Solar trends – structures, technical issues, financing ... · SolarCity CONFIDENTIAL. Which sites...

105

www.novoco.com

-

Upload

truongngoc -

Category

Documents

-

view

216 -

download

3

Transcript of Solar trends – structures, technical issues, financing ... · SolarCity CONFIDENTIAL. Which sites...

www.novoco.com

PanelistsPanelists

Arthur McDermottMike Morrison Arthur McDermottMcDermott Properties, LLC

Mike MorrisonNovogradac & Company LLP

J. William CallisonFaegre & Benson LLP

Michael NiverSolarCity Faegre & Benson LLP

Jeff NishitaNovogradac & Company LLP

Stephen EckertEckalizzi Design

[email protected] Boulder Housing [email protected]

OverviewOverview

• Solar TechnologiesSolar Technologies• Solar Tax Credits – Basics• Renewable Energy Grants• Renewable Energy Grants• Colorado Programs

Mi ll E B d• Miscellaneous – Energy Bonds• Combining Section 42 and Section 48• Developer Issues• Back-end Interest/Complex Structures

SOLAR TECHNOLOGIESSOLAR TECHNOLOGIES

Solar TechnologiesSolar Technologies

ConcentratedPhotovoltaics (PV)

Certain semiconductor

Concentrated Solar Power (CSP)

S li ht h t tmaterials (eg – silicon) create electricity

directly from sunlight

Sunlight heats water which makes steam,

which turns a turbine,hi h k l t i itwhich makes electricity

Virtually everybody who installs solar also maintains theiralso maintains their connection to the utility grid

• Also, most systems don’t generate exactly what you need at the exact time you need ity

•Grid allows you to have power at night!

www.novoco.com

have power at night!

Solar PV TechnologiesSolar PV Technologies

• While there are several sub-types of solar PVWhile there are several sub types of solar PV technology, it’s mostly interchangeable and commodity-like– Reputable vendors include Evergreen,

Sanyo, First Solar, BP, Suntech, Trina, etc.

• Choice mainly based on– cost per kWh (not just cost per Watt)– vendor warrantyy– aesthetics

Roof Sq. Ft. PV System Size

2 kHouse 4 kW

Grocery 40 k 200 kW

4 kW

Store

Large High

40 k 200 kW

Large High School 200 k 600 kW

Shopping Mall 1 Mil 1 MW

www.infinitepower.org

www.novoco.com

Morgan PlaceSystem Size 49 kW

Installed September 2008

Type Flat Roof Grand Opening withLocation Los Angeles, CA

Industry Multifamily Housing

Grand Opening with Los Angeles Mayor Villaraigosa

SolarCity CONFIDENTIAL

Valencia GardensSystem Size 13 kW

Installed October 2008

Type Flat Roof

Location San Francisco, CA

Industry Multifamily Housing

SolarCity CONFIDENTIAL

Oakland ZooSystem Size 30 kW

Installed June 2007

Type Standing Seam Metal

Location Oakland, CA

Industry Nonprofit

SolarCity CONFIDENTIAL

Capricorn HoldingsSystem Size 12 kW

Capricorn HoldingsInstalled June 2008

Type Spanish Tile

Location Palo Alto, CA

Industry Retail

SolarCity CONFIDENTIAL

eBay CampusSystem Size 685 kW

Installed March 2008

Type Non Penetrating Roof Mount

Location San Jose, CA

Industry High Tech

SolarCity CONFIDENTIAL

West LA CollegeSystem Size 356 kW

Installed January 2009

Type Carports

Location Culver City, CA

Industry Education

SolarCity CONFIDENTIAL

Montna FarmsSystem Size 394 kW

Installed August 2008

Type Ground Mount

Location Yuba City, CA

Industry Agriculture

SolarCity CONFIDENTIAL

Curtner GardensSystem Size 97 kW

Installed August 2008

Type Flat Roof

Location San Jose, CA

Industry Multifamily Housing

SolarCity CONFIDENTIAL

Grace Cathedral

System Size 6 kW

Installed October 2008

Type Historic BuildingType Historic Building

Location San Francisco, CA

Industry Houses of Worship

SolarCity CONFIDENTIAL

Otay Mesa System Size 274 kW

Border CrossingInstalled June 2008

Type Non Penetrating Roof Mount

Location San Diego, CA

Industry Government

SolarCity CONFIDENTIAL

Fenestra WinerySystem Size 19 kW

Installed April 2008

Type Comp Shingle

Location Livermore, CA

Industry Agriculture

SolarCity CONFIDENTIAL

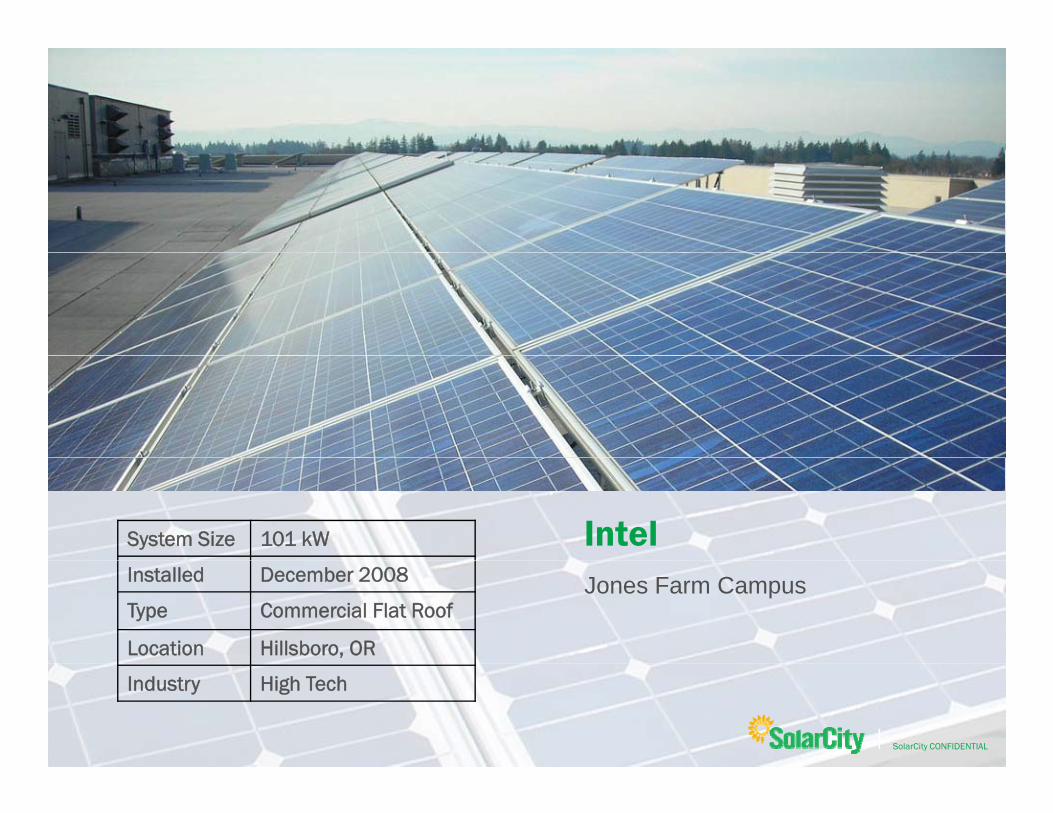

Intel System Size 101 kW

Installed December 2008

Type Commercial Flat Roof

Location Hillsboro, OR

Jones Farm Campus

Industry High Tech

SolarCity CONFIDENTIAL

Which sites have the best solar economics?Which sites have the best solar economics?Combination of these three factors:1.Lots of sun

• South/Southwest-facing buildings, no shade

2. Good local state/utility incentives• Can be 10-60% of system cost on top of theCan be 10 60% of system cost, on top of the

federal 30% credit/grant and depreciation• CA, AZ, OR, CO, New England, Ontario, TXg

3. High utility electricity rates

www.novoco.com

Where have most systems been installed?

Oregon 2%

North Carolina, 1%

Others, 5%

Where have most systems been installed?

