’spos-itionwasthatthecorporation,atraderincommodities,was“insuspense,”waitingforthepriceofoiltoincrease.Notwithstandingthetaxpayer’sfilingofa“DeclarationofNon-OperatingStatus”withtheAlbertagovernmentin1986,theTaxCourtagreed:

For1987and1988noincomewasproduced.TheevidenceshowstheCompany,albeit“insuspense,”wasstillactive.Therewereassets,liabilitiesandcontractstopursue.Further,duringthisperiodoftimesomeminimalexpenseswereincurredastheCom-panytriedtonegotiatecontractsonalocalbasisinAlberta.TheCompanyasan“activebusiness”didnotceaseuntil[theCompanywasstruckfromtheCorporateRegistryon]October31,1988.ThefinaldatewasconfirmedbyaletterfromtheVicePresidentoftheCompanytotheAppellantdatedNovember30,1988.Thus,uptoNovember30,1988,theCompanywasa“smallbusinesscorporation”asallorsubstantiallyalloftheassetswereusedinan“activebusiness”carriedoninCanada.157

Furtherontheissueofcessationofbusiness,theministerlostthecaseagainstthe taxpayer inKlein v. The Queen.158Kleinowned100percentofacorporation(“Jasag”),whichowedhimapproximately$1,000andinpartnershipwithwhichheoperatedamotelandcarwash.Whenthepartnershipmetwithfinancialdifficultiesin1995,asecuredcreditorappointedareceiver-manager.Klein’seffortstoeitherremedythedefaultorfindapurchaserwereunsuccessfulandthebusinessmetwithforeclosure.TheministertookthepositionthatJasag’sassetsceasedtobeusedinanactivebusinessuponthereceiver-manager’sappointmentandthatJasagceasedtobeanSBCatthattime,disqualifyingKleinfromanABILclaimfor1996—theyearinwhichtheforeclosuretookeffectandKleinwasdeemedtohavedisposedofhisdebt.TheTaxCourtdisagreedonthefollowingbasis:

[T]heinterimreceiver-managerwasappointedtoreplacethemanageremployedbythepartnersandtoreceiveanddisburseallfundsreceivedfromtheMotel75’soper-ations.Inmyview,thisiscertainlyanindicationthattheMotel75’soperationswerestillbeingactivelycarriedonandthatthereceiver-managerwastheretooperatethebusinessinlieuoftheformermanagerappointedbythepartners.159

155 Ibid.,atparagraph12.

156 96DTC1321(TCC).

157 Ibid.,at1323-24.

158 2001DTC443(TCC).

159 Ibid.,atparagraph31.

substantiating an abil deduction n 259