Hawaii 4%

New York, 2%

Arizona, 2%

Connecticut, 2% Oregon, 2%

Colorado

Nevada, 5%

Hawaii, 4%

California, 61%

Colorado, 8%

New Jersey, 8%

Renewable Portfolio Standards (RPS)Renewable Portfolio Standards (RPS)

• Requirements for a certain percentage of utility power generation to come from renewable sources by a given dateby a given date

• State-mandated – Colorado’s RPS requires Investor-owned utilities to comply and produce p y pmore renewable energy -- 20% by 2020

• Colorado Electric Co-ops and Municipal Utilities p pserving over 40,000 customers must produce 10% by 2020

Solar Tax Credits – BasicsSolar Tax Credits – Basics

Solar Tax Credits – Basic RulesSolar Tax Credits – Basic Rules• Sale of electricity not required

T dit t d 100% th PIS d t• Tax credits generated 100% on the PIS date• Allocated to partners by profit percentage• 1-year carryback and 20-carry forward1 year carryback and 20 carry forward

• Passive loss and at risk rules apply

• Market dominated by corporate investors

• Change in AMT rules starting to draw individual investors

• 5 year recapture period

What is the amount of the tax credit?

Investment Tax CreditIRC Section 48

30% ofFacility Cost

S l T C dit B i R lSolar Tax Credits – Basic Rules

– ITC increased from 10% to 30% by Energy Act of 2005ITC increased from 10% to 30% by Energy Act of 2005– 30% credit now sunsets on December 31, 2016

• HERA provided an 8 year extension for Section 48HERA provided an 8 year extension for Section 48investment tax credit

• $2,000 ITC cap lifted-Residential installations - Section$2,000 ITC cap lifted Residential installations Section25D

• AMT relief – 2009AMT relief 2009

• Public Utilities may now use the tax benefits

Credit is non-refundable

No cash back

Credit is non refundable

Tax Liability Tax Credits

1 year 20 years

www.novoco.com

What costs are eligible for the credit?

Solar Tax Credits – Eligible Property Defined:

What costs are eligible for the credit?

g p y

• Equipment that uses solar energy to generate electricity

• Direct and indirect costs of installation- Design, interest expense, developer fee, other soft

costs- Portion of roofing repair? Reasonable allocationg p- Carport cost? What portion? Reasonable allocation

Installed by the taxpayer

• Acquired by taxpayer and first used by taxpayer

- Exception under IRC Sec. 50(d)(4) for sale-leasebacks

What costs are not eligible for the credit?What costs are not eligible for the credit?

• Permanent loan fees, syndication costs, etc.Permanent loan fees, syndication costs, etc.

• Costs allocated to building (portion of roof, etc.)etc.)

• Transmission lines to grid generally not eligibleGenerally not applicable to Multi-family y pp yassets

• Property used for lodgingp y g g

• Property located outside the U.S.

Solar Tax Credits – When is a FacilitySolar Tax Credits – When is a Facility Placed in Service

• “Ready and available for its intended use” – IRC

definition

• Public Utility signoff – PTO Letter

PTO: Permission to Operate– PTO: Permission to Operate

• Facility completed, licenses obtained, pre-

operational testing complete

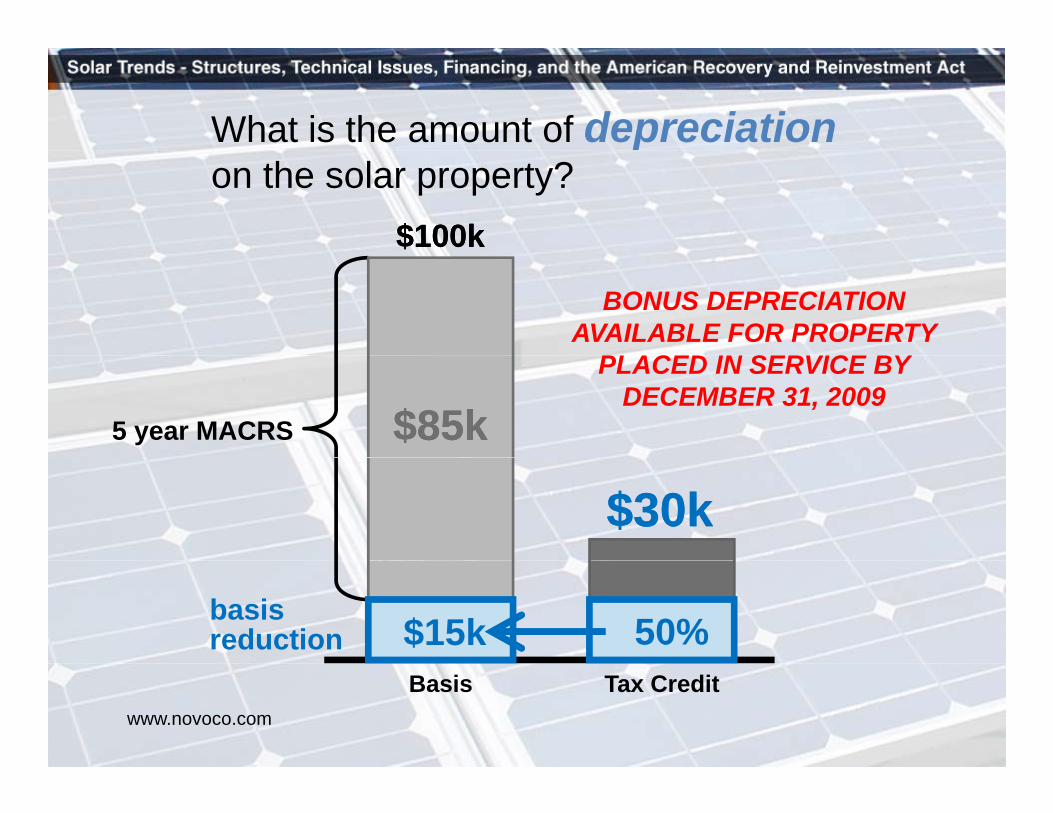

What is the amount of depreciationon the solar property?

$100k$100k

BONUS DEPRECIATION AVAILABLE FOR PROPERTY

PLACED IN SERVICE BY

5 year MACRS $85k$85kPLACED IN SERVICE BY

DECEMBER 31, 2009

$30k$30k

50% basis reduction $15k

Basis Tax Creditwww.novoco.com

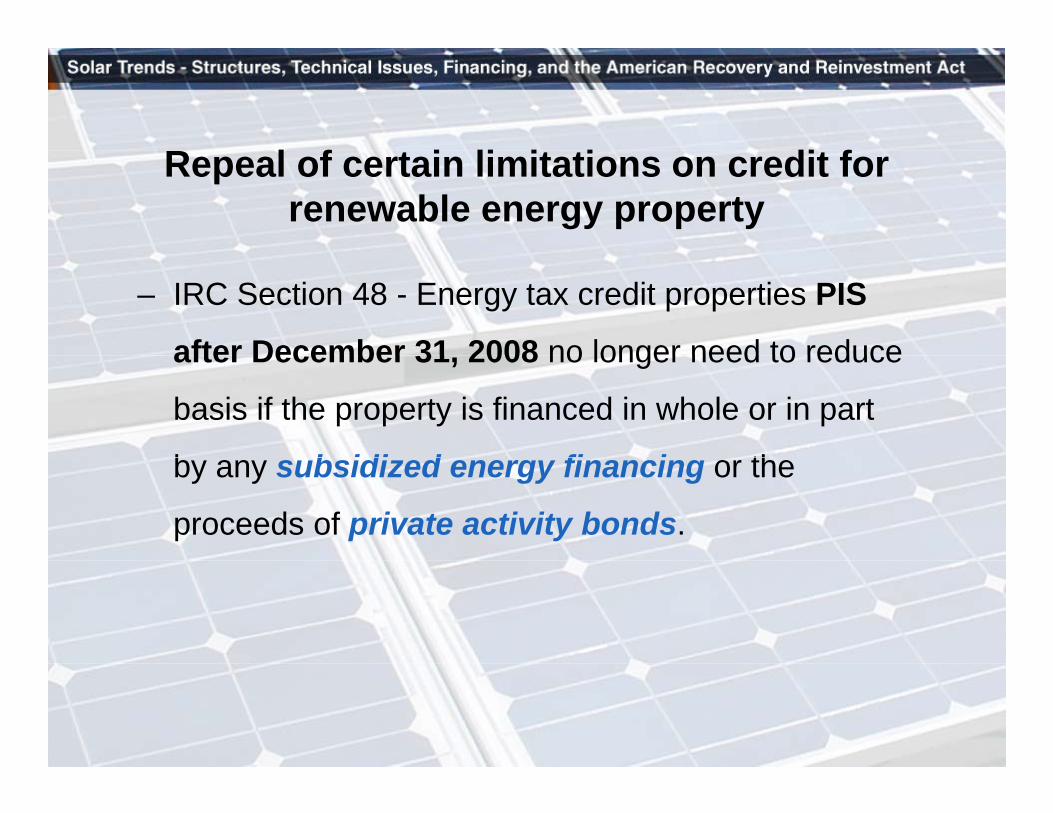

R l f i li i i di fRepeal of certain limitations on credit for renewable energy property

– IRC Section 48 - Energy tax credit properties PIS

after December 31 2008 no longer need to reduceafter December 31, 2008 no longer need to reduce

basis if the property is financed in whole or in part

b b idi d fi i thby any subsidized energy financing or the

proceeds of private activity bonds.

“subsidized energy Prior to Recovery Act of 2009subsidized energy financing” or private activity

bonds

%Prior to Recovery Act of 2009

30%

%

Basis Investment Tax Credit

“subsidized energyAfter Recovery Act of 2009

subsidized energy financing” or private activity

bonds

(property PIS after 12/31/2008)

30%

Basis Investment Tax Credit

Renewable Energy Grants

American Recovery and Reinvestment Act (“ARRA”)

H.R.1

Feb 17

AUG SEP NOVOCT DEC

2008 2009JUL JAN FEB MAR APR MAY JUN

www.novoco.com

30%

Grant = 30% or 10% of basis of facility

10%

(Subject to recapture if credits were already taken)

T G t El ti R t R l

Recapture occurs if:

Treasury Grant Election – Recapture Rules

Recapture occurs if:

1) Property ceases to be energy property2) Disposition of property to a “disqualified person” i e2) Disposition of property to a “disqualified person” i.e.

non-profit, government entity

Same recapture %’s apply as with ITC (100% 80% 60%Same recapture % s apply as with ITC (100%, 80%, 60%,40%, 20%)

Expiration of the grant 1/1/17

• Qualified fuel cellproperty

p gfor

IRC Section 48 properties30% p p y

• Solar property• Qualified small wind

energy property

/ /

30%

• Geothermal property• Qualified microturbine

t

1/1/17

property• Combined heat and power

system property• Geothermal heat pump

10%

2013 2014 2015 2016 2017 2018

p pproperty

2013 2014 2015 2016 2017 2018

Renewable Energy Grants

• Grants are not includable in the gross income of the taxpayer

Renewable Energy Grants

• Grants shall be taken into account in determining the basis of theproperty, except that the basis of such property shall be reduced underIRC Section 50(c) in the same manner as a credit allowed under IRCSection 48(a)Section 48(a)

• Property must be PIS during 2009 or 2010, or• PIS after 2010 and before the ITC termination date of January 1, 2017,

but only if the construction of such property began during 2009 or 2010but only if the construction of such property began during 2009 or 2010• Safe harbor for commencing construction:

“Physical work of a Significant Nature” incurred > 5% of the totalt f th t ( l di l d d li i ti iti )cost of the property (excluding land and preliminary activities)

• All applications must be received before October 1, 2011• The Secretary has 60 days from the later of the application for suchy y pp

grant or PIS date to fund the grant

Renewable Energy Grants

Grants cannot be made to:

Renewable Energy Grants

• Governmental bodies, political subdivisions, agencies or instrumentalities thereof

• 501(c) organizations exempt from tax under section 501(a)

• A clean renewable energy bond lender

• A cooperative electric company

• A pass-thru entity that has one of the aforementioned named as a partner

Colorado ProgramsColorado Programs

Colorado Local IncentivesColorado Local IncentivesBecause of RPS requirements, utilities increasingly

offer incentives to encourage small projectoffer incentives to encourage small-project development

Example -- XCEL

• $2/W upfront rebate (capped at $200K); and,$ p ( pp $ ); ,

• ~$0.12/kWh production incentive for 20 years

• (equivalent to ~$1.60/W when discounted back)

• Net metering benefit – each kWh of solar energy g gyreduces your utility bill by ~8 cents/kWh

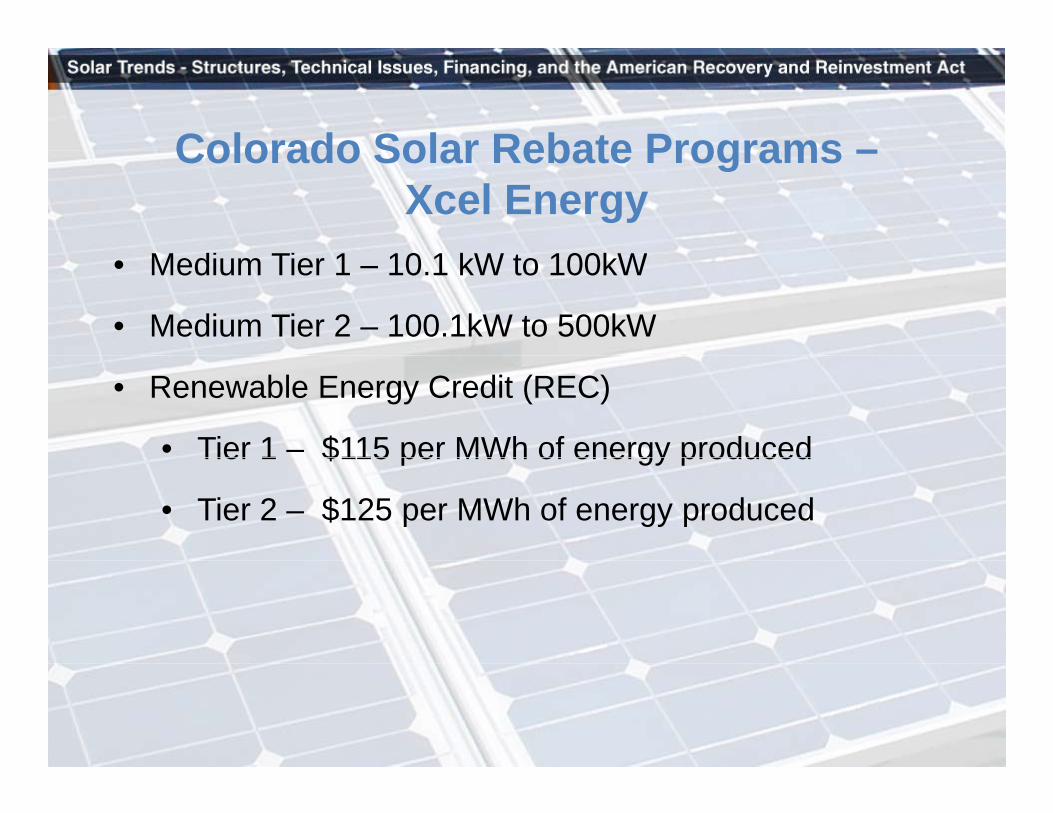

Colorado Solar Rebate Programs –Colorado Solar Rebate Programs –Xcel Energy

M di Ti 1 10 1 kW t 100kW• Medium Tier 1 – 10.1 kW to 100kW

• Medium Tier 2 – 100.1kW to 500kW

• Renewable Energy Credit (REC)

• Tier 1 – $115 per MWh of energy producedTier 1 $115 per MWh of energy produced

• Tier 2 – $125 per MWh of energy produced

Colorado Solar Rebate Programs –Colorado Solar Rebate Programs –Black Hills Energy

• Effective September 1st, 2009, a standard REC for solar systems greater than 100 kW, up to and including 500 kW will be available500 kW will be available

• System’s annual production must not exceed 120% of annual usage or exceed the service entrance capacityannual usage or exceed the service entrance capacity.

• Third Party ownership of solar systems is allowed10 kW and less (500 watt to 10 000 watt DC)and less (500 watt to 10,000 watt DC).

Colorado Solar Rebate Programs –Colorado Solar Rebate Programs –Black Hills Energy

• The total size of the PV array, in DC Watts, will be multiplied by $2.00 per Watt to determine the rebate. For

l 20 0 kil tt (20 000 W tt) t illexample, a 20.0 kilowatt (20,000 Watt) system will receive a rebate of $40,000

• In addition to the rebate, PV systems put in service in 2009 that are greater than 10kW will receive an REC

t f $115 tt h id llpayment of $115 per megawatt hour paid annually

State Grant ProgramState Grant Program

New Energy Economic Development Grant Program:

• $2 million allocated to Colorado by ARRA$2 million allocated to Colorado by ARRA• These grants will provide funding to advance energy

efficiency and renewable energy for commercial and industrial projects, including residential applications,

• These funds will target investments in energy efficiency and renewable energy installations that create jobs inand renewable energy installations that create jobs in Colorado and reduce carbon emissions.

• Funding round for 2009 has closed another round of grant funding in early 2010 is anticipated

Miscellaneous – Energy Bonds

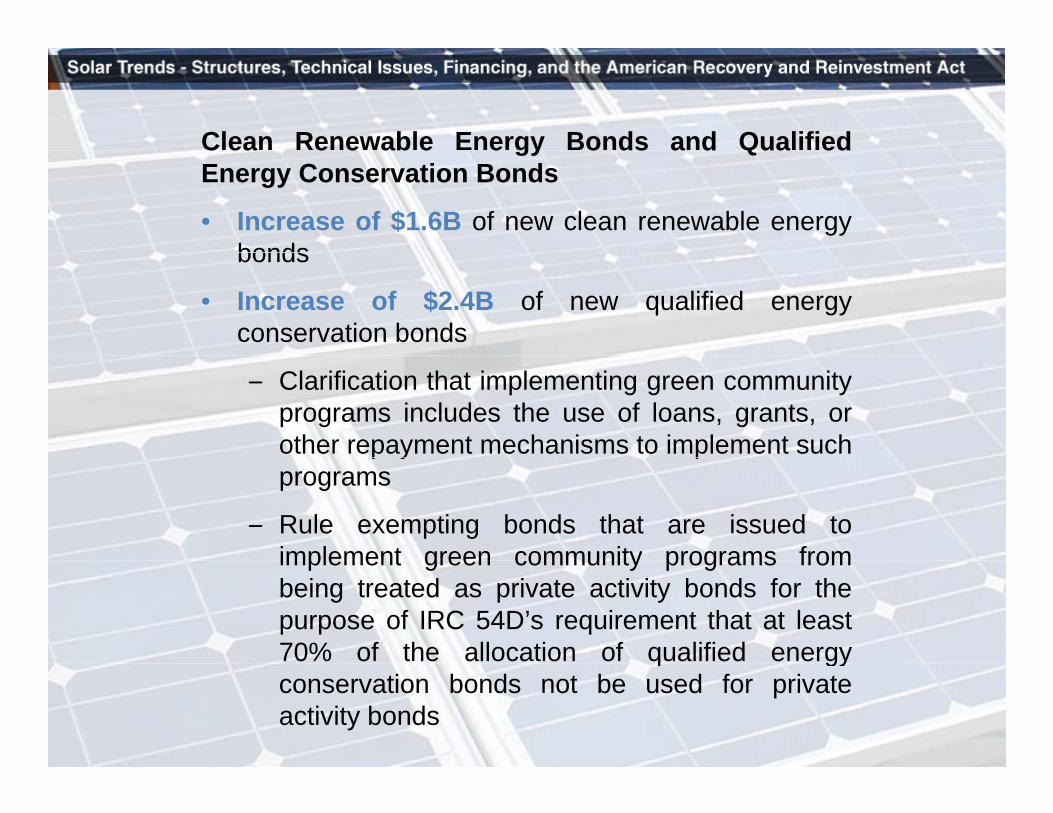

Clean Renewable Energy Bonds and QualifiedC ea e e ab e e gy o ds a d Qua edEnergy Conservation Bonds

• Increase of $1.6B of new clean renewable energybondsbonds

• Increase of $2.4B of new qualified energyconservation bonds

– Clarification that implementing green communityprograms includes the use of loans, grants, orother repayment mechanisms to implement suchp y pprograms

– Rule exempting bonds that are issued toimplement green community programs fromimplement green community programs frombeing treated as private activity bonds for thepurpose of IRC 54D’s requirement that at least70% of the allocation of qualified energyq gyconservation bonds not be used for privateactivity bonds

Combining Section 42 and Section 48

Combining Section 42 (LIHTC) and

Solar Tax Credits combined with LIHTC Issues

g ( )Section 48 (Solar ITC)

Solar Tax Credits combined with LIHTC – Issues

– How will the electricity generated by the solar panels be used by the Project?

– Electricity sold to tenants or the grid • Commercial property taint

Commercial property is not eligible for LIHTCs!Commercial property is not eligible for LIHTCs!

Combining Section 42 (LIHTC) and

Solar Tax Credits with LIHTC – Issues

g ( )Section 48 (Solar ITC)

Solar Tax Credits with LIHTC Issues

– Beware of tax-exempt entity participation (i.e. non-profit general partners)general partners)

• Tax-exempt use property not eligible for solar tax credits

• Should structure around tax-exempt use property rules to avoid losing solar tax credits – Just like LIHTC

• Tax-exempt use % ownership based on entity’s highest share of partnership items of income or gain

– i.e. profit/loss/ residual % etc. (IRC Sec. 168(h)(6))

PPA Versus Cash Purchase

• Not everybody has funds to acquire system, and some customers (eg nonprofits) can’t use thesome customers (eg – nonprofits) can t use the tax incentives

• Rather than purchasing a system yourself, you can do a Power Purchase Agreement (PPA)

• 3rd party company will own the system and collect all the federal/local incentives. This 3rd party is also

ibl f i d i tresponsible for repair and maintenance.

• Customer pays nothing upfront, they just pay for power produced by system for 15 years This ispower produced by system for ~15 years. This is usually at lower cost than utility electric price.

More about PPAsMore about PPAs• Concept of a PPA is for Host Customer to buy electricity and

avoid capital outlay for systemavoid capital outlay for system- Host customer purchases electricity at a discount- Hedge against future electricity price increases- Host customer is not responsible for maintenance, and

payment is a la carte; if the system doesn’t produce,customer doesn’t pay less riskp y

• Term of contract is typically 10-20 years

• 3rd party Owner (usually a bank) can efficiently utilize tax incentives

H t ( ff t k ) h ti t b th l i t ll ti• Host (off-taker) may have option to buy the solar installation or extend PPA term

PPA Versus Cash Purchase

Example -- 100 kW commercial system

Cash price: ~$600K before incentives

PPA: $0 upfront costPPA: $0 upfront cost

• Reduces your utility bill by ~$1000/month

• PPA payment of $~800/month

M thl i f $200/ th• Monthly savings of ~$200/month

• With a PPA, customer saves money from Day 1, with no upfront cost!

Traditional LIHTC Partnershipwith Solar - New Constructionwith Solar New Construction

Combine Solar and LIHTC

Combining Section 42 (LIHTC) and

FundFund

g ( )Section 48 (Solar ITC)

FundFundGeneral PartnerGeneral Partner 1% Investment FundInvestment Fund

Tax Credits (ITC and LIHTC)Tax Credits (ITC and LIHTC)Depreciation DeductionsDepreciation DeductionsTax Credit

E it

Operating Partnership

Tax CreditTax CreditEquity InvestorEquity Investor 99%

Depreciation DeductionsDepreciation DeductionsCash FlowCash FlowEquity

ITC & LIHTC C dit /

LIHTC

PartnershipGeneral Partner

1%Tax Credit Equity

ITC & LIHTC Credits/Tax Losses99%

Systems Integrator/Installer

LIHTC Operating Partnership(with SolarI t ll ti )

Engineering Construction and

DeveloperDeveloper

FeeInstallation)Construction and Procurement

Contract (EPC)

Fee

Combining Section 42 (LIHTC) and

Traditional LIHTC Partnership

g ( )Section 48 (Solar ITC)

p• Owner of real estate and solar installation

• Earns BOTH 30% solar energy credits and LIHTCs

• Solar credits generated 100% in year 1 – IRR additive

• 5 year MACRS depreciation deductions for energy propertyy p gy p p y

• State subsidies (www.dsireusa.org for state by state database)

– Renewable Energy Certificates

Combining Solar with LIHTC

Credit CalculationCredit Calculation

Example

Combining Section 42 (LIHTC) and Section 48 (Solar ITC)

Investment Tax Credit Calculation - Solar Installation (Sec. 48)Solar installation price per watt $ 7 50

Co b g Sect o ( C) a d Sect o 8 (So a C)

Solar installation price per watt $ 7.50

Watts (95 kilowatts) 95,000

Solar installation costs 712,500

Additional installation costs 142 500 (1)Additional installation costs 142,500 (1)

Solar installation costs before dev. fee - Solar Installation 855,000

Developer fee - Solar Installation 106,875 (2)

T t l i t ll ti t i l di d f S l I t ll ti 961 875 Total installation costs including dev. fee - Solar Installation 961,875

Less: costs ineligible for 30% solar ITC (30,000) (3)

Total costs eligible for 30% solar ITC $ 931,875

(1) Soft costs (2) 15% of hard costs (3) Org. costs, syndication, etc.

Combining Section 42 (LIHTC) and Section 48 (Solar ITC)

Investment Tax Credit Calculation - Solar Installation (Sec. 48)

Co b g Sect o ( C) a d Sect o 8 (So a C)

Total costs eligible for 30% solar ITC $ 931,875

Investment tax credit % 30%

Solar ITCs $ 279,563

Energy tax credit price .82Tax credit investor equity proceeds from 30% solar Tax credit investor equity proceeds from 30% solar ITC $ 229,241

Total costs eligible for 30% solar ITC $ 931 875 Total costs eligible for 30% solar ITC $ 931,875

50% basis reduction (50% of solar ITCs) (139,781)

Depreciable basis - 5 year MACRS $ 792,094

Combining Section 42 (LIHTC) and Section 48 (Solar ITC)Co b g Sect o ( C) a d Sect o 8 (So a C)

Low-Income Housing Tax Credit Eligible Basis (Sec. 42)

Solar installation costs before developer fee - Solar Installation $ 855,000

Less: costs ineligible for tax credit basis (30,000)

Total solar installation costs eligible for LIHTC $ 825 000 Total solar installation costs eligible for LIHTC $ 825,000

Combining Section 42 (LIHTC) and Section 48 (Solar ITC)

Total solar installation costs eligible for LIHTC $ 825,000 $ 825,000

Equity proceeds from LIHTCs 9% not in DDA 9% in DDA

Co b g Sect o ( C) a d Sect o 8 (So a C)

50% basis reduction per Section 50(c) (139,781) (4) (139,781)

Eligible basis from solar installation for LIHTC 685,219 685,219

Additional developer fee relating to LIHTC (15%) 102,783 (5) 102,783

Total eligible basis from solar installation for LIHTC 788,002 788,002

Not In DDA = 100%; In DDA = 130% 100% 130%

Adj. eligible basis from solar installation for LIHTC 788,002 1,024,402

LIHTC applicable % 9.00% 9.00%

LIHTCs - annual 70,920 92,196

10 year credit period 10 10

Total LIHTCs 709,201 921,962

LIHTC credit price 0.70 0.70

Tax credit investor equity proceeds from LIHTC $ 496,441 $ 645,373 (4) 50% of solar ITC (5) Subject to state LIHTC allocating agency’s QAP limit for developer fees

Combining Section 42 (LIHTC) and Section 48 (Solar ITC)

Net cost of solar installation 9% not in DDA 9% in DDA

Co b g Sect o ( C) a d Sect o 8 (So a C)

Total installation costs $ 961,875 $ 961,875 Tax credit investor equity proceeds from 30% energy ITC (229,241) (229,241)

Tax credit investor equity proceeds from LIHTC (496,441) (645,373)

Estimated net cost of solar installation $ 236,193 $ 87,261Before economic savings and State/local incentives including $102,783 of developer fee.

Developer IssuesDeveloper Issues

Updates to Treas. Reg. 1.42-10Jul 29

H R

Housing and Economic Recovery Act (“HERA”)

American Recovery and Reinvestment Act (“ARRA”)

H.R.3221 H.R.

1

Jul 30 Feb 17

AUG SEP NOVOCT DEC

2008 2009JUL JAN FEB MAR APR MAYMAY JUNJUN

§§ 1.42-10 Utility allowances.

(a) Inclusion of utility allowances in gross rent. If the cost of any utility (other

than telephone, cable television, or Internet) for a residential rental unit is

paid directly by the tenant(s), and not by or through the

owner of the building, the gross rent for that unit includes the

applicable utility allowance determined under this section.

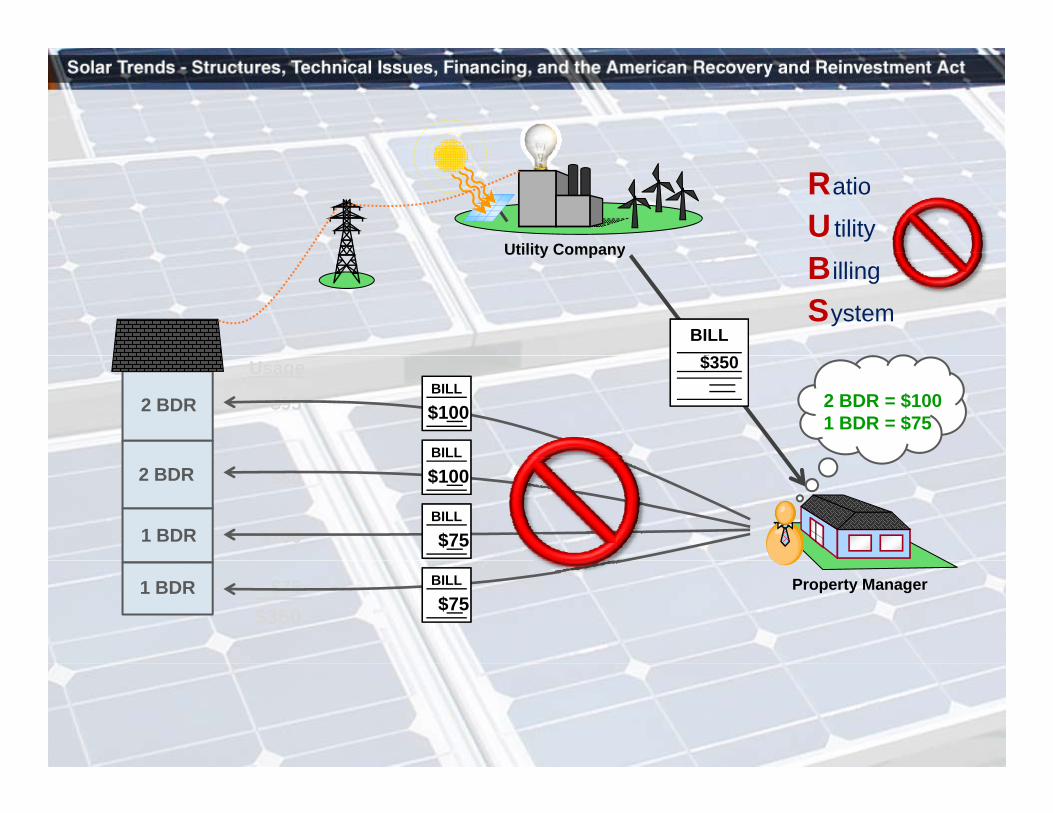

Utility CompanyUtility Company

BILL$$$$

Utility Allowance = $80

LIHTC U it

Rent limit:

Less Utility Allowance:

$935

(80)

Unit

Property ManagerCharged to tenant: $855

Utility CompanyUtility Company

BILL$

2 BDR $95

$350UsageBILL

$95

BILL

1 BDR

2 BDR $80

$100BILL

$100

$80

1 BDR Property Manager$75$350

BILL

$75

Utility Company

Ratio

Utility Utility Company

BILL$

Billing

System

2 BDR $95

$350UsageBILL

$100

BILL

2 BDR = $1001 BDR = $75

1 BDR

2 BDR $80

$100BILL

$75

$100

1 BDR Property Manager$75$350

BILL

$75

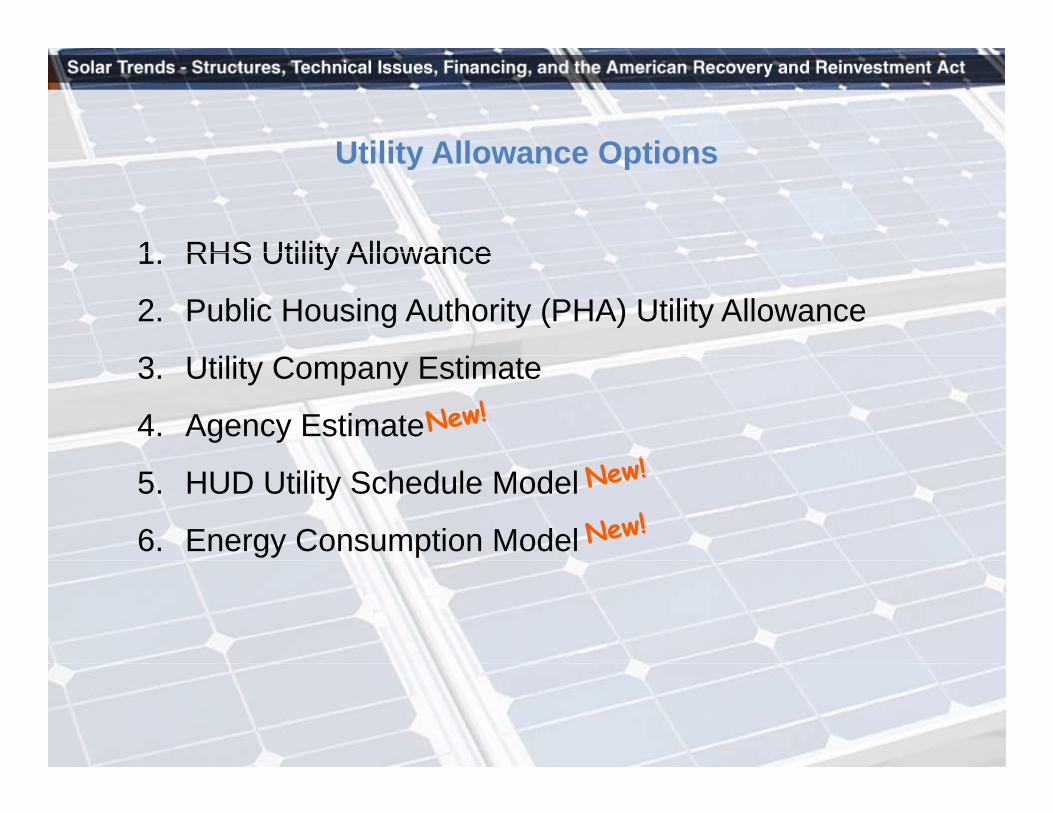

Utility Allowance OptionsUtility Allowance Options

1 RHS Utility Allowance1. RHS Utility Allowance

2. Public Housing Authority (PHA) Utility Allowance

C3. Utility Company Estimate

4. Agency Estimate

5. HUD Utility Schedule Model

6. Energy Consumption Model

CHFA Application for Energy Efficiencypp gy yMechanical Systems – Equipment (applies to all systems or system installed)

Efficiency Measure Minimum Energy Efficiency RequirementGas Forced Air Furnace-Install sealed combustion, gas h ti it ( t l )

Install with an AFUE rating = or > 90% & be EnergySt Q lifi dheating units (propane or natural gas) Star Qualified

Central Air Conditioner (split system & package units)Install a Seasonal energy Efficiency Ratio (SEER) of =

or >14.0 and be Energy Star Qualified

Air Source Heat Pumps for split systemInstall Energy Star qualified with a Heating Season

Performance Factor (HSPF) = or >8..2p p y ( )

Air Source Heat Pumps for package systemInstall Energy Star qualified with a HSPF = or >8.0

with an AC SEER = or > 14.0Ground Source Heat Pump Install Energy Star Qualified systemGas Boilers (must be a qualified sealed combustion boiler Install Energy Star Qualified with an AFUE = or >with electronic ignition) 85%.Gas Hot Water Heater tank-storage type (must be sealed combustion or power direct vent water heater)

install with an Energy Factor (EF) = or > 0.62. Willneed to be Energy Star Qualified after 1/1/09

Gas Hot Water Heater gas tankless type (must be sealed combustion or power direct vent water heater)

install with an Energy Factor (EF) = or > 0.82. Willneed to be Energy Star Qualified after 1/1/09combustion or power direct vent water heater) need to be Energy Star Qualified after 1/1/09

Gas Hot Water Heater (combination system)

Install with a Combined Applicance Efficiency (CAE) = or > 0.80, when gas heater is used as a combined

appliance to provide domestic hot water and hot wateras a heating source for the dwelling unit.

I t ll ith EF 0 89 f 80 l EFElectric Water Heater (all electric tank types)

Install with an EF = or > 0.89 for 80 gal,, EF = or >0.92 for 50 gal., EF = or > 0.93 for 40 gal.,

Electric Water Heater (tankless type) Install with an EF = or > 0.99Heat Pump Water Heater Install with an EF = or > 2.0

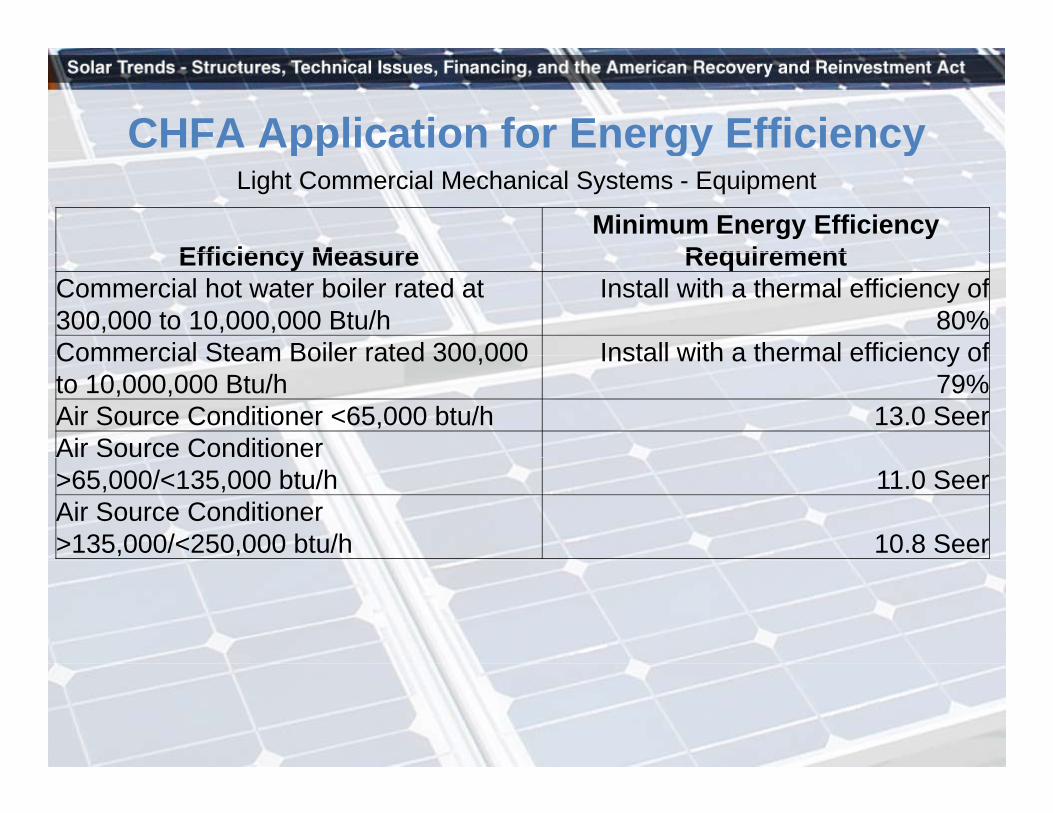

CHFA Application for Energy Efficiencypp gy yLight Commercial Mechanical Systems - Equipment

Efficiency MeasureMinimum Energy Efficiency

RequirementEfficiency Measure RequirementCommercial hot water boiler rated at 300,000 to 10,000,000 Btu/h

Install with a thermal efficiency of80%

Commercial Steam Boiler rated 300 000 Install with a thermal efficiency ofCommercial Steam Boiler rated 300,000 to 10,000,000 Btu/h

Install with a thermal efficiency of79%

Air Source Conditioner <65,000 btu/h 13.0 SeerAir Source Conditioner>65,000/<135,000 btu/h 11.0 SeerAir Source Conditioner>135,000/<250,000 btu/h 10.8 Seer

CHFA Application for Energy Efficiencypp gy yDwelling Unit

Efficiency MeasureMinimum Energy Efficiency

RequirementEfficiency Measure RequirementCeiling Fan (reversible) Energy Star QualifiedCeiling Fan (reversible with light Kit) Energy Star QualifiedBath Exhaust Fan Install with a 10-80 CFM and EnergyBath Exhaust Fan Install with a 10 80 CFM and Energy

Star QualifiedBath Exhaust Fan (in-line single or multi-port) Energy Star Qualifiedp ) gy Q

CHFA Application for Energy Efficiencypp gy yLighting

Efficiency MeasureMinimum Energy Efficiency

RequirementEfficiency Measure RequirementCompact Fluorescent Lighting, Interior Fixture

13-36 Watt Fixture in place of incandescent 65 Watt Fixture

Compact Fluorescent Lighting Interior 48 Watt Fixture in place ofCompact Fluorescent Lighting, Interior Fixture

48 Watt Fixture in place of incandescent 100 Watt Fixture

Compact Fluorescent Lighting, Interior Fixture

54 Watt Fixture in place of incandescent 120 Watt Fixture

Compact Fluorescent Lighting, Interior Fixture

72 Watt Fixture in place of incandescent 120 Watt Fixture

Compact Fluorescent Lighting, Exterior 18-20 Watt Fixture in place of Fixture incandescent 60 Watt FixtureCompact Fluorescent Lighting, Exterior Fixture

40 Watt Fixture in place of incandescent 120 Watt Fixture

C t Fl t Li hti E t i 65 W tt Fi t i l fCompact Fluorescent Lighting, Exterior Fixture

65 Watt Fixture in place of incandescent 120 Watt Fixture

CHFA Application for Energy Efficiencypp gy yWindows & Doors

Efficiency MeasureMinimum Energy Efficiency

RequirementEfficiency Measure RequirementLow-E Glass/Multiple Pane & NFRCrating that meets or exceeds Energy

Star Qualification based on theWindows

Star Qualification based on theEnergy Star climate zone map

Tubular Daylighting Device (TDD) & NFRC rating that meets or exceeds

Skylights

gEnergy Star Qualification based onthe Energy Star climate zone map

Low-E Glass/Multiple Pane & NFRC

Glass Doors (Non fire rated doors)

rating that meets or exceeds EnergyStar Qualification based on theEnergy Star climate zone map

CHFA Application for Energy Efficiencypp gy yAppliances (if installed)

Efficiency MeasureMinimum Energy Efficiency

RequirementEfficiency Measure RequirementDishwasher Energy Star QualifiedRefrigerator Energy Star QualifiedClothes Washer Energy Star QualifiedClothes Washer Energy Star Qualified

Enterprise’s Green CommunitiesEnterprise s Green Communities

• Integrated DesignIntegrated Design• Site, Location and Neighborhood Fabric

Sit I t• Site Improvements• Water Conservation• Energy Efficiency• Materials Beneficial to the EnvironmentMaterials Beneficial to the Environment• Healthy Living Environment

O ti d M i t• Operations and Maintenance

Photovoltaic System: InformationPhotovoltaic System: Information

Real Estate: MultifamilyySystem Assumptions:

Size of System (watts) 100,000System cost (per watt) $5.00

fFinancial Information:Value of RECs $115.00 per MWhPrice of Electricity (kwh): $0 0800Price of Electricity (kwh): $0.0800

Photovoltaic System: Financial AnalysisPhotovoltaic System: Financial AnalysisTotal Cost of Installed Photovoltaic System: $500,000.00Federal Income Tax Credit (30%) : <$150,000.00>Xcel Utility Rebate after taxes ($2.00/watt) : <$130,000.00>Cost of System after Incentives: $220,000.00

Total Depreciation Savings (50% accel in YR 1): $132,626.89$87,373.11

Year 1 Estimated Energy Savings: $12,160.00Annual Estimated REC Income: $11,362.00Annual Estimate Total Income: $23,522.00

Internal Rate of Return (IRR): 18.40%Return on Investment (ROI): 4 years

REC = Renewal Energy CreditsAnalysis courtesy of Douglas Colony Group

ProductionProductionLocation: DenverLocation: DenverAverage peak sun hours: 5.1Efficiency Factor (kWh/watt/year): 1 52Efficiency Factor (kWh/watt/year): 1.52Annual Production (kWh): 152,000

Back-end Interest/Complex Structures

The Captive Energy Companyp gy p y

Existing Multi-Family AssetsA way to green your existing LIHTC portfolioA way to green your existing LIHTC portfolio

The Captive Energy Company

DeveloperDeveloper

The Captive Energy Company

Investor MemberInvestor Member

pp(Managing Member)(Managing Member)

1%1%Captive EnergyCaptive EnergyCompany, LLCCompany, LLCDeveloper

Fee-- ITC (solar)ITC (solar)-- Tax Losses (depreciation)Tax Losses (depreciation)

CSI ProgramCSI Program-- MASH programMASH program-- Production basedProduction basedincentiveincentiveInvestor MemberInvestor Member

99%99%

$ 100%

Tax Losses (depreciation)Tax Losses (depreciation)-- PPA Revenues (cash flow)PPA Revenues (cash flow)-- State subsidiesState subsidies

incentiveincentive

-- Institutions?Institutions?-- Individuals?Individuals?

Developer?Developer?

Multi-familySolar 1, LLC(di d d)

Multi-familySolar 2, LLC

Multi-familySolar 3, LLC

100%

Multi-familySolar 4, LLC

-- Developer?Developer?

Systems Integrator/ Multi-family

(disregarded) (disregarded),

(disregarded)

Multi-family Multi-family

(disregarded)

Multi-family

Power Purchase/Lease Agreements

Engineering Systems Integrator/Installer

Multi familyHousing Project Host #1

yHousing Project Host #2

yHousing Project Host #3

yHousing Project Host #4

Construction and Procurement

Contract (EPC)

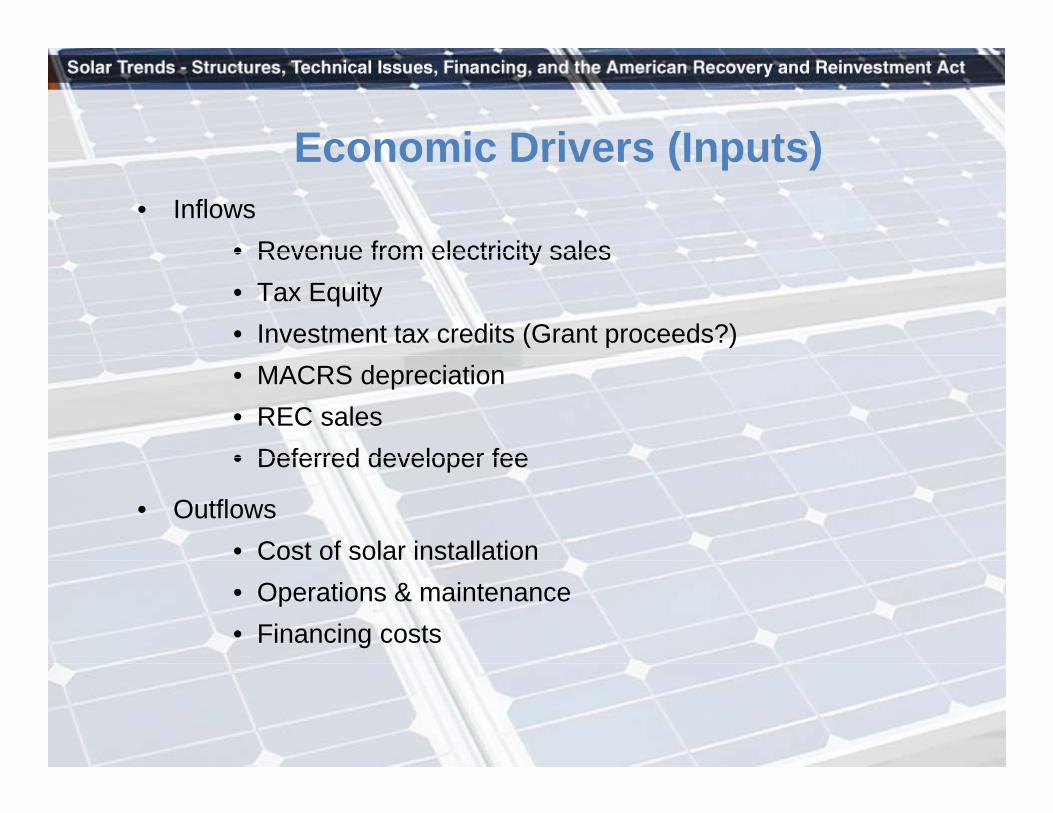

Economic Drivers (Inputs)Economic Drivers (Inputs)• Inflows

• Revenue from electricity sales• Revenue from electricity sales• Tax Equity• Investment tax credits (Grant proceeds?)• MACRS depreciation• REC sales• Deferred developer fee• Deferred developer fee

• Outflows• Cost of solar installation• Operations & maintenance• Financing costs

LIHTC Operating Partnershipp g p• Hedge against increasing energy costs

• Decreased utility bills – higher DCR

• IRS Notice 2009-44 implications

Captive Energy Companyp gy p y• Owns the solar installation

• Gets the 30% ITC

• 5 year MACRS depreciation

• Gets the state subsidies

• Earns a developer fee

• Monetizes the tax benefits

Partnership Flip

Sale-Leaseback

Lease Pass-through

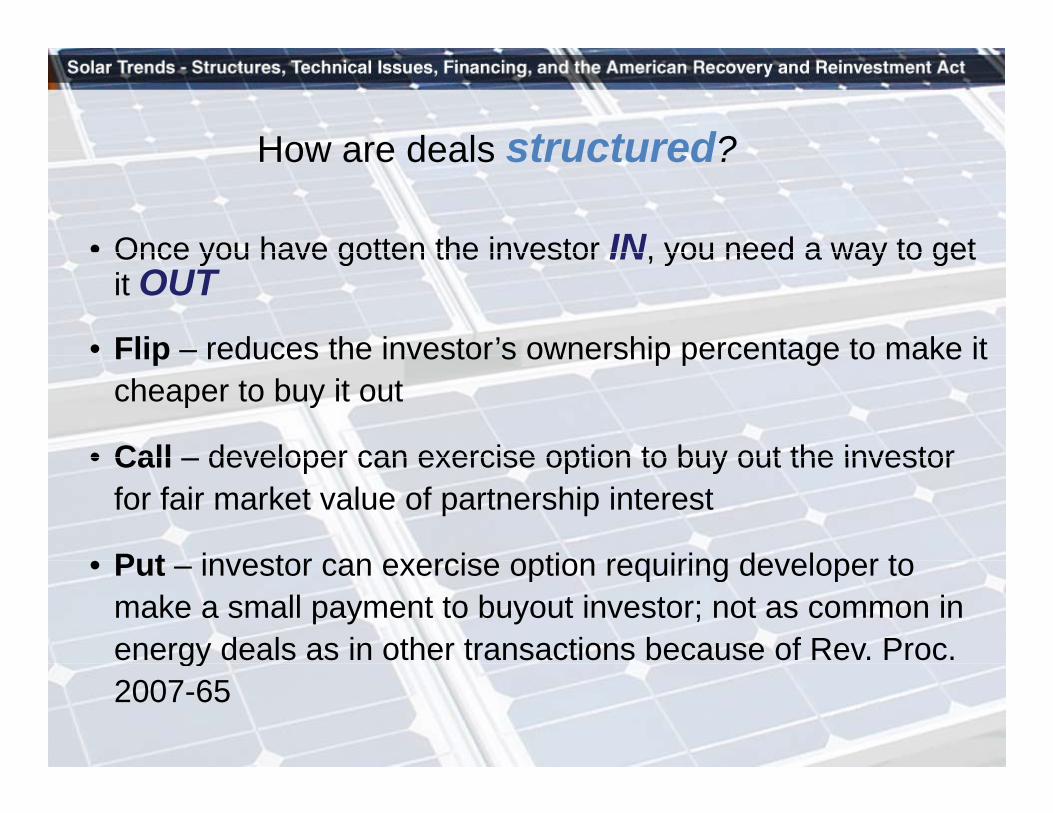

How are deals structured?How are deals structured?

• Once you have gotten the investor IN you need a way to getOnce you have gotten the investor IN, you need a way to get it OUT

• Flip – reduces the investor’s ownership percentage to make itFlip reduces the investor s ownership percentage to make it cheaper to buy it out

• Call developer can exercise option to buy out the investor• Call – developer can exercise option to buy out the investor for fair market value of partnership interest

• Put investor can exercise option requiring developer to• Put – investor can exercise option requiring developer to make a small payment to buyout investor; not as common in energy deals as in other transactions because of Rev. Proc. gy2007-65

Partnership FlipFundFund

General PartnerGeneral Partner Investment FundInvestment Fund1%

Partnership Flip

Tax CreditTax CreditEquity InvestorEquity Investor

1%1% Investment FundInvestment Fund

Tax CreditsTax CreditsDepreciation DeductionsDepreciation Deductions

Cash FlowCash Flow

$Developer DeveloperDeveloper

99%

99%99% $p

Fee

100%

DeveloperDeveloper

Solar 1, LLC Solar 2, LLC Solar 3, LLC Solar 4, LLC

System Integrator/Installer

Solar Installation

PPA/Lease Agreements

Solar Installation

Solar Installation

Solar Installation

Host #1 Host #2 Host #3 Host #4

P t hi FliPartnership Flip• Typically used by developer with mind on residual interest yp y y p

ownership

• Vehicle for larger investment funds

• Additional deals (tranches) easily added

• May appeal to short term minded tax credit equity

• 6-7 year investment

• Put/Call buy out structure

I t t F d i P t hi FliInvestment Fund in Partnership Flip• Owner of the solar installations (via lower tier LLCs

disregarded for tax purposes)disregarded for tax purposes)

• Depreciation deductions

• 30% ITC flows through to the tax credit equity investor

• State incentives – Rebates, Renewable Energy Certificates (RECs) and state tax credits(RECs) and state tax credits

• Cash flow from PPA / Lease revenue, state incentives

Allocation of Tax BenefitsAllocation of Tax Benefits• Energy investment tax credits allocated to members by

profit percentagesprofit percentages

• Maintenance of capital accounts important

Tax losses (i e depreciation) requires sufficient capital• Tax losses (i.e. depreciation) requires sufficient capital account basis

• Minimum gaing

• Investor must be a member of the energy company before the placed-in-service date of the solar installation

E it Strategies for Partnership Flip andExit Strategies for Partnership Flip and Lease Pass- Through Structures

– Investors generally want out of the transactions at the end of year 6 – Put/Call option

– Most common exit is through a flip:

• Investor ownership interest flips from 99% to 5%

• Developer/GP exercises call option to buy out investor for greater of FMV of ownership interest or amount required to achieve agreed-upon IRRamount required to achieve agreed upon IRR

Sale Leaseback StructureSolar Developer may provide certain guarantees

Solar Developer LLCSolar Developer LLC C t I tC t I t

to Corporate Investor and funds would be held in escrow accordingly. Yield guarantees, O&M, Insurance etc. Funds released to Solar

Lease Agreement

Purchase Agreement

Solar Developer, LLCSolar Developer, LLCLesseeLessee

Corporate InvestorCorporate InvestorLessorLessor

released to Solar Developer as guarantees burn off.

Sales Proceeds

Sale of SEFs and Lease Payments

Solar Solar

PPA/Lease Agreements

Energy

Lessor is owner of SEF, Investment Tax Credits, Tax Losses (Depreciation Deductions), Rebates, RECs, Recipient of lease payments, Potential residual buyout

DeveloperDeveloper

Solar 1, LLC Solar 2, LLC Solar 3, LLC

Energy Procurement Contract (“EPC”)

System Integrator/Installer

Solar Installation Host #1

Solar Installation Host #2

Solar Installation Host #3Host #1 Host #2 Host #3

Sale-Leaseback Attributes• More effectively frontloads economics toMore effectively frontloads economics to

developer

• Allows developer to grow business with current cash flow

• More effective use of corporate capital?

• Developer establishes track record

• Sacrifice of residual interest for current cash flflow

• Investor has flexibility to get into the deal within 90 days of PIS mitigating/eliminating construction risky g g g

Sale-Leaseback Attributes

Sales taxes paid over life of the lease• Sales taxes paid over life of the lease agreement

• No leakage of tax benefits (e g 1% to G P )No leakage of tax benefits (e.g. 1% to G.P.)

• Not using a partnership

• Economic substance doctrine issue N/A?• Economic substance doctrine issue N/A?

• Simplicity of structure, Cost effective

• Investor utilization of lease optimization model

Sale of PV Panels

Loan ProceedsManufacturer

$$

Developer/ Installer

Lender

Install/Maintenance Debt Service Payments

Capital Contribution

State Incentive Programs

Lease Pass-Through

No basis reduction to depreciable basisLESSOR SOLAR LPPV System Owner

General Partner51%-99%

partnership interest

$

e

P/L

$Lease Pass Through

SOLAR MASTER TENANT LP

Leas

e

1%-49% LP interest in losses

Capital ContributionPass-throughElection

$

Basis Reduction Income

Capital Contribution

CreditsCash – Preferred Return

Call Option – Cash, Capital Loss eP/L and Credits

SOLAR MASTER TENANT LP

$

Leas

e

1% General Partner(Developer)

99% Limited Partner(Corporate Investor)

Power

Lease Payments

Host

Lease Pass-Through Attributes

• Election to treat lessee as owner of solar panels for tax credit purposes

O hi d th d i ti d d ti• Ownership, and thus, depreciation deductions remain with lessor

N b i d ti t d i bl b i f l• No basis reduction to depreciable basis for lessor

Lease Pass-Through Attributes

• Lessee required to recognize income equal to 50% of credits

P t ti l IRC 704(b) i f th d l• Potential IRC 704(b) issues for the developer

• With DOE cash grant option, does lease pass-th h k ?through make sense?

Relevant Issues• Install costs• Install costs

• PPA rates

• Competition for hosts

D bt t C dit h i li ti• Debt terms – Credit crunch implications

Relevant Issues

(C )• Residual (Call) Value

• Investor typically wants to minimize “residual reliance”

• Residual payment debt financed / G P equity?Residual payment debt financed / G.P. equity?

• Investor return requirements - Credit crunch i li tiimplications

• Economic substance doctrine

Relevant Issues• Deferred Developer Fees/Installment Notes• Deferred Developer Fees/Installment Notes

• Can they be supported by project cash flow?

• Contingent question

• Potential tax consequences to developer

• Capital Accounts

• 704(b) issues704(b) issues

• Potential reallocation of tax losses

&

www.novoco.com